Median + Tendência + ATR (Yehuda Nahmias)📊 Median + Trend + ATR (By Yehuda Nahmias)

🚀 The indicator that combines Simplicity, Accuracy, and Risk Management

This script brings together three key pillars of professional trading:

✅ Dynamic Median → captures price midpoints and highlights reversal and breakout zones.

✅ Trend Filter (EMA) → ensures signals are aligned with the main market direction.

✅ Smart ADX + ATR → confirm trend strength and automatically calculate Stop Loss and Take Profit based on volatility.

🔔 How it works:

Buy/Sell Arrows: automatically appear when price crosses the median under valid trend and strength conditions (ADX).

Automatic Stops and Targets: SL and TP levels are plotted using ATR, ready for effective risk management.

3 Signal Modes:

🛡️ Conservative → fewer trades, stronger filtering.

⚖️ Standard → balance between frequency and accuracy.

⚡ Aggressive → more trades, captures shorter moves.

💡 Key Benefits:

Clear visuals: colored candles + BUY/SELL arrows.

Built-in risk management: position size is calculated based on % of equity.

Flexible: works on any asset (Forex, Crypto, Indices, Stocks).

🔑 Private access only.

If you’d like to use this strategy on your charts, contact me via my TradingView profile.

👉 Turn your analysis into objective signals and gain more confidence in your entries and exits!

Forecasting

MOHStrategy Description

Uses Heikin Ashi candles to filter market noise and identify trend direction.

Entry is allowed only when strong HA candles appear (bullish without lower wick, bearish without upper wick).

Doji candles signal possible reversal.

استخدام شموع Heikin Ashi لتقليل الضوضاء وتحديد اتجاه الترند.

الدخول فقط عند ظهور شموع قوية (صاعدة بدون ذيل سفلي، هابطة بدون ذيل علوي).

شمعة الدوجي = إشارة انعكاس محتملة.

Sr.Rma.Breakout.Fib (Merged)DO YOUR DUE DILIGENCE – THIS IS FOR EDUCATIONAL PURPOSE AND NOT A TRADE ADVICE-

This strategy is designed for traders who want to merge pattern recognition (breakouts) with market structure context (Fibonacci), while maintaining disciplined trade management through automated stop-loss and reversal logic. “Once the chart is added, please ensure the candle pattern is set to Heikin Ashi.”

1. Breakout Finder Logic

The breakout finder identifies bullish and bearish breakouts using pivots, thresholds, and test counts:

• Pivot Highs & Lows (PH/PL): Calculated using user-defined periods.

• Breakout Threshold: Dynamic channel width based on recent volatility.

• Confirmation: A breakout is validated when price action clears the breakout Conditions

• Bullish Breakout: Triggered when multiple pivot highs are cleared by bullish Conditions.

• Bearish Breakout: Triggered when multiple pivot lows are broken by bearish Conditions.

• Sessions ignored: Traders can exclude up to three custom time windows to prevent signals during low-quality periods.

Risk & Reversal Controls

• Stop-Loss: Adjustable % thresholds for both long and short trades.

• Reversal Entries: Optional signals that trigger after a stop-loss, capturing potential price reversals.

2. Strategy Order Management

The strategy executes entries and exits based on confirmed breakout and reversal signals:

• Entries:

o Long on confirmed bullish breakout.

o Short on confirmed bearish breakout.

• Stops:

o Automatic closure of open positions when stop-loss conditions are hit.

• Reversals:

o Transition directly from long to short or vice versa when reversal conditions are met.

3. Auto Fibonacci Retracement

A ZigZag-based system automatically plots Fibonacci retracement levels on the chart:

• Swing Context: Derived dynamically from pivots with adjustable depth and deviation settings.

• Fib Levels: Standard retracement and extension levels (0.236, 0.382, 0.5, 0.618, 0.786, 1.0, 1.618, 2.618, 3.618, 4.236, etc.) are supported.

• Custom Options:

o Extend lines left or right.

o Show/hide level prices and percentage values.

o Control label positions (left or right).

o Adjustable transparency for background fills between levels.

• Crossing Alerts: Alerts are fired when the price crosses specific Fibonacci levels, enhancing confluence with breakout signals.

5. Key Benefits

• Comprehensive Trading Framework: Combines breakout confirmation, risk management, and Fibonacci context.

• Visual Clarity: Automatic plotting of breakout structures and Fib levels makes the chart intuitive.

• Flexible Controls: Full customization of pivots, thresholds, sessions, stop-loss %, and Fib settings.

• Automation Ready: Alerts and strategy orders allow seamless integration with brokers or external systems.

回撤再入场引擎This is a long-only, counter-trend strategy that aims to buy dips in a medium-term downtrend. The entry logic is based on a confluence of four filters:

1. **Trend Filter:** The price must be trading below the 60-period Simple Moving Average (SMA).

2. **Oversold Condition:** The WaveTrend Oscillator must first dip below -60 and then recover above -55.

3. **Momentum Confirmation:** The MACD must show sustained bullish momentum for at least 2 bars.

4. **Re-entry Filter:** A new trade is only allowed if the price is at least a certain percentage lower than the last trade's exit price.

The exit is based on a fixed Take Profit target. This version does not include a stop-loss.

FxAST Lite Wave — Universal (Profiles: Intraday / Swing)FxAST-LW Universal (Profiles)

The FxAST Lite Wave – Universal strategy is designed for adaptability across markets and timeframes, with two ready-to-use profiles:

Intraday (5m–1H) → tuned for futures & FX scalps/day trades. Includes session filters, ATR volatility regimes, and impulse confirmation to reduce chop.

Swing (1D–3D) → tuned for swing positions. Uses relaxed impulse filters, slope + bias confirmation, and DI-spread to capture bigger moves.

Key features:

✅ Multi-EMA Lite Wave core (5/13/62/200)

✅ Regime filter via DI-spread (trend vs chop)

✅ EMA200 slope filter

✅ Optional HTF bias confirmation

✅ ATR-based stops, breakeven & trailing logic

✅ Time-stop exits to avoid capital stagnation

✅ Risk % position sizing

Usage:

Switch between Intraday and Swing modes via the Profile input. Adjust DI-spread, slope, and impulse thresholds per symbol. Sessions recommended ON for indices (NQ/ES/RTY) and OFF for FX.

⚠️ Disclaimer: This script is for research & educational purposes only. Not financial advice. Test extensively before applying live. Past performance does not guarantee future results.

© FxAST

LFT Foundation Main ReversionLFT Foundation Main Reversion

this script will tell exactly when to buy and sell with TP and SL, used the latest LLM to tone the model with a profit ratio of 1.82 in 6 years and profit ratio of 4.02 in past 6 month and have been back tested with Monte Carlo simulation, with profit ratio 1+ for 99% of the time with 1000 iterations with 500 steps, for 100 times

please contact LFT Foundation for access

Optimized ADX DI CCI Strategy### Key Features:

- Combines ADX, DI+/-, CCI, and RSI for signal generation.

- Supports customizable timeframes for indicators.

- Offers multiple exit conditions (Moving Average cross, ADX change, performance-based stop-loss).

- Tracks and displays trade statistics (e.g., win rate, capital growth, profit factor).

- Visualizes trades with labels and optional background coloring.

- Allows countertrading (opening an opposite trade after closing one).

1. **Indicator Calculation**:

- **ADX and DI+/-**: Calculated using the `ta.dmi` function with user-defined lengths for DI and ADX smoothing.

- **CCI**: Computed using the `ta.cci` function with a configurable source (default: `hlc3`) and length.

- **RSI (optional)**: Calculated using the `ta.rsi` function to filter overbought/oversold conditions.

- **Moving Averages**: Used for CCI signal smoothing and trade exits, with support for SMA, EMA, SMMA (RMA), WMA, and VWMA.

2. **Signal Generation**:

- **Buy Signal**: Triggered when DI+ > DI- (or DI+ crosses over DI-), CCI > MA (or CCI crosses over MA), and optional ADX/RSI filters are satisfied.

- **Sell Signal**: Triggered when DI+ < DI- (or DI- crosses over DI+), CCI < MA (or CCI crosses under MA), and optional ADX/RSI filters are satisfied.

3. **Trade Execution**:

- **Entry**: Long or short trades are opened using `strategy.entry` when signals are detected, provided trading is allowed (`allow_long`/`allow_short`) and equity is positive.

- **Exit**: Trades can be closed based on:

- Opposite signal (if no other exit conditions are used).

- MA cross (price crossing below/above the exit MA for long/short trades).

- ADX percentage change exceeding a threshold.

- Performance-based stop-loss (trade loss exceeding a percentage).

- **Countertrading**: If enabled, closing a trade triggers an opposite trade (e.g., closing a long opens a short).

4. **Visualization**:

- Labels are plotted at trade entries/exits (e.g., "BUY," "SELL," arrows).

- Optional background coloring highlights open trades (green for long, red for short).

- A statistics table displays real-time metrics (e.g., capital, win rates).

5. **Trade Tracking**:

- Tracks the number of long/short trades, wins, and overall performance.

- Monitors equity to prevent trading if it falls to zero.

### 2.3 Key Components

- **Indicator Calculations**: Uses `request.security` to fetch indicator data for the specified timeframe.

- **MA Function**: A custom `ma_func` handles different MA types for CCI and exit conditions.

- **Signal Logic**: Combines crossover/under checks with recent bar windows for flexibility.

- **Exit Conditions**: Multiple configurable exit strategies for risk management.

- **Statistics Table**: Updates dynamically with trade and capital metrics.

## 3. Configuration Options

The script provides extensive customization through input parameters, grouped for clarity in the TradingView settings panel. Below is a detailed breakdown of each setting and its impact.

### 3.1 Strategy Settings (Global)

- **Initial Capital**: Default `10000`. Sets the starting capital for backtesting.

- **Effect**: Determines the base equity for calculating position sizes and performance metrics.

- **Default Quantity Type**: `strategy.percent_of_equity` (50% of equity).

- **Effect**: Controls the size of each trade as a percentage of available equity.

- **Pyramiding**: Default `2`. Allows up to 2 simultaneous trades in the same direction.

- **Effect**: Enables multiple entries if conditions are met, increasing exposure.

- **Commission**: 0.2% per trade.

- **Effect**: Simulates trading fees, reducing net profit in backtesting.

- **Margin**: 100% for long and short trades.

- **Effect**: Assumes no leverage; adjust for margin trading simulations.

- **Calc on Every Tick**: `true`.

- **Effect**: Ensures real-time signal updates for precise execution.

### 3.2 Indicator Settings

- **Indicator Timeframe** (`indicator_timeframe`):

- **Options**: `""` (chart timeframe), `1`, `5`, `15`, `30`, `60`, `240`, `D`, `W`.

- **Default**: `""` (uses chart timeframe).

- **Effect**: Determines the timeframe for ADX, DI, CCI, and RSI calculations. A higher timeframe reduces noise but may delay signals.

### 3.3 ADX & DI Settings

- **DI Length** (`adx_di_len`):

- **Default**: `30`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for calculating DI+ and DI-. Longer periods smooth trends but reduce sensitivity.

- **ADX Smoothing Length** (`adx_smooth_len`):

- **Default**: `14`.

- **Range**: Minimum `1`.

- **Effect**: Smooths the ADX calculation. Longer periods produce smoother ADX values.

- **Use ADX Filter** (`use_adx_filter`):

- **Default**: `false`.

- **Effect**: If `true`, requires ADX to exceed the threshold for signals to be valid, filtering out weak trends.

- **ADX Threshold** (`adx_threshold`):

- **Default**: `25`.

- **Range**: Minimum `0`.

- **Effect**: Sets the minimum ADX value for valid signals when the filter is enabled. Higher values restrict trades to stronger trends.

### 3.4 CCI Settings

- **CCI Length** (`cci_length`):

- **Default**: `20`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for CCI calculation. Longer periods reduce noise but may lag.

- **CCI Source** (`cci_src`):

- **Default**: `hlc3` (average of high, low, close).

- **Effect**: Defines the price data for CCI. `hlc3` is standard, but users can choose other sources (e.g., `close`).

- **CCI MA Type** (`ma_type`):

- **Options**: `SMA`, `EMA`, `SMMA (RMA)`, `WMA`, `VWMA`.

- **Default**: `SMA`.

- **Effect**: Determines the moving average type for CCI signal smoothing. EMA is more responsive; VWMA weights by volume.

- **CCI MA Length** (`ma_length`):

- **Default**: `14`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for the CCI MA. Longer periods smooth the MA but may delay signals.

### 3.5 RSI Filter Settings

- **Use RSI Filter** (`use_rsi_filter`):

- **Default**: `false`.

- **Effect**: If `true`, applies RSI-based overbought/oversold filters to signals.

- **RSI Length** (`rsi_length`):

- **Default**: `14`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for RSI calculation. Longer periods reduce sensitivity.

- **RSI Lower Limit** (`rsi_lower_limit`):

- **Default**: `30`.

- **Range**: `0` to `100`.

- **Effect**: Defines the oversold threshold for buy signals. Lower values allow trades in more extreme conditions.

- **RSI Upper Limit** (`rsi_upper_limit`):

- **Default**: `70`.

- **Range**: `0` to `100`.

- **Effect**: Defines the overbought threshold for sell signals. Higher values allow trades in more extreme conditions.

### 3.6 Signal Settings

- **Cross Window** (`cross_window`):

- **Default**: `0`.

- **Range**: `0` to `5` bars.

- **Effect**: Specifies the lookback period for detecting DI+/- or CCI crosses. `0` requires crosses on the current bar; higher values allow recent crosses, increasing signal frequency.

- **Allow Long Trades** (`allow_long`):

- **Default**: `true`.

- **Effect**: Enables/disables new long trades. If `false`, only closing existing longs is allowed.

- **Allow Short Trades** (`allow_short`):

- **Default**: `true`.

- **Effect**: Enables/disables new short trades. If `false`, only closing existing shorts is allowed.

- **Require DI+/DI- Cross for Buy** (`buy_di_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a DI+ crossover DI- for buy signals; if `false`, DI+ > DI- is sufficient.

- **Require CCI Cross for Buy** (`buy_cci_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a CCI crossover MA for buy signals; if `false`, CCI > MA is sufficient.

- **Require DI+/DI- Cross for Sell** (`sell_di_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a DI- crossover DI+ for sell signals; if `false`, DI+ < DI- is sufficient.

- **Require CCI Cross for Sell** (`sell_cci_cross`):

- **Default**: `true`.

- **Effect**: If `true`, requires a CCI crossunder MA for sell signals; if `false`, CCI < MA is sufficient.

- **Countertrade** (`countertrade`):

- **Default**: `true`.

- **Effect**: If `true`, closing a trade triggers an opposite trade (e.g., close long, open short) if allowed.

- **Color Background for Open Trades** (`color_background`):

- **Default**: `true`.

- **Effect**: If `true`, colors the chart background green for long trades and red for short trades.

### 3.7 Exit Settings

- **Use MA Cross for Exit** (`use_ma_exit`):

- **Default**: `true`.

- **Effect**: If `true`, closes trades when the price crosses the exit MA (below for long, above for short).

- **MA Length for Exit** (`ma_exit_length`):

- **Default**: `20`.

- **Range**: Minimum `1`.

- **Effect**: Sets the period for the exit MA. Longer periods delay exits.

- **MA Type for Exit** (`ma_exit_type`):

- **Options**: `SMA`, `EMA`, `SMMA (RMA)`, `WMA`, `VWMA`.

- **Default**: `SMA`.

- **Effect**: Determines the MA type for exit signals. EMA is more responsive; VWMA weights by volume.

- **Use ADX Change Stop-Loss** (`use_adx_stop`):

- **Default**: `false`.

- **Effect**: If `true`, closes trades when the ADX changes by a specified percentage.

- **ADX % Change for Stop-Loss** (`adx_change_percent`):

- **Default**: `5.0`.

- **Range**: Minimum `0.0`, step `0.1`.

- **Effect**: Specifies the percentage change in ADX (vs. previous bar) that triggers a stop-loss. Higher values reduce premature exits.

- **Use Performance Stop-Loss** (`use_perf_stop`):

- **Default**: `false`.

- **Effect**: If `true`, closes trades when the loss exceeds a percentage threshold.

- **Performance Stop-Loss (%)** (`perf_stop_percent`):

- **Default**: `-10.0`.

- **Range**: `-100.0` to `0.0`, step `0.1`.

- **Effect**: Specifies the loss percentage that triggers a stop-loss. More negative values allow larger losses before exiting.

## 4. Visual and Statistical Output

- **Labels**: Displayed at trade entries/exits with arrows (↑ for buy, ↓ for sell) and text ("BUY," "SELL"). A "No Equity" label appears if equity is zero.

- **Background Coloring**: Optionally colors the chart background (green for long, red for short) to indicate open trades.

- **Statistics Table**: Displayed at the top center of the chart, updated on timeframe changes or trade events. Includes:

- **Capital Metrics**: Initial capital, current capital, capital growth (%).

- **Trade Metrics**: Total trades, long/short trades, win rate, long/short win rates, profit factor.

- **Open Trade Status**: Indicates if a long, short, or no trade is open.

## 5. Alerts

- **Buy Signal Alert**: Triggered when `buy_signal` is true ("Cross Buy Signal").

- **Sell Signal Alert**: Triggered when `sell_signal` is true ("Cross Sell Signal").

- **Usage**: Users can set up TradingView alerts to receive notifications for trade signals.

MACDEMAAutomatic Strategy for Litecoin on 5-Minute Chart in BingX Perpetual Futures. Combines MACD and 10- & 55-Period EMA. ✅

Multi Channel GRID & DCA LTF [trade_lexx]Multi Channel GRID & DCA LTF

Usage Guide

Part 1: The concept and general possibilities of the "Multi Channel GRID & DCA LTF" strategy

Introduction

Welcome to the guide to "Multi Channel GRID & DCA LTF", a powerful and versatile automated trading strategy for the TradingView platform. This tool was developed for traders who are looking for flexibility, control and a high degree of adaptability to various market conditions.

The strategy is based on a hybrid approach that combines two popular and time-tested techniques.:

1. GRID (grid trading): The classic method of averaging a position is by placing a grid of limit orders.

2. DCA (Dollar Cost averaging): Smart position averaging based on signals from external indicators.

However, "Multi Channel GRID & DCA LTF" goes far beyond the simple combination of these two techniques. The strategy includes a number of unique and innovative features, such as cascading MultiGRID grids for dealing with extreme volatility, Channel Mode range trading mode for profiting from sideways movement, and Low Time Frame analysis (LTF) to achieve surgical accuracy in backtesting. Deep customization options for risk management, capital, take profits, and stop losses allow you to configure a strategy for almost any trading style, asset, and timeframe.

The basic idea: How does it work?

Let's take a detailed look at each of the key concepts embedded in the logic of the strategy.

1. GRID — Automatic placement of buy and sell orders at certain price intervals.

This is a fundamental mode of operation. Its main goal is to systematically improve the average entry price for a position if the market is going against you.

* The principle of operation: After opening the base (first) order (`BO`), the strategy automatically places a series of pending limit orders (here they are called "safety orders" or "SO") at certain price intervals. For a long position, orders are placed below the entry price, and for a short position, orders are placed higher.

* Target: When the price moves against an open position, it consistently hits and executes safety orders. Each such execution adds additional volume to the position at a more favorable price, thereby shifting the overall average entry price (`position_avg_price') closer to the current market price. This means that a much smaller corrective movement will be required to gain ground.

* Flexibility: You have full control over the geometry of the grid: the number of safety orders, the percentage distance between them (`SO Step`), and you can even set a coefficient that will increase this step for each subsequent order (`SO Multiplier`), creating an expanding grid.

2. DCA (Signal Averaging) — Smart Averaging

This mode adds an additional layer of analysis to the averaging process. Instead of just buying/selling at the set price levels, the strategy waits for a confirmation signal.

* Working principle: You can connect any external indicator (for example, RSI, CCI, or even your own complex signal system) to the strategy, which outputs numerical values. As standard, 1 is used for a long signal, and -1 is used for a short signal. The strategy will place the next averaging order only at the moment when it receives the appropriate signal.

* Goal: To average a position not just during a fall (or a rise for a short), but at the moments that your main trading system considers the most favorable for this. This allows you to avoid "catching falling knives" and enter only if there are good reasons.

3. Hybrid Mode (GRID+DCA) is the best of the previous two modes

This mode is designed for maximum filtering and control. It requires two conditions to be fulfilled simultaneously.

* Working principle: The safety order will be executed only if the price has reached the calculated grid level and a confirmation signal has been received from your external indicator. If a confirmation signal is received from an external indicator, the next calculated grid level activates the limit order.

* Goal: To create the most reliable averaging system that protects against premature entries and requires double confirmation (both by price and indicator) before increasing the position size.

4. MultiGRID — Adaptation to extreme volatility

This is one of the most powerful and unique features of a strategy designed to survive and make a profit in the face of strong, protracted trends or "black swans".

* The problem it solves: The usual grid of orders has a limited depth. If the price goes beyond the last safety order, the strategy loses the opportunity to average and becomes vulnerable.

* The principle of operation: The MultiGRID function allows you to create "cascades" — several grids following one another. When all the orders of the first grid are executed, the strategy does not stop. Instead, she can activate the second, third (and so on) a grid of orders. The new grid can be activated by one of two triggers:

1. Offset: The new grid is activated when the price passes another set percentage deviation from the last executed order.

2. Signal: The new grid is activated when a signal is received from an external indicator.

* Goal: To significantly expand the working range of the strategy. This allows it to adapt to strong market movements that would "break" the usual grid, and continue to effectively average a position at a much greater depth of decline or growth.

5. Channel Mode — Trading in the range

This feature turns a standard averaging strategy into a machine for "farming" profits within a price channel that is formed during a sideways market movement.

* The problem it solves: In the standard grid strategy, after partially closing a take profit position, the volume of this part "leaves" the trade until the deal is fully closed. You are missing the opportunity to reuse this capital.

* Operating principle: When Channel Mode is enabled, the following happens. Suppose the price went against you, executed several safety orders, and then turned around and reached one of the partial take profits. At this point, the strategy is:

1. Fixes the profit, as it should be.

2. Instantly places a new limit order to buy (or sell for a short) at exactly the same price level where the last triggered safety order was executed. The volume of this order is equal to the volume of the part that was just closed for take profit.

3. If the price goes down again and executes this "repeat" order, the strategy immediately sets a corresponding take profit for it at the level where the previous profit was taken.

* Goal: To create a continuous buy-sell cycle within the local range (channel). The lower limit of the channel is the price of the last averaging, and the upper limit is the price of a partial take profit. This allows you to repeatedly profit from sideways price fluctuations, without waiting for the full closure of the main, large transaction.

6. LTF (Lower Timeframe Analysis) — Surgical precision of backtesting

This feature is critically important for obtaining reliable results during historical testing (backtesting) of grid strategies.

* The problem it solves: The standard testing mechanism in TradingView has a serious limitation. Working, for example, on a 4-hour chart, he sees only 4 candle points: Open, High, Low and Close. He does not know in what order the price moved within these 4 hours. He could have touched High first and then Low, or vice versa. For grid strategies, this is fatal — the engine can show that a take profit has been executed, although in reality the price first went down, collected the entire grid of orders and only then turned around.

* How it works: When you turn on the LTF mode, the strategy for each candle on your main chart (for example, 4H) requests and analyzes all candles from the lower timeframe you specified (for example, 1-minute). Then it virtually trades the entire price path for these minute candles, executing orders, take profits and stop losses in the sequence in which they would occur in reality. It works in the single take profit mode of the Grid strategy.

* Goal: To provide the most realistic and reliable backtest that reflects the real dynamics of the market. This allows you to avoid false expectations and accurately assess the potential performance of the strategy.

// ------------------------

Part 2: Detailed description of the strategy settings

This section is your main guide to all the switches and options available in the strategy. Understanding each setting is the key to unlocking the full potential of this powerful tool.

1. 🛡️ Risk Management 🛡️

This group contains fundamental parameters that determine the basic logic of risk management and the geometry of grid orders.

* Strategy type: Determines the direction of transactions.

* Long: The strategy will only open long positions (buy).

* Short: The strategy will only open short positions (sell).

* Both: The strategy will work both ways, opening long or short depending on the incoming signal.

* SO Count: Sets the maximum number of Safety (averaging) Orders (SO) that the strategy will place within the same grid. If you have MultiGRID enabled, this number applies to each individual grid.

* SO Step (%): This is the base percentage deviation from the entry price at which the first safety order will be placed. For example, at a value of 0.5, the first SO in a long trade will be placed 0.5% lower than the opening price of the base order.

* SO Multiplier: A coefficient that exponentially increases the step for each subsequent safety order. This allows you to create an expanding grid where averaging orders are placed further and further apart, which is effective with strong and accelerating price movements.

* *The step formula for the nth order*: Step(N) = (SO Step) * (SO Multiplier ^(N-1)).

* If the value is 1, all steps will be the same.

* With a value of 1.6, the step of the second SO will be 1.6 times larger than the first, the step of the third will be 1.6 times larger than the second, and so on.

* 1️⃣ TP/SL: These are simplified settings for quick configuration. They allow you to turn on/off the main take profit and stop loss and set basic percentage values for them. More detailed settings for these parameters can be found in the relevant sections below.

// ------------------------

2. 💰 Money Management 💰

Everything related to position size, leverage, and capital is configured here.

* Volume BO (Base Order): Determines the size of the trade's opening order.

* Volume BO: A fixed amount in the quote currency (for example, in USDT).

* USDT (check mark): Manages the information in the comments to the orders. If enabled, the volume of orders in USDT will be displayed in the comments. This is convenient for visual analysis and for sending the amount of USDT by the placeholder {{strategy.order.comment}} via webhooks when connecting the strategy to the exchange or trading terminals.

* or % of deposit: The amount calculated as a percentage of the available capital of the strategy. The check mark to the right of this field enables this mode. Important: using a percentage activates the effect of compounding (compound interest), as the amount of each new transaction will be automatically recalculated based on the current capital (initial capital + profit/loss). If enabled, the percentage of orders will be displayed in the comments. This is convenient for visual analysis and for sending percentages on the placeholder {{strategy.order.comment}} via webhooks when connecting the strategy to the stock exchange, trading terminals, or creating Copy trading.

* Martingale: The coefficient applied to the volume of orders. It increases the size of each subsequent insurance order compared to the base one.

* Volume formula for the nth SO: Volume SO (N) = (Volume BO) * (Martingale^N).

* With a value of 1.2, the volume of the first SO will be 1.2 times greater than the base, the second — 1.44 times (`1.2 * 1.2`) and so on.

* Leverage: Specify the size of your leverage. This parameter is used exclusively for calculating and displaying the approximate liquidation price. It does not affect the size of positions, but it helps to visually assess the risks.

* Liquidation: Enables or disables the calculation and display of the liquidation line on the chart.

* Margin type: Allows you to select a method for calculating the liquidation price, simulating the logic of exchanges:

* Isolated: The liquidation price is calculated based on the size and leverage of the current open position only.

* Cross: The calculation simulates using the entire available balance to maintain a position. In the strategy, the liquidation price is calculated as the level at which the loss on the current transaction is equal to the current capital.

* Commission (%): Specify the percentage of your exchange's commission per transaction. The correct value of this parameter is crucial for obtaining realistic backtest results.

// ------------------------

3. 🕸️ Grid Management 🕸️

This group is responsible for the logic of safety orders and advanced mechanics such as Channel Mode and MultiGRID.

* SO Type: Defines the logic of placing averaging orders.

* GRID: Classic grid. All safety orders are placed in advance as limit orders.

* DCA: Signal averaging. The strategy is waiting for a signal from an external indicator to place a market averaging order.

* GRID+DCA: Hybrid. The strategy waits for a signal, and if it arrives, places a limit order at the appropriate price level of the grid or executes a market order if the signal has arrived below the limit order level.

* Signal for SO: A data source (indicator) that will be used for signals in DCA and GRID+DCA modes.

* ↔️ Channel Mode: When this option is enabled, the strategy tries to trade in a sideways range. After partially closing a take profit position, it immediately places a limit order for re-entry at the price of the last triggered safety order. This creates a buy-sell cycle within the local channel.

* Best Price Only: This filter adds an additional condition for averaging in DCA and MultiGRID modes (when it operates on a signal). The next averaging order or a new grid will be activated only if the current price is more favorable (lower for long, higher for short) than the price of the previous entry.

* 🧩 MultiGRID ⮕ Enables cascading grid mode.

* Grid Count: The total number of grids that can be activated sequentially.

* Offset: Percentage deviation from the price of the last order of the previous grid. When this margin is reached, the following grid of orders is activated (this mode does not require a signal).

* Or signal: Allows you to use the signal from an external indicator as a trigger to activate the next grid. The checkmark on the right turns on this mode.

// ------------------------

4. 🎯 Entry and Stop 🎯

This group of settings allows you to fine-tune the conditions for starting a new trade and all aspects related to protective stop orders, including the complex mechanics of trailing and managing SL after partial take profits.

* 🎯 Signal: A data source (indicator) that will be used to determine when to enter a trade. The strategy expects a value of 1 for the start of a long trade and -1 for a short trade.

* Min Bars: Sets the minimum number of candles that must pass from the moment of opening the previous trade to the moment of opening the next one. A value of 0 disables this filter. This is a useful tool to prevent overly frequent entries in a "noisy" market.

* Non-stop: If this option is enabled, the strategy ignores the Entry Signal and opens a new trade immediately after closing the previous one (taking into account the Min Bars filter, if it is set). This turns the strategy into a constantly working mechanism that is always on the market.

* 🛑 SL Type: Defines the base price from which the stop loss percentage will be calculated. The stop loss in the first section must be enabled for this block of settings to work.

* From the entry point: SL is always calculated from the opening price of the very first base order. It remains static throughout the entire transaction unless it is moved by other functions.

* From breakeven line: SL is dynamically recalculated and shifted each time a safety order is executed. It always follows the average price of the position, being at a given percentage distance from it.

* From last executed SO: SL is recalculated from the price of the last executed order, whether it is a base or a safety order.

* From last SO: SL is calculated from the price of the most recent possible safety order in the grid. This is usually the most remote and conservative type of SL.

* Trailing SL Type: Defines the algorithm by which the stop loss will move after its activation.

* Standard: Classic trailing. After activation, SL will follow the price at a fixed distance.

* ATR: SL will follow the price at a distance equal to the value of the ATR indicator multiplied by the specified multiplier.

* External Source: SL will follow any selected line of the third-party indicator.

* Period and Multiplier: Common parameters for all types of trailing.

* Source: The source of the line for the trailing SL of the third-party indicator.

* Trailing SL after entry: The mode of activation of the trailing SL after entering the transaction

* SL management after TP (sections 1️⃣, 2️⃣, 3️⃣): These three blocks allow you to create a complex stop loss management logic as profits are recorded.

For each take profit level (TP1, TP2, TP3), you can configure:

* SL BE / SL TP1 / SL TP2: When the corresponding TP is reached, the stop loss will be moved to the breakeven point (for TP1), to the TP1 price level (for TP2) or to the TP2 price level (for TP3).

* Trailing SL: When the corresponding TP is reached, the trailing stop loss is activated according to the settings above.

* By ↔️ Signal: A very powerful option. If it is enabled, the above action (SL transfer or trailing activation) will occur when the opposite trading signal is received from an external indicator. This allows you to protect profits or reduce losses if the market turns sharply, even before reaching the target.

* SL Delay ⮕ Allows you to delay the activation of the stop loss.

* Number of Bars: The Stop loss will be physically placed on the market only after the specified number of candles has passed since entering the trade. This can help to avoid "taking out" the stop with a random short movement (squiz) immediately after opening a position.

* SL Block: Unique defensive mechanics for trading both ways (`Strategy Type: Both`).

* Number of SL: If the strategy receives the specified number of stop losses in a row in one direction (for example, 2 stops long), it temporarily blocks the opportunity to open new trades in that direction.

* Lock Reset mode:

* By direction: The lock is lifted if a profitable trade is closed in the allowed direction or if a stop loss is triggered in the opposite direction.

* First profit: The lock is lifted after closing any profitable transaction, regardless of its direction.

// ------------------------

5. ✅ Take Profit ✅

This group of settings provides comprehensive control over profit taking, from a simple take profit to a complex system of partial closures and trailing.

* ✅ TP Type: Defines the base price for calculating the percentage deviation of the take profit.

* From entry point: TP is calculated from the base order price.

* From breakeven line: TP dynamically follows the average position price.

* From last executed SO: TP is calculated from the price of the last executed order.

* Filters for closing on signal

* Only ➕: If TP is triggered by a signal, the deal will be closed only if it is in the black relative to the average price.

* Or >TP: If TP is triggered by a signal, the trade will be closed only if the closing price is better than (or equal to) the estimated price of this TP.

* TP type of trailing: Yes, take profit has a trailing too! It works differently than the SL trailing.

* Standard / ATR: After the price touches the "virtual" TP level, the trailing is activated. He does not place a stop order, but begins to move away from the price, dynamically moving the limit order to close further and further in the profitable direction, allowing him to collect the maximum from the impulse movement.

* External Source: TP will follow any selected line of the third-party indicator.

* Period and Multiplier: Parameters for calculating the trailing margin TP.

* Source: The source of the line for the trailing TP of the third-party indicator.

* TP level settings (sections 1️⃣, 2️⃣, 3️⃣, 4️⃣): The strategy supports up to four independent take profit levels, which allows for a flexible system of partial commits.

For each level, you can set:

* TP: Enable the level and set its percentage deviation from the base price.

* Size: What percentage of the current position will be closed when this level is reached. For the last active TP, this parameter is ignored, and 100% of the remaining position is closed.

* Trailing TP: Enable the above-described trailing mechanism for this particular level.

* Signal: Enable closing based on the signal from the external indicator for this level.

* Or take: If both the closing on the signal and the limit order are enabled, then whatever comes first will work.

* After SO: Activate this TP level only after the specified number of safety orders has been executed. This allows you to set closer targets for riskier (deeply averaged) positions.

// ------------------------

6. 🔬 GRID and MultiGrid Analysis on Lower TFs (LTF) 🔬

This group activates one of the most important functions for accurate testing of grid strategies.

* Enable LTF Calculation ⮕ The main switch of the analysis mode on the lower timeframes.

* Timeframe selection: A drop-down list where you can select a timeframe for detailed analysis. For example, if your main schedule is 1 hour, you can select 1 minute here. The strategy will emulate the trading of minute candles within each hour candle.

❗️Important: As mentioned in the first part, the use of this mode is critically necessary to obtain realistic backtest results, especially for strategies with a dense grid of orders. Without it, the results may be overly optimistic and not reflect the real dynamics of the market. It should be remembered that TradingView imposes a limit on the number of intra-bars (minor TF bars) that can be requested. This is usually about 100,000 bars.

// ------------------------

7. 🕘 Backtest Date Range 🕘

This group allows you to focus testing on a specific historical period.

* Limit Date Range: Enables date filtering.

* Start time: The date and time when the strategy will start analyzing and opening deals.

* End time: The date and time after which the strategy will stop opening new deals and complete testing.

// ------------------------

8. 🎨 Visualization 🎨

All the options responsible for the appearance and information content of the chart are collected here.

* Show PnL labels: Enables/disables the display of text labels with the result (profit/loss) after closing each trade.

* Statistics Table: Enables/disables the main dashboard with detailed statistics on the results of the backtest.

* Strategy Settings Table: Enables/disables an additional panel that summarizes all the key parameters of the current configuration.

* Monthly Profit Table: Enables/disables a table with a breakdown of percentage returns by month and year.

* Table settings: For each of the three tables, you can individually adjust the Text size and Table Position on the screen to position them as conveniently as possible.

* Decimal places: Defines how many decimal places will be displayed in numeric values in tables and on labels.

// ------------------------

9. ✉️ Webhook Settings ✉️

This group is intended for traders who want to automate trading on strategy signals using third-party services and exchanges (for example, 3Commas, WunderTrading, Cryptorobotics, Cryptohopper, Bitsgap, Binance, ByBit, OKX, Pionex, Bitget or proprietary solutions).

For each key event in the strategy, there is a separate switch and a text field:

* Webhook for Open: Enable and set a message for the webhook that will be sent when the base order is opened.

* Webhook for Averaging: A message sent when executing any insurance order.

* Webhook for Take Profit: A message sent when closing on take profit (including partial ones).

* Webhook for Stop-Loss: A message sent when a stop loss is closed.

You can insert a JSON code or any other message format that your service requires for automation into the text fields. The strategy supports special placeholders (for example, `{{strategy.order.alert_message}}`), which allow you to dynamically insert the necessary data into the message, such as the amount of USDT or the percentage of the deposit for entry, averaging and take profit orders.

光速量化-头皮策略v1.1Version: Unlimited trial version.

Principle: RSI and moving average complement each other, taking a bite of both oscillation and trend.

Disadvantage: High drawdown.

Disclaimer: The scalp strategy v1.1 of Lightspeed Quantification is designed for trial users. Those who use this strategy are responsible for their own assets, and any losses incurred are not the responsibility of the author.

版本:无期限试用版。

原理:RSI与均线配合,震荡与趋势都吃一口。

缺点:回撤高。

声明:光速量化的头皮策略v1.1是面向试用者体验的,使用该策略的人请为自己的资产负责,产生任何损失与作者无关。

Gold Multi TP Strategy📘 Strategy Description: Gold Multi Take-Profit Strategy (XAUUSD)

This strategy is designed for Gold (XAUUSD) and works on any timeframe (recommended: 15-min or higher). It executes trades based on a simple EMA crossover logic with optional higher-timeframe and ATR-based filters to confirm trend direction and volatility.

🔑 Core Features

✅ Directional control: Trade only long, short, or both directions (Strategy Direction)

✅ Multi-level Take Profit: Scale out at up to 4 configurable profit targets

✅ Fixed Stop Loss: Set custom SL distance for risk control

✅ Position Sizing: Allocate different percentages to each TP level

✅ HTF Trend Filter (optional): Align trades with weekly candle trend

✅ ATR Filter (optional): Improve entries with volatility-based filter

⚙️ Inputs Explained

Input Name Function

Strategy Direction Choose to trade all, long, or short only

Length of Filter Length of the moving average used for HTF trend filter

Candle Time Reference candle timeframe in minutes (e.g., 1440 for daily)

Length of ATR Period for ATR calculation (volatility)

HTF Higher timeframe for filter (e.g., 1 week)

Filter Checkbox Enable/disable trend filter

Stop Loss Fixed SL distance in price units

Qty_percent1-3 % of position allocated to TP1–TP3 (rest goes to TP4)

Take profit1–4 TP levels (in price units) from entry price

🧠 Logic Overview

Entry triggered on EMA 20/50 crossover

Optional filter: entry allowed only if current price is above its HTF MA (bullish) or below (bearish)

Position is scaled out at up to 4 profit levels using different qty_percent

SL remains fixed throughout the trade

📊 Best Use

Intraday trading on XAUUSD, ideally during London/NY sessions

Trending or breakout conditions

Works best with additional confluence (price action, S/R, news)

EUR/USD Multi-Layer Statistical Regression StrategyStrategy Overview

This advanced EUR/USD trading system employs a triple-layer linear regression framework with statistical validation and ensemble weighting. It combines short, medium, and long-term regression analyses to generate high-confidence directional signals while enforcing strict risk controls.

Core Components

Multi-Layer Regression Engine:

Parallel regression analysis across 3 customizable timeframes (short/medium/long)

Projects future price values using prediction horizons

Statistical significance filters (R-squared, correlation, slope thresholds)

Signal Validation System:

Lookback validation tests historical prediction accuracy

Ensemble weighting of layer signals (adjustable influence per timeframe)

Confidence scoring combining statistical strength, layer agreement, and validation accuracy

Risk Management:

Position sizing scaled by signal confidence (1%-100% of equity)

Daily loss circuit breaker (halts trading at user-defined threshold)

Forex-tailored execution (pip slippage, percentage-based commissions)

Visual Intelligence:

Real-time regression line plots (3 layered colors)

Projection markers for short-term forecasts

Background coloring for market bias indication

Comprehensive statistics dashboard (R-squared metrics, validation scores, P&L)

Key Parameters

Category Settings

Regression Short/Med/Long lengths (20/50/100 bars)

Statistics Min R² (0.65), Correlation (0.7), Slope (0.0001)

Validation 30-bar lookback, 10-bar projection

Risk Controls 50% position size, 12% daily loss limit, 75% confidence threshold

Trading Logic

Entries require:

Ensemble score > |0.5|

Confidence > threshold

Short & medium-term significance

Active daily loss limit not breached

Exits triggered by:

Opposite high-confidence signals

Daily loss limit violation (emergency exit)

The strategy blends quantitative finance techniques with practical trading safeguards, featuring a self-optimizing design where signal quality directly impacts position sizing. The visual dashboard provides real-time feedback on model performance and market conditions.

Long and Short Strategy with Multi Indicators [B1P5]Long and Short Strategy with RSI, ROC, MA Selection, Exit Visualization, and Strength Indicator

Enhanced Market Structure StrategyATR-Based Risk Management:

Stop Loss: 2 ATR from entry (configurable)

Take Profit: 3 ATR from entry (configurable)

Dynamic Position Sizing: Based on ATR stop distance and max risk percentage

Advanced Signal Filters:

RSI Filter:

Long trades: RSI < 70 and > 40 (avoiding overbought)

Short trades: RSI > 30 and < 60 (avoiding oversold)

Volume Filter:

Requires volume > 1.2x the 20-period moving average

Ensures institutional participation

MACD Filter (Optional):

Long: MACD line above signal line and rising

Short: MACD line below signal line and falling

EMA Trend Filter:

50-period EMA for trend confirmation

Long trades require price above rising EMA

Short trades require price below falling EMA

Higher Timeframe Filter:

Uses 4H/Daily EMA for multi-timeframe confluence

Enhanced Entry Logic:

Regular Entries: IDM + BOS + ALL filters must pass

Sweep Entries: Failed breakouts with tighter stops (1.6 ATR)

High-Probability Focus: Only trades when multiple confirmations align

Visual Improvements:

Detailed Entry Labels: Show entry, stop, target, and risk percentage

SL/TP Lines: Visual representation of risk/reward

Filter Status: Bar coloring shows when all filters align

Comprehensive Statistics: Real-time performance metrics

Key Strategy Parameters:

pinescript// Recommended Settings for Different Markets:

// Forex (4H-Daily):

// - CHoCH Period: 50-75

// - ATR SL: 2.0, ATR TP: 3.0

// - All filters enabled

// Crypto (1H-4H):

// - CHoCH Period: 30-50

// - ATR SL: 2.5, ATR TP: 4.0

// - Volume filter especially important

// Indices (4H-Daily):

// - CHoCH Period: 50-100

// - ATR SL: 1.8, ATR TP: 2.7

// - EMA and MACD filters crucial

Expected Performance Improvements:

Win Rate: 55-70% (improved filtering)

Profit Factor: 2.0-3.5+ (better risk/reward with ATR)

Reduced Drawdown: Stricter filters reduce false signals

Consistent Risk: ATR-based stops adapt to volatility

This enhanced version provides much more robust signal filtering while maintaining the core market structure edge, resulting in higher-probability trades with consistent risk management.

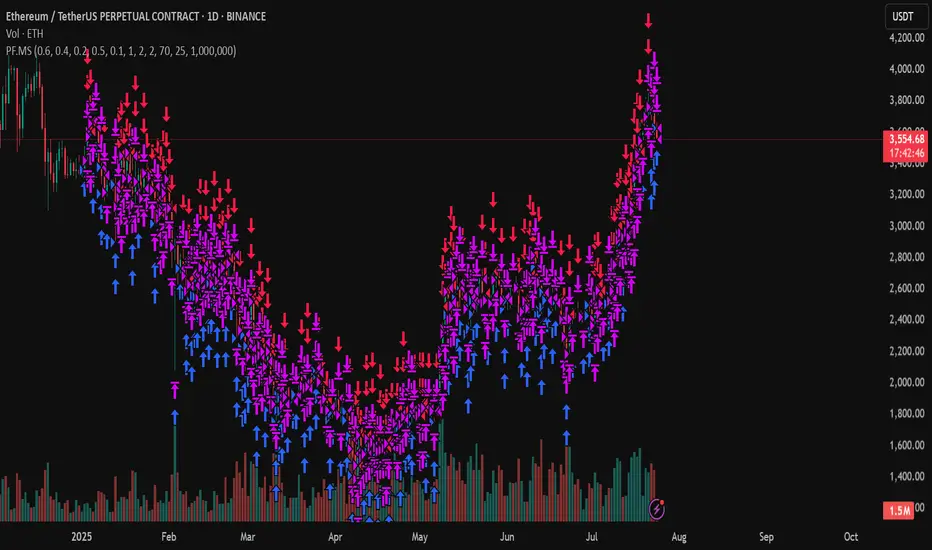

PF.MSThe Pressure & Flow Momentum Strategy (PF.MS) detects market pressure buildup through advanced candlestick analysis and captures momentum flow when conditions align, providing accurate buy and sell signals across cryptocurrencies and stocks—but even sophisticated strategies can be wrong when markets turn brutal without warning. The system reads real-time pressure dynamics (buying vs selling forces, wick patterns, volatility conditions) to identify when smart money is positioning, then captures the resulting momentum flow with precise entry and exit timing. While highly accurate at detecting pressure shifts and momentum changes, the strategy can still face losses during sudden news events or when market sentiment overrides technical patterns. The PF.MS combines intelligent pressure detection with momentum capture, trailing profit protection and strict stop losses

LANZ Strategy 6.0 [Backtest]🔷 LANZ Strategy 6.0 — Precision Backtesting Based on 09:00 NY Candle, Dynamic SL/TP, and Lot Size per Trade

LANZ Strategy 6.0 is the simulation version of the original LANZ 6.0 indicator. It executes a single LIMIT BUY order per day based on the 09:00 a.m. New York candle, using dynamic Stop Loss and Take Profit levels derived from the candle range. Position sizing is calculated automatically using capital, risk percentage, and pip value — allowing accurate trade simulation and performance tracking.

📌 This is a strategy script — It simulates real trades using strategy.entry() and strategy.exit() with full money management for risk-based backtesting.

🧠 Core Logic & Trade Conditions

🔹 BUY Signal Trigger:

At 09:00 a.m. NY (New York time), if:

The current candle is bullish (close > open)

→ A BUY order is placed at the candle’s close price (EP)

Only one signal is evaluated per day.

⚙️ Stop Loss / Take Profit Logic

SL can be:

Wick low (0%)

Or dynamically calculated using a % of the full candle range

TP is calculated using the user-defined Risk/Reward ratio (e.g., 1:4)

The TP and SL levels are passed to strategy.exit() for each trade simulation.

💰 Risk Management & Lot Size Calculation

Before placing the trade:

The system calculates pip distance from EP to SL

Computes the lot size based on:

Account capital

Risk % per trade

Pip value (auto or manual)

This ensures every trade uses consistent, scalable risk regardless of instrument.

🕒 Manual Close at 3:00 p.m. NY

If the trade is still open by 15:00 NY time, it will be closed using strategy.close().

The final result is the actual % gain/loss based on how far price moved relative to SL.

📊 Backtest Accuracy

One trade per day

LIMIT order at the candle close

SL and TP pre-defined at execution

No repainting

Session-restricted (only runs on 1H timeframe)

✅ Ideal For:

Traders who want to backtest a clean and simple daily entry system

Strategy developers seeking reproducible, high-conviction trades

Users who prefer non-repainting, session-based simulations

👨💻 Credits:

💡 Developed by: LANZ

🧠 Logic & Money Management Engine: LANZ

📈 Designed for: 1H charts

🧪 Purpose: Accurate simulation of LANZ 6.0's NY Candle Entry system

RSI Divergence StrategyOverview

The RSI Divergence Strategy Indicator is a trading tool that uses the RSI and divergences created to generate high-probability buy and sell signals.

I have provided the best formula of numbers to use for BTC on a 30 minute timeframe.

You can change where on RSI you enter and exit both long or short trades. This way you can experiment on different tokens using different entry/exit points. Can use on multiple timeframes.

This strategy is designed to open and close long or short trades based on the levels you provide it. You can then check on the RSI where the best levels are for each token you want to trade and amend it as required to generate a profitable strategy.

How It Works

The RSI Divergence Strategy Indicator uses bear and bull divergences in conjuction with a level you have input on the RSI.

RSI for Overbought/Oversold:

• Input variables for entry and exit levels and when the entry levels combine with a bear or bull divergence signal, a trade is alerted.

RSI Divergence:

• Buy and sell signals are confirmed when the RSI creates bearish or bullish divergences and these divergences are in the same area as your levels you input for entry to short or long.

After 7 years of experience and testing I have calculated the exact numbers required and produced a formula to calculate the exact input variables for a 30 minute Bitcoin chart.

Key Features

1️⃣ Divergence Identification – Ensures trades are taken only when a bull or bear divergence has formed.

2️⃣ Overbought/Oversold Input Filtering – Set up your own variables on the RSI for different markets after identifying patterns on the RSI in relation to a bearish or bullish divergence.

3️⃣ Works on any chart – Suitable for all markets and timeframes once you input the correct variables for entry and exit levels.

How to Use

🟢 Basic Trading:

• Use on any timeframe.

• Enter trade only when alert has fired off. Close when it says to exit.

• Change entry and exit levels in the properties of the strategy indicator.

• Make entry and exit levels coincide with bearish or bullish divergences on the RSI.

Check the strategy tester to see backtesting so you know if the indicator is profitable or not for that market and timeframe as each crypto token is different and so is the timeframe you choose.

📢 Webhook Automation:

• Set up TradingView Alerts to auto-execute trades via Webhook-compatible platforms.

Key additions for divergence visualization:

Divergence Arrows:

Bullish divergence: Green label with white 'bull ' text

Bearish divergence: Red label with white 'bear' text

Positioned at the pivot point

Divergence Lines:

Connects consecutive RSI pivot points

Automatically drawn between consecutive pivot points

Enhanced RSI Coloring:

Overbought zone: Red

Oversold zone: Green

Neutral zone: Gray

The visualization helps you instantly spot:

Where divergences are forming on the RSI

The pattern of higher lows (bullish) or lower highs (bearish)

Contextual coloring of RSI relative to standard levels

All divergence markers appear at the correct historical pivot points, making it easy to visually confirm divergence patterns as they develop.

Strategy levels and background zones also shown to help visual look.

Why This Combination?

This indicator is just a simple RSI tool.

It is designed to filter out weak trades and only execute trades that have:

✅ RSI Divergence

✅ Overbought or Oversold Conditions

It does not calculate downtrends or bear markets so care is recommended taking long trades during these times.

Why It’s Worth Using?

📈 Open Source – Free to use and learn from.

📉 Long or Short Term Trading Style – Entry/Exit parameters options are designed for both short or long term trades allowing you to experiment until you find a profitable strategy for that market you want to trade.

📢 Seamless Webhook Automation – Execute trades automatically with TradingView alerts.

💲 Ready to trade smarter?

✅ Add the RSI Divergence Strategy Indicator to your TradingView chart.

DVPOOverview

The DVPO (Dynamic Volume Profile Oscillator) Strategy is a comprehensive and highly customizable trading tool designed for precision and control. It is built around a unique, volume-driven oscillator that identifies potential market entries by analyzing the relationship between price, volume, and volatility.

This strategy is not just another signal generator; it's a complete framework that includes dynamic entry logic, adaptive risk management (ATR Stop Loss and R:R-based Take Profit), and a powerful dashboard of 10+ optional confirmation filters to help you tailor the strategy to your specific instrument, timeframe, and trading style.

The Core Concept: The DVPO Oscillator

The heart of this strategy is the DVPO oscillator. Unlike standard oscillators like RSI or Stochastics, the DVPO's primary goal is to quantify how far the current price has deviated from its recent volume-weighted "fair value."

Here’s how it works conceptually:

Micro Volume Profile: The indicator first analyzes a recent period of bars (defined by Lookback Period) to build a mini-profile of price and volume.

Volume-Weighted Mean: From this profile, it calculates a volume-weighted average price (VWAP) and the average deviation from that mean. This establishes the central point of value for the recent period.

Deviation Measurement: The oscillator's value is derived from how far the current price is from this calculated mean, scaled by the observed price deviation and a user-defined Sensitivity. A value above the midline suggests the price is trading at a premium, while a value below suggests it's at a discount.

Adaptive Volatility Zones: Instead of using fixed overbought/oversold levels (e.g., 70/30), the DVPO calculates dynamic upper and lower zones using the standard deviation of the oscillator itself. These zones expand and contract based on recent market volatility.

An entry signal is triggered not just when the oscillator is "overbought" or "oversold," but when it breaks out of these adaptive volatility zones, signaling that a statistically significant price movement is underway.

📈 Long Entry Condition : The oscillator crosses above the dynamic upper zone.

📉 Short Entry Condition : The oscillator crosses below the dynamic lower zone.

Integrated Risk & Trade Management

A signal is useless without proper risk management. This strategy has professional-grade risk management built directly into its logic.

Stop Loss (ATR-Based): The Stop Loss is not a fixed percentage. It is calculated using the Average True Range (ATR), allowing it to adapt automatically to the market's current volatility. In volatile periods, the stop will be wider; in quiet periods, it will be tighter.

Take Profit (Risk/Reward Ratio): The Take Profit level is calculated based on a user-defined Risk/Reward Ratio. If you set a ratio of 2.0, the Take Profit target will be placed at twice the distance of the Stop Loss from your entry price.

Dynamic Position Sizing: The strategy can automatically calculate the trade quantity for you. It determines the position size based on your specified Capital Size and the % Risk Per Trade you are willing to accept, ensuring disciplined risk control on every trade.

The Filter Dashboard : Enhance Your Signal Quality

To help reduce false signals and adapt to different market conditions, the strategy includes a comprehensive dashboard of optional confirmation filters. An entry signal will only be executed if it aligns with all the filters you have activated.

Trend & Momentum Filters :

T3, VMA, & VWAP Trend Filters: Utilize a suite of advanced moving averages (T3, Variable Moving Average, and a session-based VWAP) to ensure your trades are aligned with the dominant trend.

ADX Filter: Confirms that the market has sufficient directional strength for a trend-following trade, helping to avoid entries during choppy conditions.

Kaufman Efficiency Filter: Uses the Kaufman Efficiency Ratio to measure market noise. It only allows trades when the market is trending efficiently.

Volume & Market State Filters :

Volume Flow (VFI): A sophisticated volume-based filter that confirms whether volume is supporting the price move.

TDFI (Trader's Dynamic Index): A market state indicator designed to identify when the market is primed for a strong, directional move.

Flat Market Detector: A unique filter that identifies and avoids trading in sideways or ranging markets where trend strategies typically underperform.

Trade Condition Filters :

Min TP / Max SL %: Filter out trades where the risk/reward profile doesn't meet your minimum requirements (e.g., ignore a trade if the ATR-based stop loss is more than 10% away from the price).

Session Filters: Allows you to enable or disable trading on specific days of the week and to set a Cooldown Period (a set number of bars to wait after a trade closes before looking for a new entry).

How To Use This Strategy

Start with the Core: Begin by configuring the DVPO Oscillator settings (Lookback Period, Sensitivity, Zone Width) and your Risk Management parameters (ATR Multiplier, RR Ratio, % Risk Per Trade). These form the foundation of the strategy.

Backtest and Observe: Use TradingView's Strategy Tester to see how the core signals perform on your chosen asset and timeframe.

Layer Filters Intelligently: Enable the confirmation filters one by one and re-run your backtest. Observe how each filter impacts performance (e.g., does the T3 filter increase profitability but reduce the number of trades?). The goal is to find the optimal balance between signal quality and frequency.

Visualize and Analyze: Use the Show Risk/Reward Area option to plot your entry, stop loss, and take profit levels directly on the chart for every trade, providing a clear visual representation of your trade plan.

Disclaimer: This strategy is provided for educational and analytical purposes only. Past performance is not indicative of future results. All trading involves risk, and you should conduct your own thorough backtesting and analysis before deploying any strategy in a live market.

Price Statistical Strategy-Z Score V 1.01

Price Statistical Strategy – Z Score V 1.01

Overview

A technical breakdown of the logic and components of the “Price Statistical Strategy – Z Score V 1.01”.

This script implements a smoothed Z-Score crossover mechanism applied to the closing price to detect potential statistical deviations from local price mean. The strategy operates solely on price data (close) and includes signal spacing control and momentum-based candle filters. No volume-based or trend-detection components are included.

Core Methodology

The strategy is built on the statistical concept of Z-Score, which quantifies how far a value (closing price) is from its recent average, normalized by standard deviation. Two moving averages of the raw Z-Score are calculated: a short-term and a long-term smoothed version. The crossover between them generates long entries and exits.

Signal Conditions

Entry Condition:

A long position is opened when the short-term smoothed Z-Score crosses above the long-term smoothed Z-Score, and additional entry conditions are met.

Exit Condition:

The position is closed when the short-term Z-Score crosses below the long-term Z-Score, provided the exit conditions allow.

Signal Gapping:

A minimum number of bars (Bars gap between identical signals) must pass between repeated entry or exit signals to reduce noise.

Momentum Filter:

Entries are prevented during sequences of three or more consecutively bullish candles, and exits are prevented during three or more consecutively bearish candles.

Z-Score Function

The Z-Score is calculated as:

Z = (Close - SMA(Close, N)) / STDEV(Close, N)

Where N is the base period selected by the user.

Input Parameters

Enable Smoothed Z-Score Strategy

Enables or disables the Z-Score strategy logic. When disabled, no trades are executed.

Z-Score Base Period

Defines the number of bars used to calculate the simple moving average and standard deviation for the Z-Score. This value affects how responsive the raw Z-Score is to price changes.

Short-Term Smoothing

Sets the smoothing window for the short-term Z-Score. Higher values produce smoother short-term signals, reducing sensitivity to short-term volatility.

Long-Term Smoothing

Sets the smoothing window for the long-term Z-Score, which acts as the reference line in the crossover logic.

Bars gap between identical signals

Minimum number of bars that must pass before another signal of the same type (entry or exit) is allowed. This helps reduce redundant or overly frequent signals.

Trade Visualization Table

A table positioned at the bottom-right displays live PnL for open trades:

Entry Price

Unrealized PnL %

Text colors adapt based on whether unrealized profit is positive, negative, or neutral.

Technical Notes

This strategy uses only close prices — no trend indicators or volume components are applied.

All calculations are based on simple moving averages and standard deviation over user-defined windows.

Designed as a minimal, isolated Z-Score engine without confirmation filters or multi-factor triggers.

Adaptive Signal OracleAdaptive Signal Oracle – Precision Forecasting with Weighted KNN & HMA Trend Logic

🔍 Overview

Adaptive Signal Oracle is a forward-looking trend prediction strategy that merges non-repainting technical analysis with a machine-learning-inspired forecasting model. Built from scratch, it is not a mashup of off-the-shelf indicators. Instead, it uses a handcrafted K-Nearest Neighbors (KNN)-style prediction engine combined with a classic HMA (Hull Moving Average) trend filter to deliver actionable, high-confidence entries.

📈 Core Components Explained

🔸 1. KNN-Weighted Future Predictor (Custom Engine)

Simulates a machine learning process using historical price behavior.

Compares current conditions to a rolling dataset of past feature/label pairs.

Assigns weights based on distance, forming a probabilistic directional bias.

Generates:

Prediction Probability (% confidence)

Expected Price Movement Magnitude

Dynamic Trade Targets (TP1/TP2)

🔸 2. HMA Trend Filter (Hull Moving Average)

Used for real-time trend confirmation.

Prevents entry during whipsaws by enforcing directional alignment.

Non-repainting and adaptive to volatility swings.

🔸 3. Risk-Managed Execution Logic

Built-in 2-level take-profit system:

TP1: Partial exit (50%)

TP2: Full exit (remaining 100%)

Hard-coded stop-loss at a configurable percentage (default: 2%)

Includes cooldown logic to prevent same-bar entries and exits

🔸 4. Integrated Visual Dashboard

Tracks:

Trade status

Entry price

TP/SL hits

Trend direction

Real-time PnL

Dashboard is resizable and repositionable for user control

🔸 5. Clean Bar Coloring

Highlights predicted direction with green (bullish) and red (bearish) candles

Enhances signal visibility without interfering with price action

⚠️ Important Notes

This script does not repaint.

All calculations are based on confirmed historical data, using bar-closed logic only.

Ideal for crypto, forex, and trending asset classes, especially on the 1H+ timeframes.

Not intended for use as financial advice or automated investment decision-making.

🧠 How to Use

Set desired TP/SL levels in the strategy inputs.

Adjust k-value and lookback for best fit with your instrument.

Monitor the dashboard and colored bars for trade entries.

Use as part of a broader system with structure, support/resistance, or volume confirmation if needed.

🛡️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice. Past performance does not guarantee future results. Always test on historical data and demo environments before applying to live trading. The author is not liable for any financial decisions made based on this script.

Timeframe StrategyThis is a multi-timeframe trading strategy inspired by Ross Cameron's style, optimized for scalping and trend-following across various timeframes (1m, 5m, 15m, 1h, and 1D). The strategy integrates a comprehensive set of technical indicators, dynamic risk management, and visual tools.

Core Features

Dynamic Take Profit, Stop Loss & Trailing Stop

> Separate settings per timeframe for:

-TP% (Take Profit)

-SL% (Stop Loss)

-Trailing Stop %

-Cooldown bars

> Configurable via UI inputs.

>Smart Entry Conditions

Bullish entry: EMA9 crossover EMA20 and EMA50 > EMA200

Bearish entry: EMA9 crossunder EMA20 and EMA50 < EMA200

>Additional confirmation filters:

-Volume Filter (enabled/disabled via UI)

-Time Filter (e.g., only between 15:00–20:00 UTC)

-Spike Filter: rejects high-volatility candles

-RSI Filter: above/below 50 for trend confirmation

-ADX Filter (only applied on 1m, e.g., ADX > 15)

-Micro-Volatility Filter: minimum range percentage (1m only)

-Trend Filter (1m only): price must be above/below EMA200

>Trailing Stop Logic

-Configurable for each timeframe.

- Optional via toggle (use_trailing).

>Trade Cooldown Logic

-Prevents consecutive trades within X bars, configurable per timeframe.

>Technical Indicators Used

-EMA 9 / 20 / 50 / 200

-VWAP

-RSI (14)

-ATR (14) for volatility-based spike filtering

-Custom-calculated ADX (14) (manually implemented)

>Visual Elements

🔼/🔽 Entry signals (long/short) plotted on the chart.

📉 Table in bottom-left:

Displays current values of EMA/VWAP/volume/ATR/ADX.

> Optional "Tab info" panel in top-right (toggleable):

-Timeframe & strategy settings

-Live status of filters (volume, time, cooldown, spike, RSI, ADX, range, trend)

-Uses emoji (✅ / ❌) for quick diagnostics.

>User Customization

-Inputs per timeframe for all key parameters.

-Toggle switches for:

-Trailing stop

-Volume filter

-Info table visibility

This strategy is designed for active traders seeking a balance between momentum entry, risk control, and adaptability across timeframes. It's ideal for backtesting quick reversals or breakout setups in fast markets, especially at lower timeframes like 1m or 5m.

Funding Rate Strategy IndicatorDescription

Funding Rate Backtest Strategy uses smoothed funding‐rate dynamics to trigger long/short trades, enhanced by volume, session and daily‐limit filters, plus configurable profit-taking, stop-loss and trailing stops. It is designed for perpetual‐swap markets (e.g. BTCUSDT) where funding costs reflect market sentiment.

1. Strategy Logic & Components

Funding Rate Source

External: real exchange funding rate (e.g. Binance funding).

Custom: manual override value.

Simulate: sine‐wave test data between –3 and +3 to validate behavior.

Entry Conditions

LONG when fundingRate ≤ Long Threshold (default –2.0)

SHORT when fundingRate ≥ Short Threshold (default +2.0)

Volume Filter: requires a ≥ 5% increase vs prior bar.

4H Session Filter: only triggers on new 4-hour bars (optional).

Daily Cap: max 5 signals per calendar day (prevents overtrading).

Weekend Trading: on/off toggle for Saturday–Sunday.

Exit Conditions

Funding Normalization: exit LONG when fundingRate > –0.5; exit SHORT when fundingRate < +0.5.

Profit-Taking & Stop-Loss: default TP = 5%, SL = 3% of entry price.

Trailing Stop: optional 2% trailing (togglable).

2. Default Settings & Backtest Parameters

Account Size: $10,000

Position Sizing: 10% of equity per trade

Commission: 0.10% per side

Slippage: 0.05% per trade

Instrument & Timeframe: BTCUSDT perpetual, 1H bars, Jan 1 2022 – Dec 31 2023

Volume Increase: 5%

Session Filter: 4-hour bars only

Max Signals/Day: 5

Weekend Trading: Enabled

3. Backtest Results (Jan 2022–Dec 2023)

Total Trades: 142

Win Rate: 55.6%

Average R/R: 1 : 1.4

Max Drawdown: 14.8%

Net Return: +22.3%

These results assume realistic commission (0.1%) and slippage (0.05%). Past performance is not indicative of future results.

4. Default Properties Explained

Property Default Description

rateSourceChoice External Select funding‐rate data source

fundingRateLongThreshold –2.0 Funding ≤ –2% → LONG condition

fundingRateShortThreshold +2.0 Funding ≥ +2% → SHORT condition

volumeIncreasePercent 5.0 Min % volume increase vs prior bar

enableFourHourFilter true Only trigger on new 4H sessions

maxSignalsPerDay 5 Daily cap on entries

exitLongThreshold –0.5 Funding > –0.5% → exit LONG

exitShortThreshold +0.5 Funding < +0.5% → exit SHORT

takeProfitPercent 5.0 Fixed profit target in %

stopLossPercent 3.0 Fixed stop‐loss in %

useTrailingStop false Toggle trailing stop

trailingStopPercent 2.0 Trailing stop distance in %

allowWeekendTrading true Allow entries on Sat/Sun

5. How to Use

Add to Chart → search “Funding Rate Backtest.”

Configure Inputs → choose your funding‐rate feed, adjust thresholds, volume and session filters.

Position Sizing → defaults to 10% equity; adjust if desired.

Monitor Table & Signals → on‐chart shapes mark entries/exits; status table shows open P&L and signals count.

Risk Management → always verify commission/slippage settings; limit risk to sustainable levels (≤ 10% equity per trade).

6. Warnings & Disclaimer

This strategy is for educational purposes only. Real funding rates may differ—replace simulation or custom inputs with actual data. Always apply your own analysis and risk management. Past backtest performance does not guarantee future results.