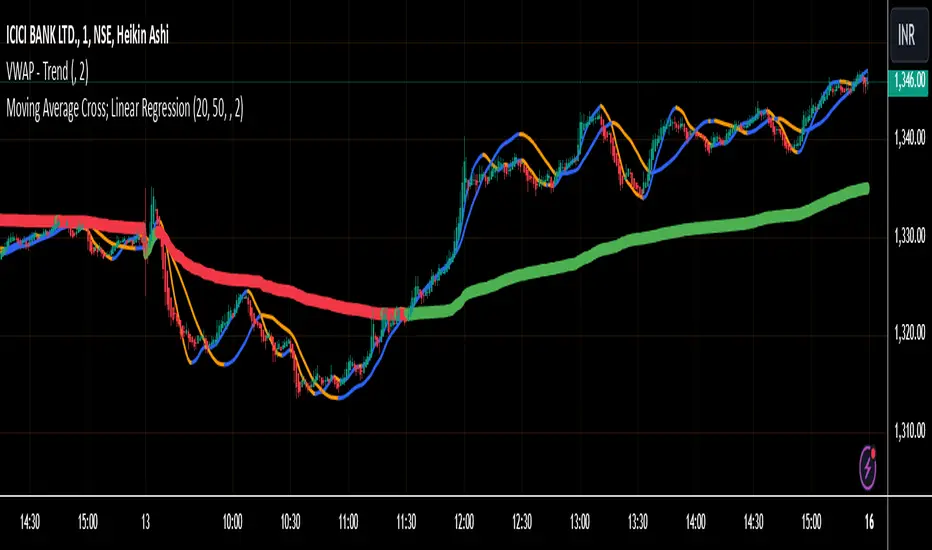

VWAP Indicator Channel | Multi Timeframe by Osbrah📊 Multi-Timeframe VWAP Indicator (Session / Weekly / Monthly)

This powerful indicator plots the Volume Weighted Average Price (VWAP) across multiple timeframes: intraday session, weekly, and monthly. It's designed to give traders a clear understanding of the market’s fair value over different horizons.

Key Features:

* Display Session VWAP (resets daily)

* Enable Weekly and Monthly VWAPs for broader market context

* Customize colors, styles, and visibility for each VWAP

* Toggle between standard VWAP or anchored to session opens

Use Cases:

* Identify value zones where price tends to gravitate

* Spot institutional levels of interest and potential reversal points

* Align entries with VWAP bounces or breaks

* Combine with EMAs or price action for high-probability setups

Perfect for day traders, swing traders, and institutional-style strategies, this VWAP tool helps you stay aligned with volume-based price dynamics across all market phases.

Penunjuk Pine Script®