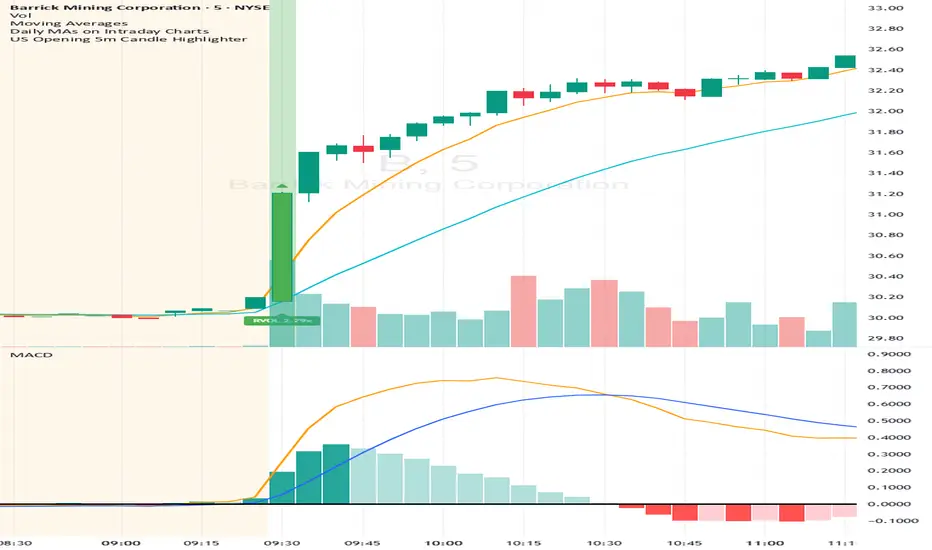

US Opening 5-Minute Candle HighlighterUS Opening 5-Minute Candle Highlighter — True RVOL (Two-Tier + Label)

What it does (in plain English)

This indicator finds the first 5-minute bar of the US cash session (09:30–09:35 ET) and highlights it when the candle has the specific “strong open” look you want:

Opens near the low of its own range, and

Closes near the high of its own range, and

Has a decisive real body (not a wick-y doji), and

(Optionally) is a green candle, and

Meets a TRUE opening-bar RVOL filter (compares today’s 09:30–09:35 volume only to prior sessions’ 09:30–09:35 volumes).

You get two visual intensities based on opening RVOL:

Tier-1 (≥ threshold 1, default 1.0×) → light green highlight + lime arrow

Tier-2 (≥ threshold 2, default 1.5×) → darker green highlight + green arrow

An RVOL label (e.g., RVOL 1.84x) can be shown above or below the opening bar.

Designed for 5-minute charts. On other timeframes the “opening bar” will be the bar that starts at 09:30 on that timeframe (e.g., 15-minute 09:30–09:45). For best results keep the chart on 5m.

How the pattern is defined

For the opening 5-minute bar, we compute:

Range = high − low

Body = |close − open|

Then we measure where the open and close sit within the bar’s own range on a 0→1 scale:

0 means exactly at the low

1 means exactly at the high

Using two quantiles:

Open ≤ position in range (0–1) (default 0.20)

Example: 0.20 means “open must be in the lowest 20% of the bar’s range.”

Close ≥ position in range (0–1) (default 0.80)

Example: 0.80 means “close must be in the top 20% of the bar’s range.”

This keeps the logic range-normalized so it adapts across different tickers and vol regimes (you’re not using fixed cents or % of price).

Body ≥ fraction of range (0–1) (default 0.55)

Requires the real body to be at least that fraction of the total range.

0.55 = body fills ≥ 55% of the candle.

Purpose: filter out indecisive, wick-heavy bars.

Raise to 0.7–0.8 for only the fattest thrusts; lower to 0.3–0.4 to admit more bars.

Require green candle? (default ON)

If ON, close > open must be true. Turn OFF if you also want to catch strong red opens for shorts.

Minimum range (ticks)

Ignore tiny, illiquid opens: e.g., set to 2–5 ticks to suppress micro bars.

TRUE Opening-Bar RVOL (why it’s “true”)

Most “RVOL” compares against any recent bars, which isn’t fair at the open.

This indicator calculates only against prior opening bars:

At 09:30–09:35 ET, take today’s opening 5-minute volume.

Compare it to the average of the last N sessions’ opening 5-minute volumes.

RVOL = today_open_volume / average_prior_open_volumes.

So:

1.0× = equal to average prior opens.

1.5× = 150% of average prior opens.

2.0× = double the typical opening participation.

A minimum prior samples guard (default 10) ensures you don’t judge with too little history. Until enough samples exist, the RVOL gate won’t pass (you can disable RVOL temporarily if needed).

Visuals & tiers

Light green highlight + lime arrow → price filters pass and RVOL ≥ Tier-1 (default 1.0×)

Dark green highlight + green arrow → price filters pass and RVOL ≥ Tier-2 (default 1.5×)

Optional bar paint in matching green tones for extra visibility.

Optional RVOL label (e.g., RVOL 1.84x) above or below the opening bar.

You can show the label only when the candle qualifies, or on every open.

Inputs (step-by-step)

Price-action filters

Open ≤ position in range (0–1): default 0.20. Smaller = stricter (must open nearer the low).

Close ≥ position in range (0–1): default 0.80. Larger = stricter (must close nearer the high).

Body ≥ fraction of range (0–1): default 0.55. Raise to demand a “fatter” body.

Require green candle?: default ON. Turn OFF to also mark bearish thrusts.

Minimum range (ticks): default 0. Set to 2–5 for liquid mid/large caps.

Time settings

Timezone: default America/New_York. Leave as is for US equities.

Start hour / minute: defaults 09:30. The bar that starts at this time is evaluated.

TRUE Opening-Bar RVOL (two-tier)

Require TRUE opening-bar RVOL?: ON = must pass Tier-1 to highlight; OFF = price filters alone can highlight (still shows Tier-2 when hit).

RVOL lookback (prior opens count): default 20. How many prior openings to average.

Min prior opens required: default 10. Warm-up guard.

Tier-1 RVOL threshold (× avg): default 1.00× (light green).

Tier-2 RVOL threshold (× avg): default 1.50× (dark green).

Display

Also paint candle body?: OFF by default. Turn ON for instant visibility on a chart wall.

Arrow size: tiny/small/normal/large.

Light/Dark opacity: tune highlight strength.

Show RVOL label?: ON/OFF.

Show label only when candle qualifies?: ON by default; OFF to see RVOL every open.

Label position: Above candle or Below candle.

Label size: tiny/small/normal/large.

How to use (quick start)

Apply to a 5-minute chart.

Keep defaults: Open ≤ 0.20, Close ≥ 0.80, Body ≥ 0.55, Require green ON.

Turn RVOL required ON, with Tier-1 = 1.0×, Tier-2 = 1.5×, Lookback = 20, Min prior = 10.

Optional: enable Paint bar and set Arrow size = large for monitor-wall visibility.

Optional: show RVOL label below the bar to keep wicks clean.

Interpretation:

Dark green = A+ opening thrust with strong participation (≥ Tier-2).

Light green = Valid opening thrust with at least average participation (≥ Tier-1).

No highlight = one or more filters failed (quantiles, body, green, range, or RVOL if required).

Alerts

Two alert conditions are included:

Opening 5m Match — Tier-2 RVOL → fires when the opening candle passes price filters and RVOL ≥ Tier-2.

Opening 5m Match — Tier-1 RVOL → fires when the opening candle passes price filters and RVOL ≥ Tier-1 (but < Tier-2).

Recommended alert settings

Condition: choose the script + desired tier.

Options: Once Per Bar Close (you want the confirmed 09:30–09:35 bar).

Set your watchlist to symbols of interest (themes/sectors) and let the alerts pull you to the right charts.

Recommended starting values

Quantiles: Open ≤ 0.20, Close ≥ 0.80

Body fraction: 0.55

Require green: ON

RVOL: Required ON, Tier-1 = 1.0×, Tier-2 = 1.5×, Lookback 20, Min prior 10

Display: Paint bar ON, Arrow large, Label ON, Below candle

Tune tighter for A-plus selectivity:

Open ≤ 0.15, Close ≥ 0.85, Body ≥ 0.65, Tier-2 2.0×.

Notes, tips & limitations

5-minute timeframe is the intended use. On higher TFs, the 09:30 bar spans more than 5 minutes; geometry may not reflect the first 5 minutes alone.

RTH only: The opening detection looks at the clock (09:30 ET). Pre-market bars are ignored for the signal and for RVOL history.

Warm-up period: Until you have Min prior opens required samples, the RVOL gate won’t pass. You can temporarily toggle RVOL off.

DST & timezone: Leave timezone on America/New_York for US equities. If you trade non-US exchanges, set the appropriate TZ and opening time.

Illiquid tickers: Use Minimum range (ticks) and require RVOL to reduce noise.

No strategy orders: This is a visual/alert tool. Combine with your execution and risk plan.

Why this is useful on multi-monitor setups

Instant pattern recognition: the two-shade green makes A vs A+ opens pop at a glance.

Adaptive thresholds: quantiles & body are within-bar, so it works across $5 and $500 names.

Fair volume test: TRUE opening RVOL avoids comparing to pre-market or midday bars.

Optional labels: glanceable RVOL x-value helps triage the strongest themes quickly.

Cari dalam skrip untuk "a股板块+沪深两市+股价不超过10元的股票+技术形态好"

Multi-Symbol and Multi-Timeframe Supertrend Screener [Pineify]Multi-Symbol and Multi-Timeframe Supertrend Screener

Advanced Supertrend screener for TradingView that monitors 6 symbols across 4 timeframes simultaneously. Features customizable ATR periods, visual alerts, and color-coded trend direction displays for efficient market scanning.

Key Features

The Supertrend Screener is a comprehensive multi-symbol market monitoring tool that displays Supertrend indicator signals across multiple assets and timeframes in a single, organized table view. This screener eliminates the need to manually check individual charts by providing real-time trend analysis for up to 6 symbols across 4 different timeframes simultaneously.

How It Works

The screener utilizes the proven Supertrend indicator methodology, which combines Average True Range (ATR) and price action to determine trend direction. The core calculation involves:

Computing the ATR using a customizable period (default: 10)

Applying a multiplication factor (default: 3.0) to create dynamic support/resistance levels

Determining trend direction based on price position relative to these levels

Displaying results through color-coded cells with customizable text labels

The indicator employs the request.security() function to fetch data from multiple symbols and timeframes, ensuring accurate cross-market analysis without chart switching.

Trading Ideas and Insights

This screener excels in several trading scenarios:

Market Overview: Quickly assess overall market sentiment across major cryptocurrencies or forex pairs

Trend Confirmation: Verify trend alignment across multiple timeframes before entering positions

Divergence Spotting: Identify when shorter timeframes diverge from longer-term trends

Opportunity Scanning: Locate assets showing consistent trend direction across all monitored timeframes

Risk Management: Monitor multiple positions simultaneously to spot potential trend reversals

The screener is particularly effective for swing traders and position traders who need to monitor multiple assets without constantly switching between charts.

How Multiple Indicators Work Together

While this screener focuses specifically on the Supertrend indicator, it incorporates several complementary technical analysis components:

ATR Foundation: Uses Average True Range to adapt to market volatility, making the indicator responsive to current market conditions

Multi-Timeframe Analysis: Combines signals from 1-minute, 5-minute, 10-minute, and 30-minute timeframes to provide comprehensive trend perspective

Price Action Integration: The Supertrend calculation inherently incorporates price action by using high, low, and close values

Volatility Adjustment: The ATR-based calculation ensures the indicator adapts to different volatility regimes across various assets

The synergy between these elements creates a robust screening system that accounts for both momentum and volatility , providing more reliable trend identification than single-timeframe analysis.

Unique Aspects

Several features distinguish this screener from standard Supertrend implementations:

Table-Based Display: Presents data in an organized, space-efficient format rather than overlay plots

Customizable Visual Elements: Full control over text labels, colors, and background styling

Multi-Asset Capability: Monitors 6 different symbols simultaneously without performance degradation

Efficient Resource Usage: Optimized code structure minimizes calculation overhead

Professional Presentation: Clean, institutional-grade visual design suitable for trading desks

How to Use

Symbol Configuration: Input your desired symbols in the Symbol section (default includes major crypto pairs)

Timeframe Setup: Configure four timeframes for analysis (default: 1m, 5m, 10m, 30m)

Supertrend Parameters: Adjust the Factor (sensitivity) and ATR Period according to your trading style

Visual Customization: Set custom text labels and colors for up/down trends

Market Analysis: Monitor the table for consistent signals across timeframes and symbols

Interpretation Guide:

- Green cells indicate uptrend (price above Supertrend line)

- Red cells indicate downtrend (price below Supertrend line)

- Look for alignment across multiple timeframes for stronger signal confidence

Customization

The screener offers extensive customization options:

Factor Setting: Adjust sensitivity (higher values = less sensitive, fewer signals)

ATR Period: Modify lookback period for volatility calculation

Text Labels: Customize up/down trend display text

Color Scheme: Full RGB color control for text and background elements

Symbol Selection: Monitor any TradingView-supported symbols

Timeframe Array: Choose any four timeframes for comprehensive analysis

Conclusion

The Supertrend Screener transforms traditional single-chart analysis into an efficient, multi-dimensional market monitoring system. By combining the reliability of the Supertrend indicator with multi-timeframe and multi-symbol capabilities, this tool empowers traders to make more informed decisions with greater market context.

Whether you're managing multiple positions, scanning for new opportunities, or confirming trend direction before entries, this screener provides the comprehensive overview needed for professional trading operations. The clean interface and customizable features make it suitable for traders of all experience levels while maintaining the analytical depth required for serious market analysis.

Perfect for day traders, swing traders, and anyone requiring efficient multi-market trend monitoring in a single view.

Euro Area vs US10YThe Euro Area GDP-Weighted Yield vs US10Y Spread is a macroeconomic indicator designed for forex traders and institutional investors who want to monitor the fundamental interest rate differential between the Eurozone and the United States. This tool aggregates sovereign bond yields from the major Eurozone member states using a weighted methodology based on outstanding government debt, providing a comprehensive view of the Euro Area’s fixed income market dynamics.

This indicator calculates a composite 10-year government bond yield for the Eurozone by combining data from seven major member countries: Germany, France, Italy, Spain, Netherlands, Belgium, and Austria. The weights are based on the proportion of government debt outstanding in each country, reflecting the actual composition of the European sovereign bond market rather than just GDP size.

The indicator then compares this Euro Area weighted yield against the US 10-Year Treasury yield (US10Y), producing a yield spread that serves as a powerful leading indicator for EUR/USD price movements.

VWAP Deviation Oscillator [BackQuant]VWAP Deviation Oscillator

Introduction

The VWAP Deviation Oscillator turns VWAP context into a clean, tradeable oscillator that works across assets and sessions. It adapts to your workflow with four VWAP regimes plus two rolling modes, and three deviation metrics: Percent, Absolute, and Z-Score. Colored zones, optional standard deviation rails, and flexible plot styles make it fast to read for both trend following and mean reversion.

What it does

This tool measures how far price is from a chosen VWAP and expresses that gap as an oscillator. You can view the deviation as raw price units, percent, or standardized Z-Score. The plot can be a histogram or a line with optional fills and sigma bands, so you can quickly spot polarity shifts, overbought and oversold conditions, and strength of extension.

VWAP modes track a session VWAP that resets (4H, Daily, Weekly) or a rolling VWAP that updates continuously over a fixed number of bars or days.

Deviation modes let you choose the lens: Percent, Absolute, or Z-Score. Each highlights different aspects of stretch and mean pressure.

Visual encoding uses a 10-zone color palette to grade the magnitude of deviation on both sides of zero.

Volatility guards compute mode-specific sigma so thresholds are stable even when volatility compresses.

Why this works

VWAP is a high signal anchor used by institutions to gauge fair participation. Deviations around VWAP cluster in regimes: mild oscillations within a band, decisive pushes that signal imbalance, and standardized extremes that often precede either continuation or snapback. Expressing that distance as a single time series adds clarity: bias is the oscillator’s sign, risk context is its magnitude, and regime is the way it behaves around sigma lines.

How to use it

Trend following

Favor the side of the zero line. Bullish when the oscillator is above zero and making higher swing highs. Bearish when below zero and making lower swing lows. Use +1 sigma and +2 sigma in your mode as strength tiers. Pullbacks that hold above zero in uptrends, or below zero in downtrends, are often continuation entries.

Mean reversion

Fade stretched readings when structure supports it. Look for tests of +2 sigma to +3 sigma that fail to progress and roll back toward zero, or the mirror on the downside. Z-Score mode is best when you want standardized gates across assets. Percent mode is intuitive for intraday scalps where a given percent stretch tends to mean revert.

Session playbook

Use Daily or Weekly VWAP for intraday or swing context. Rolling modes help when the asset lacks clean session boundaries or when you want a continuous anchor that adapts to liquidity shifts.

Key settings

VWAP computation

VWAP Mode = 4 Hours, Daily, Weekly, Rolling (Bars), Rolling (Days). Session modes reset the VWAP when a new session begins. Rolling modes compute VWAP over a fixed trailing window.

Rolling (Lookback: Bars) controls the trailing bar count when using Rolling (Bars).

Rolling (Lookback: Days) converts days to bars at runtime and uses that trailing span.

Use Close instead of HLC3 switches the price reference. HLC3 is smoother. Close makes the anchor track settlement more tightly.

Deviation measurement

Deviation Mode

Percent : 100 * (Price / VWAP - 1). Good for uniform scaling across instruments.

Absolute : Price - VWAP. Good when price units themselves matter.

Z-Score : Standardizes the absolute residual by its own mean and standard deviation over Z/Std Window . Ideal for cross-asset comparability and regime studies.

Z/Std Window sets the mean and standard deviation window for Z-Score mode.

Volatility controls

Percent Mode Volatility Lookback estimates sigma for percent deviations.

Absolute Mode Volatility Lookback estimates sigma for absolute deviations.

Minimum Sigma Guard (pct pts) prevents the percent sigma from collapsing to near zero in extremely quiet markets.

Visualization

Plot Type = Histogram or Line. Histogram emphasizes impulse and polarity changes. Line emphasizes trend waves and divergences.

Positive Color / Negative Color define the palette for line mode. Histogram uses a 10-bucket gradient automatically.

Show Standard Deviations plots symmetric rails at ±1, ±2, ±3 sigma in the current mode’s units.

Fill Line Oscillator and Fill Opacity add a soft bias band around zero for line mode.

Line Width affects both the oscillator and the sigma rails.

Reading the zones

The oscillator’s color and height map deviation to nine graded buckets on each side of zero, with deeper greens above and deeper reds below. In Percent and Absolute modes, those buckets are scaled by their mode-specific sigma. In Z-Score mode the bucket edges are fixed at 0.5, 1.0, 2.0, and 2.8.

0 to +1 sigma weak positive bias, usually rotational.

+1 to +2 sigma constructive impulse. Pullbacks that hold above zero often continue.

+2 to +3 sigma strong expansion. Watch for either trend continuation or exhaustion tells.

Beyond +3 sigma statistical extreme. Requires structure to avoid fading too soon.

Mirror logic applies on the negative side.

Suggested workflows

Trend continuation checklist

Pick a session VWAP that matches your timeframe, for example Daily for intraday or Weekly for position trades.

Wait for the oscillator to hold the correct side of zero and for a sequence of higher swing lows in the oscillator (uptrend) or lower swing highs (downtrend).

Buy pullbacks that stabilize between zero and +1 sigma in an uptrend. Sell rallies that stabilize between zero and -1 sigma in a downtrend.

Use the next sigma band or a prior price swing as your target reference.

Mean reversion checklist

Switch to Z-Score mode for standardized thresholds.

Identify tests of ±2 sigma to ±3 sigma that fail to extend while price meets support or resistance.

Enter on a polarity change through the prior histogram bar or a small hook in line mode.

Fade back to zero or to the opposite inner band, then reassess.

Notes on the three modes

Percent is easy to reason about when you care about proportional stretch. It is well suited to intraday and multi-asset dashboards.

Absolute tracks cash distance from VWAP. This is useful when instruments have tight ticks and you plan risk in price units.

Z-Score standardizes the residual and is best for quant studies, cross-asset comparisons, and threshold research that must be scale invariant.

What the alerts can tell you

Polarity changes at zero can mark the start or end of a leg.

Crosses of ±1 sigma identify overbought or oversold in the current mode’s units.

Zone changes signal an upgrade or downgrade in deviation strength.

Troubleshooting and edge cases

If your instrument has long flat periods, keep Minimum Sigma Guard above zero in Percent mode so the rails do not vanish.

In Rolling modes, very short windows will respond quickly but can whip around. Session modes smooth this by resetting at well known boundaries.

If Z-Score looks erratic, increase Z/Std Window to stabilize the estimate of mean and sigma for the residual.

Final thoughts

VWAP is the anchor. The deviation oscillator is the narrative. By separating bias, magnitude, and regime into a simple stream you can execute faster and review cleaner. Pick the VWAP mode that matches your horizon, choose the deviation lens that matches your risk framework, and let the color graded zones guide your decisions.

3/4-Bar GRG / RGR Pattern (Conditional 4th Candle)This indicator can be used to identify the Green-Red-Green or Red-Green-Red pattern.

It is a price action indicator where a price action which identifies the defeat of buyers and sellers.

If the buyers comprehensively defeat the sellers then the price moves up and if the sellers defeat the buyers then the price moves down.

In my trading experience this is what defines the price movement.

It is a 3 or 4 candle pattern, beyond that i.e, 5 or more candles could mean a very sideways market and unnecessary signal generation.

How does it work?

Upside/Green signal

Say candle 1 is Green, which means buyers stepped in, then candle 2 is Red or a Doji, that means sellers brought the price down. Then if candle 3 is forming to be Green and breaks the closing of the 1st candle and opening of the 2nd candle, then a green arrow will appear and that is the place where you want to take your trade.

Here the buyers defeated the sellers.

Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

Important - We need to enter the trade as soon as the price moves above the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close. Ignore wicks.

I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

I call it the +-+ or GRG pattern.

Stop loss can be candle 2's mid for safe traders (that includes me) or candle 2's body low for risky traders.

Back testing suggests that body low will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Downside/Red signal

Say candle 1 is Red, which means sellers stepped in, then candle 2 is Green or a Doji, that means buyers took the price up. Then if candle 3 is forming to be Red and breaks the closing of the 1st candle and opening of the 2nd candle then a Red arrow will appear and that is the place where you want to take your trade.

Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

We need to enter the trade as soon as the price moves below the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close.

I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

I call it the -+- or RGR pattern.

Stop loss can be candle 2's mid for safe traders ( that includes me) or candle 2's body high for risky traders.

Back testing suggests that body high will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Important Settings

You can enable or disable the 4th candle signal to avoid the noise, but at times I have noticed that the 4th candle gives a very strong signal or I can say that the strong signal falls on the 4th candle. This is mostly a coincidence.

You can also configure how many previous bars should the signal be generated for. 10 to 30 is good enough. To backtest increase it to 2000 or 5000 for example.

Rest are self explanatory.

Pointers

If after taking the trade, the next candle moves in your direction and closes strong bullish or bearish, then move SL to break even and after that you can trail it.

If a upside trade hits SL and immediately a down side trade signal is generated on the next candle then take it. Vice versa is true.

Trades need to be taken on previous 2 candle's body high or low combined and not the wicks.

The most losses a trader takes is on a sideways day and because in our strategy the stop loss is so small that even on a sideways day we'll get out with a little profit or worst break even.

Hold targets for longer targets and don't panic.

If last 3-4 days have been sideways then there is a good probability that day will be trending so we can hold our trade for longer targets. Target to hold the trade for whole day and not exit till the day closes.

In general avoid trading in the middle of the day for index and stocks. Divide the day into 3 parts and avoid the middle.

Use Support/Resistance, 10, 20, 50, 200 EMA/SMA, Gaps, Whole/Round numbers(very imp) for identifying targets.

Trail your SL.

For indexes I would use 5 min and 15 min timeframe.

For commodities and crypto we can use higher timeframe as well. Look for signals during volatile time durations and avoid trading the whole day. Signal usually gives good targets on those times.

If a GRG or RGR pattern appears on a daily timeframe then this is our time to go big.

Minimum Risk to Reward should be 1:2 and for longer targets can be 1:4 to 1:10.

Trade with small lot size. Money management will happen automatically.

With small lot size and correct Risk-Re ward we can be very profitable. Don't trade with big lot size.

Stay in the market for longer and collect points not money.

Very imp - Watch market and learn to generate a market view.

Very imp - Only 4 candles are needed in trading - strong bullish, strong bearish, hammer, inverse hammer and doji.

Go big on bearish days for option traders. Puts are better bought and Calls are better sold.

Cluster of green signals can lead to bigger move on the upside and vice versa for red signals.

Most of this is what I learned from successful traders (from the top 2%) only the indicator is mine.

AutoDay MA (Session-Normalized)📊 AutoDay MA (Session-Normalized Moving Average)

⚡ Daily power, intraday precision.

AutoDay MA automatically converts any N-day moving average into the exact equivalent on your current intraday timeframe.

💡 Concept inspired by Brian Shannon (Alphatrends) – mapping daily MAs onto intraday charts by normalizing session minutes.

🛠 How it works

Set Days (N) (e.g., 5, 10, 20).

Define Session Minutes per Day (⏱ 390 = US RTH, 🌍 1440 = 24h).

The indicator detects your chart’s timeframe and computes:

Length = (Days × SessionMinutes) / BarMinutes

Applies your chosen MA type (📐 SMA / EMA / RMA / WMA) with rounding (nearest, up, down).

Displays all details in a clear corner info panel.

✅ Why use it

Consistency 🔄: Same 5-day smoothing across all intraday charts.

Session-aware 🕒: Works for equities, futures, FX, crypto.

Transparency 🔍: Always shows the math & final MA length.

Alerts built-in 🔔: Cross up/down vs. price.

📈 Examples

5-Day on 1m → 1950-period MA

5-Day on 15m → 130-period MA

5-Day on 65m → 30-period MA

10-Day on 24h/15m (crypto) → 960-period MA

3SMA (1H only) by tophengzkyThis script plots three Simple Moving Averages (SMA 10, 20, 50), but they are only visible when the chart timeframe is set to 1 hour (1H).

It helps traders focus on higher timeframe trend direction without cluttering charts on other timeframes.

SMA1 = 10 (white)

SMA2 = 20 (yellow)

SMA3 = 200 (red)

Works only on 1H timeframe

Useful for swing traders and intraday traders who rely on hourly trend confirmation.

why 1 hr only? the only purpose of this is just to know the bias of the market weather it will reverse or it will continue the trend. As long as the price action did not cross this 3 SMA's the trend will continue.

as a trend trader it is very useful this strategy.. make it simple!

自定义均线(多色 & 分级线宽)Title: Multi-Color Moving Average Suite (MA5…MA4320) — Pine v6

Summary (1–2 lines):

An overlay indicator that plots a full ladder of SMA lines from MA5 up to MA4320. Each MA has a unique color, and line width scales with period (short = thin, mid = medium, long = thick) to make trend structure easy to read at a glance.

What it does

• Plots 16 simple moving averages: 5, 10, 20, 30, 60, 120, 160, 240, 480, 720, 960, 1440, 1750, 2880, 4320.

• Distinct colors for every MA to avoid confusion when lines cluster.

• Period-based thickness:

• Short-term (<60) = thin,

• Mid-term (60–160) = medium,

• Long-term (≥240) = thick (capped; no unlimited growth).

• Designed for quick trend reading across intraday to multi-year cycles (especially useful for 24/7 markets like crypto).

How to use

1. Add the indicator to any chart (works on all symbols/timeframes).

2. Use the thin/medium/thick visual hierarchy to identify short-/mid-/long-term bias and crossovers.

3. On very low timeframes, consider hiding some ultra-long MAs if your chart has insufficient history.

Notes

• Built with Pine Script v6; uses ta.sma(close, length) only (no repainting).

• Very long MAs (e.g., 2880/4320) require enough bars; they will display na until sufficient history loads.

• No inputs/alerts by default—kept intentionally simple for clarity. (Easy to extend with toggles, custom colors, EMA/WMA options, alerts, etc.)

Credits

Author: TraderFinsher (customized multi-MA visualization with color and thickness hierarchy).

⸻

标题: 多色均线系统(MA5…MA4320)— Pine v6

摘要(1–2 句):

这是一个叠加在价格上的 SMA 均线组,从 MA5 到 MA4320。为每条均线设置了 独立颜色,并按 周期长度分级线宽(短=细、中=中等、长=较粗),让趋势结构一眼可读。

功能说明

• 绘制 16 条简单移动平均线:5、10、20、30、60、120、160、240、480、720、960、1440、1750、2880、4320。

• 全部不同颜色,避免密集时混淆。

• 线宽随周期分级:

• 短期(<60)= 细,

• 中期(60–160)= 中等,

• 长期(≥240)= 粗(封顶,不再无限加粗)。

• 适合从日内到多年周期的 趋势快速判读(对加密等 24/7 市场尤为友好)。

使用建议

1. 将指标添加到任意品种/周期。

2. 结合细/中/粗的视觉层级,判断短/中/长趋势与均线交叉。

3. 在较低周期下,如果历史数据不足,可隐藏部分超长均线。

注意事项

• 使用 Pine v6,仅调用 ta.sma(close, length),不重绘。

• 超长均线需要足够历史数据,未满足前会显示 na。

• 默认不含参数和告警,追求简洁清晰(后续可扩展开关、自定义颜色/线宽、EMA/WMA 选项与告警等)。

致谢

作者:TraderFinsher(基于颜色与线宽层级的多均线可视化)。

Market Mode Risk IndicatorMarket Mode Risk Indicator v1.1

This custom indicator helps traders gauge market risk sentiment by monitoring Exponential Moving Average (EMA) or Simple Moving Average (SMA) crossovers on key indices like BIST 100 (for Turkish markets), NASDAQ Composite (tech-focused US), or Dow Jones Industrial Average (industrial US). It dynamically categorizes the market into three actionable modes based on the index's position relative to layered MAs, providing a quick visual snapshot without cluttering your chart.

Risk Modes Explained:

RISK OFF (Red): Index closes below the Long MA (default 50 periods) – signals bearish caution; time to tighten stops or reduce exposure.

RISK TEST (Orange): Index above Medium MA1 (21 periods) and Extra Long MA (55 periods), but below Short MA (10 periods) and above Long MA – a transitional "test" phase; watch for confirmation before entering.

RISK ON (Green): Index above all MAs (Short, Medium, Long, Extra Long) – bullish green light; favorable for longs or momentum plays.

How It Works:

The core logic uses boolean checks on the index's close price against user-defined MA lengths. For example:

It pulls live data from your selected index via request.security.

Computes MAs with ternary operators for EMA (ta.ema) or SMA (ta.sma) based on your choice.

Mode detection relies on AND/OR conditions (e.g., aboveShort and aboveMed1 and aboveLong and aboveExtraLong for RISK ON) to filter noise and focus on meaningful shifts.

No lookahead bias – all calculations are historical and real-time compatible. Defaults (10/21/50/55) are inspired by common Fibonacci-inspired periods for balanced sensitivity.

Alerts fire only on mode transitions (e.g., from RISK OFF to ON) to prevent spam, using alertcondition with dynamic messages including price and ticker.

Customization Options:

Index & MA Settings: Switch EMA/SMA; tweak lengths (min 1 period) for your timeframe (e.g., shorter for intraday).

Display: Position the table (top/bottom, left/right); toggle MA values on/off.

Looks: Background/border/text colors, transparency (0-100%) for theme matching.

Built in Pine Script v5 for efficiency – lightweight, no repaints.

Usage Tips:

Add to any stock chart (e.g., GARAN for BIST analysis).

Select your index in settings; refresh chart if switching MA type.

Use on daily/4H timeframes for swing trading; alerts via email/SMS for hands-free monitoring.

Pro Tip: Combine with volume or RSI for confirmation – RISK ON + rising volume = stronger buy signal.

RSI Trendlines and Divergences█OVERVIEW

The "RSI Trendlines and Divergences" indicator is an advanced technical analysis tool that leverages the Relative Strength Index (RSI) to draw trendlines and detect divergences. Designed for traders seeking precise market signals, the indicator identifies key pivot points on the RSI chart, draws trendlines between pivots, and detects bullish and bearish divergences. It offers flexible settings, background coloring for breakout signals, and divergence labels, supported by alerts for key events. The indicator is universal and works across all markets (stocks, forex, cryptocurrencies) and timeframes.

█CONCEPTS

The indicator was developed to provide an alternative signal source for the RSI oscillator. Trendline breakouts and bounces off trendlines offer a broader perspective on potential price behavior. Combining these with traditional RSI signal interpretation can serve as a foundation for creating various trading strategies.

█FEATURES

- RSI and Pivot Calculation: Calculates RSI based on the selected source price (default: close) with a customizable period (default: 14). Identifies pivot points on RSI and price for trendlines and divergences.

- RSI Trendlines: Draws trendlines connecting RSI pivots (upper for downtrends, lower for uptrends) with optional extension (default: 30 bars). The trendline appears and generates a signal only after the first RSI crossover. Lines are colored (red for upper, green for lower).

- Trendline Fill: Widens the trendline with a tolerance margin expressed in RSI points, reducing signal noise and visually highlighting trend zones. Breaking this zone is a condition for generating signals, minimizing false signals. The tolerance margin can be increased or decreased.

- Divergence Detection: Identifies bullish and bearish divergences based on RSI and price pivots, displaying labels (“Bull” for bullish, “Bear” for bearish) with adjustable transparency. Divergence labels appear with a delay equal to the specified pivot length (default: 5). Higher values yield stronger signals but with greater delay.

- Breakout Signals: Generates signals when RSI crosses the trendline (bullish for upper lines, bearish for lower lines), with background coloring for signal confirmation.

- Alerts: Built-in alerts for:

Detection of bullish and bearish divergences.

Upper trendline crossover (bullish signal).

Lower trendline crossover (bearish signal).

- Customization: Allows adjustment of RSI length, pivot settings, line colors, fills, labels, and transparency of signals and background.

█HOW TO USE

Add the indicator to your TradingView chart via the Pine Editor or Indicators menu.

Configuring Settings.

RSI Settings

- RSI Length: Period for RSI calculation (default: 14).

- SMA Length: Period for RSI moving average (default: 9).

- Source: Source price for RSI (default: close).

Pivot Settings for Trend

- Left Bars for Pivot: Number of bars back for detecting pivots (default: 10).

- Right Bars for Pivot: Number of bars forward for confirming pivots (default: 10).

- Extension after Second Pivot: Number of bars to extend the trendline (default: 30, 0 = none). Extension increases the number of signals, while shortening reduces them.

- Tolerance: Deviation in RSI points to widen the breakout margin, reducing signal noise (default: 3.0).

Divergence Settings

- Enable Divergence Detection: Enables/disables divergence detection (default: enabled).

- Pivot Length for Divergence: Pivot period for divergences (default: 5).

Style Settings

- Upper Trendline Color: Color for downtrend lines (default: red).

- Upper Fill Color: Fill color for upper lines (default: red, transparency 70).

- Lower Trendline Color: Color for uptrend lines (default: green).

- Lower Fill Color: Fill color for lower lines (default: green, transparency 70).

- SMA Color: Color for RSI moving average (default: yellow).

- Bullish Divergence Color: Color for bullish labels (default: green).

- Bearish Divergence Color: Color for bearish labels (default: red).

- Text Color: Color for label text (default: white).

- Divergence Label Transparency: Transparency of labels (0-100, default: 40).

- Signal Background Transparency: Transparency of breakout signal background (0-100, default: 80).

Interpreting Signals

- Trendlines: Upper lines (red) indicate RSI downtrends, lower lines (green) indicate uptrends. The trendline appears and generates a signal only after the first RSI crossover. Trendline breakouts suggest potential trend reversals.

- Divergences: “Bull” labels indicate bullish divergence (potential rise), “Bear” labels indicate bearish divergence (potential decline), with a delay based on pivot length (default: 5). Divergences serve as confirmation or warning of trend reversal, not as standalone signals.

- Signal Background: Green background signals bullish breakouts, red background signals bearish breakouts.

- RSI Levels: Horizontal lines at 70 (overbought), 50 (midline), and 30 (oversold) help assess market zones.

- Alerts: Set up alerts in TradingView for divergences or trendline breakouts.

Combining with Other Tools: Use with support/resistance levels, Fibonacci levels, or other indicators for signal confirmation.

█APPLICATIONS

The "RSI Trendlines and Divergence" indicator is designed to identify trends and potential reversal points, supporting both trend-following and reversal strategies:

- Trend Confirmation: Trendlines indicate the RSI trend direction, with breakouts signaling potential reversals. The indicator is functional in traditional RSI usage, allowing classic RSI interpretation (e.g., returning from overbought/oversold zones). Combining trendline breakouts with RSI signal levels, such as a return from overbought or oversold zones paired with a trendline breakout, strengthens the signal.

- Divergence Detection: Divergences serve as confirmation or warning of trend reversal, not as standalone signals.

█NOTES

- Adjust settings (e.g., RSI length, pivots, tolerance) to suit your trading style and timeframe.

- Combine with other technical analysis tools to enhance signal accuracy.

RD-DynamicTSMADescription of the RD-DynamicTSMA Pine Script Indicator:

This single indicator dynamically adjusts the three SMAs to key periods used by professional traders across timeframes:

Daily: 10, 21, 50 periods (standard for swing trading trends).

Weekly+: 10, 21, 30 periods (optimized for positional & longer-term views).

Lengths auto-update on timeframe switches.

Historical VolatilityHistorical Volatility Indicator with Custom Trading Sessions

Overview

This indicator calculates **annualized Historical Volatility (HV)** using logarithmic returns and standard deviation. Unlike standard HV indicators, this version allows you to **customize trading sessions and holidays** for different markets, ensuring accurate volatility calculations for options pricing and risk management.

Key Features

✅ Custom Trading Sessions - Define multiple trading sessions per day with precise start/end times

✅ Multiple Markets Support - Pre-configured for US, Russian, European, and crypto markets

✅ Clearing Periods Handling - Account for intraday clearing breaks

✅ Flexible Calendar - Set trading days per year for different countries

✅ All Timeframes - Works correctly on intraday, daily, weekly, and monthly charts

✅ Info Table - Optional display showing calculation parameters

How It Works

The indicator uses the classical volatility formula:

σ_annual = σ_period × √(periods per year)

Where:

- σ_period = Standard deviation of logarithmic returns over the specified period

- Periods per year = Calculated based on actual trading time (not calendar time)

Calculation Method

1. Computes log returns: ln(close / close )

2. Calculates standard deviation over the lookback period

3. Annualizes using the square root rule with accurate period count

4. Displays as percentage

Settings

Calculation

- Period (default: 10) - Lookback period for volatility calculation

Trading Schedule

- Trading Days Per Year (default: 252) - Number of actual trading days

- USA: 252

- Russia: 247-250

- Europe: 250-253

- Crypto (24/7): 365

- Trading Sessions - Define trading hours in format: `hh:mm:ss-hh:mm:ss, hh:mm:ss-hh:mm:ss`

Display

- Show Info Table - Shows calculation parameters in real-time

Market Presets

United States (NYSE/NASDAQ)

Trading Sessions: 09:30:00-16:00:00

Trading Days Per Year: 252

Trading Minutes Per Day: 390

Russia (MOEX)

Trading Sessions: 10:00:00-14:00:00, 14:05:00-18:40:00

Trading Days Per Year: 248

Trading Minutes Per Day: 515

Europe (LSE)

Trading Sessions: 08:00:00-16:30:00

Trading Days Per Year: 252

Trading Minutes Per Day: 510

Germany (XETRA)

Trading Sessions: 09:00:00-17:30:00

Trading Days Per Year: 252

Trading Minutes Per Day: 510

Cryptocurrency (24/7)

Trading Sessions: 00:00:00-23:59:59

Trading Days Per Year: 365

Trading Minutes Per Day: 1440

Use Cases

Options Trading

- Compare HV vs IV - Historical volatility compared to implied volatility helps identify mispriced options

- Volatility mean reversion - Identify when volatility is unusually high or low

- Straddle/strangle selection - Choose optimal strikes based on historical movement

Risk Management

- Position sizing - Adjust position size based on current volatility

- Stop-loss placement - Set stops based on expected price movement

- Portfolio volatility - Monitor individual asset volatility contribution

Market Analysis

- Regime identification - Detect transitions between low and high volatility environments

- Cross-market comparison - Compare volatility across different assets and markets

Why Accurate Trading Hours Matter

Standard HV indicators assume 24-hour trading or use simplified day counts, leading to significant errors in annualized volatility:

- 5-minute chart error : Can be off by 50%+ if using wrong period count

- Options pricing impact : Even 2-3% HV error affects option values substantially

- Intraday vs overnight : Correctly excludes non-trading periods

This indicator ensures your HV calculations match the methodology used in professional options pricing models.

Technical Notes

- Uses actual trading minutes, not calendar days

- Handles multiple clearing periods within a single trading day

- Properly scales volatility across all timeframes

- Logarithmic returns for more accurate volatility measurement

- Compatible with Pine Script v6

Author Notes: This indicator was designed specifically for options traders who need precise volatility measurements across different global markets. The customizable trading sessions ensure your HV calculations align with actual market hours and industry-standard options pricing models.

Volume Delta Volume Signals by Claudio [hapharmonic]// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © hapharmonic

//@version=6

FV = format.volume

FP = format.percent

indicator('Volume Delta Volume Signals by Claudio ', format = FV, max_bars_back = 4999, max_labels_count = 500)

//------------------------------------------

// Settings |

//------------------------------------------

bool usecandle = input.bool(true, title = 'Volume on Candles',display=display.none)

color C_Up = input.color(#12cef8, title = 'Volume Buy', inline = ' ', group = 'Style')

color C_Down = input.color(#fe3f00, title = 'Volume Sell', inline = ' ', group = 'Style')

// ✅ Nueva entrada para colores de señales

color buySignalColor = input.color(color.new(color.green, 0), "Buy Signal Color", group = "Signals")

color sellSignalColor = input.color(color.new(color.red, 0), "Sell Signal Color", group = "Signals")

string P_ = input.string(position.top_right,"Position",options = ,

group = "Style",display=display.none)

string sL = input.string(size.small , 'Size Label', options = , group = 'Style',display=display.none)

string sT = input.string(size.normal, 'Size Table', options = , group = 'Style',display=display.none)

bool Label = input.bool(false, inline = 'l')

History = input.bool(true, inline = 'l')

// Inputs for EMA lengths and volume confirmation

bool MAV = input.bool(true, title = 'EMA', group = 'EMA')

string volumeOption = input.string('Use Volume Confirmation', title = 'Volume Option', options = , group = 'EMA',display=display.none)

bool useVolumeConfirmation = volumeOption == 'none' ? false : true

int emaFastLength = input(12, title = 'Fast EMA Length', group = 'EMA',display=display.none)

int emaSlowLength = input(26, title = 'Slow EMA Length', group = 'EMA',display=display.none)

int volumeConfirmationLength = input(6, title = 'Volume Confirmation Length', group = 'EMA',display=display.none)

string alert_freq = input.string(alert.freq_once_per_bar_close, title="Alert Frequency",

options= ,group = "EMA",

tooltip="If you choose once_per_bar, you will receive immediate notifications (but this may cause interference or indicator repainting).

\n However, if you choose once_per_bar_close, it will wait for the candle to confirm the signal before notifying.",display=display.none)

//------------------------------------------

// UDT_identifier |

//------------------------------------------

type OHLCV

float O = open

float H = high

float L = low

float C = close

float V = volume

type VolumeData

float buyVol

float sellVol

float pcBuy

float pcSell

bool isBuyGreater

float higherVol

float lowerVol

color higherCol

color lowerCol

//------------------------------------------

// Calculate volumes and percentages |

//------------------------------------------

calcVolumes(OHLCV ohlcv) =>

var VolumeData data = VolumeData.new()

data.buyVol := ohlcv.V * (ohlcv.C - ohlcv.L) / (ohlcv.H - ohlcv.L)

data.sellVol := ohlcv.V - data.buyVol

data.pcBuy := data.buyVol / ohlcv.V * 100

data.pcSell := 100 - data.pcBuy

data.isBuyGreater := data.buyVol > data.sellVol

data.higherVol := data.isBuyGreater ? data.buyVol : data.sellVol

data.lowerVol := data.isBuyGreater ? data.sellVol : data.buyVol

data.higherCol := data.isBuyGreater ? C_Up : C_Down

data.lowerCol := data.isBuyGreater ? C_Down : C_Up

data

//------------------------------------------

// Get volume data |

//------------------------------------------

ohlcv = OHLCV.new()

volData = calcVolumes(ohlcv)

// Plot volumes and create labels

plot(ohlcv.V, color=color.new(volData.higherCol, 90), style=plot.style_columns, title='Total',display = display.all - display.status_line)

plot(ohlcv.V, color=volData.higherCol, style=plot.style_stepline_diamond, title='Total2', linewidth = 2,display = display.pane)

plot(volData.higherVol, color=volData.higherCol, style=plot.style_columns, title='Higher Volume', display = display.all - display.status_line)

plot(volData.lowerVol , color=volData.lowerCol , style=plot.style_columns, title='Lower Volume',display = display.all - display.status_line)

S(D,F)=>str.tostring(D,F)

volStr = S(math.sign(ta.change(ohlcv.C)) * ohlcv.V, FV)

buyVolStr = S(volData.buyVol , FV )

sellVolStr = S(volData.sellVol , FV )

// ✅ MODIFICACIÓN: Porcentaje sin decimales

buyPercentStr = str.tostring(math.round(volData.pcBuy)) + " %"

sellPercentStr = str.tostring(math.round(volData.pcSell)) + " %"

totalbuyPercentC_ = volData.buyVol / (volData.buyVol + volData.sellVol) * 100

sup = not na(ohlcv.V)

if sup

TC = text.align_center

CW = color.white

var table tb = table.new(P_, 6, 6, bgcolor = na, frame_width = 2, frame_color = chart.fg_color, border_width = 1, border_color = CW)

tb.cell(0, 0, text = 'Volume Candles', text_color = #FFBF00, bgcolor = #0E2841, text_halign = TC, text_valign = TC, text_size = sT)

tb.merge_cells(0, 0, 5, 0)

tb.cell(0, 1, text = 'Current Volume', text_color = CW, bgcolor = #0B3040, text_halign = TC, text_valign = TC, text_size = sT)

tb.merge_cells(0, 1, 1, 1)

tb.cell(0, 2, text = 'Buy', text_color = #000000, bgcolor = #92D050, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(1, 2, text = 'Sell', text_color = #000000, bgcolor = #FF0000, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(0, 3, text = buyVolStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(1, 3, text = sellVolStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(0, 5, text = 'Net: ' + volStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.merge_cells(0, 5, 1, 5)

tb.cell(0, 4, text = buyPercentStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

tb.cell(1, 4, text = sellPercentStr, text_color = CW, bgcolor = #074F69, text_halign = TC, text_valign = TC, text_size = sT)

cellCount = 20

filledCells = 0

for r = 5 to 1 by 1

for c = 2 to 5 by 1

if filledCells < cellCount * (totalbuyPercentC_ / 100)

tb.cell(c, r, text = '', bgcolor = C_Up)

else

tb.cell(c, r, text = '', bgcolor = C_Down)

filledCells := filledCells + 1

filledCells

if Label

sp = ' '

l = label.new(bar_index, ohlcv.V,

text=str.format('Net: {0}\nBuy: {1} ({2})\nSell: {3} ({4})\n{5}/\\\n {5}l\n {5}l',

volStr, buyVolStr, buyPercentStr, sellVolStr, sellPercentStr, sp),

style=label.style_none, textcolor=volData.higherCol, size=sL, textalign=text.align_left)

if not History

(l ).delete()

//------------------------------------------

// Draw volume levels on the candlesticks |

//------------------------------------------

float base = na,float value = na

bool uc = usecandle and sup

if volData.isBuyGreater

base := math.min(ohlcv.O, ohlcv.C)

value := base + math.abs(ohlcv.O - ohlcv.C) * (volData.pcBuy / 100)

else

base := math.max(ohlcv.O, ohlcv.C)

value := base - math.abs(ohlcv.O - ohlcv.C) * (volData.pcSell / 100)

barcolor(sup ? color.new(na, na) : ohlcv.C < ohlcv.O ? color.red : color.green,display = usecandle? display.all:display.none)

UseC = uc ? volData.higherCol:color.new(na, na)

plotcandle(uc?base:na, uc?base:na, uc?value:na, uc?value:na,

title='Body', color=UseC, bordercolor=na, wickcolor=UseC,

display = usecandle ? display.all - display.status_line : display.none, force_overlay=true,editable=false)

plotcandle(uc?ohlcv.O:na, uc?ohlcv.H:na, uc?ohlcv.L:na, uc?ohlcv.C:na,

title='Fill', color=color.new(UseC,80), bordercolor=UseC, wickcolor=UseC,

display = usecandle ? display.all - display.status_line : display.none, force_overlay=true,editable=false)

//------------------------------------------------------------

// Plot the EMA and filter out the noise with volume control. |

//------------------------------------------------------------

float emaFast = ta.ema(ohlcv.C, emaFastLength)

float emaSlow = ta.ema(ohlcv.C, emaSlowLength)

bool signal = emaFast > emaSlow

color c_signal = signal ? C_Up : C_Down

float volumeMA = ta.sma(ohlcv.V, volumeConfirmationLength)

bool crossover = ta.crossover(emaFast, emaSlow)

bool crossunder = ta.crossunder(emaFast, emaSlow)

isVolumeConfirmed(source, length, ma) =>

math.sum(source > ma ? source : 0, length) >= math.sum(source < ma ? source : 0, length)

bool ISV = isVolumeConfirmed(ohlcv.V, volumeConfirmationLength, volumeMA)

bool crossoverConfirmed = crossover and (not useVolumeConfirmation or ISV)

bool crossunderConfirmed = crossunder and (not useVolumeConfirmation or ISV)

PF = MAV ? emaFast : na

PS = MAV ? emaSlow : na

p1 = plot(PF, color = c_signal, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 80), linewidth = 10, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 90), linewidth = 20, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 95), linewidth = 30, editable = false, force_overlay = true, display = display.pane)

plot(PF, color = color.new(c_signal, 98), linewidth = 45, editable = false, force_overlay = true, display = display.pane)

p2 = plot(PS, color = c_signal, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 80), linewidth = 10, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 90), linewidth = 20, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 95), linewidth = 30, editable = false, force_overlay = true, display = display.pane)

plot(PS, color = color.new(c_signal, 98), linewidth = 45, editable = false, force_overlay = true, display = display.pane)

fill(p1, p2, top_value=crossover ? emaFast : emaSlow,

bottom_value =crossover ? emaSlow : emaFast,

top_color =color.new(c_signal, 80),

bottom_color =color.new(c_signal, 95)

)

// ✅ Usar colores configurables para señales

plotshape(crossoverConfirmed and MAV, style=shape.triangleup , location=location.belowbar, color=buySignalColor , size=size.small, force_overlay=true,display =display.pane)

plotshape(crossunderConfirmed and MAV, style=shape.triangledown, location=location.abovebar, color=sellSignalColor, size=size.small, force_overlay=true,display =display.pane)

string msg = '---------\n'+"Buy volume ="+buyVolStr+"\nBuy Percent = "+buyPercentStr+"\nSell volume = "+sellVolStr+"\nSell Percent = "+sellPercentStr+"\nNet = "+volStr+'\n---------'

if crossoverConfirmed

alert("Price (" + str.tostring(close) + ") Crossed over MA\n" + msg, alert_freq)

if crossunderConfirmed

alert("Price (" + str.tostring(close) + ") Crossed under MA\n" + msg, alert_freq)

AMHA + 4 EMAs + EMA50/200 Counter + Avg10CrossesDescription:

This script combines two types of Heikin-Ashi visualization with multiple Exponential Moving Averages (EMAs) and a counting function for EMA50/200 crossovers. The goal is to make trends more visible, measure recurring market cycles, and provide statistical context without generating trading signals.

Logic in Detail:

Adaptive Median Heikin-Ashi (AMHA):

Instead of the classic Heikin-Ashi calculation, this method uses the median of Open, High, Low, and Close. The result smooths out price movements, emphasizes trend direction, and reduces market noise.

Standard Heikin-Ashi Overlay:

Classic HA candles are also drawn in the background for comparison and transparency. Both HA types can be shifted below the chart’s price action using a customizable Offset (Ticks) parameter.

EMA Structure:

Five exponential moving averages (21, 50, 100, 200, 500) are included to highlight different trend horizons. EMA50 and EMA200 are emphasized, as their crossovers are widely monitored as potential trend signals. EMA21 and EMA100 serve as additional structure layers, while EMA500 represents the long-term trend.

EMA50/200 Counter:

The script counts how many bars have passed since the last EMA50/200 crossover. This makes it easy to see the age of the current trend phase. A colored label above the chart displays the current counter.

Average of the Last 10 Crossovers (Avg10Crosses):

The script stores the last 10 completed count phases and calculates their average length. This provides historical context and allows traders to compare the current cycle against typical past behavior.

Benefits for Analysis:

Clearer trend visualization through adaptive Heikin-Ashi calculation.

Multi-EMA setup for quick structural assessment.

Objective measurement of trend phase duration.

Statistical insight from the average cycle length of past EMA50/200 crosses.

Flexible visualization through adjustable offset positioning below the price chart.

Usage:

Add the indicator to your chart.

For a clean look, you may switch your chart type to “Line” or hide standard candlesticks.

Interpret visual signals:

White candles = bullish phases

Orange candles = bearish phases

EMAs = structural trend filters (e.g., EMA200 as a long-term boundary)

The counter label shows the current number of bars since the last cross, while Avg10 represents the historical mean.

Special Feature:

This script is not a trading system. It does not provide buy/sell recommendations. Instead, it serves as a visual and statistical tool for market structure analysis. The unique combination of Adaptive Median Heikin-Ashi, multi-EMA framework, and EMA50/200 crossover statistics makes it especially useful for trend-followers and swing traders who want to add cycle-length analysis to their toolkit.

MA Pack + Cross Signals (Short vs Long)Overview

A flexible moving average pack that lets you switch between short-term trend detection and long-term trend confirmation .

Short-term mode: plots 5, 10, 20, and 50 MAs with early crossovers (10/50, 20/50).

Long-term mode: plots 50, 100, 200 MAs with Golden Cross and Death Cross signals.

Choice of SMA or EMA .

Alerts included for all crossovers.

Why Use It

Catch early trend shifts in short-term mode.

Confirm institutional trend levels in long-term mode.

Visual signals (triangles + labels) make spotting setups easy.

Alert-ready for automated trade monitoring.

Usage

Add to chart.

In settings, choose Short-term or Long-term .

Watch for markers:

Green triangles = bullish cross

Red triangles = bearish cross

Green label = Golden Cross

Red label = Death Cross

Optional: enable alerts for notifications.

Market Pressure Oscillator█ OVERVIEW

The Market Pressure Oscillator is an advanced technical indicator for TradingView, enabling traders to identify potential trend reversals and momentum shifts through candle-based pressure analysis and divergence detection. It combines a smoothed oscillator with moving average signals, overbought/oversold levels, and divergence visualization, enhanced by customizable gradients, dynamic band colors, and alerts for quick decision-making.

█ CONCEPT

The indicator measures buying or selling pressure based on candle body size (open-to-close difference) and direction, with optional smoothing for clarity and divergence detection between price action and the oscillator. It relies solely on candle data, offering insights into trend strength, overbought/oversold conditions, and potential reversals with a customizable visual presentation.

█ WHY USE IT?

- Divergence Detection: Identifies bullish and bearish divergences to reinforce signals, especially near overbought/oversold zones.

- Candle Pressure Analysis: Measures pressure based on candle body size, normalized to a ±100 scale.

- Signal Generation: Provides buy/sell signals via overbought/oversold crossovers, zero-line crossovers, moving average zero-line crossovers, and dynamic band color changes.

- Visual Clarity: Uses dynamic colors, gradients, and fill layers for intuitive chart analysis.

Flexibility: Extensive settings allow customization to individual trading preferences.

█ HOW IT WORKS?

- Candle Pressure Calculation: Computes candle body size as math.abs(close - open), normalized against the average body size over a lookback period (avgBody = ta.sma(body, len)). - Candle direction (bullish: +1, bearish: -1, neutral: 0) is multiplied by body weight to derive pressure.

- Cumulative Pressure: Sums pressure values over the lookback period (Lookback Length) and normalizes to ±100 relative to the maximum possible value.

- Smoothing: Optionally applies EMA (Smoothing Length) to normalized pressure.

- Moving Average: Calculates SMA (Moving Average Length) for trend confirmation (Moving Average (SMA)).

- Divergence Detection: Identifies bullish/bearish divergences by comparing price and oscillator pivot highs/lows within a specified range (Pivot Length). Divergence signals appear with a delay equal to the Pivot Length.

- Signals: Generates signals for:

Crossing oversold upward (buy) or overbought downward (sell).

Crossing the zero line by the oscillator or moving average (buy/sell).

Bullish/bearish divergences, marked with labels, enhancing signals, especially near overbought/oversold zones.

Dynamic band color changes when the moving average crosses MA overbought/oversold thresholds (green for oversold, red for overbought).

- Visualization: Plots the oscillator and moving average with dynamic colors, gradient fills, transparent bands, and labels, with customizable overbought/oversold levels.

Alerts: Built-in alerts for divergences, overbought/oversold crossovers, and zero-line crossovers (oscillator and moving average).

█ SETTINGS AND CUSTOMIZATION

- Lookback Length: Period for aggregating candle pressure (default: 14).

- Smoothing Length (EMA): EMA length for smoothing the oscillator (default: 1). Higher values smooth the signal but may reduce signal frequency; adjust overbought/oversold levels accordingly.

- Moving Average Length (SMA): SMA length for the moving average (default: 14, minval=1). Higher values make SMA a trend indicator, requiring adjusted MA overbought/oversold levels.

- Pivot Length (Left/Right): Candles for detecting pivot highs/lows in divergence calculations (default: 2, minval=1). Higher values reduce noise but add delay equal to the set value.

- Enable Divergence Detection: Enables divergence detection (default: true).

- Overbought/Oversold Levels: Thresholds for the oscillator (default: 30/-30) and moving average (default: 10/-10). For the moving average, no arrows appear; bands change color from gray to green (oversold) or red (overbought), reinforcing entry signals.

- Signal Type: Select signals to display: "None", "Overbought/Oversold", "Zero Line", "MA Zero Line", "All" (default: "Overbought/Oversold").

- Colors and Gradients: Customize colors for bullish/bearish oscillator, moving average, zero line, overbought/oversold levels, and divergence labels.

- Transparency: Adjust gradient fill transparency (default: 70, minval=0, maxval=100) and band/label transparency (default: 40, minval=0, maxval=100) for consistent visuals.

- Visualizations: Enable/disable moving average, gradients for zero/overbought/oversold levels, and gradient fills.

█ USAGE EXAMPLES

- Momentum Analysis: Observe the MPO Oscillator above 0 for bullish momentum or below 0 for bearish momentum. The SMA, being smoother, reacts slower and can confirm trend direction as a noise filter.

- Reversal Signals: Look for buy triangles when the oscillator crosses oversold upward, especially when the SMA is below the MA oversold threshold and the band turns green. Similarly, seek sell triangles when crossing overbought downward, with the SMA above the MA overbought threshold and the band turning red.

- Using Divergences: Treat bullish (green labels) and bearish (red labels) divergences as reinforcement for other signals, especially near overbought/oversold zones, indicating stronger potential trend reversals.

- Customization: Adjust lookback length, smoothing, and moving average length to specific instruments and timeframes to minimize false signals.

█ USER NOTES

Combine the indicator with tools like Fibonacci levels or pivot points to enhance accuracy.

Test different settings for lookback length, smoothing, and moving average length on your chosen instrument and timeframe to find optimal values.

TA█ TA Library

📊 OVERVIEW

TA is a Pine Script technical analysis library. This library provides 25+ moving averages and smoothing filters , from classic SMA/EMA to Kalman Filters and adaptive algorithms, implemented based on academic research.

🎯 Core Features

Academic Based - Algorithms follow original papers and formulas

Performance Optimized - Pre-calculated constants for faster response

Unified Interface - Consistent function design

Research Based - Integrates technical analysis research

🎯 CONCEPTS

Library Design Philosophy

This technical analysis library focuses on providing:

Academic Foundation

Algorithms based on published research papers and academic standards

Implementations that follow original mathematical formulations

Clear documentation with research references

Developer Experience

Unified interface design for consistent usage patterns

Pre-calculated constants for optimal performance

Comprehensive function collection to reduce development time

Single import statement for immediate access to all functions

Each indicator encapsulated as a simple function call - one line of code simplifies complexity

Technical Excellence

25+ carefully implemented moving averages and filters

Support for advanced algorithms like Kalman Filter and MAMA/FAMA

Optimized code structure for maintainability and reliability

Regular updates incorporating latest research developments

🚀 USING THIS LIBRARY

Import Library

//@version=6

import DCAUT/TA/1 as dta

indicator("Advanced Technical Analysis", overlay=true)

Basic Usage Example

// Classic moving average combination

ema20 = ta.ema(close, 20)

kama20 = dta.kama(close, 20)

plot(ema20, "EMA20", color.red, 2)

plot(kama20, "KAMA20", color.green, 2)

Advanced Trading System

// Adaptive moving average system

kama = dta.kama(close, 20, 2, 30)

= dta.mamaFama(close, 0.5, 0.05)

// Trend confirmation and entry signals

bullTrend = kama > kama and mamaValue > famaValue

bearTrend = kama < kama and mamaValue < famaValue

longSignal = ta.crossover(close, kama) and bullTrend

shortSignal = ta.crossunder(close, kama) and bearTrend

plot(kama, "KAMA", color.blue, 3)

plot(mamaValue, "MAMA", color.orange, 2)

plot(famaValue, "FAMA", color.purple, 2)

plotshape(longSignal, "Buy", shape.triangleup, location.belowbar, color.green)

plotshape(shortSignal, "Sell", shape.triangledown, location.abovebar, color.red)

📋 FUNCTIONS REFERENCE

ewma(source, alpha)

Calculates the Exponentially Weighted Moving Average with dynamic alpha parameter.

Parameters:

source (series float) : Series of values to process.

alpha (series float) : The smoothing parameter of the filter.

Returns: (float) The exponentially weighted moving average value.

dema(source, length)

Calculates the Double Exponential Moving Average (DEMA) of a given data series.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Double Exponential Moving Average value.

tema(source, length)

Calculates the Triple Exponential Moving Average (TEMA) of a given data series.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Triple Exponential Moving Average value.

zlema(source, length)

Calculates the Zero-Lag Exponential Moving Average (ZLEMA) of a given data series. This indicator attempts to eliminate the lag inherent in all moving averages.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Zero-Lag Exponential Moving Average value.

tma(source, length)

Calculates the Triangular Moving Average (TMA) of a given data series. TMA is a double-smoothed simple moving average that reduces noise.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Triangular Moving Average value.

frama(source, length)

Calculates the Fractal Adaptive Moving Average (FRAMA) of a given data series. FRAMA adapts its smoothing factor based on fractal geometry to reduce lag. Developed by John Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Fractal Adaptive Moving Average value.

kama(source, length, fastLength, slowLength)

Calculates Kaufman's Adaptive Moving Average (KAMA) of a given data series. KAMA adjusts its smoothing based on market efficiency ratio. Developed by Perry J. Kaufman.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the efficiency calculation.

fastLength (simple int) : Fast EMA length for smoothing calculation. Optional. Default is 2.

slowLength (simple int) : Slow EMA length for smoothing calculation. Optional. Default is 30.

Returns: (float) The calculated Kaufman's Adaptive Moving Average value.

t3(source, length, volumeFactor)

Calculates the Tilson Moving Average (T3) of a given data series. T3 is a triple-smoothed exponential moving average with improved lag characteristics. Developed by Tim Tillson.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

volumeFactor (simple float) : Volume factor affecting responsiveness. Optional. Default is 0.7.

Returns: (float) The calculated Tilson Moving Average value.

ultimateSmoother(source, length)

Calculates the Ultimate Smoother of a given data series. Uses advanced filtering techniques to reduce noise while maintaining responsiveness. Based on digital signal processing principles by John Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the smoothing calculation.

Returns: (float) The calculated Ultimate Smoother value.

kalmanFilter(source, processNoise, measurementNoise)

Calculates the Kalman Filter of a given data series. Optimal estimation algorithm that estimates true value from noisy observations. Based on the Kalman Filter algorithm developed by Rudolf Kalman (1960).

Parameters:

source (series float) : Series of values to process.

processNoise (simple float) : Process noise variance (Q). Controls adaptation speed. Optional. Default is 0.05.

measurementNoise (simple float) : Measurement noise variance (R). Controls smoothing. Optional. Default is 1.0.

Returns: (float) The calculated Kalman Filter value.

mcginleyDynamic(source, length)

Calculates the McGinley Dynamic of a given data series. McGinley Dynamic is an adaptive moving average that adjusts to market speed changes. Developed by John R. McGinley Jr.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the dynamic calculation.

Returns: (float) The calculated McGinley Dynamic value.

mama(source, fastLimit, slowLimit)

Calculates the Mesa Adaptive Moving Average (MAMA) of a given data series. MAMA uses Hilbert Transform Discriminator to adapt to market cycles dynamically. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

fastLimit (simple float) : Maximum alpha (responsiveness). Optional. Default is 0.5.

slowLimit (simple float) : Minimum alpha (smoothing). Optional. Default is 0.05.

Returns: (float) The calculated Mesa Adaptive Moving Average value.

fama(source, fastLimit, slowLimit)

Calculates the Following Adaptive Moving Average (FAMA) of a given data series. FAMA follows MAMA with reduced responsiveness for crossover signals. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

fastLimit (simple float) : Maximum alpha (responsiveness). Optional. Default is 0.5.

slowLimit (simple float) : Minimum alpha (smoothing). Optional. Default is 0.05.

Returns: (float) The calculated Following Adaptive Moving Average value.

mamaFama(source, fastLimit, slowLimit)

Calculates Mesa Adaptive Moving Average (MAMA) and Following Adaptive Moving Average (FAMA).

Parameters:

source (series float) : Series of values to process.

fastLimit (simple float) : Maximum alpha (responsiveness). Optional. Default is 0.5.

slowLimit (simple float) : Minimum alpha (smoothing). Optional. Default is 0.05.

Returns: ( ) Tuple containing values.

laguerreFilter(source, length, gamma, order)

Calculates the standard N-order Laguerre Filter of a given data series. Standard Laguerre Filter uses uniform weighting across all polynomial terms. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Length for UltimateSmoother preprocessing.

gamma (simple float) : Feedback coefficient (0-1). Lower values reduce lag. Optional. Default is 0.8.

order (simple int) : The order of the Laguerre filter (1-10). Higher order increases lag. Optional. Default is 8.

Returns: (float) The calculated standard Laguerre Filter value.

laguerreBinomialFilter(source, length, gamma)

Calculates the Laguerre Binomial Filter of a given data series. Uses 6-pole feedback with binomial weighting coefficients. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Length for UltimateSmoother preprocessing.

gamma (simple float) : Feedback coefficient (0-1). Lower values reduce lag. Optional. Default is 0.5.

Returns: (float) The calculated Laguerre Binomial Filter value.

superSmoother(source, length)

Calculates the Super Smoother of a given data series. SuperSmoother is a second-order Butterworth filter from aerospace technology. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Period for the filter calculation.

Returns: (float) The calculated Super Smoother value.

rangeFilter(source, length, multiplier)

Calculates the Range Filter of a given data series. Range Filter reduces noise by filtering price movements within a dynamic range.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the average range calculation.

multiplier (simple float) : Multiplier for the smooth range. Higher values increase filtering. Optional. Default is 2.618.