Solana 4H RSI->MACD — Counter-Trend By TetradTetrad RSI→RSI Cross→MACD (Sequenced) — Counter-Trend (SL-Only)

Category: Market-neutral, counter-trend, sequenced entries

Timeframe default: Works on any TF; designed around 4H On Solana

Markets: Any (spot, perp, futures); parameterize to your asset

What it does

This strategy hunts reversals using a 3-step sequence on RSI and MACD, then optionally restricts entries by market regime and a price gate. It shows stop-loss lines only when hit (clean chart), and paints a Donchian glow for quick read of backdrop conditions.

Entry logic (sequenced)

1. RSI Extreme:

Long path activates when RSI < Oversold (default 27.5).

Short path activates when RSI > Overbought (default 74).

2. RSI Cross confirmation:

Long path: RSI crosses up back above the oversold level.

Short path: RSI crosses down back below the overbought level.

Each step has a max bar lookback so stale signals time out.

3. MACD Cross trigger:

Long: MACD line crosses above Signal.

Short: MACD line crosses below Signal.

→ When step 3 fires and gates are satisfied, a trade is entered.

Optional gates & filters

Regime Filter (Counter-Trend):

Longs allowed in **Range / Short Trend / Short Parabolic** regimes.

Shorts allowed in **Range / Long Trend / Long Parabolic** regimes.

Based on ADX/DI and ATR% intensity.

* Price Gate (Long Ceiling):

Toggle to **disable new longs above a chosen price (default 209.0 For SOL).

Useful for assets like SOL where you want longs only below a cap.

Exits / Risk

* Stop-Loss (% of entry):** default **14%**, toggleable.

* SL visualization:** plots a **thin dashed red line only on the bar it’s hit**.

* (No take-profit or time-based exit in this version—keep it pure to the sequence and regime. Add TP/time exits if desired.)

Visuals

* Donchian Glow (50): background band only (upper/lower lines hidden).

* Regime HUD: compact table (top-right) highlighting the active regime.

* Minimal marks: no entry/exit “arms” clutter; only SL-hit lines render.

Inputs (key)

* Core: RSI Length, Oversold/Overbought, MACD Fast/Slow/Signal.

* Sequence: Max bars from Extreme→RSI Cross and RSI Cross→MACD Cross.

* Regime: ADX Length, Trend/Parabolic thresholds, ATR length & floor.

* Stops: Enable/disable; SL %.

* Price Gate: Enable; Long ceiling price.

Alerts

Sequenced Long (CT): RSIhigh → RSI cross down → MACD bear cross.

## Notes & Tips

Designed for counter-trend fades that become trend rides. The regime filter helps avoid fading true parabolics and aligns entries with safer contexts.

The sequence is stateful (steps must occur in order). If a step times out, the path resets.

Works on lower TFs, but the 4H baseline reduces noise and over-trading.

Consider pairing with volume or structure filters if you want fewer but higher-conviction entries.

Past performance ≠ future results. **Educational use only. Not financial advice.

Cari dalam skrip untuk "rsi"

- Trading Bot – Dynamic RSI (Professional) - Robot Strategy -1. General Concept and Philosophy

This strategy was designed for systematic traders and work especially well on short timeframes (1 to 5 minutes), who seek to capture trend reversal movements with a high degree of confirmation. The goal is not to follow the trend, but to identify precise entry points in oversold or overbought zones, and then to exit the position dynamically to adapt to changing market conditions.

The originality of Trading Bot Dynamic RSI lies not in a single indicator, but in the intelligent fusion of several concepts:

Dynamic RSI bands for both entries and exits .

A triple confirmation filter to secure trade entries.

A fully parameterizable design ready for automation .

2. Originality at the Core of the Strategy: Key Features

Dynamic Exits on RSI Bands: This is a main original feature of this script. Unlike traditional strategies that use fixed Take-Profits and Stop-Losses, this one uses an exit RSI band, calculated with parameters independent of the entry ones. This allows the strategy to:

Adapt to Volatility: In a volatile market, the exit band will move further away, allowing for the capture of larger moves. In a ranging market, it will tighten to secure smaller gains.

Optimize Profits: The exit occurs when momentum genuinely fades, not at an arbitrary price level, thus maximizing the potential of each trade.

Triple Confirmation Filter for Precise Entries: To avoid false signals, each entry is validated by the convergence of three distinct conditions:

The base signal is generated when the price reaches an overbought or oversold zone, materialized by an RSI band calculated directly on the chart.

The WaveTrend oscillator must also be in an extreme zone, confirming that the short-term momentum is ready for a reversal.

Finally, the StochRSI must validate that the RSI itself is in an overbought or oversold condition, adding an extra layer of security.

"Automation Ready" Design: The strategy was developed with automation in mind.

Customizable Alert Messages: All messages for entries and exits (Long/Short) can be formatted to be compatible with automated trade execution platforms.

Precise Capital Management: The position size calculation can be set as a fixed amount (e.g., 100 USDT), a percentage of the total capital, or of the available capital, and includes leverage. These parameters are crucial for a trading bot.

3. Detailed Operation

Entry Logic: A position is opened only if the following three conditions are met:

The market price touches (or closes below/above) the entry RSI band (lower for a buy, upper for a sell).

The WaveTrend indicator is in the oversold zone (for a buy) or overbought zone (for a sell).

The Stochastic RSI indicator is also in the oversold zone (for a buy) or overbought zone (for a sell).

The order is placed as a limit order on the RSI band, allowing for execution at the best possible price.

Exit Logic: The primary exit is dynamic.

For a Long position, the trade is closed when the price reaches the upper exit RSI band.

For a Short position, the trade is closed when the price reaches the lower exit RSI band.

Optionally, a percentage-based Stop-Loss and Take-Profit can be activated for more traditional risk management, although the dynamic exit is the recommended default mechanism.

4. Ease of Use and Customization

Despite its internal complexity, the strategy is designed to be user-friendly :

Clear Settings Panel: Parameters are grouped by function (Long Entry, Long Exit, Quantity, etc.), and each option comes with an explanatory tooltip.

Integrated Display: All key information (performance, current settings) is displayed in clean and discreet tables directly on the chart, allowing you to see at a glance how the strategy is configured.

Total Flexibility: Although default settings are provided, every parameter (RSI lengths, levels, filters) can be adjusted to optimize the strategy on any asset (cryptocurrencies, Forex, indices...) and any timeframe.

5. Detailed Guide to User Settings

A comprehensive set of parameters

To offer you complete control and maximum flexibility, the strategy exposes a comprehensive set of parameters. Here is an overview of what you can customize:

Trading Mode and Display

Trading Mode: Choose to enable only long positions ("Long Only"), only short positions ("Short Only"), or both simultaneously ("Long and Short").

Display: Manage the information panels on the chart. You can opt for a full display, a minimal window showing the profit, or hide all information for a clean chart.

Filters Smoothing (StochRSI K)

Filters Smoothing: This key parameter adjusts the smoothing of the Stochastic RSI. A lower value will make the filter more responsive, generating more signals. A higher value will make it smoother, generating fewer but potentially more reliable signals.

LONG Position Settings

Long Only mode

Entry: Define the RSI length and Oversold level that draw the lower band for long position entries.

Exit: Independently configure the RSI length and Overbought level that draw the upper band for the dynamic position exit.

Options: Optionally enable a percentage-based Take-Profit and/or Stop-Loss.

SHORT Position Settings

Short Only Mode

Entry: Define the RSI length and Overbought level for the upper entry band for short positions.

Exit: Independently configure the RSI length and Oversold level for the lower dynamic exit band.

Options: Just like for long positions, you can enable a percentage-based Take-Profit and/or Stop-Loss.

Quantity and Leverage

Quantity Type: Calculate your position size in three ways: as a fixed cash amount, as a percentage of available capital, or as a percentage of the total account balance.

Amount: Specify the dollar amount or percentage to commit per trade.

Leverage: Set the leverage to be applied. This is crucial for automation.

Backtest Period

Backtest Period: Enable this option to limit the strategy's calculations to a specific time period. This is a powerful tool for testing performance under particular market conditions.

Bot Alert Messages

Bot Alert Messages: This section is dedicated to automation. Customize the exact text messages that will be sent by TradingView alerts for each event (enter long, exit long, etc.).

Other Settings (Advanced - Optional)

Other Settings: This section allows experienced users to fine-tune the confirmation engine. You can adjust the parameters of the WaveTrend and Stochastic RSI oscillators in detail.

Spread Calculator (Informative Only)

Spread Calculator: This handy tool helps you estimate the actual fees of your exchange to run a much more realistic backtest. This panel has no impact on the trading logic itself.

Disclaimer

This strategy provides signals based on past market conditions. Past performance is not indicative of future results. Trading involves risk, and it is the responsibility of each user to manage their risk appropriately. It is strongly recommended to conduct thorough backtests and to understand the functioning of each parameter before using this strategy in live conditions or automating it. Take into account transaction fees, spread, and slippage, which can impact real results.

EMA RSI Trend Reversal Ver.1Overview:

The EMA RSI Trend Reversal indicator combines the power of two well-known technical indicators—Exponential Moving Averages (EMAs) and the Relative Strength Index (RSI)—to identify potential trend reversal points in the market. The strategy looks for key crossovers between the fast and slow EMAs, and uses the RSI to confirm the strength of the trend. This combination helps to avoid false signals during sideways market conditions.

How It Works:

Buy Signal:

The Fast EMA (9) crosses above the Slow EMA (21), indicating a potential shift from a downtrend to an uptrend.

The RSI is above 50, confirming strong bullish momentum.

Visual Signal: A green arrow below the price bar and a Buy label are plotted on the chart.

Sell Signal:

The Fast EMA (9) crosses below the Slow EMA (21), indicating a potential shift from an uptrend to a downtrend.

The RSI is below 50, confirming weak or bearish momentum.

Visual Signal: A red arrow above the price bar and a Sell label are plotted on the chart.

Key Features:

EMA Crossovers: The Fast EMA crossing above the Slow EMA signals potential buying opportunities, while the Fast EMA crossing below the Slow EMA signals potential selling opportunities.

RSI Confirmation: The RSI helps confirm trend strength—values above 50 indicate bullish momentum, while values below 50 indicate bearish momentum.

Visual Cues: The strategy uses green arrows and red arrows along with Buy and Sell labels for clear visual signals of when to enter or exit trades.

Signal Interpretation:

Green Arrow / Buy Label: The Fast EMA (9) has crossed above the Slow EMA (21), and the RSI is above 50. This is a signal to buy or enter a long position.

Red Arrow / Sell Label: The Fast EMA (9) has crossed below the Slow EMA (21), and the RSI is below 50. This is a signal to sell or exit the long position.

Strategy Settings:

Fast EMA Length: Set to 9 (this determines how sensitive the fast EMA is to recent price movements).

Slow EMA Length: Set to 21 (this smooths out price movements to identify the broader trend).

RSI Length: Set to 14 (default setting to track momentum strength).

RSI Level: Set to 50 (used to confirm the strength of the trend—above 50 for buy signals, below 50 for sell signals).

Risk Management (Optional):

Use take profit and stop loss based on your preferred risk-to-reward ratio. For example, you can set a 2:1 risk-to-reward ratio (2x take profit for every 1x stop loss).

Backtesting and Optimization:

Backtest the strategy on TradingView by opening the Strategy Tester tab. This will allow you to see how the strategy would have performed on historical data.

Optimization: Adjust the EMA lengths, RSI period, and risk-to-reward settings based on your asset and time frame.

Limitations:

False Signals in Sideways Markets: Like any trend-following strategy, this indicator may generate false signals during periods of low volatility or sideways movement.

Not Suitable for All Market Conditions: This indicator performs best in trending markets. It may underperform in choppy or range-bound markets.

Strategy Example:

XRP/USD Example:

If you're trading XRP/USD and the Fast EMA (9) crosses above the Slow EMA (21), while the RSI is above 50, the indicator will signal a Buy.

Conversely, if the Fast EMA (9) crosses below the Slow EMA (21), and the RSI is below 50, the indicator will signal a Sell.

Bitcoin (BTC/USD):

On the BTC/USD chart, when the indicator shows a green arrow and a Buy label, it’s signaling a potential long entry. Similarly, a red arrow and Sell label indicate a short entry or exit from a previous long position.

Summary:

The EMA RSI Trend Reversal Indicator helps traders identify potential trend reversals with clear buy and sell signals based on the EMA crossovers and RSI confirmations. By using green arrows and red arrows, along with Buy and Sell labels, this strategy offers easy-to-understand visual signals for entering and exiting trades. Combine this with effective risk management and backtesting to optimize your trading performance.

Global Index Spread RSI StrategyThis strategy leverages the relative strength index (RSI) to monitor the price spread between a global benchmark index (such as AMEX) and the currently opened asset in the chart window. By calculating the spread between these two, the strategy uses RSI to identify oversold and overbought conditions to trigger buy and sell signals.

Key Components:

Global Benchmark Index: The strategy compares the current asset with a predefined global index (e.g., AMEX) to measure relative performance. The choice of a global benchmark allows the trader to analyze the current asset's movement in the context of broader market trends.

Spread Calculation:

The spread is calculated as the percentage difference between the current asset's closing price and the global benchmark index's closing price:

Spread=Current Asset Close−Global Index CloseGlobal Index Close×100

Spread=Global Index CloseCurrent Asset Close−Global Index Close×100

This metric provides a measure of how the current asset is performing relative to the global index. A positive spread indicates the asset is outperforming the benchmark, while a negative spread signals underperformance.

RSI of the Spread: The RSI is then calculated on the spread values. The RSI is a momentum oscillator that ranges from 0 to 100 and is commonly used to identify overbought or oversold conditions in asset prices. An RSI below 30 is considered oversold, indicating a potential buying opportunity, while an RSI above 70 is overbought, suggesting that the asset may be due for a pullback.

Strategy Logic:

Entry Condition: The strategy enters a long position when the RSI of the spread falls below the oversold threshold (default 30). This suggests that the asset may have been oversold relative to the global benchmark and might be due for a reversal.

Exit Condition: The strategy exits the long position when the RSI of the spread rises above the overbought threshold (default 70), indicating that the asset may have become overbought and a price correction is likely.

Visual Reference:

The RSI of the spread is plotted on the chart for visual reference, making it easier for traders to monitor the relative strength of the asset in relation to the global benchmark.

Overbought and oversold levels are also drawn as horizontal reference lines (70 and 30), along with a neutral level at 50 to show market equilibrium.

Theoretical Basis:

The strategy is built on the mean reversion principle, which suggests that asset prices tend to revert to a long-term average over time. When prices move too far from this mean—either being overbought or oversold—they are likely to correct back toward equilibrium. By using RSI to identify these extremes, the strategy aims to profit from price reversals.

Mean Reversion: According to financial theory, asset prices oscillate around a long-term average, and any extreme deviation (overbought or oversold conditions) presents opportunities for price corrections (Poterba & Summers, 1988).

Momentum Indicators (RSI): The RSI is widely used in technical analysis to measure the momentum of an asset. Its application to the spread between the asset and a global benchmark allows for a more nuanced view of relative performance and potential turning points in the asset's price trajectory.

Practical Application:

This strategy works best in markets where relative strength is a key factor in decision-making, such as in equity indices, commodities, or forex markets. By assessing the performance of the asset relative to a global benchmark and utilizing RSI to identify extremes in price movements, the strategy helps traders to make more informed decisions based on potential mean reversion points.

While the "Global Index Spread RSI Strategy" offers a method for identifying potential price reversals based on relative strength and oversold/overbought conditions, it is important to recognize that no strategy is foolproof. The strategy assumes that the historical relationship between the asset and the global benchmark will hold in the future, but financial markets are subject to a wide array of unpredictable factors that can lead to sudden changes in price behavior.

Risk of False Signals:

The strategy relies heavily on the RSI to trigger buy and sell signals. However, like any momentum-based indicator, RSI can generate false signals, particularly in highly volatile or trending markets. In such conditions, the strategy may enter positions too early or exit too late, leading to potential losses.

Market Context:

The strategy may not account for macroeconomic events, news, or other market forces that could cause sudden shifts in asset prices. External factors, such as geopolitical developments, monetary policy changes, or financial crises, can cause a divergence between the asset and the global benchmark, leading to incorrect conclusions from the strategy.

Overfitting Risk:

As with any strategy that uses historical data to make decisions, there is a risk of overfitting the model to past performance. This could result in a strategy that works well on historical data but performs poorly in live trading conditions due to changes in market dynamics.

Execution Risks:

The strategy does not account for slippage, transaction costs, or liquidity issues, which can impact the execution of trades in real-market conditions. In fast-moving markets, prices may move significantly between order placement and execution, leading to worse-than-expected entry or exit prices.

No Guarantee of Profit:

Past performance is not necessarily indicative of future results. The strategy should be used with caution, and risk management techniques (such as stop losses and position sizing) should always be implemented to protect against significant losses.

Traders should thoroughly test and adapt the strategy in a simulated environment before applying it to live trades, and consider seeking professional advice to ensure that their trading activities align with their risk tolerance and financial goals.

References:

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Gabriel's Witcher Strategy [65 Minute Trading Bot]Strategy Description: Gabriel's Witcher Strategy

Author: Gabriel

Platform: TradingView Pine Script (Version 5)

Backtested Asset: Avalanche (Coinbase Brokage for Volume adjustment)

Timeframe: 65 Minutes

Strategy Type: Comprehensive Trend-Following and Momentum Strategy with Scalping and Risk Management Features

Overview

Gabriel's Witcher Strategy is an advanced trading bot designed for the Avalanche pair on a 65-minute timeframe. This strategy integrates a multitude of technical indicators to identify and execute high-probability trading opportunities. By combining trend-following, momentum, volume analysis, and range filtering, the strategy aims to capitalize on both long and short market movements. Additionally, it incorporates scalping mechanisms and robust risk management features, including take-profit (TP) levels and commission considerations, to optimize trade performance and profitability.

====Key Components====

Source Selection:

Custom Source Flexibility: Allows traders to select from a wide range of price and volume sources (e.g., Close, Open, High, Low, HL2, HLC3, OHLC4, VWAP, On-Balance Volume, etc.) for indicator calculations, enhancing adaptability to various trading styles.

Various curves of Volume Analysis are employed:

Tick Volume Calculation: Utilizes tick volume as a fallback when actual volume data is unavailable, ensuring consistency across different data feeds.

Volume Indicators: Incorporates multiple volume-based indicators such as On-Balance Volume (OBV), Accumulation/Distribution (AccDist), Negative Volume Index (NVI), Positive Volume Index (PVI), and Price Volume Trend (PVT) for comprehensive market analysis.

Trend Indicators:

ADX (Average Directional Index): Measures trend strength using either the Classic or Masanakamura method, with customizable length and threshold settings. It's used to open positions when the mesured trend is strong, or exit when its weak.

Jurik Moving Average (JMA): A smooth moving average that reduces lag, configurable with various parameters including source, resolution, and repainting options.

Parabolic SAR: Identifies potential reversals in market trends with adjustable start, increment, and maximum settings.

Custom Trend Indicator: Utilizes highest and lowest price points over a specified timeframe to determine current and previous trend bases, visually represented with color-filled areas.

Momentum Indicators:

Relative Strength Index (RSI): Evaluates the speed and change of price movements, smoothed with a custom length and source. It's used to not enter the market for shorts in oversold or longs for overbought conditions, and to enter for long in oversold or shorts for overboughts.

Momentum-Based Calculations: Employs both Double Exponential Moving Averages (DEMA) on a MACD-based RSI to enhance momentum signal accuracy which is then further accelerated by a Hull MA. This is the technical analysis tool that determines bearish or bullish momentum.

OBV-Based Momentum Conditions: Uses two exponential moving averages of OBV to determine bullish or bearish momentum shifts, anomalities, breakouts where banks flow their funds in or Smart Money Concepts trade.

Moving Averages (MA):

Multiple MA Types: Includes Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), Hull Moving Average (HMA), and Volume-Weighted Moving Average (VWMA), selectable via input parameters.

MA Speed Calculation: Measures the percentage change in MA values to determine the direction and speed of the trend.

Range Filtering:

Variance-Based Filter: Utilizes variance and moving averages to filter out trades during low-volatility periods, enhancing trade quality.

Color-Coded Range Indicators: Visualizes range filtering with color changes on the chart for quick assessment.

Scalping Mechanism:

Heikin-Ashi Candles: Optionally uses Heikin-Ashi candles for smoother price action analysis.

EMA-Based Trend Detection: Employs fast, medium, and slow EMAs to determine trend direction and potential entry points.

Fractal-Based Filtering: Detects regular or BW (Black & White) fractals to confirm trade signals.

Take Profit (TP) Management:

Dynamic TP Levels: Calculates TP levels based on the number of consecutive long or short entries, adjusting targets to maximize profits.

TP Signals and Re-Entry: Plots TP signals on the chart and allows for automatic re-entry upon TP hit, maintaining continuous trade flow.

Risk Management:

Commission Integration: Accounts for trading commissions to ensure net profitability.

Position Sizing: Configured to use a percentage of equity for each trade, adjustable via input parameters.

Pyramiding: Allows up to one additional position per direction to enhance gains during strong trends.

Alerts and Visual Indicators:

Buy/Sell Signals: Plots visual indicators (triangles and flags) on the chart to signify entry and TP points.

Bar Coloring: Changes bar colors based on ADX and trend conditions for immediate visual cues.

Price Levels: Marks significant price levels related to TP and position entries with cross styles.

Input Parameters

Source Settings:

Custom Sources (srcinput): Choose from various price and volume sources to tailor indicator calculations.

ADX Settings:

ADX Type (ADX_options): Select between 'CLASSIC' and 'MASANAKAMURA' methods.

ADX Length (ADX_len): Defines the period for ADX calculation.

ADX Threshold (th): Sets the minimum ADX value to consider a strong trend.

RSI Settings:

RSI Length (len_3): Period for RSI calculation.

RSI Source (src_3): Source data for RSI.

Trend Strength Settings:

Channel Length (n1): Period for trend channel calculation.

Average Length (n2): Period for smoothing trend strength.

Jurik Moving Average (JMA) Settings:

JMA Source (inp): Source data for JMA.

JMA Resolution (reso): Timeframe for JMA calculation.

JMA Repainting (rep): Option to allow JMA to repaint.

JMA Length (lengths): Period for JMA.

Parabolic SAR Settings:

SAR Start (start): Initial acceleration factor.

SAR Increment (increment): Acceleration factor increment.

SAR Maximum (maximum): Maximum acceleration factor.

SAR Point Width (width): Visual width of SAR points.

Trend Indicator Settings:

Trend Timeframe (timeframe): Period for trend indicator calculations.

Momentum Settings:

Source Type (srcType): Select between 'Price' and 'VWAP'.

Momentum Source (srcPrice): Source data for momentum calculations.

RSI Length (rsiLen): Period for momentum RSI.

Smooth Length (sLen): Smoothing period for momentum RSI.

OBV Settings:

OBV Line 1 (e1): EMA period for OBV line 1.

OBV Line 2 (e2): EMA period for OBV line 2.

Moving Average (MA) Settings:

MA Length (length): Period for MA calculations.

MA Type (matype): Select MA type (1: SMA, 2: EMA, 3: HMA, 4: WMA, 5: VWMA).

Range Filter Settings:

Range Filter Length (length0): Period for range filtering.

Range Filter Multiplier (mult): Multiplier for range variance.

Take Profit (TP) Settings:

TP Long (tp_long0): Percentage for long TP.

TP Short (tp_short0): Percentage for short TP.

Scalping Settings:

Scalping Activation (ACT_SCLP): Enable or disable scalping.

Scalping Length (HiLoLen): Period for scalping indicators.

Fast EMA Length (fastEMAlength): Period for fast EMA in scalping.

Medium EMA Length (mediumEMAlength): Period for medium EMA in scalping.

Slow EMA Length (slowEMAlength): Period for slow EMA in scalping.

Filter (filterBW): Enable or disable additional fractal filtering.

Pullback Lookback (Lookback): Number of bars for pullback consideration.

Use Heikin-Ashi Candles (UseHAcandles): Option to use Heikin-Ashi candles for smoother trend analysis.

Strategy Logic

Indicator Calculations:

Volume and Source Selection: Determines the primary data source based on user input, ensuring flexibility and adaptability.

ADX Calculation: Computes ADX using either the Classic or Masanakamura method to assess trend strength.

RSI Calculation: Evaluates market momentum using RSI, further smoothed with custom periods.

Trend Strength Assessment: Utilizes trend channel and average lengths to gauge the robustness of current trends.

Jurik Moving Average (JMA): Smooths price data to reduce lag and enhance trend detection.

Parabolic SAR: Identifies potential trend reversals with adjustable parameters for sensitivity.

Momentum Analysis: Combines RSI with DEMA and OBV-based conditions to confirm bullish or bearish momentum.

Moving Averages: Employs multiple MA types to determine trend direction and speed.

Range Filtering: Filters out low-volatility periods to focus on high-probability trades.

Trade Conditions:

Long Entry Conditions:

ADX Confirmation: ADX must be above the threshold, indicating a strong uptrend.

RSI and Momentum: RSI below 70 and positive momentum signals.

JMA and SAR: JMA indicates an uptrend, and Parabolic SAR is below the price.

Trend Indicator: Confirms the current trend direction.

Range Filter: Ensures market is in an upward range.

Scalping Option: If enabled, additional scalping conditions must be met.

Short Entry Conditions:

ADX Confirmation: ADX must be above the threshold, indicating a strong downtrend.

RSI and Momentum: RSI above 30 and negative momentum signals.

JMA and SAR: JMA indicates a downtrend, and Parabolic SAR is above the price.

Trend Indicator: Confirms the current trend direction.

Range Filter: Ensures market is in a downward range.

Scalping Option: If enabled, additional scalping conditions must be met.

Position Management:

Entry Execution: Places long or short orders based on the identified conditions and user-selected position types (Longs, Shorts, or Both).

Take Profit (TP): Automatically sets TP levels based on predefined percentages, adjusting dynamically with consecutive trades.

Re-Entry Mechanism: Allows for automatic re-entry upon TP hit, maintaining active trading positions.

Exit Conditions: Closes positions when TP levels are reached or when opposing trend signals are detected.

Visual Indicators:

Bar Coloring: Highlights bars in green for bullish conditions, red for bearish, and orange for neutral.

Plotting Price Levels: Marks significant price levels related to TP and trade entries with cross symbols.

Signal Shapes: Displays triangle and flag shapes on the chart to indicate trade entries and TP hits.

Alerts:

Custom Alerts: Configured to notify traders of long entries, short entries, and TP hits, enabling timely trade management and execution.

Usage Instructions

Setup:

Apply the Strategy: Add the script to your TradingView chart set to BTCUSDT with a 65-minute timeframe.

Configure Inputs: Adjust the input parameters under their respective groups (e.g., Source Settings, ADX, RSI, Trend Strength, etc.) to match your trading preferences and risk tolerance.

Position Selection:

Choose Position Type: Use the Position input to select Longs, Shorts, or Both based on your market outlook.

Execution: The strategy will automatically execute and manage positions according to the selected type, ensuring targeted trading actions.

Signal Interpretation:

Buy Signals: Blue triangles below the bars indicate potential long entry points.

Sell Signals: Red triangles above the bars indicate potential short entry points.

Take Profit Signals: Flags above or below the bars signify TP hits for long and short positions, respectively.

Bar Colors: Green bars suggest bullish conditions, red bars indicate bearish conditions, and orange bars represent neutral or consolidating markets.

Risk Management:

Default Position Size: Set to 100% of equity. Adjust the default_qty_value as needed for your risk management strategy.

Commission: Accounts for a 0.1% commission per trade. Adjust the commission_value to match your broker's fees.

Pyramiding: Allows up to one additional position per direction to enhance gains during strong trends.

Backtesting and Optimization:

Historical Testing: Utilize TradingView's backtesting features to evaluate the strategy's performance over historical data.

Parameter Tuning: Optimize input parameters to align the strategy with current market dynamics and personal trading objectives.

Alerts Configuration:

Set Up Alerts: Enable and configure alerts based on the predefined alertcondition statements to receive real-time notifications of trade signals and TP hits.

Additional Features

Comprehensive Indicator Integration: Combines multiple technical indicators to provide a holistic view of market conditions, enhancing trade signal accuracy.

Scalping Options: Offers an optional scalping mechanism to capitalize on short-term price movements, increasing trading flexibility.

Dynamic Take Profit Levels: Adjusts TP targets based on the number of consecutive trades, maximizing profit potential during favorable trends.

Advanced Volume Analysis: Utilizes various volume indicators to confirm trend strength and validate trade signals.

Customizable Range Filtering: Filters trades based on market volatility, ensuring trades are taken during optimal conditions.

Heikin-Ashi Candle Support: Optionally uses Heikin-Ashi candles for smoother price action analysis and reduced noise.

====Recommendations====

Thorough Backtesting:

Historical Performance: Before deploying the strategy in a live trading environment, perform comprehensive backtesting to understand its performance under various market conditions. These are the premium settings for Avalanche Coinbase.

Optimization: Regularly review and adjust input parameters to ensure the strategy remains effective amidst changing market volatility and trends. Backtest the strategy for each crypto and make sure you are in the right brokage when using the volume sources as it will affect the overall outcome of the trading strategy.

Risk Management:

Position Sizing: Adjust the default_qty_value to align with your risk tolerance and account size.

Stop-Loss Implementation: Although the strategy includes TP levels, they're also consided to be a stop-loss mechanisms to protect against adverse market movements.

Commission Adjustment: Ensure the commission_value accurately reflects your broker's fees to maintain realistic backtesting results. Generally, 0.1~0.3% are most of the average broker's comission fees.

Slipage: The slip comssion is 1 Tick, since the strategy is adjusted to only enter/exit on bar close where most positions are available.

Continuous Monitoring:

Strategy Performance: Regularly monitor the strategy's performance to ensure it operates as expected and make adjustments as needed. A max-drawndown hit has been added to operate in case the premium Avalanche settings go wrong, but you can turn it off an adjust the equity percentage to 50% if you are confortable with the high volatile max-drown or even 100% if your account allows you to borrow cash.

Customization:

Indicator Parameters: Tailor indicator settings (e.g., ADX length, RSI period, MA types) to better fit your specific trading style and market conditions.

Scalping Options: Enable or disable scalping based on your trading preferences and risk appetite.

Conclusion

Gabriel's Witcher Strategy is a robust and versatile trading solution designed to navigate the complexities of the Crypto market. By integrating a wide array of technical indicators and providing extensive customization options, this strategy empowers traders to execute informed and strategic trades. Its comprehensive approach, combining trend analysis, momentum detection, volume evaluation, and range filtering, ensures that trades are taken during optimal market conditions. Additionally, the inclusion of scalping features and dynamic take-profit management enhances the strategy's adaptability and profitability potential. Unlike any trading strategy, with both diligent testing and continuous monitoring under the strategy tester, it's possible to achieve sustained success by adjusting the settings to the individual Crypto that need it, for example this one is preset for Avalanche Coinbase 65 Miinutes but it can be adjust for BTCUSD or Etherium if you backtest and search for the right settings.

Self Optimizing RSI and Self Adaptive TP/SL [Starbots]Self Optimizing RSI and Self Adaptive TP/SL Strategy. (non-repainting)

This script continuously backtests 20 different combinations of RSI Buy conditions across 5 different Take Profit/Stop Loss combinations. In total, it tests 100 variants on every bar close and records the Net Profit gained for each combination. The strategy then selects and uses the best-performing combination of settings currently available for you to trade.

---------------------------------------------------------------------------------------------------------

The Relative Strength Index (RSI), developed by J. Welles Wilder, is a momentum oscillator that measures the speed and change of price movements. The RSI oscillates between zero and 100. Traditionally the RSI is considered overbought when above 70 and oversold when below 30. Signals can be generated by looking for divergences and failure swings. RSI can also be used to identify the general trend.

To improve our results we are calculating Multiple Length RSI - Average RSI based on the multiple periods. You can use just 1 Length or Multiple.

Set Inputs to Min=14, Max=14 if you want to use just 1 period.

= RSI(14)

3 RSI Lengths example (12,13 and 14):

Min=12, Max=14

(12+13+14) / 3 = avg. RSI

-----------------------------------------------------------------------------------------------------------

Backtester - Optimizer Explained:

The backtester runs numerous backtests in the background to optimize trading strategies. Here’s how it works:

Default Inputs (Combinations of TP/SL)

TP 1%, SL4%

TP 2%, SL4%

TP 3%, SL4%

TP 2%, SL5%

TP 4.5%, SL10%

Default Inputs (RSI Crossover Buys) :

18 ,20,21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,45,55, 69

_______________________________________________________

Backtest RSI Crossover 18:

TP1%, SL4% => Save net profit

TP2%, SL4% => Save net profit

TP3%, SL4% => Save net profit

TP2%, SL5% => Save net profit

TP4.5%, SL10% => Save net profit

,...

,...

Backtest RSI Crossover 69:

TP1%, SL4% => Save net profit

TP2%, SL4% => Save net profit

TP3%, SL4% => Save net profit

TP2%, SL5% => Save net profit

TP4.5%, SL10% => Save net profit

Self Optimizing Buy Condition and Self Optimizing Take Profit - Stop Los

This process involves testing various combinations of RSI crossover values with different Take Profit (TP) and Stop Loss (SL) percentages. The net profit for each combination is saved, allowing the optimizer to select the best-performing settings for trading.

It recalculates on every bar close. If one combination starts performing better than others—achieving a higher net profit gain (essentially like running 100 backtests with different settings in the background)—the strategy switches to that combination of TP/SL and Buy condition. It continues trading with the new settings until another parameter starts performing better and the strategy switches to that setting.

________________________________________________________________________

If you wish to use it as INDICATOR - turn on 'Recalculate - On every tick' in Properties tab to have this script updating constantly and use it as a normal Indicator tool for manual trading.

Other functions:

Set the %fee for optimizing engine. If you set this % higher, you also punish small average trades and make the strategy prefer larger avg. trades, giving you better chances to make your strategy profitable.

Trade with trend and optimize the strategy only when the market is uptrending with EMA/HMA

Use Moving Average of avg.RSI and smooth the values for indicator even more. (Yes strategy is self optimizing RSI or avg.RSI or RSI-MA, you can select all sorts of this indicator for optimizing)

All trading alerts are working and functional, if you want to automate the strategy

This script is simple to use for any trader as it saves a lot of time for searching good parameters on your own. It's self-optimizing and adjusting to the markets on the go.

Dual RSI Differential - Strategy [presentTrading]█ Introduction and How it is Different

The Dual RSI Differential Strategy introduces a nuanced approach to market analysis and trading decisions by utilizing two Relative Strength Index (RSI) indicators calculated over different time periods. Unlike traditional strategies that employ a single RSI and may signal premature or delayed entries, this method leverages the differential between a shorter and a longer RSI. This approach pinpoints more precise entry and exit points, providing a refined tool for traders to exploit market conditions effectively, particularly in overbought and oversold scenarios.

Most important: it is a good eductional code for swing trading.

For beginners, this Pine Script provides a complete function that includes crucial elements such as holding days and the option to configure take profit/stop loss settings:

- Hold Days: This feature ensures that trades are not exited too hastily, helping traders to ride out short-term market volatility. It's particularly valuable for swing trading where maintaining positions slightly longer can lead to capturing significant trends.

- TPSL Condition (None by default): This setting allows traders to focus solely on the strategy's robust entry and exit signals without being constrained by preset profit or loss limits. This flexibility is crucial for learning to adjust strategy settings based on personal risk tolerance and market observations.

BTCUSD 6h LS Performance

█ Strategy, How It Works: Detailed Explanation

🔶 RSI Calculation:

The RSI is a momentum oscillator that measures the speed and change of price movements. It is calculated using the formula:

RSI = 100 - (100 / (1 + RS))

Where RS (Relative Strength) = Average Gain of up periods / Average Loss of down periods.

🔶 Dual RSI Setup:

This strategy involves two RSI indicators:

RSI_Short (RSI_21): Calculated over a short period (21 days).

RSI_Long (RSI_42): Calculated over a longer period (42 days).

Differential Calculation:

The strategy focuses on the differential between these two RSIs:

RSI Differential = RSI_Long - RSI_Short

This differential helps to identify when the shorter-term sentiment diverges from longer-term trends, signaling potential trading opportunities.

BTCUSD Local picuture

🔶 Signal Triggers:

Entry Signal: A buy (long) signal is triggered when the RSI Differential exceeds -5, suggesting strengthening short-term momentum. Conversely, a sell (short) signal occurs when the RSI Differential falls below +5, indicating weakening short-term momentum.

Exit Signal: Trades are generally exited when the RSI Differential reverses past these thresholds, indicating a potential momentum shift.

█ Trade Direction

This strategy accommodates various trading preferences by allowing selections among long, short, or both directions, thus enabling traders to capitalize on diverse market movements and volatility.

█ Usage

The Dual RSI Differential Strategy is particularly suited for:

Traders who prefer a systematic approach to capture market trends.

Those who seek to minimize risks associated with rapid and unexpected market movements.

Traders who value strategies that can be finely tuned to different market conditions.

█ Default Settings

- Trading Direction: Both — allows capturing of upward and downward market movements.

- Short RSI Period: 21 days — balances sensitivity to market movements.

- Long RSI Period: 42 days — smoothens out longer-term fluctuations to provide a clearer market trend.

- RSI Difference Level: 5 — minimizes false signals by setting a moderate threshold for action.

Use Hold Days: True — introduces a temporal element to trading strategy, holding positions to potentially enhance outcomes.

- Hold Days: 5 — ensures that trades are not exited too hastily, helping to ride out short-term volatility.

- TPSL Condition: None — enables traders to focus solely on the strategy's entry and exit signals without preset profit or loss limits.

- Take Profit Percentage: 15% — aims for significant market moves to lock in profits.

- Stop Loss Percentage: 10% — safeguards against large losses, essential for long-term capital preservation.

D-BoT Alpha 'Short' SMA and RSI StrategyDostlar selamlar,

İşte son derece basit ama etkili ve hızlı, HTF de çok iyi sonuçlar veren bir strateji daha, hepinize bol kazançlar dilerim ...

Nedir, Nasıl Çalışır:

Strateji, iki ana girdiye dayanır: SMA ve RSI. SMA hesaplama aralığı 200 olarak, RSI ise 14 olarak ayarlanmıştır. Bu değerler, kullanıcı tercihlerine veya geriye dönük test sonuçlarına göre ayarlanabilir.

Strateji, iki koşul karşılandığında bir short sinyali oluşturur: RSI değeri, belirlenen bir giriş seviyesini (burada 51 olarak belirlenmiş) aşar ve kapanış fiyatı SMA değerinin altındadır.

Strateji, kısa pozisyonu üç durumda kapatır: Kapanış fiyatı, takip eden durdurma seviyesinden (pozisyon açıldığından beri en düşük kapanış olarak belirlenmiştir) büyükse, RSI değeri belirlenen bir durdurma seviyesini (bu durumda 54) aşarsa veya RSI değeri belirli bir kar al seviyesinin (bu durumda 32) altına düşerse.

Güçlü Yönleri:

İki farklı gösterge (SMA ve RSI) kullanımı, yalnızca birini kullanmaktan daha sağlam bir sinyal sağlayabilir.

Strateji, karları korumaya ve fiyat dalgalanmalarında kayıpları sınırlamaya yardımcı olabilecek bir iz süren durdurma seviyesi içerir.

Script oldukça anlaşılır ve değiştirmesi nispeten kolaydır.

Zayıf Yönleri:

Strateji, hacim, oynaklık veya daha geniş piyasa eğilimleri gibi diğer potansiyel önemli faktörleri göz önünde bulundurmaz.

RSI seviyeleri ve SMA süresi için belirli parametreler sabittir ve tüm piyasa koşulları veya zaman aralıkları için optimal olmayabilir.

Strateji oldukça basittir. Trade maliyetini (kayma veya komisyonlar gibi) hesaba katmaz, bu da trade performansını önemli ölçüde etkileyebilir.

Bu Stratejiyle Nasıl İşlem Yapılır:

Strateji, short işlemler için tasarlanmıştır. RSI, 51'in üzerine çıktığında ve kapanış fiyatı 200 periyotluk SMA'nın altında olduğunda işleme girer. RSI, 54'ün üzerine çıktığında veya 32'nin altına düştüğünde veya fiyat, pozisyon açıldığından beri en düşük kapanış fiyatının üzerine çıktığında işlemi kapatır.

Lütfen Dikkat, bu strateji veya herhangi bir strateji izole bir şekilde kullanılmamalıdır. Tüm bu çalışmalar eğitsel amaçlıdır. Yatırım tavsiyesi içermez.

This script defines a trading strategy based on Simple Moving Average (SMA) and the Relative Strength Index (RSI) indicators. Here's an overview of how it works, along with its strengths and weaknesses, and how to trade using this strategy:

How it works:

The strategy involves two key inputs: SMA and RSI. The SMA length is set to 200, and the RSI length is set to 14. These values can be adjusted based on user preferences or back-testing results.

The strategy generates a short signal when two conditions are met: The RSI value crosses over a defined entry level (set at 51 here), and the closing price is below the SMA value.

When a short signal is generated, the strategy opens a short position.

The strategy closes the short position under three conditions: If the close price is greater than the trailing stop (which is set as the lowest close since the position opened), if the RSI value exceeds a defined stop level (54 in this case), or if the RSI value drops below a certain take-profit level (32 in this case).

Strengths:

The use of two different indicators (SMA and RSI) can provide a more robust signal than using just one.

The strategy includes a trailing stop, which can help to protect profits and limit losses as the price fluctuates.

The script is straightforward and relatively easy to understand and modify.

Weaknesses:

The strategy doesn't consider other potentially important factors, such as volume, volatility, or broader market trends.

The specific parameters for the RSI levels and SMA length are hard-coded, and may not be optimal for all market conditions or timeframes.

The strategy is very simplistic. It doesn't take into account the cost of trading (like slippage or commissions), which can significantly impact trading performance.

How to trade with this strategy:

The strategy is designed for short trades. It enters a trade when the RSI crosses above 51 and the closing price is below the 200-period SMA. It will exit the trade when the RSI goes above 54 or falls below 32, or when the price rises above the lowest closing price since the position was opened.

Please note, this strategy or any strategy should not be used in isolation. It's important to consider other aspects of trading such as risk management, capital allocation, and combining different strategies to diversify. Back-testing the strategy on historical data and demo trading before going live is also a recommended practice.

D-Bot Alpha RSI Breakout StrategyHello dear Traders,

Here is a simple yet effective strategy to use, for best profit higher time frame, such as daily.

Structure of the code

The code defines inputs for SMA (simple moving average) length, RSI (relative strength index) length, RSI entry level, RSI stop loss level, and RSI take profit level. The default values of these variables can be customized as per the user's preferences.

The script calculates SMA and RSI based on the input parameters and the closing price of the asset.

Trading logic

This strategy allows the placement of a long position when:

The RSI crosses above the RSI entry level and

The close price is above the SMA value.

After entering a long position, it applies a trailing stop mechanism. The stop price is updated to the close price if the close price is lower than the last close price.

The script closes the long position when:

RSI falls below the stop loss level.

RSI reaches or exceeds the take profit level.

If the trailing stop is activated (once RSI reaches or exceeds the take profit level), the closing price falls below the trailing stop level.

Strengths

The strategy includes mechanisms for entering a position, taking profit, and stopping losses, which are fundamental aspects of a trading strategy.

It applies a trailing stop mechanism that allows to capture further gains if the price keeps increasing while protecting from losses if the price starts to decrease.

Weaknesses

This strategy only contemplates long positions. Depending on the market situation, the strategy may miss opportunities for short selling when the market is on a downward trend.

The choice of the fixed RSI entry, stop loss, and take profit levels may not be ideal for all market conditions or assets. It might benefit from a more adaptive mechanism that adjusts these levels according to market volatility or trend.

The strategy doesn't factor in trading costs (such as spread or commission), which could have a significant impact on the net profit, especially if the user is trading with a high frequency or in a low liquidity market.

How to trade with this strategy

Given these parameters and the strategy outlined by the code, the trader would enter a long position when the RSI crosses above the RSI entry level (default 34) and the closing price is above the SMA value (SMA calculated with default period of 200). The trader would exit the position when either the RSI falls below the RSI stop loss level (default 30), or RSI rises above the RSI take profit level (default 50), or when the trailing stop is hit.

Remember "The strategies I have prepared are entirely for educational purposes and should not be considered as investment advice. Support your trades using other tools. Wishing everyone profitable trades..."

SMA_Cross + RSI1. long

a. RSI does not open an order when it is overbought, until the RSI falls below a certain threshold, and then open a position

b. There are already many positions. If the RSI is overbought, it will be profitable. When the RSI falls below a certain threshold, open a long position again until the moving average crossover signal turns short.

2. Short

a. RSI does not open an order when it is oversold, and then opens a position after RSI rises to a certain threshold

b. There are already short positions. If the RSI is oversold, it will be profitable to close the short position. When the RSI rises above a certain threshold, open the short position again until there is a reversal of the moving average crossing signal.

1. 做多

a. RSI在超买区间时不开单,直到RSI回落到某个阈值之下,再开仓

b. 已经有多仓,如果RSI超买,则平多获利,当RSI回落到某个阈值之下后,再次开多,直到有均线交叉信号反转做空

2. 做空

a. RSI在超卖区间时不开单,直到RSI上升到某个阈值之后,再开仓

b. 已经有空仓,如果RSI超卖,则平空获利,当RSI上升到某个阈值之上后,再次开空,直到有均线交叉信号反转做多

AVWAP+RSI Confluence — 1R TesterRSI + 1R ATR - Monthly P\&L (v4)

WHAT THIS STRATEGY DOES (OVERVIEW)

* Pine strategy (v4) that combines a simple momentum trigger with a symmetric 1R ATR risk model and an on-chart Monthly/Yearly P\&L table.

* Momentum filter: trades only when RSI crosses its own SMA in the direction of the trend (price vs Trend EMA).

* Risk engine: exits use fixed 1R ATR brackets captured at entry (no drifting targets/stops).

* Accounting: the table aggregates percentage returns by month and year using strategy equity.

ENTRY LOGIC (LONGS & OPTIONAL SHORTS)

Indicators used:

* RSI(rsiLen) and its SMA: SMA(RSI, rsiMaLen)

* Trend filter: EMA(emaTrendLen) on price

Longs:

1. RSI crosses above its RSI SMA

2. RSI > rsiBuyThr (filters weak momentum)

3. Close > EMA(emaTrendLen)

Shorts (optional via enableShort):

1. RSI crosses below its RSI SMA

2. RSI < rsiSellThr

3. Close < EMA(emaTrendLen)

EXIT LOGIC AND RISK MODEL (1R ATR)

* On entry, snapshot ATR(atrLen) into atrAtEntry and the average fill price into entryPx.

* Longs: stop = entryPx - ATR \* atrMult; target = entryPx + ATR \* atrMult

* Shorts: mirrored.

* Stops and targets are posted immediately and remain fixed for the life of the trade.

POSITION SIZING AND COSTS

* Default position size: 25% of equity per trade (adjustable in Properties/inputs).

* Commission percent and a small slippage are set in strategy() so backtests include friction by default.

MONTHLY / YEARLY P\&L TABLE (HOW IT WORKS)

* Uses strategy equity to compute bar returns: equity / equity\ - 1.

* Compounds bar returns into current month and current year; commits each finished period at month/year change (or last bar).

* Renders rows as years; columns Jan..Dec plus a Year total column.

* Cells colored by sign; precision and maximum rows are controlled by inputs.

* Values represent percentage returns, not currency P\&L.

VISUAL AIDS

* Two pivot trails (pivot high/low) are plotted for context only; they do not affect entries or exits.

CUSTOMIZATION TIPS

* Raise rsiBuyThr (long) or lower rsiSellThr (short) to filter weak momentum.

* Increase emaTrendLen to tighten trend alignment.

* Adjust atrLen and atrMult to fit your timeframe/instrument volatility.

* Leave enableShort = false if you prefer long-only behavior or shorting is constrained.

NON-REPAINTING AND BACKTEST NOTES

* Signals use bar-close crosses of built-in indicators (RSI, EMA, ATR); no future bars are referenced.

* calc\_on\_every\_tick = true for responsive visuals; Strategy Tester evaluates on bar close in history.

* Backtest stop/limit fills are simulated and may differ from live execution/liquidity.

DISCLAIMERS

* Educational use only. This is not financial advice. Markets involve risk. Past performance does not guarantee future results.

INPUTS (QUICK REFERENCE)

* rsiLen, rsiMaLen, rsiBuyThr, rsiSellThr

* emaTrendLen

* atrLen, atrMult, enableShort

* leftBars, rightBars, prec, showTable, maxYearsRows

SHORT TAGLINE

RSI momentum with 1R ATR brackets and a built-in Monthly/Yearly P\&L table.

TAGS

strategy, RSI, ATR, trend, risk-management, backtest, Pine-v4

Imbalance RSI Divergence Strategy# Imbalance RSI Divergence Strategy - User Guide

## What is This Strategy?

This strategy identifies **imbalance** zones in the market and combines them with **RSI divergence** to generate trading signals. It aims to capitalize on price gaps left by institutional investors and large volume movements.

### Main Settings

- **RSI Period (14)**: Period used for RSI calculation. Lower values = more sensitive, higher values = more stable signals.

- **ATR Period (10)**: Period for volatility measurement using Average True Range.

- **ATR Stop Loss Multiplier (2.0)**: How many ATR units to use for stop loss calculation.

- **Risk:Reward Ratio (4.0)**: Risk-reward ratio. 2.0 = 2 units of reward for 1 unit of risk.

- **Use RSI Divergence Filter (true)**: Enables/disables the RSI divergence filter.

### Imbalance Filters

- **Minimum Imbalance Size (ATR) (0.3)**: Minimum imbalance size in ATR units to filter out small imbalances.

- **Enable Lookback Limit (false)**: Activates historical lookback limitations.

- **Maximum Lookback Bars (300)**: Maximum number of bars to look back.

### Visual Settings

- **Show Imbalance Size**: Displays imbalance size in ATR units.

- **Show RSI Divergence Lines**: Shows/hides divergence lines.

- **Divergence Line Colors**: Colors for bullish/bearish divergence lines.

### Volatility-Based Adjustments

- **Low volatility markets**:

- Minimum Imbalance Size: 0.2-0.4 ATR

- ATR Stop Loss Multiplier: 1.5-2.0

- **High volatility markets**:

- Minimum Imbalance Size: 0.5-1.0 ATR

- ATR Stop Loss Multiplier: 2.5-3.5

### Risk Tolerance

- **Conservative approach**:

- Risk:Reward Ratio: 2.0-3.0

- RSI Divergence Filter: Enabled

- Minimum Imbalance Size: Higher (0.5+ ATR)

- **Aggressive approach**:

- Risk:Reward Ratio: 4.0-6.0

- Minimum Imbalance Size: Lower (0.2-0.3 ATR)

###Market Conditions

- **Trending markets**: Higher RSI Period (21-28)

- **Sideways markets**: Lower RSI Period (10-14)

- **Volatile markets**: Higher ATR Multiplier

## Recommended Testing Procedure

1. **Start with default settings** and backtest on 3-6 months of historical data

2. **Adjust RSI Period** to see which value produces better results

3. **Optimize ATR Multiplier** for stop loss levels

4. **Test different Risk:Reward ratios** comparatively

5. **Fine-tune Minimum Imbalance Size** to improve signal quality

## Important Considerations

- **False positive signals**: Imbalances may be less reliable during low volatility periods

- **Market openings**: First hours often produce more imbalances but can be riskier

- **News events**: Consider disabling strategy during major news releases

- **Backtesting**: Test across different market conditions (trending, sideways, volatile)

## Recommended Settings for Beginners

**Safe settings for new users:**

- RSI Period: 14

- ATR Period: 14

- ATR Stop Loss Multiplier: 2.5

- Risk:Reward Ratio: 3.0

- Minimum Imbalance Size: 0.5 ATR

- RSI Divergence Filter: Enabled

## Advanced Tips

### Signal Quality Improvement

- **Combine with market structure**: Look for imbalances near key support/resistance levels

- **Volume confirmation**: Higher volume during imbalance formation increases reliability

- **Multiple timeframe analysis**: Confirm signals on higher timeframes

### Risk Management

- **Position sizing**: Never risk more than 1-2% of account per trade

- **Maximum drawdown**: Set overall stop loss for the strategy

- **Market hours**: Consider avoiding low liquidity periods

### Performance Monitoring

- **Win rate**: Track percentage of profitable trades

- **Average R:R**: Monitor actual risk-reward achieved vs. target

- **Maximum consecutive losses**: Set alerts for strategy review

This strategy works best when combined with proper risk management and market analysis. Always backtest thoroughly before using real money and adjust parameters based on your specific market and trading style.

System 0530 - Stoch RSI Strategy with ATR filterStrategy Description: System 0530 - Multi-Timeframe Stochastic RSI with ATR Filter

Overview:

This strategy, "System 0530," is designed to identify trading opportunities by leveraging the Stochastic RSI indicator across two different timeframes: a shorter timeframe for initial signal triggers (assumed to be the chart's current timeframe, e.g., 5-minute) and a longer timeframe (15-minute) for signal confirmation. It incorporates an ATR (Average True Range) filter to help ensure trades are taken during periods of adequate market volatility and includes a cooldown mechanism to prevent rapid, successive signals in the same direction. Trade exits are primarily handled by reversing signals.

How It Works:

1. Signal Initiation (e.g., 5-Minute Timeframe):

Long Signal Wait: A potential long entry is considered when the 5-minute Stochastic RSI %K line crosses above its %D line, AND the %K value at the time of the cross is at or below a user-defined oversold level (default: 30).

Short Signal Wait: A potential short entry is considered when the 5-minute Stochastic RSI %K line crosses below its %D line, AND the %K value at the time of the cross is at or above a user-defined overbought level (default: 70). When these conditions are met, the strategy enters a "waiting state" for confirmation from the 15-minute timeframe.

2. Signal Confirmation (15-Minute Timeframe):

Once in a waiting state, the strategy looks for confirmation on the 15-minute Stochastic RSI within a user-defined number of 5-minute bars (wait_window_5min_bars, default: 5 bars).

Long Confirmation:

The 15-minute Stochastic RSI %K must be greater than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be below a user-defined threshold (stoch_15min_long_entry_level, default: 40).

Short Confirmation:

The 15-minute Stochastic RSI %K must be less than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be above a user-defined threshold (stoch_15min_short_entry_level, default: 60).

3. Filters:

ATR Volatility Filter: If enabled, trades are only confirmed if the current ATR value (converted to ticks) is above a user-defined minimum threshold (min_atr_value_ticks). This helps to avoid taking signals during periods of very low market volatility. If the ATR condition is not met, the strategy continues to wait for the condition to be met within the confirmation window, provided other conditions still hold.

Signal Cooldown Filter: If enabled, after a signal is generated, the strategy will wait for a minimum number of bars (min_bars_between_signals) before allowing another signal in the same direction. This aims to reduce overtrading.

4. Entry and Exit Logic:

Entry: A strategy.entry() order is placed when all trigger, confirmation, and filter conditions are met.

Exit: This strategy primarily uses reversing signals for exits. For example, if a long position is open, a confirmed short signal will close the long position and open a new short position. There are no explicit take profit or stop loss orders programmed into this version of the script.

Key User-Adjustable Parameters:

Stochastic RSI Parameters: RSI Length, Stochastic RSI Length, %K Smoothing, %D Smoothing.

Signal Trigger & Confirmation:

5-minute %K trigger levels for long and short.

15-minute %K confirmation thresholds for long and short.

Wait window (in 5-minute bars) for 15-minute confirmation.

Filters:

Enable/disable and configure the Signal Cooldown filter (minimum bars between signals).

Enable/disable and configure the ATR Volatility filter (ATR period, minimum ATR value in ticks).

Strategy Parameters:

Leverage Multiplier (Note: This primarily affects theoretical position sizing for backtesting calculations in TradingView and does not simulate actual leveraged trading risks).

Recommendations for Users:

Thorough Backtesting: Test this strategy extensively on historical data for the instruments and timeframes you intend to trade.

Parameter Optimization: Experiment with different parameter settings to find what works best for your trading style and chosen markets. The default values are starting points and may not be optimal for all conditions.

Understand the Logic: Ensure you understand how each component (Stochastic RSI on different timeframes, ATR filter, cooldown) interacts to generate signals.

Risk Management: Since this version does not include explicit stop-loss orders, ensure you have a clear risk management plan in place if trading this strategy live. You might consider manually adding stop-loss orders through your broker or using TradingView's separate strategy order settings for stop-loss if applicable.

Disclaimer:

This strategy description is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Trading involves significant risk of loss. Always do your own research and understand the risks before trading.

Forex Fire EMA/MA/RSI StrategyEURUSD

The entry method in the Forex Fire EMA/MA/RSI Strategy combines several conditions across two timeframes. Here's a breakdown of how entries are determined:

Long Entry Conditions:

15-Minute Timeframe Conditions:

EMA 13 > EMA 62 (short-term momentum is bullish)

Price > MA 200 (trading above the major trend indicator)

Fast RSI (7) > Slow RSI (28) (momentum is increasing)

Fast RSI > 50 (showing bullish momentum)

Volume is increasing compared to 20-period average

4-Hour Timeframe Confluence:

EMA 13 > EMA 62 (larger timeframe confirms bullish trend)

Price > MA 200 (confirming overall uptrend)

Slow RSI (28) > 40 (showing bullish bias)

Fast RSI > Slow RSI (momentum is supporting the move)

Additional Precision Requirement:

Either EMA 13 has just crossed above EMA 62 (crossover)

OR price has just crossed above MA 200

Short Entry Conditions:

15-Minute Timeframe Conditions:

EMA 13 < EMA 62 (short-term momentum is bearish)

Price < MA 200 (trading below the major trend indicator)

Fast RSI (7) < Slow RSI (28) (momentum is decreasing)

Fast RSI < 50 (showing bearish momentum)

Volume is increasing compared to 20-period average

4-Hour Timeframe Confluence:

EMA 13 < EMA 62 (larger timeframe confirms bearish trend)

Price < MA 200 (confirming overall downtrend)

Slow RSI (28) < 60 (showing bearish bias)

Fast RSI < Slow RSI (momentum is supporting the move)

Additional Precision Requirement:

Either EMA 13 has just crossed under EMA 62 (crossunder)

OR price has just crossed under MA 200

The key aspect of this strategy is that it requires alignment between the shorter timeframe (15m) and the larger timeframe (4h), which helps filter out false signals and focuses on trades that have strong multi-timeframe support. The crossover/crossunder requirement further refines entries by looking for actual changes in direction rather than just conditions that might have been in place for a long time.

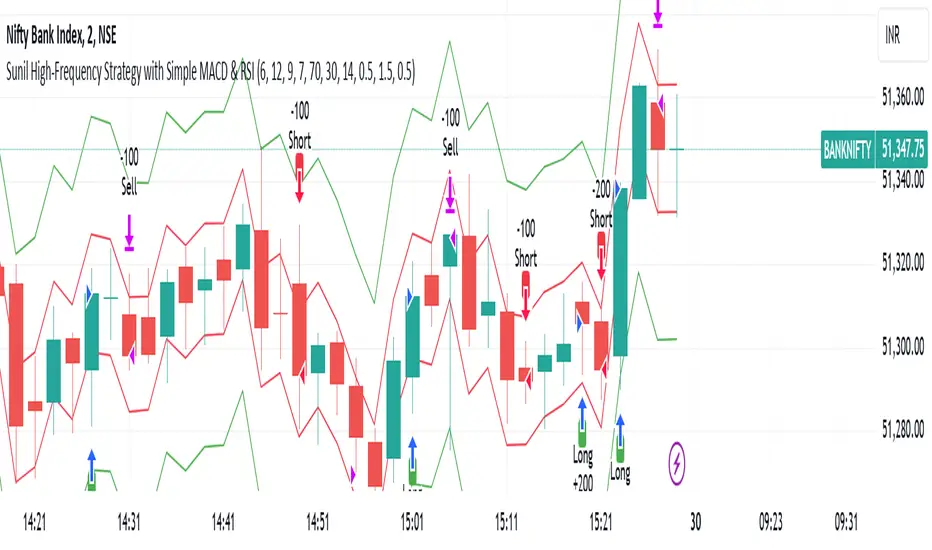

Sunil High-Frequency Strategy with Simple MACD & RSISunil High-Frequency Strategy with Simple MACD & RSI

This high-frequency trading strategy uses a combination of MACD and RSI to identify quick market opportunities. By leveraging these indicators, combined with dynamic risk management using ATR, it aims to capture small but frequent price movements while ensuring tight control over risk.

Key Features:

Indicators Used:

MACD (Moving Average Convergence Divergence): The strategy uses a shorter MACD configuration (Fast Length of 6 and Slow Length of 12) to capture quick price momentum shifts. A MACD crossover above the signal line triggers a buy signal, while a crossover below the signal line triggers a sell signal.

RSI (Relative Strength Index): A shorter RSI length of 7 is used to gauge overbought and oversold market conditions. The strategy looks for RSI confirmation, with a long trade initiated when RSI is below the overbought level (70) and a short trade initiated when RSI is above the oversold level (30).

Risk Management:

Dynamic Stop Loss and Take Profit: The strategy uses ATR (Average True Range) to calculate dynamic stop loss and take profit levels based on market volatility.

Stop Loss is set at 0.5x ATR to limit risk.

Take Profit is set at 1.5x ATR to capture reasonable price moves.

Trailing Stop: As the market moves in the strategy’s favor, the position is protected by a trailing stop set at 0.5x ATR, allowing the strategy to lock in profits as the price moves further.

Entry & Exit Signals:

Long Entry: Triggered when the MACD crosses above the signal line (bullish crossover) and RSI is below the overbought level (70).

Short Entry: Triggered when the MACD crosses below the signal line (bearish crossover) and RSI is above the oversold level (30).

Exit Conditions: The strategy exits long or short positions based on the stop loss, take profit, or trailing stop activation.

Frequent Trades:

This strategy is designed for high-frequency trading, with trade signals occurring frequently as the MACD and RSI indicators react quickly to price movements. It works best on lower timeframes such as 1-minute, 5-minute, or 15-minute charts, but can be adjusted for different timeframes based on the asset’s volatility.

Customizable Parameters:

MACD Settings: Adjust the Fast Length, Slow Length, and Signal Length to tune the MACD’s sensitivity.

RSI Settings: Customize the RSI Length, Overbought, and Oversold levels to better match your trading style.

ATR Settings: Modify the ATR Length and multipliers for Stop Loss, Take Profit, and Trailing Stop to optimize risk management according to market volatility.

Important Notes:

Market Conditions: This strategy is designed to capture smaller, quicker moves in trending markets. It may not perform well during choppy or sideways markets.

Optimizing for Asset Volatility: Adjust the ATR multipliers based on the asset’s volatility to suit the risk-reward profile that fits your trading goals.

Backtesting: It's recommended to backtest the strategy on different assets and timeframes to ensure optimal performance.

Summary:

The Sunil High-Frequency Strategy leverages a simple combination of MACD and RSI with dynamic risk management (using ATR) to trade small but frequent price movements. The strategy ensures tight stop losses and reasonable take profits, with trailing stops to lock in profits as the price moves in favor of the trade. It is ideal for scalping or intraday trading on lower timeframes, aiming for quick entries and exits with controlled risk.

EMA Crossover with RSI and DistanceEMA Crossover with RSI and Distance Strategy

This strategy combines Exponential Moving Averages (EMA) with Relative Strength Index (RSI) and distance-based conditions to generate buy, sell, and neutral signals. It is designed to help traders identify entry and exit points based on multiple technical indicators.

Key Components:

Exponential Moving Averages (EMA):

The strategy uses four EMAs: EMA 5, EMA 13, EMA 40, and EMA 55.

A buy signal (long) is triggered when EMA 5 crosses above EMA 13 and EMA 40 crosses above EMA 55.

A sell signal (short) is generated when EMA 55 crosses above EMA 40.

The distance between EMAs (5 and 13) is also important. If the current distance between EMA 5 and EMA 13 is smaller than the average distance over the last 5 candles, a neutral condition is triggered, preventing a signal even if all other conditions are met.

Relative Strength Index (RSI):

The 14-period RSI is used to determine market strength and direction.

The strategy requires RSI to be above 50 and greater than the average RSI (over the past 14 periods) for a buy signal.

If the RSI is above 60, a green signal is given, indicating a strong bullish condition, even if the EMA conditions are not fully met.

If the RSI is below 40, a red signal is given, indicating a strong bearish condition, regardless of the EMA crossover.

Distance Conditions:

The strategy calculates the distance between EMA 5 and EMA 13 on each candle and compares it to the average distance of the last 5 candles.

If the current distance between EMA 5 and EMA 13 is lower than the average of the last 5 candles, a neutral signal is triggered. This helps avoid entering a trade when the market is losing momentum.

Additionally, if the distance between EMA 40 and EMA 13 is greater than the previous distance, the previous signal is kept intact, ensuring that the trend is still strong enough for the signal to remain valid.

Signal Persistence:

Once a buy (green) or sell (red) signal is triggered, it remains intact as long as the price is closing above EMA 5 for long trades or below EMA 55 for short trades.

If the price moves below EMA 5 for long trades or above EMA 55 for short trades, the signal is recalculated based on the most recent conditions.

Signal Display:

Green Signals: Represent a strong buy signal and are shown below the candle when the RSI is above 60.

Red Signals: Represent a strong sell signal and are shown above the candle when the RSI is below 40.

Neutral Signals: Displayed when the conditions for entry are not met, specifically when the EMA distance condition is violated.

Long and Short Signals: Additional signals are shown based on the EMA crossovers and RSI conditions. These signals are plotted below the candle for long positions and above the candle for short positions.

Trade Logic:

Long Entry: Enter a long trade when EMA 5 crosses above EMA 13, EMA 40 crosses above EMA 55, and the RSI is above 50 and greater than the average RSI. Additionally, the current distance between EMA 5 and EMA 13 should be larger than the average distance of the last 5 candles.

Short Entry: Enter a short trade when EMA 55 crosses above EMA 40 and the RSI is below 40.

Neutral Condition: If the distance between EMA 5 and EMA 13 is smaller than the average distance over the last 5 candles, the strategy will not trigger a signal, even if other conditions are met.

Larry Connors RSI 3 StrategyThe Larry Connors RSI 3 Strategy is a short-term mean-reversion trading strategy. It combines a moving average filter and a modified version of the Relative Strength Index (RSI) to identify potential buying opportunities in an uptrend. The strategy assumes that a short-term pullback within a long-term uptrend is an opportunity to buy at a discount before the trend resumes.

Components of the Strategy:

200-Day Simple Moving Average (SMA): The price must be above the 200-day SMA, indicating a long-term uptrend.

2-Period RSI: This is a very short-term RSI, used to measure the speed and magnitude of recent price changes. The standard RSI is typically calculated over 14 periods, but Connors uses just 2 periods to capture extreme overbought and oversold conditions.

Three-Day RSI Drop: The RSI must decline for three consecutive days, with the first drop occurring from an RSI reading above 60.

RSI Below 10: After the three-day drop, the RSI must reach a level below 10, indicating a highly oversold condition.

Buy Condition: All the above conditions must be satisfied to trigger a buy order.

Sell Condition: The strategy closes the position when the RSI rises above 70, signaling that the asset is overbought.

Who Was Larry Connors?

Larry Connors is a trader, author, and founder of Connors Research, a firm specializing in quantitative trading research. He is best known for developing strategies that focus on short-term market movements. Connors co-authored several popular books, including "Street Smarts: High Probability Short-Term Trading Strategies" with Linda Raschke, which has become a staple among traders seeking reliable, rule-based strategies. His research often emphasizes simplicity and robust testing, which appeals to both retail and institutional traders.

Scientific Foundations