RRG Relative Strength# RRG Relative Strength (RRG RS)

Compare any symbol to a benchmark using two RRG-style lines: **RS-Ratio** (trend of relative strength) and **RS-Momentum** (momentum of that trend). Both are centered at **100**:

- **RS-Ratio > 100** → outperforming the benchmark

- **RS-Ratio < 100** → underperforming

- **RS-Momentum** often **leads** RS-Ratio (crosses 100 earlier)

# How it works

1) Relative Strength (RS): RS = Close(symbol) / Close(benchmark)

2) Normalize around 100: smooth RS with EMA and divide RS by that EMA

3) RS-Ratio: EMA( RS / EMA(RS, Length), LenSmooth ) * 100

4) RS-Momentum: RS-Ratio / EMA(RS-Ratio, LenSmooth) * 100

# Inputs

- Length (default 14): normalization window for RS

- Length Smooth (default 20): smoothing window for RS-Ratio & RS-Momentum

# Benchmark (auto)

- US: SP:SPX (S&P 500)

- Vietnam: HOSE:VNINDEX

- Crypto: INDEX:BTCUSD

(Modify the mapping if needed, or replace with your own input.symbol().)

# How to read

- Improving: RS-Momentum crosses above 100 while RS-Ratio turns up

- Leading: RS-Ratio > 100 with RS-Momentum ≥ 100

- Weakening: RS-Momentum drops below 100; RS-Ratio often follows

# Timeframes & presets

- Works on Daily and Weekly charts

- Daily (fast): 14 / 20

- Approx. weekly behavior on Daily: 50 / 60

Note: Values usually hover near 100 (e.g., ~90–110) but are not strictly bounded. Ensure your symbol and benchmark trade in comparable sessions/currencies.

Cari dalam skrip untuk "想象图:箱线图+折线组合,横轴为国家,纵轴为响应指数(0-100),箱线显示均值±标准差,叠加红色虚线标注各国确诊高峰时间点"

Fibs Has Lied 🌟 Fibs Has Lied - Indicator Overview 🌟

Designed for indices like US30, NQ, and SPX, this indicator highlights setups where price interacts with key EMA levels during specific trading sessions (default: 6:30–11:30 AM EST).

🌟 Key Features & Levels 🌟

🔹EMA Crossover Setups

The indicator uses the 100-period and 200-period EMAs to identify bullish and bearish setups:

- Bullish Setup: Triggers when the 100 EMA crosses above the 200 EMA, followed by two consecutive candles opening above the 100 EMA, with the low within a specified point distance (e.g., 20 points for US30).

- Bearish Setup: Triggers when the 100 EMA crosses below the 200 EMA, followed by two consecutive candles opening below the 100 EMA, with the high within the point distance.

- Signals are marked with green (buy) or red (sell) triangles and text, ensuring you don’t miss a setup. 📈

🔹 Reset Conditions for Re-Entries

After an initial setup, the indicator watches for “reset” opportunities:

- Buy Reset: If price moves below the 200 EMA after a bullish crossover, then returns with two consecutive candles where lows are above the 100 EMA (within point distance), a new buy signal is plotted.

- Sell Reset: If price moves above the 200 EMA after a bearish crossover, then returns with two consecutive candles where highs are below the 100 EMA (within point distance), a new sell signal is plotted.

This feature captures additional entries after liquidity grabs or fakeouts, aligning with ICT’s manipulation concepts. 🔄

🔹 Session-Based Filtering

Focus your trades during high-liquidity windows! The default session (6:30–11:30 AM EST, New York timezone) targets the London/NY overlap, where price often seeks liquidity or sets up for reversals. Toggle the time filter off for 24/7 signals if desired. 🕒

🔹Symbol-Specific Point Distance

Customizable entry zones based on your chosen index:

- US30: 20 points from the 100 EMA.

- NQ: 3 points from the 100 EMA.

- SPX: 2.5 points from the 100 EMA.

This ensures setups are tailored to the volatility of your market, maximizing relevance. 🎯

🔹 Market Structure Markers (Optional)

Visualize swing points with pivot-based labels:

- HH (Higher High): Signals uptrend continuation.

- HL (Higher Low): Indicates potential bullish support.

- LH (Lower High): Suggests weakening uptrend or reversal.

- LL (Lower Low): Points to downtrend continuation.

- Toggle these on/off to keep your chart clean while analyzing trend direction. 📊

🔹 EMA Visualization

Optionally plot the 100 EMA (blue) and 200 EMA (red) to see key levels where price reacts. These act as dynamic support/resistance, perfect for spotting liquidity pools or ICT’s Power of 3 setups. ⚖️

🌟 Customization Options 🌟

- Symbol Selection: Choose US30, NQ, or SPX to adjust point distance for entries.

- Time Filter: Enable/disable the 6:30–11:30 AM EST session to focus on high-liquidity periods.

- EMA Display: Toggle 100/200 EMAs on/off to reduce chart clutter.

- Market Structure: Show/hide HH/HL/LH/LL labels for cleaner analysis.

- Signal Markers: Green (buy) and red (sell) triangles with text are auto-plotted for easy identification.

🌟 Usage Tips 🌟

- Best Timeframes: Use on 3m for intraday scalping and 30m for swing trades.

- Combine with ICT Tools: Pair with order blocks, fair value gaps, or kill zones for stronger setups.

- Focus on Session: The default 6:30–11:30 AM EST session captures London/NY volatility—perfect for liquidity-driven moves.

- Avoid Overcrowding: Disable market structure or EMAs if you only want setup signals.

CCO_LibraryLibrary "CCO_Library"

Contrarian Crowd Oscillator (CCO) Library - Multi-oscillator consensus indicator for contrarian trading signals

@author B3AR_Trades

calculate_oscillators(rsi_length, stoch_length, cci_length, williams_length, roc_length, mfi_length, percentile_lookback, use_rsi, use_stochastic, use_williams, use_cci, use_roc, use_mfi)

Calculate normalized oscillator values

Parameters:

rsi_length (simple int) : (int) RSI calculation period

stoch_length (int) : (int) Stochastic calculation period

cci_length (int) : (int) CCI calculation period

williams_length (int) : (int) Williams %R calculation period

roc_length (int) : (int) ROC calculation period

mfi_length (int) : (int) MFI calculation period

percentile_lookback (int) : (int) Lookback period for CCI/ROC percentile ranking

use_rsi (bool) : (bool) Include RSI in calculations

use_stochastic (bool) : (bool) Include Stochastic in calculations

use_williams (bool) : (bool) Include Williams %R in calculations

use_cci (bool) : (bool) Include CCI in calculations

use_roc (bool) : (bool) Include ROC in calculations

use_mfi (bool) : (bool) Include MFI in calculations

Returns: (OscillatorValues) Normalized oscillator values

calculate_consensus_score(oscillators, use_rsi, use_stochastic, use_williams, use_cci, use_roc, use_mfi, weight_by_reliability, consensus_smoothing)

Calculate weighted consensus score

Parameters:

oscillators (OscillatorValues) : (OscillatorValues) Individual oscillator values

use_rsi (bool) : (bool) Include RSI in consensus

use_stochastic (bool) : (bool) Include Stochastic in consensus

use_williams (bool) : (bool) Include Williams %R in consensus

use_cci (bool) : (bool) Include CCI in consensus

use_roc (bool) : (bool) Include ROC in consensus

use_mfi (bool) : (bool) Include MFI in consensus

weight_by_reliability (bool) : (bool) Apply reliability-based weights

consensus_smoothing (int) : (int) Smoothing period for consensus

Returns: (float) Weighted consensus score (0-100)

calculate_consensus_strength(oscillators, consensus_score, use_rsi, use_stochastic, use_williams, use_cci, use_roc, use_mfi)

Calculate consensus strength (agreement between oscillators)

Parameters:

oscillators (OscillatorValues) : (OscillatorValues) Individual oscillator values

consensus_score (float) : (float) Current consensus score

use_rsi (bool) : (bool) Include RSI in strength calculation

use_stochastic (bool) : (bool) Include Stochastic in strength calculation

use_williams (bool) : (bool) Include Williams %R in strength calculation

use_cci (bool) : (bool) Include CCI in strength calculation

use_roc (bool) : (bool) Include ROC in strength calculation

use_mfi (bool) : (bool) Include MFI in strength calculation

Returns: (float) Consensus strength (0-100)

classify_regime(consensus_score)

Classify consensus regime

Parameters:

consensus_score (float) : (float) Current consensus score

Returns: (ConsensusRegime) Regime classification

detect_signals(consensus_score, consensus_strength, consensus_momentum, regime)

Detect trading signals

Parameters:

consensus_score (float) : (float) Current consensus score

consensus_strength (float) : (float) Current consensus strength

consensus_momentum (float) : (float) Consensus momentum

regime (ConsensusRegime) : (ConsensusRegime) Current regime classification

Returns: (TradingSignals) Trading signal conditions

calculate_cco(rsi_length, stoch_length, cci_length, williams_length, roc_length, mfi_length, consensus_smoothing, percentile_lookback, use_rsi, use_stochastic, use_williams, use_cci, use_roc, use_mfi, weight_by_reliability, detect_momentum)

Calculate complete CCO analysis

Parameters:

rsi_length (simple int) : (int) RSI calculation period

stoch_length (int) : (int) Stochastic calculation period

cci_length (int) : (int) CCI calculation period

williams_length (int) : (int) Williams %R calculation period

roc_length (int) : (int) ROC calculation period

mfi_length (int) : (int) MFI calculation period

consensus_smoothing (int) : (int) Consensus smoothing period

percentile_lookback (int) : (int) Percentile ranking lookback

use_rsi (bool) : (bool) Include RSI

use_stochastic (bool) : (bool) Include Stochastic

use_williams (bool) : (bool) Include Williams %R

use_cci (bool) : (bool) Include CCI

use_roc (bool) : (bool) Include ROC

use_mfi (bool) : (bool) Include MFI

weight_by_reliability (bool) : (bool) Apply reliability weights

detect_momentum (bool) : (bool) Calculate momentum and acceleration

Returns: (CCOResult) Complete CCO analysis results

calculate_cco_default()

Calculate CCO with default parameters

Returns: (CCOResult) CCO result with standard settings

cco_consensus_score()

Get just the consensus score with default parameters

Returns: (float) Consensus score (0-100)

cco_consensus_strength()

Get just the consensus strength with default parameters

Returns: (float) Consensus strength (0-100)

is_panic_bottom()

Check if in panic bottom condition

Returns: (bool) True if panic bottom signal active

is_euphoric_top()

Check if in euphoric top condition

Returns: (bool) True if euphoric top signal active

bullish_consensus_reversal()

Check for bullish consensus reversal

Returns: (bool) True if bullish reversal detected

bearish_consensus_reversal()

Check for bearish consensus reversal

Returns: (bool) True if bearish reversal detected

bearish_divergence()

Check for bearish divergence

Returns: (bool) True if bearish divergence detected

bullish_divergence()

Check for bullish divergence

Returns: (bool) True if bullish divergence detected

get_regime_name()

Get current regime name

Returns: (string) Current consensus regime name

get_contrarian_signal()

Get contrarian signal

Returns: (string) Current contrarian trading signal

get_position_multiplier()

Get position size multiplier

Returns: (float) Recommended position sizing multiplier

OscillatorValues

Individual oscillator values

Fields:

rsi (series float) : RSI value (0-100)

stochastic (series float) : Stochastic value (0-100)

williams (series float) : Williams %R value (0-100, normalized)

cci (series float) : CCI percentile value (0-100)

roc (series float) : ROC percentile value (0-100)

mfi (series float) : Money Flow Index value (0-100)

ConsensusRegime

Consensus regime classification

Fields:

extreme_bearish (series bool) : Extreme bearish consensus (<= 20)

moderate_bearish (series bool) : Moderate bearish consensus (20-40)

mixed (series bool) : Mixed consensus (40-60)

moderate_bullish (series bool) : Moderate bullish consensus (60-80)

extreme_bullish (series bool) : Extreme bullish consensus (>= 80)

regime_name (series string) : Text description of current regime

contrarian_signal (series string) : Contrarian trading signal

TradingSignals

Trading signals

Fields:

panic_bottom_signal (series bool) : Extreme bearish consensus with high strength

euphoric_top_signal (series bool) : Extreme bullish consensus with high strength

consensus_reversal_bullish (series bool) : Bullish consensus reversal

consensus_reversal_bearish (series bool) : Bearish consensus reversal

bearish_divergence (series bool) : Bearish price-consensus divergence

bullish_divergence (series bool) : Bullish price-consensus divergence

strong_consensus (series bool) : High consensus strength signal

CCOResult

Complete CCO calculation results

Fields:

consensus_score (series float) : Main consensus score (0-100)

consensus_strength (series float) : Consensus strength (0-100)

consensus_momentum (series float) : Rate of consensus change

consensus_acceleration (series float) : Rate of momentum change

oscillators (OscillatorValues) : Individual oscillator values

regime (ConsensusRegime) : Regime classification

signals (TradingSignals) : Trading signals

position_multiplier (series float) : Recommended position sizing multiplier

Precision Trade Zone By KittisakThis indicator is designed for Money Management calculations, helping to facilitate risk management in trading, determining suitable leverage based on acceptable risk, and adjusting the Stop Loss level to align with the calculated leverage.

Abbreviation Descriptions

LR : Suitable Leverage.

EP : Entry Price.

BEP : Break-Even Point (a point where you can move your Stop Loss to prevent losses once the price reaches a certain level).

SL : Stop Loss (a recalculated Stop Loss level to match the leverage. You should use this as the Stop Loss price instead of the initial level you set).

TP : Take Profit (a point where you take profit based on the defined risk-reward ratio).

Note

When first activating the indicator, an error may occur, and no output will be displayed. This happens because you must first specify the Entry Price and Stop Loss in the indicator settings.

How Much Leverage Should You Use?

It may seem like a simple question but is difficult to answer.

Method for Calculating Suitable Leverage

Use the formula:

Leverage = Acceptable Loss / (Distance between Entry Price and Stop Loss + (Buy Fee + Sell Fee))

Calculating the Correct Stop Loss Point

(Stop Loss levels will be slightly adjusted or extended)

For Long Positions :

New Stop Loss = Entry Price * (1 - Acceptable Loss / (Calculated Leverage * 100))

For Short Positions :

New Stop Loss = Entry Price * (1 + Acceptable Loss / (Calculated Leverage * 100))

Calculating the Correct Take Profit Point

(Take Profit levels will be slightly adjusted or extended)

For Long Positions :

Take Profit = Entry Price * (1 + (Acceptable Loss / (Calculated Leverage * 100) * RR) + ((Buy Fee + Sell Fee) / 100))

For Short Positions :

Take Profit = Entry Price * (1 - (Acceptable Loss / (Calculated Leverage * 100) * RR) + ((Buy Fee + Sell Fee) / 100))

Benefits of This Calculation

1. Accurate Risk Assessment

The calculated leverage accounts for trading fees. For example, if you aim for a 2% loss, this method ensures the actual loss is exactly 2%, not more (e.g., 2% plus fees).

2. Eliminates Guesswork

Randomly setting leverage can lead to risks because the Stop Loss level may not align with your position. This calculation ensures that the leverage aligns precisely with your desired Stop Loss level.

3. Realistic Profit Targets

For example, with a 2% acceptable loss and a 1:2 RR, you expect a 4% profit. However, without this calculation, fees may reduce your profit below 4%. This method includes fees, ensuring your profit matches the intended target.

Caution

This indicator does not account for slippage or requotes. Use it with caution and allow a buffer for slippage in your calculations.

Indicator นี้มีไว้สำหรับคำนวณ Money Management ซึ่งจะช่วยอำนวยความสะดวกในการจัดการความเสี่ยงในการเทรด การคำนวณ Leverage ที่เหมาะสมกับความเสี่ยงที่คุณยอมรับได้ และจัดการจุด Stop Loss ให้เหมาะสมกับ Leverage นั้น

คำอธิบายเกี่ยวกับคำย่อ

LR หมายถึง Leverage ที่เหมาะสม

EP หมายถึง Entry Price หรือราคาเข้าซื้อ

BEP หมายถึง Break-Even Point หรือจุดคุ้มทุน (คุณสามารถย้าย Stop Loss มาที่จุดนี้เมื่อราคาไปถึงจุดหนึ่งเพื่อป้องกันการขาดทุนได้)

SL หมายถึง Stop Loss (ซึ่งเป็น Stop Loss ที่คำนวณใหม่เพื่อให้ตำแหน่งเหมาะสมกับ Leverage ที่คำนวณได้ คุณควรใช้จุดนี้เพื่อเป็นราคา Stop Loss แทนจุด Stop Loss ที่คุณกำหนดไว้ในตอนแรก)

TP หมายถึง Take Profit (เป็นจุดที่คุณจะขายทำกำไรตาม RR ที่กำหนดไว้)

* หมายเหตุ เมื่อเริ่มเปิด Indicator จะเกิด Error ขึ้น และไม่มีผลลัพท์ใด ๆ แสดงให้เห็น นั่นเป็นเพราะคุณต้องเข้าไปกำหนด Entry Price และ Stop Loss ในการตั้งค่าของ Indicator เสียก่อน

ต้องใช้ Leverage เท่าไหร่? มันเป็นคำถามที่ดูเหมือนง่าย แต่ตอบยาก

วิธีคำนวณ Leverage ที่เหมาะสม ใช้สมการคือ

Levarage = การขาดทุนที่ยอมรับได้ / (ระยะห่างระหว่าง Entry Price และ Stop Loss + (ค่าธรรมเนียมซื้อ + ค่าธรรมเนียมขาย))

นำผลลัพท์ Leverage ที่ได้มาคำนวณเพื่อหาจุด Stop Loss ที่ถูกต้อง (จุดของ Stop Loss จะมีการยืดขยายออกไปเล็กน้อย) โดยใช้สมการ

ตำแหน่ง Stop Loss ใหม่ = Entry Price * (1 - การขาดทุนที่ยอมรับได้ / (Leverage ที่คำนวณได้ * 100)) // สำหรับ Long

ตำแหน่ง Stop Loss ใหม่ = Entry Price * (1 + การขาดทุนที่ยอมรับได้ / (Leverage ที่คำนวณได้ * 100)) // สำหรับ Short

นำผลลัพท์ Leverage ที่ได้มาคำนวณเพื่อหาจุด Take Profit ที่ถูกต้อง (จุดของ Take Profit จะมีการยืดขยายออกไปเล็กน้อย) โดยใช้สมการ

ตำแหน่ง Take Profit = Entry Price * (1 + (การขาดทุนที่ยอมรับได้ / (Leverage ที่คำนวณได้ * 100) * RR) + ((ค่าธรรมเนียมซื้อ + ค่าธรรมเนียมขาย) / 100)) // สำหรับ Long

ตำแหน่ง Take Profit = Entry Price * (1 - (การขาดทุนที่ยอมรับได้ / (Leverage ที่คำนวณได้ * 100) * RR) + ((ค่าธรรมเนียมซื้อ + ค่าธรรมเนียมขาย) / 100)) // สำหรับ Short

ข้อดีของการคำนวณคือ

1. คุณจะได้ค่า Leverage ที่เหมาะสมกับความเสี่ยงที่คุณยอมรับได้โดยรวมค่าธรรมเนียมเข้าไปในนั้นแล้ว นั่นหมายความว่า ความสูญเสียจะเป็น 2% (ตามตัวอย่าง) จริง ๆ ไม่ใช่ 2% และถูกหักค่าธรรมเนียมเพิ่มอีก กลายเป็นสูญเสียมากกว่า 2%

2. การตั้ง Leverage มั่ว ๆ กลายเป็นความเสี่ยง นั่นเพราะตำแหน่งของ Stop Loss ไม่ได้อยู่ในจุดที่ควรจะเป็น การคำนวณนี้ช่วยให้คุณได้ Leverage ในตำแหน่ง Stop Loss ที่คุณต้องการโดยแท้จริง

3. ผลกำไรที่ได้รับตรงกับความต้องการจริง ๆ เช่น การขาดทุนที่ยอมรับได้ 2% และ RR 1:2 สิ่งที่คุณคิดคือกำไร 4% แต่จริง ๆ แล้วไม่ถึง 4% นั่นเพราะว่าโดนหักค่าธรรมเนียมไปส่วนหนึ่ง การคำนวณนี้ได้รวมค่าธรรมเนียมให้แล้ว คุณจึงได้กำไรที่ 4% อย่างถูกต้องตามต้องการ

ข้อควรระวัง

Indicator นี้ไม่ได้มีการควบคุมความเสี่ยงในเรื่องของ slippage หรือ requote โปรดใช้งานอย่างระมัดระวังและมีการเผื่อระยะสำหรับ slippage ด้วย

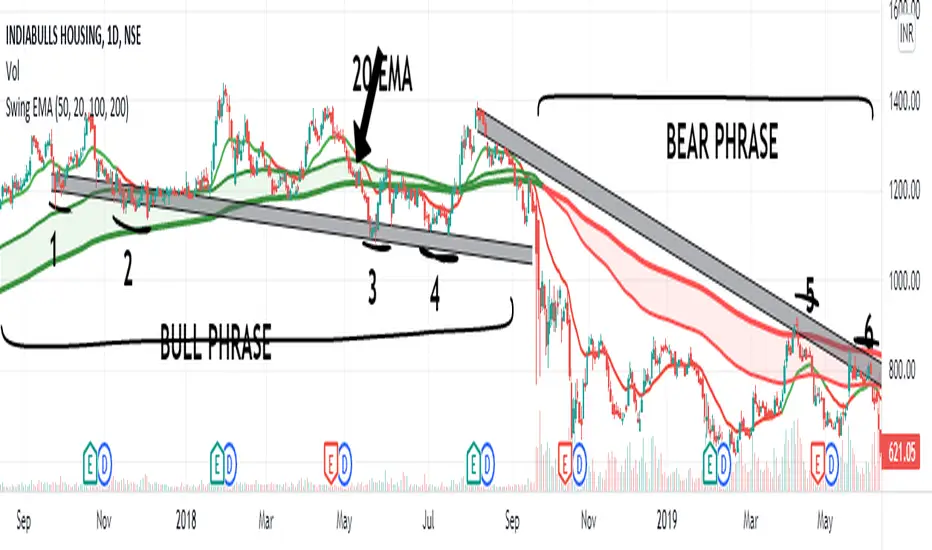

Swing EMAWhat is Swing EMA?

Swing EMA is an exponential moving average crossover-based indicator used for low-risk directional trading.

it's used for different types of Ema 20,50,100 and 200, 3 of them are plotted on chat 20,100,200.

100 and 200 Ema is used for showing support and resistance and it contains highlights area between them and its change color according to market crossover condition.

20 moving average is used for knowing Market Behaviour and changing its color according to crossover conditions of 50 and 20 Ema.

How does it work?

It contains 4 different types of moving averages 20,50,100, 200 out of 3 are plotted on the chart.

20 Ema is used for knowing current market behavior. Its changes its color based on the crossover of 50 Ema and 20 Ema, if 20 Ema is higher than 50 Ema then it changes its color to green, and its opposites are changed their color to red when 20 Ema is lower than 50 Ema.

100 and 200 Ema used as a support and resistance and is also contain highlighted areas between them its change their color based on the crossover if 100 Ema is higher than 200 Ema a then both of them are going to change color to Green and as an opposite, if 200 Ema is higher then 100 Ema is going to change its color to red.

So in simple word 100 and 200 Ema is used as support and resistance zone and 20 Ema is used to know current market behavior.

How to use it?

It is very easy to understand by looking at the example I gave where are the two different types of phrases. phrase bull phrase and bear phrase so 100 and 200 Ema is used as a support and resistance and to tell you which phrase is currently on the market on example there is a bull phrase on the left side and bear phrase on the right side by using your technical analysis you can find out a really good spot to buy your stocks on a bull phrase and too short on the bear phrase. 20 Ema is used as a knowing the current market behavior it doesn't make any difference on buying or selling as much as 100 Ema and 200 Ema.

Tips

Don't trade against the market.

Try trade on trending stocks rather than sideways stock.

The higher the area between 100 Ema and 200 Ema is the stronger the phrase.

Do Backtesting before real trading.

Enjoy Trading.

BossHouse - CCI ExtendedBossHouse - CCI Extended ( An Extended version of the Original CCI ).

The commodity channel index (CCI) is an oscillator originally introduced by Donald Lambert in 1980.

Guideline

________

Lambert's trading guidelines for the CCI focused on movements above +100 and below −100 to generate buy and sell signals. Because about 70 to 80 percent of the CCI values are between +100 and −100, a buy or sell signal will be in force only 20 to 30 percent of the time. When the CCI moves above +100, a security is considered to be entering into a strong uptrend and a buy signal is given. The position should be closed when the CCI moves back below +100. When the CCI moves below −100, the security is considered to be in a strong downtrend and a sell signal is given. The position should be closed when the CCI moves back above −100.

Since Lambert's original guidelines, traders have also found the CCI valuable for identifying reversals. The CCI is a versatile indicator capable of producing a wide array of buy and sell signals.

CCI can be used to identify overbought and oversold levels. A security would be deemed oversold when the CCI dips below −100 and overbought when it exceeds +100. From oversold levels, a buy signal might be given when the CCI moves back above −100. From overbought levels, a sell signal might be given when the CCI moved back below +100.

As with most oscillators, divergences can also be applied to increase the robustness of signals. A positive divergence below −100 would increase the robustness of a signal based on a move back above −100. A negative divergence above +100 would increase the robustness of a signal based on a move back below +100.

Trend line breaks can be used to generate signals. Trend lines can be drawn connecting the peaks and troughs. From oversold levels, an advance above −100 and trend line breakout could be considered bullish. From overbought levels, a decline below +100 and a trend line break could be considered bearish.

Settings

_______

Show 0 line

Lenght

Source

Any help and suggestions will be appreciated.

Marcos Issler @ Isslerman

marcos@bosshouse.com.br

Guitar Hero [theUltimator5]The Guitar Hero indicator transforms traditional oscillator signals into a visually engaging, game-like display reminiscent of the popular Guitar Hero video game. Instead of standard line plots, this indicator presents oscillator values as colored segments or blocks, making it easier to quickly identify market conditions at a glance.

Choose from 8 different technical oscillators:

RSI (Relative Strength Index)

Stochastic %K

Stochastic %D

Williams %R

CCI (Commodity Channel Index)

MFI (Money Flow Index)

TSI (True Strength Index)

Ultimate Oscillator

Visual Display Modes

1) Boxes Mode : Creates distinct rectangular boxes for each bar, providing a clean, segmented appearance. (default)

This visual display is limited by the amount of box plots that TradingView allows on each indictor, so it will only plot a limited history. If you want to view a similar visual display that has minor breaks between boxes, then use the fill mode.

2) Fill Mode : Uses filled areas between plot boundaries.

Use this mode when you want to view the plots further back in history without the strict drawing limitations.

Five-Level Color-Coded System

The indicator normalizes all oscillator values to a 0-100 scale and categorizes them into five distinct levels:

Level 1 (Red): Very Oversold (0-19)

Level 2 (Orange): Oversold (20-29)

Level 3 (Yellow): Neutral (30-70)

Level 4 (Aqua): Overbought (71-80)

Level 5 (Lime): Very Overbought (81-100)

Customization Options

Signal Parameters

Signal Length: Primary period for oscillator calculation (default: 14)

Signal Length 2: Secondary period for Stochastic %D and TSI (default: 3)

Signal Length 3: Tertiary period for TSI calculation (default: 25)

Display Controls

Show Horizontal Reference Lines: Toggle grid lines for better level identification

Show Information Table: Display current signal type, value, and normalized value

Table Position: Choose from 9 different screen positions for the info table

Display Mode: Switch between Boxes and Fills visualization

Max Bars to Display: Control how many historical bars to show (50-450 range)

Normalization Process

The indicator automatically normalizes different oscillator ranges to a consistent 0-100 scale:

Williams %R: Converts from -100/0 range to 0-100

CCI: Maps typical -300/+300 range to 0-100

TSI: Transforms -100/+100 range to 0-100

Other oscillators: Already use 0-100 scale (RSI, Stochastic, MFI, Ultimate Oscillator)

This was designed as an educational tool

The gamified approach makes learning about oscillators more engaging for new traders.

FlowScape PredictorFlowScape Predictor is a non-repainting, regime-aware entry qualifier that turns complex market context into two readiness scores (Long & Short, each 0/25/50/75/100) and clean, confirmed-bar signals. It blends three orthogonal pillars so you act only when trend energy, momentum, and location agree:

Regime (energy): ATR-normalized linear-regression slope of a smooth HMA → EMA baseline, gated by ADX to confirm when pressure is meaningful.

Momentum (push): RSI slope alignment so price has directional follow-through, not just drift.

Structure (location): proximity to pivot-confirmed swings, scaled by ATR, so “ready” appears near constructive pullbacks—not mid-trend chases.

A soft ATR cloud wraps the baseline for context. A yellow Predictive Baseline extends beyond the last bar to visualize near-term trajectory. It is visual-only: scores/alerts never use it.

What you see

Baseline line that turns green/red when regime is strong in that direction; gray when weak.

ATR cloud around the baseline (context for stretch and pullbacks).

Scores (Long & Short, 0–100 in steps of 25) and optional “L/S” icons on bar close.

Yellow Predictive Baseline that extends to the right for a few bars (visual trajectory of the smoothed baseline).

The scoring system (simple and transparent)

Each side (Long/Short) sums four binary checks, 25 points each:

Regime aligned: trendStrong is true and LR slope sign favors that side.

Momentum aligned: RSI side (>50 for Long, <50 for Short) and RSI slope confirms direction.

Baseline side: price is above (Long) / below (Short) the baseline.

Location constructive: distance from the last confirmed pivot is healthy (ATR-scaled; not overstretched).

Valid totals are 0, 25, 50, 75, 100.

Best-quality signal: 100/0 (your side/opposite) on bar close.

Good, still valid: 75/0, especially when the missing block is only “location” right as price re-engages the cloud/baseline.

Avoid: 75/25 or any opposition > 0 in a weak (gray) regime.

The Predictive (Kalman) line — what it is and isn’t

The yellow line is a visual forward extension of the smoothed baseline to help you see the current trajectory and time pullback resumptions. It does not predict price and is excluded from scores and alerts.

How it’s built (plain English):

We maintain a one-dimensional Kalman state x as a smoothed estimate of the baseline. Each bar we observe the current baseline z.

The filter adjusts its trust using the Kalman gain K = P / (P + R) and updates:

x := x + K*(z − x), then P := (1 − K)*P + Q.

Q (process noise): Higher Q → expects faster change → tracks turns quicker (less smoothing).

R (measurement noise): Higher R → trusts raw baseline less → smoother, steadier projection.

What you control:

Lead (how many bars forward to draw).

Kalman Q/R (visual smoothness vs. responsiveness).

Toggle the line on/off if you prefer a minimal chart.

Important: The predictive line extends the baseline, not price. It’s a visual timing aid—don’t automate off it.

How to use (step-by-step)

Keep the chart clean and use a standard OHLC/candlestick chart.

Read the regime: Prefer trades with green/red baseline (trendStrong = true).

Check scores on bar close:

Take Long 100 / Short 0 or Long 75 / Short 0 when the chart shows a tidy pullback re-engaging the cloud/baseline.

Mirror the logic for shorts.

Confirm location: If price is > ~1.5 ATR from its reference pivot, let it come back—avoid chasing.

Set alerts: Add an alert on Long Ready or Short Ready; these fire on closed bars only.

Risk management: Use ATR-buffered stops beyond the recent pivot; target fixed-R multiples (e.g., 1.5–3.0R). Manage the trade with the baseline/cloud if you trail.

Best-practice playbook (quick rules)

Green light: 100/0 (best) or 75/0 (good) on bar close in a colored (non-gray) regime.

Location first: Prefer entries near the baseline/cloud right after a pullback, not far above/below it.

Avoid mixed signals: Skip 75/25 and anything with opposition while the baseline is gray.

Use the yellow line with discretion: It helps you see rhythm; it’s not a signal source.

Timeframes & tuning (practical defaults)

Intraday indices/FX (5m–15m): Demand 100/0 in chop; allow 75/0 when ADX is awake and pullback is clean.

Crypto intraday (15m–1h): Prefer 100/0; 75/0 on the first pullback after a regime turn.

Swing (1h–4h/D1): 75/0 is often sufficient; 100/0 is excellent (fewer but cleaner signals).

If choppy: raise ADX threshold, raise the readiness bar (insist on 100/0), or lengthen the RSI slope window.

What makes FlowScape different

Energy-first regime filter: ATR-normalized LR slope + ADX gate yields a consistent read of trend quality across symbols and timeframes.

Location-aware entries: ATR-scaled pivot proximity discourages mid-air chases, encouraging pullback timing.

Separation of concerns: The predictive line is visual-only, while scores/alerts are confirmed on close for non-repainting behavior.

One simple score per side: A single 0–100 readiness figure is easier to tune than juggling multiple indicators.

Transparency & limitations

Scores are coarse by design (25-point blocks). They’re a gatekeeper, not a promise of outcomes.

Pivots confirm after right-side bars, so structure signals appear after swings form (non-repainting by design).

Avoid using non-standard chart types (Heikin Ashi, Renko, Range, etc.) for signals; use a clean, standard chart.

No lookahead, no higher-timeframe requests; alerts fire on closed bars only.

Wavelet-Trend ML Integration [Alpha Extract]Alpha-Extract Volatility Quality Indicator

The Alpha-Extract Volatility Quality (AVQ) Indicator provides traders with deep insights into market volatility by measuring the directional strength of price movements. This sophisticated momentum-based tool helps identify overbought and oversold conditions, offering actionable buy and sell signals based on volatility trends and standard deviation bands.

🔶 CALCULATION

The indicator processes volatility quality data through a series of analytical steps:

Bar Range Calculation: Measures true range (TR) to capture price volatility.

Directional Weighting: Applies directional bias (positive for bullish candles, negative for bearish) to the true range.

VQI Computation: Uses an exponential moving average (EMA) of weighted volatility to derive the Volatility Quality Index (VQI).

Smoothing: Applies an additional EMA to smooth the VQI for clearer signals.

Normalization: Optionally normalizes VQI to a -100/+100 scale based on historical highs and lows.

Standard Deviation Bands: Calculates three upper and lower bands using standard deviation multipliers for volatility thresholds.

Signal Generation: Produces overbought/oversold signals when VQI reaches extreme levels (±200 in normalized mode).

Formula:

Bar Range = True Range (TR)

Weighted Volatility = Bar Range × (Close > Open ? 1 : Close < Open ? -1 : 0)

VQI Raw = EMA(Weighted Volatility, VQI Length)

VQI Smoothed = EMA(VQI Raw, Smoothing Length)

VQI Normalized = ((VQI Smoothed - Lowest VQI) / (Highest VQI - Lowest VQI) - 0.5) × 200

Upper Band N = VQI Smoothed + (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

Lower Band N = VQI Smoothed - (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

🔶 DETAILS

Visual Features:

VQI Plot: Displays VQI as a line or histogram (lime for positive, red for negative).

Standard Deviation Bands: Plots three upper and lower bands (teal for upper, grayscale for lower) to indicate volatility thresholds.

Reference Levels: Horizontal lines at 0 (neutral), +100, and -100 (in normalized mode) for context.

Zone Highlighting: Overbought (⋎ above bars) and oversold (⋏ below bars) signals for extreme VQI levels (±200 in normalized mode).

Candle Coloring: Optional candle overlay colored by VQI direction (lime for positive, red for negative).

Interpretation:

VQI ≥ 200 (Normalized): Overbought condition, strong sell signal.

VQI 100–200: High volatility, potential selling opportunity.

VQI 0–100: Neutral bullish momentum.

VQI 0 to -100: Neutral bearish momentum.

VQI -100 to -200: High volatility, strong bearish momentum.

VQI ≤ -200 (Normalized): Oversold condition, strong buy signal.

🔶 EXAMPLES

Overbought Signal Detection: When VQI exceeds 200 (normalized), the indicator flags potential market tops with a red ⋎ symbol.

Example: During strong uptrends, VQI reaching 200 has historically preceded corrections, allowing traders to secure profits.

Oversold Signal Detection: When VQI falls below -200 (normalized), a lime ⋏ symbol highlights potential buying opportunities.

Example: In bearish markets, VQI dropping below -200 has marked reversal points for profitable long entries.

Volatility Trend Tracking: The VQI plot and bands help traders visualize shifts in market momentum.

Example: A rising VQI crossing above zero with widening bands indicates strengthening bullish momentum, guiding traders to hold or enter long positions.

Dynamic Support/Resistance: Standard deviation bands act as dynamic volatility thresholds during price movements.

Example: Price reversals often occur near the third standard deviation bands, providing reliable entry/exit points during volatile periods.

🔶 SETTINGS

Customization Options:

VQI Length: Adjust the EMA period for VQI calculation (default: 14, range: 1–50).

Smoothing Length: Set the EMA period for smoothing (default: 5, range: 1–50).

Standard Deviation Multipliers: Customize multipliers for bands (defaults: 1.0, 2.0, 3.0).

Normalization: Toggle normalization to -100/+100 scale and adjust lookback period (default: 200, min: 50).

Display Style: Switch between line or histogram plot for VQI.

Candle Overlay: Enable/disable VQI-colored candles (lime for positive, red for negative).

The Alpha-Extract Volatility Quality Indicator empowers traders with a robust tool to navigate market volatility. By combining directional price range analysis with smoothed volatility metrics, it identifies overbought and oversold conditions, offering clear buy and sell signals. The customizable standard deviation bands and optional normalization provide precise context for market conditions, enabling traders to make informed decisions across various market cycles.

Volatility Quality [Alpha Extract]The Alpha-Extract Volatility Quality (AVQ) Indicator provides traders with deep insights into market volatility by measuring the directional strength of price movements. This sophisticated momentum-based tool helps identify overbought and oversold conditions, offering actionable buy and sell signals based on volatility trends and standard deviation bands.

🔶 CALCULATION

The indicator processes volatility quality data through a series of analytical steps:

Bar Range Calculation: Measures true range (TR) to capture price volatility.

Directional Weighting: Applies directional bias (positive for bullish candles, negative for bearish) to the true range.

VQI Computation: Uses an exponential moving average (EMA) of weighted volatility to derive the Volatility Quality Index (VQI).

vqiRaw = ta.ema(weightedVol, vqiLen)

Smoothing: Applies an additional EMA to smooth the VQI for clearer signals.

Normalization: Optionally normalizes VQI to a -100/+100 scale based on historical highs and lows.

Standard Deviation Bands: Calculates three upper and lower bands using standard deviation multipliers for volatility thresholds.

vqiStdev = ta.stdev(vqiSmoothed, vqiLen)

upperBand1 = vqiSmoothed + (vqiStdev * stdevMultiplier1)

upperBand2 = vqiSmoothed + (vqiStdev * stdevMultiplier2)

upperBand3 = vqiSmoothed + (vqiStdev * stdevMultiplier3)

lowerBand1 = vqiSmoothed - (vqiStdev * stdevMultiplier1)

lowerBand2 = vqiSmoothed - (vqiStdev * stdevMultiplier2)

lowerBand3 = vqiSmoothed - (vqiStdev * stdevMultiplier3)

Signal Generation: Produces overbought/oversold signals when VQI reaches extreme levels (±200 in normalized mode).

Formula:

Bar Range = True Range (TR)

Weighted Volatility = Bar Range × (Close > Open ? 1 : Close < Open ? -1 : 0)

VQI Raw = EMA(Weighted Volatility, VQI Length)

VQI Smoothed = EMA(VQI Raw, Smoothing Length)

VQI Normalized = ((VQI Smoothed - Lowest VQI) / (Highest VQI - Lowest VQI) - 0.5) × 200

Upper Band N = VQI Smoothed + (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

Lower Band N = VQI Smoothed - (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

🔶 DETAILS

Visual Features:

VQI Plot: Displays VQI as a line or histogram (lime for positive, red for negative).

Standard Deviation Bands: Plots three upper and lower bands (teal for upper, grayscale for lower) to indicate volatility thresholds.

Reference Levels: Horizontal lines at 0 (neutral), +100, and -100 (in normalized mode) for context.

Zone Highlighting: Overbought (⋎ above bars) and oversold (⋏ below bars) signals for extreme VQI levels (±200 in normalized mode).

Candle Coloring: Optional candle overlay colored by VQI direction (lime for positive, red for negative).

Interpretation:

VQI ≥ 200 (Normalized): Overbought condition, strong sell signal.

VQI 100–200: High volatility, potential selling opportunity.

VQI 0–100: Neutral bullish momentum.

VQI 0 to -100: Neutral bearish momentum.

VQI -100 to -200: High volatility, strong bearish momentum.

VQI ≤ -200 (Normalized): Oversold condition, strong buy signal.

🔶 EXAMPLES

Overbought Signal Detection: When VQI exceeds 200 (normalized), the indicator flags potential market tops with a red ⋎ symbol.

Example: During strong uptrends, VQI reaching 200 has historically preceded corrections, allowing traders to secure profits.

Oversold Signal Detection: When VQI falls below -200 (normalized), a lime ⋏ symbol highlights potential buying opportunities.

Example: In bearish markets, VQI dropping below -200 has marked reversal points for profitable long entries.

Volatility Trend Tracking: The VQI plot and bands help traders visualize shifts in market momentum.

Example: A rising VQI crossing above zero with widening bands indicates strengthening bullish momentum, guiding traders to hold or enter long positions.

Dynamic Support/Resistance: Standard deviation bands act as dynamic volatility thresholds during price movements.

Example: Price reversals often occur near the third standard deviation bands, providing reliable entry/exit points during volatile periods.

🔶 SETTINGS

Customization Options:

VQI Length: Adjust the EMA period for VQI calculation (default: 14, range: 1–50).

Smoothing Length: Set the EMA period for smoothing (default: 5, range: 1–50).

Standard Deviation Multipliers: Customize multipliers for bands (defaults: 1.0, 2.0, 3.0).

Normalization: Toggle normalization to -100/+100 scale and adjust lookback period (default: 200, min: 50).

Display Style: Switch between line or histogram plot for VQI.

Candle Overlay: Enable/disable VQI-colored candles (lime for positive, red for negative).

The Alpha-Extract Volatility Quality Indicator empowers traders with a robust tool to navigate market volatility. By combining directional price range analysis with smoothed volatility metrics, it identifies overbought and oversold conditions, offering clear buy and sell signals. The customizable standard deviation bands and optional normalization provide precise context for market conditions, enabling traders to make informed decisions across various market cycles.

RSI Weighted Trend System I [InvestorUnknown]The RSI Weighted Trend System I is an experimental indicator designed to combine both slow-moving trend indicators for stable trend identification and fast-moving indicators to capture potential major turning points in the market. The novelty of this system lies in the dynamic weighting mechanism, where fast indicators receive weight based on the current Relative Strength Index (RSI) value, thus providing a flexible tool for traders seeking to adapt their strategies to varying market conditions.

Dynamic RSI-Based Weighting System

The core of the indicator is the dynamic weighting of fast indicators based on the value of the RSI. In essence, the higher the absolute value of the RSI (whether positive or negative), the higher the weight assigned to the fast indicators. This enables the system to capture rapid price movements around potential turning points.

Users can choose between a threshold-based or continuous weight system:

Threshold-Based Weighting: Fast indicators are activated only when the absolute RSI value exceeds a user-defined threshold. Below this threshold, fast indicators receive no weight.

Continuous Weighting: By setting the weight threshold to zero, the fast indicators always receive some weight, although this can result in more false signals in ranging markets.

// Calculate weight for Fast Indicators based on RSI (Slow Indicator weight is kept to 1 for simplicity)

f_RSI_Weight_System(series float rsi, simple float weight_thre) =>

float fast_weight = na

float slow_weight = na

if weight_thre > 0

if math.abs(rsi) <= weight_thre

fast_weight := 0

slow_weight := 1

else

fast_weight := 0 + math.sqrt(math.abs(rsi))

slow_weight := 1

else

fast_weight := 0 + math.sqrt(math.abs(rsi))

slow_weight := 1

Slow and Fast Indicators

Slow Indicators are designed to identify stable trends, remaining constant in weight. These include:

DMI (Directional Movement Index) For Loop

CCI (Commodity Channel Index) For Loop

Aroon For Loop

Fast Indicators are more responsive and designed to spot rapid trend shifts:

ZLEMA (Zero-Lag Exponential Moving Average) For Loop

IIRF (Infinite Impulse Response Filter) For Loop

Each of these indicators is calculated using a for-loop method to generate a moving average, which captures the trend of a given length range.

RSI Normalization

To facilitate the weighting system, the RSI is normalized from its usual 0-100 range to a -1 to 1 range. This allows for easy scaling when calculating weights and helps the system adjust to rapidly changing market conditions.

// Normalize RSI (1 to -1)

f_RSI(series float rsi_src, simple int rsi_len, simple string rsi_wb, simple string ma_type, simple int ma_len) =>

output = switch rsi_wb

"RAW RSI" => ta.rsi(rsi_src, rsi_len)

"RSI MA" => ma_type == "EMA" ? (ta.ema(ta.rsi(rsi_src, rsi_len), ma_len)) : (ta.sma(ta.rsi(rsi_src, rsi_len), ma_len))

Signal Calculation

The final trading signal is a weighted average of both the slow and fast indicators, depending on the calculated weights from the RSI. This ensures a balanced approach, where slow indicators maintain overall trend guidance, while fast indicators provide timely entries and exits.

// Calculate Signal (as weighted average)

sig = math.round(((DMI*slow_w) + (CCI*slow_w) + (Aroon*slow_w) + (ZLEMA*fast_w) + (IIRF*fast_w)) / (3*slow_w + 2*fast_w), 2)

Backtest Mode and Performance Metrics

This version of the RSI Weighted Trend System includes a comprehensive backtesting mode, allowing users to evaluate the performance of their selected settings against a Buy & Hold strategy. The backtesting includes:

Equity calculation based on the signals generated by the indicator.

Performance metrics table comparing Buy & Hold strategy metrics with the system’s signals, including: Mean, positive, and negative return percentages, Standard deviations (of all, positive and negative returns), Sharpe Ratio, Sortino Ratio, and Omega Ratio

f_PerformanceMetrics(series float base, int Lookback, simple float startDate, bool Annualize = true) =>

// Initialize variables for positive and negative returns

pos_sum = 0.0

neg_sum = 0.0

pos_count = 0

neg_count = 0

returns_sum = 0.0

returns_squared_sum = 0.0

pos_returns_squared_sum = 0.0

neg_returns_squared_sum = 0.0

// Loop through the past 'Lookback' bars to calculate sums and counts

if (time >= startDate)

for i = 0 to Lookback - 1

r = (base - base ) / base

returns_sum += r

returns_squared_sum += r * r

if r > 0

pos_sum += r

pos_count += 1

pos_returns_squared_sum += r * r

if r < 0

neg_sum += r

neg_count += 1

neg_returns_squared_sum += r * r

float export_array = array.new_float(12)

// Calculate means

mean_all = math.round((returns_sum / Lookback) * 100, 2)

mean_pos = math.round((pos_count != 0 ? pos_sum / pos_count : na) * 100, 2)

mean_neg = math.round((neg_count != 0 ? neg_sum / neg_count : na) * 100, 2)

// Calculate standard deviations

stddev_all = math.round((math.sqrt((returns_squared_sum - (returns_sum * returns_sum) / Lookback) / Lookback)) * 100, 2)

stddev_pos = math.round((pos_count != 0 ? math.sqrt((pos_returns_squared_sum - (pos_sum * pos_sum) / pos_count) / pos_count) : na) * 100, 2)

stddev_neg = math.round((neg_count != 0 ? math.sqrt((neg_returns_squared_sum - (neg_sum * neg_sum) / neg_count) / neg_count) : na) * 100, 2)

// Calculate probabilities

prob_pos = math.round((pos_count / Lookback) * 100, 2)

prob_neg = math.round((neg_count / Lookback) * 100, 2)

prob_neu = math.round(((Lookback - pos_count - neg_count) / Lookback) * 100, 2)

// Calculate ratios

sharpe_ratio = math.round(mean_all / stddev_all * (Annualize ? math.sqrt(Lookback) : 1), 2)

sortino_ratio = math.round(mean_all / stddev_neg * (Annualize ? math.sqrt(Lookback) : 1), 2)

omega_ratio = math.round(pos_sum / math.abs(neg_sum), 2)

// Set values in the array

array.set(export_array, 0, mean_all), array.set(export_array, 1, mean_pos), array.set(export_array, 2, mean_neg),

array.set(export_array, 3, stddev_all), array.set(export_array, 4, stddev_pos), array.set(export_array, 5, stddev_neg),

array.set(export_array, 6, prob_pos), array.set(export_array, 7, prob_neu), array.set(export_array, 8, prob_neg),

array.set(export_array, 9, sharpe_ratio), array.set(export_array, 10, sortino_ratio), array.set(export_array, 11, omega_ratio)

// Export the array

export_array

The metrics help traders assess the effectiveness of their strategy over time and can be used to optimize their settings.

Calibration Mode

A calibration mode is included to assist users in tuning the indicator to their specific needs. In this mode, traders can focus on a specific indicator (e.g., DMI, CCI, Aroon, ZLEMA, IIRF, or RSI) and fine-tune it without interference from other signals.

The calibration plot visualizes the chosen indicator's performance against a zero line, making it easy to see how changes in the indicator’s settings affect its trend detection.

Customization and Default Settings

Important Note: The default settings provided are not optimized for any particular market or asset. They serve as a starting point for experimentation. Traders are encouraged to calibrate the system to suit their own trading strategies and preferences.

The indicator allows deep customization, from selecting which indicators to use, adjusting the lengths of each indicator, smoothing parameters, and the RSI weight system.

Alerts

Traders can set alerts for both long and short signals when the indicator flips, allowing for automated monitoring of potential trading opportunities.

Cantom Chart - CL CTG vs BKDEnglish : This Pine Script indicator, named "Cantom Chart - CL CTG vs BKD," uniquely analyzes the immediate state of oil futures contracts to determine if they are in contango or backwardation. The script uses the price ratio between the nearest (CL1) and the next nearest (CL2) NYMEX crude oil futures contracts. It multiplies this ratio by 100 for clarity and scales fluctuations for enhanced visibility.

Key Features:

Dynamic Ratio Calculation: Computes the ratio (CL1/CL2 * 100) to determine the immediate market state.

Market State Interpretation: A ratio above 100 indicates backwardation, suggesting higher demand than supply, while a ratio below 100 indicates contango, suggesting higher supply than demand.

Volatility Adjustment: Amplifies market state changes by tripling the deviation from the baseline of 100, making it easier to observe subtle shifts.

Anomaly Detection: Caps the adjusted ratio at 125 for highs and 75 for lows, maintaining these limits until the ratio returns to normal levels.

Usage: This indicator is especially useful for traders analyzing supply-demand dynamics and inflationary pressures in the oil market. To apply it, simply add the script to your TradingView chart and adjust the 'Lower Threshold' and 'Upper Threshold' lines as needed based on your trading strategy.

-----

日本語 : この「Cantom Chart - CL CTG vs BKD」Pine Scriptインジケーターは、直近の原油先物契約がコンタンゴまたはバックワーデーションにあるかを特定するための独自の分析を提供します。最近の(CL1)と次の(CL2)NYMEX原油先物契約間の価格比を使用し、この比率に100を掛けて明確性を高め、変動の視認性を向上させます。

主要機能:

動的比率計算: 市場の即時状態を判断するために比率(CL1/CL2 * 100)を計算します。

市場状態の解釈: 比率が100を超える場合はバックワーデーション(需要が供給を上回る)、100未満の場合はコンタンゴ(供給が需要を上回る)を示します。

変動調整: 基準値100からの偏差を3倍にして、微妙な変化を容易に観察できるようにします。

異常値検出: 調整された比率を高値で125、低値で75に制限し、通常のレベルに戻るまでこれらの限界を維持します。

使用方法: このインジケーターは、原油市場における需給ダイナミクスとインフレ圧力を分析するトレーダーにとって特に有用です。使用するには、このスクリプトをTradingViewチャートに追加し、トレーディング戦略に基づいて「Lower Threshold」と「Upper Threshold」のラインを必要に応じて調整します。

Trend Forecasting - The Quant Science🌏 Trend Forecasting | ENG 🌏

This plug-in acts as a statistical filter, adding new information to your chart that will allow you to quickly verify the direction of a trend and the probability with which the price will be above or below the average in the future, helping you to uncover probable market inefficiencies.

🧠 Model calculation

The model calculates the arithmetic mean in relation to positive and negative events within the available sample for the selected time series. Where a positive event is defined as a closing price greater than the average, and a negative event as a closing price less than the average. Once all events have been calculated, the probabilities are extrapolated by relating each event.

Example

Positive event A: 70

Negative event B: 30

Total events: 100

Probabilities A: (100 / 70) x 100 = 70%

Probabilities B: (100 / 30) x 100 = 30%

Event A has a 70% probability of occurring compared to Event B which has a 30% probability.

🔍 Information Filter

The data on the graph show the future probabilities of prices being above average (default in green) and the probabilities of prices being below average (default in red).

The information that can be quickly retrieved from this indicator is:

1. Trend: Above-average prices together with a constant of data in green greater than 50% + 1 indicate that the observed historical series shows a bullish trend. The probability is correlated proportionally to the value of the data; the higher and increasing the expected value, the greater the observed bullish trend. On the other hand, a below-average price together with a red-coloured data constant show quantitative data regarding the presence of a bearish trend.

2. Future Probability: By analysing the data, it is possible to find the probability with which the price will be above or below the average in the future. In green are classified the probabilities that the price will be higher than the average, in red are classified the probabilities that the price will be lower than the average.

🔫 Operational Filter .

The indicator can be used operationally in the search for investment or trading opportunities given its ability to identify an inefficiency within the observed data sample.

⬆ Bullish forecast

For bullish trades, the inefficiency will appear as a historical series with a bullish trend, with high probability of a bullish trend in the future that is currently below the average.

⬇ Bearish forecast

For short trades, the inefficiency will appear as a historical series with a bearish trend, with a high probability of a bearish trend in the future that is currently above the average.

📚 Settings

Input: via the Input user interface, it is possible to adjust the periods (1 to 500) with which the average is to be calculated. By default the periods are set to 200, which means that the average is calculated by taking the last 200 periods.

Style: via the Style user interface it is possible to adjust the colour and switch a specific output on or off.

🇮🇹Previsione Della Tendenza Futura | ITA 🇮🇹

Questo plug-in funge da filtro statistico, aggiungendo nuove informazioni al tuo grafico che ti permetteranno di verificare rapidamente tendenza di un trend, probabilità con la quale il prezzo si troverà sopra o sotto la media in futuro aiutandoti a scovare probabili inefficienze di mercato.

🧠 Calcolo del modello

Il modello calcola la media aritmetica in relazione con gli eventi positivi e negativi all'intero del campione disponibile per la serie storica selezionata. Dove per evento positivo si intende un prezzo alla chiusura maggiore della media, mentre per evento negativo si intende un prezzo alla chiusura minore della media. Calcolata la totalità degli eventi le probabilità vengono estrapolate rapportando ciascun evento.

Esempio

Evento positivo A: 70

Evento negativo B: 30

Totale eventi : 100

Formula A: (100 / 70) x 100 = 70%

Formula B: (100 / 30) x 100 = 30%

Evento A ha una probabilità del 70% di realizzarsi rispetto all' Evento B che ha una probabilità pari al 30%.

🔍 Filtro informativo

I dati sul grafico mostrano le probabilità future che i prezzi siano sopra la media (di default in verde) e le probabilità che i prezzi siano sotto la media (di default in rosso).

Le informazioni che si possono rapidamente reperire da questo indicatore sono:

1. Trend: I prezzi sopra la media insieme ad una costante di dati in verde maggiori al 50% + 1 indicano che la serie storica osservata presenta un trend rialzista. La probabilità è correlata proporzionalmente al valore del dato; tanto più sarà alto e crescente il valore atteso e maggiore sarà la tendenza rialzista osservata. Viceversa, un prezzo sotto la media insieme ad una costante di dati classificati in colore rosso mostrano dati quantitativi riguardo la presenza di una tendenza ribassista.

2. Probabilità future: analizzando i dati è possibile reperire la probabilità con cui il prezzo si troverà sopra o sotto la media in futuro. In verde vengono classificate le probabilità che il prezzo sarà maggiore alla media, in rosso vengono classificate le probabilità che il prezzo sarà minore della media.

🔫 Filtro operativo

L' indicatore può essere utilizzato a livello operativo nella ricerca di opportunità di investimento o di trading vista la capacità di identificare un inefficienza all'interno del campione di dati osservato.

⬆ Previsione rialzista

Per operatività di tipo rialzista l'inefficienza apparirà come una serie storica a tendenza rialzista, con alte probabilità di tendenza rialzista in futuro che attualmente si trova al di sotto della media.

⬇ Previsione ribassista

Per operatività di tipo short l'inefficienza apparirà come una serie storica a tendenza ribassista, con alte probabilità di tendenza ribassista in futuro che si trova attualmente sopra la media.

📚 Impostazioni

Input: tramite l'interfaccia utente Input è possibile regolare i periodi (da 1 a 500) con cui calcolare la media. Di default i periodi sono impostati sul valore di 200, questo significa che la media viene calcolata prendendo gli ultimi 200 periodi.

Style: tramite l'interfaccia utente Style è possibile regolare il colore e attivare o disattivare un specifico output.

Stochastic RSI of Smoothed Price [Loxx]What is Stochastic RSI of Smoothed Price?

This indicator is just as it's title suggests. There are six different signal types, various price smoothing types, and seven types of RSI.

This indicator contains 7 different types of RSI:

RSX

Regular

Slow

Rapid

Harris

Cuttler

Ehlers Smoothed

What is RSI?

RSI stands for Relative Strength Index . It is a technical indicator used to measure the strength or weakness of a financial instrument's price action.

The RSI is calculated based on the price movement of an asset over a specified period of time, typically 14 days, and is expressed on a scale of 0 to 100. The RSI is considered overbought when it is above 70 and oversold when it is below 30.

Traders and investors use the RSI to identify potential buy and sell signals. When the RSI indicates that an asset is oversold, it may be considered a buying opportunity, while an overbought RSI may signal that it is time to sell or take profits.

It's important to note that the RSI should not be used in isolation and should be used in conjunction with other technical and fundamental analysis tools to make informed trading decisions.

What is RSX?

Jurik RSX is a technical analysis indicator that is a variation of the Relative Strength Index Smoothed ( RSX ) indicator. It was developed by Mark Jurik and is designed to help traders identify trends and momentum in the market.

The Jurik RSX uses a combination of the RSX indicator and an adaptive moving average (AMA) to smooth out the price data and reduce the number of false signals. The adaptive moving average is designed to adjust the smoothing period based on the current market conditions, which makes the indicator more responsive to changes in price.

The Jurik RSX can be used to identify potential trend reversals and momentum shifts in the market. It oscillates between 0 and 100, with values above 50 indicating a bullish trend and values below 50 indicating a bearish trend . Traders can use these levels to make trading decisions, such as buying when the indicator crosses above 50 and selling when it crosses below 50.

The Jurik RSX is a more advanced version of the RSX indicator, and while it can be useful in identifying potential trade opportunities, it should not be used in isolation. It is best used in conjunction with other technical and fundamental analysis tools to make informed trading decisions.

What is Slow RSI?

Slow RSI is a variation of the traditional Relative Strength Index ( RSI ) indicator. It is a more smoothed version of the RSI and is designed to filter out some of the noise and short-term price fluctuations that can occur with the standard RSI .

The Slow RSI uses a longer period of time than the traditional RSI , typically 21 periods instead of 14. This longer period helps to smooth out the price data and makes the indicator less reactive to short-term price fluctuations.

Like the traditional RSI , the Slow RSI is used to identify potential overbought and oversold conditions in the market. It oscillates between 0 and 100, with values above 70 indicating overbought conditions and values below 30 indicating oversold conditions. Traders often use these levels as potential buy and sell signals.

The Slow RSI is a more conservative version of the RSI and can be useful in identifying longer-term trends in the market. However, it can also be slower to respond to changes in price, which may result in missed trading opportunities. Traders may choose to use a combination of both the Slow RSI and the traditional RSI to make informed trading decisions.

What is Rapid RSI?

Same as regular RSI but with a faster calculation method

What is Harris RSI?

Harris RSI is a technical analysis indicator that is a variation of the Relative Strength Index ( RSI ). It was developed by Larry Harris and is designed to help traders identify potential trend changes and momentum shifts in the market.

The Harris RSI uses a different calculation formula compared to the traditional RSI . It takes into account both the opening and closing prices of a financial instrument, as well as the high and low prices. The Harris RSI is also normalized to a range of 0 to 100, with values above 50 indicating a bullish trend and values below 50 indicating a bearish trend .

Like the traditional RSI , the Harris RSI is used to identify potential overbought and oversold conditions in the market. It oscillates between 0 and 100, with values above 70 indicating overbought conditions and values below 30 indicating oversold conditions. Traders often use these levels as potential buy and sell signals.

The Harris RSI is a more advanced version of the RSI and can be useful in identifying longer-term trends in the market. However, it can also generate more false signals than the standard RSI . Traders may choose to use a combination of both the Harris RSI and the traditional RSI to make informed trading decisions.

What is Cuttler RSI?

Cuttler RSI is a technical analysis indicator that is a variation of the Relative Strength Index ( RSI ). It was developed by Curt Cuttler and is designed to help traders identify potential trend changes and momentum shifts in the market.

The Cuttler RSI uses a different calculation formula compared to the traditional RSI . It takes into account the difference between the closing price of a financial instrument and the average of the high and low prices over a specified period of time. This difference is then normalized to a range of 0 to 100, with values above 50 indicating a bullish trend and values below 50 indicating a bearish trend .

Like the traditional RSI , the Cuttler RSI is used to identify potential overbought and oversold conditions in the market. It oscillates between 0 and 100, with values above 70 indicating overbought conditions and values below 30 indicating oversold conditions. Traders often use these levels as potential buy and sell signals.

The Cuttler RSI is a more advanced version of the RSI and can be useful in identifying longer-term trends in the market. However, it can also generate more false signals than the standard RSI . Traders may choose to use a combination of both the Cuttler RSI and the traditional RSI to make informed trading decisions.

What is Ehlers Smoothed RSI?

Ehlers smoothed RSI is a technical analysis indicator that is a variation of the Relative Strength Index ( RSI ). It was developed by John Ehlers and is designed to help traders identify potential trend changes and momentum shifts in the market.

The Ehlers smoothed RSI uses a different calculation formula compared to the traditional RSI . It uses a smoothing algorithm that is designed to reduce the noise and random fluctuations that can occur with the standard RSI . The smoothing algorithm is based on a concept called "digital signal processing" and is intended to improve the accuracy of the indicator.

Like the traditional RSI , the Ehlers smoothed RSI is used to identify potential overbought and oversold conditions in the market. It oscillates between 0 and 100, with values above 70 indicating overbought conditions and values below 30 indicating oversold conditions. Traders often use these levels as potential buy and sell signals.

The Ehlers smoothed RSI can be useful in identifying longer-term trends and momentum shifts in the market. However, it can also generate more false signals than the standard RSI . Traders may choose to use a combination of both the Ehlers smoothed RSI and the traditional RSI to make informed trading decisions.

What is Stochastic RSI?

Stochastic RSI (StochRSI) is a technical analysis indicator that combines the concepts of the Stochastic Oscillator and the Relative Strength Index (RSI). It is used to identify potential overbought and oversold conditions in financial markets, as well as to generate buy and sell signals based on the momentum of price movements.

To understand Stochastic RSI, let's first define the two individual indicators it is based on:

Stochastic Oscillator: A momentum indicator that compares a particular closing price of a security to a range of its prices over a certain period. It is used to identify potential trend reversals and generate buy and sell signals.

Relative Strength Index (RSI): A momentum oscillator that measures the speed and change of price movements. It ranges between 0 and 100 and is used to identify overbought or oversold conditions in the market.

Now, let's dive into the Stochastic RSI:

The Stochastic RSI applies the Stochastic Oscillator formula to the RSI values, essentially creating an indicator of an indicator. It helps to identify when the RSI is in overbought or oversold territory with more sensitivity, providing more frequent signals than the standalone RSI.

The formula for StochRSI is as follows:

StochRSI = (RSI - Lowest Low RSI) / (Highest High RSI - Lowest Low RSI)

Where:

RSI is the current RSI value.

Lowest Low RSI is the lowest RSI value over a specified period (e.g., 14 days).

Highest High RSI is the highest RSI value over the same specified period.

StochRSI ranges from 0 to 1, but it is usually multiplied by 100 for easier interpretation, making the range 0 to 100. Like the RSI, values close to 0 indicate oversold conditions, while values close to 100 indicate overbought conditions. However, since the StochRSI is more sensitive, traders typically use 20 as the oversold threshold and 80 as the overbought threshold.

Traders use the StochRSI to generate buy and sell signals by looking for crossovers with a signal line (a moving average of the StochRSI), similar to the way the Stochastic Oscillator is used. When the StochRSI crosses above the signal line, it is considered a bullish signal, and when it crosses below the signal line, it is considered a bearish signal.

It is essential to use the Stochastic RSI in conjunction with other technical analysis tools and indicators, as well as to consider the overall market context, to improve the accuracy and reliability of trading signals.

Signal types included are the following;

Fixed Levels

Floating Levels

Quantile Levels

Fixed Middle

Floating Middle

Quantile Middle

Extras

Alerts

Bar coloring

Loxx's Expanded Source Types

Copy/Paste LevelsCopy/Paste Levels allows levels to be pasted onto your chart from a properly formatted source.

This tool streamlines the process of adding lines to your chart, and sharing lines from your chart.

More than one ticker at a time!

This indicator will only draw lines on charts it has values for!

This means you can input levels for every ticker you need all at once, one time, and only be displayed the levels for the current chart you are looking at. When you switch tickers, the levels for that ticker will display. (Assuming you have levels entered for that ticker)

The formatting is as follows:

Ticker,Color,Style,Width,Lvl1,Lvl2,Lvl3;

Ticker - Any ticker on Tradingview can be used in the field

Color - Available colors are: Red,Orange,Yellow,Green,Blue,Purple,White,Black,Gray

Style - Available styles are: Solid,Dashed,Dotted

Width - This can be any negative integer, ex.(-1,-2,-3,-4,-5)

Lvls - These can be any positive number (decimals allowed)

Semi-Colons separate sections, each section contains enough information to create at least 1 line.

Each additional level added within the same section will have the same styling parameters as the other levels in the section.

Example:

2 solid lines colored red with a thickness of 2 on QQQ, 1 at $300 and 1 at $400.

QQQ,RED,SOLID,-2,300,400;

IMPORTANT MUST READ!!!

Remember to not include any spaces between commas and the entries in each field!

ex. ; QQQ, red, dotted, -1, 325; <- Wrong

ex. ;QQQ,red,dotted,-1,325;)<- Right

However,

All fields must be filled out, to use default values in the fields, insert a space between the commas.

ex. ;QQQ,red,dotted,,325; <- Wrong

ex. ;QQQ,red,dotted, ,325; <- Right

While spaces can not be included line breaks can!

I recommend for easier typing and viewing to include a line break for each new line (if changing styling or ticker)

Example:

2 solid lines, one red at $300, one green at $400, both default width. Written in a single line AND using multiple lines, both give the same output.

QQQ,red,solid, ,300;QQQ,green,solid, ,400;

or

QQQ,red,solid, ,300;

QQQ,green,solid, ,400;

In this following screenshot you can see more examples of different formatting variations.

The textbox contains exactly what is pasted into the settings input box.

As you can see, capitalization does not matter.

Default Values:

Color = optimal contrast color, If this field is filled in with a space it will display the optimal contrast color of the users background.

Style = solid

Width = -1

More Examples:

Multi-Ticker: drawing 3 lines at $300, all default values, on 3 different tickers

SPY, , , ,300;QQQ, , , ,300;AAPL, , , ,300

or

SPY, , , ,300;

QQQ, , , ,300;

AAPL, , , ,300

Multiple levels: There is no limit* to the number of levels that can be included within 1 section.

* only TV default line limit per indicator (500)

This will be 4 lines all with the same styling at different values on 2 separate tickers.

SPY,BLUE,SOLID,-2,100,200,300,400;QQQ,BLUE,SOLID,-2,100,200,300,400

or

SPY,BLUE,SOLID,-2,100,200,300,400;

QQQ,BLUE,SOLID,-2,100,200,300,400

Semi-colons must separate sections, but are not required at the beginning or end, it makes no difference if they are or are not added.

SPY,BLUE,SOLID,-2,100,200,300,400;

QQQ,BLUE,SOLID,-2,100,200,300,400

==

SPY,BLUE,SOLID,-2,100,200,300,400;

QQQ,BLUE,SOLID,-2,100,200,300,400;

==

;SPY,BLUE,SOLID,-2,100,200,300,400;

QQQ,BLUE,SOLID,-2,100,200,300,400;

All the above output the same results.

Hope this is helpful for people,

Enjoy!

Kelly Position Size CalculatorThis position sizing calculator implements the Kelly Criterion, developed by John L. Kelly Jr. at Bell Laboratories in 1956, to determine mathematically optimal position sizes for maximizing long-term wealth growth. Unlike arbitrary position sizing methods, this tool provides a scientifically solution based on your strategy's actual performance statistics and incorporates modern refinements from over six decades of academic research.

The Kelly Criterion addresses a fundamental question in capital allocation: "What fraction of capital should be allocated to each opportunity to maximize growth while avoiding ruin?" This question has profound implications for financial markets, where traders and investors constantly face decisions about optimal capital allocation (Van Tharp, 2007).

Theoretical Foundation

The Kelly Criterion for binary outcomes is expressed as f* = (bp - q) / b, where f* represents the optimal fraction of capital to allocate, b denotes the risk-reward ratio, p indicates the probability of success, and q represents the probability of loss (Kelly, 1956). This formula maximizes the expected logarithm of wealth, ensuring maximum long-term growth rate while avoiding the risk of ruin.

The mathematical elegance of Kelly's approach lies in its derivation from information theory. Kelly's original work was motivated by Claude Shannon's information theory (Shannon, 1948), recognizing that maximizing the logarithm of wealth is equivalent to maximizing the rate of information transmission. This connection between information theory and wealth accumulation provides a deep theoretical foundation for optimal position sizing.

The logarithmic utility function underlying the Kelly Criterion naturally embodies several desirable properties for capital management. It exhibits decreasing marginal utility, penalizes large losses more severely than it rewards equivalent gains, and focuses on geometric rather than arithmetic mean returns, which is appropriate for compounding scenarios (Thorp, 2006).

Scientific Implementation

This calculator extends beyond basic Kelly implementation by incorporating state of the art refinements from academic research:

Parameter Uncertainty Adjustment: Following Michaud (1989), the implementation applies Bayesian shrinkage to account for parameter estimation error inherent in small sample sizes. The adjustment formula f_adjusted = f_kelly × confidence_factor + f_conservative × (1 - confidence_factor) addresses the overconfidence bias documented by Baker and McHale (2012), where the confidence factor increases with sample size and the conservative estimate equals 0.25 (quarter Kelly).

Sample Size Confidence: The reliability of Kelly calculations depends critically on sample size. Research by Browne and Whitt (1996) provides theoretical guidance on minimum sample requirements, suggesting that at least 30 independent observations are necessary for meaningful parameter estimates, with 100 or more trades providing reliable estimates for most trading strategies.

Universal Asset Compatibility: The calculator employs intelligent asset detection using TradingView's built-in symbol information, automatically adapting calculations for different asset classes without manual configuration.

ASSET SPECIFIC IMPLEMENTATION

Equity Markets: For stocks and ETFs, position sizing follows the calculation Shares = floor(Kelly Fraction × Account Size / Share Price). This straightforward approach reflects whole share constraints while accommodating fractional share trading capabilities.

Foreign Exchange Markets: Forex markets require lot-based calculations following Lot Size = Kelly Fraction × Account Size / (100,000 × Base Currency Value). The calculator automatically handles major currency pairs with appropriate pip value calculations, following industry standards described by Archer (2010).

Futures Markets: Futures position sizing accounts for leverage and margin requirements through Contracts = floor(Kelly Fraction × Account Size / Margin Requirement). The calculator estimates margin requirements as a percentage of contract notional value, with specific adjustments for micro-futures contracts that have smaller sizes and reduced margin requirements (Kaufman, 2013).

Index and Commodity Markets: These markets combine characteristics of both equity and futures markets. The calculator automatically detects whether instruments are cash-settled or futures-based, applying appropriate sizing methodologies with correct point value calculations.

Risk Management Integration

The calculator integrates sophisticated risk assessment through two primary modes:

Stop Loss Integration: When fixed stop-loss levels are defined, risk calculation follows Risk per Trade = Position Size × Stop Loss Distance. This ensures that the Kelly fraction accounts for actual risk exposure rather than theoretical maximum loss, with stop-loss distance measured in appropriate units for each asset class.

Strategy Drawdown Assessment: For discretionary exit strategies, risk estimation uses maximum historical drawdown through Risk per Trade = Position Value × (Maximum Drawdown / 100). This approach assumes that individual trade losses will not exceed the strategy's historical maximum drawdown, providing a reasonable estimate for strategies with well-defined risk characteristics.

Fractional Kelly Approaches