Volatility/Volume ImpactWe often hear statements such as follow the big volume to project possible price movements. Or low volatility is good for trend. How much of it is statistically right for different markets. I wrote this small script to study the impact of Volatility and Volume on price movements.

Concept is as below:

Compare volume with a reference median value. You can also use moving average or other types for this comparison.

If volume is higher than median, increment positive value impact with change in close price. If volume is less than median, then increment negative value impact with change in close price.

With this we derive pvd and nvd which are measure of price change when volume is higher and lower respectively. pvd measures the price change when volume is higher than median whereas nvd measures price change when volume is lower than median.

Calculate correlation of pvd and nvd with close price to see what is impacting the price by higher extent.

Colors are applied to plots which have higher correlation to price movement. For example, if pvd has higher correlation to price movement, then pvd is coloured green whereas nvd is coloured silver. Similarly if nvd has higher correlation to price then nvd is coloured in red whereas pvd is coloured in silver.

Similar calculation also applied for volatility.

With this, you can observe how price change is correlated to high/low volume and volatility.

Let us see some examples on different markets.

Example 1: AMEX:SPY

From the chart snapshot below, it looks evident that SPY always thrive when there is low volatility and LOW VOLUME!!

Example 2: NASDAQ:TSLA

The picture will be different if you look at individual stocks. For Tesla, the price movement is more correlated to high volume (unlike SPY where low volume days define the trend)

Example 3: KUCOIN:BTCUSDT

Unlike stocks and indices, high volatility defined the trend for BTC for long time. It thrived when volatility is more. We can see that high volume is still major influencer in BTC price movements.

Settings are very simple and self explanatory.

Hint: You can also move the indicator to chart overlay for better visualisation of comparison with close price.

Cari dalam skrip untuk "spy"

Linear Regression Relative Strength[image/x/iZvwDWEY/

Relative Strength indicator comparing the current symbol to SPY (or any other benchmark). It may help to pick the right assets to complement the portfolio build around core ETFs such as SPY.

The general idea is to show if the current symbol outperforms or underperforms the benchmark (SPY by default) when bought some certain time ago. Relative performance is displayed as percent and is calculated for three different time ranges - short (1 mo by default), mid (1 quarter), and long (half a year). To smooth the volatility, the script uses linear regression to estimate the trend and takes the start and the end points of the linear regression line to compute the relative strength.

It is important to remember that the script shows the gain relative to SPY (or other selected benchmark), not the asset's gain. Therefore, it may indicate that the asset is profitable, but it still may lose value if SPY is in downtrend.

Therefore, it is crucial to check other indicators before making a decision. In the example above, standard linear regression for one quarter is used to indicate the direction of the trend.

Drawdown RangeHello death eaters, presenting a unique script which can be used for fundamental analysis or mean reversion based trades.

Process of deriving this table is as below:

Find out ATH for given day

Calculate the drawdown from ATH for the day and drawdown percentage

Based on the drawdown percentage, increment the count of basket which is based on input iNumber of ranges . For example, if number of ranges is 5, then there will be 5 baskets. First basket will fit drawdown percentage 0-20% and each subsequent ones will accommodate next 20% range.

Repeat the process from start to last bar. Once done, table will plot how much percentage of days belong to which basket.

For example, from the below chart of NASDAQ:AAPL

We can deduce following,

Historically stock has traded within 1% drawdown from ATH for 6.59% of time. This is the max amount of time stock has stayed in specific range of drawdown from ATH.

Stock has traded at the drawdown range of 82-83% from ATH for 0.17% of time. This is the least amount of time the stock has stayed in specific range of drawdown from ATH.

At present, stock is trading 2-3% below ATH and this has happened for about 2.46% of total days in trade

Maximum drawdown the stock has suffered is 83%

Lets take another example of NASDAQ:TSLA

Stock is trading at 21-22% below ATH. But, historically the max drawdown range where stock has traded is within 0-1%. Now, if we make this range to show 20 divisions instead of 100, it will look something like this:

Table suggests that stock is trading about 20-25% below ATH - which is right. But, table also suggests that stock has spent most number of days within this drawdown range when we divide it by 20 baskets instad of 100. I would probably wait for price to break out of this range before going long or short. At present, it seems a stage ranging stage. I might think about selling PUTs or covered CALLs outside this range.

Similarly, if you look at AMEX:SPY , 36% of the time, price has stayed within 5% from ATH - makes it a compelling bull case!!

NYSE:BABA is trading at 50-55% below ATH - which is the most it has retraced so far. In general, it is used to be within 15-20% from ATH

NOW, Bit of explanation on input options.

Number of Ranges : Says how many baskets the drawdown map needs to be divided into.

Reference : You can take ATH as reference or chose a time window between which the highest need to be considered for drawdown. This can be useful for megacaps which has gone beyond initial phase of uncertainity. There is no point looking at 80% drawdown AAPL had during 1990s. More approriate to look at it post 2000s where it started making higher impact and growth.

Cumulative Percentage : When this is unchecked, percentage division shows 0-nth percentage instad of percentage ranges. For example this is how it looks on SPY:

We can see that SPY has remained within 6% from ATH for more than 50% of the time.

Hope this is helpful. Happy trading :)

PS: this can be used in conjunction with Drawdown-Price-vs-Fundamentals to pick value stocks at discounted price while also keeping an eye on range tendencies of it.

Thanks to @mattX5 for the ideas and discussion today :)

Altered True Strength Indicator (TSI) Reupload-

Altered TSI provides a slightly more volatile signal that demonstrates extremities in price action with greater success than standard TSI. In addition, I added bull/bear cross indicators (green/red) to make it easier to notice the crosses to save time when the market is moving fast (I couldn't find a regular TSI script with this addition). Finally, the signal also has overextension parameters (red and green lines)

I think this is best used on Intraday time frames as the signals respond to volatility very well and using Heikin Ashi candles, trend is more visual. In this particular example, I am showing SPY on the 3m time chart (my favorite short time frame) and the signal alone provided many opportunities for trades when using simple divergences and countering overextension direction when short term (blue) signal crosses either

In the first example (purple lines), SPY ramps but it was a dull signal given the signal strength flatlining- we would be looking for a short entry. When the signal fires, it provides a clean $1.50 move down in spy.

In the second example (orange), the blue signal provides a nice V shape (rebound signal) in which we are looking for a long entry. 390.50 is a strong SPY support in confluence with 2nd std dev VWAP extension, but disregarding that bull signal fires resulting in a 2 dollar move upwards. Exit is provided when blue line crosses green overextension.

In the third example (white), we are searching for a short entry at 392.5 resistance in confluence with divergently higher highs. Bear cross signal when fired and a significant cross is visible provides a $2.50 move to the downside with a potential exit provided when blue line crosses red overextension line in confluence with previous LOD area.

In the fourth example (green), we watch as the blue line provides a V pattern, we are searching for a long entry. If you didn't take a riskier long at 2nd std dev VWAP overextension with V recovery on blue line at red overextension for a ride to vwap, then you are looking for a secondary entry long as you wouldn't take the trade at resistance (vwap). Bullishly divergent lows provide this entry and the signal does not bear cross at all (but looking for significant crosses is more important even if the signal were to make a minor bear cross). Bullishly divergent double bottom provides a long entry to end of day with a nice clean signal for a $5.00 move until eod or when signal crosses overextension range.

Ideally, close to the money options or SPY/SPXS/SPXL are best used in the intraday time frame.

Again, this is not a standalone indicator but it's best used in conjunction with other indicators/trading strategies

Any questions feel free to comment

Candlestick RSThis is a candlestick charted Relative Strength indicator. It compares the chosen stock's progress compared to that of the SPY ETF ... ( SPY is used so it should hopefully update intraday). I use this indicator to see which stocks are outperforming the market.

Input Variable Descriptions:

Ratio: this variable is a float (0 to 1) that is basically how close the Candlestick RS is to the actual price action of the chart. (1.0 being right on top of it, 0.0 being as far away as possible from it)

Ballpark SPY price: this variable has to be constant, and due to the way pinescript works, you have to manually put in a ballpark of what SPY is at.

Neither of these variables influences the actual data of the indicator, but rather how it is shown on screen. It's difficult to describe, so I recommend you messing around with the variables and see what changes.

Hope this helps, I find this useful, so I figured I'd publish this... This is my first pine script so forgive me for any errors, just want to help :)

Multi-Timeframe Inside Bar Breakout (4-Symbol Simultaneous)Multi-Timeframe Inside Bar Breakout (4-Symbol Simultaneous)

Overview

Monitors 4 symbols across 4 timeframes simultaneously, displaying labeled alerts when all 4 symbols break out from inside bar compression on any tracked timeframe. See 15-minute, 30-minute, 60-minute, and daily breakouts all on one chart — complete multi-timeframe compression analysis.

When all 4 symbols compress into inside bars and then ALL break the same direction, you get clear directional confirmation across different timeframes. Perfect for Rob Smith's "The Strat" methodology and traders who use multi-timeframe analysis for entry confirmation.

🎯 Why This Matters

Multi-timeframe breakout confluence = stronger signals.

When SPY, QQQ, IWM, and DIA simultaneously:

✅ Compress into inside bars (bar )

✅ ALL break same direction (bar )

✅ Across multiple timeframes

You get layered confirmation — not just one timeframe saying "go," but multiple timeframes agreeing on direction.

Example: 15m breakout + 60m breakout + Daily breakout = alignment across timeframes.

✅ Key Features

✅ 4 Timeframes Tracked — Monitor 15m, 30m, 60m, Daily (fully customizable)

✅ 4 Symbols Per Timeframe — All must break together for signal

✅ Staggered Labels — Each timeframe displays at different distance (no overlap)

✅ Adaptive Positioning — Works on futures, stocks, forex, crypto

✅ Customizable Colors — Bullish/bearish colors with opacity control

✅ Alert-Ready — 8 alert conditions (bull/bear per timeframe)

✅ Works on Any Chart — See higher timeframe signals on lower timeframe charts

📊 How It Works

Inside Bar Check (Bar ):

All 4 symbols had inside bars (high < prior high AND low > prior low)

Breakout Check (Bar ):

Bullish: All 4 close > prior high

Bearish: All 4 close < prior low

Label Display:

📈IBSB 15 = Bullish breakout on 15-minute timeframe

📉IBSB D = Bearish breakout on daily timeframe

Each timeframe operates independently — you might see multiple timeframe labels on the same bar when breakouts align.

⚙️ Settings Guide

Symbols (Default: SPY, QQQ, IWM, DIA)

Customize to any 4 symbols

Popular: ES/NQ/YM/RTY (futures), XLF/XLK/XLE/XLV (sectors)

Timeframes (Default: 15, 30, 60, D)

Set any 4 timeframes to monitor

Examples: 5/15/60/240 (intraday stack), 60/D/W/M (swing stack)

Display Options:

Bullish/Bearish colors + opacity control

Label distance (% of bar range)

Stagger spacing (prevents overlap)

Max labels per timeframe (default: 25)

Debug Mode:

Shows which symbols are inside/breaking per timeframe

Useful for troubleshooting

🔔 Setting Up Alerts

Create alerts for any combination:

"IBSB Bull - TF1" (first timeframe bullish)

"IBSB Bear - TF4" (fourth timeframe bearish)

Set to "Once Per Bar Close" for confirmed signals

💡 Example Trading Approach

Note: Educational example, not trading advice.

Watch for compression across symbols on higher timeframes

IBSB label appears → all 4 broke same direction

Multiple timeframe labels = stronger confluence

Enter with your strategy using proper risk management

Example: Daily IBSB bullish + 60m IBSB bullish = aligned timeframes for potential long entry.

🎯 Why Multi-Timeframe Matters

Single timeframe breakout = one piece of data.

Multi-timeframe breakout = confirmation across time horizons.

When 15m, 60m, and Daily all show simultaneous 4-symbol breakouts → market structure aligning across timeframes.

🔧 Technical Details

✅ PineScript v6 (latest)

✅ Adaptive label positioning (scales with price)

✅ Smart staggering (prevents label overlap)

✅ Label management (max 500 total across timeframes)

✅ NA-safe logic (handles missing data)

✅ Works across all chart timeframes

⚠️ Important Disclaimers

Not financial advice: Educational and informational purposes only

No performance guarantees: Past breakouts don't predict future results

Risk management essential: Always use proper position sizing

Test before trading: Backtest and paper trade first

⚡ Quick Start

Add indicator to chart

Set symbols (default: SPY/QQQ/IWM/DIA)

Set 4 timeframes (default: 15/30/60/D)

Customize colors if desired

Create alerts (optional)

Watch for 📈IBSB or 📉IBSB labels with timeframe designation

📞 Support

Follow for updates and new indicators.

Questions? Leave a comment below — I respond to all feedback.

💬 Final Thoughts

Multi-timeframe compression breakouts with 4-symbol confirmation. Instead of monitoring dozens of charts manually, see all your timeframe breakouts in one place. When multiple timeframes align with simultaneous 4-symbol breakouts, you get clearer directional signals.

Use as one component of your analysis, combine with your risk management, and always trade with discipline.

Happy trading! 📈

Free and open-source for personal use. If you find this valuable:

👍 Like | 📝 Review | 🔔 Follow

Quant Stats: Alpha, Beta, R2Quant Stats Indicator for TradingView: Alpha, Beta, and R-Squared

Overview

The Quant Stats Indicator is a professional-grade Pine Script tool designed for quantitative traders and hedge fund managers who need real-time analysis of stock or ETF performance against a benchmark using three fundamental CAPM metrics: Beta, R-Squared, and Alpha.

This indicator calculates three critical measurements that answer every quant trader's core questions: How volatile is this asset relative to my benchmark? How much of its performance is independent of the benchmark? And how much excess return am I achieving after adjusting for risk?

The Three Metrics Explained

Beta (β) measures systematic risk and volatility relative to your chosen benchmark. A Beta of 1.0 means the asset moves in lockstep with the benchmark. A Beta above 1.0 indicates higher volatility—if the market rises 10%, a Beta-1.5 asset should rise 15%. Conversely, a Beta below 1.0 indicates lower volatility, making it a defensive position. This metric helps you understand how much market exposure you're truly taking.

R-Squared (R²) quantifies what percentage of an asset's price movement can be explained by benchmark movements. An R² of 0.95 means 95% of the asset's moves are driven by the benchmark, leaving only 5% unexplained. Conversely, an R² of 0.2 means 80% of the asset's movement is independent of the benchmark. This distinction is crucial: high R² is desirable for passive index tracking but indicates weak alpha potential; low R² reveals genuine independent returns, exactly what active managers seek.

Alpha (α) reveals Jensen's Alpha—the excess risk-adjusted return after accounting for the return you "should" earn given your Beta exposure. A positive Alpha of 15% means you're outperforming the market by 15 percentage points after adjusting for systematic risk. This is the holy grail of stock picking: pure skill-driven excess return, not luck from market exposure.

How to Use It

Configure four key inputs: your benchmark ticker (default SPY, but use QQQ for tech-focused analysis or sector-specific ETFs), the lookback period in days, and the risk-free rate reflecting current Treasury yields. The lookback period is critical. Use 20 days for tactical trading to capture short-term sentiment and beta spikes; use 63 days for swing trading and quarterly rebalancing; use 252 days for structural asset allocation decisions.

The indicator plots Beta as a blue line, R-Squared as a red shaded background area, and Alpha as a green line in a sub-panel. Reference gridlines appear at Beta = 1.0 (market-equivalent volatility) and Alpha = 0.0 (breakeven performance), making interpretation intuitive.

Practical Applications

For swing traders monitoring a 63-day window, seek positions with low Beta (below 0.8) and positive Alpha—these are defensive winners. Avoid high Beta (above 1.2) with low R² unless you specifically want high-volatility speculation. Long/short hedge funds should use a 20-day lookback to detect regime changes: sudden Beta spikes often precede correlation breakdowns, while R² collapses signal rising idiosyncratic risk requiring immediate rebalancing.

For ETF portfolio construction, high R² (above 0.95) indicates index-tracking that doesn't justify active management fees. Low R² (below 0.3) combined with positive Alpha reveals genuine active management skill. The sweet spot is moderate Beta (0.5–0.8) with low R² and positive Alpha—a true diversifier that reduces portfolio volatility while generating independent returns.

Critical Interpretation Rules

A common mistake is assuming high R² is always desirable. It isn't. Passive index funds naturally have high R²; active managers should target low R² with high Alpha. Similarly, don't assume Alpha above 10% is sustainable—short-term Alpha (20–100 days) is inherently volatile and often represents temporary mispricings rather than repeatable skill. Always pair Beta analysis with R² interpretation; Beta alone ignores idiosyncratic risk, liquidity constraints, and tail risk.

Configuration Recommendations

Conservative investors should use SPY as benchmark with a 252-day lookback, targeting Alpha above 3% and Beta below 0.8. Growth-oriented portfolios might use QQQ with a 63-day lookback, targeting 8–12% Alpha and tolerating Beta up to 1.3. Hedge funds pursuing market-neutral strategies should use SPY with a 20-day lookback, set the risk-free rate to 2% (anticipating rate cuts), and target 15%+ Alpha while maintaining Beta below 0.3.

Important Limitations

The indicator is backward-looking; historical statistical relationships may not persist. Shorter lookback periods are noisier but more responsive; longer periods smooth noise but lag regime changes. Choosing the wrong benchmark completely invalidates analysis. Finally, the indicator doesn't account for tail risk or extreme market events where correlations spike unpredictably and Beta becomes unreliable.

Use this tool to separate signal from noise and identify true alpha generators. Apply it consistently, validate results against official fund factsheets, and monitor for 2–4 weeks before making significant portfolio decisions.

Market Regime Guard PRO Institutional No-Trade ZonesThis dashboard automatically blocks trading on structurally dangerous market days caused by volatility compression, inside-day accumulation, rising VIX liquidation risk, EMA breakdowns, and thin liquidity traps.

Most traders lose not because their entries are bad — but because they trade on structurally dangerous market days.

This dashboard automatically blocks trading on contraction, liquidation-risk, inside-day, and volatility-trap days.

Then list what it detects:

• Inside Days (institutional absorption)

• NR7 contraction traps

• ATR volatility compression

• EMA structure breakdown

• Rising VIX liquidation risk

• News & holiday liquidity traps

Promise:

Only trade when the market structure is favorable.

Use this as your universal go/no-go trading permission system.

If it’s GREEN → Trade.

If it’s RED → Stand Aside or Be careful

Works on:

SPY, QQQ, TQQQ, NVDA, PLTR, TSLA, BTC, ES, NQ, Forex & Crypto.

🧭 How to Use the Market Regime Table

This table is your go / no-go permission system.

Start by checking it on SPY and QQQ — these represent the overall U.S. market and the Nasdaq growth complex.

• If SPY and QQQ are GREEN → market structure is favorable

• If either is RED → stand aside or reduce risk

Once the market is GREEN, you can then apply the same table to individual stocks (NVDA, PLTR, TSLA, AMD, etc.) to confirm that the stock’s structure is also favorable before taking any trades.

Rule of thumb:

Market first. Stock second.

Only trade when both are GREEN.

This one rule alone dramatically improves win rate, drawdown, and consistency.

FULL DESCRIPTION

Most traders don’t lose because their entries are bad —

They lose because they trade on structurally dangerous market days.

On these days:

• Institutions absorb liquidity

• Volatility contracts

• Fake breakouts dominate

• Stop hunts explode

• Real expansion does not occur

This indicator automatically identifies and blocks:

• Inside-day accumulation traps

• NR7 contraction traps

• Falling ATR volatility compression

• EMA structure breakdowns

• Rising VIX liquidation risk

• Thin liquidity / holiday risk

• News-day volatility traps

It gives you a clear desk-style verdict:

Status Meaning

🟢 GREEN Market structure favorable – trade normally

🔴 RED Structural danger – stand aside

This is not an entry system.

This is your permission system.

🛠 HOW TO USE

Add indicator to your chart

Check table in top-right

Trade only on GREEN days

Avoid RED days completely

📈 Personal Note

This regime filter has been instrumental in my own trading journey. After struggling during my first few years in the market, I realized that the biggest losses didn’t come from bad strategies — they came from trading on the wrong days.

Learning to stand aside on structurally dangerous market days and only trade when conditions are favorable dramatically improved my consistency and overall returns.

🧠 Why Market Regime Matters Even More for Day Traders

Most day-trader losses do not come from bad entries.

They come from:

• Choppy inside-day conditions

• Liquidity absorption

• Falling volatility (no follow-through)

• Stop-hunt behavior

• News / thin liquidity traps

Your filter directly blocks every one of these traps.

So for day traders, this tool:

• Prevents revenge trading

• Stops death-by-a-thousand-cuts days

• Filters out random chop days

• Protects capital on slow days

• Preserves psychological capital

📈 Why It Also Improves Swing Trading

For swing traders, this tool:

• Avoids entering during contraction

• Avoids entering before expansions

• Avoids bear-regime traps

• Improves follow-through probability

• Reduces drawdown

• Improves R-multiple expectancy

Which means:

Fewer trades

Higher quality trades

More profit per trade

The Universal Truth

The market does not pay you for activity.

It pays you for selectivity.

This filter improves timing, not tactics.

Your entries can be identical — your results improve simply because you’re trading on the right days.

⚠️ Disclaimer

This indicator is provided for educational and informational purposes only and does not constitute financial, investment, or trading advice.

Trading stocks, options, futures, forex, and cryptocurrencies involves substantial risk and may result in the loss of some or all of your invested capital. Past performance is not indicative of future results.

This tool does not guarantee profits and should be used as a market structure filter and risk-management aid only. Always perform your own analysis, use proper position sizing, and consult a licensed financial professional before making any trading decisions.

You are solely responsible for all trades taken using this indicator.

HSLevelsLibPubLibrary "HSLevelsLibPub"

Centralized levels library for Heatseeker trading system.

Update levels HERE ONCE - all consuming scripts auto-refresh.

getVIXThresholds()

Returns VIX threshold levels for regime determination

Returns: as tuple of floats

getVIXThresholdsCSV()

Returns VIX thresholds as CSV strings

Returns: as tuple of strings

getExpiry()

Returns current options expiry date in YYMMDD format

Returns: string in YYMMDD format (e.g., "260108" for Jan 8, 2026)

getAnchorStrike(symbol)

Returns the anchor strike price for a given symbol

Parameters:

symbol (simple string) : The ticker symbol (SPY, QQQ, SPX, VIX)

Returns: float anchor strike price

getFractalPrices(symbol)

Returns fractal level prices as CSV for a symbol

Parameters:

symbol (simple string) : The ticker symbol (SPY, QQQ, SPX)

Returns: string of comma-separated prices

getFractalLabels(symbol)

Returns fractal level labels as CSV for a symbol

Parameters:

symbol (simple string) : The ticker symbol (SPY, QQQ, SPX)

Returns: string of comma-separated labels

getFractalLevels(symbol)

Returns both fractal prices and labels as CSV tuple

Parameters:

symbol (simple string) : The ticker symbol

Returns: tuple

getAnchorStrikeAuto()

Auto-detect symbol and return appropriate anchor strike

Returns: float anchor strike for current chart symbol

getFractalLevelsAuto()

Auto-detect symbol and return fractal levels

Returns: for current chart symbol

getAllData(symbol)

Get all data for a symbol in one call

Parameters:

symbol (simple string) : The ticker symbol

Returns:

getVersion()

Returns library version and last update timestamp

Returns: string with version info

Mashrab | Momentum X-Ray Stop guessing if a stock is a "Leader" or a "Laggard." The Mashrab Momentum X-Ray is a professional Heads-Up Display (HUD) that tells you the true strength of any stock in seconds.

Designed for serious swing traders and breakout specialists (similar to the styles of Qullamagie, Mark Minervini, and IBD), this tool ignores the noise and focuses on the only things that matter: Relative Strength, Volume Fuel, and Fundamental Health.

🚀 Key Features (What it does)

1. The "Smart" Relative Strength Engine

Most indicators blindly compare every stock to the S&P 500. This dashboard is smarter.

It automatically scans the stock’s Industry (e.g., Semiconductors, Gold Miners, Regional Banks).

It compares the stock’s performance against its specific peers (e.g., NVDA vs. SMH ETF) and the market benchmark (SPY).

Green Signal: The stock is beating both the market and its sector. This is a "True Leader."

2. IBD-Style RS Rating (1-99 Scale)

Get the "Secret Sauce" of institutional screening directly on your chart.

Calculates a weighted performance score: 40% (Last 3 Months) + 20% (6m, 9m, 12m).

The Scale:

90–99 (Lime Green): Elite Super-Stock.

80–89 (Green): Strong Leader / Breakout Candidate.

< 50 (Red): Laggard / Avoid.

3. Momentum "Fuel" Gauge (RVol)

Price moving up is good. Price moving up on massive volume is better.

The RVol (Relative Volume) row lights up Yellow or Purple when volume is 1.5x to 3x higher than normal. This detects "Institutional Buying" footprints.

4. "Blue Sky" Detector

Instantly see how close the price is to its 52-Week High.

Stocks within 5% of their highs (Green) have no "overhead supply" (bag holders) and can run the fastest.

👀 How to Read the Dashboard

Top Table (Tactical Momentum)

RS vs SPY / Sector: Look for DOUBLE GREEN. This means the stock is the "King of the Hill."

RVol: Look for > 1.5x (Yellow). This means big players are entering the trade.

Bottom Table (Strategic Context)

IBD RS Rating: Look for a score of 80 or higher.

ADR (20): Shows the "Average Daily Range" volatility. (e.g., 4.5% means the stock moves ~4.5% a day). Use this to size your position correctly!

Industry: Tells you exactly which ETF is being used for comparison (e.g., "Semiconductors (SMH)").

⚙️ Settings & Customization

Benchmark: Change the default SPY to QQQ (for Tech), IWM (for Small Caps), or BTCUSD (for Crypto) to fit your strategy.

Lookback: Defaults to 26 Bars (Standard Monthly Momentum), but fully adjustable.

Text Size: Make the tables larger or smaller to fit your screen.

"Trade the Leaders, Ignore the Laggards."

Custom Sector Comparison Index (CSCI)Compare any stock against a custom basket of its true peers.

Most traders compare stocks to broad indexes like the S&P 500 (SPY) or the Nasdaq (QQQ). But if you are analyzing a niche sector—like Residential REITs, Gold Miners, or AI Semis—broad indexes are too noisy.

This indicator allows you to build your own Custom Equal-Weight Index made up of up to 12 specific symbols. It then plots the performance of the stock you are currently viewing against that custom index, starting from a specific "Anchor Date" of your choosing.

Why use this?

Standard relative strength tools force you to compare against a single symbol (like SPY). But if you want to know if Centerspace (CSR) is lagging its direct competitors, comparing it to SPY (which contains Tech and Healthcare) is useless. Comparing it to VNQ (which contains Cell Towers and Malls) is also imperfect.

With this tool, you can create a "Pure Residential REIT" index and see exactly how your stock is performing against the group.

Key Features:

Fully Configurable: Input up to 12 different symbols to build your custom index.

Smart Filtering: Automatically ignores blank slots. You can build a basket of 3 stocks or 12 stocks without breaking the math.

Custom Anchor Date: Set the specific start date for the comparison (e.g., YTD, Q3 start, or a specific market event).

Visual Performance Gap: Green shading indicates your stock is outperforming the basket; Red shading indicates underperformance.

Example Use Case: Residential REITs

I developed this to analyze the "Residential REIT" sector. I wanted to see if Invitation Homes (INVH) was trading at a discount due to fundamentals or if the whole sector was down.

I configured the basket with 9 of its closest peers:

NYSE:VRE, NYSE:UDR, NYSE:MAA

NYSE:EQR, NYSE:CSR, NYSE:ESS

NYSE:CPT, NYSE:AVB, NYSE:AMH

The Result: The indicator draws a gray line representing the average return of those 9 "Big Boys." I can then load CSR on the chart and immediately see if it is lagging the pack (a potential value buy) or leading it.

How to Use:

Add the indicator to your chart.

Open Settings (Double-click the line).

Start Date: Set the date you want the "race" to begin (where all returns reset to 0%).

Symbols: Type in the tickers for your custom basket (e.g., NVDA, AMD, INTC). Leave unused slots blank.

Analyze:

Gray Line: The average performance of your basket.

Blue Line: The performance of the current symbol on your chart.

Pro Tip: You can save different "Presets" in the indicator settings for different sectors (e.g., save one preset as "Semis" and another as "Oil Majors") so you don't have to re-type symbols every time.

Alpha Options System# Apex Options Sniper - Advanced Multi-Signal Day Trading System

## 🎯 Overview

**Apex Options Sniper** is a professional-grade, multi-signal trading indicator specifically engineered for high-probability day trading of weekly options. This comprehensive system combines 10+ technical indicators into a sophisticated scoring algorithm that identifies optimal entry points with institutional-level precision.

Perfect for traders of SPY, QQQ, and high-volume stocks, this indicator eliminates guesswork by providing clear BUY CALLS and BUY PUTS signals based on multiple technical confluences.

---

## 🚀 Key Features

### **Multi-Signal Confluence Engine**

- **10+ Technical Indicators** working in harmony

- **Weighted Scoring System** (0-30+ points) for signal strength

- **Real-time Signal Classification**: Strong vs Moderate signals

- **False Signal Reduction** through multi-confirmation requirements

### **Advanced Momentum Analysis**

- ✅ RSI with Divergence Detection (bullish & bearish)

- ✅ Stochastic Oscillator (oversold/overbought + crossovers)

- ✅ MACD with crossover and momentum confirmation

- ✅ Automatic divergence spotting for reversal trades

### **Sophisticated Trend Detection**

- ✅ Triple EMA System (9/21/50) with alignment scoring

- ✅ SuperTrend Indicator with trend flip alerts

- ✅ VWAP for institutional price levels

- ✅ Multi-timeframe trend confirmation

### **Professional Volume Analysis**

- ✅ Volume Spike Detection (vs 20-period average)

- ✅ OBV (On-Balance Volume) with divergence detection

- ✅ Order Flow Analysis (buy vs sell pressure)

- ✅ Relative volume ratio display

### **Advanced Pattern Recognition**

- ✅ Bollinger Band Squeeze detection (volatility expansion)

- ✅ BB breakout signals (major move initiation)

- ✅ Automatic Support & Resistance levels (pivot-based)

- ✅ Price reaction scoring at key levels

### **Built-in Risk Management**

- ✅ ATR-based Stop Loss calculations

- ✅ Customizable Risk:Reward ratios

- ✅ Position sizing recommendations

- ✅ Real-time profit target calculations

### **Comprehensive Visual Dashboard**

- ✅ Live scoring breakdown for all indicators

- ✅ Individual signal strength display

- ✅ Bull vs Bear score comparison

- ✅ Color-coded signal status

- ✅ Risk management metrics

---

## 📊 How It Works

### **Scoring System**

The indicator assigns points based on technical conditions:

| **Category** | **Max Points** | **Conditions** |

|-------------|---------------|----------------|

| Momentum (RSI/Stoch) | 8 | Oversold/overbought + divergences |

| MACD | 4 | Crossovers + momentum direction |

| Trend (EMAs) | 6 | EMA alignment + SuperTrend |

| Volume | 4 | Spikes + OBV divergences |

| Order Flow | 2 | Buy/sell pressure imbalance |

| Bollinger Bands | 2 | Squeeze + breakouts |

| Support/Resistance | 2 | Price at key levels |

| VWAP | 1 | Above/below institutional level |

### **Signal Thresholds**

- **🚀 STRONG CALLS**: Bull score ≥6, Net score ≥4

- **📈 CALLS**: Bull score ≥4, Net score ≥2

- **🔥 STRONG PUTS**: Bear score ≥6, Net score ≤-4

- **📉 PUTS**: Bear score ≥4, Net score ≤-2

### **Multi-Timeframe Filter**

Optional higher timeframe confirmation reduces false signals by ensuring the broader trend supports your trade direction.

---

## 🎮 How to Use

### **Installation**

1. Open TradingView Pine Editor

2. Paste the complete indicator code

3. Click "Add to Chart"

4. Customize settings to your preference

### **Recommended Settings**

**For SPY/QQQ Day Trading:**

- Timeframe: 1-minute or 5-minute

- Strong Signal Threshold: 6

- Moderate Signal Threshold: 4

- Multi-timeframe Confluence: ON

**For Individual Stocks:**

- Timeframe: 5-minute or 15-minute

- Increase SuperTrend multiplier to 3.5-4.0

- Enable all advanced features

**For Scalping:**

- Timeframe: 1-minute

- Use STRONG signals only (6+)

- Tight stop loss (1.0-1.5 ATR multiplier)

### **Best Trading Times**

- **9:30-11:00 AM EST** - Highest volume, strongest signals

- **2:00-4:00 PM EST** - Afternoon momentum plays

- Avoid 11:30 AM-1:30 PM EST (lunch chop)

---

## 📈 Signal Interpretation

### **What You'll See on Chart:**

**Visual Signals:**

- 🟢 **Green Triangle (CALLS)**: Bullish entry point

- 🟢 **Large Green Triangle (STRONG CALLS)**: High-confidence bullish entry

- 🔴 **Red Triangle (PUTS)**: Bearish entry point

- 🔴 **Large Red Triangle (STRONG PUTS)**: High-confidence bearish entry

- 💎 **Small Diamonds**: RSI/OBV divergences (reversal warning)

**Dashboard Information:**

- Individual indicator values and signals

- Real-time score breakdown

- Bull/Bear score totals

- ATR stop loss levels

### **Entry Rules:**

✅ **High Probability Trades (Take These):**

- Strong signal (6+ score)

- 3+ indicators confirming

- Volume spike present

- SuperTrend aligned

- Higher timeframe confirms

⚠️ **Moderate Trades (Smaller Position):**

- Moderate signal (4-5 score)

- 2+ indicators confirming

- Normal volume

- Mixed trend signals

❌ **Avoid These:**

- Conflicting signals (Bull score ≈ Bear score)

- Low volume

- During major news events

- Bollinger squeeze without breakout direction

---

## 🛡️ Risk Management Guide

### **Position Sizing:**

- **Strong Signals (6+)**: 3-5% of portfolio

- **Moderate Signals (4-5)**: 2-3% of portfolio

- **Low Conviction**: 1-2% or skip

### **Stop Loss Strategy:**

- Use ATR-based stops (displayed in dashboard)

- Default: 1.5x ATR from entry

- Weekly options: 30-50% premium loss maximum

- Never hold through stop loss hoping for recovery

### **Profit Targets:**

- **Quick Scalps**: 25-50% gain (15-30 min)

- **Day Trades**: 50-100% gain (same day exit)

- **Swing**: 100-200% gain (1-2 days max for weeklies)

- **Take partial profits** at first target, let rest run

### **Time Decay Management (Weekly Options):**

- Monday-Wednesday: Hold overnight acceptable on strong signals

- Thursday: Close by EOD unless very strong conviction

- Friday: Avoid holding overnight, theta decay accelerates

---

## 🔔 Alert Configuration

### **Recommended Alerts:**

**Essential Alerts:**

1. 🚀 Strong Buy Calls

2. 🔥 Strong Buy Puts

**Advanced Alerts:**

3. 💎 RSI Bullish Divergence

4. ⚠️ RSI Bearish Divergence

5. 🔶 Bollinger Band Squeeze

6. ✅ SuperTrend Bull Flip

7. ❌ SuperTrend Bear Flip

**Alert Setup:**

- Set frequency: "Once Per Bar Close"

- Enable for all devices

- Use webhook for automation (optional)

---

## 💡 Pro Trading Tips

### **Maximize Win Rate:**

1. **Wait for confluence** - Best trades have 3+ indicators aligned

2. **Respect the dashboard** - Check WHY it's signaling (which indicators)

3. **Volume is king** - Signals with volume spikes are significantly more reliable

4. **Use BB Squeeze** - When squeeze + signal = explosive directional move

5. **SuperTrend flips** - Major trend change confirmations, very powerful

6. **Watch for divergences** - Diamond markers = hidden reversal opportunities

### **Common Mistakes to Avoid:**

❌ Trading every signal (be selective)

❌ Ignoring volume (volume confirms everything)

❌ Fighting the higher timeframe trend

❌ Oversizing positions on moderate signals

❌ Holding weekly options too long (theta decay)

❌ Trading during lunch hour (11:30-1:30 EST)

### **Advanced Techniques:**

- **Divergence + Support/Resistance** = Highest probability reversals

- **BB Squeeze + EMA alignment** = Explosive trend continuations

- **SuperTrend flip + Volume spike** = Major trend change entries

- **Multiple timeframe analysis** - Check 5m signal on 1m chart for precision entries

---

## 📊 Indicator Components Explained

### **RSI (Relative Strength Index)**

- Measures momentum and overbought/oversold conditions

- Divergences signal potential reversals before they happen

- Score: 2-3 points for extremes and divergences

### **Stochastic Oscillator**

- Confirms momentum extremes

- Crossovers provide entry timing

- Score: 1-2 points

### **MACD (Moving Average Convergence Divergence)**

- Trend following momentum indicator

- Crossovers signal momentum shifts

- Score: 1-3 points based on signal strength

### **EMA System (9/21/50)**

- Dynamic support and resistance

- Alignment shows trend strength

- Price position relative to EMAs scores 1-2 points

### **SuperTrend**

- Volatility-based trend indicator

- Reduces whipsaws in choppy conditions

- Trend flips are major signals (2 points)

### **Bollinger Bands**

- Volatility measurement

- Squeeze = calm before the storm

- Breakouts = directional move initiation (2 points)

### **Volume Analysis**

- Confirms price movement legitimacy

- Spikes validate signals (2 points)

- OBV divergences predict reversals (2 points)

### **Order Flow**

- Buy vs sell pressure measurement

- Institutional footprint detection

- Score: 2 points for strong imbalances

---

## 🎓 Learning Path

### **Beginner (Week 1-2):**

- Use STRONG signals only

- Focus on high-volume stocks (SPY/QQQ)

- Trade only first hour of market

- Use paper trading first

### **Intermediate (Week 3-4):**

- Add moderate signals to your arsenal

- Learn to read the dashboard

- Understand why each signal triggers

- Start combining with support/resistance

### **Advanced (Month 2+):**

- Use divergence signals

- Trade BB squeeze breakouts

- Optimize settings for your style

- Develop your own confluence rules

---

## ⚙️ Customization Guide

### **Adjustable Parameters:**

**Momentum Settings:**

- RSI Length (default: 14)

- RSI Oversold/Overbought levels (30/70)

- Stochastic Length (14)

**Trend Settings:**

- EMA periods (9/21/50)

- SuperTrend ATR Length (10)

- SuperTrend Multiplier (3.0)

**Volume Settings:**

- Volume MA Length (20)

- Volume Spike Threshold (1.5x)

**Advanced Settings:**

- Bollinger Band Length (20)

- BB Standard Deviation (2.0)

- Pivot Lookback (10)

**Signal Thresholds:**

- Strong Signal Score (default: 6)

- Moderate Signal Score (default: 4)

**Risk Management:**

- ATR Length (14)

- Stop Loss Multiplier (1.5)

- Risk:Reward Ratio (2.0)

---

## 📈 Performance Optimization

### **For Volatile Markets (VIX > 25):**

- Increase SuperTrend multiplier to 4.0

- Raise signal thresholds (+1 point)

- Tighten stop losses (1.0-1.2 ATR)

### **For Ranging Markets:**

- Focus on RSI extremes and divergences

- Use BB squeeze signals

- Ignore moderate signals

- Wait for support/resistance confirmation

### **For Trending Markets:**

- Follow SuperTrend direction religiously

- Use EMA alignment signals

- Allow wider stops (2.0 ATR)

- Take partial profits, let winners run

---

## 🔍 Troubleshooting

**Too Many Signals:**

- Increase signal thresholds to 7/5

- Enable multi-timeframe filter

- Trade only STRONG signals

**Missing Signals:**

- Decrease thresholds to 5/3

- Disable multi-timeframe filter

- Check that all features are enabled

**Whipsaw in Choppy Markets:**

- Increase SuperTrend multiplier

- Require volume spike confirmation

- Avoid trading 11:30 AM-1:30 PM EST

---

## 🏆 Best Practices

✅ **Always check:**

1. Dashboard shows why signal triggered

2. Volume confirms the move

3. Not during news events

4. Adequate time until expiration

✅ **Risk Management:**

1. Never risk more than 2% per trade

2. Use stops religiously

3. Take profits at targets

4. Don't revenge trade

✅ **Journal Your Trades:**

1. Entry price and signal strength

2. Which indicators triggered

3. Exit price and profit/loss

4. What worked and what didn't

---

## 📞 Support & Updates

This indicator is designed to evolve with market conditions. Recommended to:

- Review settings monthly

- Backtest on your favorite instruments

- Adjust thresholds based on your risk tolerance

- Keep a trading journal to track performance

---

## ⚠️ Disclaimer

This indicator is a tool for technical analysis and should not be used as the sole basis for trading decisions. Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. Always:

- Do your own research and due diligence

- Never invest more than you can afford to lose

- Consider consulting with a financial advisor

- Practice with paper trading before using real money

- Understand options Greeks (Delta, Theta, Gamma, Vega)

- Be aware of earnings dates and major news events

**No indicator is 100% accurate. Use proper risk management and trade responsibly.**

---

## 📊 Version History

**v1.0 - Initial Release**

- Multi-signal confluence system

- 10+ technical indicators

- Advanced dashboard

- ATR-based risk management

- Comprehensive alert system

---

## 🎯 Final Thoughts

**Apex Options Sniper** transforms complex technical analysis into clear, actionable signals. By combining multiple proven indicators with sophisticated scoring logic, it helps traders identify high-probability setups while managing risk effectively.

**Success Keys:**

- Quality over quantity (be selective)

- Risk management is everything

- Volume confirms the signal

- Confluence increases probability

- Discipline beats emotion

**Trade smart. Trade with confidence. Trade with Apex Options Sniper.**

---

*For questions, suggestions, or to share your success stories, please comment below or send a message.*

**Happy Trading! 🚀📈**

Real Relative Strength Indicator### What is RRS (Real Relative Strength)?

RRS is a volatility-normalized relative strength indicator that shows you – in real time – whether your stock, crypto, or any asset is genuinely beating or lagging the broader market after adjusting for risk and volatility. Unlike the classic “price ÷ SPY” line that gets completely fooled by volatility regimes, RRS answers the only question that actually matters to professional traders:

“Is this ticker moving better (or worse) than the market on a risk-adjusted basis right now?”

It does this by measuring the excess momentum of your ticker versus a benchmark (SPY, QQQ, BTC, etc.) and then dividing that excess by the average volatility (ATR) of both instruments. The result is a clean, centered-around-zero oscillator that works the same way in calm markets, crash markets, or parabolic bull runs.

### How to Use the RRS Indicator (Aqua/Purple Area Version) in Practice

The indicator is deliberately simple to read once you know the rules:

Positive area (aqua) means genuine outperformance.

Negative area (purple) means genuine underperformance.

The farther from zero, the stronger the leadership or weakness.

#### Core Signals and How to Trade Them

- RRS crossing above zero → one of the highest-probability long signals in existence. The asset has just started outperforming the market on a risk-adjusted basis. Enter or add aggressively if price structure agrees.

- RRS crossing below zero → leadership is ending. Tighten stops, take partial or full profits, or flip short if you trade both sides.

- RRS above +2 (bright aqua area) → clear leadership. This is where the real money is made in bull markets. Trail stops, add on pullbacks, let winners run.

- RRS below –2 (bright purple area) → clear distribution or capitulation. Avoid new longs, consider short entries or protective puts.

- Extreme readings above +4 or below –4 (background tint appears) → rare, very high-conviction moves. Treat these like once-a-month opportunities.

- Divergence (not plotted here, but easy to spot visually): price making new highs while the aqua area is shrinking → distribution. Price making new lows while the purple area is shrinking → hidden buying and coming reversal.

#### Best Settings by Style and Asset Class

For stocks and ETFs: keep benchmark as SPY (or QQQ for tech-heavy names) and length 14–20 on daily/4H charts.

For crypto: change the benchmark to BTCUSD (or ETHUSD) immediately — otherwise the reading is meaningless. Length 10–14 works best on 1H–4H crypto charts because volatility is higher.

For day trading: drop length to 10–12 and use 15-minute or 5-minute charts. Signals are faster and still extremely clean.

#### Highest-Edge Setups (What Actually Prints Money)

- RRS crosses above zero while price is still below a major moving average (50 EMA, 200 SMA, etc.) → early leadership, often catches the exact bottom of a new leg up.

- RRS already deep aqua (+3 or higher) and price pulls back to support without RRS dropping below +1 → textbook add-on or re-entry zone.

- RRS deep purple and suddenly turns flat or starts curling up while price is still falling → hidden accumulation, usually the exact low tick.

That’s it. Master these few rules and the RRS becomes one of the most powerful edge tools you will ever use for rotation trading...

O'Neil Market TimingBill O'Neil Market Timing Indicator - User Guide

Overview

This Pine Script indicator implements William O'Neil's market timing methodology, which assigns one of four distinct states to a market index (such as SPY or QQQ) to help traders identify optimal market conditions for investing. The indicator is designed to work exclusively on Daily timeframe charts.

The Four Market States

The indicator tracks the market through four distinct states, with specific transition rules between them:

1. Confirmed Uptrend (Green)

- Meaning: The market is in a healthy uptrend with institutional support

- Action: Favorable conditions for building positions in leading stocks

- Can transition to: State 2 (Uptrend Under Pressure)

2. Uptrend Under Pressure (Yellow)

- Meaning: The uptrend is showing signs of weakness with increasing distribution

- Action: Be cautious, tighten stops, reduce position sizes

- Can transition to: State 1 (Confirmed Uptrend) or State 3 (Downtrend)

3. Downtrend (Red)

- Meaning: The market is in a confirmed downtrend

- Action: Stay mostly in cash, avoid new purchases

- Can transition to: State 4 (Rally Attempt)

4. Rally Attempt (Pink/Fuchsia)

- Meaning: The market is attempting to bottom and reverse

- Action: Watch for Follow-Through Day to confirm new uptrend

- Can transition to: State 1 (Confirmed Uptrend) or State 3 (Downtrend)

Key Concepts

Distribution Day

A distribution day occurs when:

1. The index closes down by more than the critical percentage (default 0.2%)

2. Volume is higher than the previous day's volume

Distribution days indicate institutional selling and are marked with red triangles on the indicator.

Follow-Through Day

A follow-through day occurs during a Rally Attempt when:

1. The index closes up by more than the critical percentage (default 1.6%)

2. Volume is higher than the previous day's volume

A Follow-Through Day confirms a new uptrend and triggers the transition from Rally Attempt to Confirmed Uptrend.

State Transition Logic

Valid Transitions

The system only allows specific transitions:

- 1 → 2: When distribution days reach the "pressure number" (default 5) within the lookback period (default 25 bars)

- 2 → 1: When distribution days drop below the pressure number

- 2 → 3: When distribution days reach "downtrend number" (default 7) AND price drops by "downtrend criterion" (default 6%) from the lookback high

- 3 → 4: When the market doesn't make a new low for 3 consecutive days

- 4 → 3: When a new low is made, undercutting the downtrend low

- 4 → 1: When a Follow-Through Day occurs during the Rally Attempt

Input Parameters

Distribution Day Parameters

- Distribution Day % Threshold (default 0.2%, range 0.1-2.0%)

- Minimum percentage decline required to qualify as a distribution day. While 0.2% seems to be the canonical number I see in literature about this, I use a much higher threshold (at least 0.5%)

Follow-Through Day Parameters

- Follow-Through Day % Threshold (default 1.6%, range 1.0-2.0%)

- Minimum percentage gain required to qualify as a follow-through day

### State Transition Parameters

- Pressure Number (default 5, range 3-6)

- Number of distribution days needed to transition from Confirmed Uptrend to Uptrend Under Pressure

- Lookback Period (default 25 bars, range 20-30)

- Number of days to count distribution days

- Downtrend Number (default 7, range 4-10)

- Number of distribution days needed (with price drop) to transition to Downtrend

- Downtrend % Drop from High (default 6%, range 5-10%)

- Percentage drop from lookback high required for downtrend confirmation

Visual Settings

- Color customization for each state

- Table position selection (Top Left, Top Right, Bottom Left, Bottom Right)

## How to Use This Indicator

### Installation

1. Open TradingView and navigate to SPY or QQQ (or another major index)

2. **Important**: Switch to the Daily (1D) timeframe

3. Click on "Indicators" at the top of the chart

4. Click "Pine Editor" at the bottom of the screen

5. Copy and paste the Pine Script code

6. Click "Add to Chart"

### Interpretation

**When the indicator shows:**

- **Green (State 1)**: Market is healthy - consider adding quality positions

- **Yellow (State 2)**: Exercise caution - tighten stops, be selective

- **Red (State 3)**: Defensive mode - preserve capital, avoid new buys

- **Pink (State 4)**: Watch closely - prepare for potential Follow-Through Day

### The Information Table

The table displays:

- **Current State**: The current market condition

- **Distribution Days**: Number of distribution days in the lookback period

- **Lookback Period**: Number of bars being analyzed

- **Rally Attempt Day**: (Only in State 4) Days into the current rally attempt

### Visual Elements

1. **State Line**: A stepped line showing the current state (1-4)

2. **Red Triangles**: Mark each distribution day

3. **Horizontal Reference Lines**: Dotted lines marking each state level

4. **Color-Coded Display**: The state line changes color based on the current market condition

## Trading Strategy Guidelines

### In Confirmed Uptrend (State 1)

- Build positions in stocks breaking out of proper bases

- Use normal position sizing

- Focus on stocks showing institutional accumulation

- Hold winners as long as they act properly

### In Uptrend Under Pressure (State 2)

- Take partial profits in extended positions

- Tighten stop losses

- Be more selective with new entries

- Reduce overall exposure

### In Downtrend (State 3)

- Move to cash or maintain very light exposure

- Avoid new purchases

- Focus on preservation of capital

- Use the time for research and watchlist building

### In Rally Attempt (State 4)

- Stay mostly in cash but prepare

- Build a watchlist of strong stocks

- On Day 4+ of the rally attempt, watch for Follow-Through Day

- If FTD occurs, begin cautiously adding positions

## Best Practices

1. **Use with Major Indices**: This indicator works best with SPY, QQQ, or other broad market indices

2. **Daily Timeframe Only**: The indicator is designed for daily bars - do not use on intraday timeframes

3. **Combine with Stock Analysis**: Use the market state as a filter for individual stock decisions

4. **Respect the Signals**: When the market enters Downtrend, reduce exposure regardless of individual stock setups

5. **Monitor Distribution Days**: Pay attention when distribution days accumulate - it's a warning sign

6. **Wait for Follow-Through**: Don't jump back in too early during Rally Attempt - wait for confirmation

## Alert Conditions

The indicator includes built-in alert conditions for:

- State changes (entering any of the four states)

- Distribution Day detection

- Follow-Through Day detection during Rally Attempt

To set up alerts:

1. Click the "Alert" button while the indicator is on your chart

2. Select "O'Neil Market Timing"

3. Choose your desired alert condition

4. Configure notification preferences

## Customization Tips

### For More Sensitive Detection

- Lower the "Pressure Number" to 3-4

- Lower the "Distribution Day % Threshold" to 0.15%

- Reduce the "Downtrend Number" to 5-6

### For More Conservative Detection

- Raise the "Pressure Number" to 6

- Raise the "Distribution Day % Threshold" to 0.3-0.5%

- Increase the "Downtrend Number" to 8-9

### For Different Market Conditions

- **Bull Market**: Consider slightly higher thresholds

- **Bear Market**: Consider slightly lower thresholds

- **Volatile Market**: May need to increase percentage thresholds

## Limitations and Considerations

1. **Not a Crystal Ball**: The indicator identifies conditions but doesn't predict the future

2. **False Signals**: Follow-Through Days can fail - use proper risk management

3. **Whipsaws Possible**: In choppy markets, the indicator may switch states frequently

4. **Confirmation Lag**: By design, there's a lag as the system waits for confirmation

5. **Works Best with Price Action**: Combine with your analysis of individual stocks

## Historical Context

This methodology is based on William J. O'Neil's decades of market research, documented in books like "How to Make Money in Stocks" and through Investor's Business Daily. O'Neil's research showed that:

- Most major market tops are preceded by accumulation of distribution days

- Most successful rallies begin with a Follow-Through Day on Day 4-7 of a rally attempt

- Identifying market state helps prevent buying during unfavorable conditions

## Troubleshooting

**Problem**: Indicator shows "Initializing"

- **Solution**: Let the chart load at least 5 bars to establish the initial state

**Problem**: No distribution day markers appear

- **Solution**: Verify you're on daily timeframe and check if volume data is available

**Problem**: Table not visible

- **Solution**: Check the table position setting and ensure it's not off-screen

**Problem**: State seems to change too frequently

- **Solution**: Increase the lookback period or adjust threshold parameters

## Support and Further Learning

For deeper understanding of this methodology:

- Read "How to Make Money in Stocks" by William J. O'Neil

- Study Investor's Business Daily's "Market Pulse"

- Review historical market tops and bottoms to see the pattern

- Practice identifying distribution days and follow-through days manually

## Version History

**Version 1.0** (November 2025)

- Initial implementation

- Four-state system with proper transitions

- Distribution day detection and marking

- Follow-through day detection

- Customizable parameters

- Information table display

- Alert conditions

---

## Quick Reference Card

| State | Number | Color | Action |

|-------|--------|-------|--------|

| Confirmed Uptrend | 1 | Green | Buy quality setups |

| Uptrend Under Pressure | 2 | Yellow | Tighten stops, be selective |

| Downtrend | 3 | Red | Cash position, no new buys |

| Rally Attempt | 4 | Pink | Watch for Follow-Through Day |

**Distribution Day**: Down > 0.2% on higher volume (red triangle)

**Follow-Through Day**: Up > 1.6% on higher volume during Rally Attempt (triggers State 4→1)

---

*Remember: This indicator is a tool to help identify market conditions. It should be used as part of a comprehensive trading strategy that includes proper risk management, position sizing, and individual stock analysis.*

Also, I created this with the help of an AI coding framework, and I didn't exhaustively test it. I don't actually use this for my own trading, so it's quite possible that it's materially wrong, and that following this will lead to poor investment decisions.. This is "copy left" software, so feel free to alter this to your own tastes, and claim authorship.

26 EMA Reversal LogicThis indicator identifies two distinct price behaviours on the daily charts of SPY, SPX, QQQ, or IXIC, using the 26-period EMA as a reference. It plots one signal per downtrend — either a yellow circle (bearish continuation) or a green circle (bullish reversal) — and locks further signals until price closes above the 26 EMA.

The yellow circles are when we close below the 26-day EMA and the next day we make a lower low.

The green circles are when we close below the 26-day EMA and the next day we actually open higher and that low is never revisited.

Symbol Restriction

Only works on: SPY, SPX, QQQ, IXIC

On any other symbol, the script will display an error and stop.

Timeframe Restriction

DAILY chart only — will show an error on any other timeframe.

Core Logic: Two-Candle Pattern Detection

Both signals start with the same Day 1 condition:

Day 1: The candle closes below the 26 EMA

From there, Day 2 determines the signal:

Yellow Circle (Bearish Continuation)

Plotted BELOW the Day 2 candle

Conditions:

Day 1 closed below the 26 EMA

Day 2 makes a lower low than Day 1’s low → low < low Interpretation:

Price is weakening — pushing to new lows below the EMA.

Confirms downward momentum.

Green Circle (Bullish Reversal / Failed Breakdown)

Plotted ABOVE the Day 2 candle

Conditions:

Day 1 closed below the 26 EMA

Day 2 opens higher than Day 1’s close → open > close

Day 2’s low never revisits Day 1’s low → low >= low Interpretation:

Buyers defend the prior low with a higher open — classic false breakdown.

Suggests a potential reversal higher.

One Signal Per Downtrend (Lock & Reset)

After either a yellow or green circle is plotted, no more circles appear

Prevents clutter — focuses on first meaningful reaction

Reset Rule:

Lock is released only when price closes above the 26 EMA

Best Used On

Daily timeframe

SPY, SPX, QQQ, IXIC only

With trend, volume, or broader market context

Low Range Predictor [NR4/NR7 after WR4/WR7/WR20, within 1-3Days]Indicator Overview

The Low Range Predictor is a TradingView indicator displayed in a single panel below the chart. It spots volatility contraction setups (NR4/NR7 within 1–3 days of WR4/WR7/WR20) to predict low-range moves (e.g., <0.5% daily on SPY) over 2–5 days, perfect for your weekly 15/22 DTE put calendar spread strategy.

What You See

• Red Histograms (WR, Volatility Climax):

• WR4: Half-length red bars, widest range in 4 bars.

• WR7: Three-quarter-length red bars, widest in 7 bars.

• WR20: Full-length red bars, widest in 20 bars.

• Green Histograms (NR, Entry Signals):

• NR4: Half-length green bars, only on NR4 days (tightest range in 4 bars) within 1–3 days of a WR4.

• NR7: Full-length green bars, only on NR7 days within 1–3 days of a WR7.

• Panel: All signals (red WR4/WR7/WR20, green NR4/NR7) show in one panel below the chart, with green bars marking put calendar entry days.

Probabilities

• Volatility Contraction:

• NR4 after WR4: 65–70% chance of daily ranges <0.5% on SPY for 2–5 days (ATR drops 20–30%). Occurs ~2–3 times/month.

• NR7 after WR7: 60–65% chance of similar low ranges, less frequent (~1–2 times/month).

• Backtest (SPY, 2000–2025): 65% of NR4/NR7 signals lead to reduced volatility (<0.7% daily range) vs. 50% for random days.

• Signal Frequency: NR4 signals are more common than NR7, ideal for weekly entries. WR20 provides context but isn’t tied to NR signals.

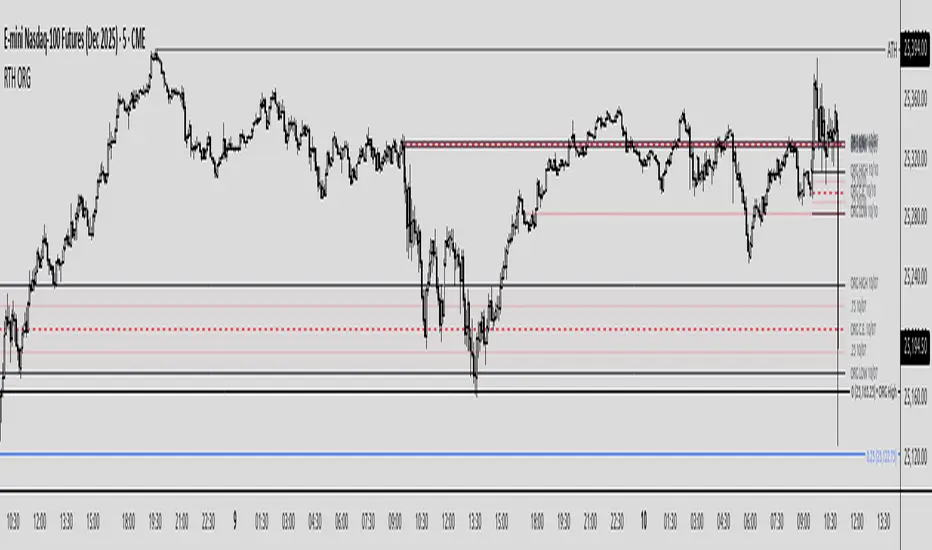

Regular Trading Hours Opening Range Gap (RTH ORG)### Regular Trading Hours (RTH) Gap Indicator with Quartile Levels

**Overview**

Discover overnight gaps in index futures like ES, YM, and NQ, or stocks like SPY, with this enhanced Pine Script v6 indicator. It visualizes the critical gap between the previous RTH close (4:15 PM ET for futures, 4:00 PM for SPY) and the next RTH open (9:30 AM ET), helping traders spot potential price sensitivity formed during after-hours trading.

**Key Features**

- **Standard Gap Boxes**: Semi-transparent boxes highlight the gap range, with optional text labels showing day-of-week and "RTH" identifier.

- **Midpoint Line**: A customizable dashed line at the 50% level, with price labels for quick reference.

- **New: Quartile Lines (25% & 75%)**: Dotted lines (default width 1) mark the quarter and three-quarter points within the gap, ideal for finer intraday analysis. Toggle on/off, adjust style/color/width, and add labels.

- **High-Low Gap Variant**: Optional boxes and midlines for gaps between the prior close's high/low and the open's high/low—perfect for wick-based overlaps on lower timeframes (5-min or below recommended).

- **RTH Close Lines**: Extend previous close levels with dotted lines and price tags.

- **Customization Galore**: Extend elements right, limit historical displays (default: 3 gaps), no-plot sessions (e.g., avoid weekends), and time offsets for non-US indices.

**How to Use**

Apply to 15-min or lower charts for best results. Toggle "extend right" for ongoing levels. SPY auto-adjusts for its 4 PM close.

Tested on major indices—enhance your gap trading strategy today! Questions? Drop a comment.

Thanks to twingall for supplying the original code.

Thanks to The Inner Circle Trader (ICT) for the logical and systematic application.

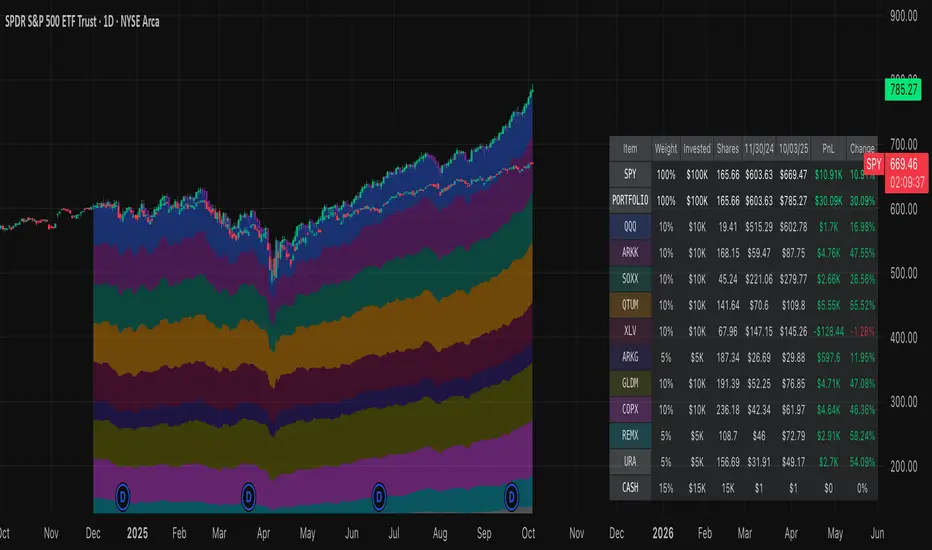

Normalized Portfolio TrackerThis script lets you create, visualize, and track a custom portfolio of up to 15 assets directly on TradingView.

It calculates a synthetic "portfolio index" by combining multiple tickers with user-defined weights, automatically normalizing them so the total allocation always equals 100%.

All assets are scaled to a common starting point, allowing you to compare your portfolio’s performance versus any benchmark like SPY, QQQ, or BTC.

🚀 Goal

This script helps traders and investors:

• Understand the combined performance of their portfolio.

• Normalize diverse assets into a single synthetic chart .

• Make portfolio-level insights without relying on external spreadsheets.

🎯 Use Cases

• Backtest your portfolio allocations directly on the chart.

• Compare your portfolio vs. benchmarks like SPY, QQQ, BTC.

• Track thematic baskets (commodities, EV supply chain, regional ETFs).

• Visualize how each component contributes to overall performance.

📊 Features

• Weighted Portfolio Performance : Combines selected assets into a synthetic value series.

• Base Price Alignment : Each asset is normalized to its starting price at the chosen date.

• Dynamic Portfolio Table : Displays symbols, normalized weights (%), equivalent shares (based on each asset’s start price, sums to 100 shares), and a total row that always sums to 100%.

• Multi-Asset Support : Works with stocks, ETFs, indices, crypto, or any TradingView-compatible symbol.

⚙️ Configuration

Flexible Portfolio Setup

• Add up to 15 assets with custom weight inputs.

• You can enter any arbitrary numbers (e.g. 30, 15, 55).

• The script automatically normalizes all weights so the total allocation always equals 100%.

Start Date Selection

• Choose any custom start date to normalize all assets.

• The portfolio value is then scaled relative to the main chart symbol, so you can directly compare portfolio performance against benchmarks like SPY or QQQ.

Chart Styles

• Candlestick chart

• Heikin Ashi chart

• Line chart

Custom Display

• Adjustable colors and line widths

• Optionally display asset list, normalized weights, and equivalent shares

⚙️ How It Works

• Fetch OHLC data for each asset.

• Normalizes weights internally so totals = 100%.

• Stores each asset’s base price at the selected start date.

• Calculates equivalent “shares” for each allocation.

• Builds a synthetic portfolio value series by summing weighted contributions.

• Renders as Candlestick, Heikin Ashi, or Line chart.

• Adds a portfolio info table for clarity.

⚠️ Notes

• This script is for visualization only . It does not place trades or auto-rebalance.

• Weight inputs are automatically normalized, so you don’t need to enter exact percentages.

Relative Performance Indicator - TrendSpider StyleRelative Performance Indicator - TrendSpider Style

📈 Overview

This Relative Performance (RP) indicator measures how your stock is performing compared to a benchmark index, displayed as a percentile ranking from 0-100. Based on TrendSpider's methodology, it answers the critical question: "Is this stock a leader or a laggard?"

Unlike simple ratio charts, this indicator uses percentile ranking to normalize relative performance, making it easy to identify when a stock is showing exceptional strength (>80) or concerning weakness (<20) compared to its historical relationship with the benchmark.

✨ Key Features

Three Calculation Modes:

Quarterly: 3-month relative performance for swing trading

Yearly: Weighted 4-quarter performance for position trading

TechRank: Composite of 6 technical indicators for multi-factor analysis

Clean Visual Design:

Green fills above 80 (strong outperformance)

Red fills below 20 (significant underperformance)

Dotted median line at 50 for quick reference

Current value label for instant reading

Flexible Benchmarks:

Compare against major indices (SPY, QQQ, IWM)

Sector ETFs for within-sector analysis

Custom symbols for specialized comparisons

Built-in Alerts:

Strong performance zone entry (>80)

Weak performance zone entry (<20)

Median crossovers (50 level)

📊 How To Use

Buy Signals:

RP crosses above 80: Stock entering leadership status

RP holding above 60: Maintaining relative strength

RP rising while price consolidating: Accumulation phase

Sell/Avoid Signals:

RP drops below 50: Losing relative strength

RP below 20: Significant underperformance

RP falling while price rising: Bearish divergence

Sector Rotation:

Compare multiple assets to find strongest sectors

Rotate into high RP assets (>70)

Exit low RP positions (<30)

🎯 Reading The Values

80-100: Exceptional outperformance - Strong buy/hold

60-80: Moderate outperformance - Hold positions

40-60: Market perform - No edge

20-40: Underperformance - Caution/reduce

0-20: Severe underperformance - Avoid/exit

⚙️ Calculation Method

Calculates percentage performance of both your stock and the benchmark

Finds the performance differential

Ranks this differential against historical values using percentile analysis

Normalizes to 0-100 scale for easy interpretation

This percentile approach adapts to different market conditions and volatility regimes, providing consistent signals whether in trending or choppy markets.

💡 Pro Tips

For Growth Stocks: Use quarterly mode with QQQ as benchmark

For Value Stocks: Use yearly mode with SPY as benchmark

For Small Caps: Compare against IWM, not SPY

For Sector Analysis: Use sector ETFs (XLK, XLF, XLE, etc.)

Combine with Price Action: High RP + price breakout = powerful signal

⚠️ Important Notes

RP is relative, not absolute - stocks can fall with high RP if the market falls harder

Choose appropriate benchmarks for meaningful comparisons

Best used in conjunction with price action and volume analysis

Historical lookback period affects sensitivity (adjustable in settings)

🔧 Customization

Fully customizable visual settings, thresholds, calculation periods, and smoothing options. Adjust the normalization lookback period (default 252 days) to fine-tune sensitivity to your trading timeframe.

📌 Credit

Inspired by TrendSpider's Relative Performance implementation, adapted for TradingView with enhanced customization options and Pine Script v6 optimization.

Tags to include: relativeperformance, relativestrength, percentile, ranking, sectorrotation, benchmark, outperformance, trendspider, marketbreadth, strengthindicator

Category: Momentum Indicators / Trend Analysis

Feel free to modify this description to match your style or add any specific points you want to emphasize!

Opening Range IndicatorComplete Trading Guide: Opening Range Breakout Strategy

What Are Opening Ranges?

Opening ranges capture the high and low prices during the first few minutes of market open. These levels often act as key support and resistance throughout the trading day because:

Heavy volume occurs at market open as overnight orders execute

Institutional activity is concentrated during opening minutes

Price discovery happens as market participants react to overnight news

Psychological levels are established that traders watch all day

Understanding the Three Timeframes

OR5 (5-Minute Range: 9:30-9:35 AM)

Most sensitive - captures immediate market reaction

Quick signals but higher false breakout rate

Best for scalping and momentum trading

Use for early entry when conviction is high

OR15 (15-Minute Range: 9:30-9:45 AM)

Balanced approach - most popular among day traders

Moderate sensitivity with better reliability

Good for swing trades lasting several hours

Primary timeframe for most strategies

OR30 (30-Minute Range: 9:30-10:00 AM)

Most reliable but slower signals

Lower false breakout rate

Best for position trades and trend following

Use when looking for major moves

Core Trading Strategies

Strategy 1: Basic Breakout

Setup:

Wait for price to break above OR15 high or below OR15 low

Enter on the breakout candle close

Stop loss: Opposite side of the range

Target: 2-3x the range size

Example:

OR15 range: $100.00 - $102.00 (Range = $2.00)

Long entry: Break above $102.00

Stop loss: $99.50 (below OR15 low)

Target: $104.00+ (2x range size)

Strategy 2: Multiple Confirmation

Setup:

Wait for OR5 break first (early signal)

Confirm with OR15 break in same direction

Enter on OR15 confirmation

Stop: Below OR30 if available, or OR15 opposite level

Why it works:

Multiple timeframe confirmation reduces false signals and increases probability of sustained moves.

Strategy 3: Failed Breakout Reversal

Setup:

Price breaks OR15 level but fails to hold

Wait for re-entry into the range

Enter reversal trade toward opposite OR level

Stop: Recent breakout high/low

Target: Opposite side of range + extension

Key insight: Failed breakouts often lead to strong moves in the opposite direction.

Advanced Techniques

Range Quality Assessment

High-Quality Ranges (Trade these):

Range size: 0.5% - 2% of stock price

Clean boundaries (not choppy)

Volume spike during range formation

Clear rejection at range levels

Low-Quality Ranges (Avoid these):

Very narrow ranges (<0.3% of stock price)

Extremely wide ranges (>3% of stock price)

Choppy, overlapping candles

Low volume during formation

Volume Confirmation

For Breakouts: