Profiling: array of UDTs vs UDT of arraysUsing Stopwatch Library by PineCoders, I am trying to test which is faster, an array of user-defined type (UDT) objects vs an object with many child arrays.

The task is to store and manipulate array of objects having total 9 values: 4 floats, 4 strings and 1 int.

Option 1: create a UDT with 9 fields and store an array of such UDT objects.

Option 2: create a UDT with 9 arrays individually for each value.

The test task is of three stages:

Populate array(s) with some (timenow) values - in the options you can choose how many values to push into the array/arrays. Note that max size of array(s) is set independently, so you can push 1000 of elements into an array capped at 100 max size and as new elements will be pushed (added to the end) the old exceeding elements will be shifted (removed from the beginning)

Write - write to random elements of the array. Two options for writing to a UDT object: (1) assign to each field independently, (2) create a UDT object and use array.set() function.

Read - read from random elements of the array.

In the options you can how many times per bar to run each of the steps (same number for each step).

I tested by adding three indicators to the chart and choosing different options for each:

1. Array of UDT's where writing is done by creating a new UDT from the values and then using set(udt)

2. Array of UDT's where writing is done by assigning the value of each of the properties of the UDT individually (saving time on creating of a new object).

3. UDT of arrays.

As of 16 Arpil 2023 the UDT of arrays seems about 20-30% faster than the array of UDT's with setting each property without creating new UDT object.

Cari dalam skrip untuk "神户胜利+VS+磐田喜悦"

ILM Overnight vs Intraday Performance - Tabular FormUse this indicator on Daily Timeframe

This script compares Overnight vs Intraday Performance based on the Day of the Week (DOW) - Sun - Sat of index/stock/currency/commodity symbols.

ON column indicates Overnight performance = open/close -1

ID column indicates Intraday performance = close-open/1

The calculations are detailed in the tooltips of the individual table cells.

Perp vs SpotJust a basic comparison of perps price vs spot price, you can select which exchanges for comparison

Crude Oil: Backwardation Vs ContangoCrude Oil, CL

Plots Futures Curve: Futures contract prices over the next 3.5 years; to easily visualize Backwardation Vs Contango(carrying charge) markets.

Carrying charge (contract prices increasing into the future) = normal, representing the costs of carrying/storage of a commodity. When this is flipped to Backwardation(As the above; contract prices decreasing into the future): it's a bullish sign: Buyers want this commodity, and they want it NOW.

Note: indicator does not map to time axis in the same way as price; it simply plots the progression of contract months out into the future; left to right; so timeframe DOESN'T MATTER for this plot

TO UPDATE (every year or so): in REQUEST CONTRACTS section, delete old contracts (top) and add new ones (bottom). Then in PLOTTING section, Delete old contract labels (bottom); add new contract labels (top); adjust the X in 'bar_index-(X+_historical)' numbers accordingly

This is one of several similar Futures Curve indicators: Meats | Metals | Grains | VIX | Crude Oil

If you want to build from this; to work on other commodities; be aware that Tradingview limits the number of contract calls to 40 (hence the multiple indicators)

Tips:

-Right click and reset chart if you can't see the plot; or if you have trouble with the scaling.

-Right click and add to new scale if you prefer this not to overlay directly on price. Or move to new pane below.

-If this takes too long to load (due to so many security calls); comment out the more distant future half of the contracts; and their respective labels. Or comment out every other contract and every other label if you prefer.

--Added historical input: input days back in time; to see the historical shape of the Futures curve via selecting 'days back' snapshot

updated 20th June 2022

© twingall

RSI vs Longs/Shorts Margin Ratio Percentage RankThis indicator plots the RSI of the current token and the percentage rank, of the RSI, of the ratio of a long margined token to a short margined token.

By default it plots the RSI of the current token with a color based on percentage rank the RSI of BITFINEX:BTCUSDLONGS divided by BITFINEX:BTCUSDSHORTS, so the assumption is that you are using it on a BTC chart. While you can select any Tradingview symbol for your Long and Short tokens I don't think you will get meaningful results unless you select a long and short margined token that matches your chart symbol, such as BITFINEX:ETHUSDLONGS and BITFINEX:ETHUSDSHORTS if you're trading ETHUSD. Even using margined tokens the results may not be meaningful, if there is not enough trade volume in the token, or if they are being manipulated, so you must backtest everything.

The three plot options are:

• Colored RSI - RSI plotted with colors based on the Longs/Shorts ratio

• Background Color - White RSI plot with Longs/Shorts ratio as background color

• RSI + Ratio - White RSI with Longs/Shorts ratio plotted in color

The chart shows all three options on an hourly BITFINEX:SOLUSD chart with BITFINEX:SOLUSDSHORTS and BITFINEX:SOLUSDLONGS.

By default it also plots a short term moving average and it can also plot the raw ratio rather than the percentage rank if selected.

This script started out as "RSI vs BITFINEX BTC Longs/Shorts Margin Ratio Percentage Rank" by me. I was interested in the ratio of BITFINEX:BTCUSDLONGS to BITFINEX:BTCUSDSHORTS as a measure of market sentiment and how that sentiment would magnify RSI changes. The volatility of the BTCUSDLONGS : BTCUSDSHORTS ratio was too low to get a good read, using a percent rank of the RSI of the ratio made the results more visible. After a discussion with @jason5480 I saw how opening it up to all margined Long / Short pairs was the best way forward. Unfortunately the name no longer matched the script, so I had to publish a new script.

NYSE New Highs vs New LowsNYSE New Highs vs New Lows is a simple market breadth indicator that compares HIGN, the number of new highs during that day, and LOWN, the number of new lows. The new highs are on top and lows are appropriately on bottom. Without averaging, it's a little chaotic so you can smooth them out as much as you want, and the top-right label shows how much you're smoothing.

Interpretation:

Essentially, we use $SPY or $QQQ as a proxy for what's going on in the market, but because the FAANG stocks are so heavily weighted, it's not always representative. If SPY is flat/down, but there are 200 new highs today, then one of the big boys is weighing down an otherwise very bullish market. It's like looking at one of those heatmap charts, but in a single number.

Bullish Trend

- Lots of new highs

- Very few new lows

Bearish Trend

- Lots of new lows

- Very few new highs

Potential Reversal

- Too high, 250+

- Too low, 150+

Open Interest Divergence (OI vs Price)This indicator show having increasing Open Interest but price still move in a range (Open Interest Divergence vs price).

It is same with Divergence of indicators as RSI Divergence, Macd Divergence, .... It is easy to understand.

Additional, with MA line OI, you can see the change of OI.

Up Volume vs Down VolumeCalculating NYSE Up Volume (UPVOL.NY) vs NYSE Down Volume (DNVOL.NY). The triangles appear when the ratio exceeds 90% in either direction.

Also has the option to switch to NQ, US, DJ, AM, or AX tickers.

Credit to @MagicEins for the original script:

ATR vs Day Trading Range and PercentageThis indicator displays the Current Daily ATR vs the current Day Range and displays the percentage.

For example if the Daily ATR is $5 and the current range of the day is $10 this would be 200% the original move.

It is color coded (and can be modified) to change color when the Daily range is over 100% the ATR.

The time frame can be changed from Daily just be aware you must be on a lower timeframe then selected. So if you want to compare the current 30 minute ATR to the current 30 minute range you will need to be showing a 30 min chart or lower for it to calculate correctly.

3GBH BTC DOM vs MCBitcoin Market Cap vs Dominance

- data normalized with RSI

Included in this indicator:

- RSI of BTC Market Cap

- RSI of BTC Dominance

- EMA of BTC Market Cap

- EMA of BTC Domiance

-----

Dominance influences the market. Is money flowing into Bitcoin?

-----

EMA's to help with Technical Analysis.

-----

User-friendly.

You can change all the inputs, they are labelled for ease-of-use.

You can toggle On/Off any or all of the options.

Higher vs Lower Pivots overlayA simple script that I made that draws lines between the high and low pivots. The color of the line define if the pivot is higher or lower than the previous pivot. The main thing to tune is the pivot look back vs look ahead, which are the same params used by the tradingview pivot indicator. There are several other params you can tweaks to get the look you want.

DTR vs ATR w RVolDTR vs ART along with Relative Volume in Percentage. So if you see RVol as 200% with input length of 10 days, today's volume is 2x compared to past 10 days. It helps if today's volume is already reached 20% or 30% within 30mins of market open, etc.

Perp vs Spot Delta (Bybit-CB)Simple script showing the delta of Bybit BTCUSD perp vs Coinbase BTCUSD spot. Orange positive candles show bybit is higher, blue negative candles show Coinbase is higher.

LER - Law of Effort vs ResultsLaw of Effort vs Results is a tool to find the price changes based on volume.

This tool shows that if there is a high volume occur but the price has small difference in one candle, this will trigger a 'spike'. This spike represents that a high activity has occurred but the price did not reflect as the volume changes.

The analogy of this tool can be represented as we drive a car on a steep hill: despite we hit the gas harder, the car just slightly move higher.

NYSE Volume UP FLOW VS Down FLOW ULTIMATE VOLDNYSE Volume UP FLOW VS Down FLOW ULTIMATE StokedStocks

BASED OFF THE VOLD INDEX

The VOLD (also $VOLD) is the difference between the up volume and down volume on the NYSE. i.e. NYSE $UVOL minus $DVOL; the net up volume.

If you consider that VOLD is the net value between UVOL (up volume) and DVOL (down volume) then you need to understand these two to understand VOLD.

UVOL or DVOL are a total of the volume on all stocks that are up or down in price. Up or down is based on the previous session's closing price. The size of the stock's price change is irrelevant.

If the stock is up only $.01, then its volume is grouped into the UVOL total. If that stock's price then drops by $.02 it will be down $.01 and the day's volume for that stock will now be grouped with the DVOL total.

Note that when a stock moves from being an up stock to a down stock its volume will be removed from the UVOL total and added to the DVOL total. Say the stocks volume is 1 million shares when it moves from up to down. The DVOL will increase by 1 million and the UVOL will decrease by 1 million which means that VOLD will decrease by 2 million.

NYSE Up/Down Volume Ratio is often used as a barometer for stocks trading on all U.S. Exchanges even though it is calculated based on stocks listed on the New York Stock Exchange.

NYSE Up/Down ratio represents the volume of NYSE stocks that are advancing divided by the volume of declining stocks.

The volume of advancing stocks or upside volume is the sum of the volume or the number of shares traded associated with stocks that closed higher.

The downside volume is the total number of shares traded that are associated with stocks that closed lower.

The interpretation of the NYSE Up/Down ratio is rather simple. A value higher than one indicates that there is more volume associated with up stocks than with down stocks and it is usually interpreted as a bullish signal.

Obviously, a bearish signal occurs when the NYSE Up/Down ratio is lower than one, which tells us that there are more volume associated with down stocks than with up stocks.

Check out my other indicators and website stokedstocks.wordpress.com for tons of free stock training books and pictures and settings

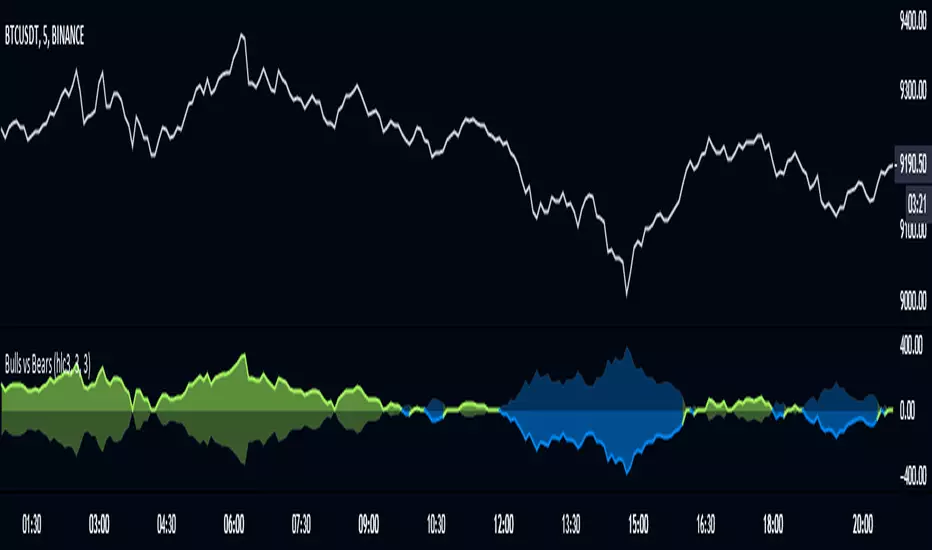

Bulls vs BearsThe script measures relative strenth of bull bars vs bear bars that complete the next rules:

1) rising price with rising volume calculates as bullish only if the next candle is higher

2) falling price with falling volume calculates as bullish only if the next candle is higher

3) rising price with falling volume calculates as bearish only if the next candle is lower

4) falling price with rising volume calculates as bearish only if the next candle is lower

examples

ethusdt

shitperp

bsvusdt

btcusdt

Strategy VS Buy & HoldSUMMARY:

A strategy wrapper that makes a detailed and visual comparison between a given strategy and the buy & hold returns of the traded security.

DESCRIPTION:

TradingView has a "Buy & Hold Return" metric in the strategy tester that is often enough to assess how our strategy compares to a simple buy hold. However, one may want more information on how and when your strategy beats or is beaten by a simple buy & hold strategy. This script aims to show such detail by providing a more comprehensive metrics and charting the profit/loss of the given strategy against buy & hold.

As seen in the script, it plots/draws 4 elements:

1) Strategy P/L: strategy net profit + strategy open profit

2) Buy & Hold P/L: unrealized return

3) Difference: Strategy P/L - Buy & Hold P/L

4) Strategy vs Buy Hold Stats

> Percent of bars strategy P/L is above Buy & Hold

> Percent of bars strategy P/L is below Buy & Hold

> All Time Average Difference

ADJUSTABLE PARAMETERS:

All labels/panels can be disabled by unchecking these two options:

>bnh_info_panel = input(true, title='Enable Info Panel')

>bnh_indicator_panel = input(true, title='Enable Indicator Panel')

Comparison Date Range can be changed to better isolate specific areas:

>From Year, From Month, From Day

default: 1970 01 01

>To Year, To Month, To Day

default: 2050 12 31

Default settings basically covers all historical data.

HOW TO USE:

The default script contains a simple 50-200 SMA cross strategy, just delete and replace it. Those are everything between these lines:

/////////////////////////////////////////////////////////////////////////////////////

//////////////////////////////STRATEGY SCRIPT START//////////////////////////////////

(STRATEGY SCRIPT GOES HERE)

//////////////////////////////STRATEGY SCRIPT END////////////////////////////////////

/////////////////////////////////////////////////////////////////////////////////////

Removing all plots and drawings from your strategy is advisable.

If you are going to use the Comparison Date Range, apply "bnh_timeCond" to your strategy to align the dates. A sample on how it’s applied can be seen on the Placeholder MA cross strategy.

Note: bnh_timeCond returns a boolean series

High and lows round vs full numbersLiterally the name, just checks if a high or low is a full number or decimal (i.e 100.5) then shows the percentage of full number highs vs percentage of full number lows.

I couldn't really find anything useful with it but maybe someone else can

Range: OHLC vs Previous OHLC - Version 2Version 1 here -

This is essentially the same as version 1 with one update. You have the freedom to independently choose OHLC for current candle and prior candle.

To elaborate further, Version 1 had 1 choice. For example, Close; you could only compare the close of prior candle to the current candle.

Version 2; you can compare close of the current candle to the low of the prior candle.

stock gain% vs index gain %This shows the relative strength or weakness of a stock vs an index on any given candle price movement.

Negative stock candle and relative strength shows accumulation

Positive stock candle and relative weakness shows distribution

accumulation will plot an 'A'

distribution will plot a 'D'