Total Info Indicator by MikePenzin

Install & Add to Chart

• Copy the script into Pine Editor → click Add to Chart .

• Open the ⚙️ Settings → Inputs to customize.

What It Does

• Displays key info in a floating table — trend, volume, ATR, RSI, stop loss, and more.

• Detects breakouts , smart SELL signals , and opening strength .

• Uses emojis and colours to make trends easy to read: 🟢 good, 🟡 neutral, 🔴 risky.

For Swing Traders

• Works best on Daily or 4H charts.

• Watch for 🟢 Uptrend + ⚡BUY / 🔥BUY breakout signals.

• Use ATR-based Stop Loss (shown in table).

• Avoid new entries a few days before earnings.

Suggested Setup

• 20/50/150 MA Lines: ON

• 200 MA Line: optional

• ATR Multiplier: 1.3

• Breakout Detection: ON (Volume + RSI + Trend filters)

• Smart SELLs: ON (RSI 70, EMA 20)

• Pivots: ON for quick swing levels

How to Read

• MA Row: 🟢 = price above MA (bullish).

• ATR/Stop Loss: Suggests where to place protective stop.

• Volume Info: Today’s vs 20-day average, plus pace.

• RSI & CCI: Shows momentum and overbought/oversold levels.

• Breakouts: ⚡BUY (early), 🔥BUY (confirmed).

• Smart SELLs: RSI🔴 / DIV🟣 / EMA🔵 mean potential exit zones.

Example Use

1️⃣ Find stocks with Uptrend 🟢 , rising volume, and ⚡BUY signal.

2️⃣ Enter near breakout; set Stop = shown level.

3️⃣ Take profits or trail when Smart SELLs appear or RSI peaks.

Tips

• Choose table corner under “Table Visualization.”

• Reduce clutter on small timeframes (turn off Pivots/200 MA).

• Use “Volume speed” to spot surging interest before breakouts.

• Compatible with most equities and ETFs.

Disclaimer

This script is for education & analysis only .

Not financial advice — always manage your own risk.

Cari dalam skrip untuk "乌德勒支+VS+赫拉克勒斯"

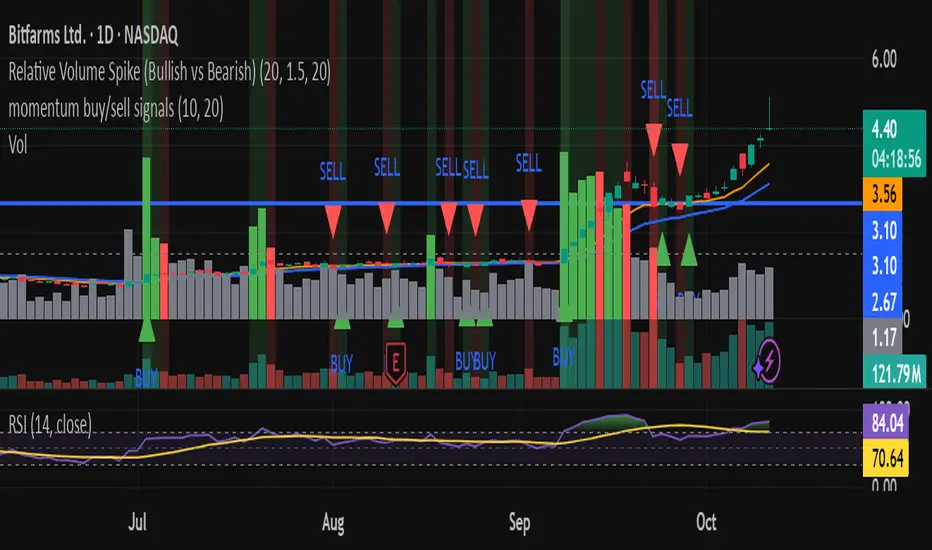

Relative Volume Spike (Bullish vs Bearish)relative volume compared to 20day averages

used to detect when big money is coming in.

Stochastic Enhanced [DCAUT]█ Stochastic Enhanced

📊 ORIGINALITY & INNOVATION

The Stochastic Enhanced indicator builds upon George Lane's classic momentum oscillator (developed in the late 1950s) by providing comprehensive smoothing algorithm flexibility. While traditional implementations limit users to Simple Moving Average (SMA) smoothing, this enhanced version offers 21 advanced smoothing algorithms, allowing traders to optimize the indicator's characteristics for different market conditions and trading styles.

Key Improvements:

Extended from single SMA smoothing to 21 professional-grade algorithms including adaptive filters (KAMA, FRAMA), zero-lag methods (ZLEMA, T3), and advanced digital filters (Kalman, Laguerre)

Maintains backward compatibility with traditional Stochastic calculations through SMA default setting

Unified smoothing algorithm applies to both %K and %D lines for consistent signal processing characteristics

Enhanced visual feedback with clear color distinction and background fill highlighting for intuitive signal recognition

Comprehensive alert system covering crossovers and zone entries for systematic trade management

Differentiation from Traditional Stochastic:

Traditional Stochastic indicators use fixed SMA smoothing, which introduces consistent lag regardless of market volatility. This enhanced version addresses the limitation by offering adaptive algorithms that adjust to market conditions (KAMA, FRAMA), reduce lag without sacrificing smoothness (ZLEMA, T3, HMA), or provide superior noise filtering (Kalman Filter, Laguerre filters). The flexibility helps traders balance responsiveness and stability according to their specific needs.

📐 MATHEMATICAL FOUNDATION

Core Stochastic Calculation:

The Stochastic Oscillator measures the position of the current close relative to the high-low range over a specified period:

Step 1: Raw %K Calculation

%K_raw = 100 × (Close - Lowest Low) / (Highest High - Lowest Low)

Where:

Close = Current closing price

Lowest Low = Lowest low over the %K Length period

Highest High = Highest high over the %K Length period

Result ranges from 0 (close at period low) to 100 (close at period high)

Step 2: Smoothed %K Calculation

%K = MA(%K_raw, K Smoothing Period, MA Type)

Where:

MA = Selected moving average algorithm (SMA, EMA, etc.)

K Smoothing = 1 for Fast Stochastic, 3+ for Slow Stochastic

Traditional Fast Stochastic uses %K_raw directly without smoothing

Step 3: Signal Line %D Calculation

%D = MA(%K, D Smoothing Period, MA Type)

Where:

%D acts as a signal line and moving average of %K

D Smoothing typically set to 3 periods in traditional implementations

Both %K and %D use the same MA algorithm for consistent behavior

Available Smoothing Algorithms (21 Options):

Standard Moving Averages:

SMA (Simple): Equal-weighted average, traditional default, consistent lag characteristics

EMA (Exponential): Recent price emphasis, faster response to changes, exponential decay weighting

RMA (Rolling/Wilder's): Smoothed average used in RSI, less reactive than EMA

WMA (Weighted): Linear weighting favoring recent data, moderate responsiveness

VWMA (Volume-Weighted): Incorporates volume data, reflects market participation intensity

Advanced Moving Averages:

HMA (Hull): Reduced lag with smoothness, uses weighted moving averages and square root period

ALMA (Arnaud Legoux): Gaussian distribution weighting, minimal lag with good noise reduction

LSMA (Least Squares): Linear regression based, fits trend line to data points

DEMA (Double Exponential): Reduced lag compared to EMA, uses double smoothing technique

TEMA (Triple Exponential): Further lag reduction, triple smoothing with lag compensation

ZLEMA (Zero-Lag Exponential): Lag elimination attempt using error correction, very responsive

TMA (Triangular): Double-smoothed SMA, very smooth but slower response

Adaptive & Intelligent Filters:

T3 (Tilson T3): Six-pass exponential smoothing with volume factor adjustment, excellent smoothness

FRAMA (Fractal Adaptive): Adapts to market fractal dimension, faster in trends, slower in ranges

KAMA (Kaufman Adaptive): Efficiency ratio based adaptation, responds to volatility changes

McGinley Dynamic: Self-adjusting mechanism following price more accurately, reduced whipsaws

Kalman Filter: Optimal estimation algorithm from aerospace engineering, dynamic noise filtering

Advanced Digital Filters:

Ultimate Smoother: Advanced digital filter design, superior noise rejection with minimal lag

Laguerre Filter: Time-domain filter with N-order implementation, adjustable lag characteristics

Laguerre Binomial Filter: 6-pole Laguerre filter, extremely smooth output for long-term analysis

Super Smoother: Butterworth filter implementation, removes high-frequency noise effectively

📊 COMPREHENSIVE SIGNAL ANALYSIS

Absolute Level Interpretation (%K Line):

%K Above 80: Overbought condition, price near period high, potential reversal or pullback zone, caution for new long entries

%K in 70-80 Range: Strong upward momentum, bullish trend confirmation, uptrend likely continuing

%K in 50-70 Range: Moderate bullish momentum, neutral to positive outlook, consolidation or mild uptrend

%K in 30-50 Range: Moderate bearish momentum, neutral to negative outlook, consolidation or mild downtrend

%K in 20-30 Range: Strong downward momentum, bearish trend confirmation, downtrend likely continuing

%K Below 20: Oversold condition, price near period low, potential bounce or reversal zone, caution for new short entries

Crossover Signal Analysis:

%K Crosses Above %D (Bullish Cross): Momentum shifting bullish, faster line overtakes slower signal, consider long entry especially in oversold zone, strongest when occurring below 20 level

%K Crosses Below %D (Bearish Cross): Momentum shifting bearish, faster line falls below slower signal, consider short entry especially in overbought zone, strongest when occurring above 80 level

Crossover in Midrange (40-60): Less reliable signals, often in choppy sideways markets, require additional confirmation from trend or volume analysis

Multiple Failed Crosses: Indicates ranging market or choppy conditions, reduce position sizes or avoid trading until clear directional move

Advanced Divergence Patterns (%K Line vs Price):

Bullish Divergence: Price makes lower low while %K makes higher low, indicates weakening bearish momentum, potential trend reversal upward, more reliable when %K in oversold zone

Bearish Divergence: Price makes higher high while %K makes lower high, indicates weakening bullish momentum, potential trend reversal downward, more reliable when %K in overbought zone

Hidden Bullish Divergence: Price makes higher low while %K makes lower low, indicates trend continuation in uptrend, bullish trend strength confirmation

Hidden Bearish Divergence: Price makes lower high while %K makes higher high, indicates trend continuation in downtrend, bearish trend strength confirmation

Momentum Strength Analysis (%K Line Slope):

Steep %K Slope: Rapid momentum change, strong directional conviction, potential for extended moves but also increased reversal risk

Gradual %K Slope: Steady momentum development, sustainable trends more likely, lower probability of sharp reversals

Flat or Horizontal %K: Momentum stalling, potential reversal or consolidation ahead, wait for directional break before committing

%K Oscillation Within Range: Indicates ranging market, sideways price action, better suited for range-trading strategies than trend following

🎯 STRATEGIC APPLICATIONS

Mean Reversion Strategy (Range-Bound Markets):

Identify ranging market conditions using price action or Bollinger Bands

Wait for Stochastic to reach extreme zones (above 80 for overbought, below 20 for oversold)

Enter counter-trend position when %K crosses %D in extreme zone (sell on bearish cross above 80, buy on bullish cross below 20)

Set profit targets near opposite extreme or midline (50 level)

Use tight stop-loss above recent swing high/low to protect against breakout scenarios

Exit when Stochastic reaches opposite extreme or %K crosses %D in opposite direction

Trend Following with Momentum Confirmation:

Identify primary trend direction using higher timeframe analysis or moving averages

Wait for Stochastic pullback to oversold zone (<20) in uptrend or overbought zone (>80) in downtrend

Enter in trend direction when %K crosses %D confirming momentum shift (bullish cross in uptrend, bearish cross in downtrend)

Use wider stops to accommodate normal trend volatility

Add to position on subsequent pullbacks showing similar Stochastic pattern

Exit when Stochastic shows opposite extreme with failed cross or bearish/bullish divergence

Divergence-Based Reversal Strategy:

Scan for divergence between price and Stochastic at swing highs/lows

Confirm divergence with at least two price pivots showing divergent Stochastic readings

Wait for %K to cross %D in direction of anticipated reversal as entry trigger

Enter position in divergence direction with stop beyond recent swing extreme

Target profit at key support/resistance levels or Fibonacci retracements

Scale out as Stochastic reaches opposite extreme zone

Multi-Timeframe Momentum Alignment:

Analyze Stochastic on higher timeframe (4H or Daily) for primary trend bias

Switch to lower timeframe (1H or 15M) for precise entry timing

Only take trades where lower timeframe Stochastic signal aligns with higher timeframe momentum direction

Higher timeframe Stochastic in bullish zone (>50) = only take long entries on lower timeframe

Higher timeframe Stochastic in bearish zone (<50) = only take short entries on lower timeframe

Exit when lower timeframe shows counter-signal or higher timeframe momentum reverses

Zone Transition Strategy:

Monitor Stochastic for transitions between zones (oversold to neutral, neutral to overbought, etc.)

Enter long when Stochastic crosses above 20 (exiting oversold), signaling momentum shift from bearish to neutral/bullish

Enter short when Stochastic crosses below 80 (exiting overbought), signaling momentum shift from bullish to neutral/bearish

Use zone midpoint (50) as dynamic support/resistance for position management

Trail stops as Stochastic advances through favorable zones

Exit when Stochastic fails to maintain momentum and reverses back into prior zone

📋 DETAILED PARAMETER CONFIGURATION

%K Length (Default: 14):

Lower Values (5-9): Highly sensitive to price changes, generates more frequent signals, increased false signals in choppy markets, suitable for very short-term trading and scalping

Standard Values (10-14): Balanced sensitivity and reliability, traditional default (14) widely used,适合 swing trading and intraday strategies

Higher Values (15-21): Reduced sensitivity, smoother oscillations, fewer but potentially more reliable signals, better for position trading and lower timeframe noise reduction

Very High Values (21+): Slow response, long-term momentum measurement, fewer trading signals, suitable for weekly or monthly analysis

%K Smoothing (Default: 3):

Value 1: Fast Stochastic, uses raw %K calculation without additional smoothing, most responsive to price changes, generates earliest signals with higher noise

Value 3: Slow Stochastic (default), traditional smoothing level, reduces false signals while maintaining good responsiveness, widely accepted standard

Values 5-7: Very slow response, extremely smooth oscillations, significantly reduced whipsaws but delayed entry/exit timing

Recommendation: Default value 3 suits most trading scenarios, active short-term traders may use 1, conservative long-term positions use 5+

%D Smoothing (Default: 3):

Lower Values (1-2): Signal line closely follows %K, frequent crossover signals, useful for active trading but requires strict filtering

Standard Value (3): Traditional setting providing balanced signal line behavior, optimal for most trading applications

Higher Values (4-7): Smoother signal line, fewer crossover signals, reduced whipsaws but slower confirmation, better for trend trading

Very High Values (8+): Signal line becomes slow-moving reference, crossovers rare and highly significant, suitable for long-term position changes only

Smoothing Type Algorithm Selection:

For Trending Markets:

ZLEMA, DEMA, TEMA: Reduced lag for faster trend entry, quick response to momentum shifts, suitable for strong directional moves

HMA, ALMA: Good balance of smoothness and responsiveness, effective for clean trend following without excessive noise

EMA: Classic choice for trending markets, faster than SMA while maintaining reasonable stability

For Ranging/Choppy Markets:

Kalman Filter, Super Smoother: Superior noise filtering, reduces false signals in sideways action, helps identify genuine reversal points

Laguerre Filters: Smooth oscillations with adjustable lag, excellent for mean reversion strategies in ranges

T3, TMA: Very smooth output, filters out market noise effectively, clearer extreme zone identification

For Adaptive Market Conditions:

KAMA: Automatically adjusts to market efficiency, fast in trends and slow in congestion, reduces whipsaws during transitions

FRAMA: Adapts to fractal market structure, responsive during directional moves, conservative during uncertainty

McGinley Dynamic: Self-adjusting smoothing, follows price naturally, minimizes lag in trending markets while filtering noise in ranges

For Conservative Long-Term Analysis:

SMA: Traditional choice, predictable behavior, widely understood characteristics

RMA (Wilder's): Smooth oscillations, reduced sensitivity to outliers, consistent behavior across market conditions

Laguerre Binomial Filter: Extremely smooth output, ideal for weekly/monthly timeframe analysis, eliminates short-term noise completely

Source Selection:

Close (Default): Standard choice using closing prices, most common and widely tested

HLC3 or OHLC4: Incorporates more price information, reduces impact of sudden spikes or gaps, smoother oscillator behavior

HL2: Midpoint of high-low range, emphasizes intrabar volatility, useful for markets with wide intraday ranges

Custom Source: Can use other indicators as input (e.g., Heikin Ashi close, smoothed price), creates derivative momentum indicators

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Responsiveness Characteristics:

Traditional SMA-Based Stochastic:

Fixed lag regardless of market conditions, consistent delay of approximately (K Smoothing + D Smoothing) / 2 periods

Equal treatment of trending and ranging markets, no adaptation to volatility changes

Predictable behavior but suboptimal in varying market regimes

Enhanced Version with Adaptive Algorithms:

KAMA and FRAMA reduce lag by up to 40-60% in strong trends compared to SMA while maintaining similar smoothness in ranges

ZLEMA and T3 provide near-zero lag characteristics for early entry signals with acceptable noise levels

Kalman Filter and Super Smoother offer superior noise rejection, reducing false signals in choppy conditions by estimations of 30-50% compared to SMA

Performance improvements vary by algorithm selection and market conditions

Signal Quality Improvements:

Adaptive algorithms help reduce whipsaw trades in ranging markets by adjusting sensitivity dynamically

Advanced filters (Kalman, Laguerre, Super Smoother) provide clearer extreme zone readings for mean reversion strategies

Zero-lag methods (ZLEMA, DEMA, TEMA) generate earlier crossover signals in trending markets for improved entry timing

Smoother algorithms (T3, Laguerre Binomial) reduce false extreme zone touches for more reliable overbought/oversold signals

Comparison with Standard Implementations:

Versus Basic Stochastic: Enhanced version offers 21 smoothing options versus single SMA, allowing optimization for specific market characteristics and trading styles

Versus RSI: Stochastic provides range-bound measurement (0-100) with clear extreme zones, RSI measures momentum speed, Stochastic offers clearer visual overbought/oversold identification

Versus MACD: Stochastic bounded oscillator suitable for mean reversion, MACD unbounded indicator better for trend strength, Stochastic excels in range-bound and oscillating markets

Versus CCI: Stochastic has fixed bounds (0-100) for consistent interpretation, CCI unbounded with variable extremes, Stochastic provides more standardized extreme readings across different instruments

Flexibility Advantages:

Single indicator adaptable to multiple strategies through algorithm selection rather than requiring different indicator variants

Ability to optimize smoothing characteristics for specific instruments (e.g., smoother for crypto volatility, faster for forex trends)

Multi-timeframe analysis with consistent algorithm across timeframes for coherent momentum picture

Backtesting capability with algorithm as optimization parameter for strategy development

Limitations and Considerations:

Increased complexity from multiple algorithm choices may lead to over-optimization if parameters are curve-fitted to historical data

Adaptive algorithms (KAMA, FRAMA) have adjustment periods during market regime changes where signals may be less reliable

Zero-lag algorithms sacrifice some smoothness for responsiveness, potentially increasing noise sensitivity in very choppy conditions

Performance characteristics vary significantly across algorithms, requiring understanding and testing before live implementation

Like all oscillators, Stochastic can remain in extreme zones for extended periods during strong trends, generating premature reversal signals

USAGE NOTES

This indicator is designed for technical analysis and educational purposes to provide traders with enhanced flexibility in momentum analysis. The Stochastic Oscillator has limitations and should not be used as the sole basis for trading decisions.

Important Considerations:

Algorithm performance varies with market conditions - no single smoothing method is optimal for all scenarios

Extreme zone signals (overbought/oversold) indicate potential reversal areas but not guaranteed turning points, especially in strong trends

Crossover signals may generate false entries during sideways choppy markets regardless of smoothing algorithm

Divergence patterns require confirmation from price action or additional indicators before trading

Past indicator characteristics and backtested results do not guarantee future performance

Always combine Stochastic analysis with proper risk management, position sizing, and multi-indicator confirmation

Test selected algorithm on historical data of specific instrument and timeframe before live trading

Market regime changes may require algorithm adjustment for optimal performance

The enhanced smoothing options are intended to provide tools for optimizing the indicator's behavior to match individual trading styles and market characteristics, not to create a perfect predictive tool. Responsible usage includes understanding the mathematical properties of selected algorithms and their appropriate application contexts.

Cumulative Volume Delta Profile and Heatmap [BackQuant]Cumulative Volume Delta Profile and Heatmap

A multi-view CVD workstation that measures buying vs selling pressure, renders a price-aligned CVD profile with Point of Control, paints an optional heatmap of delta intensity, and detects classical CVD divergences using pivot logic. Built for reading who is in control, where participation clustered, and when effort is failing to produce result.

What is CVD

Cumulative Volume Delta accumulates the difference between aggressive buys and aggressive sells over time. When CVD rises, buyers are lifting the offer more than sellers are hitting the bid. When CVD falls, the opposite is true. Plotting CVD alongside price helps you judge whether price moves are supported by real participation or are running on fumes.

Core Features

Visual Analysis Components

CVD Columns - Plot of cumulative delta, colored by side, for quick read of participation bias.

CVD Profile - Price-aligned histogram of CVD accumulation using user-set bins. Shows where net initiative clustered.

Split Buy and Sell CVD - Optional two-sided profile that separates positive and negative CVD into distinct wings.

POC - Point of Control - The price level with the highest absolute CVD accumulation, labeled and line-marked.

Heatmap - Semi-transparent blocks behind price that encode CVD intensity across the last N bars.

Divergence Engine - Pivot-based detection of Bearish and Bullish CVD divergences with optional lines and labels.

Stats Panel - Top level metrics: Total CVD, Buy and Sell totals with percentages, Delta Ratio, and current POC price.

How it works

Delta source and sampling

You select an Anchor Timeframe that defines the higher time aggregation for reading the trend of CVD.

The script pulls lower timeframe volume delta and aggregates it to the anchor window. You can let it auto-select the lower timeframe or force a custom one.

CVD is then accumulated bar by bar to form a running total. This plot shows the direction and persistence of initiative.

Profile construction

The recent price range is split into Profile Granularity bins.

As price traverses a bin, the current delta contribution is added to that bin.

If Split Buy and Sell CVD is enabled, positive CVD goes to the right wing and negative CVD to the left wing.

Widths are scaled by each side’s maximum so you can compare distribution shape at a glance.

The Point of Control is the bin with the highest absolute CVD. This marks where initiative concentrated the most.

Heatmap

For each bin, the script computes intensity as absolute CVD relative to the maximum bin value.

Color is derived from the side in control in that bin and shaded by intensity.

Heatmap Length sets how far back the panels extend, highlighting recurring participation zones.

Divergence model

You define pivot sensitivity with Pivot Left and Right .

Bearish divergence triggers when price confirms a higher high while CVD fails to make a higher high within a configurable Delta Tolerance .

Bullish divergence triggers when price confirms a lower low while CVD fails to make a lower low.

On trigger, optional link lines and labels are drawn at the pivots for immediate context.

Key Settings

Delta Source

Anchor Timeframe - Higher TF for the CVD narrative.

Custom Lower TF and Lower Timeframe - Force the sampling TF if desired.

Pivot Logic

Pivot Left and Right - Bars to each side for swing confirmation.

Delta Tolerance - Small allowance to avoid near-miss false positives.

CVD Profile

Show CVD Profile - Toggle profile rendering.

Split Buy and Sell CVD - Two-sided profile for clearer side attribution.

Show Heatmap - Project intensity panels behind price.

Show POC and POC Color - Mark the dominant CVD node.

Profile Granularity - Number of bins across the visible price range.

Profile Offset and Profile Width - Position and scale the profile.

Profile Position - Right, Left, or Current bar alignment.

Visuals

Bullish Div Color and Bearish Div Color - Colors for divergence artifacts.

Show Divergence Lines and Labels - Visualize pivots and annotations.

Plot CVD - Column plot of total CVD.

Show Statistics and Position - Toggle and place the summary table.

Reading the display

CVD columns

Rising CVD confirms buyers are in control. Falling CVD confirms sellers.

Flat or choppy CVD during wide price moves hints at passive or exhausted participation.

CVD profile wings

Thick right wing near a price zone implies heavy buy initiative accumulated there.

Thick left wing implies heavy sell initiative.

POC marks the strongest initiative node. Expect reactions on first touch and rotations around this level when the tape is balanced.

Heatmap

Brighter blocks indicate stronger historical net initiative at that price.

Stacked bright bands form CVD high volume nodes. These often behave like magnets or shelves for future trade.

Divergences

Bearish - Price prints a higher high while CVD fails to do so. Effort is not producing result. Potential fade or pause.

Bullish - Price prints a lower low while CVD fails to do so. Capitulation lacks initiative. Potential bounce or reversal.

Stats panel

Total CVD - Net initiative over the window.

Buy and Sell volume with percentages - Side composition.

Delta Ratio - Buy over Sell. Values above 1 favor buyers, below 1 favor sellers.

POC Price - Current control node for plan and risk.

Workflows

Trend following

Choose an Anchor Timeframe that matches your holding period.

Trade in the direction of CVD slope while price holds above a bullish POC or below a bearish POC.

Use pullbacks to CVD nodes on your profile as entry locations.

Trend weakens when price makes new highs but CVD stalls, or new lows while CVD recovers.

Mean reversion

Look for divergences at or near prior CVD nodes, especially the POC.

Fade tests into thick wings when the side that dominated there now fails to push CVD further.

Target rotations back toward the POC or the opposite wing edge.

Liquidity and execution map

Treat strong wings and heatmap bands as probable passive interest zones.

Expect pauses, partial fills, or flips at these shelves.

Stops make sense beyond the far edge of the active wing supporting your idea.

Alerts included

CVD Bearish Divergence and CVD Bullish Divergence.

Price Cross Above POC and Price Cross Below POC.

Extreme Buy Imbalance and Extreme Sell Imbalance from Delta Ratio.

CVD Turn Bullish and CVD Turn Bearish when net CVD crosses zero.

Price Near POC proximity alert.

Best practices

Use a higher Anchor Timeframe to stabilize the CVD story and a sensible Profile Granularity so wings are readable without clutter.

Keep Split mode on when you want to separate initiative attribution. Turn it off when you prefer a single net profile.

Tune Pivot Left and Right by instrument to avoid overfitting. Larger values find swing divergences. Smaller values find micro fades.

If volume is thin or synthetic for the symbol, CVD will be less reliable. The script will warn if volume is zero.

Trading applications

Context - Confirm or question breakouts with CVD slope.

Location - Build entries at CVD nodes and POC.

Timing - Use divergence and POC crosses for triggers.

Risk - Place stops beyond the opposite wing or outside the POC shelf.

Important notes and limits

This is a price and volume based study. It does not access off-book or venue-level order flow.

CVD profiles are built from the data available on your chart and the chosen lower timeframe sampling.

Like all volume tools, readings can distort during roll periods, holidays, or feed anomalies. Validate on your instrument.

Technical notes

Delta is aggregated from a lower timeframe into an Anchor Timeframe narrative.

Profile bins update in real time. Splitting by side scales each wing independently so both are readable in the same panel.

Divergences are confirmed using standard pivot definitions with user-set tolerances.

All profile drawing uses fixed X offsets so panels and POC do not swim when you scroll.

Quick start

Anchor Timeframe = Daily for intraday context.

Split Buy and Sell CVD = On.

Profile Granularity = 100 to 200, Profile Position = Right, Width to taste.

Pivot Left and Right around 8 to 12 to start, then adapt.

Turn on Heatmap for a fast map of interest bands.

Bottom line

CVD tells you who is doing the lifting. The profile shows where they did it. Divergences tell you when effort stops paying. Put them together and you get a clear read on control, location, and timing for both trend and mean reversion.

Nifty vs Nifty Fut Premium indicator This indicator compares Nifty Spot and Nifty Futures prices in real-time, displaying the premium (or discount) between them at the top of the pane.

Trading applications:

Arbitrage opportunities: When the premium becomes unusually high or low compared to fair value (based on cost of carry), traders can exploit the mispricing through cash-futures arbitrage

Market sentiment: A rising premium often indicates bullish sentiment as traders are willing to pay more for futures, while a declining or negative premium suggests bearish sentiment

Rollover strategy: Near expiry, monitoring the premium helps traders decide optimal timing for rolling positions from current month to next month contracts

Risk assessment: Sudden spikes in premium can signal increased demand for leveraged long positions, potentially indicating overbought conditions or strong momentum

Rolling Midpoint of Price & VWAP with ATR BandsThe Rolling Midpoint of Price & VWAP with ATR Bands indicator is a dual-equilibrium concept that fuses price-range structure and traded-volume flow into one continuously updating hybrid model. Traditional VWAPs reset each session and reflect where trading occurred by volume, while midpoints used here reveal where price has structurally balanced between extremes. This script merges both ideas into a cohesive, dynamic system. The Rolling Price Midpoint (50 % of range) represents the structural fair-value line, calculated as the average of the highest high and lowest low over a selected window. The Rolling VWAP (Volume-Weighted Window) tracks the flow-based fair-value line by weighting each bar’s typical price by its volume. Together, these components form the Hybrid Equilibrium — the adaptive center of gravity that shifts as price and volume evolve. Surrounding this equilibrium, ATR Bands at ± 2.226 ATR and ± 5.382 ATR define volatility envelopes that expand and contract with market energy. The result is a living cloud that breathes with the market: compressing during phases of balance and widening during impulsive movements, offering traders a clear visual framework for understanding equilibrium, volatility, and directional bias in real time.

➖

⚙️ Auto-Preset System

The Auto-Preset System intelligently adjusts lookback windows for both the Price Midpoint and VWAP calculations according to the active chart timeframe.

This ensures that the indicator automatically adapts to any trading style — from scalping on 1-minute charts to swing trading on daily or weekly charts — without manual tuning.

🔹 How It Works

When Auto-Preset mode is enabled, the script dynamically selects the most effective lookback lengths for each timeframe.

These presets are optimized to balance responsiveness and stability, maintaining consistent real-world coverage (e.g., the same approximate duration of price data) across all intervals.

📊 Preset Mapping Table

| Chart Timeframe | Price Midpoint Lookback | VWAP Lookback |

|:----------------:|:-----------------------:|:--------------:|

| 1–3m | 13 bars | 21 bars

| 5–10m | 21 bars | 34 bars

| 15–30m | 34 bars | 55 bars

| 1–2 hr | 55 bars | 89 bars

| 4 hr-1D | 89 bars | 144 bars

| 1W | 144 bars | 233 bars

| 1M | 233 bars | 377 bars

⚡ Notes & Customization

- Manual Override: Turn off Auto-Preset Mode to specify your own custom lookback lengths.

- Consistency Across Scales: These adaptive values keep the indicator visually coherent when switching between timeframes — avoiding distortions that can occur with static lengths.

- Practical Benefit: Traders can maintain a single chart layout that self-tunes seamlessly, removing the need to manually recalibrate settings when shifting from short-term to long-term analysis.

In short, the Auto-Preset System is designed to make this hybrid equilibrium tool timeframe-aware — automatically scaling its logic so that the cloud behaves consistently, regardless of chart resolution.

➖

🌐 Hybrid Equilibrium Envelope

The core hybrid midpoint acts as the mean of structural (price) and volumetric (VWAP) balance.

ATR-based bands project natural expansion zones:

🔸+2.226 / –2.226 ATR → inner equilibrium (controlled trend)

*🔸+5.382 / –5.382 ATR → outer volatility extension (over-stretch / reversion zones)

Color-coded fills show regime strength:

* 🟧 Upper Outer (+5.382) – strong bullish expansion

* 🟩 Upper Inner (+2.226) – trending equilibrium

* 🔴 Lower Inner (–2.226) – mild bearish control

* 🟣 Lower Outer (–5.382) – volatility exhaustion

➖

🧭 Higher-Timeframe Framework

Two macro anchors — Price length of 144 and VWAP length of 233 — outline higher-timeframe bias zones. These help confirm when local momentum aligns with (or fades against) long-term structure.

Labels on the right show active lookback values for quick readout:

`$(13) V(21)` → current rolling pair

`$144 / V233` → macro anchors

➖

🧩 Chart Examples

**AMD 15m (Equilibrium Expansion)**

Price steadily rides above the hybrid midpoint as teal and orange (bullish) ATR zones widen, confirming a phase of controlled bullish volatility and healthy trend expansion.

BTCUSD 1m (Volatility Compression)

Bitcoin coils tightly inside the teal-to-maroon equilibrium bands before breaking out.

The hybrid midpoint flattens and ATR envelopes contract, signaling a state of balance before volatility expansion.

ETHUSD 15m (Transition from Compression → Impulse)

Ethereum transitions from purple-zone compression into a clear upper-band expansion.

The hybrid midpoint breaks above the macro VWAP 233, confirming the shift from equilibrium to directional momentum.

SOFI 1m (Micro Bias Reversal)

SOFI’s intraday structure flips as price reclaims the hybrid midpoint.

The macro VWAP 233 flattens, signaling a transition from oversold lower bands back toward equilibrium and early trend recovery.

➖

🎯 How to Use

1. Bias Detection – Price > Hybrid Midpoint → bullish; < → bearish.

2. Volatility Gauge – Watch band spacing for compression / expansion cycles.

3. Confluence Checks – Align Hybrid Midpoint with HTF 233 VWAP for strong continuation signals.

4. Mean Reversion Zones – Outer bands highlight areas where probability of snap-back increases.

➖

🔧 Inputs & Customization

Auto Presets toggle

🔸Manual Lookback Overrides** for fine-tuning

🔸Plot Window Length** (show recent vs full history)

🔸ATR Sensitivity & Fill Opacity** controls

🔸Label Padding / Font Size** for cleaner overlay visuals

➖

🧮 Formula Highlights

➖Rolling Midpoint = (highest(high,N) + lowest(low,N)) / 2

➖Rolling VWAP = Σ(Typical Price×Vol) / Σ(Vol)

➖Hybrid = (PriceMid + VWAP) / 2

➖Upper₂ = Hybrid + ATR×2.226

➖Lower₂ = Hybrid − ATR×2.226

➖Upper₅ = Hybrid + ATR×5.382

➖Lower₅ = Hybrid − ATR×5.382

➖

🎯 Ideal For

➡️ Traders who want adaptive fair-value zones that evolve with both price and volume.

➡️ Analysts who shift between scalping, swing, and position timeframes, and need a tool that self-adjusts.

➡️ Those who rely on visual structure clarity to confirm setups across changing volatility conditions.

➡️ Anyone seeking a hybrid model that unites structural range logic (midpoint) and flow-based balance (VWAP).

➖

🏁 Final Word

This script is more than a visual overlay — it’s a complete trend and structure framework built to adapt with market rhythm. It helps traders visualize equilibrium, momentum, and volatility as one cohesive system. Whether you’re seeking clean trend alignment, dynamic support/resistance, or early warning signs of reversals, this indicator is tuned to help you react with confidence — not hindsight.

➖

Remember — no single indicator should ever stand alone. For best results, pair it with price action context, higher-timeframe structure, and complementary tools such as moving averages or trendlines. Use it to confirm setups, not define them in isolation.

💡 Turn logic into clarity, structure into trades, and uncertainty into confidence.

Smart Money Volume Activity [AlgoAlpha]🟠 OVERVIEW

This tool visualizes how Smart Money and Retail participants behave through lower-timeframe volume analysis. It detects volume spikes far beyond normal activity, classifies them as institutional or retail, and projects those zones as reactive levels. The script updates dynamically with each bar, showing when large players enter while tracking whether those events remain profitable. Each event is drawn as a horizontal line with bubble markers and summarized in a live P/L table comparing Smart Money versus Retail.

🟠 CONCEPTS

The core logic uses Z-score normalization on lower-timeframe volumes (like 5m inside a 1h chart). This lets the script detect statistically extreme bursts of buying or selling activity. It classifies each detected event as:

Smart Money — volume inside the candle body (suggesting hidden accumulation or distribution)

Retail — volume closing at bar extremes (suggesting chase entries or panic exits)

When new events appear, the script plots them as horizontal levels that persist until price interacts again. Each level acts as a potential reaction zone or liquidity footprint. The integrated P/L table then measures which class (Retail or Smart Money) is currently “winning” — comparing cumulative profitable versus losing volume.

🟠 FEATURES

Classifies flows into Smart Money or Retail based on candle-body context.

Displays live P/L comparison table for Smart vs Retail performance.

Alerts for each detected Smart or Retail buy/sell event.

🟠 USAGE

Setup : Add the script to any chart. Set Lower Timeframe Value (e.g., “5” for 5m) smaller than your main chart timeframe. The Period input controls how many bars are analyzed for the Z-score baseline. The Threshold (|Z|) decides how extreme a volume must be to plot a level.

Read the chart : Horizontal lines mark where heavy Smart or Retail volume occurred. Bright bubbles show the strongest events — their size reflects Z-score intensity. The on-chart table updates live: green cells show profitable flows, red cells show losing flows. A dominant green Smart Money row suggests institutions are currently controlling price.

See what others are doing :

Settings that matter : Raising Threshold (|Z|) filters noise, showing only large players. Increasing Period smooths results but reacts slower to new bursts. Use Show = “Both” for full comparison or isolate “Smart Money” / “Retail” to focus on one class.

FVG Scanner ProFVG Scanner Pro — Smart Fair Value Gap Detector (with HTF context & proximity alerts)

What it does

FVG Scanner Pro automatically finds Fair Value Gaps (FVGs) on your current chart and (optionally) on a higher timeframe (HTF), draws them as color-coded zones, and notifies you when price comes close to a gap boundary using an ADR-based proximity trigger and (optional) volume confirmation. It’s designed for ICT-style gap trading, confluence building, and clean visual execution.

How it works:

FVG definition

* Bullish FVG (gap up): low > high (the current candle’s low is above the high 2 bars ago).

* Bearish FVG (gap down): high < low (the current candle’s high is below the low 2 bars ago).

* Gaps smaller than your Min FVG Size (%) are ignored. (Gap size = (top-bottom)/bottom * 100.)

Higher-timeframe logic (auto-selected)

The script auto picks a sensible HTF:

1–5m → 15m, 15m → 1H, 1H → 4H, 4H → 1D, 1D → 1W, 1W → 1M, small 1M → 3M, big ≥3M → 12M.

You can display HTF FVGs and even filter so current-TF FVGs only show when they overlap an HTF gap.

Proximity alerts (ADR-based)

The script computes ADR on the current chart timeframe over a user-set lookback (default 20 bars).

An alert fires when price moves toward the closest actionable boundary and comes within ADR × Multiplier:

Bullish: price moving down, within distance of the bottom of a bullish FVG.

Bearish: price moving up, within distance of the top of a bearish FVG.

Yellow ▲/▼ markers show where a proximity alert triggered.

Volume filter (optional)

Require volume to be greater than SMA(20) × multiplier to accept a newly formed FVG.

Lifecycle

Each gap remains active for Extend FVG Box (Bars) bars.

You can delete the box after fill, or keep filled gaps visible as gray zones, or hide them.

Color legend

Current-TF Bullish: Pink/Magenta box

Current-TF Bearish: Cyan/Turquoise box

HTF Bullish: Gold box

HTF Bearish: Orange box

Filled (if shown): Gray box

Alert markers: Yellow ▲ (bullish), Yellow ▼ (bearish)

Inputs (what to tweak)

Show FVGs: Bullish / Bearish / Both

Max Bars Back to Find FVG: collection window & cleanup guard

Extend FVG Box (Bars): how long a zone stays tradable/active

Min FVG Size (%): ignore micro gaps

Delete Box After Fill & Show Filled FVGs: choose how you want completed gaps handled

Show Alert Markers: show/hide the yellow proximity arrows

Show Higher Timeframe FVG: overlay HTF gaps (auto TF)

HTF Filter: only display current-TF gaps that overlap an HTF gap

ADR Lookback & Proximity Multiplier: tune alert sensitivity to your market & timeframe

Volume Filter & Volume > MA Multiple: require above-average volume for new gaps

Built-in alerts (ready to use)

Create alerts in TradingView (⚠️ “Once per bar” or “Once per bar close”, your choice) and select from:

🟢 Bullish FVG Proximity — price approaching a bullish gap bottom

🔴 Bearish FVG Proximity — price approaching a bearish gap top

✅ New Bullish FVG Formed

⚠️ New Bearish FVG Formed

The alert messages include the symbol and price; proximity markers are also plotted on chart.

Tips & best practices

Use FVGs with market structure (break of structure, swing points), order blocks, or liquidity pools for confluence.

On very low timeframes, raise Min FVG Size and/or lower Max Bars Back to reduce noise and keep things fast.

Extend FVG Box controls how long a zone is considered valid; align it with your holding horizon (scalp vs swing).

Information panel (top-right)

Shows your mode, current HTF, number of gaps in memory, active bull/bear counts, and current-TF ADR.

US Opening 5-Minute Candle HighlighterUS Opening 5-Minute Candle Highlighter — True RVOL (Two-Tier + Label)

What it does (in plain English)

This indicator finds the first 5-minute bar of the US cash session (09:30–09:35 ET) and highlights it when the candle has the specific “strong open” look you want:

Opens near the low of its own range, and

Closes near the high of its own range, and

Has a decisive real body (not a wick-y doji), and

(Optionally) is a green candle, and

Meets a TRUE opening-bar RVOL filter (compares today’s 09:30–09:35 volume only to prior sessions’ 09:30–09:35 volumes).

You get two visual intensities based on opening RVOL:

Tier-1 (≥ threshold 1, default 1.0×) → light green highlight + lime arrow

Tier-2 (≥ threshold 2, default 1.5×) → darker green highlight + green arrow

An RVOL label (e.g., RVOL 1.84x) can be shown above or below the opening bar.

Designed for 5-minute charts. On other timeframes the “opening bar” will be the bar that starts at 09:30 on that timeframe (e.g., 15-minute 09:30–09:45). For best results keep the chart on 5m.

How the pattern is defined

For the opening 5-minute bar, we compute:

Range = high − low

Body = |close − open|

Then we measure where the open and close sit within the bar’s own range on a 0→1 scale:

0 means exactly at the low

1 means exactly at the high

Using two quantiles:

Open ≤ position in range (0–1) (default 0.20)

Example: 0.20 means “open must be in the lowest 20% of the bar’s range.”

Close ≥ position in range (0–1) (default 0.80)

Example: 0.80 means “close must be in the top 20% of the bar’s range.”

This keeps the logic range-normalized so it adapts across different tickers and vol regimes (you’re not using fixed cents or % of price).

Body ≥ fraction of range (0–1) (default 0.55)

Requires the real body to be at least that fraction of the total range.

0.55 = body fills ≥ 55% of the candle.

Purpose: filter out indecisive, wick-heavy bars.

Raise to 0.7–0.8 for only the fattest thrusts; lower to 0.3–0.4 to admit more bars.

Require green candle? (default ON)

If ON, close > open must be true. Turn OFF if you also want to catch strong red opens for shorts.

Minimum range (ticks)

Ignore tiny, illiquid opens: e.g., set to 2–5 ticks to suppress micro bars.

TRUE Opening-Bar RVOL (why it’s “true”)

Most “RVOL” compares against any recent bars, which isn’t fair at the open.

This indicator calculates only against prior opening bars:

At 09:30–09:35 ET, take today’s opening 5-minute volume.

Compare it to the average of the last N sessions’ opening 5-minute volumes.

RVOL = today_open_volume / average_prior_open_volumes.

So:

1.0× = equal to average prior opens.

1.5× = 150% of average prior opens.

2.0× = double the typical opening participation.

A minimum prior samples guard (default 10) ensures you don’t judge with too little history. Until enough samples exist, the RVOL gate won’t pass (you can disable RVOL temporarily if needed).

Visuals & tiers

Light green highlight + lime arrow → price filters pass and RVOL ≥ Tier-1 (default 1.0×)

Dark green highlight + green arrow → price filters pass and RVOL ≥ Tier-2 (default 1.5×)

Optional bar paint in matching green tones for extra visibility.

Optional RVOL label (e.g., RVOL 1.84x) above or below the opening bar.

You can show the label only when the candle qualifies, or on every open.

Inputs (step-by-step)

Price-action filters

Open ≤ position in range (0–1): default 0.20. Smaller = stricter (must open nearer the low).

Close ≥ position in range (0–1): default 0.80. Larger = stricter (must close nearer the high).

Body ≥ fraction of range (0–1): default 0.55. Raise to demand a “fatter” body.

Require green candle?: default ON. Turn OFF to also mark bearish thrusts.

Minimum range (ticks): default 0. Set to 2–5 for liquid mid/large caps.

Time settings

Timezone: default America/New_York. Leave as is for US equities.

Start hour / minute: defaults 09:30. The bar that starts at this time is evaluated.

TRUE Opening-Bar RVOL (two-tier)

Require TRUE opening-bar RVOL?: ON = must pass Tier-1 to highlight; OFF = price filters alone can highlight (still shows Tier-2 when hit).

RVOL lookback (prior opens count): default 20. How many prior openings to average.

Min prior opens required: default 10. Warm-up guard.

Tier-1 RVOL threshold (× avg): default 1.00× (light green).

Tier-2 RVOL threshold (× avg): default 1.50× (dark green).

Display

Also paint candle body?: OFF by default. Turn ON for instant visibility on a chart wall.

Arrow size: tiny/small/normal/large.

Light/Dark opacity: tune highlight strength.

Show RVOL label?: ON/OFF.

Show label only when candle qualifies?: ON by default; OFF to see RVOL every open.

Label position: Above candle or Below candle.

Label size: tiny/small/normal/large.

How to use (quick start)

Apply to a 5-minute chart.

Keep defaults: Open ≤ 0.20, Close ≥ 0.80, Body ≥ 0.55, Require green ON.

Turn RVOL required ON, with Tier-1 = 1.0×, Tier-2 = 1.5×, Lookback = 20, Min prior = 10.

Optional: enable Paint bar and set Arrow size = large for monitor-wall visibility.

Optional: show RVOL label below the bar to keep wicks clean.

Interpretation:

Dark green = A+ opening thrust with strong participation (≥ Tier-2).

Light green = Valid opening thrust with at least average participation (≥ Tier-1).

No highlight = one or more filters failed (quantiles, body, green, range, or RVOL if required).

Alerts

Two alert conditions are included:

Opening 5m Match — Tier-2 RVOL → fires when the opening candle passes price filters and RVOL ≥ Tier-2.

Opening 5m Match — Tier-1 RVOL → fires when the opening candle passes price filters and RVOL ≥ Tier-1 (but < Tier-2).

Recommended alert settings

Condition: choose the script + desired tier.

Options: Once Per Bar Close (you want the confirmed 09:30–09:35 bar).

Set your watchlist to symbols of interest (themes/sectors) and let the alerts pull you to the right charts.

Recommended starting values

Quantiles: Open ≤ 0.20, Close ≥ 0.80

Body fraction: 0.55

Require green: ON

RVOL: Required ON, Tier-1 = 1.0×, Tier-2 = 1.5×, Lookback 20, Min prior 10

Display: Paint bar ON, Arrow large, Label ON, Below candle

Tune tighter for A-plus selectivity:

Open ≤ 0.15, Close ≥ 0.85, Body ≥ 0.65, Tier-2 2.0×.

Notes, tips & limitations

5-minute timeframe is the intended use. On higher TFs, the 09:30 bar spans more than 5 minutes; geometry may not reflect the first 5 minutes alone.

RTH only: The opening detection looks at the clock (09:30 ET). Pre-market bars are ignored for the signal and for RVOL history.

Warm-up period: Until you have Min prior opens required samples, the RVOL gate won’t pass. You can temporarily toggle RVOL off.

DST & timezone: Leave timezone on America/New_York for US equities. If you trade non-US exchanges, set the appropriate TZ and opening time.

Illiquid tickers: Use Minimum range (ticks) and require RVOL to reduce noise.

No strategy orders: This is a visual/alert tool. Combine with your execution and risk plan.

Why this is useful on multi-monitor setups

Instant pattern recognition: the two-shade green makes A vs A+ opens pop at a glance.

Adaptive thresholds: quantiles & body are within-bar, so it works across $5 and $500 names.

Fair volume test: TRUE opening RVOL avoids comparing to pre-market or midday bars.

Optional labels: glanceable RVOL x-value helps triage the strongest themes quickly.

XAUUSD/SPX with SMA(48)📊 Gold vs S&P 500 | XAUUSD/SPX Ratio with SMA (48) – Full Pine Script Breakdown

In this video, we build and explain a custom Pine Script that plots the Gold to S&P 500 ratio (XAUUSD/SPX) along with a 48-period Simple Moving Average (SMA).

This ratio helps us analyze how Gold is performing against equities and whether smart money is shifting from risk assets (stocks) to safe haven (gold).

🔧 What’s Included in the Script:

✅ Live ratio of XAUUSD (Gold) / SPX (S&P 500)

✅ 48-period SMA for trend analysis

✅ Clean visual chart in a separate pane

✅ Pine Script v5 compatible

🧠 Why This Matters:

Tracking the XAUUSD/SPX ratio gives deeper insight into macro trends, inflation hedge behavior, and market sentiment.

A rising ratio can signal weakness in equities and strength in precious metals — a key trend for long-term investors and macro traders.

Session Volume Spike DetectorSession Volume Spike Detector (Buy/Sell, Dual Windows, MTF + Edge/Cooldown)

What it does

Detects statistically significant buy/sell volume spikes inside two DST-aware Mountain Time sessions and projects 1m / 5m / 10m signals onto any chart timeframe (even 1s). Spikes are confirmed at the close of their native bar and are edge-triggered with optional cooldowns to prevent duplicate alerts.

How spikes are detected

Volume ≥ SMA × multiplier

Optional jump vs recent highest volume

Optional Z-Score gate for significance

Separate Buy/Sell logic using your Direction Mode (Prev Close or Candle Body)

Multi-Timeframe (MTF) display

Shows 1m, 5m, 10m arrows on your current chart

Each HTF fires once on its bar close (no repaint after close)

Sessions (DST-aware, MT)

Morning: 05:30–08:30

Midday: 11:00–13:30

Spikes only count inside these windows.

Inputs & styling

Thresholds: SMA length, multipliers, recent lookback, Z-Score toggle/level

Toggles for which TFs to display (chart TF, 1m, 5m, 10m)

Per-TF colors + cooldowns (seconds) for Any TF, 1m, 5m, 10m

Alerts (edge + cooldown)

MTF Volume Spike (Any TF) — fires on the first qualifying spike across enabled TFs

1m / 5m / 10m Volume Spike — per-TF alerts, Buy or Sell

Recommended: set alert Trigger = Once per bar close. Cooldowns tame “triggered too often” warnings.

Great with

FVG zones, bank/insto levels, session range breaks, and trend filters. Use the MTF arrows as a participation/pressure tell to confirm or fade moves.

Notes

Works on any symbol/timeframe; best viewed on 1m or sub-minute charts.

HTF spikes appear on the bar close of 1m/5m/10m respectively.

No dynamic plot titles; Pine v6-safe.

Short summary (≤250 chars):

MTF volume-spike detector for intraday sessions (DST-aware, MT). Projects 1m/5m/10m buy/sell spikes onto any chart, with edge-triggered alerts and per-TF cooldowns to prevent duplicates. Ideal for spotting institutional participation.

Elipli5648This indicator displays two moving averages on the same chart — the 9-period and 200-period simple moving averages (SMA).

Both lines are customizable in color and line width directly from the settings menu.

Useful for identifying short-term vs long-term trend direction.

elipli5648 , MA 9 & 200 (Combined) — clean versionThis indicator displays two moving averages on the same chart — the 9-period and 200-period simple moving averages (SMA).

Both lines are customizable in color and line width directly from the settings menu.

Useful for identifying short-term vs long-term trend direction.

Micro SuiteWhat it is: One Pine v5 indicator that stacks several tools: EMA ribbon + a color-flipping 11/34 EMA trend line, multi-timeframe RSI pressure arrows, and a Bollinger Band re-entry system that marks Top/Bottom triggers (T/B) and later “r” confirmations. It also sprinkles in 3-Line Strike, Leledc exhaustion dots, and a small “Micro Dots” engine (ATR regime + VMA filter). Alerts for all of it.

TradingView

The core signals you’ll actually use:

RSI arrows: Up arrow when current RSI(6) < 30 and selected higher-TF RSIs are also < 30; down arrow when > 70 cluster cools. Idea = stacked OB/OS “pressure.”

TradingView

Bollinger re-entry (T/B + r):

T = first close back inside upper band; B = first close back inside lower band.

r = confirmation within N bars (price takes out the trigger bar’s high/low). These bars tint so they’re easy to see.

TradingView

Trend filter: EMA-11 vs EMA-34 color flip + optional VMA trend line; helps you ignore counter-trend stabs.

TradingView

Quick playbook (how to read it):

Reversal short: See a T near the top band → get the r within your window → bonus if a down RSI arrow or a Leledc high dot shows up.

Reversal long: Mirror that with B → r, plus an up RSI arrow/Leledc low dot.

Continuation: If Micro Dot stays green (or red) and 11>34 EMA holds, ignore isolated T/B traps.

TradingView

Inputs that matter:

confirmBars for the T/B “r” window.

Which higher-TF RSIs must agree for arrows.

Show/hide and lengths for EMAs and BB.

Micro block: show dots, VMA line, and speed (Fast/Med/Slow).

TradingView

Why people like it: You get trend, momentum, and mean-revert cues on one pane with ready-made alerts, so it’s easier to build a ruleset (e.g., “only take B→r longs when 11>34 and there’s an RSI up arrow”).

TradingView

Caveats: It’s still just TA—OB/OS clusters can persist in trends; confirmations can miss V-shaped turns; and stacking signals can be late in fast markets. Pair it with risk rules (fixed R, ATR stops) and a higher-TF bias.

One-liner cheat sheet:

Longs: B → r + RSI up arrow + 11>34 (optional Micro Dot green).

Shorts: T → r + RSI down arrow + 11<34 (optional Micro Dot red).

TradingView

4H Sell Signals at Swing Highs/LowsThis shows only zones where a 4H FVG and a 4H OB overlap (i.e., true HPZ).

Uses strict filters (FVG size vs avg body, OB body multiplier) to reduce noise and show very few, high-quality zones.

Each HPZ is drawn once (box deleted/created only when the zone changes) to avoid chart spam.

Optional label appears when price is currently inside the HPZ so you can spot active opportunities quickly.

Microgaps (plots-only, 4-channel, same-day only)Purpose:

This indicator visually highlights 3-bar price gaps on your chart, showing clear visual structure for gap zones without lag or diagonal artifacts.

It draws two outer lines (top and bottom of the gap) for every valid 3-bar gap, and optionally a midline when the gap is considered “large.”

⚙️ How it works

A bull gap is detected when the current bar’s low is higher than the high from two bars ago (low > high ).

A bear gap is detected when the current bar’s high is lower than the low from two bars ago (high < low ).

The lines are centered at the middle bar of the 3-bar sequence.

Gaps are only drawn within the same trading day to avoid false overnight gaps.

To prevent overlapping artifacts, up to four concurrent gap channels can be drawn efficiently using GPU-friendly plot() lines.

🔵 Midline logic

The midline (center of the gap) is only displayed when the gap’s vertical size is “large” relative to recent volatility.

“Large” means the gap height is greater than a user-defined fraction of the average bar range over the past N bars.

Example: if the average 8-bar range = 2 points, and the threshold = 0.3, then only gaps larger than 0.6 points will show the midline.

🧩 Parameters

Setting Description

Bull Gap Color / Width Style of bullish gaps (top and bottom lines).

Bear Gap Color / Width Style of bearish gaps (top and bottom lines).

Mid Gap Color / Width Style of the optional midline (shown only when “large”).

Large Gap — Lookback (bars) Number of bars used to calculate the average range (default: 8).

Large Gap — Size vs Avg Range Fraction of the average range that defines a “large” gap (default: 0.5). Set lower (e.g. 0.3) to show more midlines.

💡 Tips

Set threshold lower (0.2–0.4) for more midlines, higher (0.6–1.0) to highlight only extreme gaps.

Works best on intraday timeframes (1-min to 30-min).

Fully GPU-efficient — can scroll back thousands of bars without lag.

Ichimoku Screener [Pineify]Advanced Multi-Timeframe Ichimoku Screener - Complete Market Analysis Tool

This sophisticated Ichimoku Screener represents a comprehensive approach to multi-timeframe market analysis, combining four distinct Ichimoku-based indicators into a unified screening system. Unlike traditional single-symbol indicators, this screener provides simultaneous analysis across multiple assets and timeframes, enabling traders to identify optimal trading opportunities with enhanced precision and efficiency.

Key Features

Multi-asset screening capability for up to 10 symbols simultaneously

Four customizable timeframes per symbol for comprehensive analysis

Four integrated Ichimoku-based indicators working in harmony

Real-time visual feedback with color-coded signals

Customizable Ichimoku parameters for personalized analysis

Clean, organized table display for easy interpretation

Automated signal strength assessment and timing

How It Works

The screener employs the traditional Ichimoku Kinko Hyo methodology, utilizing five core components: Conversion Line (Tenkan-sen), Base Line (Kijun-sen), Leading Span A (Senkou Span A), Leading Span B (Senkou Span B), and displacement calculations. Each component is mathematically calculated using specific period lengths:

Conversion Line = (Highest High + Lowest Low) / 2 over conversion period

Base Line = (Highest High + Lowest Low) / 2 over base period

Leading Span A = (Conversion Line + Base Line) / 2

Leading Span B = (Highest High + Lowest Low) / 2 over lagging span period

The screener processes these calculations across multiple securities simultaneously using TradingView's security() function, enabling real-time cross-asset analysis. The system tracks state changes using barssince() functions to provide precise timing information for each signal type.

Trading Ideas and Insights

This screener excels in identifying momentum convergence patterns where multiple Ichimoku components align across different timeframes. The most powerful signals occur when:

Cloud color aligns with price position relative to the cloud

Conversion Line crosses above/below Base Line in the same direction as cloud bias

Multiple timeframes show consistent directional bias

Entry signals appear with minimal bars since formation (indicating fresh momentum)

For trend following strategies , focus on symbols where the cloud maintains consistent color across higher timeframes while showing recent entry signals on lower timeframes. For reversal opportunities , identify assets where cloud color changes coincide with price re-entering the cloud after extended periods above or below.

The screener particularly excels in cryptocurrency and forex markets where momentum shifts can be dramatic and sustained. By monitoring multiple timeframes simultaneously, traders can identify when short-term signals align with longer-term trends, significantly improving trade success probability.

How Multiple Indicators Work Together

The four integrated indicators create a comprehensive analytical framework through synergistic interaction:

Ichimoku Cloud (IchiCld) establishes the primary trend bias by comparing Leading Span A with Leading Span B. When Span A > Span B, the cloud displays bullish characteristics; when Span A < Span B, bearish characteristics emerge. The indicator tracks duration since the last cloud color change, providing momentum persistence insight.

Ichimoku Lagging Cloud (IchiLagCld) determines price position relative to the displaced cloud formation. This indicator identifies whether current price action occurs above, below, or within the cloud structure, revealing support/resistance dynamics and trend confirmation signals.

Conversion vs Base (IchiC>Base) monitors the relationship between short-term (Conversion Line) and medium-term (Base Line) momentum. Crossovers in this relationship often precede significant price movements and provide early trend change warnings.

Ichimoku Entry (IchiEnt) synthesizes all components into actionable signals by requiring alignment between cloud bias, price position, and conversion/base relationship. This multi-factor confirmation approach significantly reduces false signals while maintaining sensitivity to genuine momentum shifts.

The mathematical foundation ensures that each indicator contributes unique information while maintaining logical consistency. The system's strength lies in requiring multiple confirmations before generating entry signals, following Ichimoku's original philosophy of comprehensive market analysis.

Unique Aspects

This implementation distinguishes itself through several innovative features:

Advanced State Tracking : Unlike standard Ichimoku indicators that show current values, this screener tracks duration since state changes , providing crucial timing information for signal freshness and momentum strength assessment.

Multi-Asset Efficiency : The screener eliminates the need to manually check multiple charts by presenting comparative analysis across assets and timeframes in a single view, dramatically improving analytical efficiency.

Customizable Visual Feedback : The color-coding system adapts to different signal types and strengths, with recent signals receiving enhanced visual prominence to draw attention to fresh opportunities.

Professional Table Architecture : The organized display accommodates up to 40 symbol-timeframe combinations (10 symbols × 4 timeframes), with intelligent pagination for optimal screen utilization.

Signal Correlation Analysis : By displaying multiple timeframes for each symbol, traders can quickly identify timeframe confluence and divergence patterns that would otherwise require extensive manual analysis.

How to Use

Symbol Configuration : Enter up to 10 symbols in the Symbol input group. Use full exchange:ticker format for optimal compatibility (e.g., "BINANCE:BTCUSDT").

Timeframe Selection : Configure four timeframes in ascending order for logical analysis progression. Recommended combinations include 1m/5m/15m/1h for intraday analysis or 1h/4h/1D/1W for swing trading.

Ichimoku Parameters : Adjust the four core parameters based on your trading style:

Conversion Line Length (default: 9) - Controls short-term momentum sensitivity

Base Line Length (default: 26) - Determines medium-term trend identification

Leading Span B Length (default: 52) - Sets long-term trend calculation period

Displacement (default: 26) - Controls forward projection of cloud structure

Signal Interpretation :

Green backgrounds indicate bullish conditions

Red backgrounds indicate bearish conditions

Numerical values show bars since last state change

"L:" prefix indicates long entry signals

"S:" prefix indicates short entry signals

"N/A" indicates neutral/transitional states

Trading Workflow : Scan for symbols showing consistent signals across multiple timeframes, prioritize fresh signals (low bar counts), and use individual charts for precise entry timing and risk management.

Customization

The screener accommodates various trading approaches through parameter adjustment:

Scalping Configuration : Use shorter periods (Conversion: 5, Base: 13, Span B: 26) with 1m/3m/5m/15m timeframes for high-frequency opportunities.

Swing Trading Setup : Employ standard parameters with 4h/1D/3D/1W timeframes for position trading across days or weeks.

Cryptocurrency Optimization : Given crypto's 24/7 nature, consider using 4h/8h/1D/3D combinations for optimal signal timing.

Symbol selection can focus on correlated assets (e.g., major cryptocurrencies) for sector analysis or diverse assets for portfolio opportunity identification. The flexible timeframe configuration allows adaptation to any market's characteristic volatility and trading patterns.

Conclusion

This Advanced Multi-Timeframe Ichimoku Screener transforms traditional single-chart analysis into a comprehensive market monitoring system. By integrating multiple Ichimoku components across various timeframes and assets, it provides traders with unprecedented analytical efficiency and signal reliability.

The mathematical rigor of traditional Ichimoku analysis combines with modern Pine Script capabilities to deliver a professional-grade screening tool. Whether used for identifying trend continuation opportunities, spotting potential reversals, or conducting broad market analysis, this screener offers the analytical depth and practical functionality required for serious trading applications.

The system's emphasis on signal confluence across multiple timeframes and indicators significantly improves trade selection quality while reducing analysis time. For traders seeking to leverage Ichimoku's proven methodology across multiple markets simultaneously, this screener represents an essential analytical upgrade to traditional single-symbol approaches.

Multi-Timeframe MA - TCMasterThis indicator displays up to four moving averages from different timeframes on a single chart.

It’s designed for traders who want to track higher-timeframe trends while analyzing price action on lower timeframes — a key technique in multi-timeframe confluence trading.

You can freely customize the type, length, timeframe, and color for each moving average line.

⚙️ Features

4 configurable Moving Averages (each with its own type, length, and timeframe).

Supported types:

SMA, EMA, WMA, RMA, HMA, VWMA, DEMA, TEMA.

Real-time values are fetched from higher timeframes using request.security() (no repaint).

Individual visibility toggle and line width for each MA.

Dynamic info label shows current distance between price and each MA.

Built with Pine Script v6, ensuring optimal performance and flexibility.

📊 Typical Use Cases

Identify trend direction across multiple timeframes.

Confirm entries/exits using higher timeframe trend alignment.

Spot potential reversal or continuation zones when short-term price interacts with long-term MAs.

Build confluence setups for swing, scalp, or intraday strategies.

🧠 Example Setup

MA Type Length Timeframe Purpose

MA #1 SMA 200 1m Micro trend

MA #2 EMA 200 5m Short-term trend

MA #3 EMA 200 15m Medium trend

MA #4 SMA 200 30m Macro trend

🔔 Tips

Combine with oscillators (e.g., RSI, Stoch, MACD) for stronger confluence.

Use color coding to distinguish short vs long timeframe trends.

Consider adding alerts when price crosses any MA (can be extended easily in code).

⚠️ Notes

All higher-timeframe data is handled safely using lookahead=barmerge.lookahead_off to prevent repainting.

Label updates only on the latest bar for efficiency.

VWMA, DEMA, TEMA, and HMA are computed via internal formulas for compatibility with Pine Script v6.

🏁 Summary

Multi-Timeframe MA is a powerful tool for traders who want to merge the clarity of moving averages with the precision of multi-timeframe analysis.

It helps you see the bigger picture without switching charts — perfect for intraday, swing, and trend-following strategies.

Multi-Timeframe MA - TCMaster🧩 Overview

This indicator displays up to four moving averages from different timeframes on a single chart.

It’s designed for traders who want to track higher-timeframe trends while analyzing price action on lower timeframes — a key technique in multi-timeframe confluence trading.

You can freely customize the type, length, timeframe, and color for each moving average line.

⚙️ Features

4 configurable Moving Averages (each with its own type, length, and timeframe).

Supported types:

SMA, EMA, WMA, RMA, HMA, VWMA, DEMA, TEMA.

Real-time values are fetched from higher timeframes using request.security() (no repaint).

Individual visibility toggle and line width for each MA.

Dynamic info label shows current distance between price and each MA.

Built with Pine Script v6, ensuring optimal performance and flexibility.

📊 Typical Use Cases

Identify trend direction across multiple timeframes.

Confirm entries/exits using higher timeframe trend alignment.

Spot potential reversal or continuation zones when short-term price interacts with long-term MAs.

Build confluence setups for swing, scalp, or intraday strategies.

🧠 Example Setup

MA Type Length Timeframe Purpose

MA #1 SMA 200 1m Micro trend

MA #2 EMA 200 5m Short-term trend

MA #3 EMA 200 15m Medium trend

MA #4 SMA 200 30m Macro trend

🔔 Tips

Combine with oscillators (e.g., RSI, Stoch, MACD) for stronger confluence.

Use color coding to distinguish short vs long timeframe trends.

Consider adding alerts when price crosses any MA (can be extended easily in code).

⚠️ Notes

All higher-timeframe data is handled safely using lookahead=barmerge.lookahead_off to prevent repainting.

Label updates only on the latest bar for efficiency.

VWMA, DEMA, TEMA, and HMA are computed via internal formulas for compatibility with Pine Script v6.

🏁 Summary

Multi-Timeframe MA is a powerful tool for traders who want to merge the clarity of moving averages with the precision of multi-timeframe analysis.

It helps you see the bigger picture without switching charts — perfect for intraday, swing, and trend-following strategies.

Palat Trading System Entry Prices (Bear)This script gives you the entry points for 4,5,6,7 consecutive candles which got up closing vs last trading day.

Palat Trading System Entry Prices (Bull)This script gives you the entry points for 4,5,6,7 consequetive candles which got down closing vs last trading day.

DTM 444 BANDS 🚀DTM 444 BANDS 🚀:

The DTM 444 BANDS 🚀 is a powerful, multi-purpose trading indicator combining Supertrend, Dynamic Band Levels, Breakout Signals, and Volume Confirmation to help traders identify high-probability trade setups across different timeframes.

🔧 Key Features

✅ Multi-Timeframe Support

Analyze price action across any timeframe using the Timeframe input.

All band calculations (High, Low, Midline, and Supertrend) are pulled from a higher timeframe for clearer context.

✅ Dynamic Bands Based on Supertrend

High Band: Rolling highest of Supertrend over hiLen period.

Low Band: Rolling lowest of Supertrend over loLen period.

Midline: Midpoint of the above.

Acts like dynamic support/resistance, ideal for trend-following and breakout strategies.

✅ Dual Signal System

Breakout Signals (Buy and Sell): Triggered when price breaks the bands with volume confirmation.

Supertrend Crossover Signals (Buy1 and Sell1): Classic momentum entries with a confirmation twist.

Exit Signals: Optional take-profit/neutral indicators when price reverses.

✅ Volume Confirmation Filter (Optional)

Only triggers signals if the volume exceeds its 20-period SMA.

Helps filter out false breakouts and weak trends in low-liquidity periods.

✅ Visual Enhancements

Color-coded candles based on band positioning (e.g., red = weak, green = strong, etc.)

On-chart labels for each signal for quick reference.

Real-time Signal Dashboard using Pine Script tables showing:

Current signal

Volume filter status

Live volume vs volume SMA

🧪 Practical Use Cases

Trend Traders: Use the Supertrend cross and band breakouts to ride trends early.

Breakout Traders: Catch high-probability moves outside established ranges.

Swing Traders: Time entries and exits using color-coded bars and exit labels.

Volume-Sensitive Traders: Focus on trades with strong volume backing.

📊 Backtest Snapshot

Based on the example chart for Reliance Industries (RELIANCE.NS) on the weekly timeframe:

Several profitable buy and breakout signals during uptrends.

Timely exits and breakdown alerts before reversals.

Volume filter keeps trades clean and avoids noise.

⚙️ Customizable Parameters

High Length and Low Length (default: 19)

Supertrend Multiplier and ATR Length

Volume Filter: Toggle ON/OFF

Volume SMA Length: Default 20

Custom Timeframe: Choose any higher timeframe for multi-timeframe analysis

📢 Alerts Ready

Fully integrated with TradingView alerts:

Breakout & Breakdown

Supertrend crossovers

All alerts respect the volume filter setting

🏁 Final Thoughts

DTM 444 BANDS 🚀 is a versatile and adaptive trading system that blends trend analysis, volatility bands, and volume validation. Whether you're a trend trader, breakout hunter, or swing trader — this tool gives you a structured edge with clear visual cues and real-time alerts.

FEI: Futures Entry Identifier📘 FEI: Futures Entry Identifier