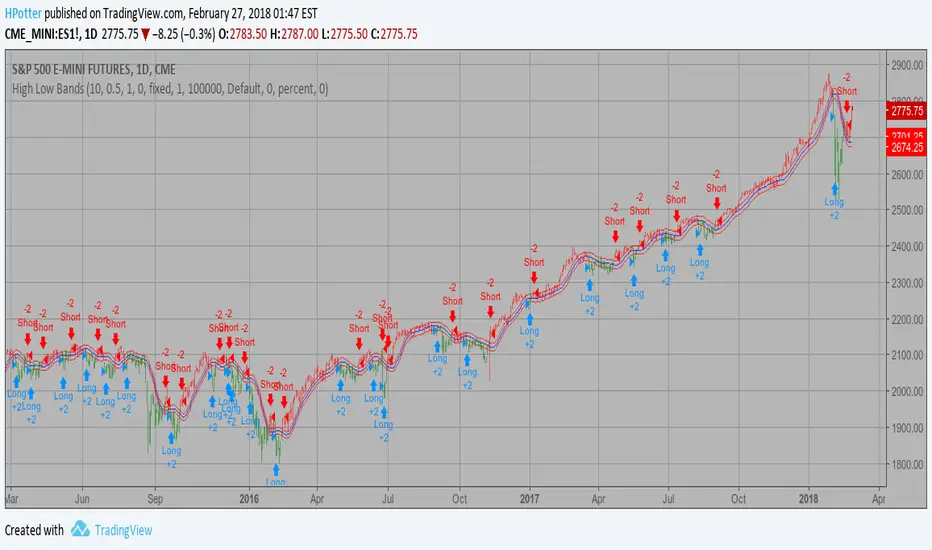

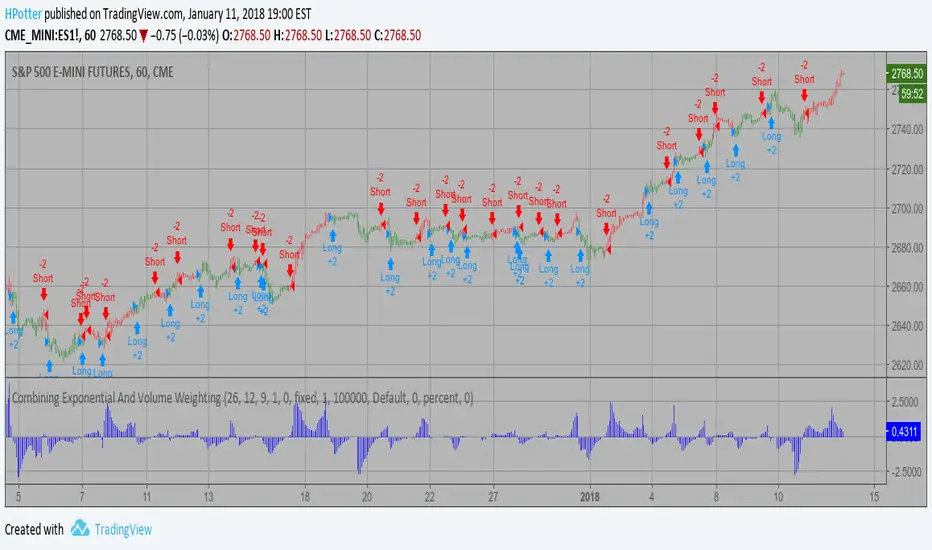

High Low Bands Backtest As the name suggests, High low bands are two bands surrounding the underlying’s

price. These bands are generated from the triangular moving averages calculated

from the underlying’s price. The triangular moving average is, in turn, shifted

up and down by a fixed percentage. The bands, thus formed, are termed as High

low bands. The main theme and concept of High low bands is based upon the triangular

moving average.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Strategi Pine Script®