Ludvig Indicator PROThe Ludvig Indicator is designed to identify high-probability breakout setups by combining trend, volume, volatility, and relative strength filters. It helps you enter stocks (or ETFs/crypto) when institutional money is likely flowing in, while avoiding false breakouts and weak trends.

🔑 Core Features

Zero-Lag EMA (ZLEMA)

Faster, less lagging trend detection compared to traditional EMAs.

Used as the basis for dynamic ATR bands.

ATR Volatility Bands

Adaptive bands based on the Average True Range (ATR).

Define the zone where price must close outside to confirm trend strength.

Breakout Confirmation

Requires price to close above recent highs (lookback configurable).

Ensures signals are “true breakouts,” not just noise around moving averages.

Volume Filter (Relative Volume)

Validates breakouts with significantly higher volume than average.

Prevents low-liquidity signals from triggering.

Trend Strength (ADX)

Built-in ADX calculation ensures only strong, trending moves are considered.

Default filter: ADX ≥ 18 (configurable).

Relative Strength vs. Benchmark

Compares the asset’s momentum against a benchmark (default: SPY).

Only signals when the asset is outperforming the benchmark.

Useful for sector rotation and picking leaders instead of laggards.

Alerts & Signals

Breakout entries are marked with small green triangles.

Built-in alerts for automated notifications (TradingView alerts).

Cari dalam skrip untuk "spy"

Credit Spread Alpha SignalCredit Spread Alpha Signal: Complete Description

Introduction and Purpose

The Credit Spread Alpha Signal is a custom indicator developed for TradingView, designed to monitor the credit spread between High Yield (HY) bond yields and the 10-Year US Treasury yield (US10Y). This indicator serves as an advanced macroeconomic tool for traders and investors, helping to identify shifts in risk sentiment, monetary policy adjustments, or financial stress in the economy. It combines credit market data with statistical analysis to generate inverted buy and sell signals, where wider spreads (deteriorated conditions) are seen as buy opportunities (green), and tight spreads (risk-on) as sell opportunities (red).

The script is original, inspired by macroeconomic concepts, and visualizes data intuitively with histograms, background colors, and signal arrows. It is particularly useful for portfolio traders seeking confirmation signals or early warnings, integrating seamlessly into charts of stocks, bonds, or crypto assets.

Key Concepts

- HY Spread : Calculated as the difference between the High Yield Corporate Effective Yield (symbol: BAMLH0A0HYM2EY) and the US10Y Yield. Wider spreads indicate higher credit risk and economic deterioration (buy opportunity in the inverted logic). Tight spreads reflect market optimism (risk-on, sell opportunity).

- Inverted Signal Logic : Unlike traditional interpretation, here widening spreads (stress) trigger green and buy arrows (↑ below the chart), suggesting entry into long positions during panics. Compressing spreads trigger red and sell arrows (↓ above the chart), indicating exit during optimism peaks.

- Visual Highlights : Green for spread > +2.2σ (financial stress, buy); Red for spread < low threshold (risk-on, sell); Optional orange for recession risk (inverted curve + high spread, strong buy).

The indicator uses statistics like simple moving average (SMA) and standard deviation for dynamic thresholds, making it adaptable to different market periods.

How It Works: Internal Calculations

1. Data Sources : Uses `request.security` to fetch daily data ("D") from US10Y, US02Y (for inverted curve), and HY Yield.

2. Spread Calculation : `spread_hy = hy_yield - us10y`.

3. Statistics :

- Average (SMA) of the spread over the last `sma_length` days (default: 120).

- Standard deviation (stdev) over the same period.

- High threshold: `avg_spread_hy + std_mult * std_spread_hy` (default: multiplier 2.2).

- Low threshold: Editable value (default: 1.5%).

4. Conditions :

- High stress (green/buy): `spread_hy > high_threshold`.

- Compression (red/sell): `spread_hy < low_threshold`.

- Recession risk (orange/strong buy, optional): Inverted curve (`us10y < us2y`) + spread > `recession_spread_threshold`.

5. Crossings for Signals :

- Buy (green ↑ below): Crossover above high threshold (`ta.crossover`).

- Sell (red ↓ above): Crossunder below low threshold (`ta.crossunder`).

These calculations are processed bar by bar, ensuring real-time updates.

Visual Elements

- Histogram : Plots the spread as columns (`plot.style_columns`), dynamically colored: Light green (90% transparency) for stress/buy; Light red (90%) for compression/sell; Gray for neutral; Orange for recession.

- Reference Line : Horizontal red line at zero for benchmark.

- Background Coloring : Applies color to the main chart (overlay=true via force_overlay): Light green for buy, Light red for sell, Orange for recession, no color for neutral.

- Signal Arrows : ↑ Green below the bar for buy (widening_cross); ↓ Red above the bar for sell (compressed_cross).

- Floating Legend : Label in the lower panel explaining thresholds and conditions, dynamically updated with editable values.

Editable Settings (Inputs)

- SMA Period (days) : Default 120; adjusts the horizon for average and standard deviation.

- Standard Deviation Multiplier : Default 2.2; sets sensitivity of the high threshold (e.g., 2.2σ for moderate alerts).

- Low Threshold for Compression (%) : Default 1.5; level to detect risk-on/sell.

- Enable Recession Risk? : Default false; activates combined condition of inverted curve + high spread.

- Spread Threshold for Recession (%) : Default 2.0; level for recession (visible if enabled).

These inputs allow customization via the TradingView interface, without editing the code.

Integrated Alerts

The indicator includes alert conditions (`alertcondition`) for notifications in TradingView:

- "ALERT: HY Spread High": Spread exceeds threshold - financial stress (Buy).

- "ALERT: HY Spread Compressed": Spread compressed - risk-on conditions (Sell).

- "ALERT: HY Spread Widening (Buy)": Crossover above - buy opportunity in stress.

- "ALERT: HY Spread Compressed (Sell)": Crossunder below - sell opportunity in risk-on.

- "ALERT: Recession Risk (Strong Buy)": Inverted curve + high spread - high recession risk, consider buy (if enabled).

Set up alerts for email, SMS, or webhook notifications.

Usage Tips and Considerations

- Recommended Timeframe : Daily ("D"), but works on others; data is forced to daily for consistency.

- Practical Application : Add to charts of indices like SPY or QQQ to correlate with market moves. Test on historical periods (e.g., 2020 for widening, 2021 for compressing) to validate signals.

- Limitations : Relies on external data (US10Y, HY Yield), which may have delays; spreads are typically positive. Not financial advice – use with complementary analysis.

- Advanced Customization : Adjust thresholds for volatile markets; enable recession for more robust macro signals.

This indicator transforms credit data into actionable alpha, helping navigate economic cycles with visual precision. For support or modifications, refer to the source code or TradingView community.

ABS NR — Fail-Safe Confirm (v4.2.2)

# ABS NR — Fail-Safe Confirm (v4.2.2)

## What it is (quick take)

**ABS NR FS** is a **non-repainting “arm → confirm” entry framework** for intraday and swing execution. It blends:

* **Regime** (EMA stack + 60-min slope),

* **Location** (Keltner basis/edges),

* **Stretch** (session-anchored **VWAP Z-score**),

* **Momentum gating** (TSI cross/slope),

* **Guards** (session window, minimum ATR%, gap filter, optional market alignment).

You’ll see a **small dot** when a setup is **armed** (candidate) and a **triangle** when that setup **confirms** within a user-defined number of bars. A **gray “X”** marks a timeout (candidate canceled).

> Tip: This entry tool works best when paired with a trend context filter and a dedicated exit tool.

---

## How to use it (operational workflow)

1. **Read the regime**

* **Bull trend**: fast > slow > long EMA **and** 60-min slope up.

* **Bear trend**: fast < slow < long EMA **and** 60-min slope down.

* **Range**: neither bull nor bear.

2. **Wait for a candidate (dot)**

Two families:

* **Reclaim (trend-following):** price crosses the **KC basis** with acceptable |Z| (not overstretched) and passes the TSI gate.

* **Fade (range-revert):** price **pokes a KC band**, prints a **reversal wick**, |Z| is stretched, and TSI gate agrees.

3. **Trade the confirmation (triangle)**

The confirm must occur **within N bars** and follow your chosen **Confirm mode** logic (see Inputs). If confirmation doesn’t arrive in time, an **X** cancels the candidate.

4. **Use guards to avoid junk**

Session windows (US focus), minimum ATR%, gap guard, and optional **market alignment** (e.g., SPY above EMA20 for longs).

5. **Manage the position**

* Entries: take **triangles** in the direction of your playbook (reclaims with trend; fades in clean ranges).

* Filters and exits: use your own process or pair with a trend/exit companion.

---

## Visual semantics & alerts

* **Candidate L / S (dot)** → a setup armed on this bar.

* **CONFIRM L / S (triangle)** → actionable signal that met confirm rules within your time window.

* **Cancel L / S (X)** → candidate expired without confirmation; ignore the dot.

**Alerts (stable names for automation):**

* **ABS FS — Confirmed** → fires on confirmed long or short.

* **ABS FS — Candidate Armed** → fires as a candidate arms.

---

## Non-repainting behavior (why signals don’t repaint)

* All HTF requests use **lookahead\_off**.

* With **Strict NR = true**, the 60-min slope uses the **prior completed** 60-min bar and arming/confirming only occurs on confirmed bars.

* Confirmation triangles finalize on bar close.

* If you disable strictness, signals may appear slightly earlier but with more intrabar sensitivity.

---

## Inputs reference (what each control does and the trade-offs)

### A) Behavior / Modes

**Mode** (`Turbo / Aggressive / Balanced / Conservative`)

Changes multiple internal thresholds:

* **Turbo** → most signals; relaxes prior-bar break & VWAP-side checks and time/vol/gap guards. Highest frequency, highest noise.

* **Aggressive** → more signals than Balanced, fewer than Turbo.

* **Balanced** → default; steady trade-off of frequency vs. quality.

* **Conservative** → tightens |Z| and other checks; fewest but cleanest signals.

**Strict NR (bar close + prior HTF 60m)**

* **true** = safer: uses prior 60-min slope; arms/confirms on confirmed bars → **fewer/cleaner** signals.

* **false** = earlier and more reactive; slightly noisier.

---

### B) Keltner Channel (location engine)

* **KC EMA Length (`kcLen`)**

Higher → smoother basis (fewer basis crosses). Lower → snappier basis (more crosses).

* **ATR Length (`atrLen`)**

Higher → steadier band width; Lower → more reactive band width.

* **KC ATR Mult (`kcMult`)**

Higher → wider bands (fewer edge pokes → fewer fades). Lower → narrower (more fades).

---

### C) Trend & HTF slope

* **Trend EMA Fast/Slow/Long (`emaFastLen / emaSlowLen / emaLongLen`)**

Larger = slower regime flips (fewer reclaims); smaller = faster flips (more reclaims).

* **HTF EMA Len (60m) (`htfLen`)**

Larger = steadier HTF slope (fewer signals); smaller = more sensitive (more signals).

---

### D) VWAP Z-Score (stretch / mean-revert logic)

* **VWAP Z-Length (`zLen`)**

Window for Z over session-anchored VWAP distance. Larger = smoother |Z| (fewer fades/re-entries). Smaller = more reactive (more).

* **Range Fade |Z| (base) (`zFadeBase`)**

Minimum |Z| to allow **fades** in ranges. Raise to demand more stretch (fewer fades). Lower to take more fades.

* **Max |Z| Trend Re-entry (base) (`maxZTrendBase`)**

Caps how stretched price can be and still permit **reclaims** with trend. Lower = stricter (avoid chases). Higher = will chase further.

---

### E) TSI Momentum Gate

* **TSI Long/Short/Signal (`tsiLong / tsiShort / tsiSig`)**

Larger = smoother/laggier momentum; smaller = snappier.

* **TSI gate (`CrossOnly / CrossOrSlope / Off`)**

* **CrossOnly**: require TSI cross of its signal (strict).

* **CrossOrSlope**: cross *or* favorable slope (balanced default).

* **Off**: no momentum gate (most signals, most noise).

---

### F) Guards (filters to avoid low-quality tape)

* **US focus 09:35–10:30 & 14:00–15:45 (base) (`useTimeBase`)**

`true` limits to high-quality windows. `false` trades all session.

* **Skip N bars after 09:30 ET (`skipFirst`)**

Skips the open scramble. Larger = skip longer.

* **Min volatility ATR% (base)** = `useVolMinBase` + `atrPctMinBase`

Requires `ATR(10)/Close*100 ≥ atrPctMinBase`. Raise threshold to avoid dead tape; lower to accept quieter sessions.

* **Gap guard (base)** = `gapGuardBase` + `gapMul`

Blocks signals when the opening gap exceeds `gapMul * ATR`. Increase `gapMul` to allow more gapped opens; decrease to be stricter.

---

### G) Visuals & Sides

* **Plot Keltner (`plotKC`)** → show/hide basis & bands.

* **Show Longs / Show Shorts** → enable/disable each side.

---

### H) Fail-Safe Confirmation

* **Confirm mode (`BreakHighOnly / BreakHigh+Hold / TwoBarImpulse`)**

* **BreakHighOnly**: confirm by taking out the armed bar’s extreme. Fastest, most frequent.

* **BreakHigh+Hold**: must **break**, have **body ≥ X·ATR**, **and** hold above/below the basis → higher quality, fewer signals.

* **TwoBarImpulse**: decisive follow-through vs. prior bar with **body ≥ X·ATR** → momentum-biased confirmations.

* **Confirm within N bars (`confirmBars`)**

Confirmation window size. Smaller = faster validation; larger = more patience (can be later).

* **Impulse body ≥ X·ATR (`impulseBodyATR`)**

Raise for stronger confirmations (fewer weak triangles). Lower to accept lighter pushes.

* **Require market alignment (`needMarket`) + `marketTicker`**

When enabled: Longs require **market > EMA20 (5m)**; Shorts require **market < EMA20 (5m)**.

* **Diagnostics: Show debug letters (`debug`)**

Tiny “B/C” audit marks for base/confirm while tuning.

---

## Tuning recipes (quick, practical)

* **If you’re getting chopped:**

* Set **Mode = Conservative**

* **Confirm mode = BreakHigh+Hold**

* Raise **impulseBodyATR** (e.g., 0.45)

* Keep **needMarket = true**

* Keep **Strict NR = true**

* **If you need more signals:**

* **Mode = Aggressive** (or Turbo if you accept more noise)

* **Confirm mode = BreakHighOnly**

* Lower **impulseBodyATR** (0.25–0.30)

* Increase **confirmBars** to 3

* **Range-day focus (fades):**

* Keep session guard on

* Raise **zFadeBase** to demand real stretch

* Keep **maxZTrendBase** moderate (don’t chase)

* **Trend-day focus (reclaims):**

* Slightly **lower `maxZTrendBase`** (avoid chasing excessive stretch)

* Use **CrossOrSlope** TSI gating

* Consider turning **needMarket** on

---

## Best practices & notes

* **Instrument specificity:** Tune Z, TSI, and guards per symbol and timeframe.

* **Session awareness:** Session filter uses **exchange-local** time; adjust for non-US markets.

* **Automation:** Use the two provided alert names; they’re stable.

* **Risk management:** Confirmation improves quality but doesn’t remove risk. Always pre-define stop/size logic.

---

## Suggested starting point (balanced profile)

* **Mode = balanced**

* **Strict NR = true**

* **Confirm mode = BreakHigh+Hold**

* **confirmBars = 2**

* **impulseBodyATR ≈ 0.35**

* **needMarket = off** (turn on for extra confluence)

* Leave Keltner/TSI defaults; then nudge `zFadeBase` and `maxZTrendBase` to match your symbol.

---

*This tool is a signal generator, not a broker or strategy. Validate on your markets/timeframes and integrate with your risk plan.*

Whaley Thrust — ADT / UDT / SPT (2010) + EDT (EMA) + Info BoxDescription

Implements Wayne Whaley’s 2010 Dow Award breadth-thrust framework on daily data, with a practical extension:

• ADT (Advances Thrust) — 5-day ratio of advances to (adv+dec). Triggers: > 73.66% (thrust), < 19.05% (capitulation).

• UDT (Up-Volume Thrust) — 5-day ratio of up-volume to (up+down). Triggers: > 77.88%, < 16.41%. Defaults to USI:UVOL / USI:DVOL (edit if your feed differs).

• SPT (Price Thrust) — 5-day % change of a benchmark (default SPY, toggle to use chart symbol). Triggers: > +10.05%, < −13.85%.

• EDT (EMA extension) — Declines-share thrust derived from WBT logic (not in Whaley’s paper): EMA/SMA of Declines / (Adv+Decl). Triggers: > 0.8095 (declines thrust), < 0.2634 (declines abating).

• All-Clear — Prints when ADT+ and UDT+ occur within N days (default 10); marks the second event and shades brighter green.

Visuals & Controls

• Shape markers for each event; toggle text labels on/off.

• Optional background shading (green for thrusts, red for capitulations; brighter green for All-Clear).

• Compact info box showing live ADT / UDT / SPT (white by default; turns green/red at thresholds).

• Min-spacing filter to prevent duplicate prints.

Tips

• Use on Daily charts (paper uses 5 trading days). Weekly views can miss mid-week crosses.

• If UDT shows 100%, verify your Down Volume symbol; the script requires both UVOL and DVOL to be > 0.

• Best use: treat capitulations (−) as setup context; act on thrusts (+)—especially when ADT+ & UDT+ cluster (All-Clear).

Credit

Core method from Wayne Whaley (2010), Planes, Trains and Automobiles (Dow Award). EDT is an added, complementary interpretation using WBT-style smoothing.

Relative Strength Buy/Sell SignalsThis Pine Script builds on the MarketSurge-style Relative Strength indicator. It calculates the RS line by comparing the stock's close to a benchmark (default: SPY). Buy signals are generated when the RS line crosses above its moving average (default 10-period SMA), indicating improving relative strength. Sell signals occur when it crosses below, suggesting weakening relative strength. Signals are labeled "BUY" (green) and "SELL" (red) on the chart, with background highlights.

It also retains the new 52-week RS highs (orange circles) and lows (purple circles), which can serve as additional confirmation for outperformance or underperformance.

Note: This approximates relative strength for trading signals but does not replicate the proprietary IBD RS Rating (a 1-99 percentile rank across all stocks). For best results, use on daily charts and combine with other analysis. Backtest thoroughly, as no strategy guarantees profits

Signal Stack MeterWhat it is

A lightweight “go or no‑go” meter that combines your manual read of Structure, Location, and Momentum with automatic context from volatility and macro timing. It surfaces a single, tradeable answer on the chart: OK to engage or Standby.

Why traders like it

You keep your discretion and nuance, and the meter adds guardrails. It prevents good trade ideas from being executed in the wrong conditions.

What it measures

Manual buckets you set each day: Structure, Location, Momentum from 0 to 2

Volatility from VIX, term structure, ATR 5 over 60, and session gaps

Time windows for CPI, NFP, and FOMC with ET inputs and an exchange‑offset

Total score and a simple gate: threshold plus a “strong bucket” rule you choose

How to use in 30 seconds

Pick a preset for your market.

Set Structure, Location, Momentum to 0, 1, or 2.

Leave defaults for the auto metrics while you get a feel.

Read the header. When it says OK to engage, you have both your read and the context.

Defaults we recommend

OK threshold: 5

Strong bucket rule: Either Structure or Location equals 2

VIX triggers: 22 and 1.25× the 20‑SMA

Term mode: Diff at 0.00 tolerance. Ratio mode at 1.00+ is available

ATR 5/60 defense: 1.25. Offense cue: 0.85 or lower

ATR smoothing: 1

Gap mode: RTH with 0.60× ATR5 wild gap. ON wild range at 0.80× ATR5

CPI window 08:25 to 08:40 ET. FOMC window 13:50 to 14:30 ET

ET to exchange offset: −60 for CME index futures. Set to 0 for NYSE symbols like SPY

Alert cadence: Once per RTH session. Snooze first 30 minutes optional

New since the last description

Parity with Defense Mode for presets, sessions, ratio vs diff term mode, ATR smoothing, RTH‑key cadence, and snooze options

Event windows in ET with a simple offset to your exchange time

Alternate row backgrounds and full color control for readability

Exposed series for automation: EngageOK(1=yes) plus TotalScore

Debug toggle to see ATR ratio, term, and gap measurements directly

Notes

Dynamic alerts require “Any alert() function call”.

The meter is designed to sit opposite Defense Mode on the chart. Use the position input to avoid overlap.

RS Ratio vs Benchmark (Colored)📈 RS Ratio vs Benchmark (with Color Change)

A simple but powerful tool to track relative strength against a benchmark like QQQ, SPY, or any other ETF.

🔍 What it Shows

RS Ratio (orange line): Measures how strong a stock is relative to a benchmark.

Moving Average (teal line): Smooths out RS to show trend direction.

Color-coded RS Line:

🟢 Green = RS is above its moving average → strength is increasing.

🔴 Red = RS is below its moving average → strength is fading.

📊 How to Read It

Above 100 = Stock is outperforming the benchmark.

Below 100 = Underperforming.

Rising & Green = Strongest signal — accelerating outperformance.

Above 100 but Red = Consolidating or losing momentum — potential rest period.

Crosses below 100 = Warning sign — underperformance.

✅ Best Uses

Spot leading stocks with strong momentum vs QQQ/SPY.

Identify rotation — when strength shifts between sectors.

Time entries and exits based on RS trends and crossovers.

RSI Cloud Zones (by AButterfly)RSI instruction: Uptrend market only. LONG only. Should use only when SPY and QQQ are above 50 SMA and 200 SMA, and the 50sma is above 200sma, and RSI(14) is above 50 ............... BUY only in the GREEN area. Do NOT buy above GREEN green area. That would be chase (after a train, a ship that left). Take profit in the RED area, preferably on a green candle. This does not encourage SHORT-ing. LONG only. Disclaimer: This is an entertainment. If you lose money, don't blame this indicator or the creator. You have to pay attention to whether the market is on uptrend.

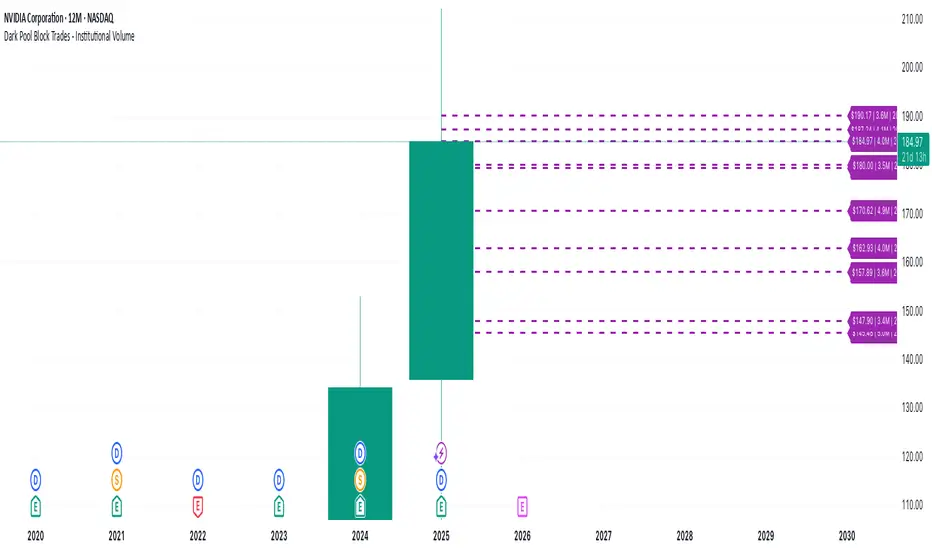

Dark Pool Block Trades - Institutional Volume📊 Dark Pool Block Trades - Institutional Volume

Visualize where institutional money positions before major price moves occur. This indicator reveals hidden dark pool block trades that often precede significant price movements - because when smart money deploys millions and billions in strategic accumulation or distribution, retail traders need to see where it's happening.

🎯 WHY DARK POOL DATA MATTERS:

Institutions don't move large capital randomly. Dark pool block trades represent strategic positioning by sophisticated money managers with superior research and conviction. These trades create hidden support/resistance levels that often predict future price action.

The key principle: Follow institutional flow, don't fight it. When institutions get involved, they create high-probability trading opportunities.

💰 HOW INSTITUTIONS INFLUENCE PRICE:

- Large block trades establish hidden accumulation/distribution zones

- Smart money builds positions BEFORE retail awareness increases

- Institutional activity creates "footprints" at key technical levels

- These trades often signal conviction plays ahead of major moves

- Institutions typically add to winning positions throughout trends

🔍 WHAT THIS INDICATOR SHOWS:

- Visual overlay of dark pool block trades directly on price charts

- Track institutional positioning across major stocks and ETFs

- Identify accumulation/distribution zones before they become obvious to retail

- Spot high-conviction institutional trades in real-time visualization

- Customizable block trade size filters and timeframe selection

- Historical institutional activity up to 5 years or custom ranges

💡 THE TRADING ADVANTAGE:

Instead of guessing price direction, see where institutions are already positioning. When large block trades appear in dark pools, you're witnessing strategic institutional commitment that frequently leads to significant price movements.

⚡ HOW IT WORKS:

This Pine Script displays institutional dark pool transactions as visual markers on your charts. The script comes with sample data for immediate use. For expanded ticker coverage and real-time updates, external data services are available.

🎯 IDEAL FOR:

- Swing traders following institutional footprints

- Traders seeking setups backed by smart money conviction

- Position traders looking for accumulation zones

- Anyone wanting to align with institutional flow rather than fight it

🔄 SAMPLE DATA INCLUDED:

Pre-loaded with institutional activity data across popular tickers, updated daily to demonstrate how dark pool activity correlates with future price movements.

The script initially covers these tickers going back 6 months showing the top 10 trades by volume over 400,000 shares: AAPL, AMD, AMZN, ARKK, ARKW, BAC, BITO, COIN, COST, DIA, ETHA, GLD, GOOGL, HD, HYG, IBB, IWM, JNJ, JPM, LQD, MA, META, MSFT, NVDA, PG, QQQ, RIOT, SLV, SMCI, SMH, SOXX, SPY, TLT, TSLA, UNH, USO, V, VEA, VNQ, VOO, VTI, VWO, WMT, XLE, XLF, XLK, XLU, XLV, XLY

SeikaAlgo–Long/Short Buy/Sell SignalSeikaAlgo–Long/Short Buy/Sell Signal — Simple, Visual, Reliable Signals

SeikaAlgo makes high-probability trading simple and actionable for everyone—no complex rules, no guesswork. Just follow these 3 steps:

How It Works

1. Watch for Buy/Sell Signals

Buy and Sell signals are printed right on your chart, only after the candle closes—never repaints, never lags. Trade with confidence.

2. Enter at Candle Close

Buy: Enter at the close of a candle when a green “B” label appears and price crosses above the green EMA 9.

Sell: Enter at the close of a candle when a red “S” label appears and price crosses below the red EMA 9.

3. Take Profit

Move your stop loss with each new candle (trailing stop), or use the EMA 9 line to trail stops.

Take profit when price reaches a Daily Fibonacci Level.

Example — 5min SPY

Buy Signal: Green label prints above green EMA 9 after candle closes. Enter at close, stop just below the signal candle’s low.

Sell Signal: Red label prints below red EMA 9 after candle closes. Enter at close, stop just above the signal candle’s high.

Key Features

No Lag, No Repainting: Signals only appear after a candle is complete—so you’re never chasing ghosts.

Clear Visual Cues: Instantly know when to buy, sell, or step aside.

Built-in Trailing Stop Logic: Protect your trades easily.

Works On Any Market/Timeframe: Perfect for stocks, futures, crypto, or forex.

SeikaAlgo is an invite-only indicator.

Add it to your chart, follow the labels and EMA, and trade with confidence—no clutter, no confusion. Simple, visual, reliable.

Cross-Symbol Price LevelsThis script enables you to map given price levels from a source symbol to the chart symbol. Originally intended for drawing Gamma Exposure levels from SPY onto ES and SPX.

Note that it uses the opening bar of the regular session to calculate the price conversion ratio.

(Developed with ChatGPT)

First Candle Low Break SignalTheory: If the SPY (or anything really) starts the day with a green candle, it never breaks below that candle on that day.

This indicator was quickly made to check that theory with some interesting results.

Requirement: The Symbol must be set to "extended trading hours", otherwise the script cannot see the changes between days.

TFPS - TradFi Pressure ScoreThe Data-Driven Answer to a New Market Reality.

This indicator quantifies the pressure exerted by Wall Street on the crypto market across four critical dimensions: Risk Appetite, Fear, Liquidity Flows, and the Opportunity Cost of Capital. Our research has found that the correlation between this 4-dimensional pressure vector and crypto price action reaches peak values of 0.87. This is your decisive macro edge, delivered in real-time.

The Irreversible Transformation

A fundamental analysis of the last five years of market data proves an irreversible transformation: The crypto market has matured into a high-beta risk asset, its fate now inextricably linked to Traditional Finance (TradFi).

The empirical data is clear:

Bitcoin increasingly behaves like a leveraged version of the S&P 500.

The correlation to major stock indices is statistically significant and persistent.

The "digital gold" narrative is refuted by the data; the correlation to gold is virtually non-existent.

This means standard technical indicators are no longer sufficient. Tools like RSI or MACD are blind to the powerful, external macro context that now dominates price action. They see the effect, but not the cause.

The Solution: A 4-Dimensional Macro-Lens

The TradFi Pressure Score (TFPS) is the answer. It is an institutional-grade dashboard that aggregates the four most dominant external forces into a single, actionable score:

S&P 500 (SPY): The Pulse of Risk Appetite. A rising S&P signals a "risk-on" environment, fueling capital flows into crypto.

VIX: The Market's Fear Gauge. A rising VIX signals a "risk-off" flight to safety, draining liquidity from crypto.

DXY (US-Dollar Index): The Anchor of Global Liquidity. A strong Dollar (rising DXY) tightens financial conditions, creating powerful headwinds for risk assets like Bitcoin.

US 10Y Yield: The Opportunity Cost of Capital. Rising yields make risk-free assets more attractive, pulling capital away from non-yielding assets like crypto.

What makes the TFPS truly unique?

1. Dynamic Weighting (The Secret Weapon):

Which macro factor matters most right now? Is it a surging Dollar or a collapsing stock market? The TFPS answers this automatically. It continuously analyzes the correlation of all four components to your chosen asset (e.g., Bitcoin) and adjusts their influence in real-time. The dashboard shows you the exact live weights, ensuring you are always focused on the factor that is currently driving the market.

2. Adaptive Engine:

The forces driving a 15-minute chart are different from those driving a daily chart. The TFPS engine automatically recalibrates its internal lookback periods to your chosen timeframe. This ensures the score is always optimally relevant, whether you are a day trader or a swing trader.

3. Designed for Actionable Insights

The Pressure Line: The indicator's core output. Is its value > 0 (tailwind) or < 0 (headwind)? This provides an instant, unambiguous read on the macro environment for your trade.

The Z-Score (The Contrarian Signal): The background "Stress Cloud" and the discrete dots provide early warnings of extreme macro greed or fear. Readings above +2 or below -2 have historically pinpointed moments of market exhaustion that often precede major trend reversals.

Lead/Lag Status: Gain a critical edge by knowing who is in the driver's seat. The dashboard tells you if TradFi is leading the price action or if crypto is moving independently, allowing you to validate your trade thesis against the dominant market force.

This is a public indicator with protected source code

Access is now available for traders who understand the new market reality at the intersection of crypto and traditional finance.

You are among the first to leverage what is a new standard for macro analysis in crypto trading. Your feedback is highly valued as I continue to refine this tool.

Follow for updates and trade with the full context!

TFPS - TradFi-Pressure-Score (Adaptive)The data-driven answer to an irreversible market reality.

This indicator quantifies the combined pressure from the S&P 500, VIX, DXY, and US10Y, whose correlation to crypto has reached peak values of 0.87. Your decisive macro edge, in real-time.

This indicator is built on a fundamental analysis of market data from the last five years. The analysis proves an irreversible transformation: The crypto market has evolved into a high-beta risk asset, its fate inextricably linked to Traditional Finance (TradFi).

The empirical data is clear:

Bitcoin increasingly behaves like a leveraged version of the S&P 500.

The correlation to stock indices, with peak values of up to 0.87, is statistically highly significant.

The "digital gold" safe-haven narrative is refuted by the data; the correlation to gold (0.04) is virtually non-existent and statistically insignificant.

This means: Standard indicators like RSI or MACD are insufficient for today's market conditions. They only see price, ignoring the powerful external context that now dominates price action.

The TradFi Pressure Score (TFPS) is the answer to this data-driven reality. It's your institutional-grade macro dashboard, aggregating the four most dominant external forces into a single, actionable score:

S&P 500 (SPY): The pulse of global risk appetite. A rising S&P signals a "risk-on" environment, fueling capital flows into crypto.

VIX: The market's "Fear Gauge". A rising VIX signals a "risk-off" flight to safety, draining liquidity from crypto.

DXY (US-Dollar Index): The counter-pole to risk assets. A strong Dollar (rising DXY) tightens global liquidity, creating significant headwinds for Bitcoin.

US 10Y Yield: The opportunity cost of capital. Rising yields make risk-free assets more attractive, pulling capital away from non-yielding assets like crypto.

What makes TFPS truly unique?

Dynamic Weighting (its secret weapon): Which factor matters most today? The DXY or the VIX? TFPS continuously analyzes the correlation of all four factors to your chosen asset (e.g., Bitcoin) and automatically adjusts their weight in real-time. This ensures you're always focused on what's currently driving the market.

Adaptive Engine : What drives a 15-minute chart is different from a daily chart. The TFPS engine automatically adapts its lookback periods and calculations to your chosen timeframe for optimal relevance.

Clear, Actionable Signals Designed for Traders:

Pressure Line (>0 or <0): Instantly see if the world's largest financial forces are providing a tailwind or a headwind for your trade.

Z-Score (Extreme Readings) : Get early warnings of extreme macro "Greed" or "Fear". Readings above +2 or below -2 have historically pinpointed moments of market exhaustion that often precede major trend reversals.

Regime Change : A fundamental shift in the nature of TradFi pressure is visualized with a clear signal, providing unambiguous macro insights.

Lead/Lag Status : Gain a critical edge by knowing who's in the driver's seat. The dashboard tells you if TradFi is LEADING the price action or if crypto is moving independently, allowing you to focus on the right information source.

This is a private beta. I am granting exclusive access to a limited number of traders who understand this new market reality. In exchange for your valuable feedback, you will be among the first to leverage what I believe is the new standard for macro analysis in crypto trading.

Request access to trade with the full context.

Assets Correlation AnalyzerAssets Correlation Analyzer

---------------------------------------------

What is it?

The Assets Correlation Analyzer is a technical indicator that measures and visualizes the statistical relationship between any two financial assets (a 'Base Asset' vs. a 'Comparison Asset', example Gold vs. SPY or Nasdaq vs. Bitcoin). The indicator calculates dynamic correlation tracking using statistical methods, confidence intervals, and category-wide analysis capabilities.

---------------------------------------------

Why was it built? / Potential Benefits

This indicator was developed to help analyze inter-asset relationships in portfolio management and trading strategies. The indicator can be used for:

Risk Assessment: Identify when assets begin moving together

Diversification Analysis: Monitor portfolio component relationships

Pairs Trading: Identify when correlated assets diverge

Market Analysis: Recognize shifts in market conditions through correlation patterns

Asset Analysis: Support decision-making based on correlation dynamics

Hedging Analysis: Identify relationships between different instruments

---------------------------------------------

How it Works

The indicator employs established statistical methods to calculate rolling correlations between two selected assets:

Data Collection: Retrieves price data for both selected assets using TradingView's security function

Returns Calculation: Computes logarithmic or simple returns based on user preference

Outlier Filtering: Optionally removes extreme price movements (beyond 2.5 standard deviations) to improve accuracy

Correlation Computation: Calculates either Pearson or Spearman rank correlation over the specified period

Signal Generation: Applies smoothing and generates a signal line (EMA) for momentum detection

Confidence Assessment: Evaluates data quality and provides confidence metrics

---------------------------------------------

How to Read the Oscillator

Main Correlation Line

Values Range: -1.0 to +1.0

+1.0: Perfect positive correlation (assets move identically)

+0.7 to +0.99: Strong positive correlation

+0.3 to +0.69: Moderate positive correlation

-0.3 to +0.29: Weak/No significant correlation

-0.69 to -0.31: Moderate negative correlation

-0.99 to -0.7: Strong negative correlation

-1.0: Perfect negative correlation (assets move oppositely)

Color Coding System

Green shades: Positive correlation levels, with brighter green indicating stronger positive correlation

Red shades: Negative correlation levels, with brighter red indicating stronger negative correlation

Gray: Insufficient data or transitional periods

The color intensity reflects both correlation strength and momentum relative to the signal line.

Signal Line (Gray)

The EMA-based signal line helps identify momentum changes:

Correlation above signal: Positive momentum in correlation

Correlation below signal: Negative momentum in correlation

Crossovers: Potential turning points in the relationship

Background Fills

Gradient fills provide a quick visual assessment of correlation strength, with intensity indicating the degree of correlation.

---------------------------------------------

Correlation Calculation Methods and Options

Calculation Methods

Spearman Rank Correlation (Default)

Uses ranked values rather than raw prices

Less sensitive to outliers and non-linear relationships

Suitable for volatile or non-normally distributed assets

Pearson Correlation (Traditional)

Standard linear correlation method

More sensitive to outliers

Suitable for assets with normal distribution patterns

---------------------------------------------

Customization Options

Correlation Period (7-500 bars): Determines the lookback window for calculation

Signal Line Period (1-200 bars): Controls the smoothing of the signal line

Outlier Removal: Automatically filters extreme price movements

Return Type: Choose between logarithmic (recommended) or simple returns

Smoothing Period: Reduces noise in correlation readings

---------------------------------------------

Asset Categories

The indicator includes 80+ pre-configured assets across multiple categories:

Metals: Gold, Silver, Copper, Platinum, Palladium, Nickel, Zinc, Aluminum

Energy: WTI/Brent Crude, Natural Gas, Uranium

Agriculture: Corn, Soybeans, Wheat, Coffee

ETFs: Major indices, sector, geographic, and specialty ETFs

Bonds: Government and corporate bond instruments

Financial: Currency pairs, treasury yields, volatility indices

Cryptocurrencies: Major digital assets and market cap indices

Real Estate: REITs and real estate focused instruments

---------------------------------------------

For Whom This Indicator Is Designed

Intended Users

Portfolio Managers: Asset allocation and risk assessment

Quantitative Traders: Correlation-based strategy development

Risk Analysts: Correlation monitoring and analysis

Institutional Investors: Diversification analysis

Active Traders: Pairs trading and arbitrage analysis

Skill Level

Intermediate to Advanced: Requires understanding of correlation concepts and statistical interpretation

Experience with Statistics: Users should be familiar with correlation analysis concepts

---------------------------------------------

Information Tables

Main Analysis Table

Displays current correlation value, data confidence percentage, and selected asset information.

Category Correlation Table

Shows correlation strength between the selected 'Base Asset' (in the chart, Gold) and all assets in the comparison asset's category.

---------------------------------------------

Alert Conditions

Four built-in alert types:

Strong Stable Positive Correlation: Triggers when correlation exceeds +0.8 with low volatility

Strong Stable Negative Correlation: Triggers when correlation falls below -0.8 with low volatility

Bullish Correlation Momentum: Signals when correlation crosses above the signal line

Bearish Correlation Momentum: Signals when correlation crosses below the signal line

---------------------------------------------

Usage Notes

Longer periods (30-50 bars) provide more stable analysis

Shorter periods (10-20 bars) provide more responsive signals

Monitor confidence levels - correlations with <75% confidence should be interpreted cautiously

Correlations tend to increase during market stress periods

Should be used in conjunction with other analysis tools

---------------------------------------------

Important Disclaimer

This indicator is for educational and informational purposes only. It should not be considered as financial advice or a recommendation to buy, sell, or hold any financial instrument. Past correlation patterns do not guarantee future relationships between assets. Users should conduct their own research and consider consulting with a qualified financial advisor before making investment decisions. Trading and investing involve substantial risk of loss, and correlation analysis cannot eliminate these risks. The accuracy of correlation calculations depends on data quality and market conditions, which can change rapidly.

IV PercentileIV Percentile Indicator - Brief Description

What It Does

The IV Percentile Indicator measures where current implied volatility ranks compared to the past year, showing what percentage of time volatility was lower than today's level.

How It Works

Data Collection:

Tracks implied volatility (or historical volatility as proxy) for each trading day

Stores the last 252 days (1 year) of volatility readings

Uses VIX data for SPY/SPX, historical volatility for other stocks

Calculation:

IV Percentile = (Days with IV below current level) ÷ (Total days) × 100

Example: If IV Percentile = 75%, it means current volatility is higher than 75% of the past year's readings.

Visual Output

Main Display:

Blue line showing percentile (0-100%)

Reference lines at key levels (20%, 30%, 50%, 70%, 80%)

Color-coded backgrounds for quick identification

Info table with current readings

Key Levels:

80%+ (Red): Very high IV → Sell premium

70-79% (Orange): High IV → Consider selling

30-20% (Green): Low IV → Consider buying

<20% (Bright Green): Very low IV → Buy premium

Trading Application

When IV Percentile is HIGH (70%+):

Options are expensive relative to recent history

Good time to sell premium (iron condors, credit spreads)

Expect volatility to decrease toward normal levels

When IV Percentile is LOW (30%-):

Options are cheap relative to recent history

Good time to buy premium (straddles, long options)

Expect volatility to increase from compressed levels

Core Logic

The indicator helps answer: "Is this a good time to buy or sell options based on how expensive/cheap they are compared to recent history?" It removes the guesswork from volatility timing by providing historical context for current option prices.

Reversal Signal avec TICK + RSIThis indicator is a potential reversal indicator for SCALPING, don't use it for swing. It's base on TICK and on an overbrought/oversold condition of the RSI. You can play with the setting, typicaly I like my TICK to be over reacting an 800/-800 and my rsi over 20 and 80, but it give not enough signal. So I set the TICK signal at 651/-651 and the RSI at 25/75. This indicator is made for SP500 and Nasdaq, so SPY/QQQ/SPX/ES/NQ should work well. It's the first version of it, so maybe I'll add so more data to it to increase signal and lower false one. For now I've test it on live market yet(26/7/25).

The RSI is Fast(5 period), I like to use it on the 1 or 5 min chart.

Please not that it only work during 9h30am to 4pm EST.(Because of the TICK)

Feel free to try and even comment. Don't be harsh on me, it's my first try!

(Sorry for my 'english' it's not my first language)

FAUCON

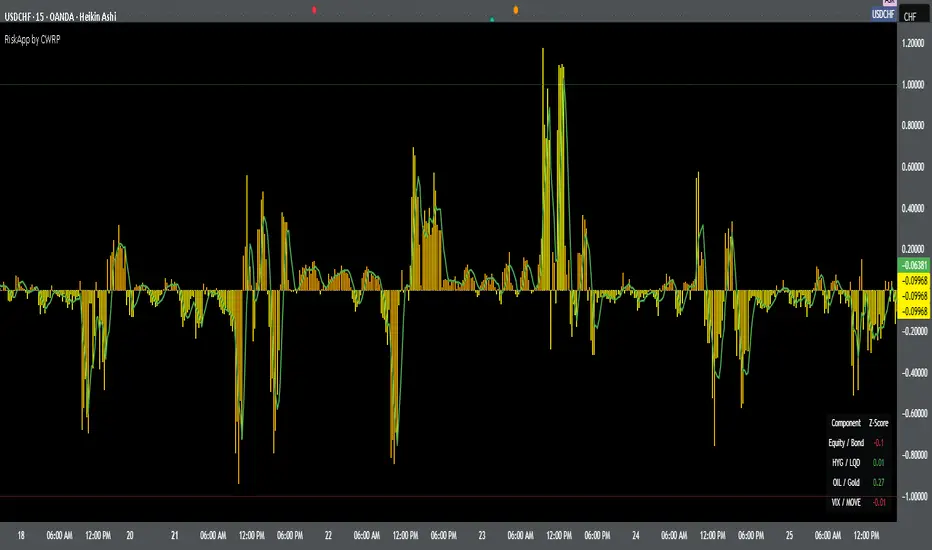

Cross-Asset Risk Appetite IndexCross-Asset Risk Appetite Index (RiskApp) by CWRP combines multiple asset classes into a single risk sentiment signal to help traders and investors detect when the market is in a risk-on or risk-off regime.

It calculates a composite Z-score index based on relative performance between:

SPY / IEF: Equities vs Bonds

HYG / LQD: High Yield vs Investment Grade Credit

CL / GC: Oil vs Gold

VIX / MOVE: Equity vs Bond Market Volatility (inverted)

Each component reflects capital flows toward riskier or safer assets, with dynamic weighting (Equity/Bond: 30%, Credit: 25%, Commodities: 25%, Volatility: 20%) and smoothing applied for a cleaner signal.

How to Read:

Highlighting

Yellow = Risk-On sentiment (market favors risk assets)

Orange = Risk-Off sentiment (flight to safety)

Black Background = Neutral design for emotional detachment

Table

Equity/Bond Z-Score:

Positive (> +1) --> Stocks outperforming bonds --> Risk-On

Negative (< -1) --> Bonds outperforming stocks --> Risk-Off

Credit Spread Z-Score (HYG/LQD):

Positive --> High yield outperforming --> Investors seeking yield

Negative --> Flight to quality --> Credit concerns

Oil/Gold Z-Score:

Positive --> Oil outperforming --> Economic optimism

Negative --> Gold outperforming --> Defensive positioning

Volatility Spread (VIX/MOVE):

Positive --> Equity vol falling relative to bond vol --> Risk stabilizing

Negative --> Equity vol rising --> Caution / Risk-Off

Composite Index:

> +1 --> Strong Risk Appetite

< -1 --> Strong Risk Aversion

Between -1 and +1 --> Neutral regime

Thank you for using the Cross-Asset Risk Appetite Index by CWRP!

I'm open to all critiques and discussion around macro-finance and hope this model adds clarity to your decision-making.

Cross-Correlation Lead/Lag AnalyzerCross-Correlation Lead/Lag Analyzer (XCorr)

Discover which instrument moves first with advanced cross-correlation analysis.

This indicator analyzes the lead/lag relationship between any two financial instruments using rolling cross-correlation at multiple time offsets. Perfect for pairs trading, market timing, and understanding inter-market relationships.

Key Features:

Universal compatibility - Works with any two symbols (stocks, futures, forex, crypto, commodities)

Multi-timeframe analysis - Automatically adjusts lag periods based on your chart timeframe

Real-time correlation table - Shows current correlation values for all lag scenarios

Visual lead/lag detection - Color-coded plots make it easy to spot which instrument leads

Smart "Best" indicator - Automatically identifies the strongest relationship

How to Use:

Set your symbols in the indicator settings (default: NQ1! vs RTY1!)

Adjust correlation length (default: 20 periods for smooth but responsive analysis)

Watch the colored lines:

• Red/Orange: Symbol 2 leads Symbol 1 by 1-2 periods

• Blue: Instruments move simultaneously

• Green/Purple: Symbol 1 leads Symbol 2 by 1-2 periods

Check the table for exact correlation values and the "Best" relationship

Interpreting Results:

Correlation > 0.7: Strong positive relationship

Correlation 0.3-0.7: Moderate relationship

Correlation < 0.3: Weak/no relationship

Highest line indicates the optimal timing relationship

Popular Use Cases:

Index Futures : NQ vs ES, RTY vs IWM

Sector Rotation : XLF vs XLK, QQQ vs SPY

Commodities : GC vs SI, CL vs NG

Currency Pairs : EURUSD vs GBPUSD

Crypto : BTC vs ETH correlation analysis

Technical Notes:

Cross-correlation measures linear relationships between two time series at different time lags. This implementation uses Pearson correlation with adjustable periods, calculating correlations from -2 to +2 period offsets to detect leading/lagging behavior.

Perfect for quantitative analysts, pairs traders, and anyone studying inter-market relationships.

🌊 Reinhart-Rogoff Financial Instability Index (RR-FII)Overview

The Reinhart-Rogoff Financial Instability Index (RR-FII) is a multi-factor indicator that consolidates historical crisis patterns into a single risk score ranging from 0 to 100. Drawing from the extensive research in "This Time is Different: Eight Centuries of Financial Crises" by Carmen M. Reinhart and Kenneth S. Rogoff, the RR-FII translates nearly a millennium of crisis data into practical insights for financial markets.

What It Does

The RR-FII acts like a real-time financial weather forecast by tracking four key stress indicators that historically signal the build-up to major financial crises. Unlike traditional indicators based only on price, it takes a broader view, examining the global market's interconnected conditions to provide a holistic assessment of systemic risk.

The Four Crisis Components

- Capital Flow Stress (Default weight: 25%)

- Data analyzed: Volatility (ATR) and price movements of the selected asset.

- Detects abrupt volatility surges or sharp price falls, which often precede debt defaults due to sudden stops in capital inflow.

- Commodity Cycle (Default weight: 20%)

- Data analyzed: US crude oil prices (customizable).

- Watches for significant declines from recent highs, since commodity price troughs often signal looming crises in emerging markets.

- Currency Crisis (Default weight: 30%)

- Data analyzed: US Dollar Index (DXY, customizable).

- Flags if the currency depreciates by more than 15% in a year, aligning with historical criteria for currency crashes linked to defaults.

- Banking Sector Health (Default weight: 25%)

- Data analyzed: Performance of financial sector ETFs (e.g., XLF) relative to broad market benchmarks (SPY).

- Monitors for underperformance in the financial sector, a strong indicator of broader financial instability.

Risk Scale Interpretation

- 0-20: Safe – Low systemic risk, normal conditions.

- 20-40: Moderate – Some signs of stress, increased caution advised.

- 40-60: Elevated – Multiple risk factors, consider adjusting positions.

- 60-80: High – Significant probability of crisis, implement strong risk controls.

- 80-100: Critical – Several crisis indicators active, exercise maximum caution.

Visual Features

- The main risk line changes color with increasing risk.

- Background colors show different risk zones for quick reference.

- Option to view individual component scores.

- A real-time status table summarizes all component readings.

- Crisis event markers appear when thresholds are breached.

- Customizable alerts notify users of changing risk levels.

How to Use

- Apply as an overlay for broad risk management at the portfolio level.

- Adjust position sizes inversely to the crisis index score.

- Use high index readings as a warning to increase vigilance or reduce exposure.

- Set up alerts for changes in risk levels.

- Analyze using various timeframes; daily and weekly charts yield the best macro insights.

Customizable Settings

- Change the weighting of each crisis factor.

- Switch commodity, currency, banking sector, and benchmark symbols for customized views or regional focus.

- Adjust thresholds and visual settings to match individual risk preferences.

Academic Foundation

Rooted in rigorous analysis of 66 countries and 800 years of data, the RR-FII uses empirically validated relationships and thresholds to assess systemic risk. The indicator embodies key findings: financial crises often follow established patterns, different types of crises frequently coincide, and clear quantitative signals often precede major events.

Best Practices

- Use RR-FII as part of a comprehensive risk management strategy, not as a standalone trading signal.

- Combine with fundamental analysis for complete market insight.

- Monitor for differences between component readings and the overall index.

- Favor higher timeframes for a broader macro view.

- Adjust component importance to suit specific market interests.

Important Disclaimers

- RR-FII assesses risk using patterns from past crises but does not predict future events.

- Historical performance is not a guarantee of future results.

- Always employ proper risk management.

- Consider this tool as one element in a broader analytical toolkit.

- Even with high risk readings, markets may not react immediately.

Technical Requirements

- Compatible with Pine Script v6, suitable for all timeframes and symbols.

- Pulls data automatically for USOIL, DXY, XLF, and SPY.

- Operates without repainting, using only confirmed data.

The RR-FII condenses centuries of financial crisis knowledge into a modern risk management tool, equipping investors and traders with a deeper understanding of when systemic risks are most pronounced.

Intradayscanner – Institutional Interest (vs. RSP)This indicator measures volatility-adjusted Relative Residual Strength (RRS) of any symbol versus RSP (the Invesco S&P 500® Equal Weight ETF) to surface potential institutional interest overlooked by cap-weighted benchmarks.

Equal-weighted benchmark: Uses RSP instead of SPY, so each S&P 500 component carries equal influence—highlighting broad institutional flows beyond the largest names.

ATR normalization: Computes a “Divergence Index” by dividing RSP’s price move by its ATR(14), then adjusts the symbol’s move by that index and rescales by its own ATR(14). This isolates true outperformance.

Residual focus: RRS represents the portion of a symbol’s move unexplained by broad-market action, making it easier to spot when institutions rotate into specific stocks.

Visualization: Plots RRS as green/red histogram bars and overlays a 14-period EMA for trend smoothing.

Daily GEX Zones & Dashboard by JCThis script plots daily options-driven gamma zones alongside a live sentiment dashboard to help traders visualize dealer positioning, support/resistance clusters, and expected price behavior.

Features:

📅 Date-based GEX Zones: Automatically draws GEX Resistance, GEX Support, Max Pain Zone, and Zero Gamma Line for a specific trading day.

📊 Gamma Flow Dashboard: Displays real-time GEX, DEX, Vanna, and Charm flows using intuitive dropdowns (Negative, Neutral, Positive) — no manual number typing.

🔢 Combo ID Calculation: Combines your gamma flow selections into a single Combo ID, quantifying net positioning pressure.

🎯 Automatic Bias Classification: Instantly highlights whether the day’s gamma structure is likely Pinned/Stable, Unpinned/Wild, Choppy, or Trap/Expansion — color-coded for quick reading.

📈 Zero Gamma Lines: Plots two critical levels where gamma flips from long to short, providing valuable confluence for intraday support/resistance.

How to Use:

1️⃣ Pick your target date (e.g., current day) to activate the GEX boxes.

2️⃣ Enter the day’s Resistance Wall, Support Wall, Max Pain, and Zero Gamma levels from your option chain analysis.

3️⃣ Use the radio-style dropdowns to select sentiment for GEX, DEX, Vanna, and Charm based on your interpretation of open interest, hedging, dealer flow, and market structure.

4️⃣ The dashboard will auto-calculate your Combo ID and bias class.

Designed for:

SPX, SPY, QQQ, NVDA, or any high-liquidity underlying with active options flow.

Active day traders, gamma scalpers, and market makers tracking dealer positioning.

Tip:

Combine with price action levels, VWAP, and intraday structure for high probability trade zones.