SHYY TFC SPX Sectors list This script provides a clean, configurable table displaying real-time data for the major SPX sectors, key indices, and market sentiment indicators such as VIX and the 10-year yield (US10Y).

It includes 16 columns with two rows:

* The top row shows the sector/asset symbol.

* The bottom row shows the most recent daily close price.

Each price cell is dynamically color-coded based on:

* Direction (green/red) during regular trading hours

* Separate colors during extended hours (pre-market or post-market)

* VIX values greater than 30 trigger a distinct background highlight

Users can fully control the position of the table on the chart via input settings. This flexibility allows traders to place the table in any screen corner or center without overlapping key price action.

The script is designed for:

* Monitoring broad market health at a glance

* Understanding sector performance in real-time

* Spotting risk-on/risk-off behavior (via SPY, QQQ, VIX, US10Y)

Unlike traditional watchlists, this table visually encodes directional movement and trading session context (regular vs. extended hours), making it highly actionable for intraday, swing, or macro-level analysis.

All data is pulled using `request.security()` on daily candles and uses pure Pine logic without external dependencies.

To use:

1. Add the indicator to your chart.

2. Adjust the table position via the input dropdown.

3. Read sector strength or weakness directly from the table.

Cari dalam skrip untuk "spx"

Relative Strength vs SPX

This indicator calculates the ratio of the current chart's price to the S&P 500 Index (SPX), providing a measure of the stock's relative strength compared to the broader market.

Key Features:

Dynamic High/Low Detection: Highlights periods when the ratio makes a new high (green) or a new low (red) based on a user-defined lookback period.

Customizable Lookback: The lookback period for detecting highs and lows can be adjusted in the settings for tailored analysis.

Visual Overlay: The ratio is plotted in a separate pane, allowing easy comparison of relative strength trends.

This tool is useful for identifying stocks outperforming or underperforming the S&P 500 over specific timeframes.

Normalized SP100/SP400 Ratio with Shiller PE Ratio (CAPE Ratio)This indicator is designed to observe market concentration and overall valuation by combining the Shiller CAPE Ratio with the SP100/SP400 ratio.

Blue Line: Represents the Shiller CAPE Ratio, which reflects the overall market valuation.

Yellow Line: Represents the SP100/SP400 ratio, which indicates market concentration.

The combination of these two metrics provides insight into market dynamics. Historically, on the SPX monthly chart, when the yellow line (SP100/SP400 ratio) crosses below the blue line (CAPE Ratio), it has been followed by a period of stock market gains.

Justification for Combination:

The Shiller CAPE Ratio is a widely recognized indicator of market valuation, providing a long-term perspective on whether the market is overvalued or undervalued. The SP100/SP400 ratio, on the other hand, measures the concentration of the market by comparing the largest 100 companies to the next 400 mid-sized companies.

By normalizing both metrics and analyzing their relationship, this script provides a unique perspective on market movements. The crossunder of the SP100/SP400 ratio below the CAPE Ratio may signal a shift in market sentiment or concentration, often leading to potential market rallies. This combination is not just a simple merger of indicators but rather a thoughtful integration that adds value by highlighting periods where market concentration and valuation dynamics align.

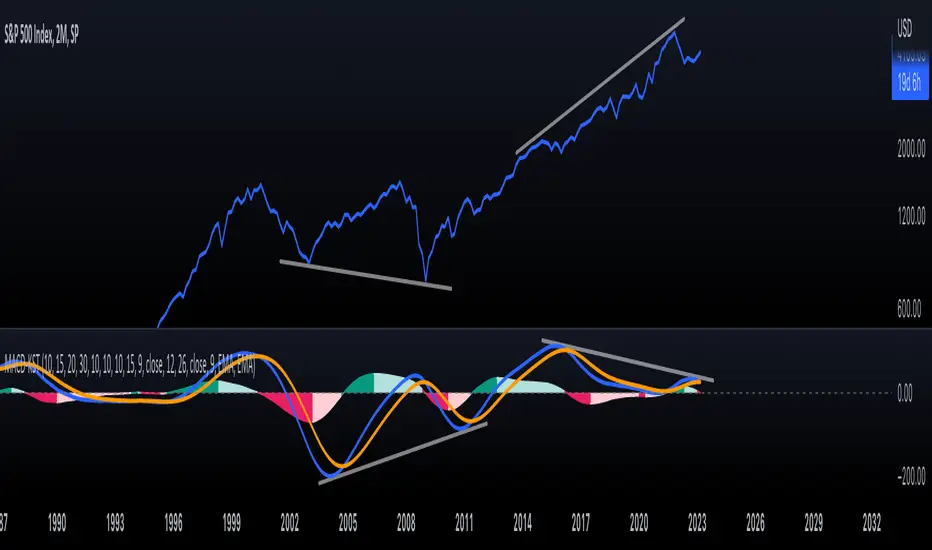

KST-Based MACDAs a follow-up to my previous script:

I am posting a stand-alone KST-based MACD.

Note that this indicator is highly laggy. Specific care must be taken when using it.

The MACD-Signal crossing is quite delayed but it is a definite confirmation.

For earlier signs, the Histogram must be analyzed. A shift from Green-White signals the 1st Bear Signal.

A MACD-Signal crossing signals the 2nd Bear SIgnal.

The same applies for bull-signs.

This indicator is useful for long-term charts on which one might want to pinpoint clear, longterm divergences.

Standard RSI, Stochastic RSI and MACD are notoriously problematic when trying to pinpoint long-term divergences.

Finally, this indicator is not meant for pinpointing entry-exit positions. I find it useful for macro analysis. In my experience, the decreased sensitivity of this indicator can show very strong signs, that can be quite laggy.

Inside the indicator there is a setting for "exotic calculations". This is an attempt to make this chart work in both linear/ negative charts (T10Y2Y) and log charts (SPX)

Tread lightly, for this is hallowed ground.

-Father Grigori

Rsi strategy for BTC with (Rsi SPX)

I hope this strategy is just an idea and a starting point, I use the correlation of the Sp500 with the Btc, this does not mean that this correlation will exist forever!. I love Trading view and I'm learning to program, I find correlations very interesting and here is a simple strategy.

This is a trading strategy script written in Pine Script language for use in TradingView. Here is a brief overview of the strategy:

The script uses the RSI (Relative Strength Index) technical indicator with a period of 14 on two securities: the S&P 500 (SPX) and the symbol corresponding to the current chart (presumably Bitcoin, based on the variable name "Btc_1h_fixed"). The RSI is plotted on the chart for both securities.

The script then sets up two trading conditions using the RSI values:

A long entry condition: when the RSI for the current symbol crosses above the RSI for the S&P 500, a long trade is opened using the "strategy.entry" function.

A short entry condition: when the RSI for the current symbol crosses below the RSI for the S&P 500, a short trade is opened using the "strategy.entry" function.

The script also includes a take profit input parameter that allows the user to set a percentage profit target for closing the trade. The take profit is set using the "strategy.exit" function.

Overall, the strategy aims to take advantage of divergences in RSI values between the current symbol and the S&P 500 by opening long or short trades accordingly. The take profit parameter allows the user to set a specific profit target for each trade. However, the script does not include any stop loss or risk management features, which should be considered when implementing the strategy in a real trading scenario.

ILM COT Financial Table - CFTCUse this indicator on Daily Timeframe

Please refer to the below link for CFTC Financials

www.cftc.gov

This script shows the Financial COT for the respective instrument by deriving the CFTC code.

Option is provided to override the CFTC code

User can also configure the historical CFTC data view

The script calculates the Long% vs Short% for various categories (Dealers/Asset Managers/Leveraged Funds/Other Reportables) and color codes the column appropriately.

The goal of this script is to show all the financial CFTC data on a single page to digest the data better in a tabular form

Fixed the default TradingView Library which has some errors with CFTC code mapping.

For example, SPX CFTC Code #13874+ which is the most important one where big players take positions is not there in the default Library.

VWAP Push StrategyThis strategy is unfortunately not finished yet.

A pretty simple strategy. If price broke through VWAP and had three consecutive candles following the breakthroughs trend, the high of the third candle will be drawn. If this happened after a crossover of the vwap and price breaks through the high of the third candle, strategy will go long. Short will be the same after crossing under the vwap. A long or short will be closed after crossing the vwap in the opposite direction, so the vwap is kind of a trailing stop.

Unfortunately, I could not manage to stop the script from entering multiple times into one drawn high or low. Of course, if a high was crossed the script should wait for a new formed high before entering a new long. If someone would find a solution to this, it would be great, because I think it is a nice strategy .

Should work great scalping 5min charts (when scripting, I used the SPX for reference).

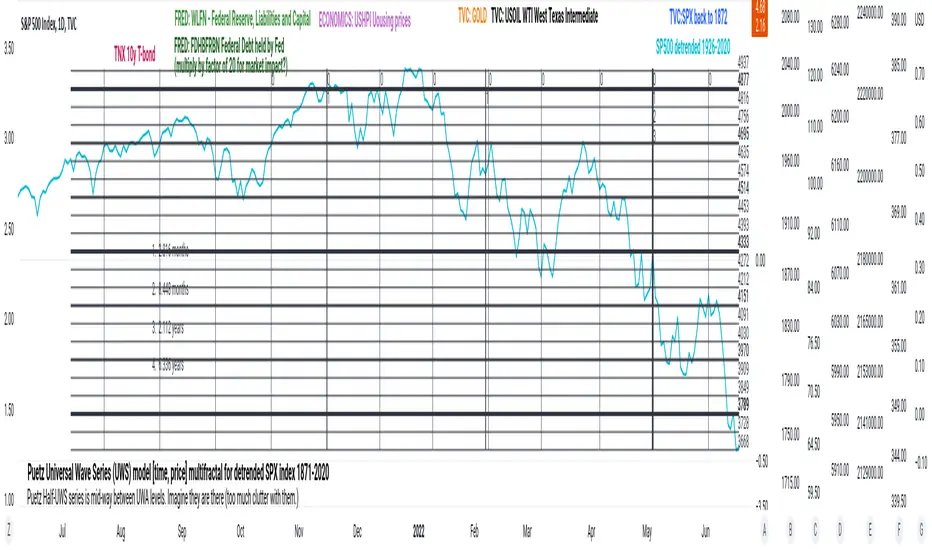

PuetzUWS [time, price] multiFractal mirrors, SPX 1872-2020This script is simply provided because a few rare people may actually be able to use one or two coding ideas. It is not possible to provide useful (description, explanation)s here. Maybe you can find those with a webSearch. If anybody is interested in the basic concept, just copy the code and run with it.

As the original was in violation of PineScript rules, I've removed many links, including :

- documentation of my code

- external sources of code

- blog solutions to Pine script programming

- math, science references, people

Hopefully it will won't be rejected this time, if so, too bad. I only made it through 10% of the conceptual objectives, and I do not believe any of the rest of the concepts are do-able in Pine Script. The current coding is (incomplete, unstable) but does give a faint idea of my "first step" intents. I have stopped all work, as I have to get back to my real projects (nothing to do with markets).

Volatility Calculator for Daily Top and Bottom RangeWith the usage of ATR, applied on the close of the daily candle, I am calculated the volatility channels for the TOP and BOTTOM

Based on this logic, we can estimate, with a huge confidence factor, where the prices are going to be compressed for the trading day.

Having said that, lets take a look at the data gathered among the most important financial markets:

SPX

TOP CROSSES : 2116

BOT CROSSES : 1954

Total Daily Candles : 18908

Occurance ratio = 0.215

NDX

TOP CROSSES : 1212

BOT CROSSES : 1183

Total Daily Candles : 9386

Occurance ratio = 0.255

DIA

TOP CROSSES : 759

BOT CROSSES : 769

Total Daily Candles : 6109

Occurance ratio = 0.25

DXY

TOP CROSSES : 1597

BOT CROSSES : 1598

Total Daily Candles : 13156

Occurance ratio = 0.243

DAX

TOP CROSSES : 1878

BOT CROSSES : 1848

Total Daily Candles : 13155

Occurance ratio = 0.283

BTC USD

TOP CROSSES : 416

BOT CROSSES : 417

Total Daily Candles : 4290

Occurance ratio = 0.194

ETH USD

TOP CROSSES : 247

BOT CROSSES : 268

Total Daily Candles : 2452

Occurance ratio = 0.21

EUR USD

TOP CROSSES : 820

BOT CROSSES : 805

Total Daily Candles : 7489

Occurance ratio = 0.217

GOLD

TOP CROSSES : 1722

BOT CROSSES : 1569

Total Daily Candles : 13747

Occurance ratio = 0.239

USOIL

TOP CROSSES : 1077

BOT CROSSES : 1089

Total Daily Candles : 10231

Occurance ratio = 0.212

US 10Y

TOP CROSSES : 1302

BOT CROSSES : 1365

Total Daily Candles : 9075

Occurance ratio = 0.294

Based on this, we can assume with a very high confidence ( 70-80%) that the market is going to stay, within the range created from the BOT and TOP ATR points.

PClose Levels 2.0This script plots the levels generated via a combination of SPX 2Y Quartiles for everyday, red days, and green days. It is intended for use solely with SPX.

These quartiles are also sorted by VIX averages into bands that expand and contract with VIX.

It gives us an idea of what levels to potentially expect resistance/support fairly well, but is designed to be used in conjunction with other indicators and macroeconomic information.

Green Dashed is your Expected Max Range (EMR+) based on Green Day averages.

Green Dotted is your Expected Range (ER+) based on full dataset averages.

Green solid lines are POS2 and POS1, based on Green Day averages.

White Dotted is your Expected Move (EM), based on full dataset averages.

Red solid lines are NEG1 and NEG2, based on Red Day averages.

Red Dotted is your Expected Range (ER-) based on full dataset averages.

Red Dashed is your Expected Max Range (EMR-) based on Red Day averages.

VIX SPX & XJOVix is a volatility indicator that lets traders know when to be cautious.

This indicator shows the volatility for the US market as well as the Australian market on seperate lines.

Blue lines are Vix for SPX (S&P 500)

If blue indicator goes above 30, high volatility is present and caution should be taken.

Green lines are Vix for XJO (ASX 200)

If green indicator goes above 20, high volatility is present and caution should be taken.

S&P Sector Advance/Decline Weighted -Tom1traderEnjoy, enhance your trading (I hope), copy or adapt to your needs and keep smiling!

Thanks to @MartinShkreli. The sector variables and the "repaint" option (approx lines 20 through 32 of this script) are used directly from your script "Sectors"

RECOMMENDATION: Update the sector weightings -inputs are provided. They change as often as monthly and the

annual changes are certainly significant. When updating weighting percentages use the decimal value. I.E. 29% is .29

Good on any time frame. Especially SPY, SPX and ES scalpers and 0DTE options traders may like this a lot.

This gives good signals on S & P and related (ES, SPY) and indicates / plots differently than the AD line or ratio.

Each sector's entire % weight is added or subtracted depending of whether that sector advanced or declined.

Example: Information Tech weight at 29% so that % of 500 (145) is added if InfoTech is up a penny and subtracted if it is

down a penny. All sectors processed the same way so that for a given bar/candle the value will be between +500 (all

sectors up) and -500 (all sectors down). This weighted AD line of sectors is scaled to +/- 350 and plotted as a red/green line

along with aqua/fuchsia columns of its 5 period ema. The line is actual sector behavior and the columns seem to make a

good signal with column zero crosses standing out.

The columns aqua / fuchsia are a 5 period ema of the Sector AD line and give pretty good signals at

zero cross for SPX. I colored the AD red green line also to emphasize the times it opposes the ema

for example the histo/colums zero cross signal is NOT true when the AD line is showing all or most sectors

going the other way.

For readability, the AD line itself is scaled to 350. This lets the columns of the ema stand out better. The hlines at

350 and at 175 give an idea for the AD green red line how much of the sector's weight is up or down.

350 is all sectors up (advancing) and -350 is all sectors down (declining). The hlines at +/- 175 seem to outline

a more or less "neutral" zone. For example in an uptrend with most of the AD level positive and the columns positive;

a negative spike that does not pass the -175 line and returns positive does not seem to impact the price as much as

a deeper negative spike.

S&P Sector CorrelationScript for Macro:

This indicator shows the 9 day average of the correlation of the 11 S&P500 sectors with the security.

Recommend you use the indicator on SPX or SPY, but you can change the values to be compared.

GLHF

- DPT

vol_premiaThis script shows the volatility risk premium for several instruments. The premium is simply "IV30 - RV20". Although Tradingview doesn't provide options prices, CBOE publishes 30-day implied volatilities for many instruments (most of which are VIX variations). CBOE calculates these in a standard way, weighting at- and out-of-the-money IVs for options that expire in 30 days, on average. For realized volatility, I used the standard deviation of log returns. Since there are twenty trading periods in 30 calendar days, IV30 can be compared to RV20. The "premium" is the difference, which reflects market participants' expectation for how much upcoming volatility will over- or under-shoot recent volatility.

The script loads pretty slow since there are lots of symbols, so feel free to delete the ones you don't care about. Hopefully the code is straightforward enough. I won't list the meaning of every symbols here, since I might change them later, but you can type them into tradingview for data, and read about their volatility index on CBOE's website. Some of the more well-known ones are:

ES: S&P futures, which I prefer to the SPX index). Its implied volatility is VIX.

USO: the oil ETF representing WTI future prices. Its IV is OVX.

GDX: the gold miner's ETF, which is usually more volatile than gold. Its IV is VXGDX.

FXI: a china ETF, whose volatility is VXFXI.

And so on. In addition to the premium, the "percentile" column shows where this premium ranks among the previous 252 trading days. 100 = the highest premium, 0 = the lowest premium.

S&P15 = 33.0% of SPXThis indicator shows what the top 15 stocks in the SPX is doing in a chart form.

VIX Implied Move Bands for ES/Emini futuresThis script uses the close of the VIX on a daily resolution to provide the 'implied move' for the E-mini SP500 futures. While it can be applied to any equity index, it's crucial to know that the VIX is calculated using SPX options, and may not reflect the implied volatility of other indices. The user can adjust the length of the moving average used to calculate the bands, the window of days used to calculate the implied move, and the multiplier that effects the width of the bands.

Compare Stock to a reference stock (e.g. SPX) Compare Stock to a reference stock (e.g. SPX) for input period

Blue barchart show the stock increment in the period > reference stock, vice versa for red barchart

ADL-NDX ADL-SPX Rank Difference Black: Adl Nasdaq + Adl Spx

Red: ADL nasdaq - ADLSPD

If red~0 and black >> 0 or << 0: wait more volatility

Relative Performance between between Stock and SPXSimply plots the close to close performance of your instrument vs SPX below your main chart

Offers further SMA of EMA of such relative performance to get a better idea of the relative strength against the major market

IV/HV ratio 1.0 [dime]This script compares the implied volatility to the historic volatility as a ratio.

The plot indicates how high the current implied volatility for the next 30 days is relative to the actual volatility realized over the set period. This is most useful for options traders as it may show when the premiums paid on options are over valued relative to the historic risk.

The default is set to one year (252 bars) however any number of bars can be set for the lookback period for HV.

The default is set to VIX for the IV on SPX or SPY but other CBOE implied volatility indexes may be used. For /CL you have OVX/HV and for /GC you have GVX/HV.

Note that the CBOE data for these indexes may be delayed and updated EOD

and may not be suitable for intraday information. (Future versions of this script may be developed to provide a realtime intraday study. )

There is a list of many volatility indexes from CBOE listed at:

www.cboe.com

(Some may not yet be available on Tradingview)

RVX Russell 2000

VXN NASDAQ

VXO S&P 100

VXD DJIA

GVX Gold

OVX OIL

VIX3M 3-Month

VIX6M S&P 500 6-Month

VIX1Y 1-Year

VXEFA Cboe EFA ETF

VXEEM Cboe Emerging Markets ETF

VXFXI Cboe China ETF

VXEWZ Cboe Brazil ETF

VXSLV Cboe Silver ETF

VXGDX Cboe Gold Miners ETF

VXXLE Cboe Energy Sector ETF

EUVIX FX Euro

JYVIX FX Yen

BPVIX FX British Pound

EVZ Cboe EuroCurrency ETF Volatility Index

Amazon VXAZN

Apple VXAPL

Goldman Sachs VXGS

Google VXGOG

IBM VXIBM