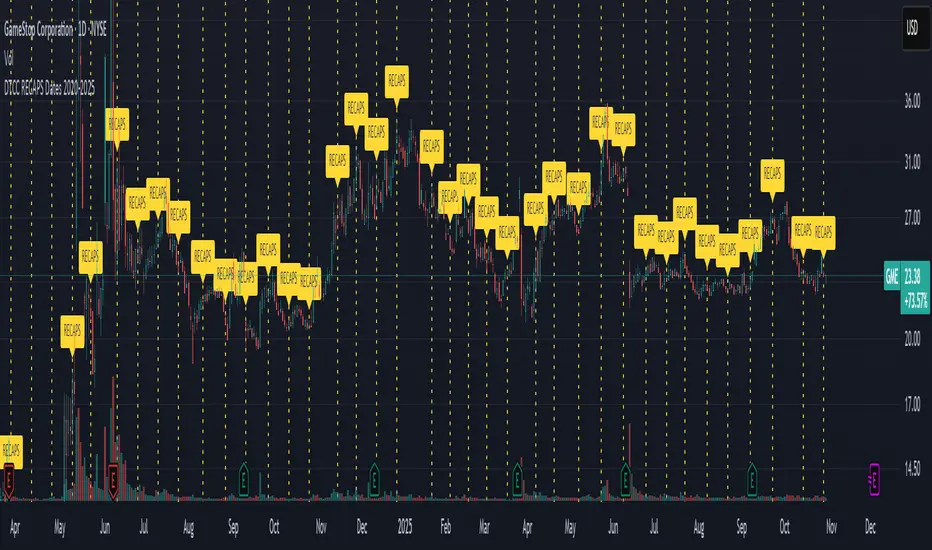

DTCC RECAPS Dates 2020-2025This is a simple indicator which marks the RECAPS dates of the DTCC, during the periods of 2020 to 2025.

These dates have marked clear settlement squeezes in the past, such as GME's squeeze of January 2021.

------------------------------------------------------------------------------------------------------------------

The Depository Trust & Clearing Corporation (DTCC) has published the 2025 schedule for its Reconfirmation and Re-pricing Service (RECAPS) through the National Securities Clearing Corporation (NSCC). RECAPS is a monthly process for comparing and re-pricing eligible equities, municipals, corporate bonds, and Unit Investment Trusts (UITs) that have aged two business days or more .

At its core, the Reconfirmation and Re-pricing Service (RECAPS) is a risk management tool used by the National Securities Clearing Corporation (NSCC), a subsidiary of the DTCC. Its primary purpose is to reduce the risks associated with aged, unsettled trades in the U.S. securities market .

When a trade is executed, it is sent to the NSCC for clearing and settlement. However, for various reasons, some trades may not settle on their scheduled date and become "aged." These unsettled trades create risk for both the trading parties and the clearinghouse (NSCC) because the value of the underlying securities can change over time. If a trade fails to settle and one of the parties defaults, the NSCC may have to step in to complete the transaction at the current market price, which could result in a loss.

RECAPS mitigates this risk by systematically re-pricing these aged, open trading obligations to the current market value. This process ensures that the financial obligations of the clearing members accurately reflect the present value of the securities, preventing the accumulation of significant, unmanaged market risk .

Detailed Mechanics: How Does it Work?

The RECAPS process revolves around two key dates you asked about: the RECAPS Date and the Settlement Date .

The RECAPS Date: On this day, the NSCC runs a process to identify all eligible trades that have remained unsettled for two business days or more. These "aged" trades are then re-priced to the current market value. This re-pricing is not just a simple recalculation; it generates new settlement instructions. The original, unsettled trade is effectively cancelled and replaced with a new one at the current market price. This is done through the NSCC's Obligation Warehouse.

The Settlement Date: This is typically the business day following the RECAPS date. On this date, the financial settlement of the re-priced trades occurs. The difference in value between the original trade price and the new, re-priced value is settled between the two trading parties. This "mark-to-market" adjustment is processed through the members' settlement accounts at the DTCC.

Essentially, the process ensures that any gains or losses due to price changes in the underlying security are realized and settled periodically, rather than being deferred until the trade is ultimately settled or cancelled.

Are These Dates Used to Check Margin Requirements?

Yes, indirectly, this process is closely tied to managing margin and collateral requirements for NSCC members. Here’s how:

The NSCC requires its members to post collateral to a clearing fund, which acts as a mutualized guarantee against defaults. The amount of collateral each member must provide is calculated based on their potential risk exposure to the clearinghouse.

By re-pricing aged trades to current market values through RECAPS, the NSCC gets a more accurate picture of each member's outstanding obligations and, therefore, their current risk profile. If a member has a large number of unsettled trades that have moved against them in value, the re-pricing will crystallize that loss, which will be settled the next day.

This regular re-pricing and settlement of aged trades prevent the build-up of large, unrealized losses that could increase a member's risk profile beyond what their posted collateral can cover. While RECAPS is not the only mechanism for calculating margin (the NSCC has a complex system for daily margin calls based on overall portfolio risk), it is a crucial component for managing the specific risk posed by aged, unsettled transactions. It ensures that the value of these obligations is kept current, which in turn helps ensure that collateral levels remain adequate.

--------------------------------------------------------------------------------------------------------------

Future dates of 2025:

- November 12, 2025 (Wed)

- November 25, 2025 (Tue)

- December 11, 2025 (Thu)

- December 29, 2025 (Mon)

The dates for 2026 haven't been published yet at this time.

The RECAPS process is essentially the industry's way of retrying the settlement of all unresolved FTDs, netting outstanding obligations, and gradually forcing resolution (either delivery or buy-in). Monitoring RECAPS cycles is one way to track the lifecycle, accumulation, and eventual resolution (or persistence) of failures to deliver in the U.S. market.

The US Stock market has become a game of settlement dates and FTDs, therefore this can be useful to track.

Cari dalam skrip untuk "山子高科2025年一季度财务报告关键指标"

2013-2025 Moon Phases & Mercury RetrogradesIndicator Description: 2013-2025 Moon Phases & Mercury Retrogrades

This Pine Script (version 5) indicator overlays key astrological events on a TradingView chart, specifically tracking full moons, new moons, and Mercury retrograde periods from 2013 to 2025. It is designed to help traders and astrology enthusiasts visualize these celestial events alongside price action, potentially identifying correlations or patterns.

Features:

New Moons:

Visualization: Plotted as small white circles above the price bars.

Data: Includes 156 specific new moon dates from January 11, 2013, to December 20, 2025.

Purpose: Marks the start of the lunar cycle, often associated with new beginnings or shifts in energy.

Full Moons:

Visualization: Plotted as small orange circles above the price bars.

Data: Includes 157 specific full moon dates from January 27, 2013, to December 15, 2025.

Purpose: Highlights the peak of the lunar cycle, often linked to heightened emotions or market volatility in astrological analysis.

Mercury Retrogrades:

Visualization: Displayed as a light red background highlight across the chart.

Data: Covers 39 Mercury retrograde periods, with precise start and end timestamps from February 23, 2013, to November 29, 2025.

Purpose: Indicates periods traditionally associated with communication issues, delays, or reversals, which some traders monitor for potential market impacts.

Technical Details:

Overlay: The indicator is set to overlay=true, meaning it displays directly on the price chart rather than in a separate pane.

Date Matching: Uses a helper function is_date(y, m, d) to check if the current chart date matches any of the predefined event dates, leveraging TradingView's year, month, and dayofmonth variables.

Visualization Methods:

plotshape: Used for new moons (white circles) and full moons (orange circles), positioned above bars for clear visibility.

bgcolor: Used for Mercury retrograde periods, applying a semi-transparent red highlight (transparency level 85) to the background during active retrograde periods.

Time Range: Spans from January 2013 to December 2025, providing a comprehensive 13-year view of these astrological events.

Usage:

Add the script to your TradingView chart to see new moons, full moons, and Mercury retrograde periods overlaid on your chosen symbol and timeframe.

The white and orange circles appear on specific dates, while the red background highlights extend across the duration of each Mercury retrograde period.

Useful for traders incorporating astrology into their analysis or anyone interested in tracking these celestial events alongside financial data.

Notes:

The script assumes accurate date data as provided; users should verify dates against astronomical sources if precision is critical.

The transparency of the Mercury retrograde background can be adjusted by modifying the value in color.new(color.red, 85) (0 = fully opaque, 100 = fully transparent).

Best viewed on daily or higher timeframes for clarity, though it works on any timeframe supported by TradingView.

This indicator provides a visual tool to explore the potential influence of lunar phases and Mercury retrograde periods on market behavior, blending astrology with technical analysis in a clear, customizable format.

Donchian x WMA Crossover (2025 Only, Adjustable TP, Real OHLC)Short Description:

Long-only breakout system that goes long when the Donchian Low crosses up through a Weighted Moving Average, and closes when it crosses back down (with an optional take-profit), restricted to calendar year 2025. All signals use the instrument’s true OHLC data (even on Heikin-Ashi charts), start with 1 000 AUD of capital, and deploy 100 % equity per trade.

Ideal parameters configured for Temple & Webster on ASX 30 minute candles. Adjust parameter to suit however best to download candle interval data and have GPT test the pine script for optimum parameters for your trading symbol.

Detailed Description

1. Strategy Concept

This strategy captures trend-driven breakouts off the bottom of a Donchian channel. By combining the Donchian Low with a WMA filter, it aims to:

Enter when volatility compresses and price breaks above the recent Donchian Low while the longer‐term WMA confirms upward momentum.

Exit when price falls back below that same WMA (i.e. when the Donchian Low crosses back down through WMA), but only if the WMA itself has stopped rising.

Optional Take-Profit: you can specify a profit target in decimal form (e.g. 0.01 = 1 %).

2. Timeframe & Universe

In-sample period: only bars stamped between Jan 1 2025 00:00 UTC and Dec 31 2025 23:59 UTC are considered.

Any resolution (e.g. 30 m, 1 h, D, etc.) is supported—just set your preferred timeframe in the TradingView UI.

3. True-Price Execution

All indicator calculations (Donchian Low, WMA, crossover checks, take-profit) are sourced from the chart’s underlying OHLC via request.security(). This guarantees that:

You can view Heikin-Ashi or other styled candles, but your strategy will execute on the real OHLC bars.

Chart styling never suppresses or distorts your backtest results.

4. Position Sizing & Equity

Initial capital: 1 000 AUD

Size per trade: 100 % of available equity

No pyramiding: one open position at a time

5. Inputs (all exposed in the “Inputs” tab):

Input Default Description

Donchian Length 7 Number of bars to calculate the Donchian channel low

WMA Length 62 Period of the Weighted Moving Average filter

Take Profit (decimal) 0.01 Exit when price ≥ entry × (1 + take_profit_perc)

6. How It Works

Donchian Low: ta.lowest(low, DonchianLength) over the specified look-back.

WMA: ta.wma(close, WMALength) applied to true closes.

Entry: ta.crossover(DonchianLow, WMA) AND barTime ∈ 2025.

Exit:

Cross-down exit: ta.crossunder(DonchianLow, WMA) and WMA is not rising (i.e. momentum has stalled).

Take-profit exit: price ≥ entry × (1 + take_profit_perc).

Calendar exit: barTime falls outside 2025.

7. Usage Notes

After adding to your chart, open the Strategy Tester tab to review performance metrics, list of trades, equity curve, etc.

You can toggle your chart to Heikin-Ashi for visual clarity without affecting execution, thanks to the real-OHLC calls.

2013-2025 EclipsesIndicator Description: 2013-2025 Eclipses

This Pine Script (version 5) indicator overlays solar and lunar eclipse events on a TradingView chart, covering the period from 2013 to 2025. It is designed for traders and astrology enthusiasts who wish to visualize these significant astronomical events alongside price action, potentially identifying correlations with market movements or key turning points.

Features:

Eclipses:

Visualization: Displayed as a semi-transparent aqua background highlight across the chart.

Data: Includes 48 specific eclipse dates (both solar and lunar) from April 25, 2013, to September 21, 2025.

Purpose: Highlights dates of eclipses, which are often considered powerful astrological events associated with sudden changes, revelations, or significant shifts in energy and market sentiment.

Technical Details:

Overlay: The indicator is set to overlay=true, ensuring it displays directly on the price chart rather than in a separate pane.

Date Matching: Utilizes a helper function is_date(y, m, d) to determine if the current chart date matches any of the predefined eclipse dates, using TradingView's year, month, and dayofmonth variables.

Visualization Method:

bgcolor: Applies a light aqua background (using color.new(color.aqua, 85)) on the specific dates of eclipses. The transparency level of 85 allows price action to remain visible through the highlight.

Time Range: Spans from April 2013 to September 2025, covering a 12+ year period of eclipse events.

Usage:

Add the script to your TradingView chart to see eclipse dates highlighted with an aqua background on your chosen symbol and timeframe.

The background highlight appears only on the exact dates of eclipses, making it easy to spot these events amidst price data.

Ideal for those incorporating astrological analysis into trading or studying the potential impact of eclipses on financial markets.

Notes:

The script uses a single-line definition for eclipse_dates to ensure compatibility with Pine Script v5 syntax and avoid line continuation errors.

The aqua color matches the original circle-based visualization, with transparency adjustable via the color.new(color.aqua, 85) parameter (0 = fully opaque, 100 = fully transparent).

Works best on daily or higher timeframes for clear visibility of individual eclipse dates, though it functions on any TradingView-supported timeframe.

Eclipse dates should be cross-checked with astronomical sources for critical applications, as the script relies on the provided data accuracy.

Purpose:

This indicator provides a straightforward way to track eclipses over a 12-year period, offering a visual representation of these potent celestial events. By using a background highlight instead of markers, it maintains chart clarity while emphasizing the specific days when eclipses occur, potentially aiding in the analysis of their influence on market behavior or personal trading strategies.

[ADDYad] Google Search Trends - Bitcoin (2012 Jan - 2025 Jan)This Pine Script shows the Google Search Trends as an indicator for Bitcoin from January 2012 to January 2025, based on monthly data retrieved from Google Trends. It calculates and displays the relative search interest for Bitcoin over time, offering a historical perspective on its popularity mainly built for BITSTAMP:BTCUSD .

Important note: This is not a live indicator. It visualizes historical search trends based on Google Trends data.

Key Features:

Data Source : Google Trends (Last retrieved in January 10 2025).

Timeframe : The script is designed to be used on a monthly chart, with the data reflecting monthly search trends from January 2012 to January 2025. For other timeframes, the data is linearly interpolated to estimate the trends at finer resolutions.

Purpose : This indicator helps visualize Bitcoin's search interest over the years, offering insights into public interest and sentiment during specific periods (e.g., major price movements or news events).

Data Handling : The data is interpolated for use on non-monthly timeframes, allowing you to view search trends on any chart timeframe. This makes it versatile for use in longer-term analysis or shorter timeframes, despite the raw data being available only on a monthly basis. However, it is most relevant for Monthly, Weekly, and Daily timeframes.

How It Works:

The script calculates the number of months elapsed since January 1, 2012, and uses this to interpolate Google Trends data values for any given point in time on the chart.

The linear interpolation function adjusts the monthly data to provide an approximate trend for intermediate months.

Why It's Useful:

Track Bitcoin's historic search trends to understand how interest in Bitcoin evolved over time, potentially correlating with price movements.

Correlate search trends with price action and other market indicators to analyze the effects of public sentiment and sentiment-driven market momentum.

Final Notes:

This script is unique because it shows real-world, non-financial dataset (Google Trends) to understand price action of Bitcoin correlating with public interest. Hopefully is a valuable addition to the TradingView community.

ADDYad

Monthly Options Expiration 2025Monthly Options Expiration 2025

Plots the monthly options expiration dates in advance for the year 2025.

Happy trading and all the best.

FOMC Fund Rate 2022–2025(0.1)This indicator visualizes the Federal Open Market Committee (FOMC) meetings from 2022 through 2025.

It plots vertical lines on the announcement dates and attaches labels showing:

The decision (rate hike ⭡, cut ⭣, or hold ⭤).

The size of the rate change in percentage points.

The cumulative Federal Funds Rate path in parentheses.

Features:

Accurate timestamps for each FOMC meeting (UTC+1).

Customizable line style, width, and color.

Label color and text color options.

Placeholder labels for future meetings to maintain the timeline.

Use this script to keep track of historical Fed policy decisions and visualize the rate path over time directly on your chart.

Maancyclus Volatiliteitsindicator (2025)This Moon Cycle Volatility Indicator for TradingView is designed to help traders track and analyze market volatility around specific lunar phases, namely the Full Moon and New Moon. The indicator marks the dates of these moon phases on the chart and measures volatility using the Average True Range (ATR) indicator, which gauges market price fluctuations.

Key Features:

Moon Phase Markers: The indicator marks the Full Moon and New Moon on the chart using labels. Blue labels are placed below bars for Full Moons, while red labels are placed above bars for New Moons. These markers are based on a manually curated list of moon phase dates for the year 2025.

Volatility Calculation: The indicator calculates market volatility using the ATR (14), which provides a sense of market movement and potential risk. Volatility is plotted as histograms, with blue histograms representing volatility around Full Moons and red histograms around New Moons.

Comparative Analysis: By comparing the volatility around these moon phases to the average volatility, traders can spot potential patterns or heightened market movements. This can inform trading strategies, such as anticipating increased market activity around specific lunar events.

In essence, this tool helps traders identify potential high-volatility periods tied to lunar cycles, which could impact market sentiment and price action.

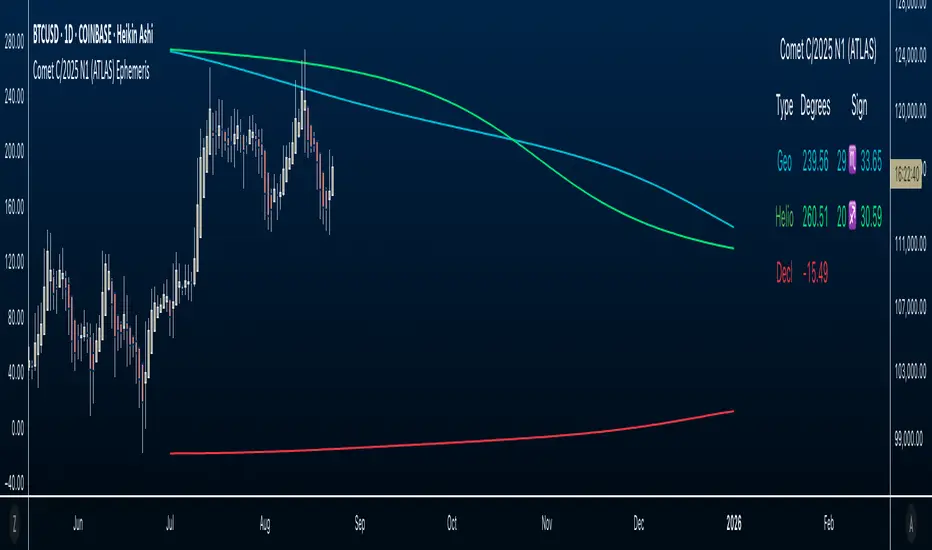

Comet C/2025 N1 (ATLAS) Ephemeris☄️ Ephemeris How-To: Plot JPL Horizons Data on TradingView (Educational)

Overview

This open-source Pine Script™ v6 indicator demonstrates how to bring external astronomical ephemeris into TradingView and plot it on a daily chart. Using Comet C/2025 N1 (ATLAS) as an example dataset, it shows the mechanics of structuring arrays, indexing by date, and drawing past and forward ( future projections ) values—strictly as an educational visualization of celestial motion.

Why This Approach

Data is generated from NASA JPL Horizons, a mission-grade, publicly available ephemeris service ( (ssd.jpl.nasa.gov)). On the daily timeframe, Horizons provides high-precision positions you can regenerate whenever solutions update—useful for educational accuracy in exploring orbital data.

What’s Plotted

- Geocentric ecliptic longitude (Earth-view)

- Heliocentric ecliptic longitude (Sun-centered)

- Declination (deg from celestial equator)

Features

- Simple arrays + date indexing (no per-row timestamps)

- Circles for historical/current bars; polylines to connect forward points, emphasizing future projections

- Toggle any series on/off via inputs

- Daily timeframe enforced (runtime error if not 1D)

- Optional table with zodiac conversion (AstroLib by BarefootJoey)

Data & Updates

The example arrays span 2025-07-01 (discovery date) → 2026-01-01. You can refresh them anytime from JPL Horizons (Observer: Geocentric; daily step; include ecliptic lon/lat and declination) and paste the new values into the script.

How we pulled the ephemeris from JPL Horizons (quick guide):

0) Open ssd.jpl.nasa.gov System

1. Ephemeris Type: Observer Table

2. Target Body: C/2025 N1 (ATLAS) (or any object you want)

3. Observer Location: Geocentric

4. Time Specification: set Start, Stop, Step = 1 day

5. Table Settings → Quantities:

* Astrometric RA & Dec

* Heliocentric ecliptic longitude & latitude

* Observer (geocentric) ecliptic longitude & latitude

6. Additional Table Settings:

* Calendar format: Gregorian

* Date/Time: calendar (UTC), Hours & Minutes (HH:MM)

* Angle format: Decimal degrees

* Refraction model: No refraction / airless

* Range units: Astronomical units (au)

7. Generate → Download results (CSV or text).

8. Use AI or a small script to parse columns (e.g., Obs ecliptic lon, Helio ecliptic lon, Declination) into arrays, then paste them into your Pine script.

Educational Note

This indicator’s goal is to show how to prepare and plot ephemeris—so you can adapt the method for other comets or celestial bodies, or swap in data from existing astro libraries, for learning about astronomical projections using JPL daily data.

Credits & License

- Ephemeris: Solar System Dynamics Group, Horizons On-Line Ephemeris System, 4800 Oak Grove Drive, Jet Propulsion Laboratory, Pasadena, CA 91109, USA.

- Zodiac conversion: AstroLib by BarefootJoey

- License: MIT

- For educational use only.

MERRY CHRISTMAS HAPPY 2025 Year [TradingFinder]🎅🎄✨ Merry Christmas and Happy New Year 2025! 🎉✨

As we bid farewell to 2024 and welcome the fresh opportunities of 2025, we want to send our warmest wishes to all the amazing TradingView users, Pine Script developers, and loyal followers of TradingFinder.

Your enthusiasm and support have made this community stronger and more inspiring every day. May this holiday season bring you happiness, success, and prosperity both in life and in trading.

We also wish for all of you to make great profits and achieve your financial goals in the new year. Let's make 2025 a year filled with innovation, growth, and great achievements together.

Thank you for being part of this journey! 🎅🌟📈

Sun Moon Conjunctions Trine Oppositions 2025this script is an astrological tool designed to overlay significant Sun-Moon aspect events for 2025 on a Bitcoin chart. It highlights key lunar phases and aspects—Conjunctions (New Moon) in blue, Squares in red, Oppositions (Full Moon) in purple, and Trines in green—using background colors and labeled markers. Users can toggle visibility for each aspect type and adjust label sizes via customizable inputs. The script accurately marks events from January through December 2025, with labels appearing once per event, making it a valuable resource for exploring potential correlations between lunar cycles and Bitcoin price movements.

SPX Year-End 2025 Targets by AnalystsJust year end analyst targets for SPX as of 02 October 2025, as answered by Grok

WorldCup Dashboard + Institutional Sessions© 2025 NewMeta™ — Educational use only.

# Full, Premium Description

## WorldCup Dashboard + Institutional Sessions

**A trade-ready, intraday framework that combines market structure, real flow, and institutional timing.**

This toolkit fuses **Institutional Sessions** with a **price–volume decision engine** so you can see *who is active*, *where value sits*, and *whether the drive is real*. You get: **CVD/Delta**, volume-weighted **Momentum**, **Aggression** spikes, **FVG (MTF)** with nearest side, **Daily Volume Profile (VAH/POC/VAL)**, **ATR regime**, a **24h position gauge**, classic **candle patterns**, IBH/IBL + **first-hour “true close”** lines, and a **10-vote confluence scoreboard**—all in one view.

---

## What’s inside (and how to trade it)

### 🌍 Institutional Sessions (Sydney • Tokyo • London • New York)

* Session boxes + a highlighted **first hour**.

* Plots the **true close** (first-hour close) as a running line with a label.

**Use:** Many desks anchor risk to this print. Above = bullish bias; below = bearish. **IBH/IBL** breaks during London/NY carry the most signal.

### 📊 CVD / Delta (Flow)

* Net buyer vs seller pressure with smooth trend state.

**Use:** **Rising CVD + acceptance above mid/POC** confirms continuation. Bearish price + rising CVD = caution (possible absorption).

### ⚡ Volume-Weighted Momentum

* Momentum adjusted by participation quality (volume).

**Use:** Momentum>MA and >0 → trend drive is “real”; <0 and falling → distribution risk.

### 🔥 Aggression Detector

* ROC × normalized volume × wick factor to flag **forceful** candles.

**Use:** On spikes, avoid fading blindly—wait for pullbacks into **aligned FVG** or for aggression to cool.

### 🟦🟪 Fair Value Gaps (with MTF)

* Detects up to 3 recent FVGs and marks the **nearest** side to price.

**Use:** Trend pullbacks into **bullish FVG** for longs; bounces into **bearish FVG** for shorts. Optional threshold to filter weak gaps.

### 🧭 24h Gauge (positioning)

* Shows current price across the 24h low⇢high with a mid reference.

**Use:** Above mid and pushing upper third = momentum continuation setups; below mid = sell the rips bias.

### 🧱 Daily Volume Profile (manual per day)

* **VAH / POC / VAL** derived from discretized rows.

**Use:** **POC below** supports longs; **POC above** caps rallies. Fade VAH/VAL in ranges; treat them as break/hold levels in trends.

### 📈 ATR Regime

* **ATR vs ATR-avg** with direction and regime flag (**HIGH / NORMAL / LOW**).

**Use:** HIGH ⇒ give trades room & favor trend following. LOW ⇒ fade edges, scale targets.

### 🕯️ Candle Patterns (contextual, not standalone)

* Engulfings, Morning/Evening Star, 3 Soldiers/Crows, Harami, Hammer/Shooting Star, Double Top/Bottom.

**Use:** Only with session + flow + momentum alignment.

### 🤝 Price–Volume Classification

* Labels each bar as **continuation**, **exhaustion**, **distribution**, or **healthy pullback**.

**Use:** Align continuation reads with trend; treat “Price↑ + Vol↓” as a caution flag.

### 🧪 Confluence Scoreboard & B/S Meter

* Ten elements vote: 🔵 bull, ⚪ neutral, 🟣 bear.

**Use:** Execution filter—take setups when the board’s skew matches your trade direction.

---

## Playbooks (actionable)

**Trend Pullback (Long)**

1. London/NY active, Momentum↑, CVD↑, price above 24h mid & POC.

2. Pullback into **nearest bullish FVG**.

3. Invalidate under FVG low or **true-close** line.

4. Targets: IBH → VAH → 24h high.

**Range Fade (Short)**

1. Asia/quiet regime, **Price↑ + Vol↓** into **VAH**, ATR low.

2. Nearest FVG bearish or scoreboard skew bearish.

3. Invalidate above VAH/IBH.

4. Targets: POC → VAL.

**News/Impulse**

Aggression spike? Don’t chase. Let it pull back into the aligned FVG; require CVD/Momentum agreement before entry.

---

## Alerts (included)

* **Bull/Bear Confluence ≥ 7/10**

* **Intraday Target Achieved** / **Daily Target Achieved**

* **Session True-Close Retests** (Sydney/Tokyo/London/NY)

*(Keep alerts “Once per bar” unless you specifically want intrabar triggers.)*

---

## Setup Tips

* **UTC**: Choose the reference that matches how you track sessions (default UTC+2).

* **Volume threshold**: 2.0× is a strong baseline; raise for noisy alts, lower for majors.

* **CVD smoothing**: 14–24 for scalps; 24–34 for slower markets.

* **ATR lengths**: Keep defaults unless your asset has a persistent regime shift.

---

## Why this framework?

Because **timing (sessions)**, **truth (flow)**, and **location (value/FVG)** together beat any single signal. You get *who is trading*, *how strong the push is*, and *where risk lives*—on one screen—so execution is faster and cleaner.

---

**Disclaimer**: Educational use only. Not financial advice. Markets are risky—backtest and size responsibly.

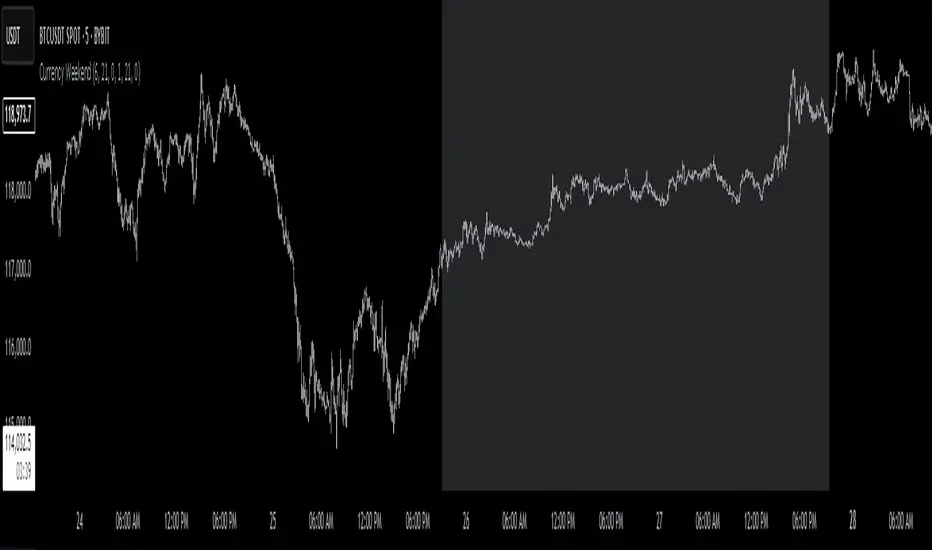

Currency Weekend - shading weekend trading// ─────────────────────────────────────────────────────────────────────────────

// © 2025, Steve / Steven Anthony – "Currency Weekend"

// This script highlights the low-liquidity weekend window that often affects

// both fiat currency markets and cryptocurrencies like Bitcoin.

//

// ╭─────────────────────────────── DESCRIPTION ───────────────────────────────╮

// | This indicator shades a customizable time window on your chart, |

// | originally set to highlight the **forex weekend lull** from |

// | **Friday 21:00 UTC to Sunday 21:00 UTC**, when traditional fiat |

// | currency markets close. |

// | |

// | Traders who observe Bitcoin, Ethereum, or other crypto assets may |

// | notice reduced liquidity or increased erratic moves during this time, |

// | due to overlapping behaviors from professional forex traders who |

// | trade both markets. |

// ╰──────────────────────────────────────────────────────────────────────────╯

//

// 🔧 Flexible Configuration:

// - Define your own start and end **day + time** for shading

// - Useful for shading other custom quiet periods or session transitions

//

// 💡 Use Cases:

// - Avoid trading during low-liquidity periods

// - Spot potential weekend traps or price gaps

// - Align crypto behavior with fiat market hours

//

// 📍 Default Settings:

// - Start: Friday 21:00 UTC

// - End: Sunday 21:00 UTC

//

// Timezone is normalized to the chart’s timezone for seamless integration.

//

// ─────────────────────────────────────────────────────────────────────────────

ITM 2x15// © 2025 Intraday Trading Machine

// This script is open-source. You may use and modify it, but please give credit.

// Colors the current 15-minute candle body green or red if the two previous candles were both bullish or bearish.

This script is designed for traders using the Scalping Intraday Trading Machine technique. It highlights when two consecutive 15-minute candles close in the same direction — either both bullish or both bearish.

For example, if you see two consecutive bearish candles, you might look for a long entry on a break above the high of the first bearish candle. This tool helps you visually identify these setups with clean, directional candle coloring — no clutter.

Yang-Zhang Volatility (YZVol) by CoryP1990 – Quant ToolkitThe Yang-Zhang Volatility (YZVol) estimator measures realized volatility using both overnight gaps and intraday moves. It combines three components: overnight returns, open-to-close returns, and the Rogers–Satchell term, weighted by Zhang’s k to reduce bias.

How to read it

Line color: Green when YZVol is rising (volatility expansion), Red when falling (volatility compression).

Background: Green tint = above High-vol threshold (active regime). Red tint = below Low-vol threshold (quiet regime).

Units: Displays Daily % by default on any timeframe (values are normalized to daily). An optional toggle shows Annualized % (√252 × Daily %).

Typical uses

Spot transitions between quiet and active regimes.

Compare realized vol vs implied vol or a risk-target.

Adapt position sizing to volatility clustering.

Defaults

Length = 20

High-vol threshold = 5% (Daily)

Low-vol threshold = 1% (Daily)

Optional: Annualized % display

Example — SPY (1D)

During the 2020 crash, YZVol surged to 5.8 % per day, capturing the height of pandemic-era volatility before compressing into a calm regime through 2021. Volatility re-expanded in 2022 due to reinflamed COVID fears and gradually stabilized through 2023. A sharp, liquidity-driven volatility event in August 2024 caused another brief YZVol surge, reflecting the historic one-day VIX spike triggered by market-wide risk-off flows and thin pre-market liquidity. A second, policy-driven expansion followed in April–May 2025, coinciding with the renewed U.S.–China tariff conflict and a sharp equity pullback. Since mid-2025, YZVol has settled near 1 % per day, with the red background confirming that realized volatility has once again compressed into a quiet, low-risk regime.

Part of the Quant Toolkit — transparent, open-source indicators for modern quantitative analysis. Built by CoryP1990.

SPX Weekly Expected Moves# SPX Weekly Expected Moves Indicator

A professional Pine Script indicator for TradingView that displays weekly expected move levels for SPX based on real options data, with integrated Fibonacci retracement analysis and intelligent alerting system.

## Overview

This indicator helps options and equity traders visualize weekly expected move ranges for the S&P 500 Index (SPX) by plotting historical and current week expected move boundaries derived from weekly options pricing. Unlike theoretical volatility calculations, this indicator uses actual market-based expected move data that you provide from options platforms.

## Key Features

### 📈 **Expected Move Visualization**

- **Historical Lines**: Display past weeks' expected moves with configurable history (10, 26, or 52 weeks)

- **Current Week Focus**: Highlighted current week with extended lines to present time

- **Friday Close Reference**: Orange baseline showing the previous Friday's close price

- **Timeframe Independent**: Works consistently across all chart timeframes (1m to 1D)

### 🎯 **Fibonacci Integration**

- **Five Fibonacci Levels**: 23.6%, 38.2%, 50%, 61.8%, 76.4% between Friday close and expected move boundaries

- **Color-Coded Levels**:

- Red: 23.6% & 76.4% (outer levels)

- Blue: 38.2% & 61.8% (golden ratio levels)

- Black: 50% (midpoint - most critical level)

- **Current Week Only**: Fibonacci levels shown only for active trading week to reduce clutter

### 📊 **Real-Time Information Table**

- **Current SPX Price**: Live market price

- **Expected Move**: ±EM value for current week

- **Previous Close**: Friday close price (baseline for calculations)

- **100% EM Levels**: Exact upper and lower boundary prices

- **Current Location**: Real-time position within the EM structure (e.g., "Above 38.2% Fib (upper zone)")

### 🚨 **Intelligent Alert System**

- **Zone-Aware Alerts**: Separate alerts for upper and lower zones

- **Key Level Breaches**: Alerts for 23.6% and 76.4% Fibonacci level crossings

- **Bar Close Based**: Alerts trigger on confirmed bar closes, not tick-by-tick

- **Customizable**: Enable/disable alerts through settings

## How It Works

### Data Input Method

The indicator uses a **manual data entry approach** where you input actual expected move values obtained from options platforms:

```pinescript

// Add entries using the options expiration Friday date

map.put(expected_moves, 20250613, 91.244) // Week ending June 13, 2025

map.put(expected_moves, 20250620, 95.150) // Week ending June 20, 2025

```

### Weekly Structure

- **Monday 9:30 AM ET**: Week begins

- **Friday 4:00 PM ET**: Week ends

- **Lines Extend**: From Monday open to Friday close (historical) or current time + 5 bars (current week)

- **Timezone Handling**: Uses "America/New_York" for proper DST handling

### Calculation Logic

1. **Base Price**: Previous Friday's SPX close price

2. **Expected Move**: Market-derived ±EM value from weekly options

3. **Upper Boundary**: Friday Close + Expected Move

4. **Lower Boundary**: Friday Close - Expected Move

5. **Fibonacci Levels**: Proportional levels between Friday close and EM boundaries

## Setup Instructions

### 1. Data Collection

Obtain weekly expected move values from options platforms such as:

- **ThinkOrSwim**: Use thinkBack feature to look up weekly expected moves

- **Tastyworks**: Check weekly options expected move data

- **CBOE**: Reference SPX weekly options data

- **Manual Calculation**: (ATM Call Premium + ATM Put Premium) × 0.85

### 2. Data Entry

After each Friday close, update the indicator with the next week's expected move:

```pinescript

// Example: On Friday June 7, 2025, add data for week ending June 13

map.put(expected_moves, 20250613, 91.244) // Actual EM value from your platform

```

### 3. Configuration

Customize the indicator through the settings panel:

#### Visual Settings

- **Show Current Week EM**: Toggle current week display

- **Show Past Weeks**: Toggle historical weeks display

- **Max Weeks History**: Choose 10, 26, or 52 weeks of history

- **Show Fibonacci Levels**: Toggle Fibonacci retracement levels

- **Label Controls**: Customize which labels to display

#### Colors

- **Current Week EM**: Default yellow for active week

- **Past Weeks EM**: Default gray for historical weeks

- **Friday Close**: Default orange for baseline

- **Fibonacci Levels**: Customizable colors for each level type

#### Alerts

- **Enable EM Breach Alerts**: Master toggle for all alerts

- **Specific Alerts**: Four alert types for Fibonacci level breaches

## Trading Applications

### Options Trading

- **Straddle/Strangle Positioning**: Visualize breakeven levels for neutral strategies

- **Directional Plays**: Assess probability of reaching target levels

- **Earnings Plays**: Compare actual vs. expected move outcomes

### Equity Trading

- **Support/Resistance**: Use EM boundaries and Fibonacci levels as key levels

- **Breakout Trading**: Monitor for moves beyond expected ranges

- **Mean Reversion**: Look for reversals at extreme Fibonacci levels

### Risk Management

- **Position Sizing**: Gauge likely price ranges for the week

- **Stop Placement**: Use Fibonacci levels for logical stop locations

- **Profit Targets**: Set targets based on EM structure probabilities

## Technical Implementation

### Performance Features

- **Memory Managed**: Configurable history limits prevent memory issues

- **Timeframe Independent**: Uses timestamp-based calculations for consistency

- **Object Management**: Automatic cleanup of drawing objects prevents duplicates

- **Error Handling**: Robust bounds checking and NA value handling

### Pine Script Best Practices

- **v6 Compliance**: Uses latest Pine Script version features

- **User Defined Types**: Structured data management with WeeklyEM type

- **Efficient Drawing**: Smart line/label creation and deletion

- **Professional Standards**: Clean code organization and comprehensive documentation

## Customization Guide

### Adding New Weeks

```pinescript

// Add after market close each Friday

map.put(expected_moves, YYYYMMDD, EM_VALUE)

```

### Color Schemes

Customize colors for different trading styles:

- **Dark Theme**: Use bright colors for visibility

- **Light Theme**: Use contrasting dark colors

- **Minimalist**: Use single color with transparency

### Label Management

Control label density:

- **Show Current Week Labels Only**: Reduce clutter for active trading

- **Show All Labels**: Full information for analysis

- **Selective Display**: Choose specific label types

## Troubleshooting

### Common Issues

1. **No Lines Appearing**: Check that expected move data is entered for current/recent weeks

2. **Wrong Time Display**: Ensure "America/New_York" timezone is properly handled

3. **Duplicate Lines**: Restart indicator if drawing objects appear duplicated

4. **Missing Fibonacci Levels**: Verify "Show Fibonacci Levels" is enabled

### Data Validation

- **Expected Move Format**: Use positive numbers (e.g., 91.244, not ±91.244)

- **Date Format**: Use YYYYMMDD format (e.g., 20250613)

- **Reasonable Values**: Verify EM values are realistic (typically 50-200 for SPX)

## Version History

### Current Version

- **Pine Script v6**: Latest version compatibility

- **Fibonacci Integration**: Five-level retracement analysis

- **Zone-Aware Alerts**: Upper/lower zone differentiation

- **Dynamic Line Management**: Smart current week extension

- **Professional UI**: Comprehensive information table

### Future Enhancements

- **Multiple Symbols**: Extend beyond SPX to other indices

- **Automated Data**: Integration with options data APIs

- **Statistical Analysis**: Success rate tracking for EM predictions

- **Additional Levels**: Custom percentage levels beyond Fibonacci

## License & Usage

This indicator is designed for educational and trading purposes. Users are responsible for:

- **Data Accuracy**: Ensuring correct expected move values

- **Risk Management**: Proper position sizing and risk controls

- **Market Understanding**: Comprehending options-based expected move concepts

## Support

For questions, issues, or feature requests related to this indicator, please refer to the code comments and documentation within the Pine Script file.

---

**Disclaimer**: This indicator is for informational purposes only. Trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results.

H2-25 cuts (bp)This custom TradingView indicator tracks and visualizes the implied pricing of Federal Reserve rate cuts in the market, specifically for the second half of 2025. It does so by comparing the price differences between two specific Fed funds futures contracts: one for June 2025 and one for December 2025. These contracts are traded on the Chicago Board of Trade (CBOT) and are a widely-used market gauge of the expected path of U.S. interest rates.

The indicator calculates the difference between the implied rates for June and December 2025, and then multiplies the result by 100 to express it in basis points (bps). Each 0.01 change in the spread corresponds to a 1-basis point change in expectations for future rate cuts. A positive value indicates that the market is pricing in a higher likelihood of one or more rate cuts in 2025, while a negative value suggests that the market expects the Fed to hold rates steady or even raise them.

The plot represents the difference in implied rate cuts (in basis points) between the two contracts:

June 2025 (ZQM2025): A contract representing the implied Fed funds rate for June 2025.

December 2025 (ZQZ2025): A contract representing the implied Fed funds rate for December 2025.

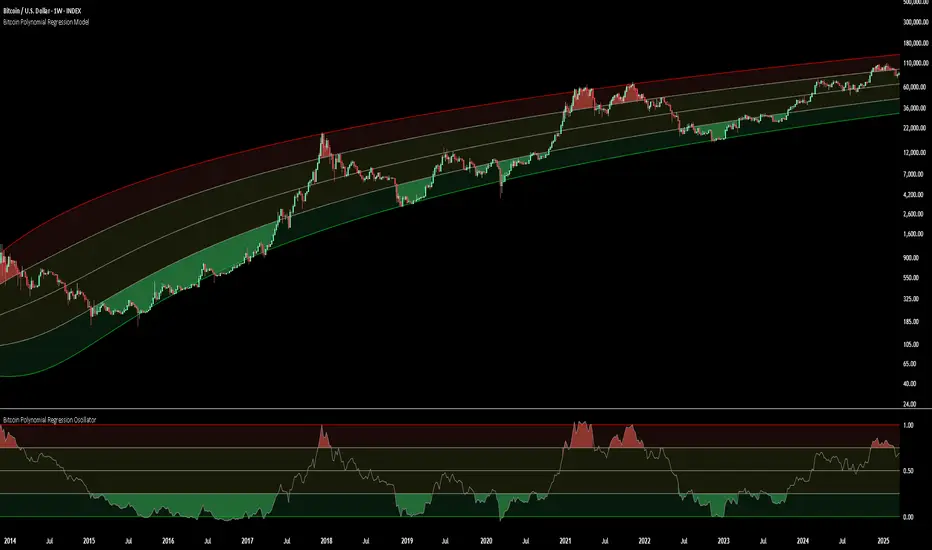

Bitcoin Polynomial Regression ModelThis is the main version of the script. Click here for the Oscillator part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines. The Oscillator version can be found here.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

Bitcoin Polynomial Regression OscillatorThis is the oscillator version of the script. Click here for the other part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

Weekly VwapsThe Weekly Vwaps indicator lets you plot weekly Volume-Weighted Average Price (VWAP) lines for up to six months of your choosing, with years ranging from 2020 to 2050. It’s a focused tool pulled straight from the weekly VWAP section of the Advanced VWAP Calendar indicator, keeping all the same controls and look but expanded to handle more months. You can use it alongside the original indicator if you need extra weekly VWAPs (up to 30 lines total) or run it on its own for a clean, dedicated setup.

How It Works: Six Month Groups: Pick any six months (e.g., Jan 2020, Sep 2025, or Jul 2040) and enable up to five weekly VWAPs per month (W1–W5), starting from Monday midnight.

Default Setup: Loads with September 2025 VWAPs turned on, with other months (August–April 2025) off but ready to enable. All default to 2025.

Customization: Toggle all weeks in a month or pick specific ones. Adjust label sizes (tiny to huge) and line widths (1–5). Colors are teal, fuchsia, red, green, and yellow/orange for weeks 1–5, with clear labels like “W1 Sep 2025 123.45”.

Label Control: A “Show All Labels” switch lets you hide labels to keep your chart tidy.

Intraday Only: Works on intraday timeframes (e.g., 5-minute, 1-hour) for accurate VWAPs.

Why Use It: Add to Advanced VWAP Calendar: If the original’s two-month limit isn’t enough, this adds six more months of weekly VWAPs for deeper analysis.

Standalone Option: Perfect if you only want weekly VWAPs without other features, with flexibility to pick any months and years.

User-Friendly: Ready to go with September 2025 enabled, easy to tweak for past or future data.

Get Started: Add it to your TradingView chart, and September 2025 VWAPs will show up instantly. Adjust months, years, or toggles in the settings to focus on what you need. Test it on intraday charts and use the label toggle to manage clutter. Great for traders wanting precise, customizable weekly VWAPs!

v2.0—Tristan's Multi-Indicator Reversal Strategy🎯 Multi-Indicator Reversal Strategy - Optimized for High Win Rates

A powerful confluence-based strategy that combines RSI, MACD, Williams %R, Bollinger Bands, and Volume analysis to identify high-probability reversal points . Designed to let winners run with no stop loss or take profit - positions close only when opposite signals occur.

Also, the 3 hour timeframe works VERY well—just a lot less trades.

📈 Proven Performance

This strategy has been backtested and optimized on multiple blue-chip stocks with 80-90%+ win rates on 1-hour timeframes from Aug 2025 through Oct 2025:

✅ V (Visa) - Payment processor

✅ MSFT (Microsoft) - Large-cap tech

✅ WMT (Walmart) - Retail leader

✅ IWM (Russell 2000 ETF) - Small-cap index

✅ NOW (ServiceNow) - Enterprise software

✅ WM (Waste Management) - Industrial services

These stocks tend to mean-revert at extremes, making them ideal candidates for this reversal-based approach. I only list these as a way to show you the performance of the script. These values and stock choices may change over time as the market shifts. Keep testing!

🔑 How to Use This Strategy Successfully

Step 1: Apply to Chart

Open your desired stock (V, MSFT, WMT, IWM, NOW, WM recommended)

Set timeframe to 1 Hour

Apply this strategy

Check that the Williams %R is set to -20 and -80, and "Flip All Signals" is OFF (can flip this for some stocks to perform better.)

Step 2: Understand the Signals

🟢 Green Triangle (BUY) Below Candle:

Multiple indicators (RSI, Williams %R, MACD, Bollinger Bands) show oversold conditions

Enter LONG position

Strategy will pyramid up to 10 entries if more buy signals occur

Hold until red triangle appears

🔴 Red Triangle (SELL) Above Candle:

Multiple indicators show overbought conditions

Enter SHORT position (or close existing long)

Strategy will pyramid up to 10 entries if more sell signals occur

Hold until green triangle appears

🟣 Purple Labels (EXIT):

Shows when positions close

Displays count if multiple entries were pyramided (e.g., "Exit Long x5")

Step 3: Let the Strategy Work

Key Success Principles:

✅ Be Patient - Signals don't occur every day, wait for quality setups

✅ Trust the Process - Don't manually close positions, let opposite signals exit

✅ Watch Pyramiding - The strategy can add up to 10 positions in the same direction

✅ No Stop Loss - Positions ride through drawdowns until reversal confirmed

✅ Session Filter - Only trades during NY session (9:30 AM - 4:00 PM ET)

⚙️ Winning Settings (Already Set as Defaults)

INDICATOR SETTINGS:

- RSI Length: 14

- RSI Overbought: 70

- RSI Oversold: 30

- MACD: 12, 26, 9 (standard)

- Williams %R Length: 14

- Williams %R Overbought: -20 ⭐ (check this! And adjust to your liking)

- Williams %R Oversold: -80 ⭐ (check this! And adjust to your liking)

- Bollinger Bands: 20, 2.0

- Volume MA: 20 periods

- Volume Multiplier: 1.5x

SIGNAL REQUIREMENTS:

- Min Indicators Aligned: 2

- Require Divergence: OFF

- Require Volume Spike: OFF

- Require Reversal Candle: OFF

- Flip All Signals: OFF ⭐

RISK MANAGEMENT:

- Use Stop Loss: OFF ⭐⭐⭐

- Use Take Profit: OFF ⭐⭐⭐

- Allow Pyramiding: ON ⭐⭐⭐

- Max Pyramid Entries: 10 ⭐⭐⭐

SESSION FILTER:

- Trade Only NY Session: ON

- NY Session: 9:30 AM - 4:00 PM ET

**⭐ = Critical settings for success**

## 🎓 Strategy Logic Explained

### **How It Works:**

1. **Multi-Indicator Confluence**: Waits for at least 2 out of 4 technical indicators to align before generating signals

2. **Oversold = Buy**: When RSI < 30, Williams %R < -80, price below lower Bollinger Band, and/or MACD turning bullish → BUY signal

3. **Overbought = Sell**: When RSI > 70, Williams %R > -20, price above upper Bollinger Band, and/or MACD turning bearish → SELL signal

4. **Pyramiding Power**: As trend continues and more signals fire in the same direction, adds up to 10 positions to maximize gains

5. **Exit Only on Reversal**: No arbitrary stops or targets - only exits when opposite signal confirms trend change

6. **Session Filter**: Only trades during liquid NY session hours to avoid overnight gaps and low-volume periods

### **Why No Stop Loss Works:**

Traditional reversal strategies fail because they:

- Get stopped out too early during normal volatility

- Miss the actual reversal that happens later

- Cut winners short with tight take profits

This strategy succeeds because it:

- ✅ Rides through temporary noise

- ✅ Captures full reversal moves

- ✅ Uses multiple indicators for confirmation

- ✅ Pyramids into winning positions

- ✅ Only exits when technical picture completely reverses

---

## 📊 Understanding the Display

**Live Indicator Counter (Top Corner / end of current candles):**

Bull: 2/4

Bear: 0/4

(STANDARD)

Shows how many indicators currently align bullish/bearish

"STANDARD" = normal reversal mode (buy oversold, sell overbought)

"FLIPPED" = momentum mode if you toggle that setting

Visual Indicators:

🔵 Blue background = NY session active (trading window)

🟡 Yellow candle tint = Volume spike detected

💎 Aqua diamond = Bullish divergence (price vs RSI)

💎 Fuchsia diamond = Bearish divergence

⚡ Advanced Tips

Optimizing for Different Stocks:

If Win Rate is Low (<50%):

Try toggling "Flip All Signals" to ON (switches to momentum mode)

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Test on different timeframe (4-hour or daily)

If Too Few Signals:

Decrease "Min Indicators Aligned" to 2

Turn OFF all requirement filters

Widen Williams %R bands to -15 and -85

If Too Many False Signals:

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Turn ON "Require Volume Spike"

Reduce Max Pyramid Entries to 5

Stock Selection Guidelines:

Best Suited For:

Large-cap stable stocks (V, MSFT, WMT)

ETFs (IWM, SPY, QQQ)

Stocks with clear support/resistance

Mean-reverting instruments

Avoid:

Ultra low-volume penny stocks

Extremely volatile crypto (try traditional settings first)

Stocks in strong one-directional trends lasting months

🔄 The "Flip All Signals" Feature

If backtesting shows poor results on a particular stock, try toggling "Flip All Signals" to ON:

STANDARD Mode (OFF):

Buy when oversold (reversal strategy)

Sell when overbought

May work best for: V, MSFT, WMT, IWM, NOW, WM

FLIPPED Mode (ON):

Buy when overbought (momentum strategy)

Sell when oversold

May work best for: Strong trending stocks, momentum plays, crypto

Test both modes on your stock to see which performs better!

📱 Alert Setup

Create alerts to notify you of signals:

📊 Performance Expectations

With optimized settings on recommended stocks:

Typical results we are looking for:

Win Rate: 70-90%

Average Winner: 3-5%

Average Loser: 1-3%

Signals Per Week: 1-3 on 1-hour timeframe

Hold Time: Several hours to days

Remember: Past performance doesn't guarantee future results. Always use proper risk management.

Traders Reality Rate Spike Monitor 0.1 betaTraders Reality Rate Spike Monitor

## **Early Warning System for Interest Rate-Driven Market Crashes**

Based on critical market analysis revealing the dangerous correlation between interest rate spikes and major market selloffs, this indicator provides **three-tier alerts** for US 10-Year Treasury yield acceleration.

### **📊 Key Market Intelligence:**

**Historical Precedent:** The 2018 market crash occurred when unrealized bank losses hit $256 billion with interest rates at just 2.5%. **Current unrealized losses have reached $560 billion** - more than double the 2018 levels - while rates sit at 4.5%.

**Critical Vulnerabilities:**

- **$559 billion in tech sector debt** maturing through 2025

- **65% of investment-grade debt** rated BBB (vulnerable to adverse conditions)

- **$9.5 trillion in total debt** requiring refinancing

- Every 1% rate increase costs the economy **$360 billion annually**

### **🚨 Alert System:**

**📊 WATCH (20+ basis points/3 days):** Early positioning signal

**⚠️ WARNING (30+ basis points/3 days):** Prepare for volatility

**🚨 CRITICAL (40+ basis points/3 days):** Historical crash threshold

### **💡 Why This Matters:**

Interest rate spikes historically trigger major market corrections:

- **2018:** 70 basis points spike → 20% S&P 500 crash

- **2025:** Similar pattern led to massive selloffs

- **Current risk:** 2x higher unrealized losses than 2018

### **⚡ Features:**

✅ **Zero chart clutter** - invisible until alerts trigger

✅ **Dynamic calculation** - automatically adjusts to current yield levels

✅ **Multi-timeframe compatibility** - works on any chart timeframe

✅ **Professional alerts** - with actual basis point calculations

### **🎯 Use Case:**

Perfect for traders and investors who understand that **debt refinancing pressure** and **unrealized bank losses** create systemic risks that manifest through interest rate volatility. When rates spike rapidly, leveraged positions unwind and markets crash.

**"Every point costs us $360 billion a year. Think of that."** - This indicator helps you see those critical rate movements before the market does.

---

**Disclaimer:** This indicator is for educational purposes. Past performance does not guarantee future results. Always manage risk appropriately.

---

This description positions your indicator as a **serious professional tool** based on real market analysis rather than just another technical indicator! 🚀