Multi-Fibonacci Trend Average[FibonacciFlux]Multi-Fibonacci Trend Average (MFTA): An Institutional-Grade Trend Confluence Indicator for Discerning Market Participants

My original indicator/Strategy:

Engineered for the sophisticated demands of institutional and advanced traders, the Multi-Fibonacci Trend Average (MFTA) indicator represents a paradigm shift in technical analysis. This meticulously crafted tool is designed to furnish high-definition trend signals within the complexities of modern financial markets. Anchored in the rigorous principles of Fibonacci ratios and augmented by advanced averaging methodologies, MFTA delivers a granular perspective on trend dynamics. Its integration of Multi-Timeframe (MTF) filters provides unparalleled signal robustness, empowering strategic decision-making with a heightened degree of confidence.

MFTA indicator on BTCUSDT 15min chart with 1min RSI and MACD filters enabled. Note the refined signal generation with reduced noise.

MFTA indicator on BTCUSDT 15min chart without MTF filters. While capturing more potential trading opportunities, it also generates a higher frequency of signals, including potential false positives.

Core Innovation: Proprietary Fibonacci-Enhanced Supertrend Averaging Engine

The MFTA indicator’s core innovation lies in its proprietary implementation of Supertrend analysis, strategically fortified by Fibonacci ratios to construct a truly dynamic volatility envelope. Departing from conventional Supertrend methodologies, MFTA autonomously computes not one, but three distinct Supertrend lines. Each of these lines is uniquely parameterized by a specific Fibonacci factor: 0.618 (Weak), 1.618 (Medium/Golden Ratio), and 2.618 (Strong/Extended Fibonacci).

// Fibonacci-based factors for multiple Supertrend calculations

factor1 = input.float(0.618, 'Factor 1 (Weak/Fibonacci)', minval=0.01, step=0.01, tooltip='Factor 1 (Weak/Fibonacci)', group="Fibonacci Supertrend")

factor2 = input.float(1.618, 'Factor 2 (Medium/Golden Ratio)', minval=0.01, step=0.01, tooltip='Factor 2 (Medium/Golden Ratio)', group="Fibonacci Supertrend")

factor3 = input.float(2.618, 'Factor 3 (Strong/Extended Fib)', minval=0.01, step=0.01, tooltip='Factor 3 (Strong/Extended Fib)', group="Fibonacci Supertrend")

This multi-faceted architecture adeptly captures a spectrum of market volatility sensitivities, ensuring a comprehensive assessment of prevailing conditions. Subsequently, the indicator algorithmically synthesizes these disparate Supertrend lines through arithmetic averaging. To achieve optimal signal fidelity and mitigate inherent market noise, this composite average is further refined utilizing an Exponential Moving Average (EMA).

// Calculate average of the three supertends and a smoothed version

superlength = input.int(21, 'Smoothing Length', tooltip='Smoothing Length for Average Supertrend', group="Fibonacci Supertrend")

average_trend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_trend = ta.ema(average_trend, superlength)

The resultant ‘Smoothed Trend’ line emerges as a remarkably responsive yet stable trend demarcation, offering demonstrably superior clarity and precision compared to singular Supertrend implementations, particularly within the turbulent dynamics of high-volatility markets.

Elevated Signal Confluence: Integrated Multi-Timeframe (MTF) Validation Suite

MFTA transcends the limitations of conventional trend indicators by incorporating an advanced suite of three independent MTF filters: RSI, MACD, and Volume. These filters function as sophisticated validation protocols, rigorously ensuring that only signals exhibiting a confluence of high-probability factors are brought to the forefront.

1. Granular Lower Timeframe RSI Momentum Filter

The Relative Strength Index (RSI) filter, computed from a user-defined lower timeframe, furnishes critical momentum-based signal validation. By meticulously monitoring RSI dynamics on an accelerated timeframe, traders gain the capacity to evaluate underlying momentum strength with precision, prior to committing to signal execution on the primary chart timeframe.

// --- Lower Timeframe RSI Filter ---

ltf_rsi_filter_enable = input.bool(false, title="Enable RSI Filter", group="MTF Filters", tooltip="Use RSI from lower timeframe as a filter")

ltf_rsi_timeframe = input.timeframe("1", title="RSI Timeframe", group="MTF Filters", tooltip="Timeframe for RSI calculation")

ltf_rsi_length = input.int(14, title="RSI Length", minval=1, group="MTF Filters", tooltip="Length for RSI calculation")

ltf_rsi_threshold = input.int(30, title="RSI Threshold", minval=0, maxval=100, group="MTF Filters", tooltip="RSI value threshold for filtering signals")

2. Convergent Lower Timeframe MACD Trend-Momentum Filter

The Moving Average Convergence Divergence (MACD) filter, also calculated on a lower timeframe basis, introduces a critical layer of trend-momentum convergence confirmation. The bullish signal configuration rigorously mandates that the MACD line be definitively positioned above the Signal line on the designated lower timeframe. This stringent condition ensures a robust indication of converging momentum that aligns synergistically with the prevailing trend identified on the primary timeframe.

// --- Lower Timeframe MACD Filter ---

ltf_macd_filter_enable = input.bool(false, title="Enable MACD Filter", group="MTF Filters", tooltip="Use MACD from lower timeframe as a filter")

ltf_macd_timeframe = input.timeframe("1", title="MACD Timeframe", group="MTF Filters", tooltip="Timeframe for MACD calculation")

ltf_macd_fast_length = input.int(12, title="MACD Fast Length", minval=1, group="MTF Filters", tooltip="Fast EMA length for MACD")

ltf_macd_slow_length = input.int(26, title="MACD Slow Length", minval=1, group="MTF Filters", tooltip="Slow EMA length for MACD")

ltf_macd_signal_length = input.int(9, title="MACD Signal Length", minval=1, group="MTF Filters", tooltip="Signal SMA length for MACD")

3. Definitive Volume Confirmation Filter

The Volume Filter functions as an indispensable arbiter of trade conviction. By establishing a dynamic volume threshold, defined as a percentage relative to the average volume over a user-specified lookback period, traders can effectively ensure that all generated signals are rigorously validated by demonstrably increased trading activity. This pivotal validation step signifies robust market participation, substantially diminishing the potential for spurious or false breakout signals.

// --- Volume Filter ---

volume_filter_enable = input.bool(false, title="Enable Volume Filter", group="MTF Filters", tooltip="Use volume level as a filter")

volume_threshold_percent = input.int(title="Volume Threshold (%)", defval=150, minval=100, group="MTF Filters", tooltip="Minimum volume percentage compared to average volume to allow signal (100% = average)")

These meticulously engineered filters operate in synergistic confluence, requiring all enabled filters to definitively satisfy their pre-defined conditions before a Buy or Sell signal is generated. This stringent multi-layered validation process drastically minimizes the incidence of false positive signals, thereby significantly enhancing entry precision and overall signal reliability.

Intuitive Visual Architecture & Actionable Intelligence

MFTA provides a demonstrably intuitive and visually rich charting environment, meticulously delineating trend direction and momentum through precisely color-coded plots:

Average Supertrend: Thin line, green/red for uptrend/downtrend, immediate directional bias.

Smoothed Supertrend: Bold line, teal/purple for uptrend/downtrend, cleaner, institutionally robust trend.

Dynamic Trend Fill: Green/red fill between Supertrends quantifies trend strength and momentum.

Adaptive Background Coloring: Light green/red background mirrors Smoothed Supertrend direction, holistic trend perspective.

Precision Buy/Sell Signals: ‘BUY’/‘SELL’ labels appear on chart when trend touch and MTF filter confluence are satisfied, facilitating high-conviction trade action.

MFTA indicator applied to BTCUSDT 4-hour chart, showcasing its effectiveness on higher timeframes. The Smoothed Length parameter is increased to 200 for enhanced smoothness on this timeframe, coupled with 1min RSI and Volume filters for signal refinement. This illustrates the indicator's adaptability across different timeframes and market conditions.

Strategic Applications for Institutional Mandates

MFTA’s sophisticated design provides distinct advantages for advanced trading operations and institutional investment mandates. Key strategic applications include:

High-Probability Trend Identification: Fibonacci-averaged Supertrend with MTF filters robustly identifies high-probability trend continuations and reversals, enhancing alpha generation.

Precision Entry/Exit Signals: Volume and momentum-filtered signals enable institutional-grade precision for optimized risk-adjusted returns.

Algorithmic Trading Integration: Clear signal logic facilitates seamless integration into automated trading systems for scalable strategy deployment.

Multi-Asset/Timeframe Versatility: Adaptable parameters ensure applicability across diverse asset classes and timeframes, catering to varied trading mandates.

Enhanced Risk Management: Superior signal fidelity from MTF filters inherently reduces false signals, supporting robust risk management protocols.

Granular Customization and Parameterized Control

MFTA offers unparalleled customization, empowering users to fine-tune parameters for precise alignment with specific trading styles and market conditions. Key adjustable parameters include:

Fibonacci Factors: Adjust Supertrend sensitivity to volatility regimes.

ATR Length: Control volatility responsiveness in Supertrend calculations.

Smoothing Length: Refine Smoothed Trend line responsiveness and noise reduction.

MTF Filter Parameters: Independently configure timeframes, lookback periods, and thresholds for RSI, MACD, and Volume filters for optimal signal filtering.

Disclaimer

MFTA is meticulously engineered for high-quality trend signals; however, no indicator guarantees profit. Market conditions are unpredictable, and trading involves substantial risk. Rigorous backtesting and forward testing across diverse datasets, alongside a comprehensive understanding of the indicator's logic, are essential before live deployment. Past performance is not indicative of future results. MFTA is for informational and analytical purposes only and is not financial or investment advice.

Cari dalam skrip untuk "GOLD"

Mark Hours/Minutes (Formula + Minutes)This Pine Script code is a TradingView indicator that analyzes the hour and minutes of each candle in a 1-minute timeframe and plots a red triangle above the candle if one of the following conditions is met:

Sum/Difference Condition: The sum or the absolute difference of the hours and minutes is equal to 29, 35, or 71, with a tolerance of +/- 1.

Minutes Condition: The minutes are equal to 00, 29, or 35.

This indicator is based on the Goldbach theory and the "algo path" concept popularized by Hopiplaka, which posits that algorithmic trading paths often initiate from minute values of 00, 29, and 35. Use this indicator according to your trading strategy.

TradZoo - EMA Crossover IndicatorDescription:

This EMA Crossover Trading Strategy is designed to provide precise Buy and Sell signals with confirmation, defined targets, and stop-loss levels, ensuring strong risk management. Additionally, a 30-candle gap rule is implemented to avoid frequent signals and enhance trade accuracy.

📌 Strategy Logic

✅ Exponential Moving Averages (EMAs):

Uses EMA 50 & EMA 200 for trend direction.

Buy signals occur when price action confirms EMA crossovers.

✅ Entry Confirmation:

Buy Signal: Occurs when either the current or previous candle touches the 200 EMA, and the next candle closes above the previous candle’s close.

Sell Signal: Occurs when either the current or previous candle touches the 200 EMA, and the next candle closes below the previous candle’s close.

✅ 30-Candle Gap Rule:

Prevents frequent entries by ensuring at least 30 candles pass before the next trade.

Improves signal quality and prevents excessive trading.

🎯 Target & Stop-Loss Calculation

✅ Buy Position:

Target: 2X the difference between the last candle’s close and the lowest low of the last 2 candles.

Stop Loss: The lowest low of the last 2 candles.

✅ Sell Position:

Target: 2X the difference between the last candle’s close and the highest high of the last 2 candles.

Stop Loss: The highest high of the last 2 candles.

📊 Visual Features

✅ Buy & Sell Signals:

Green Upward Arrow → Buy Signal

Red Downward Arrow → Sell Signal

✅ Target Levels:

Green Dotted Line: Buy Target

Red Dotted Line: Sell Target

✅ Stop Loss Levels:

Dark Red Solid Line: Stop Loss for Buy/Sell

💡 How to Use

🔹 Ideal for trend-following traders using EMAs.

🔹 Works best in volatile & trending markets (avoid sideways ranges).

🔹 Can be combined with RSI, MACD, or price action levels for added confluence.

🔹 Recommended timeframes: 1M, 5M, 15m, 1H, 4H, Daily (for best results).

🚀 Try this strategy and enhance your trading decisions with structured risk management!

Triple Differential Moving Average BraidThe Triple Differential Moving Average Braid weaves together three distinct layers of moving averages—short-term, medium-term, and long-term—providing a structured view of market trends across multiple time horizons. It is an integrated construct optimized exclusively for the 1D timeframe. For multi-timeframe analysis and/or trading the lower 1h and 15m charts, it pairs well the Granular Daily Moving Average Ribbon ... adjust the visibility settings accordingly.

Unlike traditional moving average indicators that use a single moving average crossover, this braid-style system incorporates both SMAs and EMAs. The dual-layer approach offers stability and responsiveness, allowing traders to detect trend shifts with greater confidence.

Users can, of course, specify their own color scheme. The indicator consists of three layered moving average pairs. These are named per their default colors:

1. Silver Thread – Tracks immediate price momentum.

2. Royal Guard – Captures market structure and developing trends.

3. Golden Section – Defines major market cycles and overall trend direction.

Each layer is color-coded and dynamically shaded based on whether the faster-moving average is above or below its slower counterpart, providing a visual representation of market strength and trend alignment.

🧵 Silver Thread

The Silver Thread is the fastest-moving layer, comprising the 21D SMA and a 21D EMA. The choice of 21 is intentional, as it corresponds to approximately one full month of trading days in a 5-day-per-week market and is also a Fibonacci number, reinforcing its use in technical analysis.

· The 21D SMA smooths out recent price action, offering a baseline for short-term structure.

· The 21D EMA reacts more quickly to price changes, highlighting shifts in momentum.

· When the SMA is above the EMA, price action remains stable.

· When the SMA falls below the EMA, short-term momentum weakens.

The Silver Thread is a leading indicator within the system, often flipping direction before the medium- and long-term layers follow suit. If the Silver Thread shifts bearish while the Royal Guard remains bullish, this can signal a temporary pullback rather than a full trend reversal.

👑 Royal Guard

The Royal Guard provides a broader perspective on market momentum by using a 50D EMA and a 200D EMA. EMAs prioritize recent price data, making this layer faster-reacting than the Golden Section while still offering a level of stability.

· When the 50D EMA is above the 200D EMA, the market is in a confirmed uptrend.

· When the 50D EMA crosses below the 200D EMA, momentum has shifted bearish.

This layer confirms medium-term trend structure and reacts more quickly to price changes than traditional SMAs, making it especially useful for trend-following traders who need faster confirmation than the Golden Section provides.

If the Silver Thread flips bearish while the Royal Guard remains bullish, traders may be seeing a momentary dip in an otherwise intact uptrend. Conversely, if both the Silver Thread and Royal Guard shift bearish, this suggests a deeper pullback or possible trend reversal.

📜 Golden Section

The Golden Section is the slowest and most stable layer of the system, utilizing a 50D SMA and a 200D SMA—a classic combination used by long-term traders and institutions.

· When the 50D SMA is above the 200D SMA the market is in a strong, sustained uptrend.

· When the 50D SMA falls below the 200D SMA the market is structurally bearish.

Because SMAs give equal weight to past price data, this layer moves slowly and deliberately, ensuring that false breakouts or temporary swings do not distort the bigger picture.

Traders can use the Golden Section to confirm major market trends—when all three layers are bullish, the market is strongly trending upward. If the Golden Section remains bullish while the Royal Guard turns bearish, this may indicate a medium-term correction within a larger uptrend rather than a full reversal.

🎯 Swing Trade Setups

Swing traders can benefit from the multi-layered approach of this indicator by aligning their trades with the overall market structure while capturing short-term momentum shifts.

· Bullish: Look for Silver Thread and Royal Guard alignment before entering. If the Silver Thread flips bullish first, anticipate a momentum shift. If the Royal Guard follows, this confirms a strong medium-term move.

· Bearish: If the Silver Thread turns bearish first, it may signal an upcoming reversal. Waiting for the Royal Guard to follow adds confirmation.

· Confirmation: If the Golden Section remains bullish, a pullback may be an opportunity to enter a trend continuation trade rather than exit prematurely.

🚨 Momentum Shifts

· If the Silver Thread flips bearish but the Royal Guard remains bullish, traders may opt to buy the dip rather than exit their positions.

· If both the Silver Thread and Royal Guard turn bearish, traders should exercise caution, as this suggests a more significant correction.

· When all three layers align in the same direction the market is in a strong trending phase, making swing trades higher probability.

⚠️ Risk Management

· A narrowing of the shaded areas suggests trend exhaustion—consider tightening stop losses.

· When the Golden Section remains bullish, but the other two layers weaken, potential support zones to enter or re-enter positions.

· If all three layers flip bearish, this may indicate a larger trend reversal, prompting an exit from long positions and/or consideration of short setups.

The Triple Differential Moving Average Braid is layered, structured tool for trend analysis, offering insights across multiple timeframes without requiring traders to manually compare different moving averages. It provides a powerful and intuitive way to read the market. Swing traders, trend-followers, and position traders alike can use it to align their trades with dominant market trends, time pullbacks, and anticipate momentum shifts.

By understanding how these three moving average layers interact, traders gain a deeper, more holistic perspective of market structure—one that adapts to both momentum-driven opportunities and longer-term trend positioning.

Highlight Specific Minute BarsThis is a simple way to view Goldbach Time, per the suggestion of @hopiplaka1

Any two minutes may be selected, however Hopi suggests 23 and 35.

Takes as input two user defined minutes and allows user to color each independently. Limits the painting to a user-set number of days back. Also, sets the forward projection to a user-set number of hours.

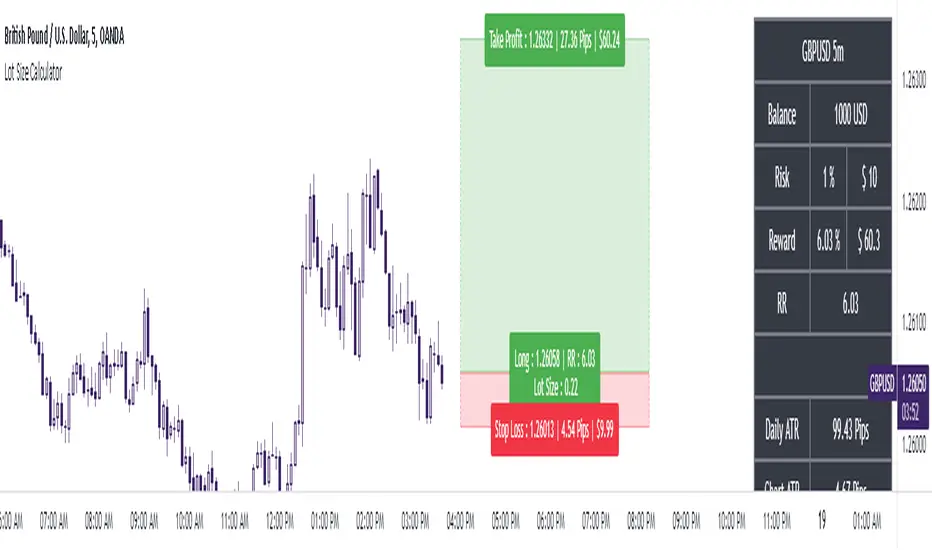

The Ultimate Lot Size Calculator Backstory

I created this Pine Script tool to calculate lot sizes with precision. While there are many lot size calculators available on TradingView, I found that most had significant flaws. I started teaching myself Pine Script over three and a half years ago with the sole purpose of building this tool. My first version was messy and lacked accuracy, so I never published it. I wanted it to be better than any other available tool, but my limited knowledge back then held me back.

Recently, I received a request to create a similar tool, as the current options still fail to deliver the precision and reliability traders need. This inspired me to revisit my original idea. With improved skills and a better understanding of Pine Script, I redesigned the tool from scratch, making it as precise, reliable, and efficient as possible.

This tool features built-in error detection to minimize mistakes and ensure accuracy in lot size calculations. I've spent more time on this project than on any other, focusing on delivering a solution that stands out on TradingView. While I plan to add more features based on user feedback, the current version is already a powerful, dependable, and easy-to-use tool for traders who value precision and efficiency in their lot size calculations.

How to use the tool ?

At first it might seem complicated, but it is quite easy to use the tool. There are two modes: auto and manual. By default, the tool is set on manual mode. When you apply the tool on the chart, it will ask you to choose the entry price, then the stop-loss price, and at last the take-profit price. Select all of them one by one. These values can be changed later.

Settings

There are various setting given for making the tool as flexible as possible. Here is the explanation for some of most important settings. Play with them and make yourself comfortable.

General settings

Auto mode : Use this mode if you want the the risk reward to be fixed and stop loss to be based on ATR. However the stop loss can be changed to be based on user input.

Manual mode : Use this mode if you want full control over entry, stop loss and take profit.

Contract Size : The tool works perfectly for all forex pairs including gold and silver but as the contract size is different for different assets it is difficult to add every single asset into the script manually so i have provided this option. In case you want to calculate lot size for a asset other then forex, gold or silver make sure to change this. Contract size = Quantity of the asset in 1 standerd lot.

Account settings

Automatic mode settings and ATR stop settings

Manual mode settings

Table and risk-reward box settings are pretty much self-explanatory i guess.

Error handling

A lot size calculator is a complex program. There are numerous points where it may fail and produce incorrect results. To make it robust and accurate, these issues must be addressed and managed properly, which practically all existing lot size calculator scripts fail to do.

Golden tip

When the symbol is changed it will display a symbol change warning as the entry, stop loss and take profit price won't change.

There are 2 ways to get fix this. Either manually enter all three values which i hate the most or remove the script from the chart and re-apply the script on chart again.

So to re-apply the indicator in most easy way follow the following instructions:

Note : If you encounter any other error then read the instruction to fix it and if it is an unknow error pleas report it to me in comments or DM.

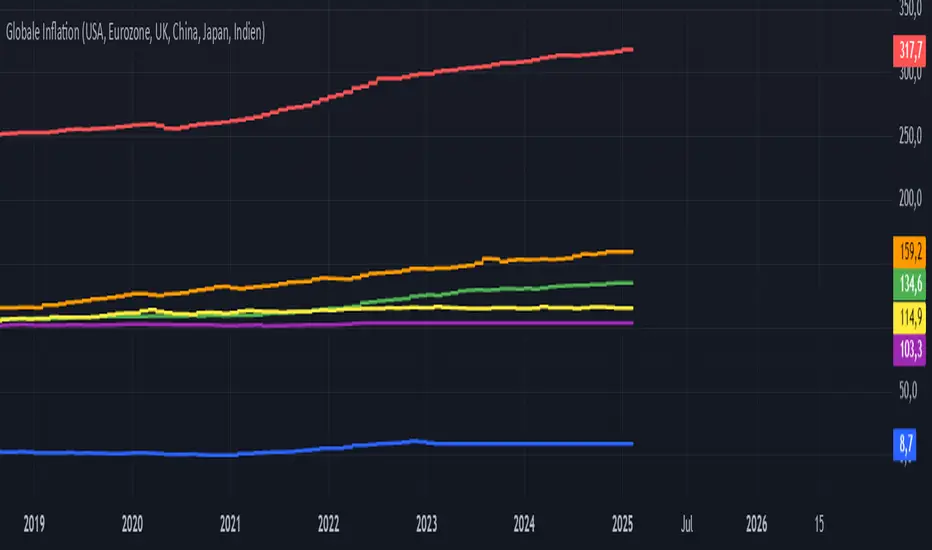

Global Inflation Indicator🔹 Overview:

The Global Inflation Indicator is a macro-analysis tool designed to track and compare inflation trends across major economies. It pulls Consumer Price Index (CPI) data from multiple regions, helping traders and investors analyze how inflation impacts global markets, particularly gold, forex, and commodities.

📊 Key Features:

✅ Tracks inflation in six major economies:

🇺🇸 USA (CPIAUCSL) – Key driver for USD and gold prices

🇪🇺 Eurozone (CPHPTT01EZM659N) – Euro inflation impact

🇬🇧 United Kingdom (GBRCPIALLMINMEI) – GBP & economic trends

🇨🇳 China (CHNCPIALLMINMEI) – Emerging market impact

🇯🇵 Japan (JPNCPIALLMINMEI) – Yen & inflation control policies

🇮🇳 India (INDCPIALLMINMEI) – Key gold-consuming economy

✅ Real-time Inflation Trends:

Provides a visual comparison of inflation levels in different regions.

Helps traders identify inflationary cycles & their effect on global assets.

✅ Macro-Driven Trading Decisions:

Gold & Forex Correlation: High inflation may increase demand for gold.

Interest Rate Expectations: Central banks respond to inflation shifts.

Currency Strength: Inflation impacts USD, EUR, GBP, JPY, CNY, INR.

📉 How to Use It:

Gold traders can assess inflation trends to predict potential price movements.

Forex traders can compare inflation effects on major currency pairs (EUR/USD, USD/JPY, GBP/USD, etc.).

Stock investors can evaluate how inflation affects central bank policies and interest rates.

📌 Conclusion:

The Global Inflation Indicator is a powerful tool for macroeconomic analysis, providing real-time insights into global inflation trends. By integrating this indicator into your gold, forex, and commodity trading strategies, you can make more informed investment decisions in response to economic changes.

Kubricks Super Colliding Indicator v2The Kubricks Super Colliding Indicator v2 is a comprehensive technical analysis tool designed for TradingView. It combines multiple indicators and conditions to help traders identify potential buy/sell signals and trend directions. The script is highly customizable, allowing users to toggle specific features on/off and adjust parameters to suit their trading style.

Key Features

Moving Averages:

Plots SMAs (Simple Moving Averages) and EMAs (Exponential Moving Averages) with customizable periods and colors.

Includes Golden Cross (bullish) and Death Cross (bearish) conditions based on SMA and EMA crossovers.

RSI (Relative Strength Index):

Identifies overbought and oversold conditions using customizable RSI levels.

Displays visual alerts (plotshapes) for overbought/oversold conditions.

MACD (Moving Average Convergence Divergence):

Detects bullish and bearish crossovers of the MACD line and signal line.

Displays visual alerts for MACD crossovers.

Customizable Alerts:

Alerts for Golden Cross, Death Cross, RSI overbought/oversold, MACD crossovers, and close above SMA.

Toggleable Indicators:

Allows users to enable/disable specific features (e.g., RSI, MACD, SMA cross signals) for a cleaner chart.

Visual Enhancements:

Highlights Golden Cross and Death Cross conditions with background colors.

Uses plotshapes to mark key signals (e.g., overbought/oversold, MACD crossovers, close above SMA).

How It Helps Traders

Trend Identification: The combination of SMAs and EMAs helps identify long-term and short-term trends.

Momentum Confirmation: RSI and MACD provide additional confirmation of momentum and potential reversals.

Customizability: Traders can tailor the script to their preferences, focusing on the indicators and conditions most relevant to their strategy.

Visual Alerts: Clear visual cues and alerts make it easier to spot trading opportunities in real-time.

Ideal For

Swing Traders: Identifying trend reversals and momentum shifts.

Position Traders: Confirming long-term trends with Golden/Death Crosses.

Day Traders: Using RSI and MACD for short-term entry/exit signals.

This script is a powerful, all-in-one tool for traders looking to combine multiple technical indicators into a single, easy-to-use interface. Let me know if you need further assistance!

Multi-Band Comparison (Uptrend)Multi-Band Comparison

Overview:

The Multi-Band Comparison indicator is engineered to reveal critical levels of support and resistance in strong uptrends. In a healthy upward market, the price action will adhere closely to the 95th percentile line (the Upper Quantile Band), effectively “riding” it. This indicator combines a modified Bollinger Band (set at one standard deviation), quantile analysis (95% and 5% levels), and power‑law math to display a dynamic picture of market structure—highlighting a “golden channel” and robust support areas.

Key Components & Calculations:

The Golden Channel: Upper Bollinger Band & Upper Std Dev Band of the Upper Quantile

Upper Bollinger Band:

Calculation:

boll_upper=SMA(close,length)+(boll_mult×stdev)

boll_upper=SMA(close,length)+(boll_mult×stdev) Here, the 20-period SMA is used along with one standard deviation of the close, where the multiplier (boll_mult) is 1.0.

Role in an Uptrend:

In a healthy uptrend, price rides near the 95th percentile line. When price crosses above this Upper Bollinger Band, it confirms strong bullish momentum.

Upper Std Dev Band of the Upper Quantile (95th Percentile) Band:

Calculation:

quant_upper_std_up=quant_upper+stdev

quant_upper_std_up=quant_upper+stdev The Upper Quantile Band, quant_upperquant_upper, is calculated as the 95th percentile of recent price data. Adding one standard deviation creates an extension that accounts for normal volatility around this extreme level.

The Golden Channel:

When the price crosses above the Upper Bollinger Band, the Upper Std Dev Band of the Upper Quantile immediately shifts to gold (yellow) and remains gold until price falls below the Bollinger level. Together, these two lines form the “golden channel”—a visual hallmark of a healthy uptrend where the price reliably hugs the 95th percentile level.

Upper Power‑Law Band

Calculation:

The Upper Power‑Law Band is derived in two steps:

Determine the Extreme Return Factor:

power_upper=Percentile(returns,95%)

power_upper=Percentile(returns,95%) where returns are computed as:

returns=closeclose −1.

returns=close close−1.

Scale the Current Price:

power_upper_band=close×(1+power_upper)

power_upper_band=close×(1+power_upper)

Rationale and Correlation:

By focusing on the upper 5% of returns (reflecting “fat tails”), the Upper Power‑Law Band captures extreme but statistically expected movements. In an uptrend, its value often converges with the Upper Std Dev Band of the Upper Quantile because both measures reflect heightened volatility and extreme price levels. When the Upper Power‑Law Band exceeds the Upper Std Dev Band, it can signal a temporary overextension.

Upper Quantile Band (95% Percentile)

Calculation:

quant_upper=Percentile(price,95%)

quant_upper=Percentile(price,95%) This level represents where 95% of past price data falls below, and in a robust uptrend the price action practically rides this line.

Color Logic:

Its color shifts from a neutral (blackish) tone to a vibrant, bullish hue when the Upper Power‑Law Band crosses above it—signaling extra strength in the trend.

Lower Quantile and Its Support

Lower Quantile Band (5% Percentile):

Calculation:

quant_lower=Percentile(price,5%)

quant_lower=Percentile(price,5%)

Behavior:

In a healthy uptrend, price remains well above the Lower Quantile Band. It turns red only when price touches or crosses it, serving as a warning signal. Under normal conditions it remains bright green, indicating the market is not nearing these extreme lows.

Lower Std Dev Band of the Lower Quantile:

This line is calculated by subtracting one standard deviation from quant_lowerquant_lower and typically serves as absolute support in nearly all conditions (except during gap or near-gap moves). Its consistent role as support provides traders with a robust level to monitor.

How to Use the Indicator:

Golden Channel and Trend Confirmation:

As price rides the Upper Quantile (95th percentile) perfectly in a healthy uptrend, the Upper Bollinger Band (1 stdev above SMA) and the Upper Std Dev Band of the Upper Quantile form a “golden channel” once price crosses above the Bollinger level. When this occurs, the Upper Std Dev Band remains gold until price dips back below the Bollinger Band. This visual cue reinforces trend strength.

Power‑Law Insights:

The Upper Power‑Law Band, which is based on extreme (95th percentile) returns, tends to align with the Upper Std Dev Band. This convergence reinforces that extreme, yet statistically expected, price moves are occurring—indicating that even though the price rides the 95th percentile, it can only stretch so far before a correction or consolidation.

Support Indicators:

Primary and Secondary Support in Uptrends:

The Upper Bollinger Band and the Lower Std Dev Band of the Upper Quantile act as support zones for minor retracements in the uptrend.

Absolute Support:

The Lower Std Dev Band of the Lower Quantile serves as an almost invariable support area under most market conditions.

Conclusion:

The Multi-Band Comparison indicator unifies advanced statistical techniques to offer a clear view of uptrend structure. In a healthy bull market, price action rides the 95th percentile line with precision, and when the Upper Bollinger Band is breached, the corresponding Upper Std Dev Band turns gold to form a “golden channel.” This, combined with the Power‑Law analysis that captures extreme moves, and the robust lower support levels, provides traders with powerful, multi-dimensional insights for managing entries, exits, and risk.

Disclaimer:

Trading involves risk. This indicator is for educational purposes only and does not constitute financial advice. Always perform your own analysis before making trading decisions.

Economic RegimeThis indicator, "Economic Regime" , provides a comprehensive analysis of market conditions by combining multiple asset classes and financial metrics. It uses normalized scores and trend analysis to classify the current economic regime into one of four categories: Goldilocks, Reflation, Inflation, or Deflation. The classification is based on inputs like S&P 500 performance, bond yields, commodity prices, volatility indices, and sector ETFs. Additionally, it plots key financial spreads, including the yield spread (10Y-2Y) and credit spread (HYG-LQD), to offer deeper insights into liquidity and market sentiment. The background color dynamically reflects the identified economic regime, facilitating quick visual interpretation.

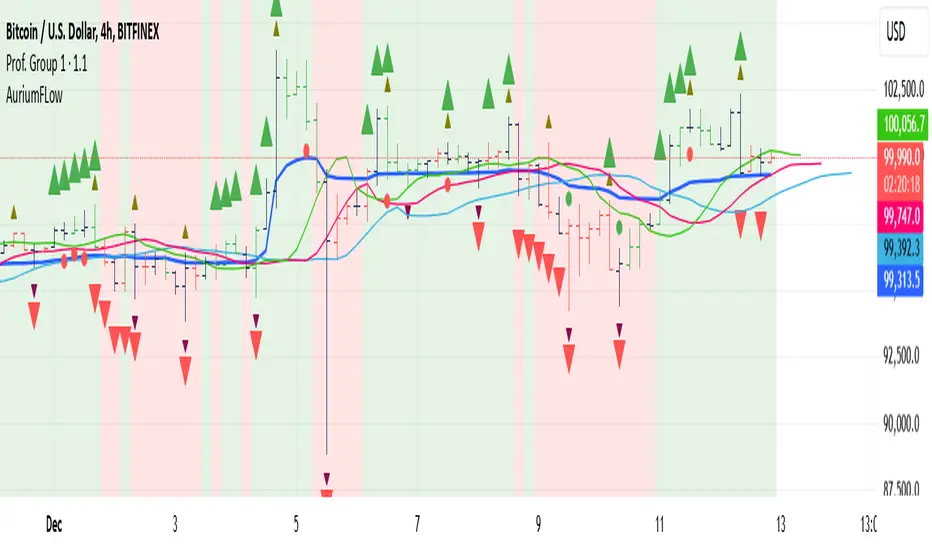

AuriumFlowAURIUM (GOLD-Weighted Average with Fractal Dynamics)

Aurium is a cutting-edge indicator that blends volume-weighted moving averages (VWMA), fractal geometry, and Fibonacci-inspired calculations to deliver a precise and holistic view of market trends. By dynamically adjusting to price and volume, Aurium uncovers key levels of confluence for trend reversals and continuations, making it a powerful tool for traders.

Key Features:

Dynamic Trendline (GOLD):

The central trendline is a weighted moving average based on price and volume, tuned using Fibonacci-based fast (34) and slow (144) exponential moving average lengths. This ensures the trendline adapts seamlessly to the flow of market dynamics.

Formula:

GOLD = VWMA(34) * Volume Factor + VWMA(144) * (1 - Volume Factor)

Fractal Highs and Lows:

Detects pivotal market points using a fractal lookback period (default 5, odd-numbered). Fractals identify local highs and lows over a defined window, capturing the structure of market cycles.

Trend Background Highlighting:

Bullish Zone: Price above the GOLD line with a green background.

Bearish Zone: Price below the GOLD line with a red background.

Buy and Sell Alerts:

Generates actionable signals when fractals align with GOLD. Bullish fractals confirm continuation or reversal in an uptrend, while bearish fractals validate a downtrend.

The Math Behind Aurium:

Volume-Weighted Adjustments:

By integrating volume into the calculation, Aurium dynamically emphasizes price levels with greater participation, giving traders insight into zones of institutional interest.

Formula:

VWMA = EMA(Close * Volume) / EMA(Volume)

Fractal Calculations:

Fractals are identified as local maxima (highs) or minima (lows) based on the surrounding bars, leveraging the natural symmetry in price behavior.

Fibonacci Relationships:

The 34 and 144 EMA lengths are Fibonacci numbers, offering a natural alignment with price cycles and market rhythms.

Ideal For:

Traders seeking a precise and intuitive indicator for aligning with trends and detecting reversals.

Strategies inspired by Bill Williams, with added volume and fractal-based insights.

Short-term scalpers and long-term trend-followers alike.

Unlock deeper market insights and trade with precision using Aurium!

Combined Zero Lag EMA with Crosses | ASHGCombined Zero Lag EMA with Crosses

This indicator combines the power of Zero Lag Exponential Moving Averages (EMAs) with the widely used Golden Cross and Death Cross signals. It provides an efficient and precise trend-following tool for traders.

Key Features:

Short and Long Zero Lag EMAs: The indicator uses two Zero Lag EMAs with customizable periods (Short and Long). The short EMA is typically more responsive to price changes, while the long EMA smooths out price data, providing a broader trend perspective.

Golden Cross and Death Cross signals: The Golden Cross occurs when the short EMA crosses above the long EMA, indicating a potential bullish trend. The Death Cross occurs when the short EMA crosses below the long EMA, signaling a possible bearish trend.

Combined Zero Lag EMA: The average of the Short and Long Zero Lag EMAs gives a balanced view of the market's overall direction.

Plotting and Alerts: The indicator plots both the short and long Zero Lag EMAs, as well as the combined EMA, with visual cues for Golden and Death Crosses. Alerts can be set for when these crosses occur.

Use this indicator for clearer entry and exit points, helping you stay ahead of market movements.

This indicator is based on Kıvanç ÖZBİLGİÇ's "Zero Lag EMA v2" indicator.

tr.tradingview.com

Birleştirilmiş Zero Lag EMA ve Cross (Kesişim) Sinyalleri

Bu gösterge, Zero Lag (Sıfır Gecikmeli) Üssel Hareketli Ortalamaların (EMA) gücünü, yaygın olarak kullanılan Golden Cross (Altın Kesişim) ve Death Cross (Ölüm Kesişimi) sinyalleriyle birleştirir. Yatırımcılar için verimli ve hassas bir trend takip aracıdır.

Öne Çıkan Özellikler:

Kısa ve Uzun Zero Lag EMA: Gösterge, özelleştirilebilir periyotlarla iki Zero Lag EMA kullanır (Kısa ve Uzun). Kısa EMA, fiyat değişimlerine daha hızlı tepki verirken, uzun EMA fiyat verilerini düzleştirerek daha geniş bir trend perspektifi sunar.

Golden Cross ve Death Cross sinyalleri: Golden Cross, kısa EMA'nın uzun EMA'yı yukarı doğru kesmesiyle oluşur ve potansiyel bir yükseliş trendine işaret eder. Death Cross ise, kısa EMA'nın uzun EMA'yı aşağı doğru kesmesiyle oluşur ve düşüş trendi sinyali verir.

Birleştirilmiş Zero Lag EMA: Kısa ve uzun Zero Lag EMA'larının ortalaması, piyasanın genel yönünü dengeli bir şekilde gösterir.

Grafik ve Uyarılar: Gösterge, kısa ve uzun Zero Lag EMA'ları ile birleştirilmiş EMA'yı çizerek Golden Cross ve Death Cross sinyalleri için görsel uyarılar sağlar. Bu kesişimler gerçekleştiğinde alarm kurabilirsiniz.

Bu göstergeleri kullanarak, piyasa hareketlerinden önce net giriş ve çıkış noktaları belirleyebilir, böylece daha bilinçli kararlar alabilirsiniz.

Bu indikatör Kıvanç ÖZBİLGİÇ'in "Zero Lag EMA v2" indikatörünü temel alarak hazırlanmıştır.

tr.tradingview.com

Pulse DPO: Major Cycle Tops and Bottoms█ OVERVIEW

Pulse DPO is an oscillator designed to highlight Major Cycle Tops and Bottoms .

It works on any market driven by cycles. It operates by removing the short-term noise from the price action and focuses on the market's cyclical nature.

This indicator uses a Normalized version of the Detrended Price Oscillator (DPO) on a 0-100 scale, making it easier to identify major tops and bottoms.

Credit: The DPO was first developed by William Blau in 1991.

█ HOW TO READ IT

Pulse DPO oscillates in the range between 0 and 100. A value in the upper section signals an OverBought (OB) condition, while a value in the lower section signals an OverSold (OS) condition.

Generally, the triggering of OB and OS conditions don't necessarily translate into swing tops and bottoms, but rather suggest caution on approaching a market that might be overextended.

Nevertheless, this indicator has been customized to trigger the signal only during remarkable top and bottom events.

I suggest using it on the Daily Time Frame , but you're free to experiment with this indicator on other time frames.

The indicator has Built-in Alerts to signal the crossing of the Thresholds. Please don't act on an isolated signal, but rather integrate it to work in conjunction with the indicators present in your Trading Plan.

█ OB SIGNAL ON: ENTERING OVERBOUGHT CONDITION

When Pulse DPO crosses Above the Top Threshold it Triggers ON the OB signal. At this point the oscillator line shifts to OB color.

When Pulse DPO enters the OB Zone, please beware! In this Area the Major Players usually become Active Sellers to the Public. While the OB signal is On, it might be wise to Consider Selling a portion or the whole Long Position.

Please note that even though this indicator aims to focus on major tops and bottoms, a strong trending market might trigger the OB signal and stay with it for a long time. That's especially true on young markets and on bubble-mode markets.

█ OB SIGNAL OFF: EXITING OVERBOUGHT CONDITION

When Pulse DPO crosses Below the Top Threshold it Triggers OFF the OB signal. At this point the oscillator line shifts to its normal color.

When Pulse DPO exits the OB Zone, please beware because a Major Top might just have occurred. In this Area the Major Players usually become Aggressive Sellers. They might wind up any remaining Long Positions and Open new Short Positions.

This might be a good area to Open Shorts or to Close/Reverse any remaining Long Position. Whatever you choose to do, it's usually best to act quickly because the market is prone to enter into panic mode.

█ OS SIGNAL ON: ENTERING OVERSOLD CONDITION

When Pulse DPO crosses Below the Bottom Threshold it Triggers ON the OS signal. At this point the oscillator line shifts to OS color.

When Pulse DPO enters the OS Zone, please beware because in this Area the Major Players usually become Active Buyers accumulating Long Positions from the desperate Public.

While the OS signal is On, it might be wise to Consider becoming a Buyer or to implement a Dollar-Cost Averaging (DCA) Strategy to build a Long Position towards the next Cycle. In contrast to the tops, the OS state usually takes longer to resolve a major bottom.

█ OS SIGNAL OFF: EXITING OVERSOLD CONDITION

When Pulse DPO crosses Above the Bottom Threshold it Triggers OFF the OS signal. At this point the oscillator line shifts to its normal color.

When Pulse DPO exits the OS Zone, please beware because a Major Bottom might already be in place. In this Area the Major Players become Aggresive Buyers. They might wind up any remaining Short Positions and Open new Long Positions.

This might be a good area to Open Longs or to Close/Reverse any remaining Short Positions.

█ WHY WOULD YOU BE INTERESTED IN THIS INDICATOR?

This indicator is built over a solid foundation capable of signaling Major Cycle Tops and Bottoms across many markets. Let's see some examples:

Early Bitcoin Years: From 0 to 1242

This chart is in logarithmic mode in order to properly display various exponential cycles. Pulse DPO is properly signaling the major early highs from 9-Jun-2011 at 31.50, to the next one on 9-Apr-2013 at 240 and the epic top from 29-Nov-2013 at 1242.

Due to the massive price movements, the OB condition stays pinned during most of the exponential price action. But as you can see, the OB condition quickly vanishes once the Cycle Top has been reached. As the market matures, the OB condition becomes more exceptional and triggers much closer from the Cycle Top.

With regards to Cycle Bottoms, the early bottom of 2 after having peaked at 31.50 doesn’t get captured by the indicator. That is the only cycle bottom that escapes the Pulse DPO when the bottom threshold is set at a value of 5. In that event, the oscillator low reached 6.95.

Bitcoin Adoption Spreading: From 257 to 73k

This chart is in logarithmic mode in order to properly display various exponential cycles. Pulse DPO is properly signaling all the major highs from 17-Dec-2017 at 19k, to the next one on 14-Apr-2021 at 64k and the most recent top from 9-Nov-2021 at 68k.

During the massive run of 2017, the OB condition still stayed triggered for a few weeks on each swing top. But on the next cycles it started to signal only for a few days before each swing top actually happened. The OB condition during the last cycle top triggered only for 3 days. Therefore the signal grows in focus as the market matures.

At the time of publishing this indicator, Bitcoin printed a new All Time High (ATH) on 13-Mar-2024 at 73k. That run didn’t trigger the OB condition. Therefore, if the indicator is correct the Bitcoin market still has some way to grow during the next months.

With regards to Cycle Bottoms, the bottom of 3k after having peaked at19k got captured within the wide OS zone. The bottom of 15k after having peaked at 68k got captured too within the OS accumulation area.

Gold

Pulse DPO behaves surprisingly well on a long standing market such as Gold. Moving back to the 197x years it’s been signaling most Cycle Tops and Bottoms with precision. During the last cycle, it shows topping at 2k and bottoming at 1.6k.

The current price action is signaling OB condition in the range of 2.5k to 2.7k. Looking at past cycles, it tends to trigger on and off at multiple swing tops until reaching the final cycle top. Therefore this might indicate the first wave within a potential gold run.

Oil

On the Oil market, we can see that most of the cycle tops and bottoms since the 80s got signaled. The only exception being the low from 2020 which didn’t trigger.

EURUSD

On Forex markets the Pulse DPO also behaves as expected. Looking back at EURUSD we can see the marketing triggering OB and OS conditions during major cycle tops and bottoms from recent times until the 80s.

S&P 500

On the S&P 500 the Pulse DPO catched the lows from 2016 and 2020. Looking at present price action, the recent ATH didn’t trigger the OB condition. Therefore, the indicator is allowing room for another leg up during the next months.

Amazon

On the Amazon chart the Pulse DPO is mirroring pretty accurately the major swings. Scrolling back to the early 2000s, this chart resembles early exponential swings in the crypto space.

Tesla

Moving onto a younger tech stock, Pulse DPO captures pretty accurately the major tops and bottoms. The chart is shown in logarithmic scale to better display the magnitude of the moves.

█ SETTINGS

This indicator is ideal for identifying major market turning points while filtering out short-term noise. You are free to adjust the parameters to align with your preferred trading style.

Parameters : This section allows you to customize any of the Parameters that shape the Oscillator.

Oscillator Length: Defines the period for calculating the Oscillator.

Offset: Shifts the oscillator calculation by a certain number of periods, which is typically half the Oscillator Length.

Lookback Period: Specifies how many bars to look back to find tops and bottoms for normalization.

Smoothing Length: Determines the length of the moving average used to smooth the oscillator.

Thresholds : This section allows you to customize the Thresholds that trigger the OB and OS conditions.

Top: Defines the value of the Top Threshold.

Bottom: Defines the value of the Bottom Threshold.

Multi-Average Trend Indicator (MATI)[FibonacciFlux]Multi-Average Trend Indicator (MATI)

Overview

The Multi-Average Trend Indicator (MATI) is a versatile technical analysis tool designed for traders who aim to enhance their market insights and streamline their decision-making processes across various timeframes. By integrating multiple advanced moving averages, this indicator serves as a robust framework for identifying market trends, making it suitable for different trading styles—from scalping to swing trading.

MATI 4-hourly support/resistance

MATI 1-hourly support/resistance

MATI 15 minutes support/resistance

MATI 1 minutes support/resistance

Key Features

1. Diverse Moving Averages

- COVWMA (Coefficient of Variation Weighted Moving Average) :

- Provides insights into price volatility, helping traders identify the strength of trends in fast-moving markets, particularly useful for 1-minute scalping .

- DEMA (Double Exponential Moving Average) :

- Minimizes lag and quickly responds to price changes, making it ideal for capturing short-term price movements during volatile trading sessions .

- EMA (Exponential Moving Average) :

- Focuses on recent price action to indicate the prevailing trend, vital for day traders looking to enter positions based on current momentum.

- KAMA (Kaufman's Adaptive Moving Average) :

- Adapts to market volatility, smoothing out price action and reducing false signals, which is crucial for 4-hour day trading strategies.

- SMA (Simple Moving Average) :

- Provides a foundational view of the market trend, useful for swing traders looking at overall price direction over longer periods.

- VIDYA (Variable Index Dynamic Average) :

- Adjusts based on market conditions, offering a dynamic perspective that can help traders capture emerging trends.

2. Combined Moving Average

- The MATI's combined moving average synthesizes all individual moving averages into a single line, providing a clear and concise summary of market direction. This feature is especially useful for identifying trend continuations or reversals across various timeframes .

3. Dynamic Color Coding

- Each moving average is visually represented with color coding:

- Green indicates bullish conditions, while Red suggests bearish trends.

- This visual feedback allows traders to quickly assess market sentiment, facilitating faster decision-making.

4. Signal Generation and Alerts

- The indicator generates buy signals when the combined moving average crosses above its previous value, indicating a potential upward trend—ideal for quick entries in scalping.

- Conversely, sell signals are triggered when the combined moving average crosses below its previous value, useful for exiting positions or entering short trades.

Insights and Applications

1. Scalping on 1-Minute Charts

- The MATI excels in fast-paced environments, allowing scalpers to identify quick entry and exit points based on short-term trends. With dynamic signals and alerts, traders can react swiftly to price movements, maximizing profit potential in brief price fluctuations.

2. Day Trading on 4-Hour Charts

- For day traders, the MATI provides essential insights into intraday trends. By analyzing the combined moving average and its relation to individual moving averages, traders can make informed decisions on when to enter or exit positions, capitalizing on daily price swings.

3. Swing Trading on Daily Charts

- The MATI also serves as a valuable tool for swing traders. By evaluating longer-term trends through the combined moving average, traders can identify potential swing points and adjust their strategies accordingly. The flexibility of adjusting the lengths of the moving averages allows for tailored approaches based on market volatility.

Benefits

1. Clarity and Insight

- The combination of diverse moving averages offers a clear visual representation of market trends, aiding traders in making informed decisions across multiple timeframes.

2. Flexibility and Customization

- With adjustable parameters, traders can adapt the MATI to their specific strategies, making it suitable for various market conditions and trading styles.

3. Real-Time Alerts and Efficiency

- Built-in alerts minimize response times, allowing traders to capitalize on opportunities as they arise, regardless of their trading style.

Conclusion

The Multi-Average Trend Indicator (MATI) is an essential tool for traders seeking to enhance their technical analysis capabilities. By seamlessly integrating multiple moving averages with dynamic color coding and real-time alerts, this indicator provides a comprehensive approach to understanding market trends. Its versatility makes it an invaluable asset for scalpers, day traders, and swing traders alike.

Important Note

As with any trading tool, thorough analysis and risk management are crucial when using this indicator. Past performance does not guarantee future results, and traders should always be prepared for market fluctuations.

Advanced Economic Indicator by USCG_VetAdvanced Economic Indicator by USCG_Vet

tldr:

This comprehensive TradingView indicator combines multiple economic and financial metrics into a single, customizable composite index. By integrating key indicators such as the yield spread, commodity ratios, stock indices, and the Federal Reserve's QE/QT activities, it provides a holistic view of the economic landscape. Users can adjust the components and their weights to tailor the indicator to their analysis, aiding in forecasting economic conditions and market trends.

Detailed Description

Overview

The Advanced Economic Indicator is designed to provide traders and investors with a powerful tool to assess the overall economic environment. By aggregating a diverse set of economic indicators and financial market data into a single composite index, it helps identify potential turning points in the economy and financial markets.

Key Features:

Comprehensive Coverage: Includes 14 critical economic and financial indicators.

Customizable Components: Users can select which indicators to include.

Adjustable Weights: Assign weights to each component based on perceived significance.

Visual Signals: Clear plotting with threshold lines and background highlights.

Alerts: Set up alerts for when the composite index crosses user-defined thresholds.

Included Indicators

Yield Spread (10-Year Treasury Yield minus 3-Month Treasury Yield)

Copper/Gold Ratio

High Yield Spread (HYG/IEF Ratio)

Stock Market Performance (S&P 500 Index - SPX)

Bitcoin Performance (BLX)

Crude Oil Prices (CL1!)

Volatility Index (VIX)

U.S. Dollar Index (DXY)

Inflation Expectations (TIP ETF)

Consumer Confidence (XLY ETF)

Housing Market Index (XHB)

Manufacturing PMI (XLI ETF)

Unemployment Rate (Inverse SPY as Proxy)

Federal Reserve QE/QT Activities (Fed Balance Sheet - WALCL)

How to Use the Indicator

Configuring the Indicator:

Open Settings: Click on the gear icon (⚙️) next to the indicator's name.

Inputs Tab: You'll find a list of all components with checkboxes and weight inputs.

Including/Excluding Components

Checkboxes: Check or uncheck the box next to each component to include or exclude it from the composite index.

Default State: By default, all components are included.

Adjusting Component Weights:

Weight Inputs: Next to each component's checkbox is a weight input field.

Default Weights: Pre-assigned based on economic significance but fully adjustable.

Custom Weights: Enter your desired weight for each component to reflect your analysis.

Threshold Settings:

Bearish Threshold: Default is -1.0. Adjust to set the level below which the indicator signals potential economic downturns.

Bullish Threshold: Default is 1.0. Adjust to set the level above which the indicator signals potential economic upswings.

Setting the Timeframe:

Weekly Timeframe Recommended: Due to the inclusion of the Fed's balance sheet data (updated weekly), it's best to use this indicator on a weekly chart.

Changing Timeframe: Select 1W (weekly) from the timeframe options at the top of the chart.

Interpreting the Indicator:

Composite Index Line

Plot: The blue line represents the composite economic indicator.

Movement: Observe how the line moves relative to the threshold lines.

Threshold Lines

Zero Line (Gray Dotted): Indicates the neutral point.

Bearish Threshold (Red Dashed): Crossing below suggests potential economic weakness.

Bullish Threshold (Green Dashed): Crossing above suggests potential economic strength.

Background Highlights

Red Background: When the composite index is below the bearish threshold.

Green Background: When the composite index is above the bullish threshold.

No Color: When the composite index is between the thresholds.

Understanding the Components

1. Yield Spread

Description: The difference between the 10-year and 3-month U.S. Treasury yields.

Economic Significance: An inverted yield curve (negative spread) has historically preceded recessions.

2. Copper/Gold Ratio

Description: The price ratio of copper to gold.

Economic Significance: Copper is tied to industrial demand; gold is a safe-haven asset. The ratio indicates risk sentiment.

3. High Yield Spread (HYG/IEF Ratio)

Description: Ratio of high-yield corporate bonds (HYG) to intermediate-term Treasury bonds (IEF).

Economic Significance: Reflects investor appetite for risk; widening spreads can signal credit stress.

4. Stock Market Performance (SPX)

Description: S&P 500 Index levels.

Economic Significance: Broad measure of U.S. equity market performance.

5. Bitcoin Performance (BLX)

Description: Bitcoin Liquid Index price.

Economic Significance: Represents risk appetite in speculative assets.

6. Crude Oil Prices (CL1!)

Description: Front-month crude oil futures price.

Economic Significance: Influences inflation and consumer spending.

7. Volatility Index (VIX)

Description: Market's expectation of volatility (fear gauge).

Economic Significance: High VIX indicates market uncertainty; inverted in the indicator to align directionally.

8. U.S. Dollar Index (DXY)

Description: Value of the U.S. dollar relative to a basket of foreign currencies.

Economic Significance: Affects international trade and commodity prices; inverted in the indicator.

9. Inflation Expectations (TIP ETF)

Description: iShares TIPS Bond ETF prices.

Economic Significance: Reflects market expectations of inflation.

10. Consumer Confidence (XLY ETF)

Description: Consumer Discretionary Select Sector SPDR Fund prices.

Economic Significance: Proxy for consumer confidence and spending.

11. Housing Market Index (XHB)

Description: SPDR S&P Homebuilders ETF prices.

Economic Significance: Indicator of the housing market's health.

12. Manufacturing PMI (XLI ETF)

Description: Industrial Select Sector SPDR Fund prices.

Economic Significance: Proxy for manufacturing activity.

13. Unemployment Rate (Inverse SPY as Proxy)

Description: Inverse of the SPY ETF price.

Economic Significance: Represents unemployment trends; higher inverse SPY suggests higher unemployment.

14. Federal Reserve QE/QT Activities (Fed Balance Sheet - WALCL)

Description: Total assets held by the Federal Reserve.

Economic Significance: Indicates liquidity injections (QE) or withdrawals (QT); impacts interest rates and asset prices.

Customization and Advanced Usage

Adjusting Weights:

Purpose: Emphasize components you believe are more predictive or relevant.

Method: Increase or decrease the weight value next to each component.

Example: If you think the yield spread is particularly important, you might assign it a higher weight.

Disclaimer

This indicator is for educational and informational purposes only. It is not financial advice. Trading and investing involve risks, including possible loss of principal. Always conduct your own analysis and consult with a professional financial advisor before making investment decisions.

Fibonacci Cloud MTF [TrendX_]The Fibonacci Cloud MTF Indicator is an innovative trading tool crafted to assist traders in dynamically identifying key Fibonacci retracement levels. Unlike traditional methods that depend on static pivot points, this indicator effectively plots the Fibonacci golden zone - ranging from 0.382 to 0.618 - using the most recent highs and lows. This dynamic approach provides a more nuanced and responsive analysis of price movements, allowing traders to observe real-time reactions to significant Fibonacci levels. Furthermore, the indicator functions as a trend-following mechanism, signaling potential uptrends when the price crosses above the 0.618 fibonacci retracement level and indicating downtrends when it dips below.

💎 KEY FEATURES

Dynamic Fibonacci Levels: The indicator calculates Fibonacci retracement levels based on the latest highs and lows, providing a more relevant framework for current market conditions.

Golden Zone Focus: It emphasizes the Fibonacci golden zone (0.382 - 0.618), which is widely regarded as a critical area for potential reversals or continuations.

Multi-timeframe Analysis: The ability to view Fibonacci levels across multiple timeframes allows traders to identify trends and potential entry points more effectively.

Trend-Following Signals: Clear trend directions relative to the 0.618 level.

⚙️ USAGES

Identifying Key Retracement Levels: Traders can use the plotted Fibonacci levels to determine potential pullback or throwback at the key Fibonacci areas.

Trend Confirmation: By observing price interactions with the 0.618 level, traders can confirm ongoing trends and make more informed decisions about entering or exiting positions.

Multi-timeframe Strategies: The indicator allows traders to align strategies across different timeframes, improving overall trading effectiveness.

🔎 BREAKDOWN

Dynamic Fibonacci Levels: By calculating Fibonacci retracement levels from the latest highs and lows, traders receive a more accurate representation of current market sentiment. This dynamic approach ensures that the levels adapt to changing market conditions, making them more relevant for decision-making.

Golden Zone Focus: This highlights the Fibonacci golden zone, particularly the range between 0.382 and 0.618. This zone is widely regarded as a pivotal area for potential price reversals or continuations, serving as key support and resistance levels. Prices often react strongly at these points, making them crucial for pinpointing potential entry and exit opportunities in your trading strategy.

Multi-timeframe Analysis: Incorporating multi-timeframe analysis allows traders to observe how Fibonacci levels behave across different timeframes. This feature helps traders identify broader trends while also pinpointing short-term opportunities.

Trend-Following Strategies: Uptrend trigger - When the price crosses above the 0.618 level, it triggers uptrend, conversely, when the price crosses below the 0.618 level, it triggers a downtrend.

DISCLAIMER

This indicator is not financial advice, it can only help traders make better decisions. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur. Therefore, one should always exercise caution and judgment when making decisions based on past performance.

RSI-based MACDThe RSI is one of the most popular indicators available. This indicator, which represents the strength of market momentum based on the gains and losses over the past 14 candlesticks, is rational and is mainly used as an oscillator to determine overbought or oversold conditions. However, because the RSI is an older indicator, its very simple design—displaying only a single line on the graph—may feel somewhat lacking in functionality to modern traders. The main issue is that there is no objective measure to determine whether the RSI is currently rising or falling.

That’s when I came up with the idea of calculating the MACD based on the smoothed values of the RSI. As is well known, the MACD is an indicator that represents the distance between moving averages, designed to show when the moving averages cross as the value falls below zero. By observing the golden crosses and death crosses of the MACD and signal line, one can anticipate the golden and death crosses of the moving averages. Applying the same logic, I thought that calculating the MACD based on RSI values would allow us to predict the rise and fall of the RSI by observing these golden and death crosses.

Currently, the RSI is often used as a contrarian indicator to determine overbought and oversold conditions, but with this approach, I believe the RSI can instead function extremely well as a trend-following indicator. Whenever an uptrend occurs, the RSI inevitably rises, and when a downtrend occurs, the RSI inevitably falls. Therefore, by predicting the rise and fall of the RSI, it becomes possible to forecast what kind of trend is likely to develop.

In this indicator, the MACD calculated from the RSI is displayed, with the original RSI line plotted above it. Since the scales of the RSI and MACD are different, I originally wanted to provide a separate scale for the RSI on the left side. However, due to TradingView’s limitations, it seems quite difficult to display more than one scale in a single panel, so I had to give up on that. Instead, I ask that you mentally multiply the RSI values displayed on the right by 10—for example, 2.11 indicates 21.1%.

Additionally, as a bonus, I’ve included a feature that detects divergences. With these features, I believe this has become the most useful indicator when compared to existing RSI-based indicators. I hope you find it helpful in your trading.

Dysmen signalsDysmen Signals Indicator

The "Dysmen Signals" indicator is designed to provide clear buy and sell signals based on the crossover of various Exponential Moving Averages (EMAs). This indicator employs a combination of short-term and long-term EMA crossovers to identify potential trading opportunities, while also highlighting significant market movements through specific signals such as the Golden Cross and Death Cross.

Indicator Components

1. Exponential Moving Averages (EMAs)

- EMA 14: A short-term EMA calculated over 14 periods.

- EMA 20: Another short-term EMA calculated over 20 periods.

- EMA 50: A mid-term EMA used as a trend filter.

- EMA 200: A long-term EMA representing the overall trend.

2. Buy and Sell Signals

- Buy Signal: This is triggered when the EMA 14 crosses above the EMA 20 and the closing price is above the EMA 50. This suggests a bullish trend in the market.

- Sell Signal: This is triggered when the EMA 14 crosses below the EMA 20 and the closing price is below the EMA 50. This indicates a bearish trend in the market.

3. Golden Cross and Death Cross

- Golden Cross (GC): Occurs when the EMA 50 crosses above the EMA 200. This is a strong bullish signal indicating a potential long-term upward trend.

- Death Cross (DC): Occurs when the EMA 50 crosses below the EMA 200. This is a strong bearish signal suggesting a potential long-term downward trend.

4. Signal Visualization

- Buy and Sell signals are marked on the chart with green and red triangles respectively. These signals help traders identify potential entry and exit points.

- Golden Cross and Death Cross signals are indicated with yellow and purple diamonds respectively, providing insight into major market trend shifts.

5. Candle Coloring

- Candles are colored green if a buy signal is active and red if a sell signal is active. This visual aid helps in quickly identifying the prevailing market sentiment.

6. EMA 200 Plotting

- The EMA 200 is plotted as a white, semi-thick line on the chart. This line serves as a reference for the overall long-term trend.

Detailed Code Explanation

- EMA Calculations: The script calculates the EMA for 14, 20, 50, and 200 periods using the ta.ema function.

- Crossover Conditions: It uses the ta.crossover and ta.crossunder functions to detect when the EMAs cross each other, triggering buy and sell signals.

- Plotting Signals: The plotshape function is utilized to display BUY and SELL signals as well as Golden Cross and Death Cross signals on the chart.

- Candle Coloring Logic: A variable direction is used to store the current market direction based on the latest signal, which then determines the candle colors using the barcolor function.

- EMA 200 Display: The plot function is used to draw the EMA 200 line on the chart with the specified color and thickness.

By employing this indicator, traders can gain valuable insights into potential market trends and make more informed trading decisions based on the crossover of key EMAs.

Support and resistance levels (Day, Week, Month) + EMAs + SMAs(ENG): This Pine 5 script provides various tools for configuring and displaying different support and resistance levels, as well as moving averages (EMA and SMA) on charts. Using these tools is an essential strategy for determining entry and exit points in trades.

Support and Resistance Levels

Daily, weekly, and monthly support and resistance levels play a key role in analyzing price movements:

Daily levels: Represent prices where a cryptocurrency has tended to bounce within the current trading day.

Weekly levels: Reflect strong prices that hold throughout the week.

Monthly levels: Indicate the most significant levels that can influence price movement over the month.

When trading cryptocurrencies, traders use these levels to make decisions about entering or exiting positions. For example, if a cryptocurrency approaches a weekly resistance level and fails to break through it, this may signal a sell opportunity. If the price reaches a daily support level and starts to bounce up, it may indicate a potential long position.

Market context and trading volumes are also important when analyzing support and resistance levels. High volume near a level can confirm its significance and the likelihood of subsequent price movement. Traders often combine analysis across different time frames to get a more complete picture and improve the accuracy of their trading decisions.

Moving Averages

Moving averages (EMA and SMA) are another important tool in the technical analysis of cryptocurrencies:

EMA (Exponential Moving Average): Gives more weight to recent prices, allowing it to respond more quickly to price changes.

SMA (Simple Moving Average): Equally considers all prices over a given period.

Key types of moving averages used by traders:

EMA 50 and 200: Often used to identify trends. The crossing of the 50-day EMA with the 200-day EMA is called a "golden cross" (buy signal) or a "death cross" (sell signal).

SMA 50, 100, 150, and 200: These periods are often used to determine long-term trends and support/resistance levels. Similar to the EMA, the crossings of these averages can signal potential trend changes.

Settings Groups:

EMA Golden Cross & Death Cross: A setting to display the "golden cross" and "death cross" for the EMA.

EMA 50 & 200: A setting to display the 50-day and 200-day EMA.

Support and Resistance Levels: Includes settings for daily, weekly, and monthly levels.

SMA 50, 100, 150, 200: A setting to display the 50, 100, 150, and 200-day SMA.

SMA Golden Cross & Death Cross: A setting to display the "golden cross" and "death cross" for the SMA.

Components:

Enable/disable the display of support and resistance levels.

Show level labels.

Parameters for adjusting offset, display of EMA and SMA, and their time intervals.

Parameters for configuring EMA and SMA Golden Cross & Death Cross.

EMA Parameters:

Enable/disable the display of 50 and 200-day EMA.

Color and style settings for EMA.

Options to use bar gaps and the "LookAhead" function.

SMA Parameters:

Enable/disable the display of 50, 100, 150, and 200-day SMA.

Color and style settings for SMA.

Options to use bar gaps and the "LookAhead" function.

Effective use of support and resistance levels, as well as moving averages, requires an understanding of technical analysis, discipline, and the ability to adapt the strategy according to changing market conditions.

(RUS) Данный Pine 5 скрипт предоставляет разнообразные инструменты для настройки и отображения различных уровней поддержки и сопротивления, а также скользящих средних (EMA и SMA) на графиках. Использование этих инструментов является важной стратегией для определения точек входа и выхода из сделок.

Уровни поддержки и сопротивления

Дневные, недельные и месячные уровни поддержки и сопротивления играют ключевую роль в анализе движения цен:

Дневные уровни: Представляют собой цены, на которых криптовалюта имела тенденцию отскакивать в течение текущего торгового дня.

Недельные уровни: Отражают сильные цены, которые сохраняются в течение недели.

Месячные уровни: Указывают на наиболее значимые уровни, которые могут влиять на движение цены в течение месяца.

При торговле криптовалютами трейдеры используют эти уровни для принятия решений о входе в позицию или закрытии сделки. Например, если криптовалюта приближается к недельному уровню сопротивления и не удается его преодолеть, это может стать сигналом для продажи. Если цена достигает дневного уровня поддержки и начинает отскакивать вверх, это может указывать на возможность открытия длинной позиции.

Контекст рынка и объемы торговли также важны при анализе уровней поддержки и сопротивления. Высокий объем при приближении к уровню может подтвердить его значимость и вероятность последующего движения цены. Трейдеры часто комбинируют анализ различных временных рамок для получения более полной картины и улучшения точности своих торговых решений.

Скользящие средние

Скользящие средние (EMA и SMA) являются еще одним важным инструментом в техническом анализе криптовалют:

EMA (Exponential Moving Average): Экспоненциальная скользящая средняя, которая придает большее значение последним ценам. Это позволяет более быстро реагировать на изменения в ценах.

SMA (Simple Moving Average): Простая скользящая средняя, которая равномерно учитывает все цены в заданном периоде.

Основные виды скользящих средних, которые используются трейдерами:

EMA 50 и 200: Часто используются для выявления трендов. Пересечение 50-дневной EMA с 200-дневной EMA называется "золотым крестом" (сигнал на покупку) или "крестом смерти" (сигнал на продажу).

SMA 50, 100, 150 и 200: Эти периоды часто используются для определения долгосрочных трендов и уровней поддержки/сопротивления. Аналогично EMA, пересечения этих средних могут сигнализировать о возможных изменениях тренда.

Группы настроек:

EMA Golden Cross & Death Cross: Настройка для отображения "золотого креста" и "креста смерти" для EMA.

EMA 50 & 200: Настройка для отображения 50-дневной и 200-дневной EMA.

Уровни поддержки и сопротивления: Включает настройки для дневных, недельных и месячных уровней.

SMA 50, 100, 150, 200: Настройка для отображения 50, 100, 150 и 200-дневных SMA.

SMA Golden Cross & Death Cross: Настройка для отображения "золотого креста" и "креста смерти" для SMA.

Компоненты:

Включение/отключение отображения уровней поддержки и сопротивления.

Показ ярлыков уровней.

Параметры для настройки смещения, отображения EMA и SMA, а также их временных интервалов.

Параметры для настройки EMA и SMA Golden Cross & Death Cross.

Параметры EMA:

Включение/отключение отображения 50 и 200-дневных EMA.

Настройки цвета и стиля для EMA.

Опции для использования разрыва баров и функции "LookAhead".

Параметры SMA:

Включение/отключение отображения 50, 100, 150 и 200-дневных SMA.

Настройки цвета и стиля для SMA.

Опции для использования разрыва баров и функции "LookAhead".

Эффективное использование уровней поддержки и сопротивления, а также скользящих средних, требует понимания технического анализа, дисциплины и умения адаптировать стратегию в зависимости от изменяющихся условий рынка.

ABC PatternThe indicator, named "ABC Pattern," is designed to identify specific bullish and bearish patterns on a price chart. Here's a simple explanation of what it does:

What the Indicator Does:

1. Identifies Bullish Patterns:

- The indicator looks for a sequence of candles where certain conditions are met to form a bullish pattern.

- When it detects a bullish pattern, it colors the candle that occurred three periods ago in gold.

2. Identifies Bearish Patterns:

- Similarly, it looks for a sequence of candles where certain conditions are met to form a bearish pattern.

- When it detects a bearish pattern, it colors the candle that occurred three periods ago in pinkish.

3. Creates Alerts:

- Whenever a bullish or bearish pattern is identified, the indicator generates an alert.

- The alert message includes the type of pattern (bullish or bearish), the price level at the time of detection, and the date and time of the pattern formation.

Detailed Conditions:

- Bullish Pattern:

- The current candle closes higher than it opened.

- The previous candle also closes higher than it opened.