RMB - High and LowDescription:

Introducing the "RMB - High and Low" indicator, a versatile and powerful tool designed for traders who seek a comprehensive view of the market across multiple time frames. This indicator is tailored to identify and display key support and resistance levels, adapting to your chosen time frame - from as short as 15 minutes to as long as a week.

Key Features:

Multi-Time Frame Flexibility : Easily switch between 15 minutes, 30 minutes, 1 hour, 2 hours, 4 hours, daily, and weekly time frames to align with your trading strategy and market analysis.

Dynamic Support and Resistance Levels : The indicator plots the highest high (resistance) and the lowest low (support) for the selected time frame, providing real-time insights into market behavior and potential pivot points.

Time Frame-Specific Labels : Each resistance and support line is labeled with the corresponding time frame, offering a clear and immediate reference, enhancing your chart analysis and decision-making process.

User-Friendly Interface : A simple and intuitive input interface allows for quick adjustments, making it easy to toggle between different time frames based on your trading needs.

Visual Clarity : Designed with distinct color coding - green for resistance and red for support - ensuring that key levels are easily identifiable at a glance.

Ideal Use Cases:

Day Trading: Utilize shorter time frames to capture quick market movements and identify intraday pivot points.

Swing Trading: Leverage longer time frames to understand broader market trends and establish entry and exit points.

Diverse Strategies: Whether you're scalping, trend following, or employing mean reversion tactics, adapt the indicator to fit your unique approach.

Conclusion:

The "RMB - High and Low" indicator is a must-have tool for traders who demand flexibility and precision in their technical analysis. By offering insights across various time frames, this indicator empowers you to make well-informed decisions, adapt to market changes swiftly, and enhance your trading performance.

Cari dalam skrip untuk "机械革命无界15+时不时闪屏"

Stock WatchOverview

Watch list are very common in trading, but most of them simply provide the means of tracking a list of symbols and their current price. Then, you click through the list and perform some additional analysis individually from a chart setup. What this indicator is designed to do is provide a watch list that employs a high/low price range analysis in a table view across multiple time ranges for a much faster analysis of the symbols you are watching.

Discussion

The concept of this Stock Watch indicator is best understood when you think in terms of a 52 Week Range indication on many financial web sites. Taken a given symbol, what is the high and the low over a 52 week range and then determine where current price is within that range from a percentage perspective between 0% and 100%.

With this concept in mind, let's see how this Stock Watch indicator is meant to benefit.

There are four different H/L ranges relative to the chart's setting and a Scope property. Let's use a three month (3M) chart as our example and set the indicator's Scope = 4. A 3M chart provides three months of data in a single candle, now when we set the Scope = 4 we are stating that 1X is going to look over four candles for the high/low range.

The Scope property is used to determine how many candles it is to scan to determine the high/low range for the corresponding 1X, 3X, 5X and 10X periods. This is how different time ranges are put into perspective. Using a 3M chart with Scope = 4 would represent the following time windows:

- 1X = 3M * 4 is a 12 Months or 1 Year High/Low Range

- 3X = 3M * 4 * 3 is a 36 Months or 3 Years High/Low Range

- 5X = 3M * 4 * 5 is a 60 Months or 5 Years High/Low Range

- 10X = 3M * 4 * 10 is a 120 Months or 10 Years High/Low Range.

With these calculations, the indicator then determines where current price is within each of these High/Low ranges from a percentage perspective between 0% and 100%.

Once the 0% to 100% value is calculated, it then will shade the value according to a color gradient from red to green (or any other two colors you set the indictor to). This color shading really helps to interpret current price quickly.

The greater power to this range and color shading comes when you are able to see where price is according to price history across the multiple time windows. In this example, there is quick analysis across 1 Year, 3 Year, 5 Year and 10 Year windows.

Now let's further improve this quick analysis over 15 different stocks for which the indicator allows you to watch up to at any one time.

For value traders this is huge, because we're always looking for the bargains and we wait for price to be in the value range. Using this indicator helps to instantly see if price has entered a value range before we decide to do further analysis with other charting and fundamental tools.

The Code

The heart of all this is really very simple as you can see in the following code snippet. We're simply looking for the highest high and lowest low across the different scopes and calculating the percentage of the range where current price is for each symbol being watched.

scope = baseScope

watch1X = math.round(((watchClose - ta.lowest(watchLow, scope)) / (ta.highest(watchHigh, scope) - ta.lowest(watchLow, scope))) * 100, 0)

table.cell(tblWatch, columnId, 2, str.format("{0, number, #}%", watch1X), text_size = size.small, text_color = colorText, bgcolor = getBackColor(watch1X))

//3X Lookback

scope := baseScope * 3

watch3X = math.round(((watchClose - ta.lowest(watchLow, scope)) / (ta.highest(watchHigh, scope) - ta.lowest(watchLow, scope))) * 100, 0)

table.cell(tblWatch, columnId, 3, str.format("{0, number, #}%", watch3X), text_size = size.small, text_color = colorText, bgcolor = getBackColor(watch3X))

Conclusion

The example I've laid out here are for large time windows, because I'm a long term investor. However, keep in mind that this can work on any chart setting, you just need to remember that your chart's time period and scope work together to determine what 1X, 3X, 5X and 10X represent.

Let me try and give you one last scenario on this. Consider your chart is set for a 60 minute chart, meaning each candle represents 60 minutes of time and you set the Stock Watch indicator to a scope = 4. These settings would now represent the following and you would be watching up to 15 different stocks across these windows at one time.

1X = 60 minutes * 4 is 240 minutes or 4 hours of time.

3X = 60 minutes * 4 * 3 = 720 minutes or 12 hours of time.

5X = 60 minutes * 4 * 5 = 1200 minutes or 20 hours of time.

10X = 60 minutes * 4 * 10 = 2400 minutes or 40 hours of time.

I hope you find value in my contribution to the cause of trading, and if you have any comments or critiques, I would love to here from you in the comments.

Back Week For BacktestIt is Backtest Calculator For Essential and Plus plan holders, the length of available intraday data is calculated as follows: from now to 6 weeks back multiplied by timeframe(in minutes), i.e. you can go 6 weeks back on the 1-minute chart, 12 weeks back on the 2-minute chart, 30 weeks back on the 5-minute chart, 90 weeks back on the 15-minute chart and so on. The higher timeframe is selected, the more intraday data is available.

This show creates a weekday label based on the data in the plans allowed by TradingView. This show creates a weekday label based on the data in the plans allowed by TradingView. How much data is available for Bar Replay? According to the article, we can replay 6 weeks backwards for a 1-minute chart. This indicator is a label that shows how far we can go back, consisting of multiplying each minute by 6 between 1 minute and 60 minutes.

1 minute => 6 week backtest

2 minutes => 12 week backtest

.....

15 minutes => 90 week backtest

...

59 minutes => 354 week backtest

G2RIntroducing G2R – The Universal Indicator! Unlock the secret to trading success with G2R an extraordinary indicator that provides automatic signals across every time frame and market, from forex, crypto, stocks, & options with over 80% signal accuracy. Say goodbye to guesswork and hello to precision as G2R empowers you with real-time insights , giving you the edge to seize opportunities in any market condition . Elevate your trading strategy and conquer the financial world with G2R – your ultimate guide to profitable trading!

Features

• Bollinger bands

• 2 exponential moving averages

• Automatic buy and sell signals

• Works for Forex, Crypto, Indices, Stocks, & Options

• Tailored for all Timeframes

Trading Tips

• Trading Signals

• 30 Secs - 1 Min | SCALPING

• 3 Min - 5 Min | DAY TRADING

• 15 Min - 1 Hr | SWING & POSITION

• Take signal trades during London, New York, & Asia sessions

• Take Profits are found on the 15 Min, 30 Min, & 1 Hr timeframe at the trend channel or Moving Averages

• Stop loss are found above or below trend channel or moving averages

Warning

Never blindly take a trade on a G2R - wait for a proper market structure to occur before considering a trade.

Tennis Ball ActionInspired by Mark Minervini's sell rules in "Think and Trade Like a Champion".

Used to determine if a stock is behaving well after a breakout

Used to determine when it might by prudent to reduce a position or sell

Used as a visual aid, but based purely off price and volume action

Here's a breakdown of what each condition checks for:

Up Close Counter: Checks for a sequence of upward closes. If there are 12 or more up closes in the last 15 days, it flags up_days as true.

Upper 50% Range Condition: Determines if 9 or more out of the last 15 closes are in the upper 50% of the price range.

Bullish Engulfing: Identifies a bullish engulfing candlestick pattern where the close is higher than the previous high and the open is lower than the previous low.

Stock Up 3% or More: Flags when the stock is up 3% or more on the day.

Inside Day Condition: Checks if the current day's high is lower than the previous day's high and the current day's low is higher than the previous day's low.

Close Below 50-day SMA: Indicates a negative confirmation when the stock closes below the 50-day Simple Moving Average (SMA).

Weak Close Condition: Similar to the Upper 50% Range Condition, but looking for lower closes.

Close Below 20-day SMA: Another negative confirmation when the stock closes below the 20-day SMA.

Three Lower Lows: Identifies a pattern where the current close is lower than the previous two closes.

Down on Above Average Volume: Flags when the stock closes lower than the previous day's close and the volume is higher than the 20-day SMA of volume.

The script then tallies up the confirmations and violations based on these conditions and plots them on a histogram. Confirmations are represented in green, violations in red.

This indicator evaluates both bullish and bearish signals based on various technical conditions to assist traders in decision-making. The confirmations suggest potential bullish movements, while violations indicate potential bearish movements in the stock.

Optimal Length BackTester [YinYangAlgorithms]This Indicator allows for a ‘Optimal Length’ to be inputted within the Settings as a Source. Unlike most Indicators and/or Strategies that rely on either Static Lengths or Internal calculations for the length, this Indicator relies on the Length being derived from an external Indicator in the form of a Source Input.

This may not sound like much, but this application may allows limitless implementations of such an idea. By allowing the input of a Length within a Source Setting you may have an ‘Optimal Length’ that adjusts automatically without the need for manual intervention. This may allow for Traditional and Non-Traditional Indicators and/or Strategies to allow modifications within their settings as well to accommodate the idea of this ‘Optimal Length’ model to create an Indicator and/or Strategy that adjusts its length based on the top performing Length within the current Market Conditions.

This specific Indicator aims to allow backtesting with an ‘Optimal Length’ inputted as a ‘Source’ within the Settings.

This ‘Optimal Length’ may be used to display and potentially optimize multiple different Traditional Indicators within this BackTester. The following Traditional Indicators are included and available to be backtested with an ‘Optimal Length’ inputted as a Source in the Settings:

Moving Average; expressed as either a: Simple Moving Average, Exponential Moving Average or Volume Weighted Moving Average

Bollinger Bands; expressed based on the Moving Average Type

Donchian Channels; expressed based on the Moving Average Type

Envelopes; expressed based on the Moving Average Type

Envelopes Adjusted; expressed based on the Moving Average Type

All of these Traditional Indicators likewise may be displayed with multiple ‘Optimal Lengths’. They have the ability for multiple different ‘Optimal Lengths’ to be inputted and displayed, such as:

Fast Optimal Length

Slow Optimal Length

Neutral Optimal Length

By allowing for the input of multiple different ‘Optimal Lengths’ we may express the ‘Optimal Movement’ of such an expressed Indicator based on different Time Frames and potentially also movement based on Fast, Slow and Neutral (Inclusive) Lengths.

This in general is a simple Indicator that simply allows for the input of multiple different varieties of ‘Optimal Lengths’ to be displayed in different ways using Tradition Indicators. However, the idea and model of accepting a Length as a Source is unique and may be adopted in many different forms and endless ideas.

Tutorial:

You may add an ‘Optimal Length’ within the Settings as a ‘Source’ as followed in the example above. This Indicator allows for the input of a:

Neutral ‘Optimal Length’

Fast ‘Optimal Length’

Slow ‘Optimal Length’

It is important to account for all three as they generally encompass different min/max length values and therefore result in varying ‘Optimal Length’s’.

For instance, say you’re calculating the ‘Optimal Length’ and you use:

Min: 1

Max: 400

This would therefore be scanning for 400 (inclusive) lengths.

As a general way of calculating you may assume the following for which lengths are being used within an ‘Optimal Length’ calculation:

Fast: 1 - 199

Slow: 200 - 400

Neutral: 1 - 400

This allows for the calculation of a Fast and Slow length within the predetermined lengths allotted. However, it likewise allows for a Neutral length which is inclusive to all lengths alloted and may be deemed the ‘Most Accurate’ for these reasons. However, just because the Neutral is inclusive to all lengths, doesn’t mean the Fast and Slow lengths are irrelevant. The Fast and Slow length inputs may be useful for seeing how specifically zoned lengths may fair, and likewise when they cross over and/or under the Neutral ‘Optimal Length’.

This Indicator features the ability to display multiple different types of Traditional Indicators within the ‘Display Type’.

We will go over all of the different ‘Display Types’ with examples on how using a Fast, Slow and Neutral length would impact it:

Simple Moving Average:

In this example above have the Fast, Slow and Neutral Optimal Length formatted as a Slow Moving Average. The first example is on the 15 minute Time Frame and the second is on the 1 Day Time Frame, demonstrating how the length changes based on the Time Frame and the effects it may have.

Here we can see that by inputting ‘Optimal Lengths’ as a Simple Moving Average we may see moving averages that change over time with their ‘Optimal Lengths’. These lengths may help identify Support and/or Resistance locations. By using an 'Optimal Length' rather than a static length, we may create a Moving Average which may be more accurate as it attempts to be adaptive to current Market Conditions.

Bollinger Bands:

Bollinger Bands are a way to see a Simple Moving Average (SMA) that then uses Standard Deviation to identify how much deviation has occurred. This Deviation is then Added and Subtracted from the SMA to create the Bollinger Bands which help Identify possible movement zones that are ‘within range’. This may mean that the price may face Support / Resistance when it reaches the Outer / Inner bounds of the Bollinger Bands. Likewise, it may mean the Price is ‘Overbought’ when outside and above or ‘Underbought’ when outside and below the Bollinger Bands.

By applying All 3 different types of Optimal Lengths towards a Traditional Bollinger Band calculation we may hope to see different ranges of Bollinger Bands and how different lookback lengths may imply possible movement ranges on both a Short Term, Long Term and Neutral perspective. By seeing these possible ranges you may have the ability to identify more levels of Support and Resistance over different lengths and Trading Styles.

Donchian Channels:

Above you’ll see two examples of Machine Learning: Optimal Length applied to Donchian Channels. These are displayed with both the 15 Minute Time Frame and the 1 Day Time Frame.

Donchian Channels are a way of seeing potential Support and Resistance within a given lookback length. They are a way of withholding the High’s and Low’s of a specific lookback length and looking for deviation within this length. By applying a Fast, Slow and Neutral Machine Learning: Optimal Length to these Donchian Channels way may hope to achieve a viable range of High’s and Low’s that one may use to Identify Support and Resistance locations for different ranges of Optimal Lengths and likewise potentially different Trading Strategies.

Envelopes / Envelopes Adjusted:

Envelopes are an interesting one in the sense that they both may be perceived as useful; however we deem that with the use of an ‘Optimal Length’ that the ‘Envelopes Adjusted’ may work best. We will start with examples of the Traditional Envelope then showcase the Adjusted version.

Envelopes:

As you may see, a Traditional form of Envelopes even produced with a Machine Learning: Optimal Length may not produce optimal results. Unfortunately this may occur with some Traditional Indicators and they may need some adjustments as you’ll notice with the ‘Envelopes Adjusted’ version. However, even without the adjustments, these Envelopes may be useful for seeing ‘Overbought’ and ‘Oversold’ locations within a Machine Learning: Optimal Length standpoint.

Envelopes Adjusted:

By adding an adjustment to these Envelopes, we may hope to better reflect our Optimal Length within it. This is caused by adding a ratio reflection towards the current length of the Optimal Length and the max Length used. This allows for the Fast and Neutral (and potentially Slow if Neutral is greater) to achieve a potentially more accurate result.

Envelopes, much like Bollinger Bands are a way of seeing potential movement zones along with potential Support and Resistance. However, unlike Bollinger Bands which are based on Standard Deviation, Envelopes are based on percentages +/- from the Simple Moving Average.

We will conclude our Tutorial here. Hopefully this has given you some insight into how useful adding a ‘Optimal Length’ within an external (secondary) Indicator as a Source within the Settings may be. Likewise, how useful it may be for automation sake in the sense that when the ‘Optimal Length’ changes, it doesn’t rely on an alert where you need to manually update it yourself; instead it will update Automatically and you may reap the benefits of such with little manual input needed (aside from the initial setup).

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

savitzkyGolay, KAMA, HPOverview

This trading indicator integrates three distinct analytical tools: the Savitzky-Golay Filter, Kaufman Adaptive Moving Average (KAMA), and Hodrick-Prescott (HP) Filter. It is designed to provide a comprehensive analysis of market trends and potential trading signals.

Components

Hodrick-Prescott (HP) Filter

Purpose: Smooths out the price data to identify the underlying trend.

Parameters: Lambda: Controls the smoothness. Range: 50 to 1600.

Impact of Parameters:

Increasing Lambda: This makes the trend line more responsive to short-term market fluctuations, suitable for short-term analysis. A higher Lambda value decreases the degree of smoothing, making the trend line follow recent market movements more closely.

Decreasing Lambda: A lower Lambda value makes the trend line smoother and less responsive to short-term market fluctuations, ideal for longer-term trend analysis. Decreasing Lambda increases the degree of smoothing, thereby filtering out minor market movements and focusing more on the long-term trend.

Kaufman Adaptive Moving Average (KAMA):

Purpose: An adaptive moving average that adjusts to price volatility.

Parameters: Length, Fast Length, Slow Length: Define the sensitivity and adaptiveness of KAMA.

Impact of Parameters:

Adjusting Length affects the base period for efficiency ratio, altering the overall sensitivity.

Fast Length and Slow Length control the speed of KAMA’s adaptation. A smaller Fast Length makes KAMA more sensitive to price changes, while a larger Slow Length makes it less sensitive.

Savitzky-Golay Filter:

Purpose: Smooths the price data using polynomial regression.

Parameters: Window Size: Determines the size of the moving window (7, 9, 11, 15, 21).

Impact of Parameters:

A larger Window Size results in a smoother curve, which is more effective for identifying long-term trends but can delay reaction to recent market changes.

A smaller Window Size makes the curve more responsive to short-term price movements, suitable for short-term trading strategies.

General Impact of Parameters

Adjusting these parameters can significantly alter the signals generated by the indicator. Users should fine-tune these settings based on their trading style, the characteristics of the traded asset, and market conditions to optimize the indicator's performance.

Signal Logic

Buy Signal: The trend from the HP filter is below both the KAMA and the Savitzky-Golay SMA, and none of these indicators are flat.

Sell Signal: The trend from the HP filter is above both the KAMA and the Savitzky-Golay SMA, and none of these indicators are flat.

Usage

Due to the combination of smoothing algorithms and adaptability, this indicator is highly effective at identifying emerging trends for both initiating long and short positions.

IMPORTANT : Although the code and user settings incorporate measures to limit false signals due to lateral (sideways) movement, they do not completely eliminate such occurrences. Users are strongly advised to avoid signals that emerge during simultaneous lateral movements of all three indicators.

Despite the indicator's success in historical data analysis using its signals alone, it is highly recommended to use this code in combination with other indicators, patterns, and zones. This is particularly important for determining exit points from positions, which can significantly enhance trading results.

Limitations and Recommendations

The indicator has shown excellent performance on the weekly time frame (TF) with the following settings:

Savitzky-Golay (SG): 11

Hodrick-Prescott (HP): 100

Kaufman Adaptive Moving Average (KAMA): 20, 2, 30

For the monthly TF, the recommended settings are:

SG: 15

HP: 100

KAMA: 30, 2, 35

Note: The monthly TF is quite variable. With these settings, there may be fewer signals, but they tend to be more relevant for long-term investors. Based on a sample of 40 different stocks from various countries and sectors, most exhibited an average trade return in the thousands of percent.

It's important to note that while these settings have been successful in past performance, market conditions vary and past performance is not indicative of future results. Users are encouraged to experiment with these settings and adjust them according to their individual needs and market analysis.

As this is my first developed trading indicator, I am very open to and appreciative of any suggestions or comments. Your feedback is invaluable in helping me refine and improve this tool. Please feel free to share your experiences, insights, or any recommendations you may have.

Breakout Detector (Previous MTF High Low Levels) [LuxAlgo]The Breakout Detector (Previous MTF High Low Levels) indicator highlights breakouts of previous high/low levels from a higher timeframe.

The indicator is able to: display take-profit/stop-loss levels based on a user selected Win/Loss ratio, detect false breakouts, and display a dashboard with various useful statistics.

Do note that previous high/low levels are subject to backpainting, that is they are drawn retrospectively in their corresponding location. Other elements in the script are not subject to backpainting.

🔶 USAGE

Breakouts occur when the price closes above a previous Higher Timeframe (HTF) High or below a previous HTF Low.

On the advent of a breakout, the closing price acts as an entry level at which a Take Profit (TP) and Stop Loss (SL) are placed. When a TP or SL level is reached, the SL/TP box border is highlighted.

When there is a breakout in the opposite direction of an active breakout, previous breakout levels stop being updated. Not reaching an SL/TP level will result in a partial loss/win,

which will result in the box being highlighted with a dotted border (default). This can also be set as a dashed or solid border.

Detection of False Breakouts (default on) can be helpful to avoid false positives, these can also be indicative of potential trend reversals.

This indicator contains visualization when a new HTF interval begins (thick vertical grey line) and a dashboard for reviewing the breakout results (both defaults enabled; and can be disabled).

As seen in the example above, the active, open breakout is colored green/red.

You can enable the setting ' Cancel TP/SL at the end of HTF ', which will stop updating previous TP/SL levels on the occurrence of a new HTF interval.

🔶 DETAILS

🔹 Principles

Every time a new timeframe period starts, the previous high and low are detected of the higher timeframe. On that bar only there won't be a breakout detection.

A breakout is confirmed when the close price breaks the previous HTF high/low

A breakout in the same direction as the active breakout is ignored.

A breakout in the opposite direction stops previous breakout levels from being updated.

Take Profit/Stop Loss, partially or not, will be highlighted in an easily interpretable manner.

🔹 Set Higher Timeframe

There are 2 options for choosing a higher timeframe:

• Choose a specific higher timeframe (in this example, Weekly higher TF on a 4h chart)

• Choose a multiple of the current timeframe (in this example, 75 minutes TF on a 15 min chart - 15 x 5)

Do mind, that when using this option, non-standard TFs can give less desired timeframe changes.

🔹 Setting Win/Loss Levels

The Stop Loss (SL) / Take Profit (TP) setting has 2 options:

W%:L% : A fixed percentage is chosen, for TP and SL.

W:L : In this case L (Loss-part) is set through Loss Settings , W (Win-part) is calculated by multiplying L , for example W : L = 2 : 1, W will be twice as large as the L .

🔹 Loss Settings

The last drawing at the right is still active (colored green/red)

The Loss part can be:

A multiple of the Average True Range (ATR) of the last 200 bars.

A multiple of the Range Cumulative Mean (RCM).

The Latest Swing (with Length setting)

Range Cumulative Mean is the sum of the Candle Range (high - low) divided by its bar index.

🔹 False Breakouts

A False Breakout is confirmed when the price of the bar immediately after the breakout bar returns above/below the breakout level.

🔹 Dashboard

🔶 ALERTS

This publication provides several alerts

Bullish/Bearish Breakout: A new Breakout.

Bullish/Bearish False Breakout: False Breakout detected, 1 bar after the Breakout.

Bullish/Bearish TP: When the TP/profit level has been reached.

Bullish/Bearish Fail: When the SL/stop-loss level has been reached.

Note that when a new Breakout causes the previous Breakout to stop being updated, only an alert is provided of the new Breakout.

🔶 SETTINGS

🔹 Set Higher Timeframe

Option : HTF/Mult

HTF : When HTF is chosen as Option , set the Higher Timeframe (higher than current TF)

Mult : When Mult is chosen as Option , set the multiple of current TF (for example 3, curr. TF 15min -> 45min)

🔹 Set Win/Loss Level

SL/TP : W:L or W%:L%: Set the Win/Loss Ratio (Take Profit/Stop Loss)

• W : L : Set the Ratio of Win (TP) against Loss (SL) . The L level is set at Loss Settings

• W% : L% : Set a fixed percentage of breakout price as SL/TP

🔹 Loss Settings

When W : L is chosen as SL/TP Option, this sets the Loss part (L)

Base :

• RCM : Range Cumulative Mean

• ATR : Average True Range of last 200 bars

• Last Swing : Last Swing Low when bullish breakout, last Swing High when bearish breakout

Multiple : x times RCM/ATR

Swing Length : Sets the 'left' period ('right' period is always 1)

Colours : colour of TP/SL box and border

Borders : Style border when breakout levels stop being updated, but TP/SL is not reached. (Default dotted dot , other option is dashed dsh or solid sol )

🔹 Extra

Show Timeframe Change : Show a grey vertical line when a new Higher Timeframe interval begins

Detect False Outbreak

Cancel TP/SL at end of HTF

🔹 Show Dashboard

Location: Location of the dashboard (Top Right or Bottom Right/Left)

Size: Text size (Tiny, Small, Normal)

See USAGE/DETAILS for more information

Vwap MTFExplanatory Note: VWAP Multi-Timeframe Script (Dedicated to Intraday Trading)

Description:

This Pine script has been specifically designed for intraday traders to display the VWAP (Volume Weighted Average Price) from four different timeframes (15 minutes, 1 hour, 4 hours, and daily) on a single TradingView chart. The VWAP is calculated by considering the volume-weighted average price over a specified period, providing a perspective on the market's average value. This script streamlines your analysis by avoiding the need to navigate through multiple timeframes to identify the trend.

Usage Instructions:

Apply the script to your TradingView chart.

The script will showcase the average VWAP for 15 minutes, 1 hour, 4 hours, and daily on the current chart.

The color of the VWAP indicates the direction: blue if the VWAP is higher than the previous period, red otherwise.

Parameters:

VWAP Period Length (length): The length of the period used for VWAP calculation. By default, the length is set to 30 bars.

Explanation of VWAP: "This VWAP will be more precise for your analysis and closer to price/volume."

VWAP is a crucial indicator for intraday traders, taking into account transaction volume. It provides a volume-weighted average price over a specified period, assisting traders in evaluating the average value at which an asset has been traded throughout the day. "It can be wise for the self-directed investor to use VWAP in combination with moving averages or other technical indicators to confirm buy and sell signals."

You have the option to change the colors.

Anticipated Profit Targets (APT)Anticipated Profit Targets (APT)

Purpose:

The Anticipated Profit Targets script is a specialized tool designed to assist traders in visualizing potential exit points for their trades. This is achieved by leveraging the Average True Range (ATR), a renowned measure of market volatility.

How It Works:

ATR Computations: At its core, the script calculates the ATR based on a user-defined number of periods. The ATR captures the range between the high and low prices of an asset over a specific duration, providing a snapshot of its volatility.

Multiplier Application: To fine-tune the profit targets, the ATR is multiplied by a user-defined multiplier. This step adjusts the ATR value, setting the profit targets at a distance from the current price, thus accounting for potential price movements.

Adaptable Timeframes: One of the standout features of this script is its adaptability. Users can select their desired timeframe for the profit target calculations. This flexibility means that a trader can be on a 15-minute chart but visualize profit targets based on the volatility of a 1-hour chart.

Visual Representation: The calculated profit targets are then overlaid onto the current chart. This visual aid provides traders with a clear perspective of potential exit points in relation to ongoing price movements.

Originality and Usefulness:

While the concept of using ATR for setting profit targets isn't new, this script's adaptability across timeframes and its user-centric customization options make it a unique offering. The combination of ATR with dynamic multipliers and timeframe adaptability ensures that traders get a tool tailored to their specific needs, rather than a one-size-fits-all solution.

Usage Guidelines:

After adding the script to the chart, traders can adjust the input parameters to their preferences. The anticipated profit targets will then be displayed, offering potential exit points. It's recommended to use these targets in conjunction with other technical indicators and chart patterns for a holistic trading strategy.

Features:

ATR Periods: The ATR is calculated using a user-defined number of periods. By default, it's set to 14 periods, a standard setting. The ATR gauges the asset's volatility, and adjusting the periods can increase or decrease its sensitivity to recent price fluctuations.

ATR Multiplier: The ATR is multiplied by a user-defined factor to determine the profit targets. With a default multiplier of 1.5, the profit target will be positioned 1.5 times the ATR above (for bullish trades) or below (for bearish trades) the current price.

Target Timeframe: Traders can choose the timeframe for which the profit targets are calculated. This feature enables viewing of profit targets from higher timeframes on the current chart. For instance, while observing a 15-minute chart, one can see the 1-hour profit targets.

Visual Indicators:

1. Two lines are plotted: the bullish target (in green) and the bearish target (in red).

2. At the onset of each new candle in the selected higher timeframe, labels indicating the precise profit target values are displayed.

3. Price scale labels also showcase the profit targets, offering a quick reference for potential exit points.

Customization:

Traders can modify the following parameters:

1. ATR Periods: Adjusting the number of periods can refine the ATR's sensitivity to price changes.

2. Multiplier for ATR: Tweaking this value alters the distance between the profit targets and the current price.

3. Timeframe for Profit Targets: A variety of timeframes are available, granting flexibility in viewing profit targets.

How to Use:

After integrating the script into their chart, traders can modify the input parameters as desired. The anticipated profit targets will then be overlaid on the chart, offering potential exit points. When used alongside other technical indicators and chart patterns, this tool can enhance trading decision-making.

Note: This script is designed for educational purposes and should not be considered as financial advice. Always conduct your own research and consult with a financial advisor before making any trading decisions.

ES S/R LevelsThis script plots support and resistance levels for /ES on your chart.

This script only works on the /ES symbol in Tradingview due to the string manipulation of the levels.

You can input support and resistance levels in the inputs.

The example format of S/R levels should be in the following form (comma-separated)

If the level is a single point, it will draw a line. If the level is a range, it will draw a box.

4260, 4267, 4275, 4283, 4289, 4297-4300, 4310-15, 4325-30

You can also add the keyword (major) in your S/R levels input which will add a (Major) label to the drawing

4260, 4267 (major), 4275, 4283, 4289, 4297-4300 (major), 4310-15, 4325-30

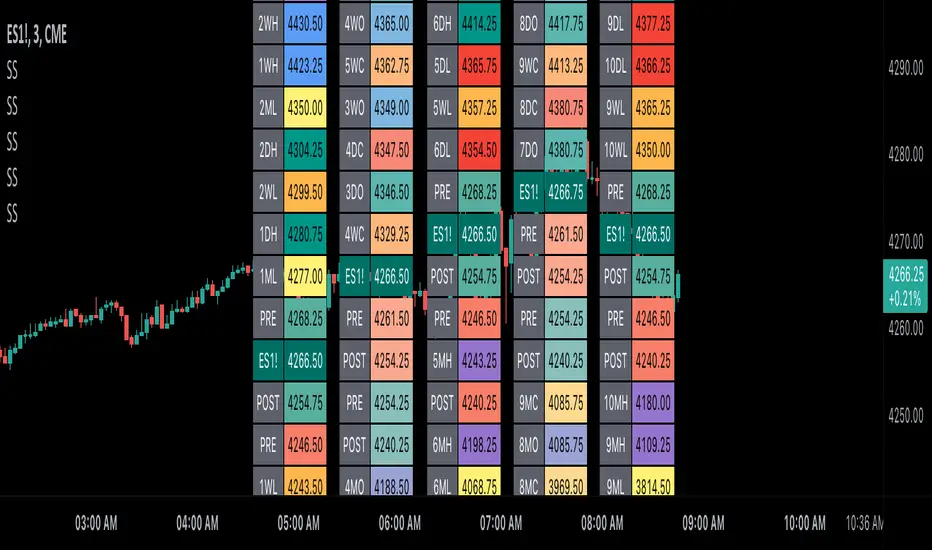

Scoopy StacksWaffle Around Multiple

(Open, High, Low, Close) Stacks On

Pre/Post Market & (Daily, Weekly,

Monthly, Yearly) Sessions With

Meticulous Columns, Rows, Tooltips,

Colors, Custom Ideas, and Alerts.

Sessions Use Two Step Incremental Values

Default Value: (1) Shows Two Previous

(O, H, L, C); Increasing Value Swaps

Sessions With Next Two Stacks.

⬛️ KEY WORDS:

🟢 Crossover | 🔴 Crossunder

📗 High | 📕 Low

📔 Open | 📓 Close

🥇 First Idea | 🥈 Second Idea

🥉 Third Idea | 🎖️ Fourth Idea

🟥 ALERTS:

Default Option: (Per Bar)

Alerts Once Conditions Are Met

(Bar Close) Alerts When Bar Closes

Default Option: (Reg)

Alerts During Regular Market

Trading Hours, (0930-1600)

(Ext) Alerts During Extended

Market Hours, (1600-0930)

(24/7) Alerts All Day

Optional Preferences:

Regular Alerts - Stocks

Extended Alerts - Futures

24/7 Alerts - Crypto

🟧 STACKS:

Default Value: (1)

Incremental Stack Value, Increasing Value

Swaps Sessions With the Next Two Stacks

(✓) Swap Stacks?

Pre/Post Market High/Lows,

1-2 Day High/Lows, 1-2 Week High/Lows,

1-2 Month High/Lows, 1-2 Year High/Lows

( ) Swap Stacks?

Pre/Post Market Open/Close,

1-2 Day Open/Close, 1-2 Week Open/Close,

1-2 Month Open/Close, 1-2 Year Open/Close

🟨 EXAMPLES:

Default Stack:

🟢 | 📗 Pre Market High (PRE) | 4600.00

🔴 | 📕 Post Market Low (POST) | 420.00

Optional: (Open)

🟢 | 📔 Post Market Open (POST) | 4400.00

Optional: (Close)

🔴 | 📓 Pre Market Close (PRE) | 430.00

Default Stack Value: (1)

🔴 | 📗 1 Day High (1DH) | 460.00

Next Stack Value: (3)

🟢 | 📕 4 Day Low (4DL) | 420.00

Optional: (Open)

🔴 | 📔 2 Day Open (2DO) | 440.00

Optional: (Close)

🟢 | 📓 3 Day Close (3DC) | 430.00

Default Stack Value: (5)

🟢 | 📗 5 Week High (5WH) | 460.00

Next Stack Value: (7)

🔴 | 📕 8 Week Low (8WL) | 420.00

Optional: (Open)

🔴 | 📔 7 Week Open (7WO) | 4400.00

Optional: (Close)

🟢 | 📓 6 Week Close (6WC) | 430.00

Default Stack Value: (9)

🔴 | 📗 9 Month High (9MH) | 460.00

Next Stack Value: (11)

🟢 | 📕 12 Month Low (12ML) | 420.00

Optional: (Open)

🟢 | 📔 11 Month Open (11MO) | 4400.00

Optional: (Close)

🔴 | 📓 10 Month Close (10MC) | 430.00

Default Stack Value: (13)

🟢 | 📗 13 Year High (13YH) | 460.00

Next Stack Value: (15)

🟢 | 📕 16 Year Low (16YL) | 420.00

Optional: (Open)

🔴 | 📔 15 Year Open (15YO) | 4400.00

Optional: (Close)

🔴 | 📓 14 Year Close (14YC) | 430.00

🟩 TABLES:

Default Value: (1)

Moves Table Up, Down, Left, or Right

Based on Second Default Value

First Default Value: (Top Right)

Sets Table Placement, Middle Center

Allows Table To Move In All Directions

Second Default Value: (Default)

Fixed Table Position, Switching Values

Moves Direction of the Table

🟦 IDEAS:

(✓) Show Ideas?

Shows Four Ideas With Custom Texts

and Values; Ideas Are Based Around

Post-It Note Reminders with Alerts

Suggestions For Text Ideas:

Take Profit, Stop Loss, Trim, Hold,

Long, Short, Bounce Spot, Retest,

Chop, Support, Resistance, Buy, Sell

🟪 EXAMPLES:

Default Value: (5)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥇)

Shown On First Table Cell and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥇 | 5.00

Default Value: (10)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥈)

Shown On Second Table Cell and

Message Appearing On Alerts

Alert Shows: 🔴 | 🥈 | 10.00

Default Value: (50)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥉)

Shown On Third Table Cell and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥉 | 50.00

Default Value: (100)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🎖️)

Shown On Fourth Table Cell and

Message Appearing On Alerts

Alert Shows: 🔴 | 🎖️ | 100.00

⬛️ REFERENCES:

Pre-market Highs & Lows on regular

trading hours (RTH) chart

By Twingall

Previous Day Week Highs & Lows

By Sbtnc

Screener for 40+ instruments

By QuantNomad

Daily Weekly Monthly Yearly Opens

By Meliksah55

Ribbit RangesBounce Around Multiple

(Open, High, Low, Close) Ranges

On Pre/Post Market & (Daily, Weekly,

Monthly, Yearly) Sessions With

Meticulous Lines, Labels, Tooltips,

Colors, Custom Ideas, and Alerts.

Sessions Use Two Step Incremental Values

Default Value: (1) Shows Two Previous

(O, H, L, C); Increasing Value Swaps

Sessions With Next Two Ranges.

⬛️ KEY WORDS:

🟢 Crossover | 🔴 Crossunder

📗 High | 📕 Low

📔 Open | 📓 Close

🥇 First Idea | 🥈 Second Idea

🥉 Third Idea | 🎖️ Fourth Idea

🟥 ALERTS:

Default Option: (Per Bar)

Alerts Once Conditions Are Met

(Bar Close) Alerts When Bar Closes

Default Option: (Reg)

Alerts During Regular Market

Trading Hours, (0930-1600)

(Ext) Alerts During Extended

Market Hours, (1600-0930)

(24/7) Alerts All Day

Optional Preferences:

Regular Alerts - Stocks

Extended Alerts - Futures

24/7 Alerts - Crypto

🟧 RANGES:

Default Value: (1)

Incremental Range Value, Increasing Value

Swaps Sessions With the Next Two Ranges

(✓) Swap Ranges?

Pre/Post Market High/Lows,

1-2 Day High/Lows, 1-2 Week High/Lows,

1-2 Month High/Lows, 1-2 Year High/Lows

( ) Swap Ranges?

Pre/Post Market Open/Close,

1-2 Day Open/Close, 1-2 Week Open/Close,

1-2 Month Open/Close, 1-2 Year Open/Close

🟨 EXAMPLES:

Default Range:

🟢 | 📗 Pre Market High (PRE) | 4600.00

🔴 | 📕 Post Market Low (POST) | 420.00

Optional: (Open)

🟢 | 📔 Post Market Open (POST) | 4400.00

Optional: (Close)

🔴 | 📓 Pre Market Close (PRE) | 430.00

Default Range Value: (1)

🔴 | 📗 1 Day High (1DH) | 460.00

Next Range Value: (3)

🟢 | 📕 4 Day Low (4DL) | 420.00

Optional: (Open)

🔴 | 📔 2 Day Open (2DO) | 440.00

Optional: (Close)

🟢 | 📓 3 Day Close (3DC) | 430.00

Default Range Value: (5)

🟢 | 📗 5 Week High (5WH) | 460.00

Next Range Value: (7)

🔴 | 📕 8 Week Low (8WL) | 420.00

Optional: (Open)

🔴 | 📔 7 Week Open (7WO) | 4400.00

Optional: (Close)

🟢 | 📓 6 Week Close (6WC) | 430.00

Default Range Value: (9)

🔴 | 📗 9 Month High (9MH) | 460.00

Next Range Value: (11)

🟢 | 📕 12 Month Low (12ML) | 420.00

Optional: (Open)

🟢 | 📔 11 Month Open (11MO) | 4400.00

Optional: (Close)

🔴 | 📓 10 Month Close (10MC) | 430.00

Default Range Value: (13)

🟢 | 📗 13 Year High (13YH) | 460.00

Next Range Value: (15)

🟢 | 📕 16 Year Low (16YL) | 420.00

Optional: (Open)

🔴 | 📔 15 Year Open (15YO) | 4400.00

Optional: (Close)

🔴 | 📓 14 Year Close (14YC) | 430.00

🟩 COLORS:

(✓) Swap Colors?

Text Color Is Shown Using

Background Color

( ) Swap Colors?

Background Color Is Shown

Using Text Color

🟦 IDEAS:

(✓) Show Ideas?

Plots Four Ideas With Custom Lines

and Labels; Ideas Are Based Around

Post-It Note Reminders with Alerts

Suggestions For Text Ideas:

Take Profit, Stop Loss, Trim, Hold,

Long, Short, Bounce Spot, Retest,

Chop, Support, Resistance, Buy, Sell

🟪 EXAMPLES:

Default Value: (5)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🥇)

Shown On First Label and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥇 | 5.00

Default Value: (10)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🥈)

Shown On Second Label and

Message Appearing On Alerts

Alert Shows: 🔴 | 🥈 | 10.00

Default Value: (50)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🥉)

Shown On Third Label and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥉 | 50.00

Default Value: (100)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🎖️)

Shown On Fourth Label and

Message Appearing On Alerts

Alert Shows: 🔴 | 🎖️ | 100.00

⬛️ REFERENCES:

Pre-market Highs & Lows on regular

trading hours (RTH) chart

By Twingall

Previous Day Week Highs & Lows

By Sbtnc

Screener for 40+ instruments

By QuantNomad

Daily Weekly Monthly Yearly Opens

By Meliksah55

TradingView.To Strategy Template (with Dyanmic Alerts)Hello traders,

If you're tired of manual trading and looking for a solid strategy template to pair with your indicators, look no further.

This Pine Script v5 strategy template is engineered for maximum customization and risk management.

Best part?

This Pine Script v5 template facilitates the dynamic construction of TradingView.TO alerts, sparing users the time and effort of mastering the TradingView.TO syntax and manually create alert commands.

This powerful tool gives much power to those who don't know how to code in Pinescript and want to automate their indicators' signals via TradingView.TO bot.

IMPORTANT NOTES

TradingView.TO is a trading bot software that forwards TradingView alerts to your brokers (examples: Binance, Oanda, Coinbase, Bybit, Metatrader 4/5, ...) for automating trading.

Many traders don't know how to create TradingView.TO dynamically-compatible alerts using the data from their TradingView scripts.

Traders using trading bots want their alerts to reflect the stop-loss/take-profit/trailing-stop/stop-loss to break options from your script and then create the orders accordingly.

This script showcases how to create TradingView.TO alerts dynamically.

TRADINGVIEW ALERTS

1) You'll have to create one alert per asset X timeframe = 1 chart.

Example: 1 alert for BTC/USDT on the 5 minutes chart, 1 alert for BTC/USDT on the 15-minute chart (assuming you want your bot to trade the BTC/USDT on the 5 and 15-minute timeframes)

2) Select the Order fills and alert() function calls condition

3) For each alert, the alert message is pre-configured with the text below

{{strategy.order.alert_message}}

Please leave it as it is.

It's a TradingView native variable that will fetch the alert text messages built by the script.

4) TradingView.TO uses webhook technology - setting a webhook URL from the alerts notifications tab is required.

KEY FEATURES

I) Modular Indicator Connection

* plug your existing indicator into the template.

* Only two lines of code are needed for full compatibility.

Step 1: Create your connector

Adapt your indicator with only 2 lines of code and then connect it to this strategy template.

To do so:

1) Find in your indicator where the conditions print the long/buy and short/sell signals.

2) Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator, whether a MACD , ZigZag, Pivots , higher-highs, lower-lows or whatever indicator with clear buy and sell conditions.

//@version=5

indicator("Supertrend", overlay = true, timeframe = "", timeframe_gaps = true)

atrPeriod = input.int(10, "ATR Length", minval = 1)

factor = input.float(3.0, "Factor", minval = 0.01, step = 0.01)

= ta.supertrend(factor, atrPeriod)

supertrend := barstate.isfirst ? na : supertrend

bodyMiddle = plot(barstate.isfirst ? na : (open + close) / 2, display = display.none)

upTrend = plot(direction < 0 ? supertrend : na, "Up Trend", color = color.green, style = plot.style_linebr)

downTrend = plot(direction < 0 ? na : supertrend, "Down Trend", color = color.red, style = plot.style_linebr)

fill(bodyMiddle, upTrend, color.new(color.green, 90), fillgaps = false)

fill(bodyMiddle, downTrend, color.new(color.red, 90), fillgaps = false)

buy = ta.crossunder(direction, 0)

sell = ta.crossunder(direction, 0)

//////// CONNECTOR SECTION ////////

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title = "Signal", display = display.data_window)

//////// CONNECTOR SECTION ////////

Important Notes

🔥 The Strategy Template expects the value to be exactly 1 for the bullish signal and -1 for the bearish signal

Now, you can connect your indicator to the Strategy Template using the method below or that one.

Step 2: Connect the connector

1) Add your updated indicator to a TradingView chart

2) Add the Strategy Template as well to the SAME chart

3) Open the Strategy Template settings, and in the Data Source field, select your 🔌Connector🔌 (which comes from your indicator)

Note it doesn’t have to be named 🔌Connector🔌 - you can name it as you want - however, I recommend an explicit name you can easily remember.

From then, you should start seeing the signals and plenty of other stuff on your chart.

🔥 Note that whenever you update your indicator values, the strategy statistics and visuals on your chart will update in real-time

II) BOT Risk Management:

- Max Drawdown:

Mode: Select whether the max drawdown is calculated in percentage (%) or USD.

Value: If the max drawdown reaches this specified value, set a value to halt the bot.

- Max Consecutive Days:

Use Max Consecutive Days BOT Halt: Enable/Disable halting the bot if the max consecutive losing days value is reached.

- Max Consecutive Days: Set the maximum number of consecutive losing days allowed before halting the bot.

- Max Losing Streak:

Use Max Losing Streak: Enable/Disable a feature to prevent the bot from taking too many losses in a row.

- Max Losing Streak Length: Set the maximum length of a losing streak allowed.

Margin Call:

- Use Margin Call: Enable/Disable a feature to exit when a specified percentage away from a margin call to prevent it.

Margin Call (%): Set the percentage value to trigger this feature.

- Close BOT Total Loss:

Use Close BOT Total Loss: Enable/Disable a feature to close all trades and halt the bot if the total loss is reached.

- Total Loss ($): Set the total loss value in USD to trigger this feature.

Intraday BOT Risk Management:

- Intraday Losses:

Use Intraday Losses BOT Halt: Enable/Disable halting the bot on reaching specified intraday losses.

Mode: Select whether the intraday loss is calculated in percentage (%) or USD.

- Max Intraday Losses (%): Set the value for maximum intraday losses.

Limit Intraday Trades:

- Use Limit Intraday Trades: Enable/Disable a feature to limit the number of intraday trades.

- Max Intraday Trades: Set the maximum number of intraday trades allowed.

Restart Intraday EA:

III) Order Types and Position Sizing

- Choose between market or limit orders.

- Set your position size directly in the template.

Please use the position size from the “Inputs” and not the “Properties” tab.

I know it's redundant. - the template needs this value from the "Inputs" tab to build the alerts, and the Backtester needs it from the "Properties" tab.

IV) Advanced Take-Profit and Stop-Loss Options

- Choose to set your SL/TP in either USD or percentages.

- Option for multiple take-profit levels and trailing stop losses.

- Move your stop loss to break even +/- offset in USD for “risk-free” trades.

V) Miscellaneous:

Retry order openings if they fail.

Order Types:

Select and specify order type and price settings.

Position Size:

Define the type and size of positions.

Leverage:

Leverage settings, including margin type and hedge mode.

Session:

Limit trades to specific sessions.

Dates:

Limit trades to a specific date range.

Trades Direction:

Direction: Specify the market direction for opening positions.

VI) Logger

The TradingView.TO commands are logged in the TradingView logger.

You'll find more information about it in this TradingView blog post .

WHY YOU MIGHT NEED THIS TEMPLATE

1) Transform your indicator into a TradingView.TO trading bot more easily than before

Connect your indicator to the template

Create your alerts

Set your EA settings

2) Save Time

Auto-generated alert messages for TradingView.TO.

I tested them all and checked with the support team what could/couldn’t be done.

3) Be in Control

Manage your trading risks with advanced features.

4) Customizable

Fits various trading styles and asset classes.

REQUIREMENTS

* Make sure you have your TradingView.TO account

* If there is any issue with the template, ask me in the comments section - I’ll answer quickly.

BACKTEST RESULTS FROM THIS POST

1) I connected this strategy template to a dummy Supertrend script.

I could have selected any other indicator or concept for this script post.

I wanted to share an example of how you can quickly upgrade your strategy, making it compatible with TradingView.TO.

2) The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

This strategy is a template to be connected to any indicator - the sky is the limit. :)

3) This template is made to take 1 trade per direction at any given time.

Pyramiding is set to 1 on TradingView.

The strategy default settings are:

* Initial Capital: 100000 USD

* Position Size: 1%

* Commission Percent: 0.075%

* Slippage: 1 tick

* No margin/leverage used

ProfitView Strategy TemplateHello traders,

This script took me a full week of coding/testing, sweat, and tears - and I’m too nice as I’m giving it for free to the community.

If you're tired of manual trading and looking for a solid strategy template to pair with your indicators, look no further.

This Pine Script v5 strategy template is engineered for maximum customization and risk management.

Best part?

This Pine Script v5 template facilitates the dynamic construction of ProfitView alerts, sparing users the time and effort of mastering the ProfitView syntax and manually creating alert commands.

This powerful tool gives much power to those who don't know how to code in Pinescript and want to automate their indicators' signals via the ProfitView Chrome extension.

IMPORTANT NOTES

ProfitView is a trading bot software that forwards TradingView alerts to your brokers (examples: Binance, Oanda, Coinbase, Bybit, etc.) for automating trading.

Many traders don't know how to dynamically create ProfitView-compatible alerts using the data from their TradingView scripts.

Traders using trading bots want their alerts to reflect the stop-loss/take-profit/trailing-stop/stop-loss to break options from your script and then create the orders accordingly.

This script showcases how to create ProfitView alerts dynamically.

TRADINGVIEW ALERTS

1) You'll have to create one alert per asset X timeframe = 1 chart.

Example: 1 alert for EUR/USD on the 5 minutes chart, 1 alert for EUR/USD on the 15-minute chart (assuming you want your bot to trade the EUR/USD on the 5 and 15-minute timeframes)

2) Select the Order fills and alert() function calls condition

3) For each alert, the alert message is pre-configured with the text below

{{strategy.order.alert_message}}

Please leave it as it is.

It's a TradingView native variable that will fetch the alert text messages built by the script.

4) ProfitView doesn't use webhook technology, so setting a webhook URL from the alerts notifications tab is unnecessary.

KEY FEATURES

I) Modular Indicator Connection

* plug your existing indicator into the template.

* Only two lines of code are needed for full compatibility.

Step 1: Create your connector

Adapt your indicator with only 2 lines of code and then connect it to this strategy template.

To do so:

1) Find in your indicator where the conditions print the long/buy and short/sell signals.

2) Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator, whether a MACD , ZigZag, Pivots , higher-highs, lower-lows or whatever indicator with clear buy and sell conditions.

//@version=5

indicator("Supertrend", overlay = true, timeframe = "", timeframe_gaps = true)

atrPeriod = input.int(10, "ATR Length", minval = 1)

factor = input.float(3.0, "Factor", minval = 0.01, step = 0.01)

= ta.supertrend(factor, atrPeriod)

supertrend := barstate.isfirst ? na : supertrend

bodyMiddle = plot(barstate.isfirst ? na : (open + close) / 2, display = display.none)

upTrend = plot(direction < 0 ? supertrend : na, "Up Trend", color = color.green, style = plot.style_linebr)

downTrend = plot(direction < 0 ? na : supertrend, "Down Trend", color = color.red, style = plot.style_linebr)

fill(bodyMiddle, upTrend, color.new(color.green, 90), fillgaps = false)

fill(bodyMiddle, downTrend, color.new(color.red, 90), fillgaps = false)

buy = ta.crossunder(direction, 0)

sell = ta.crossunder(direction, 0)

//////// CONNECTOR SECTION ////////

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title = "Signal", display = display.data_window)

//////// CONNECTOR SECTION ////////

Important Notes

🔥 The Strategy Template expects the value to be exactly 1 for the bullish signal and -1 for the bearish signal

Now, you can connect your indicator to the Strategy Template using the method below or that one.

Step 2: Connect the connector

1) Add your updated indicator to a TradingView chart

2) Add the Strategy Template as well to the SAME chart

3) Open the Strategy Template settings, and in the Data Source field, select your 🔌Connector🔌 (which comes from your indicator)

Note it doesn’t have to be named 🔌Connector🔌 - you can name it as you want - however, I recommend an explicit name you can easily remember.

From then, you should start seeing the signals and plenty of other stuff on your chart.

🔥 Note that whenever you update your indicator values, the strategy statistics and visuals on your chart will update in real-time

II) BOT Risk Management:

- Max Drawdown:

Mode: Select whether the max drawdown is calculated in percentage (%) or USD.

Value: If the max drawdown reaches this specified value, set a value to halt the bot.

- Max Consecutive Days:

Use Max Consecutive Days BOT Halt: Enable/Disable halting the bot if the max consecutive losing days value is reached.

- Max Consecutive Days: Set the maximum number of consecutive losing days allowed before halting the bot.

- Max Losing Streak:

Use Max Losing Streak: Enable/Disable a feature to prevent the bot from taking too many losses in a row.

- Max Losing Streak Length: Set the maximum length of a losing streak allowed.

Margin Call:

- Use Margin Call: Enable/Disable a feature to exit when a specified percentage away from a margin call to prevent it.

Margin Call (%): Set the percentage value to trigger this feature.

- Close BOT Total Loss:

Use Close BOT Total Loss: Enable/Disable a feature to close all trades and halt the bot if the total loss is reached.

- Total Loss ($): Set the total loss value in USD to trigger this feature.

Intraday BOT Risk Management:

- Intraday Losses:

Use Intraday Losses BOT Halt: Enable/Disable halting the bot on reaching specified intraday losses.

Mode: Select whether the intraday loss is calculated in percentage (%) or USD.

- Max Intraday Losses (%): Set the value for maximum intraday losses.

Limit Intraday Trades:

- Use Limit Intraday Trades: Enable/Disable a feature to limit the number of intraday trades.

- Max Intraday Trades: Set the maximum number of intraday trades allowed.

Restart Intraday EA:

- Use Restart Intraday EA: Enable/Disable a feature to restart the bot at the first bar of the next day if it has been stopped with an intraday risk management safeguard.

III) Order Types and Position Sizing

- Choose between market, limit, or stop orders.

- Set your position size directly in the template.

Please use the position size from the “Inputs” and not the “Properties” tab.

I know it's redundant. - the template needs this value from the "Inputs" tab to build the alerts, and the Backtester needs it from the "Properties" tab.

IV) Advanced Take-Profit and Stop-Loss Options

- Choose to set your SL/TP in either pips or percentages.

- Option for multiple take-profit levels and trailing stop losses.

- Move your stop loss to break even +/- offset in pips for “risk-free” trades.

V) Miscellaneous

Retry order openings if they fail.

Order Types:

Select and specify order type and price settings.

Position Size:

Define the type and size of positions.

Leverage:

Leverage settings, including margin type and hedge mode.

Session:

Limit trades to specific sessions.

Dates:

Limit trades to a specific date range.

Trades Direction:

Direction: Specify the market direction for opening positions.

VI) Notifications (Telegram/Discord/Email/IFTTT/Twilio/SMS)

Customize notifications sent to Telegram, Discord, Email, IFTTT, Twilio, and ProfitView Logger.

VII) Logger

The ProfitView commands are logged in the TradingView logger.

You'll find more information about it in this TradingView blog post .

WHY YOU MIGHT NEED THIS TEMPLATE

1) Transform your indicator into a ProfitView trading bot more easily than before

Connect your indicator to the template

Create your alerts

Set your EA settings

2) Save Time

Auto-generated alert messages for ProfitView.

I tested them all and checked with the support team what could/couldn’t be done.

3) Be in Control

Manage your trading risks with advanced features.

4) Customizable

Fits various trading styles and asset classes.

REQUIREMENTS

* Make sure you have your ProfitView account and do the settings correctly in your Chrome extension. If you don't know how to do it, read the documentation + ask for help in the ProfitView Discord support channel.

* If there is any issue with the template, ask me in the comments section - I’ll answer quickly.

BACKTEST RESULTS FROM THIS POST

1) I connected this strategy template to a dummy Supertrend script.

I could have selected any other indicator or concept for this script post.

I wanted to share an example of how you can quickly upgrade your strategy, making it compatible with ProfitView.

2) The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

This strategy is a template to be connected to any indicator - the sky is the limit. :)

3) This template is made to take 1 trade per direction at any given time.

Pyramiding is set to 1 on TradingView.

The strategy default settings are:

* Initial Capital: 100000 USD

* Position Size: 1%

* Commission Percent: 0.075%

* Slippage: 1 tick

* No margin/leverage used

Best regards,

Dave

Pineconnector Strategy Template (Connect Any Indicator)Hello traders,

If you're tired of manual trading and looking for a solid strategy template to pair with your indicators, look no further.

This Pine Script v5 strategy template is engineered for maximum customization and risk management.

Best part?

It’s optimized for Pineconnector, allowing seamless integration with MetaTrader 4 and 5.

This powerful tool gives a lot of power to those who don't know how to code in Pinescript and are looking to automate their indicators' signals on Metatrader 4/5.

IMPORTANT NOTES

Pineconnector is a trading bot software that forwards TradingView alerts to your Metatrader 4/5 for automating trading.

Many traders don't know how to dynamically create Pineconnector-compatible alerts using the data from their TradingView scripts.

Traders using trading bots want their alerts to reflect the stop-loss/take-profit/trailing-stop/stop-loss to break options from your script and then create the orders accordingly.

This script showcases how to create Pineconnector alerts dynamically.

Pineconnector doesn't support alerts with multiple Take Profits.

As a workaround, for 2 TPs, I had to open two trades.

It's not optimal, as we end up paying more spreads for that extra trade - however, depending on your trading strategy, it may not be a big deal.

TRADINGVIEW ALERTS

1) You'll have to create one alert per asset X timeframe = 1 chart.

Example: 1 alert for EUR/USD on the 5 minutes chart, 1 alert for EUR/USD on the 15-minute chart (assuming you want your bot to trade the EUR/USD on the 5 and 15-minute timeframes)

2) Select the Order fills and alert() function calls condition

3) For each alert, the alert message is pre-configured with the text below

{{strategy.order.alert_message}}

Please leave it as it is.

It's a TradingView native variable that will fetch the alert text messages built by the script.

4) Don't forget to set the Pineconnector webhook URL in the Notifications tab of the TradingView alerts UI.

You’ll find the URL on the Pineconnector documentation website.

EA CONFIGURATION

1) The Pyramiding in the EA on Metatrader must be set to 2 if you want to trade with 2 TPs => as it's opening 2 trades.

If you only want 1 TP, set the EA Pyramiding to 1.

Regarding the other EA settings, please refer to the Pineconnector documentation on their website.

2) In the EA, you can set a risk (= position size type) in %/lots/USD, as in the TradingView backtest settings.

KEY FEATURES

I) Modular Indicator Connection

* plug in your existing indicator into the template.

* Only two lines of code are needed for full compatibility.

Step 1: Create your connector

Adapt your indicator with only 2 lines of code and then connect it to this strategy template.

To do so:

1) Find in your indicator where the conditions print the long/buy and short/sell signals.

2) Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator, whether it's a MACD , ZigZag , Pivots , higher-highs, lower-lows, or whatever indicator with clear buy and sell conditions.

//@version=5

indicator("Supertrend", overlay = true, timeframe = "", timeframe_gaps = true)

atrPeriod = input.int(10, "ATR Length", minval = 1)

factor = input.float(3.0, "Factor", minval = 0.01, step = 0.01)

= ta.supertrend(factor, atrPeriod)

supertrend := barstate.isfirst ? na : supertrend

bodyMiddle = plot(barstate.isfirst ? na : (open + close) / 2, display = display.none)

upTrend = plot(direction < 0 ? supertrend : na, "Up Trend", color = color.green, style = plot.style_linebr)

downTrend = plot(direction < 0 ? na : supertrend, "Down Trend", color = color.red, style = plot.style_linebr)

fill(bodyMiddle, upTrend, color.new(color.green, 90), fillgaps = false)

fill(bodyMiddle, downTrend, color.new(color.red, 90), fillgaps = false)

buy = ta.crossunder(direction, 0)

sell = ta.crossunder(direction, 0)

//////// CONNECTOR SECTION ////////

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title = "Signal", display = display.data_window)

//////// CONNECTOR SECTION ////////

Important Notes

🔥 The Strategy Template expects the value to be exactly 1 for the bullish signal and -1 for the bearish signal

Now, you can connect your indicator to the Strategy Template using the method below or that one.

Step 2: Connect the connector

1) Add your updated indicator to a TradingView chart

2) Add the Strategy Template as well to the SAME chart

3) Open the Strategy Template settings, and in the Data Source field, select your 🔌Connector🔌 (which comes from your indicator)

Note it doesn’t have to be named 🔌Connector🔌 - you can name it as you want - however, I recommend an explicit name you can easily remember.

From then, you should start seeing the signals and plenty of other stuff on your chart.

🔥 Note that whenever you update your indicator values, the strategy statistics and visuals on your chart will update in real-time

II) Customizable Risk Management

- Choose between percentage or USD modes for maximum drawdown.

- Set max consecutive losing days and max losing streak length.

- I used the code from my friend @JosKodify for the maximum losing streak. :)

Will halt the EA and backtest orders fill whenever either of the safeguards above are “broken”

III) Intraday Risk Management

- Limit the maximum intraday losses both in percentage or USD.

- Option to set a maximum number of intraday trades.

- If your EA gets halted on an intraday chart, auto-restart it the next day.

IV) Spread and Account Filters

- Trade only if the spread is below a certain pip value.

- Set requirements based on account balance or equity.

V) Order Types and Position Sizing

- Choose between market, limit, or stop orders.

- Set your position size directly in the template.

Please use the position size from the “Inputs” and not the “Properties” tab.

Reason : The template sends the order on the same candle as the entry signals - at those entry signals candles, the position size isn’t computed yet, and the template can’t then send it to Pineconnector.

However, you can use the position size type (USD, contracts, %) from the “Properties” tab for backtesting.

In the EA, you can define the position size type for your orders in USD or lots or %.

VI) Advanced Take-Profit and Stop-Loss Options

- Choose to set your SL/TP in either pips or percentages.

- Option for multiple take-profit levels and trailing stop losses.

- Move your stop loss to break even +/- offset in pips for “risk-free” trades.

VII) Logger

The Pineconnector commands are logged in the TradingView logger.

You'll find more information about it in this TradingView blog post .

WHY YOU MIGHT NEED THIS TEMPLATE

1) Transform your indicator into a Pineconnector trading bot more easily than before

Connect your indicator to the template

Create your alerts

Set your EA settings

2) Save Time

Auto-generated alert messages for Pineconnector.

I tested them all, and I checked with the support team what could/can’t be done

3) Be in Control

Manage your trading risks with advanced features.

4) Customizable

Fits various trading styles and asset classes.

REQUIREMENTS

* Make sure you have your Pineconnector license ID.

* Create your alerts with the Pineconnector webhook URL

* If there is any issue with the template, ask me in the comments section - I’ll answer quickly.

BACKTEST RESULTS FROM THIS POST

1) I connected this strategy template to a dummy Supertrend script.

I could have selected any other indicator or concept for this script post.

I wanted to share an example of how you can quickly upgrade your strategy, making it compatible with Pineconnector.

2) The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

This strategy is a template to be connected to any indicator - the sky is the limit. :)

3) This template is made to take 1 trade per direction at any given time.

Pyramiding is set to 1 on TradingView.

The strategy default settings are:

* Initial Capital: 100000 USD

* Position Size: 1 contract

* Commission Percent: 0.075%

* Slippage: 1 tick

* No margin/leverage used

WHAT’S COMING NEXT FOR YOU GUYS?

I’ll make the same template for ProfitView, then for AutoView, and then for Alertatron.

All of those are free and open-source.

I have no affiliations with any of those companies - I'm publishing those templates as they will be useful to many of you.

Dave

RVI_HTFThe "RVI_HTF" indicator is a tool designed to assist traders in analyzing market trends using the Relative Vigor Index (RVI) across different timeframes. It enables users to customize various aspects of the indicator's appearance and behavior. By monitoring the RVI on different timeframes, tracking its relationship with the moving average, and paying attention to extreme arrows above the 80 or below the 20 line, traders can anticipate potential reversals, trends, or changes in market momentum.

Above 80 Line: When the RVI moves above the 80 line, it suggests that the market may be overbought. Extreme upward arrows (indicating potential sell signals) can be a sign that a bullish trend might be reaching an exhaustion point. Traders may anticipate a possible trend reversal or pullback.

Below 20 Line: When the RVI dips below the 20 line, it implies that the market might be oversold. Extreme downward arrows (indicating potential buy signals) can be an early signal of a potential bullish reversal. Traders may anticipate an upcoming uptrend or bounce.

Crossing Above Moving Average: When the RVI crosses above its moving average on the selected timeframe, it can serve as an early indication of potential bullish strength in the market. This suggests that buying pressure may be increasing.

Crossing Below Moving Average: Conversely, when the RVI crosses below its moving average, it can signal potential bearish momentum. This indicates that selling pressure may be gaining strength.

Variables:

Timeframe (TF) Selection:

The indicator allows you to select the timeframe for the RVI calculation. You can choose from various options such as 1 minute (1), 5 minutes (5), 15 minutes (15), 30 minutes (30), 60 minutes (60), 240 minutes (240), Daily (D), Weekly (W), Monthly (M), or use "Auto" to automatically select a higher timeframe based on your current chart's timeframe.

Moving Average Type (MA_Type):

Function: Allows users to select the type of moving average used in RVI calculations.

Options: You can select from various moving average types, including:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

SMMA (Smoothed Moving Average, also known as RMA)

WMA (Weighted Moving Average)

VWMA (Volume Weighted Moving Average)

DEMA (Double Exponential Moving Average)

Moving Average Length (MA_Length):

Function: Permits users to set the number of periods for the selected moving average type.

Purpose: Controls the sensitivity of the RVI indicator. Longer lengths provide smoother results, while shorter lengths react more quickly to price changes.

Up Arrow Color (upArrowColor):

Function: Enables users to customize the color of arrows that indicate potential Overbought areas. (Only shown when the TF is same as or lower than the chart TF)

Down Arrow Color (downArrowColor):

Function: Allows users to specify the color of downward-pointing arrows signaling potential Oversold areas. (Only shown when the TF is same as or lower than the chart TF)

RVI Up Color (firstColor):

Function: Defines the color of the RVI line when it indicates a bullish condition on the higher timeframe.

RVI Down Color (secondColor):

Function: Specifies the color of the RVI line when it suggests a bearish condition on the higher timeframe.

RVI-Based Moving Average Up Color (firstColorMA):

Function: Customizes the color of the RVI-based moving average line when it indicates a bullish condition.

RVI-Based Moving Average Down Color (secondColorMA):

Function: Defines the color of the RVI-based moving average line when it suggests a bearish condition.

Heatmap MACD Strategy - Pineconnector (Dynamic Alerts)Hello traders

This script is an upgrade of this template script.

Heatmap MACD Strategy

Pineconnector

Pineconnector is a trading bot software that forwards TradingView alerts to your Metatrader 4/5 for automating trading.

Many traders don't know how to dynamically create Pineconnector-compatible alerts using the data from their TradingView scripts.