Universal Breakout Strategy [KedArc Quant]Description:

A flexible breakout framework where you can test different logics (Prev Day, Bollinger, Volume, ATR, EMA Trend, RSI Confirm, Candle Confirm, Time Filter) under one system.

Choose your breakout mode, and the strategy will handle entries, exits, and optional risk management (ATR stops, take-profits, daily loss guard, cooldowns).

An on-chart info table shows live mode values (like Prev High/Low, Bollinger levels, RSI, etc.) plus P&L stats for quick analysis.

Use it to compare which breakout style works best on your instrument and timeframe, whether intraday, swing, or positional trading

🔑 Why it’s useful

* Flexibility: Switch between breakout strategies without loading different indicators.

* Clarity: On-chart info table displays current mode, relevant indicator levels, and live strategy P&L stats.

* Testing efficiency: Quickly A/B test different breakout styles under the same backtest environment.

* Transparency: Every trade is rule-based and displayed with entry/exit markers.

🚀 How it helps traders

* Lets you experiment with breakout strategies quickly without loading multiple scripts.

* Helps identify which breakout method fits your instrument & timeframe.

* Gives clear on-chart visual + statistical feedback for confident decision-making.

⚙️ Input Configuration

* Breakout Mode → choose which strategy to test:

* *Prev Day* → breakouts of yesterday’s High/Low.

* *Bollinger* → Upper/Lower BB pierce.

* *Volume* → Breakout confirmed with volume above average.

* *ATR Stop* → Wide range breakout using ATR filter.

* *Time Filter* → Breakouts inside defined session hours.

* *EMA Trend* → Breakouts only in EMA fast > slow alignment.

* *RSI Confirm* → Breakouts with RSI confirmation (e.g. >55 for longs).

* *Candle Confirm* → Breakouts validated by bullish/bearish candle.

* Lookback / ATR / Bollinger inputs → adjust sensitivity.

* Intrabar mode → option to evaluate breakouts using bar highs/lows instead of closes.

* Table options → show/hide info table, show/hide P&L stats, choose corner placement.

📈 Entry & Exit Logic

* Entry → occurs when breakout condition of chosen mode is met.

* Exit → default exits via opposite signals or optional stop/target if enabled.

* Session filter → optional auto-flat at session end.

* P&L management → optional daily loss guard, cooldown between trades, and ATR-based stop/take profit.

❓ FAQ — Choosing the best setup

Q: Which strategy should I use for which chart?

* *Prev Day Breakouts*: Best on indices, FX, and liquid futures with strong daily levels.

* *Bollinger*: Works well in range-bound environments, or crypto pairs with volatility compression.

* *Volume*: Good on equities where breakout strength is tied to volume spikes.

* *ATR Stop*: Suits volatile instruments (commodities, crypto).

* *EMA Trend*: Useful in trending markets (stocks, indices).

* *RSI Confirm*: Adds momentum filter, better for swing trades.

* *Candle Confirm*: Ideal for scalpers needing visual confirmation.

* *Time Filter*: For intraday traders who want signals only in high-liquidity sessions.

Q: What timeframe should I use?

* Intraday traders → 5m to 15m (Time Filter, Candle Confirm).

* Swing traders → 1H to 4H (EMA Trend, RSI Confirm, ATR Stop).

* Position traders → Daily (Prev Day, Bollinger).

* Breakout

A trade entry condition triggered when price crosses above a resistance level (for longs) or below a support level (for shorts).

* Prev Day High/Low

Formula:

Prev High = High of (Day )

Prev Low = Low of (Day )

* Bollinger Bands

Formula:

Basis = SMA(Close, Length)

Upper Band = Basis + (Multiplier × StdDev(Close, Length))

Lower Band = Basis – (Multiplier × StdDev(Close, Length))

* Volume Confirmation

A breakout is only valid if:

Volume > SMA(Volume, Length)

* ATR (Average True Range)

Measures volatility.

Formula:

ATR = SMA(True Range, Length)

where True Range = max(High–Low, |High–Close |, |Low–Close |)

* EMA (Exponential Moving Average)

Weighted moving average giving more weight to recent prices.

Formula:

EMA = (Price × α) + (EMA × (1–α))

with α = 2 / (Length + 1)

* RSI (Relative Strength Index)

Momentum oscillator scaled 0–100.

Formula:

RSI = 100 – (100 / (1 + RS))

where RS = Avg(Gain, Length) ÷ Avg(Loss, Length)

* Candle Confirmation

Bullish candle: Close > Open AND Close > Close

Bearish candle: Close < Open AND Close < Close

Win Rate (%)

Formula:

Win Rate = (Winning Trades ÷ Total Trades) × 100

* Average Trade P&L

Formula:

Avg Trade = Net Profit ÷ Total Trades

📊 Performance Notes

The Universal Breakout Strategy is designed as a framework rather than a single-asset optimized system. Results will vary depending on the chart, timeframe, and asset chosen.

On the current defaults (15-minute, INR-denominated example), the backtest produced 132 trades over the selected period. This provides a statistically sufficient sample size.

Win rate (~35%) is relatively low, but this is balanced by a positive reward-to-risk ratio (~1.8). In practice, a lower win rate with larger wins versus smaller losses is sustainable.

The average P&L per trade is close to breakeven under default settings. This is expected, as the strategy is not tuned for a single symbol but offered as a universal breakout framework.

Commissions (0.1%) and slippage (1 tick) are included in the simulation, ensuring realistic conditions.

Risk management is conservative, with order sizing set at 1 unit per trade. This avoids over-leveraging and keeps exposure well under the 5-10% equity risk guideline.

👉 Traders are encouraged to:

Experiment with inputs such as ATR period, breakout length, or Bollinger parameters.

Test across different timeframes and instruments (equities, futures, forex, crypto) to find optimal setups.

Combine with filters (trend direction, volatility regimes, or volume conditions) for further refinement.

⚠️ Disclaimer This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

MASA

Trading Day and Time SessionThis script provides options for the user to choose:

- Start date and End date

- Trade time during a day (With UTC offset)

- Which days of the week to trade

It return a condition if all the date and time conditions are true. It's very easy to integrate with any script.

Simple_PyramidingA simple Pyramiding / DCA Strategy. Everyday at a specified time a position is opened. The individual position is closed when a take profit is triggered. Optionally a stop loss can be activated, or the option to close the position at the and of the time frame. You can specify the max amount of open positions. The equity will be divided through the max amount of open positions.

This strategy is a result of an exploration into working with time sessions, pyramiding, for loops and possibilities to trigger individual take profits (profit) and stop loss levels (stop). This strategy is by no means a worked out and reliable strategy. Please feel free to experiment with the code in your indicators and strategies.

Time of Day and Day of Week Buying and Selling StrategyThis strategy allows you to back test longing or shorting or do nothing during time increments of 30 minutes for various days of the week. For example if you want to see if every Saturday if Bitcoin dropped in value from 1600-7000 UTC, this script will allow you to test that.

Make sure you are in the 30 minute time frame while viewing the performance and trade history.

Timeframe Time of Day Buying and Selling StrategyThis strategy allows you to back test longing or shorting or do nothing during time increments of 30 minutes. The price trends in one direction every 30 minutes and this strategy allows you to test various 30 minute time frames across a range of dates to capitalize on this.

Make sure you are in the 30 minute time frame while viewing the performance and trade history.

Combination Parabolic MA/IIR/ALMA Strategy, and other goodies Okay, so this is a lot. It started mostly with me combining indicators and looking for ideal entry criteria.

It is also a collection of conditions, whether used or unused, for my current chosen "best" strategy. It is currently set how I like it, but it has changed with time, and will continue to do so. Within, there are variables that are unused, but offer some insight into the overall odds of a trade. They were, in fact, once used but fell out of favor. And all details for this strategy are within the comment header of the script.

As this evolves, I most certainly wont keep any future findings and hope for profit from my peers (yinz). Also, I'd like to give a sincere thanks to the people of TV for what I learned in a few month's time and their flexible membership plans. Basically, I'm just a mad scientist, but this monster's a masterpiece and folks here before me made many indirect contributions to it.

--------------------------

Okay guys, lastly and most importantly,

Each smack of the like button is a vote of your confidence in me, to my beautiful landladies, Celeste and Adele, that my rent will be caught up and that it won't always be a problem. Which, in my mind, makes me a graph. And they've got strong hands and don't sell the low. I more than respect that. Seriously. And I'm very grateful for their willingness to work with me, but the thing is that I didn't ask first; life just happens. But few are tolerant of others. And quite importantly, I truly believe that I will be successful one day, and that "thumbs-up" button is your vote of confidence. If you're not sure, then don't hit it yet. Maybe my scripts will boost your confidence in me :)

-------------------------

PS: And you know what? I'ma give a shout-out to Philakone for teaching me everything that I know about Elliot Wave . Absolutely. Two years ago, I would keep telling myself that one day I will put something in his gratuity wallet or pursue the paid courses. And, I still plan on it, because I'm grateful. And so also, to everybody else, I'm recommending him to learn from. because as a trader who might not know everything for free, you can certainly fill in the gaps with his altruistic offerings. And I'm betting that you will then feel more than inclined to buy the Udemy course.

"If wave 2 retraces a lot; number 4 will not". Repetition. Philakone didn't fix my memory but he sure did find a workaround, haha

Okay, everyone, Thanks!

How To Set Backtest Time Ranges

Example how to set the time range window to be backtested for both entries and exits. Additional examples are also included showing how to set the date range and toggle plot visibility.

By incorporating this code with your own strategy's logic, it will allow you to backtest various time windows.

Much gratitude to @LucF and @a.tesla2018 for help with including ':1234567' for time ranges on weekends. Thank you both!

NOTICE: This is an example script and not meant to be used as an actual strategy. By using this script or any portion thereof, you acknowledge that you have read and understood that this is for research purposes only and I am not responsible for any financial losses you may incur by using this script!

C320up Strategy Tester Start TimeC320up Strategy Tester Start Time

This is a little snippet you can paste into your Strategy to set the testing start date and time.

It is not a Strategy per se, though is an example with the timestamp script included.

Instructions are fairly straight forward, and are listed in the script.

If for some reason you also wanted an end date, that too is possible. Just leave a note in the comments.

Disclaimer: We searched for a similar script on TV, and could not find anything at this point in time.

You can set your preferred date and time in the input section of the settings.

Enjoy!

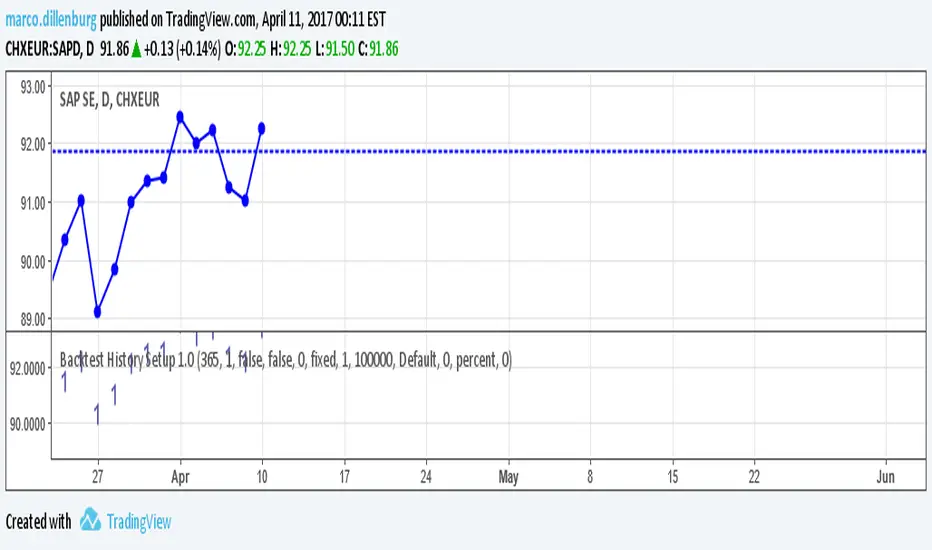

Backtest History Setup 1.0Script of strategy component to setup the backtext lookback. You setup the maximum days back in the history, which will be used for backtest.

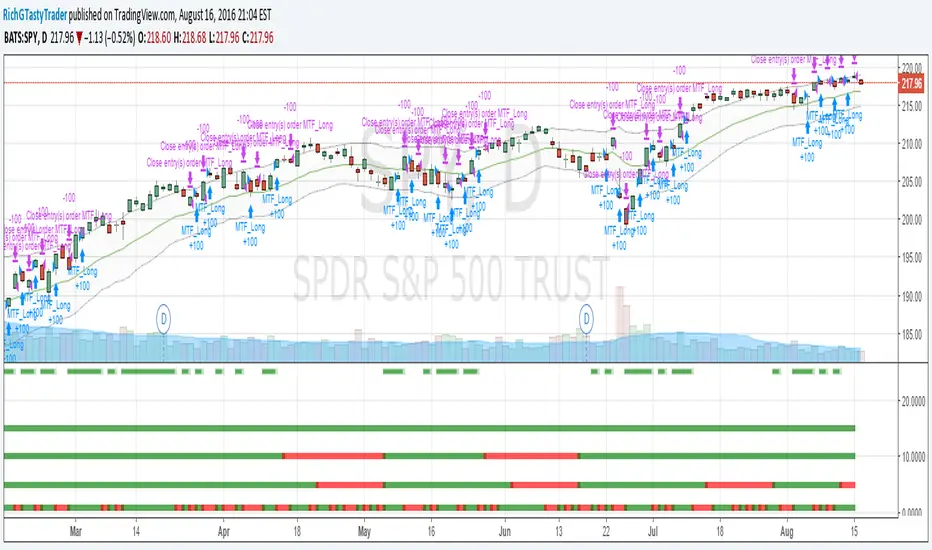

[RichG] Easy MTF Strategy v1.1This is a second attempt at an easy to understand multiple time frame strategy. This one uses ATR for exits. If the position is long, and the price closes below the ATR multiplier, it triggers a close. If the position is short, and the price closes above the ATR/multiplier, it triggers a close. This generates a lot of little trades but is useful because it uses multiple time frames along with cutting losses when the ATR disagrees.

Strategy Code Example 2 - Time Limiting*** THIS IS JUST AN EXAMPLE OF STRATEGY TIME LIMITING CODE IMPLEMENTATION ***

This is a follow up to my example for risk management implementation here:

Code remains mostly unchanged, but now includes a time limiting implementation.

Relevant code blocks for the time factor are preceded with a comment stating:

*** FOCUS OF EXAMPLE ***

Cheers!

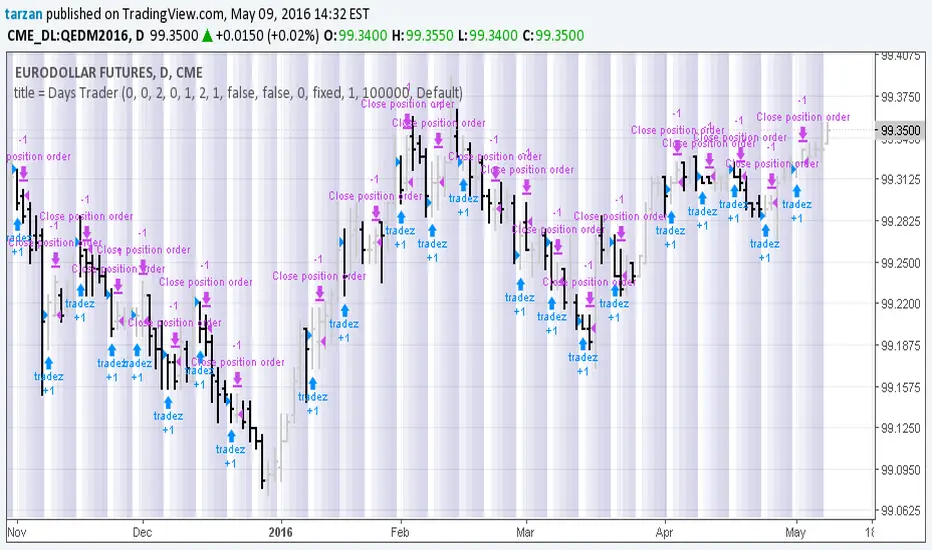

Days Trader 1.0Simple program to look for day of week or day of month patterns in chart data.

All original work by Boffin Hollow Lab

Author: Tarzan