Average Range @coldbrewroshTaking the average daily range from low to high or high to low isn't the "best" way to get an idea of how much to set targets. So, I made this indicator to make the system better.

This indicator calculates the daily range from Open to High on Bullish Days & Open to Low on Bearish Days .

Nobody can catch the absolute low of the day on bullish days and get out at the high but one can enter at a reasonable price around the open ( 17:00 EST ) .

To complement the Average Range, another table shows the movement in the opposite direction.

For Instance: On Bullish Days how much it moved from Open to Low so that we have an idea of where to put the stop loss and vice versa. The time ranges calculated are the last 5 days, last 1 month, last 3 months & last 1 year.

Note #1: Even though the date range is predefined, it has a different meaning. For Instance: date range of last 5 days means "calculation of the range of last 5 bullish daily candles & not last 5 days" .

Note #2: Exclusive to Forex at the time of posting this.

Cari dalam skrip untuk "17个交易日涨幅第一的股票(非新股)有哪些"

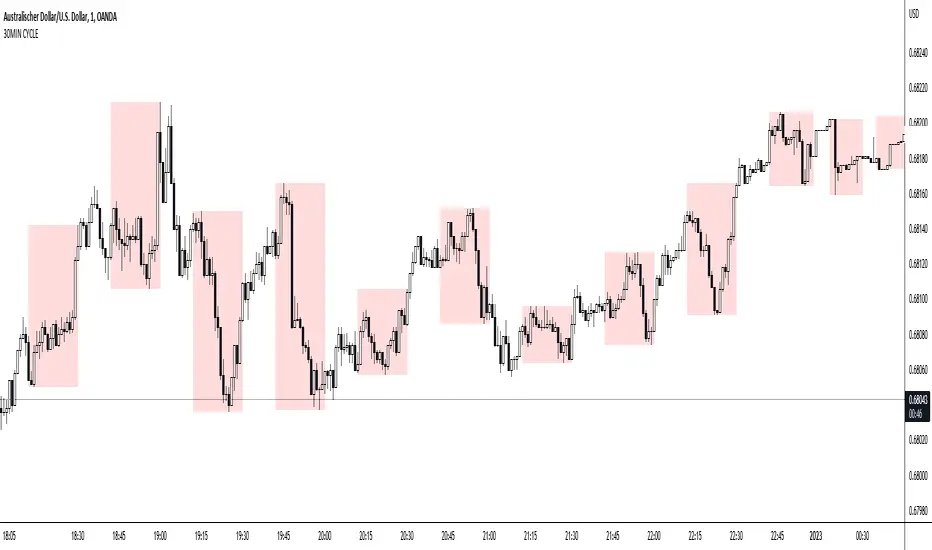

30MIN CYCLE█ HOW DOES IT WORK?

The known 90 min cycle is used as one killzone. But actually all 18 min are relevant to search for a trade. All 18 min when a new box starts only then is the placement of an order valid. If the entry candle isn't in a box then it will probably fail. The boxes should only be used in the M1 or M5 timeframe. The best hitrate is in the M1 timeframe. Included are the last 48 "Mini-Killzones" für intraday trading and backtesting. These "Mini-Killzones" can be used with the "Liquidity Inducement Strategy".

█ WHAT MAKES IT UNIQUE?

This is the first indicator on tradingview that shows all mini-killzones for trading and backtesting a whole tradingday. The well-known killzones of ICT are from 08:00-11:00 and 14:00 - 17:00 (UTC+1) but with this indicator there is finally a refinement of the ICT Smart Money Concept killzones.

█ HOW TO USE IT?

For a proper use of this indicator we suggest to know already at least SMC or better Liquidity Indcuement Trading. This indicator is a further confluence before placing an order. After you made your setup you will have these mini-killzones as a confluence. We don't suggest to open a trade only according to this indicator.

█ ADDITIONAL INFO

This indicator is free to use for all tradingview users.

█ DISCLAIMER

This is not financial advice.

Session candles & reversals / quantifytools— Overview

Like traditional candles, session based candles are a visualization of open, high, low and close values, but based on session time periods instead of typical timeframes such as daily or weekly. Session candles are formed by fetching price at session start (open), highest price during session (high), lowest price during session (low) and price at session end (close). On top of candles, session based moving average is formed and session reversals detected. Session reversals are also backtested, using win rate and magnitude metrics to better understand what to expect from session reversals and which ones have historically performed the best.

By default, following session time periods are used:

Session #1: London (08:00 - 17:00, UTC)

Session #2: New York (13:00 - 22:00, UTC)

Session #3: Sydney (21:00 - 06:00, UTC)

Session #4: Tokyo (00:00 - 09:00, UTC)

Session time periods can be changed via input menu.

— Reversals

Session reversals are patterns that show a rapid change in direction during session. These formations are more familiarly known as wicks or engulfing candles. Following criteria must be met to qualify as a session reversal:

Wick up:

Lower high, lower low, close >= 65% of session range (0% being the very low, 100% being the very high) and open >= 40% of session range.

Wick down:

Higher high, higher low, close <= 35% of session range and open <= 60% of session range.

Engulfing up:

Higher high, lower low, close >= 65% of session range.

Engulfing down:

Higher high, lower low, close <= 35% of session range.

Session reversals are always based on prior corresponding session , e.g. to qualify as a NY session engulfing up, NY session must have a higher high and lower low relative to prior NY session , not just any session that has taken place in between. Session reversals should be viewed the same way wicks/engulfing formations are viewed on traditional timeframe based candles. Essentially, wick reversals (light green/red labels) tell you most of the motion during session was reversed. Engulfing reversals (dark green/red labels) on the other hand tell you all of the motion was reversed and new direction set.

— Backtesting

Session reversals are backtested using win rate and magnitude metrics. A session reversal is considered successful when next corresponding session closes higher/lower than session reversal close . Win rate is formed by dividing successful session reversal count with total reversal count, e.g. 5 successful reversals up / 10 reversals up total = 50% win rate. Win rate tells us what are the odds (historically) of session reversal producing a clean supporting move that was persistent enough to close that way too.

When a session reversal is successful, its magnitude is measured using percentage increase/decrease from session reversal close to next corresponding session high/low . If NY session closes higher than prior NY session that was a reversal up, the percentage increase from prior session close (reversal close) to current session high is measured. If NY session closes lower than prior NY session that was a reversal down, the percentage decrease from prior session close to current session low is measured.

Average magnitude is formed by dividing all percentage increases/decreases with total reversal count, e.g. 10 total reversals up with 1% increase each -> 10% net increase from all reversals -> 10% total increase / 10 total reversals up = 1% average magnitude. Magnitude metric supports win rate by indicating the depth of successful session reversal moves.

To better understand the backtesting calculations and more importantly to verify their validity, backtesting visuals for each session can be plotted on the chart:

All backtesting results are shown in the backtesting panel on top right corner, with highest win rates and magnitude metrics for both reversals up and down marked separately. Note that past performance is not a guarantee of future performance and session reversals as they are should not be viewed as a complete strategy for long/short plays. Always make sure reversal count is sufficient to draw reliable conclusions of performance.

— Session moving average

Users can form a session based moving average with their preferred smoothing method (SMA , EMA , HMA , WMA , RMA) and length, as well as choose which sessions to include in the moving average. For example, a moving average based on New York and Tokyo sessions can be formed, leaving London and Sydney completely out of the calculation.

— Visuals

By default, script hides your candles/bars, although in the case of candles borders will still be visible. Switching to bars/line will make your regular chart visuals 100% hidden. This setting can be turned off via input menu. As some sessions overlap, each session candle can be separately offsetted forward, clearing the overlaps. Users can also choose which session candles to show/hide.

Session periods can be highlighted on the chart as a background color, applicable to only session candles that are activated. By default, session reversals are referred to as L (London), N (New York), S (Sydney) and T (Tokyo) in both reversal labels and backtesting table. By toggling on "Numerize sessions", these will be replaced with 1, 2, 3 and 4. This will be helpful when using a custom session that isn't any of the above.

Visual settings example:

Session candles are plotted in two formats, using boxes and lines as well as plotcandle() function. Session candles constructed using boxes and lines will be clear and much easier on the eyes, but will apply only to first 500 bars due to Tradingview related limitations. Rest of the session candles go back indefinitely, but won't be as clean:

All colors can be customized via input menu.

— Timeframe & session time period considerations

As a rule of thumb, session candles should be used on timeframes at or below 1H, as higher timeframes might not match with session period start/end, leading to incorrect plots. Using 1 hour timeframe will bring optimal results as greatest amount historical data is available without sacrificing accuracy of OHLC values. If you are using a custom session that is not based on hourly period (e.g. 08:00 - 15:00 vs. 08.00 - 15.15) make sure you are using a timeframe that allows correct plots.

Session time periods applied by default are rough estimates and might be out of bounds on some charts, like NYSE listed equities. This is rarely a problem on assets that have extensive trading hours, like futures or cryptocurrency. If a session is out of bounds (asset isn't traded during the set session time period) the script won't plot given session candle and its backtesting metrics will be NA. This can be fixed by changing the session time periods to match with given asset trading hours, although you will have to consider whether or not this defeats the purpose of having candles based on sessions.

— Practical guide

Whether based on traditional timeframes or sessions, reversals should always be considered as only one piece of evidence of price turning. Never react to them without considering other factors that might support the thesis, such as levels and multi-timeframe analysis. In short, same basic charting principles apply with session candles that apply with normal candles. Use discretion.

Example #1 : Focusing efforts on session reversals at distinct support/resistance levels

A reversal against a level holds more value than a reversal by itself, as you know it's a placement where liquidity can be expected. A reversal serves as a confirming reaction for this expectation.

Example #2 : Focusing efforts on highest performing reversals and avoiding poorly performing ones

As you have data backed evidence of session reversal performance, it makes sense to focus your efforts on the ones that perform best. If some session reversal is clearly performing poorly, you would want to avoid it, since there's nothing backing up its validity.

Example #3 : Reversal clusters

Two is better than one, three is better than two and so on. If there are rapid changes in direction within multiple sessions consecutively, there's heavier evidence of a dynamic shift in price. In such case, it makes sense to hold more confidence in price halting/turning.

Black Scholes Option Pricing Model w/ Greeks [Loxx]The Black Scholes Merton model

If you are new to options I strongly advise you to profit from Robert Shiller's lecture on same . It combines practical market insights with a strong authoritative grasp of key models in option theory. He explains many of the areas covered below and in the following pages with a lot intuition and relatable anecdotage. We start here with Black Scholes Merton which is probably the most popular option pricing framework, due largely to its simplicity and ease in terms of implementation. The closed-form solution is efficient in terms of speed and always compares favorably relative to any numerical technique. The Black–Scholes–Merton model is a mathematical go-to model for estimating the value of European calls and puts. In the early 1970’s, Myron Scholes, and Fisher Black made an important breakthrough in the pricing of complex financial instruments. Robert Merton simultaneously was working on the same problem and applied the term Black-Scholes model to describe new generation of pricing. The Black Scholes (1973) contribution developed insights originally proposed by Bachelier 70 years before. In 1997, Myron Scholes and Robert Merton received the Nobel Prize for Economics. Tragically, Fisher Black died in 1995. The Black–Scholes formula presents a theoretical estimate (or model estimate) of the price of European-style options independently of the risk of the underlying security. Future payoffs from options can be discounted using the risk-neutral rate. Earlier academic work on options (e.g., Malkiel and Quandt 1968, 1969) had contemplated using either empirical, econometric analyses or elaborate theoretical models that possessed parameters whose values could not be calibrated directly. In contrast, Black, Scholes, and Merton’s parameters were at their core simple and did not involve references to utility or to the shifting risk appetite of investors. Below, we present a standard type formula, where: c = Call option value, p = Put option value, S=Current stock (or other underlying) price, K or X=Strike price, r=Risk-free interest rate, q = dividend yield, T=Time to maturity and N denotes taking the normal cumulative probability. b = (r - q) = cost of carry. (via VinegarHill-Financelab )

Things to know

This can only be used on the daily timeframe

You must select the option type and the greeks you wish to show

This indicator is a work in process, functions may be updated in the future. I will also be adding additional greeks as I code them or they become available in finance literature. This indictor contains 18 greeks. Many more will be added later.

Inputs

Spot price: select from 33 different types of price inputs

Calculation Steps: how many iterations to be used in the BS model. In practice, this number would be anywhere from 5000 to 15000, for our purposes here, this is limited to 300

Strike Price: the strike price of the option you're wishing to model

% Implied Volatility: here you can manually enter implied volatility

Historical Volatility Period: the input period for historical volatility ; historical volatility isn't used in the BS process, this is to serve as a sort of benchmark for the implied volatility ,

Historical Volatility Type: choose from various types of implied volatility , search my indicators for details on each of these

Option Base Currency: this is to calculate the risk-free rate, this is used if you wish to automatically calculate the risk-free rate instead of using the manual input. this uses the 10 year bold yield of the corresponding country

% Manual Risk-free Rate: here you can manually enter the risk-free rate

Use manual input for Risk-free Rate? : choose manual or automatic for risk-free rate

% Manual Yearly Dividend Yield: here you can manually enter the yearly dividend yield

Adjust for Dividends?: choose if you even want to use use dividends

Automatically Calculate Yearly Dividend Yield? choose if you want to use automatic vs manual dividend yield calculation

Time Now Type: choose how you want to calculate time right now, see the tool tip

Days in Year: choose how many days in the year, 365 for all days, 252 for trading days, etc

Hours Per Day: how many hours per day? 24, 8 working hours, or 6.5 trading hours

Expiry date settings: here you can specify the exact time the option expires

The Black Scholes Greeks

The Option Greek formulae express the change in the option price with respect to a parameter change taking as fixed all the other inputs. ( Haug explores multiple parameter changes at once .) One significant use of Greek measures is to calibrate risk exposure. A market-making financial institution with a portfolio of options, for instance, would want a snap shot of its exposure to asset price, interest rates, dividend fluctuations. It would try to establish impacts of volatility and time decay. In the formulae below, the Greeks merely evaluate change to only one input at a time. In reality, we might expect a conflagration of changes in interest rates and stock prices etc. (via VigengarHill-Financelab )

First-order Greeks

Delta: Delta measures the rate of change of the theoretical option value with respect to changes in the underlying asset's price. Delta is the first derivative of the value

Vega: Vegameasures sensitivity to volatility. Vega is the derivative of the option value with respect to the volatility of the underlying asset.

Theta: Theta measures the sensitivity of the value of the derivative to the passage of time (see Option time value): the "time decay."

Rho: Rho measures sensitivity to the interest rate: it is the derivative of the option value with respect to the risk free interest rate (for the relevant outstanding term).

Lambda: Lambda, Omega, or elasticity is the percentage change in option value per percentage change in the underlying price, a measure of leverage, sometimes called gearing.

Epsilon: Epsilon, also known as psi, is the percentage change in option value per percentage change in the underlying dividend yield, a measure of the dividend risk. The dividend yield impact is in practice determined using a 10% increase in those yields. Obviously, this sensitivity can only be applied to derivative instruments of equity products.

Second-order Greeks

Gamma: Measures the rate of change in the delta with respect to changes in the underlying price. Gamma is the second derivative of the value function with respect to the underlying price.

Vanna: Vanna, also referred to as DvegaDspot and DdeltaDvol, is a second order derivative of the option value, once to the underlying spot price and once to volatility. It is mathematically equivalent to DdeltaDvol, the sensitivity of the option delta with respect to change in volatility; or alternatively, the partial of vega with respect to the underlying instrument's price. Vanna can be a useful sensitivity to monitor when maintaining a delta- or vega-hedged portfolio as vanna will help the trader to anticipate changes to the effectiveness of a delta-hedge as volatility changes or the effectiveness of a vega-hedge against change in the underlying spot price.

Charm: Charm or delta decay measures the instantaneous rate of change of delta over the passage of time.

Vomma: Vomma, volga, vega convexity, or DvegaDvol measures second order sensitivity to volatility. Vomma is the second derivative of the option value with respect to the volatility, or, stated another way, vomma measures the rate of change to vega as volatility changes.

Veta: Veta or DvegaDtime measures the rate of change in the vega with respect to the passage of time. Veta is the second derivative of the value function; once to volatility and once to time.

Vera: Vera (sometimes rhova) measures the rate of change in rho with respect to volatility. Vera is the second derivative of the value function; once to volatility and once to interest rate.

Third-order Greeks

Speed: Speed measures the rate of change in Gamma with respect to changes in the underlying price.

Zomma: Zomma measures the rate of change of gamma with respect to changes in volatility.

Color: Color, gamma decay or DgammaDtime measures the rate of change of gamma over the passage of time.

Ultima: Ultima measures the sensitivity of the option vomma with respect to change in volatility.

Dual Delta: Dual Delta determines how the option price changes in relation to the change in the option strike price; it is the first derivative of the option price relative to the option strike price

Dual Gamma: Dual Gamma determines by how much the coefficient will changedual delta when the option strike price changes; it is the second derivative of the option price relative to the option strike price.

Related Indicators

Cox-Ross-Rubinstein Binomial Tree Options Pricing Model

Implied Volatility Estimator using Black Scholes

Boyle Trinomial Options Pricing Model

Machine Learning: kNN (New Approach)Description:

kNN is a very robust and simple method for data classification and prediction. It is very effective if the training data is large. However, it is distinguished by difficulty at determining its main parameter, K (a number of nearest neighbors), beforehand. The computation cost is also quite high because we need to compute distance of each instance to all training samples. Nevertheless, in algorithmic trading KNN is reported to perform on a par with such techniques as SVM and Random Forest. It is also widely used in the area of data science.

The input data is just a long series of prices over time without any particular features. The value to be predicted is just the next bar's price. The way that this problem is solved for both nearest neighbor techniques and for some other types of prediction algorithms is to create training records by taking, for instance, 10 consecutive prices and using the first 9 as predictor values and the 10th as the prediction value. Doing this way, given 100 data points in your time series you could create 10 different training records. It's possible to create even more training records than 10 by creating a new record starting at every data point. For instance, you could take the first 10 data points and create a record. Then you could take the 10 consecutive data points starting at the second data point, the 10 consecutive data points starting at the third data point, etc.

By default, shown are only 10 initial data points as predictor values and the 6th as the prediction value.

Here is a step-by-step workthrough on how to compute K nearest neighbors (KNN) algorithm for quantitative data:

1. Determine parameter K = number of nearest neighbors.

2. Calculate the distance between the instance and all the training samples. As we are dealing with one-dimensional distance, we simply take absolute value from the instance to value of x (| x – v |).

3. Rank the distance and determine nearest neighbors based on the K'th minimum distance.

4. Gather the values of the nearest neighbors.

5. Use average of nearest neighbors as the prediction value of the instance.

The original logic of the algorithm was slightly modified, and as a result at approx. N=17 the resulting curve nicely approximates that of the sma(20). See the description below. Beside the sma-like MA this algorithm also gives you a hint on the direction of the next bar move.

CINCO EMAs | JC Trader (Trade Diário)Cinco médias Exponenciais, sendo elas:

- MME 8

- MME 17

- MME 34

- MME 72

- MME 305

Educational: FillThis script showcases the latest feature of colour fill between lines with gradient

There are 17 ema's, all with adjustable lengths.

In the settings there are 3 options: '1' , '2' , and '1 & 2' :

Option '1'

Here the highest - lowest lines are filled with a gradient colour,

dependable where the 3rd highest/lowest ema is situated in regard of these 2 lines:

Option '2'

Here the colour fill is applied between every ema and the one next to it.

The gradient colour is dependable where the ema is situated in regard of the highest - lowest line:

Option '1 & 2'

A combination of both options:

The setting 'switch colours at ema x' regulates the switch between bullish and bearish colours.

When close is above the chosen ema -> bullish colours, when below -> bearish colours.

Examples of other settings of 'switch colours at ema x' :

Colour switch when close above/below:

ema 14

ema 11

ema 8

ema 5

ema 2

The colours can be set below, both for option '1' and '2'

Cheers!

Stochastic Rsi+Ema - Auto Buy Scalper Scirpt v.0.3Simple concept for a scalping script, written for 5 minute candles, optimized for BTC.

1st script I've created from scratch, somewhat from scratch. Also part of the goal of this one is to hold coin as often as possible, whenever it's sideways or not dropping significantly.

Designed to buy on the stochastic bottoms (K>D and rising, and <17)

Then and sell after 1 of 3 conditions;

a. After the price goes back up at least 1 % and then 1-2 period ema reversal

b. After the rsi reversal (is dropping) and K

CDC ActionZone BF for ETHUSD-1D © PRoSkYNeT-EE

Based on improvements from "Kitti-Playbook Action Zone V.4.2.0.3 for Stock Market"

Based on improvements from "CDC Action Zone V3 2020 by piriya33"

Based on Triple MACD crossover between 9/15, 21/28, 15/28 for filter error signal (noise) from CDC ActionZone V3

MACDs generated from the execution of millions of times in the "Brute Force Algorithm" to backtest data from the past 5 years. ( 2017-08-21 to 2022-08-01 )

Released 2022-08-01

***** The indicator is used in the ETHUSD 1 Day period ONLY *****

Recommended Stop Loss : -4 % (execute stop Loss after candlestick has been closed)

Backtest Result ( Start $100 )

Winrate 63 % (Win:12, Loss:7, Total:19)

Live Days 1,806 days

B : Buy

S : Sell

SL : Stop Loss

2022-07-19 07 - 1,542 : B 6.971 ETH

2022-04-13 07 - 3,118 : S 8.98 % $10,750 12,7,19 63 %

2022-03-20 07 - 2,861 : B 3.448 ETH

2021-12-03 07 - 4,216 : SL -8.94 % $9,864 11,7,18 61 %

2021-11-30 07 - 4,630 : B 2.340 ETH

2021-11-18 07 - 3,997 : S 13.71 % $10,832 11,6,17 65 %

2021-10-05 07 - 3,515 : B 2.710 ETH

2021-09-20 07 - 2,977 : S 29.38 % $9,526 10,6,16 63 %

2021-07-28 07 - 2,301 : B 3.200 ETH

2021-05-20 07 - 2,769 : S 50.49 % $7,363 9,6,15 60 %

2021-03-30 07 - 1,840 : B 2.659 ETH

2021-03-22 07 - 1,681 : SL -8.29 % $4,893 8,6,14 57 %

2021-03-08 07 - 1,833 : B 2.911 ETH

2021-02-26 07 - 1,445 : S 279.27 % $5,335 8,5,13 62 %

2020-10-13 07 - 381 : B 3.692 ETH

2020-09-05 07 - 335 : S 38.43 % $1,407 7,5,12 58 %

2020-07-06 07 - 242 : B 4.199 ETH

2020-06-27 07 - 221 : S 28.49 % $1,016 6,5,11 55 %

2020-04-16 07 - 172 : B 4.598 ETH

2020-02-29 07 - 217 : S 47.62 % $791 5,5,10 50 %

2020-01-12 07 - 147 : B 3.644 ETH

2019-11-18 07 - 178 : S -2.73 % $536 4,5,9 44 %

2019-11-01 07 - 183 : B 3.010 ETH

2019-09-23 07 - 201 : SL -4.29 % $551 4,4,8 50 %

2019-09-18 07 - 210 : B 2.740 ETH

2019-07-12 07 - 275 : S 63.69 % $575 4,3,7 57 %

2019-05-03 07 - 168 : B 2.093 ETH

2019-04-28 07 - 158 : S 29.51 % $352 3,3,6 50 %

2019-02-15 07 - 122 : B 2.225 ETH

2019-01-10 07 - 125 : SL -6.02 % $271 2,3,5 40 %

2018-12-29 07 - 133 : B 2.172 ETH

2018-05-22 07 - 641 : S 5.95 % $289 2,2,4 50 %

2018-04-21 07 - 605 : B 0.451 ETH

2018-02-02 07 - 922 : S 197.42 % $273 1,2,3 33 %

2017-11-11 07 - 310 : B 0.296 ETH

2017-10-09 07 - 297 : SL -4.50 % $92 0,2,2 0 %

2017-10-07 07 - 311 : B 0.309 ETH

2017-08-22 07 - 310 : SL -4.02 % $96 0,1,1 0 %

2017-08-21 07 - 323 : B 0.310 ETH

Price Action Top/BottomThis script is a variation from Auto Fibo retration.

It makrs top and bottom prices. You can use to study the price action.

The user can choose the line color, to show or not, the marks green and red

The user can choose the minimal candles between top and bottom, by default is 17

The deep is the percentage of the diference about the last bottom/top from the previous one.

TR Unleaded Gasoline & Diesel Price by zdmreThe price of gasoline can change on any given day. Although a number of factors determine the price per liter, the price of crude oil makes the most impact. The per-barrel price of crude oil is most directly affected by world supply and demand. By closely monitoring the price of crude as well as keeping tabs on a few other factors you can estimate the cost to fill up.

Divide the crude oil (Moving Average) price by 159. One barrel of crude contains 159 liters. This will tell you the dollar amount per liter of refined gasoline attributed to crude. For example, if crude oil is $100 per barrel, then about $0.628 of the price of a liter of gas comes from the crude price.

By multiplying this amount by Dollar/Turkish Lira, special ratio and upper limit, you can get an estimated price per liter.

For example: using $0.628 , multiply by USD/TRY (17 TL), Special Ratio (2.1) and Upperlimit (1.03). An average cost per liter of gasoline is 23.09TL

The similar calculation applies to Diesel.

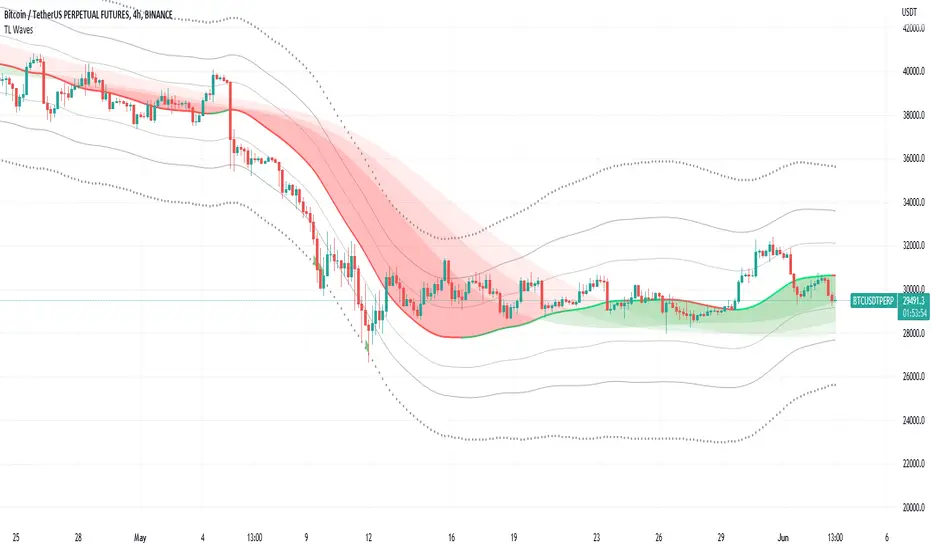

TL WavesI created this indicator inspired by the miyuki waves indicator by eto_miyuki. In my indicator we have 17 types of moving averages which can be selected in the settings.

It is a trend indicator, the base of the wave is a moving average and 4 Average True Range (ATR) Bands derived from the baseline are formed.

There are also 3 moving averages in a guppy style, these 3 moving averages can also be configured.

The moving average options are:

SMA ---> Simple

WMA ---> Weighted

VWMA ---> Volume Weighted

EMA ---> Exponential

DEMA ---> Double EMA

ALMA ---> Arnaud Legoux

HMA ---> Hull MA

SMMA ---> Smoothed

LSMA ---> Least Squares

KAMA ---> Kaufman Adaptive

TEMA ---> Triple EMA

ZLEMA ---> Zero Lag

FRAMA ---> Fractal Adaptive

VIDYA ---> Variable Index Dynamic Average

JMA ---> Jurik Moving Average

T3 ---> Tillson

TRIMA ---> Triangular

All settings are available for changing inputs.

Numbers RenkoRenko with Volume and Time in the box was developed by David Weis (Authority on Wyckoff method) and his student.

I like this style (I don't know what it is officially called) because it brings out the potential of Wyckoff method and Renko, and looks beautiful.

I can't find this style Indicator anywhere, so I made something like it, then I named "Numbers Renko" (数字 練行足 in Japanese).

Caution : This indicator only works exactly in Renko Chart.

////////// Numbers Renko General Settings //////////

Volume Divisor : To make good looking Volume Number.

ex) You set 100. When Volume is 0.056, 0.05 x 100 = 5.6. 6 is plotted in the box (Decimal are round off).

Show Only Large Renko Volume : show only Renko Volume which is larger than Average Renko Volume (it is calculated by user selected moving average, option below).

Show Renko Time : "Only Large Renko Time" show only Renko Time which is larger than Average Renko Time (it is calculated by user selected moving average, option below).

EMA period for calculation : This is used to calculate Average Renko Time and Average Renko Volume (These are used to decide Numbers colors and Candles colors). Default is EMA, You can choice SMA.

////////// Numbers Renko Coloring //////////

The Numbers in the box are color coded by compared the current Renko Volume with the Average Renko Volume.

If the current Renko Volume is 2 times larger than the ARV, Color2 will be used. If the current Renko Volume is 1.5 times larger than the ARV, Color1.5 will be used. Color1 If the current Renko Volume is larger than the ARV . Color0.5 is larger than half Athe RV and Color0 is less than or equal to half the ARV. Color1, Color1.5 and Color2 are Large Value, so only these colored Numbers are showed when use "Show Only ~ " option.

Default is Renko Volume based Color coding, You can choice Renko Time based Color coding. Therefore you can use two type coloring at the same time. ex) The Numbers Colors are Renko Volume based. Candle body, border and wick Colors are Renko Time based.

////////// Weis Wave Volume //////////

Show Effort vs Result : Weis Wave Volume divided by Wave Length.

ex) If 100 Up WWV is accumulated between 30 Up Renko Box, 100 / 30 = 3.33... will be 3.3 (Second decimal will be rounded off).

No Result Ratio : If current "Effort vs Result" is "No Result Ratio" times larger than Average Effort vs Result, Square Mark will be show. AEvsR is calculated by 5SMA.

ex) You set 1.5. If Current EvsR is 20 and AEvsR is 10, 20 > 10 x 1.5 then Square Mark will be show.

If the left and right arrows are in the same direction, the right arrow is omitted.

Show Comparison Marks : Show left side arrow by compare current value to previous previous value and show right side small arrow by compare current value to previous value.

ex) Current Up WWV is 17 and Previous Up WWV (previous previous value) is 12, left side arrow is Up. Previous Dn WWV is 20, right side small arrow is Dn.

Large Volume Ratio : If current WWV is "Large Volume Ratio" times larger than Average WWV, Large WWV color is used.

Sample layout

Natenberg's VolatilityThis indicator is historical volatility indicator created by Sheldon Natenberg , as the standard deviation of the logarithmic price changes measured at regular intervals of time.

In Mr. Natenberg's book, Option Volatility & Pricing, he covers volatility in detail and gives the formula for computing historical volatility.

My changes :

I didn't changed formula, i just added smooth version of volatility it can be used as trigger when cross(over/under) non-smoothed volatility.

Note:

There is two formulas for daily and weekly. Indicator showing only daily formula !

Who wants to display the weekly formula change line 17, namely remove "//"

Enjoy!

S and R (618-382)This script is based on Donchian channels.

It uses tree periods, 17, 72 and 305. You can also change it to 72, 305 and 1292.

The indicator calculates the channel and the 618 and 382 levels inside the channel.

If the price is above the level 618 then a support line apears indicating it with a light color.

if the price is under the level 382 then a resistance line apears indicating it with a dark color.

the small channel is Lime / Green

the medium channel is Yellow / Orange

the big channel is Red / Maroon.

Above all light colors a trend up.

under all dark colors a trend down.

Bitcoin Power Law Bands (BTC Power Law) Indicator█ OVERVIEW

The 'Bitcoin Power Law Bands' indicator is a set of three US dollar price trendlines and two price bands for bitcoin , indicating overall long-term trend, support and resistance levels as well as oversold and overbought conditions. The magnitude and growth of the middle (Center) line is determined by double logarithmic (log-log) regression on the entire USD price history of bitcoin . The upper (Resistance) and lower (Support) lines follow the same trajectory but multiplied by respective (fixed) factors. These two lines indicate levels where the price of bitcoin is expected to meet strong long-term resistance or receive strong long-term support. The two bands between the three lines are price levels where bitcoin may be considered overbought or oversold.

All parameters and visuals may be customized by the user as needed.

█ CONCEPTS

Long-term models

Long-term price models have many challenges, the most significant of which is getting the growth curve right overall. No one can predict how a certain market, asset class, or financial instrument will unfold over several decades. In the case of bitcoin , price history is very limited and extremely volatile, and this further complicates the situation. Fortunately for us, a few smart people already had some bright ideas that seem to have stood the test of time.

Power law

The so-called power law is the only long-term bitcoin price model that has a chance of survival for the years ahead. The idea behind the power law is very simple: over time, the rapid (exponential) initial growth cannot possibly be sustained (see The seduction of the exponential curve for a fun take on this). Year-on-year returns, therefore, must decrease over time, which leads us to the concept of diminishing returns and the power law. In this context, the power law translates to linear growth on a chart with both its axes scaled logarithmically. This is called the log-log chart (as opposed to the semilog chart you see above, on which only one of the axes - price - is logarithmic).

Log-log regression

When both price and time are scaled logarithmically, the power law leads to a linear relationship between them. This in turn allows us to apply linear regression techniques, which will find the best-fitting straight line to the data points in question. The result of performing this log-log regression (i.e. linear regression on a log-log scaled dataset) is two parameters: slope (m) and intercept (b). These parameters fully describe the relationship between price and time as follows: log(P) = m * log(T) + b, where P is price and T is time. Price is measured in US dollars , and Time is counted as the number of days elapsed since bitcoin 's genesis block.

DPC model

The final piece of our puzzle is the Dynamic Power Cycle (DPC) price model of bitcoin . DPC is a long-term cyclic model that uses the power law as its foundation, to which a periodic component stemming from the block subsidy halving cycle is applied dynamically. The regression parameters of this model are re-calculated daily to ensure longevity. For the 'Bitcoin Power Law Bands' indicator, the slope and intercept parameters were calculated on publication date (March 6, 2022). The slope of the Resistance Line is the same as that of the Center Line; its intercept was determined by fitting the line onto the Nov 2021 cycle peak. The slope of the Support Line is the same as that of the Center Line; its intercept was determined by fitting the line onto the Dec 2018 trough of the previous cycle. Please see the Limitations section below on the implications of a static model.

█ FEATURES

Inputs

• Parameters

• Center Intercept (b) and Slope (m): These log-log regression parameters control the behavior of the grey line in the middle

• Resistance Intercept (b) and Slope (m): These log-log regression parameters control the behavior of the red line at the top

• Support Intercept (b) and Slope (m): These log-log regression parameters control the behavior of the green line at the bottom

• Controls

• Plot Line Fill: N/A

• Plot Opportunity Label: Controls the display of current price level relative to the Center, Resistance and Support Lines

Style

• Visuals

• Center: Control, color, opacity, thickness, price line control and line style of the Center Line

• Resistance: Control, color, opacity, thickness, price line control and line style of the Resistance Line

• Support: Control, color, opacity, thickness, price line control and line style of the Support Line

• Plots Background: Control, color and opacity of the Upper Band

• Plots Background: Control, color and opacity of the Lower Band

• Labels: N/A

• Output

• Labels on price scale: Controls the display of current Center, Resistance and Support Line values on the price scale

• Values in status line: Controls the display of current Center, Resistance and Support Line values in the indicator's status line

█ HOW TO USE

The indicator includes three price lines:

• The grey Center Line in the middle shows the overall long-term bitcoin USD price trend

• The red Resistance Line at the top is an indication of where the bitcoin USD price is expected to meet strong long-term resistance

• The green Support Line at the bottom is an indication of where the bitcoin USD price is expected to receive strong long-term support

These lines envelope two price bands:

• The red Upper Band between the Center and Resistance Lines is an area where bitcoin is considered overbought (i.e. too expensive)

• The green Lower Band between the Support and Center Lines is an area where bitcoin is considered oversold (i.e. too cheap)

The power law model assumes that the price of bitcoin will fluctuate around the Center Line, by meeting resistance at the Resistance Line and finding support at the Support Line. When the current price is well below the Center Line (i.e. well into the green Lower Band), bitcoin is considered too cheap (oversold). When the current price is well above the Center Line (i.e. well into the red Upper Band), bitcoin is considered too expensive (overbought). This idea alone is not sufficient for profitable trading, but, when combined with other factors, it could guide the user's decision-making process in the right direction.

█ LIMITATIONS

The indicator is based on a static model, and for this reason it will gradually lose its usefulness. The Center Line is the most durable of the three lines since the long-term growth trend of bitcoin seems to deviate little from the power law. However, how far price extends above and below this line will change with every halving cycle (as can be seen for past cycles). Periodic updates will be needed to keep the indicator relevant. The user is invited to adjust the slope and intercept parameters manually between two updates of the indicator.

█ RAMBLINGS

The 'Bitcoin Power Law Bands' indicator is a useful tool for users wishing to place bitcoin in a macro context. As described above, the price level relative to the three lines is a rough indication of whether bitcoin is over- or undervalued. Users wishing to gain more insight into bitcoin price trends may follow the author's periodic updates of the DPC model (contact information below).

█ NOTES

The author regularly posts on Twitter using the @DeFi_initiate handle.

█ THANKS

Many thanks to the following individuals, who - one way or another - made the 'Bitcoin Power Law Bands' indicator possible:

• TradingView user 'capriole_charles', whose open-source 'Bitcoin Power Law Corridor' script was the basis for this indicator

• Harold Christopher Burger, whose Bitcoin’s natural long-term power-law corridor of growth article (2019) was the basis for the 'Bitcoin Power Law Corridor' script

• Bitcoin Forum user "Trololo", who posted the original power law model at Logarithmic (non-linear) regression - Bitcoin estimated value (2014)

Double_Based_EMA_v2Developmment of Double_Based_EMA. The version 2 brings a set of emas, with 8, 34, 144 ,610 periods.

The price source is the closes inside the upper or lower range of the Donchian Chanell with the same period.

The reading is the same as My Script 44.

The price will try to reach the next level of EMA.

if $ >8 will try 34.

if $ >8 and 8>34 will try 144.

if $ >8 and 8>34 and 34>144 will try 610.

if $ <8 will try 34.

if $ <8 and 8<34 will try 144.

if $ <8 and 8<34 and 34<144 will try 610.

//---- Consolidation

The price will oscilate between the highest ema and it´s next in period . Eg 34 > 8 > 610 > 144. $ < 34 will try 144.

The price will oscilate betwenn the lowest ema and it´s next in period. Eg 610 > 34 > 8 > 144. $ > 144 will try 610.

//---

Observe how $ swing between the emas

8 <-> 34

8 <-> 34 <-> 144

34 <-> 144 <-> 610

//---

$ > 8 > 34 > 144 > 610 - pure trend up

S < 8 < 34 < 144 < 610 - pure trend dw

//--- Optional periods - 17 , 72 , 305 , 1292

Enjoy, comment.

Silen's Financials Fair ValueIt is finally here! 🔥 My 3rd and most important script in my Financial series! 🚀

Ever imagined to see all fundamentals (or many that is) combined into one indicator that is right on your chart, showing you how your favorite stock is trading compared to its fundamentals?

Well, here is your answer! 📡

____________________________________________________________________________________________

This script shows you my own personal interpretation of fair value, based solely on the financial fundamentals of a company compared to market averages.

I don't believe that certain sectors of the market should be priced higher than others. If you look at historical data you'll see that favored sectors always rotate - placing insanely high P/E multiples on some sectors. Once they are "out" and people rotate away from those sectors you're left with nothing but the naked fundamentals that matter. So, you'll see many companies, that have been doing well on paper, see their share price decline by 70-90% for no other reasons than people favoring other sectors.

That's why it's even more important to focus on fair value that is solely fundamentals-based. Know when your stock gets to expensive. 🤯

____________________________________________________________________________________________

To give you some examples:

- Most Megacaps trade at historically high valuations, several times my fair value. Those include AAPL, MSFT, NVDA, AMZN, TSLA, JPM, TSM, V and so on. And no, in the past they partially traded below (my) fair value.

- Most Cybersecurity / Cloud companies are trading at truly massive multiples of my fair value. (NET, DDOG, etc)

- Many Smallcaps & Midcaps are trading several multiples (OESX, CODX, QFIN) below my fair value. And no, in the past they partially traded above (my) fair value.

Ok, so much about the market. You ultimately decide how much you want to orientate on fair value. 👨🏫

____________________________________________________________________________________________

This fair value indicator (purple line):

Takes the P/E rate of the company and compares it to the market (50% weight)

Takes the P/S rate of the company and compares it to the market (50% weight)

Then adds boni and mali f or debt/equity rates and debt and equity itself

Also looks at past growth and calculates future P/E and P/S rates which adds , in some cases, value to the fair value (green line)

Also compares how historical valuations have behaved compared to fair value and simulates a fair value guideline (dark blue line)

____________________________________________________________________________________________

This script is part 3️⃣ of a series of indicators that work well together.

Script 1️⃣ of the series is:

P/E & P/S Rates

Script 2️⃣ of the series is:

Debt & Equity

If you use all 3 scripts together it will look like this, giving you truly deep and simple information about the fundamentals of a company:

Example 1 - AMD

Example 2 - HZO

Example 3 - APPS

I hope this script makes your investing and stock picks a lot easier! 🔆💹🕗

Disclaimer: Fair value is always subjective. There are many different approaches to fair value. This one is only my personal interpretation.

Disclaimer 2: This script works only for the Day-Timeframe.

Disclaimer 3: This script uses 17,5 P/E and 3,0 P/S as market averages. The actual average keeps changing but, historically speaking, these seemed to be good numbers.

Feel free to share your thoughts and feedback! 🙃

action zone - ATR stop reverse order strategy v0.1 by 9nckACTION ZONE-ATR MOD v0.1 DOCUMENTATION

Overview

This tradingview pine script strategy is mainly created to enrich my coding skill. It is a combination of “CDC-ACTIONZONE” and my personal studies of trading techniques in various sources e.g.book, course or blog. This strategy purposefully built to connect with my automatic trading bot. However, It will be very useful to aid your trading routine by diminishing mental distraction which possibly leads to bad trades.

How does it work?

This strategy will do a basic simple thing that most traders do by creating entry signals on both sides long/short and also set the stop loss. Furthermore, It will also reverse the order (from long to short and vice versa (if long/short conditions are met). Finally, it will recalculate the stop loss/take profit price in every complete bar to increase the chance of winning and limit our loss.

Entry rules(Long/Short)

If you have no open order, an order will be created when a fast EMA crosses(up(long)/down(short) the slow EMA(It’s as simple as that).

If you have an open order, the current order will be (sold if long, covered if short) and the opposite side order will be created.

Exit and Reverse rules(Long/Short)

If fast EMA cross (DOWN(long), UP(short)), the current order will be closed, THE OPPOSITE SIDE ORDER WILL ALSO BE CREATED.

Risk management

FLEX STOP PRICE : initial value will be set at the bar which order created. It is a fast ema (+/-) MIDDLE ATR value.

If MIDDLE ATR value rises, it will be our new stop price.

If MIDDLE ATR value falls, stop price unchanged

If Price OVERBOUGHT(long)/SOLD(short), LOW of that bar will be a new stop price.

Minimum position hold period

In order to eliminate risk of repeatedly open, close orders in sideway trends. Minimum hold period must be passed to start exit our position. However, It always respects stop loss prices. The value refers to the number of bars.

MUST READ!!!

This strategy uses only MARKET ORDER. If you trade with a bot, make sure you choose only enormous market cap tokens.

This strategy is bi-direction strategy. It will work best in the DERIVATIVE market.

It was initially designed to compete in the cryptocurrency market which has very high volume and volatility.

I only use this strategy in 1HR (acceptable change rate, optimum trade frequency)

How (should) we use it?

Choose crypto future pairs (recommend only top 10-15 market volume pairs in Binance, let’s say 1000M+ trade value)

Choose your time frame (1H is strongly recommended)

Setup your portfolio profile (Setting->Properties) such as Initial cap, order size, commission. DO NOT USE CAL ON EVERY TICK IT WILL CAUSE REPAINTING AND YOUR CAPITAL IS BLEEDING !!!

BACKTEST FIRST!! Back test is a combination of art, math and statis(and a bit of luck). You can apply to train and test methods or whatever you are familiar with. In my opinion, your test period should include UPTREND, SIDEWAY, DOWNTREND. Fine tune fast, slow ema first(my best ema length of 1H timeframe around 7-10, 17-22). Try to eliminate fault breakout trade and use other options only necessary. Hopefully we can use automatic optimization on Pine Script soon.

Don’t forget to turn off using a specific backtest date option to start your strategy.A

THIS IS NOT A PERFECT (OR EVEN PROFITABLE) STRATEGY. USE AT YOUR OWN RISK AND TRADE RESPONSIBLY. DYOR DUDE.

FII and DII Data

Greetings to All of you.

The script is plotting FII & DII activity of buying or selling on Daily TimeFrame of Nifty Spot.

Will display only on Nifty 50 Spot on Daily TimeFrame . Codes are hardcoded because novice to PineScripting.

Data is collected from NSE website on daily basis, it's an manual process.

Observation:

Start date of observation is 16th Nov., 2021. FII bought worth 14,240 & kept buying for next 2 days & bought stocks worth 17,760 crores. But market kept falling as we can see in the chart.

Now FII's started selling & in next 5 days they sold stocks worth 18,698 crores. What makes sense from this is might have cut their losses early. FII's kept selling & Nifty made an low of 16410.

FII had sold stocks worth -21,954 crores.

FII are negative & the top green box which you see is FII & DII activity from 19th Oct 2021 when Nifty Spot made an High of 18604.45.

As of 14th Jan.,2022 they are still Negative & DII are extremely positive.

NOTE: DII have not sold any thing yet. They are PLUS +74,428 Crore . Now if they start selling we need to take care of our portfolio.

Hope the information might help in someway.

Take Care & Stay Safe why because Health is Wealth.

PS: If you have any better way to improve the hard coded codes please enlighten. Thank you in advance

5min Williams Fractals scalping (3commas)Another strategy I'm learning Pine Script on. It is inspired by a MoneyZG youtube strategy called "Easy 5 Minute Scalping Strategy (Simple to Follow Scalping Trading Strategy)".

Again this is a one order per trade strategy compatible with the 3commas bot (works also with the free 3commas subscription). This strategy is based on the signals from Williams Fractals, taking the signals in reverse - red triangle indicates a bottom and hence we go long. The green triangle indicates a top so we go short. By default these signals are only accepted if they occur between the two Emas. However, you can also turn this off and when a WF signal comes in, only the current price has to be between the Emas. Stop loss is set to the current Ema slow and the take profit is a multiple of the distance to the slow ema.

Like previously I have added different filters as well as the ability to view essential things like the WF signal and Emas. I hope the script will help you to be more successful and if so it would be great if you could share here your setups, or tips on what would be good to refine to make it an even a more profitable strategy. Kind of a community approach so that we help each other out :).

Instructions for the 3commas connector:

1. First, you need to prepare 3commas Long/Short bots that will only listen to custom TV signals.

2. Inputs for the 3commas bot can be found at the end of the user inputs.

3. Once you have entered the required details into the inputs, turn on 3commas comments. They should appear on the chart (looks messy).

4. Now you can add the alert where you should paste the 3commas Webhook URL: 3commas.io

5. For the alert message text insert the placeholder {{strategy.order.comment}} and delete the rest.

6. Once the alert is saved, you can turn off those 3commas comments to have a clearer chart.

7. With a new alert, the bot and trade should launch.

In the near future I would like to publish more scripts that will carry similar elements as the first two, incl. compatibility with 3commas (I don't have access to another bot system). I will choose some strategies myself, but I will also be glad for some tips on what strategy would be good to do and is still missing here on Tradingview (short youtube videos or brief strategy manuals would be great).

Thanks and keep it up

PS: My screen values starting at Long Target Profit and ending at Pullback NOT greater than: 1.5; 1.5; 0; ON; 1; 2; OFF; 17; 36; ON; 0.05; ON; Chart; 14; 46; 50; 48.5; 51; OFF; 1; ON; 4; 2.

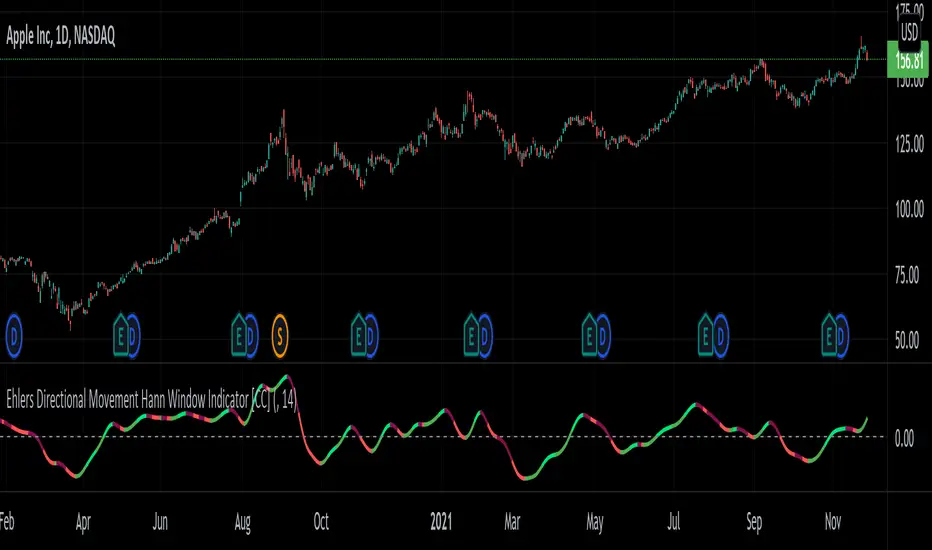

Ehlers Directional Movement Hann Window Indicator [CC]The Directional Movement Hann Window Indicator was created by John Ehlers (Stocks and Commodities Dec 2021 pgs 17-18) and this is his updated version of the classic Directional Movement indicator created by J. Welles Wilder. Ehlers uses the Hann Window Filtering after using an exponential moving average to smooth the classic directional movement indicator. This helps significantly with the lag and lack of smoothing which are both issues with the classic indicator. I have included strong buy and sell signals in addition to the normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators you would like to see me publish!

BollingerBands Strat + pending order alerts via TradingConnectorSoftware part of algotrading is simpler than you think. TradingView is a great place to do this actually. To present it, I'm publishing each of the default strategies you can find in Pinescript editor's "built-in" list with slight modification - I'm only adding 2 lines of code, which will trigger alerts, ready to be forwarded to your broker via TradingConnector and instantly executed there. Alerts added in this script: 14, 17, 20 and 23.

SCRIPT INCLUDES PENDING ORDERS AND ALERTS! Alert will be sent to MetaTrader when order is triggered, but not yet filled. That means if market conditions change and order does not get filled, it needs to be cancelled as well, and there are alerts for that in the script as well.

How it works:

1. TradingView alert fires.

2. TradingConnector catches it and forwards to MetaTrader4/5 you got from your broker.

3. Trade gets executed inside MetaTrader within 1 second of fired alert.

When configuring alert, make sure to select "alert() function calls only" in CreateAlert popup. One alert per ticker is required.

Adding stop-loss, take-profit, trailing-stop, break-even or executing pending orders is also possible. These topics have been covered in other example posts.

This routing works for Forex, indices, stocks, crypto - anything your broker offers via their MetaTrader4 or 5.

Disclaimer: This concept is presented for educational purposes only. Profitable results of trading this strategy are not guaranteed even if the backtest suggests so. By no means this post can be considered a trading advice. You trade at your own risk.

If you are thinking to execute this particular strategy, make sure to find the instrument, settings and timeframe which you like most. You can do this by your own research only.