JPM VIX Signal - Non OverlayJPMorgan Chase & Co . strategists have identified what they say is a near bulletproof indicator to strengthen their argument that stock markets are poised to rally.

The buy signal is triggered when the Cboe Volatility Index ( VIX ) rises by more than 50% of its 1-month (30 day) moving average, which it last did on January 25th 2022, according to the strategists led by Mislav Matejka. The indicator has proven 100% accurate outside of recessions over the last three decades.

Instructions:

Symbol - SPY

Timeframe - Daily

Signal - Indicator exceeds horizontal line of 1.5

Cari dalam skrip untuk "同花顺软件+美国+VIX+恐慌指数+行情代码"

Velocity To Inverse Correlation to VIX/Bonds Strategy (2020)This strategy measures and creates a signal when an asset is moving out of a correlation with high yield bonds or the CBOE VIX into an inverse correlation, as well as when an asset is losing correlation with a top corporate bonds ETF. When this signal is triggered, the simulation has the portfolio asset go long.

Additionally, exits are based on a 2% stop loss and a 2% take profit for simplicity sake to indicate whether the direct next move in the asset is up or down.

This was originally tested as a descent indicator for Ethereum's 2020 moves as institutional investors moved into the market.

Finnie's RSI + 3EMA crossover + MFI + Vix Fix-added a medium and long term rsiEMA, in addition to the previous short term, except this time there's a visual crossover :)

-added CM Williams vix fix

-and finally just a general visual overhaul!

SPY Expected Move by VIXThis indicator shows 1 and 2 standard deviation price move from the VWAP based on VIX. Implied Volatility (IV) is being used extensively in the Option world to project the Expected Move for the underlying instrument. VIX is used as a proxy for SPY's IV for 30 days.

This indicator is meaningful only for SPY but can be used in any other instrument which has a strong correlation to SPY.

Williams Vix Fix paired with Supertrend HeatmapThis script shows my mod of the powerful Williams' Vix Fix indicator paired with a modified Supertrend Heatmap, originally created by Daveatt.

Combo Williams Vix Fix (Twin version)This is a very powerful Williams' Vix Fix indicator.

My implementation of this wonderful indicator features both up and down movements. Both up & down flavors have two versions (fields tp and tp2, each having two values). Color can be reversed as desired (rev). By default colors show continuation, reversed colors show reversion (as intended originally).

VIX OscillatorVIX Oscillator for catching vol signals on the same chart as your index of choice.

- Configurable levels that alert you when certain thresholds are broken

- Shaded background that make it simple to tell when you are in low vol/high vol regimes

- Moving line tracking price so that you can easily see bull/bear divergences against SPX building

VIX Regime AnalyzerVIX Regime Analyzer

The VIX Regime Analyzer is an analytical tool that examines historical VIX patterns to provide insights into how your asset typically performs under similar volatility conditions.

Key Features:

Historical Pattern Matching: Automatically scans up to 1,000 bars of history to find all periods when VIX was at levels similar to today, using customizable tolerance ranges (absolute or percentage-based).

Forward-Looking Statistics: For each VIX regime match, calculates what actually happened to your asset over the next 1, 5, 10, and 20 trading days, providing both average returns and probability of positive outcomes.

Regime Classification System: Intelligently categorizes the current market environment as bullish or bearish: Visual Historical Context:

Background shading throughout your chart highlights every historical period when VIX matched current levels, color-coded by subsequent performance (green for gains, red for losses).

User Inputs:

VIX Level Tolerance (+/-): How closely VIX must match (default: ±5 points)

Use Relative Tolerance (%): Switch to percentage-based matching for consistency across different VIX levels

Lookback Period: How many bars to analyze

Highlight Historical VIX Matches: Toggle background highlighting of past matching periods

The Data Table

The statistics box appears in the right handside of your chart and contains three main sections:

Section 1: VIX REGIME

Current VIX: The live VIX closing price

Range: The tolerance band being searched (e.g., if VIX is 18 with ±5 tolerance, range is 13-23)

Historical Samples: Number of matching periods found in the lookback window (minimum 10 required for statistical validity)

Section 2: FORWARD RETURN

Shows the average percentage change in your asset over different timeframes following similar VIX levels:

Avg Next Day: What typically happened by the next trading session

Avg Next 5 Days: Average 5-day forward performance

Avg Next 10 Days: Average 10-day forward performance

Avg Next 20 Days: Average 20-day forward performance (approximately 1 month)

Section 3: PROBABILITY UP

Shows the win rate - the percentage of times your asset closed higher after VIX matched current levels:

Next Day: Probability of being up the next session

Next 5 Days: Probability of being up after 5 days

Next 10 Days: Probability of being up after 10 days

Next 20 Days: Probability of being up after 20 days

Colors:

🟢 Green: Bullish regimes (various strengths)

🔴 Red: Bearish regimes (various strengths)

🟡 Yellow: Choppy/uncertain regime

When "Highlight Historical VIX Matches" is enabled:

Scroll back through your chart and you'll see colored backgrounds highlighting every period when VIX matched today's level. The color tells you whether that match led to gains (green) or losses (red). This provides instant visual pattern recognition - you can quickly see if similar VIX levels historically led to bullish or bearish outcomes.

Practical Example:

If you see that most historical periods with similar VIX levels are highlighted in green, it suggests the current VIX level has historically been a bullish signal for your asset.

How The Indicator Makes Decisions

The regime classification uses both magnitude AND probability to avoid false signals:

Example of Strong Classification:

Average 5-day return: +1.5%

Win rate: 65%

Result: STRONG BULLISH (both high return and high probability)

Example of Weak Signal:

Average 5-day return: +2.0%

Win rate: 35%

Result: CHOPPY (high average but low consistency = unreliable)

This dual-factor approach ensures the indicator doesn't mislead you with regimes that had a few huge winners but mostly losers, or vice versa.

Best Practices

Combine with your existing strategy: Use this as a regime filter rather than standalone signals

Check sample size: More historical matches = more reliable statistics

Consider multiple timeframes: If 5-day and 20-day metrics disagree, proceed with caution

Asset-specific tuning: Different assets may require different tolerance settings

VIX spikes: The indicator is particularly useful during VIX spikes to understand if panic is justified

What Makes This Different

Unlike simple VIX indicators that just plot the fear index, this tool:

Quantifies the actual impact of VIX levels on YOUR specific asset

Provides probability-based forecasts rather than subjective interpretation

Shows historical context visually so you can see patterns at a glance

Uses rigorous statistical criteria to avoid false regime classifications

VIX/VVIX Spike RiskVIX/VVIX Spike Risk Analyzer

The VIX/VVIX Spike Risk Analyzer analyzes historical VIX behavior under similar market conditions to forecast future VIX spike risk.

By combining current VIX and VVIX levels as dual filters, it identifies historical precedents and calculates the probability and magnitude of VIX spikes over the next 1, 5, and 10 trading days.

IMPORTANT: This indicator must be applied to the VIX chart (CBOE:VIX) to function correctly.

Methodology

1. Dual-Filter Pattern Matching

The indicator uses both VIX and VVIX as simultaneous filters to identify historically analogous market conditions:

By requiring BOTH metrics to match historical levels, the indicator creates more precise market condition filters than using VIX alone. This dual-filter approach significantly improves predictive accuracy because:

VIX alone might be at 15, but VVIX can tell us if that 15 is stable (low VVIX) or explosive (high VVIX)

High VVIX + Low VIX often precedes major spikes

Low VVIX + Low VIX suggests sustained calm

2. Tolerance Settings

VIX Matching (Default: ±10% Relative)

Uses relative percentage matching for consistency across different VIX regimes

Example: VIX at 15 matches 13.5-16.5 (±10%)

Can switch to absolute tolerance (±5 points) if preferred

VVIX Matching (Default: ±10 Points Absolute)

Uses absolute point matching as VVIX scales differently

Example: VVIX at 100 matches 90-110

Can switch to relative percentage if preferred

3. Historical Analysis Window

The indicator scans up to 500 bars backward (limited by VVIX data availability) to find all historical periods where both VIX and VVIX were at similar levels. Each match becomes a "sample" for statistical analysis.

4. Forward-Looking Spike Analysis

For each historical match, the indicator measures VIX behavior over the next 1, 5, and 10 days

Display Metrics Explained

Average Highest Spike

Shows the average of the maximum VIX spikes observed.

Highest Single Spike

Shows the single largest spike ever recorded

Probability No 10% Spike

Shows what percentage of historical cases stayed BELOW a 10% spike:

Probability No 20% Spike

Shows what percentage of historical cases stayed BELOW a 20% spike:

Note : You'll see many more shaded bars than the sample count because each match creates up to 5 consecutive shaded bars (bars 1-5 after the match all "look back" and see it).

Short Volatility Strategies:

Enter when there's a LOW probability of big vol spikes based on today's metrics

Long Volatility Strategies

Enter when there's a HIGH probability of big vol spikes based on today's metrics

VIX and SKEW RSI Moving AveragesSKEW and VIX are both indicators of market volatility and risk, but they represent different aspects.

VIX (CBOE Volatility Index) :.

The VIX is a well-known indicator for predicting future market volatility. It is calculated primarily based on S&P 500 options premiums and indicates the degree of market instability and risk.

Typically, when the VIX is high, market participants view the future as highly uncertain and expect sharp volatility in stock prices. It is generally considered an indicator of market fear.

SKEW Index :.

The SKEW is a measure of how much market participants estimate the risk of future declines in stock prices, calculated by the CBOE (Chicago Board Options Exchange) and derived from the premium on S&P 500 options.

If the SKEW is high, market participants consider the risk of future declines in stock prices to be high. This generally indicates a "fat tail at the base" of the market and suggests that the market perceives it as very risky.

These indicators are used by market participants to indicate their concerns and expectations about future stock price volatility. In general, when the VIX is high and the SKEW is high, the market is considered volatile and risky. Conversely, when the VIX is low and the SKEW is low, the market is considered relatively stable and low risk.

Inverse Relationship between SKEW and VIX

It is often observed that there is an inverse correlation between SKEW and VIX. In general, the relationship is as follows

High VIX and low SKEW: When the VIX is high and the SKEW is low, the market is considered volatile while the risk of future stock price declines is low. This indicates that the market is exposed to sharp volatility, but market participants do not expect a major decline.

Low VIX and High SKEW: A low VIX and high SKEW indicates that the market is relatively stable, while the risk of future declines in stock prices is considered high. This indicates that the market is calm, but market participants are wary of a sharp future decline.

This inverse correlation is believed to be the result of market participants' psychology and expectations affecting the movements of the VIX and SKEW. For example, when the VIX is high, it is evident that the market is volatile, and under such circumstances, people tend to view the risk of a sharp decline in stock prices as low. Conversely, when the VIX is low, the market is considered relatively stable and the risk of future declines is likely to be higher.

SKEWVIX RSIMACROSS

In order to compare the trends of the SKEW and VIX, the 50-period moving average of the Relative Strength Index (RSI) was used for verification. the RSI is an indicator of market overheating or overcooling, and the 50-period moving average can be used to determine the medium- to long-term trend. This analysis reveals how the inverse correlation between the SKEW and the VIX relates to the long-term moving average of the RSI.

how to use

Moving Average Direction

Rising blue for VIXRSI indicates increased uncertainty in the market

Rising red for SKEWRSI indicates optimism and beyond

RSI moving average crossing

When the SKEW is dominant, market participants are considered less concerned about a black swan event (significant unexpected price volatility). This suggests that the market is stable and willing to take risks. On the other hand, when the VIX is dominant, it indicates increased market volatility. Investors are more concerned about market uncertainty and tend to take more conservative positions to avoid risk. The direction of the moving averages and the crossing of the moving averages of the two indicators can give an indication of the state of the market.

SKEW>VIX Optimistic/Goldilocks

VIX>SKEW Uncertainty/turbulence

The market can be judged as follows.

BestRegards

VIX Reference IndicatorHello everyone,

Releasing my VIX reference indicator.

What is it:

This indicator displays the current trading behaviour of the VIX.

It displays it in Z-Score Format along with identifying previous areas of reversal and displaying when the RSI is overbought or oversold on the VIX.

Who is it good for:

It is good for both day and swing traders who use the VIX in their trading plans.

It permits traders to look at different aspects of the VIX (RSI, Z-Score and Reversal areas) simultaneously while they are watching their current traded stock.

How does it work:

The indicator works by converting the VIX into a Z-Score (similar to bollinger bands).

It then plots the VIX out in Z-Score format in the indicator.

Because it is plotting the VIX based on Z-Score, it looks back to previous areas where the Z-Score led to a reversal (i.e. what was the lowest or highest Z-Score the VIX achieved in the lookback period before reversing).

It also looks at the RSI of the VIX. If the VIX RSI crosses at or above 70 (overbought), it will change the colour of the line to green. This means the VIX is overbought and will likely sell and thus, the thesis is, as the VIX sells, the stock you are trading should come up.

Below is a picture of the different aspects of the indicator:

Customaization:

Per usual, you can customize the colours and bands to your liking.

You are also able to specify the RSI length you want to look at as well as the Z-Score Reversal length and the timeframe length of the chart you are looking at.

The default settings are 75 Average Length lookback for the Z-Score Reversal and the Chart and 14 period RSI.

TIPS:

The most persuasive setups are when you get all 3 of the following:

1. A signal that supports the thesis (buy or sell) along with:

2. An RSI signal that supports the z-score signal along with:

3. The VIX trading at an extreme end of its Z-Score range

Example:

In the example above you will see the following conditions are met:

1. Z-Score historical reversal point identified (short)

2. VIX RSI is oversold (short)

3. VIX is at the bottom of its Z-Score range (short)

As always, I have done a quick tutorial video for your reference which you can see below:

Leave your questions/comments/requests below or on the video as I am always happy to get feedback on improvements and functionality.

Thank you everyone checking it out and safe trades!

VIX Spike StrategyThis script implements a trading strategy based on the Volatility Index (VIX) and its standard deviation. It aims to enter a long position when the VIX exceeds a certain number of standard deviations above its moving average, which is a signal of a volatility spike. The position is then exited after a set number of periods.

VIX Symbol (vix_symbol): The input allows the user to specify the symbol for the VIX index (typically "CBOE:VIX").

Standard Deviation Length (stddev_length): The number of periods used to calculate the standard deviation of the VIX. This can be adjusted by the user.

Standard Deviation Multiplier (stddev_multiple): This multiplier is used to determine how many standard deviations above the moving average the VIX must exceed to trigger a long entry.

Exit Periods (exit_periods): The user specifies how many periods after entering the position the strategy will exit the trade.

Strategy Logic:

Data Loading: The script loads the VIX data, both for the current timeframe and as a rescaled version for calculation purposes.

Standard Deviation Calculation: It calculates both the moving average (SMA) and the standard deviation of the VIX over the specified period (stddev_length).

Entry Condition: A long position is entered when the VIX exceeds the moving average by a specified multiple of its standard deviation (calculated as vix_mean + stddev_multiple * vix_stddev).

Exit Condition: After the position is entered, it will be closed after the user-defined number of periods (exit_periods).

Visualization:

The VIX is plotted in blue.

The moving average of the VIX is plotted in orange.

The threshold for the VIX, which is the moving average plus the standard deviation multiplier, is plotted in red.

The background turns green when the entry condition is met, providing a visual cue.

Sources:

The VIX is often used as a measure of market volatility, with high values indicating increased uncertainty in the market.

Standard deviation is a statistical measure of the variability or dispersion of a set of data points. In financial markets, it is used to measure the volatility of asset prices.

References:

Bollerslev, T. (1986). "Generalized Autoregressive Conditional Heteroskedasticity." Journal of Econometrics.

Black, F., & Scholes, M. (1973). "The Pricing of Options and Corporate Liabilities." Journal of Political Economy.

VIX Dashboard [NariCapitalTrading]Overview

This VIX Dashboard is designed to provide traders with a quick visual reference into the current volatility and trend direction of the market as measured by CBOE VIX. It uses statistical measures and indicators including Rate of Change (ROC), Average True Range (ATR), and simple moving averages (SMA) to analyze the VIX.

Components

ATR Period : The ATR Period is used to calculate the Average True Range. The default period set is 24.

Trend Period : This period is used for the Simple Moving Average (SMA) to determine the trend direction. The default is set to 48.

Speed Up/Down Thresholds : These thresholds are used to determine significant increases or decreases in the VIX’s rate of change, signaling potential market volatility spikes or drops. These are customizable in the input section.

VIX Data : The script fetches the closing price of the VIX from a specified source (CBOE:VIX) with a 60-minute interval.

Rate of Change (ROC) : The ROC measures the percentage change in price from one period to the next. The script uses a default period of 20. The period can be customized in the input section.

VIX ATR : This is the Average True Range of the VIX, indicating the daily volatility level.

Trend Direction : Determined by comparing the VIX data with its SMA, indicating if the trend is up, down, or neutral. The trend direction can be customized in the input section.

Dashboard Display : The script creates a table on the chart that dynamically updates with the VIX ROC, ATR, trend direction, and speed.

Calculations

VIX ROC : Calculated as * 100

VIX ATR : ATR is calculated using the 'atrPeriod' and is a measure of volatility.

Trend Direction : Compared against the SMA over 'trendPeriod'.

Trader Interpretation

High ROC Value : Indicates increasing volatility, which could signal a market turn or increased uncertainty.

High ATR Value : Suggests high volatility, often seen in turbulent market conditions.

Trend Direction : Helps in understanding the overall market sentiment and trend.

Speed Indicators : “Mooning” suggests rapid increase in volatility, whereas “Cratering” indicates a rapid decrease.

The interpretation of these indicators should be combined with other market analysis tools for best results.

VIX Futures Spread StrategyThis script was an exercise in learning Pinescript and exploring the futures curve of the VIX in relation to SPY. Was deleted by TV, trying to republish it now with updated parameters for slippage and commission and a more detailed description.

"VIX Futures Spread Strategy" is a trading strategy that capitalizes on the spread between the 3-month VIX futures (VIX3M) and the spot VIX index. This strategy is based on the idea that the VIX futures spread can serve as a contrarian indicator of market sentiment, with extreme negative spreads potentially signaling oversold conditions and opportunities for long positions.

Ordinarily the VIX curve is in contango as futures contracts are priced at a premium to the current spot price and are used to hedge future uncertainty in the market. When the spot price of VIX spikes the curve can invert and enter backwardation; this strategy detects this condition and uses it as a trigger to open a long position in SPY. The spread going negative tends to correlate with excessive fear and uncertainty in the short term while expecting lower volatility in the long term, in this case 3 months out.

The strategy is designed to enter a long position when the VIX futures spread is negative and to exit the position when the spread rises above 3 -- when the curve is in contango again. The strategy employs a pyramiding approach, allowing up to 10 additional orders to be placed while the entry condition is met, with each order consisting of 10 contracts. This approach aims to maximize potential profits during periods of favorable market conditions.

In this strategy, the VIX futures spread is calculated as the difference between the 3-month VIX futures (VIX3M) and the spot VIX index. The spread is plotted as a histogram on the chart, with the zero line representing no spread, and horizontal lines at 0 and 3 indicating the entry and exit thresholds, respectively.

The strategy's backtesting settings use an initial capital of HKEX:10 ,000, a commission of 0.5% per trade, and a maximum of 10 pyramiding orders, and a slippage of 2 ticks.

Please note that this strategy is intended for educational purposes and should not be considered as financial advice. Before using this strategy in live trading, make sure to thoroughly test and optimize its parameters to suit your risk tolerance and specific trading conditions.

India VIX Based Nifty/BankNifty Range Calculator (Auto Fetch)VIX-Based Expected Daily Range (Auto Volatility Forecast)

Created by: Harshiv Symposium

📖 Purpose

This indicator automatically fetches the India VIX value and calculates the expected daily price range for major Indian indices such as Nifty and BankNifty.

It helps traders understand how much the market is likely to move today based on current volatility conditions.

Designed for educational and analytical awareness, not for signals or profit-making systems.

⚙️ Core Logic

Expected Daily Move (Range) = (India VIX × Current Index Price) ÷ Multiplier

- Multiplier for Nifty: 1000

- Multiplier for BankNifty: 700

This calculation projects the 1-standard-deviation (≈ 68% probability) and 2-standard-deviation (≈ 95% probability) movement zones for the day.

📊 Example

If India VIX = 15 and Nifty = 25,000:

Expected Move ≈ (15 × 25,000) ÷ 1000 = 375 points

Hence,

- 68% Range: 24,625 – 25,375

- 95% Range: 24,250 – 25,750

This gives traders a realistic idea of daily volatility boundaries.

🧭 Key Features

✅ Auto-Fetch India VIX

No need for manual input — automatically pulls live data from NSE:INDIAVIX.

✅ Dynamic Range Visualization

Plots upper/lower boundaries for 1σ and 2σ probability zones with shaded expected-move area.

✅ Dashboard Panel

Displays:

- Current VIX

- Expected Move (in points and %)

- Upper and Lower Ranges

✅ Smart Alerts

Alerts when price crosses upper or lower volatility range — potential breakout signal.

🎯 How It Helps

Intraday Traders:

Know the likely daily movement (e.g., ±220 pts on Nifty) and plan realistic targets or stops.

Options Traders:

Quickly assess whether it’s a seller-friendly (low VIX, small range) or buyer-friendly (high VIX, large range) session.

Risk Managers:

Use volatility context for stop-loss width and position sizing.

Breakout Traders:

If price breaks beyond the 2σ range → indicates potential volatility expansion.

💡 Interpretation Guide

Condition Market Behavior Strategy Insight

VIX ↓ ( < 14 ) Calm / Range-bound Option Selling Edge

VIX ↑ ( > 20 ) Volatile Sessions Option Buying Edge

Price within Range Stable Market Mean Reversion Setups

Price breaks Range Volatility Expansion Breakout Trades

⚠️ Disclaimer

This indicator is for educational and awareness purposes only.

It does not generate buy/sell signals or guarantee returns.

Always apply your own analysis and risk management.

VIX Z-Score (Inverted)📘 Indicator: VIX Z-Score (Inverted) + Table

🔍 Overview

This indicator calculates the Z-Score of the VIX (Volatility Index) and inverts it to identify potential buying opportunities during periods of fear and caution during periods of extreme optimism. The Z-Score is smoothed and visually displayed alongside a dynamic info table.

⚙️ How It Works

VIX Data: The VIX (ticker: CBOE:VIX) is pulled in real time.

Z-Score Calculation:

𝑍

=

(

𝑉

𝐼

𝑋

−

mean

)

standard deviation

Z=

standard deviation

(VIX−mean)

Over a customizable lookback period (default: 50).

Inversion:

Since high VIX usually means fear (often a contrarian buying signal), we invert the Z-Score:

𝑍

inv

=

−

𝑍

Z

inv

=−Z

Smoothing:

An EMA is applied to reduce noise and false signals.

Clamping:

The Z-Score is linearly scaled and capped between +2 and -2 for easy visualization in the info table.

📊 Z-Score Table (Top-Right)

Range Interpretation Table Color

+1.5 to +2 Extreme fear → Buy zone 🟩 Green

+0.5 to +1.5 Moderate fear 🟨 Lime

–0.5 to +0.5 Neutral ⬜ Gray

–0.5 to –1.5 Growing complacency 🟧 Orange

–1.5 to –2 Extreme optimism → Caution 🟥 Red

The current Z-Score (clamped version) is shown in real time on the right-hand info panel.

🧠 How to Use It

+2 Zone (Table: Green):

Market fear is at an extreme. Historically, such conditions are contrarian bullish—possible entry zones.

–2 Zone (Table: Red):

Indicates extreme optimism and low fear. Often a signal to be cautious or take profits.

Middle range (±0.5):

Market is neutral. Avoid major decisions based solely on sentiment here.

🧪 Best Practices

Combine with price action, volume, or trend filters.

Works well on daily or 4H timeframes.

Not a standalone signal—best used to confirm or fade sentiment extremes.

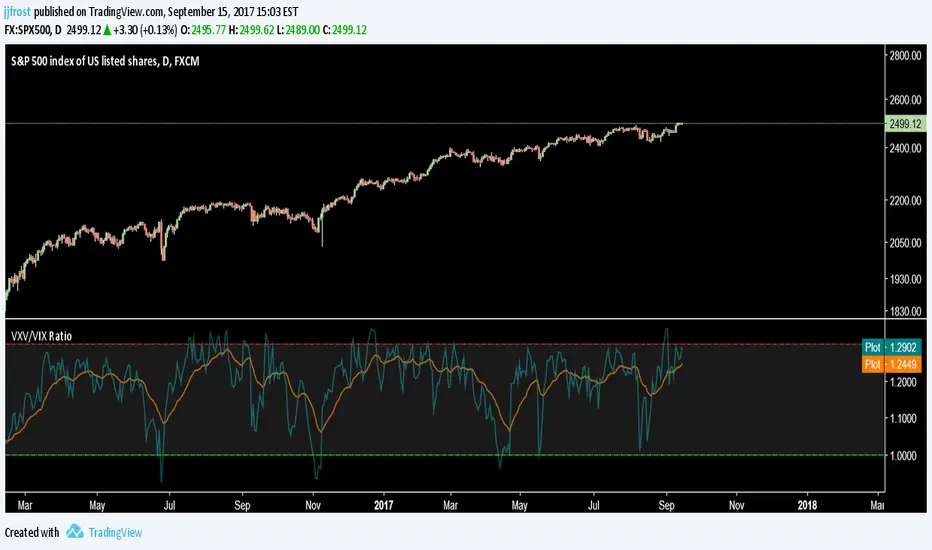

VIX OscillatorOVERVIEW

Plots an oscillating value as a percentage, derived from the VIX and VIX3M . This can help identify broader market trends and pivots on higher time frames (ie. 1D), useful when making swing trades.

DATA & MATH

The VIX is a real-time index of expected S&P 500 volatility over the next 30 days, derived from option prices with near-term expirations. Similarly, the VIX3M measures expected volatility over the next 90 days.

Dividing one by the other yields an oscillating value, normalizing the relative strength of the expected volatility. Most commonly the VIX is divided by the VIX3M. However, because the VIX is inversely correlated to market sentiment (typically), this indicator divides the VIX3M by the VIX to visually correlate the plot direction with the anticipated market direction. Further, it subtracts 1.1 from the quotient to visually center the plot, and multiplies that difference by 100 to amplify the value as a percentage:

( VIX3M / VIX - 1.1 ) * 100

This variation makes identifying sentiment extremes easier within a buy-low-sell-high paradigm, where values below zero are bearish and values above zero are bullish.

PLOTS

Two plots are used, maximizing data fidelity and convenience. Candles are used to accurately reflect the quantized math and a Linear Regression is used to simplify contextualization. If you're not familiar with what a Linear Regression is, you can think of it like a better moving average. High / Low zones are also plotted to help identify sentiment extremes.

This combination allows you to quickly identify the expected sentiment (bullish / bearish) and its relative value (normal / extreme), which you can then use to anticipate if a trend continuation or pivot is more likely.

INPUTS

Candle colors (rise and fall)

Linear regression colors and length

Zone thresholds and zero line

VIX Calm vs Choppy (Bar Version, VIX High Threshold)This indicator tracks market stability by measuring how long the VIX stays below or above a chosen intraday threshold. Instead of looking at VIX closes, it uses VIX high, so even a brief intraday spike will flip the regime into “choppy.”

The tool builds a running clock of consecutive bars spent in each regime:

Calm regime: VIX high stays below the threshold

Choppy regime: VIX high hits or exceeds the threshold

Calm streaks plot as positive bars (light blue background).

Choppy streaks plot as negative bars (dark pink background).

This gives a clean picture of how long the market has been stable vs volatile — useful for trend traders, breakout traders, and anyone who watches risk-on/risk-off conditions. A table shows the current regime and streak length for quick reference.

VIX OscillatorThis is my VIX Oscillator indicator.

About it:

This indicator takes the Z-Score of the VIX and of the current ticker you are on and presents them in the format of an oscillator.

Key parts of the indicator:

A diagram of the key elements of the indicator are displayed above.

Purple Line: Represents the Z-Score of the current Ticker.

Blue Line: Represents the Z-Score of the VIX

Green fill line: Represents bullish divergence

Red fill line: Represents bearish divergence

How to use it:

Characteristics for long entries:

- Look for recent bullish divergence (green fill line)

- Look for the ticker line (purple line) to be holding above 0 (neutrality)

- look for a bullish cross (purple line (ticker) crossing over blue line (VIX))

Characteristics for short entries:

- Look for recent Bearish divergence

- Look for the VIX line (blue line) to be holding above 0 and the Ticker

- Look for the ticker line to be holding below 0

- Look for a bearish cross (blue crossing above purple)

Some principles:

The bands represent oversold, overbought and neutral.

0 is absolute neutrality. No bias here.

Anything towards + 2.5 is considered normal, moving towards overbought (2.5 or higher).

Anything towards -2.5 is considered normal, moving towards oversold (-2.5 or lower).

+2.5 or higher is overbought.

-2.5 or lower is oversold.

As always, I have prepared a quick tutorial video for your reference of this indicator:

Please let me know your questions, comments or suggestions about this indicator below.

Thank you for checking it out!