I11L - Meanreverter 4h---Overview---

The system buys fear and sells greed.

Its relies on a Relative Strength Index (RSI) and moving averages (MA) to find oversold and overbought states.

It seems to work best in market conditions where the Bond market has a negative Beta to Stocks.

Backtests in a longer Timeframe will clearly show this.

---Parameter---

Frequency: Smothens the RSI curve, helps to "remember" recent highs better.

RsiFrequency: A Frequency of 40 implies a RSI over the last 40 Bars.

BuyZoneDistance: Spacing between the different zones. A wider spacing reduces the amount of signals and icnreases the holding duration. Should be finetuned with tradingcosts in mind.

AvgDownATRSum: The multiple of the Average ATR over 20 Bars * amount of opentrades for your average down. I choose the ATR over a fixed percent loss to find more signals in low volatility environments and less in high volatility environments.

---Some of my thoughts---

Be very careful about the good backtesting performance in many US-Stocks because the System had a favourable environment since 1970.

Be careful about the survivorship bias as well.

52% of stocks from the S&P500 were removed since 2000.

I discount my Annual Results by 5% because of this fact.

You will find yourself quite often with very few signals because of the high market correlation.

My testing suggests that there is no expected total performance difference between a signal from a bad and a signal from a good market condition but a higher volatility.

I am sharing this strategy because i am currently not able to implement it as i want to and i think that meanreversion is starting to be taken more serious by traders.

The challange in implementing this strategy is that you need to be invested 100% of the time to retrieve the expected annual performance and to reduce the fat tail risk by market crashes.

Cari dalam skrip untuk "信达股份40周年"

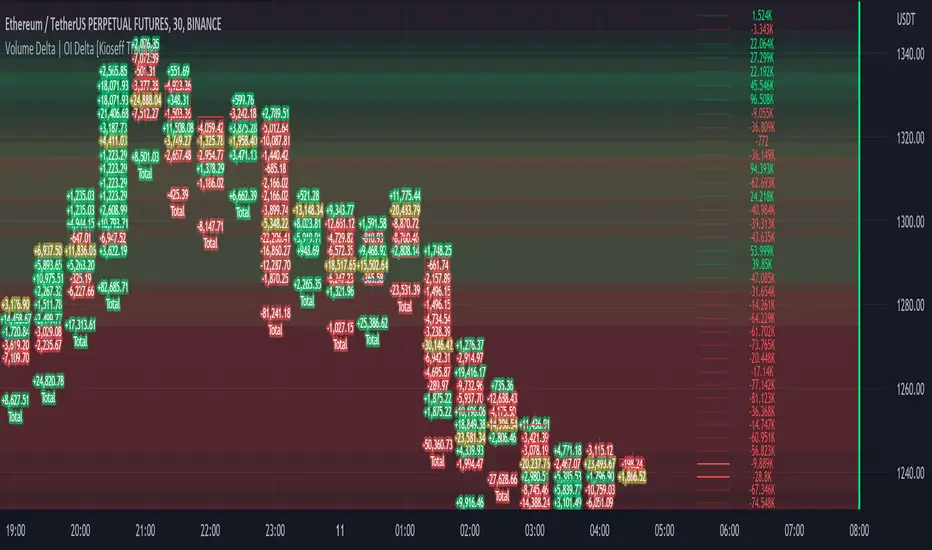

Volume Profile Volume Delta OI Delta [Kioseff Trading]Hello!

This script serves to distinguish volume delta for any asset and open interest delta for Binance perpetual futures.

The image above provides further explanation of functionality and color correspondence.

The image above shows the indicator calculating volume at each tick level and displaying the metric.

The label color outline (neon effect) is configurable; the image above is absent the feature.

The image above shows Open Interest (OI) Delta calculated - similar to how the script calculates volume delta - for a Binance Perpetual Future pair.

This feature only works for Binance Futures pairs; the script will not load when trying to calculate OI Delta on other assets.

Additionally, a heatmap is displayable should you configure the indicator to calculate it.

The image above shows a heatmap using volume delta calculations.

The image above shows a heatmap using OI delta calculations.

Of course, these calculations - when absent requisite data - require some assumptions to better replicate calculations with access to requisite data.

The indicator assumes a 60/40 split when a tick level is traded at and only one metric - "buy volume" or "sell volume" is recorded. This means there shouldn't be any levels recorded where "buy volume" is greater than 0 and "sell volume" equals 0 and vice versa. While this assumption was performed arbitrarily, it may help better replicate volume delta and OI delta calculations seen on other charting platforms.

This option is configurable; you can select to have the script not assume a 60/40 split and instead record volume "as is" at the corresponding tick level.

The script also divides volume and open interest if a one-minute bar violates multiple tick levels. The volume or open interest generated on the one-minute bar will be divided by the number of tick levels it exceeds. The results are, subsequently, appended to the violated tick levels.

Further, the script can be set to recalculate after a user-defined time threshold is exceeded. You can also define the percentage or tick distance between levels.

Also, it'd be great if this indicator can nicely replicate volume delta indicators on other charting platforms. If you've any ideas on how price action can be used to better assume volume at the corresponding price area please let me know!

Thank you (:

ICT IPDA Look BackThis script automatically calculates and updates ICT's daily IPDA look back time intervals and their respective discount / equilibrium / premium, so you don't have to :)

IPDA stands for Interbank Price Delivery Algorithm. Said algorithm appears to be referencing the past 20, 40, and 60 days intervals as points of reference to define ranges and related PD arrays.

Intraday traders can find most value in the 20 Day Look Back box, by observing imbalances and points of interest.

Longer term traders can reference the 40 and 60 Day Look Back boxes for a clear indication of current market conditions.

FATL, SATL, RFTL, & RSTL Digital Filters Raw [Loxx]FATL, SATL, RFTL, & RSTL Digital Filters Raw is an indicator to showcase FATL, SATL, RFTL, & RSTL Digital Filters with their raw output values. The coefficients used here are for an idealized environment. This is tuned for Forex.

What is FATL?

FATL (Fast Adaptive Trend Line) is calculated using low frequency digital filter (FLF-1).

FLF-1 filter is necessary for high frequency noises suppression and reduction of market cycles with a very short volatility periods that can also be considered as a noise.

Filters of low frequency FLF-1 and FLF-2 provide attenuation in the stop band with no less than 40 dB and absolutely don’t distort the amplitude and phase of entry discontinuous price series in the pass band (bandwidth). These properties of the digital filters provide significantly improved (in comparison with simple moving average) noise suppression that in its turn allows reducing sharply the probability of appearance "false" signals for buy and sell.

There are no analogues to FATL among widely known technical instruments. It is not a moving "average", but just the adaptive lines estimates of the short-term trends. Unlike moving "average", FATL has no any phase delay with regard to current prices.

What is SATL?

Slow Adaptive Trend Line (SATL) is formed with the digital filter of the low frequency FLF-2.

Filter FLF-2 serves to suppress noises and market cycles with longer periods of oscillation. Filters of low frequency FLF-1 and FLF-2 provide attenuation in the stop band with no less than 40 dB and absolutely don’t distort the amplitude and phase of entry discontinuous price series in the pass band (bandwidth).

These properties of the digital filters provide significantly improved (in comparison with simple moving average) noise suppression that in its turn allows reducing sharply the probability of appearance of "false" signals for purchase and sell.

There are no analogues to SATL among widely known technical instruments. This is not a moving "average", but just the adaptive line estimate of a long-term trend.

Unlike moving average, SATL has no any phase delay with regard to current prices.

What is RFTL?

Reference Fast Trend Line (RFTL) is a response of FLF-1 and FLF-2 digital filters to the input discrete sequence. This response is set with the delay equal to the Nyquist TNi range.

RFTL reference line is an equivalent of simple moving "averages" from the viewpoint of their delay relative to the current prices. Mentioned similarity would have been complete, in case we use an impulse parameter having 1/N weights that corresponds to the procedure of the dotted moving smoothing instead of the complicated FLF impulse parameters.

What is RSTL?

Reference Slow Trend Line (RSTL) is a response of the SATL digital filter to the series of input prices with a delay equal to the Nyquist interval of 1/2F.

FATL, SATL, RFTL, & RSTL Digital Signal Filter Smoother [Loxx]FATL, SATL, RFTL, & RSTL Digital Signal Filter (DSP) Smoother is is a baseline indicator with DSP processed source inputs

What are digital indicators: distinctions from standard tools, types of filters.

To date, dozens of technical analysis indicators have been developed: trend instruments, oscillators, etc. Most of them use the method of averaging historical data, which is considered crude. But there is another group of tools - digital indicators developed on the basis of mathematical methods of spectral analysis. Their formula allows the trader to filter price noise accurately and exclude occasional surges, making the forecast more effective in comparison with conventional indicators. In this review, you will learn about their distinctions, advantages, types of digital indicators and examples of strategies based on them.

Two non-standard strategies based on digital indicators

Basic technical analysis indicators built into most platforms are based on mathematical formulas. These formulas are a reflection of market behavior in past periods. In other words, these indicators are built based on patterns that were discovered as a result of statistical analysis, which allows one to predict further trend movement to some extent. But there is also a group of indicators called digital indicators. They are developed using mathematical analysis and are an algorithmic spectral system called ATCF (Adaptive Trend & Cycles Following). In this article, I will tell you more about the components of this system, describe the differences between digital and regular indicators, and give examples of 2 strategies with indicator templates.

ATCF - Market Spectrum Analysis Method

There is a theory according to which the market is chaotic and unpredictable, i.e. it cannot be accurately analyzed. After all, no one can tell how traders will react to certain news, or whether some large investor will want to play against the market like George Soros did with the Bank of England. But there is another theory: many general market trends are logical, and have a rationale, causes and effects. The economy is undulating, which means it can be described by mathematical methods.

Digital indicators are defined as a group of algorithms for assessing the market situation, which are based exclusively on mathematical methods. They differ from standard indicators by the form of analysis display. They display certain values: price, smoothed price, volumes. Many standard indicators are built on the basis of filtering the minute significant price fluctuations with the help of moving averages and their variations. But we can hardly call the MA a good filter, because digital indicators that use spectral filters make it possible to do a more accurate calculation.

Simply put, digital indicators are technical analysis tools in which spectral filters are used to filter out price noise instead of moving averages.

The display of traditional indicators is lines, areas, and channels. Digital indicators can be displayed both in the form of lines and in digital form (a set of numbers in columns, any data in a text field, etc.). The digital display of the data is more like an additional source of statistics; for trading, a standard visual linear chart view is used.

All digital models belong to the category of spectral analysis of the market situation. In conventional technical indicators, price indications are averaged over a fixed period of time, which gives a rather rough result. The use of spectral analysis allows us to increase trading efficiency due to the fact that digital indicators use a statistical data set of past periods, which is converted into a “frequency” of the market (period of fluctuations).

Fourier theory provides the following spectral ranging of the trend duration:

low frequency range (0-4) - a reflection of a long trend of 2 months or more

medium frequency range (5-40) - the trend lasts 10-60 days, thus it is referred to as a correction

high frequency range (41-130) - price noise that lasts for several days

The ATCF algorithm is built on the basis of spectral analysis and includes a set of indicators created using digital filters. Its consists of indicators and filters:

FATL: Built on the basis of a low-frequency digital trend filter

SATL: Built on the basis of a low-frequency digital trend filter of a different order

RFTL: High frequency trend line

RSTL: Low frequency trend line

Inclucded:

4 DSP filters

Bar coloring

Keltner channels with variety ranges and smoothing functions

Bollinger bands

40 Smoothing filters

33 souce types

Variable channels

RSI Trend Heatmap in Multi TimeframesRSI Trend Heatmap in Multi Timeframes

Description

Sometimes you want to look at the RSI Trend across multiple time frames.

You have to waste time browsing through them.

So we've put together every time frame you want to see in one indicator.

We have 10 layers of RSI Trend heatmap available for you.

You can set the timeframe as you want on the Settings page.

Description of Parameter RSI Setting ** You can change it by setting.

RSI Trend Length : (Default 50)

Source : (Default close)

RSI Sideways Length : (Default 2 = RSI between 48 .. 52)

Description of Parameter RSI Timeframe ** You can change it by setting.

""=None,

"M"=1Month, "2W"=2Weeks, "W"=1Week,

"3D"=3Days, "2D"=2Days, "D"=1Day,

"720"=12Hours, "480"=4Hours, "240"=4Hours, "180"=3Hours, "120"=2Hours,

"60"=60Minutes, "30"=30Minutes, "15"=15Minutes, "5"=5Minutes, "1"=1Minute

Default Configurate of RSI Timeframe (for a time frame of 1 hour to 1 day)

"W"= Timeframe 1 month shown in line 90-100 --> Represent Long Trend of RSI

---------------------------------------

"D2"= Timeframe 2 days shown in line 70-80 --> Represent Trend of RSI

"D"= Timeframe 1 day shown in line 60-70 --> Represent Trend of RSI

---------------------------------------

"240"= Timeframe 3 hours shown in line 40-50 --> Represent Signal Up/Signal Down/Divergence of RSI

"120"= Timeframe 2 hours shown in line 30-40 --> Represent Signal Up/Signal Down/Divergence of RSI

"60"= Timeframe 1 hour shown in line 20-30 --> Represent Signal Up/Signal Down/Divergence of RSI

"30"= Timeframe 30 minutes shown in line 10-20 --> Represent Signal Up/Signal Down/Divergence of RSI

"15"= Timeframe 15 minutes shown in line 00-10 --> Represent Signal Up/Signal Down/Divergence of RSI

Description of Colors

Dark Bule = Extreme Uptrend / Overbought / Bull Market (RSI > 67)

Light Bule = Uptrend (RSI between 50-52 .. 67)

Yellow = Sideways Trend / Trend Reversal (RSI between 48 .. 52) ** You can change it by setting.

Light Red = Downtrend (RSI between 33 .. 48-50)

Dark Red = Extreme Downtrend / Oversold / Bear Market (RSI < 33)

How to use

1. You must first know what the main trend of the RSI is (look at the 60-80 line). If it is red, it is a downtrend. and if it's blue shows that it is an uptrend

2. Throughout the period of the main trend There will always be a reversal of the sub-trend. (Can see from the 0-50 line), but eventually will return to follow the main trend.

3. Unless the sub trend persists for a long time until the main trend changes.

Nifty & BN 2 Candle Theory Back Testing and Alert Notification How To Initiate Long Trade-in Index Future/ Buy Call Options – 3 Min TF

▪ If The Index Futures Trades Above The VWAP, the Following Parameters are Checked For 2 Candle Theory on the long side

▪ RSI Trades Above 50 & Between 50-75/80

▪ Volume Of 2 Consecutive Bars Is Above 50 K for BN & 125 K For Nifty

▪ All the indicators (Parabolic SAR, Super Trend, VMA, VWAP) Below the Candles

▪ When the above conditions are met enter In 3rd Candle, With 1st Candle High As SL

How I Initiate Short Trade-In Index Future/ Buy Put Options – 3 Min TF

▪ If The Index Futures Trades Below The VWAP, the Following Parameters are Checked For 2 Candle Theory on the short side

▪ RSI Trades Below 40 & Between 40-25/20

▪ Volume Of 2 Consecutive Bars Is Above 50 K for BN & 125 K For Nifty

▪ All the Indicators (Parabolic SAR, Super Trend, VMA, VWAP) Above The Candles

▪ When the above conditions are met enter In 3rd Candle, With 1st Candle High As SL

The indicator checks the above and notifies to enter a long trade and short trade respectively. There is also volume cutoff and change in the volumes respectively, also non-trading times that can be set.

RSI Swing Trading Setup (2-Period)A simple script that adjusts the RSI visibly in order to better accommodate swing trading and certain swing trading setups/strategies.

--------------------------------------------------------------------------------------------------------------------------------------------------------

Best used in conjunction with "Linear Regression Channel by LonesomeTheBlue" with 2.2σ (std.dev) and Show Fib Levels.

^Click image for a redirect to that script.

--------------------------------------------------------------------------------------------------------------------------------------------------------

In certain price action patterns:

A bearish reversal from a previously bullish move can indicate tops of a rally if the RSI moves from 0-40 to 60 (1)

A bullish reversal from a previously bearish move can indicate bottoms of a pullback if the RSI moves from 60-100 to 40 (2)

(USE THE LINEAR REGRESSION CHANNEL TO VALIDIFY THE RETRACEMENTS)

--------------------------------------------------------------------------------------------------------------------------------------------------------

(1)

--------------------------------------------------------------------------------------------------------------------------------------------------------

(2)

--------------------------------------------------------------------------------------------------------------------------------------------------------

ALMA cross signal by hk4jerry<< ALMA CROSS signal >>

*NONE REPAINT STRATEGY*

--As a result of testing for a month, using alma does not result in repainting--

--ALMA 크로스 결과는 한달간의 테스트 결과, 리페인팅되지 않습니다--

(ENGLISH description O)

==NOTE==

1. MA 크로스 지표는 잘못된 신호들이 자주 등장합니다. 정확성을 더 높일수 있는 방법은 없을까 고민을 해봤습니다. 더 낮은 가격에 매수하고, 더 높은 가격에서 매도하는 것이 중요했습니다. 우리가 흔히 저점, 고점을 알아내기 위한 지표이자, 선행지표인 RSI를 추가하는 방법을 연구했습니다.

2. 예를 들어, MA 크로스 매수 신호가 발생했을때, rsi값이 50이면 가격이 더 떨어질 가능성이 큽니다. 하지만, rsi값이 30이하인 경우에만 매수 신호가 발생한다면, 그 가격이 저점일 확률이 매우 높아지는 원리 입니다.

3. 신호는 확률입니다. 트레이딩에 100%는 없습니다. 그 확률을 높이는 것은 리스크 관리 입니다. 분할 매수 관점으로 포지션을 잡으시거나, 단기 매매로 가져가시는걸 추천드립니다.

==rsi ma source 설정==

1. 'rsi ma' 값의 소스입니다.

2. 'rsi 길이' 는 값이 클수록 더욱 정확한 시그널이 발생합니다.

3. EMA 길이가 짧을수록 더 많은 시그널이 발생합니다. 그러나, 정확도는 떨어집니다.

==rsi ma 설정==

1. rsi를 source로한 EMA입니다.

2. rsi와 유사한 성격을 가집니다.

3. 'rsi ma' 값이 30이하이면 과매도, 70이상이면 과매수 입니다.

4. ' rsi ma long value' 이 30이면 매수 신호가 rsi ma 값이 30 이하인 경우에만 발생함을 의미 합니다.

5. "rsi ma short value' 가 70이면 매도 신호가 rsi ma 값이 70 이상인 경우에만 발생함을 의미 합니다.

==rsi 설정==

1. 실제 rsi(14,close) 값을 의미합니다.

2. rsi ma value와 비슷한 기능입니다.

3. rsi 길이가 14이므로, 값은 40~50 사이가 적당합니다.

4. 30 또는 70으로 설정할 시, 신호가 거의 발생하지 않습니다.

(ENG)

==NOTE==

1. MA cross indicator often shows false signals. I was wondering if there is a way to increase the accuracy further. It was important to buy at a lower price and sell at a higher price. We studied how to add RSI, which is a leading indicator and an indicator to find lows and highs, often.

2. For example, when a buy MA cross signal occurs, if the rsi value is 50, the price is more likely to fall. However, if a buy signal occurs only when the rsi value is below 30, the probability that the price is at the bottom is very high.

3. A signal is a probability. There is no 100% in trading. Increasing that probability is risk management. It is recommended to hold a position from the perspective of a split buy or take it as a short-term trade.

==rsi ma source option==

1. The source of the 'rsi ma' value.

2. The larger the 'rsi length' value, the more accurate the signal is generated.

3. Shorter EMA lengths produce more signals. However, the accuracy is reduced.

==rsi ma options==

1. EMA with rsi as the source.

2. It has similar characteristics to rsi.

3. If the 'rsi ma' value is below 30, it is oversold, and if it is above 70, it is overbought.

4. If 'rsi ma long value' is 30, it means that a buy signal will only occur when the rsi ma value is less than or equal to 30.

5. If "rsi ma short value' is 70, it means that a sell signal will only occur when the rsi ma value is above 70.

==rsi option==

1. It means the actual rsi(14,close) value.

2. This function is similar to rsi ma value.

3. Since the rsi length is 14, a value between 40 and 50 is appropriate.

4. When set to 30 or 70, almost no signal is generated.

Library CommonLibrary "LibraryCommon"

A collection of custom tools & utility functions commonly used with my scripts

@description TODO: add library description here

getDecimals() Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

truncate(float, float) Truncates (cuts) excess decimal places

Parameters:

float : number The number to truncate

float : decimalPlaces (default=2) The number of decimal places to truncate to

Returns: The given number truncated to the given decimalPlaces

toWhole(float) Converts pips into whole numbers

Parameters:

float : number The pip number to convert into a whole number

Returns: The converted number

toPips(float) Converts whole numbers back into pips

Parameters:

float : number The whole number to convert into pips

Returns: The converted number

getPctChange(float, float, int) Gets the percentage change between 2 float values over a given lookback period

Parameters:

float : value1 The first value to reference

float : value2 The second value to reference

int : lookback The lookback period to analyze

av_getPositionSize(float, float, float, float) Calculates OANDA forex position size for AutoView based on the given parameters

Parameters:

float : balance The account balance to use

float : risk The risk percentage amount (as a whole number - eg. 1 = 1% risk)

float : stopPoints The stop loss distance in POINTS (not pips)

float : conversionRate The conversion rate of our account balance currency

Returns: The calculated position size (in units - only compatible with OANDA)

bullFib(priceLow, priceHigh, fibRatio) Calculates a bullish fibonacci value

Parameters:

priceLow : The lowest price point

priceHigh : The highest price point

fibRatio : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio) Calculates a bearish fibonacci value

Parameters:

priceLow : The lowest price point

priceHigh : The highest price point

fibRatio : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

getMA(int, string) Gets a Moving Average based on type (MUST BE CALLED ON EVERY CALCULATION)

Parameters:

int : length The MA period

string : maType The type of MA

Returns: A moving average with the given parameters

getEAP(float) Performs EAP stop loss size calculation (eg. ATR >= 20.0 and ATR < 30, returns 20)

Parameters:

float : atr The given ATR to base the EAP SL calculation on

Returns: The EAP SL converted ATR size

getEAP2(float) Performs secondary EAP stop loss size calculation (eg. ATR < 40, add 5 pips, ATR between 40-50, add 10 pips etc)

Parameters:

float : atr The given ATR to base the EAP SL calculation on

Returns: The EAP SL converted ATR size

barsAboveMA(int, float) Counts how many candles are above the MA

Parameters:

int : lookback The lookback period to look back over

float : ma The moving average to check

Returns: The bar count of how many recent bars are above the MA

barsBelowMA(int, float) Counts how many candles are below the MA

Parameters:

int : lookback The lookback period to look back over

float : ma The moving average to reference

Returns: The bar count of how many recent bars are below the EMA

barsCrossedMA(int, float) Counts how many times the EMA was crossed recently

Parameters:

int : lookback The lookback period to look back over

float : ma The moving average to reference

Returns: The bar count of how many times price recently crossed the EMA

getPullbackBarCount(int, int) Counts how many green & red bars have printed recently (ie. pullback count)

Parameters:

int : lookback The lookback period to look back over

int : direction The color of the bar to count (1 = Green, -1 = Red)

Returns: The bar count of how many candles have retraced over the given lookback & direction

getBodySize() Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize() Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize() Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent() Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

isHammer(float, bool) Checks if the current bar is a hammer candle based on the given parameters

Parameters:

float : fib (default=0.382) The fib to base candle body on

bool : colorMatch (default=false) Does the candle need to be green? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a hammer candle

isStar(float, bool) Checks if the current bar is a shooting star candle based on the given parameters

Parameters:

float : fib (default=0.382) The fib to base candle body on

bool : colorMatch (default=false) Does the candle need to be red? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a shooting star candle

isDoji(float, bool) Checks if the current bar is a doji candle based on the given parameters

Parameters:

float : wickSize (default=2) The maximum top wick size compared to the bottom (and vice versa)

bool : bodySize (default=0.05) The maximum body size as a percentage compared to the entire candle size

Returns: A boolean - true if the current bar matches the requirements of a doji candle

isBullishEC(float, float, bool) Checks if the current bar is a bullish engulfing candle

Parameters:

float : allowance (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

float : rejectionWickSize (default=disabled) The maximum rejection wick size compared to the body as a percentage

bool : engulfWick (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bullish engulfing candle

isBearishEC(float, float, bool) Checks if the current bar is a bearish engulfing candle

Parameters:

float : allowance (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

float : rejectionWickSize (default=disabled) The maximum rejection wick size compared to the body as a percentage

bool : engulfWick (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bearish engulfing candle

isInsideBar() Detects inside bars

Returns: Returns true if the current bar is an inside bar

isOutsideBar() Detects outside bars

Returns: Returns true if the current bar is an outside bar

barInSession(string, bool) Determines if the current price bar falls inside the specified session

Parameters:

string : sess The session to check

bool : useFilter (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls within the given time session

barOutSession(string, bool) Determines if the current price bar falls outside the specified session

Parameters:

string : sess The session to check

bool : useFilter (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls outside the given time session

dateFilter(int, int) Determines if this bar's time falls within date filter range

Parameters:

int : startTime The UNIX date timestamp to begin searching from

int : endTime the UNIX date timestamp to stop searching from

Returns: A boolean - true if the current bar falls within the given dates

dayFilter(bool, bool, bool, bool, bool, bool, bool) Checks if the current bar's day is in the list of given days to analyze

Parameters:

bool : monday Should the script analyze this day? (true/false)

bool : tuesday Should the script analyze this day? (true/false)

bool : wednesday Should the script analyze this day? (true/false)

bool : thursday Should the script analyze this day? (true/false)

bool : friday Should the script analyze this day? (true/false)

bool : saturday Should the script analyze this day? (true/false)

bool : sunday Should the script analyze this day? (true/false)

Returns: A boolean - true if the current bar's day is one of the given days

atrFilter()

fillCell()

Constance Brown RSI*Re-uploading without House Violations*

Welles Wilder created the RSI momentum oscillator in the 1970s. It is a momentum oscillator that ranges from 0 to 100. The traditional idea is to buy when the oscillator is below 30 and to sell when it is above 70. However, this strategy often only catches extreme moves and misses majority of the trend.

In comes Constance Brown RSI . She theorized that in an uptrend, the buy zone exists when RSI is between 40 and 50. The sell zone in an uptrend exists between 80 and 90. In a downtrend, the sell zone exists between 55 and 65. The buy zone in a downtrend exists between 20 and 30.

I have added a moving average feature to determine trend. When the short trend is above the long trend, it is considered an uptrend. It is in a downtrend otherwise. Using short length moving averages will often produce a lot of false signals. I recommend using the 50 and 100 as they will produce less noise.

There will be times when the oscillator breaks beyond the ranges described (for ex: seeing a reading below 40 in an uptrend). This tends to happen in periods of high volatility . Refer to the traditional RSI rules in such cases.

ADX DI EMA Clouds

EMA clouds colored by DI and ADX indicator:

9 EMA and 21 EMA Cloud turns green in a bull trend and red when in a bull trend...if the trend is half bulll and half bear..the clouds turn white.

I also coded if the momentum in increasing (yellow) or if the momentum is decreasing (blue) or if the momentum is flat (white).

The Clouds are colored based off the Di (+/-)

9 EMA is colored based of ADX momentum strength

ADX:

ADX is used to quantify trend strength. ADX calculations are based on a moving average of price range expansion over a given period of time. The default setting is 14 bars, although other time periods can be used.1

ADX can be used on any trading vehicle such as stocks, mutual funds, exchange-traded funds and futures .

DI (+/-):

The directional movement index (DMI) is an indicator developed by J. Welles Wilder in 1978 that identifies in which direction the price of an asset is moving. The indicator does this by comparing prior highs and lows and drawing two lines: a positive directional movement line ( +DI ) and a negative directional movement line ( -DI ). An optional third line, called the average directional index ( ADX ), can also be used to gauge the strength of the uptrend or downtrend.

This indicator has the length changed from 14 to 9 so you can have more updated price calculation

I also add the 4 levels I use for day trading; the 10, 20, 30, 40-50 are the levels I like to see the Di to break over.

A lot of traders use different levels, but these I have and found most useful. You can set alerts when any Di crosses over the 40 for true trend breakout!

MA total distance on chartNOTE:

The name I used for this indicator was created by me and I’m not sure if it has been used or created by any other trader/creator in the past or not!

Motivation to create:

One of the most important uses of “moving averages” is indicating the trend! There are different ways you can distinguish trend by using moving averages and one of the most popular type of it is comparing closing price to a MA. In this case if close is higher than the MA, trend is bullish and if close is lower than MA, it’s bearish. This method is really useful and I see great results in my long-term back-tests, especially SMA-100 in 1H chart filter so many fake signals in many different indicator-based strategies (Personal experience). There are so many problems with using indicators that sometimes have difficult solutions but one of them is fake breakout!

Looking at the top picture, you’ll get a breakout has happened but trend did not change!

A super bearish trend is obviously visible in the chart and we know a small break out might be a fake one, but what if we have an indicator make conditions of a trend change a little harder?

Introduction:

I was careful about how I used moving averages and I got that I will take not only the last candle close price into consideration, so in these kind of false breakouts I will not fall into trap of them, On the contrary, I find a good opportunity to enter the market opposite of the MA break! (In this case short trade). I calculate the total distance of last 40 candles and divide them to 40, to get the average distance, to each a mathematical score for power of our trend comparing to the MA!

Number are just default you can change them.

In the picture below you can see how well it filtered the false breakout.

As it is obvious, Timeframe, MA length, MA source and MA type are editable.

Since I do not tested this indicator enough (for me enough means more than 5000 trades and 10 years) I can’t suggest any settings as the best one.

The distance length, which means number of candles that their distance to MA is considered in our calculations, the distance source and also smoothing of the MATD is editable too.

And without editing it will look like something like this!

Didi Index PlusAbout this indicator (translation to Portuguese on the second half of the description):

The indicator follows the way Didi Aguiar teaches his trading system. Didi Aguiar is an old school Brazilian trader with over 40 years experience, who created the Didi Index and the famous agulhadas - or how I like to say in English: threads in the needle, an explosive price movement.

This version of the Didi Index adds what matters about DMI/ADX, Stochastic and TRIX to the regular Didi Index indicator.

The lines indicate alert and confirmations:

BLUE line crossing UP white line - BUY alert

PINK line crossing DOWN white line - BUY confirmation

Simultaneous Buy Alert and Confirmation = BUY AGULHADA.

BLUE line crossing DOWN white line - SHORT alert

PINK line crossing UP white line - SHORT confirmation

Simultaneous Short Alert and Confirmation = SHORT AGULHADA.

The background color changes according to the way Didi Aguiar reads the DMI and ADX.

Blue = Up trend

Bright Blue = Accelerating up trend

Purple = Down trend

Bright Purple = Accelerating down trend

Change from bright to dark color = ADX's bounce.

No coloured background = no trend.

The triangles on the top and bottom of the chart are the exit indicators.

They appear every time the Fast Stochastic and TRIX are in agreement:

Triangle on TOP of the chart means to EXIT LONG position.

- TRIX is selling and Stochastic just gave the sell signal; OR

- Stochastic is selling and TRIX just gave the sell signal

Triangle on BOTTOM of the chart means to EXIT SHORT position.

- TRIX is buying and Stochastic just gave the buy signal; OR

- Stochastic is buying and TRIX just gave the buy signal

Use this indicator with Bollinger Bands or other volatility indicator.

Not recommended for color-blind people :)

-----------------------------------------

Esse indicador segue a maneira que Didi Aguiar ensina o seu "trading system". Didi Aguiar é um trader velha-guarda com mais de 40 anos de experiência, que criou o Didi Index e as famosas Agulhadas, um movimento the preço explosivo.

Essa versão do Didi Index inclui o que interessa sobre outros três indicadores que o Didi usa em seu sistema: DMI/ADX, TRIX, e Estocástico.

As linhas indicam alerta e confirmação para o trade:

Linha AZUL cruzando a linha branca de BAIXO PARA CIMA - Alerta de compra

Linha ROSA cruzando a linha branca de CIMA PARA BAIXO - Confirmação de compra

ALERTA e CONFIRMAÇÃO de compra simultaneos = AGULHADA DE COMPRA

Linha AZUL cruzando a linha branca de CIMA PARA BAIXO - Alerta de venda

Linha ROSA cruzando a linha branca de BAIXO PARA CIMA - Confirmação de venda

ALERTA e CONFIRMAÇÃO de cenda simultaneos = AGULHADA DE VENDA

A cor do fundo muda de acordo com a maneira que o Didi lê o DMI e ADX

Fundo AZUL = Tendencia de compra

Fundo ROXO = Tendencia de venda

Cor mais saturada (vibrante) = Tendencia acelerante

Passou de cor mais clara para mais escura = Kick do ADX

Sem coloração de fundo = Sem tendencia

Os triângulos brancos na parte de cima e de baixo do indicador sinalizam a saida do trade.

Aparecem todas a vezes que o Etocastico e o TRIX ficam de acordo.

Triangulo na parte de CIMA sinaliza a SAÍDA da COMPRA.

- TRIX está vendido e o Estocástico acabou de vender; OU

- Estocástico está vendido e o TRIX acabou de vender

Triangulo na parte de BAIXO sinaliza a SAÍDA da VENDA.

- TRIX está comprado e o Estocástico acabou de comprar; OU

- Estocástico está comprado e o TRIX acabou de comprar

Use esse indicador em conjunto com as Bandas de Bollinger ou outro indicador de volatilidade.

Não é indicado para pessoas que sofrem de daltonismo :)

Classic Long Term Trend Following SystemThis is a classic long term trend following system.

The breakout period is 50 days instead of 20 and the moving average crossover are 40 and 120.

The moving averages are also exponential instead of simple.

The stoploss is 4 ATRs away from the price.

Recommendations:

Donchian Channels settings > 50 days

Moving Averages > 40 and 120, 80 and 140

Important to note:

My first strategy, DC Breakout System | This is simplicity at its finest, is best used on the crypto market and this one for stocks, commodities, currencies, etc. Those markets tend to trend a lot longer than crypto do.

Average True Range NormalizedIntroduction

This simple script is the normalization of the common ATR indicator. The utility in normalization, in this case, is the contextualization of the absolute movements of the ATR compared to the previous candles. Not finding an indicator that reflected my needs, I created it and decided to make it available to the community.

The oscillator is fully based on the original ATR indicator, once normalized it varies its values between -50 and +50 and has a moving average based on it.

I added alarms:

- crossing of horizontal levels (default +40 -40)

- crossing of the moving average

Settings

ATR period : like a normal ATR indicator, the number of candles on which the ATR calculation is based

Smooth : like normal ATR indicator, type of moving average to smooth true range values

Normalization Period : Number of candles on which ATR normalization is based, it takes the maximum and the minimum values in the last N candles and creates the value -50 and +50, between these two values normalize the others.

MA Period : Period of MA based on ATR, this MA can be used like moving level to find the moment of low volatility

Type : Kind of MA, you can choose only between 3 types ( SMA, EMA, WMA )

Horizontal Lines Value : high and low level for high and low volatility

Alert on crossing Horizontal lines : enable alerts on crossing Horizontal Lines

Alert on crossing MA : enable alerts on crossing Moving Average

How to use

ATR isn't a directional indicator, but volatility is fuel for markets, low ATR values indicate quiet moments or consolidation movements, otherwise high ATR values indicate selling or buying pressure. A reversal in price with an increase in ATR would indicate strength behind that move.

The problem, for me, with normal ATR is that often the values have to be contextualized with older values, on the contrary being normalized you can:

- catch small fluctuations, and anticipate the decline;

- contextualize the values without having to look at the history in the previous candles

So:

- under MA or horizontal line the volatility is too low, it would be advisable to consider not opening positions;

- over MA line the volatility is raising and a reversal in price with an increase in ATR would indicate strength behind that move;

Remember that every statistical indicator is just a tool, it needs to be understood to be used at its best, otherwise, it is just a colored line in a colored graph.

Smoothed Waddah ATR~~~All Credit to LAZY BEAR for posting the original Script which is an old MT4 indicator.~~~~

No this system does not repaint... if it does let me know. Either the code is wrong or you are using a repainting chart such as renko candles.

*PURPOSE*

This Is an "Enhanced or Smoothed" version of the script that captures the heiken-ashi closing price as its main calculation variable. While using normal bar or line charts. Enhancements integrate trade filters to reduce false signals.

*WHAT TYPE OF TRADING STRATEGY IS THIS?*

This is a Long Only, Trend Trading System. Is intended to be applied to Charts/Timeframes that produce sustainable trends for which ever asset you are trading.

*NOTE OF ADVICE REGARDING SETTINGS*

Settings can be tweaked but I have found that best results come with the given settings. If a chart is too choppy to trade this indicator successfully, it is advised not to change the settings but either find a different timeframe or different asset to apply this strategy to.

TLDR

Indicator measures the change of the MacD (difference between MAC D of given EMA's) and compares it to the difference between the Upper and Lower Bollinger bands. Green bar over trigger line= entry. Red bar over trigger line = close.

*SETTINGS AND INPUTS*

-MacD of HeikenAshi chart (will always be of the Heikenashi chart even when applied to different chart type)

sensitivity = input(150, title='Sensitivity') =range should be (125-175)multiplier so that MacD can be compared to BB

fastLength = input(20, title='MacD FastEMA Length')

slowLength = input(40, title='MacD SlowEMA Length')

-Bollinger Band of currently used price chart type

channelLength = input(20, title='BB Channel Length')

mult = input(1.5, title='BB Stdev Multiplier')

-14 Period RSI Trade Filter (set to 0 to Disable)

RSI14filter = input(40, title='RSI Value trade filter') =only gives entry when RSI is higher than given value

*ABSTRACT & CONCEPT*

TLDR - Indicator measures the change of the MacD (difference between MAC D of given EMA's) and compares it to the difference between the Upper and Lower Bollinger bands. Green bar over trigger line= entry. Red bar over trigger line = close.

Indicator plots -

Bars are the change in the MAC D and the indicator line is the difference in the BB.

When Bars are higher than the indicator line then it is considered a trend "Explosion"

Green Bars are Trend Explosion to the upside, Red Bars are Trend explosion to the downside.

GENERAL DETAIL-

the core calculation is measuring the change in MacD of current candle compared to the MacD of two previous candles.

This value is multiplied by the sensitivy so it can be compared to the change in Bollinger Band Width.

if the MACD change is positive then you get a green/lime bar for that value. If the MacDchange is negative you get a red/orange bar for that value.

and are determined by whether the actual change is increasing in that direction or decreasing. (bars getting taller or bars getting shorter)

Entry signal for long is A positive change in MACD difference (Green bar) that is greater than the change of the bollinger band (orange signal line) AND if the RSI value is above your filter.

Close signal or Trend Stop Warning Signal is given when a Negative MacD Difference (red bar) is greater than the change of the bollinger band (orange Line)

*CONSIDERATIONS AND THOUGHTS*

I have over 150 iterations of this indicator and this is the most consistent and best version of settings and filters I was able to generate. I built this indicator specifically for 3 charts. SPY monthly, QQQ monthly, BTC 3 Day. However this indicator works well on any long term bullish chart. (tech stocks are great) .

Trend trading systems are intended to be homerun hitting, plunge protecting indicators that allow for long legs and expanding volatility. This indicator does this as the trigger line is Dynamic with the expansion and contraction of the bollinger band.

I do not take every signal specifically not the close signals. Instead they more like warnings in ultra bullish environments.

If i had to pair this indicator with any other filter than the RSI, it would be a long term moving average i.e. the 50 week or equivalent for your chart. signals above rising moving averages means that you are trading with an upward trending market.

Hope this helps. Happy trades.

-SnarkyPuppy

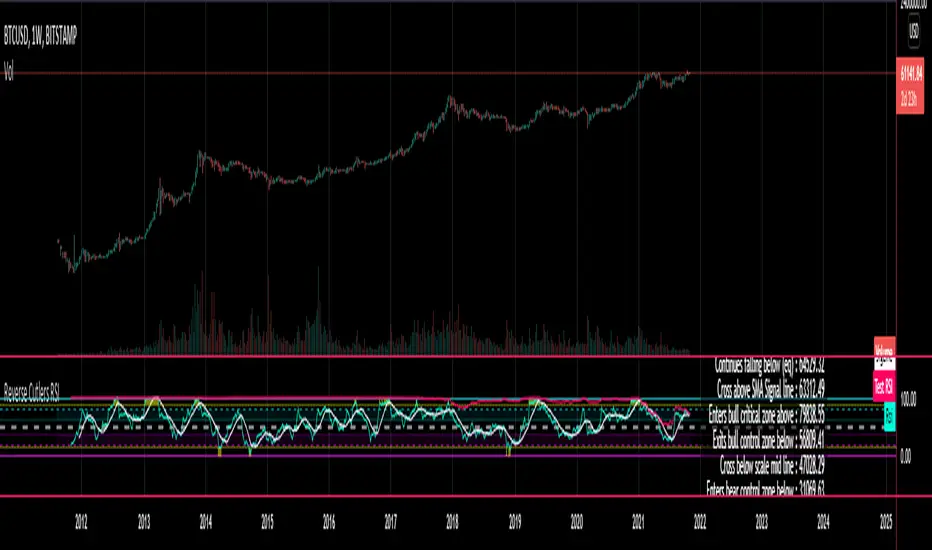

Reverse Cutlers Relative Strength Index On ChartIntroduction

The Reverse Cutlers Relative Strength Index (RCRSI) OC is an indicator which tells the user what price is required to give a particular Cutlers Relative Strength Index ( RSI ) value, or cross its Moving Average (MA) signal line.

Overview

Background & Credits:

The relative strength index ( RSI ) is a momentum indicator used in technical analysis that was originally developed by J. Welles Wilder Jr. and introduced in his seminal 1978 book, “New Concepts in Technical Trading Systems.”.

Cutler created a variation of the RSI known as “Cutlers RSI” using a different formulation to avoid an inherent accuracy problem which arises when using Wilders method of smoothing.

Further developments in the use, and more nuanced interpretations of the RSI have been developed by Cardwell, and also by well-known chartered market technician, Constance Brown C.M.T., in her acclaimed book "Technical Analysis for the Trading Professional” 1999 where she described the idea of bull and bear market ranges for RSI , and while she did not actually reveal the formulas, she introduced the concept of “reverse engineering” the RSI to give price level outputs.

Renowned financial software developer, co-author of academic books on finance, and scientific fellow to the Department of Finance and Insurance at the Technological Educational Institute of Crete, Giorgos Siligardos PHD . brought a new perspective to Wilder’s RSI when he published his excellent and well-received articles "Reverse Engineering RSI " and "Reverse Engineering RSI II " in the June 2003, and August 2003 issues of Stocks & Commodities magazine, where he described his methods of reverse engineering Wilders RSI .

Several excellent Implementations of the Reverse Wilders Relative Strength Index have been published here on Tradingview and elsewhere.

My utmost respect, and all due credits to authors of related prior works.

Introduction

It is worth noting that while the general RSI formula, and the logic dictating the UpMove and DownMove data series has remained the same as the Wilders original formulation, it has been interpreted in a different way by using a different method of averaging the upward, and downward moves.

Cutler recognized the issue of data length dependency when using wilders smoothing method of calculating RSI which means that wilders standard RSI will have a potential initialization error which reduces with every new data point calculated meaning early results should be regarded as unreliable until enough calculation iterations have occurred for convergence.

Hence Cutler proposed using Simple Moving Averaging for gain and loss data which this Indicator is based on.

Having "Reverse engineered" prices for any oscillator makes the planning, and execution of strategies around that oscillator far simpler, more timely and effective.

Introducing the Reverse Cutlers RSI which consists of plotted lines on a scale of 0 to 100, and an optional infobox.

The RSI scale is divided into zones:

• Scale high (100)

• Bull critical zone (80 - 100)

• Bull control zone (62 - 80)

• Scale midline (50)

• Bear control zone (20 - 38)

• Bear critical zone (0 - 20)

• Scale low (0)

The RSI plots which graphically display output closing price levels where Cutlers RSI value will crossover:

• RSI (eq) (previous RSI value)

• RSI MA signal line

• RSI Test price

• Alert level high

• Alert level low

The info box displays output closing price levels where Cutlers RSI value will crossover:

• Its previous value. ( RSI )

• Bull critical zone.

• Bull control zone.

• Mid-Line.

• Bear control zone.

• Bear critical zone.

• RSI MA signal line

• Alert level High

• Alert level low

And also displays the resultant RSI for a user defined closing price:

• Test price RSI

The infobox outputs can be shown for the current bar close, or the next bar close.

The user can easily select which information they want in the infobox from the setttings

Importantly:

All info box price levels for the current bar are calculated immediately upon the current bar closing and a new bar opening, they will not change until the current bar closes.

All info box price levels for the next bar are projections which are continually recalculated as the current price changes, and therefore fluctuate as the current price changes.

Understanding the Relative Strength Index

At its simplest the RSI is a measure of how quickly traders are bidding the price of an asset up or down.

It does this by calculating the difference in magnitude of price gains and losses over a specific lookback period to evaluate market conditions.

The RSI is displayed as an oscillator (a line graph that can move between two extremes) and outputs a value limited between 0 and 100.

It is typically accompanied by a moving average signal line.

Traditional interpretations

Overbought and oversold:

An RSI value of 70 or above indicates that an asset is becoming overbought (overvalued condition), and may be may be ready for a trend reversal or corrective pullback in price.

An RSI value of 30 or below indicates that an asset is becoming oversold (undervalued condition), and may be may be primed for a trend reversal or corrective pullback in price.

Midline Crossovers:

When the RSI crosses above its midline ( RSI > 50%) a bullish bias signal is generated. (only take long trades)

When the RSI crosses below its midline ( RSI < 50%) a bearish bias signal is generated. (only take short trades)

Bullish and bearish moving average signal Line crossovers:

When the RSI line crosses above its signal line, a bullish buy signal is generated

When the RSI line crosses below its signal line, a bearish sell signal is generated.

Swing Failures and classic rejection patterns:

If the RSI makes a lower high, and then follows with a downside move below the previous low, a Top Swing Failure has occurred.

If the RSI makes a higher low, and then follows with an upside move above the previous high, a Bottom Swing Failure has occurred.

Examples of classic swing rejection patterns

Bullish swing rejection pattern:

The RSI moves into oversold zone (below 30%).

The RSI rejects back out of the oversold zone (above 30%)

The RSI forms another dip without crossing back into oversold zone.

The RSI then continues the bounce to break up above the previous high.

Bearish swing rejection pattern:

The RSI moves into overbought zone (above 70%).

The RSI rejects back out of the overbought zone (below 70%)

The RSI forms another peak without crossing back into overbought zone.

The RSI then continues to break down below the previous low.

Divergences:

A regular bullish RSI divergence is when the price makes lower lows in a downtrend and the RSI indicator makes higher lows.

A regular bearish RSI divergence is when the price makes higher highs in an uptrend and the RSI indicator makes lower highs.

A hidden bullish RSI divergence is when the price makes higher lows in an uptrend and the RSI indicator makes lower lows.

A hidden bearish RSI divergence is when the price makes lower highs in a downtrend and the RSI indicator makes higher highs.

Regular divergences can signal a reversal of the trending direction.

Hidden divergences can signal a continuation in the direction of the trend.

Chart Patterns:

RSI regularly forms classic chart patterns that may not show on the underlying price chart, such as ascending and descending triangles & wedges , double tops, bottoms and trend lines etc.

Support and Resistance:

It is very often easier to define support or resistance levels on the RSI itself rather than the price chart.

Modern interpretations in trending markets:

Modern interpretations of the RSI stress the context of the greater trend when using RSI signals such as crossovers, overbought/oversold conditions, divergences and patterns.

Constance Brown, CMT , was one of the first who promoted the idea that an oversold reading on the RSI in an uptrend is likely much higher than 30%, and that an overbought reading on the RSI during a downtrend is much lower than the 70% level.

In an uptrend or bull market, the RSI tends to remain in the 40 to 90 range, with the 40-50 zone acting as support.

During a downtrend or bear market, the RSI tends to stay between the 10 to 60 range, with the 50-60 zone acting as resistance.

For ease of executing more modern and nuanced interpretations of RSI it is very useful to break the RSI scale into bull and bear control and critical zones.

These ranges will vary depending on the RSI settings and the strength of the specific market’s underlying trend.

Limitations of the RSI

Like most technical indicators, its signals are most reliable when they conform to the long-term trend.

True trend reversal signals are rare, and can be difficult to separate from false signals.

False signals or “fake-outs”, e.g. a bullish crossover, followed by a sudden decline in price, are common.

Since the indicator displays momentum, it can stay overbought or oversold for a long time when an asset has significant sustained momentum in either direction.

Data Length Dependency when using wilders smoothing method of calculating RSI means that wilders standard RSI will have a potential initialization error which reduces with every new data point calculated meaning early results should be regarded as unreliable until calculation iterations have occurred for convergence.

Reverse Cutlers Relative Strength IndexIntroduction

The Reverse Cutlers Relative Strength Index (RCRSI) is an indicator which tells the user what price is required to give a particular Cutlers Relative Strength Index (RSI) value, or cross its Moving Average (MA) signal line.

Overview

Background & Credits:

The relative strength index (RSI) is a momentum indicator used in technical analysis that was originally developed by J. Welles Wilder Jr. and introduced in his seminal 1978 book, “New Concepts in Technical Trading Systems.”.

Cutler created a variation of the RSI known as “Cutlers RSI” using a different formulation to avoid an inherent accuracy problem which arises when using Wilders method of smoothing.

Further developments in the use, and more nuanced interpretations of the RSI have been developed by Cardwell, and also by well-known chartered market technician, Constance Brown C.M.T., in her acclaimed book "Technical Analysis for the Trading Professional” 1999 where she described the idea of bull and bear market ranges for RSI, and while she did not actually reveal the formulas, she introduced the concept of “reverse engineering” the RSI to give price level outputs.

Renowned financial software developer, co-author of academic books on finance, and scientific fellow to the Department of Finance and Insurance at the Technological Educational Institute of Crete, Giorgos Siligardos PHD. brought a new perspective to Wilder’s RSI when he published his excellent and well-received articles "Reverse Engineering RSI " and "Reverse Engineering RSI II " in the June 2003, and August 2003 issues of Stocks & Commodities magazine, where he described his methods of reverse engineering Wilders RSI.

Several excellent Implementations of the Reverse Wilders Relative Strength Index have been published here on Tradingview and elsewhere.

My utmost respect, and all due credits to authors of related prior works.

Introduction

It is worth noting that while the general RSI formula, and the logic dictating the UpMove and DownMove data series as described above has remained the same as the Wilders original formulation, it has been interpreted in a different way by using a different method of averaging the upward, and downward moves.

Cutler recognized the issue of data length dependency when using wilders smoothing method of calculating RSI which means that wilders standard RSI will have a potential initialization error which reduces with every new data point calculated meaning early results should be regarded as unreliable until enough calculation iterations have occurred for convergence.

Hence Cutler proposed using Simple Moving Averaging for gain and loss data which this Indicator is based on.

Having "Reverse engineered" prices for any oscillator makes the planning, and execution of strategies around that oscillator far simpler, more timely and effective.

Introducing the Reverse Cutlers RSI which consists of plotted lines on a scale of 0 to 100, and an optional infobox.

The RSI scale is divided into zones:

• Scale high (100)

• Bull critical zone (80 - 100)

• Bull control zone (62 - 80)

• Scale midline (50)

• Bear critical zone (20 - 38)

• Bear control zone (0 - 20)

• Scale low (0)

The RSI plots are:

• Cutlers RSI

• RSI MA signal line

• Test price RSI

• Alert level high

• Alert level low

The info box displays output closing price levels where Cutlers RSI value will crossover:

• Its previous value. (RSI )

• Bull critical zone.

• Bull control zone.

• Mid-Line.

• Bear control zone.

• Bear critical zone.

• RSI MA signal line

• Alert level High

• Alert level low

And also displays the resultant RSI for a user defined closing price:

• Test price RSI

The infobox outputs can be shown for the current bar close, or the next bar close.

The user can easily select which information they want in the infobox from the setttings

Importantly:

All info box price levels for the current bar are calculated immediately upon the current bar closing and a new bar opening, they will not change until the current bar closes.

All info box price levels for the next bar are projections which are continually recalculated as the current price changes, and therefore fluctuate as the current price changes.

Understanding the Relative Strength Index

At its simplest the RSI is a measure of how quickly traders are bidding the price of an asset up or down.

It does this by calculating the difference in magnitude of price gains and losses over a specific lookback period to evaluate market conditions.

The RSI is displayed as an oscillator (a line graph that can move between two extremes) and outputs a value limited between 0 and 100.

It is typically accompanied by a moving average signal line.

Traditional interpretations

Overbought and oversold:

An RSI value of 70 or above indicates that an asset is becoming overbought (overvalued condition), and may be may be ready for a trend reversal or corrective pullback in price.

An RSI value of 30 or below indicates that an asset is becoming oversold (undervalued condition), and may be may be primed for a trend reversal or corrective pullback in price.

Midline Crossovers:

When the RSI crosses above its midline (RSI > 50%) a bullish bias signal is generated. (only take long trades)

When the RSI crosses below its midline (RSI < 50%) a bearish bias signal is generated. (only take short trades)

Bullish and bearish moving average signal Line crossovers:

When the RSI line crosses above its signal line, a bullish buy signal is generated

When the RSI line crosses below its signal line, a bearish sell signal is generated.

Swing Failures and classic rejection patterns:

If the RSI makes a lower high, and then follows with a downside move below the previous low, a Top Swing Failure has occurred.

If the RSI makes a higher low, and then follows with an upside move above the previous high, a Bottom Swing Failure has occurred.

Examples of classic swing rejection patterns

Bullish swing rejection pattern:

The RSI moves into oversold zone (below 30%).

The RSI rejects back out of the oversold zone (above 30%)

The RSI forms another dip without crossing back into oversold zone.

The RSI then continues the bounce to break up above the previous high.

Bearish swing rejection pattern:

The RSI moves into overbought zone (above 70%).

The RSI rejects back out of the overbought zone (below 70%)

The RSI forms another peak without crossing back into overbought zone.

The RSI then continues to break down below the previous low.

Divergences:

A regular bullish RSI divergence is when the price makes lower lows in a downtrend and the RSI indicator makes higher lows.

A regular bearish RSI divergence is when the price makes higher highs in an uptrend and the RSI indicator makes lower highs.

A hidden bullish RSI divergence is when the price makes higher lows in an uptrend and the RSI indicator makes lower lows.

A hidden bearish RSI divergence is when the price makes lower highs in a downtrend and the RSI indicator makes higher highs.

Regular divergences can signal a reversal of the trending direction.

Hidden divergences can signal a continuation in the direction of the trend.

Chart Patterns:

RSI regularly forms classic chart patterns that may not show on the underlying price chart, such as ascending and descending triangles & wedges, double tops, bottoms and trend lines etc.

Support and Resistance:

It is very often easier to define support or resistance levels on the RSI itself rather than the price chart.

Modern interpretations in trending markets:

Modern interpretations of the RSI stress the context of the greater trend when using RSI signals such as crossovers, overbought/oversold conditions, divergences and patterns.

Constance Brown, CMT, was one of the first who promoted the idea that an oversold reading on the RSI in an uptrend is likely much higher than 30%, and that an overbought reading on the RSI during a downtrend is much lower than the 70% level.

In an uptrend or bull market, the RSI tends to remain in the 40 to 90 range, with the 40-50 zone acting as support.

During a downtrend or bear market, the RSI tends to stay between the 10 to 60 range, with the 50-60 zone acting as resistance.

For ease of executing more modern and nuanced interpretations of RSI it is very useful to break the RSI scale into bull and bear control and critical zones.

These ranges will vary depending on the RSI settings and the strength of the specific market’s underlying trend.

Limitations of the RSI

Like most technical indicators, its signals are most reliable when they conform to the long-term trend.

True trend reversal signals are rare, and can be difficult to separate from false signals.

False signals or “fake-outs”, e.g. a bullish crossover, followed by a sudden decline in price, are common.

Since the indicator displays momentum, it can stay overbought or oversold for a long time when an asset has significant sustained momentum in either direction.

Data Length Dependency when using wilders smoothing method of calculating RSI means that wilders standard RSI will have a potential initialization error which reduces with every new data point calculated meaning early results should be regarded as unreliable until calculation iterations have occurred for convergence.

ADX and DI LevelsADX:

ADX is used to quantify trend strength. ADX calculations are based on a moving average of price range expansion over a given period of time. The default setting is 14 bars, although other time periods can be used.1

ADX can be used on any trading vehicle such as stocks, mutual funds, exchange-traded funds and futures.

DI (+/-):

The directional movement index (DMI) is an indicator developed by J. Welles Wilder in 1978 that identifies in which direction the price of an asset is moving. The indicator does this by comparing prior highs and lows and drawing two lines: a positive directional movement line (+DI) and a negative directional movement line (-DI). An optional third line, called the average directional index (ADX), can also be used to gauge the strength of the uptrend or downtrend.

This indicator has the length changed from 14 to 9 so you can have more updated price calculation

I also add the 4 levels I use for day trading; the 10, 20, 30, 40-50 are the levels I like to see the Di to break over.

A lot of traders use different levels, but these I have and found most useful. You can set alerts when any Di crosses over the 40 for true trend breakout!

Stochastic RSI - DurbtradeDurbtrade Stoch RSI -

1) Stoch RSI

A) The K line can be customized to change color based on vertical direction.

B) The space between K line and D line can be filled with a color depending on whether K line is above or below the D line.

C) There are color-coded, cross-over and cross-under background fills, to signal when the K line crosses the D line.

D) K line is drawn in front of D line (D line is drawn behind K line).

E) Default values : K = 3, D = 4, RSI Length = 14, Stoch Length = 14

2) Horizontal Lines

A) Horizontal lines can be drawn automatically, so you don't have to draw them, and they don't extend past the current bar.

B) There are 11 customizable horizontal lines,

and each line is set to non-customizable increments (zero, 10, 20, 30, 40, fifty, 60, 70, 80, 90, hundred).

C) The 11 lines are divided into 2 groups:

a) 4 PAIRS of lines WITH fill options (10/90, 20/80, 30/70, 40/60... 8 lines total), and

b) 3 INDIVIDUAL lines WITHOUT fill options (zero, fifty, hundred).

D) The 4 fills give you the option to fill the space between each pair with a customizable color and opacity,

regardless of whether the lines themselves are drawn or not.

(all default values are what I feel work best for this indicator...

and initially, only the zero, fifty, and hundred lines are drawn automatically .

You may add the other lines if you choose to, by adjusting the opacity to your liking).

3) Conclusion

A) As with my previous indicators, this one maximizes information, color, discernment, clarity, and customization.

B) It is optimized for your ability to be able to easily customize the indicator according to your preferences...

for use on your own personal television, laptop, or cellular phone screen setup... and on all chart zoom levels and layouts.

C) Please feel free to comment your thoughts, critiques, or suggestions. They are all helpful!

D) Check out my previous pine script indicators if you like this one. They work really well together.

E) I hope that you find this script useful.

F) Enjoy!

//Durbtrade

Custom Multi-Timeframe Screener with AlertsThis is a multi-timeframe screener with alerts. Use this way you can create a screener on indicators using 2 or more timeframes.

In TradingView there is a limit of 40 security function calls. Every timeframe requires another security call so you can screen fewer symbols with any additional timeframe.

In this example, I use 2 timeframes, so the maximum amount of symbols you can scan is 40/2 = 20.

For 3 timeframes - 13, 4tfs - 10, 5tfs - 8 symbols and so on.

In this simplistic example, I require a cross of EMAs on the current timeframe and confirmation that one EMA above/below another from the second timeframe.

Of course, you can create much more complicated functions for this screener.

Params

- higher timeframe

- ema params

- 20 symbol inputs for instruments you want to use in this screener

Alerts

You can create an alert from it easily by selecting the screener name from the list and then selecting "Any alert() function call".

No additional configuration is required, message and alert on close is generated in the code.

You should better change the default name for your alert. Sometimes because of big amount of inputs you might receive an error.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as good as in historical backtesting.

This post and the script don’t provide any financial advice.

RSI Relative Strength Index 3X - DurbtradeDurbtrade Triple RSI - 3 individual RSI's on 1 indicator, each distinguishable by length, as well as line color, thickness, opacity, and type.

(note: usable line TYPES are limited... try experimenting)

1) RSI's

A) Each RSI can be customized to change color based on RSI vertical direction (default = only RSI #1 changes color).

B) All 3 RSI's use a single Source (default Close).

C) You may customize the length of each RSI individually (I LOVE my default 14, 7, and 3!).

D) RSI #1 is the primary RSI, and is plotted LAST, so that it is drawn ABOVE RSI #2, which is drawn above RSI #3.

2) Horizontal Lines

A) Horizontal lines are also drawn automatically, so you don't have to, and they don't extend past the current bar.

B) There are 11 customizable lines, and each one is set to non-customizable increments (zero, 10, 20, 30, 40, fifty, 60, 70, 80, 90, hundred).

C) The 11 lines are divided into 2 groups:

a) 4 PAIRS of lines WITH fill options (10/90, 20/80, 30/70, 40/60... 8 lines total), and

b) 3 INDIVIDUAL lines WITHOUT fill options (zero, fifty, hundred).

D) The 4 fills give you the option to fill the space between each pair with a customizable color and opacity (the default is what I personally feel is best for each).

3) Conclusion

A) As with my previous indicators, this one maximizes information, discernment, clarity, and customization.

B) It is optimized for your ability to be able to customize a relatively basic but important indicator with ease

for use on your own personal television, laptop, or cellular phone screen setup... and on all chart zoom levels and layouts.

B) And, this being my 3rd script, please feel free to comment, critique, or leave suggestions. I find them helpful!

C) Check out my previous pine scripts if you like this one. They work well together.

D) I hope that you find this useful.

E) Enjoy!

//Durbtrade