Intraday vs Overnight OBV🔍 Purpose

This indicator provides a volume-weighted cumulative flow model that mimics On-Balance Volume (OBV) logic but splits the volume impact into intraday vs. overnight sessions. It allows traders to track how volume contributes to price movement in each session and identify whether buying/selling pressure is stronger during or outside of regular trading hours.

This indicator attempts to alleviate some of the downfalls of the standard OBV indicator, which only looks at total volume and total direction. The price of stocks generally behaves extremely differently during market hours and outside market hours, and many of the large moves happen outside of regular market hours on low volume.

⚙️ Core Features

1) OBV-style calculation:

If price increases → volume is added to the OBV stream.

If price decreases → volume is subtracted.

If price is flat → OBV remains unchanged.

2) Session splitting:

Intraday session: movement from today's open to close.

Overnight session: movement from yesterday’s close to today’s open.

Volume is split proportionally between these two periods based on user input.

3) Four visualization modes:

"Intraday" — plots only OBV from intraday price movement.

"Overnight" — plots only OBV from overnight price movement.

"Aggregate" — plots the sum of intraday and overnight OBV for a holistic view.

"Both Intraday and Overnight" — plots intraday and overnight OBV separately on the same chart.

📐 Inputs

1) Synthetic OBV Type:

"Intraday" — Show OBV from open to close only.

"Overnight" — Show OBV from prior close to today's open only.

"Aggregate" — Show a single line combining both.

"Both Intraday and Overnight" — Show both lines on the same chart.

2) Estimated Overnight Volume %:

Percentage of total daily volume assumed to occur during extended hours.

The rest is allocated to regular session (intraday).

Default: 20% overnight, 80% intraday.

🧮 How It Works

Volume Splitting:

Total bar volume is split into overnight Volume and intraday Volume:

Intraday change is the difference between today’s close and open.

Overnight change is the difference between today’s open and yesterday’s close.

Session OBV Calculations:

OBV is incremented/decremented by the session's allocated volume, depending on whether the session’s price change was positive or negative.

Aggregate OBV:

Combines both session deltas for a holistic volume flow view.

📊 Interpretation

Rising OBV (any stream) suggests accumulation; falling OBV suggests distribution.

Divergences between price and OBV lines (especially overnight vs. intraday) can reveal where hidden buying/selling is occurring.

Comparing intraday vs overnight OBV can help:

Spot whether institutional demand is building off-hours.

Detect retail vs. institutional behavior (retail trades often dominate intraday; institutional may prefer after-hours).

💡 Use Cases

Identify whether overnight gaps are supported by overnight volume momentum.

Detect accumulation in low-volume overnight sessions.

Compare intraday and overnight strength during earnings season or news events.

Complement traditional OBV by seeing session-based breakdowns.

Cari dalam skrip untuk "sessions"

Time Period Highlighter V2This indicator highlights custom time periods on any intraday chart in TradingView, making it easier to visualize your preferred trading sessions.

You can define up to three separate time ranges per day, each with precise start and end times down to the minute (e.g., 08:30 - 12:15, 14:00 - 16:45, and 20:00 - 22:30). The indicator shades the background of your chart during these periods, helping you quickly identify when you're most active or when specific market conditions occur.

Key Features:

Set start and end times (hours and minutes) for up to three trading sessions.

Automatically highlights these periods across any intraday timeframe.

Uses 24-hour time format aligned with your TradingView chart timezone.

Perfect for day traders, scalpers, or anyone needing clear visual cues for their trading windows.

This tool is especially useful for reviewing trading strategies, backtesting, or ensuring you're focusing on high-probability market hours.

Tip: Double-check that your chart timezone matches your desired session times for accurate highlighting.

C&B Auto MK5C&B Auto MK5.2ema BullBear

Overview

The C&B Auto MK5.2ema BullBear is a versatile Pine Script indicator designed to help traders identify bullish and bearish market conditions across various timeframes. It combines Exponential Moving Averages (EMAs), Relative Strength Index (RSI), Average True Range (ATR), and customizable time filters to generate actionable signals. The indicator overlays on the price chart, displaying EMAs, a dynamic cloud, scaled RSI levels, bull/bear signals, and market condition labels, making it suitable for swing trading, day trading, or scalping in trending or volatile markets.

What It Does

This indicator generates bull and bear signals based on the interaction of two EMAs, filtered by RSI thresholds, ATR-based volatility, a 50/200 EMA trend filter, and user-defined time windows. It adapts to market volatility by adjusting EMA lengths and RSI thresholds. A dynamic cloud highlights trend direction or neutral zones, with candlestick coloring in neutral conditions. Market condition labels (current and historical) provide real-time trend and volatility context, displayed above the chart.

How It Works

The indicator uses the following components:

EMAs: Two EMAs (short and long) are calculated on a user-selected timeframe (1, 5, 15, 30, or 60 minutes). Their crossover or crossunder triggers potential bull/bear signals. EMA lengths adjust based on volatility (e.g., 10/20 for volatile markets, 5/10 for non-volatile).

Dynamic Cloud: The area between the EMAs forms a cloud, colored green for bullish trends, red for bearish trends, or a user-defined color (default yellow) for neutral zones (when EMAs are close, determined by an ATR-based threshold). Users can widen the cloud for visibility.

RSI Filter: RSI is scaled to price levels and plotted on the chart (optional). Signals are filtered to ensure RSI is within volatility-adjusted bull/bear thresholds and not in overbought/oversold zones.

ATR Volatility Filter: An optional filter ensures signals occur during sufficient volatility (ATR(14) > SMA(ATR, 20)).

50/200 EMA Trend Filter: An optional filter restricts bull signals to bullish trends (50 EMA > 200 EMA) and bear signals to bearish trends (50 EMA < 200 EMA).

Time Filter: Signals are restricted to a user-defined UTC time window (default 9:00–15:00), aligning with active trading sessions.

Market Condition Labels: Labels above the chart display the current trend (Bullish, Bearish, Neutral) and optionally volatility (e.g., “Bullish Volatile”). Up to two historical labels persist for a user-defined number of bars (default 5) to show recent trend changes.

Visual Aids: Bull signals appear as green triangles/labels below the bar, bear signals as red triangles/labels above. Candlesticks in neutral zones are colored (default yellow).

The indicator ensures compatibility with standard chart types (e.g., candlestick or bar charts) to produce realistic signals, avoiding non-standard types like Heikin Ashi or Renko.

How to Use It

Add to Chart: Apply the indicator to a candlestick or bar chart on TradingView.

Configure Settings:

Timeframe: Choose a timeframe (1, 5, 15, 30, or 60 minutes) to match your trading style.

Filters:

Enable/disable the ATR volatility filter to focus on high-volatility periods.

Enable/disable the 50/200 EMA trend filter to align signals with the broader trend.

Enable the time filter and set custom UTC hours/minutes (default 9:00–15:00).

Cloud Settings: Adjust the cloud width, neutral zone threshold, color, and transparency.

EMA Colors: Use default trend-based colors or set custom colors for short/long EMAs.

RSI Display: Toggle the scaled RSI and its thresholds, with customizable colors.

Signal Settings: Toggle bull/bear labels and set signal colors.

Market Condition Labels: Toggle current/historical labels, include/exclude volatility, and adjust decay period.

Interpret Signals:

Bull Signal: A green triangle or “Bull” label below the bar indicates potential bullish momentum (EMA crossover, RSI above bull threshold, within time window, passing filters).

Bear Signal: A red triangle or “Bear” label above the bar indicates potential bearish momentum (EMA crossunder, RSI below bear threshold, within time window, passing filters).

Neutral Zone: Yellow candlesticks and cloud (if enabled) suggest a lack of clear trend; consider range-bound strategies or avoid trading.

Market Condition Labels: Check labels above the chart for real-time trend (Bullish, Bearish, Neutral) and volatility status to confirm market context.

Monitor Context: Use the cloud, RSI, and labels to assess trend strength and volatility before acting on signals.

Unique Features

Volatility-Adaptive EMAs: Automatically adjusts EMA lengths based on ATR to suit volatile or non-volatile markets, reducing manual configuration.

Neutral Zone Detection: Uses an ATR-based threshold to identify low-trend periods, helping traders avoid choppy markets.

Scaled RSI Visualization: Plots RSI and thresholds directly on the price chart, simplifying momentum analysis relative to price.

Flexible Time Filtering: Supports precise UTC-based trading windows, ideal for day traders targeting specific sessions.

Historical Market Labels: Displays recent trend changes (up to two) with a decay period, providing context for market shifts.

50/200 EMA Trend Filter: Aligns signals with the broader market trend, enhancing signal reliability.

Notes

Use on standard candlestick or bar charts to ensure accurate signals.

Test the indicator on a demo account to optimize settings for your market and timeframe.

Combine with other analysis (e.g., support/resistance, volume) for better decision-making.

The indicator is not a standalone system; use it as part of a broader trading strategy.

Limitations

Signals may lag in fast-moving markets due to EMA-based calculations.

Neutral zone detection may vary in extremely volatile or illiquid markets.

Time filters are UTC-based; ensure your platform’s timezone settings align.

This indicator is designed for traders seeking a customizable, trend-following tool that adapts to volatility and provides clear visual cues with robust filtering for bullish and bearish market conditions.

Session Profile AnalyzerWhat’s This Thing Do?

Hey there, trader! Meet the Session Profile Analyzer (SPA) your new go-to pal for breaking down market action within your favorite trading sessions. It’s an overlay indicator that mixes Rotation Factor (RF), Average Subperiod Range (ASPR), Volume Value Area Range (VOLVAR), and TPO Value Area Range (TPOVAR) into one tidy little toolkit. Think of it as your market vibe checker momentum, volatility, and key levels, all served up with a grin.

The Cool Stuff It Does:

Rotation Factor (RF) : Keeps tabs on whether the market’s feeling bullish, bearish, or just chilling. It’s like a mood ring for price action shows “UP ↑,” “DOWN ↓,” or “NONE ↔.”

ASPR : Averages out the range of your chosen blocks. Big swings? Tiny wiggles? This tells you the session’s energy level.

VOLVAR : Dives into volume to find where the action’s at, with a smart twist it adjusts price levels based on the session’s size and tiny timeframe moves (capped at 128 so your chart doesn’t cry).

TPOVAR : Grabs lower timeframe data to spot where price hung out the most, TPO-style. Value zones, anyone?

Dynamic Precision : No ugly decimal overload SPA matches your asset’s style (2 decimals for BTC, 5 for TRX, you get it).

How to Play With It:

Session Start/End : Pick your trading window (say, 0930-2200) and a timezone (America/New_York, or wherever you’re at).

Block Size : Set the chunk size for RF and ASPR like 30M if you’re into half-hour vibes.

Value Area Timeframe : Go micro with something like 1S for VOLVAR and TPOVAR precision.

Label : Size it (small to huge), color it (white, neon pink, whatever), and slap it where you want (start, mid, end).

How It All Works (No PhD Required):

RF : Imagine breaking your session into blocks (via Block Size). For each block, SPA checks if the high beats the last high (+1) or not (0), and if the low dips below the last low (-1) or not (0). Add those up, and boom positive RF means upward vibes, negative means downward, near zero is “meh.” Use it to catch trends or spot when the market’s napping.

ASPR : Takes those same blocks, measures high-to-low range each time, and averages them. It’s your volatility pulse big ASPR = wild ride, small ASPR = snooze fest. Great for sizing up session action.

VOLVAR : Here’s the fun part. It takes the session’s full range (high minus low), divides it by the average range of your tiny Value Area Timeframe bars (e.g., 1S), and picks a sensible number of price levels capped at 128 so it doesn’t overthink. Then it bins volume into those levels, finds the busiest price (POC), and grows a 70% value area around it. Perfect for spotting where the big players parked their cash.

TPOVAR : Grabs midpoints from those tiny timeframe bars, sorts them, and snips off the top and bottom 15% to find the 70% “value zone” where price chilled the most. Think of it as the market’s comfort zone great for support/resistance hunting.

Why You’ll Like It:

Whether you’re scalping crypto, swinging forex, or dissecting stocks, SPA’s got your back. Use RF to catch momentum shifts like jumping on an “UP ↑” trend or fading a “DOWN ↓” exhaustion. ASPR’s your secret weapon for sizing up trades: a big ASPR (say, 100 on BTC) means you can aim for juicy targets (like 1-2x ASPR) or set invalidations tight when it’s tiny (e.g., 0.001 on TRX) to dodge chop. VOLVAR and TPOVAR are your level-finders nail those key zones where price loves to bounce or break, perfect for entries, stops, or profit grabs. It’s like having a trading co-pilot who’s chill but knows their stuff.

Heads-Up:

Load enough history for those micro timeframes to shine (1S needs some bars to work with).

Keeps things light won’t bog down your chart even with decent-sized sessions.

Let’s Roll:

Slap SPA on your chart, tweak it to your style, and watch it spill the beans on your session. Happy trading, fam may your pips be plenty and your losses few!

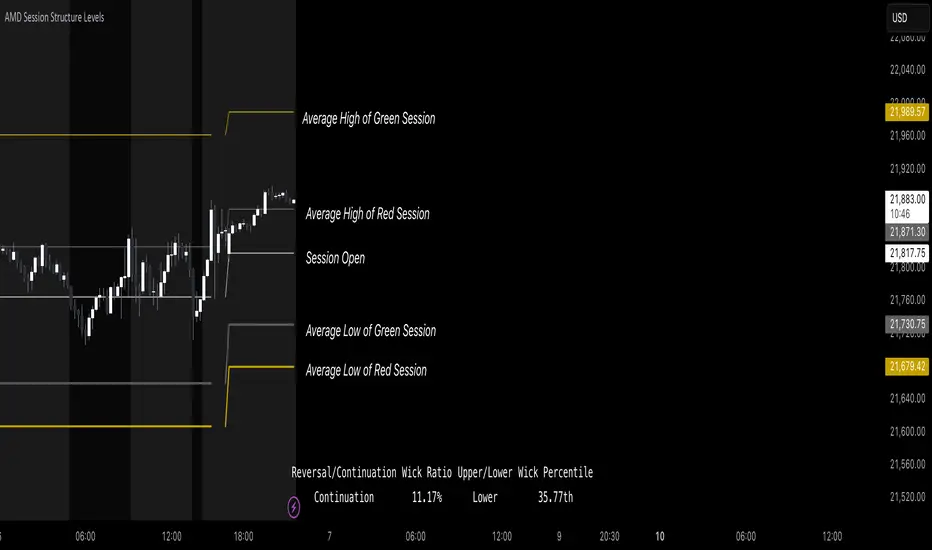

AMD Session Structure Levels# Market Structure & Manipulation Probability Indicator

## Overview

This advanced indicator is designed for traders who want a systematic approach to analyzing market structure, identifying manipulation, and assessing probability-based trade setups. It incorporates four core components:

### 1. Session Price Action Analysis

- Tracks **OHLC (Open, High, Low, Close)** within defined sessions.

- Implements a **dual tracking system**:

- **Official session levels** (fixed from the session open to close).

- **Real-time max/min tracking** to differentiate between temporary spikes and real price acceptance.

### 2. Market Manipulation Detection

- Identifies **manipulative price action** using the relationship between the open and close:

- If **price closes below open** → assumes **upward manipulation**, followed by **downward distribution**.

- If **price closes above open** → assumes **downward manipulation**, followed by **upward distribution**.

- Normalized using **ATR**, ensuring adaptability across different volatility conditions.

### 3. Probability Engine

- Tracks **historical wick ratios** to assess trend vs. reversal conditions.

- Calculates **conditional probabilities** for price moves.

- Uses a **special threshold system (0.45 and 0.03)** for reversal signals.

- Provides **real-time probability updates** to enhance trade decision-making.

### 4. Market Condition Classification

- Classifies market conditions using a **wick-to-body ratio**:

```pine

wick_to_body_ratio = open > close ? upper_wick / (high - low) : lower_wick / (high - low)

```

- **Low ratio (<0.25)** → Likely a **trend day**.

- **High ratio (>0.25)** → Likely a **range day**.

---

## Why This Indicator Stands Out

### ✅ Smarter Level Detection

- Uses **ATR-based dynamic levels** instead of static support/resistance.

- Differentiates **manipulation from distribution** for better decision-making.

- Updates probabilities **in real-time**.

### ✅ Memory-Efficient Design

- Implements **circular buffers** to maintain efficiency:

```pine

var float manipUp = array.new_float(lookbackPeriod, 0.0)

var float manipDown = array.new_float(lookbackPeriod, 0.0)

```

- Ensures **constant memory usage**, even over extended trading sessions.

### ✅ Advanced Probability Calculation

- Utilizes **conditional probabilities** instead of simple averages.

- Incorporates **market context** through wick analysis.

- Provides **actionable signals** via a probability table.

---

## Trading Strategy Guide

### **Best Entry Setups**

✅ Wait for **price to approach manipulation levels**.

✅ Confirm using the **probability table**.

✅ Check the **wick ratio for context**.

✅ Enter when **conditional probability aligns**.

### **Smart Exit Management**

✅ Use **distribution levels** as **profit targets**.

✅ Scale out **when probabilities shift**.

✅ Monitor **wick percentiles** for confirmation.

### **Risk Management**

✅ Size positions based on **probability readings**.

✅ Place stops at **manipulation levels**.

✅ Adjust position size based on **trend vs. range classification**.

---

## Configuration Tips

### **Session Settings**

```pine

sessionTime = input.session("0830-1500", "Session Hours")

weekDays = input.string("23456", "Active Days")

```

- Match these to your **primary trading session**.

- Adjust for different **market opens** if needed.

### **Analysis Parameters**

```pine

lookbackPeriod = input.int(50, "Lookback Period")

low_threshold = input.float(0.25, "Trend/Range Threshold")

```

- **50 periods** is a good starting point but can be optimized per instrument.

- The **0.25 threshold** is ideal for most markets but may need adjustments.

---

## Market Structure Breakdown

### **Trend/Continuation Days**

- **Characteristics:**

✅ Small **opposing wicks** (minimal counter-pressure).

✅ Clean, **directional price movement**.

- **Bullish Trend Day Example:**

✅ Small **lower wicks** (minimal downward pressure).

✅ Strong **closes near the highs** → **Buyers in control**.

- **Bearish Trend Day Example:**

✅ Small **upper wicks** (minimal upward pressure).

✅ Strong **closes near the lows** → **Sellers in control**.

### **Reversal Days**

- **Characteristics:**

✅ **Large opposing wicks** → Failed momentum in the initial direction.

- **Bullish Reversal Example:**

✅ **Large upper wick early**.

✅ **Strong close from the lows** → **Sellers failed to maintain control**.

- **Bearish Reversal Example:**

✅ **Large lower wick early**.

✅ **Weak close from the highs** → **Buyers failed to maintain control**.

---

## Summary

This indicator systematically quantifies market structure by measuring **manipulation, distribution, and probability-driven trade setups**. Unlike traditional indicators, it adapts dynamically using **ATR, historical probabilities, and real-time tracking** to offer a structured, data-driven approach to trading.

🚀 **Use this tool to enhance your decision-making and gain an objective edge in the market!**

Adaptive Volatility-Scaled Oscillator [AVSO] (Zeiierman)█ Overview

The Adaptive Volatility-Scaled Oscillator (AVSO) is a dynamic trading indicator that measures and visualizes volatility-adjusted market behavior. By scaling various metrics (such as volume, price changes, standard deviation, ATR, and Yang-Zhang volatility) and applying adaptive smoothing, AVSO helps traders identify market conditions where volatility deviates significantly from the norm.

This indicator uses standardized scaling (Z-Score logic) to highlight periods of abnormally high or low volatility relative to recent history. With gradient coloring and clear volatility zones, AVSO provides a visually intuitive way to analyze market volatility and adapt trading strategies accordingly.

█ How It Works

⚪ Scaling Metrics: The indicator scales user-selected metrics (e.g., volume, ATR, standard deviation) relative to the market and price, providing a standardized volatility measure.

⚪ Z-Score Standardization: The scaled metric is normalized using a Z-Score to measure how far current volatility deviates from its recent mean.

Positive Z-Score: Above-average volatility.

Negative Z-Score: Below-average volatility.

⚪ Adaptive Smoothing: An Adaptive EMA smooths the Z-Score, dynamically adjusting its length based on the strength of the volatility. Stronger deviations result in shorter smoothing, increasing responsiveness.

█ Unique Feature: Yang-Zhang Volatility

The Yang-Zhang volatility estimator sets this indicator apart by providing a more robust and accurate measure of volatility compared to traditional methods like ATR or standard deviation.

⚪ What Makes Yang-Zhang Volatility Unique?

Comprehensive Calculation: It combines overnight price gaps (log returns from the previous close to the current open) and intraday price movements (high, low, and close).

Accurate for Gapped Markets: Traditional volatility measures can misrepresent price movement when significant gaps occur between sessions. Yang-Zhang accounts for these gaps, making it highly reliable for assets prone to overnight price jumps, such as stocks, cryptocurrencies, and futures.

Adaptable to Real Market Conditions : By including both close-to-open returns and intraday volatility, it provides a balanced and adaptive measure that captures the full volatility picture.

⚪ Why This Matters to Traders

Better Volatility Insights: Yang-Zhang offers a clearer view of true market volatility, especially in markets with price gaps or uneven trading sessions.

Improved Trade Timing: By identifying volatility spikes and calm periods more effectively, traders can time their entries and exits with greater confidence.

█ How to Use

Identify High and Low Volatility

A high Z-Score (>2) indicates significant market volatility. This can signal momentum-driven moves, breakouts, or areas of increased risk.

A low Z-Score (<-2) suggests low volatility or a calm market environment. This often occurs before a potential breakout or reversal.

Trade Signals

High Volatility Zones (background highlight): Monitor for potential breakouts, trend continuations, or reversals.

Low Volatility Zones: Anticipate range-bound conditions or upcoming volatility spikes.

█ Settings

Source: Select the price source for scaling calculations (close, high, low, open).

Metric Measure: Choose the volatility measure:

Volume: Scales raw volume.

Close: Uses closing price changes.

Standard Deviation: Price dispersion.

ATR: Average True Range.

Yang: Yang-Zhang volatility estimate.

Bars to Analyze: Number of historical bars used to calculate the mean and standard deviation of the scaled metric.

ATR / Standard Deviation Period: Lookback period for ATR or Standard Deviation calculation.

Yang Volatility Period: Period for the Yang-Zhang volatility estimator.

Smoothing Period: Base smoothing length for the adaptive smoothing line.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Wyckoff Trading Strategy for XAU/USD by KAIZVIETNAMXAU/USD TF M15 TP SL 20-30 pip

- Volume: Calculates the average volume based on the SMA to compare with the current trading volume.

- ATR (Average True Range): Calculated to determine price volatility.

- Support and Resistance Levels: Identifies support and resistance levels over the last 10 trading sessions.

Specific Point Identification

- A series of functions are defined to detect critical phases in the market structure, such as:

- Finding Preliminary Support: Recognizing signals of accumulation near support levels.

- Finding Selling Climax: Detecting signals of profit-taking near resistance levels.

- Finding Last Point of Support: Identifying points that provide stability for the price.

- Finding Preliminary Supply: Recognizing supply signals near resistance levels.

- Finding Buying Climax: Identifying strong buy signals accompanied by high trading volume.

- Finding Sign of Weakness: Determining instances of price adjustments that could lead to declines.

Market State Identification

- Accumulation: When the closing price is situated between the support and resistance levels.

- Distribution: When the closing price approaches the highest level of the previous few sessions.

- Sideways: When there is no clear bias toward either an upward or downward trend.

Buy and Sell Signals

- Buy Signals: Determined through finding preliminary support, selling climax, and last point of support.

- Sell Signals: Determined through finding preliminary supply, buying climax, and signs of weakness.

Chartonaut: GlimpseDisplays an overview of some key metrics as a table.

Market Cap : value of the company.

Float Shares : number of shares available for trading.

AR# : average range over the last # sessions.

ATR# : average true range over the last # sessions.

ATR#/MA# : distance of the current price from the given moving average (MA) in terms of ATR multiples.

Rel Volatility : current session's range, including gaps from previous close, relative to the ATR.

Additionally, it highlights some metrics if they are crossing a given threshold, as to warn that some criteria might not be met.

Standard Deviation based Upper Lower RangeThis script makes use of historical data for finding the standard deviation on daily returns. Based on the mean and standard deviation, the upper and lower range for the stock is shown upto 2x standard deviation. These bounds can be treated as volatility range for the next n trading sessions. This volatility is based on historical data. Users can change the lookback historical period, and can also set the time period (days) for upcoming trading sessions.

This indicator can be useful in determining stoploss and target levels along with the traditional support/resistance levels. It can also be useful in option trading where one needs to determine a range beyond which it is safe to sell an option.

A range of 1 SD has around 65% to 68% probability that it will not be breached. A range of 2 SD has around 95% probability that it will not be breached.

The indicator is based on Normal distribution theory. In future editions, I envision to also calculate the skewness and kurtosis so that we can determine if a stock is properly following Normal Distribution theory. That may further favor the calculated range.

ka66: Bar Range BandsThis tool takes a bar's range, and reflects it above the high and below the low of that bar, drawing upper and lower bands around the bar. Repeated for each bar. There's an option to then multiply that range by some multiple. Use a value greater than 1 to get wider bands, and less than one to get narrower bands.

This tool stems out of my frustration from the use of dynamic bands (like Keltner Channels, or Bollinger Bands), in particular for estimating take profit points.

Dynamic bands work great for entries and stop loss, but their dynamism is less useful for a future event like taking profit, in my experience. We can use a smaller multiple, but then we can often lose out on a bigger chunk of gains unnecessarily.

The inspiration for this came from a friend explaining an ICT/SMC concept around estimating the magnitude of a trend, by calculating the Asian Session Range, and reflecting it above or below on to the New York and London sessions. He described this as standard deviation of the Asian Range, where the range can thus be multiplied by some multiple for a wider or narrower deviation.

This, in turn, also reminded me of the Measured Move concept in Technical Analysis. We then consider that the market is fractal in nature, and this is why patterns persist in most timeframes. Traders exist across the spectrum of timeframes. Thus, a single bar on a timeframe, is made up of multiple bars on a lower timeframe . In other words, when we reflect a bar's range above or below itself, in the event that in a lower timeframe, that bar fit a pattern whose take profit target could be estimated via a Measured Move , then the band's value becomes a more valid estimate of a take profit point .

Yet another way to think about it, by way of the fractal nature above, is that it is essentially a simplified dynamic support and resistance mechanism , even simpler than say the various Pivot calculations (e.g. Classical, Camarilla, etc.).

This tool in general, can also be used by those who manually backtest setups (and certainly can be used in an automated setting too!). It is a research tool in that regard, applicable to various setups.

One of the pitfalls of manual backtesting is that it requires more discipline to really determine an exit point, because it's easy to say "oh, I'll know more or less where to exit when I go live, I just want to see that the entry tends to work". From experience, this is a bad idea, because our mind subconsciously knows that we haven't got a trained reflex on where to exit. The setup may be decent, but without an exit point, we will never have truly embraced and internalised trading it. Again, I speak from experience!

Thus, to use this to research take profit/exit points:

Have a setup in mind, with all the entry rules.

Plot your setup's indicators, mark your signals.

Use this indicator to get an idea of where to exit after taking an entry based on your signal.

Credits:

@ICT_ID for providing the idea of using ranges to estimate how far a trend move might go, in particular he used the Asian Range projected on to the London and New York market sessions.

All the technicians who came up with the idea of the Measured Move.

Uptrick: FVG Market Zones**Uptrick: FVG Market Zones**

---

### Introduction

**Uptrick: FVG Market Zones** is a cutting-edge technical analysis tool designed to identify and visualize Fair Value Gaps (FVGs) within financial markets. This indicator focuses on pinpointing critical price levels where significant gaps occur, which can act as potential support and resistance zones. By integrating advanced volatility analysis and user-configurable parameters, the **Uptrick: FVG Market Zones** provides traders with a robust framework for understanding market dynamics and making informed trading decisions.

### Purpose and Functionality

The primary purpose of the **Uptrick: FVG Market Zones** indicator is to detect and highlight Fair Value Gaps, which are areas on a price chart where there is a significant price movement without any trading activity in between. These gaps can provide critical insights into market behavior, as they often indicate areas where the market has not fully accounted for the supply and demand dynamics. Traders use these zones to anticipate potential reversals, breakouts, or consolidations, making this tool highly valuable for both short-term and long-term trading strategies.

### Unique Features and Originality

The **Uptrick: FVG Market Zones** indicator is distinguished by its focus on FVGs and its ability to integrate this concept into a broader market analysis framework. Unlike other indicators that may offer generalized support and resistance levels, this tool specifically identifies and visualizes gaps based on volatility-adjusted criteria. This precision allows traders to focus on the most relevant market zones, improving their ability to anticipate market movements.

One of the standout features of this indicator is its user-configurable settings, which provide a high degree of customization. This flexibility ensures that traders can tailor the indicator to suit their specific trading style and the particular market they are analyzing. Additionally, the indicator's visualization capabilities are enhanced with customizable colors and gap-filling options, making it easier for traders to interpret and act on the information presented.

### Inputs and Configurations

**Uptrick: FVG Market Zones** comes with several user inputs that allow traders to customize the indicator's behavior and appearance. Each input plays a crucial role in determining how the indicator identifies and visualizes FVGs on the chart. Here’s a detailed breakdown of each input:

1. **FVG Analysis Period (fvgPeriod):**

- **Description:** This input determines the period over which the indicator analyzes the chart for identifying FVGs. By adjusting this value, traders can control how far back in time the indicator looks to detect significant gaps.

- **Default Value:** 25

- **Purpose:** A shorter period may focus on more recent market activity, making the indicator more sensitive to recent price movements. In contrast, a longer period allows the indicator to identify gaps that have remained unfilled for an extended time, potentially acting as stronger support or resistance levels.

2. **Analysis Mode (mode):**

- **Description:** The Analysis Mode input allows traders to choose between different methods of analyzing the chart for FVGs.

- **Options:** "Recent Gaps" and "Extended View"

- **Default Option:** "Recent Gaps"

- **Purpose:**

- **Recent Gaps:** Focuses on the latest significant gaps, providing traders with up-to-date information on the most relevant market zones.

- **Extended View:** Considers a broader range of gap patterns, which can be useful in markets where historical gaps may still influence current price action.

3. **Volatility Sensitivity (volatilityFactor):**

- **Description:** This input adjusts the sensitivity of the indicator to market volatility. It is used in calculating the threshold for identifying FVGs.

- **Default Value:** 0.3

- **Step Size:** 0.1

- **Purpose:** A higher sensitivity will cause the indicator to detect smaller gaps, which might be more frequent but less significant. Lower sensitivity focuses on larger, more impactful gaps, which are less frequent but potentially more powerful in predicting market behavior.

4. **Highlight Market Gaps (showGaps):**

- **Description:** A boolean input that determines whether the identified FVGs should be highlighted on the chart.

- **Default Value:** True

- **Purpose:** This input allows traders to toggle the visualization of FVGs. When enabled, the indicator highlights gaps using colored boxes, making them visually prominent on the chart.

5. **Bullish Highlight Color (bullColor):**

- **Description:** Sets the color used to highlight bullish FVGs (gaps that may indicate support).

- **Default Value:** #00FF7F (a shade of green)

- **Purpose:** The color choice is crucial for quickly distinguishing bullish zones from bearish ones. Green is typically associated with upward price movement, making it intuitive for traders to identify potential support areas.

6. **Bearish Highlight Color (bearColor):**

- **Description:** Sets the color used to highlight bearish FVGs (gaps that may indicate resistance).

- **Default Value:** #FF4500 (a shade of red)

- **Purpose:** Red is commonly associated with downward price movement, making it easy for traders to identify potential resistance areas. This color coding helps in quickly assessing the chart.

7. **Fill Gap Areas (fillGaps):**

- **Description:** A boolean input that determines whether the FVGs should be filled with a color on the chart.

- **Default Value:** True

- **Purpose:** Filling the gap areas provides a more solid visual cue for traders. It enhances the visibility of the gaps, making it easier to spot these zones during fast-paced trading sessions.

8. **Hidden Color (hidden):**

- **Description:** A color input that is used when certain elements should be hidden from the chart.

- **Default Value:** color.rgb(0,0,0,100) (a semi-transparent black)

- **Purpose:** This input is useful for controlling the visibility of certain plots or elements on the chart, ensuring that the indicator remains clean and uncluttered.

### Market Gap Detection

The core functionality of the **Uptrick: FVG Market Zones** indicator lies in its ability to detect Fair Value Gaps. These gaps occur when the price makes a significant jump from one level to another without any trading activity in between. The indicator uses a combination of price action analysis and volatility thresholds to identify these gaps.

- **Volatility Measurement:** The indicator begins by measuring market volatility using the Average True Range (ATR). This volatility measurement is then adjusted by the user-defined sensitivity factor, which determines the threshold for identifying significant gaps.

- **Gap Identification:** The indicator checks for instances where the current low is higher than the high two bars ago (bullish gap) or where the current high is lower than the low two bars ago (bearish gap). These conditions signify a potential FVG.

- **Gap Storage and Management:** Once a gap is identified, it is stored in an array. The indicator also manages the size of these arrays based on the selected analysis mode, ensuring that only the most relevant gaps are considered in the analysis.

### Visualization

Visualization is a key component of the **Uptrick: FVG Market Zones** indicator. By providing clear and customizable visual cues, the indicator ensures that traders can quickly and easily interpret the information it provides.

- **Gap Highlighting:** When enabled, the indicator highlights the identified FVGs on the chart using colored boxes. Bullish gaps are highlighted in green, while bearish gaps are highlighted in red. This color coding helps traders instantly recognize potential support and resistance zones.

- **Gap Filling:** The indicator can also fill the identified gaps with a semi-transparent color. This option enhances the visibility of the gaps, making them more prominent on the chart. Filled gaps are particularly useful for traders who want to keep track of these zones over multiple trading sessions.

- **Gap Averages:** The indicator calculates the average level of the identified gaps and plots these averages as lines on the chart. These lines represent the general area of support or resistance based on the detected gaps, providing traders with a reference point for setting their stop losses or profit targets.

- **Text Labels:** The indicator also labels each FVG with the text "FVG" inside the highlighted area. This feature ensures that traders can easily identify these zones even in charts with dense price action.

### Practical Applications

The **Uptrick: FVG Market Zones** indicator is versatile and can be applied to a wide range of trading strategies across different markets and timeframes. Here are a few examples of how this indicator can be used in practice:

1. **Support and Resistance Trading:**

- Traders can use the identified FVGs as dynamic support and resistance levels. By placing their trades based on these levels, they can take advantage of potential reversals or continuations at key market zones.

2. **Gap Filling Strategy:**

- Some traders focus on the concept of gap filling, where the market eventually returns to "fill" the gap created by rapid price movements. The **Uptrick: FVG Market Zones** indicator can

help identify such gaps and anticipate when the market might return to these levels.

3. **Breakout Trading:**

- The indicator can be used to identify breakouts from significant gaps. When the price moves beyond the identified FVGs, it may signal a strong trend continuation, providing an opportunity for breakout traders.

4. **Reversal Trading:**

- By monitoring the signals generated by the indicator, traders can identify potential market reversals. A sell signal after a prolonged uptrend or a buy signal after a downtrend may indicate a reversal, allowing traders to position themselves accordingly.

5. **Risk Management:**

- The average levels of the FVGs can be used to set stop-loss and take-profit levels. By aligning these levels with the FVG zones, traders can improve their risk management practices and enhance their trading discipline.

### Customization and Flexibility

One of the standout features of the **Uptrick: FVG Market Zones** indicator is its high level of customization. Traders can adjust various parameters to tailor the indicator to their specific needs and preferences.

- **Customizable Colors:** The indicator allows traders to choose their preferred colors for highlighting bullish and bearish gaps. This flexibility ensures that the indicator can be integrated seamlessly into any trading setup, regardless of the trader's color scheme preferences.

- **Adjustable Periods and Sensitivity:** By allowing traders to adjust the analysis period and volatility sensitivity, the indicator can be fine-tuned to suit different market conditions. For example, a trader might use a shorter analysis period and higher sensitivity in a volatile market, while opting for a longer period and lower sensitivity in a more stable market.

- **Toggling Visual Elements:** Traders can choose to enable or disable various visual elements of the indicator, such as gap highlighting, gap filling, and text labels. This level of control allows traders to declutter their charts and focus on the information that is most relevant to their trading strategy.

### Advantages and Benefits

The **Uptrick: FVG Market Zones** indicator offers several key advantages that make it a valuable tool for traders:

1. **Precision:** By focusing on Fair Value Gaps, the indicator provides highly precise levels of support and resistance, which are often more reliable than traditional horizontal levels.

2. **Clarity:** The clear visual representation of FVGs, along with the text labels and color coding, ensures that traders can quickly interpret the indicator's signals and incorporate them into their trading decisions.

3. **Adaptability:** The indicator's customizable settings allow it to be adapted to different markets, timeframes, and trading styles. Whether you are a day trader, swing trader, or long-term investor, this indicator can be tailored to meet your needs.

4. **Enhanced Decision-Making:** The trading signals generated by the indicator provide actionable insights that can help traders make more informed decisions. By aligning their trades with the identified FVG zones, traders can improve their chances of success.

5. **Risk Management:** The use of FVG zones as reference points for stop-loss and take-profit levels enhances risk management practices, helping traders protect their capital while maximizing their profit potential.

### Conclusion

The **Uptrick: FVG Market Zones** indicator is a powerful and versatile tool for traders seeking to enhance their market analysis and improve their trading outcomes. By focusing on Fair Value Gaps and providing a high level of customization, this indicator offers a unique blend of precision, clarity, and adaptability. Whether you are looking to identify key market zones, generate trading signals, or improve your risk management practices, the **Uptrick: FVG Market Zones** indicator is a valuable addition to any trader's toolkit.

With its innovative approach to market analysis and user-friendly design, **Uptrick: FVG Market Zones** stands out as an essential tool for traders who want to stay ahead of the market and make more informed trading decisions. Whether you are trading stocks, forex, commodities, or cryptocurrencies, this indicator provides the insights you need to navigate the markets with confidence and success.

Asian Range IndicatorIndicator Name:

Asian Range Indicator

Description:

This TradingView indicator is designed to accurately detect the price range during the Asian session, based on our trading strategy. This range is crucial for planning trades in the European and American sessions. Using advanced algorithms, the indicator automatically identifies and plots the highs and lows within the Asian session period, highlighting them on the chart with shaded areas for clear visualization. This helps traders anticipate breakouts and set more precise entry and exit levels.

How to Use the Indicator:

Add the indicator to your TradingView chart.

Observe the shaded areas representing the Asian range.

Use these levels to plan your trades during the European and American sessions.

Combine with other technical indicators to confirm your trading decisions.

Chart:

The chart published with this script is clean and easy to understand, clearly showing the Asian range highlighted with shaded areas. No other scripts are included, ensuring the indicator's output is easily identifiable. The shaded areas contribute to the visual understanding of the Asian range, helping traders effectively use the script.

CME Gap Detector [CryptoSea]The CME Gap Indicator , is a tool designed to identify and visualize potential price gaps in the cryptocurrency market, particularly focusing on gaps that occur during the weekend trading sessions. By highlighting these gaps, traders can gain insights into potential market movements and anticipate price behavior.

Key Features

Gap Identification: The indicator identifies gaps in price between the Friday close and the subsequent opening price on Monday. It plots these gaps on the chart, allowing traders to easily visualize and analyze their significance.

Weekend Price Comparison: It compares the closing price on Friday with the opening price on Monday to determine whether a gap exists and its magnitude.

Customizable Visualization: Traders have the option to customize the visualization of the gaps, including the color scheme for better clarity and visibility on the chart.

Neutral Candle Color Option: Users can choose to display neutral candle colors, enhancing the readability of the chart and reducing visual clutter.

How it Works

Data Fetching and Calculation: The indicator fetches the daily close price and calculates whether a gap exists between the Friday close and the subsequent Monday opening price.

Plotting: It plots the current price and the previous Friday's close on the chart, making it easy for traders to compare and analyze.

Gradient Fill: The indicator incorporates a gradient fill feature to visually represent the magnitude of the gap, providing additional insights into market sentiment.

Weekend Line Logic: It includes logic to identify Sunday bars and mark them on the chart, aiding traders in distinguishing weekend trading sessions.

Application

Gap Trading Strategy: Traders can use the identified gaps as potential entry or exit points in their trading strategies, considering the tendency of price to fill gaps over time.

Market Sentiment Analysis: Analyzing the presence and size of weekend gaps can provide valuable insights into market sentiment and participant behavior.

Risk Management: Understanding the existence and significance of gaps can help traders manage their risk exposure and make informed decisions.

The CME Gap indicator offers traders a valuable tool for analyzing weekend price gaps in the cryptocurrency market, empowering them to make informed trading decisions and capitalize on market opportunities.

Intraday Volatility Bands [Honestcowboy]The Intraday Volatility Bands aims to provide a better alternative to ATR in the calculation of targets or reversal points.

How are they different from ATR based bands?

While ATR and other measures of volatility base their calculations on the previous bars on the chart (for example bars 1954 to 1968). The volatility used in these bands measure expected volatility during that time of the day.

Why would you take this approach?

Markets behave different during certain times of the day, also called sessions.

Here are a couple examples.

Asian Session (generally low volatility)

London Session (bigger volatility starts)

New York Session (overlap of New York with London creates huge volatility)

Generally when using bands or channel type indicators intraday they do not account for the upcoming sessions. On London open price will quickly spike through a bollinger band and it will take some time for the bands to adjust to new volatility.

This script will show expected volatility targets at the start of each new bar and will not adjust during the bar. It already knows what price is expected to do at this time of day.

Script also plots arrows when price breaches either the top or bottom of the bands. You can also set alerts for when this occurs. These are non repainting as the script knows the level at start of the bar and does not change.

🔷 CALCULATION

Think of this script like an ATR but instead it uses past days data instead of previous bars data. Charts below should visualise this more clearly:

The scripts measure of volatility is based on a simple high-low.

The script also counts the number of bars that exist in a day on your current timeframe chart. After knowing that number it creates the matrix used in it's calculations and data storage.

See how it works perfectly on a lower timeframe chart below:

Getting this right was the hardest part, check the coding if you are interested in this type of stuff. I commented every step in the coding process.

🔷 SETTINGS

Every setting of the script has a tooltip but I provided a breakdown here:

Some more examples of different charts:

Kviateq - Session Opening RangesThis indicator plots the opening range for each of the market sessions.

Users can chose the length of the opening range, as well as change the time for each of the sessions.

This script is based on opening range breakout strategies, which entail taking a long/short depending on which way the price breaks out.

To trade it, we wait for the session opening range to print, and then we enter upon a candle close.

It's meant to be used on lower timeframes, ideally one hour or lower.

It can be used by itself, but it works even better in combination with other indicators, like moving averages.

Enjoy

Regression Candle Conversion IndicatorHey everyone!

I got a pseudo-request a while ago for something like this, essentially the ability to track where another ticker would fall based on an alternative ticker.

I did create my ticker correlation reference indicator which directly looks at the correlation between 2 tickers. However, this is an indicator that operates on the same principle but is more pragmatic for trading.

What does it do?

Well, in keeping with the theme of what I call my indicators, this has a title that explains exactly what it does, "Regression Candle Conversion Indicator" or "RCCI" for short. It uses simple regression to convert one ticker to another. So while you are tracking one indicator, you can see where the expected value should fall on the other.

Applications?

The big application of this for me is being able to track where SPY/QQQ or IWM is falling during overnight trading sessions. Extended trading hours close at 8 pm NYSE time. After that, you have to guess where futures prices will put the ETF version of it. This indicator will allow you to track where, theoretically, the underlying ETF ticker will fall based on the current trading behaviour.

Some other applications are just the ability to track how similar or dissimilar one stock is to the other. For example, if we wanted to trade, say, Boeing using shares of DFEN or ITA (a defence specific ETF), here is what we get:

In the chart above we can see BA as the primary chart and ITA as the RCCI converted chart. We will see 2 major things that should cause us concern.

First, there is a really poor correlation between the two tickers. This indicates that ITA may not produce the best exposure if I am directly looking for Boeing exposure.

Second, there is a wide standard error. this means that the results that the RCCI is providing may be skewed up to +/- 2 points (as indicated by the standard error chart).

Let's take a look at BA and DFEN:

In the above, we can see that the correlation is not great, but the standard error is quite low.

This means that, while this may not be the best ticker for Boeing exposure, the RCCI is able to confidently calculate the ticker within +/- 0.50 cents based on BA's underlying data.

However, its important to note that it is not advisable to really rely on these results if the correlation is less than + 0.5 or greater than -0.5.

Let's take a look at a few more examples:

Above we have BA (NYSE) vs BA (NEO TSX CAD Hedged). We can see the strong relationship and high confidence calculations.

And some others:

SPX (primary) and ES1! (secondary):

RTY and IWM:

ES1! and SPY:

Customizations:

As you can see above, it is pretty straight forward. There are 3 options:

Lookback Length: Determines the length of assessment for correlation and the regression assessment.

Manual Ticker Input: The indicator will pull the data from your current chart and compare it against a manually selected indicator. You must tell the indicator which ticker you are comparing against.

Data Table: This will show you the data table which contains the standard error assessment and the correlation assessment. These are determined by your lookback length. The lookback length is defaulted to 500.

And that's the indicator! It's pretty straight forward. Hopefully you find it helpful, especially if you track futures during overnight sessions.

Leave your comments/questions and feedback below.

Thanks for checking it out!

30 Second Futures Session Open RangeThis indicator displays 30 second opening ranges from Globex, Europe, and RTH sessions.

From the RTH session range, it also displays infinitely generating Price Targets based on a % of the opening range size.

I am retrieving the 30 second data using the new "request.security_lower_tf()" function.

The importance of these levels is based on the idea that when the market opens, algorithms establish their positions within the first 30 seconds.

These areas can also be seen as potential areas of support and resistance throughout the sessions.

Enjoy!

The Multi-day Central Pivot RangeThe indicator is a Multi-day CPR.

It shows CPR range as per yesterday's HLC and also CPR range for last n number of trading sessions.

For example: If you mention the value as two in Multi-day CPR (blue color) then it calculates the CPR using HLC of the last two trading sessions.

Also, the daily CPR is designed in such a way to highlight Virgin CPR (purple color) separately from the normal CPR(fuchsia color) .

CM Time Based Vertical LinesCM Time Based Lines

Requested by codetrader to Visually Show Day Change on Intra-Day Charts.

Custom Indicator: Ability To Plot Recurring Time Lines On Chart!

Example of Uses:

Plot Lines at Midnight to Show Daily Change.

Plot Lines at Opening of Different Sessions.

Plot Lines at Opening and Closing of Sessions.

Plot Lines Every 4 Hours (Forex) To See 4-Hour Price Action!

Ability to Change Times!

Ability to Plot Up To 6 Recurring Time Based Lines!

Plus Many Other Uses!

Ability To Turn On/Off Any of the 6 Customizable Lines in Inputs Tab!

Ability To Change Thickness of Lines to Cover Multiple Bars!

Gold Timing Composite (EURUSD + DXY + US02Y)Here's the publication-ready description for TradingView:

Gold Timing Composite Indicator - 3-Component Model

Overview

A precision-engineered multi-component oscillator designed specifically for intraday gold trading. This indicator synthesizes three critical market drivers—EUR/USD dynamics, broad US Dollar strength, and Treasury yield movements—to isolate genuine gold price catalysts from market noise, delivering high-probability timing signals through triple-layer confirmation.

Components & Methodology

The indicator employs z-score normalization (default 20-period lookback) to harmonize three distinct but correlated market signals into a unified composite reading:

Fast Price Discovery Signal (40%):

EURUSD (40%) - EUR/USD captures rapid USD repricing with the deepest FX liquidity globally

Broad USD Strength Confirmation (35%):

-DXY (35%) - Inverted US Dollar Index measures comprehensive USD strength across six major currencies (EUR 57%, JPY 14%, GBP 12%, CAD 9%, SEK 4%, CHF 4%)

Real Yield Proxy (25%):

-US02Y (25%) - Inverted 2-Year Treasury yield captures Fed policy expectations and real rate dynamics

Key Features

✅ Dual USD Validation - EURUSD (speed) + DXY (breadth) filter EUR-specific moves from true USD weakness

✅ Real Yield Sensitivity - US02Y isolates rate-driven gold moves from pure currency effects

✅ Triple Confirmation System - Visual alignment dots when all three components agree simultaneously

✅ Mean-Reversion Zones - Overbought/oversold thresholds at ±1.5 standard deviations

✅ Clean Visualization - Candle-based display (no wicks) for rapid pattern recognition

✅ EUR/USD Divergence Detection - Identifies when EURUSD moves are EUR-specific vs broad USD moves

How to Use

Basic Signals:

Green candles = Bullish gold pressure (USD weakening / yields falling)

Red candles = Bearish gold pressure (USD strengthening / yields rising)

Above +1.5 = Overbought zone → look for mean-reversion shorts

Below -1.5 = Oversold zone → look for mean-reversion longs

High-Confidence Setups (Alignment Dots):

Lime dot at top = All 3 components bullish → maximum gold long confidence

Magenta dot at bottom = All 3 components bearish → maximum gold short confidence

No dots = Components diverging → reduce position size or wait for clarity

Divergence Trading:

Gold makes new high but composite doesn't confirm → potential reversal down

Gold makes new low but composite doesn't confirm → potential reversal up

Understanding Component Interactions

Normal Correlation (High Confidence):

EURUSD ↑ + DXY ↓ + US02Y ↓ → Broad USD weakness + falling yields → Strong gold bull signal

EURUSD ↓ + DXY ↑ + US02Y ↑ → Broad USD strength + rising yields → Strong gold bear signal

EURUSD/DXY Divergence (Critical Filter):

EURUSD ↑ but DXY flat/up → EUR-specific strength (ECB, Eurozone news) → Weak gold signal

DXY flat = USD not actually weak, just EUR strong → Gold may not follow EURUSD

EURUSD flat but DXY ↓ → Broad USD weakness (JPY, GBP, CAD all strong) → Strong gold signal

True USD weakness beyond just EUR → High-probability gold long

FX vs Yields Divergence:

EURUSD ↑ + DXY ↓ but US02Y ↑ → USD weak in FX but yields rising → Mixed signal

Hawkish Fed repricing vs currency weakness → Medium confidence, smaller size

EURUSD ↓ + DXY ↑ but US02Y ↓ → USD strong but yields falling → Conflicting drivers

Could be risk-off (safe haven bid to Treasuries) → Analyze broader market context

Best Practices

Timeframes: 5-minute to 15-minute charts for intraday trading

Session Focus: London fix (10:30 AM GMT) and New York open (8:20 AM EST) for peak gold liquidity

Pair With:

Key gold technical levels (round numbers, previous highs/lows)

COMEX gold futures volume profile

Real yield charts (when available)

VIX for risk sentiment context

Risk Management:

Full position: When alignment dots appear (all 3 components agree)

Half position: When 2 of 3 components align

Wait/reduce: When all three components diverge

Weight Adjustments:

Fed announcement days (FOMC, CPI, NFP): Increase US02Y to 35%, reduce EURUSD to 35%

ECB policy days: Monitor EURUSD/DXY divergence closely (EUR-specific moves may not affect gold)

Geopolitical events: DXY and yields may diverge (safe-haven flows) → Focus on DXY + yields, reduce EURUSD weight

Asian session: EURUSD less reliable (lower liquidity), consider increasing DXY weight to 45%

Technical Details

Calculation Method: Z-score normalization with configurable lookback period

Default Weights: EURUSD 40% | -DXY 35% | -US02Y 25%

Extreme Threshold: ±1.5 standard deviations (adjustable)

Alignment Trigger: All 3 components in unanimous agreement

Customizable Parameters:

Z-score lookback period (default: 20)

15-20: Faster, more sensitive (intraday focus)

30-50: Slower, smoother (swing trade context)

Individual component weights

Extreme threshold levels (1.3 for more signals, 1.8 for extremes only)

Alignment indicator toggle

Advantages Over Simple Indicators

Unlike single-instrument or DXY-only indicators, this composite:

Filters EUR-specific noise - When EURUSD moves but DXY doesn't confirm, gold often doesn't follow

Combines speed + breadth - EURUSD for fast entries, DXY for broad confirmation

Isolates real yield drivers - US02Y separates rate-driven moves from pure FX effects

Identifies regime shifts - When FX and yields diverge, signals changing market dynamics

Adaptable weighting - Adjust for different sessions, events, or market regimes

Real-World Signal Examples

Example 1: High-Confidence Long (All Aligned)

Fed dovish surprise → US02Y falls sharply

USD sells off → EURUSD rises + DXY falls

Composite surges, lime dot appears

Action: Full position gold long

Example 2: False Signal (EUR-Specific)

ECB hawkish statement → EURUSD rallies

But DXY unchanged (JPY, GBP, CAD not moving)

US02Y also unchanged

Composite rises but no alignment dot

Action: Small/no gold position (move is EUR-specific, not USD weakness)

Example 3: Mixed Signal (FX vs Yields)

Strong US jobs data → US02Y spikes (bearish gold)

But USD sells off in FX → EURUSD up + DXY down (bullish gold)

Composite shows divergence, no dots

Action: Wait for clarity or trade with tight stops

Example 4: Divergence Entry

Gold makes new intraday high

But composite fails to confirm (makes lower high)

Bearish divergence forms

Action: Short gold on next pullback

Suggested Complementary Analysis

Fundamental:

Fed vs ECB policy divergence and forward guidance

Real yield trends (10Y TIPS when available)

Inflation expectations (breakevens)

Central bank balance sheet changes

Geopolitical risk premium

Technical:

Gold futures COT (Commitment of Traders) positioning

COMEX gold open interest

Gold/Silver ratio

Mining stock performance (GDX, GDXJ)

Intermarket:

US equity market performance (risk-on/risk-off context)

Crude oil (inflation proxy)

Copper (growth expectations)

Bitcoin correlation (alternative store of value narrative)

Limitations & Considerations

When the Indicator Struggles:

Flash crashes or circuit breakers - Extreme events can break normal correlations temporarily

Asian session gaps - Lower EURUSD liquidity can cause false signals

Central bank interventions - SNB or BOJ FX intervention distorts DXY temporarily

Geopolitical shocks - Gold can decouple from USD/yields during wars, crises (safe-haven bid)

Quarter-end flows - Rebalancing can create temporary USD moves unrelated to fundamentals

Best Used When:

Normal market conditions (liquid sessions, no major shocks)

Clear trending or mean-reverting environment

Components showing consistent correlations

Combined with price action and volume confirmation

Performance Optimization Tips

Backtest your timeframe - Test 15-25 lookback periods to find optimal sensitivity

Session-specific weights - Use different weight profiles for London vs New York vs Asia

Combine with price action - Don't trade composites alone; wait for gold to confirm with candle patterns

Monitor component correlations - If EURUSD/DXY correlation breaks down, reduce both weights temporarily

Use with stop-loss discipline - Composite extremes suggest mean-reversion, but trends can extend

Disclaimer

This indicator is a technical analysis tool and does not guarantee profitable trades. Gold markets are influenced by numerous factors including geopolitics, central bank policy, inflation, and market sentiment that cannot be fully captured by any indicator. Always employ proper risk management, position sizing, and stop-losses. Backtest thoroughly before live implementation. Past performance is not indicative of future results.

Credits

Developed for intraday precious metals traders seeking multi-factor confirmation for gold timing decisions. Built on intermarket analysis principles combining currency dynamics, interest rate differentials, and statistical normalization for robust signal generation. Designed to filter EUR-specific noise and isolate true USD weakness—the primary driver of gold price movements.

Version: 1.0

Pine Script Version: 6

Asset Class: Precious Metals (Gold, Silver)

Category: Oscillators, Multi-Timeframe Analysis, Intermarket Analysis

Use Case: Intraday mean-reversion and momentum timing for gold (XAUUSD, GC futures)

Trading gold with this indicator? Share your results, questions, or improvement suggestions in the comments!

Baby ICT Simple Asia H/L + Sweeps + FVG + Alerts + Do-NothingBaby ICT Simple+ is a lightweight, rules-based TradingView indicator designed to help traders visualize key ICT-style concepts without complexity or signal-chasing. It focuses on Asia session liquidity, after, and fair value gapsto su

This tool is intentionally simple and is meant to be used alongside session timing, price action, and risk management — not as a buy/sell signal generator.

🔍 What This Indicator Displays

But

Automatically tracks and plots the Asia session high and low

Fully customizable line colors and width

These levels often act as liquidity pools before London and New York sessions

Liquidity Sweeps (Post-Asia)

Identifies the first time price takes liquidity above or below the Asia range

Sweep detection can be based on wicks or closes

Optional sweep labels help highlight potential stop-run behavior

Asia Break & Sweep Alerts

Alerts when price breaks the Asia high or low after the Asia session ends

Optional alerts for the first sweep only, helping traders focus on high-quality context

Fair Value Gaps (FVGs)

Detects classic 3-candle price imbalances on the active timeframe

Optional filter to show only FVGs that form after a liquidity sweep

Bullish and bearish FVGs are fully customizable with separate fill and border colors

“Do Nothing” Discipline Labels

Optional warning labels during a user-defined kill zone

Designed to discourage over-trading when:

No liquidity has been taken

Price is stuck mid-range

A sweep occurred but no clean displacement or fresh FVG followed

🧠 Intended Use

This indicator supports a “Baby ICT” approach, emphasizing:

Waiting for liquidity to be taken before looking for entries

Using Fair Value Gaps as entry zones, not signals

Avoiding mid-range and low-probability environments

Trading primarily during active sessions (London / New York)

Best used on:

5-minute charts

Index futures (ES, NQ) or liquid FX pairs

With session-based execution and strict risk control

🚫 What This Indicator Is NOT

❌ Not a buy/sell signal tool

❌ Not an automated trading strategy

❌ Not predictive or guaranteed

All trade decisions remain the responsibility of the trader.

⚠️ Risk Disclaimer

Trading involves risk. This indicator is provided for educational and informational purposes only and does not constitute financial advice. Always manage risk responsibly and test any tool thoroughly before using it in live markets.

✨ Final Notes

If you are looking for a clean, non-hype way to visualize:

Where liquidity is likely taken

Where price may rebalance

When it’s best to stand aside

Baby ICT Simple+ was built for that purpose.

Multi-Session H/L - Sweep & Grab v5# Multi-Session High/Low Levels with Liquidity Sweep & Grab Detection

## Overview

This indicator automatically identifies and plots the High and Low levels of key trading sessions (Asia, London, New York AM, New York PM) and Previous Day levels. It features advanced **Liquidity Sweep** and **Liquidity Grab** detection based on ICT/SMC methodology.

## Key Features

### 📊 Multi-Session Tracking

- **Asia Session** - Captures the Asian trading range

- **London Session** - Tracks the London open volatility

- **New York AM Session** - Monitors the NY morning session

- **New York PM Session** - Follows the afternoon price action

- **Previous Day High/Low** - Key daily reference levels

### 💧 Liquidity Detection (ICT/SMC Concepts)

**Liquidity Grab:**

- Detected when price **wicks through** a level but **closes back** inside

- Single candle event with rejection

- Often signals a potential reversal

- Label shows: `"Session H/L (Grab)"`

**Liquidity Sweep:**

- Detected when price **closes beyond** the level

- Indicates liquidity has been fully taken

- Label shows: `"Session H/L (Swept)"`

### 🎯 Visual Features

- Lines automatically **stop at the candle** where liquidity was grabbed or swept

- Different line styles for Active / Grabbed / Swept levels

- Customizable colors for each session

- Optional session background highlighting

- Information table showing all levels and their status

### ⚙️ Customization Options

- Adjustable session times for any timezone (GMT+0 to GMT+5)

- Calculation timeframe selection

- Line width and style settings

- Label size options

- Toggle each session on/off

- "Stop Line on Grab" option

### 🔔 Alerts

- Separate alerts for **Liquidity Grab** events

- Separate alerts for **Liquidity Sweep** events

- Available for all sessions and Previous Day levels

## How to Use

1. **Identify Key Levels:** The indicator automatically marks session highs and lows

2. **Watch for Liquidity Events:** Monitor when price approaches these levels

3. **Grab = Potential Reversal:** A liquidity grab (wick rejection) often signals smart money has collected orders and price may reverse

4. **Sweep = Liquidity Taken:** A sweep (close beyond level) confirms the liquidity pool has been cleared

5. **Plan Your Trades:** Use these levels in confluence with other SMC concepts like Fair Value Gaps (FVG) and Order Blocks (OB)

## Status Colors in Table

- 🟢 **Green (Active)** - Level has not been touched

- 🟠 **Orange (Grab)** - Wick touched the level, potential reversal zone

- 🔴 **Red (Swept)** - Close beyond level, liquidity fully taken

## Settings Explained

| Setting | Description |

|---------|-------------|

| Calculation Timeframe | Timeframe used for session calculations |

| Timezone | Your broker's timezone (GMT+0 to GMT+5) |

| Extend Lines | Extend active lines into the future |

| Stop Line on Grab | If enabled, lines stop when grabbed (not just swept) |

| Swept/Grab Line Style | Visual differentiation for liquidity events |

## Notes

- Works on all markets (Forex, Crypto, Stocks, Indices, Commodities)

- Best used on timeframes from 1min to 1H

- Session times are fully customizable to match your time zone

- The indicator respects the ICT/SMC definition where a **Grab** is a single-candle wick rejection and a **Sweep** involves price closing beyond the level

4MAs+5VWAPs+FVG+ Fractals4MAs + 5VWAPs + FVG + Fractals

All-in-one market structure indicator combining 4 moving averages, 5 VWAP timeframes, fair value gaps, fractals, and order blocks.

🔧 Features:

· 4 MAs - SMA/EMA, customizable lengths & colors

· 5 VWAPs - Daily, Weekly, Monthly, RTH, Custom sessions

· Fractals - Market structure with breakout lines & custom colors

· FVG/Imbalances - Bullish/bearish gap detection with alerts

· Order Blocks - Dynamic institutional levels

· Smart Labels - VWAP labels with color matching

⚙️ Quick Setup:

1. Toggle groups in Master Control Panel

2. Customize colors for each component

3. Set sessions for RTH/Custom VWAP

4. Adjust fractal periods (default: 2)

📈 Trading Use:

· Identify market structure with fractals

· Find confluence at VWAP + MA levels

· Trade FVG fills and order block reactions

· Multiple timeframe analysis with 5 VWAPs

Customizable • Color-Coordinated • Performance Optimized