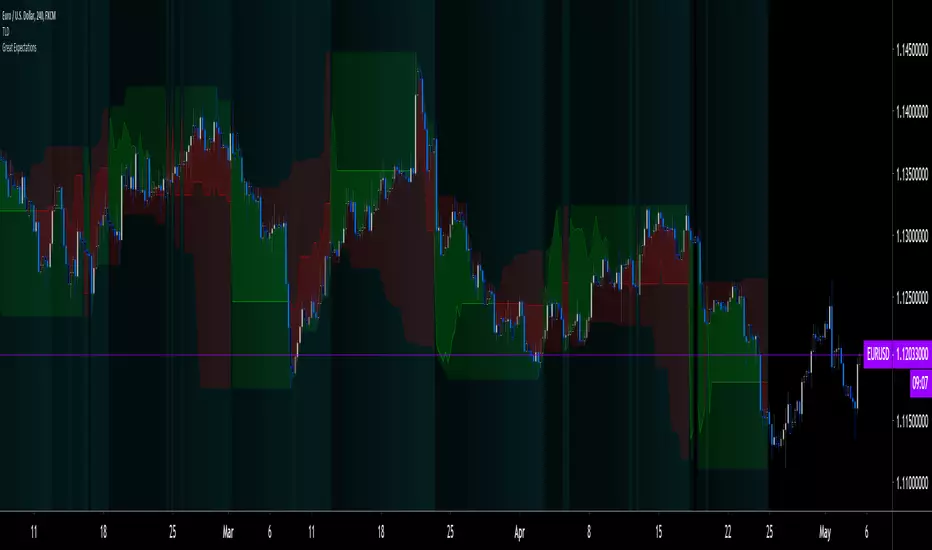

Great Expectations [LucF]Great Expectations helps traders answer the question: What is possible? It is a powerful question, yet exploration of the unknown always entails risk. A more complete set of questions better suited to traders could be:

What opportunity exists from any given point on a chart?

What portion of this opportunity can be realistically captured?

What risk will be incurred in trying to do so, and how long will it take?

Great Expectations is the result of an exploration of these questions. It is a trade simulator that generates visual and quantitative information to help strategy modelers visually identify and analyse areas of optimal expectation on charts, whether they are designing automated or discretionary strategies.

WARNING: Great Expectations is NOT an indicator that helps determine the current state of a market. It works by looking at points in the past from which the future is already known. It uses one definition of repainting extensively (i.e. it goes back in the past to print information that could not have been know at the time). Repainting understood that way is in fact almost all the indicator does! —albeit for what I hope is a noble cause. The indicator is of no use whatsoever in analyzing markets in real-time. If you do not understand what it does, please stay away!

This is an indicator—not a strategy that uses TradingView’s backtesting engine. It works by simulating trades, not unlike a backtest, but with the crucial difference that it assumes a trade (either long or short) is entered on all bars in the historic sample. It walks forward from each bar and determines possible outcomes, gathering individual trade statistics that in turn generate precious global statistics from all outcomes tested on the chart.

Great Expectations provides numbers summarizing trade results on all simulations run from the chart. Those numbers cannot be compared to backtest-produced numbers since all non-filtered bars are examined, even if an entry was taken on the bar immediately preceding the current one, which never happens in a backtest. This peculiarity does NOT invalidate Great Expectations calculations; it just entails that results be considered under a different light. Provided they are evaluated within the indicator’s context, they can be useful—sometimes even more than backtesting results, e.g. in evaluating the impact of parameter-fitting or variations in entry, exit or filtering strats.

Traders and strategy modelers are creatures of hope often suffering from blurred vision; my hope is that Great Expectations will help them appraise the validity of their setup and strat intuitions in a realistic fashion, preventing confirmation bias from obstructing perspective—and great expectations from turning into financial great deceptions.

USE CASES

You’ve identified what looks like a promising setup on other indicators. You load Great Expectations on the chart and evaluate if its high-expectation areas match locations where your setup’s conditions occur. Unless today is your lucky day, chances are the indicator will help you realize your setup is not as promising as you had hoped.

You want to get a rough estimate of the optimal trade duration for a chart and you don’t mind using the entry and exit strategies provided with the indicator. You use the trade length readouts of the indicator.

You’re experimenting with a new stop strategy and want to know how long it will keep you in trades, on average. You integrate your stop strategy in the indicator’s code and look at the average trade length it produces and the TST ratio to evaluate its performance.

You have put together your own entry and exit criteria and are looking for a filter that will help you improve backtesting results. You visually ascertain the suitability of your filter by looking at its results on the charts with great Expectations, to see if your filter is choosing its areas correctly.

You have a strategy that shows backtested trades on your chart. Great Expectations can help you evaluate how well your strategy is benefitting from high-opportunity areas while avoiding poor expectation spots.

You want more complete statistics on your set of strategies than what backtesting will provide. You use Great Expectations, knowing that it tests all bars in the sample that correspond to your criteria, as opposed to backtesting results which are limited to a subset of all possible entries.

You want to fool your friends into thinking you’ve designed the holy grail of indicators, something that identifies optimal opportunities on any chart; you show them the P&L cloud.

FEATURES

For one trade

At any given point on the chart, assuming a trade is entered there, Great Expectations shows you information specific to that trade simulation both on the chart and in the Data Window.

The chart can display:

the P & L Cloud which shows whether the trade ended profitably or not, and by how much,

the Opportunity & Risk Cloud which the maximum opportunity and risk the simulation encountered. When superimposed over the P & L cloud, you will see what I call the managed opportunity and risk, i.e the portion of maximum opportunity that was captured and the portion of the maximum risk that was incurred,

the target and if it was reached,

a background that uses a gradient to show different levels of trade length, P&L or how frequently the target was reached during simulation.

The Data Window displays more than 40 values on individual trades and global results. For any given trade you will know:

Entry/Exit levels, including slippage impact,

It’s outcome and duration,

P/L achieved,

The fraction of the maximum opportunity/risk managed by the trade.

For all trades

After going through all the possible trades on the chart, the indicator will provide you with a rare view of all outcomes expressed with the P&L cloud, which allows us to instantly see the most/least profitable areas of a chart using trade data as support, while also showing its relationship with the opportunity/risk encountered during the simulation. The difference between the two clouds is the managed opportunity and risk.

The Data Window will present you with numbers which we will go through later. Some of them are: average stop size, P/L, win rate, % opportunity managed, trade lengths for different types of trade outcomes and the TST (Target:Stop Travel) ratio.

Let’s see Great Expectations in action… and remember to open your Data Window!

INPUTS

Trade direction : You must first choose if you wish to look at long or short trades. Because of the way the indicator works and the amount of visual information on the chart, it is only practical to look at one type of trades at a time. The default is Longs.

Maximum trade Length (MaxL) : This is the maximum walk forward distance the simulator will go in analyzing outcomes from any given point in the past. It also determines the size of the dead zone among the chart’s last bars. A red background line identifies the beginning of the dead zone for which not enough bars have elapsed to analyze outcomes for the maximum trade length defined. If an ATR-based entry stop is used, that length is added to the wait time before beginning simulations, so that the first entry starts with a clean ATR value. On a sample of around 16000 bars, my tests show that the indicator runs into server errors at lengths of around 290, i.e. having completed ~4,6M simulation loop iterations. That is way too high a length anyways; 100 will usually be amply enough to ring out all the possibilities out of a simulation, and on shorter time frames, 30 can be enough. While making it unduly small will prevent simulations of expressing the market’s potential, the less you use, the faster the indicator will run. The default is 40.

Unrealized P&L base at End of Trade (EOT) : When a simulation ends and the trade is still open, we calculate unrealized P&L from an exit order executed from either the last in-trade stop on the previous bar, or the close of the last bar. You can readily see the impact of this selection on the chart, with the P&L cloud. The default is on the close.

Display : The check box besides the title does nothing.

Show target : Shows a green line displaying the trade’s target expressed as a multiple of X, i.e. the amplitude of the entry stop. I call this value “X” and use it as a unit to express profit and loss on a trade (some call it “R”). The line is highlighted for trades where the close reached the target during the trade, whether the trade ended in profit or loss. This is also where you specify the multiple of X you wish to use in calculating targets. The multiple is used even if targets are not displayed.

Show P&L Cloud : The cloud allows traders to see right away the profitable areas of the chart. The only line printed with the cloud is the “end of trade line” (EOT). The EOT line is the only way one can see the level where a trade ended on the chart (in the Data Window you can see it as the “Exit Fill” value). The EOT level for the trade determines if the trade ended in a profit or a loss. Its value represents one of the following:

- fill from order executed at close of bar where stop is breached during trade (which produces “Realized P/L”),

- simulation of a fill pseudo-fill at the user-defined EOT level (last close or stop level) if the trade runs its course through MaxL bars without getting stopped (producing Unrealized P/L).

The EOT line and the cloud fill print in green when the trade’s outcome is profitable and in red when it is not. If the trade was closed after breaching the stop, the line appears brighter.

Show Opportunity&Risk Cloud : Displays the maximum opportunity/risk that was present during the trade, i.e. the maximum and minimum prices reached.

Background Color Scheme : Allows you to choose between 3 different color schemes for the background gradients, to accommodate different types of chart background/candles. Select “None” if you don’t want a background.

Background source : Determines what value will be used to generate the different intensities of the gradient. You can choose trade length (brighter is shorter), Trade P&L (brighter is higher) or the number of times the target was reached during simulation (brighter is higher). The default is Trade Length.

Entry strat : The check box besides the title does nothing. The default strat is All bars, meaning a trade will be simulated from all bars not excluded by the filters where a MaxL bars future exists. For fun, I’ve included a pseudo-random entry strat (an indirect way of changing the seed is to vary the starting date of the simulation).

Show Filter State : Displays areas where the combination of filters you have selected are allowing entries. Filtering occurs as per your selection(s), whether the state is displayed or not. The effect of multiple selections is additive. The filters are:

1. Bar direction: Longs will only be entered if close>open and vice versa.

2. Rising Volume: Applies to both long and shorts.

3. Rising/falling MA of the length you choose over the number of bars you choose.

4. Custom indicator: You can feed your own filtering signal through this from another indicator. It must produce a signal of 1 to allow long entries and 0 to allow shorts.

Show Entry Stops :

1. Multiple of user-defined length ATR.

2. Fixed percentage.

3. Fixed value.

All entry stops are calculated using the entry fill price as a reference. The fill price is calculated from the current bar’s open, to which slippage is added if configured. This simulates the case where the strategy issued the entry signal on the previous bar for it to be executed at the next bar’s open.

The entry stop remains active until the in-trade stop becomes the more aggressive of the two stops. From then on, the entry stop will be ignored, unless a bar close breaches the in-trade stop, in which case the stop will be reset with a new entry stop and the process repeats.

Show In-trade stops : Displays in bright red the selected in-trade stop (be sure to read the note in this section about them).

1. ATR multiple: added/subtracted from the average of the two previous bars minimum/maximum of open/close.

2. A trailing stop with a deviation expressed as a multiple of entry stop (X).

3. A fixed percentage trailing stop.

Trailing stops deviations are measured from the highest/lowest high/low reached during the trade.

Note: There is a twist with the in-trade stops. It’s that for any given bar, its in-trade stop can hold multiple values, as each successive pass of the advancing simulation loops goes over it from a different entry points. What is printed is the stop from the loop that ended on that bar, which may have nothing to do with other instances of the trade’s in-trade stop for the same bar when visited from other starting points in previous simulations. There is just no practical way to print all stop values that were used for any given bar. While the printed entry stops are the actual ones used on each bar, the in-trade stops shown are merely the last instance used among many.

Include Slippage : if checked, slippage will be added/subtracted from order price to yield the fill price. Slippage is in percentage. If you choose to include slippage in the simulations, remember to adjust it by considering the liquidity of the markets and the time frame you’ll be analyzing.

Include Fees : if checked, fees will be subtracted/added to both realized an unrealized trade profits/losses. Fees are in percentage. The default fees work well for crypto markets but will need adjusting for others—especially in Forex. Remember to modify them accordingly as they can have a major impact on results. Both fees and slippage are included to remind us of their importance, even if the global numbers produced by the indicator are not representative of a real trading scenario composed of sequential trades.

Date Range filtering : the usual. Just note that the checkbox has to be selected for date filtering to activate.

DATA WINDOW

Most of the information produced by this indicator is made available in the Data Window, which you bring up by using the icon below the Watchlist and Alerts buttons at the right of the TV UI. Here’s what’s there.

Some of the information presented in the Data Window is standard trade data; other values are not so standard; e. g. the notions of managed opportunity and risk and Target:Stop Travel ratio. The interplay between all the values provided by Great Expectations is inherently complex, even for a static set of entry/filter/exit strats. During the constant updating which the habitual process of progressive refinement in building strategies that is the lot of strategy modelers entails, another level of complexity is no doubt added to the analysis of this indicator’s values. While I don’t want to sound like Wolfram presenting A New Kind of Science , I do believe that if you are a serious strategy modeler and spend the time required to get used to using all the information this indicator makes available, you may find it useful.

Trade Information

Entry Order : This is the open of the bar where simulation starts. We suppose that an entry signal was generated at the previous bar.

Entry Fill (including slip.) : The actual entry price, including slippage. This is the base price from which other values will be calculated.

Exit Order : When a stop is breached, an exit order is executed from the close of the bar that breached the stop. While there is no “In-trade stop” value included in the Data Window (other than the End of trade Stop previously discussed), this “Exit Order” value is how we can know the level where the trade was stopped during the simulation. The “Trade Length” value will then show the bar where the stop was breached.

Exit Fill (including slip.) : When the exit order is simulated, slippage is added to the order level to create the fill.

Chart: Target : This is the target calculated at the beginning of the simulation. This value also appear on the chart in teal. It is controlled by the multiple of X defined under the “Show Target” checkbox in the Inputs.

Chart: Entry Stop : This value also appears on the chart (the red dots under points where a trade was simulated). Its value is controlled by the Entry Strat chosen in the Inputs.

X (% Fill, including Fees) and X (currency) : This is the stop’s amplitude (Entry Fill – Entry Stop) + Fees. It represents the risk incurred upon entry and will be used to express P&L. We will show R expressed in both a percentage of the Entry Fill level (this value), and currency (the next value). This value represents the risk in the risk:reward ratio and is considered to be a unit of 1 so that RR can be expressed as a single value (i.e. “2” actually meaning “1:2”).

Trade Length : If trade was stopped, it’s the number of bars elapsed until then. The trade is then considered “Closed”. If the trade ends without being stopped (there is no profit-taking strat implemented, so the stop is the only exit strat), then the trade is “Open”, the length is MaxL and it will show in orange. Otherwise the value will print in green/red to reflect if the trade is winning/losing.

P&L (X) : The P&L of the trade, expressed as a multiple of X, which takes into account fees paid at entry and exit. Given our default target setting at 2 units of “X”, a trade that closes at its target will have produced a P&L of +2.0, i.e. twice the value of X (not counting fees paid at exit ). A trade that gets stopped late 50% further that the entry stop’s level will produce a P&L of -1.5X.

P&L (currency, including Fees) : same value as above, but expressed in currency.

Target first reached at bar : If price closed above the target during the trade (even if it occurs after the trade was stopped), this will show when. This value will be used in calculating our TST ratio.

Times Stop/Target reached in sim. : Includes all occurrences during the complete simulation loop.

Opportunity (X) : The highest/lowest price reached during a simulation, i.e. the maximum opportunity encountered, whether the trade was previously stopped or not, expressed as a multiple of X.

Risk (X) : The lowest/highest price reached during a simulation, i.e. the maximum risk encountered, whether the trade was previously stopped or not, expressed as a multiple of X.

Risk:Opportunity : The greater this ratio, the greater Opportunity is, compared to Risk.

Managed Opportunity (%) : The portion of Opportunity that was captured by the highest/low stop position, even if it occurred after a previous stop closed the trade.

Managed Risk (%) : The portion of risk that was protected by the lowest/highest stop position, even if it occurred after a previous stop closed the trade. When this value is greater than 100%, it means the trade’s stop is protecting more than the maximum risk, which is frequent. You will, however, never see close to those values for the Managed Opportunity value, since the stop would have to be higher than the Maximum opportunity. It is much easier to alleviate the risk than it is to lock in profits.

Managed Risk:Opportunity : The ratio of the two preceding values.

Managed Opp. vs. Risk : The Managed Opportunity minus the Managed Risk. When it is negative, which is most often is, it means your strat is protecting a greater portion of the risk than it captures opportunity.

Global Numbers

Win Rate(%) : Percentage of winning trades over all entries. Open trades are considered winning if their last stop/close (as per user selection) locks in profits.

Avg X%, Avg X (currency) : Averages of previously described values:.

Avg Profitability/Trade (APPT) : This measures expectation using: Average Profitability Per Trade = (Probability of Win × Average Win) − (Probability of Loss × Average Loss) . It quantifies the average expectation/trade, which RR alone can’t do, as the probabilities of each outcome (win/lose) must also be used to calculate expectancy. The APPT combine the RR with the win rate to yield the true expectancy of a strategy. In my usual way of expressing risk with X, APPT is the equivalent of the average P&L per trade expressed in X. An APPT of -1.5 means that we lose on average 1.5X/trade.

Equity (X), Equity (currency) : The cumulative result of all trade outcomes, expressed as a multiple of X. Multiplied by the Average X in currency, this yields the Equity in currency.

Risk:Opportunity, Managed Risk:Opportunity, Managed Opp. vs. Risk : The global values of the ones previously described.

Avg Trade Length (TL) : One of the most important values derived by going through all the simulations. Again, it is composed of either the length of stopped trades, or MaxL when the trade isn’t stopped (open). This value can help systems modelers shape the characteristics of the components they use to build their strategies.

Avg Closed Win TL and Avg Closed Lose TL : The average lengths of winning/losing trades that were stopped.

Target reached? Avg bars to Stop and Target reached? Avg bars to Target : For the trades where the target was reached at some point in the simulation, the number of bars to the first point where the stop was breached and where the target was reached, respectively. These two values are used to calculate the next value.

TST (Target:Stop Travel Ratio) : This tracks the ratio between the two preceding values (Bars to first stop/Bars to first target), but only for trades where the target was reached somewhere in the loop. A ratio of 2 means targets are reached twice as fast as stops.

The next values of this section are counts or percentages and are self-explanatory.

Chart Plots

Contains chart plots of values already describes.

NOTES

Optimization/Overfitting: There is a fine line between optimizing and overfitting. Tools like this indicator can lead unsuspecting modelers down a path of overfitting that often turns strategies into over-specialized beasts that do not perform elegantly when confronted to the real-world. Proven testing strategies like walk forward analysis will go a long way in helping modelers alleviate this risk.

Input tuning: Because the results generated by the indicator will vary with the parameters used in the active entry, filtering and exit strats, it’s important to realize that although it may be fun at first, just slapping the default settings on a chart and time frame will not yield optimal nor reliable results. While using ATR as often as possible (as I do in this indicator) is a good way to make strat parametrization adaptable, it is not a foolproof solution.

There is no data for the last MaxL bars of the chart, since not enough trade future has elapsed to run a simulation from MaxL bars back.

Modifying the code: I have tried to structure the code modularly, even if that entails a larger code base, so that you can adapt it to your needs. I’ve included a few token components in each of the placeholders designed for entry strategies, filters, entry stops and in-trade stops. This will hopefully make it easier to add your own. In the same spirit, I have also commented liberally.

You will find in the code many instances of standard trade management tasks that can be lifted to code TV strategies where, as I do in mine, you manage everything yourself and don’t rely on built-in Pine strategy functions to act on your trades.

Enjoy!

THANKS

To @scarf who showed me how plotchar() could be used to plot values without ruining scale.

To @glaz for the suggestion to include a Chandelier stop strat; I will.

To @simpelyfe for the idea of using an indicator input for the filters (if some day TV lets us use more than one, it will be useful in other modules of the indicator).

To @RicardoSantos for the random generator used in the random entry strat.

To all scripters publishing open source on TradingView; their code is the best way to learn.

To my trading buddies Irving and Bruno; who showed me way back how pro traders get it done.

Cari dalam skrip untuk "当前市场环境下综合估值百分比低于40的股票有哪些?"

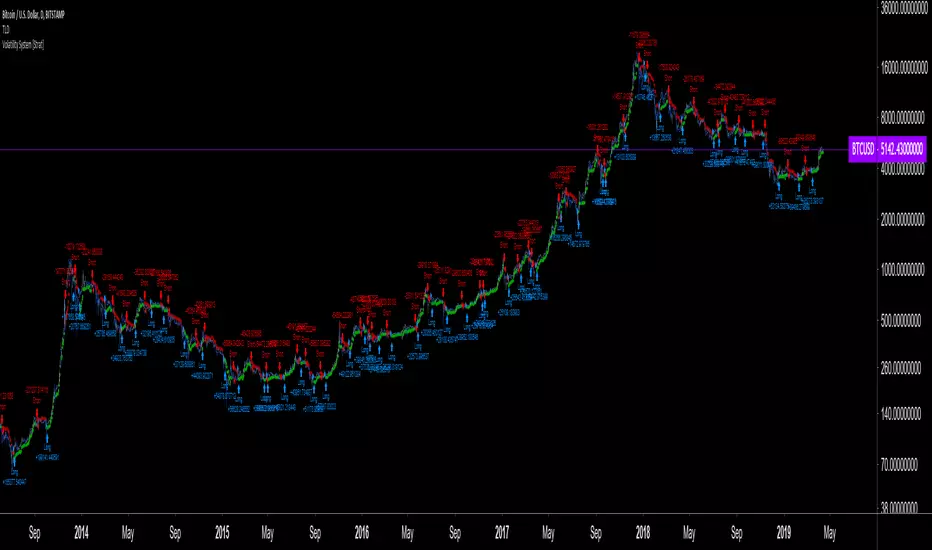

Volatility System by Wilder [LucF]The Volatility System was created by J. Welles Wilder, Jr. It first appeared in his seminal masterpiece, "New Concepts in Technical Trading Systems" (1978). He describes the system on pp.23-26, in the chapter discussing the first presentation ever of the "Volatility Index", built using a novel way of calculating a value representing volatility that he named Average True Range (ATR). The latter stuck.

The system is a pure reversal system (it is always either long or short). One of its characteristics is that its stop strategy moves up and down during a trade, widening the gap from price when volatility (ATR) increases. Because of this, this strategy can suffer large drawdowns and is not for the faint of heart.

The strategy uses a length (n) to calculate an ATR. ATR(n) is then multiplied by a factor to calculate the Average Range Constant (ARC). The ARC is then added to the lowest close n bars back to form the high Stop and Reverse points (SAR), and subtracted from the highest close n bars back to calculate the low SAR. Reversals occur when price closes above the high SAR or below the low SAR.

The system is best suited to higher time frames: 12H and above. Its performance depends heavily on calibration of the length and ARC factor. Wilder proposes a length of 7 and a factor between 2.8 to 3.1. My summary tests at 12H, 1D and 3D on stocks and cryptos yield better results with values of approximately 9-10/1.8-2.5 for cryptos and 9-10/3.0-4.0 for stocks. Small changes in the values will sometimes yield large variations in results, which I don’t particularly like because it tends to imply fragility, whereas I’d expect more robustness from a system with such simple rules. Additionally, backtests at 1D on cryptos provide so little data that no solid conclusions can be drawn from them.

All in all, the system is not very useful in my opinion; I publish it more for completeness, since as far as I can tell, it did not exist on this platform before. I also publish it out of respect for Wilder’s work. His book laid the foundation for many of the building blocks used by system designers, even today. In less than a hundred pages he presented RSI, ATR, DMI, ADXR and the Parabolic SAR indicators, some of which have become built-in functions in programming languages. This is a colossal feat and has not been repeated. Wilder is a monument.

Some lesser-known facts about his book:

It sells for the exact same price it cost in 1978: 65$,

The book has always been published by Wilder himself,

The layout hasn’t changed in 40 years,

He sells >35K copies/year.

Gotta love the guy.

The strategy is shown here on BTC /USD with settings of 12/1.8 (the defaults are 9/1.8). It shows the system under its best light. Other markets will most not reproduce such results. Also, the drawdown is as scary as the results are impressive.

Features

The code is written as a strategy but can easily be converted to an indicator if you want to use the alerts it can produce. Instructions are in the code.

You can change the length and ARC factor.

You can choose to trade only long or short positions.

You can choose to display the SARs (the stops) in multiple ways.

You can show trigger markers.

A date range can be defined.

3 alerts: reversals (both long and short), longs, shorts. Remember that for the moment, strategies cannot generate alerts in TradingView, so the strategy must be converted to an indicator in order to make the alerts available.

all EMAs-----One indicator for nine EMAsThis indicator includes 9 EMAs (5,10,20,30,40,50,60,100,200,400). You don't need to open many signal EMA indicators to compare short terms and long terms trends.

You can adjust the parameters for your favoured time period.

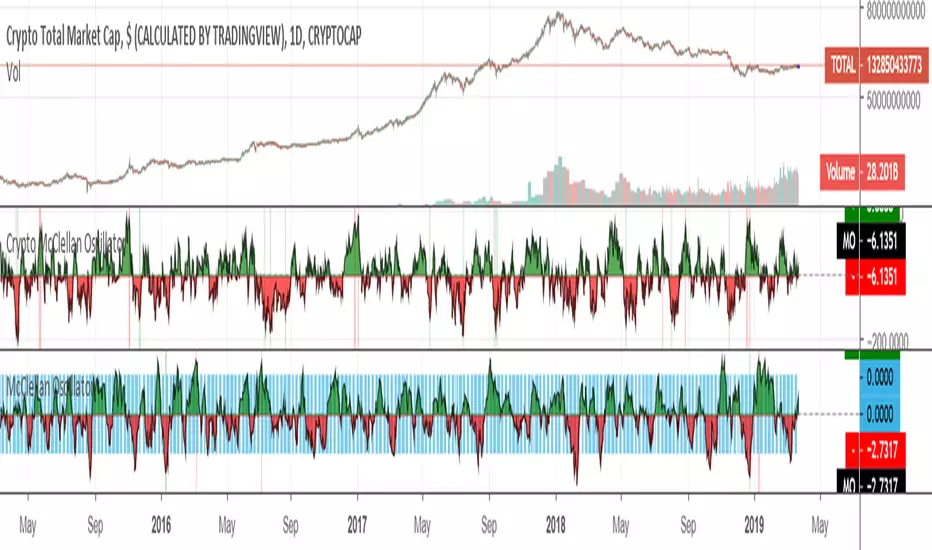

Crypto McClellan OscillatorMcClellan Oscillator for cryptocurrency, taking into account only the top 40 cryptos.

Original code was by LazyBear.

Multi SMA EMA WMA HMA BB (5x8 MAs Bollinger Bands) MAX MTF - RRBMulti SMA EMA WMA HMA 4x7 Moving Averages with Bollinger Bands MAX MTF by RagingRocketBull 2019

Version 1.0

All available MAX MTF versions are listed below (They are very similar and I don't want to publish them as separate indicators):

ver 1.0: 4x7 = 28 MTF MAs + 28 Levels + 3 BB = 59 < 64

ver 2.0: 5x6 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 3.0: 3x10 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 4.0: 5(4+1)x8 = 8 CurTF MAs + 32 MTF MAs + 20 Levels + 3 BB = 63 < 64

ver 5.0: 6(5+1)x6 = 6 CurTF MAs + 30 MTF MAs + 24 Levels + 3 BB = 63 < 64

ver 6.0: 4(3+1)x10 = 10 CurTF MAs + 30 MTF MAs + 20 Levels + 3 BB = 63 < 64

Fib numbers: 8, 13, 21, 34, 55, 89, 144, 233, 377

This indicator shows multiple MAs of any type SMA EMA WMA HMA etc with BB and MTF support, can show MAs as dynamically moving levels.

There are 4 MA groups + 1 BB group, a total of 4 TFs * 7 MAs = 28 MAs. You can assign any type/timeframe combo to a group, for example:

- EMAs 9,12,26,50,100,200,400 x H1, H4, D1, W1 (4 TFs x 7 MAs x 1 type)

- EMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 x M15, H1 (2 TFs x 14 MAs x 1 type)

- D1 EMAs and SMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 (1 TF x 14 MAs x 2 types)

- H1 WMAs 13,21,34,55,89,144,233; H4 HMAs 9,12,26,50,100,200,400; D1 EMAs 12,26,89,144,169,233,377; W1 SMAs 9,12,26,50,100,200,400 (4 TFs x 7 MAs x 4 types)

- +1 extra MA type/timeframe for BB

There are several versions: Simple, MTF, Pro MTF, Advanced MTF, MAX MTF and Ultimate MTF. This is the MAX MTF version. The Differences are listed below. All versions have BB

- Simple: you have 2 groups of MAs that can be assigned any type (5+5)

- MTF: +2 custom Timeframes for each group (2x5 MTF) +1 TF for BB, TF XY smoothing

- Pro MTF: 4 custom Timeframes for each group (4x3 MTF), 1 TF for BB, MA levels and show max bars back options

- Advanced MTF: +4 extra MAs/group (4x7 MTF), custom Ticker/Symbols, Timeframe <>= filter, Remove Duplicates Option

- MAX MTF: +2 subtypes/group, packed to the limit with max possible MAs/TFs: 4x7, 5x6, 3x10, 4(3+1)x10, 5(4+1)x8, 6(5+1)x6

- Ultimate MTF: +individual settings for each MA, custom Ticker/Symbols

MAX MTF version tests the limits of Pinescript trying to squeeze as many MAs/TFs as possible into a single indicator.

It's basically a maxed out Advanced version with subtypes allowing for mixed types within a group (i.e. both emas and smas in a single group/TF)

Pinescript has the following limits:

- max 40 security calls (6 calls are reserved for dupe checks and smoothing, 2 are used for BB, so only 32 calls are available)

- max 64 plot outputs (BB uses 3 outputs, so only 61 plot outputs are available)

- max 50000 (50kb) size of the compiled code

Based on those limits, you can only have the following MAs/TFs combos in a single script:

1. 4x7, 5x6, 3x10 - total number of MTF MAs must always be <= 32, and you can still have BB and Num Levels = total MAs, without any compromises

2. 5(4+1)x8, 6(5+1)x6, 4(3+1)x10 - you can use the Current Symbol/Timeframe as an extra (+1) fixed TF with the same number of MTF MAs

- you don't need to call security to display MAs on the Current Symbol/Timeframe, so the total number of MTF MAs remains the same and is still <= 32

- to fit that many MAs into the max 64 plot outputs limit you need to reduce the number of levels (not every MA Group will have corresponding levels)

Features:

- 4x7 = 28 MAs of any type

- 4x MTF groups with XY step line smoothing

- +1 extra TF/type for BB MAs

- 2 MA subtypes within each group/TF

- 4x7 = 28 MA levels with adjustable group offsets, indents and shift

- supports any existing type of MA: SMA, EMA, WMA, Hull Moving Average (HMA)

- custom tickers/symbols for each group

- show max bars back option

- show/hide both groups of MAs/levels/BB and individual MAs

- timeframe filter: show only MAs/Levels with TFs <>= Current TF

- hide MAs/Levels with duplicate TFs

- support for custom TFs that are not available in free accounts: 2D, 3D etc

- support for timeframes in H: H, 2H, 4H etc

Notes:

- Uses timeframe textbox instead of input resolution dropdown to allow for 240 120 and other custom TFs

- Uses symbol textbox instead of input symbol to avoid establishing multiple dummy security connections to the current ticker - otherwise empty symbols will prevent script from running

- Possible reasons for missing MAs on a chart:

- there may not be enough bars in history to start plotting it. For example, W1 EMA200 needs at least 200 bars on a weekly chart.

- for charts with low/fractional prices i.e. 0.00002 << 0.001 (default Y smoothing step) decrease Y smoothing as needed (set Y = 0.0000001) or disable it completely (set X,Y to 0,0)

- for charts with high price values i.e. 20000 >> 0.001 increase Y smoothing as needed (set Y = 10-20). Higher values exceeding MAs point density will cause it to disappear as there will be no points to plot. Different TFs may require diff adjustments

- TradingView Replay Mode UI and Pinescript security calls are limited to TFs >= D (D,2D,W,MN...) for free accounts

- attempting to plot any TF < D1 in Replay Mode will only result in straight lines, but all TFs will work properly in history and real-time modes. This is not a bug.

- Max Bars Back (num_bars) is limited to 5000 for free accounts (10000 for paid), will show error when exceeded. To plot on all available history set to 0 (default)

- Slow load/redraw times. This indicator becomes slower, its UI less responsive when:

- Pinescript Node.js graphics library is too slow and inefficient at plotting bars/objects in a browser window. Code optimization doesn't help much - the graphics engine is the main reason for general slowness.

- the chart has a long history (10000+ bars) in a browser's cache (you have scrolled back a couple of screens in a max zoom mode).

- Reload the page/Load a fresh chart and then apply the indicator or

- Switch to another Timeframe (old TF history will still remain in cache and that TF will be slow)

- in max possible zoom mode around 4500 bars can fit on 1 screen - this also slows down responsiveness. Reset Zoom level

- initial load and redraw times after a param change in UI also depend on TF. For example: D1/W1 - 2 sec, H1/H4 - 5-6 sec, M30 - 10 sec, M15/M5 - 4 sec, M1 - 5 sec. M30 usually has the longest history (up to 16000 bars) and W1 - the shortest (1000 bars).

- when indicator uses more MAs (plots) and timeframes it will redraw slower. Seems that up to 5 Timeframes is acceptable, but 6+ Timeframes can become very slow.

- show_last=last_bars plot limit doesn't affect load/redraw times, so it was removed from MA plot

- Max Bars Back (num_bars) default/custom set UI value doesn't seem to affect load/redraw times

- In max zoom mode all dynamic levels disappear (they behave like text)

- Dupe check includes symbol: symbol, tf, both subtypes - all must match for a duplicate group

- For the dupe check to work correctly a custom symbol must always include an exchange prefix. BB is not checked for dupes

Good Luck! Feel free to learn from/reuse the code to build your own indicators.

12 Exponential Moving AveragesThe Guppy Multiple Moving Average (GMMA). The short-term MAs are typically set at 3, 5, 8, 10, 12, and 15 periods. The longer-term MAs are typically set at 30, 35, 40, 45, 50, and 60.

12 Exponential Moving Averages Guppy The Guppy Multiple Moving Average (GMMA). The short-term MAs are typically set at 3, 5, 8, 10, 12, and 15 periods. The longer-term MAs are typically set at 30, 35, 40, 45, 50, and 60.

16x VWMACombination of 16 VWMAs to find out where the market makers are.

vwma 10/20/30 - red

vwma 40 - green

vwma 50/60/70/80 - orange

vwma 150/160/180/200 - blue

vwma 300/320/340/389 - black

Linear regression slope as SARThis model calculate the slope of the linear regression and give you the uptrend or the down trend of the slope

red line are downtrend and green line are up trend

using len 1 you can make it longer or shorter (I put it on length of 40 but you can change that to what ever you want )

Similar to SAR it can give us the trends of buy and sell only by doing it by the linear way

try longer length to see if it smooth the signal

4 hour graph

TheStocksDoctor_WVF + ADX + CCIThis script is a modified version of CM Williams Vix Fix for which I have added an indicator that shows when ADX and CCI are both indicating positive momentum - highlighted by green bars. This is part of TheStocksDoctor Trading System.

Inputs are as follows:

Lookback period Standard Deviation High ---> 22

Bolinger Band Length ---> 20

Bollinger Band Standard Dev.. ---> 2

Lookback period percentile high ---> 50

Highest Percentile ---> 0.85

----Highlight bars Below... --->

Show Highlight bar if WVF WAS true is now False --->

Show highlight bar if WVF IS True --->

----Highlight bars Below Use Filtered... --->

Show highlight bar for filtered entry --->

Show highlight bar for AGGRESSIVE Filtered Entry? --->

Check below to Turn all Bars Gray --->

Check box to Turn Bars gray? --->

Long-term look back current bar has to close Below... ---> 40

Medium-term look back current bar has to close below... ---> 14

Entry price action strength --close... ---> 3

--------Turn On/Off Alerts below... --->

---To activate alerts you HAVE To Check... --->

---You can un Check the box BELOW... --->

Show Williams Vix Fix Histogram... --->

Show Alert WVF = True? --->

Show Alert WVF wa true now False? --->

Show Alert WVF Filtered? --->

Show Alert WVF AGGRESSIVE Filter? --->

ADX Smoothing ---> 17

DI Length ---> 17

Stochastic for Reversal Predict [yoxxx] Usable for all markets, all time frames. (The bull bear sup/res lines are specific for stocks, but differ just a little to other instruments.)

This script is more likely a method support than a study - and your exit from the default stochastic club:

Most people use Stoch for ins and outs by 20 rsp 80 (a default behavior MM know well to deal with). C.G. Lane, the inventor of this indicator,

however used it to find divergences with quote (price / close) to predict reversals. Constance Brown refined this method by laying

a fix time cycle underneath the chart that is in rhythm with specific highs or lows of a stock or an index.

The length of one cycle divided by 2 equals the proper value for %D specified for that stock /index. The script offers an input for this specific value.

C. Brown stresses that good signals are only given within the bull or bear ranges (20-65 for bear markets, 40-80 for bull markets).

For your convenience, I laid these areas underneath the graphs. You can automate the divergence research (relative to quote)

by using my script "Bull Bear Divergence Indicator". Feedback welcome. Have fun and success.

Multiple MACD RSI simple strategySimple strategy script I've had for a while but looks like I never published.

Although it is one of my most simple it seems to have the best profitability. It is pretty rough though. the Stoch RSI has only a little weight to the trade trigger. I'll refine it more over time or you can by all means. Basically the Stoch RSI current K line has to be OVER 40 to trigger a SELL. It has no effect on buy side.

The triggers are roughly as follows:

Year - since so many assets have gone 2x, 3x, 10x+ since 2013 having a strategy that earns a 500% return from 2013 to now isn't that good if buy-and-holding would have got you 800%. This eliminates some of that noise and makes it a little easier to quickly gauge success. So buy/sell trigger need a value of greater or equal to 2018 (default)

MACD 1 - First MACD (short) needs to indicate greater than 0 to buy or less than 0 to sell.

MACD 2 - Same as MACD1 but for second MACD set (long)

Uptrend - Latest close + high divided by last periods close + high needs to be grater than 1. So if latest is 34.30 close and 34.60 high and previous interval is 34.80 close and 34.82 high, that is 0.99 and will not trigger a buy trade.

Downtrend - Same thing but close + low and less than 1.

This script/strategy is pretty rough but if there is interest I'll polish it more since it is a pretty solid but simple strategy for most assets.

Trend Lines and MoreMulti-Indicator consisting of several useful indicators in a single package.

TREND LINES

-By default the 20 SMA and 50 SMA are shown.

-Use "MOVING AVERAGE TYPE" to select SMA, EMA, Double-EMA, Triple-EMA, or Hull.

-Use "50 MA TREND COLOR" to have the 50 turn green/red for uptrend/downtrend.

-Use "DAILY SOURCE ONLY" to always show daily averages regardless of timeframe.

-Use "SHOW LONG MA" to also include 100, 150, and 200 moving averages.

-Use "SHOW MARKERS" to show a small colored marker identifying which line is which.

OTHER INDICATORS

-You can show Bollinger Bands and Parabolic SAR.

-You can highlight key reversal times (9:50-10:10 and 14:40-15:00).

-You can show price offset markers, where was the price "n" periods ago.

That last one is useful to show the level of prices which are about to "fall off" the moving average

and be replaced with current price. So for example, if current price is significantly below the

200-days-ago price, you can gauge the difficulty for the 200 MA to start climbing again.

JSE Market Breadth Stocks>MAThis indicator is for the Johannesburg Stock Exchange (JSE) and indicates the number of stocks in the Top 40 Index above its selected Smooth Moving Average (SMA). Typically the 200SMA is used to see the longer term health of the market and the 50SMA for a short term view. Currently the market has reached a point that less than 2% of stocks were above their 200SMA which is the lowest since 2013.

Triple Cross of DeathExponential moving averages in red of 4 and 16, exponential moving average of 40 in orange and simple moving average of 200 in yellow to confirm the triple crossing of 4, 16 and 40.

Taken from Lions against gazelles by Jose Luis Carpatos.

QEMA - 8 Exponential Moving Averages (20 - 55) / MadianQEMA - 8 Exponential Moving Averages (20, 25, 30, 35, 40, 45, 50, 55)

This QEMA act as support and resistance .

The Scale Of Sacred SoundsBased on the Sacred Sound Scale

How to use it:

This indicator is designed to capture the inferred behavior of traders and investors by using two groups of averages.

Meant for longer trades and trend indicator.

Used on any timescale as needed.

Can trade on long or short where the slow MA crosses fast Ma or where the Slow MA compresses and flips open again.

Follow the trend to the end - pot of gold at the end of the rainbow :-)

References:

Based on Daryl Guppy GMMA and

www.guppytraders.com

Read more at:

whatmusicreallyis.com

There is one tuning in which the frequencies 432, 528, 424 and 440 Hz can peacefully coexist. The scale has 32+1 pure harmonic tones and the reference frequency of 256 Hz. It comes from the Natural Ascending Series of Harmonics 32 to 64 of the 8 Hz Fundamental Tone, and represents its 6th double. I call this tuning The Scale of Sacred Sounds.

Representation using ancient Sumerian/Babylonian/Vedic math:

32; 33; 34; 35; 36; 37; 38; 39; 40; 41; 42; 43; 44; 45; 46; 47; 48; 49; 50; 51; 52; 53; 54; 55; 56; 57; 58; 59; 60; 61; 62; 63; 64

Representation using musical ratios:

1/1; 33/32; 17/16; 35/32; 9/8; 37/32; 19/16; 39/32; 5/4; 41/32; 21/16; 43/32; 11/8; 45/32; 23/16; 47/32; 3/2; 49/32; 25/16; 51/32; 13/8; 53/32; 27/16; 55/32; 7/4; 57/32; 29/16; 59/32; 15/8; 61/32; 31/16; 63/32; 2/1

The math for deriving one of the above series from the other is simple. Divide all numbers from the ancient series by the first, then simplify the fractions. Conversely, the series of ratios can be turned into the series of integers by calculating their least common denominator (the smallest whole number that is a multiple of all numbers under the fraction bar) and discarding it.

Logarithmic representation using musical constants (definition given further down):

0,000; 30,772; 60,625; 89,612; 117,783; 145,182; 171,850; 197,826; 223,144; 247,836; 271,934; 295,464; 318,454; 340,927; 362,905; 384,412; 405,465; 426,084; 446,287; 466,090; 485,508; 504,556; 523,248; 541,597; 559,616; 577,315; 594,707; 611,802; 628,609; 645,138; 661,398; 677,399; 693,147

5 Moving Average (Simple / Exponential)Defaults to 1 SMA with 4 EMA bands. 200 SMA is intended to show the trend; 20,40 and 55 EMA show entries; 81 EMA is used as stop/take profit. Defaults are inspired by 'Eric Choe' but you can switch between EMA and SMA as per your own preference. Philakone uses all 5 as EMA 8, 13, 21, 55, 200

Tommy Oscillator v1.0 LightRSI rules: If we break above 70 RSI, 40-50 RSI acts as support,

If we break below 30 RSI, 50-60 RSI acts as resistance

I color coded the support/resistance areas to make visuals easier. This is part of my private indicator, but I removed the buy/sell part (which is the private part). I think this will help a lot with your guy's trading.

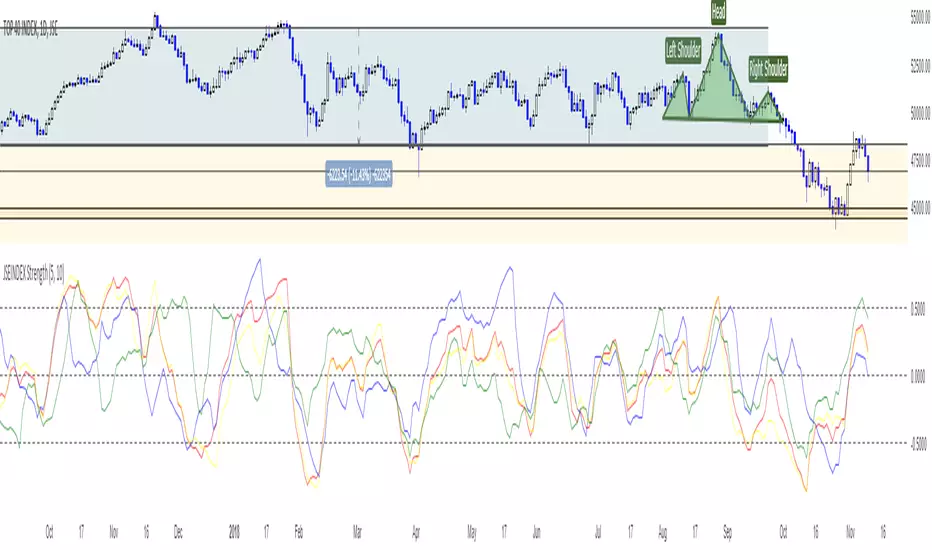

JSEINDEX StrengthJSE:J200

JSE:J210

JSE:J211

JSE:J212

This script shows all three major indecies on JSE and compare their strength.

RED = TOP 40

BLUE = RESI 10

YELLOW = INDI 25

GREEN = FIN 15

Current state of the indicator points that strongest index is FIN15 weakest is RESI10 and that INDI25 is closely following TOP40

Idea is to be short weakest index or member of the index currently RESI10

Bitfinex Longs/Shorts Ratio AlertableThis script contains Bitfinex longs/short ratio and generates alarms with a given input .default value is 60 which means alerts when either shorts/longs reach 60:40 ratio

Katana Gaps Bounty Hunter Pro (Show Gaps of All Types) by RRBKatana Gaps Bounty Hunter Pro (KGB Hunter Pro, Gap Exterminator) by RagingRocketBull 2018

Version 1.0

This indicator shows/counts/filters gaps on a chart.

There are several versions: Simple, Pro, Advanced and Zones. This is the Pro version. The Differences are listed below.

- Simple: shows/counts gaps, changes color based on gap dir (2 colors), filters out price gaps within session, large gaps, and high volume gaps

- Pro: +shows all types of gaps, multi color, pro filters (full/partial/overlapping time, price, large, candle, volume, doji, weekend gaps within delta ranges)

- Advanced: +session times mask, show/count gaps only for last N bars, +min/max/filled gaps stats, dark mode

- Zones: +shows gaps as dynamic horiz zones

KGB Hunter Pro Gap Exterminator focuses on showing you all possible types of gaps in multiple colors. Gap theory states that price tends to return and fill the gaps,

so you can use it to collect the bounty. You can apply any combination of complex filters to narrow down search results i.e., find only all:

- type 3 gaps up with allowed wick-candle overlapping of up to 10% and

- gap size larger than 200 and

- with at least one of the candles larger than 100 and

- volume change at least 40 and

- spanning less than 2 bar periods and

- excluding weekend gaps

Features:

- highlights gaps using barcolor and plotchar chars (8 colors x 2 dirs)

- supports all 3 types of gap overlapping: full gap (no overlapping), wick-wick and wick-body overlapping up to a specified % of candle body

- finds all types of gaps with pro filters for price, time, large, volume, timerange, candle size, doji gaps

- individual show/hide flags for each gap/char based on gap type

- can show/hide gaps/chars based on gap dir

- changes color of gaps/chars based on gap dir/type, multi color gap type combos

- displays chars above/below bar based on gap dir

- can show/hide weekend gaps

- counts all filtered gaps

Colors:

Basically There are 2 gap types (Price, Time) x 2 directions (Up, Down) x 2 modifiers (Large, Volume), Volume Gap is a separate class with its own modifiers, so more accurately:

- (Price, Time) x 2 directions (Up, Down) x Large modifier

- (Price Volume, Time Volume) x 2 directions (Up, Down) x Large modifier

using a total of 16+1 colors or 8+1 base colors + transparency modifier

depending on settings you can highlight gaps using any multi color combo from just 1 to all 16 colors (+1 gray color for weekends).

basic gap = 1 base color with normal transparency

price,time = 2 base colors (including basic gap) with normal transparency (+1 color)

* up,down dir = +2 new base colors with normal transparency (including 2 base colors), with a total of 2*2 = 4 price/time base colors (+2 colors)

* large = same 4 base colors with vivid transparency modifier (+4 colors)

* volume = +2 new base colors with normal transparency, a separate class (+2 colors)

* volume * up,down dir = +another 2 new base colors with normal transparency (including 2 volume base colors), with a total of 2*2 = 4 volume base colors (+2 colors)

* volume * large = 4 volume base colors with vivid transparency modifier (+4 colors)

weekend_gap = gray (+1 color)

doji gap, candle gap, timerange gap = no special color, inherits color from parent gap type

for more details, please see the Gap Color Hierarchy comments in code

_________________________________________________________________________

You can find the following gap related terminology in literature: full, partial, extreme, breakaway, runaway/continuation, common, exhaustion gaps.

There are no exact rules to distinguish between them, so this can't be implemented.

When defining a gap it all boils down to how do you plot a gap, which points between adjacent candles do you consider a gap. Different sources apply different methodology

but in practice only 3 types of gap overlapping can exist:

- full gap (no overlapping),

- partial (wick-wick overlapping) and

- extreme partial (wick-body overlapping up to a specified % of a candle body)

All these types are supported in this script. The only possible remaining option is candle-candle overlapping which is not a gap by definition.

Many other script specific subtypes are also supported. Please see description of each gap type below and comments in code.

General display modes

- gap has 3 possible overlapping modes: full gap (no overlapping), wick-wick overlapping, wick-candle overlapping up to a specified % of candle body size (for mode 3 only)

the remaining candle-candle overlapping implies not a gap by definition

full gap mode will find the least amount of gaps, wick-candle - the most

- gap can be either price or time, up or down, and shown above or below the candles (gap chars)

- by definition, a price gap is a smaller subset of a time gap, a gap within current session with a price gap and zero time lag between bars.

Therefore timerange filter is useless for price gaps, but can still be applied.

On the other hand, all price gap filters can be applied to time gaps without any distinction.

- gap can have multiple modifier subtypes: (price|time) * (up|down) * (large? + volume? + doji? + timerange? + weekend?)

i.e. price + large + volume + doji or time + large + volume + timerange + doji + weekend

- the gap is always counted only once no matter how many subtype modifiers it has

- if the gap does not satisfy any of the applied flags/filters it is not shown/counted (no gap bars/chars are shown)

- gap color can depend on a combo of gap type/dir and modifier subtypes or can be shown in a single base color

- char color can only depend on gap dir (not type/modifiers) or can be shown in a single base color

- char position can also depend on gap dir (above/below) the gap candle. Alternatively you can pin chars to the top/bottom of the screen in UI Styles.

- change_by_type = true - uses gap type base colors (2 colors + optional modifiers, up to 8 colors if volume and/or large filters are enabled)

- change_by_dir = true - uses gap dir base colors (2 colors + optional modifiers, up to 8 colors if volume and/or large filters are enabled)

- both change_by_type and change_by_dir = true - uses both gap type and dir base colors (4 colors + optional modifiers, up to 16 colors if volume and/or large filters are enabled)

- both change_by_type and change_by_dir = false - uses a single base gap color (1 color)

- don't need that much colors - disable filters

- highlight bars has priority over individual gap flags, when it is false all gaps are hidden regardless of their corresponding flag settings (does not affect dim weekend gaps)

- show chars has priority over individual gap char flags, when it is false all char flags are hidden regardless of their corresponding flag settings

- price gaps are only shown/counted when show_price_gaps flag is true. The large or volume filters can be used to narrow down results further.

- time gaps are only shown/counted when show_time_gaps flag is true. The large, volume, and timerange filters can be used to narrow down results further.

- doji gaps are only shown/counted when show_doji_gaps flag is true. The doji candle size and other filters can be used to narrow down results further.

- show weekend gaps = true and dim weekend gaps = false - shows/counts weekend gaps

- show weekend gaps = true and dim weekend gaps = true - dims weekend gaps, doesn't show/count weekwend gaps

- show/dim weekend gaps do just that - show the gap if it happens on a weekend, not all weekends

- large gaps are only shown/counted when the large filter is enabled != 0. positive values 5 (>= 5), negative -5 (<=5) are used to switch between <>

- volume gaps are only shown/counted when the volume filter is enabled != 0. positive values 5 (>= 5), negative -5 (<=5) are used to switch between <>

- timerange gaps are only shown/counted when the timerange filter is enabled != 0. positive values 5 (>= 5), negative -5 (<=5) are used to switch between <>

- candle size gaps are only shown/counted when the candle size filter is enabled != 0. positive values 5 (>= 5), negative -5 (<=5) are used to switch between <>

- candle size filter is the only filter with 2 arguments, use_and_for_delta to enable AND condition for the args (OR is the default)

Good Luck! Feel free to explore and learn from the code

TRI MA DominoBlue lines are first group (3,5,8,13,21) SMA and red lines are second group (35,40,45,50,55) SMA. When blue lines cross above red lines that signals bull market and vice versa. More lines we have above or bellow (creating domino effect) the stronger the signal for bull/bear.

This indicator should be used to determine where are we currently in the market and should we expect trend change/transition or continuation.

It should not be used as sole indicator for taking trades but as a tool to help you with TA and your trading plan.

Good hunting ;)