ETF Builder & Backtest System [TradeDots]Create, analyze, and monitor your own custom “ETF-like” portfolio directly on TradingView. This script merges up to 10 different assets with user-defined weightings into a single composite chart, allowing you to see how your personalized portfolio would have performed historically. It is an original tool designed to help traders and investors quickly gauge risk and return profiles without leaving the TradingView platform.

📝 HOW IT WORKS

1. Custom Portfolio Construction

Multiple Assets : Combine up to 10 different stocks, ETFs, cryptocurrencies, or other symbols.

User-Defined Weights : Allocate each asset a percentage weight (e.g., 15% in AAPL, 10% in MSFT, etc.).

Single Composite Value : The script calculates a weighted “ETF-style” price, effectively simulating a merged portfolio curve on your chart.

2. Performance Tracking & Return Analysis

Automatic History Capture : The indicator records each asset’s starting price when it first appears in your chosen date range.

Rolling Updates : As time progresses, all asset prices are continually evaluated and the portfolio value is updated in real time.

Buy & Hold Returns : See how each asset—and the overall portfolio—performed from the “start” date to the most recent bar.

Annualized Return : Automatically calculates CAGR (Compound Annual Growth Rate) to help visualize performance over varying timescales.

3. Table & Visual Output

Performance Table : A comprehensive table displays individual asset returns, annualized returns, and portfolio totals.

Normalized Chart Plot : The composite ETF value is scaled to 100 at the start date, making it easy to compare relative growth or decline.

Optional Time Filter : You can define a specific date range (Start/End Dates) to focus on a particular period or to limit historical data.

⚙️ KEY FEATURES

1. Flexible Asset Selection

Choose any symbols from multiple asset classes. The script will only run calculations when data is available—no need to worry about missing quotes.

2. Dynamic Table Reporting

Start Price for each asset

Percentage Weight in the portfolio

Total Return (%) and Annualized Return (%)

3. Simple Backtesting Logic

This script takes a straightforward Buy & Hold perspective. Once the start date is reached, the portfolio remains static until the end date, so you can quickly assess hypothetical growth.

4. Plot Customization

Toggle the main “ETF” plot on/off.

Alter the visual style for tables and text.

Adjust the time filter to limit or extend your performance measurement window.

🚀 HOW TO USE IT

1. Add the Script

Search for “ETF Builder & Backtest System ” in the Indicators & Strategies tab or manually add it to your chart after saving it in your Pine Editor.

2. Configure Inputs

Enable Time Filter : Choose whether to restrict the analysis to a particular date range.

Start & End Date : Define the period you want to measure performance over (e.g., from 2019-12-31 to 2025-01-01).

Assets & Weights : Enter each symbol and specify a percentage weight (up to 10 assets).

Display Options : Pick where you want the Table to appear and choose background/text colors.

3. Interpret the Table & Plots

Asset Rows : Each asset’s ticker, weighting, start price, and performance metrics.

ETF Total Row : Summarizes total weighting, composite starting value, and overall returns.

Normalized Plot : Tracks growth/decline of the combined portfolio, starting at 100 on the chart.

4. Refine Your Strategy

Compare how different weights or a new mix of assets would have performed over the same period.

Assess if certain assets contribute disproportionately to your returns or volatility.

Use the results to guide allocations in your real trading or paper trading accounts.

❗️LIMITATIONS

1. Buy & Hold Only

This script does not handle rebalancing or partial divestments. Once the portfolio starts, weights remain fixed throughout the chosen timeframe.

2. No Reinvestment Tracking

Dividends or other distributions are not factored into performance.

3. Data Availability

If historical data for a particular asset is unavailable on TradingView, related results may display as “N/A.”

4. Market Regimes & Volatility

Past performance does not guarantee similar future behavior. Markets can change rapidly, which may render historical backtests less predictive over time.

⚠️ RISK DISCLAIMER

Trading and investing carry significant risk and can result in financial loss. The “ETF Builder & Backtest System ” is provided for informational and educational purposes only. It does not constitute financial advice.

Always conduct your own research.

Use proper risk management and position sizing.

Past performance does not guarantee future results.

This script is an original creation by TradeDots, published under the Mozilla Public License 2.0.

Use this indicator as part of a broader trading or investment approach—consider fundamental and technical factors, overall market context, and personal risk tolerance. No trading tool can assure profits; exercise caution and responsibility in all financial decisions.

Portfolio

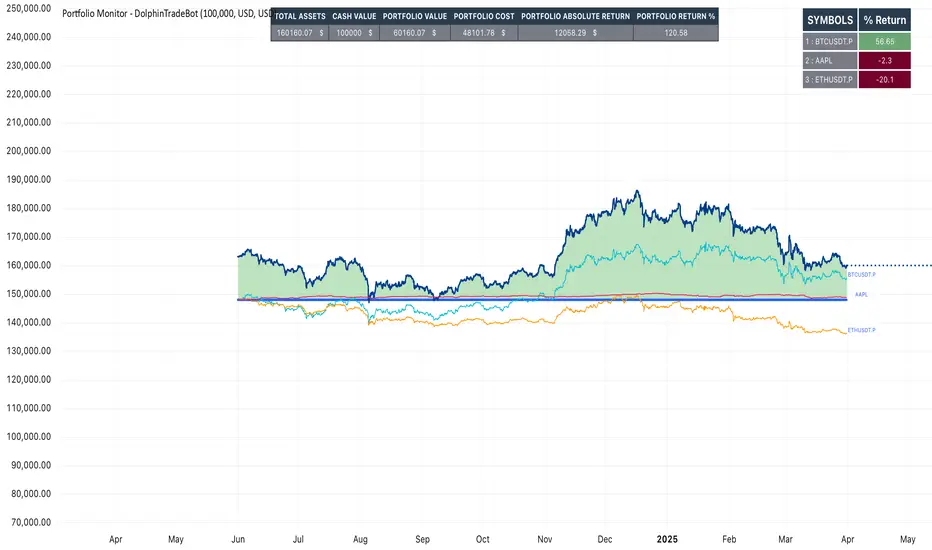

Portfolio Monitor - DolphinTradeBot1️⃣ Overview

▪️This indicator unifies the value of all your investments—whether stocks, currencies, or cryptocurrencies—in your chosen currency. This tool not only provides a clear snapshot of your overall portfolio performance but also highlights the individual growth of each asset with intuitive visualizations and an easy-to-understand performance report.

2️⃣ What sets this indicator apart

▪️is its ability to convert values from various currency pairs into any currency you choose. This means you can monitor your portfolio's performance against any currency pair you prefer, offering a flexible and comprehensive view of your investments.

3️⃣ How Is It Work ?

🔍The indicator can be analyzed under two main categories: visual representations and tables.

1- Visual representations ;

The indicator includes three different types of lines:

1. 1 - Reference Line → This represents the cost of all assets we hold, based on the selected date.

1. 2 - Total Assets Line → Displays the real-time value of all assets in our possession, including cash value, in the selected trading pair.

The area between the reference line is filled with green and red. The section above the reference line is represented in green, while the section below is shown in red.

1. 3 - Performance Lines → These visualize the performance of the assets, starting from the reference line and taking into account their weights in the portfolio. (Note: The lines are scaled for visualization purposes, so their absolute values should not be considered.)

"The names of the lines are shown in the image below."⤵️

2- Tables

The indicator includes three different types of tables:

2. 1 - Analysis Table : It provides a superficial overview of wallet statistics and values.

▪️TOTAL ASSETS → The current equivalent of all assets in the target currency

▪️CASH VALUE → The current value of the amount "Cash Value", in the target currency.

▪️PORTFOLIO VALUE → The total value of assets excluding Cash, in the target currency.

▪️POSTFOLIO COST → The cost of assets excluding Cash, in the target currency.

▪️PORTFOLIO ABSOLUTE RETURN → It shows the profit or loss relative to the cost of assets

▪️PORTFOLIO RETURN % →It shows the profit or loss relative to the cost of assets on a percentage basis

2. 2 - Performance Table : It displays the names of assets excluding Cash and their profit amounts, sorted from highest to lowest profit. If "Show as Percentage" is selected in the settings, it shows the percentage profit or loss relative to the cost. Profits are represented in green, while losses are represented in red.

"You can see the visual showing the tables below"⤵️

4️⃣How to Use ?

1- Choose the date on which the visualization will begin (📌The start date only affects the exchange rate used for calculating the reference line in the target currency.)

2- If you have cash holdings, enter the amount and specify the currency.

3- Select the currency in which your portfolio value will be displayed.(Default value is USD)

4- To set up your portfolio;

SYMBOLS - QUANTITY - PURCHASE PRICE

Enter the symbols of your assets - the number of units you hold - and their cost levels.

5- If you have cash, be sure to include your cash balance. If you also hold other currencies, enter them as separate assets with their corresponding quantities and purchase prices.

6- If you want to see the percentage returns of the assets in the performance table relative to their cost, select the "Show as Percent" option.

7- If you want to see the performance visuals of the assets, click on the "Show Asset Performance" option.

You can find an image of the settings section where the numbers above are used as references below.⤵️

📌 NOTE → By default, a few assets and their values have been pre-added in the initial settings. This is to ensure that you don’t see an empty screen when adding the indicator to the chart. Please remember to enter your own assets and values. The default settings are only provided as an example.

PnL MonitorThe PnL Monitor is a customizable tool designed to help traders track the Profit and Loss (PnL) of up to 20 currency pairs or assets in real-time. This script provides a clear and organized table that displays the entry price, and PnL percentage for each pair, making it an essential tool for monitoring open positions or tracking potential trades.

Key Features:

Multi-Asset Tracking:

Monitor up to 20 currency pairs or assets simultaneously. Simply input the pair symbol and your entry price, and the script will calculate the PnL in real-time.

Dynamic Table Positioning:

Choose where the table appears on your chart with the Table Position input. Options include:

Top Left

Top Right

Bottom Left

Bottom Right

Real-Time PnL Calculation:

The script fetches the current price of each pair and calculates the PnL percentage based on your entry price. Positive PnL is highlighted in green, while negative PnL is highlighted in red.

Exchange and Pair Separation:

The script automatically separates the exchange name (if provided) from the pair symbol, making it easier to identify the source of the data.

Customizable Inputs:

Add or remove pairs as needed.

Leave the price field blank for pairs you don’t want to track.

How to Use:

Input Your Pairs:

In the script settings, input the symbol of the pair (e.g., NASDAQ:AAPL or BTCUSD) and your entry price. Leave the price field blank for pairs you don’t want to track.

Choose Table Position:

Select where you want the table to appear on your chart.

Monitor PnL:

The table will automatically update with the current price and PnL percentage for each pair.

Why Use This Script?

Efficiency: Track multiple pairs in one place without switching charts.

Clarity: Easily identify profitable and losing positions at a glance.

Flexibility: Customize the table to fit your trading style and preferences.

Ideal For:

Forex, crypto, and stock traders managing multiple positions.

Asset Allocation CalculatorOverview

This script is a tool that automatically calculates asset allocation for your investment portfolio. Users can set the weight of multiple assets and monitor the portfolio value in real time based on price fluctuations.

Key Features

Supports input of asset allocation percentages

Dynamic allocation calculation based on real-time price data

Automatically calculates allocated amounts for each asset based on the total investment amount

User-friendly interface with intuitive visual feedback

Settings

Total Capital : Enter the total capital, including the value of assets.

Quantity rounding : Using the rounding function may cause the target allocation to exceed 100%.

Tickers, Weight, Holdings :

To retrieve accurate asset prices, specify both the exchange and the ticker.

If you want to include cash in your portfolio, use $.

Ensure that the total allocation sums to 100%.

Refer to the pre-filled example for the correct format.

Table Settings : You can adjust the table's position, height, font size, and background color.

How to Use

By buying or selling the quantity shown in the Buy column, you can continuously maintain your target allocation.

Hold - Current holdings

Buy - Quantity to buy or sell to reach the target allocation

Target - Quantity aimed for after buying or selling

Caution

It can only calculate for a single currency, so do not mix multiple currency markets.

자산 배분 계산기

소개

이 스크립트는 투자 포트폴리오의 자산 배분을 자동으로 계산해주는 도구입니다. 사용자는 여러 자산의 비중을 설정할 수 있으며, 가격 변동에 따라 포트폴리오 가치를 실시간으로 모니터링할 수 있습니다.

주요 기능

자산 배분 비율 입력 지원

실시간 가격 데이터를 기반으로 한 동적 배분 계산

총 투자 금액을 기준으로 각 자산에 할당된 금액 자동 계산

직관적인 시각적 피드백을 제공하는 사용자 친화적인 인터페이스

설정

Total Capital : 자산 가치를 포함한 총 자본금을 입력하세요.

Quantity rounding : 반올림 기능을 사용하면 목표 비중이 100%를 초과할 수 있습니다.

Tickers, Weight, Holdings :

정확한 자산 가격을 불러오기 위해 거래소와 티커를 함께 입력하세요.

포트폴리오에 현금을 포함하려면 '$'를 사용하세요.

비중 합계가 반드시 100%가 되도록 설정하세요.

예제 형식을 참고하여 올바르게 입력하세요.

한국(원화) 시장을 위한 입력 예시입니다.

KRX:360750, 17.5, 100

KRX:310960, 17.5, 120

KRX:148070, 25, 20

KRX:305080, 25, 10

KRX:139320, 10, 150

UPBIT:BTCKRW, 5, 0.002

$,0,5000000

Table Settings : 테이블의 위치, 높이, 글자 크기 및 배경색을 조정할 수 있습니다.

사용 방법

Buy 열에 표시된 수량만큼 매수 또는 매도하면 목표 비중을 지속적으로 유지할 수 있습니다.

Hold - 현재 보유 수량

Buy - 목표 비중을 맞추기 위해 매수 또는 매도해야 하는 수량

Target - 매수, 매도 후 목표로 하는 수량

주의

한 가지 통화로만 계산할 수 있으니 여러 통화 시장을 혼용하지 마세요.

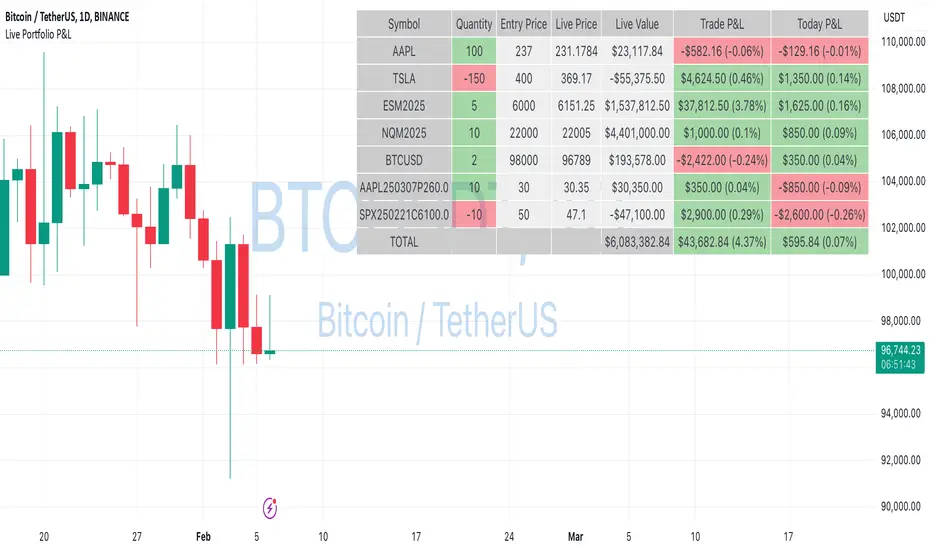

Live Portfolio P<his script calculates live P&L (Profit & Loss) for up to 40 instruments — stocks, ETFs, options, futures, and Forex pairs supported by TradingView. Instead of juggling numerous inputs, you paste your portfolio in CSV format into a single text field, and the script handles the rest. It parses each position and displays a comprehensive table showing the symbol, current price, position value, total P&L, and today’s P&L—all updated in real time.

Key Features

CSV Portfolio Input – Effortlessly import all your positions at once without filling in multiple fields. You can export the position from your broker, save it in the required format, and paste it into this script.

Supports Various Asset Classes – Works with any instrument that TradingView provides data for, including futures, options, and Forex.

Up to 40 Instruments – Track a broad and diverse set of holdings in one place.

Real-Time Updates – Get immediate feedback on live price changes, total value, and current P&L.

Today’s P&L – Monitor your daily performance to gauge short-term trends.

CSV is consumed in the following format:

Symbol (supported TradingView instruments)

Entry Price

Quantity (negative for short position)

Lot Size (for futures/options, it might not be one)

For example:

AAPL,237,100,1

TSLA,400,-150,1

ESM2025,6000,5,50

Planned Enhancements

Multi-Currency Support – Automatically convert and display your positions’ values in different currencies.

Advanced Metrics – Get deeper insights with calculations for drawdown, Sharpe ratio, and more.

Risk Management Tools – Set stop-loss and take-profit levels and receive alerts when thresholds are hit.

Option Greeks & Margin Calculations – Manage complex option strategies and track margin requirements.

Questions for You

What additional features would you like to see?

Are there any specific metrics or analytics you’d find especially valuable?

How might this script fit into your current trading workflow?

Feel free to share your thoughts and suggestions. Your feedback will help shape future updates and make this tool even more helpful for traders like you!

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

DCA Valuation & Unrealized GainsThis Pine Script for TradingView calculates and visualizes the relationship between a Dollar Cost Average (DCA) price and the All-Time High (ATH) price for over 50 different cryptocurrencies. Here's what it does:

1. Inputs for DCA Prices:

- Users can manually input DCA prices for specific cryptocurrencies (e.g., BTC, ETH, BNB).

2. Dynamic ATH Calculation:

- Dynamically calculates the ATH price for the current asset using the highest price in the chart's loaded data and persists this value across bars.

3. Percentage Change from DCA to ATH:

- Computes the percentage gain from the DCA price to the ATH price.

4. Visualizations:

- Draws a line at the DCA price and the ATH price, both extended to the right.

- Adds an arrow pointing from the DCA price to the ATH, offset by 10 bars into the future.

- Displays labels for:

- The percentage gain from DCA to ATH.

- "No DCA Configured" if no valid DCA price is set for the asset.

5. Color Coding:

- Labels and arrows are color-coded to indicate positive or negative percentage changes:

- Green for gains.

- Red for losses.

6. Adaptability:

- The script dynamically adjusts to the current asset based on its ticker and uses the corresponding DCA price.

This functionality provides traders with clear insights into their investment's performance relative to its ATH, aiding in decision-making.

-----

To add a new asset to the script:

1. Define the DCA Input: Add a new input for the asset's DCA price using the `input.float` function. For example:

dcaPriceNEW = input.float(title="NEW DCA Price", defval=0.1, tooltip="Set the DCA price for NEW")

2. Add the Asset Logic: Include a conditional check for the new asset in the ticker matching logic:

if str.contains(currentAsset, "NEW") and dcaPriceNEW != 0

dcaPrice := dcaPriceNEW

Where NEW is the ticker symbol of the asset you're adding.

NOTE: SOLO had to be put before SOL because otherwise the indicator was pulling the DCA price from SOL even on the SOLO chart. If you have a similar issue, try that fix.

Adding an asset requires only these two changes. Once done, the script dynamically incorporates the new asset into its calculations and visualizations.

Portfolio [Afnan]🚀 Portfolio - Advanced Portfolio Management Indicator 📊

A game-changing portfolio management tool designed to help traders stay on top of their positions and manage risk efficiently. This indicator combines detailed tracking, real-time analytics, and visual clarity to ensure traders are well-equipped for the dynamic world of financial markets.

📈 Key Features 💡

Track up to 14 positions with ease

Real-time Profit & Loss (P&L) updates and risk metrics

Visual representation of entry, stop-loss (SL), and target levels

Alerts for stop-loss breaches and target achievements

Comprehensive portfolio summaries for quick analysis

Customizable options to suit individual trading styles

🔍 Main Components ⚙️

📊 1. Position Tracking

Detailed position data: entry, stop-loss, target levels, and more

Real-time risk-reward ratios

Insights into position size and exposure percentages

Continuous updates on P&L in real-time

📉 2. Visual Indicators

Clear visual markers for entry, SL, and target prices

Price labels with detailed percentage changes

Indicators that show the current position's market status

💼 3. Portfolio Summary

Aggregate account values and exposure

Summarized P&L metrics across all positions

Risk management insights for better decision-making

Daily performance tracking to evaluate strategies

⚠️ 4. Alert System

Instant notifications for stop-loss breaches

Alerts when target prices are hit

Alerts operate for the current chart symbol

⚡ Customization Options 🎨

Show or hide specific data columns

Adjust the table's position and size for better visibility

Personalize color schemes and text styles

Switch between full portfolio view and single symbol focus

📱 How to Use 📝

Input your positions in the indicator's settings

Enable or disable specific positions dynamically

Customize display preferences to your liking

Set up alerts for proactive risk management

Monitor all your trading activities in one comprehensive dashboard

📌 Important Notes ℹ️

Compatible with any trading symbol

Updates seamlessly during market hours

Alerts are specific to the currently active chart symbol

Maximum capacity: 14 simultaneous positions

Created by: @AfnanTAjuddin

⚠️ Disclaimer ⚠️

This indicator is a tool for informational purposes only. Ensure all calculations are verified and consult a financial professional before making investment decisions.

🎯 "Stay disciplined, trade smart, and let data guide your decisions." 📊

[ AlgoChart ] - Compare MarketIndicator Description:

This indicator allows you to display a second asset, selectable from the input panel, in a separate window. Plotted on the same time scale as the first asset but with a distinct price scale, the indicator enables analysis of the relationships and relative movements of two financial instruments. It’s an ideal tool for understanding whether two assets move in a correlated or divergent manner.

Key Features:

Multi-Asset Comparison: Display two assets simultaneously to compare their trends.

Custom Scale: Each asset uses its own price scale, making comparative analysis easier.

Intuitive Interface: Easily select the second asset through the input panel.

Operational Applications:

Spread Trading: Identify optimal moments to execute spread trades when two highly correlated instruments move in opposite directions.

Supply & Demand: Pinpoint zones of interest on both assets, increasing the validity of support and resistance areas.

Exposure Reduction: Monitor instruments that move similarly to avoid exposing the portfolio in identical directions, thereby reducing the risk of double losses.

Additional Features:

Candle Color Change: When a directional divergence occurs between the two assets, the candles change color to highlight the event.

Customizable Notifications: Receive instant alerts when a divergence occurs, allowing you to act promptly.

Dynamic Market Correlation Analyzer (DMCA) v1.0Description

The Dynamic Market Correlation Analyzer (DMCA) is an advanced TradingView indicator designed to provide real-time correlation analysis between multiple assets. It offers a comprehensive view of market relationships through correlation coefficients, technical indicators, and visual representations.

Key Features

- Multi-asset correlation tracking (up to 5 symbols)

- Dynamic correlation strength categorization

- Integrated technical indicators (RSI, MACD, DX)

- Customizable visualization options

- Real-time price change monitoring

- Flexible timeframe selection

## Use Cases

1. **Portfolio Diversification**

- Identify highly correlated assets to avoid concentration risk

- Find negatively correlated assets for hedging strategies

- Monitor correlation changes during market events

2. Pairs Trading

- Detect correlation breakdowns for potential trading opportunities

- Track correlation strength for pair selection

- Monitor technical indicators for trade timing

3. Risk Management

- Assess portfolio correlation risk in real-time

- Monitor correlation shifts during market stress

- Identify potential portfolio vulnerabilities

4. **Market Analysis**

- Study sector relationships and rotations

- Analyze cross-asset correlations (e.g., stocks vs. commodities)

- Track market regime changes through correlation patterns

Components

Input Parameters

- **Timeframe**: Custom timeframe selection for analysis

- **Length**: Correlation calculation period (default: 20)

- **Source**: Price data source selection

- **Symbol Selection**: Up to 5 customizable symbols

- **Display Options**: Table position, text color, and size settings

Technical Indicators

1. **Correlation Coefficient**

- Range: -1 to +1

- Strength categories: Strong/Moderate/Weak (Positive/Negative)

2. **RSI (Relative Strength Index)**

- 14-period default setting

- Momentum comparison across assets

3. **MACD (Moving Average Convergence Divergence)**

- Standard settings (12, 26, 9)

- Trend direction indicator

4. **DX (Directional Index)**

- Trend strength measurement

- Based on DMI calculations

Visual Components

1. **Correlation Table**

- Symbol identifiers

- Correlation coefficients

- Correlation strength descriptions

- Price change percentages

- Technical indicator values

2. **Correlation Plot**

- Real-time correlation visualization

- Multiple correlation lines

- Reference levels at -1, 0, and +1

- Color-coded for easy identification

Installation and Setup

1. Load the indicator on TradingView

2. Configure desired symbols (up to 5)

3. Adjust timeframe and calculation length

4. Customize display settings

5. Enable/disable desired components (table, plot, RSI)

Best Practices

1. **Symbol Selection**

- Choose related but distinct assets

- Include a mix of asset classes

- Consider market cap and liquidity

2. **Timeframe Selection**

- Match timeframe to trading strategy

- Consider longer timeframes for strategic analysis

- Use shorter timeframes for tactical decisions

3. **Interpretation**

- Monitor correlation changes over time

- Consider multiple timeframes

- Combine with other technical analysis tools

- Account for market conditions and volatility

Performance Notes

- Calculations update in real-time

- Resource usage scales with number of active symbols

- Historical data availability may affect initial calculations

Version History

- v1.0: Initial release with core functionality

- Multi-symbol correlation analysis

- Technical indicator integration

- Customizable display options

Future Enhancements (Planned)

- Additional technical indicators

- Advanced correlation algorithms

- Enhanced visualization options

- Custom alert conditions

- Statistical significance testing

Portfolio SnapShot v0.3Here is a Tradingview Pinescript that I call "Portfolio Snapshot". It is based on two other separate scripts that I combined, modified and simplified - shoutout to RedKTrader (Portfolio Tracker - Table Version) and FriendOfTheTrend (Portfolio Tracker For Stocks & Crypto) for their inspiration and code. I was using both of these scripts, and decided to combine the two and increase the number of stocks to 20. I was looking for an easy way to track my entire portfolio (scattered across 5 accounts) PnL on a total and stock basis. PnL - that's it, very simple by design. The features are:

1) Track PnL across multiple accounts, from inception and current day.

2) PnL is reported in two tables, at the portfolio level and individual stock level

3) Both tables can be turned on/off and placed anywhere on the chart.

4) Input up to 20 assets (stocks, crypto, ETFs)

The user has to manually calculate total shares and average basis for stocks in multiple accounts, and then inputs this in the user input dialog. I update mine as each trade is made, or you can just update once a week or so.

I've pre-loaded it with the major indices and sector ETFs, plus URA, GLD, SLV. 100 shares of each, and prices are based on the close Jan 2 2024. So if you don't want to track your portfolio, you can use it to track other things you find interesting, such as annual performance of each sector.

Average Down CalculatorAverage Down Calculator is an indicator for investors looking to manage their portfolio. It aids in calculating the average share price, providing insights into optimizing investment strategies. Averaging down is a strategy investors use when the price of a security they own goes down. Instead of selling at a loss, they buy more shares at the lower price to reduce the average cost per share.

There are situations where a stock's price moves contrary to your expectations. The market moves downward. Despite this, your faith in the stock persists. This indicator allowing you to strategically add more stocks to lower the average price. But You must remember, it’s not without risks, as it involves investing more money in a losing position.

This Indicator allowing you to quickly understand your new position and make informed decisions. It’s designed for easy use, regardless of your experience level with investing.

Steps to use it:

1.put buy fee from your securitas

2.next put the price of the emiten from your portofolio

3.and how many lot you have

4.next is the the taget of percentage you want it become.

5 the last you can choose, the price that you want to buy for average.

this calculator is designed to help you navigate your investment better, choose it wisely.Be aware of the risks of investing more in a declining asset and consider diversification to manage potential losses.

Portfolio Index Generator [By MUQWISHI]▋ INTRODUCTION:

The “Portfolio Index Generator” simplifies the process of building a custom portfolio management index, allowing investors to input a list of preferred holdings from global securities and customize the initial investment weight of each security. Furthermore, it includes an option for rebalancing by adjusting the weights of assets to maintain a desired level of asset allocation. The tool serves as a comprehensive approach for tracking portfolio performance, conducting research, and analyzing specific aspects of portfolio investment. The output includes an index value, a table of holdings, and chart plotting, providing a deeper understanding of the portfolio's historical movement.

_______________________

▋ OVERVIEW:

The image can be taken as an example of building a custom portfolio index. I created this index and named it “My Portfolio Performance”, which comprises several global companies and crypto assets.

_______________________

▋ OUTPUTS:

The output can be divided into 4 sections:

1. Portfolio Index Title (Name & Value).

2. Portfolio Specifications.

3. Portfolio Holdings.

4. Portfolio Index Chart.

1. Portfolio Index Title, displays the index name at the top, and at the bottom, it shows the index value, along with the chart timeframe, e.g., daily change in points and percentage.

2. Portfolio Specifications, displays the essential information on portfolio performance, including the investment date range, initial capital, returns, assets, and equity.

3. Portfolio Holdings, a list of the holding securities inside a table that contains the ticker, average entry price, last price, return percentage of the portfolio's initial capital, and customized weighted percentage of the portfolio. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

4. Index Chart, display a plot of the historical movement of the index in the form of a bar, candle, or line chart.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Style Settings

(1) Naming the index.

(2) Table location on the chart and cell size.

(3) Sorting Holdings Table. By securities’ {Return(%) Portfolio, Weight(%) Portfolio, or Ticker Alphabetical} order.

(4) Choose the type of index: {Equity or Return (%)}, and the plot type for the index: {Candle, Bar, or Line}.

(5) Positive/Negative colors.

(6) Table Colors (Title, Cell, and Text).

(7) To show/hide any indicator’s components.

Section(2): Performance Settings

(1) Calculation window period: from DateTime to DateTime.

(2) Initial Capital and specifying currency.

(3) Option to enable portfolio rebalancing in {Monthly, Quarterly, or Yearly} intervals.

Section(3): Portfolio Holdings

(1) Enable and count security in the investment portfolio.

(2) Initial weight of security. For example, if the initial capital is $100,000 and the weight of XYZ stock is 4%, the initial value of the shares would be $4,000.

(3) Select and add up to 30 symbols that interested in.

Please let me know if you have any questions.

Equity CurveAn equity curve is a graphical representation of the change in the value of a trading account over a time period. The equity curve is a direct reflection of a trading strategy's effectiveness. A consistently upward-trending equity curve indicates a successful strategy, while a flat or declining curve may signal the need for adjustment.

This indicator takes traders daily account values as a comma separated list, and creates an equity curve and simple moving average of the equity curve. This serves as a mirror reflecting the outcome of past actions and decisions, guiding traders in fine-tuning their strategies, managing risk more effectively, and ultimately striving towards a consistently profitable trading journey.

New equity values should be added to the end of the current list. A space or no space after the comma has no effect.

Importance of the Equity Curve

Strategy Evaluation: The equity curve is a direct reflection of a trading strategy's effectiveness over time. A consistently upward-trending equity curve indicates a successful strategy, while a flat or declining curve may signal the need for adjustment.

Risk Management: Monitoring the equity curve helps traders to see the impact of their risk management practices. Sudden drops in equity could highlight instances of excessive risk-taking or inadequate stop-loss settings.

Performance Benchmarks: Comparing the equity curve against benchmarks or desired performance goals allows traders to assess if they are meeting, exceeding, or falling short of their trading objectives.

Psychology: Trading is as much about psychology as it is about strategy. A visual representation of one's equity curve helps maintain discipline, encouraging adherence to a trading plan during downturns and preventing overconfidence during upswings.

Having this data visually allows traders to see which category of trader they fall into.

Unprofitable

Boom or Bust

Profitable

Statistical Data

The indicator not only plots the equity curve and moving average, but includes the option to display the highest value reached by the equity curve, the percentage difference from the peak, and performance over selected periods (All Time, YTD, QTD, MTD, WTD).

Historical Analysis

The Equity Curve Indicator is not just a tool for real-time monitoring of trading performance; it also serves as a powerful instrument for conducting historical analysis. By analyzing the equity curve in conjunction with historical market conditions, traders can identify patterns or triggers that resulted in significant gains or losses.

For example, the chart below shows the equity curve overlaid on periods of net new highs / lows. The equity curve experienced declines while the market was showing net new lows or choppy periods (represented by a red or white background), while most of the equity gains were made while net new highs were present (green background).

This retrospective analysis helps in understanding how different market conditions impact trading strategies and performance.

Trading the Equity Curve

All trading strategies produce an equity curve that has winning and losing periods. In the example above, the trader could introduce a simple rule to lighten up on long positions or move to cash during periods of net new lows.

Another simple rule could be introduced to stop trading if the equity curve falls below the moving average, until favorable market conditions return again.

This indicator is intended to be used on the daily timeframe.

Test - Most correlated assetThis is a simple test to find the most and least correlated assets in a list.

BetaBeta , also known as the Beta coefficient, is a measure that compares the volatility of an individual underlying or portfolio to the volatility of the entire market, typically represented by a market index like the S&P 500 or an investible product such as the SPY ETF (SPDR S&P 500 ETF Trust). A Beta value provides insight into how an asset's returns are expected to respond to market swings.

Interpretation of Beta Values

Beta = 1: The asset's volatility is in line with the market. If the market rises or falls, the asset is expected to move correspondingly.

Beta > 1: The asset is more volatile than the market. If the market rises or falls, the asset's price is expected to rise or fall more significantly.

Beta < 1 but > 0: The asset is less volatile than the market. It still moves in the same direction as the market but with less magnitude.

Beta = 0: The asset's returns are not correlated with the market's returns.

Beta < 0: The asset moves in the opposite direction to the market.

Example

A beta of 1.20 relative to the S&P 500 Index or SPY implies that if the S&P's return increases by 1%, the portfolio is expected to increase by 12.0%.

A beta of -0.10 relative to the S&P 500 Index or SPY implies that if the S&P's return increases by 1%, the portfolio is expected to decrease by 0.1%. In practical terms, this implies that the portfolio is expected to be predominantly 'market neutral' .

Calculation & Default Values

The Beta of an asset is calculated by dividing the covariance of the asset's returns with the market's returns by the variance of the market's returns over a certain period (standard period: 1 years, 250 trading days). Hint: It's noteworthy to mention that Beta can also be derived through linear regression analysis, although this technique is not employed in this Beta Indicator.

Formula: Beta = Covariance(Asset Returns, Market Returns) / Variance(Market Returns)

Reference Market: Essentially any reference market index or product can be used. The default reference is the SPY (SPDR S&P 500 ETF Trust), primarily due to its investable nature and broad representation of the market. However, it's crucial to note that Beta can also be calculated by comparing specific underlyings, such as two different stocks or commodities, instead of comparing an asset to the broader market. This flexibility allows for a more tailored analysis of volatility and correlation, depending on the user's specific trading or investment focus.

Look-back Period: The standard look-back period is typically 1-5 years (250-1250 trading days), but this can be adjusted based on the user's preference and the specifics of the trading strategy. For robust estimations, use at least 250 trading days.

Option Delta: An optional feature in the Beta Indicator is the ability to select a specific Delta value if options are written on the underlying asset with Deltas less than 1, providing an estimation of the beta-weighted delta of the position. It involves multiplying the beta of the underlying asset by the delta of the option. This addition allows for a more precise assessment of the underlying asset's correspondence with the overall market in case you are an options trader. The default Delta value is set to 1, representing scenarios where no options on the underlying asset are being analyzed. This default setting aligns with analyzing the direct relationship between the asset itself and the market, without the layer of complexity introduced by options.

Calculation: Simple or Log Returns: In the calculation of Beta, users have the option to choose between using simple returns or log returns for both the asset and the market. The default setting is 'Simple Returns'.

Advantages of Using Beta

Risk Management: Beta provides a clear metric for understanding and managing the risk of a portfolio in relation to market movements.

Portfolio Diversification: By knowing the beta of various assets, investors can create a balanced portfolio that aligns with their risk tolerance and investment goals.

Performance Benchmarking: Beta allows investors to compare an asset's risk-adjusted performance against the market or other benchmarks.

Beta-Weighted Deltas for Options Traders

For options traders, understanding the beta-weighted delta is crucial. It involves multiplying the beta of the underlying asset by the delta of the option. This provides a more nuanced view of the option's risk relative to the overall market. However, it's important to note that the delta of an option is dynamic, changing with the asset's price, time to expiration, and other factors.

Portfolio TableA tool to manage your invested assets (stocks, crypto currencies, ...).

- Show profit of every asset as well as the total profit.

- Show/hide a bought price line on the chart if the current selected ticker is on your portfolio.

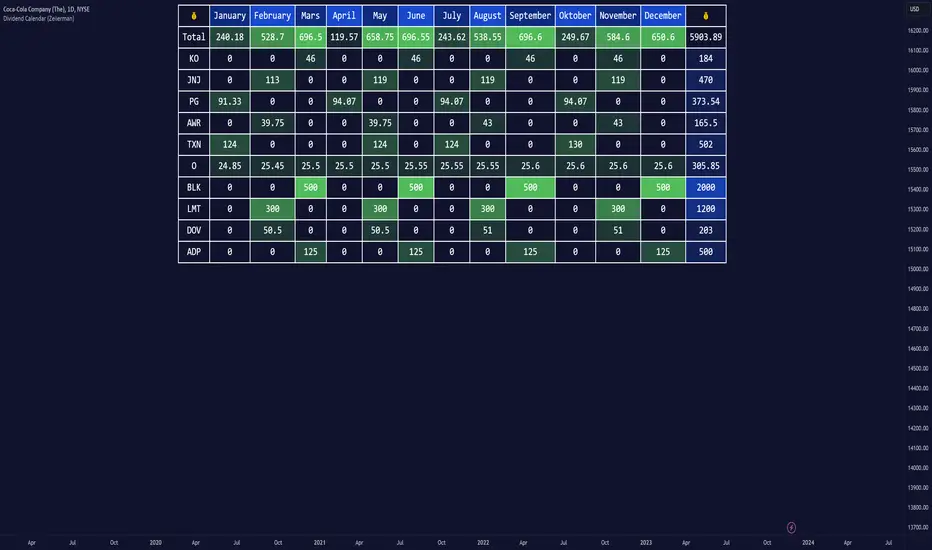

Dividend Calendar (Zeiierman)█ Overview

The Dividend Calendar is a financial tool designed for investors and analysts in the stock market. Its primary function is to provide a schedule of expected dividend payouts from various companies.

Dividends, which are portions of a company's earnings distributed to shareholders, represent a return on their investment. This calendar is particularly crucial for investors who prioritize dividend income, as it enables them to plan and manage their investment strategies with greater effectiveness. By offering a comprehensive overview of when dividends are due, the Dividend Calendar aids in informed decision-making, allowing investors to time their purchases and sales of stocks to optimize their dividend income. Additionally, it can be a valuable tool for forecasting cash flow and assessing the financial health and dividend-paying consistency of different companies.

█ How to Use

Dividend Yield Analysis:

By tracking dividend growth and payouts, traders can identify stocks with attractive dividend yields. This is particularly useful for income-focused investors who prioritize steady cash flow from their investments.

Income Planning:

For those relying on dividends as a source of income, the calendar helps in forecasting income.

Trend Identification:

Analyzing the growth rates of dividends helps in identifying long-term trends in a company's financial health. Consistently increasing dividends can be a sign of a company's strong financial position, while decreasing dividends might signal potential issues.

Portfolio Diversification:

The tool can assist in diversifying a portfolio by identifying a range of dividend-paying stocks across different sectors. This can help mitigate risk as different sectors may react differently to market conditions.

Timing Investments:

For those who follow a dividend capture strategy, this indicator can be invaluable. It can help in timing the buying and selling of stocks around their ex-dividend dates to maximize dividend income.

█ How it Works

This script is a comprehensive tool for tracking and analyzing stock dividend data. It calculates growth rates, monthly and yearly totals, and allows for custom date handling. Structured to be visually informative, it provides tables and alerts for the easy monitoring of dividend-paying stocks.

Data Retrieval and Estimation: It fetches dividend payout times and amounts for a list of stocks. The script also estimates future values based on historical data.

Growth Analysis: It calculates the average growth rate of dividend payments for each stock, providing insights into dividend consistency and growth over time.

Summation and Aggregation: The script sums up dividends on a monthly and yearly basis, allowing for a clear view of total payouts.

Customization and Alerts: Users can input custom months for dividend tracking. The script also generates alerts for upcoming or current dividend payouts.

Visualization: It produces various tables and visual representations, including full calendar views and income tables, to display the dividend data in an easily understandable format.

█ Settings

Overview:

Currency:

Description: This setting allows the user to specify the currency in which dividend values are displayed. By default, it's set to USD, but users can change it to their local currency.

Impact: Changing this value alters the currency denomination for all dividend values displayed by the script.

Ex-Date or Pay-Date:

Description: Users can select whether to show the Ex-dividend day or the Actual Payout day.

Impact: This changes the reference date for dividend data, affecting the timing of when dividends are shown as due or paid.

Estimate Forward:

Description: Enables traders to predict future dividends based on historical data.

Impact: When enabled, the script estimates future dividend payments, providing a forward-looking view of potential income.

Dividend Table Design:

Description: Choose between viewing the full dividend calendar, just the cumulative monthly dividend, or a summary view.

Impact: This alters the format and extent of the dividend data displayed, catering to different levels of detail a user might require.

Show Dividend Growth:

Description: Users can enable dividend growth tracking over a specified number of years.

Impact: When enabled, the script displays the growth rate of dividends over the selected number of years, providing insight into dividend trends.

Customize Stocks & User Inputs:

This setting allows users to customize the stocks they track, the number of shares they hold, the dividend payout amount, and the payout months.

Impact: Users can tailor the script to their specific portfolio, making the dividend data more relevant and personalized to their investments.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Portfolio PnL Tracker

This is a personal portfolio tracker that helps you track your daily profits and losses. You can track up to 64 stocks or cryptocurrencies. You can set them by specifying the symbol and average price.

FEATURES

- Set up to 64 stock or crypto symbols.

- Shows the average price line

- Show profit or loss as a percentage

- Shows only when on the chart that matches the symbol settings.

HOW TO USE

1. Double click the PnL Tracker indicator at the top left of the chart

2. Enter your symbol and average cost

The average cost line shows your current position.

PnL is calculated based on the average cost you input.

The Profit and Loss (PnL) box and the average cost line will only be displayed when your input symbol matches the chart you are currently viewing.

Modern Portfolio Management IndicatorAfter weeks of grueling over this indicator, I am excited to be releasing it!

Intro:

This is not a sexy, technical or math based indicator that will give you buy and sell signals or anything fancy, but it is an indicator that I created in hopes to bridge a gap I have noticed. That gap is the lack of indicators and technical resources for those who also like to plan their investments. This indicator is tailored to those who are either established investors and to those who are looking to get into investing but don't really know where to start.

The premise of this indicator is based on Modern Portfolio Theory (MPT). Before we get into the indicator itself, I think its important to provide a quick synopsis of MPT.

About MPT:

Modern Portfolio Theory (MPT) is an investment framework that was developed by Harry Markowitz in the 1950s. It is based on the idea that an investor can optimize their investment portfolio by considering the trade-off between risk and return. MPT emphasizes diversification and holds that the risk of an individual asset should be assessed in the context of its contribution to the overall portfolio's risk. The theory suggests that by diversifying investments across different asset classes with varying levels of risk, an investor can achieve a more efficient portfolio that maximizes returns for a given level of risk or minimizes risk for a desired level of return. MPT also introduced the concept of the efficient frontier, which represents the set of portfolios that offer the highest expected return for a given level of risk. MPT has been widely adopted and used by investors, financial advisors, and portfolio managers to construct and manage portfolios.

So how does this indicator help with MPT?

The thinking and theory that went behind this indicator was this: I wanted an indicator, or really just a "way" to test and back-test ticker performance over time and under various circumstances and help manage risk.

Over the last 3 years we have seen a massive bull market, followed by a pretty huge bear market, followed by a very unexpected bull market. We have been and continue to be plagued with economic and political uncertainty that seems to constantly be looming over everyone with each waking day. Some people have liquidated their retirement investments, while others are fomoing in to catch this current bull run. But which tickers are sound and how tickers and funds have compared amongst each other remains somewhat difficult to ascertain, absent manually reviewing and calculating each ticker individually.

That is where this indicator comes in. This indicator permits the user to define up to 5 equities that they are potentially interested in investing in, or are already invested in. The user can then select a specific period in time, say from the beginning of 2022 till now. The user can then define how much they want to invest in each company by number of shares, so if they want to buy 1 share a week, or 2 shares a month, they can input these variables into the indicator to draw conclusions. As many brokers are also now permitting fractional share trading, this ability is also integrated into the indicator. So for shares, you can put in, say, 0.25 shares of SPY and the indicator will accept this and account for this fractional share.

The indicator will then show you a portfolio summary of what your earnings and returns would be for the defined period. It will provide a percent return as well as the projected P&L based on your desired investment amount and frequency.

But it goes beyond just that, you can also have the indicator display a simple forecasting projection of the portfolio. It will show the projected P&L and % Return over various periods in time on each of the ticker (see image below):

The indicator will also break down your portfolio allocation, it will show where the majority of your holdings are and where the majority of your P&L in coming from (best performers will show a green fill and worst will show a red fill, see image below):

This colour coding also extends to the portfolio breakdown itself.

Dollar cost averaging (DCA) is incorporated into the indicator itself, by assuming ongoing contributions. If you want to stop contributions at a certain point, you just select your end time for contributions at the point in which you would stop contributing.

The indicator also provides some basic fundamental information about the company tickers (if applicable). Simply select the "Fundamental" chart and it will display a breakdown of the fundamentals, including dividends paid, market cap and earnings yield:

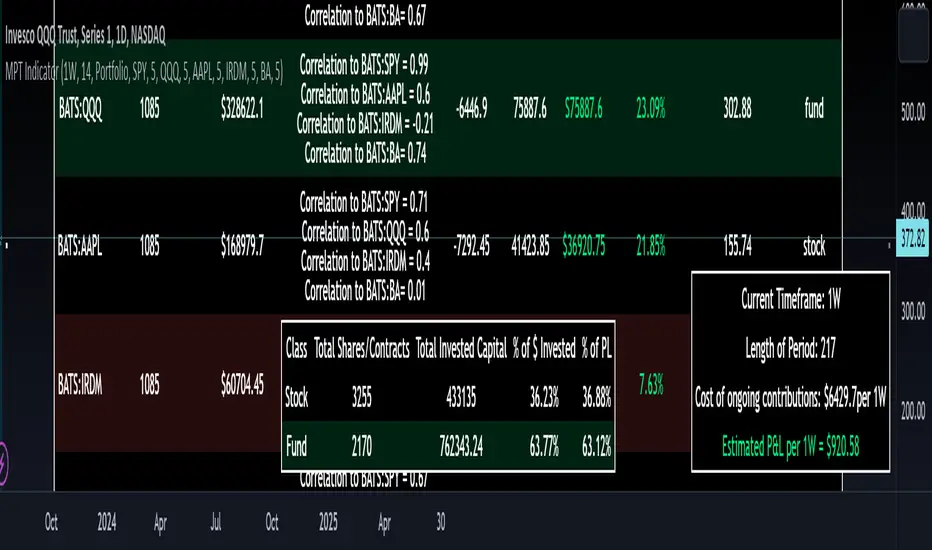

The indicator also provides a correlation assessment of each holding against each other holding. This emphasizes the profound role of diversification on portfolios. The less correlation you have in your portfolio among your holdings, the better diversified you are. As well, if you have holdings that are perfectly inverse other holdings, you have a pseudo hedge against the downturn of one of your holdings. This is even more helpful if the inverse is a company with solid fundamentals.

In the below example you will see NASDAQ:IRDM in the portfolio. You will be able to see that NASDAQ:IRDM has a slight inverse relationship to SPY:

Yet IRDM has solid fundamentals and is performing well fundamentally. Thus, this makes IRDIM a solid addition to your portfolio as it can potentially hedge against a downturn for SPY and is less risky than simply holding an inverse leveraged share on SPY which is most likely just going to cost you money than make you money.

Concluding remarks:

There are many fun and interesting things you can do with this indicator and I encourage you to try it out and have fun with it! The overall objective with the indicator is to help you plan for your portfolio and not necessarily to manage your portfolio. If you have a few stocks you are looking at and contemplating investing in, this will help you run some theoretical scenarios with this stock based on historical performance and also help give you a feel of how it will perform in the future based on past behaviour.

It is important to remember that past behaviour does not indicate future behaviour, but the indicator provides you with tools to get a feel for how a stock has performed under various circumstances and get a general feel of the fundamentals of the company you could potentially be investing in.

Please note, this indicator is not meant to replace full, fundamental analyses of individual companies. It is simply meant to give you a "gist" of how companies are fundamentally and how they have performed historically.

I hope you enjoy it!

Safe trades everyone!

Consensio Allocation ToolOriginally created and taught by Taylor Jenks, this indicator provides portfolio allocation suggestions based on the behaviour of price and 3 simple moving averages (4/10/40 by default)

(ie. when short & medium term SMAs are above the long term then allocation is to be 100%).

This percentage allocated to the stock/commodity is to be reduced as it passes below the SMA's, particularly as each moving average crosses.

Consensio is useful for scaling in and out of a position as the portfolio allocation will change according to the momentum of the asset.

The rules below are my own based on understanding of the trading system developed by Jenks and his online content.

This script has the following rules:

if fastAboveSlowMA and not mediumAboveSlowMA

allocation := 30.0

else if longAboveFastMA

allocation := 0.0

else if fastAboveMediumMA and fastAboveSlowMA

allocation := 100.0

else if not fastAboveMediumMA and fastAboveSlowMA

allocation := 80.0

else if not fastAboveMediumMA and not fastAboveSlowMA

allocation := 50.0

else if not mediumAboveSlowMA and fastAboveSlowMA

allocation := 50.0

// Calculate adjusted allocation percentage based on crossing moving averages

allocation := allocation + (priceAboveFastMA ? 10.0 : -10.0)

allocation := allocation + (priceAboveMediumMA ? 10.0 : -10.0)

Metrics using Alternative Portfolio TheoryLibrary "APT_Metrics"

Portfolio metrics using alternative portfolio theory

metrics(init, cur, start, end, alpha)

Calculates APT metrics

Parameters:

init (float) : Starting Equity (strategy.initial)

cur (float)

start (int) : Start date (UNIX)

end (int) : End Date (UNIX)

alpha (float) : Confidence interval for DaR/CDaR. Defval = 0.05

Returns: Plots table with APT metrics

The metrics are shown in the bottom pane being applied to a buy-and-hold strategy.

PLEASE NOTE: This is the first draft of the library. Some calculations may be incorrect. If you spot any mistakes then please let me know and I will correct them as soon as possible. I am also open to suggestions on how to improve this.

At the moment this only works on the daily timeframe until I can find a way to universally calculate annualized volatility.

Average Cost (Costo Promedio)ENGLISH

This 'Average Cost' script allows the user to input and visualize profit or loss for different stocks (up to 50) with average cost and quantity data on a single chart. This is useful for tracking the profit or loss of each stock in real-time.

To use this script, the user should follow these steps:

1. Add the 'Average Cost' script to your TradingView chart.

2. In the script's configuration window, input the tickers, average costs, and quantity of shares for each ticker you want to monitor.

3. Click 'Accept' to apply the changes.

This script is primarily designed for stock markets, but can also be useful in other financial markets where the user is interested in tracking the performance of multiple assets.

ESPAÑOL

Este script de "Costo Promedio" permite al usuario ingresar y visualizar si hay ganancia o perdida para diferentes acciones (hasta 50) con los datos de costos promedio y cantidad de acciones en un solo gráfico. Esto es útil para realizar un seguimiento de la ganancia o pérdida de cada acción en tiempo real.

Para utilizar este script, el usuario debe seguir estos pasos:

1. Agregue el script "Costo Promedio" a su gráfico en TradingView.

2. En la ventana de configuración del script, ingrese los tickers, costos promedio y cantidad de acciones para cada ticker que desee monitorear.

3. Haga clic en "Aceptar" para aplicar los cambios.

Este script está diseñado principalmente para los mercados de acciones, pero también puede ser útil en otros mercados financieros donde el usuario esté interesado en rastrear el rendimiento de múltiples activos.

Live Portfolio ScreenerThe live portfolio screener indicator is a tool that help users to track the performance of their investments in real-time. The indicator provides a detailed breakdown of the user's portfolio, including the current profit and loss (P&L) for each stock that is invested in. This allows users to quickly and easily see how their portfolio is performing and make informed decisions about their investments on charts. Overall, this tool is an essential tool for anyone looking to stay on top of their investments and make data-driven decisions.

This indicator can load any symbol globally usable.

How to use this indicator ?

in this indicator firstly

you have add script name. (For example if you want to add symbol you have add in 's01 ' means the first symbol)

after that

you have to add price for each (For example if you want to add buy price for the first symbol then add the buy price in ' Bp01 ')

then the quantity comes in picture which is below price list and named here as Bq01 which means 'Buy quantity for first symbol'