Low Pass Channel [DW]This is an experimental study designed to attenuate higher frequency oscillations in price and volatility with minimal lag.

In this study, a single pole low pass filter is used. The low pass filter's cutoff period is determined either by a fixed user input, or by using an Instantaneous Frequency Measurement (IFM) algorithm.

Most radar warning, electronic countermeasures, and electronic intelligence systems employ IFM to identify threats, map the electronic battlefield, and implement deceptive countermeasures.

The IFM technique used for this study was devised by John Ehlers. It calculates In Phase and Quadrature (IQ) components using the Hilbert Transform and uses them to determine the dominant price cycle.

To generate the channel, the same filter approach is applied to true range then added to and subtracted from the price filter.

Custom bar colors are included for simple wave and trend indication.

Ehlers

Ehlers Super Passband FilterAs someone hidden my old script that is just what one guy copied from a book from John Ehlers. I rewrite what i read in the book.

I also found this. So i rewrite this to the guys that was using it. If it hiddes again i will just keep it to myself and downgrade my plan in this TV

// Ehlers Super Passband Filter script may be freely distributed under the MIT license.

// Ehlers Super Passband Filter script may be freely distributed under the MIT license.

// Ehlers Super Passband Filter script may be freely distributed under the MIT license.

// Ehlers Super Passband Filter script may be freely distributed under the MIT license.

// Ehlers Super Passband Filter script may be freely distributed under the MIT license.

I wrote 5 times to be clear. If you guys dont understand portuguese go to the translator to understand what i am explaining in // inside the code.

MTF IQ IFM Moving AverageMTF ready adaptive MA using Ehler's IQ IFM ( In Phase - Quadrature Instantaneous Frequency Measurement ).

Ehler's formula is a method of quantitatively measuring the length of a market cycle. In this case it is used to calculate the "optimal" adaptive EMA.

Theoretically the length generated by Ehler's formula could be used in many indicators and it's been placed within it's own function so you should be able to simply copy/paste it. HOWEVER pine will not accept series variables for the length input used in built-in functions. You will have to manually code (or find) a version of your indicator that doesn't use the pine built in.

Options :

type : optionally add volume weighting

range : historical range used in IQ IFM

cycle length mult : method to create faster/slower MAs. eg 0.5 is half the length of a cycle and a faster EMA ie EMA10 vs EMA20

low sat fix : some cryptocurrencies with low satoshi values cause an issue with the calculation, if you get no/nonsensical lines, enable this. Shouldn't affect other instruments, but can be disabled just in case.

MTF options: run the calculation on an alternative timeframe

--------------------------------------

If you find it useful please consider a tip/donation :

BTC - 3BMEXEDyWJ58eXUEALYPadbn1wwWKmf6sA

MTF Fisher Hilbert Stoch COGMTF version of dasanc's "Fisher Stochastic Center of Gravity". Only contains the Hilbert variant from the script.

You can find his original script here : link

Center of Gravity Oscillator - Ehlers by KIVANC fr3762Center of Gravity OSCILLATOR by JOHN EHLERS

Converted the original code from his book "Cybernetic Analysis for Stocks and Futures"

This article describes a new oscillator that is unique because it is both smoothed

and has essentially zero lag. The smoothing enables clear identification of turning

points and the zero lag aspect enables action to be taken early in the move. This

oscillator is the serendipitous result of my research into adaptive filters. While the filters

have not yet produced the result I seek, this oscillator has substantial advantages over

conventional oscillators used in technical analysis . The “CG” in the name of the

oscillator stands for the Center of Gravity of the prices over the window of observation.

The Center of Gravity ( CG ) of a physical object is its balance point. For example,

if you balance a 12 inch ruler on your finger, the CG will be at its 6 inch point. If you

change the weight distribution of the ruler by putting a paper clip on one end, then the

balance point (e.g. the CG ) shifts toward the paper clip. Moving from the physical world

to the trading world, we can substitute the prices over our window of observation for the

units of weight along the ruler. With this analogy, we see that the CG of the window

moves to the right when prices increase sharply. Correspondingly, the CG of the

window moves to the left when prices decrease.

For further information:

www.mesasoftware.com

Here's the link to a complete list of all my indicators:

t.co

Şimdiye kadar paylaştığım indikatörlerin tam listesi için: t.co

Ghosty's Modded Super Bandpass Filter [DasanC]Very cool Indicator from Ehlers and published originally by @DasanC

I made minor modifications, and added a zero line and changed some values. I use this indicator differently then it is intended to be used for scalping shorter time frames (15 min - 1 hour).

I use it like a cross over, either from the zeroline or when it passes the RMS, for 5-10 pips. While no indicator is 100% this one does a nice job for small scalps.

try it out on a demo and see if you like it.

enjoy.

original Indy -

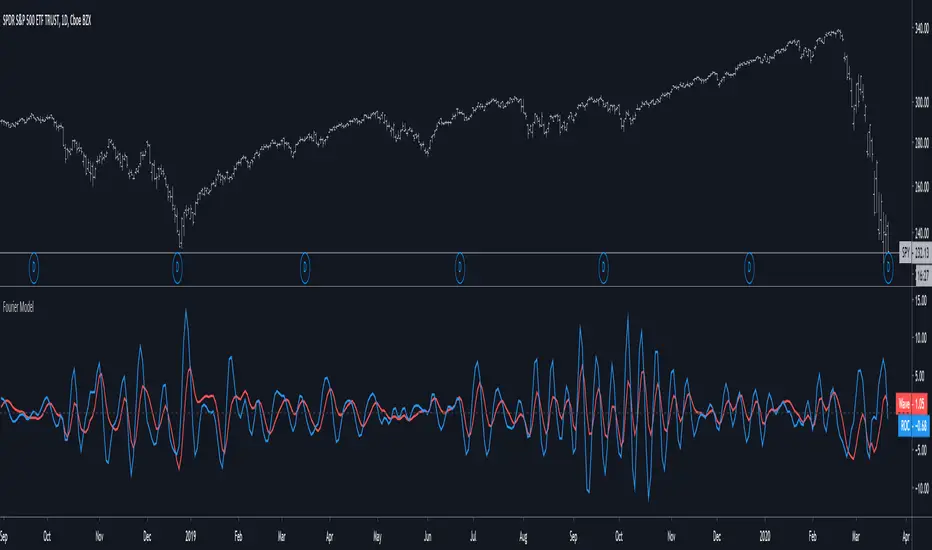

[e2] Fourier series Model Of The MarketFourier series Model Of The Market

John F. Ehlers

TASC Jun 2019

Ehlers Ideal RSIThis script has been updated to Pine v4. Original script by JustUncleL (link in code)

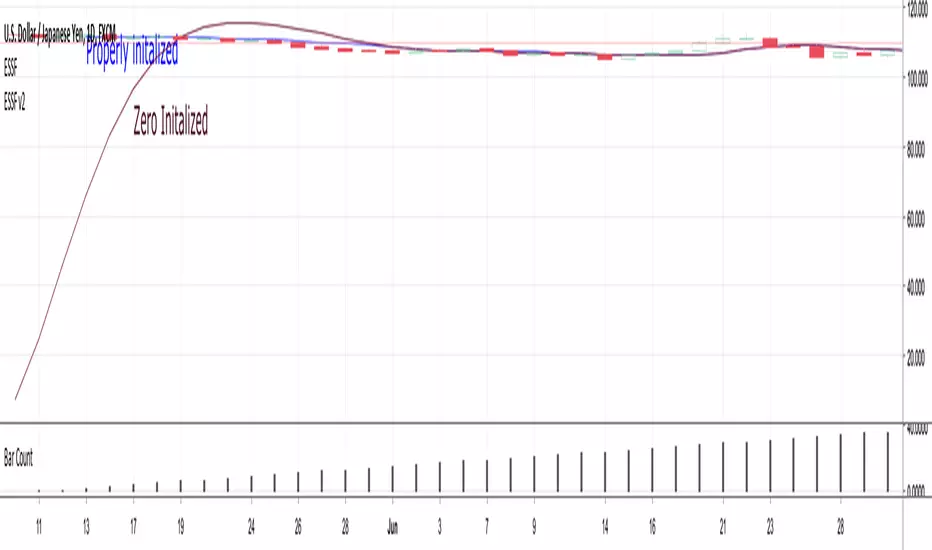

Ehler's Super Smoother 2 and 3 pole (properly initialized)John Ehlers' Super Smoother 2 and 3 pole - properly initialized

www.stockspotter.com

Failure to properly initialize early values of the super smoother will result in misleading values early in the output.

Because the SS is an IIR ( infinite impulse response) filter, this error can ring in the filter for a long time, but

is extremely evident in the first 2*len bars.

This is an implementation if the 2 and 3 pole SS filter, with special attention to initializing the early values.

It uses (src+scr)/2 per Ehlers but contains code to just use src if you prefer to calculate that outside

the function as everget does in his SS here:

there is code included to make that change.

Many thanks to everget for his terrific implementations of much of John Ehlers' work. It has been tremendously helpful to me.

Ehlers Decycler OscillatorThis indicator was originally developed by John F. Ehlers (Stocks & Commodities , V.33:10 (September, 2015): "Decyclers").

The idea is still the same as for the Simple Decycler.

Mr. Ehlers suggested to virtually eliminate lag by getting rid of the very low-frequency components. So, he applied the high-pass filter to the simple decycler.

Mr. Ehlers recommended to use two instances of the Decycler Oscillator with different parameters (high-pass filter period and multiplier). As a result, he got the Decycler Oscillator pair.

The first oscillator (red line) has a period of 125 bars, the second one (yellow line) has a period of 100 bars.

The interpretation is straightforward:

When the yellow line crosses over the red line, a trend reversal to the upside is indicated.

When the yellow line crosses under the red line, a trend reversal to the downside is indicated.

Ehlers Simple DecyclerThis indicator was originally developed by John F. Ehlers (Stocks & Commodities, V.33:10 (September, 2015): "Decyclers").

Mr. Ehlers suggested a way to improve trend identification using high-pass filters. The basic smoothers like SMA, low-pass filters, have considerable lag in their display. Mr. Ehlers applied the high-pass filter and subtracted the high-pass filter output from the time series input. Doing these steps he removed high-frequency short-wavelength components (the ones causing the wiggles) from the time series.

As a result he got a special series of the low-frequency components with virtually no lag - the Decycler.

The Decycler is plotted with two additional lines (the percent-shifts of Decycler) and together they form a hysteresis band.

If the prices are above the upper hysteresis line, then the market is in an uptrend . If the prices are below the low hysteresis line, then the market is in a downtrend . Prices within the hysteresis band are trend-neutral .

Ehlers Triple Delay-Line DetrenderThis indicator was originally developed by John F. Ehlers (Stocks & Commodities , V.18:7 (July, 2000): "Optimal Detrending").

Mr. Ehlers applied the ideas of the radar systems for the financial time series detrending.

Mr. Ehlers constructed the Triple Delay-Line Canceller first, then smoothed it with the Modified Optimum Elliptic Filter with minimal lag. The smoothed detrended signal is smoothed again with the Modified Optimum Elliptic Filter to obtain signal line.

As result, the crossings of the two indicator lines catch every major cyclic move and the detrender itself can be used as the first step in more sophisticated analyses.

Ehlers Modified Optimum Elliptic FilterThis indicator was originally developed by John F. Ehlers (Stocks & Commodities, V.18:7 (July, 2000): "Optimal Detrending").

Mr. Ehlers didn't stop and improved his Optimum Elliptic Filter. To reduce the effects of lag he added the one day momentum of the price to the price value.

This modification produce a better response.

Ehlers Optimum Elliptic FilterThis indicator was originally developed by John F. Ehlers (Stocks & Commodities, V.18:7 (July, 2000): "Optimal Detrending").

Mr. Ehlers worked on the smoother that could have no more than a one-bar lag. An elliptic filter provides the maximum amount of smoothing under the constraint of a given lag.

Fractal Adaptive Moving Averagewww.stockspotter.com

www.stockspotter.com

www.stockspotter.com

Here we measure the "fractal dimension" in order to differentiate periods of consolidation and trend. The trendline will run relatively flat during ranging price movement and quickly follow trending price action.

Instantaneous Trend [Ehlers]A low lag, trend follower for higher timeframes.

This works great as a tool to filter trades from oscillators or to provide a general trend direction.

You can also trade off the color changes, though I must recommend using timeframes higher than 1H.

-DasanC

Fisher Stochastic Center of GravityWhat happens when you take the Fisher Transform of a Stochastic Oscillator?

Well, you filter out all the stuff you don't want and are left with super-precise entries!

This indicator works especially well in with a trend-follower in a higher timeframe - iTrend, MAMA, Hull, etc...

How to trade:

Use with another indicator to tell you the current trend.

Take buy and sell signals as you would with the Stoch.

-DasanC

John Ehlers Universal Oscillator [mwlang]This version of John Ehlers Universal Oscillator fixes a degrees to radians bug in LazyBear's version published here:

Stochastic Center of Gravitywww.mesasoftware.com

Stochastic version of Ehlers CG indicator.

I'm not sure how reliable it is as a strategy since TV's backtesting engine is broken.

Will provide updates as I use it in the future.

Signal to Noise Ratio [SNR]Intro

This script measures the Signal to Noise ratio of a security and plots it in deciBels scale!

Usage

Ideally, you would want the ratio to be above 10 dB, meaning the Signal strength is 10x the noise strength.

As a baseline, you should not rely on indicators that use any kind of moving average if the SNR is below 6 dB - meaning Signal strength is only 4x noise strength.

I've written the SNR as a functional block so you may simply copy and paste, then call getSNR() to get the ratio in dB.

Principle

I consider a bar's High and Low to be the range of that period and (High + Low)/2 to be the "real" value of the signal.

This script compares a bars range (noise) to the perceived signal using a Hilbert Transform.

Cheers,

DasanC

Multi-Instantaneous Frequency MeasurementI compiled all of Ehlers' IFM methods into one script - all written as functional blocks so you can simply add them to your own scripts.

Bonus! I also dropped in the Super Smoother, which is a much more efficient and low lag averaging method. I used it to clean the data before feeding it into other indicators.

Robust Cycle Measurement [Ehlers]The last of Ehlers Instantaneous Frequency Measurement methods.

This is a more robust version of this script.

I wrote it as a function, so you can simply copy and paste it into any script to add an adaptive period setting capability.

Cheers,

DasanC