Range Trading StrategyOVERVIEW

The Range Trading Strategy is a systematic trading approach that identifies price ranges

from higher timeframe candles or trading sessions, tracks pivot points, and generates

trading signals when range extremes are mitigated and confirmed by pivot levels.

CORE CONCEPT

The strategy is based on the principle that when a candle (or session) closes within the

range of the previous candle (or session), that previous candle becomes a "range" with

identifiable high and low extremes. When price breaks through these extremes, it creates

trading opportunities that are confirmed by pivot levels.

RANGE DETECTION MODES

1. HTF (Higher Timeframe) Mode:

Automatically selects a higher timeframe based on the current chart timeframe

Uses request.security() to fetch HTF candle data

Range is created when an HTF candle closes within the previous HTF candle's range

The previous HTF candle's high and low become the range extremes

2. Sessions Mode:

- Divides the trading day into 4 sessions (UTC):

* Session 1: 00:00 - 06:00 (6 hours)

* Session 2: 06:00 - 12:00 (6 hours)

* Session 3: 12:00 - 20:00 (8 hours)

* Session 4: 20:00 - 00:00 (4 hours, spans midnight)

- Tracks high, low, and close for each session

- Range is created when a session closes within the previous session's range

- The previous session's high and low become the range extremes

PIVOT DETECTION

Pivots are detected based on candle color changes (bullish/bearish transitions):

1. Pivot Low:

Created when a bullish candle appears after a bearish candle

Pivot low = minimum of the current candle's low and previous candle's low

The pivot bar is the actual bar where the low was formed (current or previous bar)

2. Pivot High:

Created when a bearish candle appears after a bullish candle

Pivot high = maximum of the current candle's high and previous candle's high

The pivot bar is the actual bar where the high was formed (current or previous bar)

IMPORTANT: There is always only ONE active pivot high and ONE active pivot low at any

given time. When a new pivot is created, it replaces the previous one.

RANGE CREATION

A range is created when:

(HTF Mode) An HTF candle closes within the previous HTF candle's range AND a new HTF

candle has just started

(Sessions Mode) A session closes within the previous session's range AND a new session

has just started

Or Range Can Be Created when the Extreme of Another Range Gets Mitigated and We Have a Pivot low Just Above the Range Low or Pivot High just Below the Range High

Range Properties:

rangeHigh: The high extreme of the range

rangeLow: The low extreme of the range

highStartTime: The timestamp when the range high was actually formed (found by looping

backwards through bars)

lowStartTime: The timestamp when the range low was actually formed (found by looping

backwards through bars)

highMitigated / lowMitigated: Flags tracking whether each extreme has been broken

isSpecial: Flag indicating if this is a "special range" (see Special Ranges section)

RANGE MITIGATION

A range extreme is considered "mitigated" when price interacts with it:

High is mitigated when: high >= rangeHigh (any interaction at or above the level)

Low is mitigated when: low <= rangeLow (any interaction at or below the level)

Mitigation can happen:

At the moment of range creation (if price is already beyond the extreme)

At any point after range creation when price touches the extreme

SIGNAL GENERATION

1. Pending Signals:

When a range extreme is mitigated, a pending signal is created:

a) BEARISH Pending Signal:

- Triggered when: rangeHigh is mitigated

- Confirmation Level: Current pivotLow

- Signal is confirmed when: close < pivotLow

- Stop Loss: Current pivotHigh (at time of confirmation)

- Entry: Short position

Signal Confirmation

b) BULLISH Pending Signal:

- Triggered when: rangeLow is mitigated

- Confirmation Level: Current pivotHigh

- Signal is confirmed when: close > pivotHigh

- Stop Loss: Current pivotLow (at time of confirmation)

- Entry: Long position

IMPORTANT: There is only ever ONE pending bearish signal and ONE pending bullish signal

at any given time. When a new pending signal is created, it replaces the previous one

of the same type.

2. Signal Confirmation:

- Bearish: Confirmed when price closes below the pivot low (confirmation level)

- Bullish: Confirmed when price closes above the pivot high (confirmation level)

- Upon confirmation, a trade is entered immediately

- The confirmation line is drawn from the pivot bar to the confirmation bar

TRADE EXECUTION

When a signal is confirmed:

1. Position Management:

- Any existing position in the opposite direction is closed first

- Then the new position is entered

2. Stop Loss:

- Bearish (Short): Stop at pivotHigh

- Bullish (Long): Stop at pivotLow

3. Take Profit:

- Calculated using Risk:Reward Ratio (default 2:1)

- Risk = Distance from entry to stop loss

- Target = Entry ± (Risk × R:R Ratio)

- Can be disabled with "Stop Loss Only" toggle

4. Trade Comments:

- "Range Bear" for short trades

- "Range Bull" for long trades

SPECIAL RANGES

Special ranges are created when:

- A range high is mitigated AND the current pivotHigh is below the range high

- A range low is mitigated AND the current pivotLow is above the range low

In these cases:

- The pivot value is stored in an array (storedPivotHighs or storedPivotLows)

- A "special range" is created with only ONE extreme:

* If pivotHigh < rangeHigh: Creates a range with rangeHigh = pivotLow, rangeLow = na

* If pivotLow > rangeLow: Creates a range with rangeLow = pivotHigh, rangeHigh = na

- Special ranges can generate signals just like normal ranges

- If a special range is mitigated on the creation bar or the next bar, it is removed

entirely without generating signals (prevents false signals)

Special Ranges

REVERSE ON STOP LOSS

When enabled, if a stop loss is hit, the strategy automatically opens a trade in the

opposite direction:

1. Long Stop Loss Hit:

- Detects when: position_size > 0 AND position_size <= 0 AND low <= longStopLoss

- Action: Opens a SHORT position

- Stop Loss: Current pivotHigh

- Trade Comment: "Reverse on Stop"

2. Short Stop Loss Hit:

- Detects when: position_size < 0 AND position_size >= 0 AND high >= shortStopLoss

- Action: Opens a LONG position

- Stop Loss: Current pivotLow

- Trade Comment: "Reverse on Stop"

The reverse trade uses the same R:R ratio and respects the "Stop Loss Only" setting.

VISUAL ELEMENTS

1. Range Lines:

- Drawn from the time when the extreme was formed to the mitigation point (or current

time if not mitigated)

- High lines: Blue (or mitigated color if mitigated)

- Low lines: Red (or mitigated color if mitigated)

- Style: SOLID

- Width: 1

2. Confirmation Lines:

- Drawn when a signal is confirmed

- Extends from the pivot bar to the confirmation bar

- Bearish: Red, solid line

- Bullish: Green, solid line

- Width: 1

- Can be toggled on/off

STRATEGY SETTINGS

1. Range Detection Mode:

- HTF: Uses higher timeframe candles

- Sessions: Uses trading session boundaries

2. Auto HTF:

- Automatically selects HTF based on current chart timeframe

- Can be disabled to use manual HTF selection

3. Risk:Reward Ratio:

- Default: 2.0 (2:1)

- Minimum: 0.5

- Step: 0.5

4. Stop Loss Only:

- When enabled: Trades only have stop loss (no take profit)

- Trades close on stop loss or when opposite signal confirms

5. Reverse on Stop Loss:

- When enabled: Hitting a stop loss opens opposite trade with stop at opposing pivot

6. Max Ranges to Display:

- Limits the number of ranges kept in memory

- Oldest ranges are purged when limit is exceeded

KEY FEATURES

1. Dynamic Pivot Tracking:

- Pivots update on every candle color change

- Always maintains one high and one low pivot

2. Range Lifecycle:

- Ranges are created when price closes within previous range

- Ranges are tracked until mitigated

- Mitigation creates pending signals

- Signals are confirmed by pivot levels

3. Signal Priority:

- Only one pending signal of each type at a time

- New signals replace old ones

- Confirmation happens on close of bar

4. Position Management:

- Closes opposite positions before entering new trades

- Tracks stop loss levels for reverse functionality

- Respects pyramiding = 1 (only one position per direction)

5. Time-Based Drawing:

- Uses time coordinates instead of bar indices for line drawing

- Prevents "too far from current bar" errors

- Lines can extend to any historical point

USAGE NOTES

- Best suited for trending and ranging markets

- Works on any timeframe, but HTF mode adapts automatically

- Sessions mode is ideal for intraday trading

- Pivot detection requires clear candle color changes

- Range detection requires price to close within previous range

- Signals are generated on bar close, not intra-bar

The strategy combines range identification, pivot tracking, and signal confirmation to

create a systematic approach to trading breakouts and reversals based on price structure, past performance does not in any way predict future performance

Cari dalam skrip untuk "track"

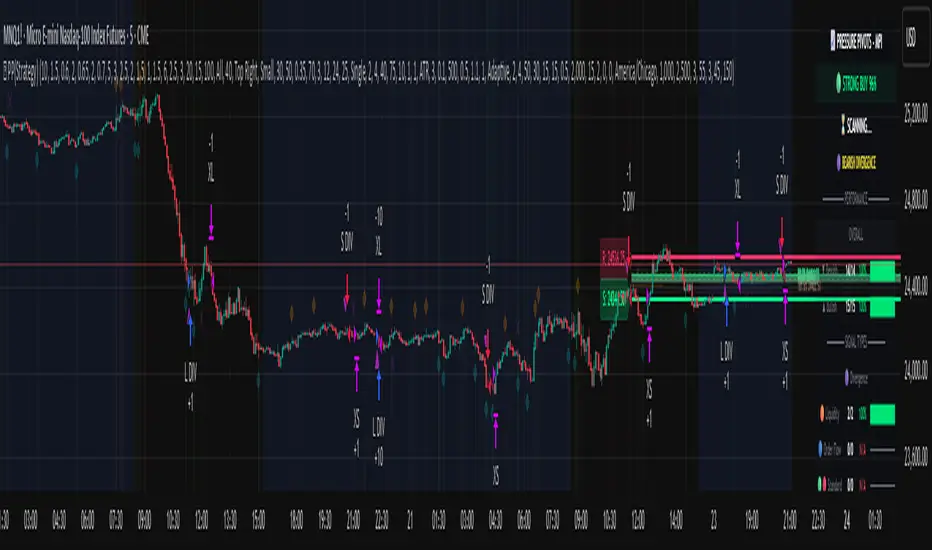

Pressure Pivots - MPI (Strategy)⇋ PRESSURE PIVOTS — MARKET PRESSURE INDEX STRATEGY

A comprehensive reversal trading system that combines order flow pressure analysis, multi-factor confluence detection, and adaptive machine learning to identify high-probability turning points in liquid markets.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

CORE INNOVATION: MARKET PRESSURE INDEX (MPI)

Traditional indicators measure price movement. The Market Pressure Index measures the force behind the movement.

How MPI Works:

Every bar tells two stories through volume distribution:

• Buy Pressure: Volume × (Close - Low) / (High - Low)

• Sell Pressure: Volume × (High - Close) / (High - Low)

• Net Pressure: Buy Pressure - Sell Pressure

This raw pressure is then normalized against baseline activity to create the bounded MPI (-1.0 to +1.0):

• Smooth Pressure: EMA(Net Pressure, period)

• Baseline Activity: SMA(|Net Pressure|, period × 2)

• MPI: (Smooth Pressure / Baseline) × Sensitivity

What MPI Reveals:

MPI > +0.7: Extreme buy pressure → Exhaustion potential

MPI = +0.2 to +0.7: Healthy bullish momentum

MPI = -0.2 to +0.2: Neutral/balanced pressure

MPI = -0.7 to -0.2: Healthy bearish momentum

MPI < -0.7: Extreme sell pressure → Exhaustion potential

Why It Works:

Two bars can both move 10 points, but if one closes at the high on high volume (aggressive buying) and the other closes mid-range on average volume (weak buying), only MPI distinguishes between sustainable momentum and exhaustion. This volume-weighted pressure analysis reveals conviction behind price moves—the key to timing reversals.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SEVEN-FACTOR CONFLUENCE SYSTEM

MPI extremes alone aren't enough. The system requires multiple independent confirmations through weighted scoring:

1. DIVERGENCE (Weight: 3.0) — Premium Signal Type: DIV

Price makes new high but MPI makes lower high (or inverse for bullish)

• Detection: Tracks pivots with 5-bar lookback, compares price vs MPI at pivot points

• Signal: Purple triangles, highest weight (pressure weakening while price extends)

2. LIQUIDITY SWEEP (Weight: 2.5) — Premium Signal Type: LIQ

Price breaks swing high/low within 0.3 ATR then reverses

• Detection: Break within tolerance + close back through level

• Signal: Orange triangles, second-highest weight (stop hunt reversal)

3. ORDER FLOW IMBALANCE (Weight: 2.0) — Premium Signal Type: OF

Aggressive buying/selling 50% above normal

• Detection: EMA(aggressive volume) vs SMA(imbalance) threshold

• Signal: Aqua triangles, institutional positioning

4. VELOCITY EXHAUSTION (Weight: 1.5)

Parabolic move (2+ ATRs in 3 bars) + extreme MPI

• Detection: |3-bar price change / ATR| > threshold + MPI > ±0.5

• Indicates: Momentum deceleration, blow-off top/bottom

5. WICK REJECTION (Weight: 1.5)

Single bar: wick > 60% of range, or sequence: 2 bars with 40% + 30% wicks

• Detection: Shooting stars (bearish) or hammers (bullish)

• Indicates: Intrabar rejection, battle won by opposing side

6. VOLUME SPIKE (Weight: 1.0)

Volume > 20-bar average × multiplier (default: 2.0x)

• Detection: Participation surge confirmation

• Lowest weight: Can be manipulated, better as confirmation

7. POSITION FACTOR (Weight: 1.0)

At 10-bar highest (bearish) or lowest (bullish)

• Detection: Structural positioning for reversal

• Base requirement: Must be at extreme to score

Scoring Logic:

Premium Signals (DIV/LIQ/OF): Must score ≥6.0 (default premiumThreshold)

Standard Signals (STD): Must score ≥4.0 (default standardThreshold)

Example Scoring:

Divergence (3.0) + Liquidity Sweep (2.5) + Volume (1.0) = 6.5 → FIRES (DIV signal)

Recent High (1.0) + Wick (1.5) + Volume (1.0) + Velocity (1.5) = 5.0 → FIRES (STD signal)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ADAPTIVE LEARNING ENGINE

Unlike static strategies, this system learns from every trade and optimizes itself.

Performance Tracking:

Every trade records:

• Entry Score: Confluence level at entry

• Signal Type: DIV / LIQ / OF / STD

• Win/Loss: Boolean outcome

• R-Multiple: (Exit - Entry) / (Entry - Stop)

• MAE: Maximum Adverse Excursion (worst drawdown)

• MFE: Maximum Favorable Excursion (best profit reached)

Three Adaptive Parameters:

1. Signal Threshold Adaptation

If Win Rate < Target (45%): RAISE threshold → fewer signals, better quality

If Win Rate > Target + 10% AND good R: LOWER threshold → more signals, profitable

2. Stop Distance Adaptation

If Avg MAE > 0.85 AND WR < 50%: WIDEN stops → reduce premature exits

If Avg MAE < 0.4 AND WR > 55%: TIGHTEN stops → reduce risk

3. Target Distance Adaptation

If Avg MFE > Target × 1.5: EXTEND targets → capture more of runners

If Avg MFE < Target × 0.7: SHORTEN targets → take profits faster

Signal Type Filtering:

The system tracks performance by type (DIV/LIQ/OF/STD):

• If Type WR < 40% AND Avg R < 0.8: Type DISABLED

• If Type WR ≥ 40% OR Avg R ≥ 0.8: Type RE-ENABLED

Example: If OF signals consistently lose while DIV signals win, system automatically stops taking OF signals and focuses on DIV.

Warmup Period:

First 30 trades (default) gather baseline data with relaxed thresholds. After warmup, full adaptation activates.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPLETE POSITION MANAGEMENT

Dynamic Position Sizing:

Base Contracts = (Equity × Risk%) / (Stop Distance × Point Value)

Then multiplied by:

• Score Bonus: Up to +50% for highest-scoring signals

• Signal Type Bonus: DIV signals +50%, LIQ signals +30%

• Streak Multiplier: After 3 losses: 50% reduction, After 3 wins: 25% increase

Example: High-scoring DIV signal on winning streak = 3-4× larger position than weak STD signal on losing streak

Entry Modes:

Single Entry: Full size at once, exit at TP2 (or partial at TP1)

Tiered Entry: 40% at TP1 (2R), 60% at TP2 (4R adaptive)

Stop Management (3 Modes):

Structural: Beyond recent 20-bar swing high/low + buffer

ATR: Fixed ATR multiplier (default: 2.0 ATR, then adapts)

Hybrid: Attempt structural, fallback to ATR if invalid

Plus:

• Breakeven: Move stop to entry ± 1 tick when 1R reached

• Trailing: Activate when 1.5R reached, trail 0.8R behind price

• Max Loss Override: Cap dollar risk regardless of calculation

Target Management:

Fixed Mode: TP1 = 2R, TP2 = 4R

Adaptive Mode: TP1 = 2R fixed, TP2 adapts based on MFE analysis

Partial Exits: Default 50% at TP1, remainder at TP2 or trailing stop

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPREHENSIVE RISK CONTROLS

Daily Limits:

• Max Daily Loss: $2,000 default → HALT trading

• Max Daily Trades: 15 default → prevent overtrading

• Max Concurrent: 2 positions → limit correlation risk

Session Controls:

• Trading Hours: Specify start/end times + timezone

• Weekend Block: Optional (avoid crypto weekend volatility)

Prop Firm Protection (Live Trading Only):

• Daily Loss Limit: Stricter of general or prop limit ($1,000 default)

• Trailing Drawdown: Tracks high water mark, HALTS if breach ($2,500 default)

• Reset on Reload: Optional high water mark reset

Liquidity Filter (Optional):

• Time-Based: Avoid first/last X minutes of session

• Volume-Based: Require minimum volume ratio (0.5× average default)

Market Regime Filter (Optional):

• ADX-Based: Only trade when ADX > threshold (trending)

• Block: Consolidation (ADX < 20) or Transitional regimes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

REAL-TIME DASHBOARD

MPI Gauge Section:

Shows current pressure: 🟢 STRONG BUY (+0.5 to +1.0), 🟩 BUY PRESSURE (+0.2 to +0.5), ⚪ NEUTRAL (-0.2 to +0.2), 🟥 SELL PRESSURE (-0.5 to -0.2), 🔴 STRONG SELL (-1.0 to -0.5)

Signal Status Section:

• Active Signals: "🔴 DIV SELL" (purple background), "🟢 LIQ BUY" (orange), "🔵 OF SELL" (aqua), "🟢 STD BUY" (green)

• Warnings: "⚠️ BEAR WARNING" / "⚠️ BULL WARNING" (yellow) — setup forming, not full signal

• Scanning: "⏳ SCANNING..." (gray) — no signal active

• Confidence Bar: Visual score display "██████░░░░" showing confluence strength

Divergence Indicator:

"🟣 BEARISH DIVERGENCE" or "🟡 BULLISH DIVERGENCE" when detected

Performance Statistics:

• Overall Win Rate: Wins/Total with visual bar (lime ≥70%, yellow 50-70%, red <50%)

• Directional: Bearish vs Bullish win rates separately

• By Signal Type: DIV / LIQ / OF / STD individual performance tracking

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

KEY PARAMETERS EXPLAINED

🎯 Pressure Engine:

• MPI Period (5-50, default: 14): Smoothing period — lower for scalping, higher for position trading

• MPI Sensitivity (0.5-5.0, default: 1.5): Amplification — lower compresses range, higher more extremes

🔍 Detection:

• Wick Threshold (0.3-0.9, default: 0.6): Minimum wick-to-range ratio for rejection

• Volume Spike (1.2-3.0x, default: 2.0): Multiplier above average for spike

• Aggressive Ratio (0.5-0.9, default: 0.65): Close position in range for aggressive orders

• Velocity Threshold (1.0-5.0 ATR, default: 2.0): ATR-normalized move for exhaustion

• MPI Extreme (0.5-0.95, default: 0.7): Level considered overbought/oversold

⚖️ Weights:

• Divergence: 3.0 (highest — pressure weakening)

• Liquidity: 2.5 (second — stop hunts)

• Order Flow: 2.0 (institutional positioning)

• Velocity: 1.5 (momentum exhaustion)

• Wick: 1.5 (rejection patterns)

• Volume: 1.0 (lowest — can be manipulated)

🎚️ Thresholds:

• Premium (4.0-15.0, default: 6.0): Score for DIV/LIQ/OF signals

• Standard (2.0-8.0, default: 4.0): Score for STD signals

• Warning Confluence (1-4, default: 2): Factors for yellow diamond warnings

🧬 Adaptive:

• Enable (true/false, default: true): Master learning switch

• Warmup Trades (5-100, default: 30): Data collection before adaptation

• Lookback (20-200, default: 50): Recent trades for performance calculation

• Adapt Speed (0.05-0.50, default: 0.15): Parameter adjustment rate

• Target Win Rate (30-70%, default: 45%): Optimization goal

• Target R-Multiple (0.5-5.0, default: 1.5): Risk/reward goal

💼 Position:

• Base Risk (0.1-10.0%, default: 1.5%): Equity risked per trade

• Max Contracts (1-100, default: 10): Hard position limit

• DIV Bonus (1.0-3.0x, default: 1.5): Size multiplier for divergence signals

• LIQ Bonus (1.0-3.0x, default: 1.3): Size multiplier for liquidity signals

🛡️ Stops:

• Mode (Structural/ATR/Hybrid, default: ATR): Stop placement method

• ATR Multiplier (0.5-5.0, default: 2.0): Stop distance in ATRs (adapts)

• Breakeven at (0.3-3.0R, default: 1.0R): When to move stop to entry

• Trail Trigger (0.5-5.0R, default: 1.5R): When to activate trailing

• Trail Offset (0.3-3.0R, default: 0.8R): Distance behind price

🎯 Targets:

• Mode (Fixed/Adaptive, default: Fixed): Target placement method

• TP1 (0.5-10.0R, default: 2.0R): First target for partial exit

• TP2 (1.0-15.0R, default: 4.0R): Final target (adapts in adaptive mode)

• Partial % (0-100%, default: 50%): Position percentage to exit at TP1

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

PROFESSIONAL USAGE PROTOCOL

Phase 1: Paper Trading (Weeks 1-4)

• Setup: Default settings, all adaptive features ON, 0.5% base risk

• Goal: 30+ trades for warmup, observe MPI behavior and signal frequency

• Adjust: MPI sensitivity if stuck near neutral or always at extremes

• Threshold: Raise/lower if too many/few signals

Phase 2: Micro Live (Weeks 5-8)

• Requirements: WR >43%, at least one type >55%, Avg R >0.8

• Setup: 10-25% intended size, 0.5-1.0% risk, 1 position max

• Focus: Execution quality, match dashboard performance

• Journal: Screenshot every signal, track outcomes

Phase 3: Full Scale (Month 3+)

• Requirements: WR >45% over 50+ trades, Avg R >1.2, drawdown <15%

• Progression: Months 3-4 (1.0-1.5% risk), 5-6 (1.5-2.0%), 7+ (1.5-2.5%)

• Maintenance: Weekly dashboard review, monthly deep analysis

• Warnings: Reduce size if WR drops >10%, consecutive losses >7, or drawdown >20%

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DEVELOPMENT INSIGHTS

The Pressure Insight: Emerged from analyzing intrabar volume distribution. Within every candlestick, volume accumulates at different price levels. MPI deconstructs this to reveal conviction behind moves.

The Confluence Challenge: Early versions using MPI extremes alone achieved only 42% win rate. The seven-factor confluence system emerged from testing which combinations produced reliable reversals. Divergence + liquidity sweep became the strongest setup (68% win rate in isolation).

The Adaptive Breakthrough: Per-signal-type performance tracking revealed DIV signals winning at 71% while OF signals languished at 38%. Adaptive filtering disabled weak types automatically, recovering win rate from 39% to 54% during the 2022 volatility spike.

The Position Sizing Revelation: Dynamic sizing based on signal quality and recent performance increased Sharpe ratio from 1.2 to 1.9 while decreasing max drawdown from 18% to 12% over 500 trades. Bigger positions on better signals = geometric edge amplification.

The Risk Control Lesson: Testing with $50K accounts revealed catastrophic failure modes: daily loss cascades, overtrading commission bleed, weekend gap blowouts. Multi-layer controls (daily limits, concurrent caps, prop firm protection) became essential.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

LIMITATIONS & ASSUMPTIONS

What This Is NOT:

• NOT a Holy Grail: Typical performance 52-58% WR, 1.3-1.8 avg R, probabilistic edge

• NOT Predictive: Identifies high-probability conditions, doesn't forecast prices

• NOT Market-Agnostic: Best on liquid auction-driven markets (futures, forex, major crypto)

• NOT Hands-Off: Requires oversight for news events, gaps, system anomalies

• NOT Immune to Regime Changes: Adaptive engine helps but cannot predict black swans

Critical Assumptions:

1. Volume reflects intent (valid for regulated markets, violated by wash trading)

2. Pressure extremes mean-revert (true in ranging/exhaustion, fails in paradigm shifts)

3. Stop hunts exist (valid in liquid markets, less in thin/random walk periods)

4. Past patterns persist (valid in stable regimes, fails when structure fundamentally changes)

Works Best On: Major futures (ES, NQ, CL), liquid forex pairs (EUR/USD, GBP/USD), large-cap stocks, BTC

Performs Poorly On: Low-volume stocks, illiquid crypto pairs, news-driven headline events

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

RISK DISCLOSURE

Trading futures, forex, and leveraged instruments involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. This strategy is provided for educational purposes only and should not be construed as financial advice.

The adaptive engine learns from historical data—there is no guarantee that past relationships will persist. Market conditions change, volatility regimes shift, and black swan events occur. No strategy can eliminate the risk of loss.

Users must validate performance on their specific instruments and timeframes before risking capital. The developer makes no warranties regarding profitability or suitability. Users assume all responsibility for trading decisions and outcomes.

"The market doesn't care about your indicators. It only cares about pressure—who's willing to pay more, who's desperate to sell. Find the exhaustion. Trade the reversal. Let the system learn the rest."

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

ATH대비 지정하락률에 도착 시 매수 - 장기홀딩 선물 전략(ATH Drawdown Re-Buy Long Only)본 스크립트는 과거 하락 데이터를 이용하여, 정해진 하락 %가 발생하는 경우 자기 자본의 정해진 %만큼을 진입하게 설계되어진 스트레티지입니다.

레버리지를 사용할 수 있으며 기본적으로 셋팅해둔 값이 내장되어있습니다.(자유롭게 바꿔서 쓰시면 됩니다.) 추가적으로 2번의 진입 외에도 다른 진입 기준, 진입 %를 설정하실 수 있으며 - ChatGPT에게 요청하면 수정해줄 것입니다.

실제 사용용도로는 KillSwitch 기능을 꺼주세요. 바 돋보기 기능을 켜주세요.

ATH Drawdown Re-Buy Long Only 전략 설명

1. 전략 개요

ATH Drawdown Re-Buy Long Only 전략은 자산의 역대 최고가(ATH, All-Time High)를 기준으로 한 하락폭(드로우다운)을 활용하여,

특정 구간마다 단계적으로 롱 포지션을 구축하는 자동 재매수(Long Only) 전략입니다.

본 전략은 다음과 같은 목적을 가지고 설계되었습니다.

급격한 조정 구간에서 체계적인 분할 매수 및 레버리지 활용

ATH를 기준으로 한 명확한 진입 규칙 제공

실시간으로

평단가

레버리지

청산가 추정

계좌 MDD

수익률

등을 시각적으로 제공하여 리스크와 포지션 상태를 직관적으로 확인할 수 있도록 지원

※ 본 전략은 교육·연구·백테스트 용도로 제공되며,

어떠한 형태의 투자 권유 또는 수익을 보장하지 않습니다.

2. 전략의 핵심 개념

2-1. ATH(역대 최고가) 기준 드로우다운

전략은 차트 상에서 항상 가장 높은 고가(High)를 ATH로 기록합니다.

새로운 고점이 형성될 때마다 ATH를 갱신하고, 해당 ATH를 기준으로 다음을 계산합니다.

현재 바의 저가(Low)가 ATH에서 몇 % 하락했는지

현재 바의 종가(Close)가 ATH에서 몇 % 하락했는지

그리고 사전에 설정한 두 개의 드로우다운 구간에서 매수를 수행합니다.

1차 진입 구간: ATH 대비 X% 하락 시

2차 진입 구간: ATH 대비 Y% 하락 시

각 구간은 ATH가 새로 갱신될 때마다 한 번씩만 작동하며,

새로운 ATH가 생성되면 다시 “1차 / 2차 진입 가능 상태”로 초기화됩니다.

2-2. 첫 포지션 100% / 300% 특수 규칙

이 전략의 중요한 특징은 **“첫 포지션 진입 시의 예외 규칙”**입니다.

전략이 현재 어떠한 포지션도 들고 있지 않은 상태에서

최초로 롱 포지션을 진입하는 시점(첫 포지션)에 대해:

기본적으로는 **자산의 100%**를 기준으로 포지션을 구축하지만,

만약 그 순간의 가격이 ATH 대비 설정값 이상(예: 약 –72.5% 이상 하락한 상황) 이라면

→ 자산의 300% 규모로 첫 포지션을 진입하도록 설계되어 있습니다.

이 규칙은 다음과 같이 동작합니다.

첫 진입이 1차 드로우다운 구간에서 발생하든,

첫 진입이 2차 드로우다운 구간에서 발생하든,

현재 하락폭이 설정된 기준 이상(예: –72.5% 이상) 이라면

→ “이 정도 하락이면 첫 진입부터 더 공격적으로 들어간다”는 의미로 300% 규모로 진입

그 이하의 하락폭이라면

→ 첫 진입은 100% 규모로 제한

즉, 전략은 다음 두 가지 모드로 동작합니다.

일반적인 상황의 첫 진입: 자산의 100%

심각한 드로우다운 구간에서의 첫 진입: 자산의 300%

이 특수 규칙은 깊은 하락에서는 공격적으로, 평소에는 상대적으로 보수적으로 진입하도록 설계된 것입니다.

3. 전략 동작 구조

3-1. 매수 조건

차트 상 High 기준으로 ATH를 추적합니다.

각 바마다 해당 ATH에서의 하락률을 계산합니다.

사용자가 설정한 두 개의 드로우다운 구간(예시):

1차 구간: 예를 들어 ATH – 50%

2차 구간: 예를 들어 ATH – 72.5%

각 구간에 대해 다음과 같은 조건을 확인합니다.

“이번 ATH 구간에서 아직 해당 구간 매수를 한 적이 없는 상태”이고,

현재 바의 저가(Low)가 해당 구간 가격 이하를 찍는 순간

→ 해당 바에서 매수 조건 충족으로 간주

실제 주문은:

해당 구간 가격에 맞춰 롱 포지션 진입(리밋/시장가 기반 시뮬레이션) 으로 처리됩니다.

3-2. ATH 갱신과 진입 기회 리셋

차트 상에서 새로운 고점(High)이 기존 ATH를 넘어서는 순간,

ATH가 갱신되고,

1차 / 2차 진입 여부를 나타내는 내부 플래그가 초기화됩니다.

이를 통해, 시장이 새로운 고점을 돌파해 나갈 때마다,

해당 구간에서 다시 한 번씩 1차·2차 드로우다운 진입 기회를 갖게 됩니다.

4. 포지션 사이징 및 레버리지

4-1. 계좌 자산(Equity) 기준 포지션 크기 결정

전략은 현재 계좌 자산을 다음과 같이 정의하여 사용합니다.

현재 자산 = 초기 자본 + 실현 손익 + 미실현 손익

각 진입 구간에서의 포지션 가치는 다음과 같이 결정됩니다.

1차 진입 구간:

“자산의 몇 %를 사용할지”를 설정값으로 입력

설정된 퍼센트를 계좌 자산에 곱한 뒤,

다시 전략 내 레버리지 배수(Leverage) 를 곱하여 실제 포지션 가치를 계산

2차 진입 구간:

동일한 방식으로, 독립된 퍼센트 설정값을 사용

즉, 포지션 가치는 다음과 같이 계산됩니다.

포지션 가치 = 현재 자산 × (해당 구간 설정 % / 100) × 레버리지 배수

그리고 이를 해당 구간의 진입 가격으로 나누어 실제 수량(토큰 단위) 를 산출합니다.

4-2. 첫 포지션의 예외 처리 (100% / 300%)

첫 포지션에 대해서는 위의 일반적인 퍼센트 설정 대신,

다음과 같은 고정 비율이 사용됩니다.

기본: 자산의 100% 규모로 첫 포지션 진입

단, 진입 시점의 ATH 대비 하락률이 설정값 이상(예: –72.5% 이상) 일 경우

→ 자산의 300% 규모로 첫 포지션 진입

이때 역시 다음 공식을 사용합니다.

포지션 가치 = 현재 자산 × (100% 또는 300%) × 레버리지

그리고 이를 가격으로 나누어 실제 진입 수량을 계산합니다.

이 규칙은:

첫 진입이 1차 구간이든 2차 구간이든 동일하게 적용되며,

“충분히 깊은 하락 구간에서는 첫 진입부터 더 크게,

평소에는 비교적 보수적으로” 라는 운용 철학을 반영합니다.

4-3. 실레버리지(Real Leverage)의 추적

전략은 각 바 단위로 다음을 추적합니다.

바가 시작할 때의 기존 포지션 크기

해당 바에서 새로 진입한 수량

이를 바탕으로, 진입이 발생한 시점에 다음을 계산합니다.

실제 레버리지 = (포지션 가치 / 현재 자산)

그리고 차트 상에 예를 들어:

Lev 2.53x 와 같은 형식의 레이블로 표시합니다.

이를 통해, 매수 시점마다 실제 계좌 레버리지가 어느 정도였는지를 직관적으로 확인할 수 있습니다.

5. 시각화 및 모니터링 요소

5-1. 차트 상 시각 요소

전략은 차트 위에 다음과 같은 정보를 직접 표시합니다.

ATH 라인

High 기준으로 계산된 역대 최고가를 주황색 선으로 표시

평단가(평균 진입가) 라인

현재 보유 포지션이 있을 때,

해당 포지션의 평균 진입가를 노란색 선으로 표시

추정 청산가(고정형 청산가) 라인

포지션 수량이 변화하는 시점을 감지하여,

당시의 평단가와 실제 레버리지를 이용해 근사적인 청산가를 계산

이를 빨간색 선으로 차트에 고정 표시

포지션이 없거나 레버리지가 1배 이하인 경우에는 청산가 라인을 제거

매수 마커 및 레이블

1차/2차 매수 조건이 충족될 때마다 해당 지점에 매수 마커를 표시

"Buy XX% @ 가격", "Lev XXx" 형태의 라벨로

진입 비율과 당시 레버리지를 함께 시각화

레이블의 위치는 설정에서 선택 가능:

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

5-2. 우측 상단 정보 테이블

차트 우측 상단에는 현재 계좌·포지션 상태를 요약한 정보 테이블이 표시됩니다.

대표적으로 다음 항목들이 포함됩니다.

Pos Qty (Token)

현재 보유 중인 포지션 수량(토큰 기준, 절대값 기준)

Pos Value (USDT)

현재 포지션의 시장 가치 (수량 × 현재 가격)

Leverage (Now)

현재 실레버리지 (포지션 가치 / 현재 자산)

DD from ATH (%)

현재 가격 기준, 최근 ATH에서의 하락률(%)

Avg Entry

현재 포지션의 평균 진입 가격

PnL (%)

현재 포지션 기준 미실현 손익률(%)

Max DD (Equity %)

전략 전체 기간 동안 기록된 계좌 기준 최대 손실(MDD, Max Drawdown)

Last Entry Price

가장 최근에 포지션을 추가로 진입한 직후의 평균 진입 가격

Last Entry Lev

위 “Last Entry Price” 시점에서의 실레버리지

Liq Price (Fixed)

위에서 설명한 고정형 추정 청산가

Return from Start (%)

전략 시작 시점(초기 자본) 대비 현재 계좌 자산의 총 수익률(%)

이 테이블을 통해 사용자는:

현재 계좌와 포지션의 상태

리스크 수준

누적 성과

를 직관적으로 파악할 수 있습니다.

6. 시간 필터 및 라벨 옵션

6-1. 전략 동작 기간 설정

전략은 옵션으로 특정 기간에만 전략을 동작시키는 시간 필터를 제공합니다.

“Use Date Range” 옵션을 활성화하면:

시작 시각과 종료 시각을 지정하여

해당 구간에 한해서만 매매가 발생하도록 제한

옵션을 비활성화하면:

전략은 전체 차트 구간에서 자유롭게 동작

6-2. 진입 라벨 위치 설정

사용자는 매수/레버리지 라벨의 위치를 선택할 수 있습니다.

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

이를 통해 개인 취향 및 차트 가독성에 맞추어

시각화 방식을 유연하게 조정할 수 있습니다.

7. 활용 대상 및 사용 예시

본 전략은 다음과 같은 목적에 적합합니다.

현물 또는 선물 롱 포지션 기준 장기·스윙 관점 추매 전략 백테스트

“고점 대비 하락률”을 기준으로 한 규칙 기반 운용 아이디어 검증

레버리지 사용 시

계좌 레버리지·청산가·MDD를 동시에 모니터링하고자 하는 경우

특정 자산에 대해

“새로운 고점이 형성될 때마다

일정한 규칙으로 깊은 조정 구간에서만 분할 진입하고자 할 때”

실거래에 그대로 적용하기보다는,

전략 아이디어 검증 및 리스크 프로파일 분석,

자신의 성향에 맞는 파라미터 탐색 용도로 사용하는 것을 권장합니다.

8. 한계 및 유의사항

백테스트 결과는 미래 성과를 보장하지 않습니다.

과거 데이터에 기반한 시뮬레이션일 뿐이며,

실제 시장에서는

유동성

슬리피지

수수료 체계

강제청산 규칙

등 다양한 변수가 존재합니다.

청산가는 단순화된 공식에 따른 추정치입니다.

거래소별 실제 청산 규칙, 유지 증거금, 수수료, 펀딩비 등은

본 전략의 계산과 다를 수 있으며,

청산가 추정 라인은 참고용 지표일 뿐입니다.

레버리지 및 진입 비율 설정에 따라 손실 폭이 매우 커질 수 있습니다.

특히 **“첫 포지션 300% 진입”**과 같이 매우 공격적인 설정은

시장 급락 시 계좌 손실과 청산 리스크를 크게 증가시킬 수 있으므로

신중한 검토가 필요합니다.

실거래 연동 시에는 별도의 리스크 관리가 필수입니다.

개별 손절 기준

포지션 상한선

전체 포트폴리오 내 비중 관리 등

본 전략 외부에서 추가적인 안전장치가 필요합니다.

9. 결론

ATH Drawdown Re-Buy Long Only 전략은 단순한 “저가 매수”를 넘어서,

ATH 기준으로 드로우다운을 구조적으로 활용하고,

첫 포지션에 대한 **특수 규칙(100% / 300%)**을 적용하며,

레버리지·청산가·MDD·수익률을 통합적으로 시각화함으로써,

하락 구간에서의 규칙 기반 롱 포지션 구축과

리스크 모니터링을 동시에 지원하는 전략입니다.

사용자는 본 전략을 통해:

자신의 시장 관점과 리스크 허용 범위에 맞는

드로우다운 구간

진입 비율

레버리지 설정

다양한 시나리오에 대한 백테스트와 분석

을 수행할 수 있습니다.

다시 한 번 강조하지만,

본 전략은 연구·학습·백테스트를 위한 도구이며,

실제 투자 판단과 책임은 전적으로 사용자 본인에게 있습니다.

/ENG Version.

This script is designed to use historical drawdown data and automatically enter positions when a predefined percentage drop from the all-time high occurs, using a predefined percentage of your account equity.

You can use leverage, and default parameter values are provided out of the box (you can freely change them to suit your style).

In addition to the two main entry levels, you can add more entry conditions and custom entry percentages – just ask ChatGPT to modify the script.

For actual/live usage, please turn OFF the KillSwitch function and turn ON the Bar Magnifier feature.

ATH Drawdown Re-Buy Long Only Strategy

1. Strategy Overview

The ATH Drawdown Re-Buy Long Only strategy is an automatic re-buy (Long Only) system that builds long positions step-by-step at specific drawdown levels, based on the asset’s all-time high (ATH) and its subsequent drawdown.

This strategy is designed with the following goals:

Systematic scaled buying and leverage usage during sharp correction periods

Clear, rule-based entry logic using drawdowns from ATH

Real-time visualization of:

Average entry price

Leverage

Estimated liquidation price

Account MDD (Max Drawdown)

Return / performance

This allows traders to intuitively monitor both risk and position status.

※ This strategy is provided for educational, research, and backtesting purposes only.

It does not constitute investment advice and does not guarantee any profits.

2. Core Concepts

2-1. Drawdown from ATH (All-Time High)

On the chart, the strategy always tracks the highest high as the ATH.

Whenever a new high is made, ATH is updated, and based on that ATH the following are calculated:

How many percent the current bar’s Low is below the ATH

How many percent the current bar’s Close is below the ATH

Using these, the strategy executes buys at two predefined drawdown zones:

1st entry zone: When price drops X% from ATH

2nd entry zone: When price drops Y% from ATH

Each zone is allowed to trigger only once per ATH cycle.

When a new ATH is created, the “1st / 2nd entry possible” flags are reset, and new opportunities open up for that ATH leg.

2-2. Special Rule for the First Position (100% / 300%)

A key feature of this strategy is the special rule for the very first position.

When the strategy currently holds no position and is about to open the first long position:

Under normal conditions, it builds the position using 100% of account equity.

However, if at that moment the price has dropped by at least a predefined threshold from ATH (e.g. around –72.5% or more),

→ the strategy will open the first position using 300% of account equity.

This rule works as follows:

Whether the first entry happens at the 1st drawdown zone or at the 2nd drawdown zone,

If the current drawdown from ATH is at or below the threshold (e.g. –72.5% or worse),

→ the strategy interprets this as “a sufficiently deep crash” and opens the initial position with 300% of equity.

If the drawdown is less severe than the threshold,

→ the first entry is capped at 100% of equity.

So the strategy has two modes for the first entry:

Normal market conditions: 100% of equity

Deep drawdown conditions: 300% of equity

This special rule is intended to be aggressive in extremely deep crashes while staying more conservative in normal corrections.

3. Strategy Logic & Execution

3-1. Entry Conditions

The strategy tracks the ATH using the High price.

For each bar, it calculates the drawdown from ATH.

The user defines two drawdown zones, for example:

1st zone: ATH – 50%

2nd zone: ATH – 72.5%

For each zone, the strategy checks:

If no buy has been executed yet for that zone in the current ATH leg, and

If the current bar’s Low touches or falls below that zone’s price level,

→ That bar is considered to have triggered a buy condition.

Order simulation:

The strategy simulates entering a long position at that zone’s price level

(using a limit/market-like approximation for backtesting).

3-2. ATH Reset & Entry Opportunity Reset

When a new High goes above the previous ATH:

The ATH is updated to this new high.

Internal flags that track whether the 1st and 2nd entries have been used are reset.

This means:

Each time the market makes a new ATH,

The strategy once again has a fresh opportunity to execute 1st and 2nd drawdown entries for that new ATH leg.

4. Position Sizing & Leverage

4-1. Position Size Based on Account Equity

The strategy defines current equity as:

Current Equity = Initial Capital + Realized PnL + Unrealized PnL

For each entry zone, the position value is calculated as follows:

The user inputs:

“What % of equity to use at this zone”

The strategy:

Multiplies current equity by that percentage

Then multiplies by the strategy’s leverage factor

Thus:

Position Value = Current Equity × (Zone % / 100) × Leverage

Finally, this position value is divided by the entry price to determine the actual position size in tokens.

4-2. Exception for the First Position (100% / 300%)

For the very first position (when there is no open position),

the strategy does not use the zone % parameters. Instead, it uses fixed ratios:

Default: Enter the first position with 100% of equity.

If the drawdown from ATH at that moment is greater than or equal to a predefined threshold (e.g. –72.5% or more)

→ Enter the first position with 300% of equity.

The position value is computed as:

Position Value = Current Equity × (100% or 300%) × Leverage

Then it is divided by the entry price to obtain the token quantity.

This rule:

Applies regardless of whether the first entry occurs at the 1st zone or 2nd zone.

Embeds the philosophy:

“In very deep crashes, go much larger on the first entry; otherwise, stay more conservative.”

4-3. Tracking Real Leverage

On each bar, the strategy tracks:

The existing position size at the start of the bar

The newly added size (if any) on that bar

When a new entry occurs, it calculates the real leverage at that moment:

Real Leverage = (Position Value / Current Equity)

This is then displayed on the chart as a label, for example:

Lev 2.53x

This makes it easy to see the actual leverage level at each entry point.

5. Visualization & Monitoring

5-1. On-Chart Visual Elements

The strategy plots the following directly on the chart:

ATH Line

The all-time high (based on High) is plotted as an orange line.

Average Entry Price Line

When a position is open, the average entry price of that position is plotted as a yellow line.

Estimated Liquidation Price (Fixed) Line

The strategy detects when the position size changes.

At each size change, it uses the current average entry price and real leverage to compute an approximate liquidation price.

This “fixed liquidation price” is then plotted as a red line on the chart.

If there is no position, or if leverage is 1x or lower, the liquidation line is removed.

Entry Markers & Labels

When 1st/2nd entry conditions are met, the strategy:

Marks the entry point on the chart.

Displays labels such as "Buy XX% @ Price" and "Lev XXx",

showing both entry percentage and real leverage at that time.

The label placement is configurable:

Below Bar

Above Bar

At Price

5-2. Information Table (Top-Right Panel)

In the top-right corner of the chart, the strategy displays a summary table of the current account and position status. It typically includes:

Pos Qty (Token)

Absolute size of the current position (in tokens)

Pos Value (USDT)

Market value of the current position (qty × current price)

Leverage (Now)

Current real leverage (position value / current equity)

DD from ATH (%)

Current drawdown (%) from the latest ATH, based on current price

Avg Entry

Average entry price of the current position

PnL (%)

Unrealized profit/loss (%) of the current position

Max DD (Equity %)

The maximum equity drawdown (MDD) recorded over the entire backtest period

Last Entry Price

Average entry price immediately after the most recent add-on entry

Last Entry Lev

Real leverage at the time of the most recent entry

Liq Price (Fixed)

The fixed estimated liquidation price described above

Return from Start (%)

Total return (%) of equity compared to the initial capital

Through this table, users can quickly grasp:

Current account and position status

Current risk level

Cumulative performance

6. Time Filters & Label Options

6-1. Strategy Date Range Filter

The strategy provides an option to restrict trading to a specific time range.

When “Use Date Range” is enabled:

You can specify start and end timestamps.

The strategy will only execute trades within that range.

When this option is disabled:

The strategy operates over the entire chart history.

6-2. Entry Label Placement

Users can customize where entry/leverage labels are drawn:

Below Bar (Below Bar)

Above Bar (Above Bar)

At the actual price level (At Price)

This allows you to adjust visualization according to personal preference and chart readability.

7. Use Cases & Applications

This strategy is suitable for the following purposes:

Long-term / swing-style re-buy strategies for spot or futures long positions

Testing rule-based strategies that rely on “drawdown from ATH” as a main signal

Monitoring account leverage, liquidation price, and MDD when using leverage

Handling situations where, for a given asset:

“Every time a new ATH is formed,

you want to wait for deep corrections and enter only at specific drawdown zones”

It is generally recommended to use this strategy not as a direct plug-and-play live system, but as a tool for:

Strategy idea validation

Risk profile analysis

Parameter exploration to match your personal risk tolerance and style

8. Limitations & Warnings

Backtest results do not guarantee future performance.

They are based on historical data only.

In live markets, additional factors exist:

Liquidity

Slippage

Fee structures

Exchange-specific liquidation rules

Funding fees, etc.

The liquidation price is only an approximate estimate, derived from a simplified formula.

Actual liquidation rules, maintenance margin requirements, fees, and other details differ by exchange.

The liquidation line should be treated as a reference indicator, not an exact guarantee.

Depending on the configured leverage and entry percentages, losses can be very large.

In particular, extremely aggressive settings such as “first position 300% of equity” can greatly increase the risk of large account drawdowns and liquidation during sharp market crashes.

Use such settings with extreme caution.

For live trading, additional risk management is essential:

Your own stop-loss rules

Maximum position size limits

Portfolio-level exposure controls

And other external safety mechanisms beyond this strategy

9. Conclusion

The ATH Drawdown Re-Buy Long Only strategy goes beyond simple “buy the dip” logic. It:

Systematically utilizes drawdowns from ATH as a structural signal

Applies a special first-position rule (100% / 300%)

Integrates visualization of leverage, liquidation price, MDD, and returns

All of this supports rule-based long position building in drawdown phases and comprehensive risk monitoring.

With this strategy, users can:

Explore different:

Drawdown zones

Entry percentages

Leverage levels

Run various backtests and scenario analyses

Better understand the risk/return profile that fits their own market view and risk tolerance

Once again, this strategy is intended for research, learning, and backtesting only.

All real trading decisions and their consequences are solely the responsibility of the user.

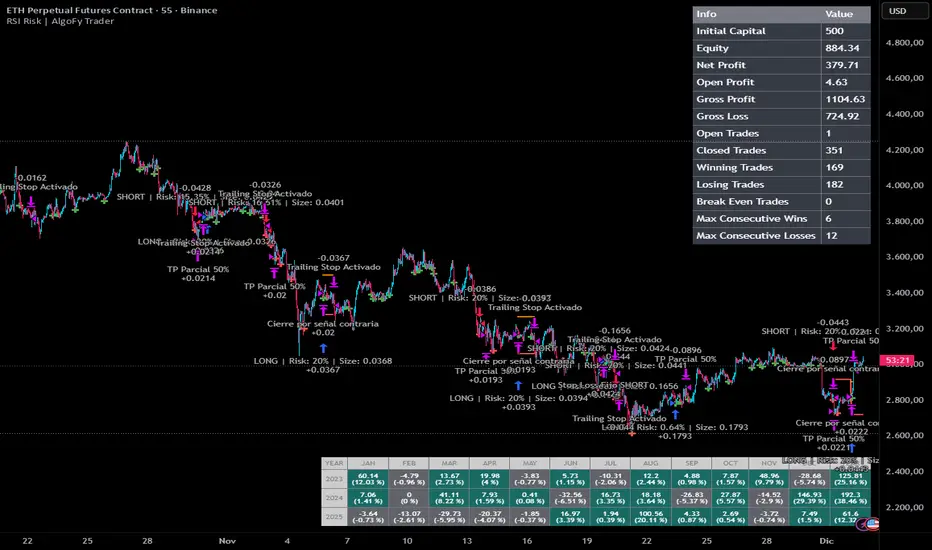

Daily Performance Analysis [Mr_Rakun]The Daily Performance Analysis indicator is a comprehensive trading performance tracker that analyzes your strategy's success rate and profitability across different days of the week and month. This powerful tool provides detailed statistics to help traders identify patterns in their trading performance and optimize their strategies accordingly.

Weekly Performance Analysis:

Tracks wins/losses for each day of the week (Monday through Sunday)

Calculates net profit/loss for each trading day

Shows profit factor (gross profit ÷ gross loss) for each day

Displays win rate percentage for each day

Monthly Performance Analysis:

Monitors performance for each day of the month (1-31)

Provides the same detailed metrics as weekly analysis

Helps identify monthly patterns and trends

Add to Your Strategy:

Copy the performance analysis code and integrate it into your existing Pine Script strategy

Optimize Strategy: Use insights to refine entry/exit timing or avoid trading on poor-performing days

Pattern Recognition: Identify which days of the week/month work best for your strategy

Risk Management: Avoid trading on historically poor-performing days

Strategy Optimization: Fine-tune your approach based on empirical data

Performance Tracking: Monitor long-term trends in your trading success

Data-Driven Decisions: Make informed adjustments to your trading schedule

Strategy Stats [presentTrading]Hello! it's another weekend. This tool is a strategy performance analysis tool. Looking at the TradingView community, it seems few creators focus on this aspect. I've intentionally created a shared version. Welcome to share your idea or question on this.

█ Introduction and How it is Different

Strategy Stats is a comprehensive performance analytics framework designed specifically for trading strategies. Unlike standard strategy backtesting tools that simply show cumulative profits, this analytics suite provides real-time, multi-timeframe statistical analysis of your trading performance.

Multi-timeframe analysis: Automatically tracks performance metrics across the most recent time periods (last 7 days, 30 days, 90 days, 1 year, and 4 years)

Advanced statistical measures: Goes beyond basic metrics to include Information Coefficient (IC) and Sortino Ratio

Real-time feedback: Updates performance statistics with each new trade

Visual analytics: Color-coded performance table provides instant visual feedback on strategy health

Integrated risk management: Implements sophisticated take profit mechanisms with 3-step ATR and percentage-based exits

BTCUSD Performance

The table in the upper right corner is a comprehensive performance dashboard showing trading strategy statistics.

Note: While this presentation uses Vegas SuperTrend as the underlying strategy, this is merely an example. The Stats framework can be applied to any trading strategy. The Vegas SuperTrend implementation is included solely to demonstrate how the analytics module integrates with a trading strategy.

⚠️ Timeframe Limitations

Important: TradingView's backtesting engine has a maximum storage limit of 10,000 bars. When using this strategy stats framework on smaller timeframes such as 1-hour or 2-hour charts, you may encounter errors if your backtesting period is too long.

Recommended Timeframe Usage:

Ideal for: 4H, 6H, 8H, Daily charts and above

May cause errors on: 1H, 2H charts spanning multiple years

Not recommended for: Timeframes below 1H with long history

█ Strategy, How it Works: Detailed Explanation

The Strategy Stats framework consists of three primary components: statistical data collection, performance analysis, and visualization.

🔶 Statistical Data Collection

The system maintains several critical data arrays:

equityHistory: Tracks equity curve over time

tradeHistory: Records profit/loss of each trade

predictionSignals: Stores trade direction signals (1 for long, -1 for short)

actualReturns: Records corresponding actual returns from each trade

For each closed trade, the system captures:

float tradePnL = strategy.closedtrades.profit(tradeIndex)

float tradeReturn = strategy.closedtrades.profit_percent(tradeIndex)

int tradeType = entryPrice < exitPrice ? 1 : -1 // Direction

🔶 Performance Metrics Calculation

The framework calculates several key performance metrics:

Information Coefficient (IC):

The correlation between prediction signals and actual returns, measuring forecast skill.

IC = Correlation(predictionSignals, actualReturns)

Where Correlation is the Pearson correlation coefficient:

Correlation(X,Y) = (nΣXY - ΣXY) / √

Sortino Ratio:

Measures risk-adjusted return focusing only on downside risk:

Sortino = (Avg_Return - Risk_Free_Rate) / Downside_Deviation

Where Downside Deviation is:

Downside_Deviation = √

R_i represents individual returns, T is the target return (typically the risk-free rate), and n is the number of observations.

Maximum Drawdown:

Tracks the largest percentage drop from peak to trough:

DD = (Peak_Equity - Trough_Equity) / Peak_Equity * 100

🔶 Time Period Calculation

The system automatically determines the appropriate number of bars to analyze for each timeframe based on the current chart timeframe:

bars_7d = math.max(1, math.round(7 * barsPerDay))

bars_30d = math.max(1, math.round(30 * barsPerDay))

bars_90d = math.max(1, math.round(90 * barsPerDay))

bars_365d = math.max(1, math.round(365 * barsPerDay))

bars_4y = math.max(1, math.round(365 * 4 * barsPerDay))

Where barsPerDay is calculated based on the chart timeframe:

barsPerDay = timeframe.isintraday ?

24 * 60 / math.max(1, (timeframe.in_seconds() / 60)) :

timeframe.isdaily ? 1 :

timeframe.isweekly ? 1/7 :

timeframe.ismonthly ? 1/30 : 0.01

🔶 Visual Representation

The system presents performance data in a color-coded table with intuitive visual indicators:

Green: Excellent performance

Lime: Good performance

Gray: Neutral performance

Orange: Mediocre performance

Red: Poor performance

█ Trade Direction

The Strategy Stats framework supports three trading directions:

Long Only: Only takes long positions when entry conditions are met

Short Only: Only takes short positions when entry conditions are met

Both: Takes both long and short positions depending on market conditions

█ Usage

To effectively use the Strategy Stats framework:

Apply to existing strategies: Add the performance tracking code to any strategy to gain advanced analytics

Monitor multiple timeframes: Use the multi-timeframe analysis to identify performance trends

Evaluate strategy health: Review IC and Sortino ratios to assess predictive power and risk-adjusted returns

Optimize parameters: Use performance data to refine strategy parameters

Compare strategies: Apply the framework to multiple strategies to identify the most effective approach

For best results, allow the strategy to generate sufficient trade history for meaningful statistical analysis (at least 20-30 trades).

█ Default Settings

The default settings have been carefully calibrated for cryptocurrency markets:

Performance Tracking:

Time periods: 7D, 30D, 90D, 1Y, 4Y

Statistical measures: Return, Win%, MaxDD, IC, Sortino Ratio

IC color thresholds: >0.3 (green), >0.1 (lime), <-0.1 (orange), <-0.3 (red)

Sortino color thresholds: >1.0 (green), >0.5 (lime), <0 (red)

Multi-Step Take Profit:

ATR multipliers: 2.618, 5.0, 10.0

Percentage levels: 3%, 8%, 17%

Short multiplier: 1.5x (makes short take profits more aggressive)

Stop loss: 20%

Parent Session Sweeps + Alert Killzone Ranges with Parent Session Sweep

Key Features:

1. Multiple Session Support: The script tracks three major trading sessions - Asia, London, and New York. Users can customize the timing of these sessions.

2. Killzone Visualization: The strategy visually represents each session's range, either as filled boxes or lines, allowing traders to easily identify key price levels.

3. Parent Session Logic: The core of the strategy revolves around identifying a "parent" session - a session that encompasses the range of the following session. This parent session becomes the basis for potential trade setups.

4. Sweep and Reclaim Setups: The strategy looks for price movements that sweep (break above or below) the parent session's high or low, followed by a reclaim of that level. This price action often indicates a potential reversal.

5. Risk-Reward Filtering: Each potential setup is evaluated based on a user-defined minimum risk-reward ratio, ensuring that only high-quality trade opportunities are considered.

6. Candle Close Filter: An optional filter that checks the characteristics of the candle that reclaims the parent session level, adding an extra layer of confirmation to the setup.

7. Performance Tracking: The strategy keeps track of bullish and bearish setup success rates, providing valuable feedback on its performance over time.

8. Visual Aids: The script draws lines to mark the parent session's high and low, making it easy for traders to identify key levels.

How It Works:

1. The script continuously monitors price action across the defined sessions.

2. When a session fully contains the range of the next session, it's identified as a potential parent session.

3. The strategy then waits for price to sweep either the high or low of this parent session.

4. If a sweep occurs, it looks for a reclaim of the swept level within the parameters set by the user.

5. If a valid setup is identified, the script generates an alert and places a trade (if backtesting or running live).

6. The strategy continues to monitor the trade for either reaching the target (opposite level of the parent session) or hitting the stop loss.

Considerations for Signals:

- Sweep: A break of the parent session's high or low.

- Reclaim: A close back inside the parent session range after a sweep.

- Candle Characteristics: Optional filter for the reclaim candle (e.g., bullish candle for long setups).

- Risk-Reward: Each setup must meet or exceed the user-defined minimum risk-reward ratio.

- Session Timing: The strategy is sensitive to the defined session times, which should be set according to the trader's preferred time zone.

This strategy aims to capitalize on institutional order flow and liquidity patterns in the forex market, providing traders with a systematic approach to identifying potential reversal points with favorable risk-reward profiles.

SigmaKernel - AdaptiveSigmaKernel - Adaptive Self-Optimizing Multi-Factor Trading System

SigmaKernel - Adaptive is a self-learning algorithmic trading strategy that combines four distinct analytical dimensions—momentum, market structure, volume flow, and reversal patterns—within a machine-learning-inspired framework that continuously adjusts its own parameters based on realized trading performance. Unlike traditional fixed-parameter strategies that maintain static weightings regardless of market conditions or results, this system implements a feedback loop that tracks which signal types, directional biases, and market conditions produce profitable outcomes, then mathematically adjusts component weightings, minimum score thresholds, position sizing multipliers, and trade spacing requirements to optimize future performance.

The strategy is designed for futures traders operating on prop firm accounts or live capital, incorporating realistic execution mechanics including configurable entry modes (stop breakout orders, limit pullback entries, or market-on-open), commission structures calibrated to retail futures contracts ($0.62 per contract default), one-tick slippage modeling, and professional risk controls including trailing drawdown guards, daily loss limits, and weekly profit targets. The system features universal futures compatibility—it automatically detects and adapts to any futures contract by reading the instrument's tick size and point value directly from the chart, eliminating the need for manual configuration across different markets.

What Makes This Approach Different

Adaptive Weight Optimization System

The core differentiation is the adaptive learning architecture. The strategy maintains four independent scoring components: momentum analysis (using RSI multi-timeframe, MACD histogram, and DMI/ADX), market structure detection (breakout identification via pivot-based support/resistance and moving average positioning), volume flow analysis (Volume Price Trend indicator with standard deviation confirmation), and reversal pattern recognition (oversold/overbought conditions combined with structural levels).

Each component generates a directional score that is multiplied by its current weight. After every closed trade, the system performs a retrospective analysis on the last N trades (configurable Learning Period, default 15 trades) to calculate win rates for each signal type independently. For example, if momentum-driven trades won 65% of the time while reversal trades won only 35%, the adaptive algorithm increases the momentum weight and decreases the reversal weight proportionally. The adjustment formula is:

New_Weight = Current_Weight + (Component_Win_Rate - Average_Win_Rate) × Adaptation_Speed

This creates a self-correcting mechanism where successful signal generators receive more influence in future composite scores, while underperforming components are de-emphasized. The system separately tracks long versus short win rates and applies directional bias corrections—if shorts consistently outperform longs, the strategy applies a 10% reduction to bullish signals to prevent fighting the prevailing market character.

Dynamic Parameter Adjustment

Beyond component weightings, three critical strategy parameters self-adjust based on performance:

Minimum Signal Score: The threshold required to trigger a trade. If overall win rate falls below 45%, the system increments this threshold by 0.10 per adjustment cycle, making the strategy more selective. If win rate exceeds 60%, the threshold decreases to allow more opportunities. This prevents the strategy from overtrading during unfavorable conditions and capitalizes on high-probability environments.

Risk Multiplier: Controls position sizing aggression. When drawdown exceeds 5%, risk per trade reduces by 10% per cycle. When drawdown falls below 2%, risk increases by 5% per cycle. This implements the professional risk management principle of "bet small when losing, bet bigger when winning" algorithmically.

Bars Between Trades: Spacing filter to prevent overtrading. Base value (default 9 bars) multiplies by drawdown factor and losing streak factor. During drawdown or consecutive losses, spacing expands up to 2x to allow market conditions to change before re-entering.

All adaptation operates during live forward-testing or real trading—there is no in-sample optimization applied to historical data. The system learns solely from its own realized trades.

Universal Futures Compatibility

The strategy implements universal futures instrument detection that automatically adapts to any futures contract without requiring manual configuration. Instead of hardcoding specific contract specifications, the system reads three critical values directly from TradingView's symbol information:

Tick Size Detection: Uses `syminfo.mintick` to obtain the minimum price increment for the current instrument. This value varies widely across markets—ES trades in 0.25 ticks, crude oil (CL) in 0.01 ticks, gold (GC) in 0.10 ticks, and treasury futures (ZB) in increments of 1/32nds. The strategy adapts all entry buffer calculations and stop placement logic to the detected tick size.

Point Value Detection: Uses `syminfo.pointvalue` to determine the dollar value per full point of price movement. For ES, one point equals $50; for crude oil, one point equals $1,000; for gold, one point equals $100. This automatic detection ensures accurate P&L calculations and risk-per-contract measurements across all instruments.

Tick Value Calculation: Combines tick size and point value to compute dollar value per tick: Tick_Value = Tick_Size × Point_Value. This derived value drives all position sizing calculations, ensuring the risk management system correctly accounts for each instrument's economic characteristics.

This universal approach means the strategy functions identically on emini indices (ES, MES, NQ, MNQ), micro indices, energy contracts (CL, NG, RB), metals (GC, SI, HG), agricultural futures (ZC, ZS, ZW), treasury futures (ZB, ZN, ZF), currency futures (6E, 6J, 6B), and any other futures contract available on TradingView. No parameter adjustments or instrument-specific branches exist in the code—the adaptation happens automatically through symbol information queries.

Stop-Out Rate Monitoring System

The strategy includes an intelligent stop-out rate tracking system that monitors the percentage of your last 20 trades (or available trades if fewer than 20) that were stopped out. This metric appears in the dashboard's Performance section with color-coded guidance:

Green (<30% stop-out rate): Very few trades are being stopped out. This suggests either your stops are too loose (giving back profits on reversals) or you're in an exceptional trending market. Consider tightening your Stop Loss ATR multiplier to lock in profits more efficiently.

Orange (30-65% stop-out rate): Healthy range. Your stop placement is appropriately sized for current market conditions and the strategy's risk-reward profile. No adjustment needed.

Red (>65% stop-out rate): Too many trades are being stopped out prematurely. Your stops are likely too tight for the current volatility regime. Consider widening your Stop Loss ATR multiplier to give trades more room to develop.

Critical Design Philosophy: Unlike some systems that automatically adjust stops based on performance statistics, this strategy intentionally keeps stop-loss control in the user's hands. Automatic stop adjustment creates dangerous feedback loops—widening stops increases risk per contract, which forces position size reduction, which distorts performance metrics, leading to incorrect adaptations. Instead, the dashboard provides visibility into stop performance, empowering you to make informed manual adjustments when warranted. This preserves the integrity of the adaptive system while giving you the critical data needed for stop optimization.

Execution Kernel Architecture

The entry system offers three distinct execution modes to match trader preference and market character:

StopBreakout Mode: Places buy-stop orders above the prior bar's high (for longs) or sell-stop orders below the prior bar's low (for shorts), plus a 2-tick buffer. This ensures entries only occur when price confirms directional momentum by breaking recent structure. Ideal for trending and momentum-driven markets.

LimitPullback Mode: Places limit orders at a pullback price calculated as: Entry_Price = Close - (ATR × Pullback_Multiplier) for longs, or Close + (ATR × Pullback_Multiplier) for shorts. Default multiplier is 0.5 ATR. This waits for mean-reversion before entering in the signal direction, capturing better prices in volatile or oscillating markets.

MarketNextOpen Mode: Executes at market on the bar immediately following signal generation. This provides fastest execution but sacrifices the filtering effect of requiring price confirmation.

All pending entry orders include a configurable Time-To-Live (TTL, default 6 bars). If an order is not filled within the TTL period, it cancels automatically to prevent stale signals from executing in changed market conditions.

Professional Exit Management

The exit system implements a three-stage progression: initial stop loss, breakeven adjustment, and dynamic trailing stop.

Initial Stop Loss: Calculated as entry price ± (ATR × User_Stop_Multiplier × Volatility_Adjustment). Users have direct control via the Stop Loss ATR multiplier (default 1.25). The system then applies volatility regime adjustments: ×1.2 in high-volatility environments (stops automatically widen), ×0.8 in low volatility (stops tighten), ×1.0 in normal conditions. This ensures stops adapt to market character while maintaining user control over baseline risk tolerance.

Breakeven Trigger: When profit reaches a configurable multiple of initial risk (default 1.0R), the stop loss automatically moves to breakeven (entry price). This locks in zero-loss status once the trade demonstrates favorable movement.

Trailing Stop Activation: When profit reaches the Trail_Trigger_R multiple (default 1.2R), the system cancels the fixed stop and activates a dynamic trailing stop. The trail uses Step and Offset parameters defined in R-multiples. For example, with Trail_Offset_R = 1.0 and Trail_Step_R = 1.5, the stop trails 1.0R behind price and moves in 1.5R increments. This captures extended moves while protecting accumulated profit.

Additional failsafes include maximum time-in-trade (exits after N bars if specified) and end-of-session flatten (automatically closes all positions X minutes before session end to avoid overnight exposure).

Core Calculation Methodology

Signal Component Scoring

Momentum Component:

- Calculates 14-period DMI (Directional Movement Index) with ADX strength filter (trending when ADX > 25)

- Computes three RSI timeframes: fast (7-period), medium (14-period), slow (21-period)

- Analyzes MACD (12/26/9) histogram for directional acceleration

- Bullish momentum: uptrend (DI+ > DI- with ADX > 25) + MACD histogram rising above zero + RSI fast between 50-80 = +1.6 score

- Bearish momentum: downtrend (DI- > DI+ with ADX > 25) + MACD histogram falling below zero + RSI fast between 20-50 = -1.6 score

- Score multiplies by volatility adjustment factor: ×0.8 in high volatility (momentum less reliable), ×1.2 in low volatility (momentum more persistent)

Structure Component:

- Identifies swing highs and lows using 10-bar pivot lookback on both sides

- Maintains most recent swing high as dynamic resistance, most recent swing low as dynamic support

- Detects breakouts: bullish when close crosses above resistance with prior bar below; bearish when close crosses below support with prior bar above

- Breakout score: ±1.0 for confirmed break

- Moving average alignment: +0.5 when price > SMA20 > SMA50 (bullish structure); -0.5 when price < SMA20 < SMA50 (bearish structure)

- Total structure range: -1.5 to +1.5

Volume Component:

- Calculates Volume Price Trend: VPT = Σ [(Close - Close ) / Close × Volume]

- Compares VPT to its 10-period EMA as signal line (similar to MACD logic)

- Computes 20-period volume moving average and standard deviation

- High volume event: current volume > (volume_average + 1× std_dev)

- Bullish volume: VPT > VPT_signal AND high_volume = +1.0

- Bearish volume: VPT < VPT_signal AND high_volume = -1.0

- No score if volume is not elevated (filters out low-conviction moves)

Reversal Component:

- Identifies extreme RSI conditions: RSI slow < 30 (oversold) or > 70 (overbought)

- Requires structural confluence: price at or below support level for bullish reversal; at or above resistance for bearish reversal

- Requires momentum shift: RSI fast must be rising (for bull) or falling (for bear) to confirm reversal in progress

- Bullish reversal: RSI < 30 AND price ≤ support AND RSI rising = +1.0

- Bearish reversal: RSI > 70 AND price ≥ resistance AND RSI falling = -1.0

Composite Score Calculation

Final_Score = (Momentum × Weight_M) + (Structure × Weight_S) + (Volume × Weight_V) + (Reversal × Weight_R)

Initial weights: Momentum = 1.0, Structure = 1.2, Volume = 0.8, Reversal = 0.6

These weights adapt after each trade based on component-specific performance as described above.

The system also applies directional bias adjustment: if recent long trades have significantly lower win rate than shorts, bullish scores multiply by 0.9 to reduce aggressive long entries. Vice versa for underperforming shorts.

Position Sizing Algorithm

The position sizing calculation incorporates multiple confidence factors and automatically scales to any futures contract:

1. Base risk amount = Account_Size × Base_Risk_Percent × Adaptive_Risk_Multiplier

2. Stop distance in price units = ATR × User_Stop_Multiplier × Volatility_Regime_Multiplier × Entry_Buffer

3. Risk per contract = Stop_Distance × Dollar_Per_Point (automatically detected from instrument)

4. Raw position size = Risk_Amount / Risk_Per_Contract

Then applies confidence scaling:

- Signal confidence = min(|Weighted_Score| / Min_Score_Threshold, 2.0) — higher scores receive larger size, capped at 2×

- Direction confidence = Long_Win_Rate (for bulls) or Short_Win_Rate (for bears)

- Type confidence = Win_Rate of dominant signal type (momentum/structure/volume/reversal)

- Total confidence = (Signal_Confidence + Direction_Confidence + Type_Confidence) / 3

Adjusted size = Raw_Size × Total_Confidence × Losing_Streak_Reduction

Losing streak reduction = 0.5 if losing_streak ≥ 5, otherwise 1.0

Universal Maximum Position Calculation: Instead of hardcoded limits per instrument, the system calculates maximum position size as: Max_Contracts = Account_Size / 25000, clamped between 1 and 10 contracts. This means a $50,000 account allows up to 2 contracts, a $100,000 account allows up to 4 contracts, regardless of which futures contract is being traded. This universal approach maintains consistent risk exposure across different instruments while preventing overleveraging.

Final size is rounded to integer and bounded by the calculated maximum.

Session and Risk Management System

Timezone-Aware Session Control

The strategy implements timezone-correct session filtering. Users specify session start hour, end hour, and timezone from 12 supported zones (New York, Chicago, Los Angeles, London, Frankfurt, Moscow, Tokyo, Hong Kong, Shanghai, Singapore, Sydney, UTC). The system converts bar timestamps to the selected timezone before applying session logic.

For split sessions (e.g., Asian session 18:00-02:00), the logic correctly handles time wraparound. Weekend trading can be optionally disabled (default: disabled) to avoid low-liquidity weekend price action.

Multi-Layer Risk Controls

Daily Loss Limit: Strategy ceases all new entries when daily P&L reaches negative threshold (default $2,000). This prevents catastrophic drawdown days. Resets at timezone-corrected day boundary.

Weekly Profit Target: Strategy ceases trading when weekly profit reaches target (default $10,000). This implements the professional principle of "take the win and stop pushing luck." Resets on timezone-corrected Monday.

Maximum Daily Trades: Hard cap on entries per day (default 20) to prevent overtrading during volatile conditions when many signals may generate.

Trailing Drawdown Guard: Optional prop-firm-style trailing stop on account equity. When enabled, if equity drops below (Peak_Equity - Trailing_DD_Amount), all trading halts. This simulates the common prop firm rule where exceeding trailing drawdown results in account termination.

All limits display status in the real-time dashboard, showing "MAX LOSS HIT", "WEEKLY TARGET MET", or "ACTIVE" depending on current state.

How To Use This Strategy

Initial Setup

1. Apply the strategy to your desired futures chart (tested on 5-minute through daily timeframes)

2. The strategy will automatically detect your instrument's specifications—no manual configuration needed for different contracts

3. Configure your account size and risk parameters in the Core Settings section

4. Set your trading session hours and timezone to match your availability

5. Adjust the Stop Loss ATR multiplier based on your risk tolerance (0.8-1.2 for tighter stops, 1.5-2.5 for wider stops)

6. Select your preferred entry execution mode (recommend StopBreakout for beginners)

7. Enable adaptation (recommended) or disable for fixed-parameter operation

8. Review the strategy's Properties in the Strategy Tester settings and verify commission/slippage match your broker's actual costs

The universal futures detection means you can switch between ES, NQ, CL, GC, ZB, or any other futures contract without changing any strategy parameters—the system will automatically adapt its calculations to each instrument's unique specifications.

Dashboard Interpretation

The strategy displays a comprehensive real-time dashboard in the top-right corner showing:

Market State Section:

- Trend: Shows UPTREND/DOWNTREND/CONSOLIDATING/NEUTRAL based on ADX and DMI analysis

- ADX Value: Current trend strength (>25 = strong trend, <20 = consolidating)

- Momentum: BULL/BEAR/NEUTRAL classification with current momentum score

- Volatility: HIGH/LOW/NORMAL regime with ATR percentage of price

Volume Profile Section (Large dashboard only):

- VPT Flow: Directional bias from volume analysis

- Volume Status: HIGH/LOW/NORMAL with relative volume multiplier

Performance Section:

- Daily P&L: Current day's profit/loss with color coding

- Daily Trades: Number of completed trades today

- Weekly P&L: Current week's profit/loss

- Target %: Progress toward weekly profit target

- Stop-Out Rate: Percentage of last 20 trades (or available trades if <20) that were stopped out. Includes all stop types: initial stops, breakeven stops, trailing stops, timeout exits, and EOD flattens. Color coded with actionable guidance:

- Green (<30%): Shows "TIGHTEN" guidance. Very few stop-outs suggests stops may be too loose or exceptional market conditions. Consider reducing Stop Loss ATR multiplier.

- Orange (30-65%): Shows "OK" guidance. Healthy stop-out rate indicating appropriate stop placement for current conditions.

- Red (>65%): Shows "WIDEN" guidance. Too many premature stop-outs. Consider increasing Stop Loss ATR multiplier to give trades more room.

- Status: Overall trading status (ACTIVE/MAX LOSS HIT/WEEKLY TARGET MET/FILTERS ACTIVE)

Adaptive Engine Section:

- Min Score: Current minimum threshold for trade entry (higher = more selective)

- Risk Mult: Current position sizing multiplier (adjusts with performance)

- Bars BTW: Current minimum bars required between trades

- Drawdown: Current drawdown percentage from equity peak

- Weights: M/S/V/R showing current component weightings

Win Rates Section:

- Type: Win rates for Momentum, Structure, Volume, Reversal signal types

- Direction: Win rates for Long vs Short trades

Color coding shows green for >50% win rate, red for <50%

Session Info Section:

- Session Hours: Active trading window with timezone

- Weekend Trading: ENABLED/DISABLED status

- Session Status: ACTIVE/INACTIVE based on current time

Signal Generation and Entry

The strategy generates entries when the weighted composite score exceeds the adaptive minimum threshold (initial value configurable, typically 1.5 to 2.5). Entries display as layered triangle markers on the chart:

- Long Signal: Three green upward triangles below the entry bar

- Short Signal: Three red downward triangles above the entry bar

Triangle tooltip shows the signal score and dominant signal type (MOMENTUM/STRUCTURE/VOLUME/REVERSAL).

Position Management and Stop Optimization

Once entered, the strategy automatically manages the position through its three-stage exit system. Monitor the Stop-Out Rate metric in the dashboard to optimize your stop placement:

If Stop-Out Rate is Green (<30%): You're rarely being stopped out. This could mean:

- Your stops are too loose, allowing trades to give back too much profit on reversals

- You're in an exceptional trending market where tight stops would work better

- Action: Consider reducing your Stop Loss ATR multiplier by 0.1-0.2 to tighten stops and lock in profits more efficiently

If Stop-Out Rate is Orange (30-65%): Optimal range. Your stops are appropriately sized for the strategy's risk-reward profile and current market volatility. No adjustment needed.

If Stop-Out Rate is Red (>65%): You're being stopped out too frequently. This means:

- Your stops are too tight for current market volatility