US Presidents (Alternating Fills by Order)📜 Indicator Description: US Presidents Background Fill

This indicator highlights the terms of U.S. Presidents on your chart with alternating red and blue background fills based on their political party:

• 🟥 Republicans = Red

• 🟦 Democrats = Blue

• 🎨 Dark/Light shading alternates with each new president to clearly distinguish consecutive terms, even within the same party.

The fill starts from President Ulysses S. Grant (18th President, 1873) through to the 47th president in 2025. It is designed to work with any asset and automatically adapts to the visible date range on your chart.

Ideal for visualizing macro trends, historical context, and how markets may have reacted under different political administrations.

Cari dalam skrip untuk "几内亚黄金2025价目表"

TASC 2025.04 The Ultimate Oscillator█ OVERVIEW

This script implements an alternative, refined version of the Ultimate Oscillator (UO) designed to reduce lag and enhance responsiveness in momentum indicators, as introduced by John F. Ehlers in his article "Less Lag In Momentum Indicators, The Ultimate Oscillator" from the April 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers states that indicators are essentially filters that remove unwanted noise (i.e., unnecessary information) from market data. Simply put, they process a series of data to place focus on specific information, providing a different perspective on price dynamics. Various filter types attenuate different periodic signals within the data. For instance, a lowpass filter allows only low-frequency signals, a highpass filter allows only high-frequency signals, and a bandpass filter allows signals within a specific frequency range .

Ehlers explains that the key to removing indicator lag is to combine filters of different types in such a way that the result preserves necessary, useful signals while minimizing delay (lag). His proposed UltimateOscillator aims to maintain responsiveness to a specific frequency range by measuring the difference between two highpass filters' outputs. The oscillator uses the following formula:

UO = (HP1 - HP2) / RMS

Where:

HP1 is the first highpass filter.

HP2 is another highpass filter that allows only shorter wavelengths than the critical period of HP1.

RMS is the root mean square of the highpass filter difference, used as a scaling factor to standardize the output.

The resulting oscillator is similar to a bandpass filter , because it emphasizes wavelengths between the critical periods of the two highpass filters. Ehlers' UO responds quickly to value changes in a series, providing a responsive view of momentum with little to no lag.

█ USAGE

Ehlers' UltimateOscillator sets the critical periods of its highpass filters using two parameters: BandEdge and Bandwidth :

The BandEdge sets the critical period of the second highpass filter, which determines the shortest wavelengths in the response.

The Bandwidth is a multiple of the BandEdge used for the critical period of the first highpass filter, which determines the longest wavelengths in the response. Ehlers suggests that a Bandwidth value of 2 works well for most applications. However, traders can use any value above or equal to 1.4.

Users can customize these parameters with the "Bandwidth" and "BandEdge" inputs in the "Settings/Inputs" tab.

The script plots the UO calculated for the specified "Source" series in a separate pane, with a color based on the chart's foreground color. Positive UO values indicate upward momentum or trends, and negative UO values indicate the opposite.

Additionally, this indicator provides the option to display a "cloud" from 10 additional UO series with different settings for an aggregate view of momentum. The "Cloud" input offers four display choices: "Bandwidth", "BandEdge", "Bandwidth + BandEdge", or "None".

The "Bandwidth" option calculates oscillators with different Bandwidth values based on the main oscillator's setting. Likewise, the "BandEdge" option calculates oscillators with varying BandEdge values. The "Bandwidth + BandEdge" option calculates the extra oscillators with different values for both parameters.

When a user selects any of these options, the script plots the maximum and minimum oscillator values and fills their space with a color gradient. The fill color corresponds to the net sum of each UO's sign , indicating whether most of the UOs reflect positive or negative momentum. Green hues mean most oscillators are above zero, signifying stronger upward momentum. Red hues mean most are below zero, indicating stronger downward momentum.

Mogwai Method with RSI and EMA - BTCUSD 15mThis is a custom TradingView indicator designed for trading Bitcoin (BTCUSD) on a 15-minute timeframe. It’s based on the Mogwai Method—a mean-reversion strategy—enhanced with the Relative Strength Index (RSI) for momentum confirmation. The indicator generates buy and sell signals, visualized as green and red triangle arrows on the chart, to help identify potential entry and exit points in the volatile cryptocurrency market.

Components

Bollinger Bands (BB):

Purpose: Identifies overextended price movements, signaling potential reversions to the mean.

Parameters:

Length: 20 periods (standard for mean-reversion).

Multiplier: 2.2 (slightly wider than the default 2.0 to suit BTCUSD’s volatility).

Role:

Buy signal when price drops below the lower band (oversold).

Sell signal when price rises above the upper band (overbought).

Relative Strength Index (RSI):

Purpose: Confirms momentum to filter out false signals from Bollinger Bands.

Parameters:

Length: 14 periods (classic setting, effective for crypto).

Overbought Level: 70 (price may be overextended upward).

Oversold Level: 30 (price may be overextended downward).

Role:

Buy signal requires RSI < 30 (oversold).

Sell signal requires RSI > 70 (overbought).

Exponential Moving Averages (EMAs) (Plotted but not currently in signal logic):

Purpose: Provides trend context (included in the script for visualization, optional for signal filtering).

Parameters:

Fast EMA: 9 periods (short-term trend).

Slow EMA: 50 periods (longer-term trend).

Role: Can be re-added to filter signals (e.g., buy only when Fast EMA > Slow EMA).

Signals (Triangles):

Buy Signal: Green upward triangle below the bar when price is below the lower Bollinger Band and RSI is below 30.

Sell Signal: Red downward triangle above the bar when price is above the upper Bollinger Band and RSI is above 70.

How It Works

The indicator combines Bollinger Bands and RSI to spot mean-reversion opportunities:

Buy Condition: Price breaks below the lower Bollinger Band (indicating oversold conditions), and RSI confirms this with a reading below 30.

Sell Condition: Price breaks above the upper Bollinger Band (indicating overbought conditions), and RSI confirms this with a reading above 70.

The strategy assumes that extreme price movements in BTCUSD will often revert to the mean, especially in choppy or ranging markets.

Visual Elements

Green Upward Triangles: Appear below the candlestick to indicate a buy signal.

Red Downward Triangles: Appear above the candlestick to indicate a sell signal.

Bollinger Bands: Gray lines (upper, middle, lower) plotted for reference.

EMAs: Blue (Fast) and Orange (Slow) lines for trend visualization.

How to Use the Indicator

Setup

Open TradingView:

Log into TradingView and select a BTCUSD chart from a supported exchange (e.g., Binance, Coinbase, Bitfinex).

Set Timeframe:

Switch the chart to a 15-minute timeframe (15m).

Add the Indicator:

Open the Pine Editor (bottom panel in TradingView).

Copy and paste the script provided.

Click “Add to Chart” to apply it.

Verify Display:

You should see Bollinger Bands (gray), Fast EMA (blue), Slow EMA (orange), and buy/sell triangles when conditions are met.

Trading Guidelines

Buy Signal (Green Triangle Below Bar):

What It Means: Price is oversold, potentially ready to bounce back toward the Bollinger Band middle line.

Action:

Enter a long position (buy BTCUSD).

Set a take-profit near the middle Bollinger Band (bb_middle) or a resistance level.

Place a stop-loss 1-2% below the entry (or based on ATR, e.g., ta.atr(14) * 2).

Best Context: Works well in ranging markets; avoid during strong downtrends.

Sell Signal (Red Triangle Above Bar):

What It Means: Price is overbought, potentially ready to drop back toward the middle line.

Action:

Enter a short position (sell BTCUSD) or exit a long position.

Set a take-profit near the middle Bollinger Band or a support level.

Place a stop-loss 1-2% above the entry.

Best Context: Effective in ranging markets; avoid during strong uptrends.

Trend Filter (Optional):

To reduce false signals in trending markets, you can modify the script:

Add and ema_fast > ema_slow to the buy condition (only buy in uptrends).

Add and ema_fast < ema_slow to the sell condition (only sell in downtrends).

Check the Fast EMA (blue) vs. Slow EMA (orange) alignment visually.

Tips for BTCUSD on 15-Minute Charts

Volatility: BTCUSD can be erratic. If signals are too frequent, increase bb_mult (e.g., to 2.5) or adjust RSI levels (e.g., 75/25).

Confirmation: Use volume spikes or candlestick patterns (e.g., doji, engulfing) to confirm signals.

Time of Day: Mean-reversion works best during low-volume periods (e.g., Asian session in crypto).

Backtesting: Use TradingView’s Strategy Tester (convert to a strategy by adding entry/exit logic) to evaluate performance with historical BTCUSD data up to March 13, 2025.

Risk Management

Position Size: Risk no more than 1-2% of your account per trade.

Stop Losses: Always use stops to protect against BTCUSD’s sudden moves.

Avoid Overtrading: Wait for clear signals; don’t force trades in choppy or unclear conditions.

Example Scenario

Chart: BTCUSD, 15-minute timeframe.

Buy Signal: Price drops to $58,000, below the lower Bollinger Band, RSI at 28. A green triangle appears.

Action: Buy at $58,000, target $59,000 (middle BB), stop at $57,500.

Sell Signal: Price rises to $60,500, above the upper Bollinger Band, RSI at 72. A red triangle appears.

Action: Sell at $60,500, target $59,500 (middle BB), stop at $61,000.

This indicator is tailored for mean-reversion trading on BTCUSD. Let me know if you’d like to tweak it further (e.g., add filters, alerts, or alternative indicators)!

Full Moon and New Moon IndicatorThe Full Moon & New Moon Indicator is a custom Pine Script indicator which marks Full Moon (Pournami) and New Moon (Amavasya) events on the price chart. This indicator helps traders who incorporate lunar cycles into their market analysis, as certain traders believe these cycles influence market sentiment and price action. The current script is added for the year 2024 and 2025 and the dates are considered as per the Telugu calendar.

Features

✅ Identifies and labels Full Moon & New Moon days on the chart for the year 2024 and 2025

How it Works!

On a Full Moon day, it places a yellow label ("Pournami") above the corresponding candle.

On a New Moon day, it places a blue label ("Amavasya") above the corresponding candle.

Example Usage

When a Full Moon label appears, check for potential trend reversals or high volatility.

When a New Moon label appears, watch for market consolidation or a shift in sentiment.

Combine with candlestick patterns, support/resistance, or momentum indicators for a stronger trading setup.

🚀 Add this indicator to your TradingView chart and explore the market’s reaction to lunar cycles! 🌕

TASC 2025.03 A New Solution, Removing Moving Average Lag█ OVERVIEW

This script implements a novel technique for removing lag from a moving average, as introduced by John Ehlers in the "A New Solution, Removing Moving Average Lag" article featured in the March 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers explains that the average price in a time series represents a statistical estimate for a block of price values, where the estimate is positioned at the block's center on the time axis. In the case of a simple moving average (SMA), the calculation moves the analyzed block along the time axis and computes an average after each new sample. Because the average's position is at the center of each block, the SMA inherently lags behind price changes by half the data length.

As a solution to removing moving average lag, Ehlers proposes a new projected moving average (PMA) . The PMA smooths price data while maintaining responsiveness by calculating a projection of the average using the data's linear regression slope.

The slope of linear regression on a block of financial time series data can be expressed as the covariance between prices and sample points divided by the variance of the sample points. Ehlers derives the PMA by adding this slope across half the data length to the SMA, creating a first-order prediction that substantially reduces lag:

PMA = SMA + Slope * Length / 2

In addition, the article includes methods for calculating predictions of the PMA and the slope based on second-order and fourth-order differences. The formulas for these predictions are as follows:

PredictPMA = PMA + 0.5 * (Slope - Slope ) * Length

PredictSlope = 1.5 * Slope - 0.5 * Slope

Ehlers suggests that crossings between the predictions and the original values can help traders identify timely buy and sell signals.

█ USAGE

This indicator displays the SMA, PMA, and PMA prediction for a specified series in the main chart pane, and it shows the linear regression slope and prediction in a separate pane. Analyzing the difference between the PMA and SMA can help to identify trends. The differences between PMA or slope and its corresponding prediction can indicate turning points and potential trade opportunities.

The SMA plot uses the chart's foreground color, and the PMA and slope plots are blue by default. The plots of the predictions have a green or red hue to signify direction. Additionally, the indicator fills the space between the SMA and PMA with a green or red color gradient based on their differences:

Users can customize the source series, data length, and plot colors via the inputs in the "Settings/Inputs" tab.

█ NOTES FOR Pine Script® CODERS

The article's code implementation uses a loop to calculate all necessary sums for the slope and SMA calculations. Ported into Pine, the implementation is as follows:

pma(float src, int length) =>

float PMA = 0., float SMA = 0., float Slope = 0.

float Sx = 0.0 , float Sy = 0.0

float Sxx = 0.0 , float Syy = 0.0 , float Sxy = 0.0

for count = 1 to length

float src1 = src

Sx += count

Sy += src

Sxx += count * count

Syy += src1 * src1

Sxy += count * src1

Slope := -(length * Sxy - Sx * Sy) / (length * Sxx - Sx * Sx)

SMA := Sy / length

PMA := SMA + Slope * length / 2

However, loops in Pine can be computationally expensive, and the above loop's runtime scales directly with the specified length. Fortunately, Pine's built-in functions often eliminate the need for loops. This indicator implements the following function, which simplifies the process by using the ta.linreg() and ta.sma() functions to calculate equivalent slope and SMA values efficiently:

pma(float src, int length) =>

float Slope = ta.linreg(src, length, 0) - ta.linreg(src, length, 1)

float SMA = ta.sma(src, length)

float PMA = SMA + Slope * length * 0.5

To learn more about loop elimination in Pine, refer to this section of the User Manual's Profiling and optimization page.

TASC 2025.02 Autocorrelation Indicator█ OVERVIEW

This script implements the Autocorrelation Indicator introduced by John Ehlers in the "Drunkard's Walk: Theory And Measurement By Autocorrelation" article from the February 2025 edition of TASC's Traders' Tips . The indicator calculates the autocorrelation of a price series across several lags to construct a periodogram , which traders can use to identify market cycles, trends, and potential reversal patterns.

█ CONCEPTS

Drunkard's walk

A drunkard's walk , formally known as a random walk , is a type of stochastic process that models the evolution of a system or variable through successive random steps.

In his article, John Ehlers relates this model to market data. He discusses two first- and second-order partial differential equations, modified for discrete (non-continuous) data, that can represent solutions to the discrete random walk problem: the diffusion equation and the wave equation. According to Ehlers, market data takes on a mixture of two "modes" described by these equations. He theorizes that when "diffusion mode" is dominant, trading success is almost a matter of luck, and when "wave mode" is dominant, indicators may have improved performance.

Pink spectrum

John Ehlers explains that many recent academic studies affirm that market data has a pink spectrum , meaning the power spectral density of the data is proportional to the wavelengths it contains, like pink noise . A random walk with a pink spectrum suggests that the states of the random variable are correlated and not independent. In other words, the random variable exhibits long-range dependence with respect to previous states.

Autocorrelation function (ACF)

Autocorrelation measures the correlation of a time series with a delayed copy, or lag , of itself. The autocorrelation function (ACF) is a method that evaluates autocorrelation across a range of lags , which can help to identify patterns, trends, and cycles in stochastic market data. Analysts often use ACF to detect and characterize long-range dependence in a time series.

The Autocorrelation Indicator evaluates the ACF of market prices over a fixed range of lags, expressing the results as a color-coded heatmap representing a dynamic periodogram. Ehlers suggests the information from the periodogram can help traders identify different market behaviors, including:

Cycles : Distinguishable as repeated patterns in the periodogram.

Reversals : Indicated by sharp vertical changes in the periodogram when the indicator uses a short data length .

Trends : Indicated by increasing correlation across lags, starting with the shortest, over time.

█ USAGE

This script calculates the Autocorrelation Indicator on an input "Source" series, smoothed by Ehlers' UltimateSmoother filter, and plots several color-coded lines to represent the periodogram's information. Each line corresponds to an analyzed lag, with the shortest lag's line at the bottom of the pane. Green hues in the line indicate a positive correlation for the lag, red hues indicate a negative correlation (anticorrelation), and orange or yellow hues mean the correlation is near zero.

Because Pine has a limit on the number of plots for a single indicator, this script divides the periodogram display into three distinct ranges that cover different lags. To see the full periodogram, add three instances of this script to the chart and set the "Lag range" input for each to a different value, as demonstrated in the chart above.

With a modest autocorrelation length, such as 20 on a "1D" chart, traders can identify seasonal patterns in the price series, which can help to pinpoint cycles and moderate trends. For instance, on the daily ES1! chart above, the indicator shows repetitive, similar patterns through fall 2023 and winter 2023-2024. The green "triangular" shape rising from the zero lag baseline over different time ranges corresponds to seasonal trends in the data.

To identify turning points in the price series, Ehlers recommends using a short autocorrelation length, such as 2. With this length, users can observe sharp, sudden shifts along the vertical axis, which suggest potential turning points from upward to downward or vice versa.

Highs & Lows RTH/OVN/IBs/D/W/M/YOverview

Plots the highs and lows of RTH, OVN/ETH, IBs of those sessions, previous Day, Week, Month, and Year.

Features

Allows the user to enable/disable plotting the high/low of each period.

Lines' length, offset, and colors can be customized

Labels' position, size, color, and style can be customized

Support

Questions, feedbacks, and requests are welcomed. Please feel free to use Comments or direct private message via TradingView.

Disclaimer

This stock chart indicator provided is for informational purposes only and should not be considered as financial or investment advice. The data and information presented in this indicator are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy.

Users should be aware that:

Any investment decisions made based on this indicator are at your own risk.

The creators and providers of this indicator disclaim all liability for any losses, damages, or other consequences resulting from its use. By using this stock chart indicator, you acknowledge and accept the inherent risks associated with trading and investing in financial markets.

Release Date: 2025-01-17

Release Version: v1 r1

Release Notes Date: 2025-01-17

SW monthly Gann Days**Script Description:**

The script you are looking at is based on the work of W.D. Gann, a famous trader and market analyst in the early 20th century, known for his use of geometry, astrology, and numerology in market analysis. Gann believed that certain days in the market had significant importance, and he observed that markets often exhibited significant price moves around specific dates. These dates were typically associated with cyclical patterns in price movements, and Gann referred to these as "Gann Days."

In this script, we have focused on highlighting certain days of the month that Gann believed to have an influence on market behavior. The specific days in question are the **6th to 7th**, **9th to 10th**, **14th to 15th**, **19th to 20th**, **23rd to 24th**, and **29th to 31st** of each month. These ranges are based on Gann’s theory that there are recurring time cycles in the market that cause turning points or critical price movements to occur around certain days of the month.

### **Why Gann Used These Days:**

1. **Mathematical and Astrological Cycles:**

Gann believed that markets were influenced by natural cycles, and that certain dates (or combinations of dates) played a critical role in the price movements. These specific days are part of his broader theory of "time cycles" where the market would often change direction, reverse, or exhibit significant volatility on particular days. Gann's research was based on both mathematical principles and astrological observations, leading him to assign importance to these days.

2. **Gann's Universal Timing Theory:**

According to Gann, financial markets operate in a universe governed by geometric and astrological principles. These cycles repeat themselves over time, and specific days in a given month correspond to key turning points within these repeating cycles. Gann found that the 6th to 7th, 9th to 10th, 14th to 15th, 19th to 20th, 23rd to 24th, and 29th to 31st often marked significant changes in the market, making them particularly important for traders to watch.

3. **Market Psychology and Sentiment:**

These specific days likely correspond to key moments where market participants tend to react in predictable ways, influenced by past market behavior on similar dates. For example, news events or scheduled economic reports might fall within these time windows, causing the market to respond in a particular way. Gann's method involves using these cyclical patterns to predict turning points in market prices, enabling traders to anticipate when the market might make a reversal or face a significant shift in direction.

4. **Turning Points:**

Gann believed that markets often reversed or encountered critical points around specific dates. This is why he considered certain days more important than others. By identifying and focusing on these days, traders can better anticipate the market’s movement and make more informed trading decisions.

5. **Numerology:**

Gann also utilized numerology in his trading system, believing that numbers, and particularly certain key numbers, had significance in predicting market movements. The days selected in this script may correspond to numerological patterns that Gann identified in his analysis of the markets, such as recurring numbers in his astrological and geometric systems.

### **Purpose of the Script:**

This script highlights these "Gann Days" within a trading chart for 2024 and 2025. The color-coding or background highlighting is intended to draw attention to these dates, so traders can observe the potential for significant market movements during these times. By identifying these specific dates, traders following Gann's theories may gain insights into possible turning points, corrections, or key price movements based on the market's historical behavior around these days.

Overall, Gann’s use of specific days was based on his deep belief in the cyclical nature of the market and his attempt to tie those cycles to the natural laws of time, geometry, and astrology. By focusing on these dates, Gann aimed to give traders an edge in predicting significant market events and price shifts.

TASC 2025.01 Linear Predictive Filters█ OVERVIEW

This script implements a suite of tools for identifying and utilizing dominant cycles in time series data, as introduced by John Ehlers in the "Linear Predictive Filters And Instantaneous Frequency" article featured in the January 2025 edition of TASC's Traders' Tips . Dominant cycle information can help traders adapt their indicators and strategies to changing market conditions.

█ CONCEPTS

Conventional technical indicators and strategies often rely on static, unchanging parameters, which may fail to account for the dynamic nature of market data. In his article, John Ehlers applies digital signal processing principles to address this issue, introducing linear predictive filters to identify cyclic information for adapting indicators and strategies to evolving market conditions.

This approach treats market data as a complex series in the time domain. Analyzing the series in the frequency domain reveals information about its cyclic components. To reduce the impact of frequencies outside a range of interest and focus on a specific range of cycles, Ehlers applies second-order highpass and lowpass filters to the price data, which attenuate or remove wavelengths outside the desired range. This band-limited analysis isolates specific parts of the frequency spectrum for various trading styles, e.g., longer wavelengths for position trading or shorter wavelengths for swing trading.

After filtering the series to produce band-limited data, Ehlers applies a linear predictive filter to predict future values a few bars ahead. The filter, calculated based on the techniques proposed by Lloyd Griffiths, adaptively minimizes the error between the latest data point and prediction, successively adjusting its coefficients to align with the band-limited series. The filter's coefficients can then be applied to generate an adaptive estimate of the band-limited data's structure in the frequency domain and identify the dominant cycle.

█ USAGE

This script implements the following tools presented in the article:

Griffiths Predictor

This tool calculates a linear predictive filter to forecast future data points in band-limited price data. The crosses between the prediction and signal lines can provide potential trade signals.

Griffiths Spectrum

This tool calculates a partial frequency spectrum of the band-limited price data derived from the linear predictive filter's coefficients, displaying a color-coded representation of the frequency information in the pane. This mode's display represents the data as a periodogram . The bottom of each plotted bar corresponds to a specific analyzed period (inverse of frequency), and the bar's color represents the presence of that periodic cycle in the time series relative to the one with the highest presence (i.e., the dominant cycle). Warmer, brighter colors indicate a higher presence of the cycle in the series, whereas darker colors indicate a lower presence.

Griffiths Dominant Cycle

This tool compares the cyclic components within the partial spectrum and identifies the frequency with the highest power, i.e., the dominant cycle . Traders can use this dominant cycle information to tune other indicators and strategies, which may help promote better alignment with dynamic market conditions.

Notes on parameters

Bandpass boundaries:

In the article, Ehlers recommends an upper bound of 125 bars or higher to capture longer-term cycles for position trading. He recommends an upper bound of 40 bars and a lower bound of 18 bars for swing trading. If traders use smaller lower bounds, Ehlers advises a minimum of eight bars to minimize the potential effects of aliasing.

Data length:

The Griffiths predictor can use a relatively small data length, as autocorrelation diminishes rapidly with lag. However, for optimal spectrum and dominant cycle calculations, the length must match or exceed the upper bound of the bandpass filter. Ehlers recommends avoiding excessively long lengths to maintain responsiveness to shorter-term cycles.

Liquidity Pools + EQ [LuxAlgo Mod]--- Original Work ---

The original work is licensed under a Attribution-NonCommercial-Share-Alike 4.0 International (CC BY-NC-SA 4.0) creativecommons.org

© LuxAlgo

--- Modifications ---

This script is a modified version of the "Liquidity Pools " indicator.

All modifications are also licensed under CC BY-NC-SA 4.0.

Modified by: on 2025-09-17

Summary of Changes:

- Added a 50% mid-line (Equilibrium) to both Bull and Bear zones.

- Added user options in the settings to toggle the mid-line and adjust its width.

VB Bots Watchlist 2025 — RangesOf course. Here is a complete Pine Script v6 indicator for TradingView that displays the On-Balance Volume (OBV) for a selectable list of the top 50 Binance coins by market capitalization.

You can copy and paste this code directly into your Pine Editor in TradingView.

Key Features:

Pine Script Version 6: Written in the latest version of Pine Script.

Dropdown Menu: Easily select which of the top 50 coins you want to see the OBV for from the indicator's settings.

Independent Data: The OBV is calculated for the selected coin, regardless of the chart you are currently viewing.

Clear Plot: Displays the OBV in a separate pane for easy analysis.

Heikin FlowHeikin Flow

by Ben Deharde, 2025

Overview

Heikin Flow is a trend and momentum oscillator built on a smoothed reverse-Heikin-Ashi baseline. It quantifies the distance between price and this baseline, then colors the histogram to reflect both direction and acceleration/deceleration. Use it standalone to read trend energy and shifts, or pair it with Heikin Rider for momentum-aware breakout confirmation.

What It Does

Computes a reverse-HA baseline and optionally smooths it with a selectable MA.

Plots a histogram of distance (price minus baseline) to visualize directional pressure.

Colors the histogram by trend state (above/below baseline) and momentum (accelerating vs. decelerating).

Provides alerts on zero-line crosses to spotlight potential momentum regime changes.

The histogram also helps to spot divergence between price and momentum (e.g., price making new highs while the histogram weakens).

How It Works

Reverse-HA Baseline

Heikin Flow derives a “reverse close” value from Heikin Ashi context (using prior HA open/close with current bar range) to capture underlying pressure. This value is range-bounded to avoid extremes, then optionally smoothed. The resulting line acts as a soft directional baseline.

Smoothing (Noise Control)

Choose SMA/EMA/HMA/VWMA/RMA and a length to control baseline responsiveness. Shorter lengths react faster, longer lengths emphasize trend consistency by filtering noise—useful when pairing with breakout tools like Rider.

Trend & Momentum Logic

Trend: If price is above the baseline, the environment is considered uptrend; below indicates downtrend.

Momentum: The change in distance bar-to-bar distinguishes acceleration (growing distance) from deceleration (shrinking distance).

This dual readout helps you see not just direction, but the quality of that direction—strong push vs. weakening move.

Coloring (Aligned with Heikin Rider Palette)

Deep Blue: Uptrend & accelerating

Light Blue: Uptrend & decelerating

Deep Red: Downtrend & accelerating

Soft Orange: Downtrend & decelerating

This mirrors the palette logic from Heikin Rider for immediate visual consistency across the suite.

How to use

Read the histogram above/below zero (price–baseline) as directional bias; watch color changes for momentum context.

Use zero-line crosses as momentum regime shifts; confirm with price action or Heikin Rider breakout signals.

Watch for divergence between price action and the histogram as an early clue of weakening moves.

Adjust smoothing method/length to fit your market and timeframe—faster for scalping, slower to highlight sustained trends.

Inputs

Smoothing Type & Length for the baseline (SMA/EMA/HMA/VWMA/RMA)

Info Box toggles (display and formatting)

Live Mode option for real-time vs. confirmed-bar behavior (avoids inadvertent lookahead)

Originality

Heikin Flow adapts the HA-driven methodology to an oscillator that focuses on distance-to-baseline and momentum quality, using a reverse-HA construction and flexible MA smoothing—complementing Heikin Rider’s smoothed HA envelope breakout design for a cohesive, momentum-aware workflow.

Alerts

Bullish Heikin Flow Cross — distance crosses above 0 (on bar close)

Bearish Heikin Flow Cross — distance crosses below 0 (on bar close)

Iani SMC Sniper XAU v2.2 (Long+Short + News Countdown, v6)Iani SMC Sniper v2.6 — Anytime • Auto Pip • FVG 50% • OB • News Panel

Smart-Money Concepts made simple for intraday XAU/USD (works on any symbol).

Finds BOS, 50% FVG “sniper” entries, optional Order Blocks, London H/L, news countdown, and a mini info panel.

What it does

BOS (Break of Structure): detects bullish/bearish BOS after London sweep logic.

FVG 50% entries: plots precise long/short entry dots at the midpoint of the gap.

Auto TP/SL: TP = RR × risk, SL below/above recent swing with a small buffer.

Order Blocks (optional): marks the last opposite candle after BOS and alerts on OB revisit.

London High/Low: tracks session range; session filter is optional.

News countdown: shows next event time and minutes left (user-selectable timezone).

Mini Panel: top-left table with Trend (last BOS), Next news, R:R, Pip size.

Inputs (key)

Auto pip size: uses syminfo.mintick. Manual override available.

Risk:Reward (RR): default 2.0.

Pivot length: swing sensitivity.

Sessions: enable if you want signals only 12:00–20:00 (symbol timezone). Off = anytime.

News timezone: pick your own (e.g., Europe/Brussels, America/New_York).

Absolute & daily times: add your events (strings like 2025-09-17 20:00 or 14:30,16:00…).

Show labels/levels/OBs: toggle on/off.

Alerts included

BOS Bullish / BOS Bearish

BUY Entry / SELL Entry (return to 50% FVG)

Bullish OB revisit / Bearish OB revisit

TP Long/Short reached, SL Long/Short hit

NEWS WARNING (warning window only; does not block signals)

To use: Add Alert → Condition: this indicator → choose any of the alertconditions.

Best use

Bias: H1 for structure.

Execution: M15 (standard) or M5 (aggressive).

Works great on XAUUSD, but is symbol-agnostic (auto pip adapts).

Notes

News times display in the timezone you pick in settings.

OBs are a simple implementation meant for quick visual guidance.

Labels: BUY/SELL near entries, TP/SL on set and when hit, BOS up/down.

Risk disclaimer

This tool is for education only. Not financial advice. Backtest and manage risk.

Reference timesThe theory behind this indicator is that sometimes the graph reaches a certain price at at a certain time according to the price it had at the same time and day in any of the previous weeks. If you could easily see what happened a few weeks ago on this day's weekday and half an hour from now, you might theoretically gain more assurance as to where the graph might go in the next half an hour.

This of course relies of the premise that some traders choose to enter or exit positions according to historical times they are referencing. Hence the name - Reference times.

Example:

it is now 08:00 ET Wednesday. I want to guess what the graph will do in the next half hour. I enter in the indicator the weekday "Wednesday", the time "8:30", and go to 30 minute candles.

I will then see all the candles the graph has been on historical Wednesdays at 8:30. If the candles are below the 08:00 price, we might guess that the graph might want to descent. If they are above the graph, we might guess that the graph might ascend.

How it works:

The user defines a weekday and time he wants to inquire on.

The script searches for past weekdays and similar hours.

It marks these bars at their wicks.

The user can also inquire "opposite hours" - 12 hours ahead or earlier.

The user can also inquire "opposite days" - Monday<->Wednesday, Tuesday<->Thursday.

In addition, the User may inquire the previous day of his selected weekday, which will mark the most recent previous day existent.

Side note: The Time zone offset is set for Jerusalem time. and so it may need future adjustment.

send debugging instances if you find any

Thank you

Assaf Fogelman 2025

Reference TimesThe theory behind this indicator is that sometime the graph will change its direction at a point that is the point it reached at that weekday on that time in the previous weeks. If you can easily see what happened a few weeks ago on this day's weekday and a half an hour from now, you might theoretically gain more assurance as to where the graph might go in the next half an hour.

This of course relies of the premise that some traders choose to enter or exit positions according to historical times they are referencing. Hence the name - Reference times.

Example:

it is now 08:00 ET Wednesday. I want to guess what the graph will do in half an hour. I enter in the indicator the weekday "Wednesday", the time "8:30", and go to 30 minute candles.

I will then see all the candles the graph has been on historical Wednesdays at 8:30. If the candles are below the 08:00 price, we might guess that the graph might want to descent. If they are above the graph, we would guess the graph might want to ascend.

How it works:

The user defines a weekday and time he wants to inquire on.

The script searches for past weekdays and similar hours.

It marks these bars at their wicks.

The user can also inquire "opposite hours" - 12 hours ahead or earlier.

The user can also inquire "opposite days" - Monday<->Wednesday, Tuesday<->Thursday.

In addition, the User may inquire the previous day of his selected weekday, which will mark the most recent previous day existent.

Side note: The Time zone offset is set for Jerusalem time. and so it may need future adjustment.

send debugging instances if you find any

Thank you

Assaf Fogelman 2025

High and Low - MS - 2.0"Showing the high and low points with numbers.

Micha the leftist didn’t say how it’s called in his video.

#LeftismIsAMentalIllness"

נותן לראות את הנקודות הגבוהות והנמוכות עם מספרים

מיכה השמאלן לא אמר איך קוראים לזה בסרטון שלו

#שמאלנותזומחלתנפש

14/09/2025

ICT 00:00, 08:30, 09:30 & 13:30 Opens (NY) — Prior-Day HistoryICT 00:00, 08:30, 09:30 & 13:30 Opens (NY)

This is a derivative of ALPHAICTRADER’s open-source script, republished under the MPL-2.0 with clear attribution and documented changes. It plots four New-York–anchored intraday reference levels—0000, 0830, 0930, 1330—as short, right-padded stubs with clean side labels. Use these time anchors (ICT-style midnight + key US windows) to frame bias, volatility pockets, and intraday trade locations.

What’s original in this version (changes)

Right-padded stubs instead of chart-wide rays — each level ends N bars past the latest candle (configurable).

Side labels at the line tip — text-only labels (0000, 0830, 0930, 1330) that sit at the right end of each stub and update every bar.

Optional prior-day history — show Today only or Today + Prior Day; older lines/labels auto-pruned.

Per-anchor controls — Display, Style, Color, Width, and Show Label for each time.

What it plots (and why)

0000 (NY Midnight): daily session anchor for bias/liquidity context.

0830 (NY): macro data window (CPI/NFP/claims) where volatility often concentrates.

0930 (NY): US cash equity market open; opening-drive structure/acceptance tests.

1330 (NY): early-afternoon anchor for continuation vs. fade.

How it works (under the hood)

Session detection: time("1", session, "America/New_York"); first bar flagged via not na(ts) and na(ts ).

Anchor price: open of that first bar per session/day.

Rendering: lines drawn with xloc=bar_index from start bar to bar_index + Right Pad; x2 updates every bar (no extend.right).

Labels: placed at line.get_x2(line) + Label Pad, soft color variant; updated per bar to stay on the tip.

History: arrays keep either today only or today + yesterday and delete anything older immediately.

How to use

Add to any intraday chart (futures/FX/indices). Anchors are always NY-time; TradingView handles DST.

Inputs

00:00 / 08:30 / 09:30 / 13:30 (NY): Display, Line Style, Color, Width, Show Label

Right Edge: Right Pad (bars) · Label Pad (bars)

History: Show Prior Day (History) — off = today only; on = today + yesterday

Suggested pads: Right Pad 2–5 bars; Label Pad 0–2.

These are context anchors, not signals. Combine with your execution model (market structure, liquidity, FVG/OBs, etc.).

Attribution & License (MPL-2.0)

Original work: “ICT NEW YORK MIDNIGHT OPEN AND 8.30 AM OPEN” by ALPHAICTRADER (MPL-2.0).

This derivative: modifications listed above; source published and kept under MPL-2.0 per license terms.

If you distribute a modified version of this Pine file, you must keep MPL-2.0, retain the copyright/licensing header, publish your modified source, and document your changes.

Notes: Pine v5. Minimalist (no day dividers). Educational tool; not financial advice.

Copyright: © ALPHAICTRADER 2022 · © Funk 2025

License: MPL-2.0

DNSE VN301!, ADX Momentum StrategyDiscover the tailored Pine Script for trading VN30F1M Futures Contracts intraday.

This strategy applies the Statistical Method (IQR) to break down the components of the ADX, calculating the threshold of "normal" momentum fluctuations in price to identify potential breakouts for entry and exit signals. The script automatically closes all positions by 14:30 to avoid overnight holdings.

www.tradingview.com

Settings & Backtest Results:

- Chart: 30-minute timeframe

- Initial capital: VND 100 million

- Position size: 4 contracts per trade (includes trading fees, excludes tax)

- Backtest period: Sep-2021 to Sep-2025

- Return: over 270% (with 5 ticks slippage)

- Trades executed: 1,000+

- Win rate: ~40%

- Profit factor: 1.2

Default Script Settings:

Calculates the acceleration of changes in the +DI and -DI components of the ADX, using IQR to define "normal" momentum fluctuations (adjustable via Lookback period).

Calculates the difference between each bar’s Open and Close prices, using IQR to define "normal" gaps (adjustable via Lookback period).

Entry & Exit Conditions:

Entry Long: Change in +DI or -DI > Avg IQR Value AND Close Price > Previous Close

Exit Long: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI < Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price < Previous Close

Entry Short: Change in +DI or -DI > Avg IQR Value AND Close Price < Previous Close

Exit Short: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI > Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price > Previous Close

Disclaimers:

Trading futures contracts carries a high degree of risk, and price movements can be highly volatile. This script is intended as a reference tool only. It should be used by individuals who fully understand futures trading, have assessed their own risk tolerance, and are knowledgeable about the strategy’s logic.

All investment decisions are the sole responsibility of the user. DNSE bears no liability for any potential losses incurred from applying this strategy in real trading. Past performance does not guarantee future results. Please contact us directly if you have specific questions about this script.

عكفة الماكد المتقدمة - أبو فارس ©// 🔒 Advanced MACD Curve © 2025

// 💡 Idea & Creativity: Engineer Abu Elias

// 🛠️ Development & Implementation: Abu Fares

// 📜 All intellectual rights reserved - Copying, modifying, or redistributing is not permitted

// 🚫 Any attempt to tamper with this code or violate intellectual property rights is legally prohibited

// 📧 For inquiries and licensing: Please contact the developer, Abu Fares

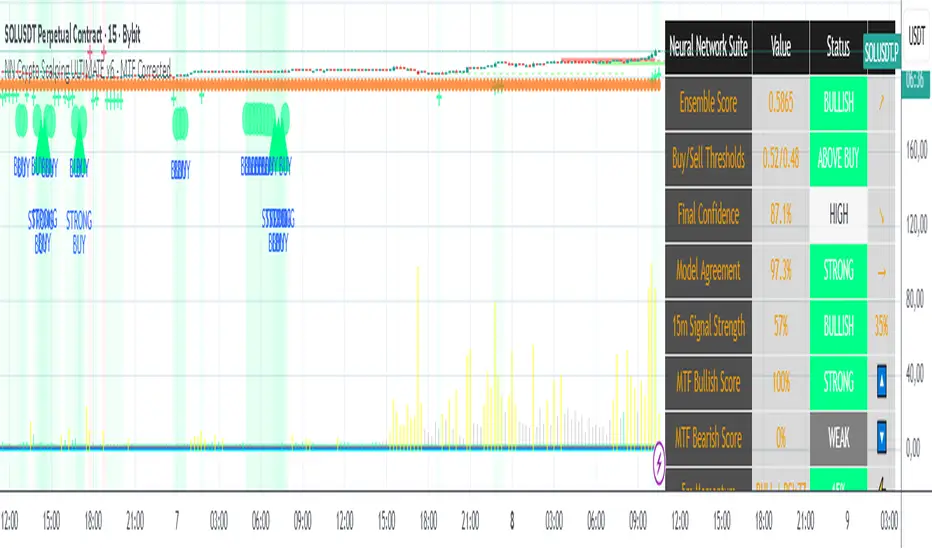

NN Crypto Scalping ULTIMATE v6 - MTF mapercivNeural Network Crypto Trading System v6.1

Complete Technical Documentation

Author

: Neural Network Ensemble Trading System

Version

: 6.1 - MTF Corrected & Bias Fixed

Date

: January 2025

Platform

: TradingView PineScript v6

Executive Summary

The

Neural Network Crypto Trading System v6.1

is an advanced algorithmic trading system that combines three specialized neural networks into an intelligent ensemble to generate cryptocurrency trading signals. The system integrates multi-timeframe analysis, crypto-specific optimizations, dynamic risk management, and continuous learning to maximize performance in highly volatile markets.

Key Features:

Ensemble of 3 specialized Neural Networks

(Primary, Momentum, Volatility)

Multi-Timeframe Analysis

with 5 timeframes (5m, 15m, 1h, 4h, 1D)

22 Advanced Features

for each model

Anti-repainting

guaranteed with confirmed data

8 Market Regime

automatic detections

6 Signal Levels

(Strong/Moderate/Weak Buy/Sell)

Professional dashboard

with 15+ real-time metrics

Intelligent alert system

with webhook integration

Fury by Tetrad on TESLA v2Fury by Tetrad — TSLA v2 (Free Version)

📊 Fury v2 on TSLA — Financial Snapshot

First trade: August 11, 2010

Last trade: September 5, 2025

Net Profit: $10,549.10 (≈ +10,549%)

Gross Profit: $10,554.36

Gross Loss: $5.26

Commission Paid: $86.95

⚖️ Risk/Return Ratios

Sharpe Ratio: 0.42

Sortino Ratio: 17.63

Profit Factor: 2005.38

🔄 Trade Statistics

Total Trades: 37

Winning Trades: 37

Losing Trades: 0

Win Rate: 100%

Fury is a momentum-reversion hybrid designed for Tesla (TSLA) on higher-liquidity timeframes. It combines Bollinger Bands (signal extremes) with RSI (exhaustion filter) to time mean-reversion pops/drops, then exits via price multipliers or optional time-based stops. A Market Direction toggle (Market Neutral / Long Only / Short Only) lets you align with macro bias or risk constraints. Intrabar simulation is enabled for realistic stop/limit behavior, and labeled entries/exits improve visual auditability.

How it works

Entries:

• Long when price pierces lower band and RSI is below the long threshold.

• Short when price pierces upper band and RSI is above the short threshold.

Exits:

• Profit targets via entry×multiplier (independent for long/short).

• Optional price-based stop factors per side.

• Optional time stop (N days) to cap trade duration.

Controls:

• Market Direction switch (Neutral / Long Only / Short Only).

• Tunable BB length/multiplier, RSI length/thresholds, exit multipliers, stops.

Intended use

Swing or position trading TSLA; can be adapted to other high-beta equities with parameter retuning. Use on liquid timeframes and validate with robust out-of-sample testing.

Disclaimers

Backtests are approximations; past performance ≠ future results. Educational use only. Not financial advice.

Stay connected

Follow on TradingView for updates • Telegram: t.me • Website: tetradprotocol.com

Bitcoin Power Law with Cycle BandsBitcoin Power Law with Cycle Bands DescriptionUnlock the power of Bitcoin’s long-term trends with the Bitcoin Power Law with Cycle Bands script, exclusively available through Bitcoin Wealth Edge! This custom TradingView indicator, built for Pine Script v6, models Bitcoin’s price behavior using a 96% R² power law trendline, derived from days since its genesis (January 3, 2009). Designed to predict cycle tops and bottoms, it features:Power Law Trendline: A cyan line representing fair value (e.g., ~$111,000 as of September 2025), based on a logarithmic regression with adjustable coefficients (a = -17.02, b = 5.83).

Cycle Bands: Adjustable red (upper) and green (lower) bands, defaulting to 3.5x and -3.5x multipliers, aligning with historical peaks (e.g., $69K in 2021) and troughs (e.g., $16K in 2022).

Dynamic Labels: Real-time labels displaying fair value, upper limit ($180K), and lower limit ($40K), updated on the last bar for quick insights.

Follow @HodlerRanch

for updates!

FNGAdataDates_Part1FNGAdataDates_Part1 provides historical trading dates for a financial instrument (e.g., FNGA index or related asset) from May 23, 2025, to approximately mid-2021, covering 950 trading days. The dates are organized into 19 chunks (dates_0 to dates_18), each containing 50 timestamps representing trading days (excluding weekends and possibly holidays). This library is part one of a two-part set due to Pine Script token limits and must be used with FNGAdataDates_Part2 for the complete dataset (1,846 dates). It is designed to align with the FNGAopenPrices and FNGAclosePrices libraries for backtesting, technical analysis, or visualization in Pine Script.