Transformer Flux DashboardHere’s a practical guide to what your Transformer Flux Dashboard does and how to use it.

What it is

A compact, two-column trading dashboard + signal pack that blends trend, MACD, and OBV into one view (“Flux Score”) and adds session awareness (pre-sessions and main sessions in Eastern time). It’s designed for regular candles by default and avoids repaint by letting you confirm on bar close.

Core pieces it calculates

Moving Averages

Two MAs: Fast (HMA/EMA) and Slow (HMA/EMA).

You choose length, line width, color, and transparency.

Trend engine (Strict/Lenient)

Uses the relation between Fast/Slow MA and a debounced fast-MA slope filter (slope > ATR×buffer).

Strict: requires fast>slow and slow rising (or the inverse for down).

Lenient: fast>slow or slow rising (or the inverse).

A confirmation window (bars) must hold true before trend flips. That window can be auto-tuned by session (Asia/London/NY) or set globally.

OBV confirmation (optional)

OBV smoothed by SMA; needs to be rising/falling for N bars (also session-aware if you enable presets).

MACD

Standard MACD Fast/Slow/Signal; the dashboard shows Bull ▲, Bear ▼ or Flat based on line vs signal.

Flux Score (top row)

A composite, smoothed gauge from 0–100:

40% Trend, 30% MACD, 30% OBV → EMA(3) smoothed.

Labels: Bullish ≥ 70, Bearish ≤ 30, otherwise Neutral.

Summary line explains why (e.g., “MACD↑, OBV↑, Trend up”).

Sessions & zones (Eastern/NY time)

Recognizes Asia / London / New York main sessions and pre-sessions using your chart’s Eastern time.

Session label (top of chart): text is white; background auto-matches the current session color (or your manual color).

Zone backgrounds (optional): off by default; when on, default transparency ≈ 95% (very light), with separate colors for each session and pre-session. A toggle lets you draw pre-session on top or beneath main sessions.

Signals & markers

Two strength tiers: Strong (Trend + OBV + MACD aligned) and Weak (2 of the 3 agree).

To reduce clutter, markers only appear on direction shifts (from last visible direction to a new one), and you can enforce a minimum bar gap.

Marker style:

Default Icons with LabelUp/LabelDown (tiny).

Colors: strong long = bright white by default; others configurable.

Weak markers are slightly offset from price using ATR so they don’t overlap wicks.

Dashboard (2-column)

Left column = label, right column = value:

Flux Score: numeric + Bullish/Neutral/Bearish tag.

Summary: short reason of the score.

Trend: UP / DOWN / FLAT (cell tinted green/red/gray).

MACD: Bull ▲ / Bear ▼ / Flat (tinted).

Signal: last printed signal + bar age (fresh signals get a lighter tint).

MA: slow MA type/length and up/down arrow.

Sess: current session label (e.g., “Pre-London”, “New York”).

VIX / VXN (optional): shows current value.

Auto tint: based on calm/watch/elevated thresholds (you control levels and colors).

Manual tint: fixed BG color if you prefer consistency.

Params: “P”=trend bars, “O”=OBV bars, mode (Strict/Lenient), and “Candles”.

You can set a global Default Transparency for the dashboard cells.

Key settings to know

Confirm On Close: when on (default), trend/OBV/MACD states use the last confirmed bar; this avoids mid-bar flicker and reduces repaint risk.

Session presets: when enabled, the number of bars required for confirmations tightens/loosens per session (e.g., Asia uses more bars than NY).

Colors & Opacity:

MA lines have their own transparency (default 0 = fully opaque).

Dashboard cells use a single global transparency (default 40%).

Session zones default to very light (95%) and are off by default.

VIX/VXN cells can auto-color by regime or use a manual background.

Markers:

“Icons” vs “Ticks.” Default is Icons with tiny labels up/down.

“Shift only” display reduces noise; you can also set min bar spacing.

How to read it (quick workflow)

Flux Score row: a fast “risk-on/off” gauge.

≥70 with green Trend/MACD cells → higher-conviction long context.

≤30 with red Trend/MACD cells → higher-conviction short context.

Summary explains why the score is what it is.

Signal row: tells you the last official signal and how many bars ago it fired. Fresh signals tint lighter.

MA row: aligns your slow baseline; arrow helps spot slow-turns early.

Sess row + label: know which market is active; behavior and your confirmation bars adapt by session if presets are on.

VIX/VXN (if enabled): extra context for risk regime (values and color band).

Good practices & caveats

It’s confirmation-based to reduce false flips; you’ll get signals slightly later, by design.

All signals are informational; there’s no position management or stops in this build (we removed the stop visuals by request).

If you switch to exotic chart types or extreme resolutions, re-tune lengths and confirmation bars (and potentially disable session presets).

For scalping, consider reducing confirmation bars and OBV smoothing; for higher timeframes, increase them.

Quick customization ideas

Want faster flips? Lower confirmBars and obvBars, increase slope buffer a bit to retain quality.

Want fewer weak signals? Show only strong markers (toggle off weak via colors/visibility or increase min bar gap).

Prefer EMA stacking? Set both Fast/Slow to EMA.

Don’t care about OBV? Turn OBV confirm off; Trend + MACD will drive

Cari dalam skrip untuk "如何用wind搜索股票的发行价和份数"

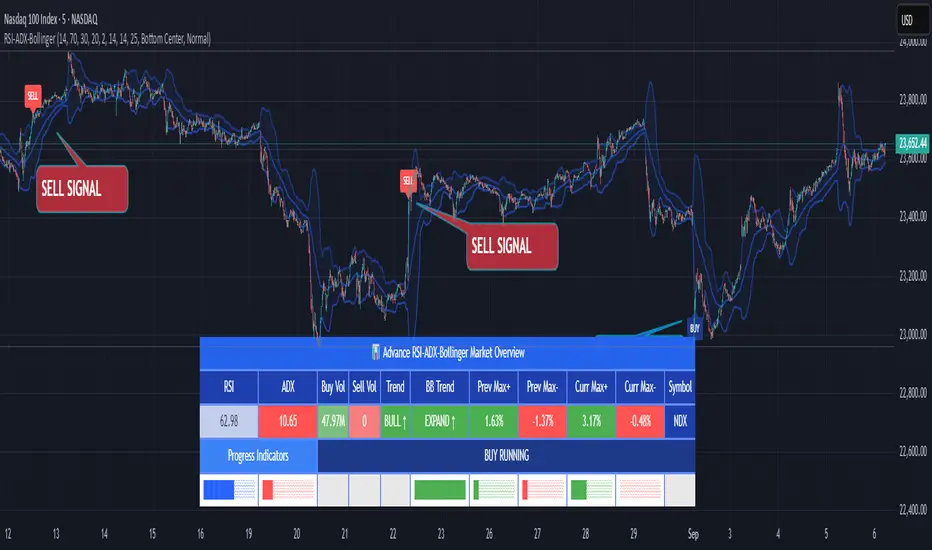

RSI ADX Bollinger Analysis High-level purpose and design philosophy

This indicator — RSI-ADX-Bollinger Analysis — is a compact, educational market-analysis toolkit that blends momentum (RSI), trend strength (ADX), volatility structure (Bollinger Bands) and simple volumetrics to provide traders a snapshot of market condition and trade idea quality. The design philosophy is explicit and layered: use each component to answer a different question about price action (momentum, conviction, volatility, participation), then combine answers to form a more robust, explainable signal. The mashup is intended for analysis and learning, not automatic execution: it surfaces the why behind signals so traders can test, learn and apply rules with risk management.

________________________________________

What each indicator contributes (component-by-component)

RSI (Relative Strength Index) — role and behavior: RSI measures short-term momentum by comparing recent gains to recent losses. A high RSI (near or above the overbought threshold) indicates strong recent buying pressure and potential exhaustion if price is extended. A low RSI (near or below the oversold threshold) indicates strong recent selling pressure and potential exhaustion or a value area for mean-reversion. In this dashboard RSI is used as the primary momentum trigger: it helps identify whether price is locally over-extended on the buy or sell side.

ADX (Average Directional Index) — role and behavior: ADX measures trend strength independently of direction. When ADX rises above a chosen threshold (e.g., 25), it signals that the market is trending with conviction; ADX below the threshold suggests range or weak trend. Because patterns and momentum signals perform differently in trending vs. ranging markets, ADX is used here as a filter: only when ADX indicates sufficient directional strength does the system treat RSI+BB breakouts as meaningful trade candidates.

Bollinger Bands — role and behavior: Bollinger Bands (20-period basis ± N standard deviations) show volatility envelope and relative price position vs. a volatility-adjusted mean. Price outside the upper band suggests pronounced extension relative to recent volatility; price outside the lower band suggests extended weakness. A band expansion (increasing width) signals volatility breakout potential; contraction signals range-bound conditions and potential squeeze. In this dashboard, Bollinger Bands provide the volatility/structural context: RSI extremes plus price beyond the band imply a stronger, volatility-backed move.

Volume split & basic MA trend — role and behavior: Buy-like and sell-like volume (simple heuristic using close>open or closeopen) or sell-like (close1.2 for validation and compare win rate and expectancy.

4. TF alignment: Accept signals only when higher timeframe (e.g., 4h) trend agrees — compare results.

5. Parameter sensitivity: Vary RSI threshold (70/30 vs 80/20), Bollinger stddev (2 vs 2.5), and ADX threshold (25 vs 30) and measure stability of results.

These exercises teach both statistical thinking and the specific failure modes of the mashup.

________________________________________

Limitations, failure modes and caveats (explicit & teachable)

• ADX and Bollinger measures lag during fast-moving news events — signals can be late or wrong during earnings, macro shocks, or illiquid sessions.

• Volume classification by open/close is a heuristic; it does not equal TAPEDATA, footprint or signed volume. Use it as supportive evidence, not definitive proof.

• RSI can remain overbought or oversold for extended stretches in persistent trends — relying solely on RSI extremes without ADX or BB context invites large drawdowns.

• Small-cap or low-liquidity instruments yield noisy band behavior and unreliable volume ratios.

Being explicit about these limitations is a strong point in a TradingView description — it demonstrates transparency and educational intent.

________________________________________

Originality & mashup justification (text you can paste)

This script intentionally combines classical momentum (RSI), volatility envelope (Bollinger Bands) and trend-strength (ADX) because each indicator answers a different and complementary question: RSI answers is price locally extreme?, Bollinger answers is price outside normal volatility?, and ADX answers is the market moving with conviction?. Volume participation then acts as a practical check for real market involvement. This combination is not a simple “indicator mashup”; it is a designed ensemble where each element reduces the others’ failure modes and together produce a teachable, testable signal framework. The script’s purpose is educational and analytical — to show traders how to interpret the interplay of momentum, volatility, and trend strength.

________________________________________

TradingView publication guidance & compliance checklist

To satisfy TradingView rules about mashups and descriptions, include the following items in your script description (without exposing source code):

1. Purpose statement: One or two lines describing the script’s objective (educational multi-indicator market overview and idea filter).

2. Component list: Name the major modules (RSI, Bollinger Bands, ADX, volume heuristic, SMA trend checks, signal tracking) and one-sentence reason for each.

3. How they interact: A succinct non-code explanation: “RSI finds momentum extremes; Bollinger confirms volatility expansion; ADX confirms trend strength; all three must align for a BUY/SELL.”

4. Inputs: List adjustable inputs (RSI length and thresholds, BB length & stddev, ADX threshold & smoothing, volume MA, table position/size).

5. Usage instructions: Short workflow (check TF alignment → confirm participation → define stop & R:R → backtest).

6. Limitations & assumptions: Explicitly state volume is approximated, ADX has lag, and avoid promising guaranteed profits.

7. Non-promotional language: No external contact info, ads, claims of exclusivity or guaranteed outcomes.

8. Trademark clause: If you used trademark symbols, remove or provide registration proof.

9. Risk disclaimer: Add the copy-ready disclaimer below.

This matches TradingView’s request for meaningful descriptions that explain originality and inter-component reasoning.

________________________________________

Copy-ready short publication description (paste into TradingView)

Advanced RSI-ADX-Bollinger Market Overview — educational multi-indicator dashboard. This script combines RSI (momentum extremes), Bollinger Bands (volatility envelope and band expansion), ADX (trend strength), simple SMA trend bias and a basic buy/sell volume heuristic to surface high-quality idea candidates. Signals require alignment of momentum, volatility expansion and rising ADX; volume participation is displayed to support signal confidence. Inputs are configurable (RSI length/levels, BB length/stddev, ADX length/threshold, volume MA, display options). This tool is intended for analysis and learning — not for automated execution. Users should back test and apply robust risk management. Limitations: volume classification here is a heuristic (close>open), ADX and BB measures lag in fast news events, and results vary by instrument liquidity.

________________________________________

Copy-ready risk & misuse disclaimer (paste into description or help file)

This script is provided for educational and analytical purposes only and does not constitute financial or investment advice. It does not guarantee profits. Indicators are heuristics and may give false or late signals; always back test and paper-trade before using real capital. The author is not responsible for trading losses resulting from the use or misuse of this indicator. Use proper position sizing and risk controls.

________________________________________

Risk Disclaimer: This tool is provided for education and analysis only. It is not financial advice and does not guarantee returns. Users assume all risk for trades made based on this script. Back test thoroughly and use proper risk management.

FX Sessions (DTS)FX Sessions (DST-Safe)

This indicator highlights the four main Forex trading sessions — Sydney, Tokyo, London, and New York — using the local timezone of each market.

• DST handled automatically: Sessions shift correctly when London or New York move clocks forward/back.

• Clear visualization: Light background shading for each session, with the London–New York overlap emphasized for peak liquidity.

• Customizable: Toggle individual sessions, labels, and the on-chart legend table.

• Intraday focus: Works best on lower timeframes (1m–1h) for identifying active trading hours and volatility windows.

Use this tool to instantly spot when liquidity and volatility are likely to increase, so you know where to focus your trading.

[GrandAlgo] Moving Averages Cross LevelsMoving Averages Cross Levels

Many traders watch for moving average crossovers – such as the golden cross (50 MA crossing above 200 MA) or death cross – as signals of changing trends. However, once a crossover happens, the exact price level where it occurred often fades from view, even though that level can be an important reference point. Moving Averages Cross Levels is an indicator that keeps those crossover price levels visible on your chart, helping you track where momentum shifts occurred and how price behaves relative to those key levels.

This tool plots horizontal line segments at the price where each pair of selected moving averages crossed within a recent window of bars. Each level is labeled with the moving average lengths (for example, “21×50” for a 21/50 MA cross) and is color-coded – green for bullish crossovers (short-term MA crossing above long-term MA) and red for bearish crossunders (short-term crossing below). By visualizing these crossover levels, you can quickly identify past trend change points and use them as potential support/resistance or decision levels in your trading. Importantly, this indicator is non-repainting – once a crossover level is plotted, it remains fixed at the historical price where the cross occurred, allowing you to continually monitor that level going forward. (As with any moving average-based analysis, crossover signals are lagging, so use these levels in conjunction with other tools for confirmation.)

Key Features:

✅ Multiple Moving Averages: Track up to 7 different MAs (e.g. 5, 8, 21, 50, 64, 83, 200 by default) simultaneously. You can enable/disable each MA and set its length, allowing flexible combinations of short-term and long-term averages.

✅ Selectable MA Type: Each average can be calculated as a Simple (SMA), Exponential (EMA), Volume-Weighted (VWMA), or Smoothed (RMA) moving average, giving you flexibility to match your preferred method.

✅ Auto Crossover Detection: The script automatically detects all crosses between any enabled MA pairs, so you don’t have to specify pairs manually. Whether it’s a fast cross (5×8) or a long-term cross (50×200), every crossover within the lookback period will be identified and marked.

✅ Horizontal Level Markers: For each detected crossover, a horizontal line segment is drawn at the exact price where the crossover occurred. This makes it easy to glance at your chart and see precisely where two moving averages intersected in the recent past.

✅ Labeled and Color-Coded: Each crossover line is labeled with the two MA lengths that crossed (e.g. “50×200”) for clear identification. Colors indicate crossover direction – by default green for bullish (positive) crossovers and red for bearish (negative) crossovers – so you can tell at a glance which way the trend shifted. (You can customize these colors in the settings.)

✅ Adjustable Lookback: A “Crosses with X candles” input lets you control how far back the script looks for crossovers to plot. This prevents your chart from getting cluttered with too many old levels – for example, set X = 100 to show crossovers from roughly the last 100 bars. Older crossover lines beyond this lookback window will automatically clear off the chart.

✅ Optional MA Plots: You can toggle the display of each moving average line on the chart. This means you can either view just the crossover levels alone for a clean look, or also overlay the MA curves themselves for additional context (to see how price and MAs were moving around the crossover).

✅ No Repainting or Hindsight Bias: Once a crossover level is plotted, it stays at that fixed price. The indicator doesn’t move levels around after the fact – each line is a true historical event marker. This allows you to backtest visually: see how price acted after the crossover by observing if it retested or respected that level later.

How It Works:

1️⃣ Add to Chart & Configure – Simply add the indicator to your chart. In the settings, choose which moving averages you want to include and set their lengths. For example, you might enable 21, 50, 200 to focus on medium and long-term crosses (including the golden cross), or turn on shorter MAs like 5 and 8 for quick momentum shifts. Adjust the lookback (number of bars to scan for crosses) if needed.

2️⃣ Visualization – The script continuously checks the latest X bars for any points where one MA crossed above or below another. Whenever a crossover is found, it calculates the exact price level at which the two moving averages intersected. On the last bar of your chart, it will draw a horizontal line segment extending from the crossover bar to the current bar at that price level, and place a label to the right of the line with the MA lengths. Green lines/labels signify bullish crossovers (where the first MA crossed above the second), and red lines indicate bearish crossunders.

3️⃣ On Your Chart – You will see these labeled levels aligned with the price scale. For example, if a 50 MA crossed above a 200 MA (bullish) 50 bars ago at price $100, there will be a green “50×200” line at $100 extending to the present, showing you exactly where that golden cross happened. You might notice price pulling back near that level and bouncing, or if price falls back through it, it could signal a failed crossover. The indicator updates in real-time: if a new crossover happens on the latest bar, a new line and label will instantly appear, and if any old cross moves out of the lookback range, its line is removed to keep the chart focused.

4️⃣ Customization – You can fine-tune the appearance: toggle any MA’s visibility, change line colors or label styles, and modify the lookback length to suit different timeframes. For instance, on a 1-hour chart you might use a lookback of 500 bars to see a few weeks of cross history, whereas on a daily chart 100 bars (about 4–5 months) may be sufficient. Adjust these settings based on how many crossover levels you find useful to display.

Ideal for Traders Who:

Use MA Crossovers in Strategy: If your strategy involves moving average crossovers (for trend confirmation or entry/exit signals), this indicator provides an extra layer of insight by keeping the price of those crossover events in sight. For example, trend-followers can watch if price stays above a bullish crossover level as a sign of trend strength, or falls below it as a sign of weakness.

Identify Support/Resistance from MA Events: Crossover levels often coincide with pivot points in market sentiment. A crossover can act like a regime change – the level where it happened may turn into support or resistance. This tool helps you mark those potential S/R levels automatically. Rather than manually noting where a golden cross occurred, you’ll have it highlighted, which can be useful for setting stop-losses (e.g. below the crossover price in a bullish scenario) or profit targets.

Track Multiple Averages at Once: Instead of focusing on just one pair of moving averages, you might be interested in the interaction of several (short, medium, and long-term trends). This indicator caters to that by plotting all relevant crossovers among your chosen MAs. It’s great for multi-timeframe thinkers as well – e.g. you could apply it on a higher timeframe chart to mark major cross levels, then drill down to lower timeframes knowing those key prices.

Value Clean Visualization: There are no flashing signals or arrows – just simple lines and labels that enhance your chart’s storytelling. It’s ideal if you prefer to make trading decisions based on understanding price interaction with technical levels rather than following automatic trade calls. Moving Averages Cross Levels gives you information to act on, without imposing any bias or strategy – you interpret the crossover levels in the context of your own trading system.

EMA Percentile Rank [SS]Hello!

Excited to release my EMA percentile Rank indicator!

What this indicator does

Plots an EMA and colors it by short-term trend.

When price crosses the EMA (up or down) and remains on that side for three subsequent bars, the cross is “confirmed.”

At the moment of the most recent cross, it anchors a reference price to the crossover point to ensure static price targets.

It measures the historical distance between price and the EMA over a lookback window, separately for bars above and below the EMA.

It computes percentile distances (25%, 50%, 85%, 95%, 99%) and draws target bands above/below the anchor.

Essentially what this indicator does, is it converts the raw “distance from EMA” behavior into probabilistic bands and historical hit rates you can use for targets, stop placement, or mean-reversion/continuation decisions.

Indicator Inputs

EMA length: Default is 21 but you can use any EMA you prefer.

Lookback: Default window is 500, this is length that the percentiles are calculated. You can increase or decrease it according to your preference and performance.

Show Accumulation Table: This allows you to see the table that shows the hits/price accumulation of each of the percentile ranges. UCL means upper confidence and LCL means lower confidence (so upper and lower targets).

About Percentiles

A percentile is a way of expressing the position of a value within a dataset relative to all the other values.

It tells you what percentage of the data points fall at or below that value.

For example:

The 25th percentile means 25% of the values are less than or equal to it.

The 50th percentile (also called the median) means half the values are below it and half are above.

The 99th percentile means only 1% of the values are higher.

Percentiles are useful because they turn raw measurements into context — showing how “extreme” or “typical” a value is compared to historical behavior.

In the EMA Percentile Rank indicator, this concept is applied to the distance between price and the EMA. By calculating percentile distances, the script can mark levels that have historically been reached often (low percentiles) or rarely (high percentiles), helping traders gauge whether current price action is stretched or within normal bounds.

Use Cases

The EMA Percentile Rank indicator is best suited for traders who want to quantify how far price has historically moved away from its EMA and use that context to guide decision-making.

One strong use case is target setting after trend shifts: when a confirmed crossover occurs, the percentile bands (25%, 50%, 85%, 95%, 99%) provide statistically grounded levels for scaling out profits or placing stops, based on how often price has historically reached those distances. This makes it valuable for traders who prefer data-driven risk/reward planning instead of arbitrary point targets. Another use case is identifying stretched conditions — if price rapidly tags the 95% or 99% band after a cross, that’s an unusually large move relative to history, which could signal exhaustion and prompt mean-reversion trades or protective actions.

Conversely, if the accumulation table shows price frequently resides in upper bands after bullish crosses, traders may anticipate continuation and hold positions longer . The indicator is also effective as a trend filter when combined with its EMA color-coding : only taking trades in the trend’s direction and using the bands as dynamic profit zones.

Additionally, it can support multi-timeframe confluence (if you align your chart to the timeframes of interest), where higher-timeframe trend direction aligns with lower-timeframe percentile behavior for higher-probability setups. Swing traders can use it to frame pullbacks — entering near lower percentile bands during an uptrend — while intraday traders might use it to fade extremes or ride breakouts past the median band. Because the anchor price resets only on EMA crosses, the indicator preserves a consistent reference for ongoing trades, which is especially helpful for managing swing positions through noise .

Overall, its strength lies in transforming raw EMA distance data into actionable, probability-weighted levels that adapt to the instrument’s own volatility and tendencies .

Summary

This indicator transforms a simple EMA into a distribution-aware framework: it learns how far price tends to travel relative to the EMA on either side, and turns those excursions into percentile bands and historical hit rates anchored to the most recent cross. That makes it a flexible tool for targets, stops, and regime filtering, and a transparent way to reason about “how stretched is stretched?”—with context from your chosen market and timeframe.

I hope you all enjoy!

And as always, safe trades!

Globex Trap w/ percentage [SLICKRICK]Globex Trap w/ Percentage

Overview

The Globex Trap w/ Percentage indicator is a powerful tool designed to help traders identify high-probability trading opportunities by analyzing price action during the Globex (overnight) session and regular trading hours. By combining Globex session ranges with Supply & Demand zones, this indicator highlights potential "trap" areas where significant price reactions may occur. Additionally, it calculates the Globex session range as a percentage of the daily Average True Range (ATR), providing valuable context for assessing market volatility.

This indicator is ideal for traders in futures markets or other instruments traded during Globex sessions, offering a visual and analytical edge for spotting key price levels and potential reversals or breakouts.

Key Features

Globex Session Tracking:

Visualizes the high and low of the Globex session (default: 3:00 PM to 6:30 AM PST) with customizable time settings.

Displays a semi-transparent box to mark the Globex range, with labels for "Globex High" and "Globex Low."

Calculates the Globex range as a percentage of the daily ATR, displayed as a label for quick reference.

Supply & Demand Zones:

Identifies Supply & Demand zones during regular trading hours (default: 6:00 AM to 8:00 AM PST) with customizable time settings.

Draws semi-transparent boxes to highlight these zones, aiding in the identification of key support and resistance areas.

Trap Area Identification:

Highlights potential trap zones where Globex ranges and Supply & Demand zones overlap, indicating areas where price may reverse or consolidate due to trapped traders.

Customizable Settings:

Adjust Globex and Supply & Demand session times to suit your trading preferences.

Toggle visibility of Globex and Supply & Demand zones independently.

Customize box colors for better chart readability.

Set the lookback period (default: 10 days) to control how many historical zones are displayed.

Configure the ATR length (default: 14) for the percentage calculation.

PST Timezone Default:

All times are based on Pacific Standard Time (PST) by default, ensuring accurate session tracking for users in this timezone or those aligning with U.S. West Coast market hours.

Recommended Usage

Timeframes: Best used on 1-hour charts or lower (e.g., 15-minute, 5-minute) for precise entry and exit points.

Markets: Optimized for futures (e.g., ES, NQ, CL) and other instruments traded during Globex sessions.

Historical Data: Ensure at least 10 days of historical data for optimal visualization of zones.

Strategy Integration: Use the indicator to identify potential reversals or breakouts at Globex highs/lows or Supply & Demand zones. The ATR percentage provides context for whether the Globex range is significant relative to typical daily volatility.

How It Works

Globex Session:

Tracks the high and low prices during the user-defined Globex session (default: 3:00 PM to 6:30 AM PST).

When the session ends, a box is drawn from the start to the end of the session, capturing the high and low prices.

Labels are placed at the midpoint of the session, showing "Globex High," "Globex Low," and the range as a percentage of the daily ATR (e.g., "75.23% of Daily ATR").

Supply & Demand Zones:

Tracks the high and low prices during the user-defined regular trading hours (default: 6:00 AM to 8:00 AM PST).

Draws a box to mark these zones, which often act as key support or resistance levels.

ATR Percentage:

Calculates the Globex range (high minus low) and divides it by the daily ATR to express it as a percentage.

This metric helps traders gauge whether the overnight price movement is significant compared to the instrument’s typical volatility.

Time Handling:

Uses PST (UTC-8) for all time calculations, ensuring accurate session timing for users aligning with this timezone.

Properly handles overnight sessions that cross midnight, ensuring seamless tracking.

Input Settings

Globex Session Settings:

Show Globex Session: Enable/disable Globex session visualization (default: true).

Globex Start/End Time: Set the start and end times for the Globex session (default: 3:00 PM to 6:30 AM PST).

Globex Box Color: Customize the color of the Globex session box (default: semi-transparent gray).

Supply & Demand Zone Settings:

Show Supply & Demand Zone: Enable/disable zone visualization (default: true).

Zone Start/End Time: Set the start and end times for Supply & Demand zones (default: 6:00 AM to 8:00 AM PST).

Zone Box Color: Customize the color of the zone box (default: semi-transparent aqua).

General Settings:

Days to Look Back: Number of historical days to display zones (default: 10).

ATR Length: Period for calculating the daily ATR (default: 14).

Notes

All times are in Pacific Standard Time (PST). Adjust the start and end times if your market operates in a different timezone or if you prefer different session windows.

The indicator is optimized for instruments with active Globex sessions, such as futures. Results may vary for non-24/5 markets.

A typo in the label "Globe Low" (should be "Globex Low") will be corrected in future updates.

Ensure your TradingView chart is set to display sufficient historical data to view the full lookback period.

Why Use This Indicator?

The Globex Trap w/ Percentage indicator provides a unique combination of session-based range analysis, Supply & Demand zone identification, and volatility context via the ATR percentage. Whether you’re a day trader, swing trader, or scalper, this tool helps you:

Pinpoint key price levels where institutional traders may act.

Assess the significance of overnight price movements relative to daily volatility.

Identify potential trap zones for high-probability setups.

Customize the indicator to fit your trading style and market preferences.

Smart Money Precision Structure [BullByte]Smart Money Precision Structure

Advanced Market Structure Analysis Using Institutional Order Flow Concepts

---

OVERVIEW

Smart Money Precision Structure (SMPS) is a comprehensive market analysis indicator that combines six analytical frameworks to identify high-probability market structure patterns. The indicator uses multi-dimensional scoring algorithms to evaluate market conditions through institutional order flow concepts, providing traders with professional-grade market analysis.

---

PURPOSE AND ORIGINALITY

Why This Indicator Was Developed

• Addresses the gap between retail and institutional analysis methods

• Consolidates multiple analysis techniques that professionals use separately

• Automates complex market structure evaluation into actionable insights

• Eliminates the need for multiple indicators by providing comprehensive analysis

What Makes SMPS Original

• Six-Layer Confluence System - Unique combination of market regime, structure, volume flow, momentum, price action, and adaptive filtering

• Institutional Pattern Recognition - Identifies smart money accumulation and distribution patterns

• Adaptive Intelligence - Parameters automatically adjust based on detected market conditions

• Real-Time Market Scoring - Proprietary algorithm rates market quality from 0-100%

• Structure Break Detection - Advanced pivot analysis identifies trend reversals early

---

HOW IT WORKS - TECHNICAL METHODOLOGY

1. Market Regime Analysis Engine

The indicator evaluates five core market dimensions:

• Volatility Score - Measures current volatility against 50-period historical baseline

• Trend Score - Analyzes alignment between 8, 21, and 50-period EMAs

• Momentum Score - Combines RSI divergence with MACD signal alignment

• Structure Score - Evaluates pivot point formation clarity

• Efficiency Score - Calculates directional movement efficiency ratio

These scores combine to classify markets into five regimes:

• TRENDING - Strong directional movement with aligned indicators

• RANGING - Sideways movement with mixed directional signals

• VOLATILE - Elevated volatility with unpredictable price swings

• QUIET - Low volatility consolidation periods

• TRANSITIONAL - Market shifting between different regimes

2. Market Structure Analysis

Advanced pivot point analysis identifies:

• Higher Highs and Higher Lows for bullish structure

• Lower Highs and Lower Lows for bearish structure

• Structure breaks when established patterns fail

• Dynamic support and resistance from recent pivot points

• Key level proximity detection using ATR-based buffers

3. Volume Flow Decoding

Institutional activity detection through:

• Volume surge identification when volume exceeds 2x average

• Buy versus sell pressure analysis using price-volume correlation

• Flow strength measurement through directional volume consistency

• Divergence detection between volume and price movements

• Institutional threshold alerts when unusual volume patterns emerge

4. Multi-Period Momentum Synthesis

Weighted momentum calculation across four timeframes:

• 1-period momentum weighted at 40%

• 3-period momentum weighted at 30%

• 5-period momentum weighted at 20%

• 8-period momentum weighted at 10%

Result smoothed with 6-period EMA for noise reduction.

5. Price Action Quality Assessment

Each bar evaluated for:

• Range quality relative to 20-period average

• Body-to-range ratio for directional conviction

• Wick analysis for rejection pattern identification

• Pattern recognition including engulfing and hammer formations

• Sequential price movement analysis

6. Adaptive Parameter System

Parameters automatically adjust based on detected regime:

• Trending markets reduce sensitivity and confirmation requirements

• Volatile markets increase filtering and require additional confirmations

• Ranging markets maintain neutral settings

• Transitional markets use moderate adjustments

---

COMPLETE SETTINGS GUIDE

Section 1: Core Analysis Settings

Analysis Sensitivity (0.3-2.0)

• Default: 1.0

• Lower values require stronger price movements

• Higher values detect more subtle patterns

• Scalpers use 0.8-1.2, swing traders use 1.5-2.0

Noise Reduction Level (2-7)

• Default: 4

• Controls filtering of false patterns

• Higher values reduce pattern frequency

• Increase in volatile markets

Minimum Move % (0.05-0.50)

• Default: 0.15%

• Sets minimum price movement threshold

• Adjust based on instrument volatility

• Forex: 0.05-0.10%, Stocks: 0.15-0.25%, Crypto: 0.20-0.50%

High Confirmation Mode

• Default: True (Enabled)

• Requires all technical conditions to align

• Reduces frequency but increases reliability

• Disable for more aggressive pattern detection

Section 2: Market Regime Detection

Enable Regime Analysis

• Default: True (Enabled)

• Activates market environment evaluation

• Essential for adaptive features

• Keep enabled for best results

Regime Analysis Period (20-100)

• Default: 50 bars

• Determines regime calculation lookback

• Shorter for responsive, longer for stable

• Scalping: 20-30, Swing: 75-100

Minimum Market Clarity (0.2-0.8)

• Default: 0.4

• Quality threshold for pattern generation

• Higher values require clearer conditions

• Lower for more patterns, higher for quality

Adaptive Parameter Adjustment

• Default: True (Enabled)

• Enables automatic parameter optimization

• Adjusts based on market regime

• Highly recommended to keep enabled

Section 3: Market Structure Analysis

Enable Structure Validation

• Default: True (Enabled)

• Validates patterns against support/resistance

• Confirms trend structure alignment

• Essential for reliability

Structure Analysis Period (15-50)

• Default: 30 bars

• Period for structure pattern analysis

• Affects support/resistance calculation

• Match to your trading timeframe

Minimum Structure Alignment (0.3-0.8)

• Default: 0.5

• Required structure score for valid patterns

• Higher values need stronger structure

• Balance with desired frequency

Section 4: Analysis Configuration

Minimum Strength Level (3-5)

• Default: 4

• Minimum confirmations for pattern display

• 5 = Maximum reliability, 3 = More patterns

• Beginners should use 4-5

Required Technical Confirmations (4-6)

• Default: 5

• Number of aligned technical factors

• Higher = fewer but better patterns

• Works with High Confirmation Mode

Pattern Separation (3-20 bars)

• Default: 8 bars

• Minimum bars between patterns

• Prevents clustering and overtrading

• Increase for cleaner charts

Section 5: Technical Filters

Momentum Validation

• Default: True (Enabled)

• Requires momentum alignment

• Filters counter-trend patterns

• Essential for trend following

Volume Confluence Analysis

• Default: True (Enabled)

• Requires volume confirmation

• Identifies institutional participation

• Critical for reliability

Trend Direction Filter

• Default: True (Enabled)

• Only shows patterns with trend

• Reduces counter-trend signals

• Disable for reversal hunting

Section 6: Volume Flow Analysis

Institutional Activity Threshold (1.2-3.5)

• Default: 2.0

• Multiplier for unusual volume detection

• Lower finds more institutional activity

• Stock: 2.0-2.5, Forex: 1.5-2.0, Crypto: 2.5-3.5

Volume Surge Multiplier (1.8-4.5)

• Default: 2.5

• Defines significant volume increases

• Adjust per instrument characteristics

• Higher for stocks, lower for forex

Volume Flow Period (12-35)

• Default: 18 bars

• Smoothing for volume analysis

• Shorter = responsive, longer = smooth

• Match to timeframe used

Section 7: Analysis Frequency Control

Maximum Analysis Points Per Hour (1-5)

• Default: 3

• Limits pattern frequency

• Prevents overtrading

• Scalpers: 4-5, Swing traders: 1-2

Section 8: Target Level Configuration

Target Calculation Method

• Default: Market Adaptive

• Three modes available:

- Fixed: Uses set point distances

- Dynamic: ATR-based calculations

- Market Adaptive: Structure-based levels

Minimum Target/Risk Ratio (1.0-3.0)

• Default: 1.5

• Minimum acceptable reward vs risk

• Higher filters lower probability setups

• Professional standard: 1.5-2.0

Fixed Mode Settings:

• Fixed Target Distance: 50 points default

• Fixed Invalidation Distance: 30 points default

• Use for consistent instruments

Dynamic Mode Settings:

• Dynamic Target Multiplier: 1.8x ATR default

• Dynamic Invalidation Multiplier: 1.0x ATR default

• Adapts to volatility automatically

Market Adaptive Settings:

• Use Structure Levels: True (default)

• Structure Level Buffer: 0.1% default

• Places levels at actual support/resistance

Section 9: Visual Display Settings

Color Theme Options

• Professional (Teal/Red)

- Bullish: Teal (#26a69a)

- Bearish: Red (#ef5350)

- Neutral: Gray (#78909c)

- Best for: Traditional traders, clean appearance

• Dark (Neon Green/Pink)

- Bullish: Neon Green (#00ff88)

- Bearish: Hot Pink (#ff0044)

- Neutral: Dark Gray (#333333)

- Best for: Dark theme users, high contrast

• Light (Green/Red Classic)

- Bullish: Green (#4caf50)

- Bearish: Red (#f44336)

- Neutral: Light Gray (#9e9e9e)

- Best for: Light backgrounds, traditional colors

• Vibrant (Cyan/Magenta)

- Bullish: Cyan (#00ffff)

- Bearish: Magenta (#ff00ff)

- Neutral: Medium Gray (#888888)

- Best for: High visibility, modern appearance

Dashboard Position

• Options: Top Left, Top Right, Bottom Left, Bottom Right, Middle Left, Middle Right

• Default: Top Right

• Choose based on chart layout preference

Dashboard Size

• Full: Complete information display (desktop)

• Mobile: Compact view for small screens

• Default: Full

Analysis Display Style

• Arrows : Simple directional markers

• Labels : Detailed text information

• Zones : Colored areas showing pattern regions

• Default: Labels (most informative)

Display Options:

• Display Analysis Strength: Shows star rating

• Display Target Levels: Shows target/invalidation lines

• Display Market Regime: Shows regime in pattern labels

---

HOW TO USE SMPS - DETAILED GUIDE

Understanding the Dashboard

Top Row - Header

• SMPS Dashboard title

• VALUE column: Current readings

• STATUS column: Condition assessments

Market Regime Row

• Shows: TRENDING, RANGING, VOLATILE, QUIET, or TRANSITIONAL

• Color coding: Green = Favorable, Red = Caution

• Status: FAVORABLE or CAUTION trading conditions

Market Score Row

• Percentage from 0-100%

• Above 60% = Strong conditions

• 40-60% = Moderate conditions

• Below 40% = Weak conditions

Structure Row

• Direction: BULLISH, BEARISH, or NEUTRAL

• Status: INTACT or BREAK

• Orange BREAK indicates structure failure

Volume Flow Row

• Direction: BUYING or SELLING

• Intensity: STRONG or WEAK

• Color indicates dominant pressure

Momentum Row

• Numerical momentum value

• Positive = Upward pressure

• Negative = Downward pressure

Volume Status Row

• INST = Institutional activity detected

• HIGH = Above average volume

• NORM = Normal volume levels

Adaptive Mode Row

• ACTIVE = Parameters adjusting

• STATIC = Fixed parameters

• Shows required confirmations

Analysis Level Row

• Minimum strength level setting

• Pattern separation in bars

Market State Row

• Current analysis: BULLISH, BEARISH, NEUTRAL

• Shows analysis price level when active

T:R Ratio Row

• Current target to risk ratio

• GOOD = Meets minimum requirement

• LOW = Below minimum threshold

Strength Row

• BULL or BEAR dominance

• Numerical strength value 0-100

Price Row

• Current price

• Percentage change

Last Analysis Row

• Previous pattern direction

• Bars since last pattern

Reading Pattern Signals

Bullish Structure Pattern

• Upward triangle or "Bullish Structure" label

• Star rating shows strength (★★★★★ = strongest)

• Green line = potential target level

• Red dashed line = invalidation level

• Appears below price bars

Bearish Structure Pattern

• Downward triangle or "Bearish Structure" label

• Star rating indicates reliability

• Green line = potential target level

• Red dashed line = invalidation level

• Appears above price bars

Pattern Strength Interpretation

• ★★★★★ = 6 confirmations (exceptional)

• ★★★★☆ = 5 confirmations (strong)

• ★★★☆☆ = 4 confirmations (moderate)

• ★★☆☆☆ = 3 confirmations (minimum)

• Below minimum = filtered out

Visual Elements on Chart

Lines and Levels:

• Gray Line = 21 EMA trend reference

• Green Stepline = Dynamic support level

• Red Stepline = Dynamic resistance level

• Green Solid Line = Active target level

• Red Dashed Line = Active invalidation level

Pattern Markers:

• Triangles = Arrow display mode

• Text Labels = Label display mode

• Colored Boxes = Zone display mode

Target Completion Labels:

• "Target" = Price reached target level

• "Invalid" = Pattern invalidated by price

---

RECOMMENDED USAGE BY TIMEFRAME

1-Minute Charts (Scalping)

• Sensitivity: 0.8-1.2

• Noise Reduction: 3-4

• Pattern Separation: 3-5 bars

• High Confirmation: Optional

• Best for: Quick intraday moves

5-Minute Charts (Precision Intraday)

• Sensitivity: 1.0 (default)

• Noise Reduction: 4 (default)

• Pattern Separation: 8 bars

• High Confirmation: Enabled

• Best for: Day trading

15-Minute Charts (Short Swing)

• Sensitivity: 1.0-1.5

• Noise Reduction: 4-5

• Pattern Separation: 10-12 bars

• High Confirmation: Enabled

• Best for: Intraday swings

30-Minute to 1-Hour (Position Trading)

• Sensitivity: 1.5-2.0

• Noise Reduction: 5-7

• Pattern Separation: 15-20 bars

• Regime Period: 75-100

• Best for: Multi-day positions

Daily Charts (Swing Trading)

• Sensitivity: 1.8-2.0

• Noise Reduction: 6-7

• Pattern Separation: 20 bars

• All filters enabled

• Best for: Long-term analysis

---

MARKET-SPECIFIC SETTINGS

Forex Pairs

• Minimum Move: 0.05-0.10%

• Institutional Threshold: 1.5-2.0

• Volume Surge: 1.8-2.2

• Target Mode: Dynamic or Market Adaptive

Stock Indices (ES, NQ, YM)

• Minimum Move: 0.10-0.15%

• Institutional Threshold: 2.0-2.5

• Volume Surge: 2.5-3.0

• Target Mode: Market Adaptive

Individual Stocks

• Minimum Move: 0.15-0.25%

• Institutional Threshold: 2.0-2.5

• Volume Surge: 2.5-3.5

• Target Mode: Dynamic

Cryptocurrency

• Minimum Move: 0.20-0.50%

• Institutional Threshold: 2.5-3.5

• Volume Surge: 3.0-4.5

• Target Mode: Dynamic

• Increase noise reduction

---

PRACTICAL APPLICATION EXAMPLES

Example 1: Strong Trending Market

Dashboard Reading:

• Market Regime: TRENDING

• Market Score: 75%

• Structure: BULLISH, INTACT

• Volume Flow: BUYING, STRONG

• Momentum: +0.45

Interpretation:

• Strong uptrend environment

• Institutional buying present

• Look for bullish patterns as continuation

• Higher probability of success

• Consider using lower sensitivity

Example 2: Range-Bound Conditions

Dashboard Reading:

• Market Regime: RANGING

• Market Score: 35%

• Structure: NEUTRAL

• Volume Flow: SELLING, WEAK

• Momentum: -0.05

Interpretation:

• No clear direction

• Low opportunity environment

• Patterns are less reliable

• Consider waiting for regime change

• Or switch to a range-trading approach

Example 3: Structure Break Alert

Dashboard Reading:

• Previous: BULLISH structure

• Current: Structure BREAK

• Volume: INST flag active

• Momentum: Shifting negative

Interpretation:

• Trend reversal potentially beginning

• Institutional participation detected

• Watch for bearish pattern confirmation

• Adjust bias accordingly

• Increase caution on long positions

Example 4: Volatile Market

Dashboard Reading:

• Market Regime: VOLATILE

• Market Score: 45%

• Adaptive Mode: ACTIVE

• Confirmations: Increased to 6

Interpretation:

• Choppy conditions

• Parameters auto-adjusted

• Fewer but higher quality patterns

• Wider stops may be needed

• Consider reducing position size

Below are a few chart examples of the Smart Money Precision Structure (SMPS) indicator in action.

• Example 1 – Bullish Structure Detection on SOLUSD 5m

• Example 2 – Bearish Structure Detected with Strong Confluence on SOLUSD 5m

---

TROUBLESHOOTING GUIDE

No Patterns Appearing

Check these settings:

• High Confirmation Mode may be too restrictive

• Minimum Strength Level may be too high

• Market Clarity threshold may be too high

• Regime filter may be blocking patterns

• Try increasing sensitivity

Too Many Patterns

Adjust these settings:

• Enable High Confirmation Mode

• Increase Minimum Strength Level to 5

• Increase Pattern Separation

• Reduce Sensitivity below 1.0

• Enable all technical filters

Dashboard Shows "CAUTION"

This indicates:

• Market conditions are unfavorable

• Regime is RANGING or QUIET

• Market score is low

• Consider waiting for better conditions

• Or adjust expectations accordingly

Patterns Not Reaching Targets

Consider:

• Market may be choppy

• Volatility may have changed

• Try Dynamic target mode

• Reduce target/risk ratio requirement

• Check if regime is VOLATILE

---

ALERTS CONFIGURATION

Alert Message Format

Alerts include:

• Pattern type (Bullish/Bearish)

• Strength rating

• Market regime

• Analysis price level

• Target and invalidation levels

• Strength percentage

• Target/Risk ratio

• Educational disclaimer

Setting Up Alerts

• Click Alert button on TradingView

• Select SMPS indicator

• Choose alert frequency

• Customize message if desired

• Alerts fire on pattern detection

---

DATA WINDOW INFORMATION

The Data Window displays:

• Market Regime Score (0-100)

• Market Structure Bias (-1 to +1)

• Bullish Strength (0-100)

• Bearish Strength (0-100)

• Bull Target/Risk Ratio

• Bear Target/Risk Ratio

• Relative Volume

• Momentum Value

• Volume Flow Strength

• Bull Confirmations Count

• Bear Confirmations Count

---

BEST PRACTICES AND TIPS

For Beginners

• Start with default settings

• Use High Confirmation Mode

• Focus on TRENDING regime only

• Paper trade first

• Learn one timeframe thoroughly

For Intermediate Users

• Experiment with sensitivity settings

• Try different target modes

• Use multiple timeframes

• Combine with price action analysis

• Track pattern success rate

For Advanced Users

• Customize per instrument

• Create setting templates

• Use regime information for bias

• Combine with other indicators

• Develop systematic rules

---

IMPORTANT DISCLAIMERS

• This indicator is for educational and informational purposes only

• Not financial advice or a trading system

• Past performance does not guarantee future results

• Trading involves substantial risk of loss

• Always use appropriate risk management

• Verify patterns with additional analysis

• The author is not a registered investment advisor

• No liability accepted for trading losses

---

VERSION NOTES

Version 1.0.0 - Initial Release

• Six-layer confluence system

• Adaptive parameter technology

• Institutional volume detection

• Market regime classification

• Structure break identification

• Real-time dashboard

• Multiple display modes

• Comprehensive settings

## My Final Thoughts

Smart Money Precision Structure represents an advanced approach to market analysis, bringing institutional-grade techniques to retail traders through intelligent automation and multi-dimensional evaluation. By combining six analytical frameworks with adaptive parameter adjustment, SMPS provides comprehensive market intelligence that single indicators cannot achieve.

The indicator serves as an educational tool for understanding how professional traders analyze markets, while providing practical pattern detection for those seeking to improve their technical analysis. Remember that all trading involves risk, and this tool should be used as part of a complete analysis approach, not as a standalone trading system.

- BullByte

Candle ShapeCandle Shape

This indicator visualizes rolling candles that aggregate price action over a chosen lookback period, allowing you to see how OHLC dynamics evolve in real time.

Instead of waiting for a higher timeframe (HTF) bar to close, you can track its development directly from a lower timeframe chart.

For example, view how a 1-hour candle is forming on a 1-minute chart — complete with rolling open, high, low, and close levels, as well as colored body and wick areas.

---

🔹 How it works

- Lookback Period (n) → sets the bucket size, defining how many bars are merged into a “meta-candle.”

- The script continuously updates the meta-open, meta-high, meta-low, and meta-close.

- Body and wick areas are filled with color , making bullish/bearish transitions easy to follow.

---

🔹 Use cases

- Monitor the intra-development of higher timeframe candles.

- Analyze rolling OHLC structures to understand how price dynamics shift across different aggregation windows.

- Explore unique perspectives for strategy confirmation, breakout anticipation, and market structure analysis.

---

✨ Candle Shape bridges the gap between timeframes and uncovers new layers of price interaction.

Pasrsifal.RegressionTrendStateSummary

The Parsifal.Regression.Trend.State Indicator analyzes the leading coefficients of linear and quadratic regressions of price (against time). It also considers their first- and second-order changes. These features are aggregated into a Trend-State background, shown as a gradient color. In addition, the indicator generates fast and slow signals that can be used as potential entry- or exit triggers.

This tool is designed for advanced trend-following strategies, leveraging information from multiple trendline features.

Background

Trendlines provide insight into the state of a trend or the “trendiness” of a price process. While moving averages or pivot-based lines can serve as envelopes and breakout levels, they are often too lagging for swing traders, who need tools that adapt more closely to price swings, ideally using trendlines, around which the price process swings continuously.

Regression lines address this by cutting directly through the data, making them a natural anchor for observing how price winds around a central trendline within a chosen lookback period.

Regression Trendlines

• Linear Regression:

o Minimizes distance to all closing values over the lookback period.

o The slope represents the short-term linear trend.

o The change of slope indicates trend acceleration or deceleration.

o Linear regression lags during phases of rapid market shifts.

• Quadratic Regression:

o Fits a second-degree polynomial to minimize deviation from closing prices.

o The convexity term (leading coefficient) reflects curvature:

Positive convexity → accelerating uptrend or fading downtrend.

Negative convexity → accelerating downtrend or fading uptrend.

o The change of convexity detects early shifts in momentum and often reacts faster than slope features.

Features Extracted

The indicator evaluates six features:

• Linear features: slope, first derivative of slope, second derivative of slope.

• Quadratic features: convexity term, first derivative of the convexity term, second derivative of the convexity term.

• Linear features: capture broad, background trend behavior.

• Quadratic features: detect deviations, accelerations, and smaller-scale dynamics.

Quadratic terms generally react first to market changes, while linear terms provide stability and context.

Dynamics of Market Moves as seen by linear and quadratic regressions

• At the start of a rapid move:

The change of convexity reacts first, capturing the shift in dynamics before other features. The convexity term then follows, while linear slope features lag further behind. Because convexity measures deviation from linearity, it reflects accelerating momentum more effectively than slope.

• At the end of a rapid move:

Again, the change of convexity responds first to fading momentum, signaling the transition from above-linear to below-linear dynamics. Even while a strong trend persists, the change of convexity may flip sign early, offering a warning of weakening strength. The convexity term itself adjusts more slowly but may still turn before the price process does. Linear features lag the most, typically only flipping after price has already reversed, thereby smoothing out the rapid, more sensitive reactions of quadratic terms.

________________________________________

Parsifal Regression.Trend.State Method

1. Feature Mapping:

Each feature is mapped to a range between -1 and 1, preserving zero-crossings (critical for sign interpretation).

2. Aggregation:

A heuristic linear combination*) produces a background information value, visualized as a gradient color scale:

o Deep green → strong positive trend.

o Deep red → strong negative trend.

o Yellow → neutral or transitional states.

3. Signals:

o Fast signal (oscillator): ranges from -1 to 1, reflecting short-term trend state.

o Slow signal (smoothed): moving average of the fast signal.

o Their interactions (crossovers, zero-crossings) provide actionable trading triggers.

How to Use

The Trend-State background gradient provides intuitive visual feedback on the aggregated regression features (slope, convexity, and their changes). Because these features reflect not only current trend strength but also their acceleration or deceleration, the color transitions help anticipate evolving market states:

• Solid Green: All features near their highs. Indicates a strong, accelerating uptrend. May also reflect explosive or hyperbolic upside moves (including gaps).

• Fading Solid Green: A recently strong uptrend is losing momentum. Price may shift into a slower uptrend, consolidation, or even a reversal.

• Fading Green → Yellow: Often appears as a dirty yellow or a rapidly mixing pattern of green and red. Signals that the uptrend is weakening toward neutrality or beginning to turn negative.

• Yellow → Deepening Red: Two possible scenarios:

o Coming from a strong uptrend → suggests a sharp fade, though the trend may still technically be up.

o Coming from a weaker uptrend or sideways market → suggests the start of an accelerating downtrend.

• Solid Red: All features near their lows. Indicates a strong, accelerating downtrend. May also reflect crash-type conditions or downside gaps.

• Fading Solid Red: A recently strong downtrend is losing strength. Market may move into a slower decline, consolidation, or early reversal upward.

• Fading Red → Yellow : The downtrend is weakening toward neutral, with potential for a bullish shift.

• Yellow → Increasing Green: Two possible scenarios:

o Coming from a strong downtrend, it reflects a sharp fade of bearish momentum, though the market may still technically be trending down.

o Coming from a weaker downtrend or sideways movement, it suggests the start of an accelerating uptrend.

Note: Market evolution does not always follow this neat “color cycle.” It may jump between states, skip stages, or reverse abruptly depending on market conditions. This makes the background coloring particularly valuable as a contextual map of current and evolving price dynamics.

Signal Crossovers:

Although the fast signal is very similar (but not identical) to the background coloring, it provides a numerical representation indicating a bullish interpretation for rising values and bearish for falling.

o High-confidence entries:

Fast signal rising from < -0.7 and crossing above the slow signal → potential long entry.

Fast signal falling from > +0.7 and crossing below the slow signal → potential short entry.

o Low-confidence entries:

Crossovers near zero may still provide a valid trigger but may be noisy and should be confirmed with other signals.

o Zero-crossings:

Indicate broader state changes, useful for conservative positioning or option strategies. For confirmation of a Fast signal 0-crossing, wait for the Slow signal to cross as well.

________________________________________

*) Note on Aggregation

While the indicator currently uses a heuristic linear combination of features, alternatives such as Principal Component Analysis (PCA) could provide a more formal aggregation. However, while in the absence of matrix algebra, the required eigenvalue decomposition can be approximated, its computational expense does not justify the marginal higher insight in this case. The current heuristic approach offers a practical balance of clarity, speed, and accuracy.

Key Session & LevelsThis indicator helps traders track key price levels for multiple timeframes and trading sessions. It plots:

Previous Day's High and Low (PD): Highlighting the high and low of the previous trading day.

Previous Week's High and Low (PW): Plotting the highest and lowest price levels for the past week.

Tokyo Session High and Low (Today): Displays the high and low levels for the Tokyo trading session (adjustable to your preferred time window).

London Session High and Low (Today): Tracks the high and low for the London trading session (also adjustable for your timezone and desired session window).

Features:

Customizable Time Zones: The indicator uses your preferred timezone to calculate session highs/lows.

Extendable Lines: Lines for each level extend to the right of the chart, providing continuous reference throughout the trading day.

Adjustable Settings: Fine-tune the visibility and width of the lines, and choose which levels to display (Previous Day, Previous Week, Tokyo, and London sessions).

Non-Repainting: This script uses historical data and only updates when new bars are confirmed, ensuring accurate and reliable signals.

Whether you're a day trader, swing trader, or just tracking key levels for strategic entries and exits, this tool provides quick visual reference to important price points across different trading sessions.

Key Session & LevelsThis indicator helps traders track key price levels for multiple timeframes and trading sessions. It plots:

Previous Day's High and Low (PD): Highlighting the high and low of the previous trading day.

Previous Week's High and Low (PW): Plotting the highest and lowest price levels for the past week.

Tokyo Session High and Low (Today): Displays the high and low levels for the Tokyo trading session (adjustable to your preferred time window).

London Session High and Low (Today): Tracks the high and low for the London trading session (also adjustable for your timezone and desired session window).

Features:

Customizable Time Zones: The indicator uses your preferred timezone to calculate session highs/lows.

Extendable Lines: Lines for each level extend to the right of the chart, providing continuous reference throughout the trading day.

Adjustable Settings: Fine-tune the visibility and width of the lines, and choose which levels to display (Previous Day, Previous Week, Tokyo, and London sessions).

Non-Repainting: This script uses historical data and only updates when new bars are confirmed, ensuring accurate and reliable signals.

Whether you're a day trader, swing trader, or just tracking key levels for strategic entries and exits, this tool provides quick visual reference to important price points across different trading sessions.

Rolling Correlation BTC vs Hedge AssetsRolling Correlation BTC vs Hedge Assets

Overview

This indicator calculates and plots the rolling correlation between Bitcoin (BTC) returns and several key hedge assets:

• XAUUSD (Gold)

• EURUSD (proxy for DXY, U.S. Dollar Index)

• VIX (Volatility Index)

• TLT (20y U.S. Treasury Bonds ETF)

By monitoring these dynamic correlations, traders can identify whether BTC is moving in sync with risk assets or decoupling as a hedge, and adjust their trading strategy accordingly.

How it works

1. Computes returns for BTC and each asset using percentage change.

2. Uses the rolling correlation function (ta.correlation) over a configurable window length (default = 12 bars).

3. Plots each correlation as a separate colored line (Gold = Yellow, EURUSD = Blue, VIX = Red, TLT = Green).

4. Adds threshold levels at +0.3 and -0.3 to help classify correlation regimes.

How to use it

• High positive correlation (> +0.3): BTC is moving together with the asset (risk-on behavior).

• Near zero (-0.3 to +0.3): BTC is showing little to no correlation — neutral/independent moves.

• Negative correlation (< -0.3): BTC is moving in the opposite direction — potential hedge opportunity.

Practical strategies:

• Watch BTC vs VIX: a spike in volatility (VIX ↑) usually coincides with BTC selling pressure.

• Track BTC vs EURUSD: stronger USD often puts downside pressure on BTC.

• Observe BTC vs Gold: during “flight to safety” events, gold rises while BTC weakens.

• Monitor BTC vs TLT: rising yields (falling TLT) often align with BTC weakness.

Inputs

• Window Length (bars): Number of bars used to calculate rolling correlations (default = 12).

• Comparison Timeframe: Default = 5m. Can be changed to align with your intraday or swing trading style.

Notes

• Works best on intraday charts (1m, 5m, 15m) for scalping and short-term setups.

• Use correlations as context, not standalone signals — combine with volume, VWAP, and price action.

• Correlations are dynamic; they can switch regimes quickly during macro events (CPI, NFP, FOMC).

This tool is designed for traders who want to manage risk exposure by monitoring whether BTC is behaving as a risk-on asset or hedge, and to exploit opportunities during decoupling phases.

Sweep2Trade Pro [CHE]Sweep2Trade Pro \ — Liquidity Sweep → Trend → Confirmation

Sweep2Trade Pro \ helps you catch high-probability reversals or continuations that start with a liquidity sweep, align with the T3 trend, and finalize with a structure confirmation (BOS). It’s designed to reduce noise, time your entries, and keep you out of weak, chop-driven signals.

What’s a “sweep”?

A liquidity sweep happens when price briefly breaks a prior swing high/low (where many stops sit), triggers those stops, and then snaps back. This “stop-hunt” creates liquidity for bigger players and often precedes a sharp move in the opposite direction if the break fails, or fuels continuation if structure actually shifts.

What’s a BOS (Break of Structure)?

A BOS is a price action event where the market takes out a recent swing level in the trend’s direction, signaling continuation and confirming that structure has shifted (bullish BOS through a recent swing high, bearish BOS through a recent swing low).

How the indicator works (at a glance)

1. Regime Filter (T3 + R²)

T3 Moving Average: A smoother, faster-responding moving average that aims to reduce lag while filtering noise, so trend direction changes are clearer.

R² (Coefficient of Determination): Measures how “linear” the recent price path is (0→1). Higher values = stronger, cleaner trend; lower values = more chop. Used here to allow trades only when trend quality exceeds a user-set threshold.

2. Sweep Detection

Bullish sweep: price pokes below a prior swing low and closes back above it.

Bearish sweep: price pokes above a prior swing high and closes back below it.

Lookback length is configurable.

3. Sequence Lock (built-in FSM)

The script manages state in phases so you don’t jump the gun:

Phase 1: Sweep detected → wait for T3 to turn in the corresponding direction.

Phase 2: T3 direction confirmed → show “SWEEP OK” and wait for final confirmation.

Trade Signal: Only fires if confirmation arrives before a timeout.

4. Confirmation Layer

BOS via wick or close (you choose),

Strong close toward the signal (top/bottom quartile of the candle),

Optional “close above/below T3” condition.

These checks help avoid weak sweeps that immediately fade.

5. Alerts & Visuals

“SWEEP OK” markers show when the sweep + T3 direction align.

Final BUY/SELL arrows appear only when the confirmation layer passes.

Ready-made alert conditions for automation.

What you can do with it

Time reversals after sweeps: Enter when a stop-hunt fades and structure confirms.

Ride continuations: Use BOS with the T3 trend to pyramid or re-enter with structure on your side.

Filter chop: Let R² gate entries to periods with cleaner directional drift.

Automate: Use the included alerts with your platform or webhook setup.

Inputs (key settings)

Regime Filter

T3 Length / Volume Factor: Controls smoothness and responsiveness. Smaller length → faster, more sensitive; higher volume factor → smoother curve.

R² Lookback & Threshold: Length of the linear fit window and the minimum “trend quality” required. Higher thresholds mean fewer, cleaner signals.

Sweep / Sequence

Swing Lookback: How far back to define the “reference” high/low for sweeps.

Timeout: Maximum bars allowed between phases to keep signals fresh.

Restart timeout on Phase 2: Optional safety so entries don’t go stale.

Confirmation

BOS Lookback: Micro-pivot window for structure breaks.

Wick vs Close BOS: Conservative traders may prefer close.

Require close above/below T3: Tightens confirmation with trend alignment.

Practical guide (quick start)

1. Timeframe & markets: Works across majors, indices, and crypto. Start with 5m–1h intraday or 1h–4h swing; adjust R² threshold upward on noisier pairs.

2. Entry recipe (Long):

Bullish sweep of a prior low → T3 turns up → BOS/strong close.

Optional: enable “close above T3” for extra confirmation.

3. Entry recipe (Short): Mirror the above.

4. Stops: Common choices are just beyond the sweep wick (tighter) or past the BOS invalidation (safer).

5. Targets: Previous structural levels, measured move, or a T3 trail (exit when price closes back through T3).

6. Avoid low-quality contexts: If R² is very low, market is likely ranging erratically—skip or widen filters.

Tips & best practices

Context first: The same sweep means different things in a strong trend vs. flat regime; that’s why the T3+R² filter exists.

BOS choice: Wick-based BOS is earlier but noisier; close-based BOS is slower but cleaner. Tune per market.

Backtest -> Forward test: Validate settings per symbol/timeframe; then paper trade before going live.

Risk: Fixed fractional risk with asymmetric R\:R (e.g., 1:1.5–1:3) generally performs better than “all-in” discretionary sizing.

Behind the scenes (for the curious)

T3 is a multi-stage EMA construction that produces a smooth curve with reduced lag versus simple/standard EMAs.

R² is the square of correlation (0–1). Here it’s used as a moving gauge of how well price aligns to a linear path—our “trend quality” dial.

Stop-hunts / sweeps are a recognized microstructure phenomenon where clustered stops provide the liquidity that fuels the next move.

Disclaimer

No indicator guarantees profits. Sweep2Trade Pro \ is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Happy trading

Chervolino

Buy Sell Volume with delta value📄 Script Description

This indicator decomposes total traded volume into buying and selling volume, and displays their relative ratios.

🔎 Key Features

Buying vs. Selling Volume Separation

Uses the candle’s high, low, and close to split total volume into buying volume and selling volume.

Formula:

Buy = volume * (close - low) / (high - low)

Sell = volume * (high - close) / (high - low)

Volume Histogram Visualization

Plots overall volume (upper/lower) and separated buy/sell volumes as color-coded columns.

UPPER V / LOWER V: total volume

BUY V: buying volume (teal)

SELL V: selling volume (red)

Buy/Sell Ratio Calculation

Computes the percentage of buy and sell volume relative to total volume.

Buy Ratio = buyVolume / totalVolume * 100

Sell Ratio = sellVolume / totalVolume * 100

Ratio Display

Shows the latest Buy Ratio in a table (top-right corner of the chart).

Adds a label above the most recent bar displaying:

"Buy XX% / Sell YY%"

Historical ratios can be inspected through the TradingView Data Window or tooltip.

🛠️ Usage

Quickly identify whether volume during each candle is dominated by buyers or sellers.

Helps to assess market pressure and confirm potential trend direction, entries, or exits.

⚠️ Notes

Labels are shown only on the most recent bar (Pine cannot track mouse cursor events).

To see historical values, use the TradingView Data Window or hover tooltips.

This method provides an approximate split of volume and does not perfectly capture all market order flows.

RRG Relative Strength# RRG Relative Strength (RRG RS)

Compare any symbol to a benchmark using two RRG-style lines: **RS-Ratio** (trend of relative strength) and **RS-Momentum** (momentum of that trend). Both are centered at **100**:

- **RS-Ratio > 100** → outperforming the benchmark

- **RS-Ratio < 100** → underperforming

- **RS-Momentum** often **leads** RS-Ratio (crosses 100 earlier)

# How it works

1) Relative Strength (RS): RS = Close(symbol) / Close(benchmark)

2) Normalize around 100: smooth RS with EMA and divide RS by that EMA

3) RS-Ratio: EMA( RS / EMA(RS, Length), LenSmooth ) * 100

4) RS-Momentum: RS-Ratio / EMA(RS-Ratio, LenSmooth) * 100

# Inputs