Rolling Performance Toolkit (Returns, Correlation and Sharpe)This script provides a flexible toolkit for evaluating rolling performance metrics between any asset and a benchmark.

Features:

Library-based: Built on a custom utilities library for consistent return and statistics calculations.

Rolling Window Control: Choose the lookback period (in days) to calculate metrics.

Multiple Modes: Toggle between Rolling Returns, Rolling Correlation, and Rolling Sharpe Ratio.

Benchmark Comparison: Compare your selected ticker against a benchmark (default: S&P 500 / SPX), but you can easily switch to any symbol.

Risk-Free Rate Options: Choose from zero, a constant annual % rate, or a proxy symbol (default: US03M – 3-Month Treasury Yield).

Annualized Sharpe: Sharpe ratios are annualized by default (×√252) for intuitive interpretation.

This tool is useful for traders and investors who want to monitor relative performance, diversification benefits, or risk-adjusted returns over time.

Cari dalam skrip untuk "半导体设备ETF"

utilitiesLibrary for commonly used utilities, for visualizing rolling returns, correlations and sharpe

MTF Options Signals (message-free)script made to help with options profitability. made using ai to increase portfolio profitability

Smart Breadth [smartcanvas]Overview

This indicator is a market breadth analysis tool focused on the S&P 500 index. It visualizes the percentage of S&P 500 constituents trading above their 50-day and 200-day moving averages, integrates the McClellan Oscillator for advance-decline analysis, and detects various breadth-based signals such as thrusts, divergences, and trend changes. The indicator is displayed in a separate pane and provides visual cues, a summary label with tooltip, and alert conditions to highlight potential market conditions.

The tool uses data symbols like S5FI (percentage above 50-day MA), S5TH (percentage above 200-day MA), ADVN/DECN (S&P advances/declines), and optionally NYSE advances/declines for certain calculations. If primary data is unavailable, it falls back to calculated breadth from advance-decline ratios.

This indicator is intended for educational and analytical purposes to help users observe market internals. My intention was to pack in one indicator things you will only find in a few. It does not provide trading signals as financial advice, and users are encouraged to use it in conjunction with their own research and risk management strategies. No performance guarantees are implied, and historical patterns may not predict future market behavior.

Key Components and Visuals

Plotted Lines:

Aqua line: Percentage of S&P 500 stocks above their 50-day MA.

Purple line: Percentage of S&P 500 stocks above their 200-day MA.

Optional orange line (enabled via "Show Momentum Line"): 10-day momentum of the 50-day MA breadth, shifted by +50 for scaling.

Optional line plot (enabled via "Show McClellan Oscillator"): McClellan Oscillator, colored green when positive and red when negative. Can use actual scale or normalized to fit breadth percentages (0-100).

Horizontal Levels:

Dotted green at 70%: "Strong" level.

Dashed green at user-defined green threshold (default 60%): "Buy Zone".

Dashed yellow at user-defined yellow threshold (default 50%): "Neutral".

Dotted red at 30%: "Oversold" level.

Optional dotted lines for McClellan (when shown and not using actual scale): Overbought (red), Oversold (green), and Zero (gray), scaled to fit.

Background Coloring:

Green shades for bullish/strong bullish states.

Yellow for neutral.

Orange for caution.

Red for bearish.

Signal Shapes:

Rocket emoji (🚀) at bottom for Zweig Breadth Thrust trigger.

Green circle at bottom for recovery signal.

Red triangle down at top for negative divergence warning.

Green triangle up at bottom for positive divergence.

Light green triangle up at bottom for McClellan oversold bounce.

Green diamond at bottom for capitulation signal.

Summary Label (Right Side):

Displays current action (e.g., "BUY", "HOLD") with emoji, breadth percentages with colored circles, McClellan value with emoji, market state, risk/reward stars, and active signals.

Hover tooltip provides detailed breakdown: action priority, breadth metrics, McClellan status, momentum/trend, market state, active signals, data quality, thresholds, recent changes, and a general recommendation category.

Calculations and Logic

Breadth Percentages: Derived from S5FI/S5TH or calculated from advances/(advances + declines) * 100, with fallback adjustments.

McClellan Oscillator: Difference between fast (default 19) and slow (default 39) EMAs of net advances (advances - declines).

Momentum: 10-day change in 50-day MA breadth percentage.

Trend Analysis: Counts consecutive rising days in breadth to detect upward trends.

Breadth Thrust (Zweig): 10-day EMA of advances/total issues crossing from below a bottom level (default 40) to above a top level (default 61.5). Can use S&P or NYSE data.

Divergences: Compares S&P 500 price highs/lows with breadth or McClellan over a lookback period (default 20) to detect positive (bullish) or negative (bearish) divergences.

Market States: Determined by breadth levels relative to thresholds, trend direction, and McClellan conditions (e.g., strong bullish if above green threshold, rising, and McClellan supportive).

Actions: Prioritized logic (0-10) selects an action like "BUY" or "AVOID LONGS" based on signals, states, and conditions. Higher priority (e.g., capitulation at 10) overrides lower ones.

Alerts: Triggered on new occurrences of key conditions, such as breadth thrust, divergences, state changes, etc.

Input Parameters

The indicator offers customization through grouped inputs, but the use of defaults is encouraged.

Usage Notes

Add the indicator to a chart of any symbol (though designed around S&P 500 data; works best on daily or higher timeframes). Monitor the label and tooltip for a consolidated view of conditions. Set up alerts for specific events.

This script relies on external security requests, which may have data availability issues on certain exchanges or timeframes. The fallback mechanism ensures continuity but may differ slightly from primary sources.

Disclaimer

This indicator is provided for informational and educational purposes only. It does not constitute investment advice, financial recommendations, or an endorsement of any trading strategy. Market conditions can change rapidly, and users should not rely solely on this tool for decision-making. Always perform your own due diligence, consult with qualified professionals if needed, and be aware of the risks involved in trading. The author and TradingView are not responsible for any losses incurred from using this script.

AI - 200 EMA with Offsets StrategyLong when close price crosses above +4% offset 200 day EMA

Sell when close price crosses below -6.5% offset 200 day EMA

Major Support and Resistance LevelsSupport and Resistance Levels shows daily with the Green and Red lines. Previous days with the crosses.

Elliott Wave Rule EngineWhat this tool does

The indicator scans price for two concurrent swing structures—a Small (shorter-degree) and a Large (higher-degree) set—then applies an Elliott/NeoWave rule engine to the most recent 5-swing motive (1-2-3-4-5) or 3-swing corrective (A-B-C). It produces:

Blue lines for Small swings and Orange lines for Large swings.

A rule dashboard (optional) showing PASS/FAIL/WARN for core rules & guidelines.

Buy/Sell labels when (a) a valid motive completes and (b) loop “consensus,” alignment, and scoring gates are satisfied.

Reading the chart

Small swings: thin blue segments, built from your Small settings.

Large swings: thicker orange segments, from your Large settings.

Background tint: faint green when a motive (impulse/diagonal) is valid right now on Small.

Labels (if enabled):

“1…5” or “A-B-C” markers on the latest detected structure.

Buy/Sell label at the last pivot when all gates pass; text may include a score %.

How it works

For both Small and Large degrees the script:

- Loops over all (left, right) combinations you specify (e.g., Small Left = 3..6, Right = 0..0) and calls ta.pivothigh/low.

- Aggregates the results:

- Keeps the most extreme pivot found in the loop (highest high or lowest low) that’s newer than the last accepted swing.

- Gates acceptance by minimum % change versus the last opposite swing (inside the loop) and a post-aggregation filter (Small Minimum swing %, Large Minimum swing %).

- Merges back-to-back same-type swings (HH or LL) by keeping only the more extreme one.

- Keeps only the last N=lookbackWaves swings (default 100).

- Consensus (used for signals) comes from the loop counts:

- sBuyConsensus = small L-count / total-combos (bullish bias)

- sSellConsensus = small H-count / total-combos (bearish bias)

(and the same for Large). This is a data-driven “how many combos agreed” measure.

2) Rule engine (Impulse/Diagonal vs. Corrective)

When there are at least 6 Small swings, the engine tests 1-2-3-4-5:

Hard rules (must pass for an Impulse):

- Wave-2 not > 100% of Wave-1 (no retrace beyond start of W1).

- Wave-3 not the shortest among 1,3,5.

- Wave-4 doesn’t overlap Wave-1 (if it does, structure may be a Diagonal).

- Diagonal eligibility: Rules 1 & 2 pass but Rule 3 fails ⇒ eligible as a Diagonal (

Guidelines (7 checks, count toward a threshold you set):

- W2 retraces a Fib level (within ±fibTol).

- W4 retraces a Fib level (within ±fibTol).

- W3 strongest momentum (speed = |Δprice| / bars).

- Alternation: W2 vs W4 have meaningfully different “sharpness” (price per bar), threshold altSlopeThr.

- Proportion (Price): |W1| and |W3| within propTolP× each other.

- Proportion (Time): W1W3 and W2W4 durations within propTolT×.

- W5 weaker than W3 (momentum divergence proxy).

A Motive is valid if:

- Impulse: all 3 hard rules pass and guideline passes ≥ Min guideline passes.

- Diagonal: diagonal-eligible and guideline passes ≥ Min guideline passes.

- if motive fails, the engine still evaluates ABC as Zigzag and Flat to populate the table:

- Zigzag: B shallower than ~0.618A; C ≈ A or 1.618A (±fibTol).

- Flat: B ≥ ~0.9A; expanded flat if B > 1.0A and C in *A; “running” note if C < A.

3) Signal logic (consensus-gated & scored)

Signals fire only on new Small pivots and only if a Small motive just validated:Direction comes from the motive’s W1 (up = bull, down = bear).

Consensus checks (from the loop):

Use Sell consensus if the last pivot is a High, or Buy consensus if it’s a Low.Require it ≥ Min SMALL loop consensus and ahead of the opposite side by at least Min consensus margin.If you also require Large quality: check the corresponding Large consensus ≥ Min LARGE loop consensus.

Alignment: If Require small/large directional alignment is ON, Small and Large directions must match (or the Large motive must be complete).

Score:

- If Large not required: finalScore = smallConsensus × smallQuality.

- If Large required: finalScore = smallConsensus × smallQuality × largeQuality.

- Need finalScore ≥ Min final score.

When all gates pass, you’ll see “Buy xx%” or “Sell xx%” at the pivot.

Inputs (explained):

- Smaller Wave Swing Detection (Looped)

- Small Left Min / Max (default 3..6): ta.pivot* left widths to scan.

- Small Right Min / Max (default 0..0): right widths to scan (0 = earliest confirmation).

- Small Minimum swing % (post-aggregation) (0.3%): filters out tiny swings after the loop.

- Larger Wave Swing Detection (Looped)

- Large Left Min / Max (100..200) and Right Min/Max (0..0): higher-degree scan (defaults are big; adjust for intraday).

- Large Minimum swing % (post-aggregation) (1.5%).

- Loop Filters (inside the loop)

- Small loop min % change (0.20%): a candidate pivot counts only if move vs. last opposite Small swing ≥ this.

- Large loop min % change (1.50%): same idea for Large.

Rule Engine Tolerances

- Fibonacci tolerance (±%) (0.05 = 5%): closeness to Fib levels.

-Same-degree TIME proportion max (x) (2.00×) and PRICE proportion max (x) (3.00×).

- Alternation slope ratio threshold (0.10): higher = stricter alternation.

- Min guideline passes (0–7) (5): threshold for motive validity.

- Signal Probability (Loop Consensus)

- Min SMALL loop consensus (0.60).

- Min LARGE loop consensus (0.50) (used only if Large validation matters).

- Min consensus margin vs opposite (0.10): e.g., 0.60 vs 0.45 fails (margin 0.15 passes).

Require LARGE 1–5 valid (or diagonal) for signal (off by default).

Min final score (0.20): gate on the composite score.

Annotate label with score % (on).

WARN (orange): guideline not met—pattern can still be valid if total passes ≥ Min guideline passes.

FAQ

Q: Why did I get a diagonal instead of an impulse?

A: Wave-4 overlapped Wave-1 (Rule 3). If Rules 1 & 2 pass and guidelines meet your minimum, it’s eligible as a Diagonal.

Q: Where do Buy/Sell labels come from?

A: Only after a valid Small motive at a new pivot, and only if consensus, alignment, and final score gates pass (per your settings).

Q: It “missed” a wave in hindsight.

A: Pivots require right bars to confirm; extremely tight settings can filter that swing; adjust Small min % or ranges.

Q: Are there repaints?

A: No, It uses standard pivot confirmation; until a pivot is confirmed, recent swings can evolve. After confirmation, lines/labels are stable.

Limitations & disclaimers

Elliott/NeoWave rules are heuristics; markets are messy. Treat outputs as structured context, not certainty.

Consensus is pattern-scan agreement, not probability of profit Not investment advice; always couple with risk management.

Draw Trend LinesSometimes the simplest indicators help traders make better decisions. This indicator draws simple trend lines, the same lines you would draw manually.

To trade with an edge, traders need to interpret the recent price action, whether it's noisy or choppy, or it's trending. Trend Lines will help traders with that interpretation.

The lines drawn are:

1. lower tops

2. higher bottoms

Because trends are defined as higher lows, or lower highs.

When you see "Wedges", formed by prices chopping between top and bottom trend lines, that's noisy environment not to be traded. When you learn to "stop yourself", you already have an edge.

Often when you see a trend, it's still not too late. Trend will continue until it doesn't. But the caveat is a very steep trend is unlikely to continue, because buying volume is extremely unbalanced to cause the steep trend, and that volume will run out of energy. (Same on the sell side of course)

Trends can reverse, and when price action breaks the trend line, Breakout/Breakdown traders can take this as an entry signal.

Enjoy, and good trading!

STRAT 3-2-2 (30m) • Upcoming / Approach / Entry + AlertsThis indicator is built for The STRAT trading method, specifically the 3-2-2 reversal pattern. It monitors price action on the 30-minute timeframe (HTF = 30m) and visually/alert-wise highlights where a 3-2-2 setup, approach, or entry trigger occurs.

---

⚙️ How it works

1. Detects bar types:

3 (Outside Bar) = range breaks both high & low of the previous bar

2u (Up bar) = higher high, not outside

2d (Down bar) = lower low, not outside

1 (Inside bar) = fully contained within prior bar

2. Looks for 3-2-2 setups:

Bullish 3-2-2 = 3 → 2d → 2u (expect reversal UP)

Bearish 3-2-2 = 3 → 2u → 2d (expect reversal DOWN)

3. Defines trigger levels:

Bullish trigger = high of the first “2d” bar

Bearish trigger = low of the first “2u” bar

4. Signals 3 phases:

Upcoming: pattern is forming, second “2” hasn’t triggered yet

Approach: price comes within 50% (adjustable) of the trigger level

Entry: price breaks the trigger (actual reversal confirmation)

5. Visualization:

Labels above/below candles show “Approach” and “Entry”

Background or bar colors (toggle in settings) highlight Setup / Approach / Entry

Optional dotted line marks the trigger level for clarity

---

🔔 Alerts

Two alert systems are built in:

1. Safe static conditions (for normal TradingView alert setup):

APPROACH: Bullish 3-2-2 (30m)

APPROACH: Bearish 3-2-2 (30m)

ENTRY: Bullish 3-2-2 (30m)

ENTRY: Bearish 3-2-2 (30m)

2. Dynamic messages (using alert() calls with price info):

If you create an alert with “Any alert() function call”, the pop-up will include the trigger price.

---

📋 Inputs (Settings)

Signal timeframe (HTF) → default 30m

Confirm signals at HTF bar close → waits for bar close (non-repainting)

Approach = % of first '2' bar range → default 50%

Show labels → On/Off

Color candles instead of background → toggle between candle color vs. chart background

Algo + Trendlines :: Medium PeriodThis indicator helps me to avoid overlooking Trendlines / Algolines. So far it doesn't search explicitly for Algolines (I don't consider volume at all), but it's definitely now already not horribly bad.

These are meant to be used on logarithmic charts btw! The lines would be displayed wrong on linear charts.

The biggest challenge is that there are some technical restrictions in TradingView, f. e. a script stops executing if a for-loop would take longer than 0.5 sec.

So in order to circumvent this and still be able to consider as many candles from the past as possible, I've created multiple versions for different purposes that I use like this:

Algo + Trendlines :: Medium Period : This script looks for "temporary highs / lows" (meaning the bar before and after has lower highs / lows) on the daily chart, connects them and shows the 5 ones that are the closest to the current price (=most relevant). This one is good to find trendlines more thoroughly, but only up to 4 years ago.

Algo + Trendlines :: Long Period : This version looks instead at the weekly charts for "temporary highs / lows" and finds out which days caused these highs / lows and connects them, Taking data from the weekly chart means fewer data points to check whether a trendline is broken, which allows to detect trendlines from up to 12 years ago! Therefore it misses some trendlines. Personally I prefer this one with "Only Confirmed" set to true to really show only the most relevant lines. This means at least 3 candle highs / lows touched the line. These are more likely stronger resistance / support lines compared to those that have been touched only twice.

Very important: sometimes you might see dotted lines that suddenly stop after a few months (after 100 bars to be precise). This indicates you need to zoom further out for TradingView to be able to load the full line. Unfortunately TradingView doesn't render lines if the starting point was too long ago, so this is my workaround. This is also the script's biggest advantage: showing you lines that you might have missed otherwise since the starting bars were outside of the screen, and required you to scroll f. e back to 2015..

One more thing to know:

Weak colored line = only 2 "collision" points with candle highs/lows (= not confirmed)

Usual colored line = 3+ "collision" points (= confirmed)

Make sure to move this indicator above the ticker in the Object Tree, so that it is drawn on top of the ticker's candles!

More infos: www.reddit.com

Customizable EMA 10/20/50/100Customizable EMA indicator. Fully adjustable with inputs so you can change EMA lengths and colors directly from the indicator settings panel.

EMA20 Entry with Lei Teacher Strategy_Trend_Follow_RuleEMA20 Entry with Lei Teacher Strategy Trend Follow Entry Alert

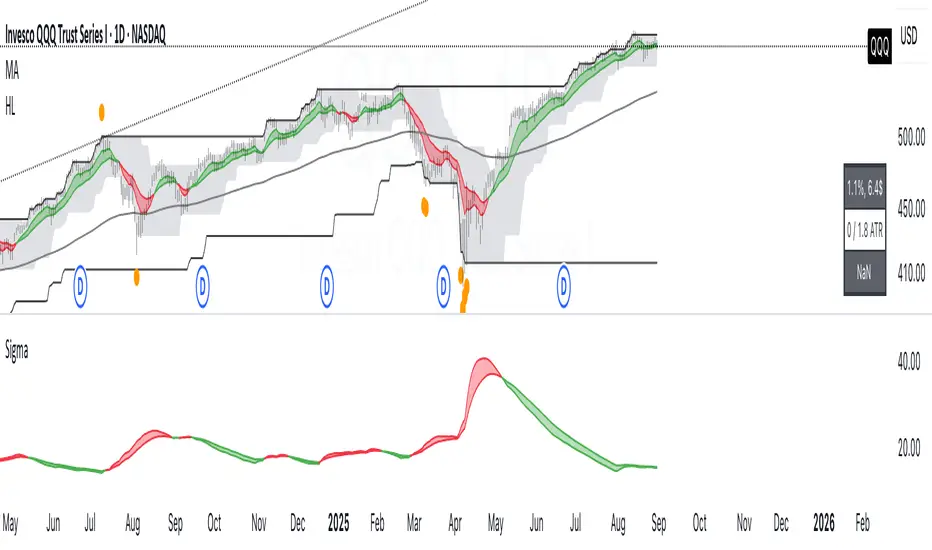

Volatility Forecast/*==============================================================================

Volatility Forecast — Publishable Documentation

Author: @BB_9791

License: Mozilla Public License 2.0

WHAT THIS INDICATOR SHOWS

- A daily volatility estimate in percent points, called sigma_day.

- A slow volatility anchor, the 10-year EMA of sigma_day.

- A blended volatility series in percent points:

sigma_blend = (1 − p) * sigma_day + p * EMA_10y(sigma_day)

where p is the Slow weight %, default 30.

- Optional annualization by multiplying by 16, this is a daily-to-annual

conversion used by Robert Carver in his writings.

METHODOLOGY, CREDIT

The estimator follows the approach popularized by Robert Carver

("Systematic Trading", "Advanced Futures Trading Strategies", blog qoppac).

Current daily volatility is computed as an exponentially weighted standard

deviation of daily percent returns, with alpha = 2 / (span + 1).

The slow leg is a long EMA of that volatility series, about 10 years.

The blend uses fixed weights. This keeps the slow leg meaningful through

large price level changes, since the blend is done in percent space first.

MATH DETAILS

Let r_t be daily percent return:

r_t = 100 * (Close_t / Close_{t−1} − 1)

EWMA mean and variance:

m_t = α * r_t + (1 − α) * m_{t−1}

v_t = α * (r_t − m_t)^2 + (1 − α) * v_{t−1}

where α = 2 / (span_current + 1)

Current daily sigma in percent points:

sigma_day = sqrt(v_t)

Slow leg:

sigma_10y = EMA(sigma_day, span_long)

Blend:

sigma_blend = (1 − p) * sigma_day + p * sigma_10y

Annualized option:

sigma_ann = 16 * sigma_blend

INPUTS

- Threshold (percent points): horizontal guide level on the chart.

- Short term span (days): EW stdev span for sigma_day.

- Long term span (days): EMA span for the slow leg, choose about 2500 for 10 years.

- Slow weight %: p in the blend.

- Annualize (x16): plot daily or annualized values.

- Show components: toggles Current and 10y EMA lines.

- The script uses the chart symbol by default.

PLOTS

- Blended σ% as the main line.

- Optional Current σ% and 10y EMA σ%.

- Editable horizontal threshold line in the same units as the plot

(percent points per day or per year).

- Optional EMA 9 and EMA 20 cloud on the blended series, green for uptrend

when EMA 9 is above EMA 20, red otherwise. Opacity is configurable.

HOW TO READ

- Values are percent points of movement per day when not annualized,

for example 1.2 means about 1.2% typical daily move.

- With annualize checked, values are percent points per year, for example 18

means about 18% annualized volatility.

- Use the threshold and the EMA cloud to mark high or low volatility regimes.

NOTES

- All calculations use daily data via request.security at the chart symbol.

- The blend is done in percent space, then optionally annualized, which avoids

bias from the price level.

- This script does not produce trading signals by itself, it is a risk and

regime indicator.

CREDITS

Volatility forecasting method and scaling convention credited to Robert Carver.

See his books and blog for background and parameter choices.

VERSION

v1.0 Initial public release.

==============================================================================*/

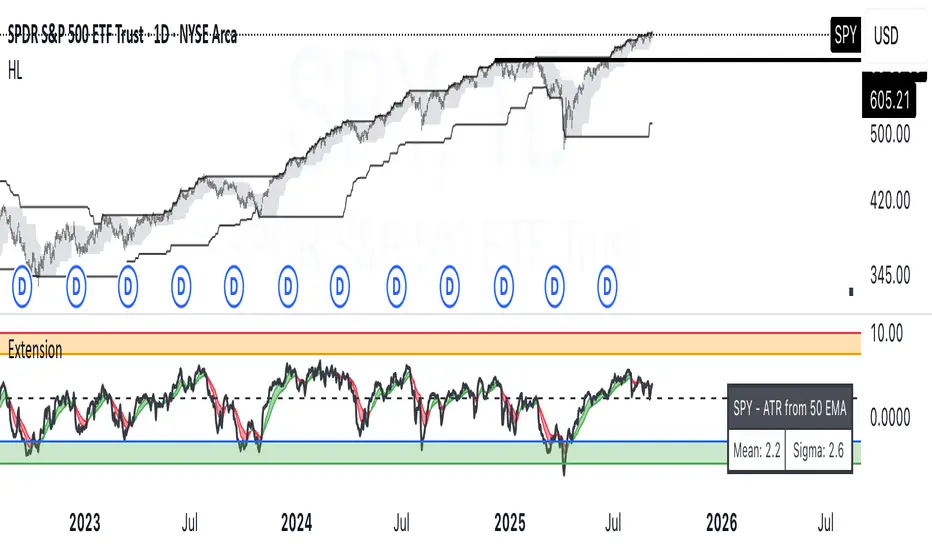

ATR Extension from Moving Average, with Robust Sigma Bands

# ATR Extension from Moving Average, with Robust Sigma Bands

**What it does**

This indicator measures how far price is from a selected moving average, expressed in **ATR multiples**, then overlays **robust sigma bands** around the long run central tendency of that extension. Positive values mean price is extended above the MA, negative values mean price is extended below the MA. The signal adapts to volatility through ATR, which makes comparisons consistent across symbols and regimes.

**Why it can help**

* Normalizes distance to an MA by ATR, which controls for changing volatility

* Uses the **bar’s extreme** against the MA, not just the close, so it captures true stretch

* Computes a **median** and **standard deviation** of the extension over a multi-year window, which yields simple, intuitive bands for trend and mean-reversion decisions

---

## Inputs

* **MA length**: default 50, options 200, 64, 50, 20, 9, 4, 3

* **MA timeframe**: Daily or Weekly. The MA is computed on the chosen higher timeframe through `request.security`.

* **MA type**: EMA or SMA

* **Years lookback**: 1 to 10 years, default 5. This sets the sample for the median and sigma calculation, `years * 365` bars.

* **Line width**: visual width of the plotted extension series

* **Table**: optional on-chart table that displays the current long run **median** and **sigma** of the extension, with selectable text size

**Fixed parameters in this release**

* **ATR length**: 20 on the daily timeframe

* **ATR type**: classic ATR. ADR percent is not enabled in this version.

---

## Plots and colors

* **Main plot**: “Extension from 50d EMA” by default. Value is in **ATR multiples**.

* **Reference lines**:

* `median` line, black dashed

* +2σ orange, +3σ red

* −2σ blue, −3σ green

---

## How it is calculated

1. **Moving average** on the selected higher timeframe: EMA or SMA of `close`.

2. **Extreme-based distance** from MA, as a percent of price:

* If `close > MA`, use `(high − MA) / close * 100`

* Else, use `(low − MA) / close * 100`

3. **ATR percent** on the daily timeframe: `ATR(20) / close * 100`

4. **ATR multiples**: extension percent divided by ATR percent

5. **Robust center and spread** over the chosen lookback window:

* Center: **median** of the ATR-multiple series

* Spread: **standard deviation** of that series

* Bands: center ± 1σ, 2σ, 3σ, with 2σ and 3σ drawn

This design yields an intuitive unit scale. A value of **+2.0** means price is about 2 ATR above the selected MA by the most stretched side of the current bar. A value of **−3.0** means roughly 3 ATR below.

---

## Practical use

* **Trend continuation**

* Sustained readings near or above **+1σ** together with a rising MA often signal healthy momentum.

* **Mean reversion**

* Spikes into **±2σ** or **±3σ** can identify stretched conditions for fade setups in range or late-trend environments.

* **Regime awareness**

* The **median** moves slowly. When median drifts positive for many months, the market spends more time extended above the MA, which often marks bullish regimes. The opposite applies in bearish regimes.

**Notes**

* The MA can be set to Weekly while ATR remains Daily. This is deliberate, it keeps the normalization stable for most symbols.

* On very short intraday charts, the extension remains meaningful since it references the session’s extreme against a higher-timeframe MA and a daily ATR.

* Symbols with short histories may not fill the lookback window. Bands will adapt as data accrues.

---

## Table overlay

Enable **Table → Show** to see:

* “ATR from \”

* Current **median** and **sigma** of the extension series for your lookback

---

## Recommended settings

* **Swing equities**: 50 EMA on Daily, 5 to 7 years

* **Index trend work**: 200 EMA on Daily, 10 years

* **Position trading**: 20 or 50 EMA on Weekly MA, 5 to 10 years

---

## Interpretation examples

* Reading **+2.7** with price above a rising 50 EMA, near prior highs

* Strong trend extension, consider pyramiding in trend systems or waiting for a pullback if you are a mean-reverter.

* Reading **−2.2** into multi-month support with flattening MA

* Stretch to the downside that often mean-reverts, size entries based on your system rules.

---

## Credits

The concept of measuring stretch from a moving average in ATR units has a rich community history. This implementation and its presentation draw on ideas popularized by **Jeff Sun**, **SugarTrader**, and **Steve D Jacobs**. Thanks to each for their contributions to ATR-based extension thinking.

---

## License

This script and description are distributed under **MPL-2.0**, consistent with the header in the source code.

---

## Changelog

* **v1.0**: Initial public release. Daily ATR normalization, EMA or SMA on D or W timeframe, robust median and sigma bands, optional table.

---

## Disclaimer

This tool is for educational use only. It is not financial advice. Always test on your own data and strategies, then manage risk accordingly.

ORB with Golden Zone FIB targets, Any Timeframe by TenAMTraderDescription:

This indicator is designed to help traders identify key price levels using Fibonacci extensions and retracements based on the Opening Range Breakout (ORB). The levels are visualized as “Golden Zones”, which can serve as potential targets for trades.

Features:

Customizable ORB Timeframe: By default, the ORB is set from 9:30 AM to 9:45 AM EST, but any timeframe can be configured in the settings to fit your trading style.

Golden Zones as Targets: Fibonacci levels are intended to be used as potential profit-taking zones or areas to monitor for reversals, providing a structured framework for intraday and swing trading.

Adjustable Chart Settings: Color-coded levels make it easy to interpret at a glance, and all lines can be customized for personal preference.

Versatile Application: The indicator works across any timeframe, enabling traders to analyze both intraday and multi-day price action.

How to Use:

Ensure Regular Trading Hours (RTH) is enabled on your chart for accurate level calculation.

Observe price action near Golden Zones: a confirmed breakout may indicate continuation, while a pullback could signal a reversal opportunity.

Use the Golden Zones as reference targets for managing risk and planning exits.

Adjust the ORB timeframe and display settings to match your preferred trading style.

Legal Disclosure:

This indicator is provided for educational purposes only and is not financial advice. Trading carries a substantial risk of loss. Users should always perform their own analysis and consult a licensed financial professional before making any trading decisions. Past performance is not indicative of future results.

EMA Touch & Bounce Counter

Simple Indicator that allows you to see how many times price has touched an EMA line and bounced off of it without crossing it. The indicator tells you the amount of times it bounced off it in a bullish and bearish trend and also gives you the total amount of bounces to both trends.

This indicator was to just help you identify how respected a given EMA line is in case you decide to go long or short based on the trend.

How to avoid repainting when using security() - viewing optionsHow to avoid repainting when using the security() - Edited PineCoders FAQ with more viewing options

This may be of value to a limited few, but I've introduced a set of Boolean inputs to PineCoders' original script because viewing all the various security lines at once was giving me a brain cramp. I wanted to study each behavior one-by-one. This version (also updated to PineScript v6) will allow users to selectively display each, or any combination, of the security plots. Each plot was updated to include a condition tied to its corresponding input, ensuring it only appears when explicitly enabled. The label-rendering logic only displays when its related plot is active; however, I've also added an input that allows you to remove all labels, enabling you to see the price action more clearly (the labels can sometimes obscure what you want to see). Run this script in replay mode to view the nuanced differences between the 12 methods while selecting/deselecting the desired plots (selecting all at once can be overcrowded and confusing).

All thanks and credit to PineCoders--these changes I made only provide more control over what’s shown on the chart without altering the core structure or intent of the original script. It helped me, so I thought I should share it. If I inadvertently messed something up, please let me know, and I will try to fix it.

I set the defaults for viewing monthly security functions on the daily timeframe. Only the first 2 security functions plot with the default settings, so change the settings as needed. Be sure to read the original notes and detailed explanations in the PineCoders posting "How to avoid repainting when using security() - PineCoders FAQ."

Bottom line, you should use one of the two functions: f_secureSecurity or f_security, depending on what you are trying to do. Hopefully, this script will make it a little easier for the visual learner to understand why (use replay mode or watch live price action on a lower timeframe).

EMA Percentile Rank [SS]Hello!

Excited to release my EMA percentile Rank indicator!

What this indicator does

Plots an EMA and colors it by short-term trend.

When price crosses the EMA (up or down) and remains on that side for three subsequent bars, the cross is “confirmed.”

At the moment of the most recent cross, it anchors a reference price to the crossover point to ensure static price targets.

It measures the historical distance between price and the EMA over a lookback window, separately for bars above and below the EMA.

It computes percentile distances (25%, 50%, 85%, 95%, 99%) and draws target bands above/below the anchor.

Essentially what this indicator does, is it converts the raw “distance from EMA” behavior into probabilistic bands and historical hit rates you can use for targets, stop placement, or mean-reversion/continuation decisions.

Indicator Inputs

EMA length: Default is 21 but you can use any EMA you prefer.

Lookback: Default window is 500, this is length that the percentiles are calculated. You can increase or decrease it according to your preference and performance.

Show Accumulation Table: This allows you to see the table that shows the hits/price accumulation of each of the percentile ranges. UCL means upper confidence and LCL means lower confidence (so upper and lower targets).

About Percentiles

A percentile is a way of expressing the position of a value within a dataset relative to all the other values.

It tells you what percentage of the data points fall at or below that value.

For example:

The 25th percentile means 25% of the values are less than or equal to it.

The 50th percentile (also called the median) means half the values are below it and half are above.

The 99th percentile means only 1% of the values are higher.

Percentiles are useful because they turn raw measurements into context — showing how “extreme” or “typical” a value is compared to historical behavior.

In the EMA Percentile Rank indicator, this concept is applied to the distance between price and the EMA. By calculating percentile distances, the script can mark levels that have historically been reached often (low percentiles) or rarely (high percentiles), helping traders gauge whether current price action is stretched or within normal bounds.

Use Cases

The EMA Percentile Rank indicator is best suited for traders who want to quantify how far price has historically moved away from its EMA and use that context to guide decision-making.

One strong use case is target setting after trend shifts: when a confirmed crossover occurs, the percentile bands (25%, 50%, 85%, 95%, 99%) provide statistically grounded levels for scaling out profits or placing stops, based on how often price has historically reached those distances. This makes it valuable for traders who prefer data-driven risk/reward planning instead of arbitrary point targets. Another use case is identifying stretched conditions — if price rapidly tags the 95% or 99% band after a cross, that’s an unusually large move relative to history, which could signal exhaustion and prompt mean-reversion trades or protective actions.

Conversely, if the accumulation table shows price frequently resides in upper bands after bullish crosses, traders may anticipate continuation and hold positions longer . The indicator is also effective as a trend filter when combined with its EMA color-coding : only taking trades in the trend’s direction and using the bands as dynamic profit zones.

Additionally, it can support multi-timeframe confluence (if you align your chart to the timeframes of interest), where higher-timeframe trend direction aligns with lower-timeframe percentile behavior for higher-probability setups. Swing traders can use it to frame pullbacks — entering near lower percentile bands during an uptrend — while intraday traders might use it to fade extremes or ride breakouts past the median band. Because the anchor price resets only on EMA crosses, the indicator preserves a consistent reference for ongoing trades, which is especially helpful for managing swing positions through noise .

Overall, its strength lies in transforming raw EMA distance data into actionable, probability-weighted levels that adapt to the instrument’s own volatility and tendencies .

Summary

This indicator transforms a simple EMA into a distribution-aware framework: it learns how far price tends to travel relative to the EMA on either side, and turns those excursions into percentile bands and historical hit rates anchored to the most recent cross. That makes it a flexible tool for targets, stops, and regime filtering, and a transparent way to reason about “how stretched is stretched?”—with context from your chosen market and timeframe.

I hope you all enjoy!

And as always, safe trades!

(Fixed-Range) Anchored VWAPThis "Fixed-Range Anchored VWAP" indicator allows traders full control over where the VWAP calculation begins and ends. VWAP combines both price and volume to reflect the true average price paid, often serving as a benchmark for gauging value, sentiment, and trend strength.

With this tool, traders can anchor VWAP to any candle, optionally define an end point, or keep it running forward with a single toggle. Up to three bands can be added around VWAP, either as standard deviations or percentage offsets.

How to Use

The indicator is particularly useful for analyzing VWAP around significant events, like earnings announcements or sharp price swings, to identify support, resistance, and mean-reversion opportunities.

Add the indicator and select a candle to set the Anchor.

Choose an End point or enable Cancel End for an open-ended VWAP.

Pick Std Dev or Percent for band mode.

Turn on up to three bands, adjust multipliers, and set fill colors.

Use VWAP and its bands to evaluate extensions, trend context, and fair value zones.

SMA-Based Candle Color 60The Trend SMA colors the moving average green when sloping upward and red when sloping downward. Candles are also colored based on whether price is above (green) or below (red) the SMA, making trends easy to spot.

REMS Snap Shot OverlayThe REMS Snap Shot indicator is a multi-factor, confluence-based system that combines momentum (RSI, Stochastic RSI), trend (EMA, MACD), and optional filters (volume, MACD histogram, session time) to identify high-probability trade setups. Signals are only triggered when all enabled conditions align, giving the trader a filtered, visually clear entry signal.

This indicator uses an optional 'look-back' feature where in it will signal an entry based on the recency of specified cross events.

To use the indicator, select which technical indicators you wish to filter, the session you wish to apply (default is 9:30am - 4pm EST, based on your chart time settings), and if which cross events you wish to trigger a reset on the cooldown.

The default settings filter the 4 major technical indicators (RSI, EMAs, MACD, Stochastic RSI) but optional filters exist to further fine tune Stochastic Range, MACD momentum and strength, and volume, with optional visual cues for MACD position, Stochastic RSI position, and volume.

EMAs can be drawn on the chart from this indicator with optional shaded background.

This indicator is an alternative to REMS First Strike, which uses a recency filter instead of a cool down.

REMS First Strike OverlayThe REMS First Strike indicator is a multi-factor, confluence-based system that combines momentum (RSI, Stochastic RSI), trend (EMA, MACD), and optional filters (volume, MACD histogram, session time) to identify high-probability trade setups. Signals are only triggered when all enabled conditions align, giving the trader a filtered, visually clear entry signal.

This indicator uses an optional 'cool down' feature where in it will signal an entry only after any of the specified cross events occur.

To use the indicator, select which technical indicators you wish to filter, the session you wish to apply (default is 9:30am - 4pm EST, based on your chart time settings), and if which cross events you wish to trigger a reset on the cooldown.

The default settings filter the 4 major technical indicators (RSI, EMAs, MACD, Stochastic RSI) but optional filters exist to further fine tune Stochastic Range, MACD momentum and strength, and volume, with optional visual cues for MACD position, Stochastic RSI position, and volume.

EMAs can be drawn on the chart from this indicator with optional shaded background.

This indicator is an alternative to REMS Snap Shot, which uses a recency filter instead of a cool down.