Momentum Shift [Bigbeluga]

This indicator identifies momentum shifts using a smoothed momentum calculation. It plots dynamic shift zones consisting of five levels that expand or contract based on price action. When momentum rises, the indicator creates an upward shift zone, and when momentum falls, it generates a downward shift zone. The shift zones dynamically react to price, stopping extension when a level is crossed.

🔵Key Features:

Smoothed Momentum Calculation:

➣ Utilizes a Hull Moving Average (HMA) to smooth momentum and reduce noise.

➣ Identifies momentum shifts with crossovers between the current momentum value and its previous state.

➣ Uses a gradient color scheme to highlight momentum strength.

Dynamic Shift Zones:

➣ When momentum rises, the indicator plots an upper shift zone with five incremental levels.

➣ When momentum falls, a lower shift zone is formed with five descending levels.

➣ Each level within the shift zone represents a progressively stronger momentum shift.

Level Extension Control:

➣ Shift zones stop extending once a level is crossed by price.

➣ Levels closer to price act as key momentum resistance or support zones.

➣ If price retraces after a shift, the remaining levels stay intact for further reference.

Momentum Direction Indications:

➣ Labels (▲ and ▼) appear at momentum shift points to indicate rising or falling momentum.

🔵Usage:

Momentum-Based Entries: Identify momentum shifts early by using shift zones as confirmation for trade entries.

Trend Continuation & Exhaustion: Observe which shift levels price respects—if momentum shift zones hold, the trend may continue; if they break, momentum may reverse.

Dynamic Support & Resistance: Use the five-level shift zones as temporary support and resistance areas that adapt to momentum shifts.

Momentum Strength Analysis: If price moves through multiple shift levels in one direction, it signals strong momentum in that direction.

Momentum Shift is a powerful tool for traders looking to analyze momentum shifts with structured visual zones. By combining smoothed momentum calculations with dynamic shift zones, this indicator provides a clear view of market momentum and helps traders navigate price action effectively.

Pricetargets

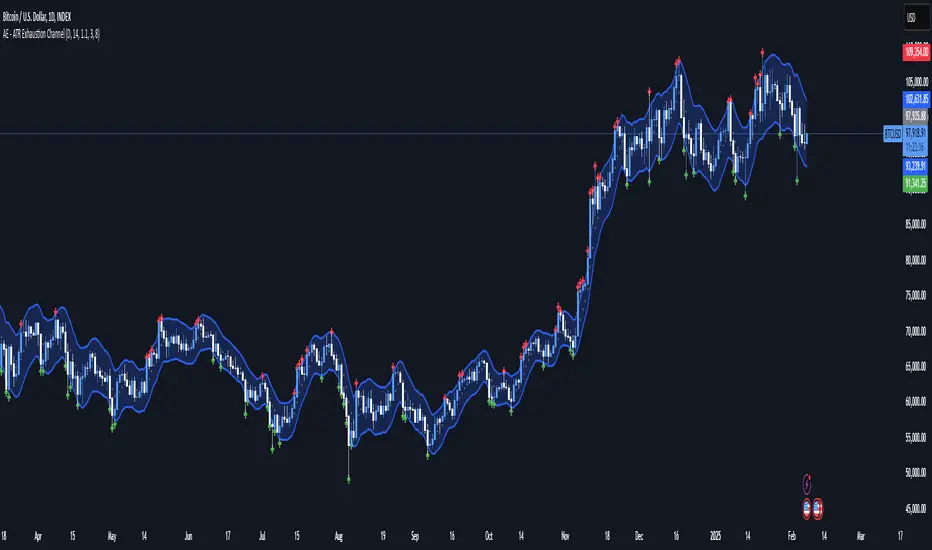

AE - ATR Exhaustion ChannelAE - ATR Exhaustion Channel

📈 Overview

Identify Exhaustion Zones & Trend Breakouts with ATR Precision!

The AE - ATR Exhaustion Channel is a powerful volatility-based trading tool that combines an averaged SMA with ATR bands to dynamically highlight potential trend exhaustion zones. It provides real-time breakout detection by marking when price moves beyond key volatility bands, helping traders spot overextensions and reversals with ease.

🔑 Key Features

✔️ ATR-SMA Hybrid Channel: Uses an averaged SMA as the core trend filter while incorporating adaptive ATR-based bands for precise volatility tracking.

✔️ Dynamic Exhaustion Markers: Marks red crosses when price exceeds the upper band and green crosses when price drops below the lower band.

✔️ Customizable ATR Sensitivity: Adjust the ATR multiplier and length settings to fine-tune band sensitivity based on market conditions.

✔️ Clear Channel Visualization: A gray SMA midpoint and a blue-filled ATR band zone make it easy to track market structure.

📚 How It Works

1️⃣ Averaged SMA Calculation: The script calculates an averaged SMA over a user-defined range (min/max period). This smooths out short-term fluctuations while preserving trend direction.

2️⃣ ATR Band Construction: The ATR value (adjusted by a multiplier) is added to/subtracted from the SMA to form dynamic upper and lower volatility bands.

3️⃣ Exhaustion Detection:

If high > upper ATR band, a red cross is plotted (potential overextension).

If low < lower ATR band, a green cross is plotted (potential reversal zone).

4️⃣ Filled ATR Channel: The area between the upper and lower bands is shaded blue, providing a visual trading range.

🎨 Customization & Settings

⚙️ ATR Length – Adjusts the ATR calculation period (default: 14).

⚙️ ATR Multiplier – Scales the ATR bands for tighter or wider volatility tracking (default: 0.8, adjustable in 0.1 steps).

⚙️ SMA Range (Min/Max Length) – Defines the period range for calculating the averaged SMA (default: 5-20).

⚙️ Rolling Lookback Length – Controls how far back the high/low comparison is calculated (default: 50 bars).

🚀 Practical Usage

📌 Spotting Exhaustion Zones – Look for red/green markers appearing outside the ATR bands, signaling potential trend exhaustion and possible reversal opportunities.

📌 Breakout Confirmation – Price consistently breaching the upper band with momentum could indicate continuation, while repeated touches without strong closes may hint at reversal zones.

📌 Trend Reversal Signals – Watch for green markers below the lower band in uptrends (buy signals) and red markers above the upper band in downtrends (sell signals).

🔔 Alerts & Notifications

📢 Set Alerts for Exhaustion Signals!

Traders can configure alerts to trigger when price breaches the ATR bands, allowing for instant notifications when volatility-based exhaustion is detected.

📊 Example Scenarios

✔ Trend Exhaustion in Overextended Moves – A series of red crosses near resistance may indicate a short opportunity.

✔ Trend Exhaustion in Overextended Moves – A series of red crosses near resistance may indicate an opportunity to open a short trade.

✔ Volatility Compression Breakouts – If price consolidates within the ATR bands and suddenly breaks out, it could signify a momentum shift.

✔ Reversal Catching in Trending Markets – Spot potential trend reversals by looking for green markers below the ATR bands in bullish markets.

🌟 Why Choose AE - ATR Exhaustion Channel?

Trade with Confidence. Spot Volatility. Catch Breakouts.

The AE - ATR Exhaustion Channel is an essential tool for traders looking to identify trend exhaustion, detect breakouts, and manage volatility effectively. Whether you're trading stocks, crypto, or forex, this ATR-SMA hybrid system provides clear visual cues to help you stay ahead of market moves.

✅ Customizable to Fit Any Market

✅ Combines Volatility & Trend Analysis

✅ Easy-to-Use with Instant Breakout Detection

Dynamic Deviation Levels [BigBeluga]Dynamic Deviation Levels is an innovative indicator designed to analyze price deviations relative to a smoothed midline. It provides traders with visual cues for overbought/oversold zones, price momentum, levels through labeled deviations and gradient candle coloring.

🔵Key Features:

Smoothed Midline:

A central line calculated as a smoothed median of the price source, serving as the baseline for price deviation analysis.

Dynamic Deviation Levels:

- Three deviation levels are plotted above and below the midline, with labels (1, 2, 3, -1, -2, -3) marking significant price movements.

- Helps traders identify overbought and oversold market conditions.

Heat-Colored Candles:

- Candle colors shift in intensity based on the deviation level, with four gradient shades for both upward and downward movements.

- Quickly highlights market extremes or stable zones.

Interactive Color Scale:

- A gradient scale at the bottom right of the chart visually represents deviation values.

- A triangle marker indicates the current price deviation in real time.

Optional Deviation Levels Display:

- Traders can enable all dynamic levels on the chart to visualize support and resistance areas dynamically.

🔵Usage and Benefits:

Identify Overbought/Oversold Zones: Use labeled deviation levels and heat-colored candles to spot stretched market conditions.

Track Trend Reversals and Momentum: Monitor price interactions with deviation levels for potential trend continuation or reversal signals.

Real-Time Deviation Insights: Leverage the color scale and triangle marker for live deviation tracking and actionable insights.

Map Dynamic Support and Resistance: Enable dynamic levels to highlight key areas where price reactions are likely to occur.

Dynamic Deviation Levels is an indispensable tool for traders aiming to combine price dynamics, momentum analysis, and visual clarity in their trading strategies.

Intraday Volatility Bands [Honestcowboy]The Intraday Volatility Bands aims to provide a better alternative to ATR in the calculation of targets or reversal points.

How are they different from ATR based bands?

While ATR and other measures of volatility base their calculations on the previous bars on the chart (for example bars 1954 to 1968). The volatility used in these bands measure expected volatility during that time of the day.

Why would you take this approach?

Markets behave different during certain times of the day, also called sessions.

Here are a couple examples.

Asian Session (generally low volatility)

London Session (bigger volatility starts)

New York Session (overlap of New York with London creates huge volatility)

Generally when using bands or channel type indicators intraday they do not account for the upcoming sessions. On London open price will quickly spike through a bollinger band and it will take some time for the bands to adjust to new volatility.

This script will show expected volatility targets at the start of each new bar and will not adjust during the bar. It already knows what price is expected to do at this time of day.

Script also plots arrows when price breaches either the top or bottom of the bands. You can also set alerts for when this occurs. These are non repainting as the script knows the level at start of the bar and does not change.

🔷 CALCULATION

Think of this script like an ATR but instead it uses past days data instead of previous bars data. Charts below should visualise this more clearly:

The scripts measure of volatility is based on a simple high-low.

The script also counts the number of bars that exist in a day on your current timeframe chart. After knowing that number it creates the matrix used in it's calculations and data storage.

See how it works perfectly on a lower timeframe chart below:

Getting this right was the hardest part, check the coding if you are interested in this type of stuff. I commented every step in the coding process.

🔷 SETTINGS

Every setting of the script has a tooltip but I provided a breakdown here:

Some more examples of different charts: