HDFC Bank Q1 FY26: Will earnings mirror balance sheet strength, going forward?

Highlights

- Loan growth muted but deposit growth solid

- The CD ratio improves

- Margin declined further, operating expenses contain

- Asset quality pristine, excess provisions comforting

- Valuation reasonable

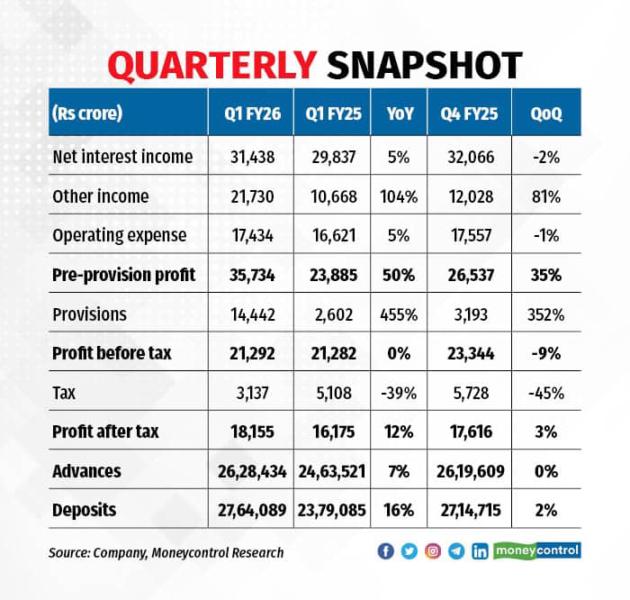

HDFC Bank (CMP: Rs 1,957; Mcap: Rs 15,00,000 crore; Rating: Overweight) has reported a profit of Rs 18,155 crore for Q1 FY26, marking a 12 percent year-on-year (YoY) increase. However, the YoY comparison is somewhat skewed due to a couple of one-off items recorded during the quarter.

The profit was supported by the stake sale in HDB Financial, which boosted the bank’s non-interest income. Gains from this transaction totalled Rs 9,130 crore, which the bank prudently used to create Rs 9,000 crore in floating provisions and Rs 1,700 crore in contingent provisions. The floating provisions are not tied to any specific asset class or anticipated risk but serve as a counter-cyclical buffer, enhancing the balance sheet’s resilience. Strengthening the balance sheet has remained a key focus for HDFC Bank following its merger.

On the operational front, the bank’s loan growth was measured and came in below the industry average in Q1 FY26. However, it posted robust deposit growth and gained market share. The strategy of slower loan growth coupled with accelerated deposit mobilisation aligns with the bank’s near-term goal of reducing its credit-to-deposit (CD) ratio.

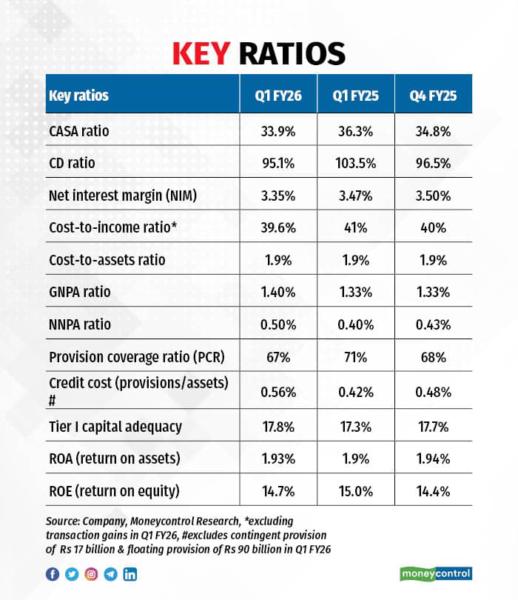

One of the key metrics to monitor for HDFC Bank is its net interest margin (NIM), which declined as expected, reflecting faster repricing of assets (loans) compared to liabilities (deposits). Asset quality remained stable overall, with a slight seasonal impact.

Despite its continued focus on balance sheet consolidation, HDFC Bank delivered strong profitability, posting a healthy ROA (return on assets) of 1.9 percent in Q1 FY26. Coupled with its reasonable valuation, the bank presents an attractive investment opportunity at current levels.

What would trigger the valuation re-rating?

The Street continues to keep watch on two key variables for HDFC Bank — advances growth and net interest margin (NIM), both of which were impacted post the merger. The management reiterated its guidance that the bank aims to match industry-level loan growth in FY26 and outpace it starting FY27. To meet this target, loan growth will need to accelerate meaningfully in the coming quarters, with the management expecting a pick-up in H2 FY26.

HDFC Bank’s NIM stood at 3.35. percent in Q1 FY26, significantly lower than the pre-merger level of 4.1 percent.

The bank expects the margin trajectory to remain challenging, particularly with the possibility of an additional 25 basis points cut in the repo rate. However, HDFC Bank is well positioned to benefit from improved system liquidity and a softening interest rate cycle. This is largely due to its higher share of borrowings in the funding mix post-merger. Although borrowings have come down from a peak of 21 percent of total liabilities in December 2023, they still account for 13 percent as of June 2025 — well above the pre-merger level of 8 percent and also higher than peers.

Margins may remain under pressure in Q2 FY26 but are expected to receive support in the second half of the year (H2 FY26), aided by the phased CRR reduction likely to take effect from October 2025. Additionally, margins should improve over the medium term as HDFC Bank gradually replaces high-cost market borrowings — carried over from the merger — with lower-cost deposits.

Overall, stronger advances growth, improving margins, and stable asset quality are likely to drive healthy earnings growth in FY26, paving the way for a potential re-rating of the stock.

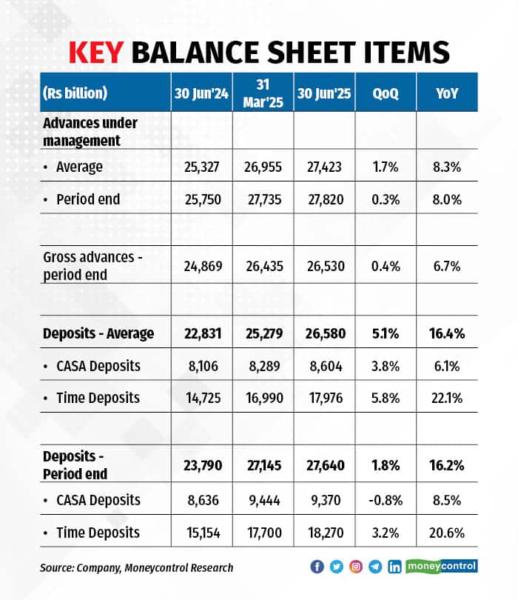

Loan growth remained subdued, while deposit growth was strong.

HDFC Bank’s gross advances at the end of June ’25 increased by 2.7 percent YoY. However, grossing up for transfers through inter-bank participation certificates, bills rediscounted and securitisation / assignment, advances under management, on an average basis, grew by 8 percent compared to June ’24.

Retail loans grew by 8 percent, small and mid-market enterprises loans grew by 17.1 percent, and corporate and other wholesale loans were lower by 1.7 percent. Within retail, the unsecured loan (personal loans and credit card) grew by 9 percent YoY in Q1 FY26.

While loan growth fell below industry growth, HDFC Bank’s deposit growth remained strong, growing by 16 percent YoY mainly driven by time deposits.

The CD ratio improves

Following the merger, HDFC Bank’s CD ratio reached a high of 110 percent at the end of December’23. It has come down since then. In Q1 FY26, the bank saw a further improvement in its CD ratio that declined to 95 percent, thanks to the strong deposit growth and slower loan growth. The LCR (liquidity coverage ratio) at 125 percent at December ’24 end is at a comfortable level.

Margins decline, asset quality benign

HDFC Bank’s margin contracted to 3.35 percent in Q1 FY26, a reduction of 15 bps compared with Mar’25 end quarter.

Asset quality saw a slight dip due to slippages in the agricultural loan portfolio, a trend typically observed in the first and third quarters in line with crop cycles. However, excluding agri-related NPAs, the bank's overall GNPA and NNPA ratios remained stable.

HDFC Bank’s credit cost rose slightly but stayed at a very low level. The excess provisions (floating and contingent) now stand at 1.4 percent of the loan book, offering strong comfort. Combined with a healthy provision coverage ratio (PCR), this is expected to keep future credit costs well contained.

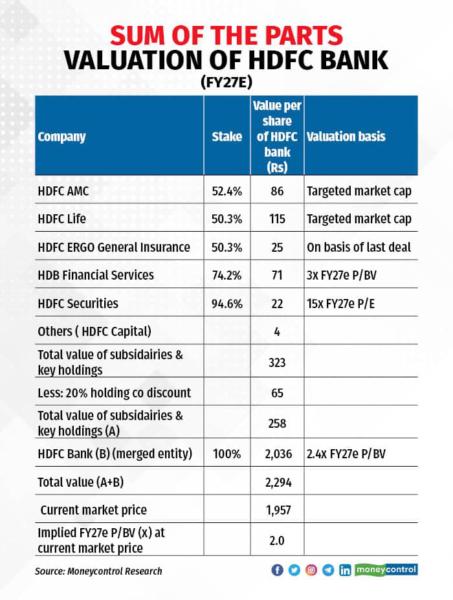

Valuation is reasonable

In terms of valuation, HDFC Bank is currently trading at 2 times the core book value estimated for FY27 after adjusting for the valuation of subsidiaries. The valuation is reasonable given an ROA (return on assets) of 1.9 percent and an ROE of 14.7 percent in Q1 FY26.

Given the healthy return ratios, reasonable valuation, potential improvement in earnings growth, and improved liquidity situation, investors should accumulate the stock at the current level for the long term.For more research articles, visit our Moneycontrol Research page