Daily High/Low Close Breakout - GOLD### **Daily High/Low Close Breakout Indicator**

This indicator is a powerful tool for identifying potential breakout opportunities based on the previous day's price action. It's built on a unique time-based logic that defines key support and resistance levels for the trading day.

---

### **How the Indicator Works**

The indicator operates in two main phases:

1. **Calculation Period (00:00 to 16:30 Tehran Time):** The indicator first observes the price action from the start of the day until 16:30. During this time, it records the highest and lowest **closing prices** of all candles. The chart background is shaded gray to visually mark this period.

2. **Trading Period (16:30 to 16:30 the next day):** At 16:30, the highest and lowest close levels are finalized and drawn as horizontal lines. These levels then become the primary breakout zones for the next 24 hours. The indicator will generate signals whenever the price crosses these lines.

---

### **Trading Signals**

The indicator uses a simple and effective crossover logic for its signals:

* **BUY Signal:** A signal is generated when a candle's closing price **crosses above** the high close line.

* **SELL Signal:** A signal is generated when a candle's closing price **crosses below** the low close line.

---

### **Important Usage Guidelines**

For optimal performance, please follow these specific recommendations:

* **Timeframe:** This indicator is designed and optimized to be used exclusively on the **15-minute timeframe**. Using it on other timeframes may produce inconsistent or unreliable results.

* **Primary Asset:** The logic for this indicator was developed and backtested primarily for **Gold (XAUUSD)**. Its performance and win rate have been observed to be the most consistent on this asset.

* **Asset Restriction:** It is strongly recommended to **avoid using this indicator on other currency pairs or assets**, as it has not been optimized for their specific market behavior.

---

### **Disclaimer**

*This indicator is provided for informational and educational purposes only. It is not financial advice. Past performance is not a guarantee of future results. All trading decisions should be based on your own research and risk analysis. Always use proper risk management.*

Cari dalam skrip untuk "GOLD"

CHN BUY SELL with EMA 200Overview

This indicator combines RSI 7 momentum signals with EMA 200 trend filtering to generate high-probability BUY and SELL entry points. It uses colored candles to highlight key market conditions and displays clear trading signals with built-in cooldown periods to prevent signal spam.

Key Features

Colored Candles: Visual momentum indicators based on RSI 7 levels

Trend Filtering: EMA 200 confirms overall market direction

Signal Cooldown: Prevents over-trading with adjustable waiting periods

Clean Interface: Simple BUY/SELL labels without clutter

How It Works

Candle Coloring System

Yellow Candles: Appear when RSI 7 ≥ 70 (overbought momentum)

Purple Candles: Appear when RSI 7 ≤ 30 (oversold momentum)

Normal Candles: All other market conditions

Trading Signals

BUY Signal: Triggered when closing price > EMA 200 AND yellow candle appears

SELL Signal: Triggered when closing price < EMA 200 AND purple candle appears

Signal Cooldown

After a BUY or SELL signal appears, the same signal type is suppressed for a specified number of candles (default: 5) to prevent excessive signals in ranging markets.

Settings

RSI 7 Length: Period for RSI calculation (default: 7)

RSI 7 Overbought: Threshold for yellow candles (default: 70)

RSI 7 Oversold: Threshold for purple candles (default: 30)

EMA Length: Period for trend filter (default: 200)

Signal Cooldown: Candles to wait between same signal type (default: 5)

How to Use

Apply the indicator to your chart

Look for yellow or purple colored candles

For LONG entries: Wait for yellow candle above EMA 200, then enter BUY when signal appears

For SHORT entries: Wait for purple candle below EMA 200, then enter SELL when signal appears

Use appropriate risk management and position sizing

Best Practices

Works best on timeframes M15 and higher

Suitable for Forex, Gold, Crypto, and Stock markets

Consider market volatility when setting stop-loss and take-profit levels

Use in conjunction with proper risk management strategies

Technical Details

Overlay: True (plots directly on price chart)

Calculation: Based on RSI momentum and EMA trend analysis

Signal Logic: Combines momentum exhaustion with trend direction

Visual Feedback: Colored candles provide immediate market condition awareness

Asia Session Reversal Strategy GOLD (Full Version)📈 Asia Session Reversal Strategy (Gold/XAUUSD)

This indicator identifies high-probability reversal trades during the second hour of the Asia session (01:00–02:00 UTC) based on 30-minute candle bias. It:

Detects initial directional push and signals reversal trades on the 1-minute chart

Plots entry, stop-loss, and take-profit levels using a 3:1 reward-to-risk ratio

Includes real-time PnL tracking, daily auto-reset, and alert notifications for BUY/SELL setups

Ideal for scalpers and intraday traders focusing on Gold during consistent, high-liquidity session windows.

ATR Volatility giua64ATR Volatility giua64 – Smart Signal + VIX Filter

📘 Script Explanation (in English)

Title: ATR Volatility giua64 – Smart Signal + VIX Filter

This script analyzes market volatility using the Average True Range (ATR) and compares it to its moving average to determine whether volatility is HIGH, MEDIUM, or LOW.

It includes:

✅ Custom or preset configurations for different asset classes (Forex, Indices, Gold, etc.).

✅ An optional external volatility index input (like the VIX) to refine directional bias.

✅ A directional signal (LONG, SHORT, FLAT) based on ATR strength, direction, and external volatility conditions.

✅ A clean visual table showing key values such as ATR, ATR average, ATR %, VIX level, current range, extended range, and final signal.

This tool is ideal for traders looking to:

Monitor the intensity of price movements

Filter trading strategies based on volatility conditions

Identify momentum acceleration or exhaustion

⚙️ Settings Guide

Here’s a breakdown of the user inputs:

🔹 ATR Settings

Setting Description

ATR Length Number of periods for ATR calculation (default: 14)

ATR Smoothing Type of moving average used (RMA, SMA, EMA, WMA)

ATR Average Length Period for the ATR moving average baseline

🔹 Asset Class Preset

Choose between:

Manual – Define your own point multiplier and thresholds

Forex (Pips) – Auto-set for FX markets (high precision)

Indices (0.1 Points) – For index instruments like DAX or S&P

Gold (USD) – Preset suitable for XAU/USD

If Manual is selected, configure:

Setting Description

Points Multiplier Multiplies raw price ranges into useful units (e.g., 10 for Gold)

Low Volatility Threshold Threshold to define "LOW" volatility

High Volatility Threshold Threshold to define "HIGH" volatility

🔹 Extended Range and VIX

Setting Description

Timeframe for Extended High/Low Used to compare larger price ranges (e.g., Daily or Weekly)

External Volatility Index (VIX) Symbol for a volatility index like "VIX" or "EUVI"

Low VIX Threshold Below this level, VIX is considered "low" (default: 20)

High VIX Threshold Above this level, VIX is considered "high" (default: 30)

🔹 Table Display

Setting Description

Table Position Where the visual table appears on the chart (e.g., bottom_center, top_left)

Show ATR Line on Chart Whether to display the ATR line directly on the chart

✅ Signal Logic Summary

The script determines the final signal based on:

ATR being above or below its average

ATR rising or falling

ATR percentage being significant (>2%)

VIX being high or low

Conditions Signal

ATR rising + high volatility + low VIX LONG

ATR falling + high volatility + high VIX SHORT

ATR flat or low volatility or low %ATR FLAT

5m Gold Strategy - Session Break + Previous Day High/LowHere is your complete Pine Script v5 code for TradingView that:

Implements your 5-minute Gold breakout strategy.

Uses previous day high/low levels.

Confirms entry based on 15-minute SMA trend (SMA 9 > SMA 21).

Marks session time.

Filters news time (pause trading 15 minutes before/after major red news from ForexFactory).

LAOS Gold Price in LAK By LSENMany people in Laos are confused about the actual price of Gold in local currency.

This script provides a simple and live updating way to convert the international gold price (XAU/USD) into Lao Kip Currency in BAHT-weight gold (15.244g).

By default, it uses an exchnage rte of 21,000 KIP = 1 USD, But you can easily customize the rate to fit your needs.

-See things as they truly are. Suffering arises when you try to resist reality. Don't let greed and FOMO fuel the fire.

ຂໍໃຫ້ທຸກທ່ານໂຊກດີ

Bullish and Bearish Breakout Alert for Gold Futures PullbackBelow is a Pine Script (version 6) for TradingView that includes both bullish and bearish breakout conditions for my intraday trading strategy on micro gold futures (MGC). The strategy focuses on scalping two-legged pullbacks to the 20 EMA or key levels with breakout confirmation, tailored for the Apex Trader Funding $300K challenge. The script accounts for the Daily Sentiment Index (DSI) at 87 (overbought, favoring pullbacks). It generates alerts for placing stop-limit orders for 175 MGC contracts, ensuring compliance with Apex’s rules ($7,500 trailing threshold, $20,000 profit target, 4:59 PM ET close).

Script Requirements

Version: Pine Script v6 (latest for TradingView, April 2025).

Purpose:

Bullish: Alert when price breaks above a rejection candle’s high after a two-legged pullback to the 20 EMA in a bullish trend (price above 20 EMA, VWAP, higher highs/lows).

Bearish: Alert when price breaks below a rejection candle’s low after a two-legged pullback to the 20 EMA in a bearish trend (price below 20 EMA, VWAP, lower highs/lows).

Context: 5-minute MGC chart, U.S. session (8:30 AM–12:00 PM ET), avoiding overbought breakouts above $3,450 (DSI 87).

Output: Alerts for stop-limit orders (e.g., “Buy: Stop=$3,377, Limit=$3,377.10” or “Sell: Stop=$3,447, Limit=$3,446.90”), quantity 175 MGC.

Apex Compliance: 175-contract limit, stop-losses, one-directional news trading, close by 4:59 PM ET.

How to Use the Script in TradingView

1. Add Script:

Open TradingView (tradingview.com).

Go to “Pine Editor” (bottom panel).

Copy the script from the content.

Click “Add to Chart” to apply to your MGC 5-minute chart .

2. Configure Chart:

Symbol: MGC (Micro Gold Futures, CME, via Tradovate/Apex data feed).

Timeframe: 5-minute (entries), 15-minute (trend confirmation, manually check).

Indicators: Script plots 20 EMA and VWAP; add RSI (14) and volume manually if needed .

3. Set Alerts:

Click the “Alert” icon (bell).

Add two alerts:

Bullish Breakout: Condition = “Bullish Breakout Alert for Gold Futures Pullback,” trigger = “Once Per Bar Close.”

Bearish Breakout: Condition = “Bearish Breakout Alert for Gold Futures Pullback,” trigger = “Once Per Bar Close.”

Customize messages (default provided) and set notifications (e.g., TradingView app, SMS).

Example: Bullish alert at $3,377 prompts “Stop=$3,377, Limit=$3,377.10, Quantity=175 MGC” .

4. Execute Orders:

Bullish:

Alert triggers (e.g., stop $3,377, limit $3,377.10).

In TradingView’s “Order Panel,” select “Stop-Limit,” set:

Stop Price: $3,377.

Limit Price: $3,377.10.

Quantity: 175 MGC.

Direction: Buy.

Confirm via Tradovate.

Add bracket order (OCO):

Stop-loss: Sell 175 at $3,376.20 (8 ticks, $1,400 risk).

Take-profit: Sell 87 at $3,378 (1:1), 88 at $3,379 (2:1) .

Bearish:

Alert triggers (e.g., stop $3,447, limit $3,446.90).

Select “Stop-Limit,” set:

Stop Price: $3,447.

Limit Price: $3,446.90.

Quantity: 175 MGC.

Direction: Sell.

Confirm via Tradovate.

Add bracket order:

Stop-loss: Buy 175 at $3,447.80 (8 ticks, $1,400 risk).

Take-profit: Buy 87 at $3,446 (1:1), 88 at $3,445 (2:1) .

5. Monitor:

Green triangles (bullish) or red triangles (bearish) confirm signals.

Avoid bullish entries above $3,450 (DSI 87, overbought) or bearish entries below $3,296 (support) .

Close trades by 4:59 PM ET (set 4:50 PM alert) .

Custom Gold Pivot LevelsThis indicator plots custom resistance and support levels based on a central Ziro Pivot Level. The levels are adjusted dynamically based on whether you're preparing for a Buy or Sell trade. The script allows you to set percentage-based levels for both resistance and support, making it a versatile tool for traders.

Features:

Pivot Level: Set the central pivot level (Ziro Pivot) around which resistance and support levels are calculated.

Dynamic Resistance & Support Levels: Input your preferred percentages for Resistance 1, Resistance 2, Support 1 , and Support 2 .

For Buy: Resistance levels are higher, and support levels are lower.

For Sell: Resistance levels are adjusted lower, and support levels are adjusted higher.

Label Display: The indicator will display a Buy label in green above the pivot level or a Sell label in red below the pivot level, depending on the trade type you select.

Adjustable Parameters:

Ziro Pivot Level: Set the central pivot level.

Resistance & Support Levels: Adjust resistance and support levels using percentages.

Trade Type: Choose between "Buy" and "Sell" to dynamically adjust resistance and support levels.

Inputs:

1- Trade Type: Select between Buy or Sell to set the relevant resistance and support levels.

Ziro Pivot Level: Set the main pivot level around which all other levels are calculated.

Resistance Level 1 & 2: Input percentages for Resistance 1 and Resistance 2.

Support Level 1 & 2: Input percentages for Support 1 and Support 2.

How to Use:

1- Select "Buy" or "Sell" from the input options.

For Buy: The indicator will plot higher resistance levels and lower support levels.

For Sell: The indicator will plot lower resistance levels and higher support levels.

2- Adjust the Pivot Level: Set the central pivot level for the levels to be calculated around.

3- Adjust the Resistance & Support Percentages: Modify the resistance and support levels to fit your trading strategy.

4- Visual Feedback: The indicator will show a Buy label in green above the pivot level or a Sell label in red below the pivot level, making it easy to identify the trade direction at a glance.

Use Cases:

Gold & Commodity Trading: This tool is particularly useful for traders working with commodities like gold, where pivot levels can help determine potential price action points.

Swing & Day Trading: The dynamic nature of this indicator makes it great for both swing and day traders who want to monitor short-term market movements.

Support and Resistance Strategy: Traders who rely on support and resistance levels to make buy/sell decisions can use this indicator to automate and visualize these levels more effectively.

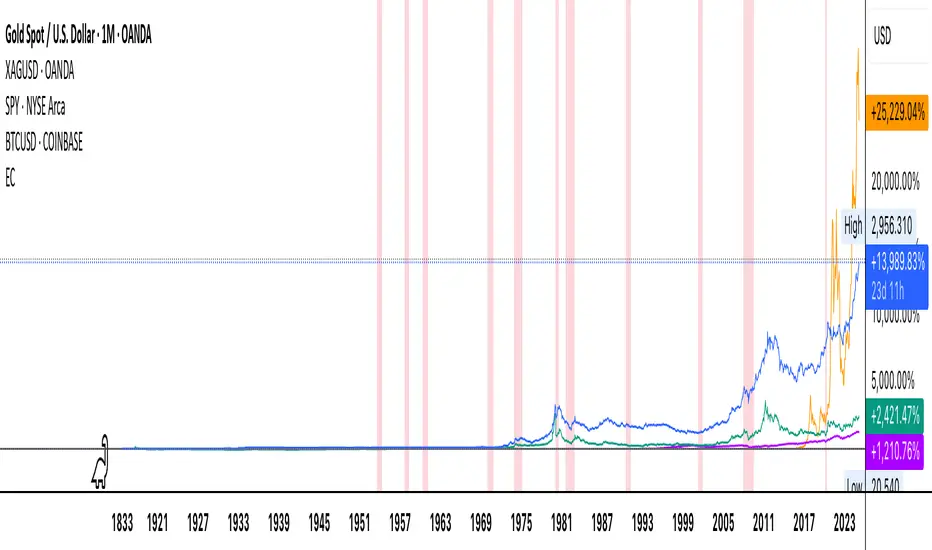

Economic Crises by @zeusbottradingEconomic Crises Indicator by @zeusbottrading

Description and Use Case

Overview

The Economic Crises Highlight Indicator is designed to visually mark major economic crises on a TradingView chart by shading these periods in red. It provides a historical context for financial analysis by indicating when major recessions occurred, helping traders and analysts assess the performance of assets before, during, and after these crises.

What This Indicator Shows

This indicator highlights the following major economic crises (from 1953 to 2020), which significantly impacted global markets:

• 1953 Korean War Recession

• 1957 Monetary Tightening Recession

• 1960 Investment Decline Recession

• 1969 Employment Crisis

• 1973 Oil Crisis

• 1980 Inflation Crisis

• 1981 Fed Monetary Policy Recession

• 1990 Oil Crisis and Gulf War Recession

• 2001 Dot-Com Bubble Crash

• 2008 Global Financial Crisis (Great Recession)

• 2020 COVID-19 Recession

Each of these periods is shaded in red with 80% transparency, allowing you to clearly see the impact of economic downturns on various financial assets.

How This Indicator is Useful

This indicator is particularly valuable for:

✅ Comparative Performance Analysis – It allows traders and investors to compare how different assets (e.g., Gold, Silver, S&P 500, Bitcoin) performed before, during, and after major economic crises.

✅ Identifying Market Trends – Helps recognize recurring patterns in asset price movements during times of financial distress.

✅ Risk Management & Strategy Development – Understanding how markets reacted in the past can assist in making better-informed investment decisions for future downturns.

✅ Gold, Silver & Bitcoin as Safe Havens – Comparing precious metals and cryptocurrencies against traditional stocks (e.g., SPY) to analyze their performance as hedges during economic turmoil.

How to Use It in Your Analysis

By overlaying this indicator on your Gold, Silver, SPY, and Bitcoin chart (for example), you can quickly spot historical market reactions and use that insight to predict possible behaviors in future downturns.

⸻

How to Apply This in TradingView?

1. Click on Use on chart under the image.

2. Overlay it with Gold ( OANDA:XAUUSD ), Silver ( OANDA:XAGUSD ), SPY ( AMEX:SPY ), and Bitcoin ( COINBASE:BTCUSD ) for comparative analysis.

⸻

Conclusion

This indicator serves as a powerful historical reference for traders analyzing asset performance during economic downturns. By studying past crises, you can develop a data-driven investment strategy and improve your market insights. 🚀📈

Let me know if you need any modifications or enhancements!

MACD Volume Strategy for XAUUSD (15m) [PineIndicators]The MACD Volume Strategy is a momentum-based trading system designed for XAUUSD on the 15-minute timeframe. It integrates two key market indicators: the Moving Average Convergence Divergence (MACD) and a volume-based oscillator to identify strong trend shifts and confirm trade opportunities. This strategy uses dynamic position sizing, incorporates leverage customization, and applies structured entry and exit conditions to improve risk management.

⚙️ Core Strategy Components

1️⃣ Volume-Based Momentum Calculation

The strategy includes a custom volume oscillator to filter trade signals based on market activity. The oscillator is derived from the difference between short-term and long-term volume trends using Exponential Moving Averages (EMAs)

Short EMA (default = 5) represents recent volume activity.

Long EMA (default = 8) captures broader volume trends.

Positive values indicate rising volume, supporting momentum-based trades.

Negative values suggest weak market activity, reducing signal reliability.

By requiring positive oscillator values, the strategy ensures momentum confirmation before entering trades.

2️⃣ MACD Trend Confirmation

The strategy uses the MACD indicator as a trend filter. The MACD is calculated as:

Fast EMA (16-period) detects short-term price trends.

Slow EMA (26-period) smooths out price fluctuations to define the overall trend.

Signal Line (9-period EMA) helps identify crossovers, signaling potential trend shifts.

Histogram (MACD – Signal) visualizes trend strength.

The system generates trade signals based on MACD crossovers around the zero line, confirming bullish or bearish trend shifts.

📌 Trade Logic & Conditions

🔹 Long Entry Conditions

A buy signal is triggered when all the following conditions are met:

✅ MACD crosses above 0, signaling bullish momentum.

✅ Volume oscillator is positive, confirming increased trading activity.

✅ Current volume is at least 50% of the previous candle’s volume, ensuring market participation.

🔻 Short Entry Conditions

A sell signal is generated when:

✅ MACD crosses below 0, indicating bearish momentum.

✅ Volume oscillator is positive, ensuring market activity is sufficient.

✅ Current volume is less than 50% of the previous candle’s volume, showing decreasing participation.

This multi-factor approach filters out weak or false signals, ensuring that trades align with both momentum and volume dynamics.

📏 Position Sizing & Leverage

Dynamic Position Calculation:

Qty = strategy.equity × leverage / close price

Leverage: Customizable (default = 1x), allowing traders to adjust risk exposure.

Adaptive Sizing: The strategy scales position sizes based on account equity and market price.

Slippage & Commission: Built-in slippage (2 points) and commission (0.01%) settings provide realistic backtesting results.

This ensures efficient capital allocation, preventing overexposure in volatile conditions.

🎯 Trade Management & Exits

Take Profit & Stop Loss Mechanism

Each position includes predefined profit and loss targets:

Take Profit: +10% of risk amount.

Stop Loss: Fixed at 10,100 points.

The risk-reward ratio remains balanced, aiming for controlled drawdowns while maximizing trade potential.

Visual Trade Tracking

To improve trade analysis, the strategy includes:

📌 Trade Markers:

"Buy" label when a long position opens.

"Close" label when a position exits.

📌 Trade History Boxes:

Green for profitable trades.

Red for losing trades.

📌 Horizontal Trade Lines:

Shows entry and exit prices.

Helps identify trend movements over multiple trades.

This structured visualization allows traders to analyze past performance directly on the chart.

⚡ How to Use This Strategy

1️⃣ Apply the script to a XAUUSD (Gold) 15m chart in TradingView.

2️⃣ Adjust leverage settings as needed.

3️⃣ Enable backtesting to assess past performance.

4️⃣ Monitor volume and MACD conditions to understand trade triggers.

5️⃣ Use the visual trade markers to review historical performance.

The MACD Volume Strategy is designed for short-term trading, aiming to capture momentum-driven opportunities while filtering out weak signals using volume confirmation.

TTZConcept GOLD XAUUSD Lot CalculatorThe Gold Lot Size Calculator for XAU/USD on TradingView is a powerful and user-friendly tool designed by TTZ Concept to help traders calculate the optimal lot size for their Gold trades based on their account size, risk tolerance, and the price movement of Gold (XAU/USD). Whether you're a beginner or an experienced trader, this tool simplifies position sizing, ensuring that your trades align with your risk management strategy.

Key Features:

Accurate Lot Size Calculation: Calculates the optimal lot size for XAU/USD trades based on your specified account balance and the percentage of risk per trade.

Flexible Risk Management**: Input your desired risk percentage (e.g., 1%, 2%) to ensure that you are not risking more than you're comfortable with on any single trade.

Customizable Inputs: Enter your account balance, risk percentage, stop loss (in pips), and leverage to get an accurate lot size recommendation.

Real-Time Data The tool uses real-time Gold price data to calculate the position size, ensuring that your risk management is always up to date with market conditions.

-Simple Interface: With easy-to-use sliders and input fields, you can quickly adjust your parameters and get the required lot size in seconds.

No Complicated Calculations Automatically factors in the pip value and contract specifications for XAU/USD, eliminating the need for manual calculations.

How It Works:

1. Input your trading account balance: The tool calculates based on your total equity.

2. Set your risk percentage: Choose how much of your account you want to risk on a single trade.

3. Define your stop loss in pips: Specify the distance of your stop loss from the entry point.

4. Get your recommended lot size: Based on your inputs, the tool will calculate the ideal lot size for your trade.

Why Use This Tool?

Precise Risk Management: Take control of your trading risk by ensuring that each trade is positioned according to your risk tolerance.

Save Time: No need for manual calculations — let the calculator handle the complex math and focus on your strategy.

Adapt to Changing Market Conditions: As the price of Gold (XAU/USD) fluctuates, your lot size adapts to ensure consistent risk management across different market conditions.

Perfect for:

- Gold traders (XAU/USD)

- Beginners seeking to understand position sizing and risk management

- Experienced traders looking to streamline their trading process

- Anyone who trades Gold futures, CFDs, or spot Gold in their trading account

Buy/Sell Signals (MACD + RSI) 1HThis is a Pine Script indicator for TradingView that plots Buy/Sell signals based on the combination of MACD and RSI indicators on a 1-hour chart.

Description of the Code:

Indicator Setup:

The script is set to overlay the Buy/Sell signals directly on the price chart (using overlay=true).

The indicator is named "Buy/Sell Signals (MACD + RSI) 1H".

MACD Settings:

The MACD (Moving Average Convergence Divergence) uses standard settings of:

Fast Length: 12

Slow Length: 26

Signal Line Smoothing: 9

The MACD line and the Signal line are calculated using the ta.macd() function.

RSI Settings:

The RSI (Relative Strength Index) is calculated with a 14-period setting using the ta.rsi() function.

Buy/Sell Conditions:

Buy Signal:

Triggered when the MACD line crosses above the Signal line (Golden Cross).

RSI value is below 50.

Sell Signal:

Triggered when the MACD line crosses below the Signal line (Dead Cross).

RSI value is above 50.

Signal Visualization:

Buy Signals:

Green "BUY" labels are plotted below the price bars where the Buy conditions are met.

Sell Signals:

Red "SELL" labels are plotted above the price bars where the Sell conditions are met.

Chart Timeframe:

While the code itself doesn't enforce a specific timeframe, the name indicates that this indicator is intended to be used on a 1-hour chart.

To use it effectively, apply the script on a 1-hour chart in TradingView.

How It Works:

This indicator combines MACD and RSI to generate Buy/Sell signals:

The MACD identifies potential trend changes or momentum shifts (via crossovers).

The RSI ensures that Buy/Sell signals align with broader momentum (e.g., Buy when RSI < 50 to avoid overbought conditions).

When the defined conditions for Buy or Sell are met, visual signals (labels) are plotted on the chart.

How to Use:

Copy the code into the Pine Script editor in TradingView.

Save and apply the script to your 1-hour chart.

Look for:

"BUY" signals (green): Indicating potential upward trends or buying opportunities.

"SELL" signals (red): Indicating potential downward trends or selling opportunities.

This script is simple and focuses purely on providing actionable Buy/Sell signals based on two powerful indicators, making it ideal for traders who prefer a clean chart without clutter. Let me know if you need further customization!

Fractal levels Gold [AstroHub]This indicator detects key fractal points on a price chart and visually marks them with shapes and levels. It helps traders identify potential reversal zones and dynamic support/resistance levels, enhancing market analysis.

Key Features:

Fractal Detection:

The indicator identifies top and bottom fractals using a 5-bar pattern.

A top fractal forms when the middle bar has a higher high compared to the two bars on either side.

A bottom fractal forms when the middle bar has a lower low compared to the two bars on either side.

Fractal Filtering:

The indicator can filter out "pristine" fractals (uninterrupted fractal patterns) based on custom conditions, making it more selective and reducing false signals.

Fractal Plotting:

are plotted as downward triangles.

are plotted as upward triangles.

Users can choose to display or hide fractal points and their corresponding labels.

Fractal Levels:

The indicator automatically plots fractals' levels on the chart, marking potential resistance and support zones.

Fractal levels change dynamically as new fractals are identified.

Customizable Display Options:

Show or hide fractals and levels with adjustable settings.

Choose whether to apply filtering for pristine fractals.

Display the pivot labels to easily track fractal positions.

How It Works:

The indicator uses a simple approach to recognize top and bottom fractals . When a valid fractal is detected, it highlights it on the chart and plots the corresponding price level.

By default, top fractals are shown above the bars (red color), and bottom fractals are shown below the bars (green color).

Fractal levels represent potential reversal points and can act as dynamic support and resistance zones.

Best Use:

The indicator is particularly useful in identifying reversal points and trend changes, helping traders to spot key price levels.

It can be used across various timeframes and markets, particularly for trend-following or reversal strategies.

Customizable Settings:

Show Pivots: Toggle the display of pivot points.

Show Pivot Labels: Display labels for pivot levels.

Show Fractals: Toggle fractal points on the chart.

Show Fractal Levels: Show or hide the levels corresponding to the detected fractals.

Filter for Pristine Fractals: Enable this option to filter out non-pristine fractals for higher accuracy.

Conclusion:

This indicator provides clear, actionable fractal signals, helping traders easily identify critical levels for entry and exit. With customizable settings and visual cues, it's suitable for both novice and expe

Roman's Ranges(GOLD FUTURES)This indicator provides the user with Gold Future's previous day’s range and how long it took for the price to reach its first extreme for the day. This information is used to predict the most probable daily direction trend and estimate how long you should expect to hold your winning trade. The distance and time are based on the market open candle (6:30 am). It measures from the retracement wick of the candle to the last 5m close of the day’s first extreme low or high point. It also includes that distance in pts.

Previous market data does not guarantee future results, however, you can leverage the knowledge of the previous day’s ranges to set reasonable take profit levels and when your target is not met automatically, you know how long it took on the previous day to reach the day’s first low/high. If you are nearing that amount of time and your trade is not as profitable as expected, it is easier to get out with less profits using this estimated time rather than hoping the market closes in your favor.

Markets go through cycles and it can be difficult to trade them all if you have a fault expectation how how far the price is expected to move. Price tends to deviate slowly from the average ranges slightly day after day, but you can expect an average range to prevail throughout the week +/- 3 points. It can be very easy to be stuck on 5-point take-profit levels that you don’t pay attention to the average range being twice or three times that distance. The same can be said for the opposite scenario with having higher profit expectations than reasonably possible.

This indicator and my statements are not financial advice. This is meant for educational purposes only.

Total Death and Golden Crosses Calculator The Indicator calculates the total number of the death and golden crosses in the total chart which can help the moving average user to compare the number of signals generated by the moving average pair in the given timeframe.

All you need is to plot any two moving average then change the source of the indicator to get the total number of crosses.

If Indicator is not plotting anything then right click on the indicator's scale and click on "Auto(data fits the screen" option.

Keltner Channel Strategy with Golden CrossOnly trade with the trend.

This Keltner Channel-based strategy that will only enter into a trade if the signal of the Keltner Channel agrees with a moving average crossover as defined by the user.

Long Position Entries

2 Conditions must be present

1. There must be a Golden Cross (lower period moving average is above higher period moving average). ex 50 period MA > 200 period MA.

2. Price must cross above the Keltner Channel ATR defined by the user.

Short Position Entries

2 Conditions must be present

1. There must be a Death Cross (lower period moving average is below higher period moving average). ex 50 period MA < 200 period MA.

2. Price must cross below the Keltner Channel ATR defined by the user

Closing Trades:

The strategy closes trades as follows:

1. Price crossing the Keltner Channel's Take Profit ATR (defined by User)

2. Price crossing the Keltner Channel's Stop Loss ATR (defined by User)

Market Relative Candle Ratio ComparatorIntroducing the Market Relative Candle Ratio Comparator, a visually captivating script that eases the way you compare two financial assets, such as cryptocurrencies and market indices. Leveraging a distinctive calculation method based on percentage changes and their averages, this tool presents a crystal-clear view of how your chosen assets perform in relation to each other, both for individual candles and over a range of previous candles.

Tailoring the script to your preferences is a walk in the park, as it allows you to easily adjust input symbols, moving average lengths, and other parameters to match your analytical approach. The visually arresting column chart it creates employs vivid red and green colors to underscore the differences between the two assets on each candle. Simultaneously, the lower-opacity columns depict the accumulated differences over a specified lookback period. This vibrant blend of colors and opacities results in a dynamic visual experience, enabling you to better grasp market trends relative to each other.

The reverse bool input is a handy feature that lets you invert the effect of the input symbol (DXY by default) in the comparison. When you set the reverse input to true, the script multiplies the calculated DXY percentage change by -1, effectively reversing the comparison. This is particularly useful when examining assets with an inverse relationship or when you'd like to analyze the input symbol's impact in the opposite direction.

For instance, if the input symbol represents a market index that generally moves in the opposite direction of the selected cryptocurrency, enabling the reverse input will help you better visualize and understand the relationship between the two assets by inverting the input symbol's effect on the comparison.

In the accompanying chart, you can observe the comparison of Bitcoin's movement relative to the Dollar, Gold, Bonds, and the S&P 500. The indicator reveals that in the last day, Bitcoin outperformed Bonds, Gold, and the Dollar but not the S&P 500!

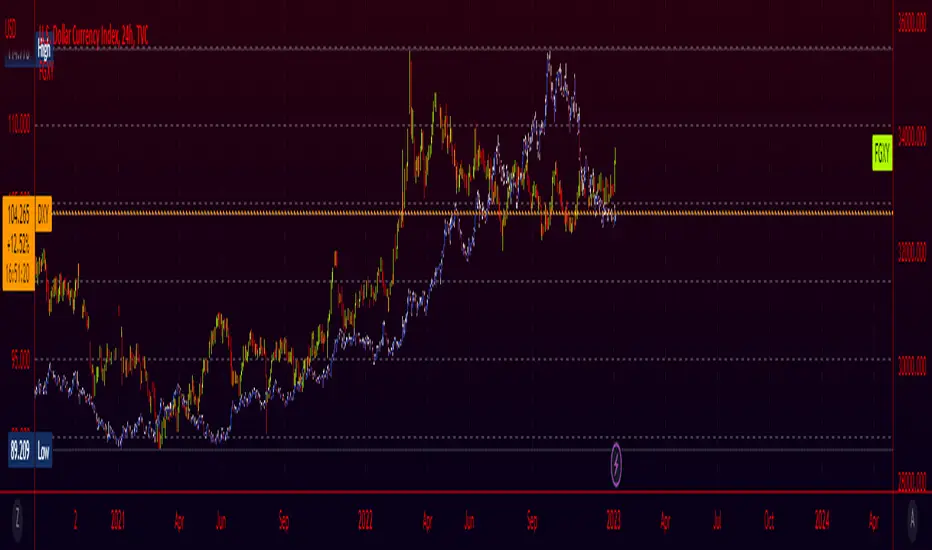

Fiat Currency and Gold Indices (FGXY) CandlesA modification of my previous indicator "Crypto Index (DXY) Candles". The idea was to create a similar currency basket to the standard DXY, but from the perspective of other currencies. Still using the standard DXY weights, this indicator allows you to create a tailored index for other currencies, provided that a currency pair exists for each of the 6 components. This means that even currencies that aren't included should work in theory; just find the 3 character currency prefix used by tradingview and give it a shot! This indicator is useful for gauging how well countries/currencies are holding up and when paired with the standard DXY may help see potential inflection points. For use on longer time frames (~1h-~3d) as some of the data being pulled seems to have issues on lower timeframes.

Money Supply Index (MSI) by zdmreThe primary objective of the states monetary policy is to maintain price stability with sustainable maximum economic growth. In anticipation of higher inflation , the Central Banks raise short-term interest rate thereby to reduce money supply. Conversely, the Central Banks reduce short-term interest rate to inject additional money into the economy in apprehension of unleashing recessionary forces. The stock markets usually respond negatively to interest rate increases and positively to interest rate decreases. The linkages between money market and stock market a wealth effect due to a change in money supply disturbs the equilibrium in the portfolio of investors.

This index indicates the long-run and short-run dynamic effects of broad money supply (M2) on U.S. stock market (this symbol is optional (Bitcoin, Gold or Oil or other markets etc.)).

#DYOR

CHN BUY SELLCHN BUY SELL is formed from two RSI indicators, those are RSI 14 and RSI 7 . I use RSI 14 to determine the trend and RSI 7 to find entry points.

+ Long (BUY) Signal:

- RSI 14 will give a "BUY" signal, then RSI 7 will give entry point to LONG when the candle turns yellow.

+ Short (SELL) Signal:

- RSI 14 will give a "EXIT" signal, then RSI 7 will give entry point to SHORT when the candle turns purple.

+ About Take Profit and Stop Loss:

- With Gold, I usually set Stop Loss and Take Profit at 50 pips

- With currency pairs, I usually keep my Stop Loss and Take Profit at 30 pips

- With crypto, I usually keep Stop Loss and Take Profit at 1.5%

Recommended to use in time frame M15 and above .

This method can be used to trade Forex, Gold and Crypto.

My idea is formed on the view that when the price is moving strongly, the RSI 14 will tell us what the current trend is through a "BUY" or "EXIT" signal. When RSI 14 reaches the oversold area it will form a "BUY" signal and when it reaches the overbought area it will give an "EXIT" signal. I believe that when the price reaches the oversold or overbought area, the price momentum has also decreased and is about to reverse.

After receiving a signal from RSI 14, my job is to wait for an Entry signal from RSI 7. When RSI 7 reaches the overbought area, a yellow candle will appear and that's when we enter a LONG order. When the RSI 7 reaches the oversold area, a purple candle will appear and that's when we enter a SHORT order.

Metals:Backwardation/ContangoMETALS: Gold , Silver , Copper ( GC , SI, HG)

Quickly visualize carrying charge market vs backwardized market by comparing the price of the next 2 years of futures contracts.

Carrying charge (contract prices increasing into the future) = normal, representing the costs of carrying/storage of a commodity. When this is flipped to Backwardation (contract prices decreasing into the future): its a bullish sign: Buyers want this commodity, and they want it NOW.

Note: indicator does not map to time axis in the same way as price; it simply plots the progression of contract months out into the future; left to right; so timeframe DOESN'T MATTER for this plot

There's likely some more efficient way to write this; e.g. when plotting for Gold ( GC ); 21 of the security requests are redundant; but they are still made; and can make this slower to load

TO UPDATE(once a year will do): in REQUEST CONTRACTS section, delete old contracts (top) and add new ones (bottom). Then in PLOTTING section, Delete old contract labels (bottom); add new contract labels (top); adjust the X in 'bar_index-(X+_historical)' numbers accordingly

This is one of three similar indicators: Meats | Metals | Grains

-If you want to build from this; to work on other commodities ; be aware that Tradingview limits the number of contract calls to 40 (hence the 3 seperate indicators)

Tips:

-Right click and reset chart if you can't see the plot; or if you have trouble with the scaling.

-Right click and add to new scale if you prefer this not to overlay directly on price. Or move to new pane below.

--Added historical input: input days back in time; to see the historical shape of the Futures curve via selecting 'days back' snapshot

updated 15th June 2022

© twingall

Macro EMA Correlation

This script is useful to see correlation between macroeconomic assets, displayed in different ema line shown in percentage to compare these assets on the same basis. Percentage will depend on the time frame selection. In the higher timeframe you will see higher variation and in small timeframe smaller variation.

You can select the timeframe who suit your trading style. The 1h and 4h fit well for longer trend swing trade and the lower time frame 15m, 5m, 1m are good for scalping or daily trading.

The following asset are available:

Bitcoin

Ethereum

Gold

Crypto total market cap excluding bitcoin (total2)

United state 10-year government bond (US10Y)

Usdt dominance show the concentration of usdt hold. For example, when trader are fearful they sell their crypto position to keep more usdt in their portfolio (USDT.D)

The USD/JPY pair the dollar usd versus the Japanese Yen one of the most forex traded pair.

You can clic on parameter to select the asset you want to analyse.

The main correlation observed are:

bitcoin negatively correlated with the usdt dominance.

bitcoin negatively correlated with the usd/jpy pair

bitcoin is positively correlated to eth, total2 (altcoin)

bitcoin positively correlated with gold

bitcoin is mostly negatively correlated to us10y

The basis of correlation is that positively correlated asset goes in the same direction and that the negatively correlated goes in opposite direction.

So, the idea is to use these information to see trend reversing.

Example 1: when bitcoin and usdt dominance are extended in opposite direction we look for a possible retracement toward 1% wich is the middle base.

Example 2 : when bitcoin make a move we look for ethereum and total 2 to follow

CRC.i Golden Death CrossThis is a simple reproduction of a common indicator used for analyzing the current momentum trend.

Golden Cross => 50 day simple moving average (sma) crosses over the 200 sma

Death Cross => 50 day simple moving average (sma) crosses under the 200 sma

Forecasting used in this indicator is a simple moving average, considering the price sma with length of (sma period - future bar count).

More articles at

mirror.xyz

medium.com