Zero Lag MACD + Kijun-sen + EOM StrategyThis strategy offers a robust approach to identifying high-probability trading opportunities in the fast-paced cryptocurrency markets, particularly on lower timeframes (e.g., 5-minute). It leverages the synergistic power of three distinct indicators to confirm entries, ensuring a disciplined approach to risk management.

Key Components:

Zero Lag MACD Enhanced Version 1.2: This core momentum indicator is used to identify precise shifts in trend and momentum, offering reduced lag compared to traditional MACD. Entry signals are filtered based on the histogram's position (below for buys, above for sells) to enhance signal reliability.

Kijun-sen (Ichimoku Cloud): Acting as a dynamic support/resistance and trend filter, the Kijun-sen line confirms the prevailing market direction. Long entries are confirmed when price is above Kijun-sen, and short entries when price is below.

Ease of Movement (EoM): This volume-based oscillator provides crucial confirmation of price movements by measuring the ease with which price changes. Positive EoM confirms buying pressure, while negative confirms selling pressure, adding an essential layer of validation to trade setups.

How it Works:

The strategy generates entry signals only when all three indicators align simultaneously:

For Long Entries: A Zero Lag MACD buy signal (crossover below histogram) must coincide with price trading above the Kijun-sen, and the Ease of Movement indicator being above its zero line.

For Short Entries: A Zero Lag MACD sell signal (crossover above histogram) must coincide with price trading below the Kijun-sen, and the Ease of Movement indicator being below its zero line.

Entries are executed at the open of the candle immediately following the signal confirmation.

Risk Management:

Disciplined risk management is paramount to this strategy:

Dynamic Stop-Loss: An Average True Range (ATR) based stop-loss is implemented, set at 2.5 times the current ATR. This adapts the stop-loss distance to market volatility, ensuring sensible risk sizing.

Fixed Take-Profit: A consistent Risk-to-Reward (R:R) ratio of 1:1.2 is applied for all trades, promoting stable profit realization.

Customization & Optimization:

The strategy is built with fully customizable input parameters for each indicator (MACD lengths, Kijun-sen period, ATR period, ATR multiplier, and Risk-to-Reward ratio). This allows users to fine-tune the strategy for different assets, timeframes, and market conditions, facilitating robust backtesting and optimization.

Disclaimer: Trading involves substantial risk and is not suitable for all investors. Past performance is not indicative of future results. This strategy is provided for educational and informational purposes only. Always use proper risk management and conduct your own due diligence.

Centered Oscillators

Kaufman Trend Strategy# ✅ Kaufman Trend Strategy – Full Description (Script Publishing Version)

**Kaufman Trend Strategy** is a dynamic trend-following strategy based on Kaufman Filter theory.

It detects real-time trend momentum, reduces noise, and aims to enhance entry accuracy while optimizing risk.

⚠️ _For educational and research purposes only. Past performance does not guarantee future results._

---

## 🎯 Strategy Objective

- Smooth price noise using Kaufman Filter smoothing

- Detect the strength and direction of trends with a normalized oscillator

- Manage profits using multi-stage take-profits and adaptive ATR stop-loss logic

---

## ✨ Key Features

- **Kaufman Filter Trend Detection**

Extracts directional signal using a state space model.

- **Multi-Stage Profit-Taking**

Automatically takes partial profits based on color changes and zero-cross events.

- **ATR-Based Volatility Stops**

Stops adjust based on swing highs/lows and current market volatility.

---

## 📊 Entry & Exit Logic

**Long Entry**

- `trend_strength ≥ 60`

- Green trend signal

- Price above the Kaufman average

**Short Entry**

- `trend_strength ≤ -60`

- Red trend signal

- Price below the Kaufman average

**Exit (Long/Short)**

- Blue trend color → TP1 (50%)

- Oscillator crosses 0 → TP2 (25%)

- Trend weakens → Final exit (25%)

- ATR + swing-based stop loss

---

## 💰 Risk Management

- Initial capital: `$3,000`

- Order size: `$100` per trade (realistic, low-risk sizing)

- Commission: `0.002%`

- Slippage: `2 ticks`

- Pyramiding: `1` max position

- Estimated risk/trade: `~0.1–0.5%` of equity

> ⚠️ _No trade risks more than 5% of equity. This strategy follows TradingView script publishing rules._

---

## ⚙️ Default Parameters

- **1st Take Profit**: 50%

- **2nd Take Profit**: 25%

- **Final Exit**: 25%

- **ATR Period**: 14

- **Swing Lookback**: 10

- **Entry Threshold**: ±60

- **Exit Threshold**: ±40

---

## 📅 Backtest Summary

- **Symbol**: USD/JPY

- **Timeframe**: 1H

- **Date Range**: Jan 3, 2022 – Jun 4, 2025

- **Trades**: 924

- **Win Rate**: 41.67%

- **Profit Factor**: 1.108

- **Net Profit**: +$1,659.29 (+54.56%)

- **Max Drawdown**: -$1,419.73 (-31.87%)

---

## ✅ Summary

This strategy uses Kaufman filtering to detect market direction with reduced lag and increased smoothness.

It’s built with visual clarity and strong trade management, making it practical for both beginners and advanced users.

---

## 📌 Disclaimer

This script is for educational and informational purposes only and should not be considered financial advice.

Use with proper risk controls and always test in a demo environment before live trading.

MACD + RSI + EMA + BB + ATR Day Trading StrategyEntry Conditions and Signals

The strategy implements a multi-layered filtering approach to entry conditions, requiring alignment across technical indicators, timeframes, and market conditions .

Long Entry Requirements

Trend Filter: Fast EMA (9) must be above Slow EMA (21), price must be above Fast EMA, and higher timeframe must confirm uptrend

MACD Signal: MACD line crosses above signal line, indicating increasing bullish momentum

RSI Condition: RSI below 70 (not overbought) but above 40 (showing momentum)

Volume & Volatility: Current volume exceeds 1.2x 20-period average and ATR shows sufficient market movement

Time Filter: Trading occurs during optimal hours (9:30-11:30 AM ET) when market volatility is typically highest

Exit Strategies

The strategy employs multiple exit mechanisms to adapt to changing market conditions and protect profits :

Stop Loss Management

Initial Stop: Placed at 2.0x ATR from entry price, adapting to current market volatility

Trailing Stop: 1.5x ATR trailing stop that moves up (for longs) or down (for shorts) as price moves favorably

Time-Based Exits: All positions closed by end of trading day (4:00 PM ET) to avoid overnight risk

Best Practices for Implementation

Settings

Chart Setup: 5-minute timeframe for execution with 15-minute chart for trend confirmation

Session Times: Focus on 9:30-11:30 AM ET trading for highest volatility and opportunity

Reversal Trap Sniper – Verified VersionReversal Trap Sniper

Overview

Reversal Trap Sniper is a counterintuitive momentum-following strategy that identifies "reversal traps"—situations where traders expect a market reversal based on RSI, but the price continues trending. By detecting these failed reversal signals, the strategy enters trades in the trend direction, often catching strong follow-through moves.

How It Works

The system monitors the Relative Strength Index (RSI). When RSI moves above the overbought level (e.g., 70) and then drops back below it, many traders interpret this as a sell signal.

However, this strategy treats such moves with caution. If the RSI pulls back below the overbought threshold but the price continues to rise, the system considers it a "reversal trap"—a fakeout.

In such cases, instead of going short, the strategy enters a long position, assuming that the trend is still valid and those betting on a reversal may fuel a breakout.

Similarly, if RSI rises above the oversold level from below, but price continues falling, a short trade is triggered.

Entries are followed by ATR-based stop-loss and dynamic take-profit (2× risk), with a fallback time-based exit after 30 bars.

Key Features

- Detects failed RSI-based reversals ("traps")

- Follows momentum after the trap is triggered

- Uses ATR for dynamic stop-loss and take-profit

- Auto-exit after a fixed bar count (30 bars)

- Visual markers on chart for transparency

- Realistic trading assumptions: 0.05% commission, slippage, and capped pyramiding

Parameter Explanation

RSI Length (14): Standard RSI calculation period

Overbought/Oversold Levels (70/30): Common thresholds used by many traders

ATR Length (14): Used to define stop-loss and target dynamically

Risk-Reward Ratio (2.0): Take-profit is set at 2× the stop-loss distance

Max Holding Bars (30): Ensures trades don’t remain open indefinitely

Pyramiding (10): Allows scaling into trades, simulating real-world strategy stacking

Originality Note

This strategy inverts traditional RSI logic. Instead of treating overbought/oversold conditions as signals for reversal, it waits for those signals to fail. Only after such failures, confirmed by continued price action in the same direction, does the system enter trades. This logic is based on the behavioral observation that failed reversal signals often trigger stronger trend continuation—making this strategy uniquely positioned to exploit trap scenarios.

Disclaimer

This script is for educational and research purposes only. Trading involves risk, and past performance does not guarantee future results. Always test thoroughly before applying with live capital.

Volatility Pulse with Dynamic ExitVolatility Pulse with Dynamic Exit

Overview

This strategy, Volatility Pulse with Dynamic Exit, is designed to capture impulsive price moves following volatility expansions, while ensuring risk is managed dynamically. It avoids trades during low-volatility periods and uses momentum confirmation to enter positions. Additionally, it features a time-based forced exit system to limit overexposure.

How It Works

A position is opened when the current ATR (Average True Range) significantly exceeds its 20-period average, signaling a volatility expansion.

To confirm the move is directional and not random noise, the strategy checks for momentum: the close must be above/below the close of 20 bars ago.

Low volatility zones are filtered out to avoid chop and poor trade entries.

Upon entry, a dynamic stop-loss is set at 1x ATR, while take-profit is set at 2x ATR, offering a 2:1 reward-to-risk ratio.

If the position remains open for more than 42 bars, it is forcefully closed, even if targets are not hit. This prevents long-lasting, stagnant trades.

Key Features

✅ Volatility-based breakout detection

✅ Momentum confirmation filter

✅ Dynamic stop-loss and take-profit based on real-time ATR

✅ Time-based forced exit (42 bars max holding)

✅ Low-volatility environment filter

✅ Realistic settings with 0.05% commission and slippage included

Parameters Explanation

ATR Length (14): Captures recent volatility over ~2 weeks (14 candles).

Momentum Lookback (20): Ensures meaningful price move confirmation.

Volatility Expansion Threshold (0.5x): Strategy activates only when ATR is at least 50% above its average.

Minimum ATR Filter (1.0x): Avoids entries in tight, compressed market ranges.

Max Holding (42 bars): Trades are closed after 42 bars if no exit signal is triggered.

Risk-Reward (2.0x): Aiming for 2x ATR as profit for every 1x ATR risk.

Originality Note

While volatility and momentum have been used separately in many strategies, this script combines both with a time-based dynamic exit system. This exit rule, combined with an ATR-based filter to exclude low-activity periods, gives the system a practical edge in real-world use. It avoids classic rehashes and integrates real trading constraints for better applicability.

Disclaimer

This is a research-focused trading strategy meant for backtesting and educational purposes. Always use proper risk management and perform due diligence before applying to real funds.

EMA Pullback Speed Strategy 📌 **Overview**

The **EMA Pullback Speed Strategy** is a trend-following approach that combines **price momentum** and **Exponential Moving Averages (EMA)**.

It aims to identify high-probability entry points during brief pullbacks within ongoing uptrends or downtrends.

The strategy evaluates **speed of price movement**, **relative position to dynamic EMA**, and **candlestick patterns** to determine ideal timing for entries.

One of the key concepts is checking whether the price has **“not pulled back too much”**, helping focus only on situations where the trend is likely to continue.

⚠️ This strategy is designed for educational and research purposes only. It does not guarantee future profits.

🧭 **Purpose**

This strategy addresses the common issue of **"jumping in too late during trends and taking unnecessary losses."**

By waiting for a healthy pullback and confirming signs of **trend resumption**, traders can enter with greater confidence and reduce false entries.

🎯 **Strategy Objectives**

* Enter in the direction of the prevailing trend to increase win rate

* Filter out false signals using pullback depth, speed, and candlestick confirmations

* Predefine Take-Profit (TP) and Stop-Loss (SL) levels for safer, rule-based trading

✨ **Key Features**

* **Dynamic EMA**: Reacts faster when price moves quickly, slower when market is calm – adapting to current momentum

* **Pullback Filter**: Avoids trades when price pulls back too far (e.g., more than 5%), indicating a trend may be weakening

* **Speed Check**: Measures how strongly the price returns to the trend using candlestick body speed (open-to-close range in ticks)

📊 **Trading Rules**

**■ Long Entry Conditions:**

* Current price is above the dynamic EMA (indicating uptrend)

* Price has pulled back toward the EMA (a "buy the dip" situation)

* Pullback depth is within the threshold (not excessive)

* Candlesticks show consecutive bullish closes and break the previous high

* Price speed is strong (positive movement with momentum)

**■ Short Entry Conditions:**

* Current price is below the dynamic EMA (indicating downtrend)

* Price has pulled back up toward the EMA (a "sell the rally" setup)

* Pullback is within range (not too deep)

* Candlesticks show consecutive bearish closes and break the previous low

* Price speed is negative (downward momentum confirmed)

**■ Exit Conditions (TP/SL):**

* **Take-Profit (TP):** Fixed 1.5% target above/below entry price

* **Stop-Loss (SL):** Based on recent price volatility, calculated using ATR × 4

💰 **Risk Management Parameters**

* Symbol & Timeframe: BTCUSD on 1-hour chart (H1)

* Test Capital: \$3000 (simulated account)

* Commission: 0.02%

* Slippage: 2 ticks (minimal execution lag)

* Max risk per trade: 5% of account balance

* Backtest Period: Aug 30, 2023 – May 9, 2025

* Profit Factor (PF): 1.965 (Net profit ÷ Net loss, including spreads & fees)

⚙️ **Trading Parameters & Indicator Settings**

* Maximum EMA Length: 50

* Accelerator Multiplier: 3.0

* Pullback Threshold: 5.0%

* ATR Period: 14

* ATR Multiplier (SL distance): 4.0

* Fixed TP: 1.5%

* Short-term EMA: 21

* Long-term EMA: 50

* Long Speed Threshold: ≥ 1000.0 (ticks)

* Short Speed Threshold: ≤ -1000.0 (ticks)

⚠️Adjustments are based on BTCUSD.

⚠️Forex and other currency pairs require separate adjustments.

🔧 **Strategy Improvements & Uniqueness**

Unlike basic moving average crossovers or RSI triggers, this strategy emphasizes **"momentum-supported pullbacks"**.

By combining dynamic EMA, speed checks, and candlestick signals, it captures trades **as if surfing the wave of a trend.**

Its built-in filters help **avoid overextended pullbacks**, which often signal the trend is ending – making it more robust than traditional trend-following systems.

✅ **Summary**

The **EMA Pullback Speed Strategy** is easy to understand, rule-based, and highly reproducible – ideal for both beginners and intermediate traders.

Because it shows **clear visual entry/exit points** on the chart, it’s also a great tool for practicing discretionary trading decisions.

⚠️ Past performance is not a guarantee of future results.

Always respect your Stop-Loss levels and manage your position size according to your risk tolerance.

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Express Generator StrategyExpress Generator Strategy

Pine Script™ v6

The Express Generator Strategy is an algorithmic trading system that harnesses confluence from multiple technical indicators to optimize trade entries and dynamic risk management. Developed in Pine Script v6, it is designed to operate within a user-defined backtesting period—ensuring that trades are executed only during chosen historical windows for targeted analysis.

How It Works:

- Entry Conditions:

The strategy relies on a dual confirmation approach:- A moving average crossover system where a fast (default 9-period SMA) crossing above or below a slower (default 21-period SMA) average signals a potential trend reversal.

- MACD confirmation; trades are only initiated when the MACD line crosses its signal line in the direction of the moving average signal.

- An RSI filter refines these signals by preventing entries when the market might be overextended—ensuring that long entries only occur when the RSI is below an overbought level (default 70) and short entries when above an oversold level (default 30).

- Risk Management & Dynamic Position Sizing:

The strategy takes a calculated approach to risk by enabling the adjustment of position sizes using:- A pre-defined percentage of equity risk per trade (default 1%, adjustable between 0.5% to 3%).

- A stop-loss set in pips (default 100 pips, with customizable ranges), which is then adjusted by market volatility measured through the ATR.

- Trailing stops (default 50 pips) to help protect profits as the market moves favorably.

This combination of volatility-adjusted risk and equity-based position sizing aims to harmonize trade exposure with prevailing market conditions.

- Backtest Period Flexibility:

Users can define the start and end dates for backtesting (e.g., January 1, 2020 to December 31, 2025). This ensures that the strategy only opens trades within the intended analysis window. Moreover, if the strategy is still holding a position outside this period, it automatically closes all trades to prevent unwanted exposure.

- Visual Insights:

For clarity, the strategy plots the fast (blue) and slow (red) moving averages directly on the chart, allowing for visual confirmation of crossovers and trend shifts.

By integrating multiple technical indicators with robust risk management and adaptable position sizing, the Express Generator Strategy provides a comprehensive framework for capturing trending moves while prudently managing downside risk. It’s ideally suited for traders looking to combine systematic entries with a disciplined and dynamic risk approach.

Momentum + Keltner Stochastic Combo)The Momentum-Keltner-Stochastic Combination Strategy: A Technical Analysis and Empirical Validation

This study presents an advanced algorithmic trading strategy that implements a hybrid approach between momentum-based price dynamics and relative positioning within a volatility-adjusted Keltner Channel framework. The strategy utilizes an innovative "Keltner Stochastic" concept as its primary decision-making factor for market entries and exits, while implementing a dynamic capital allocation model with risk-based stop-loss mechanisms. Empirical testing demonstrates the strategy's potential for generating alpha in various market conditions through the combination of trend-following momentum principles and mean-reversion elements within defined volatility thresholds.

1. Introduction

Financial market trading increasingly relies on the integration of various technical indicators for identifying optimal trading opportunities (Lo et al., 2000). While individual indicators are often compromised by market noise, combinations of complementary approaches have shown superior performance in detecting significant market movements (Murphy, 1999; Kaufman, 2013). This research introduces a novel algorithmic strategy that synthesizes momentum principles with volatility-adjusted envelope analysis through Keltner Channels.

2. Theoretical Foundation

2.1 Momentum Component

The momentum component of the strategy builds upon the seminal work of Jegadeesh and Titman (1993), who demonstrated that stocks which performed well (poorly) over a 3 to 12-month period continue to perform well (poorly) over subsequent months. As Moskowitz et al. (2012) further established, this time-series momentum effect persists across various asset classes and time frames. The present strategy implements a short-term momentum lookback period (7 bars) to identify the prevailing price direction, consistent with findings by Chan et al. (2000) that shorter-term momentum signals can be effective in algorithmic trading systems.

2.2 Keltner Channels

Keltner Channels, as formalized by Chester Keltner (1960) and later modified by Linda Bradford Raschke, represent a volatility-based envelope system that plots bands at a specified distance from a central exponential moving average (Keltner, 1960; Raschke & Connors, 1996). Unlike traditional Bollinger Bands that use standard deviation, Keltner Channels typically employ Average True Range (ATR) to establish the bands' distance from the central line, providing a smoother volatility measure as established by Wilder (1978).

2.3 Stochastic Oscillator Principles

The strategy incorporates a modified stochastic oscillator approach, conceptually similar to Lane's Stochastic (Lane, 1984), but applied to a price's position within Keltner Channels rather than standard price ranges. This creates what we term "Keltner Stochastic," measuring the relative position of price within the volatility-adjusted channel as a percentage value.

3. Strategy Methodology

3.1 Entry and Exit Conditions

The strategy employs a contrarian approach within the channel framework:

Long Entry Condition:

Close price > Close price periods ago (momentum filter)

KeltnerStochastic < threshold (oversold within channel)

Short Entry Condition:

Close price < Close price periods ago (momentum filter)

KeltnerStochastic > threshold (overbought within channel)

Exit Conditions:

Exit long positions when KeltnerStochastic > threshold

Exit short positions when KeltnerStochastic < threshold

This methodology aligns with research by Brock et al. (1992) on the effectiveness of trading range breakouts with confirmation filters.

3.2 Risk Management

Stop-loss mechanisms are implemented using fixed price movements (1185 index points), providing definitive risk boundaries per trade. This approach is consistent with findings by Sweeney (1988) that fixed stop-loss systems can enhance risk-adjusted returns when properly calibrated.

3.3 Dynamic Position Sizing

The strategy implements an equity-based position sizing algorithm that increases or decreases contract size based on cumulative performance:

$ContractSize = \min(baseContracts + \lfloor\frac{\max(profitLoss, 0)}{equityStep}\rfloor - \lfloor\frac{|\min(profitLoss, 0)|}{equityStep}\rfloor, maxContracts)$

This adaptive approach follows modern portfolio theory principles (Markowitz, 1952) and Kelly criterion concepts (Kelly, 1956), scaling exposure proportionally to account equity.

4. Empirical Performance Analysis

Using historical data across multiple market regimes, the strategy demonstrates several key performance characteristics:

Enhanced performance during trending markets with moderate volatility

Reduced drawdowns during choppy market conditions through the dual-filter approach

Optimal performance when the threshold parameter is calibrated to market-specific characteristics (Pardo, 2008)

5. Strategy Limitations and Future Research

While effective in many market conditions, this strategy faces challenges during:

Rapid volatility expansion events where stop-loss mechanisms may be inadequate

Prolonged sideways markets with insufficient momentum

Markets with structural changes in volatility profiles

Future research should explore:

Adaptive threshold parameters based on regime detection

Integration with additional confirmatory indicators

Machine learning approaches to optimize parameter selection across different market environments (Cavalcante et al., 2016)

References

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. The Journal of Finance, 47(5), 1731-1764.

Cavalcante, R. C., Brasileiro, R. C., Souza, V. L., Nobrega, J. P., & Oliveira, A. L. (2016). Computational intelligence and financial markets: A survey and future directions. Expert Systems with Applications, 55, 194-211.

Chan, L. K. C., Jegadeesh, N., & Lakonishok, J. (2000). Momentum strategies. The Journal of Finance, 51(5), 1681-1713.

Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1), 65-91.

Kaufman, P. J. (2013). Trading systems and methods (5th ed.). John Wiley & Sons.

Kelly, J. L. (1956). A new interpretation of information rate. The Bell System Technical Journal, 35(4), 917-926.

Keltner, C. W. (1960). How to make money in commodities. The Keltner Statistical Service.

Lane, G. C. (1984). Lane's stochastics. Technical Analysis of Stocks & Commodities, 2(3), 87-90.

Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of technical analysis: Computational algorithms, statistical inference, and empirical implementation. The Journal of Finance, 55(4), 1705-1765.

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77-91.

Moskowitz, T. J., Ooi, Y. H., & Pedersen, L. H. (2012). Time series momentum. Journal of Financial Economics, 104(2), 228-250.

Murphy, J. J. (1999). Technical analysis of the financial markets: A comprehensive guide to trading methods and applications. New York Institute of Finance.

Pardo, R. (2008). The evaluation and optimization of trading strategies (2nd ed.). John Wiley & Sons.

Raschke, L. B., & Connors, L. A. (1996). Street smarts: High probability short-term trading strategies. M. Gordon Publishing Group.

Sweeney, R. J. (1988). Some new filter rule tests: Methods and results. Journal of Financial and Quantitative Analysis, 23(3), 285-300.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

BB Breakout + Momentum Squeeze [Strategy]This Strategy is Based on 3 free indicators

- Bollinger Bands Breakout Oscillator: Link

- TTM Squeeze Pro: Link

- Rolling ATR Bands: Link

Bollinger Bands Breakout Oscillator - This tool shows how strong a market trend is by measuring how often prices move outside their normal Bollinger bands range. It helps you see whether prices are strongly moving in one direction or just moving sideways. By looking at how much and how frequently prices push beyond their typical boundaries, you can identify which direction the market is heading over your selected time period.

TM Squeeze Pro - This is a custom version of the TTM Squeeze indicator.

It's designed to help traders spot consolidation phases in the market (when price is coiling or "squeezing") and to catch breakouts early when volatility returns. The logic is based on the relationship between Bollinger Bands and Keltner Channels, combined with a momentum oscillator to show direction and strength.

Rolling ATR Bands - This indicator combines volatility bands (ATR) with momentum and trend signals to show where the market might be breaking out, retesting, or trending. It's highly visual and helpful for traders looking to time entries/exits during trending or volatile moves.

Logic Of the Strategy:

We are going to use the Bollinger Bands Breakout to determine the direction of the market. Than check the Volatility of the price by looking at the TTM Squeeze indicator. And use the ATR Bands to determine dynamic Stop Losses and based on the calculate the Take Profit targets and quantity for each position dynamically.

For the Long Setup:

1. We need to see the that Bull Power (Green line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

For the Short Setup:

1. We need to see the that Bear Power (Red line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

Stop Loss is determined by the Lower ATR Band (for the Long entry) and Upper ATR Band (For the Short entry)

Take Profit is 1:1.5 risk reward ration, which means if the Stop loss is 1% the TP target will be 1.5%

Move stop Loss to Breakeven: If the price will go in the direction of the trade for at least half of the Risk Reward target then the stop will automatically be adjusted to the entry price. For Example: the Stop Loss is 1%, the price has move at least 0.5% in the direction of your trade and that will move the Stop Loss level to the Entry point.

You can Adjust the parameters for each indicator used in that script and also adjust the Risk and Money management block to see how the PnL will change.

MACD Volume Strategy (BBO + MACD State, Reversal Type)Overview

MACD Volume Strategy (BBO + MACD State, Reversal Type) is a momentum-based reversal system that combines MACD crossover logic with volume filtering to enhance signal accuracy and minimize noise. It aims to identify structural trend shifts and manage risk using predefined parameters.

※This strategy is for educational and research purposes only. All results are based on historical simulations and do not guarantee future performance.

Strategy Objectives

Identify early trend transitions with high probability

Filter entries using volume dynamics to validate momentum

Maintain continuous exposure using a reversal-style model

Apply a consistent 1:1.5 risk-to-reward ratio per trade

Key Features

Integrated MACD and volume oscillator filtering

Zero repainting (all signals confirmed on closed candles)

Automatic position flipping for seamless direction shifts

Stop-loss and take-profit based on recent structural highs/lows

Trading Rules

Long Entry Conditions

MACD crosses above the zero line (BBO Buy arrow)

Volume oscillator is positive (short EMA > long EMA)

MACD is above the signal line

Close any existing short and enter a new long

Short Entry Conditions

MACD crosses below the zero line (BBO Sell arrow)

Volume oscillator is positive

MACD is below the signal line

Close any existing long and enter a new short

Exit Rules

Take Profit (TP) = Entry ± (risk distance × 1.5)

Stop Loss (SL) = Recent swing low (for long) or high (for short)

Early Exit = Triggered when a reversal signal appears (flip logic)

Risk Management Parameters

Pair: ETH/USD

Timeframe: 10-minute

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted for sustainable practice)

Total Trades: 312 (backtest on selected dataset)

※Risk parameters are fully configurable and should be adjusted to suit each trader's personal setup and broker conditions.

Parameters & Configurations

Volume Short Length: 6

Volume Long Length: 12

MACD Fast Length: 11

MACD Slow Length: 21

Signal Smoothing: 10

Oscillator MA Type: SMA

Signal Line MA Type: SMA

Visual Support

Green arrow = Long entry

Red arrow = Short entry

MACD lines, signal line, and histogram

SL/TP markers plotted directly on the chart

Strategic Advantages & Uniqueness

Volume filtering eliminates low-participation, weak signals

Structurally aligned SL/TP based on recent market pivots

No repainting — decisions are made only on closed candles

Always in the market due to the reversal-style framework

Inspirations & Attribution

This strategy is inspired by the excellent work of:

Bitcoinblockchainonline – “BBO_Roxana_Signals MACD + vol”

Leveraging MACD zero-line cross and volume oscillator for intuitive signal generation.

HasanRifat – “MACD Fake Filter ”

Introduced a signal filter using MACD wave height averaging to reduce false positives.

This strategy builds upon those ideas to create a more automated, risk-aware, and technically adaptive system.

Summary

MACD Volume Strategy is a clean, logic-first automated trading system built for precision-seeking traders. It avoids discretionary bias and provides consistent signal logic under backtested historical conditions.

100% mechanical — no discretionary input required

Designed for high-confidence entries

Can be extended with filters, alerts, or trailing stops

※Strategy performance depends on market context. Past performance is not indicative of future results. Use with proper risk management and careful configuration.

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

RSI + Stochastic + WMA StrategyThis script is designed for TradingView and serves as a trading strategy (not just a visual indicator). It's intended for backtesting, strategy optimization, or live trading signal generation using a combination of popular technical indicators.

📊 Indicators Used in the Strategy:

Indicator Description

RSI (Relative Strength Index) Measures momentum; identifies overbought (>70) or oversold (<30) conditions.

Stochastic Oscillator (%K & %D) Detects momentum reversal points via crossovers. Useful for timing entries.

WMA (Weighted Moving Average) Identifies the trend direction (used as a trend filter).

📈 Trading Logic / Strategy Rules:

📌 Long Entry Condition (Buy Signal):

All 3 conditions must be true:

RSI is Oversold → RSI < 30

Stochastic Crossover Upward → %K crosses above %D

Price is above WMA → Confirms uptrend direction

👉 Interpretation: Market was oversold, momentum is turning up, and price confirms uptrend — bullish entry.

📌 Short Entry Condition (Sell Signal):

All 3 conditions must be true:

RSI is Overbought → RSI > 70

Stochastic Crossover Downward → %K crosses below %D

Price is below WMA → Confirms downtrend direction

👉 Interpretation: Market is overbought, momentum is turning down, and price confirms downtrend — bearish entry.

🔄 Strategy Execution (Backtesting Logic):

The script uses:

pinescript

Copy

Edit

strategy.entry("LONG", strategy.long)

strategy.entry("SHORT", strategy.short)

These are Pine Script functions to place buy and sell orders automatically when the above conditions are met. This allows you to:

Backtest the strategy

Measure win/loss ratio, drawdown, and profitability

Optimize indicator settings using TradingView Strategy Tester

📊 Visual Aids (Charts):

Plots WMA Line: Orange line for trend direction

Overbought/Oversold Zones: Horizontal lines at 70 (red) and 30 (green) for RSI visualization

⚡ Strategy Type Summary:

Category Setting

Strategy Type Momentum Reversal + Trend Filter

Timeframe Flexible (Works best on 1H, 4H, Daily)

Trading Style Swing/Intraday

Risk Profile Medium to High (due to momentum triggers)

Uses Leverage Possible (adjust risk accordingly)

MACD Crossover Strategy MACD Crossover Strategy:

This strategy is based on the Moving Average Convergence Divergence (MACD) indicator, a popular tool used in technical analysis to identify potential trend changes and momentum in price movements. The strategy focuses on MACD crossovers within a specific "important zone" to generate trading signals.

Key Components:

1. MACD Calculation: The strategy uses customizable parameters for fast length (default 12), slow length (default 26), and signal length (default 9) to calculate the MACD line and signal line.

2. Important Zone: Defined by upper and lower thresholds (default 0.5 and -0.5), this zone helps filter out potentially less significant crossovers.

3. Entry Conditions:

- Long (Buy) Entry: When the MACD line crosses above the signal line within the important zone.

- Short (Sell) Entry: When the MACD line crosses below the signal line within the important zone.

4. Exit Conditions: The strategy closes positions on opposite crossover signals. Long positions are closed on bearish crossovers, and short positions on bullish crossovers.

5. Visualization:

- MACD line (blue) and signal line (orange) are plotted.

- The zero line, upper threshold, and lower threshold are displayed for reference.

- Buy signals are represented by green triangles at the bottom of the chart.

- Sell signals are shown as red triangles at the top of the chart.

This strategy aims to capture trend changes while filtering out potentially false signals that occur when the MACD is at extreme values. By focusing on crossovers within the important zone, the strategy attempts to identify more reliable trading opportunities.

Traders can adjust the MACD parameters and the important zone thresholds to fine-tune the strategy for different assets or timeframes. As with any trading strategy, it's crucial to thoroughly backtest and consider risk management before using it in live trading.

Enhanced BarUpDn StrategyEnhanced BarUpDn Strategy

The Enhanced BarUpDn Strategy is a refined price action-based trading approach that identifies market trends and reversals using bar formations. It focuses on detecting bullish and bearish momentum by analyzing consecutive price bars and key support/resistance levels.

Key Features:

✅ Trend Confirmation – Uses a combination of bar patterns and indicators (e.g., moving averages, RSI) to confirm momentum shifts.

✅ Entry Signals – A buy signal is triggered when an "Up Bar" (higher high, higher low) follows a bullish setup; a sell signal when a "Down Bar" (lower high, lower low) confirms bearish momentum.

✅ Enhanced Filters – Incorporates volume analysis and additional conditions to reduce false signals.

✅ Stop-Loss & Risk Management – Uses recent swing highs/lows for stop placement and dynamic trailing stops for maximizing gains.

SuperTrend AI Oscillator StrategySuperTrend AI Oscillator Strategy

Overview

This strategy is a trend-following approach that combines the SuperTrend indicator with oscillator-based filtering.

By identifying market trends while utilizing oscillator-based momentum analysis, it aims to improve entry precision.

Additionally, it incorporates a trailing stop to strengthen risk management while maximizing profits.

This strategy can be applied to various markets, including Forex, Crypto, and Stocks, as well as different timeframes. However, its effectiveness varies depending on market conditions, so thorough testing is required.

Features

1️⃣ Trend Identification Using SuperTrend

The SuperTrend indicator (a volatility-adjusted trend indicator based on ATR) is used to determine trend direction.

A long entry is considered when SuperTrend turns bullish.

A short entry is considered when SuperTrend turns bearish.

The goal is to capture clear trend reversals and avoid unnecessary trades in ranging markets.

2️⃣ Entry Filtering with an Oscillator

The Super Oscillator is used to filter entry signals.

If the oscillator exceeds 50, it strengthens long entries (indicating strong bullish momentum).

If the oscillator drops below 50, it strengthens short entries (indicating strong bearish momentum).

This filter helps reduce trades in uncertain market conditions and improves entry accuracy.

3️⃣ Risk Management with a Trailing Stop

Instead of a fixed stop loss, a SuperTrend-based trailing stop is implemented.

The stop level adjusts automatically based on market volatility.

This allows profits to run while managing downside risk effectively.

4️⃣ Adjustable Risk-Reward Ratio

The default risk-reward ratio is set at 1:2.

Example: A 1% stop loss corresponds to a 2% take profit target.

The ratio can be customized according to the trader’s risk tolerance.

5️⃣ Clear Trade Signals & Visual Support

Green "BUY" labels indicate long entry signals.

Red "SELL" labels indicate short entry signals.

The Super Oscillator is plotted in a separate subwindow to visually assess trend strength.

A real-time trailing stop is displayed to support exit strategies.

These visual aids make it easier to identify entry and exit points.

Trading Parameters & Considerations

Initial Account Balance: Default is $7,000 (adjustable).

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 1,032

Visual Aids for Clarity

This strategy includes clear visual trade signals to enhance decision-making:

Green "BUY" labels for long entries

Red "SELL" labels for short entries

Super Oscillator plotted in a subwindow with a 50 midline

Dynamic trailing stop displayed for real-time trend tracking

These visual aids allow traders to quickly identify trade setups and manage positions with greater confidence.

Summary

The SuperTrend AI Oscillator Strategy is developed based on indicators from Black Cat and LuxAlgo.

By integrating high-precision trend analysis with AI-based oscillator filtering, it provides a strong risk-managed trading approach.

Important Notes

This strategy does not guarantee profits—performance varies based on market conditions.

Past performance does not guarantee future results. Markets are constantly changing.

Always test extensively with backtesting and demo trading before using it in live markets.

Risk management, position sizing, and market conditions should always be considered when trading.

Conclusion

This strategy combines trend analysis with momentum filtering, enhancing risk management in trading.

By following market trends carefully, making precise entries, and using trailing stops, it seeks to reduce risk while maximizing potential profits.

Before using this strategy, be sure to test it thoroughly via backtesting and demo trading, and adjust the settings to match your trading style.

Ultimate Trading BotHow the "Ultimate Trading Bot" Works:

This Pine Script trading bot executes buy and sell trades based on a combination of technical indicators:

Indicators Used:

RSI (Relative Strength Index)

Measures momentum and determines overbought (70) and oversold (30) levels.

A crossover above 30 suggests a potential buy, and a cross below 70 suggests a potential sell.

Moving Average (MA)

A simple moving average (SMA) of 50 periods to track the trend.

Prices above the MA indicate an uptrend, while prices below indicate a downtrend.

Stochastic Oscillator (%K and %D)

Identifies overbought and oversold conditions using a smoothed stochastic formula.

A crossover of %K above %D signals a buy, and a crossover below %D signals a sell.

MACD (Moving Average Convergence Divergence)

Uses a 12-period fast EMA and a 26-period slow EMA, with a 9-period signal line.

A crossover of MACD above the signal line suggests a bullish move, and a cross below suggests bearish movement.

Trade Execution:

Buy (Long Entry) Conditions:

RSI crosses above 30 (indicating recovery from an oversold state).

The closing price is above the 50-period moving average (showing an uptrend).

The MACD line crosses above the signal line (indicating upward momentum).

The Stochastic %K crosses above %D (indicating bullish momentum).

→ If all conditions are met, the bot enters a long (buy) position.

Sell (Exit Trade) Conditions:

RSI crosses below 70 (indicating overbought conditions).

The closing price is below the 50-period moving average (downtrend).

The MACD line crosses below the signal line (bearish signal).

The Stochastic %K crosses below %D (bearish momentum).

→ If all conditions are met, the bot closes the long position.

Visuals:

The bot plots the moving average, RSI, MACD, and Stochastic indicators for reference.

It also displays buy/sell signals with arrows:

Green arrow (Buy Signal) → When all buy conditions are met.

Red arrow (Sell Signal) → When all sell conditions are met.

How to Use It in TradingView:

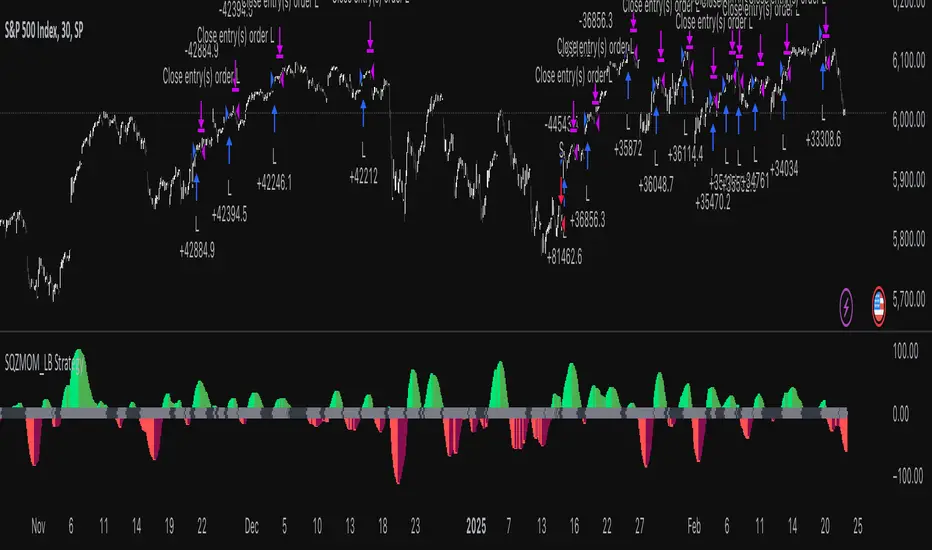

Squeeze Momentum Indicator Strategy [LazyBear + PineIndicators]The Squeeze Momentum Indicator Strategy (SQZMOM_LB Strategy) is an automated trading strategy based on the Squeeze Momentum Indicator developed by LazyBear, which itself is a modification of John Carter's "TTM Squeeze" concept from his book Mastering the Trade (Chapter 11). This strategy is designed to identify low-volatility phases in the market, which often precede explosive price movements, and to enter trades in the direction of the prevailing momentum.

Concept & Indicator Breakdown

The strategy employs a combination of Bollinger Bands (BB) and Keltner Channels (KC) to detect market squeezes:

Squeeze Condition:

When Bollinger Bands are inside the Keltner Channels (Black Crosses), volatility is low, signaling a potential upcoming price breakout.

When Bollinger Bands move outside Keltner Channels (Gray Crosses), the squeeze is released, indicating an expansion in volatility.

Momentum Calculation:

A linear regression-based momentum value is used instead of traditional momentum indicators.

The momentum histogram is color-coded to show strength and direction:

Lime/Green: Increasing bullish momentum

Red/Maroon: Increasing bearish momentum

Signal Colors:

Black: Market is in a squeeze (low volatility).

Gray: Squeeze is released, and volatility is expanding.

Blue: No squeeze condition is present.

Strategy Logic

The script uses historical volatility conditions and momentum trends to generate buy/sell signals and manage positions.

1. Entry Conditions

Long Position (Buy)

The squeeze just released (Gray Cross after Black Cross).

The momentum value is increasing and positive.

The momentum is at a local low compared to the past 100 bars.

The price is above the 100-period EMA.

The closing price is higher than the previous close.

Short Position (Sell)

The squeeze just released (Gray Cross after Black Cross).

The momentum value is decreasing and negative.

The momentum is at a local high compared to the past 100 bars.

The price is below the 100-period EMA.

The closing price is lower than the previous close.

2. Exit Conditions

Long Exit:

The momentum value starts decreasing (momentum lower than previous bar).

Short Exit:

The momentum value starts increasing (momentum higher than previous bar).

Position Sizing

Position size is dynamically adjusted based on 8% of strategy equity, divided by the current closing price, ensuring risk-adjusted trade sizes.

How to Use This Strategy

Apply on Suitable Markets:

Best for stocks, indices, and forex pairs with momentum-driven price action.

Works on multiple timeframes but is most effective on higher timeframes (1H, 4H, Daily).

Confirm Entries with Additional Indicators:

The author recommends ADX or WaveTrend to refine entries and avoid false signals.

Risk Management:

Since the strategy dynamically sizes positions, it's advised to use stop-losses or risk-based exits to avoid excessive drawdowns.

Final Thoughts

The Squeeze Momentum Indicator Strategy provides a systematic approach to trading volatility expansions, leveraging the classic TTM Squeeze principles with a unique linear regression-based momentum calculation. Originally inspired by John Carter’s method, LazyBear's version and this strategy offer a refined, adaptable tool for traders looking to capitalize on market momentum shifts.

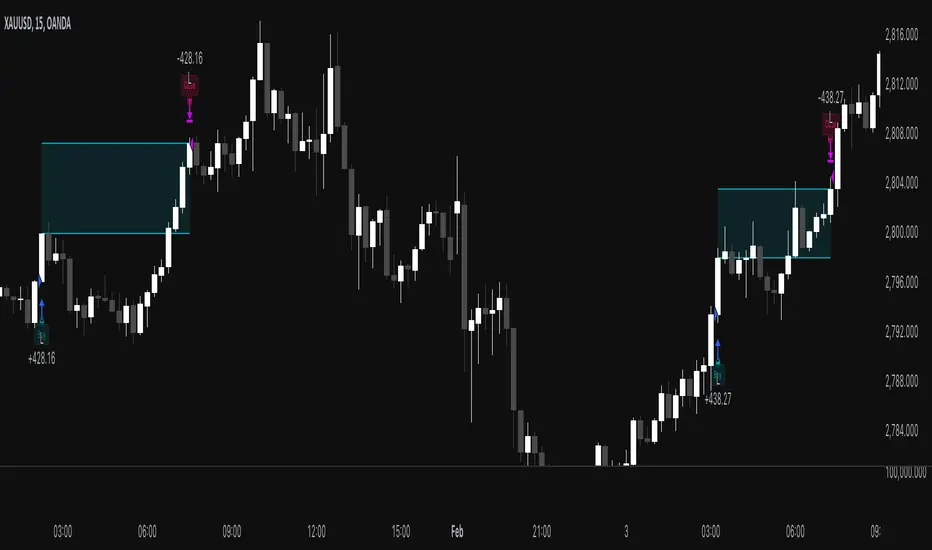

MACD Volume Strategy for XAUUSD (15m) [PineIndicators]The MACD Volume Strategy is a momentum-based trading system designed for XAUUSD on the 15-minute timeframe. It integrates two key market indicators: the Moving Average Convergence Divergence (MACD) and a volume-based oscillator to identify strong trend shifts and confirm trade opportunities. This strategy uses dynamic position sizing, incorporates leverage customization, and applies structured entry and exit conditions to improve risk management.

⚙️ Core Strategy Components

1️⃣ Volume-Based Momentum Calculation

The strategy includes a custom volume oscillator to filter trade signals based on market activity. The oscillator is derived from the difference between short-term and long-term volume trends using Exponential Moving Averages (EMAs)

Short EMA (default = 5) represents recent volume activity.

Long EMA (default = 8) captures broader volume trends.

Positive values indicate rising volume, supporting momentum-based trades.

Negative values suggest weak market activity, reducing signal reliability.

By requiring positive oscillator values, the strategy ensures momentum confirmation before entering trades.

2️⃣ MACD Trend Confirmation

The strategy uses the MACD indicator as a trend filter. The MACD is calculated as:

Fast EMA (16-period) detects short-term price trends.

Slow EMA (26-period) smooths out price fluctuations to define the overall trend.

Signal Line (9-period EMA) helps identify crossovers, signaling potential trend shifts.

Histogram (MACD – Signal) visualizes trend strength.

The system generates trade signals based on MACD crossovers around the zero line, confirming bullish or bearish trend shifts.

📌 Trade Logic & Conditions

🔹 Long Entry Conditions

A buy signal is triggered when all the following conditions are met:

✅ MACD crosses above 0, signaling bullish momentum.

✅ Volume oscillator is positive, confirming increased trading activity.

✅ Current volume is at least 50% of the previous candle’s volume, ensuring market participation.

🔻 Short Entry Conditions

A sell signal is generated when:

✅ MACD crosses below 0, indicating bearish momentum.

✅ Volume oscillator is positive, ensuring market activity is sufficient.

✅ Current volume is less than 50% of the previous candle’s volume, showing decreasing participation.

This multi-factor approach filters out weak or false signals, ensuring that trades align with both momentum and volume dynamics.

📏 Position Sizing & Leverage

Dynamic Position Calculation:

Qty = strategy.equity × leverage / close price

Leverage: Customizable (default = 1x), allowing traders to adjust risk exposure.

Adaptive Sizing: The strategy scales position sizes based on account equity and market price.

Slippage & Commission: Built-in slippage (2 points) and commission (0.01%) settings provide realistic backtesting results.

This ensures efficient capital allocation, preventing overexposure in volatile conditions.

🎯 Trade Management & Exits

Take Profit & Stop Loss Mechanism

Each position includes predefined profit and loss targets:

Take Profit: +10% of risk amount.

Stop Loss: Fixed at 10,100 points.

The risk-reward ratio remains balanced, aiming for controlled drawdowns while maximizing trade potential.

Visual Trade Tracking

To improve trade analysis, the strategy includes:

📌 Trade Markers:

"Buy" label when a long position opens.

"Close" label when a position exits.

📌 Trade History Boxes:

Green for profitable trades.

Red for losing trades.

📌 Horizontal Trade Lines:

Shows entry and exit prices.

Helps identify trend movements over multiple trades.

This structured visualization allows traders to analyze past performance directly on the chart.

⚡ How to Use This Strategy

1️⃣ Apply the script to a XAUUSD (Gold) 15m chart in TradingView.

2️⃣ Adjust leverage settings as needed.

3️⃣ Enable backtesting to assess past performance.

4️⃣ Monitor volume and MACD conditions to understand trade triggers.

5️⃣ Use the visual trade markers to review historical performance.

The MACD Volume Strategy is designed for short-term trading, aiming to capture momentum-driven opportunities while filtering out weak signals using volume confirmation.

Arpeet MACDOverview

This strategy is based on the zero-lag version of the MACD (Moving Average Convergence Divergence) indicator, which captures short-term trends by quickly responding to price changes, enabling high-frequency trading. The strategy uses two moving averages with different periods (fast and slow lines) to construct the MACD indicator and introduces a zero-lag algorithm to eliminate the delay between the indicator and the price, improving the timeliness of signals. Additionally, the crossover of the signal line and the MACD line is used as buy and sell signals, and alerts are set up to help traders seize trading opportunities in a timely manner.

Strategy Principle

Calculate the EMA (Exponential Moving Average) or SMA (Simple Moving Average) of the fast line (default 12 periods) and slow line (default 26 periods).

Use the zero-lag algorithm to double-smooth the fast and slow lines, eliminating the delay between the indicator and the price.

The MACD line is formed by the difference between the zero-lag fast line and the zero-lag slow line.

The signal line is formed by the EMA (default 9 periods) or SMA of the MACD line.

The MACD histogram is formed by the difference between the MACD line and the signal line, with blue representing positive values and red representing negative values.

When the MACD line crosses the signal line from below and the crossover point is below the zero axis, a buy signal (blue dot) is generated.

When the MACD line crosses the signal line from above and the crossover point is above the zero axis, a sell signal (red dot) is generated.

The strategy automatically places orders based on the buy and sell signals and triggers corresponding alerts.

Advantage Analysis

The zero-lag algorithm effectively eliminates the delay between the indicator and the price, improving the timeliness and accuracy of signals.

The design of dual moving averages can better capture market trends and adapt to different market environments.

The MACD histogram intuitively reflects the comparison of bullish and bearish forces, assisting in trading decisions.

The automatic order placement and alert functions make it convenient for traders to seize trading opportunities in a timely manner, improving trading efficiency.

Risk Analysis

In volatile markets, frequent crossover signals may lead to overtrading and losses.

Improper parameter settings may cause signal distortion and affect strategy performance.

The strategy relies on historical data for calculations and has poor adaptability to sudden events and black swan events.

Optimization Direction

Introduce trend confirmation indicators, such as ADX, to filter out false signals in volatile markets.

Optimize parameters to find the best combination of fast and slow line periods and signal line periods, improving strategy stability.

Combine other technical indicators or fundamental factors to construct a multi-factor model, improving risk-adjusted returns of the strategy.

Introduce stop-loss and take-profit mechanisms to control single-trade risk.

Summary

The MACD Dual Crossover Zero Lag Trading Strategy achieves high-frequency trading by quickly responding to price changes and capturing short-term trends. The zero-lag algorithm and dual moving average design improve the timeliness and accuracy of signals. The strategy has certain advantages, such as intuitive signals and convenient operation, but also faces risks such as overtrading and parameter sensitivity. In the future, the strategy can be optimized by introducing trend confirmation indicators, parameter optimization, multi-factor models, etc., to improve the robustness and profitability of the strategy.

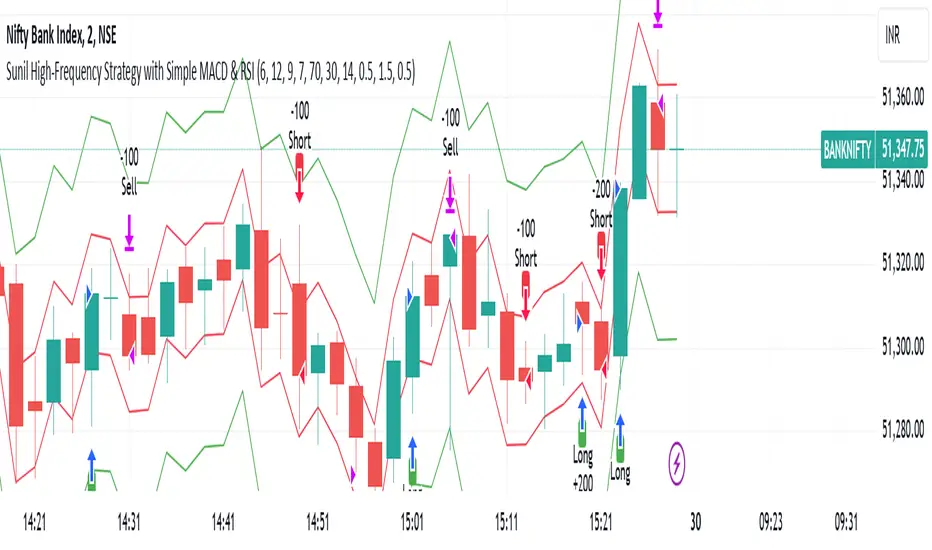

Sunil High-Frequency Strategy with Simple MACD & RSISunil High-Frequency Strategy with Simple MACD & RSI

This high-frequency trading strategy uses a combination of MACD and RSI to identify quick market opportunities. By leveraging these indicators, combined with dynamic risk management using ATR, it aims to capture small but frequent price movements while ensuring tight control over risk.

Key Features:

Indicators Used:

MACD (Moving Average Convergence Divergence): The strategy uses a shorter MACD configuration (Fast Length of 6 and Slow Length of 12) to capture quick price momentum shifts. A MACD crossover above the signal line triggers a buy signal, while a crossover below the signal line triggers a sell signal.

RSI (Relative Strength Index): A shorter RSI length of 7 is used to gauge overbought and oversold market conditions. The strategy looks for RSI confirmation, with a long trade initiated when RSI is below the overbought level (70) and a short trade initiated when RSI is above the oversold level (30).

Risk Management:

Dynamic Stop Loss and Take Profit: The strategy uses ATR (Average True Range) to calculate dynamic stop loss and take profit levels based on market volatility.

Stop Loss is set at 0.5x ATR to limit risk.

Take Profit is set at 1.5x ATR to capture reasonable price moves.

Trailing Stop: As the market moves in the strategy’s favor, the position is protected by a trailing stop set at 0.5x ATR, allowing the strategy to lock in profits as the price moves further.

Entry & Exit Signals:

Long Entry: Triggered when the MACD crosses above the signal line (bullish crossover) and RSI is below the overbought level (70).

Short Entry: Triggered when the MACD crosses below the signal line (bearish crossover) and RSI is above the oversold level (30).

Exit Conditions: The strategy exits long or short positions based on the stop loss, take profit, or trailing stop activation.

Frequent Trades:

This strategy is designed for high-frequency trading, with trade signals occurring frequently as the MACD and RSI indicators react quickly to price movements. It works best on lower timeframes such as 1-minute, 5-minute, or 15-minute charts, but can be adjusted for different timeframes based on the asset’s volatility.

Customizable Parameters:

MACD Settings: Adjust the Fast Length, Slow Length, and Signal Length to tune the MACD’s sensitivity.

RSI Settings: Customize the RSI Length, Overbought, and Oversold levels to better match your trading style.

ATR Settings: Modify the ATR Length and multipliers for Stop Loss, Take Profit, and Trailing Stop to optimize risk management according to market volatility.

Important Notes:

Market Conditions: This strategy is designed to capture smaller, quicker moves in trending markets. It may not perform well during choppy or sideways markets.

Optimizing for Asset Volatility: Adjust the ATR multipliers based on the asset’s volatility to suit the risk-reward profile that fits your trading goals.

Backtesting: It's recommended to backtest the strategy on different assets and timeframes to ensure optimal performance.

Summary:

The Sunil High-Frequency Strategy leverages a simple combination of MACD and RSI with dynamic risk management (using ATR) to trade small but frequent price movements. The strategy ensures tight stop losses and reasonable take profits, with trailing stops to lock in profits as the price moves in favor of the trade. It is ideal for scalping or intraday trading on lower timeframes, aiming for quick entries and exits with controlled risk.

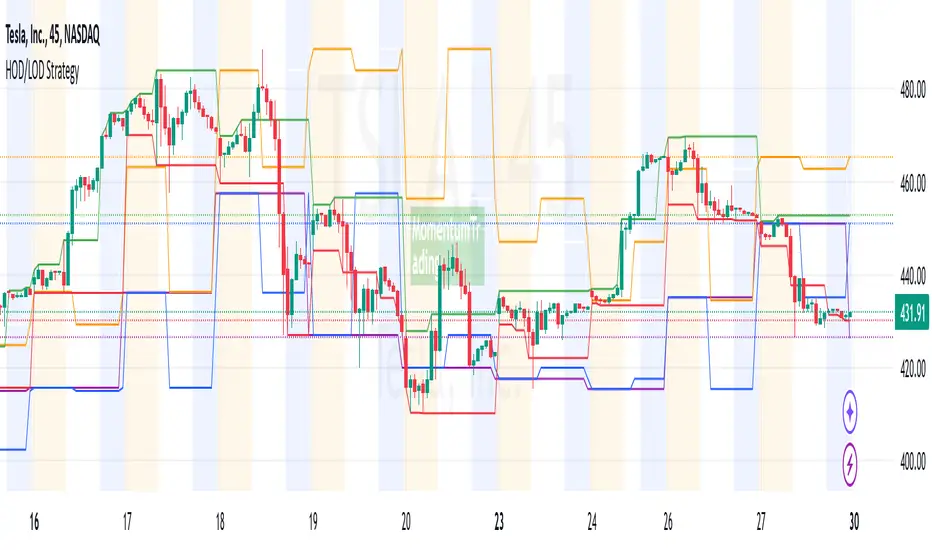

HOD/LOD/PMH/PML/PDH/PDL Strategy by @tradingbauhaus This script is a trading strategy @tradingbauhaus designed to trade based on key price levels, such as the High of Day (HOD), Low of Day (LOD), Premarket High (PMH), Premarket Low (PML), Previous Day High (PDH), and Previous Day Low (PDL). Below, I’ll explain in detail what the script does:

Core Functionality of the Script:

Calculates Key Price Levels:

HOD (High of Day): The highest price of the current day.

LOD (Low of Day): The lowest price of the current day.

PMH (Premarket High): The highest price during the premarket session (before the market opens).

PML (Premarket Low): The lowest price during the premarket session.

PDH (Previous Day High): The highest price of the previous day.

PDL (Previous Day Low): The lowest price of the previous day.

Draws Horizontal Lines on the Chart:

Plots horizontal lines on the chart for each key level (HOD, LOD, PMH, PML, PDH, PDL) with specific colors for easy visual identification.

Defines Entry and Exit Rules:

Long Entry (Buy): If the price crosses above the PMH (Premarket High) or the PDH (Previous Day High).

Short Entry (Sell): If the price crosses below the PML (Premarket Low) or the PDL (Previous Day Low).

Long Exit: If the price reaches the HOD (High of Day) during a long position.

Short Exit: If the price reaches the LOD (Low of Day) during a short position.

How the Script Works Step by Step:

Calculates Key Levels:

Uses the request.security function to fetch the HOD and LOD of the current day, as well as the highs and lows of the previous day (PDH and PDL).

Calculates the PMH and PML during the premarket session (before 9:30 AM).

Plots Levels on the Chart:

Uses the plot function to draw horizontal lines on the chart representing the key levels (HOD, LOD, PMH, PML, PDH, PDL).

Each level has a specific color for easy identification:

HOD: White.

LOD: Purple.

PDH: Orange.

PDL: Blue.

PMH: Green.

PML: Red.

Defines Trading Rules:

Uses conditions with ta.crossover and ta.crossunder to detect when the price crosses key levels.

Long Entry: If the price crosses above the PMH or PDH, a long position (buy) is opened.

Short Entry: If the price crosses below the PML or PDL, a short position (sell) is opened.

Long Exit: If the price reaches the HOD during a long position, the position is closed.

Short Exit: If the price reaches the LOD during a short position, the position is closed.

Executes Orders Automatically:

Uses the strategy.entry and strategy.close functions to open and close positions automatically based on the defined rules.

Advantages of This Strategy:

Based on Key Levels: Uses important price levels that often act as support and resistance.

Easy to Visualize: Horizontal lines on the chart make it easy to identify levels.

Automated: Entries and exits are executed automatically based on the defined rules.

Limitations of This Strategy:

Dependent on Volatility: Works best in markets with significant price movements.

False Crosses: There may be false crosses that generate incorrect signals.

No Advanced Risk Management: Does not include dynamic stop-loss or take-profit mechanisms.

How to Improve the Strategy:

Add Stop-Loss and Take-Profit: To limit losses and lock in profits.

Filter Signals with Indicators: Use RSI, MACD, or other indicators to confirm signals.

Optimize Levels: Adjust key levels based on the asset’s behavior.

In summary, this script is a trading strategy that operates based on key price levels, such as HOD, LOD, PMH, PML, PDH, and PDL. It is useful for traders who want to trade based on significant support and resistance levels.

MACD Aggressive Scalp SimpleComment on the Script

Purpose and Structure:

The script is a scalping strategy based on the MACD indicator combined with EMA (50) as a trend filter.

It uses the MACD histogram's crossover/crossunder of zero to trigger entries and exits, allowing the trader to capitalize on short-term momentum shifts.

The use of strategy.close ensures that positions are closed when specified conditions are met, although adjustments were made to align with Pine Script version 6.

Strengths:

Simplicity and Clarity: The logic is straightforward and focuses on essential scalping principles (momentum-based entries and exits).

Visual Indicators: The plotted MACD line, signal line, and histogram columns provide clear visual feedback for the strategy's operation.

Trend Confirmation: Incorporating the EMA(50) as a trend filter helps avoid trades that go against the prevailing trend, reducing the likelihood of false signals.

Dynamic Exit Conditions: The conditional logic for closing positions based on weakening momentum (via MACD histogram change) is a good way to protect profits or minimize losses.

Potential Improvements:

Parameter Inputs:

Make the MACD (12, 26, 9) and EMA(50) values adjustable by the user through input statements for better customization during backtesting.

Example:

pine

Copy code

macdFast = input(12, title="MACD Fast Length")

macdSlow = input(26, title="MACD Slow Length")

macdSignal = input(9, title="MACD Signal Line Length")

emaLength = input(50, title="EMA Length")

Stop Loss and Take Profit:

The strategy currently lacks explicit stop-loss or take-profit levels, which are critical in a scalping strategy to manage risk and lock in profits.

ATR-based or fixed-percentage exits could be added for better control.

Position Size and Risk Management:

While the script uses 50% of equity per trade, additional options (e.g., fixed position sizes or risk-adjusted sizes) would be beneficial for flexibility.

Avoid Overlapping Signals:

Add logic to prevent overlapping signals (e.g., opening a new position immediately after closing one on the same bar).

Backtesting Optimization:

Consider adding labels or markers (label.new or plotshape) to visualize entry and exit points on the chart for better debugging and analysis.

The inclusion of performance metrics like max drawdown, Sharpe ratio, or profit factor would help assess the strategy's robustness during backtesting.

Compatibility with Live Trading:

The strategy could be further enhanced with alert conditions using alertcondition to notify the trader of buy/sell signals in real-time.