Non Adaptive Moving Average - Quan DaoThis Non-Adaptive Moving Average (NAMA) is my origin work. It came from the issues that I always face when using existing famous MA like EMA or RMA:

- What length should I choose for the MA for this security?

- Is there a length that works for multiple timeframes?

- Is there a length that works for multiple securities in multiple markets?

Choosing the right length for an MA is a tedious and boring work and is very subjective. One day in early 2023, I decided to create a new MA that will not be dependant a lot (non-adaptive) on the length of it, to make my life a little bit easier. The idea came from the formula of EMA and RMA:

ma = alpha * src + (1 - alpha) * ma

in which,

alpha = 1 / length for RMA

alpha = 2 / (length + 1) for EMA

I decided to use a constant alpha for the formula, which happened to be: 1.618 / 100 (i.e., golden ratio / 100)

This NAMA is using the length in the start only, after running for a while the MA value will be the same for every value of its length, which resolves good my 3 questions above.

The application of this NAMA is wide, I think.

- It can be used like a normal MA but you don't have to choose its length anymore.

- It can be used like EMA in DEMA, TEMA (I called it DNAMA, TNAMA)

- It can be used in calculating some famous indicators (RSI, TR, ...) so that these indicators will not be dependant on the length as well

In this example script, I included an EMA (in blue color) as well so that you can see how the EMA changes and NAMA stays the same when changing the value of its Length.

Cari dalam skrip untuk "荣昌生物+2023年收入+利润+研发投入+毛利率+净利率"

Slight Swing Momentum Strategy.Introduction:

The Swing Momentum Strategy is a quantitative trading strategy designed to capture mid-term opportunities in the financial markets by combining swing trading principles with momentum indicators. It utilizes a combination of technical indicators, including moving averages, crossover signals, and volume analysis, to generate buy and sell signals. The strategy aims to identify market trends and capitalize on price momentum for profit generation.

Highlights:

The strategy offers several key highlights that make it unique and potentially attractive to traders:

Swing Trading with Momentum: The strategy combines the principles of swing trading, which aim to capture short-to-medium-term price swings, with momentum indicators that help identify strong price trends and potential breakout opportunities.

Technical Indicator Optimization: The strategy utilizes a selection of optimized technical indicators, including moving averages and crossover signals, to filter out the noise and focus on high-probability trading setups. This optimization enhances the strategy's ability to identify favourable entry and exit points.

Risk Management: The strategy incorporates risk management techniques, such as position sizing based on equity and dynamic stop loss levels, to manage risk exposure and protect capital. This helps to minimize drawdowns and preserve profits.

Buy Condition:

The buy condition in the strategy is determined by a combination of factors, including A1, A2, A3, XG, and weeklySlope. Let's break it down:

A1 Condition: The A1 condition checks for specific price relationships. It verifies that the ratio of the highest price to the closing price is less than 1.03, the ratio of the opening price to the lowest price is less than 1.03, and the ratio of the highest price to the previous day's closing price is greater than 1.06. This condition looks for a specific pattern indicating potential bullish momentum.

A2 Condition: The A2 condition checks for price relationships related to the closing price. It verifies that the ratio of the closing price to the opening price is greater than 1.05 or that the ratio of the closing price to the previous day's closing price is greater than 1.05. This condition looks for signs of upward price movement and momentum.

A3 Condition: The A3 condition focuses on volume. It checks if the current volume crosses above the highest volume over the last 60 periods. This condition aims to identify increased buying interest and potentially confirms the strength of the potential upward price movement.

XG Condition: The XG condition combines the A1 and A2 conditions and checks if they are true for both the current and previous bars. It also verifies that the ratio of the closing price to the 5-period EMA crosses above the 9-period SMA of the same ratio. This condition helps identify potential buy signals when multiple factors align, indicating a strong bullish momentum and potential entry point.

Weekly Trend Factor: The weekly slope condition calculates the slope of the 50-period SMA over a weekly timeframe. It checks if the slope is positive, indicating an overall upward trend on a weekly basis. This condition provides additional confirmation that the stock is in an upward trend.

When all of these conditions align, the buy condition is triggered, indicating a favourable time to enter a long position.

Sell Condition:

The sell condition is relatively straightforward in the strategy:

Sell Signal: The sell condition simply checks if the closing price crosses below the 10-period EMA. When this condition is met, it indicates a potential reversal or weakening of the upward price momentum, and a sell signal is generated.

Backtest Outcome:

The strategy was backtested over the period from January 22nd, 1999 to May 3rd, 2023, using daily candlestick charts for the NASDAQ: NVDA. The strategy used an initial capital of 1,000,000 USD, The order quantity is defined as 10% of the equity. The strategy allows for pyramiding with 1 order, and the transaction fee is set at 0.03% per trade. Here are the key outcomes of the backtest:

Net Profit: 539,595.84 USD, representing a return of 53.96%.

Percent Profitable: 48.82%

Total Closed Trades: 127

Profit Factor: 2.331

Max Drawdown: 68,422.70 USD

Average Trade: 4,248.79 USD

Average Number of Bars in Trades: 11, indicating the average duration of the trades.

Conclusion:

In conclusion, the Swing Momentum Strategy is a quantitative trading approach that combines swing trading principles with momentum indicators to identify and capture mid term trading opportunities. The strategy has demonstrated promising results during backtesting, including a significant net profit and a favourable profit factor.

[5-2-2023] MNQ CALCMNQ Calcultor that takes your stop loss and the prev candles close and shows you how much contracts you can enter for the amount that you're risking.

Optimized Zhaocaijinbao strategyIntroduction:

The Optimized Zhaocaijinbao strategy is a mid and long-term quantitative trading strategy that combines momentum and trend factors. It generates buy and sell signals by using a combination of exponential moving averages, moving averages, volume and slope indicators. It generates buy signals when the stock is above the 35-day moving average, the trading volume is higher than the 20-day moving average, and the stock is in an upward trend on a weekly timeframe."招财进宝" is a Chinese phrase that can be translated to "Attract Wealth and Bring in Treasure" in English. It is a common expression used to wish for good luck and prosperity in various contexts, such as in business or personal finances.

Highlights:

The strategy has several special optimizations that make it unique.

Firstly, the strategy is optimized for T+1 trading in the Chinese stock market and is only suitable for long positions. The optimizations are also applicable to international stock markets.

Secondly, the trend strategy is optimized to only show indicators on the right side and oscillations. This helps to prevent false signals in choppy markets.

Thirdly, the strategy uses a risk factor for dynamic position sizing to ensure position sizes are adjusted according to the current net asset value and risk preferences. This helps to lower drawdown risks.

The strategy has good resilience even without using stop loss modules in backtesting, making it suitable for trading hourly, 2-hourly, and daily K-line charts (depending on the stock being traded). We recommend experimenting with backtesting using SSE 1-hour or 2-hour or daily Kline charts.

Backtesting outcomes:

The strategy was backtested over the period from October 13th, 2005 to April 14th, 2023, using daily candlestick charts for the commodity code SSE:600763, with a currency of CNY and tick size of 0.01. The strategy used an initial capital of 1,000,000 CNY, with order sizes set to 10% equity and a pyramid of 1 order. The strategy also had a Max Position Size of 0.01 and a Risk Factor of 2.

Here is a summary of the performance of the trading strategy:

Total net profit: 288,577.32 CNY, representing a return of 128.86%

Total number of closed trades: 61

Winning trades: 37, representing a win rate of 60.66%

Profit factor: 2.415

Largest losing trade: 222,021.46 CNY, representing a loss of 14.08%

Average trade: 21,124.22 CNY, representing a return of 3.1%

Average holding period for all trades: 12 days

Conclusion:

In conclusion, the Optimized Zhaocaijinbao strategy is a mid and long-term quantitative trading strategy that combines momentum and trend factors. It is suitable for both Chinese stocks and global stocks. While the Optimized Zhaocaijinbao strategy has performed well in backtesting, it is important to note that past performance is not a guarantee of future results. Traders should conduct their own research and analysis and exercise caution when using any trading strategy.

Profiling: array of UDTs vs UDT of arraysUsing Stopwatch Library by PineCoders, I am trying to test which is faster, an array of user-defined type (UDT) objects vs an object with many child arrays.

The task is to store and manipulate array of objects having total 9 values: 4 floats, 4 strings and 1 int.

Option 1: create a UDT with 9 fields and store an array of such UDT objects.

Option 2: create a UDT with 9 arrays individually for each value.

The test task is of three stages:

Populate array(s) with some (timenow) values - in the options you can choose how many values to push into the array/arrays. Note that max size of array(s) is set independently, so you can push 1000 of elements into an array capped at 100 max size and as new elements will be pushed (added to the end) the old exceeding elements will be shifted (removed from the beginning)

Write - write to random elements of the array. Two options for writing to a UDT object: (1) assign to each field independently, (2) create a UDT object and use array.set() function.

Read - read from random elements of the array.

In the options you can how many times per bar to run each of the steps (same number for each step).

I tested by adding three indicators to the chart and choosing different options for each:

1. Array of UDT's where writing is done by creating a new UDT from the values and then using set(udt)

2. Array of UDT's where writing is done by assigning the value of each of the properties of the UDT individually (saving time on creating of a new object).

3. UDT of arrays.

As of 16 Arpil 2023 the UDT of arrays seems about 20-30% faster than the array of UDT's with setting each property without creating new UDT object.

Lorentzian Classification Strategy Based in the model of Machine learning: Lorentzian Classification by @jdehorty, you will be able to get into trending moves and get interesting entries in the market with this strategy. I also put some new features for better backtesting results!

Backtesting context: 2022-07-19 to 2023-04-14 of US500 1H by PEPPERSTONE. Commissions: 0.03% for each entry, 0.03% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 3 indicators are used:

Machine learning: Lorentzian Classification by @jdehorty

One Ema of 200 periods for identifying the trend

Supertrend indicator as a filter for some exits

Atr stop loss from Gatherio

Trade conditions:

For longs:

Close price is above 200 Ema

Lorentzian Classification indicates a buying signal

This gives us our long signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 1:1 and take profit of 3:1 where half position will be closed. This will be showed as buy.

The other half will be closed when the model indicates a selling signal or Supertrend indicator gives a bearish signal. This will be showed as cl buy.

For shorts:

Close price is under 200 Ema

Lorentzian Classification indicates a selling signal

This gives us our short signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 1:1 and take profit of 3:1 where half position will be closed. This will be showed as sell.

The other half will be closed when the model indicates a buying signal or Supertrend indicator gives a bullish signal. This will be showed as cl sell.

Risk management

To calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss or last swing for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss or last swing is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

> In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

> You can also choose a fixed amount, so you will have to activate fixed amount in risk management for trades and set the fixed amount for backtesting.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, a table of some stats from backtesting, etc.

You will find the settings for risk management at the end of the script if you want to change something or trying new values for other assets for backtesting.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital

I also added a function for backtesting if you had added or withdrawn money frequently:

Adding money: You can choose how often you want to add money (Monthly, yearly, daily or weekly). Then a fixed amount of money and activate or deactivate this function

Withdraw money: You can choose if you want to withdraw a fixed amount or a percentage of earnings. Then you can choose a fixed amount of money, the period of time and activate or deactivate this function. Also, the percentage of earnings if you choosed this option.

Some other assets where strategy has worked

BTCUSD 4H, 1D

ETHUSD 4H, 1D

BNBUSD 4H

SPX 1D

BANKNIFTY 4H, 15 min

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!. If you have problems loading the script reduce max bars back number in general settings

Strategies for trending markets use to have more looses than wins and it takes a long time to get profits, so do not forget to be patient and consistent !

Please, visit the post from @jdehorty called Machine Learning: Lorentzian Classification for a better understanding of his script!

Any support and boosts will be well received. If you have any question, do not doubt to ask!

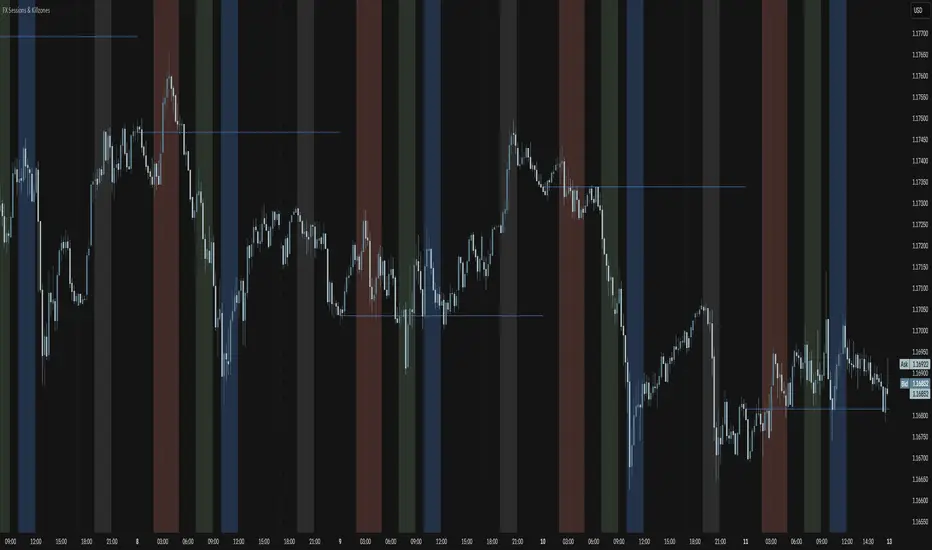

FX Sessions & Killzones ETJust another sessions indicator. Among all the many existing ones, I didn't find anything simple that would cover my needs and that would actually be correct.

New York time is forced here for plotting the stripes so you don't need to worry about the time zone currently set on your chart. The indicator will be accurate during Daylight Saving Time (which, in 2023 for example, started on Sunday, 12 March , 02:00:00 and will be in effect until Sunday, 5 November, 02:00:00).

Balance Zone ExtensionBalance zones are an aspect of trading that many traders notice. Balance Zones are formed when a market is in equilibrium and respects a certain high and low multiple times. These zones could also be called accumulation or distribution areas depending on the price action. If the term "choppy" is used to describe a given markets price action, it is probably a fair statement to say that the market is currently in a Balance Zone.

This script is a take on vwaptrader1's teachings where you take a balance zone and "double it" to get a target if/when it does break out of balance. It provides an automated way of extending levels based on a given balance range.

The lines plotted by the script are calculated based off of the balance high/low inputs, how many sections are desired per zone, and how many boxes to plot based on the other user inputs.

Warning: Due to a current limitation of the Pine, this script is only allowed to plot up to 500 lines total. If you start to notice lines starting to disappear or you begin getting a script error, double check the input settings as the script may have crossed the 500 line threshold.

This can be used in conjunction with Fixed Range Volume Profile . Select the balance range with the Fixed Volume Profile . Note the Value Area High and Value Area Low prices and input those into the balance range High/Low inputs.

Use to create price targets from Balance Zone Breakouts

A recent example of this idea in action on ticker ES1! 2 hour chart where the balance range was found and the target (double the box size of the balance range) was hit.

Another example of this same concept but on a normal security like AAPL but on a 30 minute chart:

Extending the usefulness even further to crypto on BTCUSD with a 5 minute chart:

Use to create reference levels for future price action

The other way to utilize this is to provide future reference levels from a key balance range from the past.

Here is another example utilizing the AMD daily chart . First, a balance zone was noted for all of 2017:

Moving forward to the most recent price action in 2023, notice that the box extension levels are still fairly well respected almost 6 years later!

Advanced VWAP_Pullback Strategy_Trend-Template QualifierGeneral Description and Unique Features of this Script

Introducing the Advanced VWAP Momentum-Pullback Strategy (long-only) that offers several unique features:

1. Our script/strategy utilizes Mark Minervini's Trend-Template as a qualifier for identifying stocks and other financial securities in confirmed uptrends. Mark Minervini, a 2x US Investment Champion, developed the Trend-Template, which covers eight different and independent characteristics that can be adjusted and optimized in this trend-following strategy to ensure the best results. The strategy will only trigger buy-signals in case the optimized qualifiers are being met.

2. Our strategy is based on the supply/demand balance in the market, making it timeless and effective across all timeframes. Whether you are day trading using 1- or 5-min charts or swing-trading using daily charts, this strategy can be applied and works very well.

3. We have also integrated technical indicators such as the RSI and the MA / VWAP crossover into this strategy to identify low-risk pullback entries in the context of confirmed uptrends. By doing so, the risk profile of this strategy and drawdowns are being reduced to an absolute minimum.

Minervini’s Trend-Template and the ‘Stage-Analysis’ of the Markets

This strategy is a so-called 'long-only' strategy. This means that we only take long positions, short positions are not considered.

The best market environment for such strategies are periods of stable upward trends in the so-called stage 2 - uptrend.

In stable upward trends, we increase our market exposure and risk.

In sideways markets and downward trends or bear markets, we reduce our exposure very quickly or go 100% to cash and wait for the markets to recover and improve. This allows us to avoid major losses and drawdowns.

This simple rule gives us a significant advantage over most undisciplined traders and amateurs!

'The Trend is your Friend'. This is a very old but true quote.

What's behind it???

• 98% of stocks made their biggest gains in a Phase 2 upward trend.

• If a stock is in a stable uptrend, this is evidence that larger institutions are buying the stock sustainably.

• By focusing on stocks that are in a stable uptrend, the chances of profit are significantly increased.

• In a stable uptrend, investors know exactly what to expect from further price developments. This makes it possible to locate low-risk entry points.

The goal is not to buy at the lowest price – the goal is to buy at the right price!

Each stock goes through the same maturity cycle – it starts at stage 1 and ends at stage 4

Stage 1 – Neglect Phase – Consolidation

Stage 2 – Progressive Phase – Accumulation

Stage 3 – Topping Phase – Distribution

Stage 4 – Downtrend – Capitulation

This strategy focuses on identifying stocks in confirmed stage 2 uptrends. This in itself gives us an advantage over long-term investors and less professional traders.

By focusing on stocks in a stage 2 uptrend, we avoid losses in downtrends (stage 4) or less profitable consolidation phases (stages 1 and 3). We are fully invested and put our money to work for us, and we are fully invested when stocks are in their stage 2 uptrends.

But how can we use technical chart analysis to find stocks that are in a stable stage 2 uptrend?

Mark Minervini has developed the so-called 'trend template' for this purpose. This is an essential part of our JS-TechTrading pullback strategy. For our watchlists, only those individual values that meet the tough requirements of Minervini's trend template are eligible.

The Trend Template

• 200d MA increasing over a period of at least 1 month, better 4-5 months or longer

• 150d MA above 200d MA

• 50d MA above 150d MA and 200d MA

• Course above 50d MA, 150d MA and 200d MA

• Ideally, the 50d MA is increasing over at least 1 month

• Price at least 25% above the 52w low

• Price within 25% of 52w high

• High relative strength according to IBD.

NOTE: In this basic version of the script, the Trend-Template has to be used as a separate indicator on TradingView (Public Trend-Template indicators are available in TradingView – community scripts). It is recommended to only execute buy signals in case the stock or financial security is in a stage 2 uptrend, which means that the criteria of the trend-template are fulfilled.

This strategy can be applied to all timeframes from 5 min to daily.

The VWAP Momentum-Pullback Strategy

For the JS-TechTrading VWAP Momentum-Pullback Strategy, only stocks and other financial instruments that meet the selected criteria of Mark Minervini's trend template are recommended for algorithmic trading with this startegy.

A further prerequisite for generating a buy signals is that the individual value is in a short-term oversold state (RSI).

When the selling pressure is over and the continuation of the uptrend can be confirmed by the MA / VWAP crossover after reaching a price low, a buy signal is issued by this strategy.

Stop-loss limits and profit targets can be set variably. You also have the option to make use of the trailing stop exit strategy.

Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a technical indicator developed by Welles Wilder in 1978. The RSI is used to perform a market value analysis and identify the strength of a trend as well as overbought and oversold conditions. The indicator is calculated on a scale from 0 to 100 and shows how much an asset has risen or fallen relative to its own price in recent periods.

The RSI is calculated as the ratio of average profits to average losses over a certain period of time. A high value of the RSI indicates an overbought situation, while a low value indicates an oversold situation. Typically, a value > 70 is considered an overbought threshold and a value < 30 is considered an oversold threshold. A value above 70 signals that a single value may be overvalued and a decrease in price is likely , while a value below 30 signals that a single value may be undervalued and an increase in price is likely.

For example, let's say you're watching a stock XYZ. After a prolonged falling movement, the RSI value of this stock has fallen to 26. This means that the stock is oversold and that it is time for a potential recovery. Therefore, a trader might decide to buy this stock in the hope that it will rise again soon.

The MA / VWAP Crossover Trading Strategy

This strategy combines two popular technical indicators: the Moving Average (MA) and the Volume Weighted Average Price (VWAP). The MA VWAP crossover strategy is used to identify potential trend reversals and entry/exit points in the market.

The VWAP is calculated by taking the average price of an asset for a given period, weighted by the volume traded at each price level. The MA, on the other hand, is calculated by taking the average price of an asset over a specified number of periods. When the MA crosses above the VWAP, it suggests that buying pressure is increasing, and it may be a good time to enter a long position. When the MA crosses below the VWAP, it suggests that selling pressure is increasing, and it may be a good time to exit a long position or enter a short position.

Traders typically use the MA VWAP crossover strategy in conjunction with other technical indicators and fundamental analysis to make more informed trading decisions. As with any trading strategy, it is important to carefully consider the risks and potential rewards before making any trades.

This strategy is applicable to all timeframes and the relevant parameters for the underlying indicators (RSI and MA/VWAP) can be adjusted and optimized as needed.

Backtesting

Backtesting gives outstanding results on all timeframes and drawdowns can be reduced to a minimum level. In this example, the hourly chart for MCFT has been used.

Settings for backtesting are:

- Period from Jan 2020 until March 2023

- Starting capital 100k USD

- Position size = 25% of equity

- 0.01% commission = USD 2.50.- per Trade

- Slippage = 2 ticks

Other comments

- This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

- The combination of the Trend-Template and the RSI qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

- Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

Cycle Position TradingTitle: Cycle Position Trading Strategy v1.0

Description: Cycle Position Trading Strategy is a simple yet effective trading strategy based on a 200-day Simple Moving Average (SMA). Users can select between two modes, "Buy Uptrend" and "Buy Downtrend," to customize the strategy according to their trading preferences. The strategy allows users to set their own stop loss (SL) and take profit (TP) levels, providing more flexibility and control over their trades.

Features:

Choose between two trading modes: "Buy Uptrend" and "Buy Downtrend."

Customize your stop loss (SL) and take profit (TP) levels.

Clear visual representation of the 200-day Simple Moving Average (SMA) on the chart.

How to use:

Add the strategy to your chart by searching for "Cycle Position Trading Strategy" in the TradingView "Indicators & Strategies" section.

Configure the strategy settings according to your preferences:

Select the trading mode from the dropdown menu. "Buy Uptrend" will open long positions when the closing price is above the 200-day SMA. "Buy Downtrend" will open long positions when the closing price is below the 200-day SMA.

Set your desired stop loss (SL) and take profit (TP) levels. The default values are 0.9 (10% below the entry price) for the stop loss and 1.1 (10% above the entry price) for the take profit.

Monitor the chart for trade signals based on the chosen mode and settings. The strategy will enter and exit trades automatically based on the selected mode and the configured stop loss and take profit levels.

Analyze the performance of the strategy by checking the TradingView strategy performance summary or by viewing individual trades in the "Trades" list.

Disclaimer: This strategy is intended for educational and illustrative purposes only. Use it at your own risk. Past performance is not indicative of future results. Trading stocks, cryptocurrencies, or any other financial instrument involves significant risk and may result in the loss of capital.

Version: v1.0

Release date: 2023-03-25

Author: I11L

License: Mozilla Public License 2.0 (mozilla.org)

Ehlers Undersampled Double Moving Average Indicator [CC]The Undersampled Double Moving Average was created by John Ehlers (Stocks and Commodities April 2023), and this is a double moving average system which is pretty rare for John Ehlers. For those of you who would like my other take on an Ehlers double moving average, be sure to check out my previous Ehlers double moving average script . He came up with a unique idea for this indicator to create a moving average using a sample of the price data. For example, we use his suggested length of 5 only to use the price data every 5 bars. Feel free to change this, and please let me know if you find a length that works better. He then smooths the indicator using the Hann Windowed Moving Average . I color-coded the lines to show stronger signals in darker colors or standard signals in lighter colors. Buy when the line turns green and sell when it turns red.

Let me know if there is an indicator or script you would like to see me publish!

ATR-Stepped, Another New Adaptive Moving Average [Loxx]ATR-Filtered, Another New Adaptive Moving Average is a modification of @cheatcountry's "Another New Adaptive Moving Average " shown below

I've added AT- stepped filtering. This is a standard ATR filter that works by requiring movement by XX multiple of ATR before registering a trend flip. I've also included Loxx's Expanded Source Types. You can read about those here:

From @cheatcountry on A New Adaptive Moving Average

The New Adaptive Moving Average was created by Scott Cong (Stocks and Commodities Mar 2023) and this is a companion indicator to my previous script

This indicator still works off of the same concept as before with effort vs results but this indicator takes a slightly different approach and instead defines results as the absolute difference between the closing price and a closing price x bars ago. As you can see in my chart example, this indicator works great to stay with the current trend and provides either a stop loss or take profit target depending on which direction you are going in. As always, I use darker colors to show stronger signals and lighter colors to show normal signals. Buy when the line turns green and sell when it turns red.

Included

Alerts

Signals

Loxx's Expanded Source Types

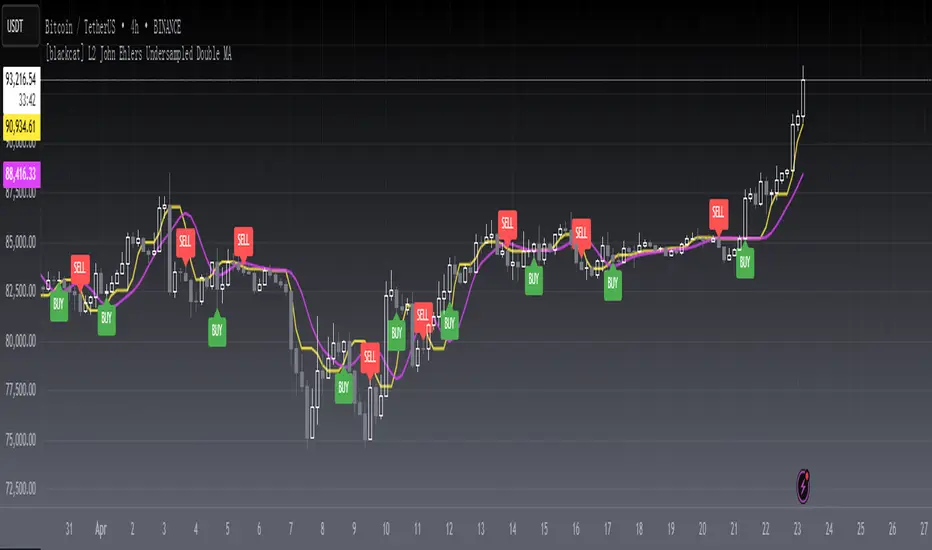

[blackcat] L2 John Ehlers Undersampled Double MALevel2

Background

This is a novel "undersampling data" processing trick proposed by John F. Ehlers in his April 2023 article "Just Ignore Them".

Function

In signal processing, undersampling, or bandpass sampling, is a technique whereby a bandpass-filtered signal is sampled at a sample rate below its Nyquist rate (twice the upper cut-off frequency), but the signal can still be reconstructed. When undersampling a bandpass signal, the samples are indistinguishable from samples of a low-frequency alias of the high-frequency signal.

John Ehlers notes that data smoothing is often used to avoid trading spikes. While this can result in fewer trading signals, it can also result in a delay in those trading signals. He describes how undersampling can be used in conjunction with Hann window finite impulse response (FIR) filters to remove high-frequency components in price data, resulting in less delay than traditional smoothing filters.

In this indicator, Hann windowing is applied a a pair of fast/slow moving averages which is used to improve their response perfomrnace. Yellow line is the fast line while fuchsia line is the slow line. You can judge bull bear stattus by checking the status it is in golden cross or in dead cross status.

Remarks

Feedbacks are appreciated.

Multi-Asset Month/Month % change 10yr Averages10 Year Averages of Month-on-Month % change: Shows current asset, and 3x user input assets

-For comparing seasonal tendencies among different assets.

-Choose from a variety of monthly average measures as source: sma(close, length), sma(ohlc4, length); as well as sma's of vwap, vwma, volume, volatility. (sma = simple moving average).

-Averages based on month cf previous month: i.e. Feb % = Feb compared to Jan; Jan % = Jan compared to prev year's Dec. Average of the last 10yrs of these values is the printed value.

-Plot on current year (2023), or previous year (2022). If Plotting on current year, and a month of year has not yet occured, a 9yr average will be printed.

/// notes ///

-daily bars in month is a global setting; so choose assets which have similar trading days per month. i.e. Crypto: length = 30 (days per month); Stocks/FX/Indices: length = 21 (days per month).

-only plots on Daily timeframe.

10yr Avgs; Plotting with Year = 2022; using sma(close, 21) as source for average M/M change

Global Unemployment RateThe Global Unemployment rate estimates what is the rate of unemployment of the whole world, taking same data from multiple countries and normalizing them.

It includes the Eurozone + 19 countries from all the continents, which are some of the richest countries as well as some of the most populous.

It sadly does not include India as its unemployment data on trading view as of today (Feb 2023) is only since year 2019, which is too short

Strategy for UT Bot Alerts indicator Using the UT Bot alerts indicator by @QuantNomad, this strategy was designed for showing an example of how this indicator could be used, also, it has the goal to help some people from a group that use to use this indicator for their trading. Under any circumstance I recommend to use it without testing it before in real time.

Backtesting context: 2020-02-05 to 2023-02-25 of BTCUSD 4H by Tvc. Commissions: 0.03% for each entry, 0.03% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 3 indicators are used:

UT Bot Alerts indicator by Quantnomad

One Ema of 200 periods for indicate the trend

Atr stop loss from Gatherio

Trade conditions:

For longs:

Close price is higher than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our long signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as buy (open long position)

The other half will be closed when close price is lower than Atr and Ema from UT Bot cross under Atr. This will be showed as cl buy (close long position)

For shorts:

Close price is lower than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our short signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as sell (open short position)

The other half will be closed when close price is higher than Atr and Ema from UT Bot cross over Atr. This will be showed as cl sell (close short position)

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital

---> Do not forget to deactivate Trades on chart option in style settings for a cleaner look of the chart <---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Strategies for trending markets use to have more looses than wins and it takes a long time to get profits, so do not forget to be patient and consistent !

---> The strategy can still be improved, you can change some parameters depending of the asset and timeframe like risk/reward for taking profits, for break even, also the main parameters of the UT Bot Alerts <----

Another New Adaptive Moving Average [CC]The New Adaptive Moving Average was created by Scott Cong (Stocks and Commodities Mar 2023) and this is a companion indicator to my previous script . This indicator still works off of the same concept as before with effort vs results but this indicator takes a slightly different approach and instead defines results as the absolute difference between the closing price and a closing price x bars ago. As you can see in my chart example, this indicator works great to stay with the current trend and provides either a stop loss or take profit target depending on which direction you are going in. As always, I use darker colors to show stronger signals and lighter colors to show normal signals. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicator scripts you would like to see me publish!

Markdown: The Pine Editor's Hidden Gem💬 Markdown, a markup language

Markdown is a portable, lightweight markup language that can be used for everything whether you're building a website, documentation, or even presentations.

Platforms like Discord, Reddit, and GitHub support Markdown and is the widely go-to option for text formatting due to its simplicity. Pine Script is a language that also utilizes Markdown, specifically in the Pine Editor where it can really be used to some extent.

Since the release of libraries, user-defined types, and methods, Pine Script is entering an age where developers will be highly dependent on libraries due to the capabilities Pine has inherited recently. It would be no surprise if a few people got together and took their time to thoroughly develop an entire project/library centered around improving Pine Script's built-in functions and providing developers with easier ways of achieving things than they thought they could.

As you're all aware, hovering over functions (and more) in the editor pops up a prompt that specifies the parameters, types, and what the function returns. Pine Script uses Markdown for that, so I figured we could go ahead and push that feature to its limits and see what we can do.

Today we'll go over how we can utilize Markdown in Pine Script, and how you can make your library's built-in functions stand out more than they did previously.

For more information, visit www.markdownguide.org

📕 General Notes

Markdown syntax only works on functions and methods.

Using arrays as parameters as of 2/21/2023 breaks the Markdown system.

The prompt window holds a max of 166 characters on one line before overflowing.

There is no limit on how long the prompt window can be.

🔽 Getting Started 🔽

▶️ Headings

If you have experience in HTML, Markdown, or even Microsoft Word then you already have a grasp of how headings work and look.

To simplify it, headings make the given text either massive or tiny depending on how many number symbols are provided.

When defining headings, you must have a space between the number (#) symbol, and the text. This is typical syntax throughout the language.

Pine Script uses bold text by applying (**) for their titles on their built-ins (e.g. @returns) but you could also use heading level 4 (####) and have it look the same.

▶️ Paragraphs & Line Breaks

You may want to provide extensive details and examples relating to one function, in this case, you could create line breaks. Creating line breaks skips to the next line so you can keep things organized as a result.

To achieve a valid line break and create a new paragraph, you must end the line with two or more spaces.

If you want to have an empty line in between, apply a backslash (\).

Backslashes (\) are generally not recommended for every line break. In this case, I only recommend using them for empty lines.

▶️ Text Formatting

Markdown provides text formatting such as bold, italics, and strikethrough.

For bolding text, you can apply open and close (**) or (__).

For italicizing text, you can apply open and close (*) or (_).

For bolding and italicizing text, you can apply open and close (***) or (___).

For s̶t̶r̶i̶k̶e̶t̶h̶r̶o̶u̶g̶h̶, you need to apply open and close (~~).

This was mentioned in the Headers section, but Pine Script's main titles (e.g. @returns or @syntax) use bold (**) by default.

▶️ Blockquotes

Blockquotes in Pine Script can be visualized as a built-in indentation system.

They are declared using greater than (>) and everything will be auto-aligned and indented until closed.

By convention you generally want to include the greater than (>) on every line that's included in the block quote. Even when not needed.

If you would like to indent even more (nested blockquotes), you can apply multiple greater than symbols (>). For example, (>>)

Blockquotes can be closed by ending the next line with only one greater than (>) symbol, or by using a horizontal rule.

▶️ Horizontal Rules

Horizontal rules in Pine Script are what you see at the very top of the prompt in built-ins.

When hovering, you can see the top of the prompt provides a line, and we can actually reproduce these lines.

These are extremely useful for separating information into their own parts and are accessed by applying 3 underscores (___), or 3 asterisks (***).

Horizontal rules were mentioned above, when we were discussing block quotes. These can also be used to close blockquotes as well.

Horizontal rules require a minimum of 3 underscores (___) or 3 asterisks (***).

▶️ Lists

Lists give us a way to structure data in a somewhat neat way. There are multiple ways to start a list, such as

1. First Item (number followed by a period)

- First Item (dash)

+ First Item (plus sign)

* First Item (asterisk)

Using number-based lists provide an ordered list, whereas using (-), (+), or (*) will provide an unordered list (bullet points).

If you want to begin an unordered list with a number that ends with a period, you must use an escape sequence (\) after the number.

Standard indentation (tab-width) list detection isn't supported, so to nest lists you have to use blockquotes (>) which may not look as appealing.

▶️ Code Blocks

Using code blocks allows you to write actual Pine Script code inside the prompt.

It's a game changer that can potentially help people understand how to execute functions quickly.

To use code blocks, apply three 3 open and close backquotes (```). Built-in's use (```pine) but there's no difference when we apply it.

Considering that tab-width indentation isn't detected properly, we can make use of the blockquotes mentioned above.

▶️ Denotation

Denoting can also be seen as highlighting a background layer behind text. They're basically code blocks, but without the "block".

Similar to how code blocks work, we apply one backquote open and close (`).

Make sure to only use this on important keywords. There really isn't a conventional way of applying this.

It's up to you to decide what people should have their eyes tracked onto when they hover over your functions.

If needed, look at how Pine Script's built-in variables and functions utilize this.

▶️ Tables

Tables are possible in Markdown, although they may look a bit different in the Pine Editor.

They are made by separating text with vertical bars (|).

The headers are detected when there is a minimum of one hyphen (-) below them.

You can align text by using a colon as I do in the photo. Hyphens must be connected to the colon in order to display correctly.

Tables aren't ideal to use in the editor but are there if anyone wants to give it a go.

▶️ Links & Images

Markdown supports images and hyperlinks, which means we can also do that here in the Pine Editor. Cool right?

If you want to create a hyperlink, surround the displayed text in open and close brackets .

If you want to load a photo into your prompt, it's the same syntax as the hyperlink, except it uses a (!)

See syntax list below.

Here are realistic usage examples. (Snippets from code below)

These follow the same syntax as the built-ins.

I'm not using horizontal rules here, but it's entirely up to you.

▶️ Syntax List

Headings

Level 1: #

Level 2: ##

Level 3: ###

Level 4: ####

Level 5: #####

Level 6: ######

Line Breaks

Text (two spaces)

Text\ (backslash)

Text Formatting

Bold (**)

Italic (**)

Strikethrough (~~)

Blockquotes

Indent (>)

Double Indent (>>)

Triple Indent (>>>) and so on.

Horizontal Rules

(___) or (***)

Lists

Ordered List (1.)

Unordered List (-) or (+) or (*)

Code Blocks

(```) or (```pine)

Denotation

(`)

Tables

(|) and (-) and (:)

Hyperlinks

(URL)

Images

! (URL)

Hope this helps. 👍

Ehlers Data Sampling Relative Strength Indicator [CC]The Data Sampling Indicator was created by John Ehlers (Stocks and Commodities Mar 2023) and this is a genius method to reduce noise in the market data but also doesn't introduce any lag while doing so. The way this works is because traditionally, people have always relied on the close price as the default input for many indicators such as the RSI or MACD as examples. Since the open is usually virtually identical to the previous close, it has been ignored by most people but Ehlers discovered that if you do a simple average of open and close for the input on any indicator, you can remove much of the noise without any added lag. I have used the RSI as he did in his example and plotted both to show the difference between the traditional RSI and using Ehlers' process as the new Data Sampling RSI. You can clearly see that this new RSI follows the price fluctuations much closer and is much smoother than the traditional RSI. As usual, I have included different colors to show the strength of the buy or sell signals so darker colors mean it is a very strong signal and lighter colors means it is a normal signal. Buy when the line turns green and sell when it turns red.

Feel free to try out this method to replace the input for any indicator and let me know how this works for you! And of course let me know if you would like me to publish any indicator script.

A New Adaptive Moving Average [CC]The New Adaptive Moving Average was created by Scott Cong (Stocks and Commodities Mar 2023) and his idea was to focus on the Adaptive Moving Average created by Perry Kaufman and to try to improve it by introducing a concept of effort vs results. In this case the effort would be the total range of the underlying price action since each bar is essentially a war of the bulls vs the bears. The result would be the total range of the close so we are looking for the highest close and lowest close in that same time period. This gives us an alpha that we can use to plug into the Kaufman Adaptive Moving Average algorithm which gives us a brand new indicator that can hug the price just enough to allow us to ride the stock up or down. I have color coded it to be darker colors when it is a strong signal and lighter colors when it is a normal signal. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators you would like to see me publish!

Investments/swing trading strategy for different assetsStop worrying about catching the lowest price, it's almost impossible!: with this trend-following strategy and protection from bearish phases, you will know how to enter the market properly to obtain benefits in the long term.

Backtesting context: 1899-11-01 to 2023-02-16 of SPX by Tvc. Commissions: 0.05% for each entry, 0.05% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 5 indicators are used:

One Ema of 200 periods

Atr Stop loss indicator from Gatherio

Squeeze momentum indicator from LazyBear

Moving average convergence/divergence or Macd

Relative strength index or Rsi

Trade conditions:

There are three type of entries, one of them depends if we want to trade against a bearish trend or not.

---If we keep Against trend option deactivated, the rules for two type of entries are:---

First type of entry:

With the next rules, we will be able to entry in a pull back situation:

Squeeze momentum is under 0 line (red)

Close is above 200 Ema and close is higher than the past close

Histogram from macd is under 0 line and is higher than the past one

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

For closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Second type of entry:

With the next rules, we will not lose a possible bullish movement:

Close is above 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entry, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

---If we keep Against trend option activated, the rules are the same as the ones above, but with one more type of entry. This is more useful in weekly timeframes, but could also be used in daily time frame:---

Third type of entry:

Close is under 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entries, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Risk management

For calculating the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

If you activate break even using rsi, when rsi crosses under overbought zone break even will be activated. This can work in some assets.

---Important: In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Some assets and timeframes where the strategy has also worked:

BTCUSD : 4H, 1D, W

SPX (US500) : 4H, 1D, W

GOLD : 1D, W

SILVER : 1D, W

ETHUSD : 4H, 1D

DXY : 1D

AAPL : 4H, 1D, W

AMZN : 4H, 1D, W

META : 4H, 1D, W

(and others stocks)

BANKNIFTY : 4H, 1D, W

DAX : 1D, W

RUT : 1D, W

HSI : 1D, W

NI225 : 1D, W

USDCOP : 1D, W

VIB / GIB v1.0The VIB / GIB indicator

V1 ----- 13 Feb 2023 ------------ Inital release.

This gives the user the ability to easily display VIB(Volume ImBalances) and GIB(Gap ImBalances) on their chart.

Volume imbalances (VIB) are created when there is a price difference between the close of a candle and the opening of the next candle. This price difference can be used as a level of support or resistance in future trading.

A Gap imbalance (GIB) has the same principles as a VIB, but also has the feature that no wick closes through the gap, showing an even more powerful imbalance in the market at that point.

GIBs and VIBs can be individually switched on or off via the settings, and optional icons can also be activated or not to show where the imbalance took place.

Please note that this is purely an indicator that should be used with other confluence before making trading decisions.

Kitti-Playbook request.earnings R0.0Date: Feb 5 2023

Objective :

Display Earnings per share

Calculation :

Get Earning value by use Function "request.earnings "

Display :

Plot Earnings Data

Earnings History Tab