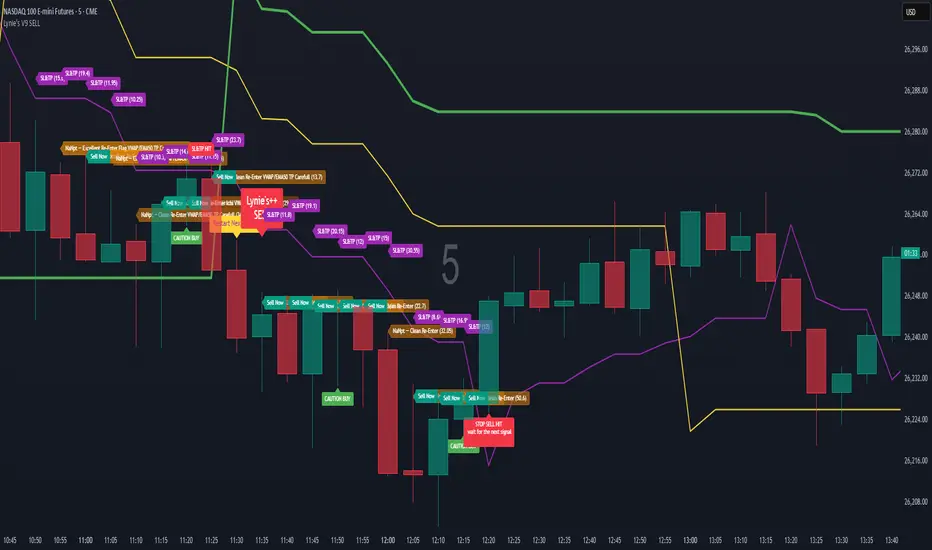

Multi-Step FlexiMA - Strategy [presentTrading]It's time to come back! hope I can not to be busy for a while.

█ Introduction and How It Is Different

The FlexiMA Variance Tracker is a unique trading strategy that calculates a series of deviations between the price (or another indicator source) and a variable-length moving average (MA). Unlike traditional strategies that use fixed-length moving averages, the length of the MA in this system varies within a defined range. The length changes dynamically based on a starting factor and an increment factor, creating a more adaptive approach to market conditions.

This strategy integrates Multi-Step Take Profit (TP) levels, allowing for partial exits at predefined price increments. It enables traders to secure profits at different stages of a trend, making it ideal for volatile markets where taking full profits at once might lead to missed opportunities if the trend continues.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

🔶 FlexiMA Concept

The FlexiMA (Flexible Moving Average) is at the heart of this strategy. Unlike traditional MA-based strategies where the MA length is fixed (e.g., a 50-period SMA), the FlexiMA varies its length with each iteration. This is done using a **starting factor** and an **increment factor**.

The formula for the moving average length at each iteration \(i\) is:

`MA_length_i = indicator_length * (starting_factor + i * increment_factor)`

Where:

- `indicator_length` is the user-defined base length.

- `starting_factor` is the initial multiplier of the base length.

- `increment_factor` increases the multiplier in each iteration.

Each iteration applies a **simple moving average** (SMA) to the chosen **indicator source** (e.g., HLC3) with a different length based on the above formula. The deviation between the current price and the moving average is then calculated as follows:

`deviation_i = price_current - MA_i`

These deviations are normalized using one of the following methods:

- **Max-Min normalization**:

`normalized_i = (deviation_i - min(deviations)) / range(deviations)`

- **Absolute Sum normalization**:

`normalized_i = deviation_i / sum(|deviation_i|)`

The **median** and **standard deviation (stdev)** of the normalized deviations are then calculated as follows:

`median = median(normalized deviations)`

For the standard deviation:

`stdev = sqrt((1/(N-1)) * sum((normalized_i - mean)^2))`

These values are plotted to provide a clear indication of how the price is deviating from its variable-length moving averages.

For more detail:

🔶 Multi-Step Take Profit

This strategy uses a multi-step take profit system, allowing for exits at different stages of a trade based on the percentage of price movement. Three take-profit levels are defined:

- Take Profit Level 1 (TP1): A small, quick profit level (e.g., 2%).

- Take Profit Level 2 (TP2): A medium-level profit target (e.g., 8%).

- Take Profit Level 3 (TP3): A larger, more ambitious target (e.g., 18%).

At each level, a corresponding percentage of the trade is exited:

- TP Percent 1: E.g., 30% of the position.

- TP Percent 2: E.g., 20% of the position.

- TP Percent 3: E.g., 15% of the position.

This approach ensures that profits are locked in progressively, reducing the risk of market reversals wiping out potential gains.

Local

🔶 Trade Entry and Exit Conditions

The entry and exit signals are determined by the interaction between the **SuperTrend Polyfactor Oscillator** and the **median** value of the normalized deviations:

- Long entry: The SuperTrend turns bearish, and the median value of the deviations is positive.

- Short entry: The SuperTrend turns bullish, and the median value is negative.

Similarly, trades are exited when the SuperTrend flips direction.

* The SuperTrend Toolkit is made by @EliCobra

█ Trade Direction

The strategy allows users to specify the desired trade direction:

- Long: Only long positions will be taken.

- Short: Only short positions will be taken.

- Both: Both long and short positions are allowed based on the conditions.

This flexibility allows the strategy to adapt to different market conditions and trading styles, whether you're looking to buy low and sell high, or sell high and buy low.

█ Usage

This strategy can be applied across various asset classes, including stocks, cryptocurrencies, and forex. The primary use case is to take advantage of market volatility by using a flexible moving average and multiple take-profit levels to capture profits incrementally as the market moves in your favor.

How to Use:

1. Configure the Inputs: Start by adjusting the **Indicator Length**, **Starting Factor**, and **Increment Factor** to suit your chosen asset. The defaults work well for most markets, but fine-tuning them can improve performance.

2. Set the Take Profit Levels: Adjust the three **TP levels** and their corresponding **percentages** based on your risk tolerance and the expected volatility of the market.

3. Monitor the Strategy: The SuperTrend and the FlexiMA variance tracker will provide entry and exit signals, automatically managing the positions and taking profits at the pre-set levels.

█ Default Settings

The default settings for the strategy are configured to provide a balanced approach that works across different market conditions:

Indicator Length (10):

This controls the base length for the moving average. A lower length makes the moving average more responsive to price changes, while a higher length smooths out fluctuations, making the strategy less sensitive to short-term price movements.

Starting Factor (1.0):

This determines the initial multiplier applied to the moving average length. A higher starting factor will increase the average length, making it slower to react to price changes.

Increment Factor (1.0):

This increases the moving average length in each iteration. A larger increment factor creates a wider range of moving average lengths, allowing the strategy to track both short-term and long-term trends simultaneously.

Normalization Method ('None'):

Three methods of normalization can be applied to the deviations:

- None: No normalization applied, using raw deviations.

- Max-Min: Normalizes based on the range between the maximum and minimum deviations.

- Absolute Sum: Normalizes based on the total sum of absolute deviations.

Take Profit Levels:

- TP1 (2%): A quick exit to capture small price movements.

- TP2 (8%): A medium-term profit target for stronger trends.

- TP3 (18%): A long-term target for strong price moves.

Take Profit Percentages:

- TP Percent 1 (30%): Exits 30% of the position at TP1.

- TP Percent 2 (20%): Exits 20% of the position at TP2.

- TP Percent 3 (15%): Exits 15% of the position at TP3.

Effect of Variables on Performance:

- Short Indicator Lengths: More responsive to price changes but prone to false signals.

- Higher Starting Factor: Slows down the response, useful for longer-term trend following.

- Higher Increment Factor: Widens the variability in moving average lengths, making the strategy adapt to both short-term and long-term price trends.

- Aggressive Take Profit Levels: Allows for quick profit-taking in volatile markets but may exit positions prematurely in strong trends.

The default configuration offers a moderate balance between short-term responsiveness and long-term trend capturing, suitable for most traders. However, users can adjust these variables to optimize performance based on market conditions and personal preferences.

Cari dalam skrip untuk "tp"

ICT Silver Bullet | Flux Charts💎 GENERAL OVERVIEW

Introducing our new ICT Silver Bullet Indicator! This indicator is built around the ICT's "Silver Bullet" strategy. The strategy has 5 steps for execution and works best in 1-5 min timeframes. For more information about the process, check the "HOW DOES IT WORK" section.

Features of the new ICT Silver Bullet Indicator :

Implementation of ICT's Silver Bullet Strategy

Customizable Execution Settings

2 NY Sessions & London Session

Customizable Backtesting Dashboard

Alerts for Buy, Sell, TP & SL Signals

📌 HOW DOES IT WORK ?

ICT's Silver Bullet strategy has 5 steps :

1. Mark your market sessions open (This indicator has 3 -> NY 10-11, NY 14-15, LDN 03-04)

2. Mark the swing liquidity points

3. Wait for market to take down one liquidity side

4. Look for a market structure-shift for reversals

5. Wait for a FVG for execution

This indicator follows these steps and inform you step by step by plotting them in your chart. You can switch execution types between FVG and MSS.

🚩UNIQUENESS

This indicator is an all-in-one suit for the ICT's Silver Bullet concept. It's capable of plotting the strategy, giving signals, a backtesting dashboard and alerts feature. It's designed for simplyfing a rather complex strategy, helping you to execute it with clean signals. The backtesting dashboard allows you to see how your settings perform in the current ticker. You can also set up alerts to get informed when the strategy is executable for different tickers.

⚙️SETTINGS

1. General Configuration

Execution Type -> FVG execution type will require a FVG to take an entry, while the MSS setting will take an entry as soon as it detects a market structure-shift.

MSS Swing Length -> The swing length when finding liquidity zones for market structure-shift detection.

Breakout Method -> If "Wick" is selected, a bar wick will be enough to confirm a market structure-shift. If "Close" is selected, the bar must close above / below the liquidity zone to confirm a market structure-shift.

FVG Detection -> "Same Type" means that all 3 bars that formed the FVG should be the same type. (Bullish / Bearish). "All" means that bar types may vary between bullish / bearish.

FVG Detection Sensitivity -> You can turn this setting on and off. If it's off, any 3 consecutive bullish / bearish bars will be calculated as FVGs. If it's on, the size of FVGs will be filtered by the selected sensitivity. Lower settings mean less but larger FVGs.

2. TP / SL

TP / SL Method -> If "Fixed" is selected, you can adjust the TP / SL ratios from the settings below. If "Dynamic" is selected, the TP / SL zones will be auto-determined by the algorithm.

Risk -> The risk you're willing to take if "Dynamic" TP / SL Method is selected. Higher risk usually means a better winrate at the cost of losing more if the strategy fails.

Close Position @ Session End -> If this setting is enabled, the current position (if any) will be closed at the beginning of a new session, regardless if it hit the TP / SL zone. If it's off, the position will be open until it hits a TP / SL zone.

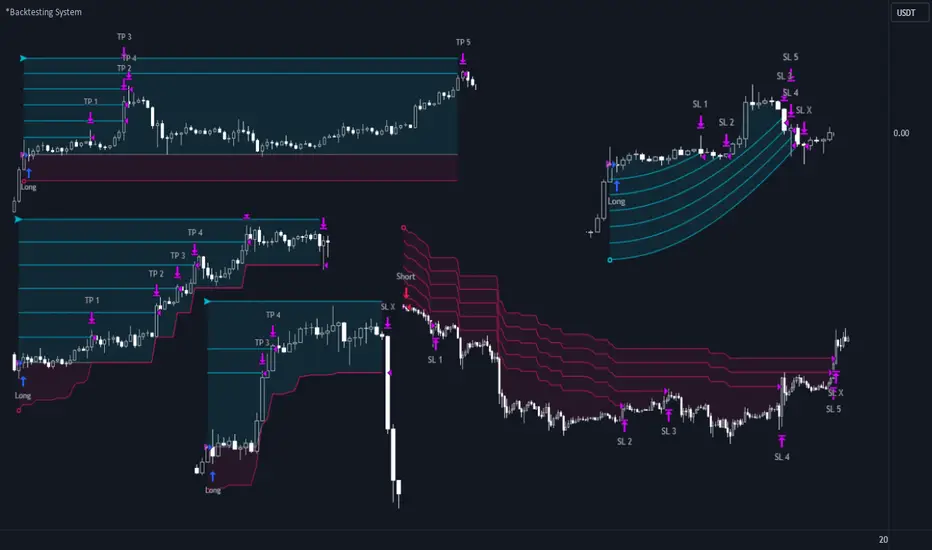

*Backtesting System ⚉ OVERVIEW ⚉

One of the best Systems for Backtesting your Strategies.

Incredibly flexible, simple, fast and feature-rich system — will solve most of your queries without much effort.

Many systems for setting StopLoss, TakeProfit, Risk Management and advanced Filters.

All you need to do is plug in your indicator and start Backtesting .

I intentionally left the option to use my System on Full Power before you load your indicator into it.

The system uses the built-in simple and popular moving average crossover signal for this purpose. (EMA 50 & 200).

Also Highly Recommend that you Fully use ALL of the features of this system so that you understand how they work before you ask questions.

Also tried to leave TIPS for each feature everywhere, read Tips, activate them and see how they work.

But before you use this system, I Recommend you to read the following description in Full.

—————— How to connect your indicator in 2 steps:

Adapt your indicator by adding only 2 lines of code and then connect it to this Backtesting System.

Step 1 — Create your connector, For doing so:

• 1 — Find or create in your indicator where are the conditions printing the Long-Buy and Short-Sell signals.

• 2 — Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator wether it's a MACD, RSI , Pivots, or whatever indicator with Clear Buy and Sell conditions.

//@version=5

indicator('Moving Average Cross', overlay = true)

MA200 = ta.𝚎𝚖𝚊(close, 200)

MA50 = ta.𝚎𝚖𝚊(close, 50)

// Generate Buy and Sell conditions

buy = ta.crossover (MA200, MA50)

sell = ta.crossunder (MA200, MA50)

plot(MA200, color=color.green)

plot(MA50 , color=color.red )

bgcolor(color = buy ? color.green : sell ? color.red : na, title='SIGNALS')

// ———————————————— SIGNAL FOR SYSTEM ————————————————

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, title='🔌Connector🔌', display = display.none)

// —————— 🔥 The Backtesting System expects the value to be exactly +1 for the 𝚋𝚞𝚕𝚕𝚒𝚜𝚑 signal, and -1 for the 𝚋𝚎𝚊𝚛𝚒𝚜𝚑 signal

Basically, I identified my Buy & Sell conditions in the code and added this at the bottom of my indicator code

Now you can connect your indicator to the Backtesting System using the Step 2

Step 2 — Connect the connector

• 1 — Add your updated indicator to a TradingView chart and Add the Backtesting System as well to the SAME chart

• 2 — Open the Backtesting System settings and in the External Source field select your 🔌Connector🔌 (which comes from your indicator)

_______________________________

⚉ MAIN SETTINGS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

𝐄𝐱𝐭𝐞𝐫𝐧𝐚𝐥 𝐒𝐨𝐮𝐫𝐜𝐞 — Select your indicator. Add your indicator by following the 2 steps described above and select it in the menu. To familiarize yourself with the system until you select your indicator, you will have an in-built strategy of crossing the two moving EMA's of 50 and 200.

Long Deals — Enable/Disable Long Deals.

Short Deals — Enable/Disable Short Deals.

Wait End Deal — Enable/Disable waiting for a trade to close at Stop Loss/Take Profit. Until the trade closes on the Stop Loss or Take Profit, no new trade will open.

Reverse Deals — To force the opening of a trade in the opposite direction.

ReEntry Deal — Automatically open the same new deal after the deal is closed.

ReOpen Deal — Reopen the trade if the same signal is received. For example, if you are already in the long and a new signal is received in the long, the trade will reopen. * Does not work if Wait End Deal is enabled.

𝐓𝐚𝐤𝐞 𝐏𝐫𝐨𝐟𝐢𝐭:

None — Disables take profit. Useful if you only want to use dynamic stoplosses such as MA, Fast-Trailing, ATR Trail.

FIXED % — Fixed take profit in percent.

FIXED $ — Fixed Take in Money.

ATR — Fixed Take based on ATR.

R:R — Fixed Take based on the size of your stop loss. For example, if your stop is 10% and R:R=1, then the Take would be 10%. R:R=3 Take would be 30%, etc.

HH / LL — Fixed Take based on the previous maximum/minimum (extremum).

𝐒𝐭𝐨𝐩 𝐋𝐨𝐬𝐬:

None — Disables Stop Loss. Useful if you want to work without a stop loss. *Be careful if Wait End Deal is enabled, the trade may not close for a long time until it reaches the Take.

FIXED % — Fixed Stop in percent.

FIXED $ — Fixed Stop in Money.

TRAILING — Dynamic Trailing Stop like on the stock exchanges.

FAST TRAIL — Dynamic Fast Trailing Stop moves immediately in profit and stays in place if the price stands still or the price moves in loss.

ATR — Fixed Stop based on the ATR.

ATR TRAIL — Dynamic Trailing Stop based on the ATR.

LO / HI — A Fixed Stop based on the last Maximum/Minimum extemum. Allows you to place a stop just behind or above the low/high candle.

MA — Dynamic Stop based on selected Moving Average. * You will have 8 types of MA (EMA, SMA, HMA, etc.) to choose from, but you can easily add dozens of other MAs, which makes this type of stop incredibly flexible.

Add % — If true, then with the "𝗦𝘁𝗼𝗽 %" parameter you can add percentages to any of the current SL. Can be especially useful when using Stop - 𝗔𝗧𝗥 or 𝗠𝗔 or 𝗟𝗢/𝗛𝗜. For example with 𝗟𝗢/𝗛𝗜 to put a stop for the last High/Low and add 0.5% additional Stoploss.

Fixed R:R — If the stop loss is Dynamic (Trailing or MA) then if R:R true can also be made Dynamic * Use it carefully, the function is experimental.

_________________________________________

⚉ TAKE PROFIT LEVELS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

A unique method of constructing intermediate Take Profit Levels will allow you to select up to 5 intermediate Take Profit Levels and one intermediate Stop Loss.

Intermediate Take Profit Levels are perfectly calculated into 5 equal parts in the form of levels from the entry point to the final Take Profit target.

All you need to do is to choose the necessary levels for fixing and how much you want to fix at each level as a percentage. For example, TP 3 will always be exactly between the entry point and the Take Profit target. And the value of TP 3 = 50 will close 50% of the amount of the remaining size of the position.

Note: all intermediate SL/TP are closed from the remaining position amount and not from the initial position size, as TV does by default.

SL 0 Position — works in the same way as TP 1-5 but it's Stop. With this parameter you can set the position where the intermediate stop will be set.

Breakeven on TP — When activated, it allows you to put the stop loss at Breakeven after the selected TP is reached. For this function to work as it should - you need to activate an intermediate Take. For example, if TP 3 is activated and Breakeven on TP = 3, then after the price reaches this level, the Stop loss will go to Breakeven.

* This function will not work with Dynamic Stoplosses, because it simply does not make sense.

CoolDown # Bars — When activated, allows you to add a delay before a new trade is opened. A new trade after CoolDown will not be opened until # bars pass and a new signal appears.

_____________________________

⚉ TIME FILTERS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

Powerful time filter code that allows you to filter data based on specific time zones, dates, and session days. This code is ideal for those who need to analyze data from different time zones and weed out irrelevant data.

With Time Filter, you can easily set the starting and ending time zones by which you want to filter the data.

You can also set a start and end date for your data and choose which days of the week to include in the analysis. In addition, you can specify start and end times for a specific session, allowing you to focus your analysis on specific time periods.

_________________________________

⚉ SIGNAL FILTERS ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

Signal Filters — allows you to easily customize and optimize your trading strategies based on 10 filters.

Each filter is designed to help you weed out inaccurate signals to minimize your risks.

Let's take a look at their features:

__________________________________

⚉ RISK MANAGEMENT ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

Risk management tools that allow you to set the maximum number of losing trades in a row, a limit on the number of trades per day or week and other filters.

Loss Streak — Set Max number of consecutive loss trades.

Win Streak — Max Winning Streak Length.

Row Loss InDay — Max of consecutive days with a loss in a row.

DrawDown % — Max DrawDown (in % of strategy equity).

InDay Loss % — Set Max Intraday Loss.

Daily Trades — Limit the number of MAX trades per day.

Weekly Trades — Limit the number of MAX trades per week.

* 🡅 I would Not Recommend using these functions without understanding how they work.

Order Size — Position Size

• NONE — Use the default position size settings in Tab "Properties".

• EQUITY — The amount of the allowed position as a percentage of the initial capital.

• Use Net Profit — On/Off the use of profit in the following trades. *Only works if the type is EQUITY.

• SIZE — The size of the allowed position in monetary terms.

• Contracts — The size of the allowed position in the contracts. 1 Сontract = Сurrent price.

________________

⚉ NOTES ⚉

‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾

It is important to note that I have never worked with Backtesting and the functions associated with them before.

It took me about a month of slow work to build this system.

I want to say Big Thanks:

• The PineScripters🌲 group, the guys suggested how to implement some features. Especially @allanster

• Thanks to all those people who share their developments for free on TV and not only.

• I also thank myself for not giving up and finishing the project, and not trying to monetize the system by selling it. * Although I really want the money :)

I tried hard to make it as fast and convenient as possible for everyone who will use my code.

That's why I didn't use any libraries and dozens of heavy functions, and I managed to fit in 8+-functions for the whole code.

Absolutely every block of code I tried to make full-fledged modular, that it was easy to import/edit for myself (you).

I have abused the Ternary Pine operator a little (a lot) so that the code was as compact as possible.

Nevertheless, I tried very hard to keep my code very understandable even for beginners.

At last I managed to write 500 lines of code, making it one of the fastest and most feature-rich systems out there.

I hope everyone enjoys my work.

Put comments and write likes.

Awesome Oscillator_VTX

Abbreviations:

AO - Awesome Oscillator

AC - Accelerator Oscillator

TP - TimePeriod (1m,2m,5m,1h....)

TP Steps - 1m,3m,12m,1h,5h,D (This steps i use)

Use-case:

Awesome Oscillator best used to find Divergence/Convergence what results in Weakening of Momentum and Price reversals.

This script calculates and plots AO/AC with minute precision, removing GAPS when projecting Higher Period AO/AC.

So you can accommodate all important information on one chart with best precision.

Made for Intraday Perioads.

Best used for DayTrading, when you need to make quick and efficient decisions.

Calculation = Preferred resolution * Length / Present resolution.

As Additional Function, this Awesome Oscillator has AC built in.

Settings:

Resolution - Most used TP included, plus some exclusive paid plans (1m, 2m, 3m, 5m, 12m, 15m, 1h, 4h, 5h, Daily). Default set to 1h

Use AO - You can switch between EMA and SMA for FastMA/SlowMA calculation. Default set to EMA

FastMA - standard function. Default set to 5

SlowMA - standard function. Default set to 34

Signal Line - Plots MA to show Momentum. Uses EMA/SMA based on "Use AO" selection. Default set to 5

Use AC - You can switch between EMA and SMA for AC calculation. Default set to SMA

Offset - standard function. Default set to 0

Accelerator - AC length. Default set to 5

Source - standard function. Default set to hlc3

Why to use it ?

Yes, i know that variable TP is standard now in TradingView. But there are some limitations, especially for DayTraders.

Problem:

Imagine you are trading/scalping on 1m.. 5m.. 15.. charts and you want to see where are your on Higher TP.

-- You can change to 1h and check it, but you will loose the picture from smaller TP.

-- You can use Standard TP function, but your data will update every 15m, 1h (depends on TP). And in result you have Gaps between bars.

Solution:

This script help to solve this problem, by breaking information down to 1m and building from there.

So whatever Intraday TP you choose to trade, your AO/AC will be updated with minute precision.

Limitations:

Sadly nothing without limitations.

1. For Best performance use only Higher TP dividable By Yours (ex. You use 3m chart, then you can plot 12m, 15m, 1h / You use 5m chart, then you can plot 15m, 1h. 12m will already have 3m of information lost using 5m Chart )

Megvie Scalping C - Pullback EMA20/50 (3-5m) by Lynda//@version=5

indicator("Megvie Scalping C - Pullback EMA20/50 (3-5m)", overlay=true, max_labels_count=500, max_lines_count=500)

// === INPUTS ===

ema_fast_len = input.int(20, "EMA fast (pullback)")

ema_slow_len = input.int(50, "EMA slow (trend)")

rsi_len = input.int(14, "RSI length")

rsi_min = input.int(40, "RSI min for entry")

atr_len = input.int(14, "ATR length (for SL/TP)")

use_atr_for_sl = input.bool(true, "Use ATR for SL size")

atr_sl_mult = input.float(1.0, "SL = ATR * multiplier", step=0.1)

rr = input.float(1.8, "Risk:Reward (TP = SL * RR)", step=0.1)

max_signals_repeat = input.int(3, "Min bars between signals", minval=1)

// === INDICATORS ===

ema_fast = ta.ema(close, ema_fast_len)

ema_slow = ta.ema(close, ema_slow_len)

rsi = ta.rsi(close, rsi_len)

atr = ta.atr(atr_len)

plot(ema_fast, color=color.new(color.green, 0), title="EMA 20")

plot(ema_slow, color=color.new(color.red, 0), title="EMA 50")

// === TREND FILTER ===

trend_bull = ema_fast > ema_slow

trend_bear = ema_fast < ema_slow

// === PULLBACK CONDITION ===

// Consider a pullback when price traded at/under EMA20 within the last 3 bars and now shows a bullish/bearish confirmation

pullback_bull = ta.lowest(low, 3) <= ema_fast and close > ema_fast

pullback_bear = ta.highest(high, 3) >= ema_fast and close < ema_fast

// === CONFIRMATION CANDLE ===

// Bullish confirmation: current close > open AND close > high (strong close)

// Bearish confirmation: current close < open AND close < low

bullish_candle = close > open and close > high

bearish_candle = close < open and close < low

// === ENTRY SIGNALS (Version C logic) ===

buySignal = trend_bull and pullback_bull and rsi >= rsi_min and bullish_candle

sellSignal = trend_bear and pullback_bear and rsi <= (100 - rsi_min) and bearish_candle

// Prevent firing signals too often

var int lastSignalBar = na

ok_to_fire = na(lastSignalBar) ? true : (bar_index - lastSignalBar) > max_signals_repeat

buyFire = buySignal and ok_to_fire

sellFire = sellSignal and ok_to_fire

if buyFire

lastSignalBar := bar_index

if sellFire

lastSignalBar := bar_index

// === SL / TP CALCULATION ===

var float sl_price = na

var float tp_price = na

var line sl_line = na

var line tp_line = na

var label sig_label = na

if buyFire

if use_atr_for_sl

sl_price := close - atr * atr_sl_mult

else

sl_price := ta.lowest(low, 3) - syminfo.mintick * 5

tp_price := close + (close - sl_price) * rr

// draw lines and label

line.delete(sl_line )

line.delete(tp_line )

label.delete(sig_label )

sl_line := line.new(bar_index, sl_price, bar_index + 50, sl_price, color=color.new(color.red, 0), width=1, extend=extend.right)

tp_line := line.new(bar_index, tp_price, bar_index + 50, tp_price, color=color.new(color.green, 0), width=1, extend=extend.right)

sig_label := label.new(bar_index, low, "BUY\nSL:" + str.tostring(sl_price, format.mintick) + "\nTP:" + str.tostring(tp_price, format.mintick), style=label.style_label_up, color=color.new(color.green,0), textcolor=color.white, size=size.small)

if sellFire

if use_atr_for_sl

sl_price := close + atr * atr_sl_mult

else

sl_price := ta.highest(high, 3) + syminfo.mintick * 5

tp_price := close - (sl_price - close) * rr

// draw lines and label

line.delete(sl_line )

line.delete(tp_line )

label.delete(sig_label )

sl_line := line.new(bar_index, sl_price, bar_index + 50, sl_price, color=color.new(color.red, 0), width=1, extend=extend.right)

tp_line := line.new(bar_index, tp_price, bar_index + 50, tp_price, color=color.new(color.green, 0), width=1, extend=extend.right)

sig_label := label.new(bar_index, high, "SELL\nSL:" + str.tostring(sl_price, format.mintick) + "\nTP:" + str.tostring(tp_price, format.mintick), style=label.style_label_down, color=color.new(color.red,0), textcolor=color.white, size=size.small)

// === PLOT SIGNAL ARROWS ===

plotshape(buyFire, title="Buy Signal", location=location.belowbar, color=color.green, style=shape.triangleup, size=size.small, text="BUY")

plotshape(sellFire, title="Sell Signal", location=location.abovebar, color=color.red, style=shape.triangledown, size=size.small, text="SELL")

// === ALERTS ===

alertcondition(buyFire, title="BUY Signal", message="Megvie C: BUY signal. SL: {{plot_0}} TP: {{plot_1}}")

alertcondition(sellFire, title="SELL Signal", message="Megvie C: SELL signal. SL: {{plot_0}} TP: {{plot_1}}")

alertcondition(ta.cross(close, tp_price), title="TP Hit", message="Megvie C: TP reached")

alertcondition(ta.cross(close, sl_price), title="SL Hit", message="Megvie C: SL reached")

// === NOTES ===

// - Optimized for 3-5 minute charts.

// - Test in paper trading before using real capital.

// - Adjust ATR multiplier and RR to match your risk management.

Moving Average Band StrategyOverview

The Moving Average Band Strategy is a fully customizable breakout and trend-continuation system designed for traders who need both simplicity and control.

The strategy creates adaptive bands around a user-selected moving average and executes trades when price breaks out of these bands, with advanced risk-management settings including optional Risk:Reward targets.

This script is suitable for intraday, swing, and positional traders across all markets — equities, futures, crypto, and forex.

Key Features

✔ Six Moving Average Types

Choose the MA that best matches your trading style:

SMA

EMA

WMA

HMA

VWMA

RMA

✔ Dynamic Bands

Upper Band built from MA of highs

Lower Band built from MA of lows

Adjustable band offset (%)

Color-coded band fill indicating price position

✔ Configurable Strategy Preferences

Toggle Long and/or Short trades

Toggle Risk:Reward Take-Profit

Adjustable Risk:Reward Ratio

Default position sizing: % of equity (configurable via strategy settings)

Entry Conditions

Long Entry

A long trade triggers when:

Price crosses above the Upper Band

Long trades are enabled

No existing long position is active

Short Entry

A short trade triggers when:

Price crosses below the Lower Band

Short trades are enabled

No existing short position is active

Clear entry markers and price labels appear on the chart.

Risk Management

This strategy includes a complete set of risk-controls:

Stop-Loss (Fixed at Entry)

Long SL: Lower Band

Short SL: Upper Band

These levels remain constant for the entire trade.

Optional Risk:Reward Take-Profit

Enabled/disabled using a toggle switch.

When enabled:

Long TP = Entry + (Risk × Risk:Reward Ratio)

Short TP = Entry – (Risk × Risk:Reward Ratio)

When disabled:

Exits are handled by reverse crossover signals.

Exit Conditions

Long Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Short Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Exit markers and price labels are plotted automatically.

Visual Tools

To improve clarity:

Upper & Lower Band (blue, adjustable width)

Middle Line

Dynamic band fill (green/red/yellow)

SL & TP line plotting when in position

Entry/Exit markers

Price labels for all executed trades

These are built to help users visually follow the strategy logic.

Alerts Included

Every trading event is covered:

Long Entry

Short Entry

Long SL / TP / Cross Exit

Short SL / TP / Cross Exit

Combined Alert for webhook/automation (JSON-formatted)

Perfect for algo trading, Discord bots, or automation platforms.

Best For

This strategy performs best in:

Trending markets

Breakout environments

High-momentum instruments

Clean intraday swings

Works seamlessly on:

Stocks

Index futures

Commodities

Crypto

Forex

⚠️ Important Disclaimer

This script is for educational purposes only.

Trading involves risk. Backtest results are not indicative of future performance.

Always validate settings and use proper position sizing.

Range Oscillator Strategy + Stoch Confirm🔹 Short summary

This is a free, educational long-only strategy built on top of the public “Range Oscillator” by Zeiierman (used under CC BY-NC-SA 4.0), combined with a Stochastic timing filter, an EMA-based exit filter and an optional risk-management layer (SL/TP and R-multiple exits). It is NOT financial advice and it is NOT a magic money machine. It’s a structured framework to study how range-expansion + momentum + trend slope can be combined into one rule-based system, often with intentionally RARE trades.

────────────────────────

0. Legal / risk disclaimer

────────────────────────

• This script is FREE and public. I do not charge any fee for it.

• It is for EDUCATIONAL PURPOSES ONLY.

• It is NOT financial advice and does NOT guarantee profits.

• Backtest results can be very different from live results.

• Markets change over time; past performance is NOT indicative of future performance.

• You are fully responsible for your own trades and risk.

Please DO NOT use this script with money you cannot afford to lose. Always start in a demo / paper trading environment and make sure you understand what the logic does before you risk any capital.

────────────────────────

1. About default settings and risk (very important)

────────────────────────

The script is configured with the following defaults in the `strategy()` declaration:

• `initial_capital = 10000`

→ This is only an EXAMPLE account size.

• `default_qty_type = strategy.percent_of_equity`

• `default_qty_value = 100`

→ This means 100% of equity per trade in the default properties.

→ This is AGGRESSIVE and should be treated as a STRESS TEST of the logic, not as a realistic way to trade.

TradingView’s House Rules recommend risking only a small part of equity per trade (often 1–2%, max 5–10% in most cases). To align with these recommendations and to get more realistic backtest results, I STRONGLY RECOMMEND you to:

1. Open **Strategy Settings → Properties**.

2. Set:

• Order size: **Percent of equity**

• Order size (percent): e.g. **1–2%** per trade

3. Make sure **commission** and **slippage** match your own broker conditions.

• By default this script uses `commission_value = 0.1` (0.1%) and `slippage = 3`, which are reasonable example values for many crypto markets.

If you choose to run the strategy with 100% of equity per trade, please treat it ONLY as a stress-test of the logic. It is NOT a sustainable risk model for live trading.

────────────────────────

2. What this strategy tries to do (conceptual overview)

────────────────────────

This is a LONG-ONLY strategy designed to explore the combination of:

1. **Range Oscillator (Zeiierman-based)**

- Measures how far price has moved away from an adaptive mean.

- Uses an ATR-based range to normalize deviation.

- High positive oscillator values indicate strong price expansion away from the mean in a bullish direction.

2. **Stochastic as a timing filter**

- A classic Stochastic (%K and %D) is used.

- The logic requires %K to be below a user-defined level and then crossing above %D.

- This is intended to catch moments when momentum turns up again, rather than chasing every extreme.

3. **EMA Exit Filter (trend slope)**

- An EMA with configurable length (default 70) is calculated.

- The slope of the EMA is monitored: when the slope turns negative while in a long position, and the filter is enabled, it triggers an exit condition.

- This acts as a trend-protection exit: if the medium-term trend starts to weaken, the strategy exits even if the oscillator has not yet fully reverted.

4. **Optional risk-management layer**

- Percentage-based Stop Loss and Take Profit (SL/TP).

- Risk/Reward (R-multiple) exit based on the distance from entry to SL.

- Implemented as OCO orders that work *on top* of the logical exits.

The goal is not to create a “holy grail” system but to serve as a transparent, configurable framework for studying how these concepts behave together on different markets and timeframes.

────────────────────────

3. Components and how they work together

────────────────────────

(1) Range Oscillator (based on “Range Oscillator (Zeiierman)”)

• The script computes a weighted mean price and then measures how far price deviates from that mean.

• Deviation is normalized by an ATR-based range and expressed as an oscillator.

• When the oscillator is above the **entry threshold** (default 100), it signals a strong move away from the mean in the bullish direction.

• When it later drops below the **exit threshold** (default 30), it can trigger an exit (if enabled).

(2) Stochastic confirmation

• Classic Stochastic (%K and %D) is calculated.

• An entry requires:

- %K to be below a user-defined “Cross Level”, and

- then %K to cross above %D.

• This is a momentum confirmation: the strategy tries to enter when momentum turns up from a pullback rather than at any random point.

(3) EMA Exit Filter

• The EMA length is configurable via `emaLength` (default 70).

• The script monitors the EMA slope: it computes the relative change between the current EMA and the previous EMA.

• If the slope turns negative while the strategy holds a long position and the filter is enabled, it triggers an exit condition.

• This is meant to help protect profits or cut losses when the medium-term trend starts to roll over, even if the oscillator conditions are not (yet) signalling exit.

(4) Risk management (optional)

• Stop Loss (SL) and Take Profit (TP):

- Defined as percentages relative to average entry price.

- Both are disabled by default, but you can enable them in the Inputs.

• Risk/Reward Exit:

- Uses the distance from entry to SL to project a profit target at a configurable R-multiple.

- Also optional and disabled by default.

These exits are implemented as `strategy.exit()` OCO orders and can close trades independently of oscillator/EMA conditions if hit first.

────────────────────────

4. Entry & Exit logic (high level)

────────────────────────

A) Time filter

• You can choose a **Start Year** in the Inputs.

• Only candles between the selected start date and 31 Dec 2069 are used for backtesting (`timeCondition`).

• This prevents accidental use of tiny cherry-picked windows and makes tests more honest.

B) Entry condition (long-only)

A long entry is allowed when ALL the following are true:

1. `timeCondition` is true (inside the backtest window).

2. If `useOscEntry` is true:

- Range Oscillator value must be above `entryLevel`.

3. If `useStochEntry` is true:

- Stochastic condition (`stochCondition`) must be true:

- %K < `crossLevel`, then %K crosses above %D.

If these filters agree, the strategy calls `strategy.entry("Long", strategy.long)`.

C) Exit condition (logical exits)

A position can be closed when:

1. `timeCondition` is true AND a long position is open, AND

2. At least one of the following is true:

- If `useOscExit` is true: Oscillator is below `exitLevel`.

- If `useMagicExit` (EMA Exit Filter) is true: EMA slope is negative (`isDown = true`).

In that case, `strategy.close("Long")` is called.

D) Risk-management exits

While a position is open:

• If SL or TP is enabled:

- `strategy.exit("Long Risk", ...)` places an OCO stop/limit order based on the SL/TP percentages.

• If Risk/Reward exit is enabled:

- `strategy.exit("RR Exit", ...)` places an OCO order using a projected R-multiple (`rrMult`) of the SL distance.

These risk-based exits can trigger before the logical oscillator/EMA exits if price hits those levels.

────────────────────────

5. Recommended backtest configuration (to avoid misleading results)

────────────────────────

To align with TradingView House Rules and avoid misleading backtests:

1. **Initial capital**

- 10 000 (or any value you personally want to work with).

2. **Order size**

- Type: **Percent of equity**

- Size: **1–2%** per trade is a reasonable starting point.

- Avoid risking more than 5–10% per trade if you want results that could be sustainable in practice.

3. **Commission & slippage**

- Commission: around 0.1% if that matches your broker.

- Slippage: a few ticks (e.g. 3) to account for real fills.

4. **Timeframe & markets**

- Volatile symbols (e.g. crypto like BTCUSDT, or major indices).

- Timeframes: 1H / 4H / **1D (Daily)** are typical starting points.

- I strongly recommend trying the strategy on **different timeframes**, for example 1D, to see how the behaviour changes between intraday and higher timeframes.

5. **No “caution warning”**

- Make sure your chosen symbol + timeframe + settings do not trigger TradingView’s caution messages.

- If you see warnings (e.g. “too few trades”), adjust timeframe/symbol or the backtest period.

────────────────────────

5a. About low trade count and rare signals

────────────────────────

This strategy is intentionally designed to trade RARELY:

• It is **long-only**.

• It uses strict filters (Range Oscillator threshold + Stochastic confirmation + optional EMA Exit Filter).

• On higher timeframes (especially **1D / Daily**) this can result in a **low total number of trades**, sometimes WELL BELOW 100 trades over the whole backtest.

TradingView’s House Rules mention 100+ trades as a guideline for more robust statistics. In this specific case:

• The **low trade count is a conscious design choice**, not an attempt to cherry-pick a tiny, ultra-profitable window.

• The goal is to study a **small number of high-conviction long entries** on higher timeframes, not to generate frequent intraday signals.

• Because of the low trade count, results should NOT be interpreted as statistically strong or “proven” – they are only one sample of how this logic would have behaved on past data.

Please keep this in mind when you look at the equity curve and performance metrics. A beautiful curve with only a handful of trades is still just a small sample.

────────────────────────

6. How to use this strategy (step-by-step)

────────────────────────

1. Add the script to your chart.

2. Open the **Inputs** tab:

- Set the backtest start year.

- Decide whether to use Oscillator-based entry/exit, Stochastic confirmation, and EMA Exit Filter.

- Optionally enable SL, TP, and Risk/Reward exits.

3. Open the **Properties** tab:

- Set a realistic account size if you want.

- Set order size to a realistic % of equity (e.g. 1–2%).

- Confirm that commission and slippage are realistic for your broker.

4. Run the backtest:

- Look at Net Profit, Max Drawdown, number of trades, and equity curve.

- Remember that a low trade count means the statistics are not very strong.

5. Experiment:

- Tweak thresholds (`entryLevel`, `exitLevel`), Stochastic settings, EMA length, and risk params.

- See how the metrics and trade frequency change.

6. Forward-test:

- Before using any idea in live trading, forward-test on a demo account and observe behaviour in real time.

────────────────────────

7. Originality and usefulness (why this is more than a mashup)

────────────────────────

This script is not intended to be a random visual mashup of indicators. It is designed as a coherent, testable strategy with clear roles for each component:

• Range Oscillator:

- Handles mean vs. range-expansion states via an adaptive, ATR-normalized metric.

• Stochastic:

- Acts as a timing filter to avoid entering purely on extremes and instead waits for momentum to turn.

• EMA Exit Filter:

- Trend-slope-based safety net to exit when the medium-term direction changes against the position.

• Risk module:

- Provides practical, rule-based exits: SL, TP, and R-multiple exit, which are useful for structuring risk even if you modify the core logic.

It aims to give traders a ready-made **framework to study and modify**, not a black box or “signals” product.

────────────────────────

8. Limitations and good practices

────────────────────────

• No single strategy works on all markets or in all regimes.

• This script is long-only; it does not short the market.

• Performance can degrade when market structure changes.

• Overfitting (curve fitting) is a real risk if you endlessly tweak parameters to maximise historical profit.

Good practices:

- Test on multiple symbols and timeframes.

- Focus on stability and drawdown, not only on how high the profit line goes.

- View this as a learning tool and a basis for your own research.

────────────────────────

9. Licensing and credits

────────────────────────

• Core oscillator idea & base code:

- “Range Oscillator (Zeiierman)”

- © Zeiierman, licensed under CC BY-NC-SA 4.0.

• Strategy logic, Stochastic confirmation, EMA Exit Filter, and risk-management layer:

- Modifications by jokiniemi.

Please respect both the original license and TradingView House Rules if you fork or republish any part of this script.

────────────────────────

10. No payments / no vendor pitch

────────────────────────

• This script is completely FREE to use on TradingView.

• There is no paid subscription, no external payment link, and no private signals group attached to it.

• If you have questions, please use TradingView’s comment system or private messages instead of expecting financial advice.

Use this script as a tool to learn, experiment, and build your own understanding of markets.

────────────────────────

11. Example backtest settings used in screenshots

────────────────────────

To avoid any confusion about how the results shown in screenshots were produced, here is one concrete example configuration:

• Symbol: BTCUSDT (or similar major BTC pair)

• Timeframe: 1D (Daily)

• Backtest period: from 2018 to the most recent data

• Initial capital: 10 000

• Order size type: Percent of equity

• Order size: 2% per trade

• Commission: 0.1%

• Slippage: 3 ticks

• Risk settings: Stop Loss and Take Profit disabled by default, Risk/Reward exit disabled by default

• Filters: Range Oscillator entry/exit enabled, Stochastic confirmation enabled, EMA Exit Filter enabled

If you change any of these settings (symbol, timeframe, risk per trade, commission, slippage, filters, etc.), your results will look different. Please always adapt the configuration to your own risk tolerance, market, and trading style.

Adaptive Trend 1m ### Overview

The "Adaptive Trend Impulse Parallel SL/TP 1m Realistic" strategy is a sophisticated trading system designed specifically for high-volatility markets like cryptocurrencies on 1-minute timeframes. It combines trend-following with momentum filters and adaptive parameters to dynamically adjust to market conditions, ensuring more reliable entries and risk management. This strategy uses SuperTrend for primary trend detection, enhanced by MACD, RSI, Bollinger Bands, and optional volume spikes. It incorporates parallel stop-loss (SL) and multiple take-profit (TP) levels based on ATR, with options for breakeven and trailing stops after the first TP. Optimized for realistic backtesting on short timeframes, it avoids over-optimization by adapting indicators to market speed and efficiency.

### Principles of Operation

The strategy operates on the principle of adaptive impulse trading, where entry signals are generated only when multiple conditions align to confirm a strong trend reversal or continuation:

1. **Trend Detection (SuperTrend)**: The core signal comes from an adaptive SuperTrend indicator. It calculates upper and lower bands using ATR (Average True Range) with dynamic periods and multipliers. A buy signal occurs when the price crosses above the lower band (from a downtrend), and a sell signal when it crosses below the upper band (from an uptrend). Adaptation is based on Rate of Change (ROC) to measure market speed, shortening periods in fast markets for quicker responses.

2. **Momentum and Trend Filters**:

- **MACD**: Uses adaptive fast and slow lengths. In "Trend Filter" mode (default when "Use MACD Cross" is false), it checks if the MACD line is above/below the signal for long/short. In cross mode, it requires a crossover/crossunder.

- **RSI**: Adaptive period RSI must be above 50 for longs and below 50 for shorts, confirming overbought/oversold conditions dynamically.

- **Bollinger Bands (BB)**: Depending on the mode ("Midline" by default), it requires the price to be above/below the BB midline for longs/shorts, or a breakout in "Breakout" mode. Deviation adapts to market efficiency.

- **Volume Spike Filter** (optional): Entries require volume to exceed an adaptive multiple of its SMA, signaling strong impulse.

3. **Volatility Filter**: Entries are only allowed if current ATR percentage exceeds a historical minimum (adaptive), preventing trades in low-volatility ranges.

4. **Risk Management (Parallel SL/TP)**:

- **Stop-Loss**: Set at an adaptive ATR multiple below/above entry for long/short.

- **Take-Profits**: Three levels at adaptive ATR multiples, with partial position closures (e.g., 51% at TP1, 25% at TP2, remainder at TP3).

- **Post-TP1 Features**: Optional breakeven moves SL to entry after TP1. Trailing SL uses BB midline as a dynamic trail.

- All levels are calculated per trade using the ATR at entry, making them "realistic" for 1m charts by widening SL and tightening initial TPs.

The strategy enters long on buy signals with all filters met, and short on sell signals. It uses pyramid margin (100% long/short) for full position sizing.

Adaptation is driven by:

- **Market Speed (normSpeed)**: Based on ROC, tightens multipliers in volatile periods.

- **Efficiency Ratio (ER)**: Measures trend strength, adjusting periods for trending vs. ranging markets.

This ensures the strategy "adapts" without manual tweaks, reducing false signals in varying conditions.

### Main Advantages

- **Adaptability**: Unlike static strategies, parameters dynamically adjust to market volatility and trend strength, improving performance across ranging and trending phases without over-optimization.

- **Realistic Risk Management for 1m**: Wider SL and tiered TPs prevent premature stops in noisy short-term charts, while partial profits lock in gains early. Breakeven/trailing options protect profits in extended moves.

- **Multi-Filter Confirmation**: Combines trend, momentum, and volume for high-probability entries, reducing whipsaws. The volatility filter avoids flat markets.

- **Debug Visualization**: Built-in plots for signals, levels, and component checks (when "Show Debug" is enabled) help users verify logic on charts.

- **Efficiency**: Low computational load, suitable for real-time trading on TradingView with alerts.

Backtesting shows robust results on volatile assets, with a focus on sustainable risk (e.g., SL at 3x ATR avoids excessive drawdowns).

### Uniqueness

What sets this strategy apart is its **fully adaptive framework** integrating multiple indicators with real-time market metrics (ROC for speed, ER for efficiency). Most trend strategies use fixed parameters, leading to poor adaptation; here, every key input (periods, multipliers, deviations) scales dynamically within bounds, creating a "self-tuning" system. The "parallel SL/TP with 1m realism" adds custom handling for micro-timeframes: tightened initial TPs for quick wins and adaptive min-ATR filter to skip low-vol bars. Unlike generic mashups, it justifies the combination—SuperTrend for trend, MACD/RSI/BB for impulse confirmation, volume for conviction—working synergistically to capture "trend impulses" while filtering noise. The post-TP1 breakeven/trailing tied to BB adds a unique profit-locking mechanism not common in open-source scripts.

### Recommended Settings

These settings are optimized and recommended for trading ASTER/USDT on Bybit, with 1-minute chart, x10 leverage, and cross margin mode. They provide a balanced risk-reward for this volatile pair:

- **Base Inputs**:

- Base ATR Period: 10

- Base SuperTrend ATR Multiplier: 2.5

- Base MACD Fast: 8

- Base MACD Slow: 17

- Base MACD Signal: 6

- Base RSI Period: 9

- Base Bollinger Period: 12

- Bollinger Deviation: 1.8

- Base Volume SMA Period: 19

- Base Volume Spike Multiplier: 1.8

- Adaptation Window: 54

- ROC Length: 10

- **TP/SL Settings**:

- Use Stop Loss: True

- Base SL Multiplier (ATR): 3

- Use Take Profits: True

- Base TP1 Multiplier (ATR): 5.5

- Base TP2 Multiplier (ATR): 10.5

- Base TP3 Multiplier (ATR): 19

- TP1 % Position: 51

- TP2 % Position: 25

- Breakeven after TP1: False

- Trailing SL after TP1: False

- Base Min ATR Filter: 0.001

- Use Volume Spike Filter: True

- BB Condition: Midline

- Use MACD Cross (false=Trend Filter): True

- Show Debug: True

For backtesting, use initial capital of 30 USD, base currency USDT, order size 100 USDT, pyramiding 1, commission 0.1%, slippage 0 ticks, long/short margin 0%.

Always backtest on your platform and use risk management—risk no more than 1-2% per trade. This is not financial advice; trade at your own risk.

ORDER BLCOK custom strategy# OB Matrix Strategy - Documentation

**Version:** 1.0

**Author:** HPotter

**Date:** 31/07/2017

The **OB Matrix Strategy** is based on the identification of **bullish and bearish Order Blocks** and the management of conditional orders with multiple Take Profit (TP) and Stop Loss (SL) levels. It uses trend filters, ATR, and percentage-based risk management.

---

## 1. Main Parameters

### Strategy

- `initial_capital`: 50

- `default_qty_type`: percentage of capital

- `default_qty_value`: 10

### Money Management

- `rr_threshold`: minimum Risk/Reward threshold to open a trade

- `risk_percent`: percentage of capital to risk per trade (default 2%)

- `maxPendingBars`: maximum number of bars for a pending order

- `maxBarsOpen`: maximum number of bars for an open position

- `qty_tp1`, `qty_tp2`, `qty_tp3`: quantity percentages for multiple TPs

---

## 2. Order Block Identification

### Order Block Parameters

- `obLookback`: number of bars to identify an Order Block

- `obmode`: method to calculate the block (`Full` or `Breadth`)

- `obmiti`: method to determine block mitigation (`Close`, `Wick`, `Avg`)

- `obMaxBlocks`: maximum number of Order Blocks displayed

### Main Variables

- `bullBlocks`: array of bullish blocks

- `bearBlocks`: array of bearish blocks

- `last_bull_volume`, `last_bear_volume`: volume of the last block

- `dom_block`: dominant block type (Bullish/Bearish/None)

- `block_strength`: block strength (normalized volume)

- `price_distance`: distance between current price and nearest block

---

## 3. Visual Parameters

- `Width`: line thickness for swing high/low

- `amountOfBoxes`: block grid segments

- `showBorder`: show block borders

- `borderWidth`: width of block borders

- `showVolume`: display volume inside blocks

- `volumePosition`: vertical position of volume text

Customizable colors:

- `obHighVolumeColor`, `obLowVolumeColor`, `obBearHighVolumeColor`, `obBearLowVolumeColor`

- `obBullBorderColor`, `obBearBorderColor`

- `obBullFillColor`, `obBearFillColor`

- `volumeTextColor`

---

## 4. Screener Table

- `showScreener`: display the screener table

- `tablePosition`: table position (`Top Left`, `Top Right`, `Bottom Left`, `Bottom Right`)

- `tableSize`: table size (`Small`, `Normal`, `Large`)

The table shows:

- Symbol, Timeframe

- Type and status of Order Block

- Number of retests

- Bullish and bearish volumes

---

## 5. Trend Filters

- EMA as a trend filter (`emaPeriod`, default 223)

- `bullishTrend` if close > EMA

- `bearishTrend` if close < EMA

---

## 6. ATR and Swing Points

- ATR calculated with a customizable period (`atrLength`)

- Swing High/Low for SL/TP calculation

- `f_getSwingTargets` function to calculate SL and TP based on direction

---

## 7. Trade Logic

### Buy Limit on Bullish OB

- Conditions:

- New bullish block

- Uptrend

- RR > threshold (`rr_threshold`)

- SL: `bullishOBPrice * (1 - atr * atrMultiplier)`

- Multiple TPs: TP1 (50%), TP2 (80%), TP3 (100% max)

- Quantity calculation based on percentage risk

### Sell Limit on Bearish OB

- Conditions:

- New bearish block

- Downtrend

- RR > threshold (`rr_threshold`)

- SL: `bearishOBPrice * (1 + atr * atrMultiplier)`

- Multiple TPs: TP1 (50%), TP2 (80%), TP3 (100% max)

- Quantity calculation based on percentage risk

---

## 8. Order Management and Timeout

- Close pending orders after `maxPendingBars` bars

- Close open positions after `maxBarsOpen` bars

- Label management for open orders

---

## 9. Alert Conditions

- `bull_touch`: price inside maximum bullish volume zone

- `bear_touch`: price inside maximum bearish volume zone

- `bull_reject`: confirmation of bullish zone rejection

- `bear_reject`: confirmation of bearish zone rejection

- `new_bull`: new bullish block

- `new_bear`: new bearish block

---

## 10. Level Calculation

- Swing levels based on selected timeframe (`SelectPeriod`)

- `xHigh` and `xLow` for S1 and R1 calculation

- Levels plotted on chart

---

## 11. Take Profit / Stop Loss

- Extended horizontal lines (`extendBars`) to visualize TP and SL

- Customizable colors (`tpColor`, `slColor`)

---

## 12. Notes

- Complete script based on Pine Script v5

- Advanced graphical management with boxes, lines, labels

- Dynamically displays volumes and Order Blocks

- Integrated internal screener

---

### End of Documentation

Stop Loss vs Take Profit Probability and EVThis stop loss and take profit calculator uses a Monte Carlo simulation to calculate the probability of hitting your Stop Loss or Take Profit levels across different time horizons (expressed in bars).

It provides data-driven insights to optimize your risk management and position sizing by showing Expected Value for each scenario.

As a quant, I love using statistical data to help my decisions and get better EV from my trades.

🔬 How It's Calculated

Monte Carlo Simulation: Runs 1,000-10,000 price simulations using a random walk model

Volatility Analysis: Combines ATR-based and Historical Volatility for accurate price movement modeling

Expected Value: Calculates profit/loss expectation using formula: (TP_Probability × Reward) - (SL_Probability × Risk)

Time Horizons: Tests multiple timeframes (1, 5, 10, 20, 50 bars) to find optimal holding periods

Risk/Reward Ratios: Automatically calculates and displays R:R ratios for quick assessment

💡 Use Cases

Position Sizing - Determine optimal risk per trade based on Expected Value

Time Horizon Optimization - Find the best holding period for your strategy

Stop Loss Placement - Validate SL levels using probability analysis

Take Profit Optimization - Set TP levels with statistical backing

Strategy Backtesting - Compare different R:R setups before entering trades

Risk Management - Avoid trades with negative Expected Value

Swing vs Day Trading - Choose timeframes with highest success probability

🎯 How to Use

Setup Trade: Enter your entry price, stop loss, and take profit levels

You can add or remove time horizons denominated in bars. Say you are looking at 1h candles, adding a 24-bar time horizon means you are looking into 24 hours

Choose Direction: Select Long or Short position

Review Table

Analyze Expected Value: Focus on positive EV scenarios (green background)

Optimize Timing: Select time horizons with best risk/reward profile

Adjust Parameters: Modify volatility calculation method and simulation count if needed

Examples

Here's how you can read the tables.

Example 1:

In this chart, we are analyzing the TP and SL probabilities as well as the EV (expected value) for a stock. I want to check what the likelihood is that my SL and TP get triggered over the next 5 days. The stock market is open for 6.5 hours per day, which is 13 bars in this 30-minute bar chart. 26 bars is 2 days, 39 bars is 3 days and so on.

Although this trade is more likely to trigger my SL than my TP, in some of the time horizons we have a positive expected value because of the risk/reward of our trade (i.e. distance of the SL and TP from the price) and the probability of hitting SL and TP.

Example 2:

In this example, we have applied the indicator to gold. Because the TP is much closer to the price, the probability of hitting the TP is much higher.

We can also observe that the expected Value in the shorter time frames is better than in the longer ones. This can give us some clues to set up our trade. If we know that the EV is positive, we can allocate more to that specific trade.

Enjoy, and please let me know your feedback! 😊🥂

LANZ Strategy 5.0 [Backtest]🔷 LANZ Strategy 5.0 — Rule-Based BUY Logic with Time Filter, Session Limits and Auto SL/TP Execution

This is the backtest version of LANZ Strategy 5.0, built as a strategy script to evaluate real performance under fixed intraday conditions. It automatically places BUY and SELL trades based on structured candle confirmation, EMA trend alignment, and session-based filters. The system simulates real-time execution with precise Stop Loss and Take Profit levels.

📌 Built for traders seeking to simulate clean intraday logic with fully automated entries and performance metrics.

🧠 Core Logic & Strategy Conditions

✅ BUY Signal Conditions:

Price is above the EMA200

The last 3 candles are bullish (close > open)

The signal occurs within the defined session window (NY time)

Daily trade limit has not been exceeded

If all are true, a BUY order is executed at market, with SL and TP set immediately.

🔻 SELL Signal Conditions (Optional):

Exactly inverse to BUY (below EMA + 3 bearish candles). Disabled by default.

🕐 Operational Time Filter (New York Time)

You can fully customize your intraday window:

Start Time: e.g., 01:15 NY

End Time: e.g., 16:00 NY

The system evaluates signals only within this range, even across midnight if configured.

🔁 Trade Management System

One trade at a time per signal

Trades include a Stop Loss (SL) and Take Profit (TP) based on pip distance

Trade result is calculated automatically

Each signal is shown with a triangle marker (BUY only, by default)

🧪 Backtest Accuracy

This version uses:

strategy.order() for entries

strategy.exit() for SL and TP

strategy.close_all() at the configured manual closing time

This ensures realistic behavior in the TradingView strategy tester.

⚙️ Flow Summary (Step-by-Step)

On every bar, check:

Is the time within the operational session?

Is the price above the EMA?

Are the last 3 candles bullish?

If conditions met → A BUY trade is opened:

SL = entry – X pips

TP = entry + Y pips

Trade closes:

If SL or TP is hit

Or at the configured manual close time (e.g., 16:00 NY)

📊 Settings Overview

Timeframe: 1-hour (ideal)

SL/TP: Configurable in pips

Max trades/day: User-defined (default = 99 = unlimited)

Manual close: Adjustable by time

Entry type: Market (not limit)

Visuals: Plotshape triangle for BUY entry

👨💻 Credits:

💡 Developed by: LANZ

🧠 Strategy logic & execution: LANZ

✅ Designed for: Clean backtesting, clarity in execution, and intraday logic simulation

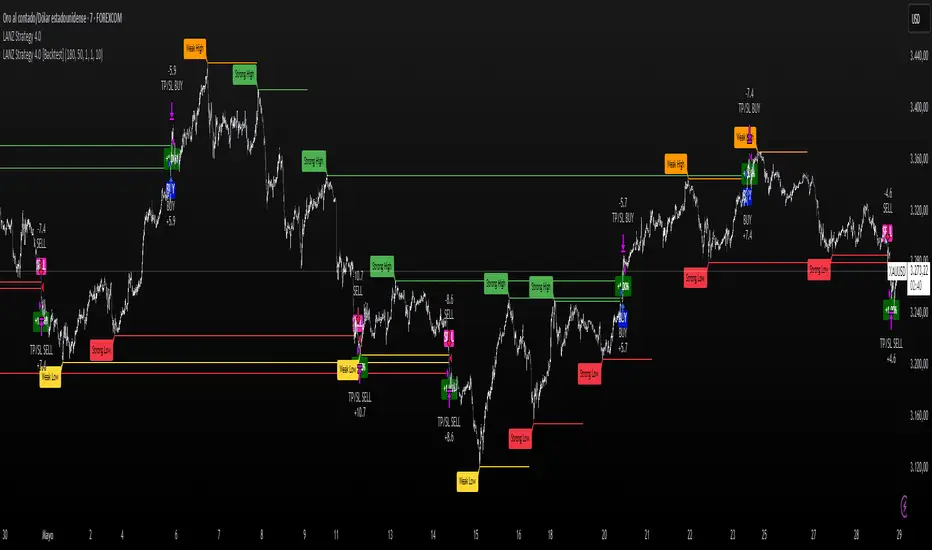

LANZ Strategy 4.0 [Backtest]🔷 LANZ Strategy 4.0 — Strategy Execution Based on Confirmed Structure + Risk-Based SL/TP

LANZ Strategy 4.0 is the official backtesting engine for the LANZ Strategy 4.0 trading logic. It simulates real-time executions based on breakout of Strong/Weak Highs or Lows, using a consistent structural system with SL/TP dynamically calculated per trade. With integrated risk management and lot size logic, this script allows traders to validate LANZ Strategy 4.0 performance with real strategy metrics.

🧠 Core Components:

Confirmed Breakout Entries: Trades are executed only when price breaks the most recent structural level (Strong High or Strong Low), detected using swing pivots.

Dynamic SL and TP Logic: SL is placed below/above the breakout point with a customizable buffer. TP is defined using a fixed Risk-Reward (RR) ratio.

Capital-Based Risk Management: Lot size is calculated based on account equity, SL distance, and pip value (e.g. $10 per pip on XAUUSD).

Clean and Controlled Executions: Only one trade is active at a time. No new entries are allowed until the current position is closed.

📊 Visual Features:

Automatic plotting of Entry, SL, and TP levels.

Full control of swing sensitivity (swingLength) and SL buffer.

SL and TP lines extend visually for clarity of trade risk and reward zones.

⚙️ How It Works:

Detects pivots and classifies trend direction.

Waits for breakout above Strong High (BUY) or below Strong Low (SELL).

Calculates dynamic SL and TP based on buffer and RR.

Computes trade size automatically based on risk per trade %.

Executes entry and manages exits via strategy engine.

📝 Notes:

Ideal for evaluating the LANZ Strategy 4.0 logic over historical data.

Must be paired with the original indicator (LANZ Strategy 4.0) for live trading.

Best used on assets with clear structural behavior (gold, indices, FX).

📌 Credits:

Backtest engine developed by LANZ based on the official rules of LANZ Strategy 4.0. This script ensures visual and logical consistency between live charting and backtesting simulations.

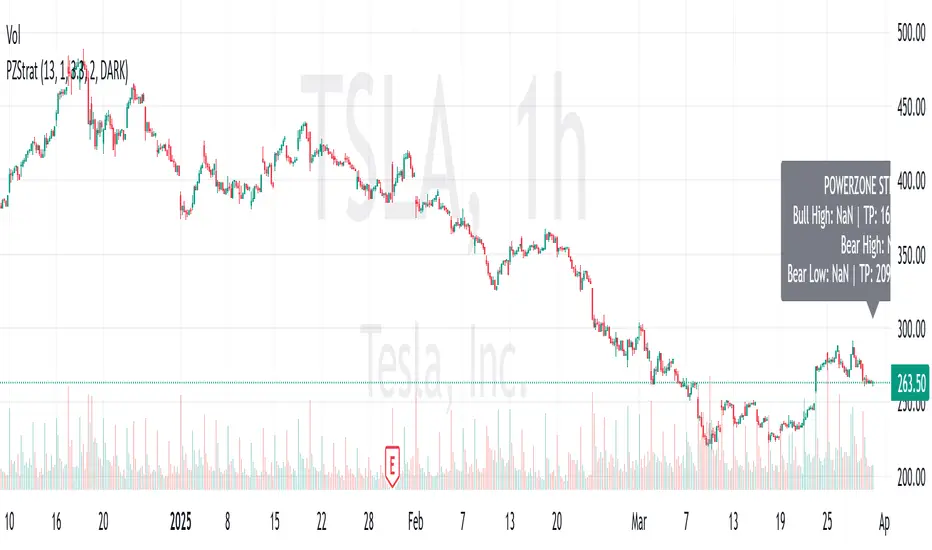

PowerZone Trading StrategyExplanation of the PowerZone Trading Strategy for Your Users

The PowerZone Trading Strategy is an automated trading strategy that detects strong price movements (called "PowerZones") and generates signals to enter a long (buy) or short (sell) position, complete with predefined take profit and stop loss levels. Here’s how it works, step by step:

1. What is a PowerZone?

A "PowerZone" (PZ) is a zone on the chart where the price has shown a significant and consistent movement over a specific number of candles (bars). There are two types:

Bullish PowerZone (Bullish PZ): Occurs when the price rises consistently over several candles after an initial bearish candle.

Bearish PowerZone (Bearish PZ): Occurs when the price falls consistently over several candles after an initial bullish candle.

The code analyzes:

A set number of candles (e.g., 5, adjustable via "Periods").

A minimum percentage move (adjustable via "Min % Move for PowerZone") to qualify as a strong zone.

Whether to use the full candle range (highs and lows) or just open/close prices (toggle with "Use Full Range ").

2. How Does It Detect PowerZones?

Bullish PowerZone:

Looks for an initial bearish candle (close below open).

Checks that the next candles (e.g., 5) are all bullish (close above open).

Ensures the total price movement exceeds the minimum percentage set.

Defines a range: from the high (or open) to the low of the initial candle.

Bearish PowerZone:

Looks for an initial bullish candle (close above open).

Checks that the next candles are all bearish (close below open).

Ensures the total price movement exceeds the minimum percentage.

Defines a range: from the high to the low (or close) of the initial candle.

These zones are drawn on the chart with lines: green or white for bullish, red or blue for bearish, depending on the color scheme ("DARK" or "BRIGHT").

3. When Does It Enter a Trade?

The strategy waits for a breakout from the PowerZone range to enter a trade:

Buy (Long): When the price breaks above the high of a Bullish PowerZone.

Sell (Short): When the price breaks below the low of a Bearish PowerZone.

The position size is set to 100% of available equity (adjustable in the code).

4. Take Profit and Stop Loss

Take Profit (TP): Calculated as a multiple (adjustable via "Take Profit Factor," default 1.5) of the PowerZone height. For example:

For a buy, TP = Entry price + (PZ height × 1.5).

For a sell, TP = Entry price - (PZ height × 1.5).

Stop Loss (SL): Calculated as a multiple (adjustable via "Stop Loss Factor," default 1.0) of the PZ height, placed below the range for buys or above for sells.

5. Visualization on the Chart

PowerZones are displayed with lines on the chart (you can hide them with "Show Bullish Channel" or "Show Bearish Channel").

An optional info panel ("Show Info Panel") displays key levels: PZ high and low, TP, and SL.

You can also enable brief documentation on the chart ("Show Documentation") explaining the basic rules.

6. Alerts

The code generates automatic alerts in TradingView:

For a bullish breakout: "Bullish PowerZone Breakout - LONG!"

For a bearish breakdown: "Bearish PowerZone Breakdown - SHORT!"

7. Customization

You can tweak:

The number of candles to detect a PZ ("Periods").

The minimum percentage move ("Min % Move").

Whether to use highs/lows or just open/close ("Use Full Range").

The TP and SL factors.

The color scheme and what elements to display on the chart.

Practical Example

Imagine you set "Periods = 5" and "Min % Move = 2%":

An initial bearish candle appears, followed by 5 consecutive bullish candles.

The total move exceeds 2%.

A Bullish PowerZone is drawn with a high and low.

If the price breaks above the high, you enter a long position with a TP 1.5 times the PZ height and an SL equal to the height below.

The system executes the trade and exits automatically at TP or SL.

Conclusion

This strategy is great for capturing strong price movements after consolidation or momentum zones. It’s automated, visual, and customizable, making it useful for both beginner and advanced traders. Try it out and adjust it to fit your trading style!

Smart Money Breakouts [iskess 01-02 11:05]This is an big update to the excellent Smart Money Breakout Script published in Oct 2023 by ChartPrime who, to my knowledge, was the original author.

FULL CREDIT GOES TO CHARTPRIME FOR THIS ORIGINAL WORK.

Per the moderator's rules, you will find below a meaningful, detailed self-contained description that does not rely on delegation to the open source code or links to other content. You will find in the description details on what the script does, how it does that, how to use it, and how it is original.

The "Smart Money Breakouts" indicator is designed to identify breakouts based on changes in character (CHOCH) or breaks of structure (BOS) patterns, facilitating automated trading with user-defined Take Profit (TP) level.

The indicator incorporates essential elements such as volume analysis and a data table to assist traders in optimizing their strategies.

🔸Breakout Detection:

The indicator scans price movements for "Change in Character" (CHOCH) and "Break of Structure" (BOS) patterns, signaling potential breakout opportunities in the market.

🔸User-Defined TP/SL :

Traders can customize the Take Profit (TP) and Stop Loss (SL) through the indicator settings, with these levels dynamically calculated based on the Average True Range (ATR). This allows for precise risk management and profit targets that adapt to market volatility. Traders can also select the lookback period for the TP/SL calculations.

🔸Volume Analysis and Trade Direction Specific Analysis:

The indicator includes a volume checker that provides valuable insights into the strength of the breakout, taking into account trade direction.

🔸If the volume label is red and the trade is long, it suggests a higher likelihood of hitting the Stop Loss (SL).

🔸If the volume label is green and the trade is long, it indicates a higher probability of hitting the Take Profit (TP).

🔸For short trades, a red volume label suggests a higher likelihood of hitting TP, while a green label suggests a higher likelihood of hitting SL.

🔸A yellow volume label suggests that the volume is inconclusive, neither favoring bullish nor bearish movements.

🔸Data Table:

The indicator features a data table that keeps track of the number of winning and losing trades for specific timeframes or configurations. It also shows the percentage of profits vs losses, and the overall profit/loss for the selected lookback period.

This table serves as a valuable tool for traders to analyze performance and discover optimal settings and timeframes.

The "Smart Money Breakouts" indicator provides traders with a comprehensive solution for breakout trading, combining technical analysis of changes in character and breaks of structure, volume insights, and performance tracking while dynamically adjusting TP and SL levels based on market volatility through the ATR.

This version of the script is a "significant improvement" from Chart Prime's original work in the following ways:

- A selectable range of candles for the profit/loss calculations to look back on.

- An updated table that includes the percentage of wins/losses, and and overall P&L during the selected lookback range.

- The user can now select only Long trades, Short trades, or both.

- The percentage gain/loss is now indicated for every trade on the chart.

- The user can now select a different multiplier for Stop Loss or Take Profit thresholds.

Daily Single Trade [SMRT Algo]The Daily Single Trade Indicator by SMRT Algo is a powerful yet simple tool designed for traders who value precision, discipline, and a focus on high-quality trade setups. With a unique approach, this indicator identifies just one signal daily, making it ideal for traders who prefer a structured and stress-free trading routine.

Please note that this indicator only works for timeframes below 1H.

Key Features:

Market Open & Pre-Market Analysis: The indicator focuses on the market’s opening range and identifies breakout opportunities based on price action during these critical periods.

Customizable Risk-Reward Ratio: Plan your trades with precision by setting your desired RR, ensuring that your take-profit (TP) levels are multiples of your stop-loss (SL). Stop loss is not shown with this indicator.

Price Offset for SL: Add a customizable buffer to your SL and TP levels. This offset accounts for market volatility, reducing the chances of premature stop-outs while maintaining alignment with your trading plan.

Increasing this value will lead to a greater invisible stop loss, which will increase the TP size. The opposite is occurs when decreasing this value (less than 0). If you set it as 2.5 for example for TSLA: price is 340 and SL is 330 for example, SL becomes 327.5. This calculation will then be applied to calculate the TP.

In simple terms, if the offset is positive, SL becomes larger, TP becomes larger as well.

Exit Point Visibility: Display exit points on your chart to better visualize trade targets and stop levels.

Adjustable Market Open Time: Easily modify the market open hour and minute to suit your asset’s trading session. For example, U.S. stock traders can set the market open time to 9:30 AM EST (UTC-5).

By providing a single signal each day, the indicator minimizes overtrading and keeps your focus on the best opportunities.

With predefined SL, TP, and RR settings, the indicator fosters disciplined trading, reducing the influence of emotional decision-making. Whether you’re trading stocks, indices, or forex, the customizable market open time and RR ratio make this indicator versatile and adaptable.

The combination of precise SL and TP calculations with offset pip adjustments helps protect your trades from market noise while maintaining a favorable RR.

Perfect for those who can’t monitor markets all day, the single-signal approach allows you to execute a high-quality trade and move on with your day.

How to Use:

Set the Market Open Time: Adjust the open time to align with your asset’s session. For example, set 9:30 AM EST for U.S. stocks.

Define Your Risk-Reward Ratio: Choose an RR multiple (e.g., 1:2 or 1:3) that aligns with your risk tolerance and trading goals.