Enhanced Retail vs Institutional ActivityThis script highlights market activity in real-time, making it easier to infer the type of market participants driving price and volume changes.

Here’s a list of what the script analyzes:

Volume:

Current volume of the candle.

Moving average of volume over a specified number of periods.

Volume spikes: Current volume compared to a threshold multiple of the moving average.

Price Movement:

Percentage change in price between the current and previous candle.

Identifies significant price changes based on a user-defined threshold.

Institutional Activity:

High volume spikes combined with significant price movements.

Retail Activity:

Periods without volume spikes or significant price changes.

VWAP (Volume-Weighted Average Price):

The average traded price over a specified lookback period, weighted by volume, used as a benchmark.

Market Context Visualization:

Background colors to differentiate institutional (red) and retail (green) activity.

Overlays for:

-Volume bars.

-Average volume line.

-VWAP line.

In summary:

Red = Institutional activity: High volume + significant price change.

Green = Retail activity: Low volume or insignificant price change.

---------------------------------------------------------------------------------------------------------------------

Analysis Explanation:

I’m forecasting that Bitcoin will retest its November 12th low (~$85,098.75) around January 20th, 2025, where the horizontal support line intersects with the downtrend line. This conclusion is based on the following:

Trend Analysis:

The chart shows a clear downtrend with price respecting the descending trendline.

The intersection of the horizontal support and the downtrend line on January 20th indicates a confluence point where price action may gravitate.

Volume and Activity Insights:

Using the Retail vs Institutional Activity indicator, the chart highlights periods dominated by institutional (red background) or retail (green background) activity.

Current price action is in a green zone, suggesting predominantly retail participation with lower volume and insignificant price movements.

Retail vs Institutional Dynamics:

Institutional activity (red zones) aligns with significant price movements and volume spikes, often marking key turning points or trends.

The recent green retail-dominated periods suggest a lack of strong momentum, which may lead to continued price decline until institutions re-enter around the confluence area.

Volume Observations:

Volume remains relatively low during the current retail phase, indicating weak buying pressure.

A potential surge in institutional activity (red zones) near the support level could trigger a rebound or breakdown.

I expect Bitcoin’s price to drop further and test the November 12th low near $85,098.75 on January 20th, 2025. This projection is supported by the convergence of the downtrend line and horizontal support, low retail-driven volume, and historical institutional activity patterns observed using the "Retail vs Institutional Activity" indicator.

Cari dalam skrip untuk "利欧股份2025年第一季度财务报表"

Advanced VWAP CalendarThe Advanced VWAP Calendar is a designed to plot Volume Weighted Average Price (VWAP) lines anchored to user-defined and preset time periods, including weekly, monthly, quarterly, and custom anchors. As of August 15, 2025, this indicator provides traders with a robust tool for analyzing price trends relative to volume-weighted averages, with clear labeling and extensive customization options. Below is a summary of its key features and functionality, with technical details and code references updated to focus on user-facing behavior and presentation, while preserving all other aspects of the original summary.

Key Features

Multiple Time Period VWAPs:

Weekly VWAPs: Supports up to five VWAPs for a user-selected month and year, starting at midnight each Monday (e.g., W1 Aug 2025, W2 Aug 2025). Enabled via a single toggle, with anchors automatically set to the first Monday of the chosen month.

Monthly VWAPs: Plots VWAPs for all 12 months of a selected year (e.g., Jan 2025, Feb 2025) or a single user-specified month/year. Labels use month abbreviations (e.g., "Aug 2025").

Quarterly VWAPs: Covers four quarters of a selected year (e.g., Q1 2025, Q2 2025), with options to enable all quarters or individual ones (Q1–Q4).

Legacy VWAPs: Provides monthly and quarterly VWAPs for a user-selected legacy year (e.g., 2024), labeled with a "Legacy" prefix (e.g., "Legacy Jan 2024," "Legacy Q1 2024"), with similar enablement options.

Custom VWAPs: Includes 10 fully customizable VWAPs, each with user-defined anchor times, labels (e.g., "Q1 2025"), colors, line widths (1–5), text colors, bubble styles, text sizes (8–40), and background options.

Clear and Dynamic Labeling:

Labels appear to the right of the chart, showing the VWAP value (e.g., "Q1 2025 123.45").

Weekly labels follow a "W# Month Year" format (e.g., "W1 Aug 2025").

Monthly labels use abbreviated months (e.g., "Aug 2025"), while quarterly labels use "Q# Year" (e.g., "Q3 2025").

Legacy labels include a "Legacy" prefix (e.g., "Legacy Q1 2024").

Labels support customizable text sizes (tiny to huge) and can be displayed with or without a background, with optional bubble styles.

Flexible Customization:

Each VWAP can be enabled or disabled independently, with user inputs for anchor times, labels, and visual properties.

Colors are predefined for weekly (red, orange, blue, green, purple), monthly (varied), quarterly (red, blue, green, yellow), and legacy VWAPs, but custom VWAPs allow any color selection.

Line widths and text sizes are adjustable, ensuring visual clarity and chart readability.

This indicator was a dual effort, code was heavily contributed in effort by AzDxB, major credit and THANKS goes to him www.tradingview.com

Boilerplate Configurable Strategy [Yosiet]This is a Boilerplate Code!

Hello! First of all, let me introduce myself a little bit. I don't come from the world of finance, but from the world of information and communication technologies (ICT) where we specialize in data processing with the aim of automating it and eliminating all human factors and actors in the processes. You could say that I am an algotrader.

That said, in my journey through trading in recent years I have understood that this world is often shown to be incomplete. All those who want to learn about trading only end up learning a small part of what it really entails, they only seek to learn how to read candlesticks. Therefore, I want to share with the entire community a fraction of what I have really understood it to be.

As a computer scientist, the most important thing is the data, it is the raw material of our work and without data you simply cannot do anything. Entropy is simple: Data in -> Data is transformed -> Data out.

The quality of the outgoing data will directly depend on the incoming data, there is no greater mystery or magic in the process. In trading it is no different, because at the end of the day it is nothing more than data. As we often say, if garbage comes in, garbage comes out.

Most people focus on the results only, on the outgoing data, because in the end we all want the same thing, to make easy money. Very few pay attention to the input data, much less to the process.

Now, I am not here to delude you, because there is no bigger lie than easy money, but I am here to give you a boilerplate code that will help you create strategies where you only have to concentrate on the quality of the incoming data.

To the Point

The code is a strategy boilerplate that applies the technique that you decide to customize for the criteria for opening a position. It already has the other factors involved in trading programmed and automated.

1. The Entry

This section of the boilerplate is the one that each individual must customize according to their needs and knowledge. The code is offered with two simple, well-known strategies to exemplify how the code can be reused for your own benefits.

For the purposes of this post on tradingview, I am going to use the simplest of the known strategies in trading for entries: SMA Crossing

// SMA Cross Settings

maFast = ta.sma(close, length)

maSlow = ta.sma(open, length)

The Strategy Properties for all cases published here:

For Stock TSLA H1 From 01/01/2025 To 02/15/2025

For Crypto XMR-USDT 30m From 01/01/2025 To 02/15/2025

For Forex EUR-USD 5m From 01/01/2025 To 02/15/2025

But the goal of this post is not to sell you a dream, else to show you that the same Entry decision works very well for some and does not for others and with this boilerplate code you only have to think of entries, not exits.

2. Schedules, Days, Sessions

As you know, there are an infinite number of markets that are susceptible to the sessions of each country and the news that they announce during those sessions, so the code already offers parameters so that you can condition the days and hours of operation, filter the best time parameters for a specific market and time frame.

3. Data Filtering

The data offered in trading are numerical series presented in vectors on a time axis where an endless number of mathematical equations can be applied to process them, with matrix calculation and non-linear regressions being the best, in my humble opinion.

4. Read Fundamental Macroeconomic Events, News

The boilerplate has integration with the tradingview SDK to detect when news will occur and offers parameters so that you can enable an exclusion time margin to not operate anything during that time window.

5. Direction and Sense

In my experience I have found the peculiarity that the same algorithm works very well for a market in a time frame, but for the same market in another time frame it is only a waste of time and money. So now you can easily decide if you only want to open LONG, SHORT or both side positions and know how effective your strategy really is.

6. Reading the money, THE PURPOSE OF EVERYTHING

The most important section in trading and the reason why many clients usually hire me as a financial programmer, is reading and controlling the money, because in the end everyone wants to win and no one wants to lose. Now they can easily parameterize how the money should flow and this is the genius of this boilerplate, because it is what will really decide if an algorithm (Indicator: A bunch of math equations) for entries will really leave you good money over time.

7. Managing the Risk, The Ego Destroyer

Many trades, little money. Most traders focus on making money and none of them know about statistics and the few who do know something about it, only focus on the winrate. Well, with this code you can unlock what really matters, the true success criteria to be able to live off of trading: Profit Factor, Sortino Ratio, Sharpe Ratio and most importantly, will you really make money?

8. Managing Emotions

Finally, the main reason why many lose money is because they are very bad at managing their emotions, because with this they will no longer need to do so because the boilerplate has already programmed criteria to chase the price in a position, cut losses and maximize profits.

In short, this is a boilerplate code that already has the data processing and data output ready, you only have to worry about the data input.

“And so the trader learned: the greatest edge was not in predicting the storm, but in building a boat that could not sink.”

DISCLAIMER

This post is intended for programmers and quantitative traders who already have a certain level of knowledge and experience. It is not intended to be financial advice or to sell you any money-making script, if you use it, you do so at your own risk.

Dskyz (DAFE) Adaptive Regime - Quant Machine ProDskyz (DAFE) Adaptive Regime - Quant Machine Pro:

Buckle up for the Dskyz (DAFE) Adaptive Regime - Quant Machine Pro, is a strategy that’s your ultimate edge for conquering futures markets like ES, MES, NQ, and MNQ. This isn’t just another script—it’s a quant-grade powerhouse, crafted with precision to adapt to market regimes, deliver multi-factor signals, and protect your capital with futures-tuned risk management. With its shimmering DAFE visuals, dual dashboards, and glowing watermark, it turns your charts into a cyberpunk command center, making trading as thrilling as it is profitable.

Unlike generic scripts clogging up the space, the Adaptive Regime is a DAFE original, built from the ground up to tackle the chaos of futures trading. It identifies market regimes (Trending, Range, Volatile, Quiet) using ADX, Bollinger Bands, and HTF indicators, then fires trades based on a weighted scoring system that blends candlestick patterns, RSI, MACD, and more. Add in dynamic stops, trailing exits, and a 5% drawdown circuit breaker, and you’ve got a system that’s as safe as it is aggressive. Whether you’re a newbie or a prop desk pro, this strat’s your ticket to outsmarting the markets. Let’s break down every detail and see why it’s a must-have.

Why Traders Need This Strategy

Futures markets are a gauntlet—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional traps that punish the unprepared. Meanwhile, platforms are flooded with low-effort scripts that recycle old ideas with zero innovation. The Adaptive Regime stands tall, offering:

Adaptive Intelligence: Detects market regimes (Trending, Range, Volatile, Quiet) to optimize signals, unlike one-size-fits-all scripts.

Multi-Factor Precision: Combines candlestick patterns, MA trends, RSI, MACD, volume, and HTF confirmation for high-probability trades.

Futures-Optimized Risk: Calculates position sizes based on $ risk (default: $300), with ATR or fixed stops/TPs tailored for ES/MES.

Bulletproof Safety: 5% daily drawdown circuit breaker and trailing stops keep your account intact, even in chaos.

DAFE Visual Mastery: Pulsing Bollinger Band fills, dynamic SL/TP lines, and dual dashboards (metrics + position) make signals crystal-clear and charts a work of art.

Original Craftsmanship: A DAFE creation, built with community passion, not a rehashed clone of generic code.

Traders need this because it’s a complete, adaptive system that blends quant smarts, user-friendly design, and DAFE flair. It’s your edge to trade with confidence, cut through market noise, and leave the copycats in the dust.

Strategy Components

1. Market Regime Detection

The strategy’s brain is its ability to classify market conditions into five regimes, ensuring signals match the environment.

How It Works:

Trending (Regime 1): ADX > 20, fast/slow EMA spread > 0.3x ATR, HTF RSI > 50 or MACD bullish (htf_trend_bull/bear).

Range (Regime 2): ADX < 25, price range < 3% of close, no HTF trend.

Volatile (Regime 3): BB width > 1.5x avg, ATR > 1.2x avg, HTF RSI overbought/oversold.

Quiet (Regime 4): BB width < 0.8x avg, ATR < 0.9x avg.

Other (Regime 5): Default for unclear conditions.

Indicators: ADX (14), BB width (20), ATR (14, 50-bar SMA), HTF RSI (14, daily default), HTF MACD (12,26,9).

Why It’s Brilliant:

Regime detection adapts signals to market context, boosting win rates in trending or volatile conditions.

HTF RSI/MACD add a big-picture filter, rare in basic scripts.

Visualized via gradient background (green for Trending, orange for Range, red for Volatile, gray for Quiet, navy for Other).

2. Multi-Factor Signal Scoring

Entries are driven by a weighted scoring system that combines candlestick patterns, trend, momentum, and volume for robust signals.

Candlestick Patterns:

Bullish: Engulfing (0.5), hammer (0.4 in Range, 0.2 else), morning star (0.2), piercing (0.2), double bottom (0.3 in Volatile, 0.15 else). Must be near support (low ≤ 1.01x 20-bar low) with volume spike (>1.5x 20-bar avg).

Bearish: Engulfing (0.5), shooting star (0.4 in Range, 0.2 else), evening star (0.2), dark cloud (0.2), double top (0.3 in Volatile, 0.15 else). Must be near resistance (high ≥ 0.99x 20-bar high) with volume spike.

Logic: Patterns are weighted higher in specific regimes (e.g., hammer in Range, double bottom in Volatile).

Additional Factors:

Trend: Fast EMA (20) > slow EMA (50) + 0.5x ATR (trend_bull, +0.2); opposite for trend_bear.

RSI: RSI (14) < 30 (rsi_bull, +0.15); > 70 (rsi_bear, +0.15).

MACD: MACD line > signal (12,26,9, macd_bull, +0.15); opposite for macd_bear.

Volume: ATR > 1.2x 50-bar avg (vol_expansion, +0.1).

HTF Confirmation: HTF RSI < 70 and MACD bullish (htf_bull_confirm, +0.2); RSI > 30 and MACD bearish (htf_bear_confirm, +0.2).

Scoring:

bull_score = sum of bullish factors; bear_score = sum of bearish. Entry requires score ≥ 1.0.

Example: Bullish engulfing (0.5) + trend_bull (0.2) + rsi_bull (0.15) + htf_bull_confirm (0.2) = 1.05, triggers long.

Why It’s Brilliant:

Multi-factor scoring ensures signals are confirmed by multiple market dynamics, reducing false positives.

Regime-specific weights make patterns more relevant (e.g., hammers shine in Range markets).

HTF confirmation aligns with the big picture, a quant edge over simplistic scripts.

3. Futures-Tuned Risk Management

The risk system is built for futures, calculating position sizes based on $ risk and offering flexible stops/TPs.

Position Sizing:

Logic: Risk per trade (default: $300) ÷ (stop distance in points * point value) = contracts, capped at max_contracts (default: 5). Point value = tick value (e.g., $12.5 for ES) * ticks per point (4) * contract multiplier (1 for ES, 0.1 for MES).

Example: $300 risk, 8-point stop, ES ($50/point) → 0.75 contracts, rounded to 1.

Impact: Precise sizing prevents over-leverage, critical for micro contracts like MES.

Stops and Take-Profits:

Fixed: Default stop = 8 points, TP = 16 points (2:1 reward/risk).

ATR-Based: Stop = 1.5x ATR (default), TP = 3x ATR, enabled via use_atr_for_stops.

Logic: Stops set at swing low/high ± stop distance; TPs at 2x stop distance from entry.

Impact: ATR stops adapt to volatility, while fixed stops suit stable markets.

Trailing Stops:

Logic: Activates at 50% of TP distance. Trails at close ± 1.5x ATR (atr_multiplier). Longs: max(trail_stop_long, close - ATR * 1.5); shorts: min(trail_stop_short, close + ATR * 1.5).

Impact: Locks in profits during trends, a game-changer in volatile sessions.

Circuit Breaker:

Logic: Pauses trading if daily drawdown > 5% (daily_drawdown = (max_equity - equity) / max_equity).

Impact: Protects capital during black swan events (e.g., April 27, 2025 ES slippage).

Why It’s Brilliant:

Futures-specific inputs (tick value, multiplier) make it plug-and-play for ES/MES.

Trailing stops and circuit breaker add pro-level safety, rare in off-the-shelf scripts.

Flexible stops (ATR or fixed) suit different trading styles.

4. Trade Entry and Exit Logic

Entries and exits are precise, driven by bull_score/bear_score and protected by drawdown checks.

Entry Conditions:

Long: bull_score ≥ 1.0, no position (position_size <= 0), drawdown < 5% (not pause_trading). Calculates contracts, sets stop at swing low - stop points, TP at 2x stop distance.

Short: bear_score ≥ 1.0, position_size >= 0, drawdown < 5%. Stop at swing high + stop points, TP at 2x stop distance.

Logic: Tracks entry_regime for PNL arrays. Closes opposite positions before entering.

Exit Conditions:

Stop-Loss/Take-Profit: Hits stop or TP (strategy.exit).

Trailing Stop: Activates at 50% TP, trails by ATR * 1.5.

Emergency Exit: Closes if price breaches stop (close < long_stop_price or close > short_stop_price).

Reset: Clears stop/TP prices when flat (position_size = 0).

Why It’s Brilliant:

Score-based entries ensure multi-factor confirmation, filtering out weak signals.

Trailing stops maximize profits in trends, unlike static exits in basic scripts.

Emergency exits add an extra safety layer, critical for futures volatility.

5. DAFE Visuals

The visuals are pure DAFE magic, blending function with cyberpunk flair to make signals intuitive and charts stunning.

Shimmering Bollinger Band Fill:

Display: BB basis (20, white), upper/lower (green/red, 45% transparent). Fill pulses (30–50 alpha) by regime, with glow (60–95 alpha) near bands (close ≥ 0.995x upper or ≤ 1.005x lower).

Purpose: Highlights volatility and key levels with a futuristic glow.

Visuals make complex regimes and signals instantly clear, even for newbies.

Pulsing effects and regime-specific colors add a DAFE signature, setting it apart from generic scripts.

BB glow emphasizes tradeable levels, enhancing decision-making.

Chart Background (Regime Heatmap):

Green — Trending Market: Strong, sustained price movement in one direction. The market is in a trend phase—momentum follows through.

Orange — Range-Bound: Market is consolidating or moving sideways, with no clear up/down trend. Great for mean reversion setups.

Red — Volatile Regime: High volatility, heightened risk, and larger/faster price swings—trade with caution.

Gray — Quiet/Low Volatility: Market is calm and inactive, with small moves—often poor conditions for most strategies.

Navy — Other/Neutral: Regime is uncertain or mixed; signals may be less reliable.

Bollinger Bands Glow (Dynamic Fill):

Neon Red Glow — Warning!: Price is near or breaking above the upper band; momentum is overstretched, watch for overbought conditions or reversals.

Bright Green Glow — Opportunity!: Price is near or breaking below the lower band; market could be oversold, prime for bounce or reversal.

Trend Green Fill — Trending Regime: Fills between bands with green when the market is trending, showing clear momentum.

Gold/Yellow Fill — Range Regime: Fills with gold/aqua in range conditions, showing the market is sideways/oscillating.

Magenta/Red Fill — Volatility Spike: Fills with vivid magenta/red during highly volatile regimes.

Blue Fill — Neutral/Quiet: A soft blue glow for other or uncertain market states.

Moving Averages:

Display: Blue fast EMA (20), red slow EMA (50), 2px.

Purpose: Shows trend direction, with trend_dir requiring ATR-scaled spread.

Dynamic SL/TP Lines:

Display: Pulsing colors (red SL, green TP for Trending; yellow/orange for Range, etc.), 3px, with pulse_alpha for shimmer.

Purpose: Tracks stops/TPs in real-time, color-coded by regime.

6. Dual Dashboards

Two dashboards deliver real-time insights, making the strat a quant command center.

Bottom-Left Metrics Dashboard (2x13):

Metrics: Mode (Active/Paused), trend (Bullish/Bearish/Neutral), ATR, ATR avg, volume spike (YES/NO), RSI (value + Oversold/Overbought/Neutral), HTF RSI, HTF trend, last signal (Buy/Sell/None), regime, bull score.

Display: Black (29% transparent), purple title, color-coded (green for bullish, red for bearish).

Purpose: Consolidates market context and signal strength.

Top-Right Position Dashboard (2x7):

Metrics: Regime, position side (Long/Short/None), position PNL ($), SL, TP, daily PNL ($).

Display: Black (29% transparent), purple title, color-coded (lime for Long, red for Short).

Purpose: Tracks live trades and profitability.

Why It’s Brilliant:

Dual dashboards cover market context and trade status, a rare feature.

Color-coding and concise metrics guide beginners (e.g., green “Buy” = go).

Real-time PNL and SL/TP visibility empower disciplined trading.

7. Performance Tracking

Logic: Arrays (regime_pnl_long/short, regime_win/loss_long/short) track PNL and win/loss by regime (1–5). Updated on trade close (barstate.isconfirmed).

Purpose: Prepares for future adaptive thresholds (e.g., adjust bull_score min based on regime performance).

Why It’s Brilliant: Lays the groundwork for self-optimizing logic, a quant edge over static scripts.

Key Features

Regime-Adaptive: Optimizes signals for Trending, Range, Volatile, Quiet markets.

Futures-Optimized: Precise sizing for ES/MES with tick-based risk inputs.

Multi-Factor Signals: Candlestick patterns, RSI, MACD, and HTF confirmation for robust entries.

Dynamic Exits: ATR/fixed stops, 2:1 TPs, and trailing stops maximize profits.

Safe and Smart: 5% drawdown breaker and emergency exits protect capital.

DAFE Visuals: Shimmering BB fill, pulsing SL/TP, and dual dashboards.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

How to Use

Add to Chart: Load on a 5min ES/MES chart in TradingView.

Configure Inputs: Set instrument (ES/MES), tick value ($12.5/$1.25), multiplier (1/0.1), risk ($300 default). Enable ATR stops for volatility.

Monitor Dashboards: Bottom-left for regime/signals, top-right for position/PNL.

Backtest: Run in strategy tester to compare regimes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see regime shifts and stops.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance does not guarantee future results. Backtest results may differ from live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Slippage: 3

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Adaptive Regime - Quant Machine Pro is more than a strategy—it’s a revolution. Crafted with DAFE’s signature precision, it rises above generic scripts with adaptive regimes, quant-grade signals, and visuals that make trading a thrill. Whether you’re scalping MES or swinging ES, this system empowers you to navigate markets with confidence and style. Join the DAFE crew, light up your charts, and let’s dominate the futures game!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Dskyz (DAFE) Aurora Divergence – Quant Master Dskyz (DAFE) Aurora Divergence – Quant Master

Introducing the Dskyz (DAFE) Aurora Divergence – Quant Master , a strategy that’s your secret weapon for mastering futures markets like MNQ, NQ, MES, and ES. Born from the legendary Aurora Divergence indicator, this fully automated system transforms raw divergence signals into a quant-grade trading machine, blending precision, risk management, and cyberpunk DAFE visuals that make your charts glow like a neon skyline. Crafted with care and driven by community passion, this strategy stands out in a sea of generic scripts, offering traders a unique edge to outsmart institutional traps and navigate volatile markets.

The Aurora Divergence indicator was a cult favorite for spotting price-OBV divergences with its aqua and fuchsia orbs, but traders craved a system to act on those signals with discipline and automation. This strategy delivers, layering advanced filters (z-score, ATR, multi-timeframe, session), dynamic risk controls (kill switches, adaptive stops/TPs), and a real-time dashboard to turn insights into profits. Whether you’re a newbie dipping into futures or a pro hunting reversals, this strat’s got your back with a beginner guide, alerts, and visuals that make trading feel like a sci-fi mission. Let’s dive into every detail and see why this original DAFE creation is a must-have.

Why Traders Need This Strategy

Futures markets are a battlefield—fast-paced, volatile, and riddled with institutional games that can wipe out undisciplined traders. From the April 28, 2025 NQ 1k-point drop to sneaky ES slippage, the stakes are high. Meanwhile, platforms are flooded with unoriginal, low-effort scripts that promise the moon but deliver noise. The Aurora Divergence – Quant Master rises above, offering:

Unmatched Originality: A bespoke system built from the ground up, with custom divergence logic, DAFE visuals, and quant filters that set it apart from copycat clutter.

Automation with Precision: Executes trades on divergence signals, eliminating emotional slip-ups and ensuring consistency, even in chaotic sessions.

Quant-Grade Filters: Z-score, ATR, multi-timeframe, and session checks filter out noise, targeting high-probability reversals.

Robust Risk Management: Daily loss and rolling drawdown kill switches, plus ATR-based stops/TPs, protect your capital like a fortress.

Stunning DAFE Visuals: Aqua/fuchsia orbs, aurora bands, and a glowing dashboard make signals intuitive and charts a work of art.

Community-Driven: Evolved from trader feedback, this strat’s a labor of love, not a recycled knockoff.

Traders need this because it’s a complete, original system that blends accessibility, sophistication, and style. It’s your edge to trade smarter, not harder, in a market full of traps and imitators.

1. Divergence Detection (Core Signal Logic)

The strategy’s core is its ability to detect bullish and bearish divergences between price and On-Balance Volume (OBV), pinpointing reversals with surgical accuracy.

How It Works:

Price Slope: Uses linear regression over a lookback (default: 9 bars) to measure price momentum (priceSlope).

OBV Slope: OBV tracks volume flow (+volume if price rises, -volume if falls), with its slope calculated similarly (obvSlope).

Bullish Divergence: Price slope negative (falling), OBV slope positive (rising), and price above 50-bar SMA (trend_ma).

Bearish Divergence: Price slope positive (rising), OBV slope negative (falling), and price below 50-bar SMA.

Smoothing: Requires two consecutive divergence bars (bullDiv2, bearDiv2) to confirm signals, reducing false positives.

Strength: Divergence intensity (divStrength = |priceSlope * obvSlope| * sensitivity) is normalized (0–1, divStrengthNorm) for visuals.

Why It’s Brilliant:

- Divergences catch hidden momentum shifts, often exploited by institutions, giving you an edge on reversals.

- The 50-bar SMA filter aligns signals with the broader trend, avoiding choppy markets.

- Adjustable lookback (min: 3) and sensitivity (default: 1.0) let you tune for different instruments or timeframes.

2. Filters for Precision

Four advanced filters ensure signals are high-probability and market-aligned, cutting through the noise of volatile futures.

Z-Score Filter:

Logic: Calculates z-score ((close - SMA) / stdev) over a lookback (default: 50 bars). Blocks entries if |z-score| > threshold (default: 1.5) unless disabled (useZFilter = false).

Impact: Avoids trades during extreme price moves (e.g., blow-off tops), keeping you in statistically safe zones.

ATR Percentile Volatility Filter:

Logic: Tracks 14-bar ATR in a 100-bar window (default). Requires current ATR > 80th percentile (percATR) to trade (tradeOk).

Impact: Ensures sufficient volatility for meaningful moves, filtering out low-volume chop.

Multi-Timeframe (HTF) Trend Filter:

Logic: Uses a 50-bar SMA on a higher timeframe (default: 60min). Longs require price > HTF MA (bullTrendOK), shorts < HTF MA (bearTrendOK).

Impact: Aligns trades with the bigger trend, reducing counter-trend losses.

US Session Filter:

Logic: Restricts trading to 9:30am–4:00pm ET (default: enabled, useSession = true) using America/New_York timezone.

Impact: Focuses on high-liquidity hours, avoiding overnight spreads and erratic moves.

Evolution:

- These filters create a robust signal pipeline, ensuring trades are timed for optimal conditions.

- Customizable inputs (e.g., zThreshold, atrPercentile) let traders adapt to their style without compromising quality.

3. Risk Management

The strategy’s risk controls are a masterclass in balancing aggression and safety, protecting capital in volatile markets.

Daily Loss Kill Switch:

Logic: Tracks daily loss (dayStartEquity - strategy.equity). Halts trading if loss ≥ $300 (default) and enabled (killSwitch = true, killSwitchActive).

Impact: Caps daily downside, crucial during events like April 27, 2025 ES slippage.

Rolling Drawdown Kill Switch:

Logic: Monitors drawdown (rollingPeak - strategy.equity) over 100 bars (default). Stops trading if > $1000 (rollingKill).

Impact: Prevents prolonged losing streaks, preserving capital for better setups.

Dynamic Stop-Loss and Take-Profit:

Logic: Stops = entry ± ATR * multiplier (default: 1.0x, stopDist). TPs = entry ± ATR * 1.5x (profitDist). Longs: stop below, TP above; shorts: vice versa.

Impact: Adapts to volatility, keeping stops tight but realistic, with TPs targeting 1.5:1 reward/risk.

Max Bars in Trade:

Logic: Closes trades after 8 bars (default) if not already exited.

Impact: Frees capital from stagnant trades, maintaining efficiency.

Kill Switch Buffer Dashboard:

Logic: Shows smallest buffer ($300 - daily loss or $1000 - rolling DD). Displays 0 (red) if kill switch active, else buffer (green).

Impact: Real-time risk visibility, letting traders adjust dynamically.

Why It’s Brilliant:

- Kill switches and ATR-based exits create a safety net, rare in generic scripts.

- Customizable risk inputs (maxDailyLoss, dynamicStopMult) suit different account sizes.

- Buffer metric empowers disciplined trading, a DAFE signature.

4. Trade Entry and Exit Logic

The entry/exit rules are precise, filtered, and adaptive, ensuring trades are deliberate and profitable.

Entry Conditions:

Long Entry: bullDiv2, cooldown passed (canSignal), ATR filter passed (tradeOk), in US session (inSession), no kill switches (not killSwitchActive, not rollingKill), z-score OK (zOk), HTF trend bullish (bullTrendOK), no existing long (lastDirection != 1, position_size <= 0). Closes shorts first.

Short Entry: Same, but for bearDiv2, bearTrendOK, no long (lastDirection != -1, position_size >= 0). Closes longs first.

Adaptive Cooldown: Default 2 bars (cooldownBars). Doubles (up to 10) after a losing trade, resets after wins (dynamicCooldown).

Exit Conditions:

Stop-Loss/Take-Profit: Set per trade (ATR-based). Exits on stop/TP hits.

Other Exits: Closes if maxBarsInTrade reached, ATR filter fails, or kill switch activates.

Position Management: Ensures no conflicting positions, closing opposites before new entries.

Built To Be Reliable and Consistent:

- Multi-filtered entries minimize false signals, a stark contrast to basic scripts.

- Adaptive cooldown prevents overtrading, especially after losses.

- Clean position handling ensures smooth execution, even in fast markets.

5. DAFE Visuals

The visuals are a DAFE hallmark, blending function with clean flair to make signals intuitive and charts stunning.

Aurora Bands:

Display: Bands around price during divergences (bullish: below low, bearish: above high), sized by ATR * bandwidth (default: 0.5).

Colors: Aqua (bullish), fuchsia (bearish), with transparency tied to divStrengthNorm.

Purpose: Highlights divergence zones with a glowing, futuristic vibe.

Divergence Orbs:

Display: Large/small circles (aqua below for bullish, fuchsia above for bearish) when bullDiv2/bearDiv2 and canSignal. Labels show strength (0–1).

Purpose: Pinpoints entries with eye-catching clarity.

Gradient Background:

Display: Green (bullish), red (bearish), or gray (neutral), 90–95% transparent.

Purpose: Sets the market mood without clutter.

Strategy Plots:

- Stop/TP Lines: Red (stops), green (TPs) for active trades.

- HTF MA: Yellow line for trend context.

- Z-Score: Blue step-line (if enabled).

- Kill Switch Warning: Red background flash when active.

What Makes This Next-Level?:

- Visuals make complex signals (divergences, filters) instantly clear, even for beginners.

- DAFE’s unique aesthetic (orbs, bands) sets it apart from generic scripts, reinforcing originality.

- Functional plots (stops, TPs) enhance trade management.

6. Metrics Dashboard

The top-right dashboard (2x8 table) is your command center, delivering real-time insights.

Metrics:

Daily Loss ($): Current loss vs. day’s start, red if > $300.

Rolling DD ($): Drawdown vs. 100-bar peak, red if > $1000.

ATR Threshold: Current percATR, green if ATR exceeds, red if not.

Z-Score: Current value, green if within threshold, red if not.

Signal: “Bullish Div” (aqua), “Bearish Div” (fuchsia), or “None” (gray).

Action: “Consider Buying”/“Consider Selling” (signal color) or “Wait” (gray).

Kill Switch Buffer ($): Smallest buffer to kill switch, green if > 0, red if 0.

Why This Is Important?:

- Consolidates critical data, making decisions effortless.

- Color-coded metrics guide beginners (e.g., green action = go).

- Buffer metric adds transparency, rare in off-the-shelf scripts.

7. Beginner Guide

Beginner Guide: Middle-right table (shown once on chart load), explains aqua orbs (bullish, buy) and fuchsia orbs (bearish, sell).

Key Features:

Futures-Optimized: Tailored for MNQ, NQ, MES, ES with point-value adjustments.

Highly Customizable: Inputs for lookback, sensitivity, filters, and risk settings.

Real-Time Insights: Dashboard and visuals update every bar.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

User-Friendly: Guide, visuals, and dashboard make it accessible yet powerful.

Original Design: DAFE’s unique logic and visuals stand out from generic scripts.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Configure Inputs: Adjust instrument, filters, or risk (defaults optimized for MNQ).

Monitor Dashboard: Watch signals, actions, and risk metrics (top-right).

Backtest: Run in strategy tester to evaluate performance.

Live Trade: Connect to a broker (e.g., Tradovate) for automation. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Use bar replay (e.g., April 28, 2025 NQ drop) to test volatility handling.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Backtest results may not reflect live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Aurora Divergence – Quant Master isn’t just a strategy—it’s a movement. Crafted with originality and driven by community passion, it rises above the flood of generic scripts to deliver a system that’s as powerful as it is beautiful. With its quant-grade logic, DAFE visuals, and robust risk controls, it empowers traders to tackle futures with confidence and style. Join the DAFE crew, light up your charts, and let’s outsmart the markets together!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

Dskyz (DAFE) Quantum Sentiment Flux - Beginners Dskyz (DAFE) Quantum Sentiment Flux - Beginners:

Welcome to the Dskyz (DAFE) Quantum Sentiment Flux - Beginners , a strategy and concept that’s your ultimate wingman for trading futures like MNQ, NQ, MES, and ES. This gem combines lightning-fast momentum signals, market sentiment smarts, and bulletproof risk management into a system so intuitive, even newbies can trade like pros. With clean DAFE visuals, preset modes for every vibe, and a revamped dashboard that’s basically a market GPS, this strategy makes futures trading feel like a high-octane sci-fi mission.

Built on the Dskyz (DAFE) legacy of Aurora Divergence, the Quantum Sentiment Flux is designed to empower beginners while giving seasoned traders a lean, sentiment-driven edge. It uses fast/slow EMA crossovers for entries, filters trades with VIX, SPX trends, and sector breadth, and keeps your account safe with adaptive stops and cooldowns. Tuned for more action with faster signals and a slick bottom-left dashboard, this updated version is ready to light up your charts and outsmart institutional traps. Let’s dive into why this strat’s a must-have and break down its brilliance.

Why Traders Need This Strategy

Futures markets are a wild ride—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional games that can wreck unprepared traders. Beginners often get lost in complex systems or burned by impulsive trades. The Quantum Sentiment Flux is the antidote, offering:

Dead-Simple Setup: Preset modes (Aggressive, Balanced, Conservative) auto-tune signals, risk, and sizing, so you can trade without a quant degree.

Sentiment Superpower: VIX filter, SPX trend, and sector breadth visuals keep you aligned with market health, dodging chop and riding trends.

Ironclad Safety: Tighter ATR-based stops, 2:1 take-profits, and preset cooldowns protect your capital, even in chaotic sessions.

Next-Level Visuals: Green/red entry triangles, vibrant EMAs, a sector breadth background, and a beefed-up dashboard make signals and context pop.

DAFE Swagger: The clean aesthetics, sleek dashboard—ties it to Dskyz’s elite brand, making your charts a work of art.

Traders need this because it’s a plug-and-play system that blends beginner-friendly simplicity with pro-level market awareness. Whether you’re just starting or scalping 5min MNQ, this strat’s your key to trading with confidence and style.

Strategy Components

1. Core Signal Logic (High-Speed Momentum)

The strategy’s engine is a momentum-based system using fast and slow Exponential Moving Averages (EMAs), now tuned for faster, more frequent trades.

How It Works:

Fast/Slow EMAs: Fast EMA (Aggressive: 5, Balanced: 7, Conservative: 9 bars) and slow EMA (12/14/18 bars) track short-term vs. longer-term momentum.

Crossover Signals:

Buy: Fast EMA crosses above slow EMA, and trend_dir = 1 (fast EMA > slow EMA + ATR * strength threshold).

Sell: Fast EMA crosses below slow EMA, and trend_dir = -1 (fast EMA < slow EMA - ATR * strength threshold).

Strength Filter: ma_strength = fast EMA - slow EMA must exceed an ATR-scaled threshold (Aggressive: 0.15, Balanced: 0.18, Conservative: 0.25) for robust signals.

Trend Direction: trend_dir confirms momentum, filtering out weak crossovers in choppy markets.

Evolution:

Faster EMAs (down from 7–10/21–50) catch short-term trends, perfect for active futures markets.

Lower strength thresholds (0.15–0.25 vs. 0.3–0.5) make signals more sensitive, boosting trade frequency without sacrificing quality.

Preset tuning ensures beginners get optimized settings, while pros can tweak via mode selection.

2. Market Sentiment Filters

The strategy leans hard into market sentiment with a VIX filter, SPX trend analysis, and sector breadth visuals, keeping trades aligned with the big picture.

VIX Filter:

Logic: Blocks long entries if VIX > threshold (default: 20, can_long = vix_close < vix_limit). Shorts are always allowed (can_short = true).

Impact: Prevents longs during high-fear markets (e.g., VIX spikes in crashes), while allowing shorts to capitalize on downturns.

SPX Trend Filter:

Logic: Compares S&P 500 (SPX) close to its SMA (Aggressive: 5, Balanced: 8, Conservative: 12 bars). spx_trend = 1 (UP) if close > SMA, -1 (DOWN) if < SMA, 0 (FLAT) if neutral.

Impact: Provides dashboard context, encouraging trades that align with market direction (e.g., longs in UP trend).

Sector Breadth (Visual):

Logic: Tracks 10 sector ETFs (XLK, XLF, XLE, etc.) vs. their SMAs (same lengths as SPX). Each sector scores +1 (bullish), -1 (bearish), or 0 (neutral), summed as breadth (-10 to +10).

Display: Green background if breadth > 4, red if breadth < -4, else neutral. Dashboard shows sector trends (↑/↓/-).

Impact: Faster SMA lengths make breadth more responsive, reflecting sector rotations (e.g., tech surging, energy lagging).

Why It’s Brilliant:

- VIX filter adds pro-level volatility awareness, saving beginners from panic-driven losses.

- SPX and sector breadth give a 360° view of market health, boosting signal confidence (e.g., green BG + buy signal = high-probability trade).

- Shorter SMAs make sentiment visuals react faster, perfect for 5min charts.

3. Risk Management

The risk controls are a fortress, now tighter and more dynamic to support frequent trading while keeping accounts safe.

Preset-Based Risk:

Aggressive: Fast EMAs (5/12), tight stops (1.1x ATR), 1-bar cooldown. High trade frequency, higher risk.

Balanced: EMAs (7/14), 1.2x ATR stops, 1-bar cooldown. Versatile for most traders.

Conservative: EMAs (9/18), 1.3x ATR stops, 2-bar cooldown. Safer, fewer trades.

Impact: Auto-scales risk to match style, making it foolproof for beginners.

Adaptive Stops and Take-Profits:

Logic: Stops = entry ± ATR * atr_mult (1.1–1.3x, down from 1.2–2.0x). Take-profits = entry ± ATR * take_mult (2x stop distance, 2:1 reward/risk). Longs: stop below entry, TP above; shorts: vice versa.

Impact: Tighter stops increase trade turnover while maintaining solid risk/reward, adapting to volatility.

Trade Cooldown:

Logic: Preset-driven (Aggressive/Balanced: 1 bar, Conservative: 2 bars vs. old user-input 2). Ensures bar_index - last_trade_bar >= cooldown.

Impact: Faster cooldowns (especially Aggressive/Balanced) allow more trades, balanced by VIX and strength filters.

Contract Sizing:

Logic: User sets contracts (default: 1, max: 10), no preset cap (unlike old 7/5/3 suggestion).

Impact: Flexible but risks over-leverage; beginners should stick to low contracts.

Built To Be Reliable and Consistent:

- Tighter stops and faster cooldowns make it a high-octane system without blowing up accounts.

- Preset-driven risk removes guesswork, letting newbies trade confidently.

- 2:1 TPs ensure profitable trades outweigh losses, even in volatile sessions like April 27, 2025 ES slippage.

4. Trade Entry and Exit Logic

The entry/exit rules are simple yet razor-sharp, now with VIX filtering and faster signals:

Entry Conditions:

Long Entry: buy_signal (fast EMA crosses above slow EMA, trend_dir = 1), no position (strategy.position_size = 0), cooldown passed (can_trade), and VIX < 20 (can_long). Enters with user-defined contracts.

Short Entry: sell_signal (fast EMA crosses below slow EMA, trend_dir = -1), no position, cooldown passed, can_short (always true).

Logic: Tracks last_entry_bar for visuals, last_trade_bar for cooldowns.

Exit Conditions:

Stop-Loss/Take-Profit: ATR-based stops (1.1–1.3x) and TPs (2x stop distance). Longs exit if price hits stop (below) or TP (above); shorts vice versa.

No Other Exits: Keeps it straightforward, relying on stops/TPs.

5. DAFE Visuals

The visuals are pure DAFE magic, blending clean function with informative metrics utilized by professionals, now enhanced by faster signals and a responsive breadth background:

EMA Plots:

Display: Fast EMA (blue, 2px), slow EMA (orange, 2px), using faster lengths (5–9/12–18).

Purpose: Highlights momentum shifts, with crossovers signaling entries.

Sector Breadth Background:

Display: Green (90% transparent) if breadth > 4, red (90%) if breadth < -4, else neutral.

Purpose: Faster breadth_sma_len (5–12 vs. 10–50) reflects sector shifts in real-time, reinforcing signal strength.

- Visuals are intuitive, turning complex signals into clear buy/sell cues.

- Faster breadth background reacts to market rotations (e.g., tech vs. energy), giving a pro-level edge.

6. Sector Breadth Dashboard

The new bottom-left dashboard is a game-changer, a 3x16 table (black/gray theme) that’s your market command center:

Metrics:

VIX: Current VIX (red if > 20, gray if not).

SPX: Trend as “UP” (green), “DOWN” (red), or “FLAT” (gray).

Trade Longs: “OK” (green) if VIX < 20, “BLOCK” (red) if not.

Sector Breadth: 10 sectors (Tech, Financial, etc.) with trend arrows (↑ green, ↓ red, - gray).

Placeholder Row: Empty for future metrics (e.g., ATR, breadth score).

Purpose: Consolidates regime, volatility, market trend, and sector data, making decisions a breeze.

- VIX and SPX metrics add context, helping beginners avoid bad trades (e.g., no longs if “BLOCK”).

Sector arrows show market health at a glance, like a cheat code for sentiment.

Key Features

Beginner-Ready: Preset modes and clear visuals make futures trading a breeze.

Sentiment-Driven: VIX filter, SPX trend, and sector breadth keep you in sync with the market.

High-Frequency: Faster EMAs, tighter stops, and short cooldowns boost trade volume.

Safe and Smart: Adaptive stops/TPs and cooldowns protect capital while maximizing wins.

Visual Mastery: DAFE’s clean flair, EMAs, dashboard—makes trading fun and clear.

Backtestable: Lean code and fixed qty ensure accurate historical testing.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Pick Preset: Aggressive (scalping), Balanced (versatile), or Conservative (safe). Balanced is default.

Set Contracts: Default 1, max 10. Stick low for safety.

Check Dashboard: Bottom-left shows preset, VIX, SPX, and sectors. “OK” + green breadth = strong buy.

Backtest: Run in strategy tester to compare modes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see VIX filter and stops in action.

Why It’s Brilliant

The Dskyz (DAFE) Quantum Sentiment Flux - Beginners is a masterpiece of simplicity and power. It takes pro-level tools—momentum, VIX, sector breadth—and wraps them in a system anyone can run. Faster signals and tighter stops make it a trading machine, while the VIX filter and dashboard keep you ahead of market chaos. The DAFE visuals and bottom-left command center turn your chart into a futuristic cockpit, guiding you through every trade. For beginners, it’s a safe entry to futures; for pros, it’s a scalping beast with sentiment smarts. This strat doesn’t just trade—it transforms how you see the market.

Final Notes

This is more than a strategy—it’s your launchpad to mastering futures with Dskyz (DAFE) flair. The Quantum Sentiment Flux blends accessibility, speed, and market savvy to help you outsmart the game. Load it, watch those triangles glow, and let’s make the markets your canvas!

Official Statement from Pine Script Team

(see TradingView help docs and forums):

"This warning may appear when you call functions such as ta.sma inside a request.security in a loop. There is no runtime impact. If you need to loop through a dynamic list of tickers, this cannot be avoided in the present version... Values will still be correct. Ignore this warning in such contexts."

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

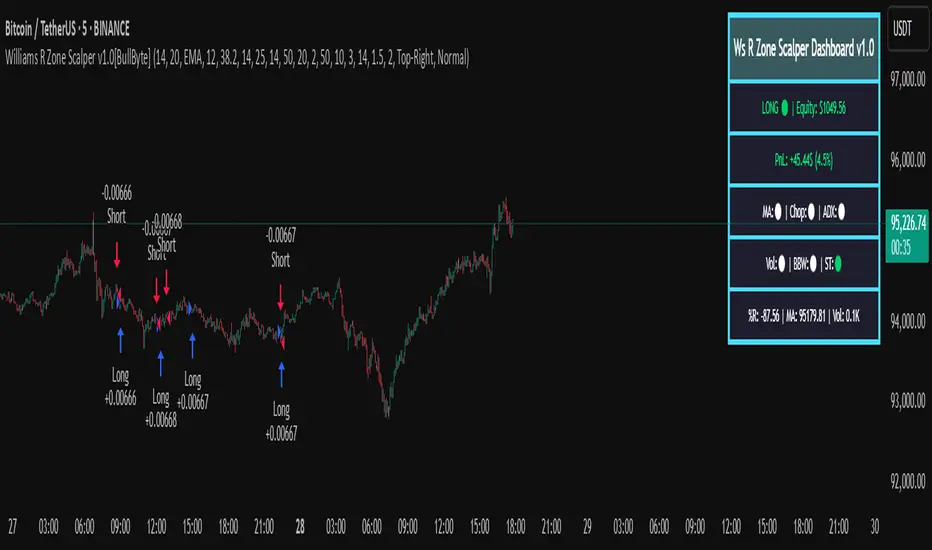

Williams R Zone Scalper v1.0[BullByte]Originality & Usefulness

Unlike standard Williams R cross-over scripts, this strategy layers five dynamic filters—moving-average trend, Supertrend, Choppiness Index, Bollinger Band Width, and volume validation —and presents a real-time dashboard with equity, PnL, filter status, and key indicator values. No other public Pine script combines these elements with toggleable filters and a custom dashboard. In backtests (BTC/USD (Binance), 5 min, 24 Mar 2025 → 28 Apr 2025), adding these filters turned a –2.09 % standalone Williams R into a +5.05 % net winner while cutting maximum drawdown in half.

---

What This Script Does

- Monitors Williams R (length 14) for overbought/oversold reversals.

- Applies up to five dynamic filters to confirm trend strength and volatility direction:

- Moving average (SMA/EMA/WMA/HMA)

- Supertrend line

- Choppiness Index (CI)

- Bollinger Band Width (BBW)

- Volume vs. its 50-period MA

- Plots blue arrows for Long entries (R crosses above –80 + all filters green) and red arrows for Short entries (R crosses below –20 + all filters green).

- Optionally sets dynamic ATR-based stop-loss (1.5×ATR) and take-profit (2×ATR).

- Shows a dashboard box with current position, equity, PnL, filter status, and real-time Williams R / MA/volume values.

---

Backtest Summary (BTC/USD(Binance), 5 min, 24 Mar 2025 → 28 Apr 2025)

• Total P&L : +50.70 USD (+5.05 %)

• Max Drawdown : 31.93 USD (3.11 %)

• Total Trades : 198

• Win Rate : 55.05 % (109/89)

• Profit Factor : 1.288

• Commission : 0.01 % per trade

• Slippage : 0 ticks

Even in choppy March–April, this multi-filter approach nets +5 % with a robust risk profile, compared to –2.09 % and higher drawdown for Williams R alone.

---

Williams R Alone vs. Multi-Filter Version

• Total P&L :

– Williams R alone → –20.83 USD (–2.09 %)

– Multi-Filter → +50.70 USD (+5.05 %)

• Max Drawdown :

– Williams R alone → 62.13 USD (6.00 %)

– Multi-Filter → 31.93 USD (3.11 %)

• Total Trades : 543 vs. 198

• Win Rate : 60.22 % vs. 55.05 %

• Profit Factor : 0.943 vs. 1.288

---

Inputs & What They Control

- wrLen (14): Williams R look-back

- maType (EMA): Trend filter type (SMA, EMA, WMA, HMA)

- maLen (20): Moving-average period

- useChop (true): Toggle Choppiness Index filter

- ciLen (12): CI look-back length

- chopThr (38.2): CI threshold (below = trending)

- useVol (true): Toggle volume-above-average filter

- volMaLen (50): Volume MA period

- useBBW (false): Toggle Bollinger Band Width filter

- bbwMaLen (50): BBW MA period

- useST (false): Toggle Supertrend filter

- stAtrLen (10): Supertrend ATR length

- stFactor (3.0): Supertrend multiplier

- useSL (false): Toggle ATR-based SL/TP

- atrLen (14): ATR period for SL/TP

- slMult (1.5): SL = slMult × ATR

- tpMult (2.0): TP = tpMult × ATR

---

How to Read the Chart

- Blue arrow (Long): Williams R crosses above –80 + all enabled filters green

- Red arrow (Short) : Williams R crosses below –20 + all filters green

- Dashboard box:

- Top : position and equity

- Next : cumulative PnL in USD & %

- Middle : green/white dots for each filter (green=passing, white=disabled)

- Bottom : Williams R, MA, and volume current values

---

Usage Tips

- Add the script : Indicators → My Scripts → Williams R Zone Scalper v1.0 → Add to BTC/USD chart on 5 min.

- Defaults : Optimized for BTC/USD.

- Forex majors : Raise `chopThr` to ~42.

- Stocks/high-beta : Enable `useBBW`.

- Enable SL/TP : Toggle `useSL`; stop-loss = 1.5×ATR, take-profit = 2×ATR apply automatically.

---

Common Questions

- * Why not trade every Williams R reversal?*

Raw Williams R whipsaws in sideways markets. Choppiness and volume filters reduce false entries.

- *Can I use on 1 min or 15 min?*

Yes—adjust ATR length or thresholds accordingly. Defaults target 5 min scalping.

- *What if all filters are on?*

Fewer arrows, higher-quality signals. Expect ~10 % boost in average win size.

---

Disclaimer & License

Trading carries risk of loss. Use this script “as is” under the Mozilla Public License 2.0 (mozilla.org). Always backtest, paper-trade, and adjust risk settings to your own profile.

---

Credits & References

- Pine Script v6, using TradingView’s built-in `ta.supertrend()`.

- TradingView House Rules: www.tradingview.com

Goodluck!

BullByte

TASC 2025.09 The Continuation Index

█ OVERVIEW

This script implements the "Continuation Index" as described by John F. Ehlers in the September 2025 edition of TASC's Trader's Tips . The Continuation Index uses Laguerre filters (featured in the July 2025 edition) to provide an early indication of trend direction, continuation, and exhaustion.

█ CONCEPTS

The idea for the Continuation Index was formed from an observation about Laguerre filters. In his article, Ehlers notes that when price is in trend, it tends to stay to one side of the filter. When considering smoothing, the UltimateSmoother was an obvious choice to reduce lag. With that in mind, The Continuation Index normalizes the difference between UltimateSmoother and the Laguerre filter to produce a two-state oscillator.

To minimize lag, the UltimateSmoother length in this indicator is fixed to half the length of the Laguerre filter.

█ USAGE

The Continuation Index consists of two primary states.

+1 suggests that the trader should position on the long side.

-1 suggests that the user should position on the short side.

Other readings can imply other opportunities, such as:

High Value Fluctuation could be used as a "buy the dip" opportunity.

Low Value Fluctuation could be used as a "sell the pop" opportunity.

█ INPUTS

By understanding the inputs and adjusting them as needed, each trader can benefit more from this indicator:

Gamma : Controls the Laguerre filter's response. This can be set anywhere between 0 and 1. If set to 0, the filter’s value will be the same as the UltimateSmoother.

Order : Controls the lag of the Laguerre filter, which is important when considering the timing of the system for spotting reversals. This can be set from 1 to 10, with lower values typically producing faster timing.

Length : Affects the smoothing of the display. Ehlers recommends starting with this value set to the intended amount of time you plan to hold a position. Consider your chart timeframe when setting this input. For example, on a daily chart, if you intend to hold a position for one month, set a value of 20.

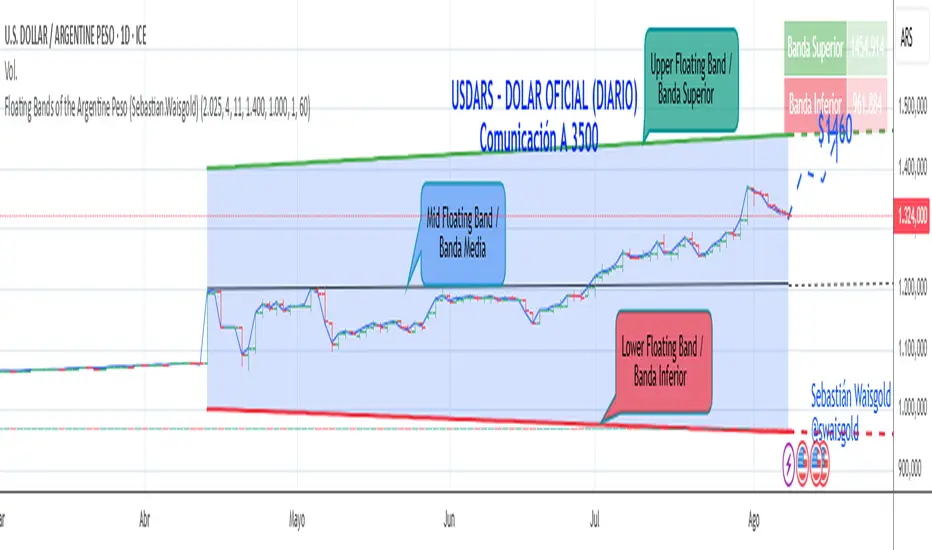

Floating Bands of the Argentine Peso (Sebastian.Waisgold)

The BCRA ( Central Bank of the Argentine Republic ) announced that as of Monday, April 15, 2025, the Argentine Peso (USDARS) will float within a system of divergent exchange rate bands.

The upper band was set at ARS 1400 per USD on 15/04/2025, with a +1% monthly adjustment distributed daily, rising by a fraction each day.

The lower band was set at ARS 1000 per USD on 15/04/2025, with a –1% monthly adjustment distributed daily, falling by a fraction each day.

This indicator is crucial for anyone trading USDARS, since the BCRA will only intervene in these situations:

- Selling : if the Peso depreciates against the USD above the upper band .

- Buying : if the Peso appreciates against the USD below the lower band .

Therefore, this indicator can be used as follows:

- If USDARS is above the upper band , it is “expensive” and you may sell .

- If USDARS is below the lower band , it is “cheap” and you may buy .

It can also be applied to other assets such as:

- USDTARS

- Dollar Cable / CCL (Contado con Liquidación) , derived from the BCBA:YPFD / NYSE:YPF ratio.

A mid band —exactly halfway between the upper and lower bands—has also been added.

Once added, the indicator should look like this:

In the following image you can see:

- Upper Floating Band

- Lower Floating Band

- Mid Floating Band

User Configuration

By double-clicking any line you can adjust:

- Start day (Dia de incio), month (Mes de inicio), and year (Año de inicio)

- Initial upper band value (Valor inicial banda superior)

- Initial lower band value (Valor inicial banda inferior)

- Monthly rate Tasa mensual %)

It is recommended not to modify these settings for the Argentine Peso, as they reflect the BCRA’s official framework. However, you may customize them—and the line colors—for other assets or currencies implementing a similar band scheme.

MSTY-WNTR Rebalancing SignalMSTY-WNTR Rebalancing Signal

## Overview

The **MSTY-WNTR Rebalancing Signal** is a custom TradingView indicator designed to help investors dynamically allocate between two YieldMax ETFs: **MSTY** (YieldMax MSTR Option Income Strategy ETF) and **WNTR** (YieldMax Short MSTR Option Income Strategy ETF). These ETFs are tied to MicroStrategy (MSTR) stock, which is heavily influenced by Bitcoin's price due to MSTR's significant Bitcoin holdings.

MSTY benefits from upward movements in MSTR (and thus Bitcoin) through a covered call strategy that generates income but caps upside potential. WNTR, on the other hand, provides inverse exposure, profiting from MSTR declines but losing in rallies. This indicator uses Bitcoin's momentum and MSTR's relative strength to signal when to hold MSTY (bullish phases), WNTR (bearish phases), or stay neutral, aiming to optimize returns by switching allocations at key turning points.

Inspired by strategies discussed in crypto communities (e.g., X posts analyzing MSTR-linked ETFs), this indicator promotes an active rebalancing approach over a "set and forget" buy-and-hold strategy. In simulated backtests over the past 12 months (as of August 4, 2025), the optimized version has shown potential to outperform holding 100% MSTY or 100% WNTR alone, with an illustrative APY of ~125% vs. ~6% for MSTY and ~-15% for WNTR in one scenario.

**Important Disclaimer**: This is not financial advice. Past performance does not guarantee future results. Always consult a financial advisor. Trading involves risk, and you could lose money. The indicator is for educational and informational purposes only.

## Key Features

- **Momentum-Based Signals**: Uses a Simple Moving Average (SMA) on Bitcoin's price to detect bullish (price > SMA) or bearish (price < SMA) trends.

- **RSI Confirmation**: Incorporates MSTR's Relative Strength Index (RSI) to filter signals, avoiding overbought conditions for MSTY and oversold for WNTR.

- **Visual Cues**:

- Green upward triangle for "Hold MSTY".

- Red downward triangle for "Hold WNTR".

- Yellow cross for "Switch" signals.

- Background color: Green for MSTY, red for WNTR.

- **Information Panel**: A table in the top-right corner displays real-time data: BTC Price, SMA value, MSTR RSI, and current Allocation (MSTY, WNTR, or Neutral).

- **Alerts**: Configurable alerts for holding MSTY, holding WNTR, or switching.

- **Optimized Parameters**: Defaults are tuned (SMA: 10 days, RSI: 15 periods, Overbought: 80, Oversold: 20) based on simulations to reduce whipsaws and capture trends effectively.

## How It Works

The indicator's logic is straightforward yet effective for volatile assets like Bitcoin and MSTR:

1. **Primary Trigger (Bitcoin Momentum)**:

- Calculate the SMA of Bitcoin's closing price (default: 10-day).

- Bullish: Current BTC price > SMA → Potential MSTY hold.

- Bearish: Current BTC price < SMA → Potential WNTR hold.

2. **Secondary Filter (MSTR RSI Confirmation)**:

- Compute RSI on MSTR stock (default: 15-period).

- For bullish signals: If RSI > Overbought (80), signal Neutral (avoid overextended rallies).

- For bearish signals: If RSI < Oversold (20), signal Neutral (avoid capitulation bottoms).

3. **Allocation Rules**:

- Hold 100% MSTY if bullish and not overbought.

- Hold 100% WNTR if bearish and not oversold.

- Neutral otherwise (e.g., during choppy or extreme markets) – consider holding cash or avoiding trades.

4. **Rebalancing**:

- Switch signals trigger when the hold changes (e.g., from MSTY to WNTR).

- Recommended frequency: Weekly reviews or on 5% BTC moves to minimize trading costs (aim for 4-6 trades/year).

This approach leverages Bitcoin's influence on MSTR while mitigating the risks of MSTY's covered call drag during downtrends and WNTR's losses in uptrends.

## Setup and Usage

1. **Chart Requirements**:

- Apply this indicator to a Bitcoin chart (e.g., BTCUSD on Binance or Coinbase, daily timeframe recommended).

- Ensure MSTR stock data is accessible (TradingView supports it natively).

2. **Adding to TradingView**:

- Open the Pine Editor.

- Paste the script code.

- Save and add to your chart.

- Customize inputs if needed (e.g., adjust SMA/RSI lengths for different timeframes).

3. **Interpretation**:

- **Green Background/Triangle**: Allocate 100% to MSTY – Bitcoin is in an uptrend, MSTR not overbought.

- **Red Background/Triangle**: Allocate 100% to WNTR – Bitcoin in downtrend, MSTR not oversold.

- **Yellow Switch Cross**: Rebalance your portfolio immediately.

- **Neutral (No Signal)**: Panel shows "Neutral" – Hold cash or previous position; reassess weekly.

- Monitor the panel for key metrics to validate signals manually.

4. **Backtesting and Strategy Integration**:

- Convert to a strategy script by changing `indicator()` to `strategy()` and adding entry/exit logic for automated testing.

- In simulations (e.g., using Python or TradingView's backtester), it has outperformed buy-and-hold in volatile markets by ~100-200% relative APY, but results vary.

- Factor in fees: ETF expense ratios (~0.99%), trading commissions (~$0.40/trade), and slippage.

5. **Risk Management**:

- Use with a diversified portfolio; never allocate more than you can afford to lose.

- Add stop-losses (e.g., 10% trailing) to protect against extreme moves.

- Rebalance sparingly to avoid over-trading in sideways markets.

- Dividends: Reinvest MSTY/WNTR payouts into the current hold for compounding.

## Performance Insights (Simulated as of August 4, 2025)

Based on synthetic backtests modeling the last 12 months:

- **Optimized Strategy APY**: ~125% (by timing switches effectively).

- **Hold 100% MSTY APY**: ~6% (gains from BTC rallies offset by downtrends).

- **Hold 100% WNTR APY**: ~-15% (losses in bull phases outweigh bear gains).

In one scenario with stronger volatility, the strategy achieved ~4533% APY vs. 10% for MSTY and -34% for WNTR, highlighting its potential in dynamic markets. However, these are illustrative; real results depend on actual BTC/MSTR movements. Test thoroughly on historical data.

## Limitations and Considerations

- **Data Dependency**: Relies on accurate BTC and MSTR data; delays or gaps can affect signals.

- **Market Risks**: Bitcoin's volatility can lead to false signals (whipsaws); the RSI filter helps but isn't perfect.

- **No Guarantees**: This indicator doesn't predict the future. MSTR's correlation to BTC may change (e.g., due to regulatory events).

- **Not for All Users**: Best for intermediate/advanced traders familiar with ETFs and crypto. Beginners should paper trade first.

- **Updates**: As of August 4, 2025, this is version 1.0. Future updates may include volume filters or EMA options.

If you find this indicator useful, consider leaving a like or comment on TradingView. Feedback welcome for improvements!

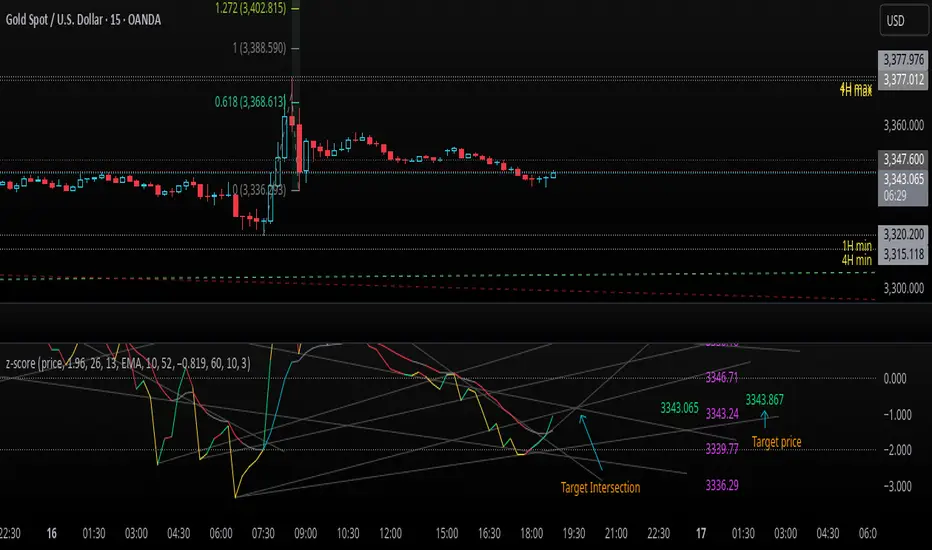

z-score-calkusi-v1.143z-scores incorporate the moment of N look-back bars to allow future price projection.

z-score = (X - mean)/std.deviation ; X = close

z-scores update with each new close print and with each new bar. Each new bar augments the mean and std.deviation for the N bars considered. The old Nth bar falls away from consideration with each new historical bar.

The indicator allows two other options for X: RSI or Moving Average.

NOTE: While trading use the "price" option only.

The other two options are provided for visualisation of RSI and Moving Average as z-score curves.

Use z-scores to identify tops and bottoms in the future as well as intermediate intersections through which a z-score will pass through with each new close and each new bar.

Draw lines from peaks and troughs in the past through intermediate peaks and troughs to identify projected intersections in the future. The most likely intersections are those that are formed from a line that comes from a peak in the past and another line that comes from a trough in the past. Try getting at least two lines from historical peaks and two lines from historical troughs to pass through a future intersection.

Compute the target intersection price in the future by clicking on the z-score indicator header to see a drag-able horizontal line to drag over the intersection. The target price is the last value displayed in the indicator's status bar after the closing price.

When the indicator header is clicked, a white horizontal drag-able line will appear to allow dragging the line over an intersection that has been drawn on the indicator for a future z-score projection and the associated future closing price.

With each new bar that appears, it is necessary to repeat the procedure of clicking the z-score indicator header to be able to drag the drag-able horizontal line to see the new target price for the selected intersection. The projected price will be different from the current close price providing a price arbitrage in time.

New intermediate peaks and troughs that appear require new lines be drawn from the past through the new intermediate peak to find a new intersection in the future and a new projected price. Since z-score curves are sort of cyclical in nature, it is possible to see where one has to locate a future intersection by drawing lines from past peaks and troughs.

Do not get fixated on any one projected price as the market decides which projected price will be realised. All prospective targets should be manually updated with each new bar.

When the z-score plot moves outside a channel comprised of lines that are drawn from the past, be ready to adjust to new market conditions.

z-score plots that move above the zero line indicate price action that is either rising or ranging. Similarly, z-score plots that move below the zero line indicate price action that is either falling or ranging. Be ready to adjust to new market conditions when z-scores move back and forth across the zero line.

A bar with highest absolute z-score for a cycle screams "reversal approaching" and is followed by a bar with a lower absolute z-score where close price tops and bottoms are realised. This can occur either on the next bar or a few bars later.

The indicator also displays the required N for a Normal(0,1) distribution that can be set for finer granularity for the z-score curve.This works with the Confidence Interval (CI) z-score setting. The default z-score is 1.96 for 95% CI.

Common Confidence Interval z-scores to find N for Normal(0,1) with a Margin of Error (MOE) of 1:

70% 1.036

75% 1.150

80% 1.282

85% 1.440

90% 1.645

95% 1.960

98% 2.326

99% 2.576

99.5% 2.807

99.9% 3.291

99.99% 3.891

99.999% 4.417

9-Jun-2025

Added a feature to display price projection labels at z-score levels 3, 2, 1, 0, -1, -2, 3.

This provides a range for prices available at the current time to help decide whether it is worth entering a trade. If the range of prices from say z=|2| to z=|1| is too narrow, then a trade at the current time may not be worth the risk.

Added plot for z-score moving average.

28-Jun-2025

Added Settings option for # of Std.Deviation level Price Labels to display. The default is 3. Min is 2. Max is 6.

This feature allows likelihood assessment for Fibonacci price projections from higher time frames at lower time frames. A Fibonacci price projection that falls outside |3.x| Std.Deviations is not likely.

Added Settings option for Chart Bar Count and Target Label Offset to allow placement of price labels for the standard z-score levels to the right of the window so that these are still visible in the window.

Target Label Offset allows adjustment of placement of Target Price Label in cases when the Target Price Label is either obscured by the price labels for the standard z-score levels or is too far right to be visible in the window.

9-Jul-2025

z-score 1.142 updates:

Displays in the status line before the close price the range for the selected Std. Deviation levels specified in Settings and |z-zMa|.

When |z-zMa| > |avg(z-zMa)| and zMa rising, |z-zMa| and zMa displays in aqua.

When |z-zMa| > |avg(z-zMa)| and zMa falling, |z-zMa| and zMa displays in red.

When |z-zMa| <= |avg(z-zMa)|, z and zMa display in gray.

z usually crosses over zMa when zMa is gray but not always. So if cross-over occurs when zMa is not gray, it implies a strong move in progress.

Practice makes perfect.

Use this indicator at your own risk

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5