Robrechtian Long-Medium Breakout Trend SystemRobrechtian Long–Medium-Term Breakout Trend System

A professional, rule-based trend-following strategy designed to capture large, sustained price movements using pure price action and breakouts.

This system follows long-established trend-following philosophy: no prediction, no volatility targeting, and no profit targets. Only disciplined entries, position additions, and exits driven entirely by trend structure.

Core Principles

Breakout-driven entries: Initial positions are taken only when price breaks above/below the 80-day Donchian channel, confirming a long–medium-term trend shift.

Short-term confirmation: Breakouts must also exceed the 20-day channel, reducing false positives.

Trend-direction filter: A 50-day moving average slope filter ensures alignment with the broader trend.

Explosive bar filter: Entries avoid excessively large, single-candle expansions (>2.5× ATR(20)) to prevent chasing exhaustion spikes.

Pyramiding into strength: Additional units are added only when price makes fresh 20-day breakouts in the direction of the trend. No scaling out. No adding on dips.

Exit only on trend violation: Positions are closed exclusively when price breaks the opposite 80-day channel. This preserves unlimited upside while enforcing disciplined exits.

Pure trend philosophy: No volatility targeting, no smoothing, no discretionary overrides, no optimization for short-term performance.

Intended Use

This system is designed primarily for diversified futures portfolios, where diversification across dozens of globally liquid markets creates robustness and stability. However, it may also be used on individual assets for educational and analytical purposes.

The system embraces the core trend-following logic:

Small losses, big winners, and unlimited upside when trends persist.

⚠️ WARNINGS / DISCLAIMERS

⚠️ Warning 1 — This strategy is not optimized for single stocks

The Robrechtian Trend System is designed for multi-asset futures portfolios, not single equities.

Performance on individual tickers may vary greatly due to lack of diversification.

⚠️ Warning 2 — Trend following includes substantial drawdowns

Deep drawdowns are a normal and expected feature of all long-term trend-following systems.

The strategy does not attempt to smooth returns or manage volatility.

If you seek steady, low-volatility equity curves, this system is not suitable.

⚠️ Warning 3 — No volatility targeting or risk smoothing

This system intentionally avoids volatility-based position sizing.

Trades may experience larger fluctuations than systems using risk parity or vol targeting.

⚠️ Warning 4 — Not financial advice

This script is for educational and research purposes only.

Past performance does not guarantee future results.

Use at your own risk.

⚠️ Warning 5 — TradingView backtests have known limitations

TradingView does not simulate:

futures contract roll logic

slippage

real bid/ask spreads

liquidity conditions

limit-up/limit-down behavior

Results may vary from live market execution.

Trendfollowing

BTC Trend-Following Strategy (Limited Version)This is a trend-following strategy designed specifically for Bitcoin (BTC).

It has demonstrated consistent performance and profitable opportunities over multiple years of historical data.

The strategy aims to capture major trends while managing risk effectively, making it suitable for traders looking for a systematic BTC trading approach.

QQQ TimingThis is a trend-following position trading strategy designed for the QQQ and the leveraged ETF QLD (ProShares Ultra QQQ). The primary goal is to capture multi-month holds for maximal profit.

Key Instruments & Performance

The strategy performs best with QLD, which yields far superior results compared to QQQ.

TQQQ (triple-leveraged) results in higher drawdowns and is not the optimal choice.

Important: The system is not intended for use with other indexes, individual stocks, or investments (like crypto or gold), as performance can vary widely.

Buy Signals

The strategy's signals are rooted in the S&P 500 Index (SPX), as testing showed it provides more reliable triggers than using QQQ itself.

Primary Buy Signal (Credit to IBD/Mike Webster): The SPX triggers a buy when its low closes above the 21-day Exponential Moving Average (EMA) for three consecutive days.

Refinement with Downtrend Lines: During corrective or bear periods, results and drawdowns can be significantly improved by incorporating downtrend lines. These lines connect lower highs. The strategy waits for the price to close above a drawn downtrend line before executing a buy. This refinement can modify the primary signal, either by allowing for an earlier entry or, in some cases, completely nullifying a false signal until the trend change proves itself.

Risk Management & Exit Strategy

Initial Buy Risk: A 3.7% stop loss is applied immediately upon the initial entry.

Initial Exit Rule: An exit is required if the QQQ's low drops below the 50-day Simple Moving Average (SMA).

Note: The 3.7% stop often provides protection when the initial buy occurs below the 50-day SMA. However, if QQQ is already trading above its 50-day SMA at the time of the SPX signal (indicating relative strength), historically, it has been better to use the 50-day SMA rule to give the position more room to run.

Trend Exit (Profit-Taking): To stay in a strong trend for the optimal amount of time, the long position is exited when a moving average crossover to the downside is triggered, based around the 107-day Simple Moving Average (SMA).

Turtles StrategyBorn from the 1980s "Turtle" experiment, this method of trading captures breakouts and places or closes trades with intrabar entries or exits and realized-equity risk controls.

How It Works

The strategy buys/sells on breakouts from recent highs/lows, using ATR for volatility-adjusted stops and sizing. It risks a fixed % (default 1%) of realized equity per trade—initial capital plus closed P&L, ignoring open positions for conservatism. Drawdown protection auto-reduces risk by 20% at 10% drops (up to three times), resetting only on full peak recovery. Single positions only, with 1-tick slippage simulated for realistic fills. Best for trending assets like forex,commodities, crypto, stocks. Backtest for optimal parameters.

Main Operations

The strategy works on any timeframe but it's meant to be used on daily charts.

Entry Signals:

Long: Buy-stop 1 tick above 20-bar high (default "Entry Period") when no position—enters intrabar on breakout.

Short: Sell-stop 1 tick below 20-bar low. OCA cancels opposites.

Size: (Realized equity × adjusted risk %) ÷ (2× ATR stop distance), scaled by point value.

Exit Signals:

Longs: Stop at tighter of (entry - 2× ATR) or (10-bar low - 1 tick trailing, default "Exit Period").

Shorts: Stop at tighter of (entry + 2× ATR) or (10-bar high + 1 tick trailing).

Locks profits in trends, exits fast on fades.

Risk Controls:

Tracks realized equity peak.

10% drawdown: Risk ×0.8; 20%/30%: Further ×0.8 (max 3x).

Full reset above peak—preserves capital in slumps.

Futures Fighter MO: Multi-Confluence Day Trading System ADX/SMI👋 Strategy Overview: The Multi-Confluence Mashup

The Futures Fighter MO is a comprehensive, multi-layered day trading strategy designed for experienced traders focusing on high-liquidity futures contracts (e.g., NQ, ES, R2K).

This strategy is a sophisticated mashup that uses the 1-minute chart for surgical entries while enforcing strict environmental filtering through higher-timeframe data. We aim to capture high-conviction moves only when multiple, uncorrelated signals align.

🧠 How the Logic Works (Concepts & Confluence)

Our logic is built on four pillars, which must align for a trade to be executed:

Primary Trend Filter

Indicators :

ADX/DMI (15-Minute Lookback)

Role :

Price action is filtered to ensure the ADX (17/14) is above 25, confirming a strong, prevailing market trend (Bullish or Bearish). Trades are strictly rejected during "Flat" (sideways) market regimes.

Entry Signal Types

The system uses multiple entry types:

- 🟢 Trend Long/Short: A breakout/rejection near the 200-Period EMA is confirmed by the primary ADX trend.

- 🔴 Engulfing Rejection: A strong signal when a Bullish/Bearish Engulfing or Doji prints near the long-term 500-Period EMA (emaGOD) while the Stochastic Momentum Index (SMI on 30M) is in an extreme overbought/oversold state (below $-40$ or above $40$).

Volatility & Volume Confirmation

Indicators: Average True Range (ATR) and 20-Period SMA of Volume

Role: Every entry requires a volume spike (Current Volume $> 1.5 \times$ SMA Volume) to confirm that the move is supported by significant liquidity. Volatility is tracked via ATR to define bar range and stop boundaries.

Structural Guardrails

Indicators: Daily Pivot Points (PP, S1-S3, R1-R3)

Role: Trades are disabled if the current bar's price range intersects with a Daily Pivot Point. This is a critical filter to avoid high-chop consolidation zones near key structural levels.

📊 Strategy Results & Required Disclosures

I strive to publish backtesting results that are transparent and realistic for the retail futures trader.

- Initial Capital: $50,000 - A realistic base for Mini/Micro futures contracts.

- Order Size: 1 Contract (Pyramiding up to 3) - Conservative risk relative to the account size.

- Commission: $0.11 USD per order - Represents realistic costs for low-cost brokers.

- Slippage: 2 Ticks - Accounts for expected market friction.

⚠️ Risk Management & Deviations

Stop-Loss: The strategy uses a dynamic stop-loss system where positions are closed upon a reversal (e.g., breaking the 50-Period EMA or failure to hold a Pivot Point), rather than a fixed tick-based stop. This is suited for experienced traders using a low relative risk (single Micro-contract entry) on a larger account. Users must confirm that the first entry's maximum potential loss remains below $10\%$ of their capital for compliance.

Trade Sample Size: Due to data limitations of the TradingView Essential plan (showing $\approx 50$ trades over 2 weeks), the sample size is under the ideal $100+$ target. Justification: This system is designed to generate signals across a portfolio of correlated futures markets (NQ, ES, R2K, Gold, Crude), meaning the real sample size for a user tracking the portfolio is significantly higher.

Drawdown Control: This strategy is designed for manual management. It requires the user to turn the script/alerts OFF after a significant drawdown and only reactivate it once a recovery trend is established externally.

The strategy uses a combination of dynamic trailing stops, structural support/resistance zones, and a fixed profit target to manage open positions.

🛑 Strategy Exit Logic

1. General Stop-Loss (Dynamic Trailing Stop)

These conditions act as the primary dynamic stop, closing the position if the market reverses past a key Moving Average (MA):

- Long Positions Closed When: The current bar's close crosses under the 50-Period EMA (emaLong).

- Short Positions Closed When: The current bar's close crosses above the 50-Period EMA (emaLong).

2. Profit Target (Fixed Percentage)

The script includes a general exit based on a user-defined profit percentage:

Take Profit Trigger: The position is closed when the currentProfitPercent meets or exceeds the input Profit Target (%) (default is 1.0% of the entry price).

3. Structural Exits (Daily Pivot Points)

These exits are high-priority, "close all" orders that trigger when the price fails to hold or reclaims a recent Daily Pivot Point, suggesting a failure of the current move.

- VR Close All - Long ($\sym{size} > 0$) - Price crosses under a Daily Resistance Level (R1, R2, or R3) minus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Resistance as support.

- VS Close All - Short ($\sym{size} < 0$) - Price crosses above a Daily Support Level (S1, S2, or S3) plus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Support as resistance.

4. Trend Failure Exit (Trend-Following Signals Only)

This exit protects against holding a position when the primary high-timeframe trend used for the entry has failed:

- Long Positions Closed When: The primary trend is no longer "bullish" for more than 2 consecutive bars (i.e., it turned "bearish" or "flat").

- Short Positions Closed When: The primary trend is no longer "bearish" for more than 2 consecutive bars (i.e., it turned "bullish" or "flat").

5. End of Day (EOD) Session Control

The final hard exits based on time:

- End of Session (EoS): At 11:30 AM, new trades are disabled (TradingDay := false). Open positions are kept.

- End of Day (EoD): At 1:30 PM, all remaining open positions are closed (strategy.close_all).

🤝 Development & Disclaimer

This script and description were created with assistance from Gemini and GitHub Copilot. My focus is on helping fellow real estate investors and day traders develop mechanically sound systems.

Disclaimer: This is for educational purposes only and does not constitute financial advice. Always abide by the Realtor Code and manage your own risk.

Tight Entry Trend Engine Strategy═══════════════════════════════════════

TIGHT ENTRY TREND ENGINE

═══════════════════════════════════════

A breakout-based trend-following system designed to capture explosive

moves by entering at precise resistance/support breakouts with minimal

entry risk and massive profit potential.

⚠️ LOW WIN RATE, HIGH REWARD SYSTEM ⚠️

This is NOT a high win-rate strategy. Expect 25-35% winners, but

when it hits, winners are typically 10X+ larger than losers.

═══════════════════════════════════════

🎯 WHAT THIS SYSTEM DOES

═══════════════════════════════════════

The Tight Entry Trend Engine identifies powerful breakout opportunities

by detecting when price breaks through established trendlines with

confirmation from higher timeframe trends:

1. DYNAMIC TRENDLINE DETECTION (3 BANKS)

• Automatically draws support and resistance trendlines

• 3 separate "banks" capture short-term, medium-term, and long-term levels

• Each bank has configurable parameters (required pivot touch count,

angle limits, lengths)

2. BREAKOUT ENTRY TIMING

• Enters LONG when price breaks ABOVE resistance trendlines

• Enters SHORT when price breaks BELOW support trendlines

• Entry Alert occurs at the exact moment of breakout = "tight entry"

• Stop-loss placed just below/above the broken trendline (configurable)

3. HIGHER TIMEFRAME TREND FILTER

• Uses Hull Moving Average (HMA) on higher timeframe for trend following

• Auto-adjusts HTF based on your chart timeframe

• Optional filters prevent entries against major trend

• Optional "overextension" filter avoids buying parabolic moves

4. VOLATILITY-ADAPTIVE RISK MANAGEMENT

• Stop-loss calculated using Average True Range (ATR)

• Tighter stops = better R:R

• Profit targets adjust dynamically with volatility

• Breakeven stop moves automatically when in profit

• Extended profit targets when far from HTF trend

═══════════════════════════════════════

📊 HOW IT WORKS (METHODOLOGY)

═══════════════════════════════════════

STEP 1: TRENDLINE FORMATION

The system continuously scans for pivot highs and pivot lows to

construct trendlines. You control:

BANK 1 (Short-Term):

- Pivot Length: How many bars to look back for swing points

- Min Touches: How many pivots needed to form a line (default: 3)

- Max Length: How far back lines can reach (default: 180 bars)

- Angle Limits: Maximum steepness allowed for valid trendlines

- Tolerance: How close pivots must align to form horizontal lines

BANK 2 (Medium-Term):

- Slightly longer pivot periods for more significant levels

- Captures medium-term trend structure

- Default Max Length: 200 bars

BANK 3 (Long-Term):

- Focuses on major support/resistance zones

- Often uses horizontal levels (angled lines disabled by default)

- Default Max Length: 300 bars

The system draws RESISTANCE lines (red) above price and SUPPORT

lines (green) below price. These adapt in real-time as new pivots form.

STEP 2: BREAKOUT DETECTION

LONG SIGNALS:

- Price closes above a resistance trendline

- Higher timeframe trend is up (optional filter)

- Price not overextended from HTF trend (optional filter)

- No position currently open

SHORT SIGNALS:

- Price closes below a support trendline

- Higher timeframe trend is down (optional filter)

- Price not overextended from HTF trend (optional filter)

- No position currently open

The "tight" aspect: Because you're entering right at the trendline

break, your stop-loss can be placed very close (just below the

broken resistance for longs), creating exceptional risk/reward ratios.

STEP 3: POSITION SIZING

Choose between:

- Fixed $ Risk Per Trade: Risk same dollar amount every trade

- % Risk Per Trade: Risk percentage of current equity

Position size automatically calculated based on:

- Your risk amount

- Distance to stop-loss (ATR-based)

- Works with stocks, futures, crypto (auto-adjusts for contract multipliers)

STEP 4: EXIT MANAGEMENT

Multiple exit methods working together:

- PROFIT TARGET: Exits when profit reaches 100x your risk

- EXTENDED PROFIT: Earlier exit (80R) when very far from HTF trend

- STOP LOSS: Fixed ATR-based stop below entry

- HTF TREND EXIT: Exits when price crosses below HTF trend with profit

- BREAKEVEN PULLBACK: Exits if profit drops below 0.6R after reaching breakeven

- PARTIAL PROFITS: Optional - take partial profits at specified R-multiple

═══════════════════════════════════════

🔧 KEY COMPONENTS EXPLAINED

═══════════════════════════════════════

HULL MOVING AVERAGE (HMA)

A smoothed moving average that reduces lag compared to traditional

MAs. The system uses HMA on a higher timeframe to determine the

dominant trend direction. You can choose:

- Auto HTF: System picks appropriate HTF based on your chart timeframe

- Manual HTF: You specify the higher timeframe

AVERAGE TRUE RANGE (ATR)

Measures current market volatility. Used for:

- Stop-loss distance (tighter when volatility low)

- Profit targets (larger when volatility high)

- Position sizing (smaller positions in volatile conditions)

- Breakeven trigger distance

TRENDLINE ANGLE FILTERING

Each trendline bank has angle limits to ensure quality:

- Resistance lines: Max downward/upward slope allowed

- Support lines: Max downward/upward slope allowed

- Angles automatically adjust based on current volatility

- Prevents overly steep/unreliable trendlines

SENSITIVITY CONTROL

One master slider adjusts multiple parameters:

- Trendline detection sensitivity

- HTF MA length

- Exit timing

- Auto-adjusts for daily+ timeframes (60% increase)

═══════════════════════════════════════

⚙️ WHAT YOU SEE ON YOUR CHART

═══════════════════════════════════════

TRENDLINES:

✓ Red resistance lines above price

✓ Green support lines below price

✓ Orange broken lines (past breakouts)

✓ Lines extend to show current levels

HTF TREND:

✓ Thick colored line showing higher timeframe trend

✓ Color gradient: Red (bearish) → Orange → Yellow → Green (bullish)

✓ 250-bar smoothed curve for visual clarity

ENTRY/EXIT SIGNALS:

✓ Small green dot below bar = Long entry

✓ Small red dot above bar = Short entry

✓ Small red dot above = Long exit

✓ Small black dot below = Short exit

OPTIONAL DETAILED LABELS:

✓ Bank number that triggered entry (Bank 1, 2, or 3)

✓ Exit reason (Profit Target, Stop Loss, HTF Exit, etc.)

✓ Partial profit notifications

POSITION TRACKING:

✓ Yellow dashed line at entry price (extends right)

✓ Green/red fill showing current profit/loss zone

✓ Lime arrows at top = Currently in long position

✓ Red arrows at bottom = Currently in short position

✓ Gray background = No position (flat)

STATS TABLE (Top Right):

✓ Current position (LONG/SHORT/FLAT)

✓ Risk per trade ($ or %)

✓ Entry price

✓ Unrealized P/L in dollars

✓ P/L in R-multiples (how many R's profit/loss)

✓ Average winner/loser R ($ mode) OR CAGR (% mode)

═══════════════════════════════════════

📈 OPTIMAL USAGE

═══════════════════════════════════════

BEST ASSETS:

- NASDAQ:QQQ on 1-hour (reg) chart ⭐ (PRIMARY OPTIMIZATION)

- Strong trending stocks: NVDA, AAPL, TSLA, MSFT, GOOGL, AMZN

- High volatility tech stocks

- Crypto: BTC, ETH

- Any liquid asset with clear trends and momentum (GOLD)

AVOID:

- Low volatility stocks

- Ranging/choppy markets

- Penny stocks or illiquid assets

- Assets without clear directional movement

BEST TIMEFRAMES:

- PRIMARY: 1-hour charts (optimal for QQQ)

- ALSO EXCELLENT: 2H, 4H, 8H

- WORKS: 15min, 30min (only momentum leaders, more noise)

- WORKS WITH ADJUSTMENTS: 1D, 2D (decrease trendline pivot lengths)

═══════════════════════════════════════

📊 BACKTEST RESULTS (QQQ 1H (Reg hours), 1999-2024)

═══════════════════════════════════════

The system showed on NASDAQ:QQQ 1-hour timeframe (regular hours):

- Total Return: 1,100,000%+ over 24 years

- Total Trades: 500+

- Win Rate: ~20-24% (LOW - this is by design!)

- Average Winner: 8-15% gain

- Average Loser: 2-4% loss

- Win/Loss Ratio: 10:1 (winners much bigger than losers)

- Profit Factor: 3+

- Max Drawdown: 45-50%

- Risk per trade: 3% of capital

KEY INSIGHT: This is a LOW WIN RATE, HIGH REWARD system. You will

lose more trades than you win, but the few winners are so large

they more than compensate for many small losses.

IMPORTANT: These are backtested results using optimal parameters

on historical data. Real trading results will vary based on:

- Your execution and timing

- Slippage and commissions

- Your emotional discipline

- Market conditions during your trading period

═══════════════════════════════════════

🎓 WHO IS THIS FOR?

═══════════════════════════════════════

IDEAL FOR:

✓ Swing traders comfortable holding winners for longer period

✓ Part-time traders (1H = check 2-3x per day)

✓ Traders seeking exceptional risk/reward ratios

✓ Those comfortable with low win rates if winners are huge

✓ Technical analysis enthusiasts

✓ Breakout traders

✓ Trend followers

═══════════════════════════════════════

🚀 GETTING STARTED - STEP BY STEP

═══════════════════════════════════════

STEP 1: APPLY TO YOUR CHART

- Search "Tight Entry Trend Engine" in indicators

- Click to apply to your chart

- Trendlines and HTF line will appear immediately

STEP 2: CHOOSE YOUR SETTINGS

For BEGINNERS - Use These Settings First:

1. Trade Direction & Filters:

• ENABLE LONGS: ✓ ON

• ENABLE SHORTS: ✗ OFF (start with longs only)

• Sensitivity: 1.0 (default)

• HTF Trend Entry Filter: ✓ ON (safer entries)

• Block Entries When Overextended: ✓ ON (avoid parabolic tops)

2. Position Sizing & Risk:

• Position Sizing: "Per Risk"

• RISK Type: "$ Per Trade"

• Risk Amount: $200 (or 1-3% of your account)

3. Visual Settings:

• Show Support Lines: ✗ OFF (unless trading shorts)

• Show Detailed Entry/Exit Labels: ✓ ON

• Show Stats Table: ✓ ON

• Show Entry Line & P/L Fill: ✓ ON

4. Leave everything else at DEFAULT for now

STEP 3: UNDERSTAND WHAT YOU SEE

When trendlines appear:

- RED lines above = Resistance (watch for price breaking UP through these)

- GREEN lines below = Support (watch for price breaking DOWN)

- When price breaks a red line = Potential LONG entry

- When price breaks a green line = Potential SHORT entry

The HTF trend line (thick colored):

- Green/lime = Strong uptrend (favorable for longs)

- Red = Strong downtrend (favorable for shorts if enabled)

- Orange/yellow = Transitioning

STEP 4: OBSERVE SIGNALS

- Small GREEN dot below bar = System entered LONG

- Small RED dot above bar = System exited LONG

- Check the label to see which "Bank" triggered (Bank 1, 2, or 3)

- Watch the yellow entry line and colored fill show your P/L

STEP 5: PAPER TRADE FIRST

- Use TradingView's paper trading feature

- Watch how signals perform on YOUR chosen asset

- Understand the win rate will be LOW (20-35%)

- Verify that winners are indeed much larger than losers

- Test for at least 20-30 signals before going live

STEP 6: OPTIMIZE FOR YOUR ASSET (OPTIONAL)

If default settings aren't working well:

For FASTER signals (more trades):

- Reduce Pivot Length 1 to 3-4

- Reduce Max Length 1 to 120-150

- Increase Sensitivity to 1.2-1.5

For SLOWER signals (higher quality):

- Increase Pivot Length 1 to 7-10

- Increase Max Length 1 to 250+

- Decrease Sensitivity to 0.7-0.9

For DAILY timeframes:

- Increase all Pivot Lengths by 30-50%

- Increase all Max Lengths significantly

- Sensitivity: 0.6-0.8

═══════════════════════════════════════

⚙️ ADVANCED SETTINGS EXPLAINED

═══════════════════════════════════════

TRENDLINE BANK SETTINGS:

Each bank (1, 2, 3) has these parameters:

- Min Touches: Minimum pivots to form a line

- Lower (2) = More lines, earlier detection

- Higher (4+) = Fewer lines, higher quality

- Pivot Length: Lookback for swing points

- Lower (3-5) = Reacts to recent price action

- Higher (10+) = Only major swing points

- Max Length: How old a trendline can be

- Shorter (100-150) = Only recent lines

- Longer (300+) = Include historical levels

- Tolerance: Alignment strictness for horizontal lines

- Lower (3.0-3.5) = Very strict horizontal

- Higher (4.5+) = More forgiving alignment

- Allow Angled Lines: Enable diagonal trendlines

- ON = Catches sloped support/resistance

- OFF = Only horizontal levels

- Angle Limits: Maximum steepness allowed

- Lower (1-2) = Only gentle slopes

- Higher (4-6) = Accept steeper angles

- Automatically adjusts for volatility

ATR MULTIPLIERS:

- STOP LOSS ATR (0.6): Distance to stop-loss

- Lower (0.4-0.5) = Tighter stops, stopped out more

- Higher (0.8-1.0) = Wider stops, more room

- PROFIT TARGET ATR (100): Main profit target

- This is 100x your risk = 10,000% R:R

- Lower (50-80) = Take profits sooner

- Higher (120+) = Let winners run longer

- BREAKEVEN ATR (40): When to move stop to breakeven

- Lower (20-30) = Protect profits earlier

- Higher (60+) = Give more room before protecting

HIGHER TIMEFRAME:

- Auto HTF: Automatically selects appropriate HTF

- 5min chart → uses 2H

- 15-30min → uses 6H

- 1-4H → uses 2D

- Daily → uses 4D

- HTF MA Length (300): HMA period for trend

- Lower (150-250) = More responsive

- Higher (400-500) = Smoother, less whipsaw

- HTF Trend Following Exit: Exits when crossing HTF

- ON = Additional exit method

- OFF = Rely only on profit targets/stops

- HTF Trend Entry Filter: Only trade with HTF trend

- ON = Safer, fewer signals

- OFF = More aggressive, more signals

- Block Entries When Overextended: Prevents chasing

- ON = Avoids parabolic tops/bottoms

- OFF = Enter all breakouts regardless

═══════════════════════════════════════

💡 TRADING PHILOSOPHY & EXPECTATIONS

═══════════════════════════════════════

This system is built on one core principle:

"ACCEPT SMALL, FREQUENT LOSSES TO CAPTURE RARE, MASSIVE WINS"

What this means:

- You WILL lose 65%-75% of your trades

- Most losses will be small (1-2R)

- Some winners hit 80R+

- Over time, math works in your favour

Trend-Following & Breakout — Index Quant Strategy (NASDAQ)📈 Trend-Following & Breakout — Index Quant Strategy (NASDAQ & S&P 500)

Type: Invite-only strategy

Markets: NASDAQ 100 (NAS100 / US100 / NQ), S&P 500 (US500 / SPX), and other major equity indices.

🧠 Concept: Continuous trend model combining EWMAC (trend-following) and Donchian (breakout) signals, scaled by forecast strength and portfolio risk.

⚙️ Execution: Rebalances only on decision-bar closes, using hysteresis and a no-trade band to reduce churn.

📊 Default bias: Long-only — aligned with equity index drift.

🧩 How it works

• EWMAC Trend: Difference between fast and slow EMAs, normalized by an EWMA of absolute returns.

• Donchian Breakout: Distance beyond a 200-bar channel (Strict mode) or relative z-score position within it.

• Forecast combination: Weighted sum of trend and breakout points, clamped to ± capPoints.

• Hysteresis: Prevents quick sign flips near zero forecast.

• Risk scaling: Maps forecast strength to position size using equity × risk budget × ATR-based stop distance.

• Rebalance: Executes only if the required quantity change exceeds the Δqty threshold; can optionally block increases on Sundays (for CFDs).

⚙️ Default parameters

Deployed on NQ / US100 / NAS100 on Daily Timeframe

• Decision timeframe = 360 min (other options from 1 min to 1 week).

• Trend (EWMAC): Fast = 64, Slow = 256, Vol Norm = 32, Weight = 0.8.

• Breakout (Donchian): Length = 200, Mode = Strict, Weight = 0.2.

• Forecast scaling: ptsPerSigma = 1.0, capPoints = 10.

• Risk % per rebalance = 4 % of equity.

• ATR stop: ATR(14) × 1.0.

• No-trade band (Δqty) = 4 units.

• Hysteresis = 2 forecast points.

• Bias = Long-only (Neutral / Long-bias 50 % optional).

• Skip Sunday increases = false (default).

📋 Backtest properties (documented)

• Initial capital = 100 000 USD.

• Commission = 0.20 % per trade.

• Pyramiding = 10.

• Calc on every tick = false.

• Point value = 1 (for NAS100 CFD).

• No financing or slippage modeled.

• If using CFDs, account for overnight funding.

• On futures (NQ / ES), carry is implicit.

📊 Typical behaviour

• Many small scratches, a few large winners.

• Performs best during multi-week / multi-month trends.

• Underperforms in tight or volatile ranges.

• Average hold ≈ 30 – 90 days in historical tests.

💡 Risk and performance guide (illustrative)

Sharpe ≈ 1.25

Sortino ≈ 1.10 – 1.30

Max drawdown ≈ –18 % to –25 %

Annual volatility ≈ 24 – 28 %

CAGR ≈ 50 – 60 % (at 4 % risk)

Edge ratio ≈ 5 (MFE / MAE)

Historical backtests only — past performance does not guarantee future results.

🌍 Intended markets and timeframes

Optimized for NASDAQ 100 and S&P 500; also effective on similar indices (DAX, Dow Jones, FTSE).

Best on Daily or higher timeframes.

Aligns with long-term index drift — suitable for long-bias systematic trend portfolios.

⚠️ Limitations

• Backtests exclude CFD funding costs.

• Trend models will have losing streaks in range-bound markets.

• Designed for experienced traders seeking systematic exposure.

🔑 Requesting access

Send a private TradingView message to with the text:

“Request access to Trend-Following & Breakout — Index Quant Strategy.”

Access is granted only on explicit request.

For further information, see my TradingView Signature.

🆕 Release notes (v1.0)

• Initial release (360 min TF): EWMAC 64/256 + Donchian 200 Strict.

• Risk 4 %, ATR × 1.0, Long-only bias, hysteresis 2 pts, Δqty ≥ 4.

• Developed for NASDAQ 100 and S&P 500 indices.

• Implements continuous risk-scaled positioning and no-trade band logic.

🧾 Originality statement

This strategy is original work built entirely from TradingView built-ins (EMA, ATR, Highest, Lowest).

It does not reuse open-source invite-only code.

Any future reuse of open scripts will be done with explicit permission and credit.

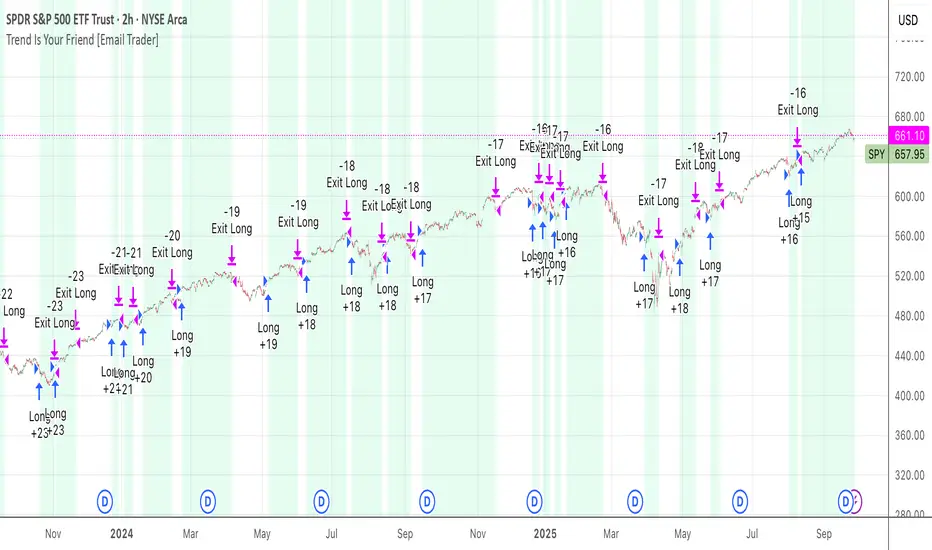

TrendIsYourFriend Strategy (SPY,IWM,VYM,XLK,SPXL,BTC,GOLD,VT...)Personal disclaimer

Don’t trust this strategy. Don’t trust any other model either just because of its author or a backtest curve. Overfitting is an easy trap, and beginners often fall into it. This script isn’t meant to impress you. It’s meant to survive reality. If it does, maybe it will raise questions and you’ll remember it.

Legal disclaimer

Educational purposes only. Not financial advice. Past performance is not indicative of future results.

Strategy description

Long-only, trend-based logic with two entry types (trend continuation or excess-move reversion), dynamic stop-losses, and a VIX filter to avoid turbulent markets.

Minimal number of parameters with enough trades to support robustness.

For backtest, each trade is sized at $10,000 flat (no compounding, to focus on raw model quality and the regularity of its results over time).

Fees = $0 (neutral choice, as brokers differ).

Slippage = $0, deliberate choice: most entries occur on higher timeframes, and some assets start their history on charts at very low prices, which would otherwise distort results.

What makes this script original

Beyond a classical trend calculation, both excess-move entries and dynamic stop-loss exits also rely on trend logic. Except for the VIX filter, everything comes from trend functions, with very few parameters.

Pre-configurations are fixed in the code, allowing sincere performance tracking across a dozen cases over the medium to long term.

Allowed

SPY (ARCA) — 2-hour chart: S&P 500 ETF, most liquid equity benchmark

IWM (ARCA) — Daily chart: Russell 2000 ETF, US small caps

VYM (ARCA) — Daily chart: Vanguard High Dividend Yield ETF

XLK (ARCA) — Daily chart: Technology Select Sector SPDR

SPXL (ARCA) — Daily chart: 3× leveraged S&P 500 ETF

BTCUSD (COINBASE) — 4-hour chart: Bitcoin vs USD

GOLD (TVC) — Daily chart: Gold spot price

VT (ARCA) — Daily chart: Vanguard Total World Stock ETF

PG (NYSE) — Daily chart: Procter & Gamble Co.

CQQQ (ARCA) — Daily chart: Invesco China Technology ETF

EWC (ARCA) — Daily chart: iShares MSCI Canada ETF

EWJ (ARCA) — Daily chart: iShares MSCI Japan ETF

How to use and form an opinion on it

Works only on the pairs above.

Feel free to modify the input parameters (slippage, fees, order size, margins, …) to see how the model behaves under your own conditions

Compare it with a simple Buy & Hold (requires an order size of 100% equity).

You may also want to look at its time-in-market — the share of time your capital is actually at risk.

Finally, let me INSIST on this : let it run live for months before forming an opinion!

Share your thoughts in the comments 🚀 if you’d like to discuss its live performance.

Nirvana True Duel전략 이름

열반의 진검승부 (영문: Nirvana True Duel)

컨셉과 철학

“열반의 진검승부”는 시장 소음은 무시하고, 확실할 때만 진입하는 전략입니다.

EMA 리본으로 추세 방향을 확인하고, 볼린저 밴드 수축/확장으로 변동성 돌파를 포착하며, OBV로 거래량 확인을 통해 가짜 돌파를 필터링합니다.

전략 로직

매수 조건 (롱)

20EMA > 50EMA (상승 추세)

밴드폭 수축 후 확장 시작

종가가 상단 밴드 돌파

OBV 상승 흐름 유지

매도 조건 (숏)

20EMA < 50EMA (하락 추세)

밴드폭 수축 후 확장 시작

종가가 하단 밴드 이탈

OBV 하락 흐름 유지

진입·청산

손절: ATR × 1.5 배수

익절: 손절폭의 1.5~2배에서 부분 청산

시간 청산: 설정한 최대 보유 봉수 초과 시 강제 청산

장점

✅ 추세·변동성·거래량 3중 필터 → 노이즈 최소화

✅ 백테스트·알람 지원 → 기계적 매매 가능

✅ 5분/15분 차트에 적합 → 단타/스윙 트레이딩 활용 가능

주의점

⚠ 횡보장에서는 신호가 적거나 실패 가능

⚠ 수수료·슬리피지 고려 필요

📜 Nirvana True Duel — Strategy Description (English)

Name:

Nirvana True Duel (a.k.a. Nirvana Cross)

Concept & Philosophy

The “Nirvana True Duel” strategy focuses on trading only meaningful breakouts and avoiding unnecessary noise.

Nirvana: A calm, patient state — waiting for the right opportunity without emotional trading.

True Duel: When the signal appears, enter decisively and let the market reveal the outcome.

In short: “Ignore market noise, trade only high-probability breakouts.”

🧩 Strategy Components

Trend Filter (EMA Ribbon): Stay aligned with the main market trend.

Volatility Squeeze (Bollinger Band): Detect volatility contraction & expansion to catch explosive moves early.

Volume Confirmation (OBV): Filter out false breakouts by confirming with volume flow.

⚔️ Entry & Exit Conditions

Long Setup:

20 EMA > 50 EMA (uptrend)

BB width breaks out from recent squeeze

Close > Upper Bollinger Band

OBV shows positive flow

Short Setup:

20 EMA < 50 EMA (downtrend)

BB width breaks out from recent squeeze

Close < Lower Bollinger Band

OBV shows negative flow

Risk Management:

Stop Loss: ATR × 1.5 below/above entry

Take Profit: 1.5–2× stop distance, partial take-profit allowed

Time Stop: Automatically closes after max bars held (e.g. 8h on 5m chart)

✅ Strengths

Triple Filtering: Trend + Volatility + Volume → fewer false signals

Mechanical & Backtestable: Ideal for objective trading & performance validation

Adaptable: Works well on Bitcoin, Nasdaq futures, and other high-volatility markets (5m/15m)

⚠️ Things to Note

Low signal frequency or higher failure rate in sideways/range markets

Commission & slippage should be factored in, especially on lower timeframes

ATR multiplier and R:R ratio should be optimized per asset

Backtest - Strategy Builder [AlgoAlpha]🟠 OVERVIEW

This script by AlgoAlpha is a modular Strategy Builder designed to let traders test custom trade entry and exit logic on TradingView without writing their own Pine code. It acts as a framework where users can connect multiple external signals, chain them in sequences, and run backtests with built-in leverage, margin, and risk controls. Its main strength is flexibility—you can define up to five sequential steps for entry and exit conditions on both long and short sides, with logic connectors (AND/OR) controlling how conditions combine. This lets you test complex multi-step confirmation workflows in a controlled, visual backtesting environment.

🟠 CONCEPTS

The system works by linking external signals —these can be values from other indicators, and/or custom sources—to conditional checks like “greater than,” “less than,” or “crossover.” You can stack these checks into steps , where all conditions in a step must pass before the sequence moves to the next. This creates a chain of logic that must be completed before a trade triggers. On execution, the strategy sizes positions according to your chosen leverage mode ( Cross or Isolated ) and allocation method ( Percent of equity or absolute USD value]). Liquidation prices are simulated for both modes, allowing realistic margin behaviour in testing. The script also tracks performance metrics like Sharpe, Sortino, profit factor, drawdown, and win rate in real time.

🟠 FEATURES

Up to 5 sequential steps for both long and short entries, each with multiple conditions linked by AND/OR logic.

Two leverage modes ( Cross and Isolated ) with independent long/short leverage multipliers.

Separate multi-step exit triggers for longs and shorts, with optional TP/SL levels or opposite-side triggers for flipping positions.

Position sizing by equity percent or fixed USD amount, applied before leverage.

Realistic liquidation price simulation for margin testing.

Built-in trade gating and validation—prevents trades if configuration rules aren’t met (e.g., no exit defined for an active side).

Full performance dashboard table showing live strategy status, warnings, and metrics.

Configurable bar coloring based on position side and TP/SL level drawing on chart.

Integration with TradingView's strategy backtester, allowing users to view more detailed metrics and test the strategy over custom time horizons.

🟠 USAGE

Add the strategy to your chart. In the settings, under Master Settings , enable longs/shorts, select leverage mode, set leverage multipliers, and define position sizing. Then, configure your Long Trigger and Short Trigger groups: turn on conditions, pick which external signal they reference, choose the comparison type, and assign them to a sequence step. For exits, use the corresponding Exit Long Trigger and Exit Short Trigger groups, with the option to link exits to opposite-side entries for auto-flips. You can also enable TP and/or SL exits with custom sources for the TP/SL levels. Once set, the strategy will simulate trades, show performance stats in the on-chart table, and highlight any configuration issues before execution. This makes it suitable for testing both simple single-signal systems and complex, multi-filtered strategies under realistic leverage and margin constraints.

🟠 EXAMPLE

The backtester on its own does not contain any indicator calculation; it requires input from external indicators to function. In this example, we'll be using AlgoAlpha's Smart Signals Assistant indicator to demonstrate how to build a strategy using this script.

We first define the conditions beforehand:

Entry :

Longs – SSA Bullish signal (strong OR weak)

Shorts – SSA Bearish signal (strong OR weak)

Exit

Longs/Shorts: (TP/SL hit OR opposing signal fires)

Other Parameters (⚠️Example only, tune this based on proper risk management and settings)

Long Leverage: default (3x)

Short Leverage: default (3x)

Position Size: default (10% of equity)

Steps

Load up the required indicators (in this example, the Smart Signals Assistant).

Ensure the required plots are being output by the indicator properly (signals and TP/SL levels are being plotted).

Open the Strategy Builder settings and scroll down to "CONDITION SETUP"; input the signals from the external indicator.

Configure the exit conditions, add in the TP/SL levels from the external indicator, and add an additional exit condition → {{Opposite Direction}} Entry Trigger.

After configuring the entry and exit conditions, the strategy should now be running. You can view information on the strategy in TradingView's backtesting report and also in the Strategy Builder's information table (default top right corner).

It is important to note that the strategy provided above is just an example, and the complexity of possible strategies stretches beyond what was shown in this short demonstration. Always incorporate proper risk management and ensure thorough testing before trading with live capital.

Skrip berbayar

Dynamic DCA Envelope – Beta V1.1Dynamic DCA Envelope-Beta V1.1 is a preview version of a Dollar-Cost Averaging (DCA) strategy designed for trending or volatile markets.

-Long Positions Only

-Intended for Cryptocurrency, but can be used in any market

-1 and 4 hour timeframe

-Average Commissions 0.1%-0.3% per trade (Cryptocurrency)

What it does:

This strategy identifies buying opportunities when price closes below a dynamic envelope (based on EMA). After 3 consecutive closes below the lower envelope, the system arms a buy condition. A DCA buy-in is triggered when price bounces by a configurable percentage from the trailing low. The strategy supports up to 3 buy-ins, each equally sized, and closes the entire position at a fixed take profit or stop loss.

How it works:

-Entry logic is based on price deviation from an EMA envelope

-Waits for 3 closes below the envelope to detect weakness

-Uses bounce percentage from the lowest point to trigger each buy

-Includes cooldown logic between buys to avoid clustering

-All positions are closed when TP or SL is hit

How to use it:

-Use on trending assets with volatility (e.g., crypto, tech stocks)

-Adjust inputs to match asset behavior:

-EMA Length

-Envelope Offset %

-Bounce % (Trailing DCA)

-Take Profit / Stop Loss

-View strategy performance in the Strategy Tester tab

What’s unique:

Unlike most DCA scripts that immediately average down, this version includes:

-Trigger logic requiring multiple closes below trend

-Bounce-based entry to avoid catching a falling knife

-Cooldown resets to prevent overtrading

-A true entry–wait–buy–reset loop mimicking disciplined execution

*This is a beta version intended as a preview. A full Pro version is in development, which includes:

-SmartScaling logic

-Trailing take profit

-Multi-symbol scanning

-Backtest range limits

-Risk-adjusted filtering

RSI-Adaptive T3 + Squeeze Momentum Strategy✅ Strategy Guide: RSI-Adaptive T3 + Squeeze Momentum Strategy

📌 Overview

The RSI-Adaptive T3 + Squeeze Momentum Strategy is a dynamic trend-following strategy based on an RSI-responsive T3 moving average and Squeeze Momentum detection .

It adapts in real-time to market volatility to enhance entry precision and optimize risk.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main objective of this strategy is to catch the early phase of a trend and generate consistent entry signals.

Designed to be intuitive and accessible for traders from beginner to advanced levels.

✨ Key Features

RSI-Responsive T3: T3 length dynamically adjusts according to RSI values for adaptive trend detection

Squeeze Momentum: Combines Bollinger Bands and Keltner Channels to identify trend buildup phases

Visual Triggers: Entry signals are generated from T3 crossovers and momentum strength after squeeze release

📊 Trading Rules

Long Entry:

When T3 crosses upward, momentum is positive, and the squeeze has just been released.

Short Entry:

When T3 crosses downward, momentum is negative, and the squeeze has just been released.

Exit (Reversal):

When the opposite condition to the entry is triggered, the position is reversed.

💰 Risk Management Parameters

Pair & Timeframe: BTC/USD (30-minute chart)

Capital (simulated): $30,00

Order size: `$100` per trade (realistic, low-risk sizing)

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 5%

Number of Trades (backtest period): 181

📊 Performance Overview

Symbol: BTC/USD

Timeframe: 30-minute chart

Date Range: January 1, 2024 – July 3, 2025

Win Rate: 47.8%

Profit Factor: 2.01

Net Profit: 173.16 (units not specified)

Max Drawdown: 5.77% or 24.91 (0.79%)

⚙️ Indicator Parameters

Indicator Name: RSI-Adaptive T3 + Squeeze Momentum

RSI Length: 14

T3 Min Length: 5

T3 Max Length: 50

T3 Volume Factor: 0.7

BB Length: 27 (Multiplier: 2.0)

KC Length: 20 (Multiplier: 1.5, TrueRange enabled)

🖼 Visual Support

T3 slope direction, squeeze status, and momentum bars are visually plotted on the chart,

providing high clarity for quick trend analysis and execution.

🔧 Strategy Improvements & Uniqueness

Inspired by the RSI Adaptive T3 by ChartPrime and Squeeze Momentum Indicator by LazyBear ,

this strategy fuses both into a hybrid trend-reversal and momentum breakout detection system .

Compared to traditional trend-following methods, it excels at capturing early trend signals with greater sensitivity .

✅ Summary

The RSI-Adaptive T3 + Squeeze Momentum Strategy combines momentum detection with volatility-responsive risk management.

With a strong balance between visual clarity and practicality, it serves as a powerful tool for traders seeking high repeatability.

⚠️ This strategy is based on historical data and does not guarantee future profits.

Always use appropriate risk management when applying it.

Kaufman Trend Strategy# ✅ Kaufman Trend Strategy – Full Description (Script Publishing Version)

**Kaufman Trend Strategy** is a dynamic trend-following strategy based on Kaufman Filter theory.

It detects real-time trend momentum, reduces noise, and aims to enhance entry accuracy while optimizing risk.

⚠️ _For educational and research purposes only. Past performance does not guarantee future results._

---

## 🎯 Strategy Objective

- Smooth price noise using Kaufman Filter smoothing

- Detect the strength and direction of trends with a normalized oscillator

- Manage profits using multi-stage take-profits and adaptive ATR stop-loss logic

---

## ✨ Key Features

- **Kaufman Filter Trend Detection**

Extracts directional signal using a state space model.

- **Multi-Stage Profit-Taking**

Automatically takes partial profits based on color changes and zero-cross events.

- **ATR-Based Volatility Stops**

Stops adjust based on swing highs/lows and current market volatility.

---

## 📊 Entry & Exit Logic

**Long Entry**

- `trend_strength ≥ 60`

- Green trend signal

- Price above the Kaufman average

**Short Entry**

- `trend_strength ≤ -60`

- Red trend signal

- Price below the Kaufman average

**Exit (Long/Short)**

- Blue trend color → TP1 (50%)

- Oscillator crosses 0 → TP2 (25%)

- Trend weakens → Final exit (25%)

- ATR + swing-based stop loss

---

## 💰 Risk Management

- Initial capital: `$3,000`

- Order size: `$100` per trade (realistic, low-risk sizing)

- Commission: `0.002%`

- Slippage: `2 ticks`

- Pyramiding: `1` max position

- Estimated risk/trade: `~0.1–0.5%` of equity

> ⚠️ _No trade risks more than 5% of equity. This strategy follows TradingView script publishing rules._

---

## ⚙️ Default Parameters

- **1st Take Profit**: 50%

- **2nd Take Profit**: 25%

- **Final Exit**: 25%

- **ATR Period**: 14

- **Swing Lookback**: 10

- **Entry Threshold**: ±60

- **Exit Threshold**: ±40

---

## 📅 Backtest Summary

- **Symbol**: USD/JPY

- **Timeframe**: 1H

- **Date Range**: Jan 3, 2022 – Jun 4, 2025

- **Trades**: 924

- **Win Rate**: 41.67%

- **Profit Factor**: 1.108

- **Net Profit**: +$1,659.29 (+54.56%)

- **Max Drawdown**: -$1,419.73 (-31.87%)

---

## ✅ Summary

This strategy uses Kaufman filtering to detect market direction with reduced lag and increased smoothness.

It’s built with visual clarity and strong trade management, making it practical for both beginners and advanced users.

---

## 📌 Disclaimer

This script is for educational and informational purposes only and should not be considered financial advice.

Use with proper risk controls and always test in a demo environment before live trading.

SOXL Trend Surge v3.0.2 – Profit-Only RunnerSOXL Trend Surge v3.0.2 – Profit-Only Runner

This is a trend-following strategy built for leveraged ETFs like SOXL, designed to ride high-momentum waves with minimal interference. Unlike most short-term scalping scripts, this model allows trades to develop over multiple days to even several months, capitalizing on the full power of extended directional moves — all without using a stop-loss.

🔍 How It Works

Entry Logic:

Price is above the 200 EMA (long-term trend confirmation)

Supertrend is bullish (momentum confirmation)

ATR is rising (volatility expansion)

Volume is above its 20-bar average (liquidity filter)

Price is outside a small buffer zone from the 200 EMA (to avoid whipsaws)

Trades are restricted to market hours only (9 AM to 2 PM EST)

Cooldown of 15 bars after each exit to prevent overtrading

Exit Strategy:

Takes partial profit at +2× ATR if held for at least 2 bars

Rides the remaining position with a trailing stop at 1.5× ATR

No hard stop-loss — giving space for volatile pullbacks

⚙️ Strategy Settings

Initial Capital: $500

Risk per Trade: 100% of equity (fully allocated per entry)

Commission: 0.1%

Slippage: 1 tick

Recalculate after order is filled

Fill orders on bar close

Timeframe Optimized For: 45-minute chart

These parameters simulate an aggressive, high-volatility trading model meant for forward-testing compounding potential under realistic trading costs.

✅ What Makes This Unique

No stop-loss = fewer premature exits

Partial profit-taking helps lock in early wins

Trailing logic gives room to ride large multi-week moves

Uses strict filters (volume, ATR, EMA bias) to enter only during high-probability windows

Ideal for leveraged ETF swing or position traders looking to hold longer than the typical intraday or 2–3 day strategies

⚠️ Important Note

This is a high-risk, high-reward strategy meant for educational and testing purposes. Without a stop-loss, trades can experience deep drawdowns that may take weeks or even months to recover. Always test thoroughly and adjust position sizing to suit your risk tolerance. Past results do not guarantee future returns. Backtest range: May 8, 2020 – May 23, 2025

EMA 12/26 With ATR Volatility StoplossThe EMA 12/26 With ATR Volatility Stoploss

The EMA 12/26 With ATR Volatility Stoploss strategy is a meticulously designed systematic trading approach tailored for navigating financial markets through technical analysis. By integrating the Exponential Moving Average (EMA) and Average True Range (ATR) indicators, the strategy aims to identify optimal entry and exit points for trades while prioritizing disciplined risk management. At its core, it is a trend-following system that seeks to capitalize on price momentum, employing volatility-adjusted stop-loss mechanisms and dynamic position sizing to align with predefined risk parameters. Additionally, it offers traders the flexibility to manage profits either by compounding returns or preserving initial capital, making it adaptable to diverse trading philosophies. This essay provides a comprehensive exploration of the strategy’s underlying concepts, key components, strengths, limitations, and practical applications, without delving into its technical code.

=====

Core Philosophy and Objectives

The EMA 12/26 With ATR Volatility Stoploss strategy is built on the premise of capturing short- to medium-term price trends with a high degree of automation and consistency. It leverages the crossover of two EMAs—a fast EMA (12-period) and a slow EMA (26-period)—to generate buy and sell signals, which indicate potential trend reversals or continuations. To mitigate the inherent risks of trading, the strategy incorporates the ATR indicator to set stop-loss levels that adapt to market volatility, ensuring that losses remain within acceptable bounds. Furthermore, it calculates position sizes based on a user-defined risk percentage, safeguarding capital while optimizing trade exposure.

A distinctive feature of the strategy is its dual profit management modes:

SnowBall (Compound Profit): Profits from successful trades are reinvested into the capital base, allowing for progressively larger position sizes and potential exponential portfolio growth.

ZeroRisk (Fixed Equity): Profits are withdrawn, and trades are executed using only the initial capital, prioritizing capital preservation and minimizing exposure to market downturns.

This duality caters to both aggressive traders seeking growth and conservative traders focused on stability, positioning the strategy as a versatile tool for various market environments.

=====

Key Components of the Strategy

1. EMA-Based Signal Generation

The strategy’s trend-following mechanism hinges on the interaction between the Fast EMA (12-period) and Slow EMA (26-period). EMAs are preferred over simple moving averages because they assign greater weight to recent price data, enabling quicker responses to market shifts. The key signals are:

Buy Signal: Triggered when the Fast EMA crosses above the Slow EMA, suggesting the onset of an uptrend or bullish momentum.

Sell Signal: Occurs when the Fast EMA crosses below the Slow EMA, indicating a potential downtrend or the end of a bullish phase.

To enhance signal reliability, the strategy employs an Anchor Point EMA (AP EMA), a short-period EMA (e.g., 2 days) that smooths the input price data before calculating the primary EMAs. This preprocessing reduces noise from short-term price fluctuations, improving the accuracy of trend detection. Additionally, users can opt for a Consolidated EMA (e.g., 18-period) to display a single trend line instead of both EMAs, simplifying chart analysis while retaining trend insights.

=====

2. Volatility-Adjusted Risk Management with ATR

Risk management is a cornerstone of the strategy, achieved through the use of the Average True Range (ATR), which quantifies market volatility by measuring the average price range over a specified period (e.g., 10 days). The ATR informs the placement of stop-loss levels, which are set at a multiple of the ATR (e.g., 2x ATR) below the entry price for long positions. This approach ensures that stop losses are proportionate to current market conditions—wider during high volatility to avoid premature exits, and narrower during low volatility to protect profits.

For example, if a stock’s ATR is $1 and the multiplier is 2, the stop loss for a buy at $100 would be set at $98. This dynamic adjustment enhances the strategy’s adaptability, preventing stop-outs from normal market noise while capping potential losses.

=====

3. Dynamic Position Sizing

The strategy calculates position sizes to align with a user-defined Risk Per Trade, typically expressed as a percentage of capital (e.g., 2%). The position size is determined by:

The available capital, which varies depending on whether SnowBall or ZeroRisk mode is selected.

The distance between the entry price and the ATR-based stop-loss level, which represents the per-unit risk.

The desired risk percentage, ensuring that the maximum loss per trade does not exceed the specified threshold.

For instance, with a $1,000 capital, a 2% risk per trade ($20), and a stop-loss distance equivalent to 5% of the entry price, the strategy computes the number of units (shares or contracts) to ensure the total loss, if the stop loss is hit, equals $20. To prevent over-leveraging, the strategy includes checks to ensure that the position’s dollar value does not exceed available capital. If it does, the position size is scaled down to fit within the capital constraints, maintaining financial discipline.

=====

4. Flexible Capital Management

The strategy’s dual profit management modes—SnowBall and ZeroRisk—offer traders strategic flexibility:

SnowBall Mode: By compounding profits, traders can increase their capital base, leading to larger position sizes over time. This is ideal for those with a long-term growth mindset, as it harnesses the power of exponential returns.

ZeroRisk Mode: By withdrawing profits and trading solely with the initial capital, traders protect their gains and limit exposure to market volatility. This conservative approach suits those prioritizing stability over aggressive growth.

These options allow traders to tailor the strategy to their risk tolerance, financial goals, and market outlook, enhancing its applicability across different trading styles.

=====

5. Time-Based Trade Filtering

To optimize performance and relevance, the strategy includes an option to restrict trading to a specific time range (e.g., from 2018 onward). This feature enables traders to focus on periods with favorable market conditions, avoid historically volatile or unreliable data, or align the strategy with their backtesting objectives. By confining trades to a defined timeframe, the strategy ensures that performance metrics reflect the intended market context.

=====

Strengths of the Strategy

The EMA 12/26 With ATR Volatility Stoploss strategy offers several compelling advantages:

Systematic and Objective: By adhering to predefined rules, the strategy eliminates emotional biases, ensuring consistent execution across market conditions.

Robust Risk Controls: The combination of ATR-based stop losses and risk-based position sizing caps losses at user-defined levels, fostering capital preservation.

Customizability: Traders can adjust parameters such as EMA periods, ATR multipliers, and risk percentages, tailoring the strategy to specific markets or preferences.

Volatility Adaptation: Stop losses that scale with market volatility enhance the strategy’s resilience, accommodating both calm and turbulent market phases.

Enhanced Visualization: The use of color-coded EMAs (green for bullish, red for bearish) and background shading provides intuitive visual cues, simplifying trend and trade status identification.

=====

Limitations and Considerations

Despite its strengths, the strategy has inherent limitations that traders must address:

False Signals in Range-Bound Markets: EMA crossovers may generate misleading signals in sideways or choppy markets, leading to whipsaws and unprofitable trades.

Signal Lag: As lagging indicators, EMAs may delay entry or exit signals, causing traders to miss rapid trend shifts or enter trades late.

Overfitting Risk: Excessive optimization of parameters to fit historical data can impair the strategy’s performance in live markets, as past patterns may not persist.

Impact of High Volatility: In extremely volatile markets, wider stop losses may result in larger losses than anticipated, challenging risk management assumptions.

Data Reliability: The strategy’s effectiveness depends on accurate, continuous price data, and discrepancies or gaps can undermine signal accuracy.

=====

Practical Applications

The EMA 12/26 With ATR Volatility Stoploss strategy is versatile, applicable to diverse markets such as stocks, forex, commodities, and cryptocurrencies, particularly in trending environments. To maximize its potential, traders should adopt a rigorous implementation process:

Backtesting: Evaluate the strategy’s historical performance across various market conditions to assess its robustness and identify optimal parameter settings.

Forward Testing: Deploy the strategy in a demo account to validate its real-time performance, ensuring it aligns with live market dynamics before risking capital.

Ongoing Monitoring: Continuously track trade outcomes, analyze performance metrics, and refine parameters to adapt to evolving market conditions.

Additionally, traders should consider market-specific factors, such as liquidity and volatility, when applying the strategy. For instance, highly liquid markets like forex may require tighter ATR multipliers, while less liquid markets like small-cap stocks may benefit from wider stop losses.

=====

Conclusion

The EMA 12/26 With ATR Volatility Stoploss strategy is a sophisticated, systematic trading framework that blends trend-following precision with disciplined risk management. By leveraging EMA crossovers for signal generation, ATR-based stop losses for volatility adjustment, and dynamic position sizing for risk control, it offers a balanced approach to capturing market trends while safeguarding capital. Its flexibility—evident in customizable parameters and dual profit management modes—makes it suitable for traders with varying risk appetites and objectives. However, its limitations, such as susceptibility to false signals and signal lag, necessitate thorough testing and prudent application. Through rigorous backtesting, forward testing, and continuous refinement, traders can harness this strategy to achieve consistent, risk-adjusted returns in trending markets, establishing it as a valuable tool in the arsenal of systematic trading.

Donchian Breakout Strategy📈 Donchian Breakout Strategy (Inspired by Way of the Turtle)

This strategy is a modern adaptation of the legendary Turtle Trading system as taught in Way of the Turtle by Curtis Faith — re-engineered for the crypto market’s volatility, 24/7 nature, and frequent fakeouts.

⸻

🐢 Original Inspiration

The original Turtle system, created by Richard Dennis and William Eckhardt, used:

• Breakouts of Donchian Channels (20-day for entry, 10-day for exit)

• Volatility-based position sizing using ATR (N)

• Simple rules, big trend exposure, and pyramiding to grow winners

It was built for futures and commodities, trading daily bars, assuming stable trading hours and regulated markets.

⸻

🚀 What’s Different in This Strategy?

✅ Optimized for Crypto

• Adapts to constant volatility and price manipulation common in crypto

• Adds commission modeling for realistic results (0.045% default)

✅ Improved Entry Filtering

• Uses EMA filter to align with trend direction

• Adds RSI momentum check to avoid early or weak breakouts

• Optional volatility and volume filters to reduce false signals

✅ Smarter Exits

• ATR-based volatility stop loss, not just Donchian reversal

• Avoids pyramiding to reduce risk from sudden reversals

✅ Backtest-Friendly

• Default backtest window starts from 2025-01-01

• Fully configurable: long/short toggle, filter control, stop loss multiplier

⸻

🧪 Use Case

• Best on trending coins with strong directional moves

• Avoids chop via filters, preserving capital

• Can be tuned for aggressive or conservative setups with just a few tweaks

Qullamaggie [Modified] | FractalystWhat's the purpose of this strategy?

The strategy aims to identify high-probability breakout setups in trending markets, inspired by Kristjan "Qullamaggie" Kullamägi’s approach.

It focuses on capturing explosive price moves after periods of consolidation, using technical criteria like moving averages, breakouts, trailing stop-loss and momentum confirmation.

Ideal for swing traders seeking to ride strong trends while managing risk.

----

How does the strategy work?

The strategy follows a systematic process to capture high-momentum breakouts:

Pre-Breakout Criteria:

Prior Price Surge: Identifies stocks that have rallied 30-100%+ in recent month(s), signaling strong underlying momentum (per Qullamaggie’s volatility expansion principles).

Consolidation Phase: Looks for a tightening price range (e.g., flag, pennant, or tight base), indicating a potential "coiling" before continuation.

Trend Confirmation: Uses moving averages (e.g., 20/50/200 EMA) to ensure the stock is trading above key averages on the daily chart, confirming an uptrend.

Price Break: Enters when price clears the consolidation high with conviction.

Risk Management:

Initial Stop Loss: Placed below the consolidation low or a recent swing point to limit downside.

Break-Even Adjustment: Moves stop loss to breakeven once the trade reaches 1.5x risk-to-reward (RR), securing a "free trade" while letting winners run.

Trailing Stop (Unique Edge):

Market Structure Trailing: Instead of trailing via moving averages, the stop is dynamically adjusted using structural invalidation level. This adapts to price action, allowing the trade to stay open during volatile retracements while locking in gains as new structure forms.

Why This Matters: Most strategies use rigid trailing stops (e.g., below the 10EMA), which often exit prematurely in choppy markets. By trailing based on structure, this strategy avoids "noise" and captures larger trends, directly boosting overall returns.

----

What markets or timeframes is this suited for?

This is a long-only strategy designed for trending markets, and it performs best in:

Markets: Stocks (especially high-growth, liquid equities), cryptocurrencies (major pairs with strong volatility), commodities (e.g., oil, gold), and futures (index/commodity futures).

Timeframes: Primarily daily charts for swing trades (1-30 day holds), though weekly charts can help confirm broader trends.

Key Advantage: The TradingView script allows instant backtesting with adjustable parameters

You can:

- Test historical performance across multiple markets to identify which assets align best with the strategy.

- Optimize settings (e.g., trailing stop sensitivity, moving averages etc.) to match a market’s volatility profile.

Build a diversified portfolio by filtering for markets that show consistent profitability in backtests.

For example, you might discover cryptos require tighter trailing stops due to volatility, while stocks thrive with wider structural stops. The script automates this analysis, letting you to trade confidently.

----

What indicators or tools does the strategy use?

The strategy combines customizable technical tools with strict anti-lookahead safeguards:

Core Indicators:

Moving Averages: Adjustable periods (e.g., 20/50/200 EMA or SMA) and timeframes (daily/weekly) to confirm trend alignment. Users can test combinations (e.g., 10EMA vs. 20EMA) to optimize for specific markets.

Breakout Parameters:

Consolidation Length: Adjustable window to define the "tightness" of the pre-breakout pattern.

Entry Models: Flexible entry logics (Breakouts and fractals)

Anti-Lookahead Design:

All calculations (e.g., moving averages, consolidation ranges, volume averages) use only closed/confirmed data available at the time of the signal.

----

How do I manage risk with this strategy?

The strategy prioritizes customizable risk controls to align with your trading style and account size:

User-Defined Risk Inputs:

Risk Per Trade: Set a % of Equity (e.g., 1-2%) to determine position size. The strategy auto-calculates shares/contracts to match your selected risk per trade.

Flexibility: Choose between fixed risk or equity-based scaling.

The script adjusts position sizing dynamically based on your selection.

Pyramiding Feature:

Customizable Entries: Adjust the number of pyramiding trades allowed (e.g., 1-3 additional positions) in the strategy settings. Each new entry is triggered only if the prior trade hits its 1.5x RR target and the trend remains intact.

Risk-Scaled Additions: New positions use profits from prior trades, compounding gains without increasing initial risk.

Risk-Free Trade Mechanic:

Once a trade reaches 1.5x RR, the stop loss is moved to breakeven, eliminating downside risk.

The strategy then opens a new position (if pyramiding is enabled) using a portion of the locked-in profit. This "snowballs" winners while keeping total capital exposure stable.

Impact on Net Profit & Drawdown:

Net Profit Boost: Pyramiding lets you ride multi-leg trends aggressively. For example, a 100% runner could generate 2-3x more profit vs. a single-entry approach.

Controlled Drawdowns: Since new positions are funded by profits (not initial capital), max drawdown stays anchored to your original risk per trade (e.g., 1-2% of account). Even if later entries fail, the breakeven stop on prior trades protects overall equity.

Why This Works: Most strategies either over-leverage (increasing drawdowns) or exit too early. By recycling profits into new positions only after securing risk-free capital, this approach mimics hedge fund "scaling in" tactics while staying retail-trader friendly.

----

How does the strategy identify market structure for its trailing stoploss?

The strategy identifies market structure by utilizing an efficient logic with for loops to pinpoint the first swing candle that features a pivot of 2. This marks the beginning of the break of structure, where the market's previous trend or pattern is considered invalidated or changed.

----

What are the underlying calculations?

The underlying calculations involve:

Identifying Swing Points: The strategy looks for swing highs (marked with blue Xs) and swing lows (marked with red Xs). A swing high is identified when a candle's high is higher than the highs of the candles before and after it. Conversely, a swing low is when a candle's low is lower than the lows of the candles before and after it.

Break of Structure (BOS):

Bullish BOS: This occurs when the price breaks above the swing high level of the previous structure, indicating a potential shift to a bullish trend.

Bearish BOS: This happens when the price breaks below the swing low level of the previous structure, signaling a potential shift to a bearish trend.

Structural Liquidity and Invalidation:

Structural Liquidity: After a break of structure, liquidity levels are updated to the first swing high in a bullish BOS or the first swing low in a bearish BOS.

Structural Invalidation: If the price moves back to the level of the first swing low before the bullish BOS or the first swing high before the bearish BOS, it invalidates the break of structure, suggesting a potential reversal or continuation of the previous trend.

This method provides users with a technical approach to filter market regimes, offering an advantage by minimizing the risk of overfitting to historical data, which is often a concern with traditional indicators like moving averages.

By focusing on identifying pivotal swing points and the subsequent breaks of structure, the strategy maintains a balance between sensitivity to market changes and robustness against historical data anomalies, ensuring a more adaptable and potentially more reliable market analysis tool.

----

What entry criteria are used in this script?

The script uses two entry models for trading decisions: BreakOut and Fractal.

Underlying Calculations:

Breakout: The script records the most recent swing high by storing it in a variable. When the price closes above this recorded level, and all other predefined conditions are satisfied, the script triggers a breakout entry. This approach is considered conservative because it waits for the price to confirm a breakout above the previous high before entering a trade. As shown in the image, as soon as the price closes above the new candle (first tick), the long entry gets taken. The stop-loss is initially set and then moved to break-even once the price moves in favor of the trade.

Fractal: This method involves identifying a swing low with a period of 2, which means it looks for a low point where the price is lower than the two candles before and after it. Once this pattern is detected, the script executes the trade. This is an aggressive approach since it doesn't wait for further price confirmation. In the image, this is represented by the 'Fractal 2' label where the script identifies and acts on the swing low pattern.

----

What type of stop-loss identification method are used in this strategy?

This strategy employs two types of stop-loss methods: Initial Stop-loss and Trailing Stop-Loss.

Underlying Calculations:

Initial Stop-loss:

ATR Based: The strategy uses the Average True Range (ATR) to set an initial stop-loss, which helps in accounting for market volatility without predicting price direction.

Calculation:

- First, the True Range (TR) is calculated for each period, which is the greatest of:

- Current Period High - Current Period Low

- Absolute Value of Current Period High - Previous Period Close

- Absolute Value of Current Period Low - Previous Period Close

- The ATR is then the moving average of these TR values over a specified period, typically 14 periods by default. This ATR value can be used to set the stop-loss at a distance from the entry price that reflects the current market volatility.

Swing Low Based:

For this method, the stop-loss is set based on the most recent swing low identified in the market structure analysis. This approach uses the lowest point of the recent price action as a reference for setting the stop-loss.

Trailing Stop-Loss:

The strategy uses structural liquidity and structural invalidation levels across multiple timeframes to adjust the stop-loss once the trade is profitable. This method involves:

Detecting Structural Liquidity: After a break of structure, the liquidity levels are updated to the first swing high in a bullish scenario or the first swing low in a bearish scenario. These levels serve as potential areas where the price might find support or resistance, allowing the stop-loss to trail the price movement.

Detecting Structural Invalidation: If the price returns to the level of the first swing low before a bullish break of structure or the first swing high before a bearish break of structure, it suggests the trend might be reversing or invalidating, prompting the adjustment of the stop-loss to lock in profits or minimize losses.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop. The ATR-based stop-loss adapts to the current market conditions by considering the volatility, ensuring that the stop-loss is not too tight during volatile periods, which could lead to premature exits, nor too loose during calm markets, which might result in larger losses. Similarly, the swing low based stop-loss provides a logical exit point if the market structure changes unfavorably.