Straight Regression Line + Normalized Slope (Adaptive Length)Find the regression line of available candles.

It will print the slope and the normalized slope

Educational

VX Levels and Ranch Ranges with Price ConverterThis is a indicator for all Vexly subscribers to plot the following:

1. Plot SPY/SPX levels on your ES chart. Or QQQ levels on your NQ chart

2. VX levels obtained from vx_levels command. SPY on ES chart and QQQ on NQ chart

3. Ranch Range levels from the discord channel for ES and NQ chart.

You can enable/disable any of them at your discretion.

Swing TraderCore Logic

This is a swing reversal system designed to catch bounces at swing lows (LONG) and rejections at swing highs (SHORT).

Signal Flow:

Warning Phase: Yellow diamonds appear when price makes new lows/highs within the lookback period

Entry Phase: Signals fire when price bounces back after the warning (close > previous low for LONG, close < previous high for SHORT)

Swing Size Filter: Requires minimum point movement (default 50 points) between the stored high/low levels

Strengths

✅ Two-step system prevents premature entries - warns first, then confirms

✅ Alternating signals - won't fire consecutive LONGs or SHORTs

✅ Swing size requirement ensures meaningful moves

✅ Clean visuals - large labels, thick lines, clear table

Pops Dividend 7-Day RadarHow traders use it as a strategy anyway 🧠

In real life, this becomes a manual or semi-systematic strategy:

Strategy logic (human-driven):

Scan for highest yield stocks

Filter for ex-date within 7 days

Apply technical rules (trend, EMAs, support)

Enter before ex-date

Exit:

Before ex-date (momentum run-up)

On ex-date

Or after dividend (reversion play)

Indicator’s role:

“Tell me when a stock qualifies so I can decide how to trade it.”

That’s exactly what this tool does.

How we could turn this into a strategy-style framework

Even though Pine won’t let us backtest dividends properly, we can:

Build a rules-based checklist (entry/exit rules)

Create alerts that behave like strategy triggers

Combine with:

EMA trend filters

Volume conditions

ATR-based exits

Label it as:

“Pops Dividend Capture Playbook” (manual execution)

This keeps it honest, legal, and reliable.

Bottom line

🧩 Indicator = what we built

📘 Strategy = how you trade it using the indicator

⚠️ TradingView limitations prevent a true dividend strategy backtest

Multi-Timeframe CPR Pattern AnalyzerMulti-Timeframe CPR + Advanced Pattern Analyzer

A powerful, all-in-one indicator designed for professional price-action traders who use CPR (Central Pivot Range) as the core of their intraday, positional, and swing-trading strategies.

This script automatically plots Daily, Weekly, and Monthly CPR, identifies major CPR patterns, highlights Developing / Next CPR, and displays everything neatly in an interactive dashboard.

✨ Key Features

1️⃣ Daily, Weekly & Monthly CPR

Fully configurable CPR for all three timeframes

Clean plots with no vertical connector lines

Automatic zone shading

Adjustable line width, transparency, and colors

2️⃣ Support & Resistance (S1–S3, R1–R3)

Choose which timeframe’s S/R you want

Only plotted for the current day/week/month (no cluttering past charts)

Helps traders identify reaction zones and breakout levels

3️⃣ Next / Developing CPR

A unique feature rarely found in CPR indicators.

You can display:

Developing Daily CPR

Developing Weekly CPR

Next Monthly CPR (after month close)

All next/developing CPRs are plotted in a dashed style with optional transparency, plus labels:

“Developing Daily CPR”

“Developing Weekly CPR”

“Next Weekly CPR”

“Next Monthly CPR”

This allows you to anticipate the next session’s CPR in advance, a major edge for intraday, swing, and options traders.

4️⃣ Advanced CPR Pattern Detection

The script automatically detects all important CPR market structures:

📌 Narrow CPR

Uses statistical percentiles based on historical CPR width

Helps identify potential high-volatility breakout days

📌 CPR Width Contraction

Detects compression zones

Excellent for identifying trending days after tight ranges

📌 Ascending / Descending CPR

Bullish trend continuation (Ascending)

Bearish trend continuation (Descending)

📌 Virgin CPR

Highlights untouched CPR zones

Strong support/resistance zones for future days/weeks

📌 Overshoots

Detects:

Bullish Overshoot

Bearish Overshoot

Useful for understanding trend exhaustion.

📌 Breakouts

Identifies when price breaks above TC or below BC, signaling trend shifts.

📌 Rejections

Shows wick-based CPR rejections — reversal cues used by many price-action traders.

5️⃣ CPR Pattern Dashboard

A beautifully formatted dynamic table showing:

For Daily, Weekly, Monthly:

TC, Pivot, BC values

Current CPR Pattern

CPR Width with %

+ Next/Developing CPR values and patterns (for Daily/Weekly)

No need to manually calculate anything — everything is displayed in a clean, compact panel.

6️⃣ Completely Dynamic Across Timeframes

Works on all intraday, daily, weekly, and monthly charts

Automatically adjusts CPR length based on chart timeframe

Perfect for NIFTY, BANKNIFTY, FINNIFTY, stocks, crypto, forex

7️⃣ Alerts Included

Receive alerts for:

Narrow CPR formation

Virgin CPR

CPR breakouts

Pattern transitions

Great for traders who want automated monitoring.

8️⃣ Clean Chart, No Clutter

The script includes:

No vertical connecting lines

S/R only on the current period

Smart hiding of CPR on boundaries (to avoid "jump lines")

Fully toggleable features

You get a professional-grade, clutter-free CPR experience.

🎯 Why This Indicator?

This script goes beyond standard CPR tools by offering:

Next AND Developing CPR

Multi-timeframe CPR analysis

Professional CPR pattern detection

Smart dashboard visualization

Perfect setup for trend traders, reversal traders, and breakout traders

Whether you're scalping, day trading, swing trading, or doing positional analysis — this tool gives you context, structure, and precision.

📌 Recommended Use Cases

Intraday index trading (NIFTY, BANKNIFTY, NIFTY 50 Stocks)

Swing trading stocks

Crypto CPR analysis

Options directional setups

CPR-based breakout and reversal strategies

Trend continuation identification

Understanding volatility days (Narrow CPR Days)

⚠️ Disclaimer

This is a technical tool for chart analysis and does not guarantee profits. Always combine CPR analysis with price action, volume, and risk management.

S&R Detector by Rakesh SharmaSupport & Resistance Auto-Detector

Automatically identifies key Support and Resistance levels with strength ratings

✨ Key Features:

🎯 Intelligent S/R Detection

Automatically finds Support and Resistance levels based on swing highs/lows

Shows strength rating (Very Strong, Strong, Medium, Weak)

Displays number of touches at each level

📅 Key Time-Based Levels

Previous Day High/Low (PDH/PDL) - Blue lines

Previous Week High/Low (PWH/PWL) - Purple lines

Optional Round Numbers for psychological levels

⚙️ Fully Customizable

Adjust sensitivity (5-20 pivot length)

Filter by minimum touches (1-10)

Control maximum levels displayed (3-20)

Optional S/R zones (shaded areas)

📊 Live Dashboard

Shows nearest Support/Resistance

Distance to key levels

Total S/R levels detected

🔔 Smart Alerts

PDH/PDL breakout signals

Visual markers on chart

Perfect for: Intraday traders, Swing traders, Price action analysis

RSI Multi-TimeFrame [PACHI]This will show a Table with multiple time frames RSI levels.

> 68 the table cell will be red for given timeframe to indicate overbought

< 35 the table cell will be green for given timeframe to indicate oversold

there are few settings you can play with. if you have any suggestions, let me know.

// Pachi

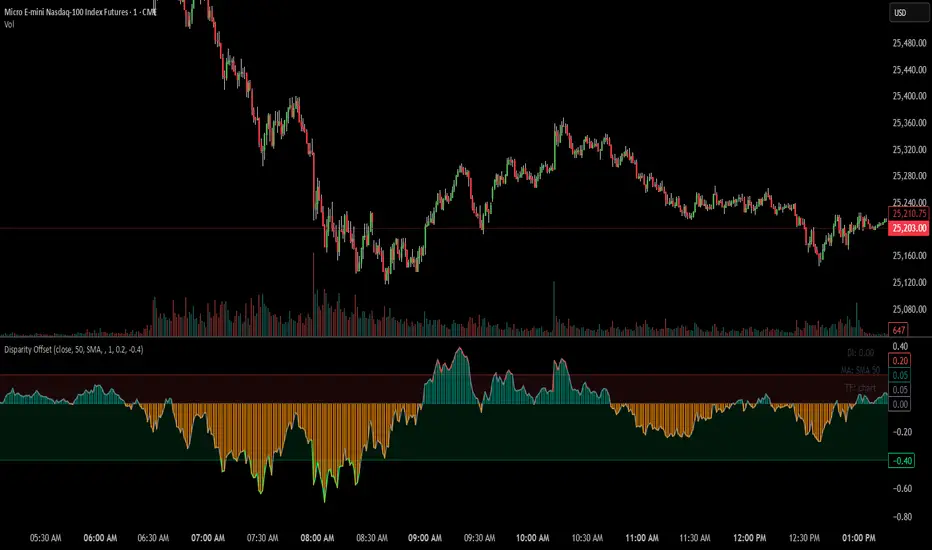

Disparity Offset [WizardTrendsInc]Disparity Offset

Description

Disparity Offset measures how far price is offset from a selected moving average, expressed as a percentage. It shows whether price is trading above or below its average and by how much, helping visualize price extension, balance, and deviation from the mean. The indicator oscillates around a zero line, where zero represents price being aligned with the moving average.

How to Use Disparity Offset

Zero Line (0%)

When the Disparity Offset is near zero, price is close to the moving average, suggesting equilibrium.

Positive Values

Values above zero indicate price is above the moving average. Larger positive readings show stronger upward offset from the average.

Negative Values

Values below zero indicate price is below the moving average. Larger negative readings show stronger downward offset

Upper & Lower Offset Zones

The configurable upper and lower percentage levels highlight when price is relatively far from the moving average. Movement back toward the zero line can be used to study mean-reversion behavior.

Visual Aids

Histogram bars show direction and intensity of the offset

Shaded zones emphasize overextended conditions

Optional markers display crossings of offset levels and the zero line for observation and learning

"Disclaimer: This indicator is intended for educational purposes only and does not constitute financial advice. Trading involves significant risk, and users should perform their own research and consult with a licensed financial advisor before making any trading decisions.

Visible Range / POC / Volume / SNR Detector PROVisible Range POC & Volume SNR Detector PRO

Visible Range POC & Volume SNR Detector PRO is a professional-grade volume-based market structure tool designed to identify institutional Support & Resistance zones, Point of Control (POC), and Value Areas directly from the visible chart range.

This indicator goes beyond traditional swing highs and lows by analyzing real traded volume, revealing where large players are active, where price finds fair value, and where high-probability reactions are most likely to occur.

🔍 Core Features

📊 Visible Range Volume Profile

🔹Builds a full Volume Profile using only the visible chart range

🔹Splits price into configurable precision bins for maximum accuracy

🔹Detects true volume clusters instead of subjective price levels

🎯 Point of Control (POC)

🔹 Automatically identifies the highest-volume price level

🔹Acts as a magnet price where market participants agree on value

🔹Fully customizable line style, width, and color

🔹 Optional label with timeframe + price + volume (K / M / B)

📦 Value Area (VAH / VAL)

* Calculates Value Area High & Low around the POC

* Default **70% volume range** (institutional standard)

* Optional Value Area fill for clear fair-value visualization

* Helps distinguish **range conditions vs trending moves**

🧱 Volume-Based Support & Resistance Zones

🔹Automatically detects high-impact S&R zones from volume behavior

🔹Zones are visually classified by strength:

🔹 🟢 Strong

🔹 🟡 Medium

🔹 🔴 Weak

🔹Clean box rendering with customizable borders:

🔹 Solid / Dashed / Dotted

🔹 Zones extend dynamically into the future for planning trades

🔄 Dynamic Flip Logic (PRO Standard)

🔹 Advanced Dynamic Flip system:

🔹 Support ➜ Resistance after a breakdown

🔹Resistance ➜ Support after a breakout

🔹 Reflects real market structure shifts

🔹Eliminates outdated static levels

🔁 True Retest & Zone Intelligence

🔹Each zone includes detailed contextual data:

🔹🔄 True Retest Count (price leaves zone and comes back)

🔹⏳ Zone Age (minutes / hours / days)

🔹💪 Strength Classification

🔹🔁 Flip Status

🔹⏱️ Timeframe

🔹💲 Exact price level

🔹All information is displayed in a single clean label.

🔔 Smart Alerts System

🔹Never miss key interactions:

🔹🟢 Touch Alert — price enters a zone

🔹⬇️⬆️ Break Alert — zone failure or breakout

🔹🔄 Retest Alert — classic break & retest setup

Alerts trigger on confirmed bars to reduce noise and false signals.

📋 Professional Dashboard

🔹At-a-glance market overview:

🔹Total Support & Resistance zones

🔹🎯 POC level

🔹📦 VA High / VA Low

🔹💪 Strong / Medium / Weak zone distribution

🔹📍 Nearest Support & Resistance

🔹📏 Distance to key levels

🔹 🎨 Auto / Dark / Light theme support

🔹 📐 Adjustable size & position

GIX-Treid-2Timeframes: M15 – H1 (and higher)

An advanced SuperTrend, more stable and more intelligent, based on statistical calculations, not market noise.

It calculates a statistical moving average, significantly smoother than EMA or SMA.

It builds an adaptive channel around this average, using fixed pip/tick steps (not a classic ATR).

The trend changes only when price breaks the channel, not on minor fluctuations.

The main line moves in discrete steps, not continuously → no repaint and no whipsawing.

Line color indicates direction:

Green = bullish trend

Red = bearish trend

HTF Candle BoxFor HTF pattern in real time LTF view.

Used for AMD pattern, to always keep eye on the progress of HTF, but with stay in the LTF.

It will improve your confirmations.

MACD X SignalsThis is a fundamental signal indicator based on MACD crossovers. It enhances the standard MACD by adding visual labels that classify signals based on their location relative to the Zero Line. This helps identify whether a trend is reversing, continuing, or potentially overextended.

Signal Legend:

B (Reversal): Bullish crossover in the Negative Zone .

B+ (Neutral): Bullish crossover in the Middle Zone .

B- (Trend): Bullish crossover in the Positive Zone

S : MACD crossing down (Bearish signal).

Daily Auto-Fib Zones (Custom Colors)This indicator automatically draws daily Fibonacci-based zones using the current session’s high and low. The levels update dynamically as new price action forms and include optional visual regions for several commonly referenced retracement percentages.

Features include:

• Automatic detection of the daily high and low

• Real-time updates throughout the session

• Optional zones for 0.11–0.17, 0.5, and 0.618–0.786 levels

• Custom color inputs for every line and zone

• Dynamic boxes that expand with the day’s range

• Lightweight visual layout with toggleable components

The tool is intended purely for chart visualization. It does not provide signals or trade recommendations.

Weekly Auto-Fib Zones (Custom Colors) This script automatically plots weekly Fibonacci-based zones using the current week’s high and low. It updates dynamically as new price action forms and provides optional visual regions for key retracement areas.

The indicator includes:

• Weekly high/low anchor lines

• Optional 0.11–0.17 zones

• Optional 0.5 midpoint (premium/discount)

• Optional 0.618–0.786 retracement band

• Customizable colors for each level

• Dynamic boxes that expand as the week progresses

It is designed as a visual aid for identifying weekly ranges, contextual zones, and potential areas of interest based solely on Fibonacci percentages. No signals, alerts, or trading recommendations are included.

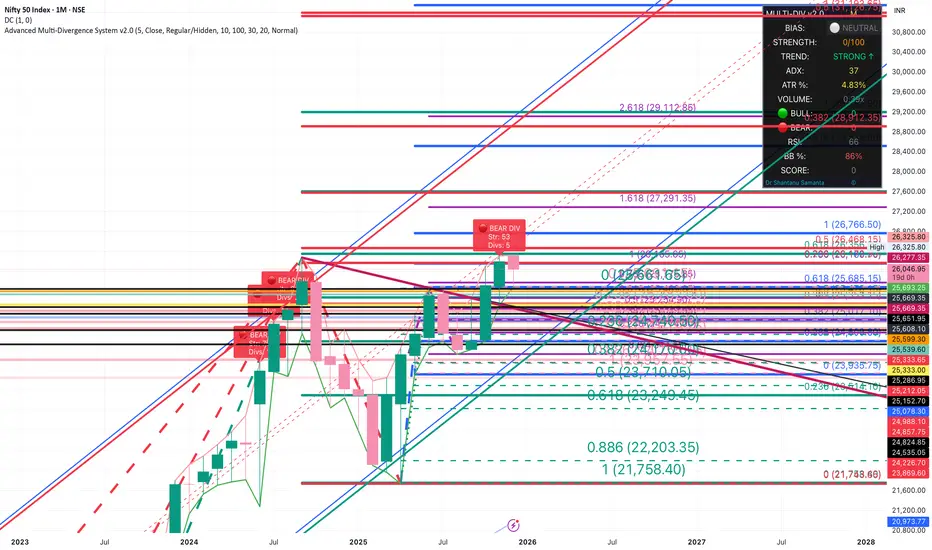

Critical Advanced Multi-Divergence Dashboard

Complete Dashboard Interpretation Guide

Dashboard Metrics Explained

1. Timeframe

What it shows: Current chart timeframe (15m, 1H, 4H, 1D, etc.)

How to interpret:

The script auto-detects your chart timeframe

Higher timeframes (4H, 1D) = more reliable signals but fewer trades

Lower timeframes (5m, 15m) = more signals but higher noise

Best practice: Use multiple timeframes - get signal on 1H, confirm on 15m for entry

2. Signal Bias: BULLISH / BEARISH / NEUTRAL

What it shows: Overall market direction based on divergence consensus

Color coding:

🟢 BULLISH (Green) = Net strength > +10 → Expect upward move

🔴 BEARISH (Red) = Net strength < -10 → Expect downward move

⚪ NEUTRAL (Gray) = Net strength between -10 to +10 → No clear direction

How to interpret:

BULLISH: Multiple bullish divergences detected → Look for LONG entries

BEARISH: Multiple bearish divergences detected → Look for SHORT entries

NEUTRAL: Conflicting signals or weak divergences → WAIT, don't trade

Trading Action:

BULLISH + Strength > 60 = Strong BUY signal

BEARISH + Strength > 60 = Strong SELL signal

NEUTRAL = Stay out, wait for clarity

3. Signal Strength: 0-100

What it shows: Quantified power of the divergence signal

Strength Scale:

🔴 0-30 (Red): Weak signal → Don't trade

🟠 31-60 (Orange): Moderate signal → Trade with caution, reduce position size

🟢 61-100 (Green): Strong signal → High confidence trade

Calculation factors:

Number of divergences detected

Volume confirmation (1.3x multiplier if high volume)

Trend filter (ADX reduces counter-trend signals by 40%)

Weighted scoring (volume-based indicators get 1.5x weight)

How to use:

Strength > 70 + ADX < 20 = Best reversal trades

Strength > 60 + Volume HIGH = Excellent entry

Strength < 40 = Skip the trade

Example Scenarios:

Strength = 85 → Take full position size

Strength = 55 → Take 50% position, tight stop loss

Strength = 25 → No trade, wait for better setup

4. Quality Score: 0-100

What it shows: Overall reliability and confidence rating

Components (max 100 points):

Divergence count (40 points): More indicators confirming = higher quality

Volume confirmation (20 points): High volume adds 20, normal adds 10

Trend alignment (20 points): Signal aligning with trend = 20, against trend but weak ADX = 15

Detection timing (20 points): Confirmed signals = 20, early detection = 15

Quality Tiers:

80-100: Excellent - High probability setup

60-79: Good - Tradeable with proper risk management

40-59: Fair - Only for experienced traders

Below 40: Poor - Avoid trading

How to use:

Quality > 75 + Strength > 60 = Grade A setup

Quality > 60 + Strength > 50 = Grade B setup (reduce size)

Quality < 50 = Don't trade regardless of strength

5. Bullish Divs: 3R/2H (Example)

What it shows: Count of bullish divergences detected

R = Regular divergences (price LL, indicator HL)

H = Hidden divergences (price HL, indicator LL)

Interpretation:

Regular divergences = Reversal signals (more important)

Hidden divergences = Continuation signals (trend confirmation)

Examples:

4R/1H → Strong bullish reversal expected

1R/3H → Bullish trend continuation likely

5R/0H → Very strong reversal setup

Trading Logic:

High R count = Look for trend reversal

High H count = Trend is strong, look for pullback entries

R+H both high = Very strong signal, major move expected

6. Bearish Divs: 2R/1H (Example)

Same logic as Bullish Divs but for downside:

2R/1H → Moderate bearish reversal setup

0R/4H → Strong downtrend continuation

4R/3H → Extremely strong bearish signal

7. ADX (Trend): 35

What it shows: Average Directional Index - measures trend strength

ADX Scale:

0-20: Weak or no trend → Range-bound market

20-25: Emerging trend → Early trend formation

25-50: Strong trend → Trend is established

50-75: Very strong trend → Major directional move

75+: Extremely strong trend → Parabolic move, be cautious

Color Coding:

🟠 Orange (ADX > threshold): Strong trending market

⚪ Gray (ADX < threshold): Weak trend/ranging

How to interpret:

ADX < 20 + BULLISH Signal = Best for reversal trades (range breakout)

ADX > 25 + BEARISH Signal = Counter-trend, risky (signal strength reduced 40%)

ADX > 40 + Signal against trend = Dangerous, skip

ADX < 20 + High Strength = Perfect reversal setup

Trading Examples:

ADX = 15, BULLISH strength 75 → Perfect buy at bottom

ADX = 45, BEARISH strength 60 → Caution: Market in strong uptrend, bearish signal gets discounted

ADX = 50, BULLISH strength 80 → Trend continuation: Pullback in uptrend, good long entry

8. Volume: HIGH / Normal

What it shows: Current volume vs 20-period moving average

Volume Status:

🟡 HIGH (Yellow): Volume > 1.5x average → Signal multiplied by 1.3x

⚪ Normal (Gray): Volume ≤ 1.5x average → Signal multiplied by 0.8x

Why it matters:

High volume = More participation = More reliable signal

Normal/low volume = Weak conviction = Less reliable

Trading Rules:

HIGH volume + Strong signal = Take trade immediately

Normal volume + Strong signal = Wait for volume confirmation

HIGH volume + Weak signal = Still tradable (volume validates)

Normal volume + Weak signal = Definitely skip

Example:

Strength 50 + HIGH volume → Effective strength = 65 (tradable)

Strength 50 + Normal volume → Effective strength = 40 (skip)

9. Volatility: 2.35%

What it shows: ATR (Average True Range) as percentage of price

Volatility Scale:

< 1%: Very low volatility → Tight ranges, breakout coming

1-2%: Normal volatility → Standard market conditions

2-3%: Elevated volatility → Bigger moves expected

> 3%: High volatility → Large swings, wider stops needed

How to use:

Low volatility (< 1%) = Tighten stops, smaller targets

Normal (1-2%) = Standard position sizing

High (> 3%) = Reduce position size, wider stops

Impact on trading:

High volatility → Script auto-adjusts pivot periods (better divergence detection)

Stop loss placement: Use ATR × 2 for stop distance

Position sizing: Reduce size in high volatility

10. Detection: EARLY / Confirmed

What it shows: Whether signal detected before or after pivot confirmation

Detection Modes:

🟡 EARLY (Yellow): Signal detected before pivot confirms → Earlier entry but slightly less reliable

🟢 Confirmed (Green): Signal after pivot confirmation → More reliable but later entry

Trade-off:

EARLY mode:

+ Enter 2-5 bars earlier

+ Better risk/reward ratio

- 10-15% more false signals

Confirmed mode:

+ Higher reliability

+ Better for conservative traders

- May miss 10-20% of move

How to use:

Aggressive traders: Use EARLY mode + higher quality threshold (>70)

Conservative traders: Use Confirmed mode + moderate quality (>60)

🎯 Complete Trading Decision Matrix

STRONG BUY Signal ✅

Signal Bias: BULLISH

Signal Strength: > 70

Quality Score: > 75

Bullish Divs: ≥ 3 (preferably high R count)

ADX: < 25 (weak trend/reversal) OR > 30 with DI+ > DI-

Volume: HIGH

Action: Enter LONG with full position

STRONG SELL Signal ✅

Signal Bias: BEARISH

Signal Strength: > 70

Quality Score: > 75

Bearish Divs: ≥ 3 (preferably high R count)

ADX: < 25 (weak trend/reversal) OR > 30 with DI- > DI+

Volume: HIGH

Action: Enter SHORT with full position

Moderate Trade ⚠️

Signal Strength: 50-70

Quality Score: 60-75

Volume: Normal

Action: Enter with 50% position size, tight stop loss

NO TRADE ❌

Signal Bias: NEUTRAL

Signal Strength: < 50

Quality Score: < 60

ADX: > 40 (signal against strong trend)

Volume: Normal + Strength < 50

Action: Stay out, wait for better setup

📊 Real Trading Examples

Example 1: Perfect Bullish Setup

Timeframe: 1H

Signal Bias: BULLISH 🟢

Signal Strength: 82/100 🟢

Quality Score: 88/100

Bullish Divs: 5R/2H (excellent)

Bearish Divs: 0R/0H

ADX: 18 (weak trend, perfect for reversal)

Volume: HIGH 🟡

Volatility: 1.8%

Detection: EARLY 🟡

INTERPRETATION: Grade A+ setup

- Strong bullish consensus (5 regular divergences)

- Low ADX = perfect reversal condition

- High volume confirms the signal

- Quality 88 = highly reliable

ACTION:

✅ Enter LONG immediately with full position

✅ Stop loss: 2 × ATR below entry (3.6%)

✅ Target: Previous swing high or 2:1 R/R

Example 2: Risky Counter-Trend Signal

Timeframe: 15m

Signal Bias: BEARISH 🔴

Signal Strength: 55/100 🟠

Quality Score: 62/100

Bearish Divs: 2R/1H

ADX: 45 (very strong uptrend)

Volume: Normal

Detection: EARLY

INTERPRETATION: Dangerous setup

- ADX 45 = strong uptrend in place

- Bearish signal is counter-trend

- Script already reduced strength by 40%

- Moderate quality, normal volume

ACTION:

❌ SKIP this trade

⏸️ Wait for ADX to drop below 25

⏸️ Or wait for bearish strength > 70 with HIGH volume

Example 3: Wait and Watch

Signal Bias: NEUTRAL ⚪

Signal Strength: 35/100 🔴

Quality Score: 48/100

Bullish Divs: 1R/1H

Bearish Divs: 1R/0H

ADX: 22

Volume: Normal

INTERPRETATION: Conflicting signals

- Both bullish and bearish divergences present

- Low strength and quality

- No clear direction

ACTION:

⏸️ Don't trade - wait for clarity

👀 Watch for one side to dominate

📊 Check higher timeframe for context

🎓 Pro Tips for Dashboard Reading

Check Multiple Timeframes:

Signal on 4H + confirmation on 1H = Best trades

Higher TF gives direction, lower TF gives entry

Volume is King:

Never ignore HIGH volume signals (even if strength is moderate)

Be extra cautious with normal volume + weak signals

ADX Context Matters:

ADX < 20 + Divergence = Reversal opportunity

ADX > 40 + Counter-trend divergence = Dangerous

Quality Over Strength:

Quality 80 + Strength 60 > Quality 50 + Strength 80

High quality ensures the signal is real, not noise

Regular vs Hidden Divergences:

High R count = Reversal expected (more important)

High H count = Continuation (use for re-entries)

Early Detection Trade-off:

Use EARLY for swing trading (better R/R)

Use Confirmed for day trading (higher accuracy)

⚡ Quick Decision Flowchart

Step 1: Check Signal Bias

├─ NEUTRAL? → ❌ Don't trade

└─ BULLISH/BEARISH? → Continue

Step 2: Check Signal Strength

├─ < 50? → ❌ Don't trade

├─ 50-60? → Reduce position 50%

└─ > 60? → Continue

Step 3: Check Quality Score

├─ < 60? → ❌ Don't trade

└─ ≥ 60? → Continue

Step 4: Check ADX

├─ > 40 AND counter-trend? → ❌ Don't trade

└─ < 40 OR with-trend? → Continue

Step 5: Check Volume

├─ HIGH → ✅ Take trade (boost confidence)

└─ Normal → Check if strength > 60, then ✅ trade

Step 6: Position Sizing

├─ Strength > 70 + Quality > 75 → 100% position

├─ Strength 60-70 + Quality 60-75 → 75% position

└─ Strength 50-60 + Quality 60-70 → 50% position

This dashboard gives you a complete edge in divergence trading by quantifying what was previously subjective! 🚀

Only for Educational purpose

Capitulation Finder(Sahebson)The Capitulation Finder detects potential exhaustion points in trend moves by identifying price dislocations combined with surging volume and extreme RSI levels.

A bullish capitulation signal is generated when price drops significantly below a user-defined moving average while RSI is oversold and volume spikes above the average.

A bearish capitulation signal is triggered under the opposite conditions—price extended above the moving average, RSI overbought, and volume elevated.

Additional confirmation signals highlight persistent overbought or oversold conditions with volume strength. This tool helps traders pinpoint possible reversal zones during volatile market conditions.

Critical Advanced Multi-Divergence System v2.0Auto calculates 15 indicators , assigns different strength to each and auto adds up to give a Final bias . Auto detects scrip & time frame . Sums up everything in a Dashboard. For educational use only

CandleMapTF - Automatic Candle Structure ToolDescription:

This Pine Script creates an "Automatic Candle Structure Tool" for TradingView that visually manages market structure and dealing ranges across multiple timeframes.

All elements, including colors, opacity, and displayed levels are fully customizable.

Disclaimer:

This script is for educational and informational purposes only and does not

constitute financial advice, investment advice, or a trading recommendation.

Use at your own risk.

Prime -Hub Prime -Hub is a comprehensive, all-in-one technical analysis toolkit designed for professional Intraday and Swing traders on Nifty, BankNifty, and Stocks. This script consolidates three powerful institutional logic systems into a single, clean interface, replacing the need for multiple indicators.

Disclaimer: This tool is for educational and analytical purposes only. Past performance does not guarantee future results. Trading involves substantial risk.

Institutional Dominance/Trapped Trader Profile @MaxMaserati 3.0📊 Institutional Dominance & Trapped Trader Delta Profile

@MaxMaserati 3.0

═════════════════════════════════════════════════════════════

🎯 OVERVIEW

The IDT Auction Profile is a professional-grade volume order flow analysis tool that reveals where institutional traders hold Positional Advantage and where retail participants are Trapped. Unlike traditional Volume Profile indicators, the IDT Profile integrates Volume Point Delta (VPD) analysis with advanced pattern recognition to identify the exact price levels where profitable institutional positions create support/resistance, and where losing positions are forced to exit.

This indicator answers the critical questions: Who is in profit? Who is trapped? And where will they defend or exit their positions?

═════════════════════════════════════════════════════════════

✨ FEATURES

═════════════════════════════════════════════════════════════

⚡ Quick Presets - One-click configuration for:

• Scalper (1m-5m): 75 bars, 50 rows, ★3 confluence

• Day Trader (15m-1h): 150 bars, 60 rows, ★3 confluence

• Swing Trader (4h-D): 300 bars, 80 rows, ★4 confluence

🔔 Price Alerts - Get notified when price touches:

• VAH (Value Area High) - Resistance zone

• VAL (Value Area Low) - Support zone

• Adjustable sensitivity (0.05% - 1.0%)

📏 POC Line Extensions - Historical context lines extending left from key institutional levels

👻 Previous Session POCs - Dotted reference lines showing prior period levels (carry-over zones)

📊 Real-Time Statistics Panel:

• Total Volume

• Net Delta

• Buy/Sell Pressure %

🎨 Visual Enhancements:

• Column dividers for clarity

• Transparency controls

• Profile auto-hide when price moves away

• Cached color schemes for 30% performance boost

═════════════════════════════════════════════════════════════

🧠 CORE CONCEPT: DOMINANCE VS TRAPPED POSITIONING

═════════════════════════════════════════════════════════════

The indicator categorizes all market participants into two strategic positions based on their entry price relative to current market price:

📍 ABOVE CURRENT PRICE (Resistance Zones)

🔴 Aggressive Sellers in Profit - Sold higher, currently winning. Will defend positions or add to winners.

🟥 Trapped Buyers at Loss - Bought higher, currently losing. Must exit at breakeven, creating resistance.

📍 BELOW CURRENT PRICE (Support Zones)

🟢 Aggressive Buyers in Profit - Bought lower, currently winning. Will defend positions or add to winners.

🟩 Trapped Sellers at Loss - Sold lower, currently losing. Must cover at breakeven, creating support.

⚡ MAXIMUM CONFLUENCE ZONES

When Dominant (Profitable) and Trapped (Loss) positions align at the same level, you get the strongest support/resistance zones:

🟧 Orange Boxes (Above Price) = Aggressive Sellers + Trapped Buyers = STRONGEST RESISTANCE

🟨 Yellow Boxes (Below Price) = Aggressive Buyers + Trapped Sellers = STRONGEST SUPPORT

═════════════════════════════════════════════════════════════

📊 VOLUME ANALYSIS COLUMNS

═════════════════════════════════════════════════════════════

1️⃣ VPD Column (Volume Point Delta)

Net aggressive pressure at each price level (Buying Volume - Selling Volume)

- Bullish Delta (Green): Buyers dominated the auction at this level

- Bearish Delta (Red): Sellers dominated the auction at this level

- Smart Coloring: Automatically highlights institutional patterns

2️⃣ VPS Column (Volume Point of Sell - ASK Volume)

Aggressive buying volume that "lifted the offer" by hitting ask prices

- Represents participants who paid the ask price to enter long

- When price is below this level = These buyers are in profit

- When price is above this level = These sellers who got hit are in profit

- Shows institutional bid volume absorption

3️⃣ VPB Column (Volume Point of Buy - BID Volume)

Aggressive selling volume that "hit the bid" by taking bid prices

- Represents participants who sold at bid price to enter short

- When price is above this level = These sellers are in profit

- When price is below this level = These buyers who got hit are in profit

- Shows institutional ask volume absorption

4️⃣ SVP Column (Optional - Session Volume Profile)

Traditional combined volume profile without bid/ask separation

═════════════════════════════════════════════════════════════

🔍 ADVANCED INSTITUTIONAL PATTERNS DETECTION

═════════════════════════════════════════════════════════════

The indicator uses statistical analysis (standard deviation, moving averages, hit counting) to identify institutional footprints:

⚡ Failed Auctions - "BUYERS TRAPPED" or "SELLERS TRAPPED" labels

• High volume entered, but price immediately reversed

• Creates extreme concentrations of losing positions

• Trading Implication: High-probability reversal zones where trapped participants must exit

📈 Volume Spikes - Bright green/red bars in VPD column

• Volume exceeds average by 2+ standard deviations

• Represents aggressive institutional entry

• Trading Implication: Potential trend continuation or setup for failed auction

🛡️ Absorption Zones - Yellow/Orange colored bars

• Large passive orders absorbing aggressive volume without price movement

• Indicates accumulation (bullish) or distribution (bearish)

• Trading Implication: Institutional positioning before major moves

🧊 Iceberg Orders - Cyan colored bars with high hit counts

• Same price level shows repeated volume without clearing

• Reveals hidden institutional limit orders split into small pieces

• Trading Implication: Strong liquidity magnets, price often returns here

💜 Volume Exhaustion - Purple colored bars

• Sharp volume drop (50%+) after spike

• Momentum exhausted, participants depleted

• Trading Implication: Potential reversal or consolidation ahead

═════════════════════════════════════════════════════════════

🎨 SMART INSTITUTIONAL COLORING

═════════════════════════════════════════════════════════════

Colors bars based on detected patterns vs simple red/green:

🟨 Yellow = Bullish battles won (buyers + trapped sellers)

🟧 Orange = Bearish battles won (sellers + trapped buyers)

🔵 Cyan = Iceberg orders (hidden liquidity)

🟣 Purple = Large passive orders

🟢 Bright Green = Buying spikes (institutional aggression)

🔴 Bright Red = Selling spikes (institutional aggression)

═════════════════════════════════════════════════════════════

⭐ CONFLUENCE SCORING SYSTEM

═════════════════════════════════════════════════════════════

Each price level receives 1-5 stars based on:

★★ Volume spike presence (+2 stars)

★ Absorption pattern (+1 star)

★ Large passive orders (+1 star)

★ Proximity to Value Area (+1 star)

★★ Iceberg detection (+2 stars)

★★ Failed auction (+2 stars)

Minimum Signal Strength filter lets you show only levels with ★3+ confluence for highest-quality signals.

═════════════════════════════════════════════════════════════

🎯 VALUE AREA ANALYSIS

═════════════════════════════════════════════════════════════

VAH (Value Area High) - Blue Line

- Top of the 70% volume acceptance zone

- Price at VAH often rejects downward (resistance)

- Alert triggers when price approaches

VAL (Value Area Low) - Red Line

- Bottom of the 70% volume acceptance zone

- Price at VAL often bounces upward (support)

- Alert triggers when price approaches

Trading Applications:

- Price outside Value Area → Mean reversion opportunity

- Price breaks VA with volume → Trend continuation

- Price oscillates within VA → Range-bound, fade extremes

- Previous session VA lines show carryover levels

═════════════════════════════════════════════════════════════

📋 EXPECTED PRICE BEHAVIOR AT KEY LEVELS

═════════════════════════════════════════════════════════════

⚠️ IMPORTANT: These are observed behavioral patterns for educational purposes and backtesting research. Always validate with 250-500+ backtest trades before risking capital.

1️⃣ POC BOX ZONES (Highest Statistical Relevance)

🟨 Yellow Boxes (Below Current Price - SUPPORT)

Expected Behavior:

- Price approaching from above typically encounters buying pressure

- Both profitable institutional buyers and trapped short sellers create demand

- Common reaction: Price slows, consolidates, or bounces

- Failed bounces often lead to rapid breakdown (trapped buyers capitulate)

What Often Happens:

- Initial dip into zone → Weak bounce attempt

- Second test → Stronger bounce (trapped sellers covering + buyers defending)

- Break below → Quick acceleration as both groups exit

🟧 Orange Boxes (Above Current Price - RESISTANCE)

Expected Behavior:

- Price rallying into zone typically encounters selling pressure

- Both profitable institutional sellers and trapped long buyers create supply

- Common reaction: Price stalls, consolidates, or rejects

What Often Happens:

- Initial push into zone → Weak rejection

- Second test → Stronger rejection (trapped buyers exiting + sellers defending)

- Break above → Quick acceleration as resistance becomes support

2️⃣ FAILED AUCTION ZONES

"SELLERS TRAPPED" Labels (Below Price):

- High-volume selling that immediately reversed = maximum trapped shorts

- When price returns, trapped sellers face pressure to cover

- Typical pattern: Price approaches → Initial hesitation → Sharp bounce

"BUYERS TRAPPED" Labels (Above Price):

- High-volume buying that immediately failed = maximum trapped longs

- Price returning forces trapped buyers to exit at breakeven

- Typical pattern: Price approaches → Distribution → Rejection

3️⃣ VALUE AREA DYNAMICS

Price Outside Value Area (VAH/VAL):

- Price beyond 70% volume zone = statistical outlier

- Two outcomes: Mean reversion OR trend continuation

- Key differentiator: Presence of confluence zones

Mean Reversion Pattern (No Strong Confluence):

- Price extends 1-2% beyond VA → Typically reverts toward POC

- Weak volume on extension → Higher probability of reversal

Breakout Pattern (With ★4+ Confluence):

- Price breaks VA with institutional patterns → Often continues

- Strong volume + confluence = New value area forming

4️⃣ ICEBERG ORDER BEHAVIOR

Cyan Bars with High Hit Counts:

- Repeated volume at same level = Large hidden order absorbing

- Price typically "tests" iceberg multiple times before resolution

- Two outcomes: Absorption complete (break) OR rejection (bounce)

5️⃣ VOLUME SPIKE PATTERNS

Bright Green/Red Bars (Institutional Aggression):

- Extreme delta spikes indicate institutional entry

- Trend Continuation Spikes: Spike aligned with trend = Often continues

- Exhaustion Spikes: Spike against trend = Failed auction forming

═════════════════════════════════════════════════════════════

⚙️ CONFIGURATION GUIDE

═════════════════════════════════════════════════════════════

🎯 QUICK START

1. Select your trading style preset (Scalper/Day/Swing)

2. Enable VAH/VAL alerts in settings

3. Adjust alert sensitivity (0.1% recommended)

4. Add alert condition to TradingView alert system

📊 CORE SETTINGS

- Lookback Period: How many bars to analyze

- Scalping: 50-100 bars

- Day Trading: 100-200 bars

- Swing Trading: 200-500 bars

- Price Row Granularity: How finely to divide price

- 40-50 rows = Fast markets

- 60-80 rows = Balanced (RECOMMENDED)

- 100+ rows = Maximum precision

- Minimum Signal Strength: Filter weak signals

- ★3 = Balanced quality/quantity (RECOMMENDED)

- ★4-5 = Highest quality, fewer opportunities

🎨 VISUAL SETTINGS

- Color Theme: Classic/Institutional/Monochrome/Bold/Minimal/Custom

- Smart Coloring: ON (recommended) - Shows institutional patterns

- Transparency: Adjust profile opacity

- Column Dividers: Visual separators between columns

- POC Extensions: Show historical level significance

📈 ADVANCED FEATURES

- Auto-Hide Distance: Hide profile when price moves X% away

- Statistics Panel: Real-time metrics display

- Previous POCs: Show prior session levels

- Alert Sensitivity: How close price must be to trigger alerts

═════════════════════════════════════════════════════════════

💡 BEST PRACTICES

═════════════════════════════════════════════════════════════

✅ Start with defaults (200 lookback, 60 rows, ★3 confluence, Smart Coloring ON)

✅ Focus on POC boxes first - These are your highest-probability zones

✅ Combine with price action - Use the profile to explain WHY support/resistance exists

✅ Watch for alignment - Yellow/Orange boxes = strongest levels

✅ Respect failed auctions - "TRAPPED" labels are extreme reversal setups

✅ Use Value Area for context - Price outside VA = mean reversion opportunity

✅ Trust confluence scores - ★4-5 signals are institutional-grade setups

✅ Set up alerts for VAH/VAL touches - Don't miss key levels

✅ Check previous session POCs - Institutions defend same zones across sessions

✅ Monitor statistics panel - Understand market conviction in real-time

═════════════════════════════════════════════════════════════

🔧 TECHNICAL SPECIFICATIONS

═════════════════════════════════════════════════════════════

Calculation Method: Enhanced delta using OHLC and volume with wick ratio analysis

Update Frequency: Real-time on every bar close

Performance: Optimized with color caching and pre-calculated values (~30% faster)

Max Capacity: Supports up to 1500 bars lookback and 250 price rows

Compatibility: Works on all symbols and timeframes

Memory Usage: Efficient array management with proper initialization

Alert System: Built-in VAH/VAL touch detection with visual markers

═════════════════════════════════════════════════════════════

🎯 UNIQUE VALUE PROPOSITION

═════════════════════════════════════════════════════════════

Unlike standard Volume Profile indicators that only show where volume occurred, the IDT Auction Profile:

✅ Separates bid vs ask volume to reveal true order flow

✅ Identifies who is profitable vs who is trapped at each level

✅ Detects institutional patterns (icebergs, absorption, failed auctions)

✅ Calculates confluence scores combining multiple factors

✅ Provides clear POC boxes showing exact institutional positioning

✅ Maps positional advantage rather than just volume density

✅ Alerts you to key level touches in real-time

✅ Shows historical context with POC extensions

✅ Displays live statistics for market conviction

This transforms Volume Profile from a historical volume chart into a strategic positioning map showing institutional dominance and trapped participants.

═════════════════════════════════════════════════════════════

📖 HOW TO INTEGRATE WITH YOUR STRATEGY

═════════════════════════════════════════════════════════════

✅ PROPER USES:

- Entry refinement within your existing setups

- Intelligent stop placement beyond institutional levels

- Objective profit targets at next confluence zones

- Trade filtering (only take setups at ★4+ zones)

- Understanding market positioning before entry

- Alert-based monitoring of key support/resistance levels

❌ WHAT IT CANNOT DO:

- Predict direction with certainty

- Replace risk management

- Account for news/external events

- Guarantee profitability

- Work in all market conditions

═════════════════════════════════════════════════════════════

📚 DEVELOPMENT PATH (12-16 Weeks)

═════════════════════════════════════════════════════════════

Weeks 1-2: Observation Only

- Watch price behavior at key levels

- Document patterns without trading

- Set up alerts and observe responses

Weeks 3-8: Paper Trading

- Simulate trades, track all metrics

- Minimum 100 paper trades

- Test different confluence thresholds

Weeks 9-16: Small Size Testing

- Minimal capital, real market conditions

- Continue tracking, refine rules

- Adjust alert sensitivity based on results

After Proven Edge you could potentially include it in your set-up

═════════════════════════════════════════════════════════════

⚠️ CRITICAL DISCLAIMERS

═════════════════════════════════════════════════════════════

⚠️ Past volume ≠ Future price action

⚠️ Institutional positions change rapidly - these are static snapshots

⚠️ No indicator works 100% - risk management is mandatory

⚠️ Market conditions change - adapt your approach

⚠️ Backtest with YOUR style, YOUR timeframe, YOUR risk tolerance

⚠️ Alerts are notifications, not trade signals - you decide the action

The indicator reveals WHERE institutions are positioned and HOW they might behave. YOU decide IF, WHEN, and HOW to trade that information.

═════════════════════════════════════════════════════════════

📞 SUPPORT & UPDATES

═════════════════════════════════════════════════════════════

For questions, suggestions, or bug reports:

- Comment below the indicator

- Follow for updates and new features

- Check documentation for detailed examples

═════════════════════════════════════════════════════════════

Not financial advice. For educational and research purposes only.

STEFAN TEAM LogoSTEFAN TEAM Logo.

"On-Screen Logo for TradingView – A Sharp Brand Accent"

This template is specifically designed for seamless integration into digital spaces: streams, video lessons, presentations, and webinars about trading. The logo maintains perfect readability and a professional appearance on any background—overlaid on charts, in a screen corner, or on an intro screen.

Why this template is an excellent choice:

Optimized for screen: High contrast and clean outlines ensure visibility even at small sizes.

Universal placement: Looks perfect overlaid on the TradingView interface without obscuring key data (candles, indicators, quotes).

Professional signal: Makes your broadcast or video recognizable and strengthens audience trust.

Perfect for: trading streamers, educational course authors, financial analysts, and content creators on YouTube and Twitch.

Entry Scanner Conservative Option AKeeping it simple,

Trend,

RSI,

Stoch RSI,

MACD, checked.

Do not have entry where there is noise on selection, look for cluster of same entry signals.

If you can show enough discipline, you will be profitable.

CT

ATR + True RangeOne indicator for ATR & TR its a common indictor which can be used as one

instead of 2 different its is trial mode only not to be used with out other references