ETF Builder & Backtest System [TradeDots]Create, analyze, and monitor your own custom “ETF-like” portfolio directly on TradingView. This script merges up to 10 different assets with user-defined weightings into a single composite chart, allowing you to see how your personalized portfolio would have performed historically. It is an original tool designed to help traders and investors quickly gauge risk and return profiles without leaving the TradingView platform.

📝 HOW IT WORKS

1. Custom Portfolio Construction

Multiple Assets : Combine up to 10 different stocks, ETFs, cryptocurrencies, or other symbols.

User-Defined Weights : Allocate each asset a percentage weight (e.g., 15% in AAPL, 10% in MSFT, etc.).

Single Composite Value : The script calculates a weighted “ETF-style” price, effectively simulating a merged portfolio curve on your chart.

2. Performance Tracking & Return Analysis

Automatic History Capture : The indicator records each asset’s starting price when it first appears in your chosen date range.

Rolling Updates : As time progresses, all asset prices are continually evaluated and the portfolio value is updated in real time.

Buy & Hold Returns : See how each asset—and the overall portfolio—performed from the “start” date to the most recent bar.

Annualized Return : Automatically calculates CAGR (Compound Annual Growth Rate) to help visualize performance over varying timescales.

3. Table & Visual Output

Performance Table : A comprehensive table displays individual asset returns, annualized returns, and portfolio totals.

Normalized Chart Plot : The composite ETF value is scaled to 100 at the start date, making it easy to compare relative growth or decline.

Optional Time Filter : You can define a specific date range (Start/End Dates) to focus on a particular period or to limit historical data.

⚙️ KEY FEATURES

1. Flexible Asset Selection

Choose any symbols from multiple asset classes. The script will only run calculations when data is available—no need to worry about missing quotes.

2. Dynamic Table Reporting

Start Price for each asset

Percentage Weight in the portfolio

Total Return (%) and Annualized Return (%)

3. Simple Backtesting Logic

This script takes a straightforward Buy & Hold perspective. Once the start date is reached, the portfolio remains static until the end date, so you can quickly assess hypothetical growth.

4. Plot Customization

Toggle the main “ETF” plot on/off.

Alter the visual style for tables and text.

Adjust the time filter to limit or extend your performance measurement window.

🚀 HOW TO USE IT

1. Add the Script

Search for “ETF Builder & Backtest System ” in the Indicators & Strategies tab or manually add it to your chart after saving it in your Pine Editor.

2. Configure Inputs

Enable Time Filter : Choose whether to restrict the analysis to a particular date range.

Start & End Date : Define the period you want to measure performance over (e.g., from 2019-12-31 to 2025-01-01).

Assets & Weights : Enter each symbol and specify a percentage weight (up to 10 assets).

Display Options : Pick where you want the Table to appear and choose background/text colors.

3. Interpret the Table & Plots

Asset Rows : Each asset’s ticker, weighting, start price, and performance metrics.

ETF Total Row : Summarizes total weighting, composite starting value, and overall returns.

Normalized Plot : Tracks growth/decline of the combined portfolio, starting at 100 on the chart.

4. Refine Your Strategy

Compare how different weights or a new mix of assets would have performed over the same period.

Assess if certain assets contribute disproportionately to your returns or volatility.

Use the results to guide allocations in your real trading or paper trading accounts.

❗️LIMITATIONS

1. Buy & Hold Only

This script does not handle rebalancing or partial divestments. Once the portfolio starts, weights remain fixed throughout the chosen timeframe.

2. No Reinvestment Tracking

Dividends or other distributions are not factored into performance.

3. Data Availability

If historical data for a particular asset is unavailable on TradingView, related results may display as “N/A.”

4. Market Regimes & Volatility

Past performance does not guarantee similar future behavior. Markets can change rapidly, which may render historical backtests less predictive over time.

⚠️ RISK DISCLAIMER

Trading and investing carry significant risk and can result in financial loss. The “ETF Builder & Backtest System ” is provided for informational and educational purposes only. It does not constitute financial advice.

Always conduct your own research.

Use proper risk management and position sizing.

Past performance does not guarantee future results.

This script is an original creation by TradeDots, published under the Mozilla Public License 2.0.

Use this indicator as part of a broader trading or investment approach—consider fundamental and technical factors, overall market context, and personal risk tolerance. No trading tool can assure profits; exercise caution and responsibility in all financial decisions.

Cari dalam skrip untuk "国泰黄金ETF联接C相关行业指数的最新政策"

ETF 3-Day Reversion StrategyIntroduction: This strategy is a modification of the “3-day Mean Reversion Strategy” from the book "High Probability ETF Trading" by Larry Connors and Cesar Alvarez. In the book, the authors discuss a high-probability ETF mean reversion strategy for a 1-day time-frame with these simple rules:

The price must be above the 200 day SMA and below the 5 day SMA.

The low of today must be lower than the low of yesterday (must be true for 3 consecutive days)

The high of today must be lower than the high of yesterday (must be true for 3 consecutive days)

If the 3 rules above are true, then buy on the close of the current day.

Exit when the closing price crosses above the 5 day SMA.

In practice and in backtesting, I’ve found that the strategy consistently works better when using an EMA for the trend-line instead of an SMA. So, this script uses an EMA for the trend-line. I’ve also made the length of the exit EMA adjustable.

How it works:

The Strategy will buy when the buy conditions above are true. The strategy will sell when the closing price crosses over the Exit Moving Average

Plots:

Green line = Exit Moving Average (Default 5 Day EMA)

Blue line = 5 Day EMA (Used as Entry Criteria)

Disclaimer: Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

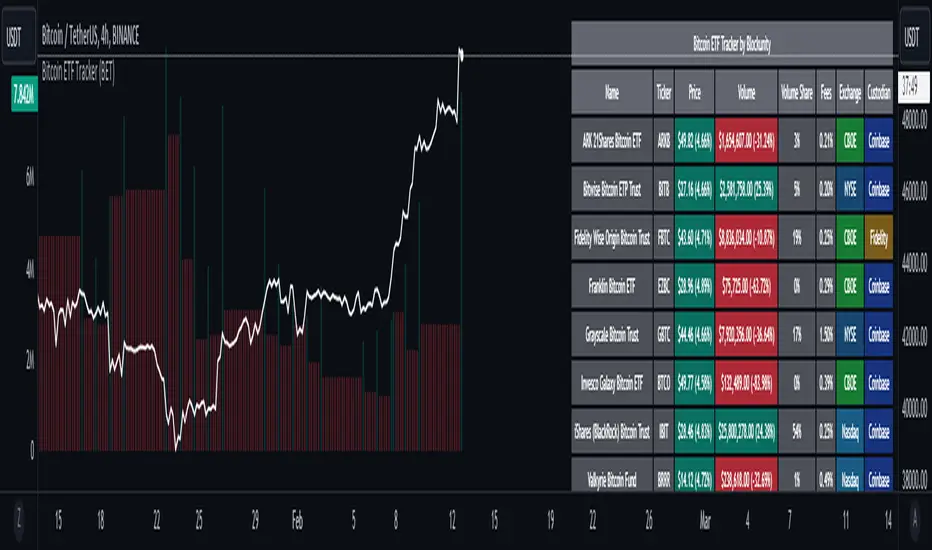

Bitcoin ETF Tracker (BET)Get all the information you need about all the different Bitcoin ETFs.

With the Bitcoin ETF Tracker, you can observe all possible Bitcoin ETF data:

The ETF name.

The ticker.

The price.

The volume.

The share of total ETF volume.

The ETF fees.

The exchange and custodian.

At the bottom of the table, you'll find the day's total volume.

In addition, you can see the volume for the different Exchanges, as well as for the different Custodians.

If you don't want to display these lines to save space, you can uncheck "Show Additional Data" in the indicator settings.

The Idea

The goal is to provide the community with a tool for tracking all Bitcoin ETF data in a synthesized way, directly in your TradingView chart.

How to Use

Simply read the information in the table. You can hover above the Fees and Exchanges cells for more details.

The table takes space on the chart, you can remove the extra lines by unchecking "Show Additional Data" in the indicator settings or reduce text size by changing the "Table Text Size" parameter.

Upcoming Features

As soon as we have a little more history, we'll add variation rates as well as plots to observe the breakdown between the various Exchanges and Custodians.

The Lazy Trader - Index (ETF) Trend Following Robot50/150 moving average, index (ETF) trend following robot. Coded for people who cannot psychologically handle dollar-cost-averaging through bear markets and extreme drawdowns (although DCA can produce better results eventually), this robot helps you to avoid bear markets. Be a fair-weathered friend of Mr Market, and only take up his offer when the sun is shining! Designed for the lazy trader who really doesn't care...

Recommended Chart Settings:

Asset Class: ETF

Time Frame: Daily

Necessary ETF Macro Conditions:

a) Country must have healthy demographics, good ratio of young > old

b) Country population must be increasing

c) Country must be experiencing price-inflation

Default Robot Settings:

Slow Moving Average: 50 (integer) //adjust to suit your underlying index

Fast Moving Average: 150 (integer) //adjust to suit your underlying index

Bullish Slope Angle: 5 (degrees) //up angle of moving averages

Bearish Slope Angle: -5 (degrees) //down angle of moving averages

Average True Range: 14 (integer) //input for slope-angle formula

Risk: 100 (%) //100% risk means using all equity per trade

ETF Test Results (Default Settings):

SPY (1993 to 2020, 27 years), 332% profit, 20 trades, 6.4 profit factor, 7% drawdown

EWG (1996 to 2020, 24 years), 310% profit, 18 trades, 3.7 profit factor, 10% drawdown

EWH (1996 to 2020, 24 years), 4% loss, 26 trades, 0.9 profit factor, 36% drawdown

QQQ (1999 to 2020, 21 years), 232% profit, 17 trades, 3.6 profit factor, 2% drawdown

EEM (2003 to 2020, 17 years), 73% profit, 17 trades, 1.1 profit factor, 3% drawdown

GXC (2007 to 2020, 13 years), 18% profit, 14 trades, 1.3 profit factor, 26% drawdown

BKF (2009 to 2020, 11 years), 11% profit, 13 trades, 1.2 profit factor, 33% drawdown

A longer time in the markets is better, with the exception of EWH. 6 out of 7 tested ETFs were profitable, feel free to test on your favourite ETF (default settings) and comment below.

Risk Warning:

Not tested on commodities nor other financial products like currencies (code will not work), feel free to leave comments below.

Moving Average Slope Angle Formula:

Reproduced and modified from source:

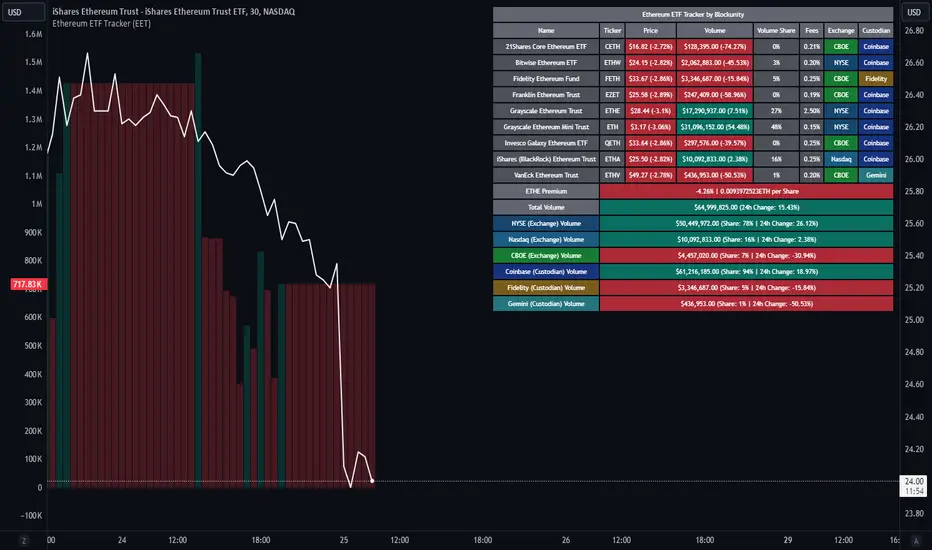

Ethereum ETF Tracker (EET)Get all the information you need about all the different Ethereum ETF.

With the Ethereum ETF Tracker, you can observe all possible Ethereum ETF data:

ETF name.

Ticker.

Price.

Volume.

Share of total ETF volume.

Fees.

Exchange.

Custodian.

At the bottom of the table, you'll find the ETHE Premium (and ETH per Share), and day's total volume.

In addition, you can see the volume for the different Exchanges, as well as for the different Custodians.

If you don't want to display these lines to save space, you can uncheck "Show Additional Data" in the indicator settings.

The Idea

The goal is to provide the community with a tool for tracking all Ethereum ETF data in a synthesized way, directly in your TradingView chart.

How to Use

Simply read the information in the table. You can hover above the Fees and Exchanges cells for more details.

The table takes space on the chart, you can remove the extra lines by unchecking "Show Additional Data" in the indicator settings or reduce text size by changing the "Table Text Size" parameter.

Aggregate volume can be displayed directly on the graph (this volume can be displayed on any asset, such as Ethereum itself). The display can be disabled in the settings.

BTC ETF VolumesVolume

This script plots the trading volume of all BTC spot ETFs as well as the aggregate volume. Works on any chart and any timeframe.

Indicators

The volume of every ETF is plotted in a different color, with the total column adding up to the aggregate volume.

If you have price and indicator labels enabled you will also see individual ETF volume on your price scale on the right hand side.

If more BTC ETFs get launched I will add them.

ETFs Sector PerformanceDisplays a table of the Top 8 performing ETFs over a selected period (1M / 2M / 3M / 6M) to quickly identify industry strength.

Pre-Set Universe (39 ETFs)

ITA — iShares U.S. Aerospace & Defense ETF

DBA — Invesco DB Agriculture Fund

BOTZ — Global X Robotics & Artificial Intelligence ETF

JETS — U.S. Global Jets ETF

XLB — Materials Select Sector SPDR Fund

XBI — SPDR S&P Biotech ETF

PKB — Invesco Dynamic Building & Construction ETF

ICLN — iShares Global Clean Energy ETF

SKYY — First Trust Cloud Computing ETF

DBC — Invesco DB Commodity Index Tracking Fund

XLY — Consumer Discretionary Select Sector SPDR Fund

XLP — Consumer Staples Select Sector SPDR Fund

BLOK — Amplify Transformational Data Sharing ETF

KARS — KraneShares Electric Vehicles & Future Mobility ETF

XLE — Energy Select Sector SPDR Fund

ESPO — VanEck Video Gaming and eSports ETF

XLF — Financial Select Sector SPDR Fund

PBJ — Invesco Dynamic Food & Beverage ETF

ITB — iShares U.S. Home Construction ETF

XLI — Industrial Select Sector SPDR Fund

PAVE — Global X U.S. Infrastructure Development ETF

PEJ — Invesco Dynamic Leisure & Entertainment ETF

LIT — Global X Lithium & Battery Tech ETF

IHI — iShares U.S. Medical Devices ETF

XME — SPDR S&P Metals & Mining ETF

FCG — First Trust Natural Gas ETF

URA — Global X Uranium ETF

PPH — VanEck Pharmaceutical ETF

QTUM — Defiance Quantum Computing & Machine Learning ETF

IYR — iShares U.S. Real Estate ETF

XRT — SPDR S&P Retail ETF

SOXX — iShares Semiconductor ETF

BOAT — SonicShares Global Shipping ETF

IGV — iShares Expanded Tech-Software Sector ETF

TAN — Invesco Solar ETF

SLX — VanEck Steel ETF

IYZ — iShares U.S. Telecommunications ETF

IYT — iShares U.S. Transportation ETF

XLU — Utilities Select Sector SPDR Fund

ETF-Benchmark AnalyzerHave you ever wondered which ETF performs the best? Which one is the most volatile, or which one has the smallest drawdown?

This Pine Script™ "ETF-Benchmark Analyzer" compares the performance of an ETF (such as SPY, the S&P 500 ETF) against a benchmark, which can also be adjusted by the user. It provides several key financial metrics, such as:

Performance (%): Displays the total return over a specified lookback period (e.g., 1 year). It compares the performance of the ETF against the benchmark and shows the difference.

Alpha (%): Measures the excess return of the ETF over the expected return, which is calculated using the benchmark’s return. Positive alpha indicates that the ETF has outperformed the benchmark, while negative alpha suggests underperformance. This metric is important because it isolates performance that cannot be explained by exposure to the benchmark's movements.

Sharpe Ratio: A risk-adjusted measure of return. It is calculated by dividing the excess return of the ETF (above the risk-free rate) by its standard deviation (volatility). A higher Sharpe ratio indicates better risk-adjusted returns. The Sharpe ratio is calculated for both the ETF and the benchmark, and their difference is displayed as well.

Drawdown: The percentage decrease from the highest price to the lowest price over the lookback period. This is a critical measure of risk, as it shows the largest potential loss an investor might face during a specific period.

Beta: Measures the ETF’s sensitivity to movements in the benchmark. A beta of 1 means the ETF moves in line with the benchmark; greater than 1 means it is more volatile, while less than 1 means it is less volatile.

These metrics provide a holistic view of the ETF’s performance compared to the benchmark, allowing traders to assess the risk and return profile more effectively.

Scientific Sources

Sharpe Ratio: Sharpe, W. F. (1994). The Sharpe Ratio. Journal of Portfolio Management, 21(1), 49-58. This paper defines and develops the Sharpe ratio as a measure of risk-adjusted return.

Alpha and Beta: Jensen, M. C. (1968). The Performance of Mutual Funds in the Period 1945–1964. The Journal of Finance, 23(2), 389-416. This paper discusses the concepts of alpha and beta in the context of mutual fund performance.

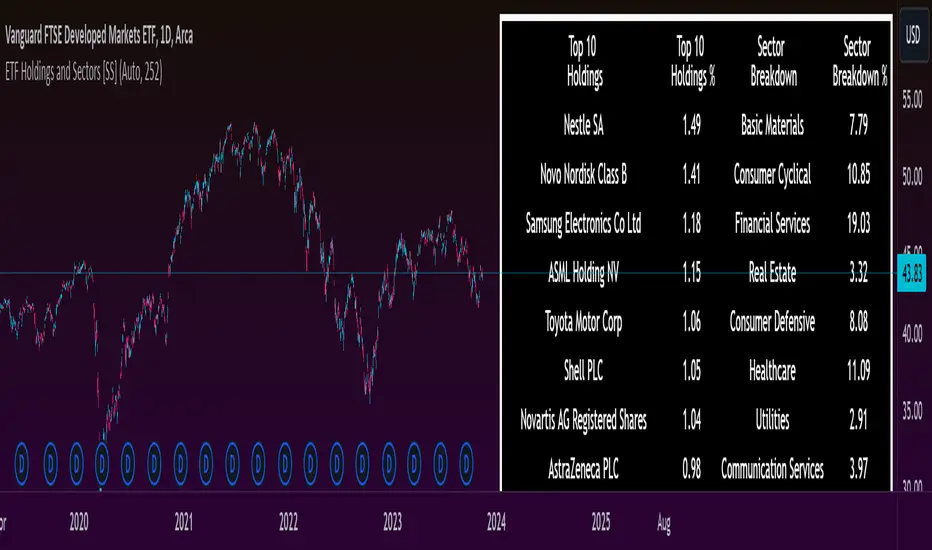

ETF Holdings and Sectors [SS]Made this fun little indicator.

It is another showcase one, just demonstrating the ETF library that contains the top 10 holdings of various US-based ETFs, as well as a breakdown by sector.

The indicator is defaulted to auto settings. This means it will automatically populate with ETF data when you are on that ETF chart. If you are on another chart, it will disappear for which no information is available, it will disappear. (Note, it is also programmed to recognize the leveraged share versions, such as TNA, TZA, SPXL, UPRO, etc.)

However, there is another cool little function it does, which is, it will search all available ETFs in the database to find if any of them hold the ticker you are on and, if so, what percentage of the ETF is invested in that particular ticker.

We can look at some examples:

MSFT:

NVDA:

BA:

AAPL:

JPM:

And if you are on a chart that is neither an ETF or is not found in any of the databases, the indicator disappears:

It made it so you could leave it running in the background and it would do its thing.

You can also choose to manually search through the available ETFs in the list.

Another function is, that when you are on the ETF itself, it will display the past 252 (1 trading year) day return. You can modify this to any amount of days you would like in the settings.

All of the settings are customizable. You can choose what you want and don't want to be plotted.

That's the indicator in a nutshull, just something fun and interesting to play around with.

Hope you enjoy!

Safe trades everyone and thanks for reading!

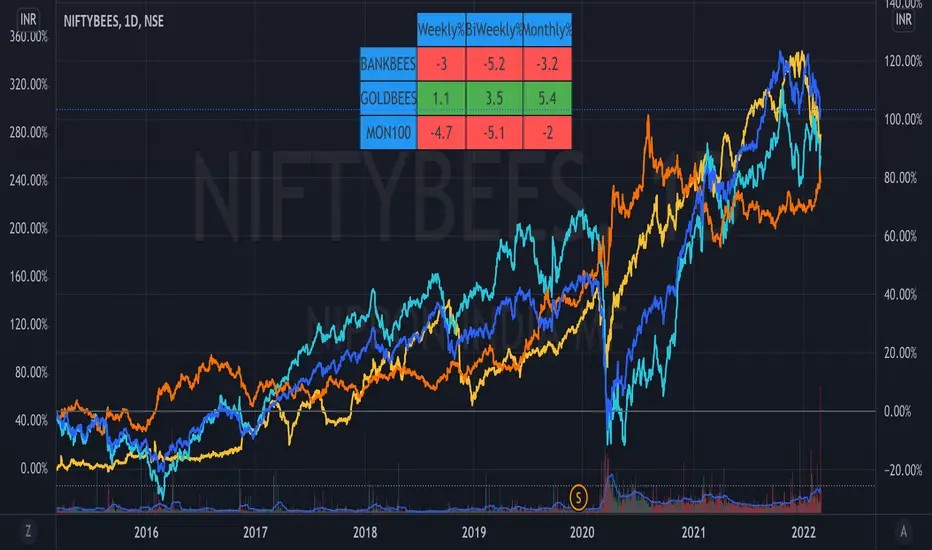

ETF Trends//@Devendra Akolkar - @dakolkar - This indicator will compare and show relative performance of 3 symbols.

// It'll compare those 3 symbols on 3 different Timeframe (Weekly - 5 sessions , BiWeekly - 10 sessions and Monthly - 20 sessions) and display performance in %

TASC 2024.06 REIT ETF Trading System█ OVERVIEW

This strategy script demonstrates the application of the Real Estate Investment Trust (REIT) ETF trading system presented in the article by Markos Katsanos titled "Is The Price REIT?" from TASC's June 2024 edition of Traders' Tips .

█ CONCEPTS

REIT stocks and ETFs offer a simplified, diversified approach to real estate investment. They exhibit sensitivity to interest rates, often moving inversely to interest rate and treasury yield changes. Markos Katsanos explores this relationship and the correlation of prices with the broader market to develop a trading strategy for REIT ETFs.

The script employs Bollinger Bands and Donchian channel indicators to identify oversold conditions and trends in REIT ETFs. It incorporates the 10-year treasury yield index (TNX) as a proxy for interest rates and the S&P 500 ETF (SPY) as a benchmark for the overall market. The system filters trade entries based on their behavior and correlation with the REIT ETF price.

█ CALCULATIONS

The strategy initiates long entries (buy signals) under two conditions:

1. Oversold condition

The weekly ETF low price dips below the 15-week Bollinger Band bottom, the closing price is above the value by at least 0.2 * ATR ( Average True Range ), and the price exceeds the week's median.

Either of the following:

– The TNX index is down over 15% from its 25-week high, and its correlation with the ETF price is less than 0.3.

– The yield is below 2%.

2. Uptrend

The weekly ETF price crosses above the previous week's 30-week Donchian channel high.

The SPY ETF is above its 20-week moving average.

Either of the following:

– Over ten weeks have passed since the TNX index was at its 30-week high.

– The correlation between the TNX value and the ETF price exceeds 0.3.

– The yield is below 2%.

The strategy also includes three exit (sell) rules:

1. Trailing (Chandelier) stop

The weekly close drops below the highest close over the last five weeks by over 1.5 * ATR.

The TNX value rises over the latest 25 weeks, with a yield exceeding 4%, or its value surges over 15% above the 25-week low.

2. Stop-loss

The ETF's price declines by at least 8% of the previous week's close and falls below the 30-week moving average.

The SPY price is down by at least 8%, or its correlation with the ETF's price is negative.

3. Overbought condition

The ETF's value rises above the 100-week low by over 50%.

The ETF's price falls over 1.5 * ATR below the 3-week high.

The ETF's 10-week Stochastic indicator exceeds 90 within the last three weeks.

█ DISCLAIMER

This strategy script educates users on the system outlined by the TASC article. However, note that its default properties might not fully represent real-world trading conditions for an individual. By default, it uses 10% of equity as the order size and a slippage amount of 5 ticks. Traders should adjust these settings and the commission amount when using this script. Additionally, since this strategy utilizes compound conditions on weekly data to trigger orders, it will generate significantly fewer trades than other, higher-frequency strategies.

Trendflex - Another new Ehlers indicatorSource: Stocks and Commodities V38

Hooray! Another new John Ehlers indicator!

John claims this indicator is lag-less and uses the SPY on the Daily as an example.

This indicator is a slight modification of Reflex, which I have posted here

I think it's better for Stocks and ETFs than Reflex since it factors in long trends. It tends to keep you in winning trades for a long time.

I believe this indicator can be used for entries or exits, potentially both.

Entry

1. Entering Long positions at the pivot low points (Stocks and ETFs)

2. Entering Long when the Reflex crosses above the zero lines (Stocks, ETFs, Commodities )

Exit

1. Exiting Long positions at a new pivot high point (Stocks and ETFs)

2. Exiting Long when the Reflex crosses below the zero lines (Stocks, ETFs, Commodities )

In this example, I place a Long order on the SPY every time the Reflex crosses above the zero level and exit when it crosses below or pops my stop loss, set at 1.5 * Daily ATR.

2/3 Wins

+16.05%

Let me know in the comment section if you're able to use this in a strategy.

Reflex - A new Ehlers indicatorSource: Stocks and Commodities V38

Hooray! A new John Ehlers indicator!

John claims this indicator is lag-less and uses the SPY on the Daily as an example.

He states that drawing a line from peak to peak (or trough to trough) will correspond perfectly with the Asset.

I have to say I agree! There is typically one bar of lag or no lag at all!

I believe this indicator can be used for either entries or exits, but not both.

Entry

1. Entering Long positions at the pivot low points (Stocks and ETFs)

2. Entering Long when the Reflex crosses above the zero lines (Stocks, ETFs, Commodities)

Exit

1. Exiting Long positions at a new pivot high point (Stocks and ETFs)

2. Exiting Long when the Reflex crosses below the zero lines (Stocks, ETFs, Commodities)

In this example, I place a Long order on the SPY every time the Reflex crosses above the zero level and exit when it crosses below or pops my stop loss, set at 1.5 * Daily ATR.

4/6 Wins

+10.76%

For me, that's good enough to create a strategy and backtest on several Indices and ETFs, which is what I have a hunch this will work on.

I think there is a lot of promise from a single Indicator!

Let me know in the comment section if you're able to use this in a strategy.

Earnings Date Highlighter - from0_to_1This indicator, called "Earnings Date Highlighter," is designed to visualize earnings data for up to four different stocks on a single chart. It's particularly useful for traders or investors who want to track earnings events for multiple companies simultaneously, such as the top holdings of an ETF.

Key features:

1. Tracks earnings data (estimates and actuals) for four user-defined symbols.

2. Plots earnings data points with customizable colors for each symbol.

3. Highlights earnings dates with background colors.

4. Displays green up arrows for earnings beats and red down arrows for earnings misses.

Why someone would use it:

1. To monitor earnings events for multiple stocks in a single view.

2. To quickly identify potential market-moving events for key components of an ETF or portfolio.

3. To spot patterns in earnings performance across different companies or sectors.

4. To help with timing trades or adjusting positions around earnings announcements.

This tool can be particularly valuable for investors focused on ETFs, as it allows them to visualize earnings dates and performance for the ETF's major holdings all in one place, potentially providing insights into how the ETF might behave around these key events.

Author:

www.tradingview.com

Sector Rotation Hedging With Volatility Index [TradeDots]The "Sector Rotation Hedging Strategy With Volatility Index" is a comprehensive trading indicator developed to optimally leverage the S&P500 volatility index. It is designed to switch between distinct ETF sectors, strategically hedging to moderate risk exposure during harsh market volatility.

HOW DOES IT WORK

The core of this indicator is grounded on the S&P500 volatility index (VIX) close price and its 60-day moving average. This serves to determine whether the prevailing market volatility is above or below the quarterly average.

In periods of elevated market volatility, risk exposure escalates significantly. Traders retaining stocks in sectors with disproportionately high volatility face increased vulnerability to negative returns. To tackle this, our indicator employs a two-pronged approach utilizing two sequential candlestick close prices to confirm if volatility surpasses the average value.

Upon confirming above-average volatility, a hedging table is deployed to spotlight ETFs with low volatility, such as the Utilities Select Sector SPDR Fund (XLU), to derisk the overall portfolio.

Conversely, in low-volatility conditions, sectors yielding higher returns like the Technology Select Sector SPDR Fund (XLK) are preferred. The hedging table is utilized to earmark high-return sector ETFs.

Thus, during highly volatile market periods, the strategy recommends enhancing portfolio allocation to low-volatility ETFs. During low-volatility windows, the portfolio is calibrated towards high-volatility ETFs for heightened returns.

IMPORTANT CONSIDERATION

In real trading, additional considerations encompassing trading commissions, management fees, and ancillary rotation costs should be factored in. False signals may arise, potentially leading to losses from these fees.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

Daily Spot BTC ETF flowsIndicator for use on the daily timeframe to show combined capital flows into 8 of the largest spot bitcoin ETFs to allow the user to track potential buy and selling pressure on spot BTC.

The included ETFs are:

GBTC

ARKB

FBTC

HODL

IBIT

EZBC

BTCO

BITB

Net daily volume is derived from lower timeframe data (5 minute chart by default) for each ETF and multiplied by the average price for the period (defined by the mean of the high, low + close values). This gives the net capital inflow or outflow for each ETF, every period. The individual daily values are added together to give a total capital flow per day and plotted as columns. The cumulative sum of all previous periods is also calculated each period/day and plotted as a line chart.

This is the only indicator currently collating this capital flow data together and presents it as an easy to understand chart to help the user gauge market conditions. By using low time frame bars to calculate the up and down volumes, accuracy is improved.

All-Time High with Percentage Drops for ETF's and Large CapsPlots the percentage drop levels from the All-Time High of any ticker. You can use this within a pullback trading system. For example, if you historically look at the average pullback of large cap stocks and ETF's, you can use this indicator to plot the levels it could pullback to for an entry to go long. It can be used as potential targets when trading a ticker short. Another use for this is to backtest the set percentage targets using TradingView's bar replay feature to see how ETF's and large cap stocks have reacted at these levels.

Currently percentage levels are statically set to 1, 2, 3, 5, 7, 10, & 20% levels below the All-Time High.

*Not financial advice but in my opinion the current percentage levels set (see above) are best used for ETF's and Large Cap Stocks.

FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion

Components

• Directional Liquidity Pulse DLP. Measures signed participation from body and wick imbalance scaled by normalized volume and variance stabilized

• Volatility Curvature. Second difference of realized volatility from returns highlights expansion or compression

• Impact Efficiency. Price change per unit range and volume boosts gain during efficient moves

• Energy score. Z scores of the above form a single energy that controls the state gain

• One bar projection. Current slope extended by one bar for anticipatory checks

Fusion rule

Weighted sum inside the energy score then logistic mapping to a gain between k min and k max. The state updates toward price plus a small flow push.

Signal rule

• Long suggestion and order when close is below trend and the one bar projection is above the trend

• Short suggestion and flip when close is above trend and the one bar projection is below the trend

• WAIT is implicit when neither condition holds

• In position states end on the opposite condition

What you will see on the chart

• Colored trendline teal for rising red for falling gray for flat

• Optional projection line one bar ahead

• Optional background can be enabled in code

• Alerts on price cross and on slope flips

Inputs with guidance

Setup

• Price source. Close by default

Logic

• Flow window. Typical range 20 to 80. Higher smooths the pulse and reduces flips

• Vol window. Typical range 30 to 120. Higher calms curvature

• Energy window. Typical range 20 to 80. Higher slows regime changes

• Min gain and Max gain. Raise max to react faster. Raise min to keep momentum in chop

UI

• Show 1 bar projection. Colors for up down flat

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• Commission percent 0.03

• Slippage 5

• Default order size method percent of equity value 3%

• Pyramiding 0

• Process orders on close off

• Calc on every tick off

• Recalculate after order is filled off

Realism and responsible publication

• No performance claims

• Intrabar reminder. Shapes can move while a bar forms and settle on close

• Strategy uses standard candles only

Honest limitations and failure modes

• Sudden gaps and thin liquidity can still produce fast flips

• Very quiet regimes reduce contrast. Use larger windows and lower max gain

• Session time uses the exchange time of the chart if you enable any windows later

• Past results never guarantee future outcomes

Open source reuse and credits

• None

SOXL Trend Surge v3.0.2 – Profit-Only RunnerSOXL Trend Surge v3.0.2 – Profit-Only Runner

This is a trend-following strategy built for leveraged ETFs like SOXL, designed to ride high-momentum waves with minimal interference. Unlike most short-term scalping scripts, this model allows trades to develop over multiple days to even several months, capitalizing on the full power of extended directional moves — all without using a stop-loss.

🔍 How It Works

Entry Logic:

Price is above the 200 EMA (long-term trend confirmation)

Supertrend is bullish (momentum confirmation)

ATR is rising (volatility expansion)

Volume is above its 20-bar average (liquidity filter)

Price is outside a small buffer zone from the 200 EMA (to avoid whipsaws)

Trades are restricted to market hours only (9 AM to 2 PM EST)

Cooldown of 15 bars after each exit to prevent overtrading

Exit Strategy:

Takes partial profit at +2× ATR if held for at least 2 bars

Rides the remaining position with a trailing stop at 1.5× ATR

No hard stop-loss — giving space for volatile pullbacks

⚙️ Strategy Settings

Initial Capital: $500

Risk per Trade: 100% of equity (fully allocated per entry)

Commission: 0.1%

Slippage: 1 tick

Recalculate after order is filled

Fill orders on bar close

Timeframe Optimized For: 45-minute chart

These parameters simulate an aggressive, high-volatility trading model meant for forward-testing compounding potential under realistic trading costs.

✅ What Makes This Unique

No stop-loss = fewer premature exits

Partial profit-taking helps lock in early wins

Trailing logic gives room to ride large multi-week moves

Uses strict filters (volume, ATR, EMA bias) to enter only during high-probability windows

Ideal for leveraged ETF swing or position traders looking to hold longer than the typical intraday or 2–3 day strategies

⚠️ Important Note

This is a high-risk, high-reward strategy meant for educational and testing purposes. Without a stop-loss, trades can experience deep drawdowns that may take weeks or even months to recover. Always test thoroughly and adjust position sizing to suit your risk tolerance. Past results do not guarantee future returns. Backtest range: May 8, 2020 – May 23, 2025

Daily BreadWhat it does:

This script uses specific multiple true ranges from a 30 EMA baseline to plot lines that represent 10% buying increments. Although the common period for ATR is 14, this script employs a period of 20 for smoothing that I have determined is more effective when used with a daily candle chart. It includes onscreen trend signals to identify an uptrend or downtrend when the 50 EMA crosses the 90 EMA and will also display a coloured directional signal at each candle beyond an EMA cross to identify the current trend.

The script plots a scale of percentage labels at the end of each line to identify the percent of an account intended to be in short or longer term trades.

How it does it:

The script uses a 30 EMA baseline and then multiplies ATR increments of +1, +2, +4 and -1 through -7. These ATR multiples and the EMA are plotted as 11 lines, 10 of which make up the range of 10% increments from 10% to 100% with the 11th line being the High Band representing the extreme high or expected sale of any holdings. The percentage label scale uses variable declarations to position and colour match a percentage label to each line.

Intended use:

It is intended to be used for short term trading or long term investing with a daily market index chart such as SPY and multiple exchange traded funds that track said market index. A different ETF is purchased when a daily SPY candle reaches a lower buy band using 10% of a total account value. The sale of any ETFs is at the discretion of the trader and dependent on investment strategy (short term trading or long term inventing) and the trend. When short term trading in a downtrend or when daily candles are below the 50 EMA, selling would be done every 2 to 3 bands above a buy to mitigate the risk of a significant portion of an account getting caught in a downtrend. In an uptrend the High Band would be used to sell any holdings.

RightFlow Universal Volume Profile - Any Market Any TimeframeSummary in one paragraph

RightFlow is a right anchored microstructure volume profile for stocks, futures, FX, and liquid crypto on intraday and daily timeframes. It acts only when several conditions align inside a session window and presents the result as a compact right side profile with value area, POC, a bull bear mix by price bin, and a HUD of profile VWAP and pressure shares. It is original because it distributes each bar’s weight into multiple mid price slices, blends bull bear pressure per bin with a CLV based split, and grows the profile to the right so price action stays readable. Add to a clean chart, read the table, and use the visuals. For conservative workflows read on bar close.

Scope and intent

• Markets. Major FX pairs, index futures, large cap equities and ETFs, liquid crypto.

• Timeframes. One minute to daily.

• Default demo used in the publication. SPY on 15 minute.

• Purpose. See where participation concentrates, which side dominated by price level, and how far price sits from VA and POC.

Originality and usefulness

• Unique fusion. Right anchored growth plus per bar slicing and CLV split, with weight modes Raw, Notional, and DeltaProxy.

• Failure mode addressed. False reads from single bar direction and coarse binning.

• Testability. All parts sit in Inputs and the HUD.

• Portable yardstick. Value Area percent and POC are universal across symbols.

• Protected scripts. Not applicable. Method and use are fully disclosed.

Method overview in plain language

Pick a scope Rolling or Today or This Week. Define a window and number of price bins. For each bar, split its range into small slices, assign each slice a weight from the selected mode, and split that weight by CLV or by bar direction. Accumulate totals per bin. Find the bin with the highest total as POC. Expand left and right until the chosen share of total volume is covered to form the value area. Compute profile VWAP for all, buyers, and sellers and show them with pressure shares.

Base measures

Range basis. High minus low and mid price samples across the bar window.

Return basis. Not used. VWAP trio is price weighted by weights.

Components

• RightFlow Bins. Price histogram that grows to the right.

• Bull Bear Split. CLV based 0 to 1 share or pure bar direction.

• Weight Mode. Raw volume, notional volume times close, or DeltaProxy focus.

• Value Area Engine. POC then outward expansion to target share.

• HUD. Profile VWAP, Buy and Sell percent, winner delta, split and weight mode.

• Session windows optional. Scope resets on day or week.

Fusion rule

Color of each bin is the convex blend of bull and bear shares. Value area shading is lighter inside and darker outside.

Signal rule

This is context, not a trade signal. A strong separation between buy and sell percent with price holding inside VA often confirms balance. Price outside VA with skewed pressure often marks initiative moves.

What you will see on the chart

• Right side bins with blended colors.

• A POC line across the profile width.

• Labels for POC, VAH, and VAL.

• A compact HUD table in the top right.

Table fields and quick reading guide

• VWAP. Profile VWAP.

• Buy and Sell. Pressure shares in percent.

• Delta Winner. Winner side and margin in percent.

• Split and Weight. The active modes.

Reading tip. When Session scope is Today or This Week and Buy minus Sell is clearly positive or negative, that side often controls the day’s narrative.

Inputs with guidance

Setup

• Profile scope. Rolling or session reset. Rolling uses window bars.

• Rolling window bars. Typical 100 to 300. Larger is smoother.

Binning

• Price bins. Typical 32 to 128. More bins increase detail.

• Slices per bar. Typical 3 to 7. Raising it smooths distribution.

Weighting

• Weight mode. Raw, Notional, DeltaProxy. Notional emphasizes expensive prints.

• Bull Bear split. CLV or BarDir. CLV is more nuanced.

• Value Area percent. Typical 68 to 75.

View

• Profile width in bars, color split toggle, value area shading, opacities, POC line, VA labels.

Usage recipes

Intraday trend focus

• Scope Today, bins 64, slices 5, Value Area 70.

• Split CLV, Weight Notional.

Intraday mean reversion

• Scope Today, bins 96, Value Area 75.

• Watch fades back to POC after initiative pushes.

Swing continuation

• Scope Rolling 200 bars, bins 48.

• Use Buy Sell skew with price relative to VA.

Realism and responsible publication

No performance claims. Shapes can move while a bar forms and settle on close. Education only.

Honest limitations and failure modes

Thin liquidity and data gaps can distort bin weights. Very quiet regimes reduce contrast. Session time is the chart venue time.

Open source reuse and credits

None.

Legal

Education and research only. Not investment advice. Test on history and simulation before live use.

[SHORT ONLY] 10 Bar Low Pullback█ STRATEGY DESCRIPTION

The "10 Bar Low Pullback" strategy is a contrarian short trading system designed to capture pullbacks after a new 10‐bar low is made. it identifies a potential short opportunity when the current bar’s low breaks below the lowest low of the previous 10 bars, provided that the bar exhibits strong internal momentum as measured by its IBS value. An optional trend filter further refines entries by requiring that the close is below a 200-period EMA.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

ibs = (close - low) / (high - low)

- Low IBS (≤ 0.2): Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8): Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current bar’s low is below the lowest low of the past X bars (default: 10).

The bar’s IBS is greater than the specified threshold (default: 0.85).

The signal occurs within the defined trading window (between Start Time and End Time).

If the EMA Filter is enabled, the close must be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

Lookback Period: Defines the number of bars (default is 10) over which the lowest low is calculated.

IBS Threshold: Sets the minimum required IBS value (default is 0.85) to qualify as a pullback.

Trading Window: Trades are only executed between the user-defined Start Time and End Time.

EMA Filter (Optional): When enabled, short entries are only considered if the current close is below the 200-period EMA, with the EMA period being adjustable (default is 200).

█ PERFORMANCE OVERVIEW

Designed for shorting opportunities, this strategy aims to capture pullbacks following an aggressive 10-bar low break.

It leverages a combination of a lookback low and IBS measurement to identify overextended bullish moves that may revert.

The optional EMA filter helps confirm a bearish market environment by ensuring the price remains under the trend line.

Suitable for use on various assets, including stocks and ETFs, on daily or similar timeframes.

Backtesting and parameter optimization are recommended to tailor the strategy to specific market conditions.

[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.