Understanding contract sizes in a strategyThis simple strat fires up on green bars, down on red bars. cannot get any simpler. So, it's a good example to check how returns are calculated.

First, the internal firing mechanism for the strategy.entry function is something hardcore. As result, the entry points can be confusing, and seem to appear in a wrong bar (as the 2nd and 3rd signals are good examples), but i'll put that aside to keep it simple. And, because i don't yet get it myself ;)

The example is simple, so that numbers can be followed easy. Chart in BTC/USD, so USD is the "base" currency used by strat to calculate. A contract/unit is the value of 1 unit in base currency. 1 Apple share is 600$, 1 bitcoin is 600$, 1 oz gold is 1330 bucks. So, here in each bar, the value of 1 contract is the value of the BTC in USD. simple as that.

The strat properties, can be passed as input fields (line 2) or accessed/changed in the right click->properties pop-up. To make it easier, initial capital is 1000 bucks, and "order size" is 1 contract. This means that the strat will open a position of 1 BTC when it fires. Value "Initial capital" makes no difference at all, at least with these choices. It's just for show. Try to put 1$ and 1 contract, the strat will still trade anyway. It manages to trade 1 contract(or BTC) values at ~600$, with a single dollar. nice ;)

Check the chart. see the little blue "BarUp +1" ? that's it, strat goes long 1 BTC. there's a little blue triangle on the bar, points to the value of entry.

Then later, on second move, the "BarDn -2", the strat goes short 2BTC. 1BTC to close the long +1 more to open a short.

The profit here is the difference between the value of the long opening and the long closing. The extra BTC (shorted) is part of the next position. Since this dumb strat just reverses the direction, there are always +2, -2 , +2.... 1 to close previous position, 1 to open another. At the strategy tester tab, the option "list of trades" shows in details each of the moves

Checking each move and comparing what we see with the chart itself helps to achieve ilumination :)

Bonus feature: as soon as you get it, try to increase the option "pyramiding" and see how the strat adds more contracts, and how it reverses the positions. sometimes it even makes sense!!!! :)

Cari dalam skrip untuk "the strat"

Super-AO with Risk Management Strategy Template - 11-29-25Super-AO Strategy with Advanced Risk Management Template

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

Welcome to the Super-AO Strategy. This is more than just a buy/sell indicator; it is a complete, open-source Risk Management (RM) Template designed for the Pine Script community.

At its core, this script implements a robust swing-trading strategy combining the SuperTrend (for macro direction) and the Awesome Oscillator (for momentum). However, the real power lies under the hood: a custom-built Risk Management Engine that handles trade states, prevents repainting, and manages complex exit conditions like Staged Take Profits and Advanced Adaptive Trailing Stops (AATS).

We are releasing this code to help traders transition from simple indicators to professional-grade strategy structures.

2. Quick Action Guide (TL;DR)

Best Timeframe: 4 Hours (H4) and above. Designed for Swing Trading.

Best Assets: "Well-behaved" assets with clear liquidity (Major Forex pairs, BTC, ETH, Indices).

Strategy Type: Trend Following + Momentum Confirmation.

Key Feature: The Risk Management Engine is modular. You can strip out the "Super-AO" logic and insert your own strategy logic into the template easily.

Repainting: Strictly Non-Repainting. The engine calculates logic based on confirmed candle closes.

3. Detailed Report: How It Works

A. The Strategy Logic: Super-AO

The entry logic is based on the convergence of two classic indicators:

SuperTrend: Determines the overall trend bias (Green/Red).

Awesome Oscillator (AO): Measures market momentum.

The Signal:

LONG (+2): SuperTrend is Green AND AO is above the Zero Line AND AO is Rising.

SHORT (-2): SuperTrend is Red AND AO is below the Zero Line AND AO is Falling.

By requiring momentum to agree with the trend, this system filters out many false signals found in ranging markets.

B. The Risk Management (RM) Engine

This script features a proprietary State Machine designed by Signal Lynx. Unlike standard strategies that simply fire orders, this engine separates the Signal from the Execution.

Logic Injection: The engine listens for a specific integer signal: +2 (Buy) or -2 (Sell). This makes the code a Template. You can delete the Super-AO section, write your own logic, and simply pass a +2 or -2 to the RM_EngineInput variable. The engine handles the rest.

Trade States: The engine tracks the state of the trade (Entry, In-Trade, Exiting) to prevent signal spamming.

Aggressive vs. Conservative:

Conservative Mode: Waits for a full trend reversal before taking a new trade.

Aggressive Mode: Allows for re-entries if the trend is strong and valid conditions present themselves again (Pyramiding Type 1).

C. Advanced Exit Protocols

The strategy does not rely on a single exit point. It employs a "Layered Defense" approach:

Hard Stop Loss: A fixed percentage safety net.

Staged Take Profits (Scaling Out): The script allows you to set 3 distinct Take Profit levels. For example, you can close 10% of your position at TP1, 10% at TP2, and let the remaining 80% ride the trend.

Trailing Stop: A standard percentage-based trailer.

Advanced Adaptive Trailing Stop (AATS): This is a highly sophisticated volatility stop. It calculates market structure using Hirashima Sugita (HSRS) levels and Bollinger Bands to determine the "floor" and "ceiling" of price action.

If volatility is high: The stop loosens to prevent wicking out.

If volatility is low: The stop tightens to protect profit.

D. Repainting Protection

Many Pine Script strategies look great in backtesting but fail in live trading because they rely on "real-time" price data that disappears when the candle closes.

This Risk Management engine explicitly pulls data from the previous candle close (close , high , low ) for its calculations. This ensures that the backtest results you see match the reality of live execution.

4. For Developers & Modders

We encourage you to tear this code apart!

Look for the section titled // Super-AO Strategy Logic.

Replace that block with your own RSI, MACD, or Price Action logic.

Ensure your logic outputs a 2 for Buy and -2 for Sell.

Connect it to RM_EngineInput.

You now have a fully functioning Risk Management system for your custom strategy.

5. About Signal Lynx

Automation for the Night-Shift Nation 🌙

This code has been in action since 2022 and is a known performer in PineScript v5. We provide this open source to help the community build better, safer automated systems.

If you are looking to automate your strategies, please take a look at Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source). If you make beneficial modifications, please release them back to the community!

ATH대비 지정하락률에 도착 시 매수 - 장기홀딩 선물 전략(ATH Drawdown Re-Buy Long Only)본 스크립트는 과거 하락 데이터를 이용하여, 정해진 하락 %가 발생하는 경우 자기 자본의 정해진 %만큼을 진입하게 설계되어진 스트레티지입니다.

레버리지를 사용할 수 있으며 기본적으로 셋팅해둔 값이 내장되어있습니다.(자유롭게 바꿔서 쓰시면 됩니다.) 추가적으로 2번의 진입 외에도 다른 진입 기준, 진입 %를 설정하실 수 있으며 - ChatGPT에게 요청하면 수정해줄 것입니다.

실제 사용용도로는 KillSwitch 기능을 꺼주세요. 바 돋보기 기능을 켜주세요.

ATH Drawdown Re-Buy Long Only 전략 설명

1. 전략 개요

ATH Drawdown Re-Buy Long Only 전략은 자산의 역대 최고가(ATH, All-Time High)를 기준으로 한 하락폭(드로우다운)을 활용하여,

특정 구간마다 단계적으로 롱 포지션을 구축하는 자동 재매수(Long Only) 전략입니다.

본 전략은 다음과 같은 목적을 가지고 설계되었습니다.

급격한 조정 구간에서 체계적인 분할 매수 및 레버리지 활용

ATH를 기준으로 한 명확한 진입 규칙 제공

실시간으로

평단가

레버리지

청산가 추정

계좌 MDD

수익률

등을 시각적으로 제공하여 리스크와 포지션 상태를 직관적으로 확인할 수 있도록 지원

※ 본 전략은 교육·연구·백테스트 용도로 제공되며,

어떠한 형태의 투자 권유 또는 수익을 보장하지 않습니다.

2. 전략의 핵심 개념

2-1. ATH(역대 최고가) 기준 드로우다운

전략은 차트 상에서 항상 가장 높은 고가(High)를 ATH로 기록합니다.

새로운 고점이 형성될 때마다 ATH를 갱신하고, 해당 ATH를 기준으로 다음을 계산합니다.

현재 바의 저가(Low)가 ATH에서 몇 % 하락했는지

현재 바의 종가(Close)가 ATH에서 몇 % 하락했는지

그리고 사전에 설정한 두 개의 드로우다운 구간에서 매수를 수행합니다.

1차 진입 구간: ATH 대비 X% 하락 시

2차 진입 구간: ATH 대비 Y% 하락 시

각 구간은 ATH가 새로 갱신될 때마다 한 번씩만 작동하며,

새로운 ATH가 생성되면 다시 “1차 / 2차 진입 가능 상태”로 초기화됩니다.

2-2. 첫 포지션 100% / 300% 특수 규칙

이 전략의 중요한 특징은 **“첫 포지션 진입 시의 예외 규칙”**입니다.

전략이 현재 어떠한 포지션도 들고 있지 않은 상태에서

최초로 롱 포지션을 진입하는 시점(첫 포지션)에 대해:

기본적으로는 **자산의 100%**를 기준으로 포지션을 구축하지만,

만약 그 순간의 가격이 ATH 대비 설정값 이상(예: 약 –72.5% 이상 하락한 상황) 이라면

→ 자산의 300% 규모로 첫 포지션을 진입하도록 설계되어 있습니다.

이 규칙은 다음과 같이 동작합니다.

첫 진입이 1차 드로우다운 구간에서 발생하든,

첫 진입이 2차 드로우다운 구간에서 발생하든,

현재 하락폭이 설정된 기준 이상(예: –72.5% 이상) 이라면

→ “이 정도 하락이면 첫 진입부터 더 공격적으로 들어간다”는 의미로 300% 규모로 진입

그 이하의 하락폭이라면

→ 첫 진입은 100% 규모로 제한

즉, 전략은 다음 두 가지 모드로 동작합니다.

일반적인 상황의 첫 진입: 자산의 100%

심각한 드로우다운 구간에서의 첫 진입: 자산의 300%

이 특수 규칙은 깊은 하락에서는 공격적으로, 평소에는 상대적으로 보수적으로 진입하도록 설계된 것입니다.

3. 전략 동작 구조

3-1. 매수 조건

차트 상 High 기준으로 ATH를 추적합니다.

각 바마다 해당 ATH에서의 하락률을 계산합니다.

사용자가 설정한 두 개의 드로우다운 구간(예시):

1차 구간: 예를 들어 ATH – 50%

2차 구간: 예를 들어 ATH – 72.5%

각 구간에 대해 다음과 같은 조건을 확인합니다.

“이번 ATH 구간에서 아직 해당 구간 매수를 한 적이 없는 상태”이고,

현재 바의 저가(Low)가 해당 구간 가격 이하를 찍는 순간

→ 해당 바에서 매수 조건 충족으로 간주

실제 주문은:

해당 구간 가격에 맞춰 롱 포지션 진입(리밋/시장가 기반 시뮬레이션) 으로 처리됩니다.

3-2. ATH 갱신과 진입 기회 리셋

차트 상에서 새로운 고점(High)이 기존 ATH를 넘어서는 순간,

ATH가 갱신되고,

1차 / 2차 진입 여부를 나타내는 내부 플래그가 초기화됩니다.

이를 통해, 시장이 새로운 고점을 돌파해 나갈 때마다,

해당 구간에서 다시 한 번씩 1차·2차 드로우다운 진입 기회를 갖게 됩니다.

4. 포지션 사이징 및 레버리지

4-1. 계좌 자산(Equity) 기준 포지션 크기 결정

전략은 현재 계좌 자산을 다음과 같이 정의하여 사용합니다.

현재 자산 = 초기 자본 + 실현 손익 + 미실현 손익

각 진입 구간에서의 포지션 가치는 다음과 같이 결정됩니다.

1차 진입 구간:

“자산의 몇 %를 사용할지”를 설정값으로 입력

설정된 퍼센트를 계좌 자산에 곱한 뒤,

다시 전략 내 레버리지 배수(Leverage) 를 곱하여 실제 포지션 가치를 계산

2차 진입 구간:

동일한 방식으로, 독립된 퍼센트 설정값을 사용

즉, 포지션 가치는 다음과 같이 계산됩니다.

포지션 가치 = 현재 자산 × (해당 구간 설정 % / 100) × 레버리지 배수

그리고 이를 해당 구간의 진입 가격으로 나누어 실제 수량(토큰 단위) 를 산출합니다.

4-2. 첫 포지션의 예외 처리 (100% / 300%)

첫 포지션에 대해서는 위의 일반적인 퍼센트 설정 대신,

다음과 같은 고정 비율이 사용됩니다.

기본: 자산의 100% 규모로 첫 포지션 진입

단, 진입 시점의 ATH 대비 하락률이 설정값 이상(예: –72.5% 이상) 일 경우

→ 자산의 300% 규모로 첫 포지션 진입

이때 역시 다음 공식을 사용합니다.

포지션 가치 = 현재 자산 × (100% 또는 300%) × 레버리지

그리고 이를 가격으로 나누어 실제 진입 수량을 계산합니다.

이 규칙은:

첫 진입이 1차 구간이든 2차 구간이든 동일하게 적용되며,

“충분히 깊은 하락 구간에서는 첫 진입부터 더 크게,

평소에는 비교적 보수적으로” 라는 운용 철학을 반영합니다.

4-3. 실레버리지(Real Leverage)의 추적

전략은 각 바 단위로 다음을 추적합니다.

바가 시작할 때의 기존 포지션 크기

해당 바에서 새로 진입한 수량

이를 바탕으로, 진입이 발생한 시점에 다음을 계산합니다.

실제 레버리지 = (포지션 가치 / 현재 자산)

그리고 차트 상에 예를 들어:

Lev 2.53x 와 같은 형식의 레이블로 표시합니다.

이를 통해, 매수 시점마다 실제 계좌 레버리지가 어느 정도였는지를 직관적으로 확인할 수 있습니다.

5. 시각화 및 모니터링 요소

5-1. 차트 상 시각 요소

전략은 차트 위에 다음과 같은 정보를 직접 표시합니다.

ATH 라인

High 기준으로 계산된 역대 최고가를 주황색 선으로 표시

평단가(평균 진입가) 라인

현재 보유 포지션이 있을 때,

해당 포지션의 평균 진입가를 노란색 선으로 표시

추정 청산가(고정형 청산가) 라인

포지션 수량이 변화하는 시점을 감지하여,

당시의 평단가와 실제 레버리지를 이용해 근사적인 청산가를 계산

이를 빨간색 선으로 차트에 고정 표시

포지션이 없거나 레버리지가 1배 이하인 경우에는 청산가 라인을 제거

매수 마커 및 레이블

1차/2차 매수 조건이 충족될 때마다 해당 지점에 매수 마커를 표시

"Buy XX% @ 가격", "Lev XXx" 형태의 라벨로

진입 비율과 당시 레버리지를 함께 시각화

레이블의 위치는 설정에서 선택 가능:

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

5-2. 우측 상단 정보 테이블

차트 우측 상단에는 현재 계좌·포지션 상태를 요약한 정보 테이블이 표시됩니다.

대표적으로 다음 항목들이 포함됩니다.

Pos Qty (Token)

현재 보유 중인 포지션 수량(토큰 기준, 절대값 기준)

Pos Value (USDT)

현재 포지션의 시장 가치 (수량 × 현재 가격)

Leverage (Now)

현재 실레버리지 (포지션 가치 / 현재 자산)

DD from ATH (%)

현재 가격 기준, 최근 ATH에서의 하락률(%)

Avg Entry

현재 포지션의 평균 진입 가격

PnL (%)

현재 포지션 기준 미실현 손익률(%)

Max DD (Equity %)

전략 전체 기간 동안 기록된 계좌 기준 최대 손실(MDD, Max Drawdown)

Last Entry Price

가장 최근에 포지션을 추가로 진입한 직후의 평균 진입 가격

Last Entry Lev

위 “Last Entry Price” 시점에서의 실레버리지

Liq Price (Fixed)

위에서 설명한 고정형 추정 청산가

Return from Start (%)

전략 시작 시점(초기 자본) 대비 현재 계좌 자산의 총 수익률(%)

이 테이블을 통해 사용자는:

현재 계좌와 포지션의 상태

리스크 수준

누적 성과

를 직관적으로 파악할 수 있습니다.

6. 시간 필터 및 라벨 옵션

6-1. 전략 동작 기간 설정

전략은 옵션으로 특정 기간에만 전략을 동작시키는 시간 필터를 제공합니다.

“Use Date Range” 옵션을 활성화하면:

시작 시각과 종료 시각을 지정하여

해당 구간에 한해서만 매매가 발생하도록 제한

옵션을 비활성화하면:

전략은 전체 차트 구간에서 자유롭게 동작

6-2. 진입 라벨 위치 설정

사용자는 매수/레버리지 라벨의 위치를 선택할 수 있습니다.

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

이를 통해 개인 취향 및 차트 가독성에 맞추어

시각화 방식을 유연하게 조정할 수 있습니다.

7. 활용 대상 및 사용 예시

본 전략은 다음과 같은 목적에 적합합니다.

현물 또는 선물 롱 포지션 기준 장기·스윙 관점 추매 전략 백테스트

“고점 대비 하락률”을 기준으로 한 규칙 기반 운용 아이디어 검증

레버리지 사용 시

계좌 레버리지·청산가·MDD를 동시에 모니터링하고자 하는 경우

특정 자산에 대해

“새로운 고점이 형성될 때마다

일정한 규칙으로 깊은 조정 구간에서만 분할 진입하고자 할 때”

실거래에 그대로 적용하기보다는,

전략 아이디어 검증 및 리스크 프로파일 분석,

자신의 성향에 맞는 파라미터 탐색 용도로 사용하는 것을 권장합니다.

8. 한계 및 유의사항

백테스트 결과는 미래 성과를 보장하지 않습니다.

과거 데이터에 기반한 시뮬레이션일 뿐이며,

실제 시장에서는

유동성

슬리피지

수수료 체계

강제청산 규칙

등 다양한 변수가 존재합니다.

청산가는 단순화된 공식에 따른 추정치입니다.

거래소별 실제 청산 규칙, 유지 증거금, 수수료, 펀딩비 등은

본 전략의 계산과 다를 수 있으며,

청산가 추정 라인은 참고용 지표일 뿐입니다.

레버리지 및 진입 비율 설정에 따라 손실 폭이 매우 커질 수 있습니다.

특히 **“첫 포지션 300% 진입”**과 같이 매우 공격적인 설정은

시장 급락 시 계좌 손실과 청산 리스크를 크게 증가시킬 수 있으므로

신중한 검토가 필요합니다.

실거래 연동 시에는 별도의 리스크 관리가 필수입니다.

개별 손절 기준

포지션 상한선

전체 포트폴리오 내 비중 관리 등

본 전략 외부에서 추가적인 안전장치가 필요합니다.

9. 결론

ATH Drawdown Re-Buy Long Only 전략은 단순한 “저가 매수”를 넘어서,

ATH 기준으로 드로우다운을 구조적으로 활용하고,

첫 포지션에 대한 **특수 규칙(100% / 300%)**을 적용하며,

레버리지·청산가·MDD·수익률을 통합적으로 시각화함으로써,

하락 구간에서의 규칙 기반 롱 포지션 구축과

리스크 모니터링을 동시에 지원하는 전략입니다.

사용자는 본 전략을 통해:

자신의 시장 관점과 리스크 허용 범위에 맞는

드로우다운 구간

진입 비율

레버리지 설정

다양한 시나리오에 대한 백테스트와 분석

을 수행할 수 있습니다.

다시 한 번 강조하지만,

본 전략은 연구·학습·백테스트를 위한 도구이며,

실제 투자 판단과 책임은 전적으로 사용자 본인에게 있습니다.

/ENG Version.

This script is designed to use historical drawdown data and automatically enter positions when a predefined percentage drop from the all-time high occurs, using a predefined percentage of your account equity.

You can use leverage, and default parameter values are provided out of the box (you can freely change them to suit your style).

In addition to the two main entry levels, you can add more entry conditions and custom entry percentages – just ask ChatGPT to modify the script.

For actual/live usage, please turn OFF the KillSwitch function and turn ON the Bar Magnifier feature.

ATH Drawdown Re-Buy Long Only Strategy

1. Strategy Overview

The ATH Drawdown Re-Buy Long Only strategy is an automatic re-buy (Long Only) system that builds long positions step-by-step at specific drawdown levels, based on the asset’s all-time high (ATH) and its subsequent drawdown.

This strategy is designed with the following goals:

Systematic scaled buying and leverage usage during sharp correction periods

Clear, rule-based entry logic using drawdowns from ATH

Real-time visualization of:

Average entry price

Leverage

Estimated liquidation price

Account MDD (Max Drawdown)

Return / performance

This allows traders to intuitively monitor both risk and position status.

※ This strategy is provided for educational, research, and backtesting purposes only.

It does not constitute investment advice and does not guarantee any profits.

2. Core Concepts

2-1. Drawdown from ATH (All-Time High)

On the chart, the strategy always tracks the highest high as the ATH.

Whenever a new high is made, ATH is updated, and based on that ATH the following are calculated:

How many percent the current bar’s Low is below the ATH

How many percent the current bar’s Close is below the ATH

Using these, the strategy executes buys at two predefined drawdown zones:

1st entry zone: When price drops X% from ATH

2nd entry zone: When price drops Y% from ATH

Each zone is allowed to trigger only once per ATH cycle.

When a new ATH is created, the “1st / 2nd entry possible” flags are reset, and new opportunities open up for that ATH leg.

2-2. Special Rule for the First Position (100% / 300%)

A key feature of this strategy is the special rule for the very first position.

When the strategy currently holds no position and is about to open the first long position:

Under normal conditions, it builds the position using 100% of account equity.

However, if at that moment the price has dropped by at least a predefined threshold from ATH (e.g. around –72.5% or more),

→ the strategy will open the first position using 300% of account equity.

This rule works as follows:

Whether the first entry happens at the 1st drawdown zone or at the 2nd drawdown zone,

If the current drawdown from ATH is at or below the threshold (e.g. –72.5% or worse),

→ the strategy interprets this as “a sufficiently deep crash” and opens the initial position with 300% of equity.

If the drawdown is less severe than the threshold,

→ the first entry is capped at 100% of equity.

So the strategy has two modes for the first entry:

Normal market conditions: 100% of equity

Deep drawdown conditions: 300% of equity

This special rule is intended to be aggressive in extremely deep crashes while staying more conservative in normal corrections.

3. Strategy Logic & Execution

3-1. Entry Conditions

The strategy tracks the ATH using the High price.

For each bar, it calculates the drawdown from ATH.

The user defines two drawdown zones, for example:

1st zone: ATH – 50%

2nd zone: ATH – 72.5%

For each zone, the strategy checks:

If no buy has been executed yet for that zone in the current ATH leg, and

If the current bar’s Low touches or falls below that zone’s price level,

→ That bar is considered to have triggered a buy condition.

Order simulation:

The strategy simulates entering a long position at that zone’s price level

(using a limit/market-like approximation for backtesting).

3-2. ATH Reset & Entry Opportunity Reset

When a new High goes above the previous ATH:

The ATH is updated to this new high.

Internal flags that track whether the 1st and 2nd entries have been used are reset.

This means:

Each time the market makes a new ATH,

The strategy once again has a fresh opportunity to execute 1st and 2nd drawdown entries for that new ATH leg.

4. Position Sizing & Leverage

4-1. Position Size Based on Account Equity

The strategy defines current equity as:

Current Equity = Initial Capital + Realized PnL + Unrealized PnL

For each entry zone, the position value is calculated as follows:

The user inputs:

“What % of equity to use at this zone”

The strategy:

Multiplies current equity by that percentage

Then multiplies by the strategy’s leverage factor

Thus:

Position Value = Current Equity × (Zone % / 100) × Leverage

Finally, this position value is divided by the entry price to determine the actual position size in tokens.

4-2. Exception for the First Position (100% / 300%)

For the very first position (when there is no open position),

the strategy does not use the zone % parameters. Instead, it uses fixed ratios:

Default: Enter the first position with 100% of equity.

If the drawdown from ATH at that moment is greater than or equal to a predefined threshold (e.g. –72.5% or more)

→ Enter the first position with 300% of equity.

The position value is computed as:

Position Value = Current Equity × (100% or 300%) × Leverage

Then it is divided by the entry price to obtain the token quantity.

This rule:

Applies regardless of whether the first entry occurs at the 1st zone or 2nd zone.

Embeds the philosophy:

“In very deep crashes, go much larger on the first entry; otherwise, stay more conservative.”

4-3. Tracking Real Leverage

On each bar, the strategy tracks:

The existing position size at the start of the bar

The newly added size (if any) on that bar

When a new entry occurs, it calculates the real leverage at that moment:

Real Leverage = (Position Value / Current Equity)

This is then displayed on the chart as a label, for example:

Lev 2.53x

This makes it easy to see the actual leverage level at each entry point.

5. Visualization & Monitoring

5-1. On-Chart Visual Elements

The strategy plots the following directly on the chart:

ATH Line

The all-time high (based on High) is plotted as an orange line.

Average Entry Price Line

When a position is open, the average entry price of that position is plotted as a yellow line.

Estimated Liquidation Price (Fixed) Line

The strategy detects when the position size changes.

At each size change, it uses the current average entry price and real leverage to compute an approximate liquidation price.

This “fixed liquidation price” is then plotted as a red line on the chart.

If there is no position, or if leverage is 1x or lower, the liquidation line is removed.

Entry Markers & Labels

When 1st/2nd entry conditions are met, the strategy:

Marks the entry point on the chart.

Displays labels such as "Buy XX% @ Price" and "Lev XXx",

showing both entry percentage and real leverage at that time.

The label placement is configurable:

Below Bar

Above Bar

At Price

5-2. Information Table (Top-Right Panel)

In the top-right corner of the chart, the strategy displays a summary table of the current account and position status. It typically includes:

Pos Qty (Token)

Absolute size of the current position (in tokens)

Pos Value (USDT)

Market value of the current position (qty × current price)

Leverage (Now)

Current real leverage (position value / current equity)

DD from ATH (%)

Current drawdown (%) from the latest ATH, based on current price

Avg Entry

Average entry price of the current position

PnL (%)

Unrealized profit/loss (%) of the current position

Max DD (Equity %)

The maximum equity drawdown (MDD) recorded over the entire backtest period

Last Entry Price

Average entry price immediately after the most recent add-on entry

Last Entry Lev

Real leverage at the time of the most recent entry

Liq Price (Fixed)

The fixed estimated liquidation price described above

Return from Start (%)

Total return (%) of equity compared to the initial capital

Through this table, users can quickly grasp:

Current account and position status

Current risk level

Cumulative performance

6. Time Filters & Label Options

6-1. Strategy Date Range Filter

The strategy provides an option to restrict trading to a specific time range.

When “Use Date Range” is enabled:

You can specify start and end timestamps.

The strategy will only execute trades within that range.

When this option is disabled:

The strategy operates over the entire chart history.

6-2. Entry Label Placement

Users can customize where entry/leverage labels are drawn:

Below Bar (Below Bar)

Above Bar (Above Bar)

At the actual price level (At Price)

This allows you to adjust visualization according to personal preference and chart readability.

7. Use Cases & Applications

This strategy is suitable for the following purposes:

Long-term / swing-style re-buy strategies for spot or futures long positions

Testing rule-based strategies that rely on “drawdown from ATH” as a main signal

Monitoring account leverage, liquidation price, and MDD when using leverage

Handling situations where, for a given asset:

“Every time a new ATH is formed,

you want to wait for deep corrections and enter only at specific drawdown zones”

It is generally recommended to use this strategy not as a direct plug-and-play live system, but as a tool for:

Strategy idea validation

Risk profile analysis

Parameter exploration to match your personal risk tolerance and style

8. Limitations & Warnings

Backtest results do not guarantee future performance.

They are based on historical data only.

In live markets, additional factors exist:

Liquidity

Slippage

Fee structures

Exchange-specific liquidation rules

Funding fees, etc.

The liquidation price is only an approximate estimate, derived from a simplified formula.

Actual liquidation rules, maintenance margin requirements, fees, and other details differ by exchange.

The liquidation line should be treated as a reference indicator, not an exact guarantee.

Depending on the configured leverage and entry percentages, losses can be very large.

In particular, extremely aggressive settings such as “first position 300% of equity” can greatly increase the risk of large account drawdowns and liquidation during sharp market crashes.

Use such settings with extreme caution.

For live trading, additional risk management is essential:

Your own stop-loss rules

Maximum position size limits

Portfolio-level exposure controls

And other external safety mechanisms beyond this strategy

9. Conclusion

The ATH Drawdown Re-Buy Long Only strategy goes beyond simple “buy the dip” logic. It:

Systematically utilizes drawdowns from ATH as a structural signal

Applies a special first-position rule (100% / 300%)

Integrates visualization of leverage, liquidation price, MDD, and returns

All of this supports rule-based long position building in drawdown phases and comprehensive risk monitoring.

With this strategy, users can:

Explore different:

Drawdown zones

Entry percentages

Leverage levels

Run various backtests and scenario analyses

Better understand the risk/return profile that fits their own market view and risk tolerance

Once again, this strategy is intended for research, learning, and backtesting only.

All real trading decisions and their consequences are solely the responsibility of the user.

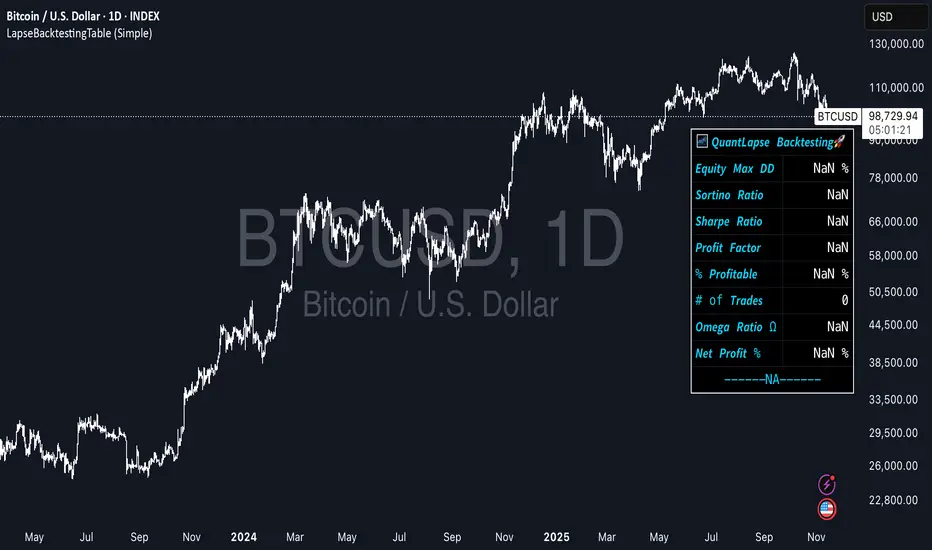

LapseBacktestingTableLibrary "LapseBacktestingMetrics"

This library provides a robust set of quantitative backtesting and performance evaluation functions for Pine Script strategies. It’s designed to help traders, quants, and developers assess risk, return, and robustness through detailed statistical metrics — including Sharpe, Sortino, Omega, drawdowns, and trade efficiency.

Built to enhance any trading strategy’s evaluation framework, this library allows you to visualize performance with the quantlapseTable() function, producing an interactive on-chart performance table.

Credit to EliCobra and BikeLife76 for original concept inspiration.

curve(disp_ind)

Retrieves a selected performance curve of your strategy.

Parameters:

disp_ind (simple string): Type of curve to plot. Options include "Equity", "Open Profit", "Net Profit", "Gross Profit".

Returns: (float) Corresponding performance curve value.

cleaner(disp_ind, plot)

Filters and displays selected strategy plots for clean visualization.

Parameters:

disp_ind (simple string): Type of display.

plot (simple float): Strategy plot variable.

Returns: (float) Filtered plot value.

maxEquityDrawDown()

Calculates the maximum equity drawdown during the strategy’s lifecycle.

Returns: (float) Maximum equity drawdown percentage.

maxTradeDrawDown()

Computes the worst intra-trade drawdown among all closed trades.

Returns: (float) Maximum intra-trade drawdown percentage.

consecutive_wins()

Finds the highest number of consecutive winning trades.

Returns: (int) Maximum consecutive wins.

consecutive_losses()

Finds the highest number of consecutive losing trades.

Returns: (int) Maximum consecutive losses.

no_position()

Counts the maximum consecutive bars where no position was held.

Returns: (int) Maximum flat days count.

long_profit()

Calculates total profit generated by long positions as a percentage of initial capital.

Returns: (float) Total long profit %.

short_profit()

Calculates total profit generated by short positions as a percentage of initial capital.

Returns: (float) Total short profit %.

prev_month()

Measures the previous month’s profit or loss based on equity change.

Returns: (float) Monthly equity delta.

w_months()

Counts the number of profitable months in the backtest.

Returns: (int) Total winning months.

l_months()

Counts the number of losing months in the backtest.

Returns: (int) Total losing months.

checktf()

Returns the time-adjusted scaling factor used in Sharpe and Sortino ratio calculations based on chart timeframe.

Returns: (float) Annualization multiplier.

stat_calc()

Performs complete statistical computation including drawdowns, Sharpe, Sortino, Omega, trade stats, and profit ratios.

Returns: (array)

.

f_colors(x, nv)

Generates a color gradient for performance values, supporting dynamic table visualization.

Parameters:

x (simple string): Metric label name.

nv (simple float): Metric numerical value.

Returns: (color) Gradient color value for table background.

quantlapseTable(option, position)

Displays an interactive Performance Table summarizing all major backtesting metrics.

Includes Sharpe, Sortino, Omega, Profit Factor, drawdowns, profitability %, and trade statistics.

Parameters:

option (simple string): Table type — "Full", "Simple", or "None".

position (simple string): Table position — "Top Left", "Middle Right", "Bottom Left", etc.

Returns: (table) On-chart performance visualization table.

This library empowers advanced quantitative evaluation directly within Pine Script®, ideal for strategy developers seeking deeper performance diagnostics and intuitive on-chart metrics.

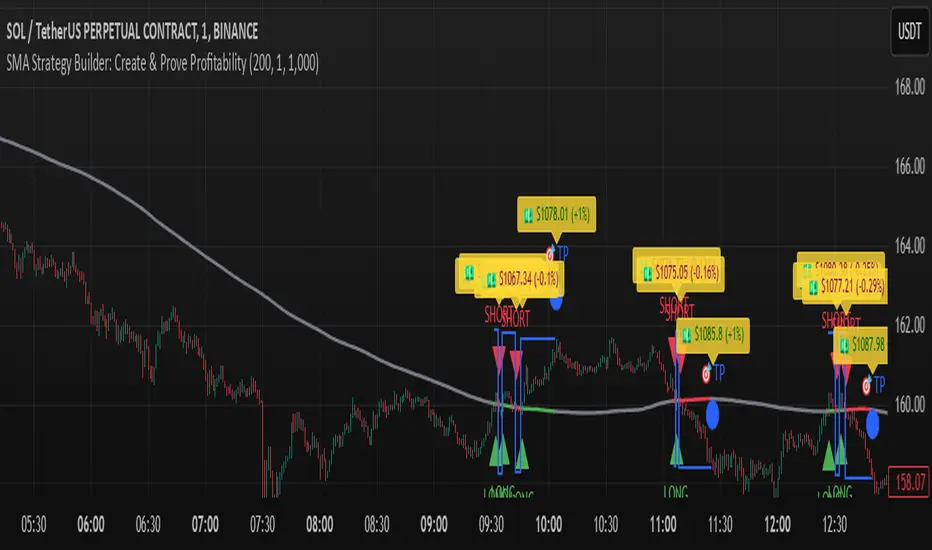

W%R Pullback+EMA Trend [TS_Indie]🔰 Core Concept of the Strategy

The main idea is “Trend-Following with Momentum Pullback.”

This means trading in the direction of the main trend (defined by EMA) while using Williams %R to identify pullback entries (buying the dip or selling the rally) where momentum returns to the trend direction.

📊 Indicators Used

1. EMA Fast – Defines the short-term trend.

2. EMA Slow – Defines the long-term trend (used as a trend filter).

3. Williams %R

• Overbought zone: above -20

• Oversold zone: below -80

⚙️ Entry Rules

🔹 Buy Setup

1. EMA Fast > EMA Slow → Uptrend condition.

2. Williams %R on the previous candle dropped below -80, and on the current candle, it crosses back above -80 → indicates momentum returning to the upside.

3. Current close is above EMA Fast.

4. Entry Buy at the close of the candle where %R crosses above -80.

🎯 Entry, Stop Loss, and Take Profit

1. Entry : At the candle close where the signal occurs.

2. Stop Loss : At the lowest low between the current and previous candles.

3. Take Profit : Calculated based on entry price and stop loss distance multiplied by the Risk/Reward Ratio.

🔹 Sell Setup

1. EMA Fast < EMA Slow → Downtrend condition.

2. Williams %R on the previous candle went above -20, and on the current candle, it crosses back below -20 → indicates renewed selling momentum.

3. Current price is below EMA Fast.

4. Entry Sell at the close of the candle where %R crosses below -20.

🎯 Entry, Stop Loss, and Take Profit

1. Entry : At the candle close where the signal occurs.

2. Stop Loss : At the highest high between the current and previous candles.

3. Take Profit : Calculated based on entry price and stop loss distance multiplied by the Risk/Reward Ratio.

⚙️ Optional Parameters

• Custom Risk/Reward Ratio for Take Profit.

• Option to add ATR buffer to Stop Loss.

• Adjustable EMA Fast period.

• Adjustable EMA Slow period.

• Adjustable Williams %R period.

• Option to enable Long only / Short only positions.

• Customizable Backtest start and end date.

• Customizable trading session time.

⏰ Alert Function

Alerts display:

• Entry price

• Stop Loss price

• Take Profit price

Guys, try adjusting the parameters yourselves!

I’ve been tweaking the settings for several days and managed to get great results on XAU/USD in the 5-minute timeframe.

I think this strategy is quite interesting and could potentially deliver good results on other instruments as well.

⚠️ Disclaimer

This indicator is designed for educational and research purposes only.

It does not guarantee profits and should not be considered financial advice.

Trading in financial markets involves significant risk, including the potential loss of capital.

Luxy BIG beautiful Dynamic ORBThis is an advanced Opening Range Breakout (ORB) indicator that tracks price breakouts from the first 5, 15, 30, and 60 minutes of the trading session. It provides complete trade management including entry signals, stop-loss placement, take-profit targets, and position sizing calculations.

The ORB strategy is based on the concept that the opening range of a trading session often acts as support/resistance, and breakouts from this range tend to lead to significant moves.

What Makes This Different?

Most ORB indicators simply draw horizontal lines and leave you to figure out the rest. This indicator goes several steps further:

Multi-Stage Tracking

Instead of just one ORB timeframe, this tracks FOUR simultaneously (5min, 15min, 30min, 60min). Each stage builds on the previous one, giving you multiple trading opportunities throughout the session.

Active Trade Management

When a breakout occurs, the indicator automatically calculates and displays entry price, stop-loss, and multiple take-profit targets. These lines extend forward and update in real-time until the trade completes.

Cycle Detection

Unlike indicators that only show the first breakout, this tracks the complete cycle: Breakout → Retest → Re-breakout. You can see when price returns to test the ORB level after breaking out (potential re-entry).

Failed Breakout Warning

If price breaks out but quickly returns inside the range (within a few bars), the label changes to "FAILED BREAK" - warning you to exit or avoid the trade.

Position Sizing Calculator

Built-in risk management that tells you exactly how many shares to buy based on your account size and risk tolerance. No more guessing or manual calculations.

Advanced Filtering

Optional filters for volume confirmation, trend alignment, and Fair Value Gaps (FVG) to reduce false signals and improve win rate.

Core Features Explained

### 1. Multi-Stage ORB Levels

The indicator builds four separate Opening Range levels:

ORB 5 - First 5 minutes (fastest signals, most volatile)

ORB 15 - First 15 minutes (balanced, most popular)

ORB 30 - First 30 minutes (slower, more reliable)

ORB 60 - First 60 minutes (slowest, most confirmed)

Each level is drawn as a horizontal range on your chart. As time progresses, the ranges expand to include more price action. You can enable or disable any stage and assign custom colors to each.

How it works: During the opening minutes, the indicator tracks the highest high and lowest low. Once the time period completes, those levels become your ORB high and low for that stage.

### 2. Breakout Detection

When price closes outside the ORB range, a label appears:

BREAK UP (green label above price) - Price closed above ORB High

BREAK DOWN (red label below price) - Price closed below ORB Low

The label shows which ORB stage triggered (ORB5, ORB15, etc.) and the cycle number if tracking multiple breakouts.

Important: Signals appear on bar close only - no repainting. What you see is what you get.

### 3. Retest Detection

After price breaks out and moves away, if it returns to test the ORB level, a "RETEST" label appears (orange). This indicates:

The original breakout level is now acting as support/resistance

Potential re-entry opportunity if you missed the first breakout

Confirmation that the level is significant

The indicator requires price to move a minimum distance away before considering it a valid retest (configurable in settings).

### 4. Failed Breakout Detection

If price breaks out but returns inside the ORB range within a few bars (before the breakout is "committed"), the original label changes to "FAILED BREAK" in orange.

This warns you:

The breakout lacked conviction

Consider exiting if already in the trade

Wait for better setup

Committed Breakout: The indicator tracks how many bars price stays outside the range. Only after staying outside for the minimum number of bars does it become a committed breakout that can be retested.

### 5. TP/SL Lines (Trade Management)

When a breakout occurs, colored horizontal lines appear showing:

Entry Line (cyan for long, orange for short) - Your entry price (the ORB level)

Stop Loss Line (red) - Where to exit if trade goes against you

TP1, TP2, TP3 Lines (same color as entry) - Profit targets at 1R, 2R, 3R

These lines extend forward as new bars form, making it easy to track your trade. When a target is hit, the line turns green and the label shows a checkmark.

Lines freeze (stop updating) when:

Stop loss is hit

The final enabled take-profit is hit

End of trading session (optional setting)

### 6. Position Sizing Dashboard

The dashboard (bottom-left corner by default) shows real-time information:

Current ORB stage and range size

Breakout status (Inside Range / Break Up / Break Down)

Volume confirmation (if filter enabled)

Trend alignment (if filter enabled)

Entry and Stop Loss prices

All enabled Take Profit levels with percentages

Risk/Reward ratio

Position sizing: Max shares to buy and total risk amount

Position Sizing Example:

If your account is $25,000 and you risk 1% per trade ($250), and the distance from entry to stop loss is $0.50, the calculator shows you can buy 500 shares (250 / 0.50 = 500).

### 7. FVG Filter (Fair Value Gap)

Fair Value Gaps are price inefficiencies - gaps left by strong momentum where one candle's high doesn't overlap with a previous candle's low (or vice versa).

When enabled, this filter:

Detects bullish and bearish FVGs

Draws semi-transparent boxes around these gaps

Only allows breakout signals if there's an FVG near the breakout level

Why this helps: FVGs indicate institutional activity. Breakouts through FVGs tend to be stronger and more reliable.

Proximity setting: Controls how close the FVG must be to the ORB level. 2.0x means the breakout can be within 2 times the FVG size - a reasonable default.

### 8. Volume & Trend Filters

Volume Filter:

Requires current volume to be above average (customizable multiplier). High volume breakouts are more likely to sustain.

Set minimum multiplier (e.g., 1.5x = 50% above average)

Set "strong volume" multiplier (e.g., 2.5x) that bypasses other filters

Dashboard shows current volume ratio

Trend Filter:

Only shows breakouts aligned with a higher timeframe trend. Choose from:

VWAP - Price above/below volume-weighted average

EMA - Price above/below exponential moving average

SuperTrend - ATR-based trend indicator

Combined modes (VWAP+EMA, VWAP+SuperTrend) for stricter filtering

### 9. Pullback Filter (Advanced)

Purpose:

Waits for price to pull back slightly after initial breakout before confirming the signal.

This reduces false breakouts from immediate reversals.

How it works:

- After breakout is detected, indicator waits for a small pullback (default 2%)

- Once pullback occurs AND price breaks out again, signal is confirmed

- If no pullback within timeout period (5 bars), signal is issued anyway

Settings:

Enable Pullback Filter: Turn this filter on/off

Pullback %: How much price must pull back (2% is balanced)

Timeout (bars): Max bars to wait for pullback (5 is standard)

When to use:

- Choppy markets with many fake breakouts

- When you want higher quality signals

- Combine with Volume filter for maximum confirmation

Trade-off:

- Better signal quality

- May miss some valid fast moves

- Slight entry delay

How to Use This Indicator

### For Beginners - Simple Setup

Add the indicator to your chart (5-minute or 15-minute timeframe recommended)

Leave all default settings - they work well for most stocks

Watch for BREAK UP or BREAK DOWN labels to appear

Check the dashboard for entry, stop loss, and targets

Use the position sizing to determine how many shares to buy

Basic Trading Plan:

Wait for a clear breakout label

Enter at the ORB level (or next candle open if you're late)

Place stop loss where the red line indicates

Take profit at TP1 (50% of position) and TP2 (remaining 50%)

### For Advanced Traders - Customized Setup

Choose which ORB stages to track (you might only want ORB15 and ORB30)

Enable filters: Volume (stocks) or Trend (trending markets)

Enable FVG filter for institutional confirmation

Set "Track Cycles" mode to catch retests and re-breakouts

Customize stop loss method (ATR for volatile stocks, ORB% for stable ones)

Adjust risk per trade and account size for accurate position sizing

Advanced Strategy Example:

Enable ORB15 only (disable others for cleaner chart)

Turn on Volume filter at 1.5x with Strong at 2.5x

Enable Trend filter using VWAP

Set Signal Mode to "Track Cycles" with Max 3 cycles

Wait for aligned breakouts (Volume + Trend + Direction)

Enter on retest if you missed the initial break

### Timeframe Recommendations

5-minute chart: Scalping, very active trading, crypto

15-minute chart: Day trading, balanced approach (most popular)

30-minute chart: Swing entries, less screen time

60-minute chart: Position trading, longer holds

The indicator works on any intraday timeframe, but ORB is fundamentally a day trading strategy. Daily charts don't make sense for ORB.

DEFAULT CONFIGURATION

ON by Default:

• All 4 ORB stages (5/15/30/60)

• Breakout Detection

• Retest Labels

• All TP levels (1/1.5/2/3)

• TP/SL Lines (Detailed mode)

• Dashboard (Bottom Left, Dark theme)

• Position Size Calculator

OFF by Default (Optional Filters):

• FVG Filter

• Pullback Filter

• Volume Filter

• Trend Filter

• HTF Bias Check

• Alerts

Recommended for Beginners:

• Leave all defaults

• Session Mode: Auto-Detect

• Signal Mode: Track Cycles

• Stop Method: ATR

• Add Volume Filter if trading stocks

Recommended for Advanced:

• Enable ORB15 + ORB30 only (disable 5 & 60)

• Enable: Volume + Trend + FVG

• Signal Mode: Track Cycles, Max 3

• Stop Method: ATR or Safer

• Enable HTF Daily bias check

## Settings Guide

The settings are organized into logical groups. Here's what each section controls:

### ORB COLORS Section

Show Edge Labels: Display "ORB 5", "ORB 15" labels at the right edge of the levels

Background: Fill the area between ORB high/low with color

Transparency: How see-through the background is (95% is nearly invisible)

Enable ORB 5/15/30/60: Turn each stage on or off individually

Colors: Assign colors to each ORB stage for easy identification

### SESSION SETTINGS Section

Session Mode: Choose trading session (Auto-Detect works for most instruments)

Custom Session Hours: Define your own hours if needed (format: HHMM-HHMM)

Auto-Detect uses the instrument's natural hours (stocks use exchange hours, crypto uses 24/7).

### BREAKOUT DETECTION Section

Enable Breakout Detection: Master switch for signals

Show Retest Labels: Display retest signals

Label Size: Visual size for all labels (Small recommended)

Enable FVG Filter: Require Fair Value Gap confirmation

Show FVG Boxes: Display the gap boxes on chart

Signal Mode: "First Only" = one signal per direction per day, "Track Cycles" = multiple signals

Max Cycles: How many breakout-retest cycles to track (6 is balanced)

Breakout Buffer: Extra distance required beyond ORB level (0.1-0.2% recommended)

Min Distance for Retest: How far price must move away before retest is valid (2% recommended)

Min Bars Outside ORB: Bars price must stay outside for committed breakout (2 is balanced)

### TARGETS & RISK Section

Enable Targets & Stop-Loss: Calculate and show trade management

TP1/TP2/TP3 checkboxes: Select which profit targets to display

Stop Method: How to calculate stop loss placement

- ATR: Based on volatility (best for most cases)

- ORB %: Fixed % of ORB range

- Swing: Recent swing high/low

- Safer: Widest of all methods

ATR Length & Multiplier: Controls ATR stop distance (14 period, 1.5x is standard)

ORB Stop %: Percentage beyond ORB for stop (20% is balanced)

Swing Bars: Lookback period for swing high/low (3 is recent)

### TP/SL LINES Section

Show TP/SL Lines: Display horizontal lines on chart

Label Format: "Short" = minimal text, "Detailed" = shows prices

Freeze Lines at EOD: Stop extending lines at session close

### DASHBOARD Section

Show Info Panel: Display the metrics dashboard

Theme: Dark or Light colors

Position: Where to place dashboard on chart

Toggle rows: Show/hide specific information rows

Calculate Position Size: Enable the position sizing calculator

Risk Mode: Risk fixed $ amount or % of account

Account Size: Your total trading capital

Risk %: Percentage to risk per trade (0.5-1% recommended)

### VOLUME FILTER Section

Enable Volume Filter: Require volume confirmation

MA Length: Average period (20 is standard)

Min Volume: Required multiplier (1.5x = 50% above average)

Strong Volume: Multiplier that bypasses other filters (2.5x)

### TREND FILTER Section

Enable Trend Filter: Require trend alignment

Trend Mode: Method to determine trend (VWAP is simple and effective)

Custom EMA Length: If using EMA mode (50 for swing, 20 for day trading)

SuperTrend settings: Period and Multiplier if using SuperTrend mode

### HIGHER TIMEFRAME Section

Check Daily Trend: Display higher timeframe bias in dashboard

Timeframe: What TF to check (D = daily, recommended)

Method: Price vs MA (stable) or Candle Direction (reactive)

MA Period: EMA length for Price vs MA method (20 is balanced)

Min Strength %: Minimum strength threshold for HTF bias to be considered

- For "Price vs MA": Minimum distance (%) from moving average

- For "Candle Direction": Minimum candle body size (%)

- 0.5% is balanced - increase for stricter filtering

- Lower values = more signals, higher values = only strong trends

### ALERTS Section

Enable Alerts: Master switch (must be ON to use any alerts)

Breakout Alerts: Notify on ORB breakouts

Retest Alerts: Notify when price retests after breakout

Failed Break Alerts: Notify on failed breakouts

Stage Complete Alerts: Notify when each ORB stage finishes forming

After enabling desired alert types, click "Create Alert" button, select this indicator, choose "Any alert() function call".

## Tips & Best Practices

### General Trading Tips

ORB works best on liquid instruments (stocks with good volume, major crypto pairs)

First hour of the session is most important - that's when ORB is forming

Breakouts WITH the trend have higher success rates - use the trend filter

Failed breakouts are common - use the "Min Bars Outside" setting to filter weak moves

Not every day produces good ORB setups - be patient and selective

### Position Sizing Best Practices

Never risk more than 1-2% of your account on a single trade

Use the built-in calculator - don't guess your position size

Update your account size monthly as it grows

Smaller accounts: use $ Amount mode for simplicity

Larger accounts: use % of Account mode for scaling

### Take Profit Strategy

Most traders use: 50% at TP1, 50% at TP2

Aggressive: Hold through TP1 for TP2 or TP3

Conservative: Full exit at TP1 (1:1 risk/reward)

After TP1 hits, consider moving stop to breakeven

TP3 rarely hits - only on strong trending days

### Filter Combinations

Maximum Quality: Volume + Trend + FVG (fewest signals, highest quality)

Balanced: Volume + Trend (good quality, reasonable frequency)

Active Trading: No filters or Volume only (many signals, lower quality)

Trending Markets: Trend filter essential (indices, crypto)

Range-Bound: Volume + FVG (avoid trend filter)

### Common Mistakes to Avoid

Chasing breakouts - wait for the bar to close, don't FOMO into wicks

Ignoring the stop loss - always use it, move it manually if needed

Over-leveraging - the calculator shows MAX shares, you can buy less

Trading every signal - quality > quantity, use filters

Not tracking results - keep a journal to see what works for YOU

## Pros and Cons

### Advantages

Complete all-in-one solution - from signal to position sizing

Multiple timeframes tracked simultaneously

Visual clarity - easy to see what's happening

Cycle tracking catches opportunities others miss

Built-in risk management eliminates guesswork

Customizable filters for different trading styles

No repainting - what you see is locked in

Works across multiple markets (stocks, forex, crypto)

### Limitations

Intraday strategy only - doesn't work on daily charts

Requires active monitoring during first 1-2 hours of session

Not suitable for after-hours or extended sessions by default

Can produce many signals in choppy markets (use filters)

Dashboard can be overwhelming for complete beginners

Performance depends on market conditions (trends vs ranges)

Requires understanding of risk management concepts

### Best For

Day traders who can watch the first 1-2 hours of market open

Traders who want systematic entry/exit rules

Those learning proper position sizing and risk management

Active traders comfortable with multiple signals per day

Anyone trading liquid instruments with clear sessions

### Not Ideal For

Swing traders holding multi-day positions

Set-and-forget / passive investors

Traders who can't watch market open

Complete beginners unfamiliar with trading concepts

Low volume / illiquid instruments

## Frequently Asked Questions

Q: Why are no signals appearing?

A: Check that you're on an intraday timeframe (5min, 15min, etc.) and that the current time is within your session hours. Also verify that "Enable Breakout Detection" is ON and at least one ORB stage is enabled. If using filters, they might be blocking signals - try disabling them temporarily.

Q: What's the best ORB stage to use?

A: ORB15 (15 minutes) is most popular and balanced. ORB5 gives faster signals but more noise. ORB30 and ORB60 are slower but more reliable. Many traders use ORB15 + ORB30 together.

Q: Should I enable all the filters?

A: Start with no filters to see all signals. If too many false signals, add Volume filter first (stocks) or Trend filter (trending markets). FVG filter is most restrictive - use for maximum quality but fewer signals.

Q: How do I know which stop loss method to use?

A: ATR works for most cases - it adapts to volatility. Use ORB% if you want predictable stop placement. Swing is for respecting chart structure. Safer gives you the most room but largest risk.

Q: Can I use this for swing trading?

A: Not really - ORB is fundamentally an intraday strategy. The ranges reset each day. For swing trading, look at weekly support/resistance or moving averages instead.

Q: Why do TP/SL lines disappear sometimes?

A: Lines freeze (stop extending) when: stop loss is hit, the last enabled take-profit is hit, or end of session arrives (if "Freeze at EOD" is enabled). This is intentional - the trade is complete.

Q: What's the difference between "First Only" and "Track Cycles"?

A: "First Only" shows one breakout UP and one DOWN per day maximum - clean but might miss opportunities. "Track Cycles" shows breakout-retest-rebreak sequences - more signals but busier chart.

Q: Is position sizing accurate for options/forex?

A: The calculator is designed for shares (stocks). For options, ignore the share count and use the risk amount. For forex, you'll need to adapt the lot size calculation manually.

Q: How much capital do I need to use this?

A: The indicator works for any account size, but practical day trading typically requires $25,000 in the US due to Pattern Day Trader rules. Adjust the "Account Size" setting to match your capital.

Q: Can I backtest this strategy?

A: This is an indicator, not a strategy script, so it doesn't have built-in backtesting. You can visually review historical signals or code a strategy script using similar logic.

Q: Why does the dashboard show different entry price than the breakout label?

A: If you're looking at an old breakout, the ORB levels may have changed when the next stage completed. The dashboard always shows the CURRENT active range and trade setup.

Q: What's a good win rate to expect?

A: ORB strategies typically see 40-60% win rate depending on market conditions and filters used. The strategy relies on positive risk/reward ratios (2:1 or better) to be profitable even with moderate win rates.

Q: Does this work on crypto?

A: Yes, but crypto trades 24/7 so you need to define what "session start" means. Use Session Mode = Custom and set your preferred daily reset time (e.g., 0000-2359 UTC).

## Credits & Transparency

### Development

This indicator was developed with the assistance of AI technology to implement complex ORB trading logic.

The strategy concept, feature specifications, and trading logic were designed by the publisher. The implementation leverages modern development tools to ensure:

Clean, efficient, and maintainable code

Comprehensive error handling and input validation

Detailed documentation and user guidance

Performance optimization

### Trading Concepts

This indicator implements several public domain trading concepts:

Opening Range Breakout (ORB): Trading strategy popularized by Toby Crabel, Mark Fisher and many more talanted traders.

Fair Value Gap (FVG): Price imbalance concept from ICT methodology

SuperTrend: ATR-based trend indicator using public formula

Risk/Reward Ratio: Standard risk management principle

All mathematical formulas and technical concepts used are in the public domain.

### Pine Script

Uses standard TradingView built-in functions:

ta.ema(), ta.atr(), ta.vwap(), ta.highest(), ta.lowest(), request.security()

No external libraries or proprietary code from other authors.

## Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice.

Trading involves substantial risk of loss and is not suitable for every investor. Past performance shown in examples is not indicative of future results.

The indicator provides signals and calculations, but trading decisions are solely your responsibility. Always:

Test strategies on paper before using real money

Never risk more than you can afford to lose

Understand that all trading involves risk

Consider seeking advice from a licensed financial advisor

The publisher makes no guarantees regarding accuracy, profitability, or performance. Use at your own risk.

---

Version: 3.0

Pine Script Version: v6

Last Updated: October 2024

For support, questions, or suggestions, please comment below or send a private message.

---

Happy trading, and remember: consistent risk management beats perfect entry timing every time.

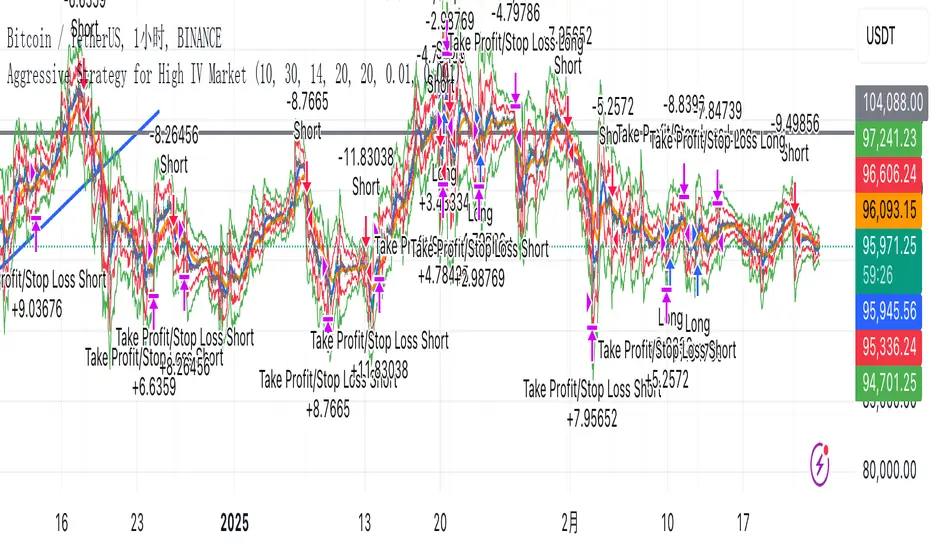

Zero Lag Trend Signals (MTF) [Quant Trading] V7Overview

The Zero Lag Trend Signals (MTF) V7 is a comprehensive trend-following strategy that combines Zero Lag Exponential Moving Average (ZLEMA) with volatility-based bands to identify high-probability trade entries and exits. This strategy is designed to reduce lag inherent in traditional moving averages while incorporating dynamic risk management through ATR-based stops and multiple exit mechanisms.

This is a longer term horizon strategy that takes limited trades. It is not a high frequency trading and therefore will also have limited data and not > 100 trades.

How It Works

Core Signal Generation:

The strategy uses a Zero Lag EMA (ZLEMA) calculated by applying an EMA to price data that has been adjusted for lag:

Calculate lag period: floor((length - 1) / 2)

Apply lag correction: src + (src - src )

Calculate ZLEMA: EMA of lag-corrected price

Volatility bands are created using the highest ATR over a lookback period multiplied by a band multiplier. These bands are added to and subtracted from the ZLEMA line to create upper and lower boundaries.

Trend Detection:

The strategy maintains a trend variable that switches between bullish (1) and bearish (-1):

Long Signal: Triggers when price crosses above ZLEMA + volatility band

Short Signal: Triggers when price crosses below ZLEMA - volatility band

Optional ZLEMA Trend Confirmation:

When enabled, this filter requires ZLEMA to show directional momentum before entry:

Bullish Confirmation: ZLEMA must increase for 4 consecutive bars

Bearish Confirmation: ZLEMA must decrease for 4 consecutive bars

This additional filter helps avoid false signals in choppy or ranging markets.

Risk Management Features:

The strategy includes multiple stop-loss and take-profit mechanisms:

Volatility-Based Stops: Default stop-loss is placed at ZLEMA ± volatility band

ATR-Based Stops: Dynamic stop-loss calculated as entry price ± (ATR × multiplier)

ATR Trailing Stop: Ratcheting stop-loss that follows price but never moves against position

Risk-Reward Profit Target: Take-profit level set as a multiple of stop distance

Break-Even Stop: Moves stop to entry price after reaching specified R:R ratio

Trend-Based Exit: Closes position when price crosses EMA in opposite direction

Performance Tracking:

The strategy includes optional features for monitoring and analyzing trades:

Floating Statistics Table: Displays key metrics including win rate, GOA (Gain on Account), net P&L, and max drawdown

Trade Log Labels: Shows entry/exit prices, P&L, bars held, and exit reason for each closed trade

CSV Export Fields: Outputs trade data for external analysis

Default Strategy Settings

Commission & Slippage:

Commission: 0.1% per trade

Slippage: 3 ticks

Initial Capital: $1,000

Position Size: 100% of equity per trade

Main Calculation Parameters:

Length: 70 (range: 70-7000) - Controls ZLEMA calculation period

Band Multiplier: 1.2 - Adjusts width of volatility bands

Entry Conditions (All Disabled by Default):

Use ZLEMA Trend Confirmation: OFF - Requires ZLEMA directional momentum

Re-Enter on Long Trend: OFF - Allows multiple entries during sustained trends

Short Trades:

Allow Short Trades: OFF - Strategy is long-only by default

Performance Settings (All Disabled by Default):

Use Profit Target: OFF

Profit Target Risk-Reward Ratio: 2.0 (when enabled)

Dynamic TP/SL (All Disabled by Default):

Use ATR-Based Stop-Loss & Take-Profit: OFF

ATR Length: 14

Stop-Loss ATR Multiplier: 1.5

Profit Target ATR Multiplier: 2.5

Use ATR Trailing Stop: OFF

Trailing Stop ATR Multiplier: 1.5

Use Break-Even Stop-Loss: OFF

Move SL to Break-Even After RR: 1.5

Use Trend-Based Take Profit: OFF

EMA Exit Length: 9

Trade Data Display (All Disabled by Default):

Show Floating Stats Table: OFF

Show Trade Log Labels: OFF

Enable CSV Export: OFF

Trade Label Vertical Offset: 0.5

Backtesting Date Range:

Start Date: January 1, 2018

End Date: December 31, 2069

Important Usage Notes

Default Configuration: The strategy operates in its most basic form with default settings - using only ZLEMA crossovers with volatility bands and volatility-based stop-losses. All advanced features must be manually enabled.

Stop-Loss Priority: If multiple stop-loss methods are enabled simultaneously, the strategy will use whichever condition is hit first. ATR-based stops override volatility-based stops when enabled.

Long-Only by Default: Short trading is disabled by default. Enable "Allow Short Trades" to trade both directions.

Performance Monitoring: Enable the floating stats table and trade log labels to visualize strategy performance during backtesting.

Exit Mechanisms: The strategy can exit trades through multiple methods: stop-loss hit, take-profit reached, trend reversal, or trailing stop activation. The trade log identifies which exit method was used.

Re-Entry Logic: When "Re-Enter on Long Trend" is enabled with ZLEMA trend confirmation, the strategy can take multiple long positions during extended uptrends as long as all entry conditions remain valid.

Capital Efficiency: Default setting uses 100% of equity per trade. Adjust "default_qty_value" to manage position sizing based on risk tolerance.

Realistic Backtesting: Strategy includes commission (0.1%) and slippage (3 ticks) to provide realistic performance expectations. These values should be adjusted based on your broker and market conditions.

Recommended Use Cases

Trending Markets: Best suited for markets with clear directional moves where trend-following strategies excel

Medium to Long-Term Trading: The default length of 70 makes this strategy more appropriate for swing trading rather than scalping

Risk-Conscious Traders: Multiple stop-loss options allow traders to customize risk management to their comfort level

Backtesting & Optimization: Comprehensive performance tracking features make this strategy ideal for testing different parameter combinations

Limitations & Considerations

Like all trend-following strategies, performance may suffer in choppy or ranging markets

Default 100% position sizing means full capital exposure per trade - consider reducing for conservative risk management

Higher length values (70+) reduce signal frequency but may improve signal quality

Multiple simultaneous risk management features may create conflicting exit signals

Past performance shown in backtests does not guarantee future results

Customization Tips

For more aggressive trading:

Reduce length parameter (minimum 70)

Decrease band multiplier for tighter bands

Enable short trades

Use lower profit target R:R ratios

For more conservative trading:

Increase length parameter

Enable ZLEMA trend confirmation

Use wider ATR stop-loss multipliers

Enable break-even stop-loss

Reduce position size from 100% default

For optimal choppy market performance:

Enable ZLEMA trend confirmation

Increase band multiplier

Use tighter profit targets

Avoid re-entry on trend continuation

Visual Elements

The strategy plots several elements on the chart:

ZLEMA line (color-coded by trend direction)

Upper and lower volatility bands

Long entry markers (green triangles)

Short entry markers (red triangles, when enabled)

Stop-loss levels (when positions are open)

Take-profit levels (when enabled and positions are open)

Trailing stop lines (when enabled and positions are open)

Optional ZLEMA trend markers (triangles at highs/lows)

Optional trade log labels showing complete trade information

Exit Reason Codes (for CSV Export)

When CSV export is enabled, exit reasons are coded as:

0 = Manual/Other

1 = Trailing Stop-Loss

2 = Profit Target

3 = ATR Stop-Loss

4 = Trend Change

Conclusion

Zero Lag Trend Signals V7 provides a robust framework for trend-following with extensive customization options. The strategy balances simplicity in its core logic with sophisticated risk management features, making it suitable for both beginner and advanced traders. By reducing moving average lag while incorporating volatility-based signals, it aims to capture trends earlier while managing risk through multiple configurable exit mechanisms.

The modular design allows traders to start with basic trend-following and progressively add complexity through ZLEMA confirmation, multiple stop-loss methods, and advanced exit strategies. Comprehensive performance tracking and export capabilities make this strategy an excellent tool for systematic testing and optimization.

Note: This strategy is provided for educational and backtesting purposes. All trading involves risk. Past performance does not guarantee future results. Always test thoroughly with paper trading before risking real capital, and adjust position sizing and risk parameters according to your risk tolerance and account size.

================================================================================

TAGS:

================================================================================

trend following, ZLEMA, zero lag, volatility bands, ATR stops, risk management, swing trading, momentum, trend confirmation, backtesting

================================================================================

CATEGORY:

================================================================================

Strategies

================================================================================

CHART SETUP RECOMMENDATIONS:

================================================================================

For optimal visualization when publishing:

Use a clean chart with no other indicators overlaid

Select a timeframe that shows multiple trade signals (4H or Daily recommended)

Choose a trending asset (crypto, forex major pairs, or trending stocks work well)

Show at least 6-12 months of data to demonstrate strategy across different market conditions

Enable the floating stats table to display key performance metrics

Ensure all indicator lines (ZLEMA, bands, stops) are clearly visible

Use the default chart type (candlesticks) - avoid Heikin Ashi, Renko, etc.

Make sure symbol information and timeframe are clearly visible

================================================================================

COMPLIANCE NOTES:

================================================================================

✅ Open-source publication with complete code visibility

✅ English-only title and description

✅ Detailed explanation of methodology and calculations

✅ Realistic commission (0.1%) and slippage (3 ticks) included

✅ All default parameters clearly documented

✅ Performance limitations and risks disclosed

✅ No unrealistic claims about performance

✅ No guaranteed results promised

✅ Appropriate for public library (original trend-following implementation with ZLEMA)

✅ Educational disclaimers included

✅ All features explained in detail

================================================================================

3-1-2 Strat Combo by NaturalBelleThe 3-1-2 Strat Combo by NaturalBelle automatically detects and highlights one of The Strat’s most powerful reversal patterns — the 3-1-2 setup.

When a 3 (outside bar) is followed by a 1 (inside bar) and then a 2 that breaks direction, this script plots yellow triangles and draws yellow box zones across the sequence, giving traders a clean visual cue for potential reversals or continuations.

Features:

Highlights both bullish (3-1-2-Up) and bearish (3-1-2-Down) sequences

Draws yellow boxes covering the 3-1-2 structure for easy zone recognition

Optional text labels for clarity

Adjustable box extension and transparency

Built-in alert conditions for both up and down setups

This clean, no-clutter version focuses purely on price action — no indicators, no noise. Just the pattern.

🟡 Best used on: Any timeframe

🟡 Strategy: Combine with market structure, EMAs, or supply & demand zones for confirmation

Created by NaturalBelle — keeping Strat analysis simple, visual, and precise.

LBM-Strategy Engine Pro: The Ultimate Confluence IndicatorOverview

Welcome to the Strategy Engine Pro , the ultimate confluence indicator designed for traders who demand precision and full control over their trading signals. This is not just an indicator; it is a complete, customizable strategy-building framework.

It seamlessly integrates three powerful concepts into a single, intuitive tool:

Advanced Moving Average Trend Analysis to define the market context.

An intelligent Support & Resistance Cycle Engine to identify key price levels.

A flexible 10-rule Strategy Builder that lets you design, test, and refine your own entry signals with surgical precision.

Core Features

1. Advanced Moving Average Trend Analysis

The indicator plots 5 fully configurable Moving Averages (MAs). You can choose the Period and Type (SMA, EMA, WMA, HMA, RMA) for each one. But its true power lies in its unique color-coding system, which analyzes the slope and momentum of each MA, not just its price.

MA Color Code:

Green: The MA is in a strong, confirmed uptrend.

Red: The MA is in a strong, confirmed downtrend.

Yellow: The MA is flat or in a transitional (sideways) phase.

This provides an instant visual snapshot of the market trend across five different timeframes.

2. Support & Resistance Cycle Engine

Forget simple pivot points. This indicator incorporates a sophisticated engine that identifies and plots significant "Master Cycle" levels on your chart.

Anchored Levels: These S/R lines are persistent and intelligent. When a key resistance level is broken, it automatically "flips" and becomes the new anchored support level, and vice-versa. This accurately maps out the market's structural progression.

The Strategy Builder: Your Personal Trading Lab

This is the heart of the indicator. You have 10 sequential rules that allow you to define the exact conditions for a Buy signal. The Sell signal is generated as the logical, symmetrical opposite.

For each rule, you can configure:

Source A & Source B: Choose from a wide range of data points:

Price values: Close, Open, High, Low.

Previous candle values: Close Before, Open Before, etc.

Moving Average values: MA 1 through MA 5.

MA Trend Colors: MA 1 Color, MA 2 Color Before, etc.

Operator: Define the comparison logic:

Standard: >, <, >=, <=

Events: Crossover, Crossunder

Color Logic: Is Color, Is NOT Color, Turned Color, Ceased to be Color

Important Note on Sell Signals: Sell conditions are designed to be the symmetrical opposite of the buy conditions you create.

If Buy is Close > MA 1, Sell will be Close < MA 1.

If Buy is MA 1 Color Is Green, Sell will be MA 1 Color Is Red.

If Buy is MA 1 Color Turned Green, Sell will be MA 1 Color Turned Red.

This ensures your sell strategy mirrors the logic of your buy strategy, preventing the "inverse problem" of getting sell signals on every candle that isn't a buy signal.

Mastering the Connectors: ( ) AND and ( ) OR

The true power of the Strategy Builder lies in its connectors, which allow you to create complex, multi-layered logic. The connector on a rule defines how it connects to the next active rule.

AND & OR: These work as you'd expect, creating a continuous chain of conditions.

Rule 1 (AND) & Rule 2 is evaluated as (R1 AND R2).

( ) OR (The Group Separator): This is your most powerful tool. It acts like closing a parenthesis in an equation. It finalizes the current group of rules and connects it to the

next group with a big "OR".

Example: (R1 AND R2) OR (R3 AND R4)

This creates two possible paths for a signal.

- Rule 1: Condition R1, Connector AND

- Rule 2: Condition R2, Connector ( ) OR <-- This closes the first group and links to the next with OR.

- Rule 3: Condition R3, Connector AND

- Rule 4: Condition R4

( ) AND (The Super-Filter): This allows you to create a "master" condition that must be true in addition to other complex conditions.

Example: (R1 OR R2) AND (R3 OR R4)

This requires a condition from the first group and a condition from the second group to be true.

- Rule 1: Condition R1, Connector OR

- Rule 2: Condition R2, Connector ( ) AND <-- This closes the first OR group and links to the next with AND.

- Rule 3: Condition R3, Connector OR

- Rule 4: Condition R4

By strategically combining these connectors, you can build any logical trading scenario you can imagine. We look forward to seeing the powerful strategies the community creates with this engine.

Enhanced Ichimoku Cloud Strategy V1 [Quant Trading]Overview

This strategy combines the powerful Ichimoku Kinko Hyo system with a 171-period Exponential Moving Average (EMA) filter to create a robust trend-following approach. The strategy is designed for traders seeking to capitalize on strong momentum moves while using the Ichimoku cloud structure to identify optimal entry and exit points.

This is a patient, low-frequency trading system that prioritizes quality over quantity. In backtesting on Solana, the strategy achieved impressive results with approximately 3600% profit over just 29 trades, demonstrating its effectiveness at capturing major trend movements rather than attempting to profit from every market fluctuation. The extended parameters and strict entry criteria are specifically optimized for Solana's price action characteristics, making it well-suited for traders who prefer fewer, higher-conviction positions over high-frequency trading approaches.

What Makes This Strategy Original

This implementation enhances the traditional Ichimoku system by:

Custom Ichimoku Parameters: Uses non-standard periods (Conversion: 7, Base: 211, Lagging Span 2: 120, Displacement: 41) optimized for different market conditions

EMA Confirmation Filter: Incorporates a 171-period EMA as an additional trend confirmation layer

State Memory System: Implements a sophisticated memory system to track buy/sell states and prevent false signals

Dual Trade Modes: Offers both traditional Ichimoku signals ("Ichi") and cloud-based signals ("Cloud")

Breakout Confirmation: Requires price to break above the 25-period high for long entries

How It Works

Core Components

Ichimoku Elements:

-Conversion Line (Tenkan-sen): 7-period Donchian midpoint

-Base Line (Kijun-sen): 211-period Donchian midpoint

-Span A (Senkou Span A): Average of Conversion and Base lines, plotted 41 periods ahead

-Span B (Senkou Span B): 120-period Donchian midpoint, plotted 41 periods ahead

-Lagging Span (Chikou Span): Current close plotted 41 periods back

EMA Filter: 171-period EMA acts as a long-term trend filter

Entry Logic (Ichi Mode - Default)

A long position is triggered when ALL conditions are met:

Cloud Bullish: Span A > Span B (41 periods ago)

Breakout Confirmation: Current close > 25-period high

Ichimoku Bullish: Conversion Line > Base Line

Trend Alignment: Current close > 171-period EMA

State Memory: No previous buy signal is still active

Exit Logic

Positions are closed when:

Ichimoku Bearish: Conversion Line < Base Line

Alternative Cloud Mode

When "Cloud" mode is selected, the strategy uses:

Entry: Span A crosses above Span B with additional cloud and EMA confirmations

Exit: Span A crosses below Span B with cloud and EMA confirmations

Default Settings Explained

Strategy Properties

Initial Capital: $1,000 (realistic for average traders)

Position Size: 100% of equity (appropriate for backtesting single-asset strategies)

Commission: 0.1% (realistic for most brokers)

Slippage: 3 ticks (accounts for realistic execution costs)

Date Range: January 1, 2018 to December 31, 2069

Key Parameters

Conversion Periods: 7 (faster than traditional 9, more responsive to price changes)

Base Periods: 211 (much longer than traditional 26, provides stronger trend confirmation)

Lagging Span 2 Periods: 120 (custom period for stronger support/resistance levels)

Displacement: 41 (projects cloud further into future than standard 26)

EMA Period: 171 (long-term trend filter, approximately 8.5 months of daily data)

How to Use This Strategy