8MA Compass — HTF map + GC/DC cues8MA Compass provides a clean trend context by combining strict 4-of-4 confluence (Current TF vs Higher TF) with SMA200 repainting on Golden/Death Cross (GC/DC).

What it shows

4-of-4 background (context): compares EMA10, EMA20, SMA50, SMA200 on the Current TF against the same four MAs on the Higher TF (HTF).

All 4 above their HTF values → bullish background.

All 4 below their HTF values → bearish background.

SMA200 color on GC/DC (Current TF):

Last signal is DC and price below SMA200 → SMA200 turns red.

Price above SMA200 but the last signal is DC (no GC afterward) → SMA200 stays base color.

Last signal is GC and price above SMA200 → SMA200 turns green #089981.

Why “8MA” ? The 4-of-4 logic uses 8 moving averages in total: 4 on the Current TF and 4 on the HTF (EMA10/20 and SMA50/200 on both frames). HTF EMAs are used in calculations but are not plotted by default—hence the name 8MA Compass.

Auto HTF mapping

Current 1H → HTF 4H

Current 4H → HTF 1D

Current 1D → HTF 1W

All other timeframes: HTF defaults to Current TF (4-of-4 will typically be neutral).

Manual mode: choose any HTF. If Manual HTF equals Current TF, HTF SMAs are hidden to avoid overlap.

Settings

1. Display

Show CURRENT TF — plot EMA10/20, SMA50/200 on Current TF.

Show HARD TF — plot SMA50/200 on HTF (hidden if HTF == Current TF).

HTF mode — Auto / Manual, with Hard TF (Manual) selector.

2. Filter

Show base background (4-of-4) — enable/disable confluence shading.

Epsilon (in ticks) — small tolerance in Cur vs HTF comparisons to reduce flicker.

3. Golden/Death

Color SMA200 on GC/DC (Cur TF) — repaint SMA200 on GC/DC per rules above (enabled by default).

Alerts

GC/DC (Current TF, SMA50/200): Golden Cross / Death Cross (on bar close).

EMA10/20 (Current TF): “Bull regime ON” / “Bear regime ON” on crossovers.

Optional HTF GC/DC alerts (SMA50/200 on chosen HTF).

Visual details

HTF SMA50/200 are drawn first; Current TF lines are drawn on top for clarity.

SMA200 (Current TF) is drawn last (and slightly thicker) to remain readable.

HTF EMAs are used in 4-of-4 logic but not plotted by design.

Usage

1. Use the 4-of-4 background as inter-timeframe momentum context.

2. Use SMA200 color to gauge long-term regime confirmation:

Prefer longs when last GC and price holds above SMA200 (#089981 line).

Avoid longs when last DC and price is below SMA200 (red line).

Disclaimer : For educational purposes only. Not financial advice. Trading involves risk.

Cari dalam skrip untuk "神户胜利+VS+磐田喜悦"

Confluence Engine Confluence Engine is a practical, non-repainting decision aid that scores market conditions from −100…+100 by combining six proven modules: Trend, Momentum, Volatility, Volume, Structure, and an HTF confirmation. It’s designed for crypto, forex, indices, and stocks, and it fires entries only on confirmed bar closes.

What’s inside

Trend: EMA 20/50/200 alignment plus a Supertrend/KAMA toggle (you choose the baseline).

Momentum: RSI + MACD with confirmed-pivot divergence detection.

Volatility: ATR% and Bollinger Band width vs its average to favor expansion over chop.

Volume: OBV-style cumulative flow slope + volume surge vs SMA×multiplier.

Market Structure: Confirmed pivots, BOS (break of structure) and CHOCH (change of character).

HTF Filter: Closed higher-timeframe context via request.security(..., barmerge.gaps_on, barmerge.lookahead_off).

Why it does not repaint

Signals are computed and plotted on closed bars only.

Pivots/divergences use confirmed pivot points (no forward look).

HTF series are fetched with lookahead_off and use the last closed HTF bar in realtime.

No future bar references are used for entries or alerts.

How to use (3 steps)

Pick a timeframe pair: use a 4–6× HTF multiplier (5m→30m, 15m→1h, 1h→4h, 4h→1D, 1D→1W).

Trade with the HTF: take longs only when the HTF filter is bullish; shorts only when bearish.

Prefer expansion: act when BB width > its average and ATR% is elevated; skip most signals in compression.

Suggested presets (start here)

Crypto (BTC/ETH): 15m→1h, 1h→4h. stLen=10, stMult=3.0, bbLen=20, surgeMul=1.8–2.2, thresholds +40 / −40 (intraday can try +35 / −35).

Forex majors: 15m→1h, 1h→4h. stLen=10–14, stMult=2.5–3.0, surgeMul=1.5–1.8, thresholds +35 / −35 (swing: +45 / −45).

US equities (liquid): 5m→30m/1h, 15m→1h/2h. stMult=3.0–3.5, surgeMul=1.6–2.0, thresholds +45 / −45 to reduce chop.

Indices (ES/NQ): 5m→30m, 15m→1h. Defaults are fine; start at +40 / −40.

Gold/Oil: 15m→1h, 1h→4h. Thresholds +35 / −35, surgeMul=1.6–1.9.

Inputs (plain English)

Use Supertrend (off = KAMA): choose the trend baseline.

EMA Fast/Mid/Slow: 20/50/200 by default for classic stack.

RSI/MACD + divergence pivots: momentum and exhaustion context.

ATR Length & BB Length: volatility regime detection.

Volume SMA & Surge Multiplier: defines “meaningful” volume spikes.

Pivot left/right & “Confirm BOS/CHOCH on Close”: structure strictness.

Enable HTF & Higher Timeframe: confirms the lower timeframe direction.

Thresholds (+long / −short): when the score crosses these, you get signals.

Signals & alerts (IDs preserved)

Entry shapes plot at bar close when the score crosses thresholds.

Alerts you can enable:

CONFLUENCE LONG — long entry signal

CONFLUENCE SHORT — short entry signal

BULLISH BIAS — score turned positive

BEARISH BIAS — score turned negative

Best practices

Focus on signals with HTF agreement and volatility expansion; require volume participation (surge or rising OBV slope) for higher quality.

Raise thresholds (+45/−45 or +50/−50) to reduce whipsaws in choppy sessions.

Lower thresholds (+35/−35) only if you also require volatility/volume filters.

Performance & scope

Works across crypto/FX/equities/indices; no broker data or special feeds required.

No repainting by design; signals/alerts are computed on closed bars.

As with any tool, results vary by regime; always combine with risk management.

Disclosure

This script is for educational purposes only and is not financial advice. Trading involves risk. Test on historical data and paper trade before using live.

LP Sweep / Reclaim & Breakout Grading: Long-onlySignals

1) LP Sweep & Reclaim (mean-reversion entry)

Compute LP bounds from prior-bar window extremes:

lpLL_prev = lowest low of the last N bars (offset 1).

lpHH_prev = highest high of the last N bars (offset 1).

Sweep long trigger: current low dips below lpLL_prev and closes back above it.

Real-time quality grading (A/B/C) for sweep:

Trend filter & slope via EMA(88).

BOS bonus: close > last confirmed swing high.

Body size vs ATR, location above a long EMA, headroom to swing high (penalty if too close), and multi-sweep count bonus.

Sum → score → grade A/B/C; A or B required for sweep entry.

2) Trend Breakout (momentum entry)

Core trigger: close > previous Donchian high (length boLen) + ATR buffer.

Optional filter: close must be above the default EMA.

Breakout grading (A/B/C) in real time combining:

Trend up (price > EMA and EMA rising),

Body/ATR, Gap above breakout level (in ATR),

Volume vs MA,

Upper-wick penalty,

Position-in-Score: headroom to last swing high (penalty if too near) + EMA slope bonus.

Sum → score → A or B required if grading enabled.

Transformer Flux DashboardHere’s a practical guide to what your Transformer Flux Dashboard does and how to use it.

What it is

A compact, two-column trading dashboard + signal pack that blends trend, MACD, and OBV into one view (“Flux Score”) and adds session awareness (pre-sessions and main sessions in Eastern time). It’s designed for regular candles by default and avoids repaint by letting you confirm on bar close.

Core pieces it calculates

Moving Averages

Two MAs: Fast (HMA/EMA) and Slow (HMA/EMA).

You choose length, line width, color, and transparency.

Trend engine (Strict/Lenient)

Uses the relation between Fast/Slow MA and a debounced fast-MA slope filter (slope > ATR×buffer).

Strict: requires fast>slow and slow rising (or the inverse for down).

Lenient: fast>slow or slow rising (or the inverse).

A confirmation window (bars) must hold true before trend flips. That window can be auto-tuned by session (Asia/London/NY) or set globally.

OBV confirmation (optional)

OBV smoothed by SMA; needs to be rising/falling for N bars (also session-aware if you enable presets).

MACD

Standard MACD Fast/Slow/Signal; the dashboard shows Bull ▲, Bear ▼ or Flat based on line vs signal.

Flux Score (top row)

A composite, smoothed gauge from 0–100:

40% Trend, 30% MACD, 30% OBV → EMA(3) smoothed.

Labels: Bullish ≥ 70, Bearish ≤ 30, otherwise Neutral.

Summary line explains why (e.g., “MACD↑, OBV↑, Trend up”).

Sessions & zones (Eastern/NY time)

Recognizes Asia / London / New York main sessions and pre-sessions using your chart’s Eastern time.

Session label (top of chart): text is white; background auto-matches the current session color (or your manual color).

Zone backgrounds (optional): off by default; when on, default transparency ≈ 95% (very light), with separate colors for each session and pre-session. A toggle lets you draw pre-session on top or beneath main sessions.

Signals & markers

Two strength tiers: Strong (Trend + OBV + MACD aligned) and Weak (2 of the 3 agree).

To reduce clutter, markers only appear on direction shifts (from last visible direction to a new one), and you can enforce a minimum bar gap.

Marker style:

Default Icons with LabelUp/LabelDown (tiny).

Colors: strong long = bright white by default; others configurable.

Weak markers are slightly offset from price using ATR so they don’t overlap wicks.

Dashboard (2-column)

Left column = label, right column = value:

Flux Score: numeric + Bullish/Neutral/Bearish tag.

Summary: short reason of the score.

Trend: UP / DOWN / FLAT (cell tinted green/red/gray).

MACD: Bull ▲ / Bear ▼ / Flat (tinted).

Signal: last printed signal + bar age (fresh signals get a lighter tint).

MA: slow MA type/length and up/down arrow.

Sess: current session label (e.g., “Pre-London”, “New York”).

VIX / VXN (optional): shows current value.

Auto tint: based on calm/watch/elevated thresholds (you control levels and colors).

Manual tint: fixed BG color if you prefer consistency.

Params: “P”=trend bars, “O”=OBV bars, mode (Strict/Lenient), and “Candles”.

You can set a global Default Transparency for the dashboard cells.

Key settings to know

Confirm On Close: when on (default), trend/OBV/MACD states use the last confirmed bar; this avoids mid-bar flicker and reduces repaint risk.

Session presets: when enabled, the number of bars required for confirmations tightens/loosens per session (e.g., Asia uses more bars than NY).

Colors & Opacity:

MA lines have their own transparency (default 0 = fully opaque).

Dashboard cells use a single global transparency (default 40%).

Session zones default to very light (95%) and are off by default.

VIX/VXN cells can auto-color by regime or use a manual background.

Markers:

“Icons” vs “Ticks.” Default is Icons with tiny labels up/down.

“Shift only” display reduces noise; you can also set min bar spacing.

How to read it (quick workflow)

Flux Score row: a fast “risk-on/off” gauge.

≥70 with green Trend/MACD cells → higher-conviction long context.

≤30 with red Trend/MACD cells → higher-conviction short context.

Summary explains why the score is what it is.

Signal row: tells you the last official signal and how many bars ago it fired. Fresh signals tint lighter.

MA row: aligns your slow baseline; arrow helps spot slow-turns early.

Sess row + label: know which market is active; behavior and your confirmation bars adapt by session if presets are on.

VIX/VXN (if enabled): extra context for risk regime (values and color band).

Good practices & caveats

It’s confirmation-based to reduce false flips; you’ll get signals slightly later, by design.

All signals are informational; there’s no position management or stops in this build (we removed the stop visuals by request).

If you switch to exotic chart types or extreme resolutions, re-tune lengths and confirmation bars (and potentially disable session presets).

For scalping, consider reducing confirmation bars and OBV smoothing; for higher timeframes, increase them.

Quick customization ideas

Want faster flips? Lower confirmBars and obvBars, increase slope buffer a bit to retain quality.

Want fewer weak signals? Show only strong markers (toggle off weak via colors/visibility or increase min bar gap).

Prefer EMA stacking? Set both Fast/Slow to EMA.

Don’t care about OBV? Turn OBV confirm off; Trend + MACD will drive

Ichimoku Fractal Flow### Ichimoku Fractal Flow (IFF)

By Gurjit Singh

Ichimoku Fractal Flow (IFF) distills the Ichimoku system into a single oscillator by merging fractal echoes of price and cloud dynamics into one flow signal. Instead of static Ichimoku lines, it measures the "flow" between Conversion/Base, Span A/B, price echoes, and cloud echoes. The result is a multidimensional oscillator that reveals hidden rhythm, momentum shifts, and trend bias.

#### 📌 Key Features

1. Fourfold Fusion – The oscillator blends:

* Phase: Tenkan vs. Kijun spread (short vs. medium trend).

* Kumo Phase: Span A vs. Span B spread (cloud thickness).

* Echo: Price vs lagged reflection.

* Cloud Echo: Price vs. projected cloud center.

2. Oscillator Output – A unified flow line oscillating around zero.

3. Dual Calculation Modes – Oscillator can be built using:

* High-Low Midpoint (classic Ichimoku-style averaging).

* Wilder’s RMA (smoother, less noisy averaging averaging).

4. Optional Smoothing – EMA or Wilder’s RMA creates a trend line, enabling MACD-style crossovers.

5. Dynamic Coloring – Bullish/Bearish color shifts for quick bias recognition.

6. Fill Styling – Highlighted regions between oscillator & smoothing line.

7. Zero Line Reference – Acts as a structural pivot (bull vs. bear).

#### 🔑 How to Use

1. Add to Chart: Works across all assets and timeframes.

2. Flow Bias (Zero Line):

* Above 0 → Bullish flow 🐂

* Below 0 → Bearish flow 🐻

3. With Signal Line:

* Oscillator above smoothing line → Possible upward trend shift.

* Oscillator below smoothing line → Possible downward trend shift.

4. Strength:

* Wide separation from smoothing = strong trend.

* Flat, tight clustering = indecision/range.

5. Contextual Edge: Combine signals with Ichimoku Cloud analysis for stronger confluence.

#### ⚙️ Inputs & Options

* Conversion Line (Tenkan, default 9)

* Base Line (Kijun, default 26)

* Leading Span B (default 52)

* Lag/Lead Shift (default 26)

* Oscillator Mode: High-Low Midpoint vs Wilder’s RMA

* Use Smoothing (toggle on/off)

* Signal Smoothing: Wilder/EMA option

* Smoothing Length (default 9)

* Bullish/Bearish Colors + Transparency

#### 💡 Tips

* Wilder’s RMA (both oscillator & smoothing) is gentler, reducing whipsaws in sideways markets.

* High-Low Mid captures pure Ichimoku-style ranges, good for structure-based traders.

* EMA reacts faster than RMA; use if you want early momentum signals.

* Zero-line flips act like momentum pivots—watch them near cloud boundaries.

* Signal line crossovers behave like MACD-style triggers.

* Strongest signals appear when oscillator, signal line, and Ichimoku Cloud all align.

👉 In short: Ichimoku Fractal Flow compresses multi-layered Ichimoku system into a single fractal oscillator that detects flow, pivotal shifts, and momentum with clarity—bridging price, cloud, and echoes into one signal. Where the cloud shows structure, IFF reveals the underlying flow. Together, they offer a fractal lens into market rhythm.

High Probability Order Blocks [AlgoAlpha]🟠 OVERVIEW

This script detects and visualizes high-probability order blocks by combining a volatility-based z-score trigger with a statistical survival model inspired by Kaplan-Meier estimation. It builds and manages bullish and bearish order blocks dynamically on the chart, displays live survival probabilities per block, and plots optional rejection signals. What makes this tool unique is its use of historical mitigation behavior to estimate and plot how likely each zone is to persist, offering traders a probabilistic perspective on order block strength—something rarely seen in retail indicators.

🟠 CONCEPTS

Order blocks are regions of strong institutional interest, often marked by large imbalances between buying and selling. This script identifies those areas using z-score thresholds on directional distance (up or down candles), detecting statistically significant moves that signal potential smart money footprints. A bullish block is drawn when a strong up-move (zUp > 4) follows a down candle, and vice versa for bearish blocks. Over time, each block is evaluated: if price “mitigates” it (i.e., closes cleanly past the opposite side and confirmed with a 1 bar delay), it’s considered resolved and logged. These resolved blocks then inform a Kaplan-Meier-like survival curve, estimating the likelihood that future blocks of a given age will remain unbroken. The indicator then draws a probability curve for each side (bull/bear), updating it in real time.

🟠 FEATURES

Live label inside each block showing survival probability or “N.E.D.” if insufficient data.

Kaplan-Meier survival curves drawn directly on the chart to show estimated strength decay.

Rejection markers (▲ ▼) if price bounces cleanly off an active order block.

Alerts for zone creation and rejection signals, supporting rule-based trading workflows.

🟠 USAGE

Read the label inside each block for Age | Survival% (or N.E.D. if there aren’t enough samples yet); higher survival % suggests blocks of that age have historically lasted longer.

Use the right-side survival curves to gauge how probability decays with age for bull vs bear blocks, and align entries with the side showing stronger survival at current age.

Treat ▲ (bullish rejection) and ▼ (bearish rejection) as optional confluence when price tests a boundary and fails to break.

Turn on alerts for “Bullish Zone Created,” “Bearish Zone Created,” and rejection signals so you don’t need to watch constantly.

If your chart gets crowded, enable Prevent Overlap ; tune Max Box Age to your timeframe; and adjust KM Training Window / Minimum Samples to trade off responsiveness vs stability.

Theil-Sen Line Filter [BackQuant]Theil-Sen Line Filter

A robust, median-slope baseline that tracks price while resisting outliers. Designed for the chart pane as a clean, adaptive reference line with optional candle coloring and slope-flip alerts.

What this is

A trend filter that estimates the underlying slope of price using a Theil-Sen style median of past slopes, then advances a baseline by a controlled fraction of that slope each bar. The result is a smooth line that reacts to real directional change while staying calm through noise, gaps, and single-bar shocks.

Why Theil-Sen

Classical moving averages are sensitive to outliers and shape changes. Ordinary least squares is sensitive to large residuals. The Theil-Sen idea replaces a single fragile estimate with the median of many simple slopes, which is statistically robust and less influenced by a few extreme bars. That makes the baseline steadier in choppy conditions and cleaner around regime turns.

What it plots

Filtered baseline that advances by a fraction of the robust slope each bar.

Optional candle coloring by baseline slope sign for quick trend read.

Alerts when the baseline slope turns up or down.

How it behaves (high level)

Looks back over a fixed window and forms many “current vs past” bar-to-bar slopes.

Takes the median of those slopes to get a robust estimate for the bar.

Optionally caps the magnitude of that per-bar slope so a single volatile bar cannot yank the line.

Moves the baseline forward by a user-controlled fraction of the estimated slope. Lower fractions are smoother. Higher fractions are more responsive.

Inputs and what they do

Price Source — the series the filter tracks. Typical is close; HL2 or HLC3 can be smoother.

Window Length — how many bars to consider for slopes. Larger windows are steadier and slower. Smaller windows are quicker and noisier.

Response — fraction of the estimated slope applied each bar. 1.00 follows the robust slope closely; values below 1.00 dampen moves.

Slope Cap Mode — optional guardrail on each bar’s slope:

None — no cap.

ATR — cap scales with recent true range.

Percent — cap scales with price level.

Points — fixed absolute cap in price points.

ATR Length / Mult, Cap Percent, Cap Points — tune the chosen cap mode’s size.

UI Settings — show or hide the line, paint candles by slope, choose long and short colors.

How to read it

Up-slope baseline and green candles indicate a rising robust trend. Pullbacks that do not flip the slope often resolve in trend direction.

Down-slope baseline and red candles indicate a falling robust trend. Bounces against the slope are lower-probability until proven otherwise.

Flat or frequent flips suggest a range. Increase window length or decrease response if you want fewer whipsaws in sideways markets.

Use cases

Bias filter — only take longs when slope is up, shorts when slope is down. It is a simple way to gate faster setups.

Stop or trail reference — use the line as a trailing guide. If price closes beyond the line and the slope flips, consider reducing exposure.

Regime detector — widen the window on higher timeframes to define major up vs down regimes for asset rotation or risk toggles.

Noise control — enable a cap mode in very volatile symbols to retain the line’s continuity through event bars.

Tuning guidance

Quick swing trading — shorter window, higher response, optionally add a percent cap to keep it stable on large moves.

Position trading — longer window, moderate response. ATR cap tends to scale well across cycles.

Low-liquidity or gappy charts — prefer longer window and a points or ATR cap. That reduces jumpiness around discontinuities.

Alerts included

Theil-Sen Up Slope — baseline’s one-bar change crosses above zero.

Theil-Sen Down Slope — baseline’s one-bar change crosses below zero.

Strengths

Robust to outliers through median-based slope estimation.

Continuously advances with price rather than re-anchoring, which reduces lag at turns.

User-selectable slope caps to tame shock bars without over-smoothing everything.

Minimal visuals with optional candle painting for fast regime recognition.

Notes

This is a filter, not a trading system. It does not account for execution, spreads, or gaps. Pair it with entry logic, risk management, and higher-timeframe context if you plan to use it for decisions.

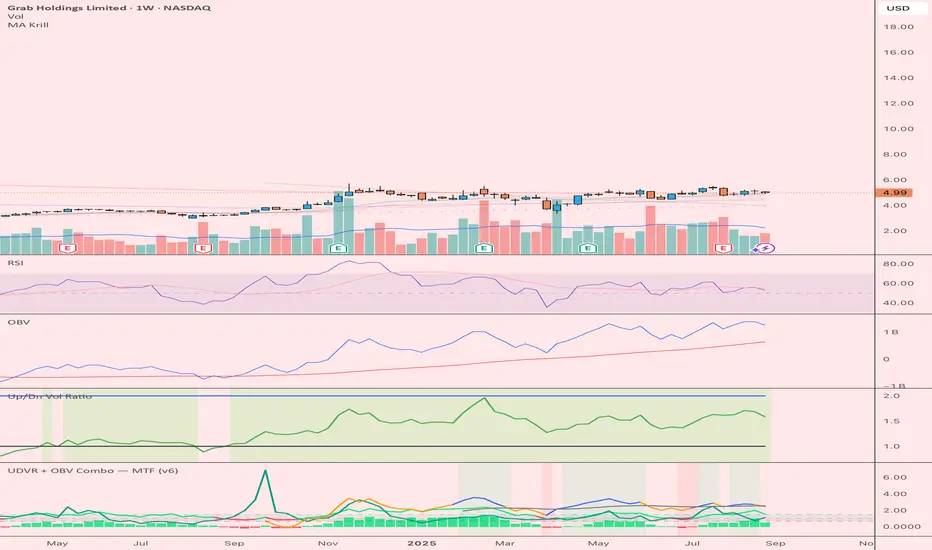

UDVR + OBV Combo — MTF (v6)The UDVR + OBV Combo is a multi-timeframe volume analysis tool that blends the Up/Down Volume Ratio with a normalized On-Balance Volume signal. It highlights when accumulation or distribution truly supports price action, adds higher-timeframe context, and shades the background when both indicators align. Use it to confirm breakouts, spot divergences, and filter trades with the backing of real volume flows.

1.Up/Down Volume Ratio (UDVR)

•Compares the rolling sum of up-volume (bars where price closed higher) vs down-volume (bars where price closed lower).

•A ratio > 1.0 = more accumulation (bullish pressure).

•A ratio < 1.0 = more distribution (bearish pressure).

•Optional histogram shows deviations from the 1.0 baseline.

•Customizable handling of equal closes (count as up, down, split, or ignore).

•Configurable lookback length and optional EMA smoothing.

2. On-Balance Volume (OBV)

•Classic cumulative OBV implemented natively (adds volume on up-bars, subtracts on down-bars).

•Normalized with a z-score so it can be compared across different symbols/timeframes.

•Includes an EMA signal line for slope detection.

•Alignment of OBV vs its EMA highlights rising or waning participation.

3. Multi-Timeframe Support

•Both UDVR and OBV can be plotted from a higher timeframe (HTF) (e.g. Daily UDVR shown on a 1h chart).

•Lets you see big-money accumulation/distribution while trading intraday.

•Shaded background when current TF and HTF agree (both bullish or both bearish).

How to read it

• Bullish confirmation = UDVR > 1 (accumulation) and OBV above EMA (rising participation).

• Bearish confirmation = UDVR < 1 (distribution) and OBV below EMA (falling participation).

• Mixed signals (e.g. UDVR > 1 but OBV falling) = caution; price may lack conviction.

• Divergences : If price makes a new high but OBV or UDVR does not, it’s a warning of weakening trend.

• Higher timeframe context : set HTF = Daily or Weekly and watch how short-term signals align with institutional flows. A long trade on the 15m chart is stronger when Daily UDVR is also above 1.

Inputs

•UDVR Lookback: number of bars for rolling volume sums.

•Smoothing EMA: smooths UDVR for stability.

•Equal Close Handling: decide how equal closes affect UDVR.

•Signal Band: optional UDVR extreme thresholds.

•Show Histogram: toggle UDVR histogram around baseline.

•Higher Timeframe UDVR: overlay Daily/Weekly UDVR on lower timeframe charts.

•OBV EMA length: slope proxy for normalized OBV.

•OBV Normalization window: controls z-score sensitivity.

•Higher Timeframe OBV: overlay higher timeframe OBV.

Alerts

•UDVR Bullish/Bearish cross at the 1.0 baseline.

•OBV slope up/down when OBV crosses its EMA.

•Alignment signals when UDVR and OBV agree (both confirm bullish or bearish conditions).

Why it’s useful

•Combines trend, momentum, and participation in one place.

•Helps avoid false breakouts by checking if volume supports the move.

•Lets you spot accumulation/distribution shifts before they show up in price.

•Gives a higher timeframe context so you’re not trading against the “big picture.”

Once applied, the indicator creates a dedicated pane below price with the following components:

UDVR Line (green/red)

• Green when UDVR > 1.0 (more up-volume than down-volume → accumulation).

• Red when UDVR < 1.0 (more down-volume → distribution).

UDVR Baseline and Bands

• Grey baseline at 1.0 = balance between buying and selling volume.

• Optional upper/lower bands (default 1.5 and 0.67) highlight extreme imbalances.

• Shaded areas between baseline and bands provide visual context for strength/weakness.

UDVR Histogram (optional)

• Columns around the baseline showing (UDVR – 1.0).

• Quick way to gauge how far above/below balance the ratio is.

Higher-Timeframe UDVR (teal line)

• Overlays the UDVR from a higher timeframe (e.g. Daily) on your intraday chart.

• Lets you see whether institutional flows support your shorter-term signals.

OBV Normalized (blue/orange line)

• Classic OBV, but normalized with a z-score so it stays readable across assets.

• Blue when OBV is above its EMA (rising participation).

• Orange when below its EMA (waning participation).

OBV EMA (grey line)

• Signal line showing the slope of OBV.

• Crosses between OBV and this line mark shifts in participation.

Higher-Timeframe OBV (purple line, optional)

• Plots OBV from a higher timeframe for additional context.

Background Shading

• Light green = both UDVR > 1 and OBV > OBV-EMA (bullish alignment).

• Light red = both UDVR < 1 and OBV < OBV-EMA (bearish alignment).

PumpC PAC & MAsPumpC – PAC & MAs (Open Source)

A complete Price Action Candles (PAC) toolkit combining classical price action patterns (Fair Value Gaps, Inside Bars, Hammers, Inverted Hammers, and Volume Imbalances) with a flexible Moving Averages (MAs) module and an advanced bar-coloring system.

This script highlights supply/demand inefficiencies and micro-patterns with forward-extending boxes, recolors zones when mitigated, qualifies patterns with a global High-Volume filter, and ships with ready-to-use alerts. It works across intraday through swing trading on any market (e.g., NASDAQ:QQQ , $CME:ES1!, FX:EURUSD , BITSTAMP:BTCUSD ).

This is an open-source script. The description is detailed so users understand what the script does, how it works, and how to use it. It makes no performance claims and does not provide trade advice.

Acknowledgment & Credits

This script originates from the structural and box-handling logic found in the Super OrderBlock / FVG / BoS Tools by makuchaku & eFe. Their pioneering framework provided the base methods for managing arrays of boxes, extending zones forward, and recoloring once mitigated.

Building on that foundation, I have substantially expanded and adapted the code to create a unified Price Action Candles toolkit . This includes Al Brooks–inspired PAC logic, additional patterns like Inside Bars, Hammers, Inverted Hammers, and the new Volume Imbalance module, along with strong-bar coloring, close-threshold detection, a flexible global High-Volume filter, and a multi-timeframe Moving Averages system.

What it does

Fair Value Gaps (FVG) : Detects 3-bar displacement gaps, plots forward-extending boxes, and optionally recolors them once mitigated.

Inside Bars (IB) : Highlights bars fully contained within the prior candle’s range, with optional high-volume filter.

Hammers (H) & Inverted Hammers (IH) : Identifies rejection candles using configurable body/upper/lower wick thresholds. High-volume qualification optional.

Volume Imbalances (VI) : Detects inter-body gaps where one candle’s body does not overlap the prior candle’s body. Boxes extend forward until wick-based mitigation occurs (only after the two-bar formation completes). Alerts available for creation and mitigation.

Mitigation Recolor : Each pattern can flip to a mitigated color once price trades back through its vertical zone.

Moving Averages (MAs) : Four configurable EMAs/SMAs, with per-MA timeframe, length, color, and clutter-free plotting rules.

Strong Bar Coloring : Highlights bullish/bearish engulfing reversals with different colors for high-volume vs low-volume cases.

Close Threshold Bars : Marks candles that close in the top or bottom portion of their range, even if the body is small. Helps spot continuation pressure before a full trend bar forms.

Alerts : Notifications available for FVG+, FVG−, IB, H, IH, VI creation, and VI mitigation.

Connection to Al Brooks’ PAC teachings

This script reflects Al Brooks’ Price Action Candle methodology. PAC patterns like Inside Bars, Hammers, and Inverted Hammers are not trade signals on their own—they gain meaning in context of trend, failed breakouts, and effort vs. result.

By layering in volume imbalances, strong-bar reversals, and volume filters, this script focuses attention on the PACs that show true participation and conviction, aligning with Brooks’ emphasis on reading crowd psychology through price action.

Why the High-Volume filter matters

Volume is a key proxy for conviction. A PAC or VI formed on light volume can be misleading noise; one formed on above-average volume carries more weight.

Elevates Inside Bars that show absorption/compression with heavy activity.

Distinguishes Hammers that reject price aggressively vs. weak drifts.

Filters Inverted Hammers to emphasize true supply pressure.

Highlights VI zones where institutional order flow left inefficiencies.

Differentiates strong engulfing reversals from weaker, low-participation moves.

Inputs & Customization

Inputs are grouped logically for fast configuration:

High-Volume Filter : Global lookback & multiple, per-pattern toggles.

FVG : Visibility, mitigated recolor, box style/transparency, label controls.

IB : Visibility, require high volume, mitigated recolor, colors, label settings.

Hammer / IH : Visibility, require high volume, mitigated recolor, wick/body thresholds.

VI : Visibility, require high volume, mitigated recolor, box style, labels, mitigation alerts.

Strong Bars : Enable/disable, separate colors for high-volume and low-volume outcomes.

Close Threshold Bars : Customizable close thresholds, labels, optional count markers.

MAs : EMA/SMA type, per-MA toggle, length, timeframe, color.

Alerts

New Bullish FVG (+)

New Bearish FVG (−)

New Inside Bar (IB)

New Hammer (H)

New Inverted Hammer (IH)

New Volume Imbalance (VI)

VI Mitigated

Strong Bullish Engulfing / Bearish Engulfing (high- and low-volume variants)

Suggested workflow

Choose your market & timeframe (script works across equities, futures, FX, crypto).

Toggle only the PACs you actually trade. Assign distinct colors for clarity.

Use MAs for directional bias and higher timeframe structure.

Enable High-Volume filters when you want to emphasize conviction.

Watch mitigation recolors to see which levels/zones have been interacted with.

Use alerts selectively for setups aligned with your plan.

Originality

Builds upon Super OrderBlock / FVG / BoS Tools (makuchaku & eFe) for FVG/box framework.

Expanded into a unified PAC toolkit including IB, H, IH, and VI patterns.

Brooks-inspired design: Patterns contextualized with volume and trend, not isolated.

Flexible high-volume gating with per-pattern toggles.

New VI integration with wick-based mitigation.

Strong Bar Coloring differentiates conviction vs weak reversals.

MTF-aware MAs prevent clutter while providing structure.

Open-source: Transparent for learning, editing, and extension.

Disclaimer

For educational and informational purposes only. This script is not financial advice. Trading carries risk—always test thoroughly before live use.

Volume Profile + VAH, VAL, and POCWhat it is

A clean, on-chart volume profile that approximates your visible range using a configurable Bars Back window. It builds a horizontal histogram of volume by price, splits each price bin into Buy vs Sell volume, draws POC, and computes Value Area High/Low (VAH/VAL). A Stealth Mode toggle switches to a subtle grayscale palette for low-key charts.

Why this instead of the built-in VPVR?

Buy/Sell split per bin: See which prices were defended by buyers vs sellers, not just total volume.

Value Area from POC outward: Classic expansion method until the selected % of total volume (default 70%).

Sleek borders & Stealth Mode: Crisp bin outlines and a one-click professional colorway.

Deterministic & fast: No sessions or anchors needed—set your Bars Back and go.

How it works (under the hood)

Window selection – Pine can’t read your viewport, so we approximate it with Bars Back (user input).

Binning – The window’s price range is divided into N bins.

Volume allocation – For each bar in the window:

Distribute Across Hi–Lo (optional): Spread volume across all bins the bar overlaps, weighted by overlap; or

Single-price mode: Assign all volume to one bin using a representative price (hlc3).

Buy/Sell split (two methods):

Body Proportional (recommended): Split by relative up/down body size (|close−open|).

Up/Down Candle: 100% buy if close ≥ open, else 100% sell.

POC & VA: Point of Control is the bin with max total volume. VAH/VAL expands from POC toward the higher-volume neighbor until the selected % of total volume is included.

Reading the visuals

Horizontal bars (right side): Total volume per price bin.

Left sub-segment = Sell volume

Right sub-segment = Buy volume

POC line: Price level with peak total volume.

VAH / VAL (dashed): Upper and lower bounds of the selected Value Area.

Borders: Each bin has a clean outer outline so the profile looks tight and organized.

Stealth Mode: Grayscale palette that preserves contrast without loud colors.

Key inputs (organized for clarity)

Theme

Stealth Mode: Toggles the grayscale look.

Core

Price Bins: Vertical resolution of the profile.

Lookback (Bars): Approximates your visible range.

Style

Profile Width (bars): How far the histogram extends to the right.

Bin Border Width: Outline thickness.

Markers & Lines

Show POC, Show VAH/VAL, Value Area %, VA line width.

Advanced

Distribute Volume Across Hi–Lo: More accurate, heavier compute.

Buy/Sell Split Method: Body Proportional (realistic) or Up/Down (simple).

Tips & best practices

Start with Body Proportional + Distribute Across ON for intraday accuracy.

If the chart lags, reduce Price Bins or Bars Back, or switch off distribution.

For small windows, fewer bins often looks cleaner (e.g., 30–60).

Stealth Mode plays nicely with both dark and light chart themes.

Limitations & notes

Viewport: Pine can’t access the actual visible bars; Bars Back is a practical stand-in.

Buy/Sell split: This is an approximation from candle bodies, not true bid/ask delta.

Designed for overlay; profile renders to the right of the latest bar.

Same-Direction Candles (Two Symbols)Same-Direction Candles (Two Symbols)

What it does

Highlights bars on your chart when two symbols print the same candle direction on the chosen timeframe:

Both Bullish → one color

Both Bearish → another color

Great for spotting synchronous moves (e.g., NQ & ES, QQQ & SPY), or confirming risk-on/risk-off with an inverse asset (e.g., NQ vs DXY with inversion).

How it works

For each bar, the script checks whether close > open (bullish), close < open (bearish), or equal (doji) for:

The chart’s symbol

A second symbol pulled via request.security() (optionally on a different timeframe)

If both symbols are bullish, it paints Bull color; if both are bearish, it paints Bear color. Dojis can be ignored.

Inputs

Second symbol: Ticker to compare (e.g., CME_MINI:ES1!, NASDAQ:QQQ, TVC:DXY).

Second symbol timeframe: Leave blank to use the chart’s TF, or set a specific one (e.g., 5, 15, D).

Invert second symbol direction?: Flips the second symbol’s candle direction (useful for inversely related assets like DXY vs indices).

Ignore doji candles: Skip highlights when either candle is neutral (open == close).

Coloring options: Toggle bar coloring and/or background shading; pick colors; set background transparency.

Alerts

Three alert conditions:

Both Bullish

Both Bearish

Both Same Direction (bullish or bearish)

Create alerts from the Add Alert dialog after adding the script.

Use cases

Index confluence: NQ & ES moving in lockstep

ETF confirmation: QQQ & SPY agreement

FX/Index risk signals: Invert DXY against NQ/ES to see when equity strength aligns with dollar weakness

Tips

For mixed timeframes (e.g., chart on 1m, ES on 5m), set Second symbol timeframe to the higher TF to reduce noise.

Keep Ignore dojis on for cleaner signals.

Combine with your own entry rules (structure, FVGs, liquidity sweeps).

Notes

Works on any symbol/timeframe supported by TradingView.

Overlay script; no strategy/entries/exits are executed.

Past performance ≠ future results; for education only.

Version: 1.0 – initial release (bar/background highlights, doji filter, inversion, multi-TF support, alerts).

Prev Day Close Line + Label — White Text / Royal Blue (v6)Previous Day Close line with clear labeling.

- Gap up vs PDC

- Gap down vs PDC

Helps analyze what yesterday attempted to do helps to confirm whether the attempt was successful.

Inside Candle DivergenceStudy Material: Inside Candle Divergence Indicator (aiTrendview)

1. Introduction

The Inside Candle Divergence Indicator is a custom tool built on TradingView using Pine Script. It is designed to help traders identify potential reversal points or trend continuations using a mix of candlestick analysis, RSI (Relative Strength Index), VWAP (Volume Weighted Average Price), Pivot Points, and Volume analytics. The tool also provides a dashboard table on the chart, summarizing all key values in a single glance for traders and analysts.

This indicator is not just a signal generator but also an educational framework—explaining how different concepts in technical analysis combine to build a systematic approach for market entries and exits.

________________________________________

2. Core Concepts Behind the Tool

A. Inside Candle Pattern

An Inside Candle forms when the current candle’s high is lower than or equal to the previous candle’s high, and the low is higher than or equal to the previous candle’s low.

• This means the entire price action of the current candle is "inside" the range of the previous candle.

• A bullish inside candle occurs when the close is higher than the open.

• A bearish inside candle occurs when the close is lower than the open.

This pattern shows market indecision but also sets up potential breakouts or trend reversals.

________________________________________

B. RSI (Relative Strength Index)

The indicator calculates RSI using the formula from the ta.rsi() function in TradingView. RSI helps measure momentum in the market.

• A low RSI (below 25) signals an oversold zone → possible buy.

• A high RSI (above 75) signals an overbought zone → possible sell.

By combining RSI with the Inside Candle, the indicator ensures that signals are triggered only when momentum and price patterns confirm each other.

________________________________________

C. Buy & Sell Signals

• Buy Signal: Triggered when RSI < Buy Level (default 25) and a bullish inside candle forms.

• Sell Signal: Triggered when RSI > Sell Level (default 75) and a bearish inside candle forms.

When triggered, the chart displays a BUY (green label below candle) or SELL (red label above candle) marker. The indicator also saves the entry price and signal bar for future reference inside the dashboard.

________________________________________

D. VWAP (Volume Weighted Average Price)

VWAP is calculated using the typical price (H+L+C)/3 and weighting it by volume.

• VWAP shows the average trading price weighted by volume, widely used by institutions.

• The tool calculates the distance of price from VWAP in % terms.

• If price is far above VWAP, the market may be overheated (overbought). If far below, it may be undervalued (oversold).

________________________________________

E. Volume Analysis

The tool splits volume into Buy Volume and Sell Volume:

• Buy Volume: If close > open.

• Sell Volume: If close ≤ open.

• Cumulative totals are maintained, and percentages are calculated to show what proportion of total market volume is bullish vs bearish.

• A progress bar style visual (using blocks █) shows the dominance of buyers or sellers.

This allows traders to quickly measure whether buyers or sellers are controlling the market trend.

________________________________________

F. Daily Pivot Points

Pivot Points are calculated using the previous day’s high, low, and close:

• Pivot = (High + Low + Close) / 3

• R1, S1, R2, S2, R3, S3 levels are derived from this pivot.

• These levels act as support and resistance zones.

The script plots Pivot, R1, and S1 lines on the chart for easy reference.

________________________________________

G. Trend Direction

The indicator checks where the price is compared to R1 and S1:

• If price > R1 → Bullish Trend

• If price < S1 → Bearish Trend

• Otherwise → Neutral Trend

The trend direction is displayed in the dashboard with arrows (↑, ↓, →).

________________________________________

H. Price Change Calculation

The tool calculates:

• Price Change = Current Close – Previous Close

• Percentage Change = (Change / Previous Close) × 100

• Displays ▲ (green upward) or ▼ (red downward) with the exact percentage.

This gives traders a quick snapshot of intraday price movement.

________________________________________

I. Dashboard Table

One of the most powerful features is the real-time dashboard table shown on the chart. It contains:

1. Symbol & Price Info (Current ticker, price, change %)

2. RSI Reading (with color coding: green for oversold, red for overbought)

3. VWAP and Distance from VWAP

4. Volume Analysis with Progress Bar (Buy vs Sell %)

5. Pivot Levels (Pivot, R1, S1)

6. Trend Direction (Bullish, Bearish, Neutral)

7. Signal Status (Last Buy/Sell signal with entry price)

This reduces the need for multiple indicators and gives traders a command-center view directly on the chart.

________________________________________

J. Alerts

The tool generates alerts whenever a Buy or Sell condition is met. Traders can set up TradingView alerts to be notified instantly when:

• Buy Signal Alert → RSI oversold + Bullish inside candle

• Sell Signal Alert → RSI overbought + Bearish inside candle

This ensures no opportunity is missed even if you’re not actively monitoring the chart.

________________________________________

K. Background Highlights

The chart background also changes faintly (light green or light red) when a Buy or Sell condition is triggered. This gives traders visual confirmation along with signals and alerts.

________________________________________

3. Practical Use of This Tool

• Scalpers & Intraday Traders can use it for quick momentum-based entries.

• Swing Traders can use the RSI + Inside Candle + Pivot Points to find medium-term reversals.

• Analysts can use the dashboard for real-time summaries in reports.

• Volume Analysis helps understand institutional activity.

Remember: This is not a standalone holy grail. It must be used with proper risk management and confirmation from higher timeframes.

________________________________________

4. Strict Disclaimer (aiTrendview)

⚠️ Disclaimer from aiTrendview:

This indicator is designed for educational and analytical purposes only. It is not financial advice or a guaranteed trading strategy. Markets are inherently risky and unpredictable; past performance of indicators does not ensure future results. Trading involves risk of financial loss, and traders must use proper risk management, stop-loss, and independent judgment.

aiTrendview strictly follows TradingView.com rules and compliance guidelines.

Any misuse of this tool, its code, or analytical features for unauthorized commercial purposes, false promises, or misleading activities is strictly discouraged. The creators of this script and aiTrendview will not be responsible for any losses, damages, or misuse arising from its application. Always trade responsibly and only with money you can afford to lose.

________________________________________

BPS Multi-MA 5 — 22/30, SMA/WMA/EMA# Multi-MA 5 — 22/30 base, SMA/WMA/EMA

**What it is**

A lightweight 5-line moving-average ribbon for fast visual bias and trend/mean-reversion reads. You can switch the MA type (SMA/WMA/EMA) and choose between two ways of setting lengths: by monthly “session-based” base (22 or 30) with multipliers, or by entering exact lengths manually. An optional info table shows the effective settings in real time.

---

## How it works

* Calculates five moving averages from the selected price source.

* Lengths are either:

* **Multipliers mode:** `Base × Multiplier` (e.g., base 22 → 22/44/66/88/110), or

* **Manual mode:** any five exact lengths (e.g., 10/22/50/100/200).

* Plots five lines with fixed legend titles (MA1…MA5); the **info table** displays the actual type and lengths.

---

## Inputs

**Length Mode**

* **Multipliers** — choose a **Base** of **22** (≈ trading sessions per month) or **30** (calendar-style, smoother) and set **×1…×5** multipliers.

* **Manual** — enter **Len1…Len5** directly.

**MA Settings**

* **MA Type:** SMA / WMA / EMA

* **Source:** any series (e.g., `close`, `hlc3`, etc.)

* **Use true close (ignore Heikin Ashi):** when enabled, the MA is computed from the underlying instrument’s real `close`, not HA candles.

* **Show info table:** toggles the on-chart table with the current mode, type, base, and lengths.

---

## Quick start

1. Add the indicator to your chart.

2. Pick **MA Type** (e.g., **WMA** for faster response, **SMA** for smoother).

3. Choose **Length Mode**:

* **Multipliers:** set **Base = 22** for session-based monthly lengths (stocks/FX), or **30** for heavier smoothing.

* **Manual:** enter your exact lengths (e.g., 10/22/50/100/200).

4. (Optional) On **Heikin Ashi** charts, enable **Use true close** if you want the lines based on the instrument’s real close.

---

## Tips & notes

* **1 month ≈ 21–22 sessions.** Using 30 as “monthly” yields a smoother, more delayed curve.

* **WMA** reacts faster than **SMA** at the same length; expect earlier signals but more whipsaws in chop.

* **Len = 1** makes the MA track the chosen source (e.g., `close`) almost exactly.

* If changing lengths doesn’t move the lines, ensure you’re editing fields for the **active Length Mode** (Multipliers vs Manual).

* For clean comparisons, use the **same timeframe**. If you later wrap this in MTF logic, keep `lookahead_off` and handle gaps appropriately.

---

## Use cases

* Trend ribbon and dynamic bias zones

* Pullback entries to the mid/slow lines

* Crossovers (fast vs slow) for confirmation

* Volatility filtering by spreading lengths (e.g., 22/44/88/132/176)

---

**Credits:** Built for clarity and speed; designed around session-based “monthly” lengths (22) or smoother calendar-style (30).

Liquidity-Weighted Business Cycle (Satoshi Global Base)🌍 BTC-Affinity Global Liquidity Business Cycle (MACD Model)

This indicator models Bitcoin’s macroeconomic business cycle using a BTC-weighted global liquidity index as its foundation. It adapts a MACD-based framework to visualize expansions and contractions in fiat liquidity across major economies with high Bitcoin affinity.

🔍 What It Does:

🧠 Constructs a Global M2 Liquidity Index from the top 10 most BTC-relevant fiat currencies

(USD, EUR, JPY, GBP, INR, CNY, KRW, BRL, CAD, AUD)

— each weighted by its Bitcoin adoption score and FX-converted into USD.

📊 Applies a MACD (Moving Average Convergence Divergence) signal to the index to detect macro liquidity trends.

🟢 Plots a histogram of business cycle momentum (red = expansion, green = contraction).

🔴 Marks potential cycle peaks, useful for macro trading alignment.

⚖️ BTC Affinity-Weighted Countries:

🇺🇸 United States

🇪🇺 Eurozone

🇯🇵 Japan

🇬🇧 United Kingdom

🇮🇳 India

🇨🇳 China

🇰🇷 South Korea

🇧🇷 Brazil

🇨🇦 Canada

🇦🇺 Australia

Weights are user-adjustable to reflect evolving capital controls, regulation, and real-world BTC adoption trends.

✅ Use Cases:

Confirm macro risk-on vs risk-off regimes for BTC and crypto.

Identify ideal entry and exit zones in macro pair trades (e.g., MSTR vs MSTY).

Monitor how global monetary expansion feeds into BTC valuations.

Time Based Range CandleThis indicator creates a visual candle representation from price action during a specified time period.

Key Features:

Configurable Sessions: Set any calculation period (when range is measured) and display period (when visualization appears)

Candle Visualization: Draws a large candle showing open, close, high, low with proper body coloring

Wick/Tail Analysis: Displays wicks and tails with quarter-level subdivisions based on candle type (bullish vs bearish)

End Marker: Vertical line marks exactly when the calculation period ends

Quarter Lines: Optional dotted/dashed lines showing 25%, 50%, 75% levels within body, wicks, and tails

Common Use Cases:

Overnight range analysis (18:00 - 6:00 ET) displayed during regular hours

Session-based range trading (Asian, London, NY sessions)

Custom time period analysis for any market

The indicator follows proper candle terminology where wicks and tails are measured differently for bullish vs bearish candles, making it useful for precise level analysis and range trading strategies.

MSS BoxesWhat it is

The MSS Boxes indicator finds Market Structure Shifts (a decisive break in structure with displacement) and draws actionable zones (“boxes”) from the candle that caused the shift. Those boxes then act as mitigation / continuation areas for the rest of the session (or until they’re invalidated). It’s designed to be clean, non-repainting, and to work as a confluence layer with your SD and ATR Trigger grids.

What you’ll see on the chart

Green boxes for bullish MSS (demand); red boxes for bearish MSS (supply).

A compact label at the box origin (e.g., BOS↑ / BOS↓, or CHOCH) with the time-frame tag if you enable MTF.

Optional status badge on the right edge:

active (untouched), mitigated (tapped and respected), invalid (closed through), expired.

Clean behavior: once a box is printed it does not slide; coordinates are fixed to the confirmed signal candle.

Inputs (quick guide)

Swing detection

Swing length (for swing highs/lows), lookback for break validity, strict wick rule on/off.

Displacement factor (0 = off; typical 1.2–2.0).

Box recipe

Use full wick vs. use body for top/bottom.

Minimum box height (ticks), auto-merge overlapping (joins adjacent boxes of the same side).

Max lifetime (bars), session reset (e.g., clear on NY 18:00).

MTF alignment

Toggle H1 / M15 filters; choose “Plot only when aligned” vs “Plot all but alert only when aligned.”

Visuals

Fill/outline colors, opacity, label size, extend style (full-width vs to last bar).

Six Meridian Divine Swords [theUltimator5]The Six Meridian Divine Sword is a legendary martial arts technique in the classic wuxia novel “Demi-Gods and Semi-Devils” (天龙八部) by Jin Yong (金庸). The technique uses powerful internal energy (qi) to shoot invisible sword-like energy beams from the six meridians of the hand. Each of the six fingers/meridians corresponds to a “sword,” giving six different sword energies.

The Six Meridian Divine Swords indicator is a compact “signal dashboard” that fuses six classic indicators (fingers)—MACD, KDJ, RSI, LWR (Williams %R), BBI, and MTM—into one pane. Each row is a traffic-light dot (green/bullish, red/bearish, gray/neutral). When all six align, the script draws a confirmation line (“All Bullish” or “All Bearish”). It’s designed for quick consensus reads across trend, momentum, and overbought/oversold conditions.

How to Read the Dashboard

The pane has 6 horizontal rows (explained in depth later):

MACD

KDJ

RSI

LWR (Larry Williams %R)

BBI (Bull & Bear Index)

MTM (Momentum)

Each tick in the row is a dot, with sentiment identified by a color.

Green = bullish condition met

Red = bearish condition met

Gray = inside a neutral band (filtering chop), shown when Use Neutral (Gray) Colors is ON

There are two lines that track the dots on the top or bottom of the pane.

All Bullish Signal Line: appears only if all 6 are strongly bullish (default color = white)

All Bearish Signal Line: appears only if all 6 are strongly bearish (default color = fuchsia)

The Six Meridians (Indicators) — What They Mean:

1) MACD — Trend & Momentum

What it is: A trend-following momentum indicator based on the relationship between two moving averages (typically 12-EMA and 26-EMA)

Logic used: Classic MACD line (EMA12−EMA26) vs its 9-EMA signal.

Bullish: MACD > Signal and |MACD−Signal| > Neutral Threshold

Bearish: MACD < Signal and |diff| > threshold

Neutral: |diff| ≤ threshold

Why: Small crosses can whipsaw. The neutral band ignores tiny separations to reduce noise.

Inputs: Fast/Slow/Signal lengths, Neutral Threshold.

2) KDJ — Stochastic with J-line boost

What it is: A variation of the stochastic oscillator popular in Chinese trading systems

Logic used: K = SMA(Stochastic, smooth), D = SMA(K, smooth), J = 3K − 2D.

Bullish: K > D and |K−D| > 2

Bearish: K < D and |K−D| > 2

Neutral: |K−D| ≤ 2

Why: K–D separation filters tiny wiggles; J offers an “extreme” early-warning context in the value label.

Inputs: Length, Smoothing.

3) RSI — Momentum balance (0–100)

What it is: A momentum oscillator measuring speed and magnitude of price changes (0–100)

Logic used: RSI(N).

Bullish: RSI > 50 + Neutral Zone

Bearish: RSI < 50 − Neutral Zone

Neutral: Between those bands

Why: Centerline/adaptive bands (around 50) give a directional bias without relying on fixed 70/30.

Inputs: Length, Neutral Zone (± around 50).

4) LWR (Williams %R) — Overbought/Oversold

What it is: An oscillator similar to stochastic, measuring how close the close is to the high-low range over N periods

Logic used: %R over N bars (0 to −100).

Bullish: %R > −50 + Neutral Zone

Bearish: %R < −50 − Neutral Zone

Neutral: Between those bands

Why: Uses a centered band around −50 instead of only −20/−80, making it act like a directional filter.

Inputs: Length, Neutral Zone (± around −50).

5) BBI (Bull & Bear Index) — Smoothed trend bias

What it is: A composite moving average, essentially the average of several different moving averages (often 3, 6, 12, 24 periods)

Logic used: Average of 4 SMAs (3/6/12/24 by default):

BBI = (MA3 + MA6 + MA12 + MA24) / 4

Bullish: Close > BBI and |Close−BBI| > 0.2% of BBI

Bearish: Close < BBI and |diff| > threshold

Neutral: |diff| ≤ threshold

Why: Multiple MAs blended together reduce single-MA whipsaw. A dynamic 0.2% band ignores tiny drift.

Inputs: 4 lengths (default 3/6/12/24). Threshold is auto-scaled at 0.2% of BBI.

6) MTM (Momentum) — Rate of change in price

What it is: A simple measure of rate of change

Logic used: MTM = Close − Close

Bullish: MTM > 0.5% of Close

Bearish: MTM < −0.5% of Close

Neutral: |MTM| ≤ threshold

Why: A percent-based gate adapts across prices (e.g., $5 vs $500) and mutes insignificant moves.

Inputs: Length. Threshold auto-scaled to 0.5% of current Close.

Display & Inputs You Can Tweak

🎨 Use Neutral (Gray) Colors

ON (default): 3-color mode with clear “no-trade”/“weak” states.

OFF: classic binary (green/red) without neutral filtering.

Volume Imbalance Analyzer - 70% & 80% Version1.01Here’s a clean “definition” you can drop into your docs. It explains **what** the indicator is, **what it helps with**, and **how** to use it—plain and practical.

# Definition

**Volume Imbalance Analyzer (70% & 80%)** flags bars where estimated buy vs. sell volume is heavily one-sided. It colors those bars, adds labels (B70/B80 or S70/S80), and can alert you in real time. The goal is to quickly spot spots of **aggressive participation** (buyers or sellers) that often act as magnets for a **retest** or as **exhaustion/continuation** areas.

# What it helps you do

* **Find high-energy bars** where one side dominates (potential turning or continuation points).

* **Plan retests:** Track when price comes back into the imbalance candle’s range (common entry/take-profit logic).

* **Filter trades:** Only act when the market shows unusual pressure (≥70% or ≥80%).

* **Add context to setups:** Combine with S/R, FVGs, or trend tools to time entries with less guesswork.

* **Alert-driven workflow:** Get notified the moment extreme pressure prints.

# How it helps (workflow)

1. **Scan for signals:**

* **B80/B70** = strong buying; **S80/S70** = strong selling.

* 80% is “extreme” and overrides 70%.

2. **Mark the zone:** The imbalance candle’s **high–low** defines a zone. Many traders wait for a **retest** into that range.

3. **Decide intent:**

* After **B80/B70**, look for pullbacks to buy (or fades if you see exhaustion).

* After **S80/S70**, look for rallies to sell (or fades if exhaustion).

4. **Confirm with context:** Check trend, key levels, liquidity, session timing, ATR/volatility.

5. **Manage risk:** Place stops beyond the zone; size trades so a failed retest doesn’t ruin the day.

# How it works (under the hood, briefly)

The script **estimates buy/sell volume** from each candle’s body, wicks, and total volume, then computes an **imbalance %**. If the % crosses **70%** or **80%** (scaled by a Sensitivity setting), it paints the bar, drops a label, and optionally fires an alert. It also stores the imbalance candle’s range so you can watch for a **retest**.

# Reading the signals (quick guide)

* **B80**: Extreme buyer pressure → watch for pullback buys or exhaustion shorts, depending on context.

* **B70**: Strong buyer pressure → mild continuation bias.

* **S80**: Extreme seller pressure → watch for rally sells or exhaustion longs.

* **S70**: Strong seller pressure → higher reversal probability noted in the table (informational).

# Configuration tips

* **Sensitivity**: Higher = more bars qualify (more signals).

* **Label distance**: Scales with ATR so labels don’t overlap candles.

* **Colors/opacity**: Separate for 70% vs 80% and buyer vs seller.

* **Alerts**: Enable to catch signals live without staring at the screen.

# Notes & limits

* Uses **estimation** (not true bid/ask) on most symbols; treat as a **context tool**, not a stand-alone system.

* The optional stats table’s “expected outcomes” are **informational**, not live probabilities.

* Works on any timeframe; results improve when combined with structure and risk controls.

Candle AnalyzerThis tool classifies candles based on their body size and wick proportions, helping you quickly identify:

"Strong" Candles: When the body dominates, showing clear bullish or bearish momentum.

"Rejection" Candles: Long wicks indicate price was pushed back, suggesting potential reversals.

"Indecisive" Candles: When neither buyers nor sellers are clearly in control, or if wicks are balanced.

"Doji/Indecision": Very small or non-existent bodies, highlighting significant uncertainty.

Features

Manual Entry Time (Defaults to NY Open): The indicator analyzes the candle at this specific time.

Current Bar Analysis: This feature classifies the current, developing candle in real-time.

Analysis Table: A table displays details for the last four completed bars, including body size and wick percentages.

Customizable Thresholds: Adjust the "Min Body vs Wick %" and "Dominant Wick vs Body Ratio" to fine-tune how "strong" or "rejection" candles are identified.

Impulse Convexity Trend Gate [T1][T69]OVERVIEW 🧭

• A price-only trend engine that opens a “gate” only when trend strength, acceleration, and impulse dominance align.

• Built from three cooperating parts: adaptive slope, directional convexity, and an impulse-vs-pullback ratio.

• Output is a bounded oscillator (−100…+100) plus side-specific gate states (bull/bear), with optional pullback and weakness highlights.

THE IDEA & USEFULNESS 🧪

• Not a simple mashup: each component plays a distinct role—slope for direction, convexity for acceleration agreement, and an impulse ratio to suppress correction noise.

• Adaptive EMA length (series-based) lets the midline adjust to conditions without external indicators.

• Approximation of hyperbolic tangent and clamp keep signals bounded and stable while avoiding library dependencies.

• Designed to help trend traders act only when continuation is likely, and stand down during pullbacks or chop.

HOW IT WORKS (PIPELINE) ⚙️

• Price transform

• Uses log price for scale stability.

• Adaptive midline

• Volatility-aware EMA length is clamped between minimum and maximum, then applied via a custom recursive EMA.

• Slope & convexity

• Slope (first difference of the midline) defines direction; convexity (second difference) verifies acceleration agrees with that direction.

• Impulse vs pullback ratio (R)

• Sums directional progress versus counter-direction pullbacks over a window; requires impulse to dominate.

• Normalization & score

• Slope and convexity are normalized by recent dispersion; combined into a raw score and squashed to −100…+100 using manual tanh.

• Trend gate

• Gate opens only when: R ≥ threshold, |normalized slope| ≥ threshold, and slope/convexity share the same sign.

• States & visuals

• Bull/Bear Gate Entry when gate is open, oscillator crosses ±15 in the correct direction, price is on the correct side of the midline, and slope/convexity agree.

• Pullbacks mark counter-moves while a gate is active; Weakness flags specific fade patterns after pullbacks.

FEATURES ✨

• Bull and Bear Gate Entries (green/red columns).

• Pullback shading and optional trend-weakness highlights (yellow/orange + teal/maroon).

• Background tint reflects the active side (bull or bear).

• Pure price logic; no volume or external filters required.

HOW TO USE 🎯

• Regime filter

• Trade only in the direction of the open gate; ignore signals when the gate is closed.

• Pullback entries

• During an open gate, wait for a pullback zone, then act on trend-resumption (e.g., oscillator re-push through ±15 or structure break in gate direction).

• Exits & risk

• Consider trimming when the oscillator relaxes toward 0 while the gate remains open, or when convexity flips against slope and R deteriorates.

• Timeframes & markets

• Suited for trend following on crypto/FX/indices from M30 to 4H/1D; raise thresholds on lower timeframes to reduce noise.

CONFIGURATION 🔧

• Impulse ratio gate (R ≥): raises/lowers the standard for continuation dominance.

• Slope strength gate (|sN| ≥): controls how strong a slope must be to count.

• Show Pullback Impulse (toggle): enable/disable pullback highlights.

• Show Trend Weakness (toggle): enable/disable weakness flags.

LIMITATIONS ⚠️

• As a trend tool, it can lag at regime transitions; expect whipsaws in tight ranges.

• Parameters are instrument- and timeframe-dependent; tune thresholds before live use.

• Pullback/weakness flags are contextual—not trade signals by themselves; use them with gate state and your execution rules.

ADVANCED TIPS 🛠️

• Tighten R and slope thresholds for lower timeframes; loosen for higher timeframes.

• Pair with NNFX-style money management and pair-level filters; let the gate be the confirmation layer, not the entry trigger by itself.

• Batch-test across 100+ symbols, export metrics, and run Monte Carlo to validate LLN reliability and Sharpe/IQR stability.

• For system hedging, disable entries when both sides trigger on the same asset to avoid internal conflict.

NOTES 📝

• Price-only construction reduces data-vendor differences and keeps behavior consistent across markets.

• Manual tanh/clamp ensure stable, bounded scores even during extremes.

DISCLAIMER 🛡️

• For research and education. No financial advice. Test thoroughly, size conservatively, and respect your risk rules.

Projected 65min VolumeThe script provides relative volume for the first 5min candle after its close vs 14 avg and estimates projected volume for the first 65min candle in the trading session vs avg value.

!!!The indicator is designed to work only at 5min TF!!!

Multi-Timeframe Bias Dashboard + VolatilityWhat it is: A corner table (overlay) that gives a quick higher-timeframe read for Daily / 4H / 1H using EMA alignment, MACD, RSI, plus a volatility gauge.

How it works (per timeframe):

EMA block (50/100/200): “Above/Below/Mixed” based on price vs all three EMAs.

MACD: “Bullish/Bearish/Neutral” from MACD line vs Signal and histogram sign.

RSI: Prints the value and an ↑/↓ based on 50 line.

Volatility: Compares ATR(14) to its SMA over 20 bars → High (>*1.2), Normal, Low (<*0.8).

Bias: Combines three votes (EMA, MACD, RSI):

Bullish if ≥2 bullish, Bearish if ≥2 bearish, else Mixed.

Display:

Rows: D / 4H / 1H.

Columns: Bias, EMA(50/100/200), RSI, MACD, Volatility.

Bias cell is color-coded (green/red/gray).

Position setting lets you park the table in Top Right / Bottom Right / Bottom Left (works on mobile too).

Use it for:

Quickly aligning intraday setups with higher-TF direction.

Skipping low-volatility periods.

Confirming momentum (MACD/RSI) when price returns to your OB/FVG zones.