VIX Futures Basis StrategyVIX Futures Basis Strategy

The VIX Futures Basis Strategy is a trading approach that takes advantage of the unique characteristics of the VIX index and its futures market. The VIX, often referred to as the "fear index," measures market expectations of near-term volatility. This strategy focuses on how the VIX futures contracts behave in relation to the spot VIX index and seeks to capitalize on the market's contango and backwardation phases.

Key Concepts:

VIX Index and VIX Futures:

The VIX index reflects the market's expectation of volatility over the next 30 days.

VIX futures allow traders to speculate on the future value of the VIX index.

Contango and Backwardation:

Contango occurs when the futures price is higher than the spot price, often indicating that the market expects volatility to rise in the future.

Backwardation is when the futures price is lower than the spot price, suggesting that the market expects a decrease in volatility.

Basis:

The basis is the difference between the futures price and the spot price. This strategy examines the basis for two consecutive VIX futures contracts.

Strategy Overview:

The VIX Futures Basis Strategy uses the relationship between the VIX index and its futures contracts to generate trading signals:

Long Position on Contango:

When both the front month and the second month VIX futures contracts are in contango (their prices are above the spot VIX index by a specified threshold), the strategy takes a long position.

This implies an expectation that the market will move from a state of expected higher future volatility to a more stable state, allowing profits to be made as the futures prices converge toward the spot price.

Closing Position on Backwardation:

If the basis for both futures contracts indicates backwardation (their prices are below the spot VIX index by a threshold), the strategy closes any long positions.

This condition suggests that the market anticipates decreasing volatility, and closing positions helps to avoid potential losses.

Cari dalam skrip untuk "Futures"

BTC CME Futures Divergence TrackerThis script tracks divergences between price action and open interest for the BTC CME Futures contract (symbol "BTC1!") using the following components:

Key Features:

1. Price Analysis: Identifies lower highs in the price over a specified lookback period. Marks these points with red upward-facing triangles above the bars.

2. Open Interest Analysis: Retrieves open interest (OI) data for the BTC CME Futures contract via request.security. Detects lower highs in open interest over the same lookback period. Highlights these points with blue downward-facing triangles below the bars.

3. Divergence Detection: A divergence is identified when both price and open interest form lower highs simultaneously. Highlights such occurrences with a purple background, indicating potential bearish sentiment or weakening momentum.

4. Alerts: If divergences are detected, an alert is triggered (if enabled), notifying the trader to take action.

5. Visualization: Open interest is plotted as a blue line in a separate pane for added context. Red and blue markers highlight significant points in price and open interest trends.

Use Cases:

- Spot Weakening Trends: Divergences between price and open interest may indicate a loss of momentum or bearish sentiment, allowing traders to preemptively adjust their strategies.

- Monitor Institutional Activity: Open interest changes reflect shifts in market participation, especially in derivative markets like CME Futures.

- Set Alerts for Key Signals: With automated alerts, traders can stay informed of potential divergence signals without constant monitoring.

Customization Options:

- Lookback Period: Adjust the number of bars used to detect lower highs.

- Timeframe: Choose the timeframe for fetching open interest data (e.g., daily, hourly).

- Alert Activation: Enable or disable alerts for divergences.

This tool combines price action with open interest dynamics to provide a robust method for identifying market trends and potential reversals in BTC CME Futures.

SessionLibrary "Session"

Helper functions for trading sessions. TradingView doesn't provide correct data when

calling some of the convenience methods like session.ismarket when you are looking at futures charts. This library corrects those mistakes by providing functions with the same names as the TradingView default properties. that reference a custom defined set of session hours for futures. It also provides a way for consumers to customize the map values by calling getSessionMap() and then overwriting (or adding) custom session definitions.

getSessionMap()

Returns a map of the futures rth & eth session hours. The map is keyed with symbol:session format (eg. ES:market or ES:overnight).

Returns: A map of futures symbols and their associated session hours.

getSessionString(session, symbol, sessionMap)

Returns a session string representing the session hours (and days) for the requested symbol (or the chart's symbol if the symbol value is not provided). If the session string is not found in the collection, it will return a blank string.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

symbol (string) : The symbol to check. Optional. Defaults to chart symbol.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

inSession(session, sessionMap, barsBack)

Returns true if the current symbol is currently in the session parameters defined by sessionString.

Parameters:

session (string) : A string representing the session hour being requested. One of: market (regular trading hours), overnight (extended/electronic trading hours), postmarket (after-hours), premarket

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

barsBack (int) : Private. Only used by futures to check islastbar. Optional. The default is 0.

ismarket(sessionMap)

Returns true if the current bar is a part of the regular trading hours (i.e. market hours), false otherwise. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar()

Returns true if the current bar is the first bar of the day's session, false otherwise. If extended session information is used, only returns true on the first bar of the pre-market bars. Works for futures (TradingView's methods do not).

Returns: bool

islastbar()

Returns true if the current bar is the last bar of the day's session, false otherwise. If extended session information is used, only returns true on the last bar of the post-market bars. Works for futures (TradingView's methods do not).

Returns: bool

ispremarket(sessionMap)

Returns true if the current bar is a part of the pre-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

ispostmarket(sessionMap)

Returns true if the current bar is a part of the post-market, false otherwise. On non-intraday charts always returns false. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isfirstbar_regular(sessionMap)

Returns true on the first regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

islastbar_regular(sessionMap)

Returns true on the last regular session bar of the day, false otherwise. The result is the same whether extended session information is used or not. Works for futures (TradingView's methods do not).

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

isovernight(sessionMap)

Returns true if the current bar is a part of the pre-market or post-market, false otherwise. On non-intraday charts always returns false.

Parameters:

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: bool

getSessionHighAndLow(session, sessionMap)

Returns a tuple containing the high and low print during the specified session.

Parameters:

session (string) : The session for which to get the high & low prints. Defaults to market.

sessionMap (map) : The map of futures session hours. Optional. Uses default if not provided.

Returns: A tuple containing

Risk-On / Risk-Off Toolkit [SB1] (NQ, RTY, YM) VIXDescription:

The Risk-On / Risk-Off Toolkit is a professional-grade market context indicator designed to help traders quickly identify broad market sentiment shifts and gauge risk appetite. By combining major US equity futures (NQ, RTY, YM) with VIX dynamics, this toolkit provides clear visual signals of “Risk-On” (bullish, lower volatility environment) and “Risk-Off” (bearish, higher volatility environment) conditions. This is ideal for traders using discretionary analysis, swing strategies, intraday scalping, or portfolio positioning decisions.

My Personal Thoughts: Utilize all 3 charts to Identify which is Leading and who is lagging between the 3 (NQ, RTY, YM) Key Features:

Futures Trend Analysis:

Monitors the Nasdaq 100 (NQ), Russell 2000 (RTY), and Dow Jones (YM) futures in real-time.

Determines bullish/bearish bias based on each futures contract’s current close relative to its open.

Identifies when all three indices are moving in sync, highlighting broad market directional alignment.

VIX Confirmation:

Integrates the CBOE Volatility Index (VIX) to gauge market risk sentiment.

Confirms Risk-On conditions when VIX is falling while all three futures are bullish.

Confirms Risk-Off conditions when VIX is rising while all three futures are bearish.

Optional background shading visually highlights Risk-On (green) and Risk-Off (red) conditions for quick, intuitive assessment.

Strong Body Candle Signals:

Detects high conviction candlestick moves where the body represents at least 85% of the total range.

Confirms whether the candle closes near its extreme (top for bullish, bottom for bearish) within 15% of the range.

Plots arrows for strong bullish or bearish candles:

Green triangle-up for bullish strong candles

Red triangle-down for bearish strong candles

Provides a visual cue for intraday or swing traders to confirm trend momentum without cluttering the chart with labels.

Alert System:

Alerts can be set for Risk-On alignment: all monitored futures are bullish and VIX is falling.

Alerts can also be set for Risk-Off alignment: all monitored futures are bearish and VIX is rising.

Ensures traders never miss shifts in broad market sentiment, suitable for both intraday and end-of-day review.

Table Summary:

Provides a top-right summary table of each monitored market and VIX:

Displays Index Name and Current Bias (Bullish/Bearish/Neutral).

Highlights bullish conditions in green and bearish conditions in red.

Includes VIX status as “↓ Falling”, “↑ Rising”, or “Flat”, providing a quick visual reference of volatility trends.

Customizable Visuals:

Control the visibility of strong candle arrows.

Maintains dynamic bar coloring for strong candle moves (green for bullish, red for bearish).

How to Use the Risk-On / Risk-Off Toolkit:

Trend Confirmation: Use the alignment of NQ, RTY, and YM to determine whether the overall market environment is bullish or bearish.

Risk Sentiment Filter: Use VIX confirmation to identify if traders are in a risk-on or risk-off sentiment. This is especially useful for adjusting position sizing, hedging, or timing entries.

Momentum Validation: Strong candle arrows indicate decisive moves, providing additional confirmation for trade entries, breakouts, or trend continuation.

Alerts & Visual Cues: Set alerts to be notified whenever Risk-On or Risk-Off conditions are met, helping you act in real-time.

Quick Reference: Use the summary table for a bird’s-eye view of market alignment across indices and VIX, avoiding the need to track multiple charts simultaneously.

Why This Indicator is Unique:

Combines three major US indices with volatility confirmation to identify true macro market sentiment shifts.

Provides both visual and alert-based signals for actionable insights.

The inclusion of strong candle arrows gives intraday and swing traders a clear, low-latency cue for high-probability moves.

Perfect for multi-timeframe analysis and adaptable to both short-term and long-term strategies.

Indicator Name Justification:

The name “Risk-On / Risk-Off Toolkit ” accurately reflects the core function: identifying broad market risk appetite and sentiment alignment across key indices with volatility confirmation. It communicates instantly that the tool helps traders understand when the market is favoring risk-taking (Risk-On) versus risk-aversion (Risk-Off).

FlowSpike ES — BB • RSI • VWAP + AVWAP + News MuteThis indicator is purpose-built for E-mini S&P 500 (ES) futures traders, combining volatility bands, momentum filters, and session-anchored levels into a streamlined tool for intraday execution.

Key Features:

• ES-Tuned Presets

Automatically optimized settings for scalping (1–2m), daytrading (5m), and swing trading (15–60m) timeframes.

• Bollinger Band & RSI Signals

Entry signals trigger only at statistically significant extremes, with RSI filters to reduce false moves.

• VWAP & Anchored VWAPs

Session VWAP plus anchored VWAPs (RTH open, weekly, monthly, and custom) provide high-confidence reference levels used by professional order-flow traders.

• Volatility Filter (ATR in ticks)

Ensures signals are only shown when the ES is moving enough to offer tradable edges.

• News-Time Mute

Suppresses signals around scheduled economic releases (customizable windows in ET), helping traders avoid whipsaw conditions.

• Clean Alerts

Long/short alerts are generated only when all conditions align, with optional bar-close confirmation.

Why It’s Tailored for ES Futures:

• Designed around ES tick size (0.25) and volatility structure.

• Session settings respect RTH hours (09:30–16:00 ET), the period where most liquidity and institutional flows concentrate.

• ATR thresholds and RSI bands are pre-tuned for ES market behavior, reducing the need for manual optimization.

⸻

This is not a generic indicator—it’s a futures-focused tool created to align with the way ES trades day after day. Whether you scalp the open, manage intraday swings, or align to weekly/monthly anchored flows, FlowSpike ES gives you a clear, rules-based signal framework.

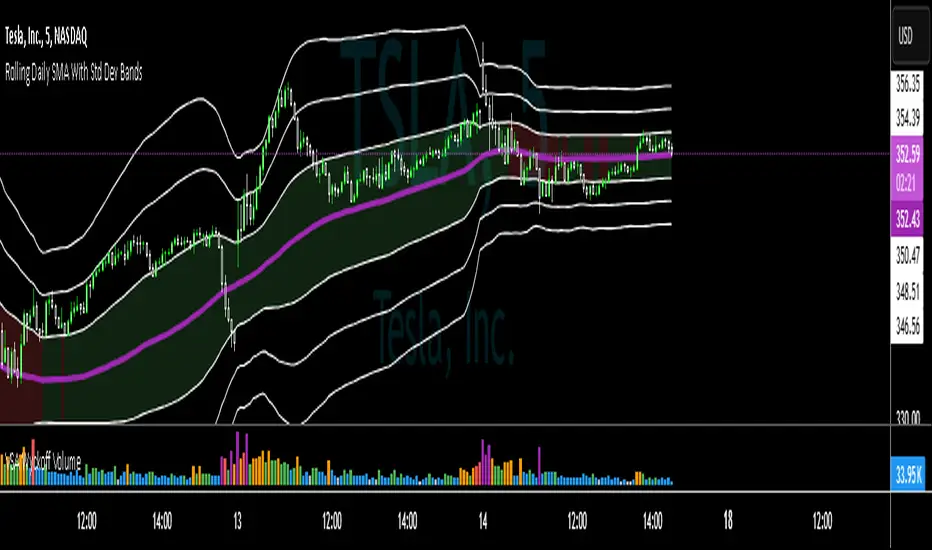

SMA with Std Dev Bands (Futures/US Stocks RTH)Rolling Daily SMA With Std Dev Bands

Upgrade your technical analysis with Rolling Daily SMA With Std Dev Bands, a powerful indicator that dynamically adjusts to your trading instrument. Whether you’re analyzing futures or US stocks during regular trading hours (RTH), this indicator seamlessly applies the correct logic to calculate a rolling daily Simple Moving Average (SMA) with customizable standard deviation bands for precise trend and volatility tracking.

Key Features:

✅ Automatic Instrument Detection– The indicator automatically recognizes whether you're trading futures or US equities and applies the correct daily lookback period based on your chart’s timeframe.

- Futures: Uses full trading day lengths (e.g., 1380 bars for 1‑minute charts).

- US Stocks (RTH): Uses regular session lengths (e.g., 390 bars for 1‑minute charts).

✅ Rolling Daily SMA (3‑pt Purple Line) – A continuously updated daily moving average, giving you an adaptive trend indicator based on market structure.

✅ Three Standard Deviation Bands (1‑pt White Lines) –

- Customizable multipliers allow you to adjust each band’s width.

- Toggle each band on or off to tailor the indicator to your strategy.

- The inner band area is color-filled: light green when the SMA is rising, light red when falling, helping you quickly identify trend direction.

✅ Works on Any Chart Timeframe – Whether you trade on 1-minute, 3-minute, 5-minute, or 15-minute charts, the indicator adjusts dynamically to provide accurate rolling daily calculations.

# How to Use:

📌 Identify Trends & Volatility Zones – The rolling daily SMA acts as a dynamic trend guide, while the standard deviation bands help spot potential overbought/oversold conditions.

📌 Customize for Precision – Adjust band multipliers and toggle each band on/off to match your trading style.

📌 Trade Smarter – The filled inner band offers instant visual feedback on market momentum, while the outer bands highlight potential breakout zones.

🔹 This is the perfect tool for traders looking to combine trend-following with volatility analysis in an easy-to-use, adaptive indicator.

🚀 Add Rolling Daily SMA With Std Dev Bands to your chart today and enhance your market insights!

---

*Disclaimer: This indicator is for informational and educational purposes only and should not be considered financial advice. Always use proper risk management and conduct your own research before trading.*

Crude Oil: Backwardation Vs ContangoCrude Oil, CL

Plots Futures Curve: Futures contract prices over the next 3.5 years; to easily visualize Backwardation Vs Contango(carrying charge) markets.

Carrying charge (contract prices increasing into the future) = normal, representing the costs of carrying/storage of a commodity. When this is flipped to Backwardation(As the above; contract prices decreasing into the future): it's a bullish sign: Buyers want this commodity, and they want it NOW.

Note: indicator does not map to time axis in the same way as price; it simply plots the progression of contract months out into the future; left to right; so timeframe DOESN'T MATTER for this plot

TO UPDATE (every year or so): in REQUEST CONTRACTS section, delete old contracts (top) and add new ones (bottom). Then in PLOTTING section, Delete old contract labels (bottom); add new contract labels (top); adjust the X in 'bar_index-(X+_historical)' numbers accordingly

This is one of several similar Futures Curve indicators: Meats | Metals | Grains | VIX | Crude Oil

If you want to build from this; to work on other commodities; be aware that Tradingview limits the number of contract calls to 40 (hence the multiple indicators)

Tips:

-Right click and reset chart if you can't see the plot; or if you have trouble with the scaling.

-Right click and add to new scale if you prefer this not to overlay directly on price. Or move to new pane below.

-If this takes too long to load (due to so many security calls); comment out the more distant future half of the contracts; and their respective labels. Or comment out every other contract and every other label if you prefer.

--Added historical input: input days back in time; to see the historical shape of the Futures curve via selecting 'days back' snapshot

updated 20th June 2022

© twingall

LibraryCOT█ OVERVIEW

This library is a Pine programmer's tool that provides functions to access Commitment of Traders (COT) data for futures. Four of our scripts use it:

• Commitment of Traders: Legacy Metrics

• Commitment of Traders: Disaggregated Metrics

• Commitment of Traders: Financial Metrics

• Commitment of Traders: Total

If you do not program in Pine and want to use COT data, please see the indicators linked above.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

Accessing COT data from a Pine script requires the generation of a ticker ID string for use with request.security() . The ticker string must be encoded in a special format that includes both CFTC and TradingView-specific content. The format of the ticker IDs is somewhat complex; this library's functions make their generation easier. Note that if you know the COT ticker ID string for specific data, you can enter it from the chart's "Symbol Search" dialog box.

A ticker for COT data in Pine has the following structure:

COT:__<_metricDirection><_metricType>

where an underscore prefixing a component name inside <> is only included if the component is not a null string, and:

Is a digit representing the type of the COT report the data comes from: "" for legacy COT data, "2" for disaggregated data and "3" for financial data.

Is a six digit code that represents a commodity. Example: wheat futures (root "ZW") have the code "001602".

Is either "F" if the report data should exclude Options data, or "FO" if such data is included.

Is the TradingView code of the metric. This library's `metricNameAndDirectionToTicker()` function creates both

the and components of a COT ticker from the metric names and directions listed in the above chart.

The different metrics are explained in the CFTC's Explanatory Notes .

Is the direction of the metric: "Long", "Short", "Spreading" or "No direction".

Not all directions are applicable to all metrics. The valid ones are listed next to each metric in the above chart.

Is the type of the metric, possible values are "All", "Old" and "Other".

The difference between the types is explained in the "Old and Other Futures" section of the CFTC's Explanatory Notes .

As an example, the Legacy report Open Interest data for ZW futures (options included) in the old standard has the ticker "COT:001602_FO_OI_OLD". The same data using the current standard without futures has the ticker "COT:001602_F_OI".

█ USING THE LIBRARY

The first functions in the library are helper functions that generate components of a COT ticker ID. The last function, `COTTickerid()`, is the one that generates the full ticker ID string by calling some of the helper functions. We use it like this in our example:

exampleTicker = COTTickerid(

COTType = "Legacy",

CFTCCode = convertRootToCOTCode("Auto"),

includeOptions = false,

metricName = "Open Interest",

metricDirection = "No direction",

metricType = "All")

This library's chart displays the valid values for the `metricName` and `metricDirection` arguments. They vary for each of the three types of COT data (the `COTType` argument). The chart also displays the COT ticker ID string in the `exampleTicker` variable.

Look first. Then leap.

The library's functions are:

rootToCFTCCode(root)

Accepts a futures root and returns the relevant CFTC code.

Parameters:

root : Root prefix of the future's symbol, e.g. "ZC" for "ZC1!"" or "ZCU2021".

Returns: The part of a COT ticker corresponding to `root`, or "" if no CFTC code exists for the `root`.

currencyToCFTCCode(curr)

Converts a currency string to its corresponding CFTC code.

Parameters:

curr : Currency code, e.g., "USD" for US Dollar.

Returns: The corresponding to the currency, if one exists.

optionsToTicker(includeOptions)

Returns the part of a COT ticker using the `includeOptions` value supplied, which determines whether options data is to be included.

Parameters:

includeOptions : A "bool" value: 'true' if the symbol should include options and 'false' otherwise.

Returns: The part of a COT ticker: "FO" for data that includes options and "F" for data that doesn't.

metricNameAndDirectionToTicker(metricName, metricDirection)

Returns a string corresponding to a metric name and direction, which is one component required to build a valid COT ticker ID.

Parameters:

metricName : One of the metric names listed in this library's chart. Invalid values will cause a runtime error.

metricDirection : Metric direction. Possible values are: "Long", "Short", "Spreading", and "No direction".

Valid values vary with metrics. Invalid values will cause a runtime error.

Returns: The part of a COT ticker ID string, e.g., "OI_OLD" for "Open Interest" and "No direction",

or "TC_L" for "Traders Commercial" and "Long".

typeToTicker(metricType)

Converts a metric type into one component required to build a valid COT ticker ID.

See the "Old and Other Futures" section of the CFTC's Explanatory Notes for details on types.

Parameters:

metricType : Metric type. Accepted values are: "All", "Old", "Other".

Returns: The part of a COT ticker.

convertRootToCOTCode(mode, convertToCOT)

Depending on the `mode`, returns a CFTC code using the chart's symbol or its currency information when `convertToCOT = true`.

Otherwise, returns the symbol's root or currency information. If no COT data exists, a runtime error is generated.

Parameters:

mode : A string determining how the function will work. Valid values are:

"Root": the function extracts the futures symbol root (e.g. "ES" in "ESH2020") and looks for its CFTC code.

"Base currency": the function extracts the first currency in a pair (e.g. "EUR" in "EURUSD") and looks for its CFTC code.

"Currency": the function extracts the quote currency ("JPY" for "TSE:9984" or "USDJPY") and looks for its CFTC code.

"Auto": the function tries the first three modes (Root -> Base Currency -> Currency) until a match is found.

convertToCOT : "bool" value that, when `true`, causes the function to return a CFTC code.

Otherwise, the root or currency information is returned. Optional. The default is `true`.

Returns: If `convertToCOT` is `true`, the part of a COT ticker ID string.

If `convertToCOT` is `false`, the root or currency extracted from the current symbol.

COTTickerid(COTType, CTFCCode, includeOptions, metricName, metricDirection, metricType)

Returns a valid TradingView ticker for the COT symbol with specified parameters.

Parameters:

COTType : A string with the type of the report requested with the ticker, one of the following: "Legacy", "Disaggregated", "Financial".

CTFCCode : The for the asset, e.g., wheat futures (root "ZW") have the code "001602".

includeOptions : A boolean value. 'true' if the symbol should include options and 'false' otherwise.

metricName : One of the metric names listed in this library's chart.

metricDirection : Direction of the metric, one of the following: "Long", "Short", "Spreading", "No direction".

metricType : Type of the metric. Possible values: "All", "Old", and "Other".

Returns: A ticker ID string usable with `request.security()` to fetch the specified Commitment of Traders data.

█ AVAILABLE METRICS

Different COT types provide different metrics. The table of all metrics available for each of the types can be found below.

+------------------------------+------------------------+

| Legacy (COT) Metric Names | Directions |

+------------------------------+------------------------+

| Open Interest | No direction |

| Noncommercial Positions | Long, Short, Spreading |

| Commercial Positions | Long, Short |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No direction |

| Traders Noncommercial | Long, Short, Spreading |

| Traders Commercial | Long, Short |

| Traders Total Reportable | Long, Short |

| Concentration Gross LT 4 TDR | Long, Short |

| Concentration Gross LT 8 TDR | Long, Short |

| Concentration Net LT 4 TDR | Long, Short |

| Concentration Net LT 8 TDR | Long, Short |

+------------------------------+------------------------+

+-----------------------------------+------------------------+

| Disaggregated (COT2) Metric Names | Directions |

+-----------------------------------+------------------------+

| Open Interest | No Direction |

| Producer Merchant Positions | Long, Short |

| Swap Positions | Long, Short, Spreading |

| Managed Money Positions | Long, Short, Spreading |

| Other Reportable Positions | Long, Short, Spreading |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No Direction |

| Traders Producer Merchant | Long, Short |

| Traders Swap | Long, Short, Spreading |

| Traders Managed Money | Long, Short, Spreading |

| Traders Other Reportable | Long, Short, Spreading |

| Traders Total Reportable | Long, Short |

| Concentration Gross LE 4 TDR | Long, Short |

| Concentration Gross LE 8 TDR | Long, Short |

| Concentration Net LE 4 TDR | Long, Short |

| Concentration Net LE 8 TDR | Long, Short |

+-----------------------------------+------------------------+

+-------------------------------+------------------------+

| Financial (COT3) Metric Names | Directions |

+-------------------------------+------------------------+

| Open Interest | No Direction |

| Dealer Positions | Long, Short, Spreading |

| Asset Manager Positions | Long, Short, Spreading |

| Leveraged Funds Positions | Long, Short, Spreading |

| Other Reportable Positions | Long, Short, Spreading |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No Direction |

| Traders Dealer | Long, Short, Spreading |

| Traders Asset Manager | Long, Short, Spreading |

| Traders Leveraged Funds | Long, Short, Spreading |

| Traders Other Reportable | Long, Short, Spreading |

| Traders Total Reportable | Long, Short |

| Concentration Gross LE 4 TDR | Long, Short |

| Concentration Gross LE 8 TDR | Long, Short |

| Concentration Net LE 4 TDR | Long, Short |

| Concentration Net LE 8 TDR | Long, Short |

+-------------------------------+------------------------+

Daily Floor PivotsDaily Floor Pivots with Comprehensive Statistical Analysis

Overview

This indicator combines traditional floor pivot levels with golden zone analysis and comprehensive statistical insights derived from 15 years of historical NQ futures data. While the pivot levels and golden zones can be applied to any instrument, the statistical tables are specifically calibrated for NQ/MNQ futures based on analysis of 2,482 NY Regular Trading Hours (RTH) sessions from 2010-2025.

What Makes This Indicator Original

Unlike standard pivot indicators that merely plot levels, this tool provides:

Enhanced Golden Zone Analysis: Calculates not only the main golden zone (0.5-0.618 retracement of previous day's range) but also golden zones between each pivot pair (PP-R1, R1-R2, R2-R3, PP-S1, S1-S2, S2-S3)

Data-Driven Statistical Tables: Two comprehensive tables displaying real statistics from 2,482 trading days of NQ analysis, including:

Probability-based touch rates and continuation patterns

Context-aware statistics based on opening position

Gap analysis and behavioral patterns

First touch dynamics and time-to-reach averages

Granular Customization: Every visual element and statistical section can be independently toggled, allowing traders to focus on what matters most to their strategy

How It Works

Pivot Calculation Methodology

The indicator uses the standard floor pivot formula based on the previous day's price action:

Pivot Point (PP) = (Previous High + Previous Low + Previous Close) / 3

Resistance Levels: R1, R2, R3 calculated from PP and previous range

Support Levels: S1, S2, S3 calculated from PP and previous range

Golden Zone Calculations

Main Golden Zone: The 0.5 to 0.618 Fibonacci retracement of the previous day's range, representing a key reversal and continuation area.

Inter-Pivot Golden Zones: For each adjacent pivot pair, golden zones are calculated as:

Resistance pairs (PP→R1, R1→R2, R2→R3): 0.5-0.618 range from the lower pivot

Support pairs (PP→S1, S1→S2, S2→S3): 0.382-0.5 range from the upper pivot

These zones represent high-probability areas where price tends to react when moving between pivot levels.

Statistical Analysis Source

All statistics displayed in the tables are derived from external Python analysis of 15 years of 1-minute NQ futures data (2010-2025), specifically analyzing NY RTH sessions (9:30 AM - 4:00 PM EST). The analysis tracked:

2,482 complete trading days

Intraday pivot touches and closes

Opening position context

Gap behavior relative to previous day

Time-of-day patterns

Sequential pivot interactions

IMPORTANT: While the pivot levels and golden zones are universally applicable mathematical calculations that work on any instrument, the statistical percentages shown in the tables are specific to NQ/MNQ behavior only. Do not assume these statistics transfer to other instruments.

Configuration Guide

Basic Settings

Number of Periods Back (1-20, default: 3)

Controls how many historical pivot periods are displayed on the chart

Setting to 1 shows only current day's pivots

Higher values show more historical context

Labels Position (Left/Right)

Choose whether pivot labels appear on the left or right side of each level line

Line Width (1-5, default: 2)

Adjust the thickness of all pivot and golden zone lines

Golden Zone Customization

Show Daily Golden Zone (0.5-0.618)

Toggle the main golden zone on/off

When enabled, displays a shaded box between the 0.5 and 0.618 retracement levels

Line Color / Fill Color

Customize the appearance of the main golden zone

Fill color determines the shaded box transparency

Show Labels / Show Prices

Control whether "0.5" and "0.618" labels appear

Control whether price values are displayed on labels

Inter-Pivot Golden Zones

Six toggle options allow you to show/hide individual golden zones:

PP to R1 / PP to S1: Most frequently touched (60.8% / 50.9%)

R1 to R2 / S1 to S2: Moderately touched (25.2% / 24.0%)

R2 to R3 / S2 to S3: Rarely touched (9.4% / 10.5%)

Line Color / Fill Color: Customize appearance of all inter-pivot zones

Show Labels / Show Prices: Control labeling for inter-pivot zones

Usage Tip: Disable outer zones (R2-R3, S2-S3) on lower volatility days to reduce chart clutter.

Pivot Display

Show Support/Resistance Levels: Master toggle for all pivot lines

Show SR Labels / Show SR Prices: Control labeling on pivot levels

Individual level toggles and colors:

PP (Pivot Point): The central reference point

R1/S1: Primary resistance/support (38.9% / 35.4% touch rate)

R2/S2: Secondary levels (15.6% / 16.1% touch rate)

R3/S3: Extended levels (5.1% / 7.3% touch rate)

Color Customization: Each level's color can be independently set

Overall Statistics Table

Show Overall Statistics Table: Master toggle

Table Size: tiny/small/normal/large/huge/auto

Table Position: Top Left/Top Right/Bottom Left/Bottom Right

Section Toggles (enable/disable individual sections):

Current Session Info

Touch & Close Rates

Continue & Reject Rates

First Touch Statistics

Golden Zone Statistics

Daily Close Distribution

Highest/Lowest Levels Reached

Context Statistics Table

Show Context Statistics Table: Master toggle

Table Size: tiny/small/normal/large/huge/auto

Table Position: Top Left/Top Right/Bottom Left/Bottom Right

Section Toggles:

Current Opening Zone

Opening Zone Statistics

Previous Day Gap Context

Understanding the Statistical Tables

TABLE 1: OVERALL STATISTICS

This table presents universal statistics from 2,482 days of NQ analysis.

Current Session Info

Displays real-time context for the active session:

Open: Where the current RTH session opened relative to pivots (e.g., "GZ_TO_R1" means opened between the PP-R1 golden zone and R1)

Now: Current price position relative to pivots

Direction: Bull (close > open), Bear (close < open), or Flat

How to use: This section helps you quickly understand where price opened and where it currently is, providing immediate context for the day's action.

Touch & Close Rates

Shows probability that each pivot level will be reached during RTH:

Touch %: Percentage of days where price touched this level at any point

Example: R1 touched 38.9% of days, PP touched 57.5% of days

Close %: Percentage of days where price closed beyond this level

Example: R1 close beyond happened 39.8% of days

How to interpret:

Higher touch rates indicate more reliable levels for intraday targeting

The difference between touch and close rates shows rejection frequency

PP has the highest touch rate (57.5%), making it the most magnetic level

Outer levels (R3/S3) have low touch rates (5.1%/7.3%), indicating rare extension days

Continue & Reject Rates

When a level is touched, these statistics show what happens next:

Continue %: Probability price continues through the level

Example: When PP is touched, price continues 88.1% of the time

Reject %: Probability price rejects from the level and reverses

Example: When R1 is touched, price rejects 50.9% of the time

How to interpret:

PP shows highest continuation (88.1%), confirming it's a poor reversal level

Support levels (S1/S2/S3) show strong rejection rates (62.5%/60.7%/56.1%), making them better reversal candidates

Continuation rates above 80% suggest the level is better as a target than an entry

First Touch Statistics

Analyzes which pivot is typically touched first during RTH:

1st Touch %: Probability this level is the first pivot encountered

PP is first touched 37.1% of days (most common)

R1 is first touched 26.0% of days

S1 is first touched 10.9% of days

1st→Continue: If this level is touched first, probability of continuation

S1-S3 show 95.6%-100% continuation when touched first

This means when price reaches support first, it usually continues lower

Avg Time: Minutes after 9:30 AM EST before first touch

PP: 1h 6m average

S3: 19m average (when bearish)

R3: 3h 19m average (when bullish)

How to interpret:

Opening away from PP means higher probability of reaching extremes (R2/R3 or S2/S3)

When support is touched first (within first 2 hours), expect continuation lower

Late-day first touches (after 2 PM) often indicate strong trending days

Multi-Touch: Shows how often levels are tested multiple times (92.8%-95.0% across all levels)

Golden Zone Statistics

Main GZ: 58.5% touch rate for the 0.5-0.618 zone

Inter-Pivot zones:

PP-R1: 60.8% (highest probability)

PP-S1: 50.9%

R1-R2: 25.2%

S1-S2: 24.0%

R2-R3: 9.4%

S2-S3: 10.5%

How to interpret:

Main GZ is touched more often than any individual resistance level

PP-R1 and PP-S1 golden zones are high-probability mean reversion areas

Outer golden zones (R2-R3, S2-S3) are only relevant on high volatility days

Daily Close Distribution

Shows where RTH sessions typically close:

Above/Below PP: 58.5% close above, 41.5% below (slight bullish bias)

Above R1: 24.5% of days

Below S1: 18.7% of days

In GZ: Only 6.3% close in the golden zone (typically transits through it)

How to interpret:

Most days (58.5%) have bullish bias (close above PP)

Less than 25% of days are strong trending days (beyond R1/S1)

Golden zone is an action area, not a resting area

Highest/Lowest Levels Reached

Distribution of the most extreme level reached:

High Resist: R1 (26.0%), R2 (10.8%), R3 (5.1%)

Low Support: S1 (35.4%), S2 (1.9%), S3 (0.6%)

How to interpret:

Most days don't reach beyond R1 or S1

R3/S3 are rare events (5.1%/0.6%), indicating major trending days

S1 is reached as lowest level more often than R1 as highest, suggesting downside is more frequently tested

TABLE 2: CONTEXT STATISTICS

This table provides conditional statistics based on how the session opened.

Current Opening Zone

Displays which of 13 possible zones the RTH session opened in:

ABOVE_R3, R2_TO_R3, R1_TO_R2, GZ_TO_R1, IN_GZ, PP_TO_GZ, AT_PP, GZ_TO_PP, S1_TO_GZ, S2_TO_S1, S3_TO_S2, BELOW_S3

How to use: This immediately tells you the market structure and what type of day to expect.

Opening Zone Statistics

Detailed statistics for the current opening zone (only shows for 6 major zones):

For each zone, you see:

Occurs: How often this opening scenario happens

GZ_TO_R1: 38.4% (most common)

AT_PP: 12.8%

S1_TO_GZ: 24.2%

R1_TO_R2: 9.4%

S2_TO_S1: 6.3%

IN_GZ: 3.8%

Bull/Bear %: Close direction probability

Example: GZ_TO_R1 is perfectly balanced (50.0% bull / 49.6% bear)

R1_TO_R2 is bullish (58.1% bull / 41.0% bear)

Levels Hit: Probability of reaching each pivot level from this opening

Helps identify high-probability targets

Example: From GZ_TO_R1, PP is hit 52.9%, R1 is hit 49.0%, S1 is hit 21.6%

How to interpret:

GZ_TO_R1 (most common): Balanced day, watch PP and GZ for direction clues

AT_PP: Slight bullish bias (56.9%), high chance of touching both PP (92.8%) and GZ (90.3%)

R1_TO_R2: Bullish bias (58.1%), expect continuation to R2 (58.1% chance)

S2_TO_S1: Bullish reversal setup (59.9%), very high chance of S1 touch (82.8%)

IN_GZ: Rare opening (3.8%), bullish bias, virtually guaranteed GZ touch (100%)

Previous Day Gap Context

Shows current gap scenario and typical behavior:

Three scenarios:

GAP UP: Opened Above Yesterday's High (20.5% of days)

R1 Touch: 65.9% (high probability)

R2 Touch: 42.1%

S1 Touch: 15.0% (low probability)

Bias: Bullish continuation

GAP DOWN: Opened Below Yesterday's Low (11.3% of days)

S1 Touch: 71.5% (high probability)

S2 Touch: 55.2%

R1 Touch: 12.1% (low probability)

Bias: Bearish continuation

NO GAP: Opened Within Yesterday's Range (68.2% of days)

PP Touch: 69.5%

GZ Touch: 71.7%

R1 Touch: 35.2%

Bias: Balanced (watch for direction at PP/GZ)

How to interpret:

Gap days (up or down) tend to continue in the gap direction

When gapping, fade trades are low probability (15.0% and 12.1%)

Most days (68.2%) open within previous range, making PP and GZ critical decision zones

The "bias" line provides clear directional guidance for trade selection

Practical Application Examples

Example 1: Standard Day Setup

Scenario: RTH opens at 20,450

PP: 20,400

GZ: 20,390-20,395

R1: 20,425

Previous day high: 20,460

What the tables tell you:

Opening Zone: "GZ_TO_R1" (38.4% occurrence)

Gap Context: "NO GAP" (68.2% occurrence)

Expected behavior: Balanced (50/50 bull/bear)

High probability: PP touch (52.9%), GZ touch (56.8%)

Moderate probability: R1 touch (49.0%), S1 touch (21.6%)

Trade plan:

Wait for price to reach PP (52.9% chance) or GZ (56.8% chance)

Look for directional confirmation at these levels

First target R1 if bullish, S1 if bearish

Avoid assuming direction without confirmation (perfectly balanced opening)

Example 2: Gap Up Day

Scenario: RTH opens at 20,510

Previous day high: 20,460

R1: 20,425

R2: 20,475

What the tables tell you:

Gap Context: "GAP UP" (20.5% occurrence)

R1 touch: 65.9% probability

R2 touch: 42.1% probability

S1 touch: Only 15.0% probability

Bias: Bullish continuation

Trade plan:

Favor long setups

Target R1 first (65.9% chance), then R2 (42.1%)

If R1 breaks, R2 becomes likely target

Shorting is low probability (only 15.0% reach S1)

Example 3: Opening in Golden Zone

Scenario: RTH opens at 20,393

PP: 20,400

GZ: 20,390-20,395

What the tables tell you:

Opening Zone: "IN_GZ" (rare, only 3.8% occurrence)

Bullish bias: 58.1%

GZ touch: 100% (guaranteed - already there)

PP touch: 75.3%

R1 touch: 41.9%

Trade plan:

Expect price to test PP (75.3% chance)

Slight bullish bias suggests long setups better than shorts

Watch how price reacts at PP - likely to continue to R1 (41.9%)

This is an uncommon opening, suggesting potential for larger moves

Best Practices

Match Your Instrument: Remember, statistics are NQ-specific. If trading other instruments, use the levels but disregard the statistical percentages.

Combine with Price Action: Use the statistics for probability context, not as standalone signals. Always confirm with price action, volume, and your trading methodology.

Adapt Table Display: Don't display all sections all the time. Toggle based on your trading phase:

Pre-market: Focus on "Gap Context" to understand the setup

Market open: Watch "Opening Zone Statistics" for directional bias

Intraday: Monitor "Current Session Info" for position tracking

Understand Context: A 60% touch rate doesn't mean guaranteed—it means 40% of days don't touch. Use these probabilities to size positions and manage expectations.

Inter-Pivot Golden Zones: These are most useful when price is already in motion toward a level. For example, if price breaks above PP heading to R1, the PP-R1 golden zone (60.8% touch rate) becomes a high-probability pullback area.

Time Awareness: The "Avg Time" statistics help you understand urgency. If it's 10:30 AM and S1 hasn't been touched (average is 55 minutes), the window for bearish moves is closing.

Technical Notes

Time Zone: All times referenced are NY/EST

Session Definition: RTH is 9:30 AM - 4:00 PM EST

Calculation Period: Pivots update daily based on previous 24-hour period (18:00 previous day to 17:00 current day)

Data Source: Statistics derived from 12 years of NQ 1-minute futures data (2013-2025)

Sample Size: 2,482 complete RTH trading sessions

Disclaimer

This indicator provides statistical probabilities based on historical NQ futures data. Past performance does not guarantee future results. The statistical tables are educational tools and should not be the sole basis for trading decisions. Always:

Use proper risk management

Combine with your own analysis

Understand that probabilities are not certainties

Remember that statistics are instrument-specific (NQ/MNQ only)

Credits

Statistical analysis performed using Python analysis of 12 years of historical NQ futures data. All pivot and golden zone calculations use standard mathematical formulas applicable to any instrument.

4H HOD/LOD Checkpoint Analysis4H HOD/LOD Checkpoint Analysis - Detailed User Guide

OVERVIEW

This indicator is a data-driven probability framework for NQ Futures traders that predicts High-of-Day (HOD) and Low-of-Day (LOD) placement based on statistical analysis of 3,136+ trading days (2013-2025). Unlike traditional indicators that rely on technical signals, this tool uses checkpoint-based state analysis with zero forward-looking bias to provide real-time probabilities of whether the daily range is complete.

⚠️ IMPORTANT: This indicator is specifically designed for NQ FUTURES ONLY. All probabilities, patterns, and statistics were derived from a 10+ year historical dataset of NQ 1-minute bars. Using this on other instruments will produce inaccurate results.

CORE CONCEPT: CHECKPOINT METHODOLOGY

What is a Checkpoint?

A checkpoint occurs when a 4-hour candle closes. At this moment, the indicator "locks" the current market state and calculates probabilities for the remainder of the trading day. The key innovation is that state never changes after locking - probabilities remain constant throughout the session until the next checkpoint.

The Six 4-Hour Candles (EST):

6PM (18:00-22:00) - Evening/Globex open

10PM (22:00-02:00) - Asia session

2AM (02:00-06:00) - Early London

6AM (06:00-10:00) - Late London + NY Open

10AM (10:00-14:00) - NY Morning

2PM (14:00-17:00) - NY Afternoon (3 hours only)

Five Checkpoints:

10PM Checkpoint - After 6PM closes

2AM Checkpoint - After 10PM closes

6AM Checkpoint - After 2AM closes

10AM Checkpoint - After 6AM closes (most critical)

2PM Checkpoint - After 10AM closes (highest conviction fade signals)

HOW IT WORKS: THE THREE-FACTOR STATE SYSTEM

At each checkpoint, the indicator evaluates three critical factors to determine probability:

1. ELIMINATIONS (Quantity)

An "elimination" occurs when a candle trades beyond a previous candle's high or low, effectively removing that candle from contention for HOD/LOD.

Example at 10AM Checkpoint:

6PM high = 18,000

10PM high = 18,050 (eliminates 6PM high)

2AM high = 18,100 (eliminates 10PM high)

6AM high = 18,075 (does NOT eliminate 2AM high)

Result: 2 eliminations

The number of eliminations indicates trend strength:

0 eliminations = Range-bound, high probability extremes already set

1-2 eliminations = Moderate trend

3-4 eliminations = Strong trend day, range likely to extend

2. STRUCTURE (Pattern Type)

The indicator distinguishes between two elimination patterns:

Sequential: Eliminations occur in order (6pm → 10pm → 2am → 6am → 10am)

Indicates smooth, consistent trend

Example: 10pm eliminates 6pm, then 2am eliminates 10pm (sequential)

Skip: Eliminations skip candles

Indicates choppy/reversal behavior

Example: 2am eliminates 6pm but NOT 10pm (skip pattern)

Why it matters: Skip patterns show 2X probability differences compared to sequential patterns. At 10AM checkpoint with 2 eliminations, skip pattern shows 64% participation rate vs 36% for sequential pattern with previous survived.

3. PREVIOUS CANDLE STATUS

Did the immediately prior candle get eliminated?

Eliminated: Previous candle's high/low was taken out

Indicates relentless trend

Higher probability of continuation

Survived: Previous candle's high/low still intact

Indicates trend pause

Higher probability of mean reversion or range completion

Critical insight: High and low are tracked separately. At 2AM checkpoint, 10PM might have eliminated 6PM high (relentless uptrend) but NOT eliminated 6PM low (low survived). This creates different probabilities for HOD vs LOD.

VISUAL ELEMENTS

4-Hour Candle Boxes

Each 4H candle is displayed as a colored box showing its range:

Gray = 6PM (evening)

Blue = 10PM (Asia)

Purple = 2AM (early London)

Orange = 6AM (London + NY Open) - THE CURVE SESSION

Teal = 10AM (NY morning) - THE MONEY SESSION

Red = 2PM (NY afternoon) - THE FADE SESSION

HOD/LOD Lines

Black horizontal lines extend from current HOD/LOD with labels showing:

Which candle set the extreme

Current price level

THE CHECKPOINT TABLE EXPLAINED

Table Header:

Shows current checkpoint (e.g., "🎯 10AM CHECKPOINT") or "⏳ PRE-CHECKPOINT" if between checkpoints.

Main Metrics (Side-by-Side Comparison):

The table displays HOD and LOD separately in two columns because they can have different patterns:

METRIC

HODLOD Eliminations

Number of candles eliminated so far for highs

Number of candles eliminated so far for lows

Structure

Sequential or Skip pattern for highs

Sequential or Skip pattern for lows

Prev Candle

Was previous candle's high eliminated or did it survive?

Was previous candle's low eliminated or did it survive?

Pattern

Combined interpretation: Relentless/Paused/Skip/Early

Combined interpretation: Relentless/Paused/Skip/Early

Color Coding:

Structure Row:

White = Sequential (smooth trend)

Orange = Skip (choppy/reversal)

Previous Candle Row:

Red = Eliminated (relentless trend continuing)

Blue = Survived (trend paused)

Pattern Row:

Red = Relentless (previous eliminated + sequential = strong trend)

Blue = Paused (previous survived + sequential = trend pause)

Orange = Skip/Chop (skip pattern = reversal likely)

Gray = Early (0-1 eliminations, too early to tell)

Probability Section:

Prob Already In: Percentage chance that HOD/LOD has already been set

Color coding:

Green (>75%) = High confidence extreme is in, FADE

Yellow (45-75%) = Moderate confidence

Red (<45%) = Low confidence extreme is in, CONTINUATION likely

Sample Size: Shows how many historical occurrences match this exact state (n=XXX)

Larger samples = higher confidence

Most common states have n=500-2,000+

Current: Which candle currently holds HOD/LOD

Pattern Guide Section:

Appears when you have 2+ eliminations. Provides interpretation:

📈 Paused: Trend has paused, 2pm more likely to set extreme

📈 Relentless: Breaking higher/lower, continuation expected

📈 Skip/Chop: Choppy pattern, next session likely

Same for lows with 📉 symbol.

PRACTICAL TRADING EXAMPLES

Example 1: High Conviction Fade Setup

State at 10AM Checkpoint:

Eliminations: 0 (both HOD/LOD)

Structure: None (no eliminations yet)

Prev Candle: Survived

Table shows:

HOD Prob Already In: 68.9% (n=582)

LOD Prob Already In: 73.6% (n=785)

Interpretation: Range is likely complete. Fade extremes. With 0 eliminations and 70%+ probability, this is a high-conviction mean reversion signal.

Example 2: Strong Continuation Signal

State at 10AM Checkpoint:

Eliminations: 3 (both HOD/LOD)

Structure: Sequential

Prev Candle: Eliminated (relentless)

Table shows:

HOD Prob Already In: 29.8% (n=1,758)

LOD Prob Already In: 34.6% (n=1,451)

Pattern: 📈 Relentless / 📉 Relentless

Interpretation: Strong trend day. Only 30-35% chance range is complete. Look for breakouts in direction of trend. 10AM and 2PM likely to extend range.

Example 3: Pattern Structure Edge

State at 10AM Checkpoint:

Eliminations: 2 (HOD)

Structure: Skip (orange background)

Prev Candle: Eliminated vs Alternative State:

Eliminations: 2 (HOD)

Structure: Sequential

Prev Candle: Survived

Result: Skip pattern shows 64% chance 10AM participates vs 36% for sequential+survived. Skip pattern = 2X more likely to see 10AM high. This structural edge is unique to this indicator.

Example 4: Different HOD vs LOD Patterns

State at 10AM Checkpoint:

HOD: 2 eliminations, Sequential, Previous Eliminated (Relentless) = 46.7% in

LOD: 2 eliminations, Skip, Previous Eliminated (Choppy) = 48.4% in

Interpretation: Highs show relentless uptrend but lows show choppy behavior. This divergence suggests potential for upside continuation but with volatility. Not a clean trend day.

KEY CHECKPOINT STATISTICS (DERIVED FROM 10-YEAR DATASET)

10PM Checkpoint (After 6PM):

Very early in day

13.5% HOD in, 21.3% LOD in

Most likely outcome: Range extends into 6AM/10AM

2AM Checkpoint (After 10PM):

Still early

With 0 elims: 22-31% in (balanced)

With 1 elim: 8-12% in (strong trend signal)

6AM Checkpoint (After 2AM) - Critical Decision Point:

With 0 elims: 40-47% in (balanced, could go either way)

With 2 elims: 18-22% in (strong trend into 6AM/10AM)

Most likely outcome: 10AM sets extremes (~38-40%)

10AM Checkpoint (After 6AM) - Highest Conviction:

With 0 elims: 69-74% in → FADE (high confidence)

With 3 elims: 30-35% in → BUY/SELL continuation

This is THE money checkpoint for high-probability setups

2PM Checkpoint (After 10AM) - Maximum Fade Conviction:

With 0-3 elims: 67-95% in → FADE strongly

With 4 elims: 49-61% in (monster trend, weaker fade)

2PM is primarily a mean reversion session

UNDERSTANDING THE UNDERLYING DATA

All probabilities are derived from analysis of:

Instrument: NQ Futures (E-mini NASDAQ-100)

Timeframe: 1-minute bars

Period: January 2013 - December 2025

Sample: 3,136+ complete trading days

Methodology: Real-time checkpoint analysis with zero forward-looking bias

Why NQ-Specific?

Each futures contract has unique:

Session characteristics (6AM in NQ shows 60-64% curve behavior, other sessions differ)

Timing patterns (NQ's 10AM session has 67-74% immediate takeouts)

Volatility profiles (NQ 2PM shows 56% bullish bias vs ES shows different bias)

Using this indicator on ES, RTY, or other instruments will produce inaccurate results because the probability tables are NQ-specific.

ORIGINALITY & INNOVATION

What Makes This Indicator Unique:

Zero Forward-Looking Bias: State locks at checkpoint moments. Traditional indicators recalculate continuously, introducing bias. This indicator freezes probabilities at the exact moment a 4H candle closes.

Three-Factor State System: Combines elimination count, structure pattern, and previous candle status. Most indicators only track one dimension. This multi-factor approach provides 2X+ probability differentials.

Separate HOD/LOD Tracking: Highs and lows can have different patterns simultaneously (relentless high with choppy low). This indicator tracks them separately for precision.

Pattern Structure Analysis: Distinguishes between sequential and skip patterns, a concept not found in standard indicators. Skip patterns show mean reversion while sequential shows continuation.

10+ Year Statistical Foundation: Every probability is backed by hundreds to thousands of historical occurrences (sample sizes shown in table). Not based on theories or assumptions.

Checkpoint-Specific Probabilities: Different checkpoints have different probability profiles. 10AM checkpoint with 0 eliminations = 70%+ fade. 6AM checkpoint with same state = 40%+ fade. Context matters.

HOW TO USE THIS INDICATOR

Step 1: Wait for Checkpoint

The table will show "⏳ PRE-CHECKPOINT" until a 4H candle closes. Probabilities are only valid at checkpoint moments.

Step 2: Read the State

Check the three factors:

How many eliminations?

Sequential or skip?

Previous candle eliminated or survived?

Step 3: Check Probability

Look at "Prob Already In" percentage:

>75% (Green) = High confidence extreme is set, fade

45-75% (Yellow) = Moderate confidence, use other confirmation

<45% (Red) = Low confidence extreme is set, continuation likely

Step 4: Check Sample Size

Larger sample (n=1,000+) = higher confidence

Smaller sample (n=50-200) = use caution, edge is real but less robust

Step 5: Consider Pattern

Read the pattern guide:

Relentless = trend continuing

Paused = trend stalled, mean reversion

Skip/Chop = reversal/range likely

Step 6: Compare HOD vs LOD

If both show similar patterns = cleaner signal

If divergent patterns = complex day, be cautious

BEST PRACTICES

Focus on 10AM and 2PM checkpoints - These have the highest conviction signals

Combine with price action - Don't fade blindly at 90% probability if price is breaking out strongly

Larger samples = better edges - Prioritize setups with n=500+

Watch for pattern divergence - When HOD and LOD show different patterns, expect complexity

Remember session characteristics:

6AM = THE CURVE SESSION (60-64% mean reversion when Q2 breaks Q1)

10AM = THE MONEY SESSION (67-74% immediate takeouts, highest conviction)

2PM = THE FADE SESSION (67-95% extremes already in)

SETTINGS

Show 4H Candle Boxes - Display colored boxes for each 4H candle

Show HOD/LOD Lines - Display horizontal lines at current extremes

Show Checkpoint Analysis - Display probability table

Table Position - Choose where to place the checkpoint table

Table Size - Tiny/Small/Normal

Colors - Customize box colors for each session

LIMITATIONS & DISCLAIMERS

NQ FUTURES ONLY - Do not use on other instruments

Not a standalone system - Use as confluence with your strategy

Historical data - Past performance doesn't guarantee future results

Sample size variance - Some states have smaller samples, use judgment

Requires understanding - Read this guide fully before trading with this tool

FINAL NOTES

This indicator represents 10+ years of NQ futures data distilled into actionable, real-time probabilities. The checkpoint methodology ensures zero forward-looking bias, while the three-factor state system provides granular edge that traditional indicators miss.

Remember: This tool provides probabilities, not certainties. Trade with proper risk management, and use this as one input in your decision-making process.

First presented FVG (w/stats) w/statistical hourly ranges & biasOverview

This indicator identifies the first Fair Value Gap (FVG) that forms during each hourly session and provides comprehensive statistical analysis based on 12 years of historical NASDAQ (NQ) data. It combines price action analysis with probability-based statistics to help traders make informed decisions.

⚠️ IMPORTANT - Compatibility

Market: This indicator is designed exclusively for NASDAQ futures (NQ/MNQ)

Timeframe: Statistical data is based on FVGs formed on the 5-minute timeframe

FVG Detection: Works on any timeframe, but use 5-minute for accuracy matching the statistical analysis

All hardcoded statistics are derived from 12 years of NQ historical data

What It Does

1. FVG Detection & Visualization

Automatically detects the first FVG (bullish or bearish) that forms each hour

Draws colored boxes around FVGs:

Blue boxes = Bullish FVG (gap up)

Red boxes = Bearish FVG (gap down)

FVG boxes extend to the end of the hour

Optional midpoint lines show the center of each FVG

Uses volume imbalance logic (outside prints) to refine FVG boundaries

2. Hourly Reference Lines

Vertical Delimiter: Marks the start of each hour

Hourly Open Line: Shows where the current hour opened

Expected Range Lines: Projects the anticipated high/low based on historical data

Choose between Mean (average) or Median (middle value) statistics

Upper range line (teal/green)

Lower range line (red)

All lines span exactly one hour from the moment it opens

Optional labels show price values at line ends

3. Real-Time Statistics Table

The table displays live data for the current hour only:

Hour: Current hour in 12-hour format (AM/PM)

FVG Status: Shows if a Bull FVG, Bear FVG, or no FVG has formed yet

Green background = Bullish FVG detected

Red background = Bearish FVG detected

1st 15min: Direction of the first 15 minutes (Bullish/Bearish/Neutral/Pending)

Continuation %: Historical probability that the hour continues in the first 15-minute direction

Color-coded: Green for bullish, red for bearish

Avg Range %: Expected percentage range for the current hour (based on 12-year mean)

FVG Effect %: Historical probability that FVG direction predicts hourly close direction

Shows BISI→Bull % for bullish FVGs

Shows SIBI→Bear % for bearish FVGs

Blank if no FVG has formed yet

Time Left: Countdown timer showing MM:SS remaining in the hour (updates in real-time)

Hourly Bias: Historical directional tendency (bullish % or bearish %)

H Open: Current hour's opening price

Exp Range: Projected price range (Low - High) based on historical average

Customization Options

Detection Settings:

Lower Timeframe Selection (15S, 1min, 5min) - controls FVG detection granularity

Display Settings:

FVG box colors (bullish/bearish)

Midpoint lines (show/hide, color, style)

Table Settings:

Position (9 locations: corners, edges, center)

Text size (Tiny, Small, Normal, Large)

Hourly Lines:

Toggle each line type on/off

Hour delimiter (color, width)

Open line (color, width, style)

Range lines (color, width, style)

Choose Mean or Median statistics for range calculation

Show/hide labels with customizable text size

How to Use

Apply to NQ futures chart (NQ1! or MNQ1!)

Set chart to 5-minute timeframe for optimal FVG detection matching the statistical data

Watch for the first FVG to form each hour

Reference the table for probability-based decision support:

High continuation % = strong directional bias

FVG Effect % shows reliability of the FVG signal

Time Left helps manage entries/exits within the hour

Use range lines as potential targets or reversal zones

Statistical Foundation

All statistics are derived from:

12 years of NASDAQ (NQ) historical data

Hourly analysis of FVG formation patterns

First 15-minute directional analysis

Mean and Median calculations for range expectations

Data encompasses 2,400+ samples per hour

Best Practices

✅ Use on NQ/MNQ futures only

✅ Best on 5-minute charts (matches statistical data)

✅ Combine FVG signals with continuation probabilities

✅ Use range lines as potential profit targets

✅ Watch the countdown timer for hour-end setups

❌ Do not use on other markets (statistics won't apply)

❌ Avoid using during low-liquidity hours (5PM ET has minimal data)

Technical Notes

Timezone: America/New_York (EST/EDT)

Weekend filtering: Automatically hides data during market closure

Updates in real-time on live bars

Maximum 500 boxes/lines for performance

FVG detection includes volume imbalance (body gap) refinement

Credits

Statistical analysis based on 12 years of NASDAQ historical data. FVG detection methodology follows ICT concepts with volume imbalance refinement.

Disclaimer: This indicator provides statistical analysis based on historical data. Past performance does not guarantee future results. Always use proper risk management.

Would you like me to adjust any section or add/remove anything?6-9 Session & Levels - Customizable Range Analysis Indicator

Description:

This indicator provides comprehensive session-based range analysis designed for intraday traders. It calculates and displays key levels based on a customizable session period (default 6:00-9:00 AM ET).

Core Features:

Sespastedthis is a summary for another indicator- i was hoping for something more like this in terms of content etc22:23Architected comprehensive indicator summary matching professional documentation style.The user wants me to rewrite the summary for their FVG indicator in a similar style to the example provided. The example is more structured, detailed, and professional. Let me create a comprehensive summary that follows that format:

Clear title

Description/Overview

Core Features (broken down into sections)

Input Settings Explained (detailed breakdown of all customization options)

How It Works section

Use Case

Note/Disclaimer

Let me make it thorough and match the style while being accurate to their indicator's functionality.Here's a detailed summary in that format:

Every Hour 1st FVG with Statistical Analysis - NASDAQ Hourly Trading Intelligence

Description:

This indicator identifies the first Fair Value Gap (FVG) that forms during each hourly session and provides comprehensive probability-based statistical analysis derived from 12 years of NASDAQ (NQ) historical data. It combines real-time FVG detection with hardcoded statistical probabilities to help intraday traders make informed decisions based on historical patterns and hourly price action dynamics.

IMPORTANT: This indicator is specifically calibrated for NASDAQ futures (NQ/MNQ) only. All statistical data is derived from 12 years of NQ historical analysis with FVGs detected on the 5-minute timeframe. Using this indicator on other markets will produce invalid statistical results.

Core Features:

FVG Detection & Visualization

Automatically detects and displays the first Fair Value Gap (bullish or bearish) that forms within each hourly session

Color-coded boxes mark FVG zones: Blue for bullish FVGs (gap up), Red for bearish FVGs (gap down)

FVG boxes extend precisely to the end of the hour boundary

Optional midpoint lines show the center point of each FVG

Uses volume imbalance logic (outside prints) to refine FVG boundaries beyond simple wick-to-wick gaps

Supports both chart timeframe detection and lower timeframe detection via request.security_lower_tf

Hourly Reference Lines

Vertical Hour Delimiter: Marks the exact start of each new hour with an extendable vertical line

Hourly Open Line: Displays the opening price of the current hour

Expected Range Lines: Projects anticipated high and low levels based on 12 years of statistical data

Choose between Mean (average) or Median (middle value) calculations

Upper range line shows expected high

Lower range line shows expected low

All lines span exactly one hour from open to close

Optional labels display exact price values at the end of each line

Real-Time Statistics Table

Displays comprehensive live data for the current hour only:

Hour: Current hour in 12-hour format (e.g., "9AM", "2PM")

FVG Status: Shows detection state with color coding

"None Yet" (white background) - No FVG detected

"Bull FVG" (green background) - Bullish FVG identified

"Bear FVG" (red background) - Bearish FVG identified

1st 15min: Direction of first 15 minutes (Bullish/Bearish/Neutral/Pending)

Continuation %: Historical probability that the hour closes in the direction of the first 15 minutes

Green background with up arrow (↑) for bullish continuation probability

Red background with down arrow (↓) for bearish continuation probability

Avg Range %: Expected percentage range for the current hour based on 12-year mean

FVG Effect %: Historical effectiveness of FVG directional prediction

Shows "BISI→Bull %" for bullish FVGs (gap up predicting bullish hourly close)

Shows "SIBI→Bear %" for bearish FVGs (gap down predicting bearish hourly close)

Displays blank if no FVG has formed yet

Time Left: Real-time countdown timer showing minutes and seconds remaining in the hour (MM:SS format)

Hourly Bias: Historical directional tendency showing bullish or bearish percentage bias

H Open: Current hour's opening price

Exp Range: Projected price range showing "Low - High" based on selected statistic (mean or median)

Input Settings Explained:

Detection Settings

Lower Timeframe: Select the base timeframe for FVG detection

Options: 15S (15 seconds), 1 (1 minute), 5 (5 minutes)

Recommendation: Use 5-minute to match the statistical data sample

The indicator uses this timeframe to scan for FVG patterns even when viewing higher timeframes

Display Settings

Bullish FVG Color: Set the color and transparency for bullish (upward) FVG boxes

Bearish FVG Color: Set the color and transparency for bearish (downward) FVG boxes

Show Midpoint Lines: Toggle horizontal lines at the center of each FVG box

Midpoint Line Color: Customize the midpoint line color

Midpoint Line Style: Choose between Solid, Dotted, or Dashed line styles

Table Settings

Table Position: Choose from 9 locations:

Top: Left, Center, Right

Middle: Left, Center, Right

Bottom: Left, Center, Right

Table Text Size: Select from Tiny, Small, Normal, or Large for readability on different screen sizes

Hourly Lines Settings

Show Hourly Lines: Master toggle for all hourly reference lines

Show Hour Delimiter: Toggle the vertical line marking each hour's start

Delimiter Color: Customize color and transparency

Delimiter Width: Set line thickness (1-5)

Show Hourly Open: Toggle the horizontal line at the hour's opening price

Open Line Color: Customize color

Open Line Width: Set thickness (1-5)

Open Line Style: Choose Solid, Dashed, or Dotted

Show Range Lines: Toggle the expected high/low projection lines

Range Statistic: Choose "Mean" (12-year average) or "Median" (12-year middle value)

Range High Color: Customize upper range line color and transparency

Range Low Color: Customize lower range line color and transparency

Range Line Width: Set thickness (1-5)

Range Line Style: Choose Solid, Dashed, or Dotted

Show Line Labels: Toggle price labels at the end of all horizontal lines

Label Text Size: Choose Tiny, Small, or Normal

How It Works:

FVG Detection Logic:

The indicator scans price action on the selected lower timeframe (default: 1-minute) looking for Fair Value Gaps using a 3-candle pattern:

Bullish FVG: Formed when candle 's high is below candle 's low, creating an upward gap

Bearish FVG: Formed when candle 's low is above candle 's high, creating a downward gap

The detection is refined using volume imbalance logic by checking for body gaps (outside prints) on both sides of the middle candle. This narrows the FVG zone to areas where bodies don't touch, indicating stronger imbalances.

Only the first FVG that forms during each hour is displayed. If a bullish FVG forms first, it takes priority. The FVG box is drawn from the formation time through to the end of the hour.

Statistical Analysis:

All probability statistics are hardcoded from 12 years (2,400+ samples per hour) of NASDAQ futures analysis:

First 15-Minute Direction: At 15 minutes into each hour, the indicator determines if price closed above, below, or equal to the hour's opening price

Continuation Probability: Historical analysis shows the likelihood that the hour closes in the same direction as the first 15 minutes

Example: If 9AM's first 15 minutes are bullish, there's a 60.1% chance the entire 9AM hour closes bullish (lowest continuation hour)

4PM shows the highest continuation at 86.1% for bullish first 15 minutes

FVG Effectiveness: Tracks how often the first FVG's direction correctly predicts the hourly close direction

BISI (Bullish Imbalance/Sell-side Inefficiency) → Bullish close probability

SIBI (Bearish Imbalance/Buy-side Inefficiency) → Bearish close probability

Range Expectations: Mean and median values represent typical price movement percentage for each hour

9AM and 10AM show the largest ranges (~0.6%)

5PM shows minimal range (~0.06%) due to low liquidity

Hourly Reference Lines:

When each new hour begins:

Vertical delimiter marks the hour's start

Hourly open line plots at the first bar's opening price

Range projection lines calculate expected high/low:

Upper Range = Hourly Open + (Range% / 100 × Hourly Open)

Lower Range = Hourly Open - (Range% / 100 × Hourly Open)

Lines extend exactly to the hour's end time

Labels appear at line endpoints showing exact prices

Real-Time Updates:

FVG Status: Updates immediately when the first FVG forms

First 15min Direction: Locked in at the 15-minute mark

Countdown Timer: Uses timenow to update every second

Table Statistics: Refresh on every bar close

Timezone Handling:

All times are in America/New_York (Eastern Time)

Automatically filters weekend periods (Saturday and Sunday before 6PM)

Hour detection accounts for daylight saving time changes

Use Cases:

Intraday Trading Strategy Development:

FVG Entry Signals: Use the first hourly FVG as a directional bias

Bullish FVG + High continuation % = Strong long setup

Bearish FVG + High continuation % = Strong short setup

First 15-Minute Breakout: Combine first 15-min direction with continuation probabilities

Wait for first 15 minutes to complete

If continuation % is above 70%, trade in that direction

Example: 4PM bullish first 15 min = 86.1% chance hour closes bullish

Range Targeting: Use expected high/low lines as profit targets or reversal zones

Price approaching mean high = potential resistance

Price approaching mean low = potential support

Compare mean vs median for different risk tolerance (median is more conservative)

Hour Selection: Focus trading on hours with:

High FVG effectiveness (11AM: 81.5% BISI→Bull)

High continuation rates (4PM: 86.1% bull continuation)

Avoid low-continuation hours like 9AM (60.1%)

Time Management: Use the countdown timer to:

Enter early in the hour when FVG forms

Exit before hour-end if no follow-through

Avoid late-hour entries with <15 minutes remaining

Statistical Edge Identification:

Compare current hour's FVG against historical effectiveness

Identify when first 15-min direction contradicts FVG direction (conflict = caution)

Use hourly bias to confirm or contradict FVG signals