E9 PLRRThe E9 PLRR (Power Law Residual Ratio) is a custom-built indicator designed to evaluate the overvaluation or undervaluation of an asset, specifically by utilizing logarithmic price data and a power law-based model. It leverages a dynamic regression technique to assess the deviation of the current price from its expected value, giving insights into how much the price deviates from its long-term trend.

This indicator is primarily used to detect market extremes and cycles, often used in the analysis of long-term price movements in assets like Bitcoin, where cyclical behavior and significant price deviations are common.

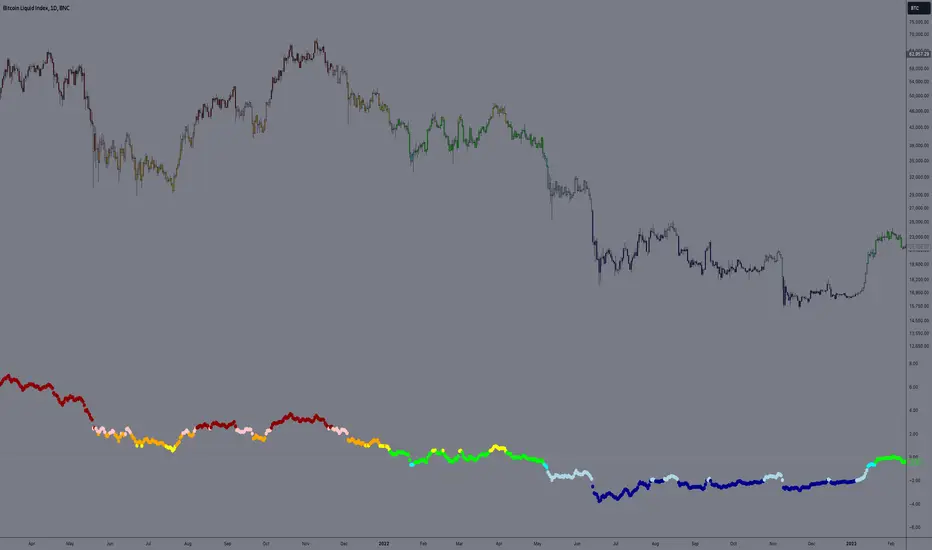

This chart is back from 2019 and shows (From left to right) 2018 Bear market bottom at $3.5k (Dark Blue) , following a peak at 12k (dark red) before the Covid crash back down to EUROTLX:4K (Dark blue)

Key Components

Logarithmic Price Data:

The indicator works with logarithmic price data (ohlc4), which represents the average of open, high, low, and close prices. The logarithmic transformation is crucial in financial modeling, especially when analyzing long-term price data, as it normalizes exponential price growth patterns.

Dynamic Exponent 𝑘:

The model calculates a dynamic exponent k using regression, which defines the power law relationship between time and price. This exponent is essential in determining the expected power law price return and how far the current price deviates from that expected trend.

Power Law Price Return:

The power law price return is computed using the dynamic exponent

k over a defined period, such as 365 days (1 year). It represents the theoretical price return based on a power law relationship, which is used to compare against the actual logarithmic price data.

Risk-Free Rate:

The indicator incorporates an adjustable risk-free rate, allowing users to model the opportunity cost of holding an asset compared to risk-free alternatives. By default, the risk-free rate is set to 0%, but this can be modified depending on the user's requirements.

Volatility Adjustment:

A key feature of the PLRR is its ability to adjust for price volatility. The indicator smooths out short-term price fluctuations using a moving average, helping to detect longer-term cycles and trends.

PLRR Calculation:

The core of the indicator is the calculation of the Power Law Residual Ratio (PLRR). This is derived by subtracting the expected power law price return and risk-free rate from the logarithmic price return, then multiplying the result by a user-defined multiplier.

Color Gradient:

The PLRR values are represented visually using a color gradient. This gradient helps the user quickly identify whether the asset is in an undervalued, fair value, or overvalued state:

Dark Blue to Light Blue: Indicates undervaluation, with increasing blue tones representing a higher degree of undervaluation.

Green to Yellow: Represents fair value, where the price is aligned with the expected power law return.

Orange to Dark Red: Indicates overvaluation, with increasing red tones representing a higher degree of overvaluation.

Zero Line:

A zero line is plotted on the indicator chart, serving as a reference point. Values above the zero line suggest potential overvaluation, while values below indicate potential undervaluation.

Dots Visualization:

The PLRR is plotted using dots, with each dot color-coded based on the PLRR value. This dot-based visualization makes it easier to spot significant changes or reversals in market sentiment without overwhelming the user with continuous lines.

Bar Coloring:

The chart’s bars are colored in accordance with the PLRR value at each point in time, making it visually clear when an asset is potentially overvalued or undervalued.

Indicator Functionality

Cycle Identification : The E9 PLRR is especially useful for identifying cyclical market behavior. In assets like Bitcoin, which are known for their boom-bust cycles, the PLRR can help pinpoint when the market is likely entering a peak (overvaluation) or a trough (undervaluation).

Overvaluation and Undervaluation Detection: By comparing the current price to its expected power law return, the PLRR helps traders assess whether an asset is trading above or below its fair value. This is critical for long-term investors seeking to enter the market at undervalued levels and exit during periods of overvaluation.

Trend Following: The indicator helps users identify the broader trend by smoothing out short-term volatility. This makes it useful for both momentum traders looking to ride trends and contrarian traders seeking to capitalize on market extremes.

Customization

The E9 PLRR allows users to fine-tune several parameters based on their preferences or specific market conditions:

Lookback Period:

The user can adjust the lookback period (default: 100) to modify how the moving average and regression are calculated.

Risk-Free Rate:

Adjusting the risk-free rate allows for more realistic modeling of the opportunity cost of holding the asset.

Multiplier:

The multiplier (default: 5.688) amplifies the sensitivity of the PLRR, allowing users to adjust how aggressively the indicator responds to price movements.

This indicator was inspired by the works of Ashwin & PlanG and their work around powerLaw. Thank you. I hall be working on the calculation of this indicator moving forward to make improvements and optomisations.

Cari dalam skrip untuk "Cycle"

Ehlers Stochastic Center Of Gravity [CC]The Stochastic Center Of Gravity Indicator was created by John Ehlers (Cybernetic Analysis For Stocks And Futures pgs 79-80), and this is one of the many cycle scripts that I have created but not published yet because, to be honest, I don't use cycle indicators in my everyday trading. Many of you probably do, so I will start publishing my big backlog of cycle-based indicators. These indicators work best with a trend confirmation or some other confirmation indicator to pair with it. The current cycle is the length of the trend, and since most stocks generally change their underlying trend quite often, especially during the day, it makes sense to adjust the length of this indicator to match the stock you are using it on. As you can see, the indicator gives constant buy and sell signals during a trend which is why I recommend using a confirmation indicator.

I have color-coded it to use lighter colors for normal signals and darker colors for strong signals. Buy when the line turns green and sell when it turns red.

Let me know if there are any other scripts you would like to see me publish!

BTC Fear & Greed Incremental StrategyIMPORTANT: READ SETUP GUIDE BELOW OR IT WON'T WORK

# BTC Fear & Greed Incremental Strategy — TradeMaster AI (Pure BTC Stack)

## Strategy Overview

This advanced Bitcoin accumulation strategy is designed for long-term hodlers who want to systematically take profits during greed cycles and accumulate during fear periods, while preserving their core BTC position. Unlike traditional strategies that start with cash, this approach begins with a specified BTC allocation, making it perfect for existing Bitcoin holders who want to optimize their stack management.

## Key Features

### 🎯 **Pure BTC Stack Mode**

- Start with any amount of BTC (configurable)

- Strategy manages your existing stack, not new purchases

- Perfect for hodlers who want to optimize without timing markets

### 📊 **Fear & Greed Integration**

- Uses market sentiment data to drive buy/sell decisions

- Configurable thresholds for greed (selling) and fear (buying) triggers

- Automatic validation to ensure proper 0-100 scale data source

### 🐂 **Bull Year Optimization**

- Smart quarterly selling during bull market years (2017, 2021, 2025)

- Q1: 1% sells, Q2: 2% sells, Q3/Q4: 5% sells (configurable)

- **NO SELLING** during non-bull years - pure accumulation mode

- Preserves BTC during early bull phases, maximizes profits at peaks

### 🐻 **Bear Market Intelligence**

- Multi-regime detection: Bull, Early Bear, Deep Bear, Early Bull

- Different buying strategies based on market conditions

- Enhanced buying during deep bear markets with configurable multipliers

- Visual regime backgrounds for easy market condition identification

### 🛡️ **Risk Management**

- Minimum BTC allocation floor (prevents selling entire stack)

- Configurable position sizing for all trades

- Multiple safety checks and validation

### 📈 **Advanced Visualization**

- Clean 0-100 scale with 2 decimal precision

- Three main indicators: BTC Allocation %, Fear & Greed Index, BTC Holdings

- Real-time portfolio tracking with cash position display

- Enhanced info table showing all key metrics

## How to Use

### **Step 1: Setup**

1. Add the strategy to your BTC/USD chart (daily timeframe recommended)

2. **CRITICAL**: In settings, change the "Fear & Greed Source" from "close" to a proper 0-100 Fear & Greed indicator

---------------

I recommend Crypto Fear & Greed Index by TIA_Technology indicator

When selecting source with this indicator, look for "Crypto Fear and Greed Index:Index"

---------------

3. Set your "Starting BTC Quantity" to match your actual holdings

4. Configure your preferred "Start Date" (when you want the strategy to begin)

### **Step 2: Configure Bull Year Logic**

- Enable "Bull Year Logic" (default: enabled)

- Adjust quarterly sell percentages:

- Q1 (Jan-Mar): 1% (conservative early bull)

- Q2 (Apr-Jun): 2% (moderate mid bull)

- Q3/Q4 (Jul-Dec): 5% (aggressive peak targeting)

- Add future bull years to the list as needed

### **Step 3: Fine-tune Thresholds**

- **Greed Threshold**: 80 (sell when F&G > 80)

- **Fear Threshold**: 20 (buy when F&G < 20 in bull markets)

- **Deep Bear Fear Threshold**: 25 (enhanced buying in bear markets)

- Adjust based on your risk tolerance

### **Step 4: Risk Management**

- Set "Minimum BTC Allocation %" (default 20%) - prevents selling entire stack

- Configure sell/buy percentages based on your position size

- Enable bear market filters for enhanced timing

### **Step 5: Monitor Performance**

- **Orange Line**: Your BTC allocation percentage (target: fluctuate between 20-100%)

- **Blue Line**: Actual BTC holdings (should preserve core position)

- **Pink Line**: Fear & Greed Index (drives all decisions)

- **Table**: Real-time portfolio metrics including cash position

## Reading the Indicators

### **BTC Allocation Percentage (Orange Line)**

- **100%**: All portfolio in BTC, no cash available for buying

- **80%**: 80% BTC, 20% cash ready for fear buying

- **20%**: Minimum allocation, maximum cash position

### **Trading Signals**

- **Green Buy Signals**: Appear during fear periods with available cash

- **Red Sell Signals**: Appear during greed periods in bull years only

- **No Signals**: Either allocation limits reached or non-bull year

## Strategy Logic

### **Bull Years (2017, 2021, 2025)**

- Q1: Conservative 1% sells (preserve stack for later)

- Q2: Moderate 2% sells (gradual profit taking)

- Q3/Q4: Aggressive 5% sells (peak targeting)

- Fear buying active (accumulate on dips)

### **Non-Bull Years**

- **Zero selling** - pure accumulation mode

- Enhanced fear buying during bear markets

- Focus on rebuilding stack for next bull cycle

## Important Notes

- **This is not financial advice** - backtest thoroughly before use

- Designed for **long-term holders** (4+ year cycles)

- **Requires proper Fear & Greed data source** - validate in settings

- Best used on **daily timeframe** for major trend following

- **Cash calculations**: Use allocation % and BTC holdings to calculate available cash: `Cash = (Total Portfolio × (1 - Allocation%/100))`

## Risk Disclaimer

This strategy involves active trading and position management. Past performance does not guarantee future results. Always do your own research and never invest more than you can afford to lose. The strategy is designed for educational purposes and long-term Bitcoin accumulation thesis.

---

*Developed by Sol_Crypto for the Bitcoin community. Happy stacking! 🚀*

Global M2 Money Supply Growth (GDP-Weighted)📊 Global M2 Money Supply Growth (GDP-Weighted)

This indicator tracks the weighted aggregate M2 money supply growth across the world's four largest economies: United States, China, Eurozone, and Japan. These economies represent approximately 69.3 trillion USD in combined GDP and account for the majority of global liquidity, making this a comprehensive macro indicator for analyzing worldwide monetary conditions.

════════════════════════════════════════════

🔧 KEY FEATURES:

📈 GDP-Weighted Aggregation

Each economy is weighted proportionally by its nominal GDP using 2025 IMF World Economic Outlook data:

• United States: 44.2% (30.62 trillion USD)

• China: 28.0% (19.40 trillion USD)

• Eurozone: 21.6% (15.0 trillion USD)

• Japan: 6.2% (4.28 trillion USD)

The weights are fully adjustable through the indicator settings, allowing you to update them annually as new IMF forecasts are released (typically April and October).

⏱️ Multiple Time Period Options

Choose between three calculation methods to analyze different timeframes:

• YoY (Year-over-Year): 12-month growth rate for identifying long-term liquidity trends and cycles

• MoM (Month-over-Month): 1-month growth rate for detecting short-term monetary policy shifts

• QoQ (Quarter-over-Quarter): 3-month growth rate for medium-term trend analysis

🔄 Advanced Offset Function

Shift the entire indicator forward by 0-365 days to test lead/lag relationships between global liquidity and asset prices. Research suggests a 56-70 day lag between M2 changes and Bitcoin price movements, but you can experiment with different offsets for various assets (equities, gold, commodities, etc.).

🌍 Individual Country Breakdown

Real-time display of each economy's M2 growth rate with:

• Current percentage change (YoY/MoM/QoQ)

• GDP weight contribution

• Color-coded values (green = monetary expansion, red = contraction)

📊 Smart Overlay Capability

Displays directly on your main price chart with an independent left-side scale, allowing you to visually correlate global liquidity trends with any asset's price action without cluttering the chart.

🔧 Customizable GDP Weights

All GDP values can be adjusted through the indicator settings without editing code, making annual updates simple and accessible for all users.

════════════════════════════════════════════

📡 DATA SOURCES:

All M2 money supply data is sourced from ECONOMICS (Trading Economics) for consistency and reliability:

• ECONOMICS:USM2 (United States)

• ECONOMICS:CNM2 (China)

• ECONOMICS:EUM2 (Eurozone)

• ECONOMICS:JPM2 (Japan)

All values are normalized to USD using current daily exchange rates (USDCNY, EURUSD, USDJPY) before GDP-weighted aggregation, ensuring accurate cross-country comparisons.

══════════════════════════════════════════════

💡 USE CASES & APPLICATIONS:

🔹 Liquidity Cycle Analysis

Track global monetary expansion/contraction cycles to identify when central banks are coordinating loose or tight monetary policies.

🔹 Market Timing & Risk Assessment

High M2 growth (>10%) historically correlates with risk-on environments and rising asset prices across crypto, equities, and commodities. Negative M2 growth signals monetary tightening and potential market corrections.

🔹 Bitcoin & Crypto Correlation

Compare with Bitcoin price using the offset feature to identify the optimal lag period. Many traders use 60-70 day offsets to predict crypto market movements based on liquidity changes.

🔹 Macro Portfolio Allocation

Use as a regime filter to adjust portfolio exposure: increase risk assets during liquidity expansion, reduce during contraction.

🔹 Central Bank Policy Divergence

Monitor individual country metrics to identify when major central banks are pursuing divergent policies (e.g., Fed tightening while China eases).

🔹 Inflation & Economic Forecasting

Rapid M2 growth often leads inflation by 12-18 months, making this a leading indicator for future inflation trends.

🔹 Recession Early Warning

Negative M2 growth is extremely rare and has preceded major recessions, making this a valuable risk management tool.

════════════════════════════════════════════

📊 INTERPRETATION GUIDE:

🟢 +10% or Higher

Aggressive monetary expansion, typically during crises (2001, 2008, 2020). The COVID-19 period saw M2 growth reach 20-27%, which preceded significant inflation and asset price surges. Strong bullish signal for risk assets.

🟢 +6% to +10%

Above-average liquidity growth. Central banks are providing stimulus beyond normal levels. Generally favorable for equities, crypto, and commodities.

🟡 +3% to +6%

Normal/healthy growth rate, roughly in line with GDP growth plus 2% inflation targets. Neutral environment with moderate support for risk assets.

🟠 0% to +3%

Slowing liquidity, potential tightening phase beginning. Central banks may be raising rates or reducing balance sheets. Caution warranted for high-beta assets.

🔴 Negative Growth

Monetary contraction - extremely rare. Only occurred during aggressive Fed tightening in 2022-2023. Strong warning signal for risk assets, often precedes recessions or major market corrections.

════════════════════════════════════════════

🎯 OPTIMAL USAGE:

📅 Recommended Timeframes:

• Daily or Weekly charts for macro analysis

• Monthly charts for very long-term trends

💹 Compatible Asset Classes:

• Cryptocurrencies (especially Bitcoin, Ethereum)

• Equity indices (S&P 500, NASDAQ, global markets)

• Commodities (Gold, Silver, Oil)

• Forex majors (DXY correlation analysis)

⚙️ Suggested Settings:

• Default: YoY calculation with 0 offset for current liquidity conditions

• Bitcoin traders: YoY with 60-70 day offset for predictive analysis

• Short-term traders: MoM with 0 offset for recent policy changes

• Quarterly rebalancers: QoQ with 0 offset for medium-term trends

════════════════════════════════════════════

📋 VISUAL DISPLAY:

The indicator plots a blue line showing the selected growth metric (YoY/MoM/QoQ), with a dashed reference line at 0% to clearly identify expansion vs. contraction regimes.

A comprehensive table in the top-right corner displays:

• Current global M2 growth rate (large, prominent display)

• Individual country breakdowns with their GDP weights

• Color-coded growth rates (green for positive, red for negative)

════════════════════════════════════════════

🔄 MAINTENANCE & UPDATES:

GDP weights should be updated annually (ideally in April or October) when the IMF releases new World Economic Outlook forecasts. Simply adjust the four GDP input parameters in the indicator settings - no code editing required.

The relative GDP proportions between the Big 4 economies change very gradually (typically <1-2% per year), so even if you update weights once every 1-2 years, the impact on the indicator's accuracy is minimal.

════════════════════════════════════════════

💭 TRADING PHILOSOPHY:

This indicator embodies the principle that "liquidity drives markets." By tracking the combined M2 money supply of the world's largest economies, weighted by their economic size, you gain insight into the fundamental liquidity conditions that underpin all asset prices.

Unlike single-country M2 indicators, this GDP-weighted approach captures the true global picture, accounting for the fact that US monetary policy has 2x the impact of Japanese policy due to economic size differences.

Perfect for macro-focused traders, long-term investors, and anyone seeking to understand the "tide that lifts all boats" in financial markets.

════════════════════════════════════════════

Created for traders and investors who incorporate global liquidity trends into their decision-making process. Best used alongside other technical and fundamental analysis tools for comprehensive market assessment.

⚠️ Disclaimer: M2 money supply is a lagging macroeconomic indicator. Past correlations do not guarantee future results. Always use proper risk management and combine with other analysis methods.

BTC Power-Law Decay Channel Oscillator (0–100)🟠 BTC Power-Law Decay Channel Oscillator (0–100)

This indicator calculates Bitcoin’s position inside its long-term power-law decay channel and normalizes it into an easy-to-read 0–100 oscillator.

🔎 Concept

Bitcoin’s long-term price trajectory can be modeled by a log-log power-law channel.

A baseline is fitted, then an upper band (excess/euphoria) and a lower band (capitulation/fear).

The oscillator shows where the current price sits between those bands:

0 = near the lower band (historical bottoms)

100 = near the upper band (historical tops)

📊 How to Read

Oscillator > 80 → euphoric excess, often cycle tops

Oscillator < 20 → capitulation, often cycle bottoms

Works best on weekly or bi-weekly timeframes.

⚙️ Adjustable Parameters

Anchor date: starting point for the power-law fit (default: 2011).

Smoothing days: moving average applied to log-price (default: 365 days).

Upper / Lower multipliers: scale the bands to align with historical highs and lows.

✅ Best Use

Combine with other cycle signals (dominance ratios, macro indicators, sentiment).

Designed for long-term cycle analysis, not intraday trading.

Fractal Wave MarkerFractal Wave Marker is an indicator that processes relative extremes of fluctuating prices within 2 periodical aspects. The special labeling system detects and visually marks multi-scale turning points, letting you visualize fractal echoes within unfolding cycles dynamically.

What This Indicator Does

Identifies major and minor swing highs/lows based on adjustable period.

Uses Phi in power exponent to compute a higher-degree swing filter.

Labels of higher degree appear only after confirmed base swings — no phantom levels, no hindsight bias. What you see is what the market has validated.

Swing points unfold in a structured, alternating rhythm . No two consecutive pivots share the same hierarchical degree!

Inspired by the Fractal Market Hypothesis, this script visualizes the principle that market behavior repeats across time scales, revealing structured narrative of "random walk". This inherent sequencing ensures fractal consistency across timeframes. "Fractal echoes" demonstrate how smaller price swings can proportionally mirror larger ones in both structure and timing, allowing traders to anticipate movements by recursive patterns. Cycle Transitions highlight critical inflection points where minor pivots flip polarity such as a series of lower highs progress into higher highs—signaling the birth of a new macro trend. A dense dense clusters of swing points can indicate Liquidity Zones, acting as footprints of institutional accumulation or distribution where price action validates supply and demand imbalances.

Visualization of nested cycles within macro trend anchors - a main feature specifically designed for the chartists who prioritize working with complex wave oscillations their analysis.

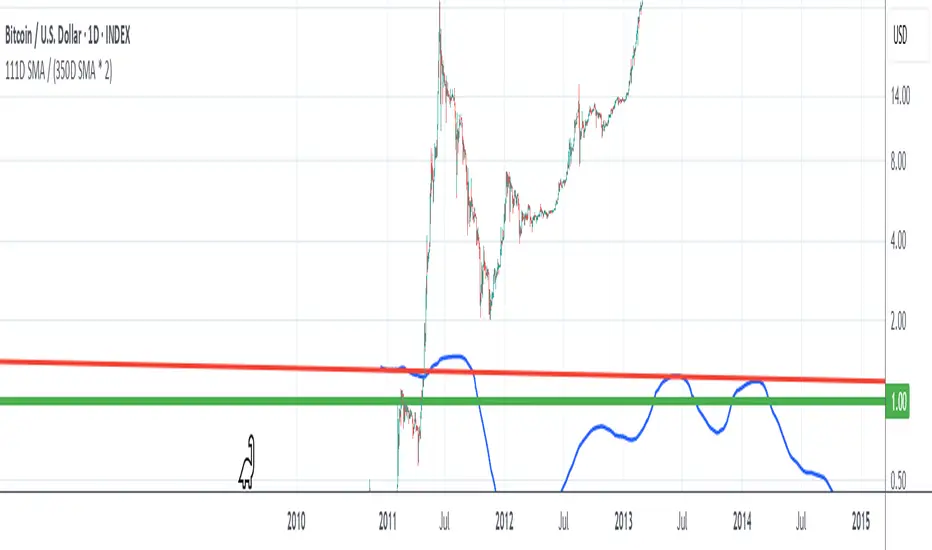

111D SMA / (350D SMA * 2)Indicator: Pi Cycle Ratio

This custom technical indicator calculates a ratio between two moving averages that are used for the PI Cycle Top indicator. The PI Cycle Top indicator triggers when the 111-day simple moving average (111D SMA) crosses up with the 350-day simple moving average (350D SMA *2).

The line value is ratio is calculated as:

Line Value = 111DSMA / (350D SMA × 2)

When the 111D SMA crosses with the 350D SMA triggering the PI Cycle Top, the value of the ratio between the two lines is 1.

This visualizes the ratio between the two moving averages into a single line. This indicator can be used for technical analysis for historical and future moves.

The Investment Clock Orbital GraphThe Investment Clock Orbital Graph is an advanced visualization tool designed to help traders and investors track economic cycles using a dynamic scatter plot of GDP growth vs. CPI inflation rates.

This indicator is a fusion of two powerful TradingView indicators:

LuxAlgo ’s Relative Strength Scatter Plot – A robust scatter plot for tracking relative strength.

The Investment Clock Indicator – A cycle-based approach to market rotation. This indicator contains more information regarding The Investment Clock.

By combining these approaches, the Investment Clock Orbital Graph enables traders to visualize economic momentum and inflationary trends in a unique, orbital-style scatter plot.

Key Features & Improvements

Orbital Graph Representation – Displays GDP growth and CPI inflation as a dynamic, evolving scatter plot, showing how the economy moves through different phases.

Quadrant-Based Market Regimes – Identifies four key economic phases:

1)🔥 Overheating (High Growth, High Inflation)

2)📉 Stagflation (Low Growth, High Inflation)

3)🤒 Recovery (High Growth, Low Inflation)

4)🎈 Reflation (Low Growth, Low Inflation)

Data-Driven Analysis – Utilizes FRED (Federal Reserve Economic Data) for accurate real-world GDP & CPI data.

Trailing Path of Economic Evolution – Tracks historical economic cycles over time to show momentum and cyclical movements.

Customizable Parameters – Set sustainable GDP growth and inflation thresholds, adjust trail length, and fine-tune scatter plot resolution.

Auto-Labeled Quadrants & Revised Accurate Market Guidance – Each quadrant includes newly updated tooltips and annotations (like ETF suggestions) to help traders make informed decisions.

Live Macro Forecasting Tool – Helps traders anticipate future market conditions, rate hikes/cuts, and sector rotations.

How to Use for Trading Decisions

The Investment Clock Orbital Graph helps traders and macro investors by identifying market phases and providing insights into asset class performance during different economic conditions.

📌 Step 1: Identify the Current Quadrant

Locate the most recent point on the orbital graph to see if the economy is in Overheating, Stagflation, Recovery, or Reflation.

📌 Step 2: Forecast Market Trends

The trajectory of the points can predict upcoming economic shifts:

Overheating → Stagflation ➡️ Expect economic slowdowns, bearish stock markets.

Stagflation → Reflation ➡️ Interest rate cuts likely, bonds and defensive stocks perform well.

Reflation → Recovery ➡️ Risk-on rally, technology and cyclicals perform best.

Recovery → Overheating ➡️ Commodities surge, inflation rises, and central banks intervene.

📌 Step 3: Align Trading & Investing Strategies

🔥 Overheating – Favor commodities & energy (Oil, Industrial Stocks, Materials).

📉 Stagflation – Favor defensive assets (Cash, Utilities, Healthcare).

🤒 Recovery – Favor growth stocks (Technology, Consumer Discretionary).

🎈 Reflation – Favor bonds, value stocks, and financials.

📌 Step 4: Monitor Trends Over Time

The indicator visualizes economic movement over multiple months, allowing traders to confirm long-term trends vs. short-term noise.

The Investment Clock Orbital Graph is an essential macro trading tool, providing a real-time visualization of economic conditions. By tracking GDP growth vs. CPI inflation, traders and investors can align their portfolios with major macroeconomic shifts, predict sector rotations, and anticipate central bank policy changes.

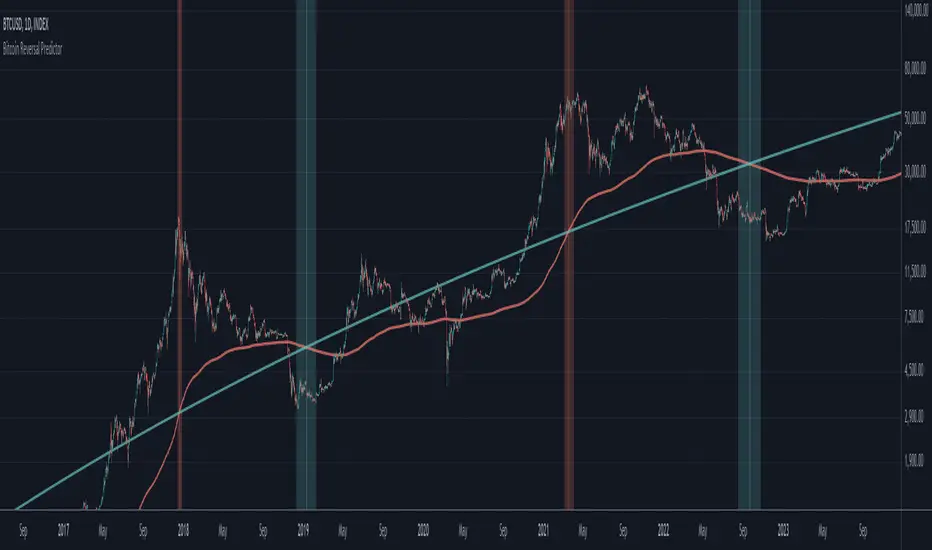

Bitcoin Reversal PredictorOverview

This indicator displays two lines that, when they cross, signal a potential reversal in Bitcoin's price trend. Historically, the high or low of a bull market cycle often occurs near the moment these lines intersect. The lines consist of an Exponential Moving Average (EMA) and a logarithmic regression line fitted to all of Bitcoin's historical data.

Inspiration

The inspiration for this indicator came from the PI Cycle Top indicator, which has accurately predicted past bull market peaks. However, I believe the PI Cycle Top indicator may not be as effective in the future. In that indicator, two lines cross to mark the top, but the extent of the cross has been diminishing over time. This was especially noticeable in the 2021 cycle, where the lines barely crossed. Because of this, I created a new indicator that I think will continue to provide reliable reversal signals in the future.

How It Works

The logarithmic regression line is fitted to the Bitcoin (BTCUSD) chart using two key factors: the 'a' factor (slope) and the 'b' factor (intercept). This results in a steadily decreasing line. The EMA oscillates above and below this regression line. Each time the two lines cross, a vertical colored bar appears, indicating that Bitcoin's price momentum is likely to reverse.

Use Cases

- Price Bottoming:

Bitcoin often bottoms out when the EMA crosses below the logarithmic regression line.

- Price Topping:

In contrast, Bitcoin often peaks when the EMA crosses above the logarithmic regression line.

- Profitable Strategy:

Trading at the crossovers of these lines can be a profitable strategy, as these moments often signal significant price reversals.

Detrended Price Oscillator [NexusSignals]Detrended Price Oscillator (DPO) is a detrended price oscillator, used in technical analysis, strips out price trends in an effort to estimate the length of price cycles from peak to peak or trough to trough.

DPO is not a momentum indicator, instead highlights peaks and troughs in price, which are used to estimate buy and sell points in line with the historical cycle. (cf. to investopedia)

DPO indicator made by NexusSignals components :

a filled area that allow users to see easy the trend of an asset;

a sma moving average on chart (default length is 20)

a 20 sma on oscillator, both ma's are color coded to show uptrend / downtrend

a donchian channel applied to the dpo to show breakouts, breakdowns and resistances/support, reversals

few alerts for price crossing above ma, cross above the 0 dpo line, and for cross above and below the donchian channels top and bottom

How you can use DPO indicator ?

The detrended price oscillator (DPO) can be used for measuring the distance between peaks and troughs in the indicator that may help traders to make future decisions as they can locate the most recent trough and determine when the next one may occur in the meassured distance on oscillator between peaks and troughs.

You can use the indicator to find the potential price reversals, for example when the price of an asset is in a bearish trend and the dpo is bouncing from the donchian channel bottom, that may be a potential swing low for that asset, same thing in a bullish trend when the dpo rejecting at top of donchian channel may be a trend reversal, a pullback or swing high.

When DPO is above the 0 trend is in an uptrend and when dpo is below the zero the asset is possible to move into a downtrend.

Also crosses of DPO above and below the DPO moving average may signalising a trend change.

Fourier For Loop [BackQuant]Fourier For Loop

PLEASE Read the following, as understanding an indicator's functionality is essential before integrating it into a trading strategy. Knowing the core logic behind each tool allows for a sound and strategic approach to trading.

Introducing BackQuant's Fourier For Loop (FFL) — a cutting-edge trading indicator that combines Fourier transforms with a for-loop scoring mechanism. This innovative approach leverages mathematical precision to extract trends and reversals in the market, helping traders make informed decisions. Let's break down the components, rationale, and potential use-cases of this indicator.

Understanding Fourier Transform in Trading

The Fourier Transform decomposes price movements into their frequency components, allowing for a detailed analysis of cyclical behavior in the market. By transforming the price data from the time domain into the frequency domain, this indicator identifies underlying patterns that traditional methods may overlook.

In this script, Fourier transforms are applied to the specified calculation source (defaulted to HLC3). The transformation yields magnitude values that can be used to score market movements over a defined range. This scoring process helps uncover long and short signals based on relative strength and trend direction.

Why Use Fourier Transforms?

Fourier Transforms excel in identifying recurring cycles and smoothing noisy data, making them ideal for fast-paced markets where price movements may be erratic. They also provide a unique perspective on market volatility, offering traders additional insights beyond standard indicators.

Calculation Logic: For-Loop Scoring Mechanism

The For Loop Scoring mechanism compares the magnitude of each transformed point in the series, summing the results to generate a score. This score forms the backbone of the signal generation system.

Long Signals: Generated when the score surpasses the defined long threshold (default set at 40). This indicates a strong bullish trend, signaling potential upward momentum.

Short Signals: Triggered when the score crosses under the short threshold (default set at -10). This suggests a bearish trend or potential downside risk.'

Thresholds & Customization

The indicator offers customizable settings to fit various trading styles:

Calculation Periods: Control how many periods the Fourier transform covers.

Long/Short Thresholds: Adjust the sensitivity of the signals to match different timeframes or risk preferences.

Visualization Options: Traders can visualize the thresholds, change the color of bars based on trend direction, and even color the background for enhanced clarity.

Trading Applications

This Fourier For Loop indicator is designed to be versatile across various market conditions and timeframes. Some of its key use-cases include:

Cycle Detection: Fourier transforms help identify recurring patterns or cycles, giving traders a head-start on market direction.

Trend Following: The for-loop scoring system helps confirm the strength of trends, allowing traders to enter positions with greater confidence.

Risk Management: With clearly defined long and short signals, traders can manage their positions effectively, minimizing exposure to false signals.

Final Note

Incorporating this indicator into your trading strategy adds a layer of mathematical precision to traditional technical analysis. Be sure to adjust the calculation start/end points and thresholds to match your specific trading style, and remember that no indicator guarantees success. Always backtest thoroughly and integrate the Fourier For Loop into a balanced trading system.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future .

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

CME Quarterly ShiftsCME Quarterly Shifts - Institutional Quarter Levels

Overview:

The CME Quarterly Shifts indicator tracks price action based on actual CME futures contract rollover dates, not calendar quarters. This indicator plots the Open, High, Low, and Close (OHLC) for each quarter, with quarters defined by the third Friday of March, June, September, and December - the exact dates when CME quarterly futures contracts expire and roll over.

Why CME Contract Dates Matter:

Institutional traders, hedge funds, and large market participants typically structure their positions around futures contract expiration cycles. By tracking quarters based on CME rollover dates rather than calendar months, this indicator aligns with how major institutional players view quarterly timeframes and position their capital.

Key Features:

✓ Automatic CME contract rollover date calculation (3rd Friday of Mar/Jun/Sep/Dec)

✓ Displays Quarter Open, High, Low, and Close levels

✓ Vertical break lines marking the start of each new quarter

✓ Quarter labels (Q1, Q2, Q3, Q4) for easy identification

✓ Adjustable history - show up to 20 previous quarters

✓ Fully customizable colors and line widths

✓ Works on any instrument and timeframe

✓ Toggle individual OHLC levels on/off

How to Use:

Quarter Open: The opening price when the new quarter begins (at CME rollover)

Quarter High: The highest price reached during the current quarter

Quarter Low: The lowest price reached during the current quarter

Quarter Close: The closing price from the previous quarter

These levels often act as key support/resistance zones as institutions reference them for quarterly performance, rebalancing, and position management.

Settings:

Display Options: Toggle quarterly break lines, OHLC levels, and labels

Max Quarters: Control how many historical quarters to display (1-20)

Colors: Customize colors for each level and break lines

Styles: Adjust line widths for OHLC levels and quarterly breaks

Best Practices:

Combine with other Smart Money Concepts (liquidity, order blocks, FVGs)

Watch for price reactions at quarterly Open levels

Monitor quarterly highs/lows as potential targets or stop levels

Use on higher timeframes (4H, Daily, Weekly) for clearer institutional perspective

Pairs well with monthly and yearly levels for multi-timeframe confluence

Perfect For:

ICT (Inner Circle Trader) methodology followers

Smart Money Concepts traders

Swing and position traders

Institutional-focused technical analysis

Traders tracking quarterly performance levels

Works on all markets: Forex, Indices, Commodities, Crypto, Stocks

Vertical Timelines Pro |MC|Vertical Timelines Pro |MC|

Credits go to lucemanb for the great work 👍

This indicator has been further developed and enhanced with additional features.

Vertical Timelines Pro is a customizable time-based indicator designed to mark important intraday timestamps directly on the chart. It helps traders visualize recurring market moments such as True Day Open, session opens, macro events, or personal timing models with precise vertical reference lines.

The indicator allows you to define multiple custom times, each with its own color and on/off toggle. All timestamps are calculated using a selectable timezone, ensuring consistent and accurate alignment across different markets and chart settings.

Optional labels can be displayed at each timeline to clearly identify the corresponding time. To keep the chart clean and readable, the number of visible labels can be limited retroactively. Due to Pine Script limitations, this setting only affects labels—plotted lines are not impacted.

💎 Key Features 💎

Multiple configurable intraday time markers

Timezone-aware calculations

Individual color and visibility control per line

Optional time labels with customizable size and colors

Historical label limiting to reduce chart clutter

Lightweight and suitable for all intraday timeframes

This indicator is ideal for traders who rely on time-based market behavior, session structure, or repeatable intraday cycles.

Happy Trading!

Macro Valuation Oscillator (MVO)Macro Valuation Oscillator (MVO) is a macro-relative-strength indicator that compares the current valuation of an asset against three key benchmarks: Gold, USD, and Bond. It helps visualize how the asset performs in relative macro terms over time.

When the MVO line for Gold (yellow) moves below the neutral zone (0), it reflects relative weakness against gold. When it rises above +80, it indicates relative strength or potential overheating compared to gold. The same concept applies to USD (blue) and Bond (purple) lines.

The indicator highlights macro-rotation behavior, showing periods when assets outperform (green) or underperform (red) in relative value. It is mainly intended for daily charts, providing a clear visual framework for assessing long-term macro relationships and timing within broader market cycles.

Hurst‑Millard FLD Normalized 2.0 – Signals "Hurst-Millard FLD Normalized 2.0 – Signals" indicator. It analyzes price data using a combination of moving averages (MAs) and the Hurst exponent to decompose price movements into trend, swing, and noise components, generating buy and sell signals. Here's a brief overview of its functionality:Inputs and Modes:Offers Auto Mode (cycle-based) and Manual Mode for configuring three moving averages: Long-Term (LT), Mid-Term (MT), and Short-Term (ST).

Auto Mode calculates MA lengths and offsets based on user-defined target cycle lengths (e.g., LT: 400 bars, MT: 100 bars, ST: 25 bars) with predefined offset ratios (0.2, 0.333, 0.5 respectively).

Manual Mode allows direct input of MA lengths and offsets.

Moving Averages:Computes Simple Moving Averages (SMAs) for LT, MT, and ST based on the closing price.

Applies forward-shifting to simulate future price behavior (e.g., maLongFwd shifts the LT MA by the specified offset).

Decomposition:Trend: Derived from the forward-shifted LT MA (maLongFwd).

Swing: Calculated as the difference between MT and LT MAs, scaled as a percentage of the closing price and amplified (using ATR or a manual factor).

Noise: Calculated as the difference between ST and MT MAs, similarly scaled and amplified.

Hurst Exponent:Estimates the Hurst exponent to measure the persistence or mean-reversion of the noise component.

Uses a 50-bar lookback period, smoothed with a 5-period SMA.

Signal Generation:Generates buy signals when the noise component is less than the swing component and their difference is within a user-defined proximity threshold (default: 25% of swing).

Generates sell signals when noise exceeds swing within the same threshold.

Signals are plotted as diamond shapes at the calculated proximity price level.

Visualization:Plots the trend, swing, and noise components as lines with customizable colors and gradient intensity based on their relative strength.

Optional debugging plots for raw forward-shifted MAs and proximity thresholds.

Displays a periodic debug table (every 100 bars) showing key metrics like close price, MAs, trend, swing, noise, Hurst exponent, and more.

Additional Features:Supports ATR-based amplification for scaling swing and noise.

Allows customization of signal colors, diamond offsets, and proximity thresholds.

Includes debugging options to visualize raw MAs and proximity bands.

In summary, this indicator uses cycle-based or manually configured MAs to break down price action into trend, swing, and noise, calculates the Hurst exponent for noise analysis, and generates buy/sell signals based on the relationship between swing and noise within a proximity threshold. It’s designed for traders to identify potential trend reversals or continuations.

QLitCycle QuarterlyQLITCYCLE

QLitCycle is an intraday cycle visualization tool that divides each trading day into multiple segments, helping traders identify time-based patterns and recurring market behaviors. By splitting the day into distinct periods, this indicator allows for better analysis of intraday rhythms, cycle alignment, and time-specific market tendencies.

It can be applied to various markets and timeframes, but is most effective on intraday charts where precise time segmentation can reveal valuable insights.

CirclesCircles - Support & Resistance Levels

Overview

This indicator plots horizontal support and resistance levels based on W.D. Gann's mathematical approach of dividing 360 degrees by 2 and by 3. These divisions create natural price magnetism points that have historically acted as significant support and resistance levels across all markets and timeframes.

How It Works

360÷2 Levels (Blue): 5.63, 11.25, 33.75, 56.25, 78.75, etc.

360÷3 Levels (Red): 7.5, 15, 30, 37.5, 52.5, 60, 75, etc.

Both Levels (Yellow): 22.5, 45, 67.5, 90, 112.5, 135, 157.5, 180 - These are "doubly strong" as they appear in both calculations

Key Features

Auto-Scaling: Automatically adjusts for any price range (from $0.001 altcoins to $100K+ Bitcoin)

Manual Scaling: Choose from 0.001x to 1000x multipliers or set custom values

Full Customization: Colors, line widths, styles (solid/dashed/dotted)

Historical View: Option to show all levels regardless of current price

Clean Display: Adjustable label positioning and line extensions

Use Cases

Identify potential reversal zones before price reaches them

Set profit targets and stop losses at key mathematical levels

Confirm breakouts when price decisively moves through major levels

Works on all timeframes and all markets (stocks, crypto, forex, commodities)

Gann Theory

W.D. Gann believed that markets move in mathematical harmony based on geometric angles and time cycles. These 360-degree divisions represent natural balance points where price often finds support or resistance, making them valuable for both short-term trading and long-term analysis.

Perfect for traders who use:

Support/Resistance trading

Fibonacci levels

Pivot points

Mathematical/geometric analysis

Multi-timeframe analysis

Bitcoin NUPL IndicatorThe Bitcoin NUPL (Net Unrealized Profit/Loss) Indicator is a powerful metric that shows the difference between Bitcoin's market cap and realized cap as a percentage of market cap. This indicator helps identify different market cycle phases, from capitulation to euphoria.

// How It Works

NUPL measures the aggregate profit or loss held by Bitcoin investors, calculated as:

```

NUPL = ((Market Cap - Realized Cap) / Market Cap) * 100

```

// Market Cycle Phases

The indicator automatically color-codes different market phases:

• **Deep Red (< 0%)**: Capitulation Phase - Most coins held at a loss, historically excellent buying opportunities

• **Orange (0-25%)**: Hope & Fear Phase - Early accumulation, price uncertainty and consolidation

• **Yellow (25-50%)**: Optimism & Anxiety Phase - Emerging bull market, increasing confidence

• **Light Green (50-75%)**: Belief & Denial Phase - Strong bull market, high conviction

• **Bright Green (> 75%)**: Euphoria & Greed Phase - Potential market top, historically good profit-taking zone

// Features

• Real-time NUPL calculation with customizable smoothing

• RSI indicator for additional momentum confirmation

• Color-coded background reflecting current market phase

• Reference lines marking key transition zones

• Detailed metrics table showing NUPL value, market sentiment, market cap, realized cap, and RSI

// Strategy Applications

• **Long-term investors**: Use extreme negative NUPL values (deep red) to identify potential bottoms for accumulation

• **Swing traders**: Look for transitions between phases for potential trend changes

• **Risk management**: Consider taking profits when entering the "Euphoria & Greed" phase (bright green)

• **Mean reversion**: Watch for overbought/oversold conditions when NUPL reaches historical extremes

// Settings

• **RSI Length**: Adjusts the period for RSI calculation

• **NUPL Smoothing Length**: Applies moving average smoothing to reduce noise

// Notes

• Premium TradingView subscription required for Glassnode and Coin Metrics data

• Best viewed on daily timeframes for macro analysis

• Historical NUPL extremes have often marked cycle bottoms and tops

• Use in conjunction with other indicators for confirmation

Simple Parallel Channel TrackerThis script will automatically draw price channels with two parallel trends lines, the upper trendline and lower trendline. These lines can be changed in terms of appearance at any time.

The Script takes in fractals from local and historic price action points and connects them over a certain period or amount of candles as inputted by the user. It tracks the most recent highs and lows formed and uses this data to determine where the channel begins.

The Script will decide whether to use the most recent high, or low, depending on what comes first.

Why is this useful?

Often, Traders either have no trend lines on their charts, or they draw them incorrectly. Whichever category a trader falls into, there can only be benefits from having Trend lines and Parallel Channels drawn automatically.

Trends naturally occur in all Markets, all the time. These oscillations when tracked allow for a more reliable following of Markets and management of Market cycles.

Abdozo - Highlight First DaysAbdozo - Highlight First Days Indicator

This Pine Script indicator helps traders easily identify key timeframes by highlighting the first trading day of the week and the first day of the month. It provides visual markers directly on your chart, helping you stay aware of potential market trends and turning points.

Features:

- Highlight First Day of the Week (Monday): Automatically marks Mondays to help you track weekly market cycles.

- Highlight First Day of the Month: Spot the start of each month with ease to analyze monthly performance and trends.

Market Health MonitorThe Market Health Monitor is a comprehensive tool designed to assess and visualize the economic health of a market, providing traders with vital insights into both current and future market conditions. This script integrates a range of critical economic indicators, including unemployment rates, inflation, Federal Reserve funds rates, consumer confidence, and housing market indices, to form a robust understanding of the overall economic landscape.

Drawing on a variety of data sources, the Market Health Monitor employs moving averages over periods of 3, 12, 36, and 120 months, corresponding to quarterly, annual, three-year, and ten-year economic cycles. This selection of timeframes is specifically chosen to capture the nuances of economic movements across different phases, providing a balanced view that is sensitive to both immediate changes and long-term trends.

Key Features:

Economic Indicators Integration: The script synthesizes crucial economic data such as unemployment rates, inflation levels, and housing market trends, offering a multi-dimensional perspective on market health.

Adaptability to Market Conditions: The inclusion of both short-term and long-term moving averages allows the Market Health Monitor to adapt to varying market conditions, making it a versatile tool for different trading strategies.

Oscillator Thresholds for Recession and Growth: The script sets specific thresholds that, when crossed, indicate either potential economic downturns (recessions) or periods of growth (expansions), allowing traders to anticipate and react to changing market conditions proactively.

Color-Coded Visualization: The Market Health Monitor employs a color-coding system for ease of interpretation:

-- A red background signals unhealthy economic conditions, cautioning traders about potential risks.

-- A bright red background indicates a confirmed recession, as declared by the NBER, signaling a critical time for traders to reassess risk exposure.

-- A green background suggests a healthy market with expected economic expansion, pointing towards growth-oriented opportunities.

Comprehensive Market Analysis: By combining various economic indicators, the script offers a holistic view of the market, enabling traders to make well-informed decisions based on a thorough understanding of the economic environment.

Key Criteria and Parameters:

Economic Indicators:

Labor Market: The unemployment rate is a critical indicator of economic health.

High or rising unemployment indicates reduced consumer spending and economic stress.

Inflation: Key for understanding monetary policy and consumer purchasing power.

Persistent high inflation can lead to economic instability, while deflation can signal weak

demand.

Monetary Policy: Reflected by the Federal Reserve funds rate.

Changes in the rate can influence economic activity, borrowing costs, and investor

sentiment.

Consumer Confidence: A predictor of consumer spending and economic activity.

Reflects the public’s perception of the economy

Housing Market: The housing market often leads the economy into recession and recovery.

Weakness here can signal broader economic problems.

Market Data:

Stock Market Indices: Reflect overall investor sentiment and economic

expectations. No gains in a stock market could potentially indicate that economy is

slowing down.

Credit Conditions: Indicated by the tightness of bank lending, signaling risk

perception.

Commodity Insight:

Crude Oil Prices: A proxy for global economic activity.

Indicator Timeframe:

A default monthly timeframe is chosen to align with the release frequency of many economic indicators, offering a balanced view between timely data and avoiding too much noise from short-term fluctuations. Surely, it can be chosen by trader / analyst.

The Market Health Monitor is more than just a trading tool—it's a comprehensive economic guide. It's designed for traders who value an in-depth understanding of the economic climate. By offering insights into both current conditions and future trends, it encourages traders to navigate the markets with confidence, whether through turbulent times or in periods of growth. This tool doesn't just help you follow the market—it helps you understand it.

Dark Energy Divergence OscillatorThe Dark Energy Divergence Oscillator (DEDO)

What makes The Universe grow at an accelerating pace?

Dark Energy.

What makes The Economy grow at an accelerating pace?

Debt.

Debt is the Dark Energy of The Economy.

I pronounce DEDO "Deed-oh", but variations are fine with me.

Note: The Pine Script version of DEDO is improved from the original formula, which used a constant all-time high calculation in the normalization factor. This was technically not as accurate for calculating liquidity pressure in historical data because it meant that historical prices were being tested against future liquidity factors. Now using Pine, the functions can be normalized for the bar at the time of calculation, so the liquidity factors are normalized per candle, not across the entire series, which feels like an improvement to me.

Thought Process:

It's all about the liquidity. What I started with is a correlation between major stock indices such as SPX and WRESBAL , a balance sheet metric on FRED

After September 2008, when QE was initiated, many asset valuations started to follow more closely with liquidity factors. This led me to create a function that could combine asset prices and liquidity in WRESBAL , in order to calculate their divergence and chart the signal in TradingView.

The original formula:

First, we don't want "non-QE" data. we only want data for the market affected by QE .

So, find SPX on the day of pre-QE: 1255.08 and subtract that from the 2022 top 4818.62 = 3563.54

With this post-QE SPX range, now you can normalize the price level simply by dividing by the range = ( SPX -1255.08)/3563.54)

Normalization produces values from 0 to 1 so that they can be compared with other normalized figures.

In order to test the 0 to 1 normalized SPX range measure against the liquidity number, WRESBAL , it's the same idea: normalize it using the max as the denominator and you get a 0 to 1 liquidity index:

( WRESBAL /4276000000000)

Subtract one from the other to get the divergence:

(( WRESBAL /4276000000000)-(( SPX -1255.08)/3563.54))*10

x10 to reduce decimal places, but this option is configurable in DEDO's input settings tab.

Positive values indicate there's ample liquidity to hold up price or even create bullish momentum in some cases. Negative values mean price levels are potentially extended beyond what liquidity levels can support.

Note: many viewers of the charts on social media wanted the values to go down in alignment with price moving down, so inverting the chart is what I do with Option + I. I like the fact that negative values represent a deficit in liquidity to hold up price but that's just me.

Now with Pine Script and some help from other liquidity focused accounts on TradingView , I was able to derive a script that includes central bank liquidity and Reverse Repo liquidity drain, all in one algorithm, with adjustable settings.

Central bank assets included in this version:

-JPY (Japan)

-CNY (China)

-UK (British Pound)

-SNB (Swiss National Bank)

-ECB (European Central Bank )

Central Bank assets can be adjusted to an allocation % so that the formula is adjusted for the market cap of the asset.

A handy table in the lower right corner displays useful information about the asset market cap, and percentage it represents in the liquidity pool.

Reverse repo soak is also an optional addition in the Input settings using the RRPONTSYD value from FRED. This value is subtracted from global liquidity used to determine divergence since it is swept away from markets when residing in the Fed's reverse repo facility.

There is an option to draw a line at the Zero bound. This provides a convenience so that the line doesn't keep having to be redrawn on every chart. The normalized equation produces a value that should oscillate around zero, as price/valuation grows past liquidity support, falls under it, and repeats in cycles.

S&P 500 Quandl Data & RatiosTradingView has a little-known integration that allows you to pull in 3rd party data-sets from Nasdaq Data Link, also known as Quandl. Today, I am open-sourcing for the community an indicator that uses the Quandl integration to pull in historical data and ratios on the S&P500. I originally coded this to study macro P/E ratios during peaks and troughs of boom/bust cycles.

The indicator pulls in each of the following datasets, as defined and provided by Quandl. The user can select which datasets to pull in using the indicator settings:

Dividend Yield : S&P 500 dividend yield (12 month dividend per share)/price. Yields following June 2022 (including the current yield) are estimated based on 12 month dividends through June 2022, as reported by S&P. Sources: Standard & Poor's for current S&P 500 Dividend Yield. Robert Shiller and his book Irrational Exuberance for historic S&P 500 Dividend Yields.

Price Earning Ratio : Price to earnings ratio, based on trailing twelve month as reported earnings. Current PE is estimated from latest reported earnings and current market price. Source: Robert Shiller and his book Irrational Exuberance for historic S&P 500 PE Ratio.

CAPE/Shiller PE Ratio : Shiller PE ratio for the S&P 500. Price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio (CAPE Ratio), Shiller PE Ratio, or PE 10 FAQ. Data courtesy of Robert Shiller from his book, Irrational Exuberance.

Earnings Yield : S&P 500 Earnings Yield. Earnings Yield = trailing 12 month earnings divided by index price (or inverse PE) Yields following March, 2022 (including current yield) are estimated based on 12 month earnings through March, 2022 the latest reported by S&P. Source: Standard & Poor's

Price Book Ratio : S&P 500 price to book value ratio. Current price to book ratio is estimated based on current market price and S&P 500 book value as of March, 2022 the latest reported by S&P. Source: Standard & Poor's

Price Sales Ratio : S&P 500 Price to Sales Ratio (P/S or Price to Revenue). Current price to sales ratio is estimated based on current market price and 12 month sales ending March, 2022 the latest reported by S&P. Source: Standard & Poor's

Inflation Adjusted SP500 : Inflation adjusted SP500. Other than the current price, all prices are monthly average closing prices. Sources: Standard & Poor's Robert Shiller and his book Irrational Exuberance for historic S&P 500 prices, and historic CPIs.

Revenue Per Share : Trailing twelve month S&P 500 Sales Per Share (S&P 500 Revenue Per Share) non-inflation adjusted current dollars. Source: Standard & Poor's

Earnings Per Share : S&P 500 Earnings Per Share. 12-month real earnings per share inflation adjusted, constant August, 2022 dollars. Sources: Standard & Poor's for current S&P 500 Earnings. Robert Shiller and his book Irrational Exuberance for historic S&P 500 Earnings.

Disclaimer: This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!