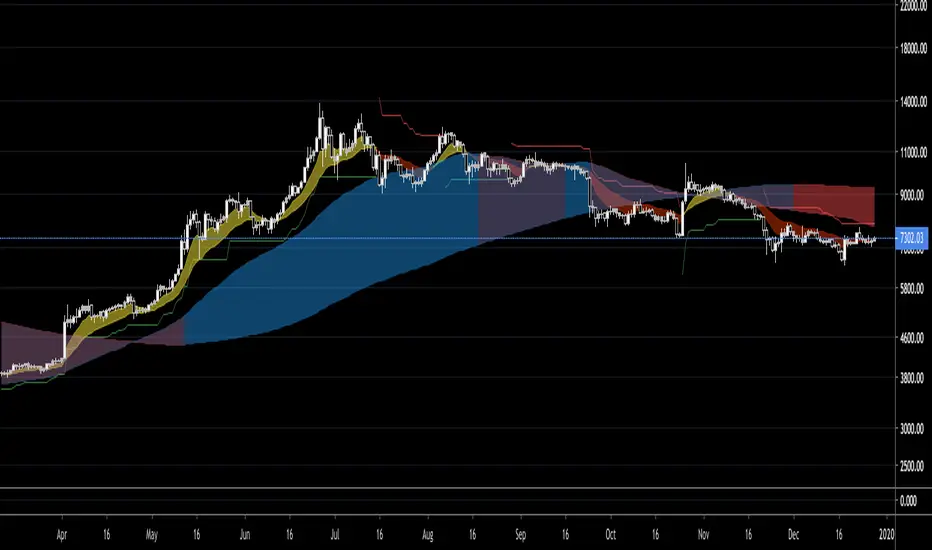

CloudRest ATR based cloudThis is an indicator I have been working on for the past 2 years, developed specifically for cryptocurrency.

It is primarily a trend following indicator with great success and it performs the best in 4hrs to the weekly chart.

There are two components of this indicator.

The baseline from Ichimoku cloud and volatility stop .

baseline period = 26

volatility stop = 1.5ATR, 3

You can view this as the main component of a trend following system but you will need other confirmation indicators to confirm your entry.

Feel free to modify the script for your own system.

Feel free to follow me on twitter @Lancelot_Auger

I will be posting more content in the future, stay tuned.

And lastly,

Free hong kong, the revolution of our time!

Penunjuk Pine Script®