Portfolio Backtester Engine█ OVERVIEW

Portfolio Backtester Engine (PBTE). This tool will allow you to backtest strategies across multiple securities at once. Allowing you to easier understand if your strategy is robust. If you are familiar with the PineCoders backtesting engine , then you will find this indicator pleasant to work with as it is an adaptation based on that work. Much of the functionality has been kept the same, or enhanced, with some minor adjustments I made on the account of creating a more subjectively intuitive tool.

█ HISTORY

The original purpose of the backtesting engine (`BTE`) was to bridge the gap between strategies and studies . Previously, strategies did not contain the ability to send alerts, but were necessary for backtesting. Studies on the other hand were necessary for sending alerts, but could not provide backtesting results . Often, traders would have to manage two separate Pine scripts to take advantage of each feature, this was less than ideal.

The `BTE` published by PineCoders offered a solution to this issue by generating backtesting results under the context of a study(). This allowed traders to backtest their strategy and simultaneously generate alerts for automated trading, thus eliminating the need for a separate strategy() script (though, even converting the engine to a strategy was made simple by the PineCoders!).

Fast forward a couple years and PineScript evolved beyond these issues and alerts were introduced into strategies. The BTE was not quite as necessary anymore, but is still extremely useful as it contains extra features and data not found under the strategy() context. Below is an excerpt of features contained by the BTE:

"""

More than `40` built-in strategies,

Customizable components,

Coupling with your own external indicator,

Simple conversion from Study to Strategy modes,

Post-Exit analysis to search for alternate trade outcomes,

Use of the Data Window to show detailed bar by bar trade information and global statistics, including some not provided by TV backtesting,

Plotting of reminders and generation of alerts on in-trade events.

"""

Before I go any further, I want to be clear that the BTE is STILL a good tool and it is STILL very useful. The Portfolio Backtesting Engine I am introducing is only a tangental advancement and not to be confused as a replacement, this tool would not have been possible without the `BTE`.

█ THE PROBLEM

Most strategies built in Pine are limited by one thing. Data. Backtesting should be a rigorous process and researchers should examine the performance of their strategy across all market regimes; that includes, bullish and bearish markets, ranging markets, low volatility and high volatility. Depending on your TV subscription The Pine Engine is limited to 5k-20k historical bars available for backtesting, which can often leave the strategy results wanting. As a general rule of thumb, strategies should be tested across a quantity of historical bars which will allow for at least 100 trades. In many cases, the lack of historical bars available for backtesting and frequency of the strategy signals produces less than 100 trades, rendering your strategy results inconclusive.

█ THE SOLUTION

In order to be confident that we have a robust strategy we must test it across all market regimes and we must have over 100 trades. To do this effectively, researchers can use the Portfolio Backtesting Engine (PBTE).

By testing a strategy across a carefully selected portfolio of securities, researchers can now gather 5k-20k historical bars per security! Currently, the PTBE allows up to 5 securities, which amounts to 25k-100k historical bars.

█ HOW TO USE

1 — Add the indicator to your chart.

• Confirm inputs. These will be the most important initial values which you can change later by clicking the gear icon ⚙ and opening up the settings of the indicator.

2 — Select a portfolio.

• You will want to spend some time carefully selecting a portfolio of securities.

• Each security should be uncorrelated.

• The entire portfolio should contain a mix of different market regimes.

You should understand that strategies generally take advantage of one particular type of market regime. (trending, ranging, low/high volatility)

For example, the default RSI strategy is typically advantageous during ranging markets, whereas a typical moving average crossover strategy is advantageous in trending markets.

If you were to use the standard RSI strategy during a trending market, you might be selling when you should be buying.

Similarily, if you use an SMA crossover during a ranging market, you will find that the MA's may produce many false signals.

Even if you build a strategy that is designed to be used only in a trending market, it is still best to select a portfolio of all market regimes

as you will be able to test how your strategy will perform when the market does something unexpected.

3 — Test a built-in strategy or add your own.

• Navigate to gear icon ⚙ (settings) of strategy.

• Choose your options.

• Select a Main Entry Strat and Alternate Entry Strat .

• If you want to add your own strategy, you will need to modify the source code and follow the built-in example.

• You will only need to generate (buy 1 / sell -1/ neutral 0) signals.

• Select a Filter , by default these are all off.

• Select an Entry Stop - This will be your stop loss placed at the trade entry.

• Select Pyamiding - This will allow you to stack positions. By default this is off.

• Select Hard Exits - You can also think of these as Take Profits.

• Let the strategy run and take note of the display tables results.

• Portfolio - Shows each security.

• The strategy runs on each asset in your portfolio.

• The initial capital is equally distributed across each security.

So if you have 5 securities and a starting capital of 100,000$ then each security will run the strategy starting with 20,000$

The total row will aggregate the results on a bar by bar basis showing the total results of your initial capital.

• Net Profit (NP) - Shows profitability.

• Number of Trades (#T) - Shows # of trades taken during backtesting period.

• Typically will want to see this number greater than 100 on the "Total" row.

• Average Trade Length (ATL) - Shows average # of days in a trade.

• Maximum Drawdown (MD ) - Max peak-to-valley equity drawdown during backtesting period.

• This number defines the minimum amount of capital required to trade the system.

• Typically, this shouldn’t be lower than 34% and we will want to allow for at least 50% beyond this number.

• Maximum Loss (ML) - Shows largest loss experienced on a per-trade basis.

• Normally, don’t want to exceed more than 1-2 % of equity.

• Maximum Drawdown Duration (MDD) - The longest duration of a drawdown in equity prior to a new equity peak.

• This number is important to help us psychologically understand how long we can expect to wait for a new peak in account equity.

• Maximum Consecutive Losses (MCL) - The max consecutive losses endured throughout the backtesting period.

• Another important metric for trader psychology, this will help you understand how many losses you should be prepared to handle.

• Profit to Maximum Drawdown (P:MD) - A ratio for the average profit to the maximum drawdown.

• The higher the ratio is, the better. Large profits and small losses contribute to a good PMD.

• This metric allows us to examine the profit with respect to risk.

• Profit Loss Ratio (P:L) - Average profit over the average loss.

• Typically this number should be higher in trend following systems.

• Mean reversion systems show lower values, but compensate with a better win %.

• Percent Winners (% W) - The percentage of winning trades.

• Trend systems will usually have lower win percentages, since statistically the market is only trending roughly 30% of the time.

• Mean reversion systems typically should have a high % W.

• Time Percentage (Time %) - The amount of time that the system has an open position.

• The more time you are in the market, the more you are exposed to market risk, not to mention you could be using that money for something else right?

• Return on Investment (ROI) - Your Net Profit over your initial investment, represented as a percentage.

• You want this number to be positive and high.

• Open Profit (OP) - If the strategy has any open positions, the floating value will be represented here.

• Trading Days (TD) - An important metric showing how many days the strategy was active.

• This is good to know and will be valuable in understanding how long you will need to run this strategy in order to achieve results.

█ FEATURES

These are additional features that extend the original `BTE` features.

- Portfolio backtesting.

- Color coded performance results.

- Circuit Breakers that will stop trading.

- Position reversals on exit. (Simulating the function of always in the market. Similar to strategy.entry functionality)

- Whipsaw Filter

- Moving Average Filter

- Minimum Change Filter

- % Gain Equity Exit

- Popular strategies, (MACD, MA cross, supertrend)

Below are features that were excluded from the original `BTE`

- 2 stage in-trade stops with kick-in rules (This was a subjective decision to remove. I found it to be complex and thwarted my use of the `BTE` for some time.)

- Simple conversion from Study to Strategy modes. (Not possible with multiple securities)

- Coupling with your own external indicator (Not really practical to use with multiple securities, but could be used if signals were generated based on some indicator which was not based on the current chart)

- Use of the Data Window to show detailed bar by bar trade information and global statistics.

- Post Exit Analysis.

- Plotting of reminders and generation of alerts on in-trade events.

- Alerts (These may be added in the future by request when I find the time.)

█ THANKS

The whole PineCoders team for all their shared knowledge and original publication of the BTE and Richard Weismann for his ideas on building robust strategies.

═════════════════════════════════════════════════════════════════════════

Cari dalam skrip untuk "backtesting"

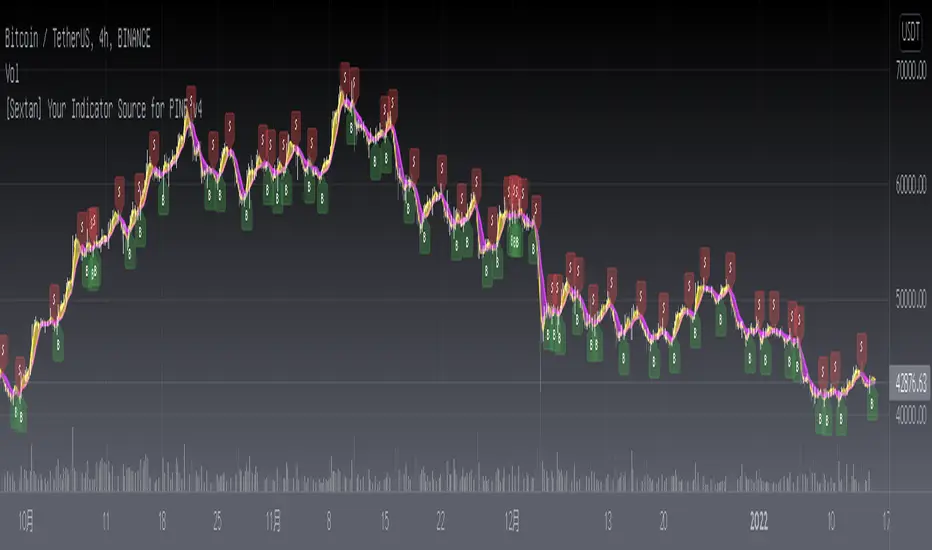

[Sextan] Your Indicator SourceLevel: 1

NOTE: This is ONLY an EXAMPLE on HOW-TO produce a customized "{Sextan} PINEv4 Sextans Backtest Framework" intput signal source, you can define your own indicator in the highlighted area in compliance with the uniform format, which guarantee when you use "Indicator on Indicator" function, it would not produce any error.

I use two simple moving average crossings to produce long and short entry signal with SMA3 and SMA8 in the example.

Background

Backtesting of technical indicators and strategies is the most common way to understand a quantitative strategy. However, the complicated configuration and adaptation work of backtesting many quantitative tools makes many traders who do not understand the code daunted. Moreover, although I have written a lot of strategies, I am still not very satisfied with the backtest configuration and writing efficiency. Therefore, I have been thinking about how to build a backtesting framework that can quickly and easily evaluate the backtesting performance of any indicator with a "long/short entry" indicator, that is, a "simple backtesting tool for dummies". The performance requirements should be stable, and the operation should be simple and convenient. It is best to "copy", "paste", and "a few mouse clicks" to complete the quick backtest and evaluation of a new indicator.

Luckily, I recently realized that TradingView provides an "Indicator on Indicator" feature, which is the perfect foundation for doing "hot swap" backtesting. My basic idea is to use a two-layer design. The first layer is the technical indicator signal source that needs to be embedded, which is only used to provide buy and sell signals of custom strategies; the second layer is the trading system, which is used to receive the output signals of the first layer, and filter the signals according to the agreed specifications. , Take Profit, Stop Loss, draw buy and sell signals and cost lines, define and send custom buy and sell alert messages to mobile phones, social software or trading interfaces. In general, this two-layer design is a flexible combination of "death and alive", which can meet the needs of most traders to quickly evaluate the performance of a certain technical indicator. The first layer here is flexible. Users can insert their own strategy codes according to my template, and they can draw buy and sell signals and output them to the second layer. The second layer is fixed, and the overall framework is solidified to ensure the stability and unity of the trading system. It is convenient to compare different or similar strategies under the same conditions. Finally, all trading signals are drawn on the chart, and the output strategy returns. test report.

The main function:

The first layer: "{Sextan} Your Indicator Source", the script provides a template for personalized strategy input, and the signal and definition interfaces ensure full compatibility with the second layer. Backtesting is performed stably in the backtesting framework of the layer. The first layer of this script is also relatively simple: enter your script in the highlighted custom script area, and after ensuring the final buy and sell signals long = bool condition, short = bool condition, the design of the first layer is considered complete. Input it into the PINE script editor of TradingView, save it and add it to the chart, you can see the pulse sequence in yellow (buy) and purple (sell) on the sub-picture, corresponding to the main picture, you can subjectively judge that the quality of the trading point of the strategy is good Bad.

The second layer: "{Sextan} PINEv4 Sextans Backtest Framework". This script is the standardized trading system strategy execution and alarm, used to generate the final report of the strategy backtest and some key indicators that I have customized that I find useful, such as: winning rate , Odds, Winning Surface, Kelly Ratio, Take Profit and Stop Loss Thresholds, Trading Frequency, etc. are evaluated according to the Kelly formula. To use the second layer, first load it into the TrainingView chart, no markers will appear on the chart, since you have not specified any strategy source signals, click on the gear-shaped setting next to the "{Sextan} PINEv4 Sextans BTFW" header button, you can open the backtest settings, the first item is to select your custom strategy source. Because we have added the strategy source to the chart in the previous step, you can easily find an option "{Sextan} Your Indicator Source: Signal" at the bottom of the list, this is the strategy source input we need, select and confirm , you can see various markers on the main graph, and quickly generate a backtesting profit graph and a list of backtesting reports. You can generate files and download the backtesting reports locally. You can also click the gear on the backtest chart interface to customize some conditions of the backtest, including: initial capital amount, currency type, percentage of each order placed, amount of pyramid additions, commission fees, slippage, etc. configuration. Note: The configuration in the interface dialog overrides the same configuration implemented by the code in the backtest script.

How to output charts:

The first layer: "{Sextan} Your Indicator Source", the output of this script is the pulse value of yellow and purple, yellow +1 means buy, purple -1 means sell.

The second layer: PINEv4 Sextans Backtest Framework". The output of this script is a bit complicated. After all, it is the entire trading system with a lot of information:

1. Blue and red arrows. The blue upward arrow indicates long position, the red downward arrow indicates short position, and the horizontal bar at the end of the purple arrow indicates take profit or stop loss exit.

2. Red and green lines. This is the holding cost line of the strategy, green represents the cost of holding a long position, and red represents the cost of holding a short position. The cost line is a continuous solid line and the price action is relatively close.

3. Green and yellow long take profit and stop loss area and green and yellow long take profit and stop loss fork. Once a long position is held, there is a conditional order for take profit and stop loss. The green horizontal line is the long take profit ratio line, and the yellow is the long stop loss ratio line; the green cross indicates the long take profit price, and the yellow cross indicates the long position. Stop loss price. It's worth noting that the prongs and wires don't necessarily go together. Because of the optimization of the algorithm, for a strong market, the take profit will occur after breaking the take profit line, and the profit will not be taken until the price falls.

4. The purple and red short take profit and stop loss area and the purple red short stop loss fork. Once a short position is held, there will be a take profit and stop loss conditional order, the red is the short take profit ratio line, and the purple is the short stop loss ratio line; the red cross indicates the short take profit price, and the purple cross indicates the short stop loss price.

5. In addition to the above signs, there are also text and numbers indicating the profit and loss values of long and short positions. "L" means long; "S" means short; "XL" means close long; "XS" means close short.

TradingView Strategy Tester Panel:

The overview graph is an intuitive graph that plots the blue (gain) and red (loss) curves of all backtest periods together, and notes: the absolute value and percentage of net profit, the number of all closed positions, the winning percentage, the profit factor, The maximum trading loss, the absolute value and ratio of the average trading profit and loss, and the average number of K-lines held in all trades.

Another is the performance summary. This is to display all long and short statistical indicators of backtesting in the form of a list, such as: net profit, gross profit, Sharpe ratio, maximum position, commission, times of profit and loss, etc.

Finally, the transaction list is a table indexed by the transaction serial number, showing the signal direction, date and time, price, profit and loss, accumulated profit and loss, maximum transaction profit, transaction loss and other values.

Remarks

Finally, I will explain that this is just the beginning of this model. I will continue to optimize the trading system of the second layer. Various optimization feedback and suggestions are welcome. For valuable feedback, I am willing to provide some L4/L5 technical indicators as rewards for free subscription rights.

BullBear with Volume-Percentile TP - Strategy [presentTrading] Happy New Year, everyone! I hope we have a fantastic year ahead.

It's been a while since I published an open script, but it's time to return.

This strategy introduces an indicator called Bull Bear Power, combined with an advanced take-profit system, which is the main innovative and educational aspect of this script. I hope all of you find some useful insights here. Welcome to engage in meaningful exchanges. This is a versatile tool suitable for both novice and experienced traders.

█ Introduction and How it is Different

Unlike traditional strategies that rely solely on price or volume indicators, this approach combines Bull Bear Power (BBP) with volume percentile analysis to identify optimal entry and exit points. It features a dynamic take-profit mechanism based on ATR (Average True Range) multipliers adjusted by volume and percentile factors, ensuring adaptability to diverse market conditions. This multifaceted strategy not only improves signal accuracy but also optimizes risk management, distinguishing it from conventional trading methods.

BTCUSD 6hr performance

Disable the visualization of Bull Bear Power (BBP) to clearly view the Z-Score.

█ Strategy, How it Works: Detailed Explanation

The BBP Strategy with Volume-Percentile TP utilizes several interconnected components to analyze market data and generate trading signals. Here's an overview with essential equations:

🔶 Core Indicators and Calculations

1. Exponential Moving Average (EMA):

- **Purpose:** Smoothens price data to identify trends.

- **Formula:**

EMA_t = (Close_t * (2 / (lengthInput + 1))) + (EMA_(t-1) * (1 - (2 / (lengthInput + 1))))

- Usage: Baseline for Bull and Bear Power.

2. Bull and Bear Power:

- Bull Power: `BullPower = High_t - EMA_t`

- Bear Power: `BearPower = Low_t - EMA_t`

- BBP:** `BBP = BullPower + BearPower`

- Interpretation: Positive BBP indicates bullish strength, negative indicates bearish.

3. Z-Score Calculation:

- Purpose: Normalizes BBP to assess deviation from the mean.

- Formula:

Z-Score = (BBP_t - bbp_mean) / bbp_std

- Components:

- `bbp_mean` = SMA of BBP over `zLength` periods.

- `bbp_std` = Standard deviation of BBP over `zLength` periods.

- Usage: Identifies overbought or oversold conditions based on thresholds.

🔶 Volume Analysis

1. Volume Moving Average (`vol_sma`):

vol_sma = (Volume_1 + Volume_2 + ... + Volume_vol_period) / vol_period

2. Volume Multiplier (`vol_mult`):

vol_mult = Current Volume / vol_sma

- Thresholds:

- High Volume: `vol_mult > 2.0`

- Medium Volume: `1.5 < vol_mult ≤ 2.0`

- Low Volume: `1.0 < vol_mult ≤ 1.5`

🔶 Percentile Analysis

1. Percentile Calculation (`calcPercentile`):

Percentile = (Number of values ≤ Current Value / perc_period) * 100

2. Thresholds:

- High Percentile: >90%

- Medium Percentile: >80%

- Low Percentile: >70%

🔶 Dynamic Take-Profit Mechanism

1. ATR-Based Targets:

TP1 Price = Entry Price ± (ATR * atrMult1 * TP_Factor)

TP2 Price = Entry Price ± (ATR * atrMult2 * TP_Factor)

TP3 Price = Entry Price ± (ATR * atrMult3 * TP_Factor)

- ATR Calculation:

ATR_t = (True Range_1 + True Range_2 + ... + True Range_baseAtrLength) / baseAtrLength

2. Adjustment Factors:

TP_Factor = (vol_score + price_score) / 2

- **vol_score** and **price_score** are based on current volume and price percentiles.

Local performance

🔶 Entry and Exit Logic

1. Long Entry: If Z-Score crosses above 1.618, then Enter Long.

2. Short Entry: If Z-Score crosses below -1.618, then Enter Short.

3. Exiting Positions:

If Long and Z-Score crosses below 0:

Exit Long

If Short and Z-Score crosses above 0:

Exit Short

4. Take-Profit Execution:

- Set multiple exit orders at dynamically calculated TP levels based on ATR and adjusted by `TP_Factor`.

█ Trade Direction

The strategy determines trade direction using the Z-Score from the BBP indicator:

- Long Positions:

- Condition: Z-Score crosses above 1.618.

- Short Positions:

- Condition: Z-Score crosses below -1.618.

- Exiting Trades:

- Long Exit: Z-Score drops below 0.

- Short Exit: Z-Score rises above 0.

This approach aligns trades with prevailing market trends, increasing the likelihood of successful outcomes.

█ Usage

Implementing the BBP Strategy with Volume-Percentile TP in TradingView involves:

1. Adding the Strategy:

- Copy the Pine Script code.

- Paste it into TradingView's Pine Editor.

- Save and apply the strategy to your chart.

2. Configuring Settings:

- Adjust parameters like EMA length, Z-Score thresholds, ATR multipliers, volume periods, and percentile settings to match your trading preferences and asset behavior.

3. Backtesting:

- Use TradingView’s backtesting tools to evaluate historical performance.

- Analyze metrics such as profit factor, drawdown, and win rate.

4. Optimization:

- Fine-tune parameters based on backtesting results.

- Test across different assets and timeframes to enhance adaptability.

5. Deployment:

- Apply the strategy in a live trading environment.

- Continuously monitor and adjust settings as market conditions change.

█ Default Settings

The BBP Strategy with Volume-Percentile TP includes default parameters designed for balanced performance across various markets. Understanding these settings and their impact is essential for optimizing strategy performance:

Bull Bear Power Settings:

- EMA Length (`lengthInput`): 21

- **Effect:** Balances sensitivity and trend identification; shorter lengths respond quicker but may generate false signals.

- Z-Score Length (`zLength`): 252

- **Effect:** Long period for stable mean and standard deviation, reducing false signals but less responsive to recent changes.

- Z-Score Threshold (`zThreshold`): 1.618

- **Effect:** Higher threshold filters out weaker signals, focusing on significant market moves.

Take Profit Settings:

- Use Take Profit (`useTP`): Enabled (`true`)

- **Effect:** Activates dynamic profit-taking, enhancing profitability and risk management.

- ATR Period (`baseAtrLength`): 20

- **Effect:** Shorter period for sensitive volatility measurement, allowing tighter profit targets.

- ATR Multipliers:

- **Effect:** Define conservative to aggressive profit targets based on volatility.

- Position Sizes:

- **Effect:** Diversifies profit-taking across multiple levels, balancing risk and reward.

Volume Analysis Settings:

- Volume MA Period (`vol_period`): 100

- **Effect:** Longer period for stable volume average, reducing the impact of short-term spikes.

- Volume Multipliers:

- **Effect:** Determines volume conditions affecting take-profit adjustments.

- Volume Factors:

- **Effect:** Adjusts ATR multipliers based on volume strength.

Percentile Analysis Settings:

- Percentile Period (`perc_period`): 100

- **Effect:** Balances historical context with responsiveness to recent data.

- Percentile Thresholds:

- **Effect:** Defines price and volume percentile levels influencing take-profit adjustments.

- Percentile Factors:

- **Effect:** Modulates ATR multipliers based on price percentile strength.

Impact on Performance:

- EMA Length: Shorter EMAs increase sensitivity but may cause more false signals; longer EMAs provide stability but react slower to market changes.

- Z-Score Parameters:*Longer Z-Score periods create more stable signals, while higher thresholds reduce trade frequency but increase signal reliability.

- ATR Multipliers and Position Sizes: Higher multipliers allow for larger profit targets with increased risk, while diversified position sizes help in securing profits at multiple levels.

- Volume and Percentile Settings: These adjustments ensure that take-profit targets adapt to current market conditions, enhancing flexibility and performance across different volatility environments.

- Commission and Slippage: Accurate settings prevent overestimation of profitability and ensure the strategy remains viable after accounting for trading costs.

Conclusion

The BBP Strategy with Volume-Percentile TP offers a robust framework by combining BBP indicators with volume and percentile analyses. Its dynamic take-profit mechanism, tailored through ATR adjustments, ensures that traders can effectively capture profits while managing risks in varying market conditions.

Bollinger Pair TradeNYSE:MA-1.6*NYSE:V

Revision: 1

Author: @ozdemirtrading

Revision 2 Considerations :

- Simplify and clean up plotting

Disclaimer: This strategy is currently working on the 5M chart. Change the length input to accommodate your needs.

For the backtesting of more than 3 months, you may need to upgrade your membership.

Description:

The general idea of the strategy is very straightforward: it takes positions according to the lower and upper Bollinger bands.

But I am mainly using this strategy for pair trading stocks. Do not forget that you will get better results if you trade with cointegrated pairs.

Bollinger band: Moving average & standard deviation are calculated based on 20 bars on the 1H chart (approx 240 bars on a 5m chart). X-day moving averages (20 days as default) are also used in the background in some of the exit strategy choices.

You can define position entry levels as the multipliers of standard deviation (for exp: mult2 as 2 * standard deviation).

There are 4 choices for the exit strategy:

SMA: Exit when touches simple moving average (SMA)

SKP: Skip SMA and do not stop if moving towards 20D SMA, and exit if it touches the other side of the band

SKPXDSMA: Skip SMA if moving towards 20D SMA, and exit if it touches 20D SMA

NoExit: Exit if it touches the upper & lower band only.

Options:

- Strategy hard stop: if trade loss reaches a point defined as a percent of the initial capital. Stop taking new positions. (not recommended for pair trade)

- Loss per trade: close position if the loss is at a defined level but keeps watching for new positions.

- Enable expected profit for trade (expected profit is calculated as the distance to SMA) (recommended for pair trade)

- Enable VIX threshold for the following options: (recommended for volatile periods)

- Stop trading if VIX for the previous day closes above the threshold

- Reverse active trade direction if VIX for the previous day is above the threshold

- Take reverse positions (assuming the Bollinger band is going to expand) for all trades

Backtesting:

Close positions after a defined interval: mark this if you want the close the final trade for backtesting purposes. Unmark it to get live signals.

Use custom interval: Backtest specific time periods.

Other Options:

- Use EMA: use an exponential moving average for the calculations instead of simple moving average

- Not against XDSMA: do not take a position against 20D SMA (if X is selected as 20) (recommended for pairs with a clear trend)

- Not in XDSMA 1 DEV: do not take a position in 20D SMA 1*standart deviation band (recommended if you need to decrease # of trades and increase profit for trade)

- Not in XDSMA 2 DEV: do not take a position in 20D SMA 2*standart deviation band

Session management:

- Not in session: Session start and end times can be defined here. If you do not want to trade in certain time intervals, mark that session.(helps to reduce slippage and get more realistic backtest results)

High/Low of week: Stats & Day of Week tendencies// Purpose:

-To show High of Week (HoW) day and Low of week (LoW) day frequencies/percentages for an asset.

-To further analyze Day of Week (DoW) tendencies based on averaged data from all various custom weeks. Giving a more reliable measure of DoW tendencies ('Meta Averages').

-To backtest day-of-week tendencies: across all asset history or across custom user input periods (i.e. consolidation vs trending periods).

-Education: to see how how data from a 'hard-defined-week' may be misleading when seeking statistical evidence of DoW tendencies.

// Notes & Tips:

-Only designed for use on DAILY timeframe.

-Verification table is to make sure HoW / LoW DAY (referencing previous finished week) is printing correctly and therefore the stats table is populating correctly.

-Generally, leaving Timezone input set to "America/New_York" is best, regardless of your asset or your chart timezone. But if misaligned by 1 day =>> tweak this timezone input to correct

-If you want to use manual backtesting period (e.g. for testing consolidation periods vs trending periods): toggle these settings on, then click the indicator display line three dots >> 'Reset Points' to quickly set start & end dates.

// On custom week start days:

-For assets like BTC which trade 7 days a week, this is quite simple. Pick custom start day, use verification table to check all is well. See the start week day & time in said verification table.

-For traditional assets like S&P which trade only 5 days a week and suffer from occasional Holidays, this is a bit more complicated. If the custom start day input is a bank holiday, its custom 'week' will be discounted from the data set. E.g.1: if you choose 'use custom start day' and set it to Monday, then bank holiday Monday weeks will be discounted from the data set. E.g.2: If you choose 'use custom start day' and set it to Thursday, then the Holiday Thursday custom week (e.g Thanksgiving Thursday >> following Weds) would be discounted from the data set.

// On 'Meta Averages':

-The idea is to try and mitigate out the 'continuation bias' that comes from having a fixed week start/end time: i.e. sometimes a market is trending through the week start/end time, so the start/end day stats are over-weighted if one is trying to tease out typical weekly profile tendencies or typical DoW tendencies. You'll notice this if you compare the stats with various custom start days ('bookend' start/end days are always more heavily weighted). I wanted to try to mitigate out this 'bias' by cycling through all the possible new week start/end days and taking an average of the results. i.e. on BTC/USD the 'meta average' for Tuesday would be the average of the Tuesday HoW frequencies from the set of all 7 possible custom weeks(Mon-Sun, Tues-Mon, Weds-Tues, etc etc).

// User Inputs:

~Week Start:

-use custom week start day (default toggled OFF); Choose custom week start day

-show Meta Averages (default toggled ON)

~Verification Table:

-show table, show new week lines, number of new week lines to show

-table formatting options (position, color, size)

-timezone (only for tweaking if printed DoW is misaligned by 1 day)

~Statistics Table:

-show table, table formatting options (position, color, size)

~Manual Backtesting:

-Use start date (default toggled OFF), choose start date, choose vline color

-Use end date (defautl toggled OFF), choose end date, choose vline color

// Demo charts:

NQ1! (Nasdaq), Full History, Traditional week (Mon>>Friday) stats. And Meta Averages. Annotations in purple:

NQ1! (Nasdaq), Full History, Custom week (custom start day = Wednesday). And Meta Averages. Annotations in purple:

Simple and Profitable Scalping Strategy (ForexSignals TV)Strategy is based on the "SIMPLE and PROFITABLE Forex Scalping Strategy" taken from YouTube channel ForexSignals TV.

See video for a detailed explaination of the whole strategy.

I'm not entirely happy with the performance of this strategy yet however I do believe it has potential as the concept makes a lot of sense.

I'm open to any ideas people have on how it could be improved.

Strategy incorporates the following features:

Risk management:

Configurable X% loss per stop (default to 1%)

Configurable R:R ratio

Trade entry:

Based on stratgey conditions outlined below

Trade exit:

Based on stratgey conditions outlined below

Backtesting:

Configurable backtesting range by date

Trade drawings:

Each entry condition indicator can be turned on and off

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: On higher timeframe trend EMAs, Fast EMA must be above Slow EMA

C2: On higher timeframe trend EMAs, price must be above Fast EMA

C3: On current timeframe entry EMAs, Fast EMA must be above Medium EMA and Medium EMA must be above Slow EMA

C4: On current timeframe entry EMAs, all 3 EMA lines must have fanned out in upward direction for previous X candles (configurable)

C5: On current timeframe entry EMAs, previous candle must have closed above and not touched any EMA lines

C6: On current timeframe entry EMAs, current candle must have pulled back to touch the EMA line(s)

C7: Price must break through the high of the last X candles (plus price buffer) to trigger entry (stop order entry)

SHORT

C1: On higher timeframe trend EMAs, Fast EMA must be below Slow EMA

C2: On higher timeframe trend EMAs, price must be below Fast EMA

C3: On current timeframe entry EMAs, Fast EMA must be below Medium EMA and Medium EMA must be below Slow EMA

C4: On current timeframe entry EMAs, all 3 EMA lines must have fanned out in downward direction for previous X candles (configurable)

C5: On current timeframe entry EMAs, previous candle must have closed above and not touched any EMA lines

C6: On current timeframe entry EMAs, current candle must have pulled back to touch the EMA line(s)

C7: Price must break through the low of the last X candles (plus price buffer) to trigger entry (stop order entry)

Trade entry:

Calculated position size based on risk tolerance

Entry price is a stop order set just above (buffer configurable) the recent swing high/low (long/short)

Trade exit:

Stop Loss is set just below (buffer configurable) trigger candle's low/high (long/short)

Take Profit calculated from Stop Loss using R:R ratio

Credits

"SIMPLE and PROFITABLE Forex Scalping Strategy" taken from YouTube channel ForexSignals TV

SSL + Wave Trend StrategyStrategy incorporates the following features:

Risk management:

Configurable X% loss per stop loss

Configurable R:R ratio

Trade entry:

Based on strategy conditions below

Trade exit:

Based on strategy conditions below

Backtesting:

Configurable backtesting range by date

Trade drawings:

Each entry condition indicator can be turned on and off

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Alerting:

Alerts on LONG and SHORT trade entries

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: SSL Hybrid baseline is BLUE

C2: SSL Channel crosses up (green above red)

C3: Wave Trend crosses up (represented by pink candle body)

C4: Entry candle height is not greater than configured threshold

C5: Entry candle is inside Keltner Channel (wicks or body depending on configuration)

C6: Take Profit target does not touch EMA (represents resistance)

SHORT

C1: SSL Hybrid baseline is RED

C2: SSL Channel crosses down (red above green)

C3: Wave Trend crosses down (represented by orange candle body)

C4: Entry candle height is not greater than configured threshold

C5: Entry candle is inside Keltner Channel (wicks or body depending on configuration)

C6: Take Profit target does not touch EMA (represents support)

Trade exit:

Stop Loss: Size configurable with NNFX ATR multiplier

Take Profit: Calculated from Stop Loss using R:R ratio

Credits

Strategy is based on the YouTube video "This Unique Strategy Made 47% Profit in 2.5 Months " by TradeSmart.

It combines the following indicators to determine trade entry/exit conditions:

Wave Trend: Indicator: WaveTrend Oscillator by @LazyBear

SSL Channel: SSL channel by @ErwinBeckers

SSL Hybrid: SSL Hybrid by @Mihkel00

Keltner Channels: Keltner Channels Bands by @ceyhun

Candle Height: Candle Height in Percentage - Columns by @FreeReveller

NNFX ATR: NNFX ATR by @sueun123

Risk Management Strategy TemplateThis strategy is intended to be used as a base template for building new strategies.

It incorporates the following features:

Risk management:

Configurable X% loss per stop loss

Configurable R:R ratio

Trade entry:

Calculated position size based on risk tolerance

Trade exit:

Stop Loss currently configurable ATR multiplier but can be replaced based on strategy

Take Profit calculated from Stop Loss using R:R ratio

Backtesting:

Configurable backtesting range by date

Trade drawings:

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: Price is above EMA line

C2: RSI is crossing out of oversold area

SHORT

C1: Price is below EMA line

C2: RSI is crossing out of overbought area

Trade exit:

Stop Loss: Stop Loss ATR multiplier is hit

Take Profit: R:R multiplier * Stop Loss is hit

The idea is to use RSI to catch pullbacks within the main trend.

Note that this strategy is intended to be a simple base strategy for building upon. It was not designed to be traded in its current form.

DeeptestDeeptest: Quantitative Backtesting Library for Pine Script

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ OVERVIEW

Deeptest is a Pine Script library that provides quantitative analysis tools for strategy backtesting. It calculates over 100 statistical metrics including risk-adjusted return ratios (Sharpe, Sortino, Calmar), drawdown analysis, Value at Risk (VaR), Conditional VaR, and performs Monte Carlo simulation and Walk-Forward Analysis.

█ WHY THIS LIBRARY MATTERS

Pine Script is a simple yet effective coding language for algorithmic and quantitative trading. Its accessibility enables traders to quickly prototype and test ideas directly within TradingView. However, the built-in strategy tester provides only basic metrics (net profit, win rate, drawdown), which is often insufficient for serious strategy evaluation.

Due to this limitation, many traders migrate to alternative backtesting platforms that offer comprehensive analytics. These platforms require other language programming knowledge, environment setup, and significant time investment—often just to test a simple trading idea.

Deeptest bridges this gap by bringing institutional-level quantitative analytics directly to Pine Script. Traders can now perform sophisticated analysis without leaving TradingView or learning complex external platforms. All calculations are derived from strategy.closedtrades.* , ensuring compatibility with any existing Pine Script strategy.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ ORIGINALITY AND USEFULNESS

This library is original work that adds value to the TradingView community in the following ways:

1. Comprehensive Metric Suite: Implements 112+ statistical calculations in a single library, including advanced metrics not available in TradingView's built-in tester (p-value, Z-score, Skewness, Kurtosis, Risk of Ruin).

2. Monte Carlo Simulation: Implements trade-sequence randomization to stress-test strategy robustness by simulating 1000+ alternative equity curves.

3. Walk-Forward Analysis: Divides historical data into rolling in-sample and out-of-sample windows to detect overfitting by comparing training vs. testing performance.

4. Rolling Window Statistics: Calculates time-varying Sharpe, Sortino, and Expectancy to analyze metric consistency throughout the backtest period.

5. Interactive Table Display: Renders professional-grade tables with color-coded thresholds, tooltips explaining each metric, and period analysis cards for drawdowns/trades.

6. Benchmark Comparison: Automatically fetches S&P 500 data to calculate Alpha, Beta, and R-squared, enabling objective assessment of strategy skill vs. passive investing.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ KEY FEATURES

Performance Metrics

Net Profit, CAGR, Monthly Return, Expectancy

Profit Factor, Payoff Ratio, Sample Size

Compounding Effect Analysis

Risk Metrics

Sharpe Ratio, Sortino Ratio, Calmar Ratio (MAR)

Martin Ratio, Ulcer Index

Max Drawdown, Average Drawdown, Drawdown Duration

Risk of Ruin, R-squared (equity curve linearity)

Statistical Distribution

Value at Risk (VaR 95%), Conditional VaR

Skewness (return asymmetry)

Kurtosis (tail fatness)

Z-Score, p-value (statistical significance testing)

Trade Analysis

Win Rate, Breakeven Rate, Loss Rate

Average Trade Duration, Time in Market

Consecutive Win/Loss Streaks with Expected values

Top/Worst Trades with R-multiple tracking

Advanced Analytics

Monte Carlo Simulation (1000+ iterations)

Walk-Forward Analysis (rolling windows)

Rolling Statistics (time-varying metrics)

Out-of-Sample Testing

Benchmark Comparison

Alpha (excess return vs. benchmark)

Beta (systematic risk correlation)

Buy & Hold comparison

R-squared vs. benchmark

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK START

Basic Usage

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as *

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ METRIC EXPLANATIONS

The Deeptest table displays 23 metrics across the main row, with 23 additional metrics in the complementary row. Each metric includes detailed tooltips accessible by hovering over the value.

Main Row — Performance Metrics (Columns 0-6)

Net Profit — (Final Equity - Initial Capital) / Initial Capital × 100

— >20%: Excellent, >0%: Profitable, <0%: Loss

— Total return percentage over entire backtest period

Payoff Ratio — Average Win / Average Loss

— >1.5: Excellent, >1.0: Good, <1.0: Losses exceed wins

— Average winning trade size relative to average losing trade. Breakeven win rate = 100% / (1 + Payoff)

Sample Size — Count of closed trades

— >=30: Statistically valid, <30: Insufficient data

— Number of completed trades. Includes 95% confidence interval for win rate in tooltip

Profit Factor — Gross Profit / Gross Loss

— >=1.5: Excellent, >1.0: Profitable, <1.0: Losing

— Ratio of total winnings to total losses. Uses absolute values unlike payoff ratio

CAGR — (Final / Initial)^(365.25 / Days) - 1

— >=10%: Excellent, >0%: Positive growth

— Compound Annual Growth Rate - annualized return accounting for compounding

Expectancy — Sum of all returns / Trade count

— >0.20%: Excellent, >0%: Positive edge

— Average return per trade as percentage. Positive expectancy indicates profitable edge

Monthly Return — Net Profit / (Months in test)

— >0%: Profitable month average

— Average monthly return. Geometric monthly also shown in tooltip

Main Row — Trade Statistics (Columns 7-14)

Avg Duration — Average time in position per trade

— Mean holding period from entry to exit. Influenced by timeframe and trading style

Max CW — Longest consecutive winning streak

— Maximum consecutive wins. Expected value = ln(trades) / ln(1/winRate)

Max CL — Longest consecutive losing streak

— Maximum consecutive losses. Important for psychological risk tolerance

Win Rate — Wins / Total Trades

— Higher is better

— Percentage of profitable trades. Breakeven win rate shown in tooltip

BE Rate — Breakeven Trades / Total Trades

— Lower is better

— Percentage of trades that broke even (neither profit nor loss)

Loss Rate — Losses / Total Trades

— Lower is better

— Percentage of unprofitable trades. Together with win rate and BE rate, sums to 100%

Frequency — Trades per month

— Trading activity level. Displays intelligently (e.g., "12/mo", "1.5/wk", "3/day")

Exposure — Time in market / Total time × 100

— Lower = less risk

— Percentage of time the strategy had open positions

Main Row — Risk Metrics (Columns 15-22)

Sharpe Ratio — (Return - Rf) / StdDev × sqrt(Periods)

— >=3: Excellent, >=2: Good, >=1: Fair, <1: Poor

— Measures risk-adjusted return using total volatility. Annualized using sqrt(252) for daily

Sortino Ratio — (Return - Rf) / DownsideDev × sqrt(Periods)

— >=2: Excellent, >=1: Good, <1: Needs improvement

— Similar to Sharpe but only penalizes downside volatility. Can be higher than Sharpe

Max DD — (Peak - Trough) / Peak × 100

— <5%: Excellent, 5-15%: Moderate, 15-30%: High, >30%: Severe

— Largest peak-to-trough decline in equity. Critical for risk tolerance and position sizing

RoR — Risk of Ruin probability

— <1%: Excellent, 1-5%: Acceptable, 5-10%: Elevated, >10%: Dangerous

— Probability of losing entire trading account based on win rate and payoff ratio

R² — R-squared of equity curve vs. time

— >=0.95: Excellent, 0.90-0.95: Good, 0.80-0.90: Moderate, <0.80: Erratic

— Coefficient of determination measuring linearity of equity growth

MAR — CAGR / |Max Drawdown|

— Higher is better, negative = bad

— Calmar Ratio. Reward relative to worst-case loss. Negative if max DD exceeds CAGR

CVaR — Average of returns below VaR threshold

— Lower absolute is better

— Conditional Value at Risk (Expected Shortfall). Average loss in worst 5% of outcomes

p-value — Binomial test probability

— <0.05: Significant, 0.05-0.10: Marginal, >0.10: Likely random

— Probability that observed results are due to chance. Low p-value means statistically significant edge

Complementary Row — Extended Metrics

Compounding — (Compounded Return / Total Return) × 100

— Percentage of total profit attributable to compounding (position sizing)

Avg Win — Sum of wins / Win count

— Average profitable trade return in percentage

Avg Trade — Sum of all returns / Total trades

— Same as Expectancy (Column 5). Displayed here for convenience

Avg Loss — Sum of losses / Loss count

— Average unprofitable trade return in percentage (negative value)

Martin Ratio — CAGR / Ulcer Index

— Similar to Calmar but uses Ulcer Index instead of Max DD

Rolling Expectancy — Mean of rolling window expectancies

— Average expectancy calculated across rolling windows. Shows consistency of edge

Avg W Dur — Avg duration of winning trades

— Average time from entry to exit for winning trades only

Max Eq — Highest equity value reached

— Peak equity achieved during backtest

Min Eq — Lowest equity value reached

— Trough equity point. Important for understanding worst-case absolute loss

Buy & Hold — (Close_last / Close_first - 1) × 100

— >0%: Passive profit

— Return of simply buying and holding the asset from backtest start to end

Alpha — Strategy CAGR - Benchmark CAGR

— >0: Has skill (beats benchmark)

— Excess return above passive benchmark. Positive alpha indicates genuine value-added skill

Beta — Covariance(Strategy, Benchmark) / Variance(Benchmark)

— <1: Less volatile than market, >1: More volatile

— Systematic risk correlation with benchmark

Avg L Dur — Avg duration of losing trades

— Average time from entry to exit for losing trades only

Rolling Sharpe/Sortino — Dynamic based on win rate

— >2: Good consistency

— Rolling metric across sliding windows. Shows Sharpe if win rate >50%, Sortino if <=50%

Curr DD — Current drawdown from peak

— Lower is better

— Present drawdown percentage. Zero means at new equity high

DAR — CAGR adjusted for target DD

— Higher is better

— Drawdown-Adjusted Return. DAR^5 = CAGR if max DD = 5%

Kurtosis — Fourth moment / StdDev^4 - 3

— ~0: Normal, >0: Fat tails, <0: Thin tails

— Measures "tailedness" of return distribution (excess kurtosis)

Skewness — Third moment / StdDev^3

— >0: Positive skew (big wins), <0: Negative skew (big losses)

— Return distribution asymmetry

VaR — 5th percentile of returns

— Lower absolute is better

— Value at Risk at 95% confidence. Maximum expected loss in worst 5% of outcomes

Ulcer — sqrt(mean(drawdown^2))

— Lower is better

— Ulcer Index - root mean square of drawdowns. Penalizes both depth AND duration

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ MONTE CARLO SIMULATION

Purpose

Monte Carlo simulation tests strategy robustness by randomizing the order of trades while keeping trade returns unchanged. This simulates alternative equity curves to assess outcome variability.

Method

Extract all historical trade returns

Randomly shuffle the sequence (1000+ iterations)

Calculate cumulative equity for each shuffle

Build distribution of final outcomes

Output

The stress test table shows:

Median Outcome: 50th percentile result

5th Percentile: Worst 5% of outcomes

95th Percentile: Best 95% of outcomes

Success Rate: Percentage of simulations that were profitable

Interpretation

If 95% of simulations are profitable: Strategy is robust

If median is far from actual result: High variance/unreliability

If 5th percentile shows large loss: High tail risk

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ WALK-FORWARD ANALYSIS

Purpose

Walk-Forward Analysis (WFA) is the gold standard for detecting strategy overfitting. It simulates real-world trading by dividing historical data into rolling "training" (in-sample) and "validation" (out-of-sample) periods. A strategy that performs well on unseen data is more likely to succeed in live trading.

Method

The implementation uses a non-overlapping window approach following AmiBroker's gold standard methodology:

Segment Calculation: Total trades divided into N windows (default: 12), IS = ~75%, OOS = ~25%, Step = OOS length

Window Structure: Each window has IS (training) followed by OOS (validation). Each OOS becomes the next window's IS (rolling forward)

Metrics Calculated: CAGR, Sharpe, Sortino, MaxDD, Win Rate, Expectancy, Profit Factor, Payoff

Aggregation: IS metrics averaged across all IS periods, OOS metrics averaged across all OOS periods

Output

IS CAGR: In-sample annualized return

OOS CAGR: Out-of-sample annualized return ( THE key metric )

IS/OOS Sharpe: In/out-of-sample risk-adjusted return

Success Rate: % of OOS windows that were profitable

Interpretation

Robust: IS/OOS CAGR gap <20%, OOS Success Rate >80%

Some Overfitting: CAGR gap 20-50%, Success Rate 50-80%

Severe Overfitting: CAGR gap >50%, Success Rate <50%

Key Principles:

OOS is what matters — Only OOS predicts live performance

Consistency > Magnitude — 10% IS / 9% OOS beats 30% IS / 5% OOS

Window count — More windows = more reliable validation

Non-overlapping OOS — Prevents data leakage

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ TABLE DISPLAY

Main Table — Organized into three sections:

Performance Metrics (Cols 0-6): Net Profit, Payoff, Sample Size, Profit Factor, CAGR, Expectancy, Monthly

Trade Statistics (Cols 7-14): Avg Duration, Max CW, Max CL, Win, BE, Loss, Frequency, Exposure

Risk Metrics (Cols 15-22): Sharpe, Sortino, Max DD, RoR, R², MAR, CVaR, p-value

Color Coding

🟢 Green: Excellent performance

🟠 Orange: Acceptable performance

⚪ Gray: Neutral / Fair

🔴 Red: Poor performance

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ IMPLEMENTATION NOTES

Data Source: All metrics calculated from strategy.closedtrades , ensuring compatibility with any Pine Script strategy

Calculation Timing: All calculations occur on barstate.islastconfirmedhistory to optimize performance

Limitations: Requires at least 1 closed trade for basic metrics, 30+ trades for reliable statistical analysis

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK NOTES

➙ This library has been developed and refined over two years of real-world strategy testing. Every calculation has been validated against industry-standard quantitative finance references.

➙ The entire codebase is thoroughly documented inline. If you are curious about how a metric is calculated or want to understand the implementation details, dive into the source code -- it is written to be read and learned from.

➙ This description focuses on usage and concepts rather than exhaustively listing every exported type and function. The library source code is thoroughly documented inline -- explore it to understand implementation details and internal logic.

➙ All calculations execute on barstate.islastconfirmedhistory to minimize runtime overhead. The library is designed for efficiency without sacrificing accuracy.

➙ Beyond analysis, this library serves as a learning resource. Study the source code to understand quantitative finance concepts, Pine Script advanced techniques, and proper statistical methodology.

➙ Metrics are their own not binary good/bad indicators. A high Sharpe ratio with low sample size is misleading. A deep drawdown during a market crash may be acceptable. Study each function and metric individually -- evaluate your strategy contextually, not by threshold alone.

➙ All strategies face alpha decay over time. Instead of over-optimizing a single strategy on one timeframe and market, build a diversified portfolio across multiple markets and timeframes. Deeptest helps you validate each component so you can combine robust strategies into a trading portfolio.

➙ Screenshots shown in the documentation are solely for visual representation to demonstrate how the tables and metrics will be displayed. Please do not compare your strategy's performance with the metrics shown in these screenshots -- they are illustrative examples only, not performance targets or benchmarks.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ HOW-TO

Using Deeptest is intentionally straightforward. Just import the library and call DT.runDeeptest() at the end of your strategy code in main scope. .

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as DT

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

And yes... it's compatible with any TradingView Strategy! 🪄

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ CREDITS

Author: @Fractalyst

Font Library: by @fikira - @kaigouthro - @Duyck

Community: Inspired by the @PineCoders community initiative, encouraging developers to contribute open-source libraries and continuously enhance the Pine Script ecosystem for all traders.

if you find Deeptest valuable in your trading journey, feel free to use it in your strategies and give a shoutout to @Fractalyst -- Your recognition directly supports ongoing development and open-source contributions to Pine Script.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ DISCLAIMER

This library is provided for educational and research purposes. Past performance does not guarantee future results. Always test thoroughly and use proper risk management. The author is not responsible for any trading losses incurred through the use of this code.

Manual Backtest - Flat the ChartThis script is an utility tool for manual backtesting.

The main problem in backtesting a discretionary strategy is the bias of knowing the future result of the market, in this way all the market will be crushed into a flat line, this way you can avoid bias.

The way to use this indicator is easy and made by 4 step:

Step 1 : add to an asset you won't backtest and put the auto scale on

Step 2 : go to the asset you will backtest and scroll left until the date you want to start

Step 3 : use the replay function of tradingview (15 min chart won't go back more than 18 month)

Step 4: toggle off the indicator or remove from the chart (untill next asset to backtest)

That's not a complex indicator but is what you need to do a fair backtesting

TV signal for DCA backtestThis script allows you to backtest Trading View's "Technical Ratings" (Buy, Strong buy, Sell, Strong Sell) using Gavin's backtest script.

To use it add the backtest script to the chart together with this script and then from the back test settings connect the external indicator. You should select "TV Signal" as the source.

Backtesting works best on the 5m chart, but you can still change this script from its settings to higher timeframes.

Encoding

Buy is 1

Strong Buy is 2

Sell is -1

Strong Sell is -2

In the backtest script you can decide which rating you want to use for open deal and which one for close deal.

For example, if you were backtesting a long bot you could enter a long position when TV signal is Buy (1) and close the deal when TV signal is Sell (-1).

You have the full flexibility to decide which technical rating to use for your backtesting.

Enjoy!

Price Legs: Time & Distance. Measuring moves in time & price-Tool to measure price legs in terms of both time and price; gives an idea of frequency of market movements and their typical extent and duration.

-Written for backtesting: seeing times of day where setups are most likely to unfold dynamically; getting an idea of typical and minimum sizes of small/large legs.

-Two sets of editable lookback numbers to measure both small and large legs independently.

-Works across timeframes and assets (units = mins/hours/days dependent on timeframe; units = '$' for indices & futures, 'pips' for FX).

~toggle on/off each set of bull/bear boxes.

~choose lookback/forward length for each set. Increase number for larger legs, decrease for smaller legs.

(for assets outside of the big Indices and FX, you may want to edit the multiplier, pMult, on lines 23-24)

small legs

large legs

RF+ Replay for Heikin AshiRF+ Replay for Heikin Ashi

RF+ Replay for Heikin Ashi generates fully customisable Heikin Ashi candlesticks presented on a standard chart, enabling traders to utilise the Tradingview Replay feature with Heikin Ashi candlesticks when analysing and backtesting HA style strategies.

The features of this indicator include:

- Fully customisable Heikin Ashi Candles, including custom colour options for candle bodies, borders and wicks.

- Optional real-time, real-price close dots painted onto each candlestick.

- A optional set of 2 x Range Filters designed to indicate short term trend identification upon color change, ideal for low timeframe scalping.

- A optional set of 3 x fully customisable Moving Averages.

- An option to enable Heikin Ashi calculated data for the Range Filters and Moving Averages, so they present as they would on a Heikin Ashi non-standard chart type, without having to use an actual Heikin Ashi chart. Enabled by default.

- An optional sessions indicator, to highlight your prefered trading session for the purpose of backtesting.

- An optional watermark featuring customisable text and well as symbol and timeframe information, as seen in the screenshot of this indicator.

Instructions for use:

1) Because this indicator generates candlesticks and presents them onto your chart, you will need to hide the existing candlesticks so you do not see two sets of candles. You can do this by going into your Tradingview chart settings and making the candle bodies, borders and wicks fully transparent. You can then save this as a layout template. You can access your Chart Settings by clicking on the cog icon, or by right clicking on the chart itself and selecting 'Chart Settings' from the list.

2) Ensure you have the standard chart type selected - you do not need to select a Heikin Ashi type chart.

3) You will now be able to analyise and even backtest your Heikin Ashi style strategies including the use of the Tradingview Replay feature found at the top of the chart.

Heikin Ashi means 'average bar' in Japanese, which speaks to the fact that Heikin Ashi candles are calculated differently to standard Japanese candlesticks. The general idea of Heikin Ashi candles is to 'smooth' the appearance of price movement, by the use of averages within their calculation. It is important to understand that the Open and Close values of a Heikin Ashi candlestick do not reflect real Open and Close prices. You can use the real price dots feature to clearly see the real time and real price Close of each candle.

The formula for calculating a Heikin Ashi candlestick is as follows:

High = Maximum of High, Open, or Close (whichever is highest)

Low = Minimum of Low, Open, or Close (whichever is lowest)

Open = Open (previous bar) + Close (previous bar) /2

Close = (Open + High + Low + Close) / 4

If you found this useful, be sure to leave a like, comment and subscribe to show your support.

Until next time.

Grid Spot Trading Algorithm V2 - The Quant ScienceGrid Spot Trading Algorithm V2 is the last grid trading algorithm made by our developer team.

Grid Spot Trading Algorithm V2 is a fixed 10-level grid trading algorithm. The grid is divided into an accumulation area (red) and a selling area (green).

In the accumulation area, the algorithm will place new buy orders, selling the long positions on the top of the grid.

BUYING AND SELLING LOGIC

The algorithm places up to 5 limit orders on the accumulation section of the grid, each time the price cross through the middle grid. Each single order uses 20% of the equity.

Positions are closed at the top of the grid by default, with the algorithm closing all orders at the first sell level. The exit level can be adjusted using the user interface, from the first level up to the fifth level above.

CONFIGURING THE ALGORITHM

1) Add it to the chart: Add the script to the current chart that you want to analyze.

2) Select the top of the grid: Confirm a price level with the mouse on which to fix the top of the grid.

3) Select the bottom of the grid: Confirm a price level with the mouse on which to fix the bottom of the grid.

4) Wait for the automatic creation of the grid.

USING THE ALGORITHM

Once the grid configuration process is completed, the algorithm will generate automatic backtesting.

You can add a stop loss that destroys the grid by setting the destruction price and activating the feature from the user interface. When the stop loss is activated, you can view it on the chart.

Bar Count for BacktestingHello!

Not much special about this script; you can use date & time, or bar count, to ascertain the number of bars in a time period for backtesting.

This script can be used in conjunction with large scripts incorporating complex intricacies that won't load on 20,000+ bar data sets.

If your script's load time transcends the TV allotted load time - use this script to quickly determine the number of bars in the data set.

Through trial & error you should be able to determine the approximate number of bars your script can execute on without exceeding the imposed time limit!

The image above shows a user-defined time window and, consequently, the script returns the number of bars that constitute the time period.

You can drag the white vertical lines to efficiently configure the calculated time period.

The image above shows functionality for the "Bars Back" feature.

Enjoy!

Custom Triple Moving Average Strategy | Auto BacktestingCreate your own MA Strategy set of up to three moving averages!

Auto Backtesting.

Cloud between MA1 and MA2.

Many different MA types to choose from.

Totally Custom!

Happy Trading, and algorithm analysis!

[FN] Session Range & Date Range For BacktestingThis has been done before in different ways, however, my goal is to publish a single, simplified copy/paste version of the idea so you can quickly and easily incorporate it into your strategy backtesting.

You can designate weekdays, weekdays + weekends for 24/7 markets, and also session range.

So, you trade bitcoin? It works. CME futures? It works. You are a discretionary trader so the only signals that matter are the ones that happen when you're awake? It works. Copy and paste.

The goal is that its that easy. You'll have to let me know if it is. glhf everyone.

If I'm not mistaken, you should be able to copy/paste this directly into your strategy script (Paste it in before your entry declarations). Just leave out the last 2 lines where the bgcolor() is declared... unless you want the background color lit up, that's up to you. It's just for demonstration purposes in this script.

After you've pasted it in, then in your strategy.entry() function you are adding: to the strategy.entry() function.

e.g:

strategy.entry("Long", strategy.long, qty=1, when = ENTRY_SIGNAL and signal_backtest())

Shoutouts to @zenandtheartoftrading and @allanster for providing the basis of this code that I put together here. We stand on the shoulders of giants.

Gold Friday Anomaly StrategyThis script implements the " Gold Friday Anomaly Strategy ," a well-known historical trading strategy that leverages the gold market's behavior from Thursday evening to Friday close. It is a backtesting-focused strategy designed to assess the historical performance of this pattern. Traders use this anomaly as it captures a recurring market tendency observed over the years.

What It Does:

Entry Condition: The strategy enters a long position at the beginning of the Friday trading session (Thursday evening close) within the defined backtesting period.

Exit Condition: Friday evening close.

Backtesting Controls: Allows users to set custom backtesting periods to evaluate strategy performance over specific date ranges.

Key Features:

Custom Backtest Periods: Easily configurable inputs to set the start and end date of the backtesting range.

Fixed Slippage and Commission Settings: Ensures realistic simulation of trading conditions.

Process Orders on Close: Backtesting is optimized by processing orders at the bar's close.

Important Notes:

Backtesting Only: This script is intended purely for backtesting purposes. Past performance is not indicative of future results.

Live Trading Recommendations: For live trading, it is highly recommended to use limit orders instead of market orders, especially during evening sessions, as market order slippage can be significant.

Default Settings:

Entry size: 10% of equity per trade.

Slippage: 1 tick.

Commission: 0.05% per trade.

[fareid] Quick Backtest Framework█ OVERVIEW

This Framework allows Pine Coders to quickly code Study() based signal/strategy and validate its viability before proceed to code with more advance/complex customized rules for entry, exit, trailstop, risk management etc..

This is somewhat an upgraded version of my earlier personal template with different strategy used, cleaner code

and additional features.

█ USE CASES

- You have an idea for trade signal and need a quick way to verify its potential before writing lengthy/complicated code

- You found a study script for trading signal in public library and want to validate it profitability with minimum effort before including it in your trading playbook

█ FEATURES

- Alert: Ready to use alert function based on signals from your custom indicator.

- Visual Backtest: Auto-plot entry, stop-loss and take profit for simple strategy performance analysis

- Backtest Statistic: Provide basic key metrics based on backtest strategy

- BTE External Signal Protocol: Ready to use code that will supply required state to PineCoders Backtesting & Trading Engine if you wish to have more advance and sophisticated backtesting engine

Notes: All of the above features have On/Off toggle

█ Description & How To Use

This Framework consist of 5 Modules but you only need to edit the first 2 Modules:

Module1: Indicator

Module2: Framework Input Protocol

Module3: Alert

Module4: Backtest

Module5: Backtest & Trading Engine

Tips: The source-code includes collapsible block by module for easy navigating

Module1: Indicator:

-----------------------------------------------------------------------------------

Main Module. Place custom indicator input parameter/calculation/indicator plotting here

Sample Strategy: Double MACD Crossover

MACD Signal: 1st MACD Cross above signal line indicate Buy Signal

1st MACD Cross below signal line indicate Sell Signal

MACD Filter: 2nd MACD is above 0 line indicate Uptrend

2nd MACD is below 0 line indicate Downtrend

Module2: Framework Input Protocol:

-----------------------------------------------------------------------------------

Use this module to connect main indicator/signal calculated in Module1 to the rest of the framework's module

4 variables needed to be defined here:

1. Uptrend

2. Dntrend

3. BuySignal

4. SellSignal

i'm not sure how to place a code snippet here to show you example so in the source code i already put a comment in Module2 on which part u need to edit. I hope its pretty simple to use.

Module3: Alert Module Description:

-----------------------------------------------------------------------------------

As long as the variables in Module2 properly defined, the alert module is ready to use without any further modification.

Input:

Enable Alert --> Enable TV's alert and plot signal to chart

Alert Type --> Set to take Buy only, Sell only or Both alert

Module4: Backtest Module Description:

-----------------------------------------------------------------------------------

As long as the variables in Module2 properly defined, the backtest module is ready to use without any further modification.

Input:

Backtest Stat --> Enable Backtest Statistic Label

Backtest Visual --> Enable Backtest visual simulation

Backtest Type --> Set to take Buy only or Sell only or both

SL Type -->

ATR : Set SL in ATR times Multiplier below entry price

Fixed : Set SL in fixed point below entry point (in 'Dollar'). e.g. for Stocks -> 0.5 equals to 50cent while for EURUSD currency -> 0.005 equal to 50 pips

HiLo Bar: Set SL at highest/lowest wick of previous bar plus/minus Fixed point. e.g. EURUSD HiLo=3 and Fixed Point = 0.0005, buy trade will place SL 5 Pips below lowest of previous 3 bar

SL ATR Multi --> Set Lookback Period used for SL's ATR calculation

SL ATR Multi --> Set ATR Multiplier for SL

SL Fixed --> Set Fixed Level for SL

SL Bar --> Set Number of previous bar to check for SL placement

TP RR Ratio --> Set TP based on RR multiplier. e.g. 2 means TP level will be twice further from entry point compared to Entry-SL distance.

Notes: The point is for preliminary testing, so it only supports 1 trade at a time and no Trailing Stop

Module5: Backtest & Trading Engine Description:

-----------------------------------------------------------------------------------

As long as the variables in Module2 properly defined, the Pinecoders BTE module is ready to use without any further modification.

Input:

External Signal Protocol --> Set ESP State to send to "Backtesting & Trading Engine "

Signal With Filter --> Use this to send entry signal that already filtered by this study indicator (without stoploss level)

Signal Without Filter --> Use this to send raw entry signal that are NOT YET FILTERED by this study indicator (without stoploss level)

Signal and Stop With Filter --> Use this to send entry signal WITH StopLoss that already filtered by this study indicator (with stoploss level)

Signal and Stop Without Filter --> Use this to send raw entry signal WITH StopLoss that are NOT YET FILTERED by this study indicator (with stoploss level)

Notes: Backtesting & Trading Engine already have built-in Filter, Entries and Stop Level. e.g. Unselect all their filter state if only want to use custom filter and make sure send Signal with Filter (with or without SL level)

█ DISCLAIMER:

This framework main objective is to create my personal indicator template so that i just have to modify the indicator module for preliminary testing in future.

The sample strategy included are for educational purpose only. Use at your own risk

credit: LucF/PineCoders for a lot of his scripts that i use as a guide to complete this

Great Expectations [LucF]Great Expectations helps traders answer the question: What is possible? It is a powerful question, yet exploration of the unknown always entails risk. A more complete set of questions better suited to traders could be:

What opportunity exists from any given point on a chart?

What portion of this opportunity can be realistically captured?

What risk will be incurred in trying to do so, and how long will it take?

Great Expectations is the result of an exploration of these questions. It is a trade simulator that generates visual and quantitative information to help strategy modelers visually identify and analyse areas of optimal expectation on charts, whether they are designing automated or discretionary strategies.