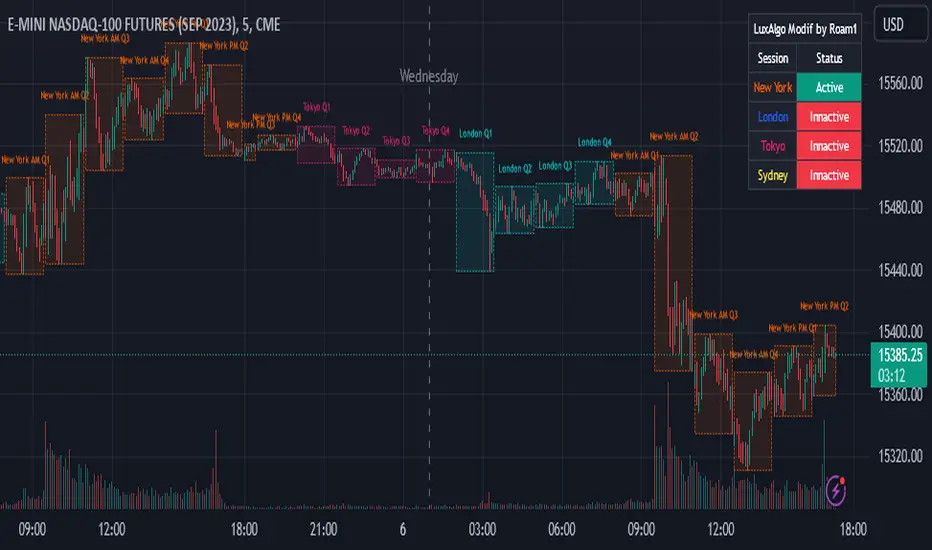

ShadowCorp Time Cycle'sThis indicator marks key intraday windows — 7:00–8:30, 8:30–10:00 (NYO), 10:00–11:30, 11:30–13:00, 13:00–14:30, 14:30–16:00, and 18:00–19:00 — and draws a true **price-range box** for each window.

Each box builds **in real time** from that window’s running **high/low**, then **persists on the chart** after the window ends for historical study. It’s **timezone-aware** (configurable) and gives you **per-window color** controls. Use it to visualize session volatility, ranges, and liquidity sweeps across the day on any intraday chart.

Penunjuk Pine Script®