Advanced Time Dividers & Killzones IndicatorOverview

A comprehensive Pine Script v6 indicator that displays customizable time period dividers and trading session killzones on your chart. Perfect for intraday traders who need clear visual separation of time periods and want to identify key trading sessions.

✨ Features

Time Period Dividers

Weekly Lines: Vertical lines marking the start of each week

Monthly Lines: Vertical lines marking the start of each month

Quarterly Lines: Vertical lines marking the start of each quarter (Q1, Q2, Q3, Q4)

Yearly Lines: Vertical lines marking the start of each year

Trading Session Killzones

London Session: 2:00-5:00 GMT (Blue shaded box)

New York Session: 7:00-10:00 GMT (Green shaded box)

London Close: 10:00-12:00 GMT (Orange shaded box)

Asia Session: 20:00-00:00 GMT (Pink shaded box)

🎨 Customization Options

Display Controls

Toggle each time divider type individually

Toggle each killzone individually

Adjust historical and future display range

Show/hide labels on dividers and killzones

Style Customization

Line Styles: Choose between Solid, Dashed, or Dotted lines

Line Width: Adjustable from 1 to 5 pixels

Colors: Fully customizable colors for each element with transparency control

Label Size: Choose from Tiny, Small, Normal, or Large

Period Settings

Control how many bars to display in the past (0-5000)

Control how many bars to display in the future (0-1000)

📋 Usage Instructions

Add to Chart: Add the indicator to any chart

Select Timeframe: Works best on intraday timeframes (1H, 15min, 5min) for killzones

Customize: Open settings to enable/disable features and customize colors

Trading: Use the dividers to identify time periods and killzones to spot high-liquidity sessions

💡 Trading Applications

Time Dividers

Weekly/Monthly Analysis: Identify major time period transitions

Market Structure: Analyze how price behaves at period boundaries

Event Correlation: Align with economic calendar events

Killzones

High Liquidity Periods: Trade during peak market activity

ICT Strategy: Follows Inner Circle Trader killzone concepts

Session-Based Trading: Focus on specific trading sessions

Volatility Windows: Identify when major moves typically occur

⚙️ Technical Details

Version: Pine Script v6

Type: Overlay indicator

Max Lines: 500 (optimized performance)

Max Boxes: 500 (for killzone visualization)

Timezone: GMT/UTC for killzones

Memory Efficient: Automatic cleanup of old objects

🎯 Best Practices

Combine with Price Action: Use dividers to frame your analysis

Focus on Killzones: Most significant price moves occur during these sessions

Adjust Transparency: Find the right balance between visibility and chart clarity

Use Labels Wisely: Toggle labels on/off based on your needs

Timeframe Selection: Use lower timeframes (≤1H) to see killzones clearly

📝 Notes

Killzone times are in GMT/UTC timezone

Works on all instruments (Forex, Crypto, Stocks, Futures)

Optimized for performance with automatic memory management

Fully compatible with other indicators

🔄 Updates & Support

This indicator is actively maintained. Feel free to suggest improvements or report issues in the comments.

Kitaran

Alchemist Ranges By KousickAlchemist Ranges By Kousick

A Indicator For Alchemist Ranges and How He Trades in time

amir Liquidity Sweeps [amir]this indicator is from luxalgon i think this is the code that made this incdicator never get destroyed by aanyone

VIX Counter-Trend StrategyVIX Panic Index VOO Bottom-Fishing Strategy

📊 Strategy Overview

This strategy utilizes the VIX (Volatility Index) as a market sentiment indicator to help investors rationally enter positions during periods of extreme market panic, using objective technical signals to avoid emotional decision-making. It is designed to capture rebound opportunities in VOO (or other US equity ETFs) following panic-driven selloffs.

🎯 Entry and Exit Conditions

Entry Conditions (both must be met):

VIX reaches or exceeds the set threshold (default 25, adjustable)

VIX death crosses below its moving average (default 5-day MA), confirming panic sentiment is beginning to recede

Exit Conditions (three modes available):

Holding Period Mode: Exit after holding for the set number of days (default 100 days)

VIX Decline Mode: Exit when VIX falls below the set threshold (default 20)

Either Condition Mode: Exit when either condition is met

⚠️ Important Warnings

Not Suitable for Leveraged ETF Bottom-Fishing: VIX reflects market volatility. Using leveraged ETFs (such as TQQQ, SOXL) increases risk due to decay effects and greater volatility, potentially causing larger losses during panic periods.

Bear Market Inaccuracy Risk: This strategy assumes markets will rebound from panic. However, during prolonged bear markets or systemic risks (such as the 2008 financial crisis or 2022 rate hike cycle), VIX may remain elevated for extended periods, triggering multiple buy signals while prices continue declining, rendering the strategy ineffective.

Recommended to Combine with Market Trend Analysis: Works better in bull market conditions. In bear markets, consider raising VIX thresholds or suspending use.

For Reference Only, Not Investment Advice: Historical performance does not guarantee future results. Please use cautiously according to your personal risk tolerance.

VIX 恐慌指數 VOO 抄底策略

📊 策略目的

本策略利用 VIX 恐慌指數作為市場情緒指標,幫助投資人在市場極度恐慌時理性進場抄底,並透過客觀的技術訊號避免情緒化操作。適合用於捕捉 VOO(或其他美股 ETF)在恐慌性下跌後的反彈機會。

🎯 進出場條件

進場條件(同時滿足):

VIX 指數達到設定門檻以上(預設 25,可調整)

VIX 死亡交叉其均線(預設 5 日均線),確認恐慌情緒開始回落

出場條件(三種模式可選):

持有天數模式:持有達到設定天數後出場(預設 100 天)

VIX 回落模式:VIX 降至設定門檻以下時出場(預設 20)

兩者皆可模式:任一條件滿足即出場

⚠️ 重要警語

不適合槓桿型 ETF 抄底:VIX 反映的是市場波動度,使用槓桿 ETF(如 TQQQ、SOXL)會因為衰減效應和更大波動而增加風險,可能在恐慌期間造成更大虧損。

空頭市場失準風險:本策略假設市場會從恐慌中反彈,但在長期空頭或系統性風險(如 2008 金融危機、2022 升息循環)中,VIX 可能長期處於高檔,多次觸發買入訊號卻持續下跌,導致策略失效。

建議搭配大盤趨勢判斷:在多頭格局中使用效果較佳,空頭格局建議提高 VIX 門檻或暫停使用。

僅供參考,非投資建議:歷史績效不代表未來表現,請依個人風險承受度謹慎使用。

Advanced Elliott Wave PlotterAdvanced Elliott Wave plotter, Parameters can be adjusted.

AI Generated, so no particular credits to anyone.

Three-Year Pullback Indicator根據 VOO (Vanguard S&P 500 ETF) 和 0050 (元大台灣50) 的歷史數據,製作了一個 「回檔百分比」 指標,幫助大家在市場回調時,有更明確的底部加碼參考依據!

📌 指標特色與設計概念:

觀察過去走勢,像 VOO 和 0050 這種追蹤大盤的 ETF,自歷史高點回檔通常極少超過 30%。

分批加碼策略: 30% 以下的回檔區間,分為三個等份級距

30% 回檔 (紅色線): 第一筆加碼區

20% 回檔 (橘色線): 第二筆加碼區

10% 回檔 (綠色線): 第三筆加碼區

兩種回檔計算:

指標同時顯示兩種回檔百分比 (黑色/藍色線),讓您對價格所處位置一目瞭然:

黑色線表式從「歷史高點」 的回檔

藍色線表示從「自定義期間高點」 (預設 3 年/720 根 K 棒) 的回檔

請注意: 本指標僅供技術參考與研究交流。指標非投資建議! 投資人仍須根據自身的資金狀況、風險承受度及獨立判斷進行調整與決策。

Based on the historical data of VOO (Vanguard S&P 500 ETF) and 0050 (Yuanta Taiwan 50), I've created a practical "Drawdown Percentage" indicator. It aims to provide a clearer reference point for dollar-cost averaging (DCA) during market pullbacks!

📌 Indicator Features and Design Concept:

Historical Basis: Observing past trends, broad market tracking ETFs like VOO and 0050 have historically experienced very few drawdowns exceeding 30% from their all-time highs.Staged Accumulation Strategy: The drawdown range below 30% is divided into three equal tiers, serving as a reference for investors to deploy funds in stages:

30% Drawdown (Red Line): First Accumulation Zone

20% Drawdown (Orange Line): Second Accumulation Zone

10% Drawdown (Green Line): Third Accumulation Zone

🔍 Two Drawdown Calculations:

The indicator simultaneously displays two drawdown percentages (Black/Blue lines) for a clear view of the price's current position:

Black Line: Represents the drawdown from the "All-Time High".

Blue Line: Represents the drawdown from the "User-Defined Period High" (default is 3 years / 720 bars).

Please note: This indicator is provided for technical reference and educational purposes only. It is NOT investment advice! Investors must make adjustments and decisions based on their own financial condition, risk tolerance, and independent judgment.

Bull & Bear Candle By Background ColorThe essential chart overlay for high-speed momentum confirmation.

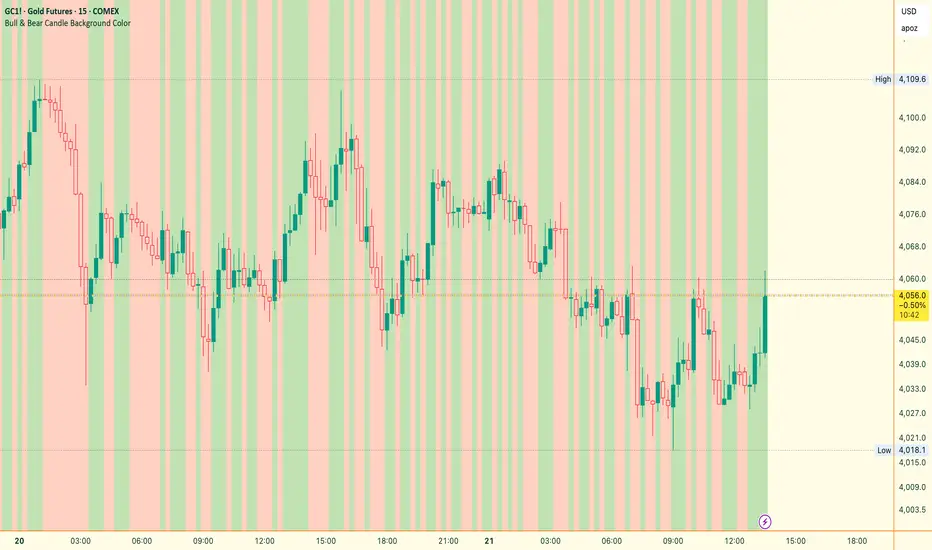

This professional-grade Pine Script v5 indicator provides instant, unfiltered visual feedback on the market's immediate bias by coloring the chart background based on the short-term relationship between Close and Open. It’s designed to streamline decision-making and enhance trade conviction.

Why Traders Use This Tool

In dynamic markets, reading momentum rapidly is critical. This indicator removes visual clutter and cognitive lag.

Zero-Lag Momentum Filter: Instantly identifies if control belongs to buyers (Close > Open) or sellers (Close < Open). A sustained background color acts as a directional bias filter for all your setups.

Trade Confirmation & Conviction: Use the background color as a high-level confluence factor. Only execute Long trades when the background is Bullish and Short trades when it is Bearish. This drastically reduces counter-trend entries.

Risk Management Signal: The appearance of the Neutral/Doji Color flags market equilibrium and consolidation, often preceding a critical structural shift. This is your immediate signal to tighten stops or prepare for a potential reversal setup.

Dual Confirmation: The script offers a highly requested feature: Bar Coloring layered atop the background to provide a second, granular layer of visual context, making momentum shifts impossible to miss.

⚙️ Key Features & Settings Usage

All settings are optimized for clarity, using high transparency to prevent the indicator from obscuring underlying price action or other analytical tools.

🎨 Background Color Settings (Primary)

These controls allow you to define the market state you are reading:

1. Background: Bullish Color: Confirms short-term buying pressure (Close > Open). Set a distinct color for confirmed upward momentum.

2. Background: Bearish Color: Confirms short-term selling pressure (Close < Open). Set a high-contrast color for immediate recognition of downward pressure.

3. Background: Neutral/Doji Color: Signals market indecision (Close ≈ Open). Use as a caution flag, highlighting pivot points and ranging periods.

✨ Added Feature: Bar Coloring

4. FEATURE: Enable Bar Coloring: When enabled, the individual candles are colored with a lighter hue matching the background. This provides dual visual confirmation, maximizing impact on lower timeframes where momentum flips quickly.

🧭 How to Achieve Confluence

Entry Filter: Wait for the background color to flip to your desired direction, then seek your primary entry signal (e.g., breakout, pullback, or MACD cross).

Trade Hold: As long as the background color remains consistent, the short-term momentum is confirmed, justifying the continuation of your trade.

Exit Signal: A flip to the Neutral/Doji Color should be treated as a warning shot, signaling a mandatory review of your position and stops.

Disclaimer: This indicator is a powerful visual and confirmation tool and does not generate buy/sell signals on its own. It is designed to be used in conjunction with your established trading strategy and comprehensive risk management principles

Jace's Range DetectionAttempts to identify when an instrument is trading in a range. It uses Price Movement %, ATR and ADX. The following parameters are configurable: Range Detection Period, Range Threshold(%), ATR Period, ATR Range Multiplier.

Directional Imbalance Index [BigBeluga]🔵 OVERVIEW

The Directional Imbalance Index is designed to track market strength by counting how often price sets new highs or lows over a defined lookback period. Every time a bar forms a new extreme, the indicator records a +1 count for either bullish (highs) or bearish (lows). These counts are aggregated into a rolling calculation, allowing traders to see which side dominates and how directional imbalance evolves.

🔵 CONCEPTS

Each new highest high → adds a bullish count (+1).

Each new lowest low → adds a bearish count (+1).

Counts are stored inside arrays over a user-defined Calculation Period .

for i = 0 to period-1

h = high

l = low

if h == upper

countUp.push(1)

if l == lower

countDn.push(1)

The balance between bullish and bearish counts highlights dominance and imbalance.

Normalized percentages help compare both sides (e.g., 65% bullish vs 35% bearish).

🔵 FEATURES

Counts new highs/lows over a chosen Highest/Lowest Length .

Aggregates values over a rolling Calculation Period .

Plots cumulative bullish vs bearish totals in the subchart.

Displays % share of bulls vs bears from total counts.

On-chart labels mark bars where a count was added.

Plots reference lines of the current upper (high) and lower (low) ranges.

Dynamic fill between bullish/bearish plots to visualize which side dominates.

🔵 HOW TO USE

Look for persistent bullish imbalance (bull % > bear %) as confirmation of upward momentum.

Look for persistent bearish imbalance (bear % > bull %) as confirmation of downward momentum.

Watch for shifts in % dominance — often early signs of trend reversal or weakening strength.

Use labels on the chart to visually confirm which bars contributed to directional bias.

Combine with trend or volume tools to confirm whether imbalance aligns with market direction.

🔵 CONCLUSION

The Directional Imbalance Index offers a systematic way to measure directional pressure. By counting how often price pushes into new territory, the indicator reveals whether bulls or bears are taking control. This makes it a valuable tool for detecting early signs of trend continuation or exhaustion, helping traders align with the side most likely to dominate.

Top-Down Analysis - Multi-Timeframe AlignmentThis indicator implements a Top-Down Multi-Timeframe Trading Analysis System. Here's what it does:

Core Functionality

1. Multi-Timeframe Bias Detection

Monitors three timeframes: Daily, 4-Hour, and 1-Hour

Determines if each timeframe is bullish, bearish, or neutral based on two EMAs (9 and 21 period by default)

A timeframe is bullish when: Fast EMA > Slow EMA AND price is above Fast EMA

A timeframe is bearish when: Fast EMA < Slow EMA AND price is below Fast EMA

2. Alignment Tier System

Tier 1 (Full Alignment): All three timeframes agree (Daily = 4H = 1H direction)

Tier 2 (Partial Alignment): Daily and 1H agree, but 4H differs

No Alignment: Timeframes disagree

3. Previous Day Support & Resistance Levels

Automatically plots key levels from the previous day:

Previous Day High (PDH) - resistance

Previous Day Low (PDL) - support

Previous Day Close (PDC)

Previous Day Midpoint (PDM)

4. Execution Zone (15-Minute Window)

Highlights the first 15 minutes after each new 4H candle opens

This is the optimal entry window when alignment conditions are met

5. Pattern Recognition

Detects trading setups:

Double tops/bottoms

Long wicks at support/resistance

Bullish/bearish closes aligned with bias

6. Trade Signals

Generates entry signals when:

There's Tier 1 or Tier 2 alignment

Price is in the 15-minute execution zone

A valid pattern forms (double top/bottom or wick rejection)

7. Visual Dashboard

Shows a real-time table with:

Each timeframe's current bias

Alignment status

Next 4H prediction

Whether price is at a key support/resistance level

Trading Strategy

The indicator helps traders follow the principle of "trade with the higher timeframe trend" by only taking trades when multiple timeframes agree, focusing entries during specific windows, and respecting previous day's key price levels as potential reaction zones.

Macketings 1min ScalpingThis is a hyper-reactive scalping strategy designed for the 1-minute chart. It utilizes a strict four-EMA hierarchy (80/90/340/500) to ensure trades are only taken in the strongest aligned market trend. The strategy is built to be extremely tight on risk and focuses on capturing the immediate, high-momentum swing that follows a confirmed EMA retest or breakout.

Key Mechanics (How it Works):

Strict Trend Alignment: Entry is only permitted when the faster EMA band (80/90) and the price action are correctly aligned with the slow trend (340/500).

Long: EMA 80/90 must be above EMA 340/500, AND EMA 340 must be above EMA 500. (And vice-versa for Short.)

Expanded Retest Entry: The strategy waits for the price to retest or briefly enter the 80/90 band, then immediately enters upon the confirmed momentum breakout from that band.

Dynamic Risk Management (Tight Ride): The strategy is engineered to ride the wave aggressively while protecting capital immediately:

Extremely Tight Initial Stop Loss (0.2% default): Limits initial risk instantly.

Break-Even Security: Once profit hits 0.3%, the Stop Loss is automatically trailed to secure 0.2% profit (a risk-free trade).

Aggressive Exit Logic: Positions are closed not only upon hitting the Take Profit target (2.5%) but also immediately if the 80/90 EMA band crosses the 340 EMA, signaling a critical loss of momentum.

Disclaimer:

This strategy requires high-liquidity instruments and is best used on low timeframes (1-minute) due to its dependency on fast momentum shifts and tight stops. Backtesting and forward testing are crucial before deployment.

Pi Cycle BTC Top + Pre-Alert BandsPi Cycle BTC Top + Pre-Alert Bands is an advanced implementation of the classic Pi Cycle Top model, designed for Bitcoin cycle analysis on higher timeframes (especially 1D BTCUSD/BTCUSD·INDEX).

The original Pi Cycle Top uses two moving averages:

• 111-day SMA (short MA)

• 350-day SMA ×2 (long MA)

A Pi Top is signaled when the 111 SMA crosses above the 350×2 SMA. Historically, this has occurred near major BTC cycle highs.

This script extends that idea with a 3-step early-warning sequence:

• Pi Green – early compression: short/long MA ratio crosses upward into the green band (convergence from below is required).

• Pi Yellow – mid-cycle warning: only fires if a valid Green has already occurred in the same cycle.

• Pi Cycle Top – final top: the classic Pi Cycle cross, limited to one top signal per cycle. After a top, no new Yellow or Top signals can appear until a new Green event starts the next cycle.

Background shading shows the active phase (Green / Yellow / late-cycle zone), so you can see at a glance where BTC is within its Pi-based macro structure.

All logic is non-repainting: request.security() uses lookahead_off and no future data is accessed.

Typical use

This indicator is intended as a macro-cycle timing and risk-awareness tool, not a stand-alone entry system. Many traders use it to:

• Watch for Pi Green as the start of a potential late-cycle advance.

• Treat Pi Yellow as a rising-risk environment and tighten risk management.

• Use the Pi Cycle Top as a historical high-risk zone where large profit-taking or hedging may be considered.

Always combine this with your own analysis (trend, volume, on-chain, macro) before making decisions.

How to set alerts

Add the indicator to your chart (1D BTCUSD or BTCUSD·INDEX recommended).

Click Alerts → Condition → Pi Cycle BTC Top + Pre-Alert Bands.

Choose one of:

• Pi Cycle – Green Pre-Alert (early convergence)

• Pi Cycle – Yellow Pre-Alert (after Green only)

• Pi Cycle – TOP (Single per Cycle, after Green)

Use “Once per bar close” for higher-timeframe reliability.

Disclaimer

This tool is for educational and analytical purposes only. The Pi Cycle concept is based on historical behavior and does not guarantee future results. This is not financial advice; always do your own research and manage risk appropriately.

Institutional Volume Flow (IVF) with VWAP & Zones. Accumulation Zone (Green Background)Logic: Signals potential institutional buying at the low.Conditions: The current close price is below VWAP $\text{(close} < \text{VWAP)}$, AND there has been at least one Aggressive Buy (IVF) bar within the last $\text{N}$ bars.2. Manipulation Zone (Red Background)Logic: Signals a Stop Hunt or False Breakout where the market briefly takes out a previous extreme before reversing with institutional conviction.Conditions:False Break High: Current high is a new 2-bar high, immediately followed by an Aggressive Sell (IVF) bar.False Break Low: Current low is a new 2-bar low, immediately followed by an Aggressive Buy (IVF) bar.3. Compression Zone (Purple Background)Logic: Signals a period of low volatility where price is "coiling up" for a large move.Conditions: The bar's range $\text{(high} - \text{low)}$ is consistently small (less than a multiplier of the Average True Range (ATR)) for a specific number of bars.The zones are plotted using bgcolor() for a visual area on the chart and plotshape() to mark the specific bar where the condition is met. Manipulation is given the highest plotting priority to ensure it's visible over other zones if conditions overlap.Would you like me to elaborate on the typical trading strategy associated with any of these three zones (Accumulation, Manipulation, or Compression)?

Premarket Breakout (TP1 → BE → ATR Trail)this is the best ever you will really like i t and it does a lot its a really good scirpt please use it to make trades

Premarket Breakout (TP1 → BE → ATR Trail)the best one you can find a very good indicator and strategy to help with al l trading needs in every way

Fibonacci Set-upThe indicator plots Fibonacci retracements based on recent lows and highs.

Additionally it calculates position size, max leverage, max drawdown and pricelevels.

Breakouts & Pullbacks [Trendoscope®]🎲 Breakouts & Pullbacks - All-Time High Breakout Analyzer

Probability-Based Post-Breakout Behavior Statistics | Real-Time Pullback & Runup Tracker

A professional-grade Pine Script v6 indicator designed specifically for analyzing the historical and real-time behavior of price after strong All-Time High (ATH) breakouts. It automatically detects significant ATH breakouts (with configurable minimum gap), measures the depth and duration of pullbacks, the speed of recovery, and the subsequent run-up strength — then turns all this data into easy-to-read statistical probabilities and percentile ranks.

Perfect for swing traders, breakout traders, and anyone who wants objective, data-driven insight into questions like:

“How deep do pullbacks usually get after a strong ATH breakout?”

“How many bars does it typically take to recover the breakout level?”

“What is the median run-up after recovery?”

“Where is the current pullback or run-up relative to historical ones?”

🎲 Core Concept & Methodology

Indicator is more suitable for indices or index ETFs that generally trade in all-time highs however subjected to regular pullbacks, recovery and runups.

For every qualified ATH breakout, the script identifies 4 distinct phases:

Breakout Point – The exact bar where price closes above the previous ATH after at least Minimum Gap bars.

Pullback Phase – From breakout candle high → lowest low before price recovers back above the breakout level.

Recovery Phase – From the pullback low → the bar where price first trades back above the original breakout price.

Post-Recovery Run-up Phase – From the recovery point → current price (or highest high achieved so far).

Each completed cycle is stored permanently and used to build a growing statistical database unique to the loaded chart and timeframe.

🎲 Visual Elements

Yellow polyline triangle connecting Previous ATH / Pullback point(start), New ATH Breakout point (end), Recovery point (lowest pullback price), and extends to recent ATH price.

Small green label at the pullback low showing detailed tooltip on hover with all measured values

Clean, color-coded statistics table in the top-right corner (visible only on the last bar)

Powerful Statistics Table – The Heart of the Indicator

The table constantly compares the current situation against all past qualified breakouts and shows details about pullbacks, and runups that help us calculate the probability of next pullback, recovery or runup.

🎲 Settings & Inputs

Minimum Gap

The minimum number of bars that must pass between breaking a new ATH and the previous one.

Higher values = stricter filter → only the strongest, cleanest breakouts are counted.

Lower values = more data points (useful on lower timeframes or very trending instruments).

Recommendation:

Daily charts: 30–50

4H charts: 40–80

1H charts: 100–200

🎲 How to Use It in Practice

This indicator helps investors to understand when to be bullish, bearish or cautious and anticipate regular pullbacks, recovery of markets using quantitative methods.

The indicator does not generate buy/sell signals. However, helps traders set expectations and anticipate market movements based on past behavior.

Weekly price boxWeekend Trap / Custom Timebox Analyzer

This indicator allows traders to define a specific time window (e.g., the "Weekend Trap" period from Friday to Sunday, or a full weekly range) and automatically draws a box highlighting the price action during that session. It is designed to help visualize gaps, ranges, and trend direction over specific timeframes.

Key Features

Dynamic Range Detection: automatically draws a box connecting the Highest High and Lowest Low occurring between your start and end times.

Trend Visualization: The box changes color dynamically based on price performance:

Bullish (Blue): Close is higher than the Open of the defined period.

Bearish (Red): Close is lower than the Open of the defined period.

Smart Labeling: Displays a customizable label (default: "Box") along with the real-time Percentage Change of the period. The label is positioned intelligently outside the box to avoid cluttering the price action.

Flexible Timing:

Supports standard intraday sessions (e.g., Mon 09:00 to Mon 17:00).

Supports "wrap-around" sessions (e.g., Friday 23:00 to Sunday 17:00).

New: Supports full-week monitoring (e.g., Friday to Friday) by handling start times that are later than end times on the same day.

Fully Customizable:

Configure specific Bullish and Bearish colors (Border, Background, Text).

Adjust line styles (Solid, Dashed, Dotted) and widths.

Select days via easy-to-use dropdown menus.

How to Use

Time Settings:

Select your Start Day and Time (e.g., Friday 23:00).

Select your End Day and Time (e.g., Sunday 17:00).

Note: Times are based on the Chart/Exchange time.

Visual Settings:

Go to the settings menu to define your preferred colors for Bullish and Bearish scenarios.

Toggle the Label on/off and adjust text size.

Use Cases

Weekend Gaps: Monitor price action that occurs during off-hours or between market close and open.

Opening Range Breakouts: Define the first hour of trading to see the initial range.

Weekly Profiles: Set the start and end day to the same day (e.g., Friday to Friday) to visualize the entire week's range and net performance.

Built with Pine Script™ v6

Diodato 'All Stars Align' Signal (Trend Filtered)This indicator implements the Diodato "All Stars Align" strategy, a breadth-based system designed to identify high-probability reversal points by analyzing internal market strength rather than just price action. It works by monitoring Advancing versus Declining issues and volume across the exchange to detect moments of extreme market panic. When these internal breadth metrics hit specific oversold thresholds and align simultaneously with a standard Stochastic oscillator, the script signals a potential bottom.

I have modified this version to strictly enforce trend alignment. The signals are now filtered so that they will only appear if the 50 SMA is trading above the 200 SMA. This ensures that the indicator only highlights buying opportunities during established uptrends while completely filtering out signals during bearish market regimes.

You should use this tool to time entries during market pullbacks. A green cross indicates that one of the major breadth components has aligned with oversold Stochastics, while a purple cross indicates a stronger signal where both volume and issue-based breadth metrics have triggered together.

Relative Performance Areas [LuxAlgo]The Relative Performance Areas tool enables traders to analyze the relative performance of any asset against a user-selected benchmark directly on the chart, session by session.

The tool features three display modes for rescaled benchmark prices, as well as a statistics panel providing relevant information about overperforming and underperforming streaks.

🔶 USAGE

Usage is straightforward. Each session is highlighted with an area displaying the asset price range. By default, a green background is displayed when the asset outperforms the benchmark for the session. A red background is displayed if the asset underperforms the benchmark.

The benchmark is displayed as a green or red line. An extended price area is displayed when the benchmark exceeds the asset price and is set to SPX by default, but traders can choose any ticker from the settings panel.

Using benchmarks to compare performance is a common practice in trading and investing. Using indexes such as the S&P 500 (SPX) or the NASDAQ 100 (NDX) to measure our portfolio's performance provides a clear indication of whether our returns are above or below the broad market.

As the previous chart shows, if we have a long position in the NASDAQ 100 and buy an ETF like QQQ, we can clearly see how this position performs against BTSUSD and GOLD in each session.

Over the last 15 sessions, the NASDAQ 100 outperformed the BTSUSD in eight sessions and the GOLD in six sessions. Conversely, it underperformed the BTCUSD in seven sessions and the GOLD in nine sessions.

🔹 Display Mode

The display mode options in the Settings panel determine how benchmark performance is calculated. There are three display modes for the benchmark:

Net Returns: Uses the raw net returns of the benchmark from the start of the session.

Rescaled Returns: Uses the benchmark net returns multiplied by the ratio of the benchmark net returns standard deviation to the asset net returns standard deviation.

Standardized Returns: Uses the z-score of the benchmark returns multiplied by the standard deviation of the asset returns.

Comparing net returns between an asset and a benchmark provides traders with a broad view of relative performance and is straightforward.

When traders want a better comparison, they can use rescaled returns. This option scales the benchmark performance using the asset's volatility, providing a fairer comparison.

Standardized returns are the most sophisticated approach. They calculate the z-score of the benchmark returns to determine how many standard deviations they are from the mean. Then, they scale that number using the asset volatility, which is measured by the asset returns standard deviation.

As the chart above shows, different display modes produce different results. All of these methods are useful for making comparisons and accounting for different factors.

🔹 Dashboard

The statistics dashboard is a great addition that allows traders to gain a deep understanding of the relationship between assets and benchmarks.

First, we have raw data on overperforming and underperforming sessions. This shows how many sessions the asset performance at the end of the session was above or below the benchmark.

Next, we have the streaks statistics. We define a streak as two or more consecutive sessions where the asset overperformed or underperformed the benchmark.

Here, we have the number of winning and losing streaks (winning means overperforming and losing means underperforming), the median duration of each streak in sessions, the mode (the number of sessions that occurs most frequently), and the percentages of streaks with durations equal to or greater than three, four, five, and six sessions.

As the image shows, these statistics are useful for traders to better understand the relative behavior of different assets.

🔶 SETTINGS

Benchmark: Benchmark for comparison

Display Mode: Choose how to display the benchmark; Net Returns: Uses the raw net returns of the benchmark. Rescaled Returns: Uses the benchmark net returns multiplied by the ratio of the benchmark and asset standard deviations. Standardized Returns: Uses the benchmark z-score multiplied by the asset standard deviation.

🔹 Dashboard

Dashboard: Enable or disable the dashboard.

Position: Select the location of the dashboard.

Size: Select the dashboard size.

🔹 Style

Overperforming: Enable or disable displaying overperforming sessions and choose a color.

Underperforming: Enable or disable displaying underperforming sessions and choose a color.

Benchmark: Enable or disable displaying the benchmark and choose colors.

Aspects of Mars-Saturn by BTThis script displays the most commonly used aspects between Mars and Saturn. It uses a +/-2 degree orb (deviation), meaning the script shows the dates when the calculated distance between Mars and Saturn is within a 2 degree deviation of a major aspect.

Most of the astrological applications uses 3 degree or more for orb however this will cause chart overload. So please keep in mind to consider a couple of dates before or after if you want to use bigger orb.

The script includes an option to plot only the start date of sequential aspect events to reduce visual clutter and improve chart clarity. It currently covers dates from 2020 to 2030, but more will be added soon.

Currently available aspects:

Conjunction - 0 Degree

Opposition - 180 Degree

Trine - 120 Degree

Square - 90 Degree

Sextile - 60 Degree

Inconjunction - 150 Degree

Semi-Sextile - 30 Degree

Semi-Square - 45 Degree

Sesquiquadrate - 135 Degree