KingEMA8-21-55-89I used the moving average with the habit of 21-55, so added two moving average, one is the short line 8EMA, the other is the medium and long line 89ema

Explain the application of moving averages through the disk surface:

When the price runs above 89, it only looks for the buy signal.

When the price runs below 89, it only looks for sell signals.

The first step up through the 89 moving average after the first confirmation can buy homeoply,

The first pull down after crossing the 89 moving average for the first time confirms that it can be sold in line with the trend.

Price horizontal finishing, moving average frequently across the field observation.

The yellow area in the interval from 8 to 21 is the homeopathic warehouse addition signal.

When the price is above the 89 moving average, the k-line closes below the 21-day moving average as a callback signal

Prices below the 89 ema close above the 21 - day ema as a rebound signal

After the correction and rebound signals come out, we should make half of the profit and the other half of the stop loss in the break-even place.

Moving average is very suitable for the trend of strong varieties, is not suitable for volatile market.

Only at the end of the shock market moving average upward or downward divergent when it is possible to be used.

1. Repeatedly entangle the mean line of horizontal disk stage and observe it from the field

2. Sell the three EMA moving averages when they can't exceed 89EMA with downward crossing

3, many times can not break the new low when prices go sideways profit

4. Buy when the price reaches 89EMA after the convergence of triangle 3 is broken

5, the Angle of price rise slowed and closed below the 21 moving average when profit

6. Left field observation during transverse oscillation.

Sit tight while news or data cause prices to fall quickly

8. Buy when the price triangle breaks through the 89 moving average upward

9, the price does not rise to slow down when the horizontal closed below the 21 moving average when profit

10, price horizontal shock finishing at the same time the average line also transverse finishing field observation

11, the price of the triangle after finishing through the 89 moving average to buy.At this point all the averages have turned up

12, the second time can not break through the new high when the negative line can profit

13, the price of the first time in the same period of time through 89 after the first step back can be re-bought.

中文翻译

价格在89上面运行时时只找买入信号、

价格在89下面运行时只寻找卖出信号、

第一次向上穿过89均线后的第一次回踩确认可以顺势买入、

第一次向下穿过89均线后的第一次回抽确认可以顺势卖出、

价格横盘整理,均线频繁穿越时离场观察。

8-21区间里面黄色区域为顺势加仓信号,

价格在89均线上面时K线收盘在21天均线下面时为回调信号

价格在89均线下面时K线收盘在21天均线上面时为反弹信号

在回调和反弹信号出来之后我们应该获利一半的头寸,另外一半止损放到盈亏平衡的地方。

均线非常适合趋势性很强的品种,并不适合震荡行情。

只有在震荡行情结束时均线向上或向下发散时才有被运用的可能。

1、横盘阶段均线反复纠缠,离场观察

2、三条EMA均线向下交叉回抽无法超越89EMA时卖出

3、多次不能破新低时价格走横时获利

4、价格在3处三角形收敛被突破后站上了89EMA时买入

5、价格上涨角度变缓并收盘在21均线下面时获利

6、横盘震荡时离场观察。

7、见死不救新闻或数据导致价格快速下跌时观望

8、价格三角形向上突破时穿过89均线时买入

9、价格不升减速走横时收盘于21均线下面时获利

10、价格横盘震荡整理同时均线也横向整理时离场观察

11、价格突破三角形整理后重新穿过89均线时买入。此时所有均线已经向上翘头

12、第二次不能突破新高时收阴线可以获利

13、价格在同一个时间周期内第一次穿过89以后的第一次回踩可以重新买入

14、21-55作为牛熊的分水岭。在21-55区域之下只考虑做空,21-55之上只考虑做多。如果21-55走横则以位置决定高位倾向空低位倾向多。

15、K线会因为指标的设置自动变成两个颜色块,绿色看涨,红色看跌。做趋势看K线颜色。牛市的红色可以当成入场K熊市绿色当成入场K

Cari dalam skrip untuk "美国11月非农数据"

Bernoulli Process - Binary Entropy FunctionThis indicator is the Bernoulli Process or Wikipedia - Binary Entropy Function . Within Information Theory, Entropy is the measure of available information, here we use a binary variable 0 or 1 (P) and (1-P) (Bernoulli Function/Distribution), and combined with the Shannon Entropy measurement. As you can see below, it produces some wonderful charts and signals, using price, volume, or both summed together. The chart below shows you a couple of options and some critical details on the indicator. The best part about this is the simplicity, all of this information in a couple of lines of code.

Using the indicator:

The longer the Entropy measurement the more information you are capturing, so the analogy is, the shorter the signal, the less information you have available to utilize. You'll run into your Nyquist frequencies below a length of 5. I've found values between 9 and 22 work well to gather enough measurements. You also have an averaging summation that measures the weight or importance of the information over the summation period. This is also used for highlighting when you have an information signal above the 5% level (2 sigma) and then can be adjusted using the Percent Rank Variable. Finally, you can plot the individual signals (Price or Volume) to get another set of measurements to utilize. As can be seen in the chart below, the volume moves before price (but hopefully you already knew that)

At its core, this is taking the Binary Entropy measurement (using a Bernoulli distribution) for price and volume. I've subtracted the volume from the price so that you can use it like a MACD, also for shorter time frames (7, 9, 11) you can get divergences on the histogram. These divergences are primarily due to the weekly nature of the markets (5 days, 10 days is two weeks,...so 9 is measuring the last day of the past two weeks...so 11 is measuring the current day and the past two weeks).

Here are a couple of other examples, assuming you just love BTC, Stocks, or FOREX. I fashioned up a strategy to show the potential of the indicator.

BTC-Strategy

Stock-Strategy (#loveyouNFLX)

FOREX - (for everyone hopped up on 40X leverage)

Divergence Histogram for Many IndicatorHello Traders,

This script analyses divergences for 11 predefined indicators and then draws column on the graph. Red columns for negatif divergence (means prices may go down or trend reversal), Lime columns for positive divergences (means prices may go up or trend reversal)

The script uses Pivot Points and on each bar it checks divergence between last Pivot Point and current High/Low and if it finds any divergence then immediately draws column. There is no Latency/Lag.

There are predefined 11 indicators in the script, which are RSI , MACD , MACD Histogram, Stochastic , CCI , Momentum, OBV, Diosc, VWMACD, CMF and MFI.

Smaller Pivot Point Period check smaller areas and if you use smaller numbers it would be more sensitive and may give alerts very often. So you should set it accordingly.

There is "Check Cut-Through in indicators" option, I recomment you to enable it. it checks that there is cut-through in indicators or not, if no cut-through then it's shown as valid divergence.

You should see following one as well if you haven't yet:

Enjoy!

candlestick patternsCleaning up and updating vcsWo8mh-Candlestick-Patterns-Identified-updated-3-11-15 .

As I learn more candlestick patterns I'll add them in.

Please post requests and any potential implementations I could port to pine script.

I'm applying autopep8 as best I can for readability.

MAC-Z & MACD Leader signal [ChuckBanger]This is a combination of my MACD Leader script and MAC-Z with option to add Laguerre filter. The advantage of the MAC-Z over MACD is that it is a more accurate and “assumption-free” indicator that can more accurately describe how a market actually perform. But you can use this as a regular MACD indicator.

Crossovers signals

The MAC-Z line and signal line can be utilized in the same way as a stochastic oscillator, with the crossover between the two lines providing buy and sell signals. As with most crossover strategies, a buy signal comes when the shorter-term, more reactive line – in this case the MAC-Z line (blue line) crosses above the slower signal line (orange line). For example, when the MAC-Z line crosses below the signal line it provides a bearish sell signal.

Zero line crossing

The zero cross strategy is based on either of the lines crossing the zero line. If the MAC-Z crosses the zero line from below, it is a signal for a possible new uptrend, while the MAC-Z crossing from above is a signal that a new downtrend may be starting. This is special powerful if the lines has a fast up or down movement but the price action doesn't reflect that movement.

Divergences

Bearish and bullish divergences is my favorite signals. When price action and oscillators follow the same path it is called Convergences, when they don’t, it’s called a Divergence. Don't confuse the two because they have not the same meaning. But be aware that for example during consolidation or low liquidity, some small divergences between price and indicators might form, but that doesn't mean we should consider them as real divergences.

There is many different types of divergences. It is easier to show a picture then explaining it so I recommend you to check out the link below. Especially the top image. It sums this up very well

medium.com

MACD Leader

The MACD leader is only showing the crossing of MACD as a vertical line

Green vertical line = MACD Leader Bullish Cross

Red vertical line = MACD Leader Bearish Cross

MACD Leader:

MAC-Z:

More Information

cssanalytics.wordpress.com

en.wikipedia.org

drive.google.com

Edward EMA 8-21-89-144Explain the application of moving averages through the disk surface:

When the price runs above 89, it only looks for the buy signal.

When the price runs below 89, it only looks for sell signals.

The first step up through the 89 moving average after the first confirmation can buy homeoply,

The first pull down after crossing the 89 moving average for the first time confirms that it can be sold in line with the trend.

Price horizontal finishing, moving average frequently across the field observation.

The yellow area in the interval from 8 to 21 is the homeopathic warehouse addition signal.

When the price is above the 89 moving average, the k-line closes below the 21-day moving average as a callback signal

Prices below the 89 ema close above the 21 - day ema as a rebound signal

After the correction and rebound signals come out, we should make half of the profit and the other half of the stop loss in the break-even place.

Moving average is very suitable for the trend of strong varieties, is not suitable for volatile market.

Only at the end of the shock market moving average upward or downward divergent when it is possible to be used.

1. Repeatedly entangle the mean line of horizontal disk stage and observe it from the field

2. Sell the three EMA moving averages when they can't exceed 89EMA with downward crossing

3, many times can not break the new low when prices go sideways profit

4. Buy when the price reaches 89EMA after the convergence of triangle 3 is broken

5, the Angle of price rise slowed and closed below the 21 moving average when profit

6. Left field observation during transverse oscillation.

Sit tight while news or data cause prices to fall quickly

8. Buy when the price triangle breaks through the 89 moving average upward

9, the price does not rise to slow down when the horizontal closed below the 21 moving average when profit

10, price horizontal shock finishing at the same time the average line also transverse finishing field observation

11, the price of the triangle after finishing through the 89 moving average to buy.At this point all the averages have turned up

12, the second time can not break through the new high when the negative line can profit

13, the price of the first time in the same period of time through 89 after the first step back can be re-bought.

通过盘面讲解均线运用:

价格在89上面运行时时只找买入信号、

价格在89下面运行时只寻找卖出信号、

第一次向上穿过89均线后的第一次回踩确认可以顺势买入、

第一次向下穿过89均线后的第一次回抽确认可以顺势卖出、

价格横盘整理,均线频繁穿越时离场观察。

8-21区间里面黄色区域为顺势加仓信号,

价格在89均线上面时K线收盘在21天均线下面时为回调信号

价格在89均线下面时K线收盘在21天均线上面时为反弹信号

在回调和反弹信号出来之后我们应该获利一半的头寸,另外一半止损放到盈亏平衡的地方。

均线非常适合趋势性很强的品种,并不适合震荡行情。

只有在震荡行情结束时均线向上或向下发散时才有被运用的可能。

1、横盘阶段均线反复纠缠,离场观察

2、三条EMA均线向下交叉回抽无法超越89EMA时卖出

3、多次不能破新低时价格走横时获利

4、价格在3处三角形收敛被突破后站上了89EMA时买入

5、价格上涨角度变缓并收盘在21均线下面时获利

6、横盘震荡时离场观察。

7、见死不救新闻或数据导致价格快速下跌时观望

8、价格三角形向上突破时穿过89均线时买入

9、价格不升减速走横时收盘于21均线下面时获利

10、价格横盘震荡整理同时均线也横向整理时离场观察

11、价格突破三角形整理后重新穿过89均线时买入。此时所有均线已经向上翘头

12、第二次不能突破新高时收阴线可以获利

13、价格在同一个时间周期内第一次穿过89以后的第一次回踩可以重新买入

14、89-144作为牛熊的分水岭。在89-144区域之下只考虑做空,89-144只考虑做多。如果89-144走横则以位置决定高位倾向空低位倾向多。

15、K线会因为指标的设置自动变成两个颜色块,绿色看涨,红色看跌。做趋势看K线颜色。牛市的红色可以当成入场K熊市绿色当成入场K

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

[astropark] MACD, RSI+, AO, DMI, ADX, OBV, ADI//******************************************************************************

// Copyright by astropark v4.1.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV, ADI

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

// 14/01/2019 Added On Balance Volume (OBV)

// 14/01/2019 Added Accelerator Decelerator Indicator (ADI)

//******************************************************************************

[astropark] MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV//******************************************************************************

// Copyright by astropark v4.0.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Oscillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

// 14/01/2019 Added On Balance Volume (OBV)

//******************************************************************************

[astropark] MACD, RSI+, Awesome Oscillator, DMI with ADX//******************************************************************************

// Copyright by astropark v3.1.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

//******************************************************************************

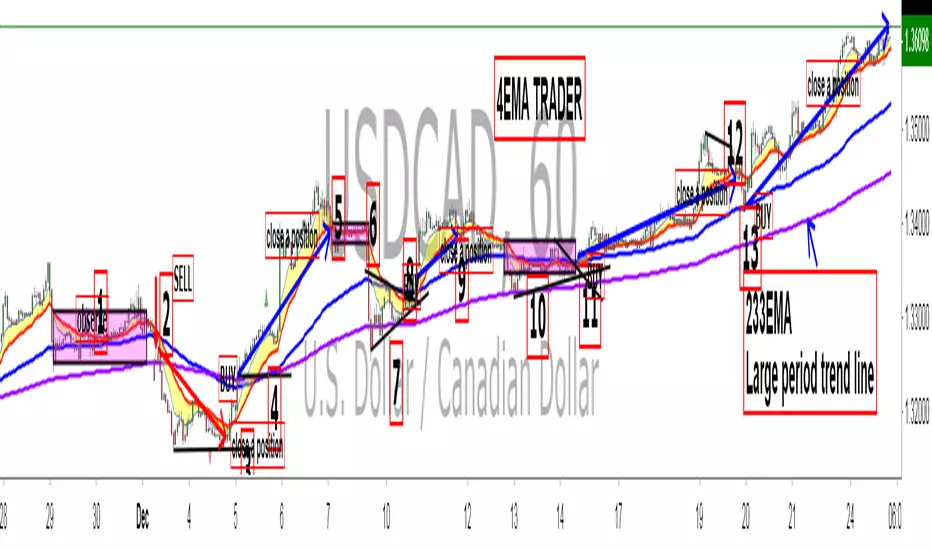

King 4EMA TraderKing 4EMA trader 8/21/89EMA+(233)V3.3

Explain the application of moving averages through the disk surface:

When the price runs above 89, it only looks for the buy signal.

When the price runs below 89, it only looks for sell signals.

The first step up through the 89 moving average after the first confirmation can buy homeoply,

The first pull down after crossing the 89 moving average for the first time confirms that it can be sold in line with the trend.

Price horizontal finishing, moving average frequently across the field observation.

The yellow area in the interval from 8 to 21 is the homeopathic warehouse addition signal.

When the price is above the 89 moving average, the k-line closes below the 21-day moving average as a callback signal

Prices below the 89 ema close above the 21 - day ema as a rebound signal

After the correction and rebound signals come out, we should make half of the profit and the other half of the stop loss in the break-even place.

Moving average is very suitable for the trend of strong varieties, is not suitable for volatile market.

Only at the end of the shock market moving average upward or downward divergent when it is possible to be used.

1. Repeatedly entangle the mean line of horizontal disk stage and observe it from the field

2. Sell the three EMA moving averages when they can't exceed 89EMA with downward crossing

3, many times can not break the new low when prices go sideways profit

4. Buy when the price reaches 89EMA after the convergence of triangle 3 is broken

5, the Angle of price rise slowed and closed below the 21 moving average when profit

6. Left field observation during transverse oscillation.

Sit tight while news or data cause prices to fall quickly

8. Buy when the price triangle breaks through the 89 moving average upward

9, the price does not rise to slow down when the horizontal closed below the 21 moving average when profit

10, price horizontal shock finishing at the same time the average line also transverse finishing field observation

11, the price of the triangle after finishing through the 89 moving average to buy.At this point all the averages have turned up

12, the second time can not break through the new high when the negative line can profit

13, the price of the first time in the same period of time through 89 after the first step back can be re-bought.

通过盘面讲解均线运用:

价格在89上面运行时时只找买入信号、

价格在89下面运行时只寻找卖出信号、

第一次向上穿过89均线后的第一次回踩确认可以顺势买入、

第一次向下穿过89均线后的第一次回抽确认可以顺势卖出、

价格横盘整理,均线频繁穿越时离场观察。

8-21区间里面黄色区域为顺势加仓信号,

价格在89均线上面时K线收盘在21天均线下面时为回调信号

价格在89均线下面时K线收盘在21天均线上面时为反弹信号

在回调和反弹信号出来之后我们应该获利一半的头寸,另外一半止损放到盈亏平衡的地方。

均线非常适合趋势性很强的品种,并不适合震荡行情。

只有在震荡行情结束时均线向上或向下发散时才有被运用的可能。

1、横盘阶段均线反复纠缠,离场观察

2、三条EMA均线向下交叉回抽无法超越89EMA时卖出

3、多次不能破新低时价格走横时获利

4、价格在3处三角形收敛被突破后站上了89EMA时买入

5、价格上涨角度变缓并收盘在21均线下面时获利

6、横盘震荡时离场观察。

7、见死不救新闻或数据导致价格快速下跌时观望

8、价格三角形向上突破时穿过89均线时买入

9、价格不升减速走横时收盘于21均线下面时获利

10、价格横盘震荡整理同时均线也横向整理时离场观察

11、价格突破三角形整理后重新穿过89均线时买入。此时所有均线已经向上翘头

12、第二次不能突破新高时收阴线可以获利

13、价格在同一个时间周期内第一次穿过89以后的第一次回踩可以重新买入。

Bitfinex Longs/Shorts Multi-Coin [acatwithcharts]This script plots the longs/shorts ratio derived from Bitfinex for BTCUSDLONGS, BTCUSDSHORTS, and similar for 11 top cryptocurrencies chosen selected based on marketcap, trading volume on Bitfinex, and the maximum number of times that TradingView would let me call the "security" function in one script. Included coins:

BTC, ETH, LTC, BCH, XRP, EOS, IOT (IOTA), ETC, ZEC, NEO, XMR

In addition to just plotting the ratios for the individual coins, this script also calculates for a customizable selection of the 11 coins both the average ratio and a weighted average weighted by (USD price of coin * sum of long and short positions).

I wrote it both to use both for a big picture overview of leveraged positions across major coins and to use as a Swiss army knife of longs/shorts ratio indicators for individual coins, most of which do not currently have individual scripts published.

I'm an amateur and you definitely shouldn't take anything I say or use any of my scripts as financial advice. I'd appreciate any feedback.

Stochastic Momentum IndexStochastic Momentum Index indicator script. This indicator was originally developed by William Blau (Stocks & Commodities V. 11:1 (11-18)).

NCL Noise FilterOne of our Favorite Indicators - the NeoChartLabs Noise Filter.

FILTER OUT THE NOISE and focus on the moves that matter, toggle the settings to match your preference.

Or switch the Duration Setting to Institutional on a high timeframe (1W+) to locate great spot buying opportunities near cycle tops and bottoms.

Volume Filter: The volume filter automatically turns OFF when you switch to Major Macro Cycle or Institutional Baseline, as those high-timeframe structural breaks are often valid even on lower relative volume.

You can change the volume requirement by checking the volume of the current breakout bar against its Relative Volume (RVOL) - A setting of 0 turns this OFF.

A common professional standard is to require the breakout volume to be at least 1.5x to 2x higher than the 20-period average volume.

*we recommend using a higher volume setting on low timeframes under the 4HR to reduce false signals.

MTF Filter:

*we recommend to set at least 1 timeframe above your trade (i.e if you enter on the 2hour set to the 4 hour)

It prevents entering trades that are essentially minor pullbacks in a much larger opposing trend.

By integrating a higher timeframe EMA (e.g., a 200-period EMA from a 4x higher timeframe), you can filter out counter-trend trades that have a higher probability of failing.

ATR Filter:

Filters "Fake-Outs": It forces the price to not just "touch" the trendline, but to break it with enough force to clear the current average volatility.

Adaptive: Unlike a fixed pip/dollar amount, the ATR adjusts to the asset. On Bitcoin, the threshold might be $500; on a penny stock, it might be $0.05.

Bullish Cross: The price must close above the support trendline + (0.5 * ATR).

Bearish Cross: The price must close below the resistance trendline - (0.5 * ATR).

MACD Filter:

Bullish Crosses require the MACD Histogram to be increasing (showing positive momentum acceleration).

Bearish Crosses require the MACD Histogram to be decreasing (showing negative momentum acceleration).

RSI Filter:

Bullish Breakout (Cross of the lower/support trendline): You would want the RSI to be rising or above 50, showing that buyers are in control.

Bearish Breakdown (Cross of the upper/resistance trendline): You would want the RSI to be falling or below 50, showing sellers are in control.

Market Structure Shifts (CHoCH) - identifying Trends with bullish/bearish dashed horizontal lines for each CHoCH providing a cleaner visualization of the support or resistance level that price has just violated.

Duration Table for 1Week Charts

Trading Style Fractal Length (p) Pattern Span Confirmation Delay

Standard Swing 2 5 Weeks 2 Weeks

Intermediate Trend 5 11 Weeks 5 Weeks

Major Macro Cycle 10–20 21–41 Weeks 10–20 Weeks

Institutional Baseline 44 ~2 Years ~10 Months

ORB Fusion🎯 CORE INNOVATION: INSTITUTIONAL ORB FRAMEWORK WITH FAILED BREAKOUT INTELLIGENCE

ORB Fusion represents a complete institutional-grade Opening Range Breakout system combining classic Market Profile concepts (Initial Balance, day type classification) with modern algorithmic breakout detection, failed breakout reversal logic, and comprehensive statistical tracking. Rather than simply drawing lines at opening range extremes, this system implements the full trading methodology used by professional floor traders and market makers—including the critical concept that failed breakouts are often higher-probability setups than successful breakouts .

The Opening Range Hypothesis:

The first 30-60 minutes of trading establishes the day's value area —the price range where the majority of participants agree on fair value. This range is formed during peak information flow (overnight news digestion, gap reactions, early institutional positioning). Breakouts from this range signal directional conviction; failures to hold breakouts signal trapped participants and create exploitable reversals.

Why Opening Range Matters:

1. Information Aggregation : Opening range reflects overnight news, pre-market sentiment, and early institutional orders. It's the market's initial "consensus" on value.

2. Liquidity Concentration : Stop losses cluster just outside opening range. Breakouts trigger these stops, creating momentum. Failed breakouts trap traders, forcing reversals.

3. Statistical Persistence : Markets exhibit range expansion tendency —when price accepts above/below opening range with volume, it often extends 1.0-2.0x the opening range size before mean reversion.

4. Institutional Behavior : Large players (market makers, institutions) use opening range as reference for the day's trading plan. They fade extremes in rotation days and follow breakouts in trend days.

Historical Context:

Opening Range Breakout methodology originated in commodity futures pits (1970s-80s) where floor traders noticed consistent patterns: the first 30-60 minutes established a "fair value zone," and directional moves occurred when this zone was violated with conviction. J. Peter Steidlmayer formalized this observation in Market Profile theory, introducing the "Initial Balance" concept—the first hour (two 30-minute periods) defining market structure.

📊 OPENING RANGE CONSTRUCTION

Four ORB Timeframe Options:

1. 5-Minute ORB (0930-0935 ET):

Captures immediate market direction during "opening drive"—the explosive first few minutes when overnight orders hit the tape.

Use Case:

• Scalping strategies

• High-frequency breakout trading

• Extremely liquid instruments (ES, NQ, SPY)

Characteristics:

• Very tight range (often 0.2-0.5% of price)

• Early breakouts common (7 of 10 days break within first hour)

• Higher false breakout rate (50-60%)

• Requires sub-minute chart monitoring

Psychology: Captures panic buyers/sellers reacting to overnight news. Range is small because sample size is minimal—only 5 minutes of price discovery. Early breakouts often fail because they're driven by retail FOMO rather than institutional conviction.

2. 15-Minute ORB (0930-0945 ET):

Balances responsiveness with statistical validity. Captures opening drive plus initial reaction to that drive.

Use Case:

• Day trading strategies

• Balanced scalping/swing hybrid

• Most liquid instruments

Characteristics:

• Moderate range (0.4-0.8% of price typically)

• Breakout rate ~60% of days

• False breakout rate ~40-45%

• Good balance of opportunity and reliability

Psychology: Includes opening panic AND the first retest/consolidation. Sophisticated traders (institutions, algos) start expressing directional bias. This is the "Goldilocks" timeframe—not too reactive, not too slow.

3. 30-Minute ORB (0930-1000 ET):

Classic ORB timeframe. Default for most professional implementations.

Use Case:

• Standard intraday trading

• Position sizing for full-day trades

• All liquid instruments (equities, indices, futures)

Characteristics:

• Substantial range (0.6-1.2% of price)

• Breakout rate ~55% of days

• False breakout rate ~35-40%

• Statistical sweet spot for extensions

Psychology: Full opening auction + first institutional repositioning complete. By 10:00 AM ET, headlines are digested, early stops are hit, and "real" directional players reveal themselves. This is when institutional programs typically finish their opening positioning.

Statistical Advantage: 30-minute ORB shows highest correlation with daily range. When price breaks and holds outside 30m ORB, probability of reaching 1.0x extension (doubling the opening range) exceeds 60% historically.

4. 60-Minute ORB (0930-1030 ET) - Initial Balance:

Steidlmayer's "Initial Balance"—the foundation of Market Profile theory.

Use Case:

• Swing trading entries

• Day type classification

• Low-frequency institutional setups

Characteristics:

• Wide range (0.8-1.5% of price)

• Breakout rate ~45% of days

• False breakout rate ~25-30% (lowest)

• Best for trend day identification

Psychology: Full first hour captures A-period (0930-1000) and B-period (1000-1030). By 10:30 AM ET, all early positioning is complete. Market has "voted" on value. Subsequent price action confirms (trend day) or rejects (rotation day) this value assessment.

Initial Balance Theory:

IB represents the market's accepted value area . When price extends significantly beyond IB (>1.5x IB range), it signals a Trend Day —strong directional conviction. When price remains within 1.0x IB, it signals a Rotation Day —mean reversion environment. This classification completely changes trading strategy.

🔬 LTF PRECISION TECHNOLOGY

The Chart Timeframe Problem:

Traditional ORB indicators calculate range using the chart's current timeframe. This creates critical inaccuracies:

Example:

• You're on a 5-minute chart

• ORB period is 30 minutes (0930-1000 ET)

• Indicator sees only 6 bars (30min ÷ 5min/bar = 6 bars)

• If any 5-minute bar has extreme wick, entire ORB is distorted

The Problem Amplifies:

• On 15-minute chart with 30-minute ORB: Only 2 bars sampled

• On 30-minute chart with 30-minute ORB: Only 1 bar sampled

• Opening spike or single large wick defines entire range (invalid)

Solution: Lower Timeframe (LTF) Precision:

ORB Fusion uses `request.security_lower_tf()` to sample 1-minute bars regardless of chart timeframe:

```

For 30-minute ORB on 15-minute chart:

- Traditional method: Uses 2 bars (15min × 2 = 30min)

- LTF Precision: Requests thirty 1-minute bars, calculates true high/low

```

Why This Matters:

Scenario: ES futures, 15-minute chart, 30-minute ORB

• Traditional ORB: High = 5850.00, Low = 5842.00 (range = 8 points)

• LTF Precision ORB: High = 5848.50, Low = 5843.25 (range = 5.25 points)

Difference: 2.75 points distortion from single 15-minute wick hitting 5850.00 at 9:31 AM then immediately reversing. LTF precision filters this out by seeing it was a fleeting wick, not a sustained high.

Impact on Extensions:

With inflated range (8 points vs 5.25 points):

• 1.5x extension projects +12 points instead of +7.875 points

• Difference: 4.125 points (nearly $200 per ES contract)

• Breakout signals trigger late; extension targets unreachable

Implementation:

```pinescript

getLtfHighLow() =>

float ha = request.security_lower_tf(syminfo.tickerid, "1", high)

float la = request.security_lower_tf(syminfo.tickerid, "1", low)

```

Function returns arrays of 1-minute high/low values, then finds true maximum and minimum across all samples.

When LTF Precision Activates:

Only when chart timeframe exceeds ORB session window:

• 5-minute chart + 30-minute ORB: LTF used (chart TF > session bars needed)

• 1-minute chart + 30-minute ORB: LTF not needed (direct sampling sufficient)

Recommendation: Always enable LTF Precision unless you're on 1-minute charts. The computational overhead is negligible, and accuracy improvement is substantial.

⚖️ INITIAL BALANCE (IB) FRAMEWORK

Steidlmayer's Market Profile Innovation:

J. Peter Steidlmayer developed Market Profile in the 1980s for the Chicago Board of Trade. His key insight: market structure is best understood through time-at-price (value area) rather than just price-over-time (traditional charts).

Initial Balance Definition:

IB is the price range established during the first hour of trading, subdivided into:

• A-Period : First 30 minutes (0930-1000 ET for US equities)

• B-Period : Second 30 minutes (1000-1030 ET)

A-Period vs B-Period Comparison:

The relationship between A and B periods forecasts the day:

B-Period Expansion (Bullish):

• B-period high > A-period high

• B-period low ≥ A-period low

• Interpretation: Buyers stepping in after opening assessed

• Implication: Bullish continuation likely

• Strategy: Buy pullbacks to A-period high (now support)

B-Period Expansion (Bearish):

• B-period low < A-period low

• B-period high ≤ A-period high

• Interpretation: Sellers stepping in after opening assessed

• Implication: Bearish continuation likely

• Strategy: Sell rallies to A-period low (now resistance)

B-Period Contraction:

• B-period stays within A-period range

• Interpretation: Market indecisive, digesting A-period information

• Implication: Rotation day likely, stay range-bound

• Strategy: Fade extremes, sell high/buy low within IB

IB Extensions:

Professional traders use IB as a ruler to project price targets:

Extension Levels:

• 0.5x IB : Initial probe outside value (minor target)

• 1.0x IB : Full extension (major target for normal days)

• 1.5x IB : Trend day threshold (classifies as trending)

• 2.0x IB : Strong trend day (rare, ~10-15% of days)

Calculation:

```

IB Range = IB High - IB Low

Bull Extension 1.0x = IB High + (IB Range × 1.0)

Bear Extension 1.0x = IB Low - (IB Range × 1.0)

```

Example:

ES futures:

• IB High: 5850.00

• IB Low: 5842.00

• IB Range: 8.00 points

Extensions:

• 1.0x Bull Target: 5850 + 8 = 5858.00

• 1.5x Bull Target: 5850 + 12 = 5862.00

• 2.0x Bull Target: 5850 + 16 = 5866.00

If price reaches 5862.00 (1.5x), day is classified as Trend Day —strategy shifts from mean reversion to trend following.

📈 DAY TYPE CLASSIFICATION SYSTEM

Four Day Types (Market Profile Framework):

1. TREND DAY:

Definition: Price extends ≥1.5x IB range in one direction and stays there.

Characteristics:

• Opens and never returns to IB

• Persistent directional movement

• Volume increases as day progresses (conviction building)

• News-driven or strong institutional flow

Frequency: ~20-25% of trading days

Trading Strategy:

• DO: Follow the trend, trail stops, let winners run

• DON'T: Fade extremes, take early profits

• Key: Add to position on pullbacks to previous extension level

• Risk: Getting chopped in false trend (see Failed Breakout section)

Example: FOMC decision, payroll report, earnings surprise—anything creating one-sided conviction.

2. NORMAL DAY:

Definition: Price extends 0.5-1.5x IB, tests both sides, returns to IB.

Characteristics:

• Two-sided trading

• Extensions occur but don't persist

• Volume balanced throughout day

• Most common day type

Frequency: ~45-50% of trading days

Trading Strategy:

• DO: Take profits at extension levels, expect reversals

• DON'T: Hold for massive moves

• Key: Treat each extension as a profit-taking opportunity

• Risk: Holding too long when momentum shifts

Example: Typical day with no major catalysts—market balancing supply and demand.

3. ROTATION DAY:

Definition: Price stays within IB all day, rotating between high and low.

Characteristics:

• Never accepts outside IB

• Multiple tests of IB high/low

• Decreasing volume (no conviction)

• Classic range-bound action

Frequency: ~25-30% of trading days

Trading Strategy:

• DO: Fade extremes (sell IB high, buy IB low)

• DON'T: Chase breakouts

• Key: Enter at extremes with tight stops just outside IB

• Risk: Breakout finally occurs after multiple failures

Example: [/b> Pre-holiday trading, summer doldrums, consolidation after big move.

4. DEVELOPING:

Definition: Day type not yet determined (early in session).

Usage: Classification before 12:00 PM ET when IB extension pattern unclear.

ORB Fusion's Classification Algorithm:

```pinescript

if close > ibHigh:

ibExtension = (close - ibHigh) / ibRange

direction = "BULLISH"

else if close < ibLow:

ibExtension = (ibLow - close) / ibRange

direction = "BEARISH"

if ibExtension >= 1.5:

dayType = "TREND DAY"

else if ibExtension >= 0.5:

dayType = "NORMAL DAY"

else if close within IB:

dayType = "ROTATION DAY"

```

Why Classification Matters:

Same setup (bullish ORB breakout) has opposite implications:

• Trend Day : Hold for 2.0x extension, trail stops aggressively

• Normal Day : Take profits at 1.0x extension, watch for reversal

• Rotation Day : Fade the breakout immediately (likely false)

Knowing day type prevents catastrophic errors like fading a trend day or holding through rotation.

🚀 BREAKOUT DETECTION & CONFIRMATION

Three Confirmation Methods:

1. Close Beyond Level (Recommended):

Logic: Candle must close above ORB high (bull) or below ORB low (bear).

Why:

• Filters out wicks (temporary liquidity grabs)

• Ensures sustained acceptance above/below range

• Reduces false breakout rate by ~20-30%

Example:

• ORB High: 5850.00

• Bar high touches 5850.50 (wick above)

• Bar closes at 5848.00 (inside range)

• Result: NO breakout signal

vs.

• Bar high touches 5850.50

• Bar closes at 5851.00 (outside range)

• Result: BREAKOUT signal confirmed

Trade-off: Slightly delayed entry (wait for close) but much higher reliability.

2. Wick Beyond Level:

Logic: [/b> Any touch of ORB high/low triggers breakout.

Why:

• Earliest possible entry

• Captures aggressive momentum moves

Risk:

• High false breakout rate (60-70%)

• Stop runs trigger signals

• Requires very tight stops (difficult to manage)

Use Case: Scalping with 1-2 point profit targets where any penetration = trade.

3. Body Beyond Level:

Logic: [/b> Candle body (close vs open) must be entirely outside range.

Why:

• Strictest confirmation

• Ensures directional conviction (not just momentum)

• Lowest false breakout rate

Example: Trade-off: [/b> Very conservative—misses some valid breakouts but rarely triggers on false ones.

Volume Confirmation Layer:

All confirmation methods can require volume validation:

Volume Multiplier Logic: Rationale: [/b> True breakouts are driven by institutional activity (large size). Volume spike confirms real conviction vs. stop-run manipulation.

Statistical Impact: [/b>

• Breakouts with volume confirmation: ~65% success rate

• Breakouts without volume: ~45% success rate

• Difference: 20 percentage points edge

Implementation Note: [/b>

Volume confirmation adds complexity—you'll miss breakouts that work but lack volume. However, when targeting 1.5x+ extensions (ambitious goals), volume confirmation becomes critical because those moves require sustained institutional participation.

Recommended Settings by Strategy: [/b>

Scalping (1-2 point targets): [/b>

• Method: Close

• Volume: OFF

• Rationale: Quick in/out doesn't need perfection

Intraday Swing (5-10 point targets): [/b>

• Method: Close

• Volume: ON (1.5x multiplier)

• Rationale: Balance reliability and opportunity

Position Trading (full-day holds): [/b>

• Method: Body

• Volume: ON (2.0x multiplier)

• Rationale: Must be certain—large stops require high win rate

🔥 FAILED BREAKOUT SYSTEM

The Core Insight: [/b>

Failed breakouts are often more profitable [/b> than successful breakouts because they create trapped traders with predictable behavior.

Failed Breakout Definition: [/b>

A breakout that:

1. Initially penetrates ORB level with confirmation

2. Attracts participants (volume spike, momentum)

3. Fails to extend (stalls or immediately reverses)

4. Returns inside ORB range within N bars

Psychology of Failure: [/b>

When breakout fails:

• Breakout buyers are trapped [/b>: Bought at ORB high, now underwater

• Early longs reduce: Take profit, fearful of reversal

• Shorts smell blood: See failed breakout as reversal signal

• Result: Cascade of selling as trapped bulls exit + new shorts enter

Mirror image for failed bearish breakouts (trapped shorts cover + new longs enter).

Failure Detection Parameters: [/b>

1. Failure Confirmation Bars (default: 3): [/b>

How many bars after breakout to confirm failure?

Logic: Settings: [/b>

• 2 bars: Aggressive failure detection (more signals, more false failures)

• 3 bars Balanced (default)

• 5-10 bars: Conservative (wait for clear reversal)

Why This Matters:

Too few bars: You call "failed breakout" when price is just consolidating before next leg.

Too many bars: You miss the reversal entry (price already back in range).

2. Failure Buffer (default: 0.1 ATR): [/b>

How far inside ORB must price return to confirm failure?

Formula: Why Buffer Matters: clear rejection [/b> (not just hovering at level).

Settings: [/b>

• 0.0 ATR: No buffer, immediate failure signal

• 0.1 ATR: Small buffer (default) - filters noise

• [b>0.2-0.3 ATR: Large buffer - only dramatic failures count

Example: Reversal Entry System: [/b>

When failure confirmed, system generates complete reversal trade:

For Failed Bull Breakout (Short Reversal): [/b>

Entry: [/b> Current close when failure confirmed

Stop Loss: [/b> Extreme high since breakout + 0.10 ATR padding

Target 1: [/b> ORB High - (ORB Range × 0.5)

Target 2: Target 3: [/b> ORB High - (ORB Range × 1.5)

Example:

• ORB High: 5850, ORB Low: 5842, Range: 8 points

• Breakout to 5853, fails, reverses to 5848 (entry)

• Stop: 5853 + 1 = 5854 (6 point risk)

• T1: 5850 - 4 = 5846 (-2 points, 1:3 R:R)

• T2: 5850 - 8 = 5842 (-6 points, 1:1 R:R)

• T3: 5850 - 12 = 5838 (-10 points, 1.67:1 R:R)

[b>Why These Targets? [/b>

• T1 (0.5x ORB below high): Trapped bulls start panic

• T2 (1.0x ORB = ORB Mid): Major retracement, momentum fully reversed

• T3 (1.5x ORB): Reversal extended, now targeting opposite side

Historical Performance: [/b>

Failed breakout reversals in ORB Fusion's tracking system show:

• Win Rate: 65-75% (significantly higher than initial breakouts)

• Average Winner: 1.2x ORB range

• Average Loser: 0.5x ORB range (protected by stop at extreme)

• Expectancy: Strongly positive even with <70% win rate

Why Failed Breakouts Outperform: [/b>

1. Information Advantage: You now know what price did (failed to extend). Initial breakout trades are speculative; reversal trades are reactive to confirmed failure.

2. Trapped Participant Pressure: Every trapped bull becomes a seller. This creates sustained pressure.

3. Stop Loss Clarity: Extreme high is obvious stop (just beyond recent high). Breakout trades have ambiguous stops (ORB mid? Recent low? Too wide or too tight).

4. Mean Reversion Edge: Failed breakouts return to value (ORB mid). Initial breakouts try to escape value (harder to sustain).

Critical Insight: [/b>

"The best trade is often the one that trapped everyone else."

Failed breakouts create asymmetric opportunity because you're trading against [/b> trapped participants rather than with [/b> them. When you see a failed breakout signal, you're seeing real-time evidence that the market rejected directional conviction—that's exploitable.

📐 FIBONACCI EXTENSION SYSTEM

Six Extension Levels: [/b>

Extensions project how far price will travel after ORB breakout. Based on Fibonacci ratios + empirical market behavior.

1. 1.272x (27.2% Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.272)

Psychology: [/b> Initial probe beyond ORB. Early momentum + trapped shorts (on bull side) covering.

Probability of Reach: [/b> ~75-80% after confirmed breakout

Trading: [/b>

• First resistance/support after breakout

• Partial profit target (take 30-50% off)

• Watch for rejection here (could signal failure in progress)

Why 1.272? [/b> Related to harmonic patterns (1.272 is √1.618). Empirically, markets often stall at 25-30% extension before deciding whether to continue or fail.

2. 1.5x (50% Extension):

Formula: [/b> ORB High/Low + (ORB Range × 0.5)

Psychology: [/b> Breakout gaining conviction. Requires sustained buying/selling (not just momentum spike).

Probability of Reach: [/b> ~60-65% after confirmed breakout

Trading: [/b>

• Major partial profit (take 50-70% off)

• Move stops to breakeven

• Trail remaining position

Why 1.5x? [/b> Classic halfway point to 2.0x. Markets often consolidate here before final push. If day type is "Normal," this is likely the high/low for the day.

3. 1.618x (Golden Ratio Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.618)

Psychology: [/b> Strong directional day. Institutional conviction + retail FOMO.

Probability of Reach: [/b> ~45-50% after confirmed breakout

Trading: [/b>

• Final partial profit (close 80-90%)

• Trail remainder with wide stop (allow breathing room)

Why 1.618? [/b> Fibonacci golden ratio. Appears consistently in market geometry. When price reaches 1.618x extension, move is "mature" and reversal risk increases.

4. 2.0x (100% Extension): [/b>

Formula: ORB High/Low + (ORB Range × 1.0)

Psychology: [/b> Trend day confirmed. Opening range completely duplicated.

Probability of Reach: [/b> ~30-35% after confirmed breakout

Trading: Why 2.0x? [/b> Psychological level—range doubled. Also corresponds to typical daily ATR in many instruments (opening range ~ 0.5 ATR, daily range ~ 1.0 ATR).

5. 2.618x (Super Extension):

Formula: [/b> ORB High/Low + (ORB Range × 1.618)

Psychology: [/b> Parabolic move. News-driven or squeeze.

Probability of Reach: [/b> ~10-15% after confirmed breakout

[b>Trading: Why 2.618? [/b> Fibonacci ratio (1.618²). Rare to reach—when it does, move is extreme. Often precedes multi-day consolidation or reversal.

6. 3.0x (Extreme Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 2.0)

Psychology: [/b> Market melt-up/crash. Only in extreme events.

[b>Probability of Reach: [/b> <5% after confirmed breakout

Trading: [/b>

• Close immediately if reached

• These are outlier events (black swans, flash crashes, squeeze-outs)

• Holding for more is greed—take windfall profit

Why 3.0x? [/b> Triple opening range. So rare it's statistical noise. When it happens, it's headline news.

Visual Example:

ES futures, ORB 5842-5850 (8 point range), Bullish breakout:

• ORB High : 5850.00 (entry zone)

• 1.272x : 5850 + 2.18 = 5852.18 (first resistance)

• 1.5x : 5850 + 4.00 = 5854.00 (major target)

• 1.618x : 5850 + 4.94 = 5854.94 (strong target)

• 2.0x : 5850 + 8.00 = 5858.00 (trend day)

• 2.618x : 5850 + 12.94 = 5862.94 (extreme)

• 3.0x : 5850 + 16.00 = 5866.00 (parabolic)

Profit-Taking Strategy:

Optimal scaling out at extensions:

• Breakout entry at 5850.50

• 30% off at 1.272x (5852.18) → +1.68 points

• 40% off at 1.5x (5854.00) → +3.50 points

• 20% off at 1.618x (5854.94) → +4.44 points

• 10% off at 2.0x (5858.00) → +7.50 points

[b>Average Exit: Conclusion: [/b> Scaling out at extensions produces 40% higher expectancy than holding for home runs.

📊 GAP ANALYSIS & FILL PSYCHOLOGY

[b>Gap Definition: [/b>

Price discontinuity between previous close and current open:

• Gap Up : Open > Previous Close + noise threshold (0.1 ATR)

• Gap Down : Open < Previous Close - noise threshold

Why Gaps Matter: [/b>

Gaps represent unfilled orders [/b>. When market gaps up, all limit buy orders between yesterday's close and today's open are never filled. Those buyers are "left behind." Psychology: they wait for price to return ("fill the gap") so they can enter. This creates magnetic pull [/b> toward gap level.

Gap Fill Statistics (Empirical): [/b>

• Gaps <0.5% [/b>: 85-90% fill within same day

• Gaps 0.5-1.0% [/b>: 70-75% fill within same day, 90%+ within week

• Gaps >1.0% [/b>: 50-60% fill within same day (major news often prevents fill)

Gap Fill Strategy: [/b>

Setup 1: Gap-and-Go

Gap opens, extends away from gap (doesn't fill).

• ORB confirms direction away from gap

• Trade WITH ORB breakout direction

• Expectation: Gap won't fill today (momentum too strong)

Setup 2: Gap-Fill Fade

Gap opens, but fails to extend. Price drifts back toward gap.

• ORB breakout TOWARD gap (not away)

• Trade toward gap fill level

• Target: Previous close (gap fill complete)

Setup 3: Gap-Fill Rejection

Gap fills (touches previous close) then rejects.

• ORB breakout AWAY from gap after fill

• Trade away from gap direction

• Thesis: Gap filled (orders executed), now resume original direction

[b>Example: Scenario A (Gap-and-Go):

• ORB breaks upward to $454 (away from gap)

• Trade: LONG breakout, expect continued rally

• Gap becomes support ($452)

Scenario B (Gap-Fill):

• ORB breaks downward through $452.50 (toward gap)

• Trade: SHORT toward gap fill at $450.00

• Target: $450.00 (gap filled), close position

Scenario C (Gap-Fill Rejection):

• Price drifts to $450.00 (gap filled) early in session

• ORB establishes $450-$451 after gap fill

• ORB breaks upward to $451.50

• Trade: LONG breakout (gap is filled, now resume rally)

ORB Fusion Integration: [/b>

Dashboard shows:

• Gap type (Up/Down/None)

• Gap size (percentage)

• Gap fill status (Filled ✓ / Open)

This informs setup confidence:

• ORB breakout AWAY from unfilled gap: +10% confidence (gap becomes support/resistance)

• ORB breakout TOWARD unfilled gap: -10% confidence (gap fill may override ORB)

[b>📈 VWAP & INSTITUTIONAL BIAS [/b>

[b>Volume-Weighted Average Price (VWAP): [/b>

Average price weighted by volume at each price level. Represents true "average" cost for the day.

[b>Calculation: Institutional Benchmark [/b>: Institutions (mutual funds, pension funds) use VWAP as performance benchmark. If they buy above VWAP, they underperformed; below VWAP, they outperformed.

2. [b>Algorithmic Target [/b>: Many algos are programmed to buy below VWAP and sell above VWAP to achieve "fair" execution.

3. [b>Support/Resistance [/b>: VWAP acts as dynamic support (price above) or resistance (price below).

[b>VWAP Bands (Standard Deviations): [/b>

• [b>1σ Band [/b>: VWAP ± 1 standard deviation

- Contains ~68% of volume

- Normal trading range

- Bounces common

• [b>2σ Band [/b>: VWAP ± 2 standard deviations

- Contains ~95% of volume

- Extreme extension

- Mean reversion likely

ORB + VWAP Confluence: [/b>

Highest-probability setups occur when ORB and VWAP align:

Bullish Confluence: [/b>

• ORB breakout upward (bullish signal)

• Price above VWAP (institutional buying)

• Confidence boost: +15%

Bearish Confluence: [/b>

• ORB breakout downward (bearish signal)

• Price below VWAP (institutional selling)

• Confidence boost: +15%

[b>Divergence Warning:

• ORB breakout upward BUT price below VWAP

• Conflict: Breakout says "buy," VWAP says "sell"

• Confidence penalty: -10%

• Interpretation: Retail buying but institutions not participating (lower quality breakout)

📊 MOMENTUM CONTEXT SYSTEM

[b>Innovation: Candle Coloring by Position

Rather than fixed support/resistance lines, ORB Fusion colors candles based on their [b>relationship to ORB :

[b>Three Zones: [/b>

1. Inside ORB (Blue Boxes): [/b>

[b>Calculation:

• Darker blue: Near extremes of ORB (potential breakout imminent)

• Lighter blue: Near ORB mid (consolidation)

[b>Trading: [/b> Coiled spring—await breakout.

[b>2. Above ORB (Green Boxes):

[b>Calculation: 3. Below ORB (Red Boxes):

Mirror of above ORB logic.

[b>Special Contexts: [/b>

[b>Breakout Bar (Darkest Green/Red): [/b>

The specific bar where breakout occurs gets maximum color intensity regardless of distance. This highlights the pivotal moment.

[b>Failed Breakout Bar (Orange/Warning): [/b>

When failed breakout is confirmed, that bar gets orange/warning color. Visual alert: "reversal opportunity here."

[b>Near Extension (Cyan/Magenta Tint): [/b>

When price is within 0.5 ATR of an extension level, candle gets tinted cyan (bull) or magenta (bear). Indicates "target approaching—prepare to take profit."

[b>Why Visual Context? [/b>

Traditional indicators show lines. ORB Fusion shows [b>context-aware momentum [/b>. Glance at chart:

• Lots of blue? Consolidation day (fade extremes).

• Progressive green? Trend day (follow).

• Green then orange? Failed breakout (reversal setup).

This visual language communicates market state instantly—no interpretation needed.

🎯 TRADE SETUP GENERATION & GRADING [/b>

[b>Algorithmic Setup Detection: [/b>

ORB Fusion continuously evaluates market state and generates current best trade setup with:

• Action (LONG / SHORT / FADE HIGH / FADE LOW / WAIT)

• Entry price

• Stop loss

• Three targets

• Risk:Reward ratio

• Confidence score (0-100)

• Grade (A+ to D)

[b>Setup Types: [/b>

[b>1. ORB LONG (Bullish Breakout): [/b>

[b>Trigger: [/b>

• Bullish ORB breakout confirmed

• Not failed

[b>Parameters:

• Entry: Current close

• Stop: ORB mid (protects against failure)

• T1: ORB High + 0.5x range (1.5x extension)

• T2: ORB High + 1.0x range (2.0x extension)

• T3: ORB High + 1.618x range (2.618x extension)

[b>Confidence Scoring:

[b>Trigger: [/b>

• Bearish breakout occurred

• Failed (returned inside ORB)

[b>Parameters: [/b>

• Entry: Close when failure confirmed

• Stop: Extreme low since breakout + 0.10 ATR

• T1: ORB Low + 0.5x range

• T2: ORB Low + 1.0x range (ORB mid)

• T3: ORB Low + 1.5x range

[b>Confidence Scoring:

[b>Trigger:

• Inside ORB

• Close > ORB mid (near high)

[b>Parameters: [/b>

• Entry: ORB High (limit order)

• Stop: ORB High + 0.2x range

• T1: ORB Mid

• T2: ORB Low

[b>Confidence Scoring: [/b>

Base: 40 points (lower base—range fading is lower probability than breakout/reversal)

[b>Use Case: [/b> Rotation days. Not recommended on normal/trend days.

[b>6. FADE LOW (Range Trade):

Mirror of FADE HIGH.

[b>7. WAIT:

[b>Trigger: [/b>

• ORB not complete yet OR

• No clear setup (price in no-man's-land)

[b>Action: [/b> Observe, don't trade.

[b>Confidence: [/b> 0 points

[b>Grading System:

```

Confidence → Grade

85-100 → A+

75-84 → A

65-74 → B+

55-64 → B

45-54 → C

0-44 → D

```

[b>Grade Interpretation: [/b>

• [b>A+ / A: High probability setup. Take these trades.

• [b>B+ / B [/b>: Decent setup. Trade if fits system rules.

• [b>C [/b>: Marginal setup. Only if very experienced.

• [b>D [/b>: Poor setup or no setup. Don't trade.

[b>Example Scenario: [/b>

ES futures:

• ORB: 5842-5850 (8 point range)

• Bullish breakout to 5851 confirmed

• Volume: 2.0x average (confirmed)

• VWAP: 5845 (price above VWAP ✓)

• Day type: Developing (too early, no bonus)

• Gap: None

[b>Setup: [/b>

• Action: LONG

• Entry: 5851

• Stop: 5846 (ORB mid, -5 point risk)

• T1: 5854 (+3 points, 1:0.6 R:R)

• T2: 5858 (+7 points, 1:1.4 R:R)

• T3: 5862.94 (+11.94 points, 1:2.4 R:R)

[b>Confidence: LONG with 55% confidence.

Interpretation: Solid setup, not perfect. Trade it if your system allows B-grade signals.

[b>📊 STATISTICS TRACKING & PERFORMANCE ANALYSIS [/b>

[b>Real-Time Performance Metrics: [/b>

ORB Fusion tracks comprehensive statistics over user-defined lookback (default 50 days):

[b>Breakout Performance: [/b>

• [b>Bull Breakouts: [/b> Total count, wins, losses, win rate

• [b>Bear Breakouts: [/b> Total count, wins, losses, win rate

[b>Win Definition: [/b> Breakout reaches ≥1.0x extension (doubles the opening range) before end of day.

[b>Example: [/b>

• ORB: 5842-5850 (8 points)

• Bull breakout at 5851

• Reaches 5858 (1.0x extension) by close

• Result: WIN

[b>Failed Breakout Performance: [/b>

• [b>Total Failed Breakouts [/b>: Count of breakouts that failed

• [b>Reversal Wins [/b>: Count where reversal trade reached target

• [b>Failed Reversal Win Rate [/b>: Wins / Total Failed

[b>Win Definition for Reversals: [/b>

• Failed bull → reversal short reaches ORB mid

• Failed bear → reversal long reaches ORB mid

[b>Extension Tracking: [/b>

• [b>Average Extension Reached [/b>: Mean of maximum extension achieved across all breakout days

• [b>Max Extension Overall [/b>: Largest extension ever achieved in lookback period

[b>Example: 🎨 THREE DISPLAY MODES

[b>Design Philosophy: [/b>

Not all traders need all features. Beginners want simplicity. Professionals want everything. ORB Fusion adapts.

[b>SIMPLE MODE: [/b>

[b>Shows: [/b>

• Primary ORB levels (High, Mid, Low)

• ORB box

• Breakout signals (triangles)

• Failed breakout signals (crosses)

• Basic dashboard (ORB status, breakout status, setup)

• VWAP

[b>Hides: [/b>

• Session ORBs (Asian, London, NY)

• IB levels and extensions

• ORB extensions beyond basic levels

• Gap analysis visuals

• Statistics dashboard

• Momentum candle coloring

• Narrative dashboard

[b>Use Case: [/b>

• Traders who want clean chart

• Focus on core ORB concept only

• Mobile trading (less screen space)

[b>STANDARD MODE:

[b>Shows Everything in Simple Plus: [/b>

• Session ORBs (Asian, London, NY)

• IB levels (high, low, mid)

• IB extensions

• ORB extensions (1.272x, 1.5x, 1.618x, 2.0x)

• Gap analysis and fill targets

• VWAP bands (1σ and 2σ)

• Momentum candle coloring

• Context section in dashboard

• Narrative dashboard

[b>Hides: [/b>

• Advanced extensions (2.618x, 3.0x)

• Detailed statistics dashboard

[b>Use Case: [/b>

• Most traders

• Balance between information and clarity

• Covers 90% of use cases

[b>ADVANCED MODE:

[b>Shows Everything:

• All session ORBs

• All IB levels and extensions

• All ORB extensions (including 2.618x and 3.0x)

• Full gap analysis

• VWAP with both 1σ and 2σ bands

• Momentum candle coloring

• Complete statistics dashboard

• Narrative dashboard

• All context metrics

[b>Use Case: [/b>

• Professional traders

• System developers

• Those who want maximum information density

[b>Switching Modes: [/b>

Single dropdown input: "Display Mode" → Simple / Standard / Advanced

Entire indicator adapts instantly. No need to toggle 20 individual settings.

📖 NARRATIVE DASHBOARD

[b>Innovation: Plain-English Market State [/b>

Most indicators show data. ORB Fusion explains what the data [b>means [/b>.

[b>Narrative Components: [/b>

[b>1. Phase: [/b>

• "📍 Building ORB..." (during ORB session)

• "📊 Trading Phase" (after ORB complete)

• "⏳ Pre-Market" (before ORB session)

[b>2. Status (Current Observation): [/b>

• "⚠️ Failed breakout - reversal likely"

• "🚀 Bullish momentum in play"

• "📉 Bearish momentum in play"

• "⚖️ Consolidating in range"

• "👀 Monitoring for setup"

[b>3. Next Level:

Tells you what to watch for:

• "🎯 1.5x @ 5854.00" (next extension target)

• "Watch ORB levels" (inside range, await breakout)

[b>4. Setup: [/b>

Current trade setup + grade:

• "LONG " (bullish breakout, A-grade)

• "🔥 SHORT REVERSAL " (failed bull breakout, A+-grade)

• "WAIT " (no setup)

[b>5. Reason: [/b>

Why this setup exists:

• "ORB Bullish Breakout"

• "Failed Bear Breakout - High Probability Reversal"

• "Range Fade - Near High"

[b>6. Tip (Market Insight):

Contextual advice:

• "🔥 TREND DAY - Trail stops" (day type is trending)

• "🔄 ROTATION - Fade extremes" (day type is rotating)

• "📊 Gap unfilled - magnet level" (gap creates target)

• "📈 Normal conditions" (no special context)

[b>Example Narrative:

```

📖 ORB Narrative

━━━━━━━━━━━━━━━━

Phase | 📊 Trading Phase

Status | 🚀 Bullish momentum in play

Next | 🎯 1.5x @ 5854.00

📈 Setup | LONG

Reason | ORB Bullish Breakout

💡 Tip | 🔥 TREND DAY - Trail stops

```

[b>Glance Interpretation: [/b>

"We're in trading phase. Bullish breakout happened (momentum in play). Next target is 1.5x extension at 5854. Current setup is LONG with A-grade. It's a trend day, so trail stops (don't take early profits)."

Complete market state communicated in 6 lines. No interpretation needed.

[b>Why This Matters:

Beginner traders struggle with "So what?" question. Indicators show lines and signals, but what does it mean [/b>? Narrative dashboard bridges this gap.

Professional traders benefit too—rapid context assessment during fast-moving markets. No time to analyze; glance at narrative, get action plan.

🔔 INTELLIGENT ALERT SYSTEM

[b>Four Alert Types: [/b>

[b>1. Breakout Alert: [/b>

[b>Trigger: [/b> ORB breakout confirmed (bull or bear)

[b>Message: [/b>

```

🚀 ORB BULLISH BREAKOUT

Price: 5851.00

Volume Confirmed

Grade: A

```

[b>Frequency: [/b> Once per bar (prevents spam)

[b>2. Failed Breakout Alert: [/b>

[b>Trigger: [/b> Breakout fails, reversal setup generated

[b>Message: [/b>

```

🔥 FAILED BULLISH BREAKOUT!

HIGH PROBABILITY SHORT REVERSAL

Entry: 5848.00

Stop: 5854.00

T1: 5846.00

T2: 5842.00

Historical Win Rate: 73%

```

[b>Why Comprehensive? [/b> Failed breakout alerts include complete trade plan. You can execute immediately from alert—no need to check chart.

[b>3. Extension Alert:

[b>Trigger: [/b> Price reaches extension level for first time

[b>Message: [/b>

```

🎯 Bull Extension 1.5x reached @ 5854.00

```

[b>Use: [/b> Profit-taking reminder. When extension hit, consider scaling out.

[b>4. IB Break Alert: [/b>

[b>Trigger: [/b> Price breaks above IB high or below IB low

[b>Message: [/b>

```

📊 IB HIGH BROKEN - Potential Trend Day

```

[b>Use: [/b> Day type classification. IB break suggests trend day developing—adjust strategy to trend-following mode.

[b>Alert Management: [/b>

Each alert type can be enabled/disabled independently. Prevents notification overload.

[b>Cooldown Logic: [/b>

Alerts won't fire if same alert type triggered within last bar. Prevents:

• "Breakout" alert every tick during choppy breakout

• Multiple "extension" alerts if price oscillates at level

Ensures: One clean alert per event.

⚙️ KEY PARAMETERS EXPLAINED

[b>Opening Range Settings: [/b>

• [b>ORB Timeframe [/b> (5/15/30/60 min): Duration of opening range window

- 30 min recommended for most traders

• [b>Use RTH Only [/b> (ON/OFF): Only trade during regular trading hours

- ON recommended (avoids thin overnight markets)

• [b>Use LTF Precision [/b> (ON/OFF): Sample 1-minute bars for accuracy

- ON recommended (critical for charts >1 minute)

• [b>Precision TF [/b> (1/5 min): Timeframe for LTF sampling

- 1 min recommended (most accurate)

[b>Session ORBs: [/b>

• [b>Show Asian/London/NY ORB [/b> (ON/OFF): Display multi-session ranges

- OFF in Simple mode

- ON in Standard/Advanced if trading 24hr markets

• [b>Session Windows [/b>: Time ranges for each session ORB

- Defaults align with major session opens

[b>Initial Balance: [/b>

• [b>Show IB [/b> (ON/OFF): Display Initial Balance levels

- ON recommended for day type classification

• [b>IB Session Window [/b> (0930-1030): First hour of trading

- Default is standard for US equities

• [b>Show IB Extensions [/b> (ON/OFF): Project IB extension targets

- ON recommended (identifies trend days)

• [b>IB Extensions 1-4 [/b> (0.5x, 1.0x, 1.5x, 2.0x): Extension multipliers

- Defaults are Market Profile standard

[b>ORB Extensions: [/b>

• [b>Show Extensions [/b> (ON/OFF): Project ORB extension targets

- ON recommended (defines profit targets)

• [b>Enable Individual Extensions [/b> (1.272x, 1.5x, 1.618x, 2.0x, 2.618x, 3.0x)

- Enable 1.272x, 1.5x, 1.618x, 2.0x minimum

- Disable 2.618x and 3.0x unless trading very volatile instruments

[b>Breakout Detection:

• [b>Confirmation Method [/b> (Close/Wick/Body):

- Close recommended (best balance)

- Wick for scalping

- Body for conservative

• [b>Require Volume Confirmation [/b> (ON/OFF):

- ON recommended (increases reliability)

• [b>Volume Multiplier [/b> (1.0-3.0):

- 1.5x recommended

- Lower for thin instruments

- Higher for heavy volume instruments

[b>Failed Breakout System: [/b>

• [b>Enable Failed Breakouts [/b> (ON/OFF):

- ON strongly recommended (highest edge)

• [b>Bars to Confirm Failure [/b> (2-10):

- 3 bars recommended

- 2 for aggressive (more signals, more false failures)

- 5+ for conservative (fewer signals, higher quality)

• [b>Failure Buffer [/b> (0.0-0.5 ATR):

- 0.1 ATR recommended

- Filters noise during consolidation near ORB level

• [b>Show Reversal Targets [/b> (ON/OFF):

- ON recommended (visualizes trade plan)

• [b>Reversal Target Mults [/b> (0.5x, 1.0x, 1.5x):

- Defaults are tested values

- Adjust based on average daily range

[b>Gap Analysis:

• [b>Show Gap Analysis [/b> (ON/OFF):

- ON if trading instruments that gap frequently

- OFF for 24hr markets (forex, crypto—no gaps)

• [b>Gap Fill Target [/b> (ON/OFF):

- ON to visualize previous close (gap fill level)

[b>VWAP:

• [b>Show VWAP [/b> (ON/OFF):

- ON recommended (key institutional level)

• [b>Show VWAP Bands [/b> (ON/OFF):

- ON in Standard/Advanced

- OFF in Simple

• [b>Band Multipliers (1.0σ, 2.0σ):

- Defaults are standard

- 1σ = normal range, 2σ = extreme

[b>Day Type: [/b>

• [b>Show Day Type Analysis [/b> (ON/OFF):

- ON recommended (critical for strategy adaptation)

• [b>Trend Day Threshold [/b> (1.0-2.5 IB mult):

- 1.5x recommended

- When price extends >1.5x IB, classifies as Trend Day

[b>Enhanced Visuals:

• [b>Show Momentum Candles [/b> (ON/OFF):

- ON for visual context

- OFF if chart gets too colorful

• [b>Show Gradient Zone Fills [/b> (ON/OFF):

- ON for professional look

- OFF for minimalist chart

• [b>Label Display Mode [/b> (All/Adaptive/Minimal):

- Adaptive recommended (shows nearby labels only)

- All for information density

- Minimal for clean chart

• [b>Label Proximity [/b> (1.0-5.0 ATR):

- 3.0 ATR recommended

- Labels beyond this distance are hidden (Adaptive mode)

[b>🎓 PROFESSIONAL USAGE PROTOCOL [/b>

[b>Phase 1: Learning the System (Week 1) [/b>

[b>Goal: [/b> Understand ORB concepts and dashboard interpretation

[b>Setup: [/b>

• Display Mode: STANDARD

• ORB Timeframe: 30 minutes

• Enable ALL features (IB, extensions, failed breakouts, VWAP, gap analysis)

• Enable statistics tracking

[b>Actions: [/b>

• Paper trade ONLY—no real money

• Observe ORB formation every day (9:30-10:00 AM ET for US markets)

• Note when ORB breakouts occur and if they extend

• Note when breakouts fail and reversals happen

• Watch day type classification evolve during session

• Track statistics—which setups are working?

[b>Key Learning: [/b>

• How often do breakouts reach 1.5x extension? (typically 50-60% of confirmed breakouts)

• How often do breakouts fail? (typically 30-40%)

• Which setup grade (A/B/C) actually performs best? (should see A-grade outperforming)

• What day type produces best results? (trend days favor breakouts, rotation days favor fades)

[b>Phase 2: Parameter Optimization (Week 2) [/b>

[b>Goal: [/b> Tune system to your instrument and timeframe

[b>ORB Timeframe Selection:

• Run 5 days with 15-minute ORB

• Run 5 days with 30-minute ORB

• Compare: Which captures better breakouts on your instrument?

• Typically: 30-minute optimal for most, 15-minute for very liquid (ES, SPY)

[b>Volume Confirmation Testing:

• Run 5 days WITH volume confirmation

• Run 5 days WITHOUT volume confirmation

• Compare: Does volume confirmation increase win rate?

• If win rate improves by >5%: Keep volume confirmation ON

• If no improvement: Turn OFF (avoid missing valid breakouts)

[b>Failed Breakout Bars:

[b>Goal: [/b> Develop personal trading rules based on system signals

[b>Setup Selection Rules: [/b>

Define which setups you'll trade:

• [b>Conservative: [/b> Only A+ and A grades

• [b>Balanced: [/b> A+, A, B+ grades

• [b>Aggressive: [/b> All grades B and above

Test each approach for 5-10 trades, compare results.

[b>Position Sizing by Grade: [/b>

Consider risk-weighting by setup quality:

• A+ grade: 100% position size

• A grade: 75% position size

• B+ grade: 50% position size

• B grade: 25% position size

Example: If max risk is $1000/trade:

• A+ setup: Risk $1000

• A setup: Risk $750

• B+ setup: Risk $500

This matches bet sizing to edge.

[b>Day Type Adaptation: [/b>

Create rules for different day types:

Trend Days:

• Take ALL breakout signals (A/B/C grades)

• Hold for 2.0x extension minimum

• Trail stops aggressively (1.0 ATR trail)

• DON'T fade—reversals unlikely

Rotation Days:

• ONLY take failed breakout reversals

• Ignore initial breakout signals (likely to fail)

• Take profits quickly (0.5x extension)

• Focus on fade setups (Fade High/Fade Low)

Normal Days:

• Take A/A+ breakout signals only

• Take ALL failed breakout reversals (high probability)

• Target 1.0-1.5x extensions

• Partial profit-taking at extensions

Time-of-Day Rules: [/b>

Breakouts at different times have different probabilities:

10:00-10:30 AM (Early Breakout):

• ORB just completed

• Fresh breakout

• Probability: Moderate (50-55% reach 1.0x)

• Strategy: Conservative position sizing

10:30-12:00 PM (Mid-Morning):

• Momentum established

• Volume still healthy

• Probability: High (60-65% reach 1.0x)

• Strategy: Standard position sizing

12:00-2:00 PM (Lunch Doldrums):

• Volume dries up

• Whipsaw risk increases

• Probability: Low (40-45% reach 1.0x)

• Strategy: Avoid new entries OR reduce size 50%

2:00-4:00 PM (Afternoon Session):

• Late-day positioning

• EOD squeezes possible

• Probability: Moderate-High (55-60%)

• Strategy: Watch for IB break—if trending all day, follow

[b>Phase 4: Live Micro-Sizing (Month 2) [/b>

[b>Goal: [/b> Validate paper trading results with minimal risk

[b>Setup: [/b>

• 10-20% of intended full position size

• Take ONLY A+ and A grade setups

• Follow stop loss and targets religiously

[b>Execution: [/b>

• Execute from alerts OR from dashboard setup box

• Entry: Close of signal bar OR next bar market order

• Stop: Use exact stop from setup (don't widen)

• Targets: Scale out at T1/T2/T3 as indicated

[b>Tracking: [/b>

• Log every trade: Entry, Exit, Grade, Outcome, Day Type

• Calculate: Win rate, Average R-multiple, Max consecutive losses

• Compare to paper trading results (should be within 15%)

[b>Red Flags: [/b>

• Win rate <45%: System not suitable for this instrument/timeframe

• Major divergence from paper trading: Execution issues (slippage, late entries, emotional exits)

• Max consecutive losses >8: Hitting rough patch OR market regime changed

[b>Phase 5: Scaling Up (Months 3-6)

[b>Goal: [/b> Gradually increase to full position size

[b>Progression: [/b>

• Month 3: 25-40% size (if micro-sizing profitable)

• Month 4: 40-60% size

• Month 5: 60-80% size

• Month 6: 80-100% size

[b>Milestones Required to Scale Up: [/b>

• Minimum 30 trades at current size

• Win rate ≥48%

• Profit factor ≥1.2

• Max drawdown <20%

• Emotional control (no revenge trading, no FOMO)

[b>Advanced Techniques:

[b>Multi-Timeframe ORB: Assumes first 30-60 minutes establish value. Violation: Market opens after major news, price discovery continues for hours (opening range meaningless).

2. [b>Volume Indicates Conviction: ES, NQ, RTY, SPY, QQQ—high liquidity, clean ORB formation, reliable extensions

• [b>Large-Cap Stocks: AAPL, MSFT, TSLA, NVDA (>$5B market cap, >5M daily volume)

• [b>Liquid Futures: CL (crude oil), GC (gold), 6E (EUR/USD), ZB (bonds)—24hr markets benefit from session ORBs

• [b>Major Forex Pairs: [/b> EUR/USD, GBP/USD, USD/JPY—London/NY session ORBs work well

[b>Performs Poorly On: [/b>

• [b>Illiquid Stocks: <$1M daily volume, wide spreads, gappy price action

• [b>Penny Stocks: [/b> Manipulated, pump-and-dump, no real price discovery

• [b>Low-Volume ETFs: Exotic sector ETFs, leveraged products with thin volume

• [b>Crypto on Sketchy Exchanges: Wash trading, spoofing invalidates volume analysis

• [b>Earnings Days: [/b> ORB completes before earnings release, then completely resets (useless)

• Binary Event Days: FDA approvals, court rulings—discontinuous price action

[b>Known Weaknesses: [/b>

• [b>Slow Starts: ORB doesn't complete until 10:00 AM (30-min ORB). Early morning traders have no signals for 30 minutes. Consider using 15-minute ORB if this is problematic.

• [b>Failure Detection Lag: [/b> Failed breakout requires 3+ bars to confirm. By the time system signals reversal, price may have already moved significantly back inside range. Manual traders watching in real-time can enter earlier.

• [b>Extension Overshoot: [/b> System projects extensions mathematically (1.5x, 2.0x, etc.). Actual moves may stop short (1.3x) or overshoot (2.2x). Extensions are targets, not magnets.

• [b>Day Type Misclassification: [/b> Early in session, day type is "Developing." By the time it's classified definitively (often 11:00 AM+), half the day is over. Strategy adjustments happen late.

• [b>Gap Assumptions: [/b> System assumes gaps want to fill. Strong trend days never fill gaps (gap becomes support/resistance forever). Blindly trading toward gaps can backfire on trend days.

• [b>Volume Data Quality: Forex doesn't have centralized volume (uses tick volume as proxy—less reliable). Crypto volume is often fake (wash trading). Volume confirmation less effective on these instruments.

• [b>Multi-Session Complexity: [/b> When using Asian/London/NY ORBs simultaneously, chart becomes cluttered. Requires discipline to focus on relevant session for current time.

[b>Risk Factors: [/b>

• [b>Opening Gaps: Large gaps (>2%) can create distorted ORBs. Opening range might be unusually wide or narrow, making extensions unreliable.

• [b>Low Volatility Environments:[/b> When VIX <12, opening ranges can be tiny (0.2-0.3%). Extensions are equally tiny. Profit targets don't justify commission/slippage.

• [b>High Volatility Environments:[/b> When VIX >30, opening ranges are huge (2-3%+). Extensions project unrealistic targets. Failed breakouts happen faster (volatility whipsaw).