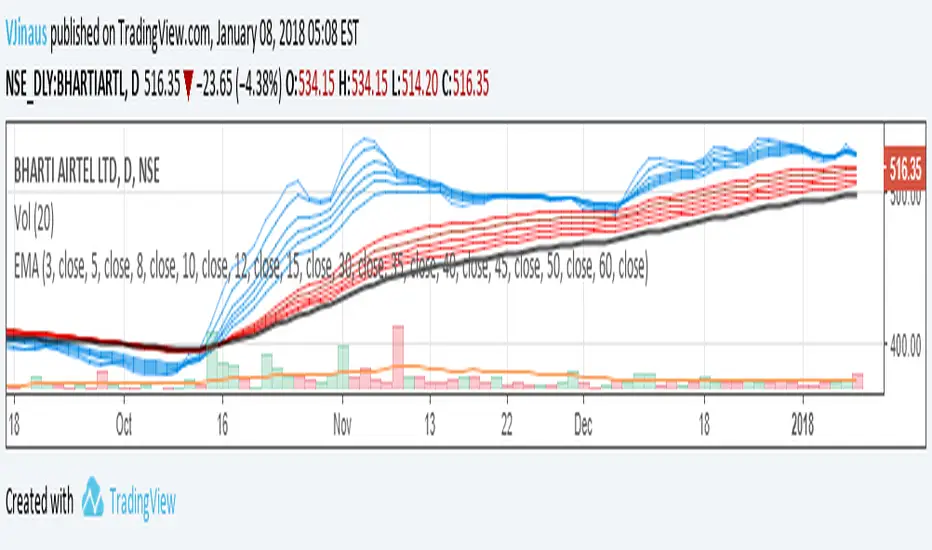

Guppy MMA 3, 5, 8, 10, 12, 15 and 30, 35, 40, 45, 50, 60Guppy Multiple Moving Average

Short Term EMA 3, 5, 8, 10, 12, 15

Long Term EMA 30, 35, 40, 45, 50, 60

Use for SFTS Class

Cari dalam skrip untuk "大位科技同行业可替代股票的技术面分析数据(如5日均线、10日均线、支撑位、压力位)"

10 EMA + 20 EMA + Previous Day High/Low (Day-Bounded)it gives the reand and also plot the day's lowest volume.it is very helpful in reversals

10/21 EMA + 50/200 Daily SMAAll four relevant moving averages in one script to allow you to add move indicators.

10MAs + BB10 MAs riboon + Bollinger Bands

I used two basic Multiple MA ribbons. so I just merge them to one indicaotor

10-2 Year Treasury Yield Spread by zdmreLong-term bond yield reflects inflation. Short-term bond yields are tools used to predict Fed's interest rate policy. Spread between the two represents four cycles of an economy.

1. Growth

Short-term yield rises as interest rates rise. Spread narrows.

2. Slow growth

Central bank raises interest rates faster and short-term yield exceeds long-term yield. Spread turns negative.

3. Recession

High interest rates lead to more defaults. Inflation caps consumption. Central bank lowers interest rate to stimulate the economy and short-term yield falls. Spread widens.

4. Recovery

Central bank continues easing. Spread remains wide and yield curve remains steep.

0 = Recession Risk

2.6 = Recovery Plan

DYOR

6 Figures Scalping 2x MACD10-11-2019

This script plots a double MACD in a new indicator pane

The default settings:

Pink = STD MACD , settings 12-26-9

Green - Fast MACD, settings 5-15-1

The MACD settings can be changed in the indicators setting window

10/20/50/100/200 SMA'sMultiple MA's to get a good feel for momentum and interim supports and resistances

Moving Average x10 (SMA, EMA)10 configurable Simple and Exponential moving averages combined in one indicator

SMA RIBBON10 SMA's arranged in a ribbon. Color coded depending on price close. Free to use, open source. As seen in some charts.

10Y Bond Yield Spread (beta)10-Year Bond Yield Spread using Quandl data

See also:

- seekingalpha.com

- www.babypips.com

- www.forexfactory.com

10 Simple & 6 Exponential Moving Averages (w/ 18 day,week,month)* This is for the trader who wants tons of moving averages on their chart from one indicator

* Using the options, you should be able ot turn off some of them if the screen is too noisy for you

* You should also be able to change colors and thickness of the bars

* The thicker bars are for longer term averages

* This version is similar to my other script except it adds the 18 day, 18 week, and 18 Month SMa

* I added them after watching ira Epstein's YouTube videos

* Let me know if there are any bugs or things that need to be change