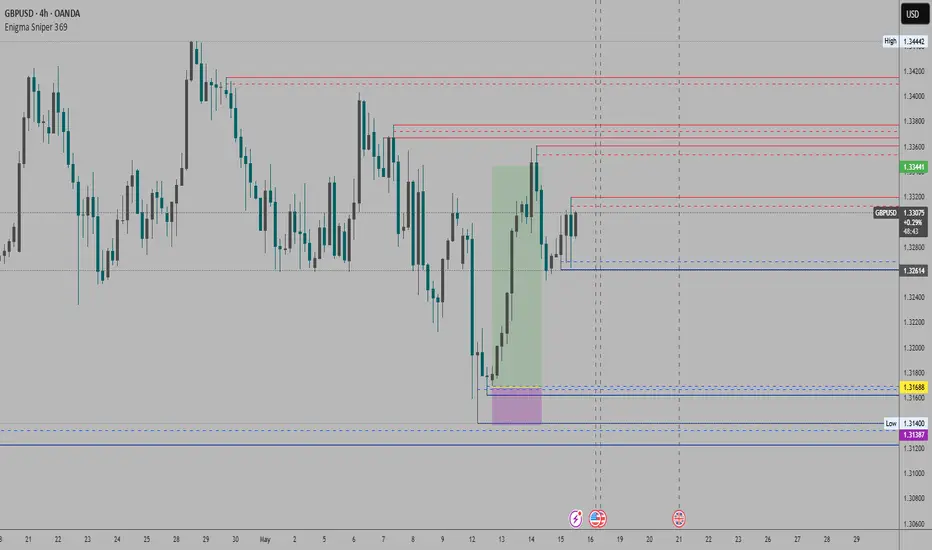

Enigma Sniper 369The "Enigma Sniper 369" is a custom-built Pine Script indicator designed for TradingView, tailored specifically for forex traders seeking high-probability entries during high-volatility market sessions.

Unlike generic trend-following or scalping tools, this indicator uniquely combines session-based "kill zones" (London and US sessions), momentum-based candle analysis, and an optional EMA trend filter to pinpoint liquidity grabs and reversal opportunities.

Its originality lies in its focus on liquidity hunting—identifying levels where stop losses are likely clustered (around swing highs/lows and wick midpoints)—and providing visual entry zones that are dynamically removed once price breaches them, reducing clutter and focusing on actionable signals.

The name "369" reflects the structured approach of three key components (session timing, candle logic, and trend filter) working in harmony to snipe precise entries.

What It Does

"Enigma Sniper 369" identifies potential buy and sell opportunities by drawing two types of horizontal lines on the chart during user-defined London and US

session kill zones:

Solid Lines: Mark the swing low (for buys) or swing high (for sells) of a trigger candle, indicating a potential entry point where stop losses might be clustered.

Dotted Lines: Mark the 50% level of the candle’s wick (lower wick for buys, upper wick for sells), serving as a secondary confirmation zone for entries or tighter stop-loss placement.

These lines are plotted only when specific candle conditions are met within the kill zones, and they are automatically deleted once the price crosses them, signaling that the liquidity at that level has likely been grabbed. The indicator also includes an optional EMA filter to ensure trades align with the broader trend, reducing false signals in choppy markets.

How It Works

The indicator’s logic is built on a multi-layered approach:

Kill Zone Timing: Trades are only considered during user-defined London and US session hours (e.g., London from 02:00 to 12:00 UTC, as seen in the screenshots). These sessions are known for high volatility and liquidity, making them ideal for capturing institutional moves.

Candle-Based Momentum Logic:

Buy Signal: A candle must close above its midpoint (indicating bullish momentum) and have a lower low than the previous candle (suggesting a potential liquidity grab below the previous swing low). This is expressed as close > (high + low) / 2 and low < low .

Sell Signal: A candle must close below its midpoint (bearish momentum) and have a higher high than the previous candle (indicating a potential liquidity grab above the previous swing high), expressed as close < (high + low) / 2 and high > high .

These conditions ensure the indicator targets candles that break recent structure to hunt stop losses while showing directional momentum.

Optional EMA Filter: A 50-period EMA (customizable) can be enabled to filter signals based on trend direction.

Buy signals are only generated if the EMA is trending upward (ema_value > ema_value ), and sell signals require a downward EMA trend (ema_value < ema_value ). This reduces noise by aligning entries with the broader market trend.

Liquidity Levels and Deletion Logic:

For a buy signal, a solid green line is drawn at the candle’s low, and a dotted green line at the 50% level of the lower wick (from the candle body’s bottom to the low).

For a sell signal, a solid red line is drawn at the candle’s high, and a dotted red line at the 50% level of the upper wick (from the body’s top to the high).

These lines extend to the right until the price crosses them, at which point they are deleted, indicating the liquidity at that level has been taken (e.g., stop losses triggered).

Alerts: The indicator includes alert conditions for buy and sell signals, notifying traders when a new setup is identified.

Underlying Concepts

The indicator is grounded in the concept of liquidity hunting, a strategy often employed by institutional traders. Markets frequently move to levels where stop losses are clustered—typically just beyond swing highs or lows—before reversing in the opposite direction. The "Enigma Sniper 369" targets these moves by identifying candles that break structure (e.g., a lower low or higher high) during high-volatility sessions, suggesting a potential sweep of stop losses. The 50% wick level acts as a secondary confirmation, as this midpoint often represents a zone where tighter stop losses are placed by retail traders. The optional EMA filter adds a trend-following element, ensuring entries are taken in the direction of the broader market momentum, which is particularly useful on lower timeframes like the 15-minute chart shown in the screenshots.

How to Use It

Here’s a step-by-step guide based on the provided usage example on the GBP/USD 15-minute chart:

Setup the Indicator: Add "Enigma Sniper 369" to your TradingView chart. Adjust the London and US session hours to match your timezone (e.g., London from 02:00 to 12:00 UTC, US from 13:00 to 22:00 UTC). Customize the EMA period (default 50) and line styles/colors if desired.

Identify Kill Zones: The indicator highlights the London session in light green and the US session in light purple, as seen in the screenshots. Focus on these periods for signals, as they are the most volatile and likely to produce liquidity grabs.

Wait for a Signal: Look for solid and dotted lines to appear during the kill zones:

Buy Setup: A solid green line at the swing low and a dotted green line at the 50% lower wick level indicate a potential buy. This suggests the market may have grabbed liquidity below the swing low and is now poised to move higher.

Sell Setup: A solid red line at the swing high and a dotted red line at the 50% upper wick level indicate a potential sell, suggesting liquidity was taken above the swing high.

Place Your Trade:

For a buy, set a buy limit order at the dotted green line (50% wick level), as this is a more conservative entry point. Place your stop loss just below the solid green line (swing low) to cover the full swing. For example, in the screenshots, the market retraces to the dotted line at 1.32980 after a liquidity grab below the swing low, triggering a buy limit order.

For a sell, set a sell limit order at the dotted red line, with a stop loss just above the solid red line.

Monitor Price Action: Once the price crosses a line, it is deleted, indicating the liquidity at that level has been taken. In the screenshots, after the buy limit is triggered, the market moves higher, confirming the setup. The caption notes, “The market returns and tags us in long with a buy limit,” highlighting this retracement strategy.

Additional Context: Use the indicator to identify liquidity levels that may be targeted later. For example, the screenshot notes, “If a new session is about to open I will wait for the grab liquidity to go long,” showing how the indicator can be used to anticipate future moves at session opens (e.g., London open at 1.32980).

Risk Management: Always set a stop loss below the swing low (for buys) or above the swing high (for sells) to protect against adverse moves. The 50% wick level helps tighten entries, improving the risk-reward ratio.

Practical Example

On the GBP/USD 15-minute chart, during the London session (02:00 UTC), the indicator identifies a buy setup with a solid green line at 1.32901 (swing low) and a dotted green line at 1.32980 (50% wick level). The market initially dips below the swing low, grabbing liquidity, then retraces to the dotted line, triggering a buy limit order. The price subsequently rises to 1.33404, yielding a profitable trade. The user notes, “The logic is in the last candle it provides new level to go long,” emphasizing the indicator’s ability to identify fresh levels after a liquidity sweep.

Customization Tips

Adjust the EMA period to suit your timeframe (e.g., a shorter period like 20 for faster signals on lower timeframes).

Modify the session hours to align with your broker’s timezone or specific market conditions.

Use the alert feature to get notified of new setups without constantly monitoring the chart.

Why It’s Useful for Traders

The "Enigma Sniper 369" stands out by combining session timing, momentum-based candle analysis, and liquidity hunting into a single tool. It provides clear, actionable levels for entries and stop losses, removes invalid signals dynamically, and aligns trades with high-probability market conditions. Whether you’re a scalper looking for quick moves during London open or a swing trader targeting session-based reversals, this indicator offers a structured, data-driven approach to trading.

Cari dalam skrip untuk "机械革命无界15+时不时闪屏"

Trader’s One-Liner Reminder⚠️ このインジケーターは日本語でのメッセージ表示に特化しています。英語でのリマインドは含まれていません。

This script displays reminders only in Japanese.

【日本語説明】

本インジケーターは、日本時間(JST)8:00〜翌1:00までの時間帯に合わせて、15分刻みで一言メッセージを表示します。

トレード中の焦りや過信を防ぐための心理的リマインダーとして設計されています。

- 「Frankモード」では、関西弁風のユーモアあるメッセージを自動表示

- 「Customモード」では、全時間帯のメッセージを自分で自由に設定可能

- メッセージはチャート上部中央に、大きな文字・黄色背景で表示され、視認性にも配慮

💡ポジポジ病対策、メンタル強化、時間管理などに最適です。

---

【English Description】

This indicator displays motivational reminders in Japanese every 15 minutes from 8:00 JST to 1:00 JST (the next day).

It is designed to support traders mentally during market hours.

- “Frank mode” automatically shows prewritten humorous messages (in Kansai dialect tone)

- “Custom mode” lets users input their own message for each 15-minute time block

- Messages are shown in large text at the top-center of the chart with a yellow background for clear visibility

💡 Ideal for discipline, overtrading prevention, and improving trading psychology.

---

🔔 This indicator is intended for Japanese-speaking users. If you'd like an English version, feel free to fork and customize it!

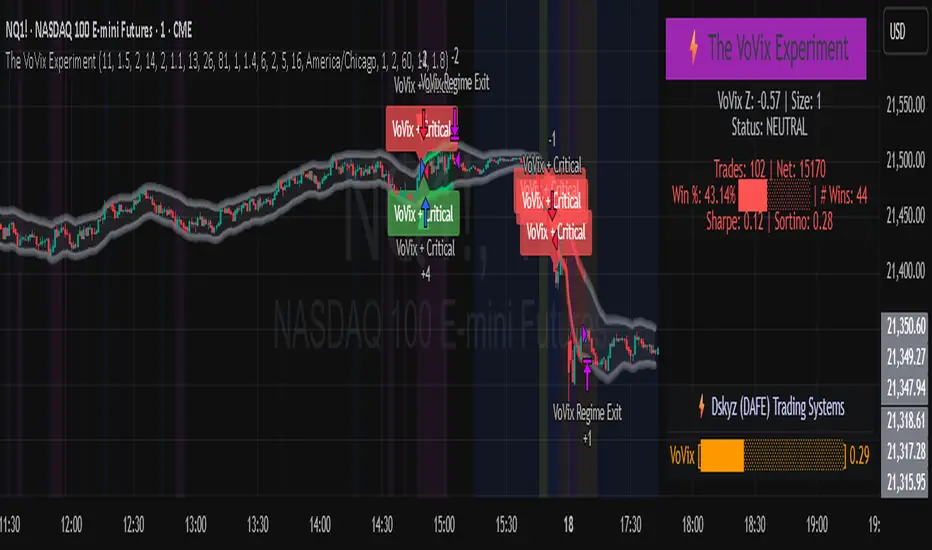

The VoVix Experiment The VoVix Experiment

The VoVix Experiment is a next-generation, regime-aware, volatility-adaptive trading strategy for futures, indices, and more. It combines a proprietary VoVix (volatility-of-volatility) anomaly detector with price structure clustering and critical point logic, only trading when multiple independent signals align. The system is designed for robustness, transparency, and real-world execution.

Logic:

VoVix Regime Engine: Detects pre-move volatility anomalies using a fast/slow ATR ratio, normalized by Z-score. Only trades when a true regime spike is detected, not just random volatility.

Cluster & Critical Point Filters: Price structure and volatility clustering must confirm the VoVix signal, reducing false positives and whipsaws.

Adaptive Sizing: Position size scales up for “super-spikes” and down for normal events, always within user-defined min/max.

Session Control: Trades only during user-defined hours and days, avoiding illiquid or high-risk periods.

Visuals: Aurora Flux Bands (From another Original of Mine (Options Flux Flow): glow and change color on signals, with a live dashboard, regime heatmap, and VoVix progression bar for instant insight.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 15 min (but works on all timeframes)

Order size: Adaptive, 1–2 contracts

Session: 5:00–15:00 America/Chicago (default, fully adjustable)

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for MNQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Forward Testing: (This is no guarantee. I've provided these results to show that executions perform as intended. Test were done on Tradovate)

ALL TRADES

Gross P/L: $12,907.50

# of Trades: 64

# of Contracts: 186

Avg. Trade Time: 1h 55min 52sec

Longest Trade Time: 55h 46min 53sec

% Profitable Trades: 59.38%

Expectancy: $201.68

Trade Fees & Comm.: $(330.95)

Total P/L: $12,576.55

Winning Trades: 59.38%

Breakeven Trades: 3.12%

Losing Trades: 37.50%

Link: www.dropbox.com

Inputs & Tooltips

VoVix Regime Execution: Enable/disable the core VoVix anomaly detector.

Volatility Clustering: Require price/volatility clusters to confirm VoVix signals.

Critical Point Detector: Require price to be at a statistically significant distance from the mean (regime break).

VoVix Fast ATR Length: Short ATR for fast volatility detection (lower = more sensitive).

VoVix Slow ATR Length: Long ATR for baseline regime (higher = more stable).

VoVix Z-Score Window: Lookback for Z-score normalization (higher = smoother, lower = more reactive).

VoVix Entry Z-Score: Minimum Z-score for a VoVix spike to trigger a trade.

VoVix Exit Z-Score: Z-score below which the regime is considered decayed (exit).

VoVix Local Max Window: Bars to check for local maximum in VoVix (higher = stricter).

VoVix Super-Spike Z-Score: Z-score for “super” regime events (scales up position size).

Min/Max Contracts: Adaptive position sizing range.

Session Start/End Hour: Only trade between these hours (exchange time).

Allow Weekend Trading: Enable/disable trading on weekends.

Session Timezone: Timezone for session filter (e.g., America/Chicago for CME).

Show Trade Labels: Show/hide entry/exit labels on chart.

Flux Glow Opacity: Opacity of Aurora Flux Bands (0–100).

Flux Band EMA Length: EMA period for band center.

Flux Band ATR Multiplier: Width of bands (higher = wider).

Compliance & Transparency

* No hidden logic, no repainting, no pyramiding.

* All signals, sizing, and exits are fully explained and visible.

* Backtest settings are stricter than most real accounts.

* All visuals are directly tied to the strategy logic.

* This is not a mashup or cosmetic overlay; every component is original and justified.

Disclaimer

Trading is risky. This script is for educational and research purposes only. Do not trade with money you cannot afford to lose. Past performance is not indicative of future results. Always test in simulation before live trading.

Proprietary Logic & Originality Statement

This script, “The VoVix Experiment,” is the result of original research and development. All core logic, algorithms, and visualizations—including the VoVix regime detection engine, adaptive execution, volatility/divergence bands, and dashboard—are proprietary and unique to this project.

1. VoVix Regime Logic

The concept of “volatility of volatility” (VoVix) is an original quant idea, not a standard indicator. The implementation here (fast/slow ATR ratio, Z-score normalization, local max logic, super-spike scaling) is custom and not found in public TradingView scripts.

2. Cluster & Critical Point Logic

Volatility clustering and “critical point” detection (using price distance from a rolling mean and standard deviation) are general quant concepts, but the way they are combined and filtered here is unique to this script. The specific logic for “clustered chop” and “critical point” is not a copy of any public indicator.

3. Adaptive Sizing

The adaptive sizing logic (scaling contracts based on regime strength) is custom and not a standard TradingView feature or public script.

4. Time Block/Session Control

The session filter is a common feature in many strategies, but the implementation here (with timezone and weekend control) is written from scratch.

5. Aurora Flux Bands (From another Original of Mine (Options Flux Flow)

The “glowing” bands are inspired by the idea of volatility bands (like Bollinger Bands or Keltner Channels), but the visual effect, color logic, and integration with regime signals are original to this script.

6. Dashboard, Watermark, and Metrics

The dashboard, real-time Sharpe/Sortino, and VoVix progression bar are all custom code, not copied from any public script.

What is “standard” or “common quant practice”?

Using ATR, EMA, and Z-score are standard quant tools, but the way they are combined, filtered, and visualized here is unique. The structure and logic of this script are original and not a mashup of public code.

This script is 100% original work. All logic, visuals, and execution are custom-coded for this project. No code or logic is directly copied from any public or private script.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Bober XM v2.0# ₿ober XM v2.0 Trading Bot Documentation

**Developer's Note**: While our previous Bot 1.3.1 was removed due to guideline violations, this setback only fueled our determination to create something even better. Rising from this challenge, Bober XM 2.0 emerges not just as an update, but as a complete reimagining with multi-timeframe analysis, enhanced filters, and superior adaptability. This adversity pushed us to innovate further and deliver a strategy that's smarter, more agile, and more powerful than ever before. Challenges create opportunity - welcome to Cryptobeat's finest work yet.

## !!!!You need to tune it for your own pair and timeframe and retune it periodicaly!!!!!

## Overview

The ₿ober XM v2.0 is an advanced dual-channel trading bot with multi-timeframe analysis capabilities. It integrates multiple technical indicators, customizable risk management, and advanced order execution via webhook for automated trading. The bot's distinctive feature is its separate channel systems for long and short positions, allowing for asymmetric trade strategies that adapt to different market conditions across multiple timeframes.

### Key Features

- **Multi-Timeframe Analysis**: Analyze price data across multiple timeframes simultaneously

- **Dual Channel System**: Separate parameter sets for long and short positions

- **Advanced Entry Filters**: RSI, Volatility, Volume, Bollinger Bands, and KEMAD filters

- **Machine Learning Moving Average**: Adaptive prediction-based channels

- **Multiple Entry Strategies**: Breakout, Pullback, and Mean Reversion modes

- **Risk Management**: Customizable stop-loss, take-profit, and trailing stop settings

- **Webhook Integration**: Compatible with external trading bots and platforms

### Strategy Components

| Component | Description |

|---------|-------------|

| **Dual Channel Trading** | Uses either Keltner Channels or Machine Learning Moving Average (MLMA) with separate settings for long and short positions |

| **MLMA Implementation** | Machine learning algorithm that predicts future price movements and creates adaptive bands |

| **Pivot Point SuperTrend** | Trend identification and confirmation system based on pivot points |

| **Three Entry Strategies** | Choose between Breakout, Pullback, or Mean Reversion approaches |

| **Advanced Filter System** | Multiple customizable filters with multi-timeframe support to avoid false signals |

| **Custom Exit Logic** | Exits based on OBV crossover of its moving average combined with pivot trend changes |

### Note for Novice Users

This is a fully featured real trading bot and can be tweaked for any ticker — SOL is just an example. It follows this structure:

1. **Indicator** – gives the initial signal

2. **Entry strategy** – decides when to open a trade

3. **Exit strategy** – defines when to close it

4. **Trend confirmation** – ensures the trade follows the market direction

5. **Filters** – cuts out noise and avoids weak setups

6. **Risk management** – controls losses and protects your capital

To tune it for a different pair, you'll need to start from scratch:

1. Select the timeframe (candle size)

2. Turn off all filters and trend entry/exit confirmations

3. Choose a channel type, channel source and entry strategy

4. Adjust risk parameters

5. Tune long and short settings for the channel

6. Fine-tune the Pivot Point Supertrend and Main Exit condition OBV

This will generate a lot of signals and activity on the chart. Your next task is to find the right combination of filters and settings to reduce noise and tune it for profitability.

### Default Strategy values

Default values are tuned for: Symbol BITGET:SOLUSDT.P 5min candle

Filters are off by default: Try to play with it to understand how it works

## Configuration Guide

### General Settings

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Long Positions** | Enable or disable long trades | Enabled |

| **Short Positions** | Enable or disable short trades | Enabled |

| **Risk/Reward Area** | Visual display of stop-loss and take-profit zones | Enabled |

| **Long Entry Source** | Price data used for long entry signals | hl2 (High+Low/2) |

| **Short Entry Source** | Price data used for short entry signals | hl2 (High+Low/2) |

The bot allows you to trade long positions, short positions, or both simultaneously. Each direction has its own set of parameters, allowing for fine-tuned strategies that recognize the asymmetric nature of market movements.

### Multi-Timeframe Settings

1. **Enable Multi-Timeframe Analysis**: Toggle 'Enable Multi-Timeframe Analysis' in the Multi-Timeframe Settings section

2. **Configure Timeframes**: Set appropriate higher timeframes based on your trading style:

- Timeframe 1: Default is now 15 minutes (intraday confirmation)

- Timeframe 2: Default is 4 hours (trend direction)

3. **Select Sources per Indicator**: For each indicator (RSI, KEMAD, Volume, etc.), choose:

- The desired timeframe (current, mtf1, or mtf2)

- The appropriate price type (open, high, low, close, hl2, hlc3, ohlc4)

### Entry Strategies

- **Breakout**: Enter when price breaks above/below the channel

- **Pullback**: Enter when price pulls back to the channel

- **Mean Reversion**: Enter when price is extended from the channel

You can enable different strategies for long and short positions.

### Core Components

### Risk Management

- **Position Size**: Control risk with percentage-based position sizing

- **Stop Loss Options**:

- Fixed: Set a specific price or percentage from entry

- ATR-based: Dynamic stop-loss based on market volatility

- Swing: Uses recent swing high/low points

- **Take Profit**: Multiple targets with percentage allocation

- **Trailing Stop**: Dynamic stop that follows price movement

## Advanced Usage Strategies

### Moving Average Type Selection Guide

- **SMA**: More stable in choppy markets, good for higher timeframes

- **EMA/WMA**: More responsive to recent price changes, better for entry signals

- **VWMA**: Adds volume weighting for stronger trends, use with Volume filter

- **HMA**: Balance between responsiveness and noise reduction, good for volatile markets

### Multi-Timeframe Strategy Approaches

- **Trend Confirmation**: Use higher timeframe RSI (mtf2) for overall trend, current timeframe for entries

- **Entry Precision**: Use KEMAD on current timeframe with volume filter on mtf1

- **False Signal Reduction**: Apply RSI filter on mtf1 with strict KEMAD settings

### Market Condition Optimization

| Market Condition | Recommended Settings |

|------------------|----------------------|

| **Trending** | Use Breakout strategy with KEMAD filter on higher timeframe |

| **Ranging** | Use Mean Reversion with strict RSI filter (mtf1) |

| **Volatile** | Increase ATR multipliers, use HMA for moving averages |

| **Low Volatility** | Decrease noise parameters, use pullback strategy |

## Webhook Integration

The strategy features a professional webhook system that allows direct connectivity to your exchange or trading platform of choice through third-party services like 3commas, Alertatron, or Autoview.

The webhook payload includes all necessary parameters for automated execution:

- Entry price and direction

- Stop loss and take profit levels

- Position size

- Custom identifier for webhook routing

## Performance Optimization Tips

1. **Start with Defaults**: Begin with the default settings for your timeframe before customizing

2. **Adjust One Component at a Time**: Make incremental changes and test the impact

3. **Match MA Types to Market Conditions**: Use appropriate moving average types based on the Market Condition Optimization table

4. **Timeframe Synergy**: Create logical relationships between timeframes (e.g., 5min chart with 15min and 4h higher timeframes)

5. **Periodic Retuning**: Markets evolve - regularly review and adjust parameters

## Common Setups

### Crypto Trend-Following

- MLMA with EMA or HMA

- Higher RSI thresholds (75/25)

- KEMAD filter on mtf1

- Breakout entry strategy

### Stock Swing Trading

- MLMA with SMA for stability

- Volume filter with higher threshold

- KEMAD with increased filter order

- Pullback entry strategy

### Forex Scalping

- MLMA with WMA and lower noise parameter

- RSI filter on current timeframe

- Use highest timeframe for trend direction only

- Mean Reversion strategy

## Webhook Configuration

- **Benefits**:

- Automated trade execution without manual intervention

- Immediate response to market conditions

- Consistent execution of your strategy

- **Implementation Notes**:

- Requires proper webhook configuration on your exchange or platform

- Test thoroughly with small position sizes before full deployment

- Consider latency between signal generation and execution

### Backtesting Period

Define a specific historical period to evaluate the bot's performance:

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Start Date** | Beginning of backtest period | January 1, 2025 |

| **End Date** | End of backtest period | December 31, 2026 |

- **Best Practice**: Test across different market conditions (bull markets, bear markets, sideways markets)

- **Limitation**: Past performance doesn't guarantee future results

## Entry and Exit Strategies

### Dual-Channel System

A key innovation of the Bober XM is its dual-channel approach:

- **Independent Parameters**: Each trade direction has its own channel settings

- **Asymmetric Trading**: Recognizes that markets often behave differently in uptrends versus downtrends

- **Optimized Performance**: Fine-tune settings for both bullish and bearish conditions

This approach allows the bot to adapt to the natural asymmetry of markets, where uptrends often develop gradually while downtrends can be sharp and sudden.

### Channel Types

#### 1. Keltner Channels

Traditional volatility-based channels using EMA and ATR:

| Setting | Long Default | Short Default |

|---------|--------------|---------------|

| **EMA Length** | 37 | 20 |

| **ATR Length** | 13 | 17 |

| **Multiplier** | 1.4 | 1.9 |

| **Source** | low | high |

- **Strengths**:

- Reliable in trending markets

- Less prone to whipsaws than Bollinger Bands

- Clear visual representation of volatility

- **Weaknesses**:

- Can lag during rapid market changes

- Less effective in choppy, non-trending markets

#### 2. Machine Learning Moving Average (MLMA)

Advanced predictive model using kernel regression (RBF kernel):

| Setting | Description | Options |

|---------|-------------|--------|

| **Source MA** | Price data used for MA calculations | Any price source (low/high/close/etc.) |

| **Moving Average Type** | Type of MA algorithm for calculations | SMA, EMA, WMA, VWMA, RMA, HMA |

| **Trend Source** | Price data used for trend determination | Any price source (close default) |

| **Window Size** | Historical window for MLMA calculations | 5+ (default: 16) |

| **Forecast Length** | Number of bars to forecast ahead | 1+ (default: 3) |

| **Noise Parameter** | Controls smoothness of prediction | 0.01+ (default: ~0.43) |

| **Band Multiplier** | Multiplier for channel width | 0.1+ (default: 0.5-0.6) |

- **Strengths**:

- Predictive rather than reactive

- Adapts quickly to changing market conditions

- Better at identifying trend reversals early

- **Weaknesses**:

- More computationally intensive

- Requires careful parameter tuning

- Can be sensitive to input data quality

### Entry Strategies

| Strategy | Description | Ideal Market Conditions |

|----------|-------------|-------------------------|

| **Breakout** | Enters when price breaks through channel bands, indicating strong momentum | High volatility, emerging trends |

| **Pullback** | Enters when price retraces to the middle band after testing extremes | Established trends with regular pullbacks |

| **Mean Reversion** | Enters at channel extremes, betting on a return to the mean | Range-bound or oscillating markets |

#### Breakout Strategy (Default)

- **Implementation**: Enters long when price crosses above the upper band, short when price crosses below the lower band

- **Strengths**: Captures strong momentum moves, performs well in trending markets

- **Weaknesses**: Can lead to late entries, higher risk of false breakouts

- **Optimization Tips**:

- Increase channel multiplier for fewer but more reliable signals

- Combine with volume confirmation for better accuracy

#### Pullback Strategy

- **Implementation**: Enters long when price pulls back to middle band during uptrend, short during downtrend pullbacks

- **Strengths**: Better entry prices, lower risk, higher probability setups

- **Weaknesses**: Misses some strong moves, requires clear trend identification

- **Optimization Tips**:

- Use with trend filters to confirm overall direction

- Adjust middle band calculation for market volatility

#### Mean Reversion Strategy

- **Implementation**: Enters long at lower band, short at upper band, expecting price to revert to the mean

- **Strengths**: Excellent entry prices, works well in ranging markets

- **Weaknesses**: Dangerous in strong trends, can lead to fighting the trend

- **Optimization Tips**:

- Implement strong trend filters to avoid counter-trend trades

- Use smaller position sizes due to higher risk nature

### Confirmation Indicators

#### Pivot Point SuperTrend

Combines pivot points with ATR-based SuperTrend for trend confirmation:

| Setting | Default Value |

|---------|---------------|

| **Pivot Period** | 25 |

| **ATR Factor** | 2.2 |

| **ATR Period** | 41 |

- **Function**: Identifies significant market turning points and confirms trend direction

- **Implementation**: Requires price to respect the SuperTrend line for trade confirmation

#### Weighted Moving Average (WMA)

Provides additional confirmation layer for entries:

| Setting | Default Value |

|---------|---------------|

| **Period** | 15 |

| **Source** | ohlc4 (average of Open, High, Low, Close) |

- **Function**: Confirms trend direction and filters out low-quality signals

- **Implementation**: Price must be above WMA for longs, below for shorts

### Exit Strategies

#### On-Balance Volume (OBV) Based Exits

Uses volume flow to identify potential reversals:

| Setting | Default Value |

|---------|---------------|

| **Source** | ohlc4 |

| **MA Type** | HMA (Options: SMA, EMA, WMA, RMA, VWMA, HMA) |

| **Period** | 22 |

- **Function**: Identifies divergences between price and volume to exit before reversals

- **Implementation**: Exits when OBV crosses its moving average in the opposite direction

- **Customizable MA Type**: Different MA types provide varying sensitivity to OBV changes:

- **SMA**: Traditional simple average, equal weight to all periods

- **EMA**: More weight to recent data, responds faster to price changes

- **WMA**: Weighted by recency, smoother than EMA

- **RMA**: Similar to EMA but smoother, reduces noise

- **VWMA**: Factors in volume, helpful for OBV confirmation

- **HMA**: Reduces lag while maintaining smoothness (default)

#### ADX Exit Confirmation

Uses Average Directional Index to confirm trend exhaustion:

| Setting | Default Value |

|---------|---------------|

| **ADX Threshold** | 35 |

| **ADX Smoothing** | 60 |

| **DI Length** | 60 |

- **Function**: Confirms trend weakness before exiting positions

- **Implementation**: Requires ADX to drop below threshold or DI lines to cross

## Filter System

### RSI Filter

- **Function**: Controls entries based on momentum conditions

- **Parameters**:

- Period: 15 (default)

- Overbought level: 71

- Oversold level: 23

- Multi-timeframe support: Current, MTF1 (15min), or MTF2 (4h)

- Customizable price source (open, high, low, close, hl2, hlc3, ohlc4)

- **Implementation**: Blocks long entries when RSI > overbought, short entries when RSI < oversold

### Volatility Filter

- **Function**: Prevents trading during excessive market volatility

- **Parameters**:

- Measure: ATR (Average True Range)

- Period: Customizable (default varies by timeframe)

- Threshold: Adjustable multiplier

- Multi-timeframe support

- Customizable price source

- **Implementation**: Blocks trades when current volatility exceeds threshold × average volatility

### Volume Filter

- **Function**: Ensures adequate market liquidity for trades

- **Parameters**:

- Threshold: 0.4× average (default)

- Measurement period: 5 (default)

- Moving average type: Customizable (HMA default)

- Multi-timeframe support

- Customizable price source

- **Implementation**: Requires current volume to exceed threshold × average volume

### Bollinger Bands Filter

- **Function**: Controls entries based on price relative to statistical boundaries

- **Parameters**:

- Period: Customizable

- Standard deviation multiplier: Adjustable

- Moving average type: Customizable

- Multi-timeframe support

- Customizable price source

- **Implementation**: Can require price to be within bands or breaking out of bands depending on strategy

### KEMAD Filter (Kalman EMA Distance)

- **Function**: Advanced trend confirmation using Kalman filter algorithm

- **Parameters**:

- Process Noise: 0.35 (controls smoothness)

- Measurement Noise: 24 (controls reactivity)

- Filter Order: 6 (higher = more smoothing)

- ATR Length: 8 (for bandwidth calculation)

- Upper Multiplier: 2.0 (for long signals)

- Lower Multiplier: 2.7 (for short signals)

- Multi-timeframe support

- Customizable visual indicators

- **Implementation**: Generates signals based on price position relative to Kalman-filtered EMA bands

## Risk Management System

### Position Sizing

Automatically calculates position size based on account equity and risk parameters:

| Setting | Default Value |

|---------|---------------|

| **Risk % of Equity** | 50% |

- **Implementation**:

- Position size = (Account equity × Risk %) ÷ (Entry price × Stop loss distance)

- Adjusts automatically based on volatility and stop placement

- **Best Practices**:

- Start with lower risk percentages (1-2%) until strategy is proven

- Consider reducing risk during high volatility periods

### Stop-Loss Methods

Multiple stop-loss calculation methods with separate configurations for long and short positions:

| Method | Description | Configuration |

|--------|-------------|---------------|

| **ATR-Based** | Dynamic stops based on volatility | ATR Period: 14, Multiplier: 2.0 |

| **Percentage** | Fixed percentage from entry | Long: 1.5%, Short: 1.5% |

| **PIP-Based** | Fixed currency unit distance | 10.0 pips |

- **Implementation Notes**:

- ATR-based stops adapt to changing market volatility

- Percentage stops maintain consistent risk exposure

- PIP-based stops provide precise control in stable markets

### Trailing Stops

Locks in profits by adjusting stop-loss levels as price moves favorably:

| Setting | Default Value |

|---------|---------------|

| **Stop-Loss %** | 1.5% |

| **Activation Threshold** | 2.1% |

| **Trailing Distance** | 1.4% |

- **Implementation**:

- Initial stop remains fixed until profit reaches activation threshold

- Once activated, stop follows price at specified distance

- Locks in profit while allowing room for normal price fluctuations

### Risk-Reward Parameters

Defines the relationship between risk and potential reward:

| Setting | Default Value |

|---------|---------------|

| **Risk-Reward Ratio** | 1.4 |

| **Take Profit %** | 2.4% |

| **Stop-Loss %** | 1.5% |

- **Implementation**:

- Take profit distance = Stop loss distance × Risk-reward ratio

- Higher ratios require fewer winning trades for profitability

- Lower ratios increase win rate but reduce average profit

### Filter Combinations

The strategy allows for simultaneous application of multiple filters:

- **Recommended Combinations**:

- Trending markets: RSI + KEMAD filters

- Ranging markets: Bollinger Bands + Volatility filters

- All markets: Volume filter as minimum requirement

- **Performance Impact**:

- Each additional filter reduces the number of trades

- Quality of remaining trades typically improves

- Optimal combination depends on market conditions and timeframe

### Multi-Timeframe Filter Applications

| Filter Type | Current Timeframe | MTF1 (15min) | MTF2 (4h) |

|-------------|-------------------|-------------|------------|

| RSI | Quick entries/exits | Intraday trend | Overall trend |

| Volume | Immediate liquidity | Sustained support | Market participation |

| Volatility | Entry timing | Short-term risk | Regime changes |

| KEMAD | Precise signals | Trend confirmation | Major reversals |

## Visual Indicators and Chart Analysis

The bot provides comprehensive visual feedback on the chart:

- **Channel Bands**: Keltner or MLMA bands showing potential support/resistance

- **Pivot SuperTrend**: Colored line showing trend direction and potential reversal points

- **Entry/Exit Markers**: Annotations showing actual trade entries and exits

- **Risk/Reward Zones**: Visual representation of stop-loss and take-profit levels

These visual elements allow for:

- Real-time strategy assessment

- Post-trade analysis and optimization

- Educational understanding of the strategy logic

## Implementation Guide

### TradingView Setup

1. Load the script in TradingView Pine Editor

2. Apply to your preferred chart and timeframe

3. Adjust parameters based on your trading preferences

4. Enable alerts for webhook integration

### Webhook Integration

1. Configure webhook URL in TradingView alerts

2. Set up receiving endpoint on your trading platform

3. Define message format matching the bot's output

4. Test with small position sizes before full deployment

### Optimization Process

1. Backtest across different market conditions

2. Identify parameter sensitivity through multiple tests

3. Focus on risk management parameters first

4. Fine-tune entry/exit conditions based on performance metrics

5. Validate with out-of-sample testing

## Performance Considerations

### Strengths

- Adaptability to different market conditions through dual channels

- Multiple layers of confirmation reducing false signals

- Comprehensive risk management protecting capital

- Machine learning integration for predictive edge

### Limitations

- Complex parameter set requiring careful optimization

- Potential over-optimization risk with so many variables

- Computational intensity of MLMA calculations

- Dependency on proper webhook configuration for execution

### Best Practices

- Start with conservative risk settings (1-2% of equity)

- Test thoroughly in demo environment before live trading

- Monitor performance regularly and adjust parameters

- Consider market regime changes when evaluating results

## Conclusion

The ₿ober XM v2.0 represents a significant evolution in trading strategy design, combining traditional technical analysis with machine learning elements and multi-timeframe analysis. The core strength of this system lies in its adaptability and recognition of market asymmetry.

### Market Asymmetry and Adaptive Approach

The strategy acknowledges a fundamental truth about markets: bullish and bearish phases behave differently and should be treated as distinct environments. The dual-channel system with separate parameters for long and short positions directly addresses this asymmetry, allowing for optimized performance regardless of market direction.

### Targeted Backtesting Philosophy

It's counterproductive to run backtests over excessively long periods. Markets evolve continuously, and strategies that worked in previous market regimes may be ineffective in current conditions. Instead:

- Test specific market phases separately (bull markets, bear markets, range-bound periods)

- Regularly re-optimize parameters as market conditions change

- Focus on recent performance with higher weight than historical results

- Test across multiple timeframes to ensure robustness

### Multi-Timeframe Analysis as a Game-Changer

The integration of multi-timeframe analysis fundamentally transforms the strategy's effectiveness:

- **Increased Safety**: Higher timeframe confirmations reduce false signals and improve trade quality

- **Context Awareness**: Decisions made with awareness of larger trends reduce adverse entries

- **Adaptable Precision**: Apply strict filters on lower timeframes while maintaining awareness of broader conditions

- **Reduced Noise**: Higher timeframe data naturally filters market noise that can trigger poor entries

The ₿ober XM v2.0 provides traders with a framework that acknowledges market complexity while offering practical tools to navigate it. With proper setup, realistic expectations, and attention to changing market conditions, it delivers a sophisticated approach to systematic trading that can be continuously refined and optimized.

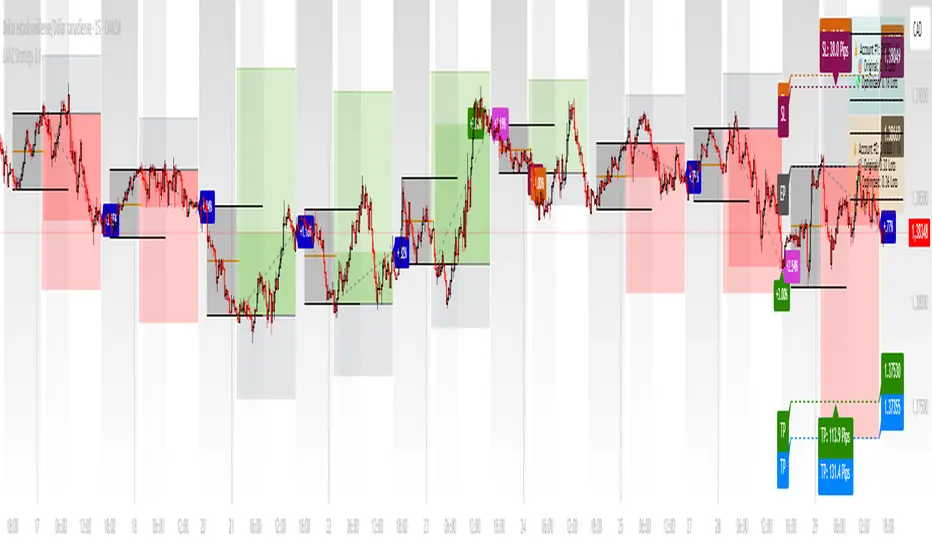

LANZ Strategy 3.0🔷 LANZ Strategy 3.0 — Asian Range Fibonacci Strategy with Execution Window Logic

LANZ Strategy 3.0 is a rule-based trading system that utilizes the Asian session range to project Fibonacci levels and manage entries during a defined execution window. Designed for Forex and index traders, this strategy focuses on structured price behavior around key levels before the New York session.

🧠 Core Components:

Asian Session Range Mapping: Automatically detects the high, low, and midpoint during the Asian session.

Fibonacci Level Projection: Projects configurable Fibonacci retracement and extension levels based on the Asian range.

Execution Window Logic: Uses the 01:15 NY candle as a reference to validate potential reversals or continuation setups.

Conditional Entry System: Includes logic for limit order entries (buy or sell) at specific Fib levels, with reversal logic if price breaks structure before execution.

Risk Management: Entry orders are paired with dynamic SL and TP based on Fibonacci-based distances, maintaining a risk-reward ratio consistent with intraday strategies.

📊 Visual Features:

Asian session high/low/mid lines.

Fibonacci levels: Original (based on raw range) and Optimized (user-adjustable).

Session background coloring for Asia, Execution Window, and NY session.

Labels and lines for entry, SL, and TP targets.

Dynamic deletion of untriggered orders after execution window expires.

⚙️ How It Works:

The script calculates the Asian session range.

Projects Fibonacci levels from the range.

Waits for the 01:15 NY candle to close to validate a signal.

If valid, a limit entry order (BUY or SELL) is plotted at the selected level.

If price structure changes (e.g., breaks the high/low), reversal logic may activate.

If no trade is triggered, orders are cleared before the NY session.

🔔 Alerts:

Alerts trigger when a valid setup appears after 01:15 NY candle.

Optional alerts for order activation, SL/TP hit, or trade cancellation.

📝 Notes:

Intended for semi-automated or discretionary trading.

Best used on highly liquid markets like Forex majors or indices.

Script parameters include session times, Fib ratios, SL/TP settings, and reversal logic toggle.

Credits:

Developed by LANZ, this script merges traditional session-based analysis with Fibonacci tools and structured execution timing, offering a unique framework for morning volatility plays.

Opening Range and Market BoundariesOpening Range and Market Boundaries

This versatile and insightful indicator combines two powerful concepts frequently used by professional traders: Opening Range Analysis and Market Boundaries derived from previous high/low levels. It is specifically designed to support intraday trading strategies and helps you identify key price zones for entries, exits, and breakout confirmations.

🔍 Features & Utility

1. Opening Range Box

What it does:

Highlights the high and low of the first candle after market open (9:15 AM IST) with a shaded box. This box spans the full trading session, from 9:15 AM to 3:30 PM, representing the key price range where the initial balance is formed.

Timeframe Compatibility:

The Opening Range box is optimized for 1-minute to 1-hour charts. It is most effective on lower timeframes (1m, 5m, 15m, 30m) where intraday price movements and breakout patterns can be clearly observed.

Usage Tips:

Breakouts above or below the Opening Range box can signal potential directional bias for the rest of the trading day.

Price consolidating within the range may indicate a choppy or range-bound session.

Works well with volume and momentum indicators for confirmation.

2. Market Boundaries

What it does:

Plots horizontal lines at:

Previous Day High/Low

Previous Week High/Low

Previous Month High/Low

Why it matters:

These levels act as natural support and resistance zones, and are commonly watched by institutional traders, making them crucial for:

Spotting reversals or breakouts

Planning stop-loss and target zones

Avoiding trades around high-rejection areas

Customization Options:

Toggle ON/OFF for Daily, Weekly, and Monthly levels.

Independent colors and line thickness for each level, enabling you to distinguish between different timeframes easily.

🛠️ How to Use Effectively

Use during market open:

Switch to a 5-minute or 15-minute chart during the first few candles of the session. Observe the Opening Range box formation and plan trades based on breakout direction.

Confluence Trading:

Look for price action near previous session highs/lows in confluence with the Opening Range box edges. These intersections often become high-probability zones for breakouts or reversals.

Session Preparation:

Before the market opens, analyze where the price is relative to past high/low boundaries. If it's near a weekly/monthly level, be cautious — those areas can cause whipsaws or false breakouts.

Avoid low-volume breakouts:

Use this indicator in conjunction with volume tools or price action confirmation to validate the strength of a move outside the Opening Range or Market Boundaries.

📌 Summary

This indicator is designed for intraday traders, scalpers, and swing traders who want a reliable structure to guide their decisions. It visually marks the opening balance of the market and essential higher timeframe boundaries, helping you trade with discipline and precision.

Reintegration OPR zone 9h30📝 Indicator Description (for TradingView):

Name: Reintegration OPR Zone – 9:30 AM EST (UTC-4)

Purpose:

This indicator is designed for US indices like NAS100, US30, or SPX500. It helps identify potential false breakouts or retests by tracking when the price re-enters the Opening Price Range (OPR) after an initial breakout.

🔍 How it works:

At 9:30 AM New York time (UTC-4), the script captures the high and low of the first 15-minute candle (which is key for the US session open).

It then draws a horizontal box (rectangle) from the high to the low of that candle.

The box extends horizontally for 7 hours (28 candles on a 15-minute chart).

The script tracks if price:

Breaks above or below the OPR zone

Then re-enters the zone (a potential "fakeout" or "retest" signal)

No label or text is displayed on the chart (you requested it to be hidden).

🕒 Timeframe:

Designed for the 15-minute chart (M15)

Assumes New York session open at 9:30 AM EST (UTC-4)

Adaptive Freedom Machine w/labelsAdaptive Freedom Machine w/ Labels

Overview

The Adaptive Freedom Machine w/ Labels is a versatile Pine Script indicator designed to assist traders in identifying buy and sell opportunities across various market conditions (trending, ranging, or volatile). It combines Exponential Moving Averages (EMAs), Relative Strength Index (RSI), Average True Range (ATR), and customizable time filters to generate actionable signals. The indicator overlays on the price chart, displaying EMAs, a dynamic cloud, scaled RSI levels, buy/sell signals, and market condition labels, making it suitable for swing trading, day trading, or scalping.

What It Does

This indicator generates buy and sell signals based on the interaction of two EMAs, filtered by RSI thresholds, ATR-based volatility, and user-defined time windows. It adapts to the selected market condition by adjusting EMA lengths, RSI thresholds, and trading hours. A dynamic cloud highlights trend direction or neutral zones, and candlestick bodies are colored in neutral conditions for clarity. A table displays real-time trend and volatility status.

How It Works

The indicator uses the following components:

EMAs: Two EMAs (short and long) are calculated on a user-selected timeframe (1, 5, 15, 30, or 60 minutes). Their crossover or crossunder generates potential buy/sell signals, with lengths adjusted based on the market condition (e.g., longer EMAs for trending markets, shorter for ranging).

Dynamic Cloud: The area between the EMAs forms a cloud, colored green for uptrends, red for downtrends, or a user-defined color (default yellow) for neutral zones (when EMAs are close, determined by an ATR-based threshold). Users can widen the cloud for visibility.

RSI Filter: RSI is scaled to price levels and plotted on the chart (optional). Signals are filtered to ensure RSI is within user-defined buy/sell thresholds and not in overbought/oversold zones, with thresholds tailored to the market condition.

ATR Volatility Filter: An optional filter ensures signals occur during sufficient volatility (ATR(14) > SMA(ATR, 20)).

Time Filter: Signals are restricted to a user-defined or market-specific time window (e.g., 10:00–15:00 UTC for volatile markets), with an option for custom hours.

Visual Aids: Buy/sell signals appear as green triangles (buy) or red triangles (sell). Candlesticks in neutral zones are colored (default yellow). A table in the top-right corner shows the current trend (Uptrend, Downtrend, Neutral) and volatility (High or Low).

The indicator ensures compatibility with standard chart types (e.g., candlestick charts) to produce realistic signals, avoiding non-standard types like Heikin Ashi or Renko.

How to Use It

Add to Chart: Apply the indicator to a candlestick or bar chart on TradingView.

Configure Settings:

Timeframe: Choose a timeframe (1, 5, 15, 30, or 60 minutes) to align with your trading style.

Market Condition: Select one market condition (Trending, Ranging, or Volatile). Volatile is the default if none is selected. Only one condition can be active.

Filters:

Enable/disable the ATR volatility filter to trade only in high-volatility periods.

Enable the time filter and choose default hours (specific to the market condition) or set custom UTC hours.

Cloud Settings: Adjust the cloud width, neutral zone threshold, and color. Enable/disable the neutral cloud.

RSI Display: Toggle the scaled RSI and its thresholds on the chart.

Interpret Signals:

Buy Signal: A green triangle below the bar indicates a potential long entry (EMA crossover, RSI above buy threshold, within time window, and passing volatility filter).

Sell Signal: A red triangle above the bar indicates a potential short entry (EMA crossunder, RSI below sell threshold, within time window, and passing volatility filter).

Neutral Zone: Yellow candlesticks and cloud (if enabled) suggest a lack of clear trend; avoid trading or use for range-bound strategies.

Monitor the Table: Check the top-right table for real-time trend (Uptrend, Downtrend, Neutral) and volatility (High or Low) to confirm market context.

Unique Features

Adaptive Parameters: Automatically adjusts EMA lengths, RSI thresholds, and trading hours based on the selected market condition, reducing manual tweaking.

Neutral Zone Detection: Uses an ATR-based threshold to identify low-trend periods, helping traders avoid choppy markets.

Scaled RSI Visualization: Plots RSI and thresholds directly on the price chart, making it easier to assess momentum relative to price action.

Flexible Time Filtering: Supports both default and custom UTC-based trading windows, ideal for day traders targeting specific sessions.

Dynamic Cloud: Enhances trend visualization with customizable width and neutral zone coloring, improving readability.

Notes

Use on standard candlestick or bar charts to ensure realistic signals.

Test the indicator on a demo account to understand its behavior in your chosen market and timeframe.

Adjust settings to match your trading strategy, but avoid over-optimizing for past data.

The indicator is not a standalone system; combine it with other analysis (e.g., support/resistance, news events) for better results.

Limitations

Signals may lag in fast-moving markets due to EMA-based calculations.

Neutral zone detection may vary in extremely volatile or illiquid markets.

Time filters are UTC-based; ensure your platform’s timezone settings align.

This indicator is designed for traders seeking a customizable, trend-following tool that adapts to different market environments while providing clear visual cues and robust filtering.

EMA Crossover Signal (15min)📈 EMA Crossover Signal (15min)

This indicator generates Buy and Sell signals based on a simple yet effective Exponential Moving Average (EMA) crossover strategy, strictly evaluated on the 15-minute timeframe.

✅ Strategy:

Buy Signal: Triggered when the 5 EMA crosses above the 10 EMA.

Sell Signal: Triggered when the 5 EMA crosses below the 10 EMA.

📌 Features:

Signals are evaluated using 15-minute data, regardless of your current chart timeframe.

Clear Buy/Sell labels are displayed directly on the chart.

Optional plotting of the 5 EMA and 10 EMA from the 15-minute chart for visual confirmation.

This tool is ideal for traders who want to follow short-term momentum shifts with high clarity and precision.

Dskyz Adaptive Futures Elite (DAFE)Dskyz Adaptive Futures Edge (DAFE)

imgur.com

A Dynamic Futures Trading Strategy

DAFE adapts to market volatility and price action using technical indicators and advanced risk management. It’s built for high-stakes futures trading (e.g., MNQ, BTCUSDT.P), offering modular logic for scalpers and swing traders alike.

Key Features

Adaptive Moving Averages

Dynamic Logic: Fast and slow SMAs adjust lengths via ATR, reacting to momentum shifts and smoothing in calm markets.

Signals: Long entry on fast SMA crossing above slow SMA with price confirmation; short on cross below.

RSI Filtering (Optional)

Momentum Check: Confirms entries with RSI crossovers (e.g., above oversold for longs). Toggle on/off with custom levels.

Fine-Tuning: Adjustable lookback and thresholds (e.g., 60/40) for precision.

Candlestick Pattern Recognition

Eng|Enhanced Detection: Identifies strong bullish/bearish engulfing patterns, validated by volume and range strength (vs. 10-period SMA).

Conflict Avoidance: Skips trades if both patterns appear in the lookback window, reducing whipsaws.

Multi-Timeframe Trend Filter

15-Minute Alignment: Syncs intrabar trades with 15-minute SMA trends; optional for flexibility.

Dollar-Cost Averaging (DCA) New!

Scaling: Adds up to a set number of entries (e.g., 4) on pullbacks/rallies, spaced by ATR multiples.

Control: Caps exposure and resets on exit, enhancing trend-following potential.

Trade Execution & Risk Management

Entry Rules: Prioritizes moving averages or patterns (user choice), with volume, volatility, and time filters.

Stops & Trails:

Initial Stop: ATR-based (2–3.5x, volatility-adjusted).

Trailing Stop: Locks profits with configurable ATR offset and multiplier.

Discipline

Cooldown: Pauses post-exit (e.g., 0–5 minutes).

Min Hold: Ensures trades last a set number of bars (e.g., 2–10).

Visualization & Tools

Charts: Overlays MAs, stops, and signals; trend shaded in background.

Dashboard: Shows position, P&L, win rate, and more in real-time.

Debugging: Logs signal details for optimization.

Input Parameters

Parameter Purpose Suggested Use

Use RSI Filter - Toggle RSI confirmation *Disable 4 price-only

trading

RSI Length - RSI period (e.g., 14) *7–14 for sensitivity

RSI Overbought/Oversold - Adjust for market type *Set levels (e.g., 60/40)

Use Candlestick Patterns - Enables engulfing signals *Disable for MA focus

Pattern Lookback - Pattern window (e.g., 19) *10–20 bars for balance

Use 15m Trend Filter - Align with 15-min trend *Enable for trend trades

Fast/Slow MA Length - Base MA lengths (e.g., 9/19) *10–25 / 30–60 per

timeframe

Volatility Threshold - Filters volatile spikes *Max ATR/close (e.g., 1%)

Min Volume - Entry volume threshold *Avoid illiquid periods

(e.g., 10)

ATR Length - ATR period (e.g., 14) *Standard volatility

measure

Trailing Stop ATR Offset - Trail distance (e.g., 0.5) *0.5–1.5 for tightness

Trailing Stop ATR Multi - Trail multiplier (e.g., 1.0) *1–3 for trend room

Cooldown Minutes - Post-exit pause (e.g., 0–5) *Prevents overtrading

Min Bars to Hold - Min trade duration (e.g., 2) *5–10 for intraday

Trading Hours - Active window (e.g., 9–16) *Focus on key sessions

Use DCA - Toggle DCA *Enable for scaling

Max DCA Entries - Cap entries (e.g., 4) *Limit risk exposure

DCA ATR Multiplier Entry spacing (e.g., 1.0) *1–2 for wider gaps

Compliance

Realistic Testing: Fixed quantities, capital, and slippage for accurate backtests.

Transparency: All logic is user-visible and adjustable.

Risk Controls: Cooldowns, stops, and hold periods ensure stability.

Flexibility: Adapts to various futures and timeframes.

Summary

DAFE excels in volatile futures markets with adaptive logic, DCA scaling, and robust risk tools. Currently in prop account testing, it’s a powerful framework for precision trading.

Caution

DAFE is experimental, not a profit guarantee. Futures trading risks significant losses due to leverage. Backtest, simulate, and monitor actively before live use. All trading decisions are your responsibility.

Nifty Range % and Points by Time BlocksPine Script that gives you day-wise intraday range percentage for these 3 time blocks (9:16–10:45, 10:45–1:15, 1:15–3:15), we can:

Detect time blocks during the day

Track High/Low for each block

Calculate range % for each block:

\text{Range %} = \frac{(High - Low)}{\text{Previous Day Close}} \times 100

Plot / Label it on the chart at the end of each block

Ichimoku Cloud Auto TF🧠 Timeframe Breakdown for Ichimoku Cloud Auto TF

Each timeframe in this indicator is carefully calibrated to reflect meaningful Ichimoku behavior relative to its scale. Here's how each one is structured and what it's best used for:

⏱️ 1 Minute (1m)

Tenkan / Kijun / Span B: 5 / 15 / 45

Use: Scalping fast price action.

Logic: Quick reaction to short-term momentum. Best for highly active traders or bots.

⏱️ 2 Minutes (2m)

Tenkan / Kijun / Span B: 6 / 18 / 54

Use: Slightly smoother than 1m, still ideal for scalping with a little more stability.

⏱️ 5 Minutes (5m)

Tenkan / Kijun / Span B: 8 / 24 / 72

Use: Intraday setups, quick trend capture.

Logic: Balanced between reactivity and noise reduction.

⏱️ 15 Minutes (15m)

Tenkan / Kijun / Span B: 9 / 27 / 81

Use: Short-term swing and intraday entries with higher reliability.

⏱️ 30 Minutes (30m)

Tenkan / Kijun / Span B: 10 / 30 / 90

Use: Intra-swing entries or confirmation of 5m/15m signals.

🕐 1 Hour (1H)

Tenkan / Kijun / Span B: 12 / 36 / 108

Use: Ideal for swing trading setups.

Logic: Anchored to Daily reference (1H × 24 ≈ 1D).

🕐 2 Hours (2H)

Tenkan / Kijun / Span B: 14 / 42 / 126

Use: High-precision swing setups with better context.

🕒 3 Hours (3H)

Tenkan / Kijun / Span B: 15 / 45 / 135

Use: Great compromise between short and mid-term vision.

🕓 4 Hours (4H)

Tenkan / Kijun / Span B: 18 / 52 / 156

Use: Position traders & intraday swing confirmation.

Logic: Designed to echo the structure of 1D Ichimoku but on smaller scale.

📅 1 Day (1D)

Tenkan / Kijun / Span B: 9 / 26 / 52

Use: Classic Ichimoku settings.

Logic: Standard used globally for technical analysis. Suitable for swing and position trading.

📆 1 Week (1W)

Tenkan / Kijun / Span B: 12 / 24 / 120

Use: Long-term position trading & institutional swing confirmation.

Logic: Expanded ratios for broader perspective and noise filtering.

🗓️ 1 Month (1M)

Tenkan / Kijun / Span B: 6 / 12 / 24

Use: Macro-level trend visualization and investment planning.

Logic: Condensed but stable structure to handle longer data cycles.

📌 Summary

This indicator adapts Ichimoku settings dynamically to your chart's timeframe, maintaining logical ratios between Tenkan, Kijun, and Span B. This ensures each timeframe remains responsive yet meaningful for its respective market context.

Multi-TF Support LevelsThe Multi-TF Support Levels indicator identifies and displays key support levels based on swing lows across three user-selected timeframes.

How it works:

Input Parameters:

Lookback Period (100) — historical depth to search for swing lows.

Timeframe 1-3 (15, 45, 240) — three timeframes (e.g., 15min, 45min, 4hr).

Logic:

For each timeframe, a swing low is detected: the lowest price within the lookback period that is also lower than the two preceding candles.

Support levels update dynamically when new swing lows are formed.

The most recent levels are plotted as horizontal cross marks (blue, red, green for each timeframe).

Purpose: Visualize significant support zones from multiple timeframes to identify confluent areas for trading decisions.

Индикатор Multi-TF Support Levels (Мультитаймфреймовые уровни поддержки) определяет и отображает ключевые уровни поддержки на основе минимумов свингов (swing lows) на трёх выбранных таймфреймах.

Как работает:

Входные параметры:

Lookback Period (100) — глубина анализа для поиска минимумов.

Timeframe 1-3 (15, 45, 240) — три таймфрейма (например, 15 минут, 45 минут, 4 часа).

Логика:

Для каждого таймфрейма определяется свинг-минимум: цена, которая является самой низкой за период lookback и ниже двух предыдущих свечей.

Уровни поддержки обновляются при появлении новых свинг-минимумов.

Последние актуальные уровни отображаются на графике в виде горизонтальных линий-крестиков (синий, красный, зелёный для каждого таймфрейма).

Цель: Визуализировать значимые уровни поддержки с разных таймфреймов для поиска зон "конфлюэнса".

Granular MA Ribbon🎗️ The Granular MA Ribbon provides a structured view of price action on lower timeframes by incorporating both price-based and volume-weighted moving averages, offering a more nuanced view of market trends and momentum shifts. Furthermore, by using 15-minute intervals for its calculations, it ensures that intraday traders receive a smooth and responsive representation of higher timeframe trends.

⚠️ Note that this indicator is specifically optimized for the 15-minute and 1-hour charts; applying it to longer or shorter periods will distort its calculations and reduce its effectiveness. Adjust visibility settings accordingly.

🧰 Unlike traditional moving averages that may lag or fail to reflect real-time shifts in price dynamics, the Granular MA Ribbon includes a one-day exponential moving average (1D EMA), a one-day volume-weighted moving average (1D VWMA), and a one-week exponential moving average (1W EMA). Together, these elements allow traders to stay aligned with the broader market while making precise intraday trading decisions.

🤷🏻 Why Two Daily Moving Averages?

🔊 Instead of relying on a single moving average, this indicator uses both an EMA and a VWMA to provide a clearer picture of price movement. The EMA reacts quickly to price changes, making it a useful tool for identifying short-term momentum shifts. The VWMA, meanwhile, accounts for volume, ensuring that price movements supported by higher trading activity carry greater weight in the trend calculation.

💪🏻 When the EMA and VWMA diverge significantly, it signals strong momentum. If they begin to converge, it suggests that momentum is weakening or that price may be entering consolidation. The space between these two moving averages is filled with a ribbon, making it easier to see shifts in trend strength. A wide ribbon typically indicates strong momentum, while a narrowing ribbon suggests the trend may be losing steam.

🧮 Calculation Rationale

🔎 The 1D EMA and 1D VWMA are constructed using 15-minute blocks to maintain accuracy on lower timeframes. A full trading day consists of 96 fifteen-minute intervals. Instead of relying on daily candle data, which would reduce the granularity of the moving averages, this method allows the indicator to reflect intra-day trends more accurately. By breaking the day into smaller increments, the moving averages adapt more smoothly to changes in price and volume, making them more reliable for traders working on shorter timeframes.

🔍 The weekly EMA follows the same logic, adjusting based on the selected five-day or seven-day setting. If the market follows a standard five-day trading week, the one-week EMA is calculated using 480 fifteen-minute bars. If the market trades seven days a week, such as in crypto, the weekly EMA is adjusted accordingly to reflect 672 fifteen-minute bars. This setting ensures that traders using the indicator across different asset classes receive accurate trend information.

🫤 Sideways Markets

🔄 When the broader market is in a range-bound state, with no clear trend on the one-day or one-week chart, this indicator helps traders make sense of the short-term price structure. In these conditions, the ribbon will often appear flat, with the 1D EMA and 1D VWMA frequently crossing each other. This suggests that momentum is weak and that price action lacks a strong directional bias.

⚠️ A narrowing ribbon in a sideways market indicates reduced volatility and a potential breakout. If the EMA crosses above the VWMA during consolidation, it may signal a short-term upward move, especially if volume begins to increase. Conversely, if the EMA moves below the VWMA, it could indicate that selling pressure is increasing. However, in choppy conditions, crossovers alone are not enough to confirm a trade. Traders should wait for additional confirmation, such as a breakout from a defined range or a shift in volume.

♭ If the weekly EMA remains flat while the daily ribbon fluctuates, it confirms that the market lacks a strong trend. In such cases, traders may consider fading moves near the top and bottom of a range rather than expecting sustained breakouts.

💹 Trending Markets

🏗️ When the market is in a strong uptrend or downtrend, the ribbon takes on a more structured shape. A widening ribbon that slopes upward signals strong bullish momentum, with price consistently respecting the 1D EMA and VWMA as support. In a downtrend, the ribbon slopes downward, acting as dynamic resistance.

📈 In trending conditions, traders can use the ribbon to time pullback entries. In an uptrend, price often retraces to the VWMA before resuming its upward move. If price holds above both the EMA and VWMA, the trend remains strong. If price begins to close below the VWMA but remains above the EMA, it suggests weakening momentum but not necessarily a reversal. A clean break below both moving averages indicates a shift in trend structure.

📊 The one-week EMA serves as a higher timeframe guide. When price remains above the weekly EMA, it confirms that the broader trend is intact. If price pulls back to the weekly EMA and bounces, it can provide a high-confidence trade entry. Conversely, if price breaks below the weekly EMA and fails to reclaim it, it suggests that the trend may be reversing.

⏳ 5-Day and 7-Day Week Variants

🎚️ The setting for a five-day or seven-day trading week adjusts the calculation of the one-week EMA. This ensures that the indicator remains accurate across different asset classes.

5️⃣ A five-day trading week is appropriate for stocks, futures, and forex markets, where trading pauses on weekends. Using a seven-day week for these markets would create artificial distortions by including non-trading days. 7️⃣ In contrast, the seven-day week setting is ideal for crypto markets, which trade continuously. Without this adjustment, the weekly EMA would fail to reflect weekend price action, leading to misleading trend signals.

🧐 This indicator is expressly designed to complement its higher timeframe counterpart, the Triple Differential Moving Average Braid, optimized for the 1-Day chart.

CVD Oscillator - Short Term SwiftEdgeOverview

The CVD Oscillator - Short Term is a technical indicator designed to assist traders in identifying short-term buying and selling pressure in the market. It calculates the Cumulative Volume Delta (CVD) to measure the net volume difference between buying and selling activity, displayed as an oscillator in a separate panel. This indicator is tailored for short-term trading strategies, such as scalping or day trading, on low timeframes (e.g., 1-minute, 5-minute, or 15-minute charts).

How It Works

Cumulative Volume Delta (CVD): The indicator calculates CVD by assigning volume to buyers (when close > open) or sellers (when close < open). If close = open, the volume is neutral.

Short-Term Focus: The CVD is calculated over a user-defined lookback period (default: 10 candles), making it sensitive to recent market activity.

Normalization: The raw CVD is normalized by dividing it by the average volume (over a short period, default: 5 candles) and scaled to fit within a range of -100 to +100, creating an oscillator-like behavior.

Reset Options: Users can reset the CVD at specific intervals (e.g., every minute, 5 minutes, 15 minutes, or daily) to focus on intraday movements.

Live CVD Value: The raw (unnormalized) CVD value is displayed as a label on each candle for real-time monitoring.

Key Features

Customizable Lookback Period: Adjust the number of recent candles (default: 10) to calculate CVD, allowing for precise short-term analysis.

Flexible Reset Periods: Choose to reset the CVD every 1 minute, 5 minutes, 15 minutes, daily, or never, to suit your trading style.

Normalized Oscillator: The CVD is scaled between -100 and +100, making it easier to visualize short-term momentum.

Live CVD Labels: Displays the raw CVD value on each candle, with options to position the label above or below the oscillator line.

How to Use

Add to Chart: Apply the indicator to your chart on a low timeframe (e.g., 1m, 5m, or 15m) for short-term trading.

Interpret the Oscillator:

Above 0 (Green): Indicates buying pressure dominates.

Below 0 (Red): Indicates selling pressure dominates.

Near 0: Suggests neutral market conditions.

Monitor Live CVD: Use the raw CVD value (shown in the label) to assess the exact net volume difference over the lookback period.

Combine with Other Tools: Use the oscillator alongside price action, support/resistance levels, or other indicators to confirm trading decisions.

Adjust Settings:

CVD Lookback Period: Set to a small value (e.g., 5-20 candles) for scalping.

CVD Reset Period: Choose "1m" or "5m" for intraday resets to focus on very short-term trends.

Volume Average Length: Use a short length (e.g., 3-5) for faster responsiveness.

Scale Factor: Increase (e.g., 2.0-3.0) to amplify small changes in CVD.

Settings

CVD Reset Period: Defines when to reset the CVD calculation ("None", "D" for daily, "15m", "5m", "1m").

CVD Lookback Period (Candles): Number of recent candles to calculate CVD (default: 10).

Volume Average Length: Period for averaging volume to normalize CVD (default: 5).

CVD Scale Factor: Adjusts the sensitivity of the normalized CVD (default: 2.0).

CVD Label Position: Choose to display the raw CVD label above or below the oscillator line.

CVD Label Color: Customize the color of the CVD label (default: white).

Limitations

Not a Standalone Tool: This indicator should be used in conjunction with other technical analysis tools, as it does not guarantee profitable trades.

Volume Dependency: The accuracy of CVD relies on the quality of volume data provided by your broker or exchange.

Short-Term Focus: The indicator is optimized for low timeframes and may produce noise on higher timeframes unless adjusted.

No Predictive Claims: The CVD Oscillator reflects past and current market activity but does not predict future price movements.

Notes

This indicator is designed for informational purposes and does not constitute financial advice. Trading involves risk, and past performance is not indicative of future results.

Test the indicator on a demo account to understand its behavior before using it in live trading.

Feedback is welcome! If you have suggestions for improvements, feel free to share them in the comments.

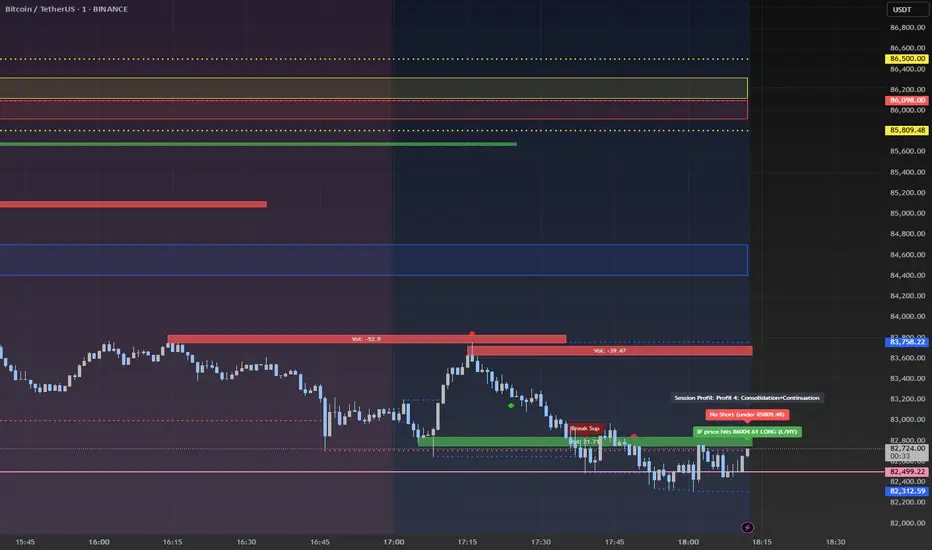

Advanced Session Profile Predictor with SR Boxes & ORAdvanced Session Profile Predictor with Momentum Arrows

Designed for intraday traders, this indicator analyzes price action across Asia, London, and New York sessions to predict market profiles and highlight key trading opportunities. By combining session-based profiling, Opening Range (OR) visualization, and momentum signals from Traders Dynamic Index (TDI), it offers a unique tool for anticipating trends, reversals, and breakouts. Ideal for forex, indices, and crypto on 15M–1H charts.

What Makes This Indicator Unique?

Unlike typical session indicators that only mark time zones or standard TDI scripts that focus on momentum, this tool:

Predicts market profiles (e.g., "Trend Continuation," "NY Manipulation") by analyzing session ranges and directional moves, offering actionable insights into how sessions interact.

Visualizes Opening Range (OR) boxes for the first 15 minutes of each session, helping traders spot early breakout levels.

Integrates TDI with momentum to generate precise bullish/bearish arrows, filtered by session context for improved reliability.

Simplifies decision-making with dynamic profile labels showing real-time long/short conditions based on price levels.

How Does It Work?

Session Tracking:

Asia (00:00–08:00 UTC, yellow), London (08:00–16:00 UTC, red), and New York (13:00–21:00 UTC, blue) sessions are highlighted with background colors and high/low lines (crosses).

OR boxes (first 15 minutes) are drawn for each session: yellow for Asia, red for London, blue for NY.

Profile Prediction:

Compares Asia and London session ranges and directions (e.g., trending if range > 1.5x 5-period SMA).

Examples:

Trend Continuation: Asia and London trend in the same direction—long above Asia high (uptrend) or short below Asia low (downtrend).

NY Manipulation: Asia trends, London consolidates—watch for NY breakouts at London high/low.

Displays the predicted profile and entry conditions in labels (e.g., "IF price hits 1.2000 LONG").

Momentum Arrows:

Uses TDI (RSI period 21, bands 34, fast MA 2) and 12-period momentum.

Green up arrow: Fast MA > upper band (>68) and momentum rising (bullish).

Red down arrow: Fast MA < lower band (<32) and momentum falling (bearish).

Support/Resistance (SR):