Trend Vector Pro v2.0Trend Vector Pro v2.0

👨💻 Developed by: Mohammed Bedaiwi

💡 Strategy Overview & Coherence

Trend Vector Pro (TVPro) is a momentum-based trend & reversal strategy that uses a custom smoothed oscillator, an optional ADX filter, and classic Pivot Points to create a single, coherent trading framework.

Instead of stacking random indicators, TVPro is built around these integrated components:

A custom momentum engine (signal generation)

An optional ADX filter (trend quality control)

Daily Pivot Points (context, targets & S/R)

Swing-based “Golden Bar” trailing stops (trade management)

Optional extended bar detection (overextension alerts)

All parts are designed to work together and are documented below to address originality & usefulness requirements.

🔍 Core Components & Justification

1. Custom Momentum Engine (Main Signal Source)

TVPro’s engine is a custom oscillator derived from the bar midpoint ( hl2 ), similar in spirit to the Awesome Oscillator but adapted and fully integrated into the strategy. It measures velocity and acceleration of price, letting the script distinguish between strong impulses, weakening trends, and pure noise.

2. ADX Filter (Trend Strength Validation – Optional)

Uses Average Directional Index (ADX) as a gatekeeper.

Why this matters: This prevents the strategy from firing signals in choppy, non-trending environments (when ADX is below the threshold) and keeps trades focused on periods of clear directional strength.

3. Classic Pivot Points (Context & Targets)

Calculates Daily Pivot Points ( PP, R1-R3, S1-S3 ) via request.security() using prior session data.

Why this matters: Momentum gives the signal, ADX validates the environment, and Pivots add external structure for risk and target planning. This is a designed interaction, not a random mashup.

🧭 Trend State Logic (5-State Bar Coloring)

The strategy uses the momentum's value + slope to define five states, turning the chart into a visual momentum map:

🟢 STRONG BULL (Bright Green): Momentum accelerating UP. → Strong upside impulse.

🌲 WEAK BULL (Dark Green): Momentum decelerating DOWN (while positive). → Pullback/pause zone.

🔴 STRONG BEAR (Bright Red): Momentum accelerating DOWN. → Strong downside impulse.

🍷 WEAK BEAR (Dark Red): Momentum decelerating UP (while negative). → Rally/short-covering zone.

🔵 NEUTRAL / CHOP (Cyan): Momentum is near zero (based on noise threshold). → Consolidation / low volatility.

🎯 Signal Logic Modes

TVPro provides two selectable entry styles, controlled by input:

Reversals Only (Cleaner Mode – Default): Targets trend flips. Entry triggers when the current state is Bullish (or Bearish) and the previous state was not. This reduces noise and over-trading.

All Strong Pulses (Aggressive Mode): Targets acceleration phases. Entry triggers when the bar turns to STRONG BULL or STRONG BEAR after any other state. This mode produces more trades.

📌 Risk Management Tools

🟡 Golden Bars – Trailing Stops: Yellow “Trail” Arrows mark confirmed Swing Highs/Lows. These are used as logical trailing stop levels based on market structure.

Extended Bars: Detects when price closes outside a 2-standard-deviation channel, flagging overextension where a pullback is more likely.

Pivot Points: Used as external targets for Take Profit and structural stop placement.

⚙️ Strategy Defaults (Crucial for Publication Compliance)

To keep backtest results realistic and in line with House Rules, TVPro is published with the following fixed default settings:

Order Size: 5% of equity per trade ( default_qty_value = 5 )

Commission: 0.04% per order ( commission_value = 0.04 )

Slippage: 2 ticks ( slippage = 2 )

Initial Capital: 10,000

📘 How to Trade with Trend Vector Pro

Entry: Take Long when a Long signal appears and confirm the bar is Green (Bull state). Short for Red (Bear state).

Stop Loss: Place the initial SL near the latest swing High/Low, or near a relevant Pivot level.

Trade Management: Follow Golden (Trail) Arrows to trail your stop behind structure.

Exits: Exit when: the trailing stop is hit, Price reaches a major Pivot level, or an opposite signal prints.

🛑 Disclaimer

This script is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always forward-test and use proper risk management before applying any strategy to live trading.

Momentumstrategy

ChronoPulse MS-MACD Resonance StrategyChronoPulse MS-MACD Resonance Strategy

A systematic trading strategy that combines higher-timeframe market structure analysis with dual MACD momentum confirmation, ATR-based risk management, and real-time quality assurance monitoring.

Core Principles

The strategy operates on the principle of multi-timeframe confluence, requiring agreement between:

Market structure breaks (CHOCH/BOS) on a higher timeframe

Dual MACD momentum confirmation (classic and crypto-tuned profiles)

Trend alignment via directional EMAs

Volatility and volume filters

Quality score composite threshold

Strategy Components

Market Structure Engine : Detects Break of Structure (BOS) and Change of Character (CHOCH) events using confirmed pivots on a configurable higher timeframe. Default structure timeframe is 240 minutes (4H).

Dual MACD Fusion : Requires agreement between two MACD configurations:

Classic MACD: 12/26/9 (default)

Fusion MACD: 8/21/5 (default, optimized for crypto volatility)

Both must agree on direction before trade execution. This can be disabled to use single MACD confirmation.

Trend Alignment : Uses two EMAs for directional bias:

Directional EMA: 55 periods (default)

Execution Trend Guide: 34 periods (default)

Both must align with trade direction.

ATR Risk Management : All risk parameters are expressed in ATR multiples:

Stop Loss: 1.5 × ATR (default)

Take Profit: 3.0 × ATR (default)

Trail Activation: 1.0 × ATR profit required (default)

Trail Distance: 1.5 × ATR behind price (default)

Volume Surge Filter : Optional gate requiring current volume to exceed a multiple of the volume SMA. Default threshold is 1.4× the 20-period volume SMA.

Quality Score Gate : Composite score (0-1) combining:

Structure alignment (0.0-1.0)

Momentum strength (0.0-1.0)

Trend alignment (0.0-1.0)

ATR volatility score (0.0-1.0)

Volume intensity (0.0-1.0)

Default threshold: 0.62. Trades only execute when quality score exceeds this threshold.

Execution Discipline : Trade budgeting system:

Maximum trades per session: 6 (default)

Cooldown bars between entries: 5 (default)

Quality Assurance Console : Real-time monitoring panel displaying:

Structure status (pass/fail)

Momentum confirmation (pass/fail)

Volatility readiness (pass/fail)

Quality score (pass/fail)

Discipline compliance (pass/fail)

Performance metrics (win rate, profit factor)

Net PnL

Certification requires: Win Rate ≥ 40%, Profit Factor ≥ 1.4, Minimum 25 closed trades, and positive net profit.

Integrity Suite : Optional validation panel that audits:

Configuration sanity checks

ATR data readiness

EMA hierarchy validity

Performance realism checks

Strategy Settings

strategy(

title="ChronoPulse MS-MACD Resonance Strategy",

shorttitle="ChronPulse",

overlay=true,

max_labels_count=500,

max_lines_count=500,

initial_capital=100000,

currency=currency.USD,

pyramiding=0,

commission_type=strategy.commission.percent,

commission_value=0.015,

slippage=2,

default_qty_type=strategy.percent_of_equity,

default_qty_value=2.0,

calc_on_order_fills=true,

calc_on_every_tick=true,

process_orders_on_close=true

)

Key Input Parameters

Structure Timeframe : 240 (4H) - Higher timeframe for structure analysis

Structure Pivot Left/Right : 3/3 - Pivot confirmation periods

Structure Break Buffer : 0.15% - Buffer for structure break confirmation

MACD Fast/Slow/Signal : 12/26/9 - Classic MACD parameters

Fusion MACD Fast/Slow/Signal : 8/21/5 - Crypto-tuned MACD parameters

Directional EMA Length : 55 - Primary trend filter

Execution Trend Guide : 34 - Secondary trend filter

ATR Length : 14 - ATR calculation period

ATR Stop Multiplier : 1.5 - Stop loss in ATR units

ATR Target Multiplier : 3.0 - Take profit in ATR units

Trail Activation : 1.0 ATR - Profit required before trailing

Trail Distance : 1.5 ATR - Distance behind price

Volume Threshold : 1.4× - Volume surge multiplier

Quality Threshold : 0.62 - Minimum quality score (0-1)

Max Trades Per Session : 6 - Daily trade limit

Cooldown Bars : 5 - Bars between entries

Win-Rate Target : 40% - Minimum for QA certification

Profit Factor Target : 1.4 - Minimum for QA certification

Minimum Trades for QA : 25 - Required closed trades

Signal Generation Logic

A trade signal is generated when ALL of the following conditions are met:

Higher timeframe structure shows bullish (CHOCH/BOS) or bearish structure break

Both MACD profiles agree on direction (if fusion enabled)

Price is above both EMAs for longs (below for shorts)

ATR data is ready and above minimum threshold

Volume exceeds threshold × SMA (if volume gate enabled)

Quality score ≥ quality threshold

Trade budget available (under max trades per day)

Cooldown period satisfied

Risk Management

Stop loss and take profit are set immediately on entry

Trailing stop activates after 1.0 ATR of profit

Trailing stop maintains 1.5 ATR distance behind highest profit point

Position sizing uses 2% of equity per trade (default)

No pyramiding (single position per direction)

Limitations and Considerations

The strategy requires sufficient historical data for higher timeframe structure analysis

Quality gate may filter out many potential trades, reducing trade frequency

Performance metrics are based on historical backtesting and do not guarantee future results

Commission and slippage assumptions (0.015% + 2 ticks) may vary by broker

The strategy is optimized for trending markets with clear structure breaks

Choppy or ranging markets may produce false signals

Crypto markets may require different parameter tuning than traditional assets

Optimization Notes

The strategy includes several parameters that can be tuned for different market conditions:

Quality Threshold : Lower values (0.50-0.60) allow more trades but may reduce average quality. Higher values (0.70+) are more selective but may miss opportunities.

Structure Timeframe : Use 240 (4H) for intraday trading, Daily for swing trading, Weekly for position trading

Volume Gate : Disable for low-liquidity pairs or when volume data is unreliable

Dual MACD Fusion : Disable for mean-reverting markets where single MACD may be more responsive

Trade Discipline : Adjust max trades and cooldown based on your risk tolerance and market volatility

Non-Repainting Guarantee

All higher timeframe data requests use lookahead=barmerge.lookahead_off to prevent repainting. Pivot detection waits for full confirmation before registering structure breaks. All visual elements (tables, labels) update only on closed bars.

Alerts

Three alert conditions are available:

ChronoPulse Long Setup : Fires when all long entry conditions are met

ChronoPulse Short Setup : Fires when all short entry conditions are met

ChronoPulse QA Certification : Fires when Quality Assurance console reaches CERTIFIED status

Configure alerts with "Once Per Bar Close" delivery to match the non-repainting design.

Visual Elements

Structure Labels : CHOCH↑, CHOCH↓, BOS↑, BOS↓ markers on structure breaks

Directional EMA : Orange line showing trend bias

Trailing Stop Lines : Green (long) and red (short) trailing stop levels

Dashboard Panel : Real-time status display (structure, MACD, ATR, quality, PnL)

QA Console : Quality assurance monitoring panel

Integrity Suite Panel : Optional validation status display

Recommended Usage

Forward test with paper trading before live deployment

Monitor the QA console until it reaches CERTIFIED status

Adjust parameters based on your specific market and timeframe

Respect the trade discipline limits to avoid over-trading

Review quality scores and adjust threshold if needed

Use appropriate commission and slippage settings for your broker

Technical Implementation

The strategy uses Pine Script v6 with the following key features:

Multi-timeframe data requests with lookahead protection

Confirmed pivot detection for structure analysis

Dynamic trailing stop management

Real-time quality score calculation

Trade budgeting and cooldown enforcement

Comprehensive dashboard and monitoring panels

All source code is open and available for review and modification.

Disclaimer

This script is for educational and informational purposes only. It is not intended as financial, investment, or trading advice. Past performance does not guarantee future results. Trading involves substantial risk of loss and is not suitable for all investors. Always conduct your own research and consult with a qualified financial advisor before making any trading decisions. The author and TradingView are not responsible for any losses incurred from using this strategy.

Momentum Swing 1–3 Weeks

✅ Entry (LONG) Conditions

Price above EMA9 and SMA20

SMA20 > SMA50 (trend confirmation)

MACD above the signal line

RSI between 50–65 (healthy momentum)

Volume at least 20% above the 20-day average

When all conditions align, a LONG signal is generated.

✅ Exit (SELL) Conditions

Price closes below EMA9

MACD gives a bearish crossover

Or TP/SL levels are hit

Position is closed.

✅ Multi-Stage Take Profit

TP1: ATR × 1.5 → closes 50% of the position

TP2: ATR × 3.0 → closes remaining 50%

✅ Stop Loss

ATR × 1.5 dynamic SL

✅ What This Strategy Aims For

Catching early trend continuation signals

Filtering weak / low-volume breakouts

Exiting when momentum fades

Eliminating emotional decision-making through rules

📌 Note

Backtest performance may vary by symbol and volatility. Proper risk management is strongly recommended.

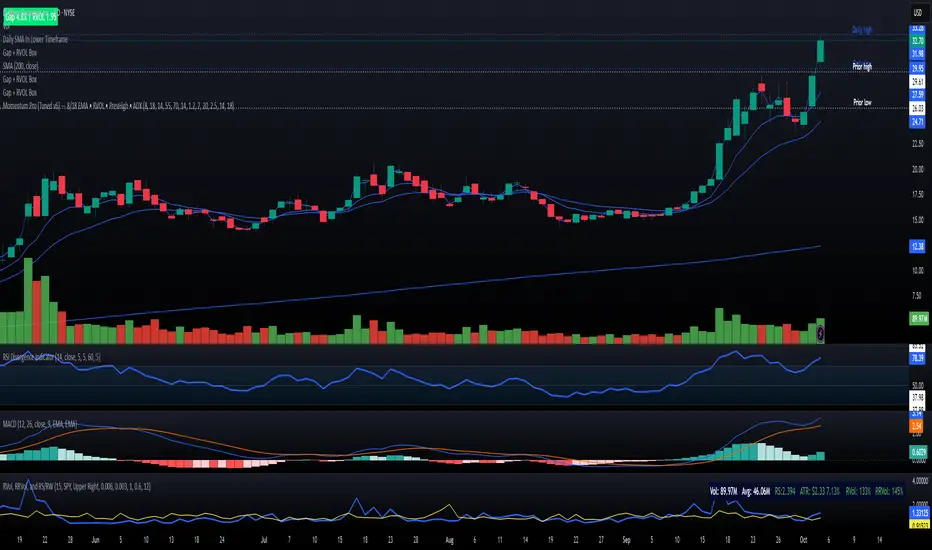

Momentum Pro (Tuned v6) — 8/18 EMA • RVOL • PrevHigh • ADXMomentum strategy with signals (VWAP + 9/20 EMA alignment, MACD hist > 0, RSI 55–70, RVOL filter, ATR stop, 2R target

RSI Momentum ScalperOverview

The "RSI Momentum Scalper" is a Pine Script v5 strategy crafted for trading highly volatile markets, with a special focus on newly listed cryptocurrencies. This strategy harnesses the Relative Strength Index (RSI) alongside volume analysis and momentum thresholds to pinpoint short-term trading opportunities. It supports both long and short trades, managed with customizable take profit, stop loss, and trailing stop levels, which are visually plotted on the chart for easy tracking.

Why I Created This Strategy

I developed the "RSI Momentum Scalper" because I was seeking a reliable trading strategy tailored to newly listed, highly volatile cryptocurrencies. These assets often experience rapid price fluctuations, rendering traditional strategies less effective. I aimed to create a tool that could exploit momentum and volume spikes while managing risk through adaptable exit parameters. This strategy is designed to address that need, offering a flexible approach for traders in dynamic crypto markets.

How It Works

The strategy utilizes RSI to identify momentum shifts, combined with volume confirmation, to trigger long or short entries. Trades are controlled with take profit, stop loss, and trailing stop levels, which adjust dynamically as the price moves in your favor. The trailing stop helps lock in profits, while the plotted exit levels provide clear visual cues for trade management.

Customizable Settings

The script is highly customizable, allowing you to adjust it to various market conditions and trading styles. Here’s a brief overview of the key settings:

Trade Mode: Select "Both," "Long Only," or "Short Only" to determine the trade direction.

(Default: Both)

RSI Length: Sets the lookback period for the RSI calculation (2 to 30).

(Default: 8)

A shorter length increases RSI sensitivity, suitable for volatile assets.

RSI Overbought: Defines the upper RSI threshold (60 to 99) for short entries.

(Default: 90)

Higher values signal stronger overbought conditions.

RSI Oversold: Defines the lower RSI threshold (1 to 40) for long entries.

(Default: 10)

Lower values indicate stronger oversold conditions.

RSI Momentum Threshold: Sets the minimum RSI momentum change (1 to 15) to trigger entries.

(Default: 14)

Adjusts the sensitivity to price momentum.

Volume Multiplier: Multiplies the volume moving average to filter high-volume bars (1.0 to 3.0).

(Default: 1)

Higher values require stronger volume confirmation.

Volume MA Length: Sets the lookback period for the volume moving average (5 to 50).

(Default: 13)

Influences the volume trend sensitivity.

Take Profit %: Sets the profit target as a percentage of the entry price (0.1 to 10.0).

(Default: 4.15)

Determines when to close a winning trade.

Stop Loss %: Sets the loss limit as a percentage of the entry price (0.1 to 6.0).

(Default: 1.85)

Protects against significant losses.

Trailing Stop %: Sets the trailing stop distance as a percentage (0.1 to 4.0).

(Default: 2.55)

Locks in profits as the price moves favorably.

Visual Features

Exit Levels: Take profit (green), fixed stop loss (red), and trailing stop (orange) levels are plotted when in a position.

Performance Table: Displays win rate, total trades, and net profit in the top-right corner.

How to Use

Add the strategy to your chart in TradingView.

Adjust the input settings based on the cryptocurrency and timeframe you’re trading.

Monitor the plotted exit levels for trade management.

Use the performance table to assess the strategy’s performance over time.

Notes

Test the strategy on a demo account or with historical data before live trading.

The strategy is optimized for short-term scalping; adjust settings for longer timeframes if needed.

Momentum Breakout StrategyBacktest a strategy where, when a candlestick on a timeframe rises more than a certain %, it enters a trade.

EMA Pullback Speed Strategy 📌 **Overview**

The **EMA Pullback Speed Strategy** is a trend-following approach that combines **price momentum** and **Exponential Moving Averages (EMA)**.

It aims to identify high-probability entry points during brief pullbacks within ongoing uptrends or downtrends.

The strategy evaluates **speed of price movement**, **relative position to dynamic EMA**, and **candlestick patterns** to determine ideal timing for entries.

One of the key concepts is checking whether the price has **“not pulled back too much”**, helping focus only on situations where the trend is likely to continue.

⚠️ This strategy is designed for educational and research purposes only. It does not guarantee future profits.

🧭 **Purpose**

This strategy addresses the common issue of **"jumping in too late during trends and taking unnecessary losses."**

By waiting for a healthy pullback and confirming signs of **trend resumption**, traders can enter with greater confidence and reduce false entries.

🎯 **Strategy Objectives**

* Enter in the direction of the prevailing trend to increase win rate

* Filter out false signals using pullback depth, speed, and candlestick confirmations

* Predefine Take-Profit (TP) and Stop-Loss (SL) levels for safer, rule-based trading

✨ **Key Features**

* **Dynamic EMA**: Reacts faster when price moves quickly, slower when market is calm – adapting to current momentum

* **Pullback Filter**: Avoids trades when price pulls back too far (e.g., more than 5%), indicating a trend may be weakening

* **Speed Check**: Measures how strongly the price returns to the trend using candlestick body speed (open-to-close range in ticks)

📊 **Trading Rules**

**■ Long Entry Conditions:**

* Current price is above the dynamic EMA (indicating uptrend)

* Price has pulled back toward the EMA (a "buy the dip" situation)

* Pullback depth is within the threshold (not excessive)

* Candlesticks show consecutive bullish closes and break the previous high

* Price speed is strong (positive movement with momentum)

**■ Short Entry Conditions:**

* Current price is below the dynamic EMA (indicating downtrend)

* Price has pulled back up toward the EMA (a "sell the rally" setup)

* Pullback is within range (not too deep)

* Candlesticks show consecutive bearish closes and break the previous low

* Price speed is negative (downward momentum confirmed)

**■ Exit Conditions (TP/SL):**

* **Take-Profit (TP):** Fixed 1.5% target above/below entry price

* **Stop-Loss (SL):** Based on recent price volatility, calculated using ATR × 4

💰 **Risk Management Parameters**

* Symbol & Timeframe: BTCUSD on 1-hour chart (H1)

* Test Capital: \$3000 (simulated account)

* Commission: 0.02%

* Slippage: 2 ticks (minimal execution lag)

* Max risk per trade: 5% of account balance

* Backtest Period: Aug 30, 2023 – May 9, 2025

* Profit Factor (PF): 1.965 (Net profit ÷ Net loss, including spreads & fees)

⚙️ **Trading Parameters & Indicator Settings**

* Maximum EMA Length: 50

* Accelerator Multiplier: 3.0

* Pullback Threshold: 5.0%

* ATR Period: 14

* ATR Multiplier (SL distance): 4.0

* Fixed TP: 1.5%

* Short-term EMA: 21

* Long-term EMA: 50

* Long Speed Threshold: ≥ 1000.0 (ticks)

* Short Speed Threshold: ≤ -1000.0 (ticks)

⚠️Adjustments are based on BTCUSD.

⚠️Forex and other currency pairs require separate adjustments.

🔧 **Strategy Improvements & Uniqueness**

Unlike basic moving average crossovers or RSI triggers, this strategy emphasizes **"momentum-supported pullbacks"**.

By combining dynamic EMA, speed checks, and candlestick signals, it captures trades **as if surfing the wave of a trend.**

Its built-in filters help **avoid overextended pullbacks**, which often signal the trend is ending – making it more robust than traditional trend-following systems.

✅ **Summary**

The **EMA Pullback Speed Strategy** is easy to understand, rule-based, and highly reproducible – ideal for both beginners and intermediate traders.

Because it shows **clear visual entry/exit points** on the chart, it’s also a great tool for practicing discretionary trading decisions.

⚠️ Past performance is not a guarantee of future results.

Always respect your Stop-Loss levels and manage your position size according to your risk tolerance.

PEAD strategy█ OVERVIEW

This strategy trades the classic post-earnings announcement drift (PEAD).

It goes long only when the market gaps up after a positive EPS surprise.

█ LOGIC

1 — Earnings filter — EPS surprise > epsSprThresh %

2 — Gap filter — first regular 5-minute bar gaps ≥ gapThresh % above yesterday’s close

3 — Timing — only the first qualifying gap within one trading day of the earnings bar

4 — Momentum filter — last perfDays trading-day performance is positive

5 — Risk management

• Fixed stop-loss: stopPct % below entry

• Trailing exit: price < Daily EMA( emaLen )

█ INPUTS

• Gap up threshold (%) — 1 (gap size for entry)

• EPS surprise threshold (%) — 5 (min positive surprise)

• Past price performance — 20 (look-back bars for trend check)

• Fixed stop-loss (%) — 8 (hard stop distance)

• Daily EMA length — 30 (trailing exit length)

Note — Back-tests fill on the second 5-minute bar (Pine limitation).

Live trading: enable calc_on_every_tick=true for first-tick entries.

────────────────────────────────────────────

█ 概要(日本語)

本ストラテジーは決算後の PEAD を狙い、

EPS サプライズがプラス かつ 寄付きギャップアップ が発生した銘柄をスイングで買い持ちします。

█ ロジック

1 — 決算フィルター — EPS サプライズ > epsSprThresh %

2 — ギャップフィルター — レギュラー時間最初の 5 分足が前日終値+ gapThresh %以上

3 — タイミング — 決算当日または翌営業日の最初のギャップのみエントリー

4 — モメンタムフィルター — 過去 perfDays 営業日の騰落率がプラス

5 — リスク管理

• 固定ストップ:エントリー − stopPct %

• 利確:終値が日足 EMA( emaLen ) を下抜け

█ 入力パラメータ

• Gap up threshold (%) — 1 (ギャップ条件)

• EPS surprise threshold (%) — 5 (EPS サプライズ最小値)

• Past price performance — 20 (パフォーマンス判定日数)

• Fixed stop-loss (%) — 8 (固定ストップ幅)

• Daily EMA length — 30 (利確用 EMA 期間)

注意 — Pine の仕様上、バックテストでは寄付き 5 分足の次バーで約定します。

実運用で寄付き成行に合わせたい場合は calc_on_every_tick=true を有効にしてください。

────

ご意見や質問があればお気軽にコメントください。

Happy trading!

DEMA Trend Oscillator Strategy📌 Overview

The DEMA Trend Oscillator Strategy is a dynamic trend-following approach based on the Normalized DEMA Oscillator SD.

It adapts in real-time to market volatility with the goal of improving entry accuracy and optimizing risk management.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main goal of this strategy is to respond quickly to sudden price movements and trend reversals,

by combining momentum-based signals with volatility filters.

It is designed to be user-friendly for traders of all experience levels.

✨ Key Features

Normalized DEMA Oscillator: A momentum indicator that normalizes DEMA values on a 0–100 scale, allowing intuitive identification of trend strength

Two-Bar Confirmation Filter: Requires two consecutive bullish or bearish candles to reduce noise and enhance entry reliability

ATR x2 Trailing Stop: In addition to fixed stop-loss levels, a trailing stop based on 2× ATR is used to maximize profits during strong trends

📊 Trading Rules

Long Entry:

Normalized DEMA > 55 (strong upward momentum)

Candle low is above the upper SD band

Two consecutive bullish candles appear

Short Entry:

Normalized DEMA < 45 (downward momentum)

Candle high is below the lower SD band

Two consecutive bearish candles appear

Exit Conditions:

Take-profit at a risk-reward ratio of 1.5

Stop-loss triggered if price breaks below (long) or above (short) the SD band

Trailing stop activated based on 2× ATR to secure and extend profits

💰 Risk Management Parameters

Symbol & Timeframe: Any (AUDUSD 5M example)

Account size (virtual): $3000

Commission: 0.4PIPS(0.0004)

Slippage: 2 pips

Risk per trade: 5%

Number of trades (backtest):534

All parameters can be adjusted based on broker specifications and individual trading profiles.

⚙️ Trading Parameters & Considerations

Indicator: Normalized DEMA Oscillator SD

Parameter settings:

DEMA Period (len_dema): 40

Base Length: 20

Long Threshold: 55

Short Threshold: 45

Risk-Reward Ratio: 1.5

ATR Multiplier for Trailing Stop: 2.0

🖼 Visual Support

The chart displays the following visual elements:

Upper and lower SD bands (±2 standard deviations)

Entry signals shown as directional arrows

🔧 Strategy Improvements & Uniqueness

This strategy is inspired by “Normalized DEMA Oscillator SD” by QuantEdgeB,

but introduces enhancements such as a two-bar confirmation filter and an ATR-based trailing stop.

Compared to conventional trend-following strategies, it offers superior noise filtering and profit optimization.

✅ Summary

The DEMA Trend Oscillator Strategy is a responsive and practical trend-following method

that combines momentum detection with adaptive risk management.

Its visual clarity and logical structure make it a powerful and repeatable tool

for traders seeking consistent performance in trending markets.

⚠️ Always apply appropriate risk management. This strategy is based on historical data and does not guarantee future results.

BB Breakout + Momentum Squeeze [Strategy]This Strategy is Based on 3 free indicators

- Bollinger Bands Breakout Oscillator: Link

- TTM Squeeze Pro: Link

- Rolling ATR Bands: Link

Bollinger Bands Breakout Oscillator - This tool shows how strong a market trend is by measuring how often prices move outside their normal Bollinger bands range. It helps you see whether prices are strongly moving in one direction or just moving sideways. By looking at how much and how frequently prices push beyond their typical boundaries, you can identify which direction the market is heading over your selected time period.

TM Squeeze Pro - This is a custom version of the TTM Squeeze indicator.

It's designed to help traders spot consolidation phases in the market (when price is coiling or "squeezing") and to catch breakouts early when volatility returns. The logic is based on the relationship between Bollinger Bands and Keltner Channels, combined with a momentum oscillator to show direction and strength.

Rolling ATR Bands - This indicator combines volatility bands (ATR) with momentum and trend signals to show where the market might be breaking out, retesting, or trending. It's highly visual and helpful for traders looking to time entries/exits during trending or volatile moves.

Logic Of the Strategy:

We are going to use the Bollinger Bands Breakout to determine the direction of the market. Than check the Volatility of the price by looking at the TTM Squeeze indicator. And use the ATR Bands to determine dynamic Stop Losses and based on the calculate the Take Profit targets and quantity for each position dynamically.

For the Long Setup:

1. We need to see the that Bull Power (Green line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

For the Short Setup:

1. We need to see the that Bear Power (Red line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

Stop Loss is determined by the Lower ATR Band (for the Long entry) and Upper ATR Band (For the Short entry)

Take Profit is 1:1.5 risk reward ration, which means if the Stop loss is 1% the TP target will be 1.5%

Move stop Loss to Breakeven: If the price will go in the direction of the trade for at least half of the Risk Reward target then the stop will automatically be adjusted to the entry price. For Example: the Stop Loss is 1%, the price has move at least 0.5% in the direction of your trade and that will move the Stop Loss level to the Entry point.

You can Adjust the parameters for each indicator used in that script and also adjust the Risk and Money management block to see how the PnL will change.

MACD Volume Strategy (BBO + MACD State, Reversal Type)Overview

MACD Volume Strategy (BBO + MACD State, Reversal Type) is a momentum-based reversal system that combines MACD crossover logic with volume filtering to enhance signal accuracy and minimize noise. It aims to identify structural trend shifts and manage risk using predefined parameters.

※This strategy is for educational and research purposes only. All results are based on historical simulations and do not guarantee future performance.

Strategy Objectives

Identify early trend transitions with high probability

Filter entries using volume dynamics to validate momentum

Maintain continuous exposure using a reversal-style model

Apply a consistent 1:1.5 risk-to-reward ratio per trade

Key Features

Integrated MACD and volume oscillator filtering

Zero repainting (all signals confirmed on closed candles)

Automatic position flipping for seamless direction shifts

Stop-loss and take-profit based on recent structural highs/lows

Trading Rules

Long Entry Conditions

MACD crosses above the zero line (BBO Buy arrow)

Volume oscillator is positive (short EMA > long EMA)

MACD is above the signal line

Close any existing short and enter a new long

Short Entry Conditions

MACD crosses below the zero line (BBO Sell arrow)

Volume oscillator is positive

MACD is below the signal line

Close any existing long and enter a new short

Exit Rules

Take Profit (TP) = Entry ± (risk distance × 1.5)

Stop Loss (SL) = Recent swing low (for long) or high (for short)

Early Exit = Triggered when a reversal signal appears (flip logic)

Risk Management Parameters

Pair: ETH/USD

Timeframe: 10-minute

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted for sustainable practice)

Total Trades: 312 (backtest on selected dataset)

※Risk parameters are fully configurable and should be adjusted to suit each trader's personal setup and broker conditions.

Parameters & Configurations

Volume Short Length: 6

Volume Long Length: 12

MACD Fast Length: 11

MACD Slow Length: 21

Signal Smoothing: 10

Oscillator MA Type: SMA

Signal Line MA Type: SMA

Visual Support

Green arrow = Long entry

Red arrow = Short entry

MACD lines, signal line, and histogram

SL/TP markers plotted directly on the chart

Strategic Advantages & Uniqueness

Volume filtering eliminates low-participation, weak signals

Structurally aligned SL/TP based on recent market pivots

No repainting — decisions are made only on closed candles

Always in the market due to the reversal-style framework

Inspirations & Attribution

This strategy is inspired by the excellent work of:

Bitcoinblockchainonline – “BBO_Roxana_Signals MACD + vol”

Leveraging MACD zero-line cross and volume oscillator for intuitive signal generation.

HasanRifat – “MACD Fake Filter ”

Introduced a signal filter using MACD wave height averaging to reduce false positives.

This strategy builds upon those ideas to create a more automated, risk-aware, and technically adaptive system.

Summary

MACD Volume Strategy is a clean, logic-first automated trading system built for precision-seeking traders. It avoids discretionary bias and provides consistent signal logic under backtested historical conditions.

100% mechanical — no discretionary input required

Designed for high-confidence entries

Can be extended with filters, alerts, or trailing stops

※Strategy performance depends on market context. Past performance is not indicative of future results. Use with proper risk management and careful configuration.

Premarket Gap MomoTrader(SC)🚀 Pre-Market Momentum Trader | Dynamic Position Sizing 🔥

📈 Trade explosive pre-market breakouts with confidence! This algorithmic strategy automatically detects high-momentum setups, dynamically adjusts position size, and ensures risk control with a one-trade-per-day rule.

⸻

🎯 Key Features

✅ Pre-Market Trading (4:00 - 9:30 AM EST) – Only trades during the most volatile session for early breakouts.

✅ Dynamic Position Sizing – Adapts trade size based on candle strength:

• ≥90% body → 100% position

• ≥85% body → 50% position

• ≥75% body → 25% position

✅ 1 Trade Per Day – Avoids overtrading by allowing only one high-quality trade daily.

✅ Momentum Protection – Stays in the trade as long as:

• Every candle remains green (no red candles).

• Each new candle has increasing volume (confirming strong buying).

✅ Automated Exit – Closes position if:

• A red candle appears.

• Volume fails to increase on a green candle.

⸻

🔍 How It Works

📌 Entry Conditions:

✔️ Candle gains ≥5% from previous close.

✔️ Candle is green & body size ≥75% of total range.

✔️ Volume >15K (confirming liquidity).

✔️ Occurs within pre-market session (4:00 - 9:30 AM EST).

✔️ Only the first valid trade of the day is taken.

📌 Exit Conditions:

❌ First red candle after entry → Exit trade.

❌ First green candle with lower volume → Exit trade.

⸻

🏆 Why Use This?

🔹 Eliminates Fake Breakouts – No trade unless volume & momentum confirm.

🔹 Prevents Overtrading – Restricts to one quality trade per day.

🔹 Adaptable to Any Market – Works on stocks, crypto, or forex.

🔹 Hands-Free Execution – No manual chart watching required!

⸻

🚨 Important Notes

📢 Not financial advice. Trading involves risk—always backtest & practice on paper trading before using real money.

📢 Enable pre-market data in your TradingView settings for accurate results.

📢 Optimized for 1-minute & 5-minute timeframes.

🔔 Like this strategy? Leave a comment, share your results, and don’t forget to hit Follow for more strategies! 🚀🔥

Kernel Regression Envelope with SMI OscillatorThis script combines the predictive capabilities of the **Nadaraya-Watson estimator**, implemented by the esteemed jdehorty (credit to him for his excellent work on the `KernelFunctions` library and the original Nadaraya-Watson Envelope indicator), with the confirmation strength of the **Stochastic Momentum Index (SMI)** to create a dynamic trend reversal strategy. The core idea is to identify potential overbought and oversold conditions using the Nadaraya-Watson Envelope and then confirm these signals with the SMI before entering a trade.

**Understanding the Nadaraya-Watson Envelope:**

The Nadaraya-Watson estimator is a non-parametric regression technique that essentially calculates a weighted average of past price data to estimate the current underlying trend. Unlike simple moving averages that give equal weight to all past data within a defined period, the Nadaraya-Watson estimator uses a **kernel function** (in this case, the Rational Quadratic Kernel) to assign weights. The key parameters influencing this estimation are:

* **Lookback Window (h):** This determines how many historical bars are considered for the estimation. A larger window results in a smoother estimation, while a smaller window makes it more reactive to recent price changes.

* **Relative Weighting (alpha):** This parameter controls the influence of different time frames in the estimation. Lower values emphasize longer-term price action, while higher values make the estimator more sensitive to shorter-term movements.

* **Start Regression at Bar (x\_0):** This allows you to exclude the potentially volatile initial bars of a chart from the calculation, leading to a more stable estimation.

The script calculates the Nadaraya-Watson estimation for the closing price (`yhat_close`), as well as the highs (`yhat_high`) and lows (`yhat_low`). The `yhat_close` is then used as the central trend line.

**Dynamic Envelope Bands with ATR:**

To identify potential entry and exit points around the Nadaraya-Watson estimation, the script uses **Average True Range (ATR)** to create dynamic envelope bands. ATR measures the volatility of the price. By multiplying the ATR by different factors (`nearFactor` and `farFactor`), we create multiple bands:

* **Near Bands:** These are closer to the Nadaraya-Watson estimation and are intended to identify potential immediate overbought or oversold zones.

* **Far Bands:** These are further away and can act as potential take-profit or stop-loss levels, representing more extreme price extensions.

The script calculates both near and far upper and lower bands, as well as an average between the near and far bands. This provides a nuanced view of potential support and resistance levels around the estimated trend.

**Confirming Reversals with the Stochastic Momentum Index (SMI):**

While the Nadaraya-Watson Envelope identifies potential overextended conditions, the **Stochastic Momentum Index (SMI)** is used to confirm a potential trend reversal. The SMI, unlike a traditional stochastic oscillator, oscillates around a zero line. It measures the location of the current closing price relative to the median of the high/low range over a specified period.

The script calculates the SMI on a **higher timeframe** (defined by the "Timeframe" input) to gain a broader perspective on the market momentum. This helps to filter out potential whipsaws and false signals that might occur on the current chart's timeframe. The SMI calculation involves:

* **%K Length:** The lookback period for calculating the highest high and lowest low.

* **%D Length:** The period for smoothing the relative range.

* **EMA Length:** The period for smoothing the SMI itself.

The script uses a double EMA for smoothing within the SMI calculation for added smoothness.

**How the Indicators Work Together in the Strategy:**

The strategy enters a long position when:

1. The closing price crosses below the **near lower band** of the Nadaraya-Watson Envelope, suggesting a potential oversold condition.

2. The SMI crosses above its EMA, indicating positive momentum.

3. The SMI value is below -50, further supporting the oversold idea on the higher timeframe.

Conversely, the strategy enters a short position when:

1. The closing price crosses above the **near upper band** of the Nadaraya-Watson Envelope, suggesting a potential overbought condition.

2. The SMI crosses below its EMA, indicating negative momentum.

3. The SMI value is above 50, further supporting the overbought idea on the higher timeframe.

Trades are closed when the price crosses the **far band** in the opposite direction of the trade. A stop-loss is also implemented based on a fixed value.

**In essence:** The Nadaraya-Watson Envelope identifies areas where the price might be deviating significantly from its estimated trend. The SMI, calculated on a higher timeframe, then acts as a confirmation signal, suggesting that the momentum is shifting in the direction of a potential reversal. The ATR-based bands provide dynamic entry and exit points based on the current volatility.

**How to Use the Script:**

1. **Apply the script to your chart.**

2. **Adjust the "Kernel Settings":**

* **Lookback Window (h):** Experiment with different values to find the smoothness that best suits the asset and timeframe you are trading. Lower values make the envelope more reactive, while higher values make it smoother.

* **Relative Weighting (alpha):** Adjust to control the influence of different timeframes on the Nadaraya-Watson estimation.

* **Start Regression at Bar (x\_0):** Increase this value if you want to exclude the initial, potentially volatile, bars from the calculation.

* **Stoploss:** Set your desired stop-loss value.

3. **Adjust the "SMI" settings:**

* **%K Length, %D Length, EMA Length:** These parameters control the sensitivity and smoothness of the SMI. Experiment to find settings that work well for your trading style.

* **Timeframe:** Select the higher timeframe you want to use for SMI confirmation.

4. **Adjust the "ATR Length" and "Near/Far ATR Factor":** These settings control the width and sensitivity of the envelope bands. Smaller ATR lengths make the bands more reactive to recent volatility.

5. **Customize the "Color Settings"** to your preference.

6. **Observe the plots:**

* The **Nadaraya-Watson Estimation (yhat)** line represents the estimated underlying trend.

* The **near and far upper and lower bands** visualize potential overbought and oversold zones based on the ATR.

* The **fill areas** highlight the regions between the near and far bands.

7. **Look for entry signals:** A long entry is considered when the price touches or crosses below the lower near band and the SMI confirms upward momentum. A short entry is considered when the price touches or crosses above the upper near band and the SMI confirms downward momentum.

8. **Manage your trades:** The script provides exit signals when the price crosses the far band. The fixed stop-loss will also close trades if the price moves against your position.

**Justification for Combining Nadaraya-Watson Envelope and SMI:**

The combination of the Nadaraya-Watson Envelope and the SMI provides a more robust approach to identifying potential trend reversals compared to using either indicator in isolation. The Nadaraya-Watson Envelope excels at identifying potential areas where the price is overextended relative to its recent history. However, relying solely on the envelope can lead to false signals, especially in choppy or volatile markets. By incorporating the SMI as a confirmation tool, we add a momentum filter that helps to validate the potential reversals signaled by the envelope. The higher timeframe SMI further helps to filter out noise and focus on more significant shifts in momentum. The ATR-based bands add a dynamic element to the entry and exit points, adapting to the current market volatility. This mashup aims to leverage the strengths of each indicator to create a more reliable trading strategy.

Tomas Ratio Strategy with Multi-Timeframe AnalysisHello,

I would like to present my new indicator I have compiled together inspired by Calmar Ratio which is a ratio that measures gains vs losers but with a little twist.

Basically the idea is that if HLC3 is above HLC3 (or previous one) it will count as a gain and it will calculate the percentage of winners in last 720 hourly bars and then apply 168 hour standard deviation to the weekly average daily gains.

The idea is that you're supposed to buy if the thick blue line goes up and not buy if it goes down (signalized by the signal line). I liked that idea a lot, but I wanted to add an option to fire open and close signals. I have also added a logic that it not open more trades in relation the purple line which shows confidence in buying.

As input I recommend only adjusting the amount of points required to fire a signal. Note that the lower amount you put, the more open trades it will allow (and vice versa)

Feel free to remove that limiter if you want to. It works without it as well, this script is meant for inexperienced eye.

I will also publish a indicator script with this limiter removed and alerts added for you to test this strategy if you so choose to.

Also, I have added that the trades will enter only if price is above 720 period EMA

Disclaimer

This strategy is for educational purposes only and should not be considered financial advice. Always backtest thoroughly and adjust parameters based on your trading style and market conditions.

Made in collaboration with ChatGPT.

SuperATR 7-Step Profit - Strategy [presentTrading] Long time no see!

█ Introduction and How It Is Different

The SuperATR 7-Step Profit Strategy is a multi-layered trading approach that integrates adaptive Average True Range (ATR) calculations with momentum-based trend detection. What sets this strategy apart is its sophisticated 7-step take-profit mechanism, which combines four ATR-based exit levels and three fixed percentage levels. This hybrid approach allows traders to dynamically adjust to market volatility while systematically capturing profits in both long and short market positions.

Traditional trading strategies often rely on static indicators or single-layered exit strategies, which may not adapt well to changing market conditions. The SuperATR 7-Step Profit Strategy addresses this limitation by:

- Using Adaptive ATR: Enhances the standard ATR by making it responsive to current market momentum.

- Incorporating Momentum-Based Trend Detection: Identifies stronger trends with higher probability of continuation.

- Employing a Multi-Step Take-Profit System: Allows for gradual profit-taking at predetermined levels, optimizing returns while minimizing risk.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy revolves around detecting strong market trends and capitalizing on them using an adaptive ATR and momentum indicators. Below is a detailed breakdown of each component of the strategy.

🔶 1. True Range Calculation with Enhanced Volatility Detection

The True Range (TR) measures market volatility by considering the most significant price movements. The enhanced TR is calculated as:

TR = Max

Where:

High and Low are the current bar's high and low prices.

Previous Close is the closing price of the previous bar.

Abs denotes the absolute value.

Max selects the maximum value among the three calculations.

🔶 2. Momentum Factor Calculation

To make the ATR adaptive, the strategy incorporates a Momentum Factor (MF), which adjusts the ATR based on recent price movements.

Momentum = Close - Close

Stdev_Close = Standard Deviation of Close over n periods

Normalized_Momentum = Momentum / Stdev_Close (if Stdev_Close ≠ 0)

Momentum_Factor = Abs(Normalized_Momentum)

Where:

Close is the current closing price.

n is the momentum_period, a user-defined input (default is 7).

Standard Deviation measures the dispersion of closing prices over n periods.

Abs ensures the momentum factor is always positive.

🔶 3. Adaptive ATR Calculation

The Adaptive ATR (AATR) adjusts the traditional ATR based on the Momentum Factor, making it more responsive during volatile periods and smoother during consolidation.

Short_ATR = SMA(True Range, short_period)

Long_ATR = SMA(True Range, long_period)

Adaptive_ATR = /

Where:

SMA is the Simple Moving Average.

short_period and long_period are user-defined inputs (defaults are 3 and 7, respectively).

🔶 4. Trend Strength Calculation

The strategy quantifies the strength of the trend to filter out weak signals.

Price_Change = Close - Close

ATR_Multiple = Price_Change / Adaptive_ATR (if Adaptive_ATR ≠ 0)

Trend_Strength = SMA(ATR_Multiple, n)

🔶 5. Trend Signal Determination

If (Short_MA > Long_MA) AND (Trend_Strength > Trend_Strength_Threshold):

Trend_Signal = 1 (Strong Uptrend)

Elif (Short_MA < Long_MA) AND (Trend_Strength < -Trend_Strength_Threshold):

Trend_Signal = -1 (Strong Downtrend)

Else:

Trend_Signal = 0 (No Clear Trend)

🔶 6. Trend Confirmation with Price Action

Adaptive_ATR_SMA = SMA(Adaptive_ATR, atr_sma_period)

If (Trend_Signal == 1) AND (Close > Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Elif (Trend_Signal == -1) AND (Close < Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Else:

Trend_Confirmed = False

Local Performance

🔶 7. Multi-Step Take-Profit Mechanism

The strategy employs a 7-step take-profit system

█ Trade Direction

The SuperATR 7-Step Profit Strategy is designed to work in both long and short market conditions. By identifying strong uptrends and downtrends, it allows traders to capitalize on price movements in either direction.

Long Trades: Initiated when the market shows strong upward momentum and the trend is confirmed.

Short Trades: Initiated when the market exhibits strong downward momentum and the trend is confirmed.

█ Usage

To implement the SuperATR 7-Step Profit Strategy:

1. Configure the Strategy Parameters:

- Adjust the short_period, long_period, and momentum_period to match the desired sensitivity.

- Set the trend_strength_threshold to control how strong a trend must be before acting.

2. Set Up the Multi-Step Take-Profit Levels:

- Define ATR multipliers and fixed percentage levels according to risk tolerance and profit goals.

- Specify the percentage of the position to close at each level.

3. Apply the Strategy to a Chart:

- Use the strategy on instruments and timeframes where it has been tested and optimized.

- Monitor the positions and adjust parameters as needed based on performance.

4. Backtest and Optimize:

- Utilize TradingView's backtesting features to evaluate historical performance.

- Adjust the default settings to optimize for different market conditions.

█ Default Settings

Understanding default settings is crucial for optimal performance.

Short Period (3): Affects the responsiveness of the short-term MA.

Effect: Lower values increase sensitivity but may produce more false signals.

Long Period (7): Determines the trend baseline.

Effect: Higher values reduce noise but may delay signals.

Momentum Period (7): Influences adaptive ATR and trend strength.

Effect: Shorter periods react quicker to price changes.

Trend Strength Threshold (0.5): Filters out weaker trends.

Effect: Higher thresholds yield fewer but stronger signals.

ATR Multipliers: Set distances for ATR-based exits.

Effect: Larger multipliers aim for bigger moves but may reduce hit rate.

Fixed TP Levels (%): Control profit-taking on smaller moves.

Effect: Adjusting these levels affects how quickly profits are realized.

Exit Percentages: Determine how much of the position is closed at each TP level.

Effect: Higher percentages reduce exposure faster, affecting risk and reward.

Adjusting these variables allows you to tailor the strategy to different market conditions and personal risk preferences.

By integrating adaptive indicators and a multi-tiered exit strategy, the SuperATR 7-Step Profit Strategy offers a versatile tool for traders seeking to navigate varying market conditions effectively. Understanding and adjusting the key parameters enables traders to harness the full potential of this strategy.

Trend Signals with TP & SL [UAlgo] StrategyThe "Trend Signals with TP & SL Strategy" is a trading strategy designed to capture trend continuation signals while incorporating sophisticated risk management techniques. This strategy is tailored for traders who wish to capitalize on trending market conditions with precise entry and exit points, automatically calculating Take Profit (TP) and Stop Loss (SL) levels based on either Average True Range (ATR) or percentage values. The strategy aims to enhance trade management by preventing multiple simultaneous positions and dynamically adapting to changing market conditions.

This strategy is highly configurable, allowing traders to adjust sensitivity, the ATR calculation method, and the cloud moving average length. Additionally, the strategy can display buy and sell signals directly on the chart, along with visual representation of entry points, stop losses, and take profits. It also features a cloud-based trend analysis using a MACD-driven color fill that indicates the strength and direction of the trend.

🔶 Key Features

Configurable Trend Continuation Signals:

Source Selection: The strategy uses the midpoint of the high-low range as the default source, but it is adjustable.

Sensitivity: The sensitivity of the trend signals can be adjusted using a multiplier, ranging from 0.5 to 5.

ATR Calculation: The strategy allows users to choose between two ATR calculation methods for better adaptability to different market conditions.

Cloud Moving Average: Traders can adjust the cloud moving average length, which is used in conjunction with MACD to provide a visual trend indication.

Take Profit & Stop Loss Management:

ATR-Based or Percent-Based: The strategy offers flexibility in setting TP and SL levels, allowing traders to choose between ATR-based multipliers or fixed percentage values.

Dynamic Adjustment: TP and SL levels are dynamically adjusted according to the selected method, ensuring trades are managed based on real-time market conditions.

Prevention of Multiple Positions:

Single Position Control: To reduce risk and enhance strategy reliability, the strategy includes an option to prevent multiple positions from being opened simultaneously.

Visual Trade Indicators:

Buy/Sell Signals: Clearly displays buy and sell signals on the chart for easy interpretation.

Entry, SL, and TP Lines: Draws lines for entry price, stop loss, and take profit directly on the chart, helping traders to monitor trades visually.

Trend Cloud: A color-filled cloud based on MACD and the cloud moving average provides a visual cue of the trend’s direction and strength.

Performance Summary Table:

In-Chart Statistics: A table in the top right of the chart displays key performance metrics, including total trades, wins, losses, and win rate percentage, offering a quick overview of the strategy’s effectiveness.

🔶 Interpreting the Indicator

Trend Signals: The strategy identifies trend continuation signals based on price action relative to an ATR-based threshold. A buy signal is generated when the price crosses above a key level, indicating an uptrend. Conversely, a sell signal occurs when the price crosses below a level, signaling a downtrend.

Cloud Visualization: The cloud, derived from MACD and moving averages, changes color to reflect the current trend. A positive cloud in aqua suggests an uptrend, while a red cloud indicates a downtrend. The transparency of the cloud offers further nuance, with more solid colors denoting stronger trends.

Entry and Exit Management: Once a trend signal is generated, the strategy automatically sets TP and SL levels based on your chosen method (ATR or percentage). The stop loss and take profit lines will appear on the chart, showing where the strategy will exit the trade. If the price reaches either the SL or TP, the trade is closed, and the respective line is deleted from the chart.

Performance Metrics: The strategy’s performance is tracked in real-time with an in-chart table. This table provides essential information about the number of trades executed, the win/loss ratio, and the overall win rate. This information helps traders assess the strategy's effectiveness and make necessary adjustments.

This strategy is designed for those who seek to engage with trending markets, offering robust tools for entry, exit, and overall trade management. By understanding and leveraging these features, traders can potentially improve their trading outcomes and risk management.

🔷 Related Script

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Bitcoin Momentum StrategyThis is a very simple long-only strategy I've used since December 2022 to manage my Bitcoin position.

I'm sharing it as an open-source script for other traders to learn from the code and adapt it to their liking if they find the system concept interesting.

General Overview

Always do your own research and backtesting - this script is not intended to be traded blindly (no script should be) and I've done limited testing on other markets beyond Ethereum and BTC, it's just a template to tweak and play with and make into one's own.

The results shown in the strategy tester are from Bitcoin's inception so as to get a large sample size of trades, and potential returns have diminished significantly as BTC has grown to become a mega cap asset, but the script includes a date filter for backtesting and it has still performed solidly in recent years (speaking from personal experience using it myself - DYOR with the date filter).

The main advantage of this system in my opinion is in limiting the max drawdown significantly versus buy & hodl. Theoretically much better returns can be made by just holding, but that's also a good way to lose 70%+ of your capital in the inevitable bear markets (also speaking from experience).

In saying all of that, the future is fundamentally unknowable and past results in no way guarantee future performance.

System Concept:

Capture as much Bitcoin upside volatility as possible while side-stepping downside volatility as quickly as possible.

The system uses a simple but clever momentum-style trailing stop technique I learned from one of my trading mentors who uses this approach on momentum/trend-following stock market systems.

Basically, the system "ratchets" up the stop-loss to be much tighter during high bearish volatility to protect open profits from downside moves, but loosens the stop loss during sustained bullish momentum to let the position ride.

It is invested most of the time, unless BTC is trading below its 20-week EMA in which case it stays in cash/USDT to avoid holding through bear markets. It only trades one position (no pyramiding) and does not trade short, but can easily be tweaked to do whatever you like if you know what you're doing in Pine.

Default parameters:

HTF: Weekly Chart

EMA: 20-Period

ATR: 5-period

Bar Lookback: 7

Entry Rule #1:

Bitcoin's current price must be trading above its higher-timeframe EMA (Weekly 20 EMA).

Entry Rule #2:

Bitcoin must not be in 'caution' condition (no large bearish volatility swings recently).

Enter at next bar's open if conditions are met and we are not already involved in a trade.

"Caution" Condition:

Defined as true if BTC's recent 7-bar swing high minus current bar's low is > 1.5x ATR, or Daily close < Daily 20-EMA.

Trailing Stop:

Stop is trailed 1 ATR from recent swing high, or 20% of ATR if in caution condition (ie. 0.2 ATR).

Exit on next bar open upon a close below stop loss.

I typically use a limit order to open & exit trades as close to the open price as possible to reduce slippage, but the strategy script uses market orders.

I've never had any issues getting filled on limit orders close to the market price with BTC on the Daily timeframe, but if the exchange has relatively low slippage I've found market orders work fine too without much impact on the results particularly since BTC has consistently remained above $20k and highly liquid.

Cost of Trading:

The script uses no leverage and a default total round-trip commission of 0.3% which is what I pay on my exchange based on their tier structure, but this can vary widely from exchange to exchange and higher commission fees will have a significantly negative impact on realized gains so make sure to always input the correct theoretical commission cost when backtesting any script.

Static slippage is difficult to estimate in the strategy tester given the wide range of prices & liquidity BTC has experienced over the years and it largely depends on position size, I set it to 150 points per buy or sell as BTC is currently very liquid on the exchange I trade and I use limit orders where possible to enter/exit positions as close as possible to the market's open price as it significantly limits my slippage.

But again, this can vary a lot from exchange to exchange (for better or worse) and if BTC volatility is high at the time of execution this can have a negative impact on slippage and therefore real performance, so make sure to adjust it according to your exchange's tendencies.

Tax considerations should also be made based on short-term trade frequency if crypto profits are treated as a CGT event in your region.

Summary:

A simple, but effective and fairly robust system that achieves the goals I set for it.

From my preliminary testing it appears it may also work on altcoins but it might need a bit of tweaking/loosening with the trailing stop distance as the default parameters are designed to work with Bitcoin which obviously behaves very differently to smaller cap assets.

Good luck out there!

The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)

Are you tired of manually analyzing charts and trying to find profitable trading opportunities? Look no further! Our algorithmic trading strategy, "Flash," is here to simplify your trading process and maximize your profits.

Flash is an advanced trading algorithm that combines three powerful indicators to generate highly selective and accurate trading signals. The Momentum-RSI, Super-Trend Analysis and EMA-Strategy indicators are used to identify the strength and direction of the underlying trend.

The Momentum-RSI signals the strength of the trend and only generates trading signals in confirmed upward or downward trends. The Super-Trend Analysis confirms the trend direction and generates signals when the price breaks through the super-trend line. The EMA-Strategy is used as a qualifier for the generation of trading signals, where buy signals are generated when the EMA crosses relevant trend lines.

Flash is highly selective, as it only generates trading signals when all three indicators align. This ensures that only the highest probability trades are taken, resulting in maximum profits.

Our trading strategy also comes with two profit management options. Option 1 uses the so-called supertrend-indicator which uses the dynamic ATR as a key input, while option 2 applies pre-defined, fixed SL and TP levels.

The settings for each indicator can be customized, allowing you to adjust the length, limit value, factor, and source value to suit your preferences. You can also set the time period in which you want to run the backtest and how many dollar trades you want to open in each position for fully automated trading.

Choose your preferred trade direction and stop-loss/take-profit settings, and let Flash do the rest. Say goodbye to manual chart analysis and hello to consistent profits with Flash. Try it now!

General Comments

This Flash Strategy has been developed in cooperation between Baby_whale_to_moon and JS-TechTrading. Cudos to Baby_whale_to_moon for doing a great job in transforming sophisticated trading ideas into pine scripts.

Detailed Description

The “Flash” script considers the following indicators for the generation of trading signals:

1. Momentum-RSI

2. ‘Super-Trend’-Analysis

3. EMA-Strategy

1. Momentum-RSI

• This indicator signals the strength of the underlying upward- or downward-trend.

• The signal range of this indicator is from 0 to 100. Values > 60 indicate a confirmed upward- or downward-trend.

• The strategy will only generate trading signals in case the stock (or any other financial security) is in a confirmed upward- (long entry signals) or downward-trend (short entry signals).

• This indicator provides information with regards to the strength of the underlying trend and it does not give any insight with regard to the direction of the trend. Therefore, this strategy also considers other indicators which provide technical confirmation with regards to the direction of the underlying trend.

Graph 1 shows this concept:

• The Momentum-RSI indicator gives lower readings during consolidation phases and no trading signals are generated during these periods.

Example (graph 2):

2. Super-Trend Analysis

• The red line in the graph below represents the so-called super-trend-line. Trading signals are only generated in case the price action breaks through this super-trend-line indicating a new confirmed upward-trend (or downward-trend, respectively).

• If that happens, the super trend-line changes its color from red to green, giving confirmation that the trend changed from bearish to bullish and long-entries can be considered.

• The vice-versa approach can be considered for short entries.

Graph 3 explains this concept:

3. Exponential Moving Average / EMA-Strategy

The functionality of this EMA-element of the strategy has been programmed as follows:

• The exponential moving average and two other trend lines are being used as qualifiers for the generation of trading-signals.

• Buy-signals for long-entries are only considered in case the EMA (yellow line in the graph below) crosses the red line.

• Sell-signals for short-entries are only considered in case the EMA (yellow line in the graph below) crosses the green line.

An example is shown in graph 4 below:

We use this indicator to determine the new trend direction that may occur by using the data of the price's past movement.

4. Bringing it all together

This section describes in detail, how this strategy combines the Momentum-RSI, the super-trend analysis and the EMA-strategy.

The strategy only generates trading-signals in case all of the following conditions and qualifiers are being met:

1. Momentum-RSI is higher than the set value of this strategy. The standard and recommended value is 60 (graph 5):

2. The super-trend analysis needs to indicate a confirmed upward-trend (for long-entry signals) or a confirmed downward-trend (for short-entry signals), respectively.

3. The EMA-strategy needs to indicate that the stock or financial security is in a confirmed upward-trend (long-entries) or downward-trend (short-entries), respectively.

The strategy will only generate trading signals if all three qualifiers are being met. This makes this strategy highly selective and is the key secret for its success.

Example for Long-Entry (graph 6):

When these conditions are met, our Long position is opened.

Example for Short-Entry (graph 7):

Trade Management Options (graph 8)

Option 1

In this dynamic version, the so-called supertrend-indicator is being used for the trade exit management. This supertrend-indicator is a sophisticated and optimized methodology which uses the dynamic ATR as one of its key input parameters.

The following settings of the supertrend-indicator can be changed and optimized (graph 9):

The dynamic SL/TP-lines of the supertrend-indicator are shown in the charts. The ATR-length and the supertrend-factor result in a multiplier value which can be used to fine-tune and optimize this strategy based on the financial security, timeframe and overall market environment.

Option 2 (graph 10):

Option 2 applies pre-defined, fixed SL and TP levels which will appear as straight horizontal lines in the chart.

Settings options (graph 11):

The following settings can be changed for the three elements of this strategy:

1. (Length Mom-Rsi): Length of our Mom-RSI indicator.

2. Mom-RSI Limit Val: the higher this number, the more momentum of the underlying trend is required before the strategy will start creating trading signals.

3. The length and factor values of the super trend indicator can be adjusted:ATR Length SuperTrend and Factor Super Trend

4. You can set the source value used by the ema trend indicator to determine the ema line: Source Ema Ind

5. You can set the EMA length and the percentage value to follow the price: Length Ema Ind and Percent Ema Ind

6. The backtesting period can be adjusted: Start and End time of BackTest

7. Dollar cost per position: this is relevant for 100% fully automated trading.

8. Trade direction can be adjusted: LONG, SHORT or BOTH

9. As we explained above, we can determine our stop-loss and take-profit levels dynamically or statically. (Version 1 or Version 2 )

Display options on the charts graph 12):

1. Show horizontal lines for the Stop-Loss and Take-profit levels on the charts.

2. Display relevant Trend Lines, including color setting options for the supertrend functionality. In the example below, green lines indicate a confirmed uptrend, red lines indicate a confirmed downtrend.

Other comments

• This indicator has been optimized to be applied for 1 hour-charts. However, the underlying principles of this strategy are supply and demand in the financial markets and the strategy can be applied to all timeframes. Daytraders can use the 1min- or 5min charts, swing-traders can use the daily charts.

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The combination of the qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

8 Day Run - Momentum StrategyInspired by Linda Bradford Raschke.

Entry criteria:

This strategy is used to capture momentum effects on the daily periodicities. Once prices have had a run of 8 or more consecutive closes above or below the 5-period simple moving average the strategy is primed to trade.

It will then enter a short on the first close above the 5sma after a run of 8 or more closes below the 5sma (it will enter a long when the price closes below the 5sma after a run of 8 or more closes above the 5sma).

Exit criteria:

All trades are exited on the first close back above/ below the 5sma.

Open DriveOpen Drive is a market profile concept introduced by Jim Dalton. It occurs when the price moves directionally and persistently for the first 30 minutes from the cash market open.

It is necessary to use 30-minute bars as there needs to be enough time to measure an extreme move of the cash open. This means there will be fewer trades than other strategies using faster time periodicities.

The script finds open drives from these time points 0700/ 0800 and 1300/1430.

The entry signal also has a breakout threshold using the 5-bar high and 5-bar low to only take trades moving away from the prior 5-bar range. This weeds out most mid-range trades and small range expansion bars.

If the price has had a strong move from the open and has broken either below the prior 5-bar low or above the prior 5-bar high by an amount equal to the prior 5-bar range a trade is entered in the direction of the move.

The Exit criteria; exit after 3 bars which is 90mins when using a 30min periodicity.

Note, this script is shared to show that momentum generated on or around the cash open tends to persist. The entry and exits of this strategy are quite naive but there are plenty of ways to take more aggressive entries on faster time frames when an open drive occurs. The times chosen for this strategy will suit stock index futures mainly. The user can experiment with other futures products and their corresponding pit/ cash open hours.

Google "open drive market profile" for more information on open drives and market profile concepts.

Happy trading!

DRM StrategyOne of the ways I go when I develop strategies is by reducing the number of parameters and removing fixed parameters and levels.

In this strategy, I'm trying to create an RSI indicator with a dynamic length.

Length is computed based on the correlation between Price and its momentum.

You can set min and max values for the RSI, and if the correlation is close to 1, we'll be at a min RSI value. When it's -1, we'll be at the max level.

I got this idea from Sofien Kaabar's book.

The strategy is super simple, and there might be much room for improvement.

Performance on the deep backtesting is not excellent, so I think the strategy needs some filters for regimes, etc.

Thanks to @MUQWISHI for helping me code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

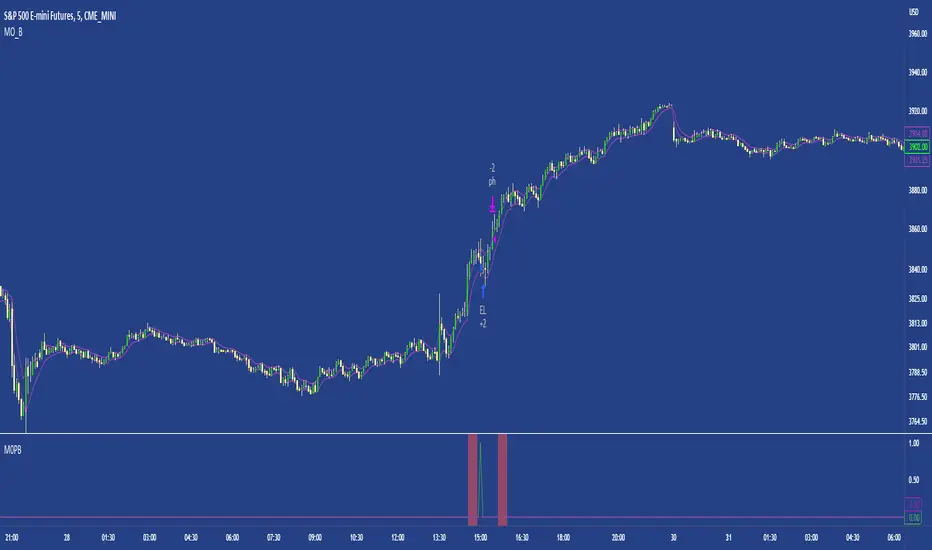

M0PB (Momentum Pullback)Long/short strategy that identifies extreme readings on the rsi as a *momentum signal*, unlike most RSI strategies the script will look to buy or sell the first pullback in the direction of the extreme RSI reading.

Enters positions on the first pullback to the 5ema(low)/ 5ema(high) and exits at rolling 12 bar high/ low. The rolling high/ low feature means that if the price enters into a prolonged consolidation the profit target will begin to reduce with each new bar. The best trades tend to work within 2-6 bars.

Built for use on 5 min intervals on FX, Indexes, and Crypto. Lower than 5 minute time frames tend to be noisier and mean more commissions and a higher risk of slippage so the suggested timeframe is 5 mins.

Hard stop is X ATR (users can experiment with this) from the position entry price. This can be adjusted in user inputs.

There is a lot of slack left in entries and exits but the overall strategy is fairly robust across timeframes and markets and has between 60%-70% win rate with larger winners.

Signals that occur from economic news volatility are best avoided.