Vantage_NewsVantage News is a Pine Script library that provides pre-market economic event filtering defaults intended for strategies that trade on YM futures. It determines a default for whether trading should be blocked, delayed, or allowed on any given day.

Core Concept

News events are pre-compiled into Pine Script data libraries organized by half-year (LO1_News2025H1, LO1_News2025H2, etc.), updated weekly on Sundays. There are no API calls — events are baked into arrays of dates, times, type IDs, and severities.

Severity System

Can be configured to define or override three default severity tiers:

- Sev 3 (CPI, NFP, FOMC) — defaults to blocks the entire day or delays, depending on policy

- Sev 2 (ISM PMI, claims) — defaults to delay trading until the event time + a configurable post-delay window

- Sev 1 (secondary indicators) — defaults to no delays

Blocking vs Delaying

- Block: No trading for the full session. WillTradeToday() returns false.

- Delay: Trading allowed after eventTime + delayMinutes. IsDelayed(currentTimeMs) returns true until the release time passes.

Provides a per-event-type policy mechanism so overrides can force any event to block, delay, or be ignored regardless of its base severity.

Next Trading Window Calculation

FindNextTradingWindow() scans forward up to 14 days, skipping weekends and blocked days based on the provided configuration. If the next tradeable day has a delay, it returns the delayed start time — so an info panel can show e.g. "Mon 7:35 AM" to indicate the next trading opening

Exception Mappings

Each half-year library can ship per-event-type overrides (different severity, custom delay minutes, tags). When the applyLibExceptionMappings configuration is enabled, these override the base severity — allowing the data to carry date-specific adjustments.

Special Handling

CME early close days are encoded as a special event type. CheckCmeEarlyClose() returns a halt timestamp so a strategy can truncate the session.

Caching

Evaluation is lazy and memoized by date string — EvaluateForDate() only recomputes when the date changes. The event cache is built once at initialization via a day index for fast date lookups.

Strategies

TPOSmartMoneyLibLibrary "TPOSmartMoneyLib"

Library for TPO (Time Price Opportunity) and Smart Money concepts including session management, PDH/PDL detection, sweeping logic, and volume profile utilities

f_price_to_tick(p)

Convert price to tick

Parameters:

p (float) : Price value

Returns: Tick value

f_tick_to_row(t, row_ticks_in)

Convert tick to row

Parameters:

t (int) : Tick value

row_ticks_in (int) : Number of ticks per row

Returns: Row index

f_row_to_price(row, row_ticks_in)

Convert row to price (midpoint)

Parameters:

row (int) : Row index

row_ticks_in (int) : Number of ticks per row

Returns: Price at row midpoint

f_calc_row_ticks(natr_ref, row_gran_mult)

Calculate dynamic row size based on normalized ATR

Parameters:

natr_ref (float) : Daily normalized ATR reference value

row_gran_mult (float) : Row granularity multiplier

Returns: Number of ticks per row

f_more_transp_pct(c, pct)

Increase color transparency by percentage

Parameters:

c (color) : Input color

pct (float) : Percentage to increase transparency (0.0 to 1.0)

Returns: Color with increased transparency

f_dom_color(dom, buy_col, sell_col, gamma, transp_weak, transp_strong)

Calculate dominance color based on buy/sell ratio

Parameters:

dom (float) : Dominance ratio (-1 to 1, negative = sell, positive = buy)

buy_col (color) : Buy dominant color

sell_col (color) : Sell dominant color

gamma (float) : Gamma correction for color intensity

transp_weak (int) : Transparency for weak dominance

transp_strong (int) : Transparency for strong dominance

Returns: Blended color

f_sess_part(sess_str, get_start)

Parse session string to get start or end time

Parameters:

sess_str (string) : Session string in format "HHMM-HHMM"

get_start (bool) : True to get start time, false to get end time

Returns: Time string in HHMM format

f_hhmm_to_h(hhmm)

Convert HHMM string to hours

Parameters:

hhmm (string) : Time string in HHMM format

Returns: Hours (0-23)

f_hhmm_to_m(hhmm)

Convert HHMM string to minutes

Parameters:

hhmm (string) : Time string in HHMM format

Returns: Minutes (0-59)

f_prev_day_window_bounds(today_day_rth, win_start, win_end, session_tz)

Calculate previous day window bounds

Parameters:

today_day_rth (int) : Today's RTH start timestamp

win_start (string) : Window start time in HHMM format

win_end (string) : Window end time in HHMM format

session_tz (string) : Session timezone

Returns: Tuple of

f_default_session_colors()

Get default session colors

Returns: Array of 4 colors

f_session_names()

Get session names

Returns: Array of 4 session names

f_process_hl(arr, rng, keep_bars, lock_to_live)

Process high/low lines with sweeping detection

Parameters:

arr (array) : Array of HLLine objects

rng (float) : Price range for visibility filtering

keep_bars (int) : Maximum bars to keep lines

lock_to_live (bool) : Whether to lock line end to current bar

Returns: 0 (for chaining)

f_process_naked_lines(arr, calc_bars, bars_per_day, keep_to_day_end)

Process naked lines (POC/VAH/VAL) with sweeping detection

Parameters:

arr (array) : Array of NakedLine objects

calc_bars (int) : Maximum calculation bars

bars_per_day (int) : Bars per day for scope calculation

keep_to_day_end (bool) : Whether to extend to day end

Returns: 0 (for chaining)

f_update_pdhl_lines(pd_hl, pdh, pdl, new_day, pd_rng, bars_per_day, pdh_color, pdl_color)

Detect and create PDH/PDL lines

Parameters:

pd_hl (array) : Array to store HLLine objects

pdh (float) : Previous day high

pdl (float) : Previous day low

new_day (bool) : Whether it's a new day

pd_rng (float) : Price range for visibility

bars_per_day (int) : Bars per day

pdh_color (color) : PDH line color

pdl_color (color) : PDL line color

Returns: 0 (for chaining)

f_poc_from_vals(keys, vals)

Calculate POC from sorted keys and values

Parameters:

keys (array) : Sorted array of row keys

vals (array) : Array of volume values

Returns: POC row key

f_value_area(keys, vals, poc_key, va_pct)

Calculate Value Area from volume distribution

Parameters:

keys (array) : Sorted array of row keys

vals (array) : Array of volume values

poc_key (int) : POC row key

va_pct (float) : Value Area percentage (typically 0.70)

Returns: Tuple of

f_find_key_sorted(keys, target)

Find key in sorted array using binary search

Parameters:

keys (array) : Sorted array of keys

target (int) : Target key to find

Returns: Index of key, or -1 if not found

f_zscore_safe(x, len)

Safe z-score calculation using built-in functions

Parameters:

x (float) : Input series

len (int) : Lookback length

Returns: Z-score

HLLine

Represents a high/low line with sweeping detection

Fields:

ln (series line) : Line object

lb (series label) : Label object

lvl (series float) : Price level

startBar (series int) : Bar index where line starts

swept (series bool) : Whether the level has been swept

isHigh (series bool) : True if this is a high, false if low

col (series color) : Line color

NakedLine

Represents a naked POC/VAH/VAL line

Fields:

ln (series line) : Line object

lb (series label) : Label object

lvl (series float) : Price level

startBar (series int) : Bar index where line starts

swept (series bool) : Whether the level has been swept

sweptBar (series int) : Bar index where swept occurred

endBar (series int) : Bar index where line should end

LiveTracker by N&MLiveTracker is a real-time trade execution and accounting engine built on top of statistically validated backtest states.

It mirrors live trading conditions with precise fee modeling, partial take-profits, trailing stops, and liquidation logic.

Each trade is tracked with both mark-to-market PnL and “net if closed now” metrics for full transparency.

Designed as a modular Pine Script® library, it enables reliable, state-driven live execution without repainting.

TradingHelperLibLibrary "TradingHelperLib"

Trading Helper Library - Limit order, pip calculation and utility functions for trading bots

f_pipValue()

Calculates pip value based on symbol info

Returns: Pip value

f_pipsToPrice(pips)

Converts pip count to price difference

Parameters:

pips (float) : Number of pips

Returns: Price difference

calcExpireBarCount(minutesToExpire)

Converts minutes to bar count based on timeframe

Parameters:

minutesToExpire (float) : Duration in minutes

Returns: Bar count

calcLimitPrice(isLong, signalPrice, deviation, deviationType)

Calculates limit order price with deviation

Parameters:

isLong (bool) : True for long, false for short

signalPrice (float) : Signal price

deviation (float) : Deviation amount

deviationType (string) : Deviation type ("USDT" or "%")

Returns: Limit price

checkLimitFill(isLong, limitPrice)

Checks if limit order is filled

Parameters:

isLong (bool) : True for long, false for short

limitPrice (float) : Limit price to check

Returns: True if filled

f_multiplier(lvl, mode)

Calculates DCA multiplier based on level and mode

Parameters:

lvl (int) : DCA level

mode (string) : Multiplier mode ("Sabit", "Fibonacci", "Martingale", etc.)

Returns: Multiplier value

f_pctToPrice(pct, basePrice)

Converts percentage value to price difference

Parameters:

pct (float) : Percentage value (e.g. 2.0 = 2%)

basePrice (float) : Reference price

Returns: Price difference

f_priceChange_toPct(priceChange, basePrice)

Converts price change to percentage

Parameters:

priceChange (float) : Price difference

basePrice (float) : Reference price

Returns: Percentage value

calcMargin(notional, leverage)

Calculates margin from notional value

Parameters:

notional (float) : Trade size (e.g. $1000)

leverage (int) : Leverage value (e.g. 100)

Returns: Margin value

calcNotional(margin, leverage)

Calculates notional from margin

Parameters:

margin (float) : Collateral value

leverage (int) : Leverage value

Returns: Notional value

calcLiqPriceLongSimple(avgPrice, leverage)

Calculates simple liquidation price for Long position

Parameters:

avgPrice (float) : Average entry price

leverage (int) : Leverage value

Returns: Estimated liquidation price

calcLiqPriceShortSimple(avgPrice, leverage)

Calculates simple liquidation price for Short position

Parameters:

avgPrice (float) : Average entry price

leverage (int) : Leverage value

Returns: Estimated liquidation price

calcPnlLong(entryPrice, currentPrice, notional)

Calculates Long position PNL

Parameters:

entryPrice (float) : Entry price

currentPrice (float) : Current price

notional (float) : Position size

Returns: PNL value

calcPnlShort(entryPrice, currentPrice, notional)

Calculates Short position PNL

Parameters:

entryPrice (float) : Entry price

currentPrice (float) : Current price

notional (float) : Position size

Returns: PNL value

calcFee(notional, feeRate)

Calculates trading fee

Parameters:

notional (float) : Trade size

feeRate (float) : Fee rate in percentage (e.g. 0.1 = 0.1%)

Returns: Fee value

ArgentinaBondsLib - Argentina Sovereign Bonds Cashflow LibraryArgentinaBondsLib

A Pine Script v6 library providing cashflow data and financial calculation functions for Argentine sovereign bonds (Bonares and Globales).

## Supported Bonds

**Bonares** (Argentina legislation, USD MEP): AE38, AL29, AL30, AL35, AL41, AN29

**Globales** (Foreign legislation, USD Cable): GD29, GD30, GD35, GD38, GD41, GD46

## Exported Functions

### Cashflow Data

- `getCashflows_ ()` - Returns timestamps, cashflows, and count for each bond

### Bond Identification

- `getBondType(ticker)` - Returns BONAR() or GLOBAL()

- `getBaseTicker(ticker)` - Extracts base ticker without prefix/suffix

- `getCurrencyType(ticker)` - Returns 0=ARS, 1=MEP, 2=Cable

- `isSupported(baseTicker)` - Checks if bond is supported

### Financial Calculations

- `calcPV()` - Present Value calculation

- `calcIRR()` - Internal Rate of Return using Newton-Raphson method

- `calcPriceFromIRR()` - Calculate price from target IRR

### Currency Conversion

- `convertToNativeCurrency()` - Converts price to cashflow currency (MEP for Bonares, Cable for Globales)

### Utilities

- `getSettlementDate()` - Returns T+1 timestamp

- `BONAR()` / `GLOBAL()` - Bond type constants

## Methodology

- Day count convention: Actual/365

- Settlement: T+1

- IRR solver: Newton-Raphson iterative method

## Usage Example

```

import EcoValores/ArgentinaBondsLib/1 as Bonds

= Bonds.getCashflows_AL30()

settlementDate = Bonds.getSettlementDate()

irr = Bonds.calcIRR(ts, cf, count, settlementDate, close)

```

---

## Español

Librería Pine Script v6 con datos de flujos de fondos y funciones de cálculo financiero para bonos soberanos argentinos.

### Bonos Soportados

- **Bonares** (Legislación argentina, USD MEP): AE38, AL29, AL30, AL35, AL41, AN29

- **Globales** (Legislación extranjera, USD Cable): GD29, GD30, GD35, GD38, GD41, GD46

### Metodología

- Convención de días: Actual/365

- Liquidación: T+1

- Solver TIR: Método iterativo Newton-Raphson

---

**DISCLAIMER**: This library is for informational and educational purposes only. Eco Valores S.A. does NOT provide investment advice or recommendations. Consult a qualified financial advisor before making investment decisions.

**AVISO LEGAL**: Esta librería es solo para fines informativos y educativos. Eco Valores S.A. NO brinda asesoramiento ni recomendaciones de inversión. Consulte con un asesor financiero calificado antes de invertir.

LO1_News2024H1Library "LO1_News2024H1"

Support Library for News Events

f_loadNewsRows()

f_loadExcSevByTypeId()

f_loadExcTagByTypeId()

f_loadExcDelayAfterNewsMins()

LO1_News2026H1Library "LO1_News2026H1"

Support Library for News Events

f_loadNewsRows()

f_loadExcSevByTypeId()

f_loadExcTagByTypeId()

f_loadExcDelayAfterNewsMins()

LO1_News2025H2Library "LO1_News2025H2"

Support Library for News Events

f_loadNewsRows()

f_loadExcSevByTypeId()

f_loadExcTagByTypeId()

f_loadExcDelayAfterNewsMins()

LO1_News2025H1Library "LO1_News2025H1"

Support Library for News Events

f_loadNewsRows()

f_loadExcSevByTypeId()

f_loadExcTagByTypeId()

f_loadExcDelayAfterNewsMins()

LO1_News2024H2Library "LO1_News2024H2"

Support Library for News Events

f_loadNewsRows()

f_loadExcSevByTypeId()

f_loadExcTagByTypeId()

f_loadExcDelayAfterNewsMins()

LO1_TradersPostLibrary "LO1_TradersPost"

Enhanced TradersPost integration library with comprehensive order management

_buildJSONField(key, value, required)

Build a JSON field with proper handling of required vs optional fields

Parameters:

key (string) : The JSON key name

value (string) : The value to include (any type, will be converted to string)

required (bool) : If true, field is always included even if value is na/empty

Returns: String containing JSON field or empty string if optional and na/empty

_buildConditionalField(key, value)

Build a conditional JSON field that's only included if value is valid

Parameters:

key (string) : The JSON key name

value (string) : The value to include

Returns: String containing JSON field or empty string if value is na/empty

_buildConditionalNumericField(key, value)

Build a conditional JSON field for numeric values

Parameters:

key (string) : The JSON key name

value (float) : The numeric value

Returns: String containing JSON field or empty string if value is na

_buildNestedObject(objectType, price, amount, percent, stopType, limitPrice, trailAmount, trailPercent)

Build nested JSON objects for takeProfit/stopLoss

Parameters:

objectType (string) : The type of object being built ("takeProfit" or "stopLoss")

price (float) : The limit price for TP or stop price for SL

amount (float) : The dollar amount (optional)

percent (float) : The percentage (optional)

stopType (series StopLossType) : The stop loss type - only for stopLoss

limitPrice (float) : The limit price for stop_limit orders - only for stopLoss

trailAmount (float) : Trailing amount for trailing stops - only for stopLoss

trailPercent (float) : Trailing percent for trailing stops - only for stopLoss

Returns: String containing nested JSON object or empty string if no valid data

_validateAndBuildJSON(ticker, action, quantity, quantityType, orderType, sentiment, cancel, timeInForce, limitPrice, stopPrice, trailAmount, trailPercent, takeProfitPrice, takeProfitAmount, takeProfitPercent, stopLossPrice, stopLossAmount, stopLossPercent, stopLossType, stopLossLimitPrice, extendedHours, optionType, intrinsicValue, expiration, strikePrice, signalPrice, comment)

Master JSON builder that validates parameters and constructs JSON

Parameters:

ticker (string) : The trading symbol

action (series Action) : The order action (buy, sell, exit, etc.)

quantity (float) : The order quantity

quantityType (series QuantityType) : The type of quantity (fixed, dollar, percent)

orderType (series OrderType) : The order type (market, limit, stop, etc.)

sentiment (series Sentiment) : The position sentiment (long, short, flat) - optional

cancel (bool) : Controls order cancellation (true = cancel existing orders, false = don't cancel)

timeInForce (series TimeInForce) : Time in force for the order (DAY, GTC, IOC, FOK)

limitPrice (float) : Price for limit orders

stopPrice (float) : Price for stop orders

trailAmount (float) : Trailing amount for trailing stops

trailPercent (float) : Trailing percent for trailing stops

takeProfitPrice (float) : Take profit limit price (absolute)

takeProfitAmount (float) : Take profit dollar amount (relative)

takeProfitPercent (float) : Take profit percentage (relative)

stopLossPrice (float) : Stop loss price (absolute)

stopLossAmount (float) : Stop loss dollar amount (relative)

stopLossPercent (float) : Stop loss percentage (relative)

stopLossType (series StopLossType) : Stop loss order type

stopLossLimitPrice (float) : Limit price for stop_limit orders

extendedHours (bool) : Enable extended hours trading (boolean)

optionType (series OptionType) : Option type for options trading (both/call/put)

intrinsicValue (series IntrinsicValue) : Intrinsic value filter for options (itm/otm)

expiration (string) : Option expiration (date string)

strikePrice (float) : Option strike price

signalPrice (float) : The market price at alert time (for slippage tracking)

comment (string) : Optional comment for the order (shows in TradersPost UI for debugging)

Returns: ErrorResponse with success status and JSON string or error details

ValidateOrder(ticker, action, orderType, limitPrice, stopPrice)

Validate order parameters before JSON construction

Parameters:

ticker (string) : Trading symbol

action (series Action) : Order action

orderType (series OrderType) : Order type (market, limit, stop, etc.)

limitPrice (float) : Limit price for limit orders

stopPrice (float) : Stop price for stop orders

Returns: ErrorResponse with validation results

ValidateQuantity(quantity, quantityType)

Validate quantity based on type and constraints

Parameters:

quantity (float) : The quantity value

quantityType (series QuantityType) : The type of quantity

Returns: ErrorResponse with validation results

ValidatePrices(entryPrice, stopPrice, takeProfitPrice, action)

Validate price relationships and values

Parameters:

entryPrice (float) : Entry price for the order

stopPrice (float) : Stop loss price

takeProfitPrice (float) : Take profit price

action (series Action) : Order action (buy/sell)

Returns: ErrorResponse with validation results

ValidateSymbol(ticker)

Validate trading symbol format

Parameters:

ticker (string) : The symbol to validate

Returns: ErrorResponse with validation results

CombineValidationResults(validationResults)

Create validation error collection and reporting system

Parameters:

validationResults (array) : Array of ErrorResponse objects from multiple validations

Returns: Combined ErrorResponse with all validation results

ValidateCompleteOrder(ticker, action, quantity, quantityType, orderType, limitPrice, stopPrice, takeProfitPrice)

Comprehensive validation for all order parameters

Parameters:

ticker (string) : Trading symbol

action (series Action) : Order action

quantity (float) : Order quantity

quantityType (series QuantityType) : Type of quantity

orderType (series OrderType) : Order type

limitPrice (float) : Limit price (optional)

stopPrice (float) : Stop price (optional)

takeProfitPrice (float) : Take profit price (optional)

Returns: ErrorResponse with complete validation results

CreateErrorResponse(success, errorMessages, message, severity, context, functionName)

Create standardized error response

Parameters:

success (bool) : Whether the operation succeeded

errorMessages (array) : Array of error messages

message (string) : Summary message

severity (series ErrorSeverity) : Error severity level

context (string) : Context where error occurred

functionName (string) : Name of function that generated error

Returns: EnhancedErrorResponse with all error details

HandleValidationError(validationResult, context, functionName)

Handle validation errors with context

Parameters:

validationResult (ErrorResponse) : The validation result to handle

context (string) : Description of what was being validated

functionName (string) : Name of calling function

Returns: Processed error response with enhanced context

LogError(errorResponse, displayOnChart)

Log error with appropriate level

Parameters:

errorResponse (EnhancedErrorResponse) : The error response to log

displayOnChart (bool) : Whether to show error on chart

CreateSuccessResponse(message, context, functionName)

Create success response

Parameters:

message (string) : Success message

context (string) : Context of successful operation

functionName (string) : Name of function

Returns: Success response

_validateJSONConstruction(jsonString)

Validate JSON construction and handle malformed data

Parameters:

jsonString (string) : The constructed JSON string

Returns: ErrorResponse indicating if JSON is valid

CreateDetailedError(success, errors, warnings, severity, context)

Create detailed error response with context

Parameters:

success (bool) : Operation success status

errors (array) : Array of error messages

warnings (array) : Array of warning messages

severity (series ErrorSeverity) : Error severity level

context (string) : Context where error occurred

Returns: DetailedErrorResponse object

LogDetailedError(response)

Log detailed error response with appropriate severity

Parameters:

response (DetailedErrorResponse) : DetailedErrorResponse to log

Returns: Nothing - logs to Pine Script console

CombineIntoDetailedResponse(responses, context)

Combine multiple error responses into detailed response

Parameters:

responses (array) : Array of ErrorResponse objects to combine

context (string) : Context for the combined operation

Returns: DetailedErrorResponse with combined results

SendAdvancedOrder(ticker, action, quantity, quantityType, orderType, sentiment, cancel, limitPrice, stopPrice, trailAmount, trailPercent, takeProfitPrice, takeProfitAmount, takeProfitPercent, stopLossPrice, stopLossAmount, stopLossPercent, stopLossType, stopLossLimitPrice, extendedHours, optionType, intrinsicValue, expiration, strikePrice, signalPrice, comment)

Send advanced order with comprehensive parameter validation and JSON construction

Parameters:

ticker (string) : Symbol to trade (defaults to syminfo.ticker)

action (series Action) : Order action (buy/sell/exit/cancel/add)

quantity (float) : Order quantity

quantityType (series QuantityType) : Type of quantity (fixed/dollar/percent)

orderType (series OrderType) : Type of order (market/limit/stop/stop_limit/trailing_stop)

sentiment (series Sentiment) : Position sentiment (long/short/flat, optional)

cancel (bool) : Controls order cancellation (true = cancel existing, false = don't cancel, na = use defaults)

limitPrice (float) : Limit price for limit orders

stopPrice (float) : Stop price for stop orders

trailAmount (float) : Trailing amount for trailing stops

trailPercent (float) : Trailing percent for trailing stops

takeProfitPrice (float) : Take profit limit price (absolute)

takeProfitAmount (float) : Take profit dollar amount (relative)

takeProfitPercent (float) : Take profit percentage (relative)

stopLossPrice (float) : Stop loss price (absolute)

stopLossAmount (float) : Stop loss dollar amount (relative)

stopLossPercent (float) : Stop loss percentage (relative)

stopLossType (series StopLossType) : Stop loss order type

stopLossLimitPrice (float) : Limit price for stop_limit orders

extendedHours (bool) : Enable extended hours trading (boolean)

optionType (series OptionType) : Option type for options trading (both/call/put)

intrinsicValue (series IntrinsicValue) : Intrinsic value filter for options (itm/otm)

expiration (string) : Option expiration (date string)

strikePrice (float) : Option strike price

signalPrice (float) : The market price at alert time (for slippage tracking)

comment (string) : Optional comment for the order (shows in TradersPost UI for debugging)

Returns: ErrorResponse with success status and JSON or error details

SendSentiment(ticker, sentiment, quantity, quantityType, signalPrice, comment)

Send sentiment-based position management order

Parameters:

ticker (string) : Symbol to manage (defaults to syminfo.ticker)

sentiment (series Sentiment) : Target position sentiment (long/short/flat)

quantity (float) : Position size (optional, uses account default if not specified)

quantityType (series QuantityType) : Type of quantity specification

signalPrice (float) : The market price at alert time (for slippage tracking)

comment (string) : Optional comment

Returns: ErrorResponse with success status

SendCancelAll(ticker, comment)

Cancel all open orders for the specified symbol

Parameters:

ticker (string) : Symbol to cancel orders for (defaults to syminfo.ticker)

comment (string) : Optional comment for the cancellation

Returns: ErrorResponse with success status

SendOrderNoCancelExisting(ticker, action, quantity, quantityType, orderType, sentiment, limitPrice, stopPrice, takeProfitPrice, takeProfitAmount, takeProfitPercent, stopLossPrice, stopLossAmount, stopLossPercent, stopLossType, stopLossLimitPrice, signalPrice, comment)

Send order without canceling existing orders

Parameters:

ticker (string) : Symbol to trade (defaults to syminfo.ticker)

action (series Action) : Order action (buy/sell/exit)

quantity (float) : Order quantity

quantityType (series QuantityType) : Type of quantity (fixed/dollar/percent)

orderType (series OrderType) : Type of order (market/limit/stop/stop_limit)

sentiment (series Sentiment) : Position sentiment (long/short/flat, optional)

limitPrice (float) : Limit price for limit orders

stopPrice (float) : Stop price for stop orders

takeProfitPrice (float) : Take profit price

takeProfitAmount (float) : Take profit amount (optional)

takeProfitPercent (float)

stopLossPrice (float) : Stop loss price

stopLossAmount (float) : Stop loss amount (optional)

stopLossPercent (float) : Stop loss percentage (optional)

stopLossType (series StopLossType) : Stop loss order type

stopLossLimitPrice (float) : Limit price for stop_limit orders

signalPrice (float) : The market price at alert time (for slippage tracking)

comment (string) : Optional comment

Returns: ErrorResponse with success status

_buildBracketOrderParams(orderType, entryPrice, entryLimitPrice)

Build bracket order parameters by routing entryPrice to correct parameter based on orderType

This helper function maps the conceptual "entryPrice" to the technical parameters needed

Parameters:

orderType (series OrderType) : The order type for the entry order

entryPrice (float) : The desired entry price (trigger for stops, limit for limits)

entryLimitPrice (float) : The limit price for stop_limit orders (optional)

Returns: array with correct routing

SendBracketOrder(ticker, action, quantity, quantityType, orderType, entryPrice, entryLimitPrice, takeProfitPrice, stopLossPrice, takeProfitAmount, takeProfitPercent, stopLossAmount, stopLossPercent, stopLossType, stopLossLimitPrice, signalPrice, comment)

Send bracket order (entry + take profit + stop loss)

Parameters:

ticker (string) : Symbol to trade

action (series Action) : Entry action (buy/sell)

quantity (float) : Order quantity

quantityType (series QuantityType) : Type of quantity specification

orderType (series OrderType) : Type of entry order

entryPrice (float) : Entry price (trigger price for stop orders, limit price for limit orders)

entryLimitPrice (float) : Entry limit price (only for stop_limit orders, defaults to entryPrice if na)

takeProfitPrice (float) : Take profit price

stopLossPrice (float) : Stop loss price

takeProfitAmount (float) : Take profit dollar amount (alternative to price)

takeProfitPercent (float) : Take profit percentage (alternative to price)

stopLossAmount (float) : Stop loss dollar amount (alternative to price)

stopLossPercent (float) : Stop loss percentage (alternative to price)

stopLossType (series StopLossType) : Stop loss order type

stopLossLimitPrice (float) : Limit price for stop_limit orders

signalPrice (float) : The market price at alert time (for slippage tracking)

comment (string) : Optional comment

Returns: ErrorResponse with success status

SendOTOOrder(primaryTicker, primaryAction, primaryQuantity, primaryOrderType, primaryPrice, secondaryTicker, secondaryAction, secondaryQuantity, secondaryOrderType, secondaryPrice, signalPrice, comment)

Send One-Triggers-Other (OTO) order sequence

Note: OTO linking must be configured in TradersPost strategy settings

This sends two separate orders - TradersPost handles the OTO logic

Parameters:

primaryTicker (string) : Primary order ticker

primaryAction (series Action) : Primary order action

primaryQuantity (float) : Primary order quantity

primaryOrderType (series OrderType) : Primary entry type

primaryPrice (float) : Primary order price

secondaryTicker (string) : Secondary order ticker (defaults to primary ticker)

secondaryAction (series Action) : Secondary order action

secondaryQuantity (float) : Secondary order quantity

secondaryOrderType (series OrderType) : Secondary entry type

secondaryPrice (float) : Secondary order price

signalPrice (float) : The market price at alert time (for slippage tracking)

comment (string) : Optional comment for both orders

Returns: ErrorResponse with success status

SendOCOOrder(ticker, firstAction, firstQuantity, firstOrderType, firstPrice, secondAction, secondQuantity, secondOrderType, secondPrice, signalPrice, comment)

Send One-Cancels-Other (OCO) order pair

Note: OCO linking must be configured in TradersPost strategy settings

This sends two separate orders - TradersPost handles the OCO logic

Parameters:

ticker (string) : Symbol for both orders

firstAction (series Action) : Action for first order

firstQuantity (float) : Quantity for first order

firstOrderType (series OrderType) : Order type for first order

firstPrice (float) : Price for first order

secondAction (series Action) : Action for second order

secondQuantity (float) : Quantity for second order

secondOrderType (series OrderType) : Order type for second order

secondPrice (float) : Price for second order

signalPrice (float) : The market price at alert time (for slippage tracking)

comment (string) : Optional comment

Returns: ErrorResponse with success status

ErrorResponse

Fields:

success (series bool)

errors (array)

message (series string)

EnhancedErrorResponse

Fields:

success (series bool)

errors (array)

message (series string)

severity (series ErrorSeverity)

context (series string)

timestamp (series int)

functionName (series string)

DetailedErrorResponse

Fields:

success (series bool)

errors (array)

warnings (array)

severity (series ErrorSeverity)

context (series string)

message (series string)

DeeptestDeeptest: Quantitative Backtesting Library for Pine Script

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ OVERVIEW

Deeptest is a Pine Script library that provides quantitative analysis tools for strategy backtesting. It calculates over 100 statistical metrics including risk-adjusted return ratios (Sharpe, Sortino, Calmar), drawdown analysis, Value at Risk (VaR), Conditional VaR, and performs Monte Carlo simulation and Walk-Forward Analysis.

█ WHY THIS LIBRARY MATTERS

Pine Script is a simple yet effective coding language for algorithmic and quantitative trading. Its accessibility enables traders to quickly prototype and test ideas directly within TradingView. However, the built-in strategy tester provides only basic metrics (net profit, win rate, drawdown), which is often insufficient for serious strategy evaluation.

Due to this limitation, many traders migrate to alternative backtesting platforms that offer comprehensive analytics. These platforms require other language programming knowledge, environment setup, and significant time investment—often just to test a simple trading idea.

Deeptest bridges this gap by bringing institutional-level quantitative analytics directly to Pine Script. Traders can now perform sophisticated analysis without leaving TradingView or learning complex external platforms. All calculations are derived from strategy.closedtrades.* , ensuring compatibility with any existing Pine Script strategy.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ ORIGINALITY AND USEFULNESS

This library is original work that adds value to the TradingView community in the following ways:

1. Comprehensive Metric Suite: Implements 112+ statistical calculations in a single library, including advanced metrics not available in TradingView's built-in tester (p-value, Z-score, Skewness, Kurtosis, Risk of Ruin).

2. Monte Carlo Simulation: Implements trade-sequence randomization to stress-test strategy robustness by simulating 1000+ alternative equity curves.

3. Walk-Forward Analysis: Divides historical data into rolling in-sample and out-of-sample windows to detect overfitting by comparing training vs. testing performance.

4. Rolling Window Statistics: Calculates time-varying Sharpe, Sortino, and Expectancy to analyze metric consistency throughout the backtest period.

5. Interactive Table Display: Renders professional-grade tables with color-coded thresholds, tooltips explaining each metric, and period analysis cards for drawdowns/trades.

6. Benchmark Comparison: Automatically fetches S&P 500 data to calculate Alpha, Beta, and R-squared, enabling objective assessment of strategy skill vs. passive investing.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ KEY FEATURES

Performance Metrics

Net Profit, CAGR, Monthly Return, Expectancy

Profit Factor, Payoff Ratio, Sample Size

Compounding Effect Analysis

Risk Metrics

Sharpe Ratio, Sortino Ratio, Calmar Ratio (MAR)

Martin Ratio, Ulcer Index

Max Drawdown, Average Drawdown, Drawdown Duration

Risk of Ruin, R-squared (equity curve linearity)

Statistical Distribution

Value at Risk (VaR 95%), Conditional VaR

Skewness (return asymmetry)

Kurtosis (tail fatness)

Z-Score, p-value (statistical significance testing)

Trade Analysis

Win Rate, Breakeven Rate, Loss Rate

Average Trade Duration, Time in Market

Consecutive Win/Loss Streaks with Expected values

Top/Worst Trades with R-multiple tracking

Advanced Analytics

Monte Carlo Simulation (1000+ iterations)

Walk-Forward Analysis (rolling windows)

Rolling Statistics (time-varying metrics)

Out-of-Sample Testing

Benchmark Comparison

Alpha (excess return vs. benchmark)

Beta (systematic risk correlation)

Buy & Hold comparison

R-squared vs. benchmark

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK START

Basic Usage

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as *

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ METRIC EXPLANATIONS

The Deeptest table displays 23 metrics across the main row, with 23 additional metrics in the complementary row. Each metric includes detailed tooltips accessible by hovering over the value.

Main Row — Performance Metrics (Columns 0-6)

Net Profit — (Final Equity - Initial Capital) / Initial Capital × 100

— >20%: Excellent, >0%: Profitable, <0%: Loss

— Total return percentage over entire backtest period

Payoff Ratio — Average Win / Average Loss

— >1.5: Excellent, >1.0: Good, <1.0: Losses exceed wins

— Average winning trade size relative to average losing trade. Breakeven win rate = 100% / (1 + Payoff)

Sample Size — Count of closed trades

— >=30: Statistically valid, <30: Insufficient data

— Number of completed trades. Includes 95% confidence interval for win rate in tooltip

Profit Factor — Gross Profit / Gross Loss

— >=1.5: Excellent, >1.0: Profitable, <1.0: Losing

— Ratio of total winnings to total losses. Uses absolute values unlike payoff ratio

CAGR — (Final / Initial)^(365.25 / Days) - 1

— >=10%: Excellent, >0%: Positive growth

— Compound Annual Growth Rate - annualized return accounting for compounding

Expectancy — Sum of all returns / Trade count

— >0.20%: Excellent, >0%: Positive edge

— Average return per trade as percentage. Positive expectancy indicates profitable edge

Monthly Return — Net Profit / (Months in test)

— >0%: Profitable month average

— Average monthly return. Geometric monthly also shown in tooltip

Main Row — Trade Statistics (Columns 7-14)

Avg Duration — Average time in position per trade

— Mean holding period from entry to exit. Influenced by timeframe and trading style

Max CW — Longest consecutive winning streak

— Maximum consecutive wins. Expected value = ln(trades) / ln(1/winRate)

Max CL — Longest consecutive losing streak

— Maximum consecutive losses. Important for psychological risk tolerance

Win Rate — Wins / Total Trades

— Higher is better

— Percentage of profitable trades. Breakeven win rate shown in tooltip

BE Rate — Breakeven Trades / Total Trades

— Lower is better

— Percentage of trades that broke even (neither profit nor loss)

Loss Rate — Losses / Total Trades

— Lower is better

— Percentage of unprofitable trades. Together with win rate and BE rate, sums to 100%

Frequency — Trades per month

— Trading activity level. Displays intelligently (e.g., "12/mo", "1.5/wk", "3/day")

Exposure — Time in market / Total time × 100

— Lower = less risk

— Percentage of time the strategy had open positions

Main Row — Risk Metrics (Columns 15-22)

Sharpe Ratio — (Return - Rf) / StdDev × sqrt(Periods)

— >=3: Excellent, >=2: Good, >=1: Fair, <1: Poor

— Measures risk-adjusted return using total volatility. Annualized using sqrt(252) for daily

Sortino Ratio — (Return - Rf) / DownsideDev × sqrt(Periods)

— >=2: Excellent, >=1: Good, <1: Needs improvement

— Similar to Sharpe but only penalizes downside volatility. Can be higher than Sharpe

Max DD — (Peak - Trough) / Peak × 100

— <5%: Excellent, 5-15%: Moderate, 15-30%: High, >30%: Severe

— Largest peak-to-trough decline in equity. Critical for risk tolerance and position sizing

RoR — Risk of Ruin probability

— <1%: Excellent, 1-5%: Acceptable, 5-10%: Elevated, >10%: Dangerous

— Probability of losing entire trading account based on win rate and payoff ratio

R² — R-squared of equity curve vs. time

— >=0.95: Excellent, 0.90-0.95: Good, 0.80-0.90: Moderate, <0.80: Erratic

— Coefficient of determination measuring linearity of equity growth

MAR — CAGR / |Max Drawdown|

— Higher is better, negative = bad

— Calmar Ratio. Reward relative to worst-case loss. Negative if max DD exceeds CAGR

CVaR — Average of returns below VaR threshold

— Lower absolute is better

— Conditional Value at Risk (Expected Shortfall). Average loss in worst 5% of outcomes

p-value — Binomial test probability

— <0.05: Significant, 0.05-0.10: Marginal, >0.10: Likely random

— Probability that observed results are due to chance. Low p-value means statistically significant edge

Complementary Row — Extended Metrics

Compounding — (Compounded Return / Total Return) × 100

— Percentage of total profit attributable to compounding (position sizing)

Avg Win — Sum of wins / Win count

— Average profitable trade return in percentage

Avg Trade — Sum of all returns / Total trades

— Same as Expectancy (Column 5). Displayed here for convenience

Avg Loss — Sum of losses / Loss count

— Average unprofitable trade return in percentage (negative value)

Martin Ratio — CAGR / Ulcer Index

— Similar to Calmar but uses Ulcer Index instead of Max DD

Rolling Expectancy — Mean of rolling window expectancies

— Average expectancy calculated across rolling windows. Shows consistency of edge

Avg W Dur — Avg duration of winning trades

— Average time from entry to exit for winning trades only

Max Eq — Highest equity value reached

— Peak equity achieved during backtest

Min Eq — Lowest equity value reached

— Trough equity point. Important for understanding worst-case absolute loss

Buy & Hold — (Close_last / Close_first - 1) × 100

— >0%: Passive profit

— Return of simply buying and holding the asset from backtest start to end

Alpha — Strategy CAGR - Benchmark CAGR

— >0: Has skill (beats benchmark)

— Excess return above passive benchmark. Positive alpha indicates genuine value-added skill

Beta — Covariance(Strategy, Benchmark) / Variance(Benchmark)

— <1: Less volatile than market, >1: More volatile

— Systematic risk correlation with benchmark

Avg L Dur — Avg duration of losing trades

— Average time from entry to exit for losing trades only

Rolling Sharpe/Sortino — Dynamic based on win rate

— >2: Good consistency

— Rolling metric across sliding windows. Shows Sharpe if win rate >50%, Sortino if <=50%

Curr DD — Current drawdown from peak

— Lower is better

— Present drawdown percentage. Zero means at new equity high

DAR — CAGR adjusted for target DD

— Higher is better

— Drawdown-Adjusted Return. DAR^5 = CAGR if max DD = 5%

Kurtosis — Fourth moment / StdDev^4 - 3

— ~0: Normal, >0: Fat tails, <0: Thin tails

— Measures "tailedness" of return distribution (excess kurtosis)

Skewness — Third moment / StdDev^3

— >0: Positive skew (big wins), <0: Negative skew (big losses)

— Return distribution asymmetry

VaR — 5th percentile of returns

— Lower absolute is better

— Value at Risk at 95% confidence. Maximum expected loss in worst 5% of outcomes

Ulcer — sqrt(mean(drawdown^2))

— Lower is better

— Ulcer Index - root mean square of drawdowns. Penalizes both depth AND duration

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ MONTE CARLO SIMULATION

Purpose

Monte Carlo simulation tests strategy robustness by randomizing the order of trades while keeping trade returns unchanged. This simulates alternative equity curves to assess outcome variability.

Method

Extract all historical trade returns

Randomly shuffle the sequence (1000+ iterations)

Calculate cumulative equity for each shuffle

Build distribution of final outcomes

Output

The stress test table shows:

Median Outcome: 50th percentile result

5th Percentile: Worst 5% of outcomes

95th Percentile: Best 95% of outcomes

Success Rate: Percentage of simulations that were profitable

Interpretation

If 95% of simulations are profitable: Strategy is robust

If median is far from actual result: High variance/unreliability

If 5th percentile shows large loss: High tail risk

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ WALK-FORWARD ANALYSIS

Purpose

Walk-Forward Analysis (WFA) is the gold standard for detecting strategy overfitting. It simulates real-world trading by dividing historical data into rolling "training" (in-sample) and "validation" (out-of-sample) periods. A strategy that performs well on unseen data is more likely to succeed in live trading.

Method

The implementation uses a non-overlapping window approach following AmiBroker's gold standard methodology:

Segment Calculation: Total trades divided into N windows (default: 12), IS = ~75%, OOS = ~25%, Step = OOS length

Window Structure: Each window has IS (training) followed by OOS (validation). Each OOS becomes the next window's IS (rolling forward)

Metrics Calculated: CAGR, Sharpe, Sortino, MaxDD, Win Rate, Expectancy, Profit Factor, Payoff

Aggregation: IS metrics averaged across all IS periods, OOS metrics averaged across all OOS periods

Output

IS CAGR: In-sample annualized return

OOS CAGR: Out-of-sample annualized return ( THE key metric )

IS/OOS Sharpe: In/out-of-sample risk-adjusted return

Success Rate: % of OOS windows that were profitable

Interpretation

Robust: IS/OOS CAGR gap <20%, OOS Success Rate >80%

Some Overfitting: CAGR gap 20-50%, Success Rate 50-80%

Severe Overfitting: CAGR gap >50%, Success Rate <50%

Key Principles:

OOS is what matters — Only OOS predicts live performance

Consistency > Magnitude — 10% IS / 9% OOS beats 30% IS / 5% OOS

Window count — More windows = more reliable validation

Non-overlapping OOS — Prevents data leakage

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ TABLE DISPLAY

Main Table — Organized into three sections:

Performance Metrics (Cols 0-6): Net Profit, Payoff, Sample Size, Profit Factor, CAGR, Expectancy, Monthly

Trade Statistics (Cols 7-14): Avg Duration, Max CW, Max CL, Win, BE, Loss, Frequency, Exposure

Risk Metrics (Cols 15-22): Sharpe, Sortino, Max DD, RoR, R², MAR, CVaR, p-value

Color Coding

🟢 Green: Excellent performance

🟠 Orange: Acceptable performance

⚪ Gray: Neutral / Fair

🔴 Red: Poor performance

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ IMPLEMENTATION NOTES

Data Source: All metrics calculated from strategy.closedtrades , ensuring compatibility with any Pine Script strategy

Calculation Timing: All calculations occur on barstate.islastconfirmedhistory to optimize performance

Limitations: Requires at least 1 closed trade for basic metrics, 30+ trades for reliable statistical analysis

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK NOTES

➙ This library has been developed and refined over two years of real-world strategy testing. Every calculation has been validated against industry-standard quantitative finance references.

➙ The entire codebase is thoroughly documented inline. If you are curious about how a metric is calculated or want to understand the implementation details, dive into the source code -- it is written to be read and learned from.

➙ This description focuses on usage and concepts rather than exhaustively listing every exported type and function. The library source code is thoroughly documented inline -- explore it to understand implementation details and internal logic.

➙ All calculations execute on barstate.islastconfirmedhistory to minimize runtime overhead. The library is designed for efficiency without sacrificing accuracy.

➙ Beyond analysis, this library serves as a learning resource. Study the source code to understand quantitative finance concepts, Pine Script advanced techniques, and proper statistical methodology.

➙ Metrics are their own not binary good/bad indicators. A high Sharpe ratio with low sample size is misleading. A deep drawdown during a market crash may be acceptable. Study each function and metric individually -- evaluate your strategy contextually, not by threshold alone.

➙ All strategies face alpha decay over time. Instead of over-optimizing a single strategy on one timeframe and market, build a diversified portfolio across multiple markets and timeframes. Deeptest helps you validate each component so you can combine robust strategies into a trading portfolio.

➙ Screenshots shown in the documentation are solely for visual representation to demonstrate how the tables and metrics will be displayed. Please do not compare your strategy's performance with the metrics shown in these screenshots -- they are illustrative examples only, not performance targets or benchmarks.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ HOW-TO

Using Deeptest is intentionally straightforward. Just import the library and call DT.runDeeptest() at the end of your strategy code in main scope. .

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as DT

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

And yes... it's compatible with any TradingView Strategy! 🪄

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ CREDITS

Author: @Fractalyst

Font Library: by @fikira - @kaigouthro - @Duyck

Community: Inspired by the @PineCoders community initiative, encouraging developers to contribute open-source libraries and continuously enhance the Pine Script ecosystem for all traders.

if you find Deeptest valuable in your trading journey, feel free to use it in your strategies and give a shoutout to @Fractalyst -- Your recognition directly supports ongoing development and open-source contributions to Pine Script.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ DISCLAIMER

This library is provided for educational and research purposes. Past performance does not guarantee future results. Always test thoroughly and use proper risk management. The author is not responsible for any trading losses incurred through the use of this code.

SharelineCore_LibraryLibrary "SharelineCore_Library"

funding_premium(premiumSym, funding_period, plot_type, interest_rate, fundScale)

Parameters:

premiumSym (string)

funding_period (string)

plot_type (string)

interest_rate (float)

fundScale (float)

cvd_vwap_delta(spotSym, perpSym, normLen, resetCVD)

Parameters:

spotSym (string)

perpSym (string)

normLen (int)

resetCVD (bool)

cvd_trend_norm(spotSymbol, perpSymbol, normLen, resetOnSession)

Parameters:

spotSymbol (string)

perpSymbol (string)

normLen (int)

resetOnSession (bool)

trend_strength_engine(cvdSpot, cvdPerp)

Parameters:

cvdSpot (float)

cvdPerp (float)

bias_engine(plot_value, spotTrendVal, perpTrendVal, spotStrength, perpStrength)

Parameters:

plot_value (float)

spotTrendVal (float)

perpTrendVal (float)

spotStrength (float)

perpStrength (float)

smc_engine(h, l, c, v, ms_len, bos_len, vol_filter, scale_factor, smooth_len, signal_len)

Parameters:

h (float)

l (float)

c (float)

v (float)

ms_len (int)

bos_len (int)

vol_filter (bool)

scale_factor (float)

smooth_len (simple int)

signal_len (simple int)

momentum_engine(o, c, v, fast, slow, signal, rsiLen, normLen, smaShort, smaLong, wMacd, wRsi, wCvd, wVpi)

Parameters:

o (float)

c (float)

v (float)

fast (simple int)

slow (simple int)

signal (simple int)

rsiLen (simple int)

normLen (int)

smaShort (int)

smaLong (int)

wMacd (float)

wRsi (float)

wCvd (float)

wVpi (float)

oi_engine(quotecur, useBinance, useBinance2, useBinance3, useBitmex, useBitmex2, useKraken, d_mult, strength1_mult, strength2_mult)

Parameters:

quotecur (string)

useBinance (bool)

useBinance2 (bool)

useBinance3 (bool)

useBitmex (bool)

useBitmex2 (bool)

useKraken (bool)

d_mult (float)

strength1_mult (float)

strength2_mult (float)

LuxyEnergyIndexThe Luxy Energy Index (LEI) library provides functions to measure price movement exhaustion by analyzing three dimensions: Extension (distance from fair value), Velocity (speed of movement), and Volume (confirmation level).

LEI answers a different question than traditional momentum indicators: instead of "how far has price gone?" (like RSI), LEI asks "how tired is this move?"

This library allows Pine Script developers to integrate LEI calculations into their own indicators and strategies.

How to Import

//@version=6

indicator("My Indicator")

import OrenLuxy/LuxyEnergyIndex/1 as LEI

Main Functions

`lei(src)` → float

Returns the LEI value on a 0-100 scale.

src (optional): Price source, default is `close`

Returns : LEI value (0-100) or `na` if insufficient data (first 50 bars)

leiValue = LEI.lei()

leiValue = LEI.lei(hlc3) // custom source

`leiDetailed(src)` → tuple

Returns LEI with all component values for detailed analysis.

= LEI.leiDetailed()

Returns:

`lei` - Final LEI value (0-100)

`extension` - Distance from VWAP in ATR units

`velocity` - 5-bar price change in ATR units

`volumeZ` - Volume Z-Score

`volumeModifier` - Applied modifier (1.0 = neutral)

`vwap` - VWAP value used

Component Functions

| Function | Description | Returns |

|-----------------------------------|---------------------------------|---------------|

| `calcExtension(src, vwap)` | Distance from VWAP / ATR | float |

| `calcVelocity(src)` | 5-bar price change / ATR | float |

| `calcVolumeZ()` | Volume Z-Score | float |

| `calcVolumeModifier(volZ)` | Volume modifier | float (≥1.0) |

| `getVWAP()` | Auto-detects asset type | float |

Signal Functions

| Function | Description | Returns |

|---------------------------------------------|----------------------------------|-----------|

| `isExhausted(lei, threshold)` | LEI ≥ threshold (default 70) | bool |

| `isSafe(lei, threshold)` | LEI ≤ threshold (default 30) | bool |

| `crossedExhaustion(lei, threshold)` | Crossed into exhaustion | bool |

| `crossedSafe(lei, threshold)` | Crossed into safe zone | bool |

Utility Functions

| Function | Description | Returns |

|----------------------------|-------------------------|-----------|

| `getZone(lei)` | Zone name | string |

| `getColor(lei)` | Recommended color | color |

| `hasEnoughHistory()` | Data check | bool |

| `minBarsRequired()` | Required bars | int (50) |

| `version()` | Library version | string |

Interpretation Guide

| LEI Range | Zone | Meaning |

|-------------|--------------|--------------------------------------------------|

| 0-30 | Safe | Low exhaustion, move may continue |

| 30-50 | Caution | Moderate exhaustion |

| 50-70 | Warning | Elevated exhaustion |

| 70-100 | Exhaustion | High exhaustion, increased reversal risk |

Example: Basic Usage

//@version=6

indicator("LEI Example", overlay=false)

import OrenLuxy/LuxyEnergyIndex/1 as LEI

// Get LEI value

leiValue = LEI.lei()

// Plot with dynamic color

plot(leiValue, "LEI", LEI.getColor(leiValue), 2)

// Reference lines

hline(70, "High", color.red)

hline(30, "Low", color.green)

// Alert on exhaustion

if LEI.crossedExhaustion(leiValue) and barstate.isconfirmed

alert("LEI crossed into exhaustion zone")

Technical Details

Fixed Parameters (by design):

Velocity Period: 5 bars

Volume Period: 20 bars

Z-Score Period: 50 bars

ATR Period: 14

Extension/Velocity Weights: 50/50

Asset Support:

Stocks/Forex: Uses Session VWAP (daily reset)

Crypto: Uses Rolling VWAP (50-bar window) - auto-detected

Edge Cases:

Returns `na` until 50 bars of history

Zero volume: Volume modifier defaults to 1.0 (neutral)

Credits and Acknowledgments

This library builds upon established technical analysis concepts:

VWAP - Industry standard volume-weighted price measure

ATR by J. Welles Wilder Jr. (1978) - Volatility normalization

Z-Score - Statistical normalization method

Volume analysis principles from Volume Spread Analysis (VSA) methodology

Disclaimer

This library is provided for **educational and informational purposes only**. It does not constitute financial advice. Past performance does not guarantee future results. The exhaustion readings are probabilistic indicators, not guarantees of price reversal. Always conduct your own research and use proper risk management when trading.

CEDEARDataLibrary "CEDEARData"

getUnderlying(cedearTicker)

Parameters:

cedearTicker (simple string)

getRatio(cedearTicker)

Parameters:

cedearTicker (simple string)

getCurrency(cedearTicker)

Parameters:

cedearTicker (simple string)

isValidCedear(cedearTicker)

Parameters:

cedearTicker (simple string)

BybitMinOrderSizeBybit Order Quantity Compliance Library

This library provides all utility functions required for TradingView strategies

that execute orders on Bybit via webhooks.

Problem:

Bybit enforces two strict rules on every order submitted:

Minimum Order Size – each symbol has its own minimum quantity.

Quantity Precision – each symbol requires rounding to the correct number of decimals.

TradingView does not expose this metadata, so strategies can easily submit

quantities that Bybit rejects as invalid.

Solution (This Library):

This library embeds full Bybit contract metadata, including:

A complete mapping of Bybit symbols → minimum order size

A complete mapping of Bybit symbols → allowed precision (decimal places)

A helper to normalize tickers (removing `.P` suffix for Bybit perpetuals)

It also exposes utility functions to automatically make your quantities valid:

`normalizeTicker()` — removes `.P` for consistent lookup

`getMinOrderSize()` — returns the correct minimum order size

`getPrecisionForTicker()` — returns required quantity precision

`floorQty()` — floors quantities to valid minimum increments

`roundQty()` — rounds quantities to valid decimal precision

Use Cases:

Ensuring webhook strategies never send too-small orders

Rounding limit/market orders correctly before execution

Making Pine strategies execution-accurate for Bybit

Avoiding "order rejected: qty too small / invalid precision" errors

This library is recommended for:

Live trading via TradingView → Bybit webhooks

Backtesting strategies that simulate real Bybit constraints

Source: www.bybit.com

Updated: 2025-11-25 — Bybit contract metadata

normalizeTicker(symbol)

Normalizes Bybit perpetual tickers by removing the ".P" suffix.

precisionFromMinOrder(minOrder)

Derives precision (decimal places) from minimum order size.

getMinOrderSize(symbol)

Retrieves the minimum order size for the current or given symbol.

getPrecisionForTicker(symbol)

Retrieves the required quantity precision (decimal places) for a given Bybit symbol.

floorQty(qty, symbol)

Rounds a quantity down to the nearest valid minimum order size for a given symbol.

roundQty(qty, symbol)

Rounds a quantity to the valid precision for the specified symbol.

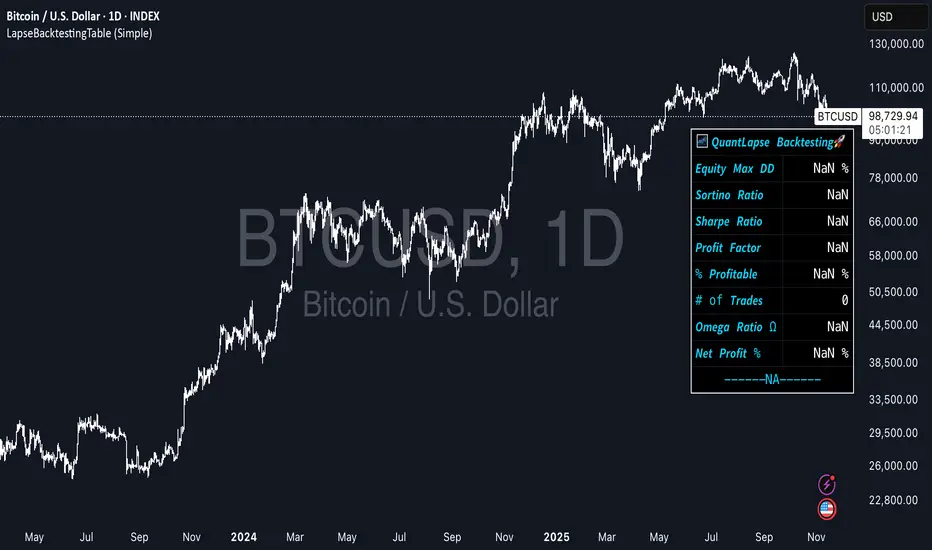

LapseBacktestingTableLibrary "LapseBacktestingMetrics"

This library provides a robust set of quantitative backtesting and performance evaluation functions for Pine Script strategies. It’s designed to help traders, quants, and developers assess risk, return, and robustness through detailed statistical metrics — including Sharpe, Sortino, Omega, drawdowns, and trade efficiency.

Built to enhance any trading strategy’s evaluation framework, this library allows you to visualize performance with the quantlapseTable() function, producing an interactive on-chart performance table.

Credit to EliCobra and BikeLife76 for original concept inspiration.

curve(disp_ind)

Retrieves a selected performance curve of your strategy.

Parameters:

disp_ind (simple string): Type of curve to plot. Options include "Equity", "Open Profit", "Net Profit", "Gross Profit".

Returns: (float) Corresponding performance curve value.

cleaner(disp_ind, plot)

Filters and displays selected strategy plots for clean visualization.

Parameters:

disp_ind (simple string): Type of display.

plot (simple float): Strategy plot variable.

Returns: (float) Filtered plot value.

maxEquityDrawDown()

Calculates the maximum equity drawdown during the strategy’s lifecycle.

Returns: (float) Maximum equity drawdown percentage.

maxTradeDrawDown()

Computes the worst intra-trade drawdown among all closed trades.

Returns: (float) Maximum intra-trade drawdown percentage.

consecutive_wins()

Finds the highest number of consecutive winning trades.

Returns: (int) Maximum consecutive wins.

consecutive_losses()

Finds the highest number of consecutive losing trades.

Returns: (int) Maximum consecutive losses.

no_position()

Counts the maximum consecutive bars where no position was held.

Returns: (int) Maximum flat days count.

long_profit()

Calculates total profit generated by long positions as a percentage of initial capital.

Returns: (float) Total long profit %.

short_profit()

Calculates total profit generated by short positions as a percentage of initial capital.

Returns: (float) Total short profit %.

prev_month()

Measures the previous month’s profit or loss based on equity change.

Returns: (float) Monthly equity delta.

w_months()

Counts the number of profitable months in the backtest.

Returns: (int) Total winning months.

l_months()

Counts the number of losing months in the backtest.

Returns: (int) Total losing months.

checktf()

Returns the time-adjusted scaling factor used in Sharpe and Sortino ratio calculations based on chart timeframe.

Returns: (float) Annualization multiplier.

stat_calc()

Performs complete statistical computation including drawdowns, Sharpe, Sortino, Omega, trade stats, and profit ratios.

Returns: (array)

.

f_colors(x, nv)

Generates a color gradient for performance values, supporting dynamic table visualization.

Parameters:

x (simple string): Metric label name.

nv (simple float): Metric numerical value.

Returns: (color) Gradient color value for table background.

quantlapseTable(option, position)

Displays an interactive Performance Table summarizing all major backtesting metrics.

Includes Sharpe, Sortino, Omega, Profit Factor, drawdowns, profitability %, and trade statistics.

Parameters:

option (simple string): Table type — "Full", "Simple", or "None".

position (simple string): Table position — "Top Left", "Middle Right", "Bottom Left", etc.

Returns: (table) On-chart performance visualization table.

This library empowers advanced quantitative evaluation directly within Pine Script®, ideal for strategy developers seeking deeper performance diagnostics and intuitive on-chart metrics.

UTBotLibrary "UTBot"

is a powerful and flexible trading toolkit implemented in Pine Script. Based on the widely recognized UT Bot strategy originally developed by Yo_adriiiiaan with important enhancements by HPotter, this library provides users with customizable functions for dynamic trailing stop calculations using ATR (Average True Range), trend detection, and signal generation. It enables developers and traders to seamlessly integrate UT Bot logic into their own indicators and strategies without duplicating code.

Key features include:

Accurate ATR-based trailing stop and reversal detection

Multi-timeframe support for enhanced signal reliability

Clean and efficient API for easy integration and customization

Detailed documentation and examples for quick adoption

Open-source and community-friendly, encouraging collaboration and improvements

We sincerely thank Yo_adriiiiaan for the original UT Bot concept and HPotter for valuable improvements that have made this strategy even more robust. This library aims to honor their work by making the UT Bot methodology accessible to Pine Script developers worldwide.

This library is designed for Pine Script programmers looking to leverage the proven UT Bot methodology to build robust trading systems with minimal effort and maximum maintainability.

UTBot(h, l, c, multi, leng)

Parameters:

h (float) - high

l (float) - low

c (float)-close

multi (float)- multi for ATR

leng (int)-length for ATR

Returns:

xATRTS - ATR Based TrailingStop Value

pos - pos==1, long position, pos==-1, shot position

signal - 0 no signal, 1 buy, -1 sell

AlertSenderLibrary_TradingFinderLibrary "AlertSenderLibrary_TradingFinder"

TODO: add library description here

AlertSender(Condition, Alert, AlertName, AlertType, DetectionType, SetupData, Frequncy, UTC, MoreInfo, Message, o, h, l, c, Entry, TP, SL, Distal, Proximal)

Parameters:

Condition (bool)

Alert (string)

AlertName (string)

AlertType (string)

DetectionType (string)

SetupData (string)

Frequncy (string)

UTC (string)

MoreInfo (string)

Message (string)

o (float)

h (float)

l (float)

c (float)

Entry (float)

TP (float)

SL (float)

Distal (float)

Proximal (float)

WCWebLibLibrary "WCWebLib"

method buildWebhookJson(msg, constants)

Builds the final JSON payload from a webhookMessage type.

Namespace types: webhookMessage

Parameters:

msg (webhookMessage) : (webhookMessage) A prepared webhookMessage.

constants (CONSTANTS)

Returns: A JSON Payload.

method buildTakeProfitJson(msg)

Builds the takeProfit JSON message to be used in a webhook message.

Namespace types: takeProfitMessage

Parameters:

msg (takeProfitMessage)

method buildStopLossJson(msg, constants)

Builds the stopLoss JSON message to be used in a webhook message.

Namespace types: stopLossMessage

Parameters:

msg (stopLossMessage)

constants (CONSTANTS)

CONSTANTS

Constants for payload values.

Fields:

ACTION_BUY (series string)

ACTION_SELL (series string)

ACTION_EXIT (series string)

ACTION_CANCEL (series string)

ACTION_ADD (series string)

SENTIMENT_BULLISH (series string)

SENTIMENT_BEARISH (series string)

SENTIMENT_LONG (series string)

SENTIMENT_SHORT (series string)

SENTIMENT_FLAT (series string)

STOP_LOSS_TYPE_STOP (series string)

STOP_LOSS_TYPE_STOP_LIMIT (series string)

STOP_LOSS_TYPE_TRAILING_STOP (series string)

EXTENDEDHOURS (series bool)

ORDER_TYPE_LIMIT (series string)

ORDER_TYPE_MARKET (series string)

TIF_DAY (series string)

webhookMessage

Final webhook message.

Fields:

ticker (series string)

action (series string)

sentiment (series string)

price (series float)

quantity (series int)

takeProfit (series string)

stopLoss (series string)

extendedHours (series bool)

type (series string)

timeInForce (series string)

takeProfitMessage

Take profit message.

Fields:

limitPrice (series float)

percent (series float)

amount (series float)

stopLossMessage

Stop loss message.

Fields:

type (series string)

percent (series float)

amount (series float)

stopPrice (series float)

limitPrice (series float)

trailPrice (series float)

trailPercent (series float)

RifleShooterLibLibrary "RifleShooterLib"

Provides a collection of helper functions in support of the Rifle Shooter Indicators.

Functions support the key components of the Rifle Trade algorithm including

* measuring momentum

* identifying paraboloic price action (to disable the algorthim during such time)

* determine the lookback criteria of X point movement in last N minutes

* processing and navigating between the 23/43/73 levels

* maintaining a status table of algorithm progress

toStrRnd(val, digits)

Parameters:

val (float)

digits (int)

_isValidTimeRange(startTimeInput, endTimeInput)

Parameters:

startTimeInput (string)

endTimeInput (string)

_normalize(_src, _min, _max)

_normalize Normalizes series with unknown min/max using historical min/max.

Parameters:

_src (float) : Source series to normalize

_min (float) : minimum value of the rescaled series

_max (float) : maximum value of the rescaled series

Returns: The series scaled with values between min and max

arrayToSeries(arrayInput)

arrayToSeries Return an array from the provided series.

Parameters:

arrayInput (array) : Source array to convert to a series

Returns: The array as a series datatype

f_parabolicFiltering(_activeCount, long, shooterRsi, shooterRsiLongThreshold, shooterRsiShortThreshold, fiveMinuteRsi, fiveMinRsiLongThreshold, fiveMinRsiShortThreshold, shooterRsiRoc, shooterRsiRocLongThreshold, shooterRsiRocShortThreshold, quickChangeLookbackBars, quckChangeThreshold, curBarChangeThreshold, changeFromPrevBarThreshold, maxBarsToholdParabolicMoveActive, generateLabels)

f_parabolicFiltering Return true when price action indicates a parabolic active movement based on the provided inputs and thresholds.

Parameters:

_activeCount (int)

long (bool)

shooterRsi (float)

shooterRsiLongThreshold (float)

shooterRsiShortThreshold (float)

fiveMinuteRsi (float)

fiveMinRsiLongThreshold (float)

fiveMinRsiShortThreshold (float)

shooterRsiRoc (float)

shooterRsiRocLongThreshold (float)

shooterRsiRocShortThreshold (float)

quickChangeLookbackBars (int)

quckChangeThreshold (int)

curBarChangeThreshold (int)

changeFromPrevBarThreshold (int)

maxBarsToholdParabolicMoveActive (int)

generateLabels (bool)

rsiValid(rsi, buyThreshold, sellThreshold)

rsiValid Returns true if the provided RSI value is withing the associated threshold. For the unused threshold set it to na

Parameters:

rsi (float)

buyThreshold (float)

sellThreshold (float)

squezeBands(source, length)

squezeBands Returns the squeeze bands momentum color of current source series input

Parameters:

source (float)

length (int)

f_momentumOscilator(source, length, transperency)

f_momentumOscilator Returns the squeeze pro momentum value and bar color states of the series input

Parameters:

source (float)

length (int)

transperency (int)

f_getLookbackExtreme(lowSeries, highSeries, lbBars, long)

f_getLookbackExtreme Return the highest high or lowest low over the look back window

Parameters:

lowSeries (float)

highSeries (float)

lbBars (int)

long (bool)

f_getInitialMoveTarget(lbExtreme, priveMoveOffset, long)

f_getInitialMoveTarget Return the point delta required to achieve an initial rifle move (X points over Y lookback)

Parameters:

lbExtreme (float)

priveMoveOffset (int)

long (bool)

isSymbolSupported(sym)

isSymbolSupported Return true if provided symbol is one of the supported DOW Rifle Indicator symbols

Parameters:

sym (string)

getBasePrice(price)

getBasePrice Returns integer portion of provided float

Parameters:

price (float)

getLastTwoDigitsOfPrice(price)

getBasePrice Returns last two integer numerals of provided float value

Parameters:

price (float)

getNextLevelDown(price, lowestLevel, middleLevel, highestLevel)

getNextLevelDown Returns the next level above the provided price value

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

getNextLevelUp(price, lowestLevel, middleLevel, highestLevel)

getNextLevelUp Returns the next level below the provided price value

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

isALevel(price, lowestLevel, middleLevel, highestLevel)

isALevel Returns true if the provided price is onve of the specified levels

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

getClosestLevel(price, lowestLevel, middleLevel, highestLevel)

getClosestLevel Returns the level closest to the price value provided

Parameters:

price (float)

lowestLevel (float)

middleLevel (float)

highestLevel (float)

f_fillSetupTableCell(_table, _col, _row, _text, _bgcolor, _txtcolor, _text_size)

f_fillSetupTableCell Helper function to fill a setup table celll

Parameters:

_table (table)

_col (int)

_row (int)

_text (string)

_bgcolor (color)

_txtcolor (color)

_text_size (string)

f_fillSetupTableRow(_table, _row, _col0Str, _col1Str, _col2Str, _bgcolor, _textColor, _textSize)

f_fillSetupTableRow Helper function to fill a setup table row

Parameters:

_table (table)

_row (int)

_col0Str (string)

_col1Str (string)

_col2Str (string)

_bgcolor (color)

_textColor (color)

_textSize (string)

f_addBlankRow(_table, _row)

f_addBlankRow Helper function to fill a setup table row with empty values

Parameters:

_table (table)

_row (int)

f_updateVersionTable(versionTable, versionStr, versionDateStr)

f_updateVersionTable Helper function to fill the version table with provided values

Parameters:

versionTable (table)

versionStr (string)

versionDateStr (string)

f_updateSetupTable(_table, parabolicMoveActive, initialMoveTargetOffset, initialMoveAchieved, shooterRsi, shooterRsiValid, rsiRocEnterThreshold, shooterRsiRoc, fiveMinuteRsi, fiveMinuteRsiValid, requireValid5MinuteRsiForEntry, stallLevelOffset, stallLevelExceeded, stallTargetOffset, recoverStallLevelValid, curBarChangeValid, volumeRoc, volumeRocThreshold, enableVolumeRocForTrigger, tradeActive, entryPrice, curCloseOffset, curSymCashDelta, djiCashDelta, showDjiDelta, longIndicator, fontSize)

f_updateSetupTable Manages writing current data to the setup table