Arnaud Legoux Gaussian Flow | AlphaNattArnaud Legoux Gaussian Flow | AlphaNatt

A sophisticated trend-following and mean-reversion indicator that combines the power of the Arnaud Legoux Moving Average (ALMA) with advanced Gaussian distribution analysis to identify high-probability trading opportunities.

🎯 What Makes This Indicator Unique?

This indicator goes beyond traditional moving averages by incorporating Gaussian mathematics at multiple levels:

ALMA uses Gaussian distribution for superior price smoothing with minimal lag

Dynamic envelopes based on Gaussian probability zones

Multi-layer gradient visualization showing probability density

Adaptive envelope modes that respond to market conditions

📊 Core Components

1. Arnaud Legoux Moving Average (ALMA)

The ALMA is a highly responsive moving average that uses Gaussian distribution to weight price data. Unlike simple moving averages, ALMA can be fine-tuned to balance responsiveness and smoothness through three key parameters:

ALMA Period: Controls the lookback window (default: 21)

Gaussian Offset: Shifts the Gaussian curve to adjust lag vs. responsiveness (default: 0.85)

Gaussian Sigma: Controls the width of the Gaussian distribution (default: 6.0)

2. Gaussian Envelope System

The indicator features three envelope calculation modes:

Fixed Mode: Uses ATR-based fixed width for consistent envelope sizing

Adaptive Mode: Dynamically adjusts based on price acceleration and volatility

Hybrid Mode: Combines ATR and standard deviation for balanced adaptation

The envelopes represent statistical probability zones. Price moving beyond these zones suggests potential mean reversion opportunities.

3. Momentum-Adjusted Envelopes

The envelope width automatically expands during strong trends and contracts during consolidation, providing context-aware support and resistance levels.

⚡ Key Features

Multi-Layer Gradient Visualization

The indicator displays 10 gradient layers between the ALMA and envelope boundaries, creating a visual "heat map" of probability density. This helps traders quickly assess:

Distance from the mean

Potential support/resistance strength

Overbought/oversold conditions in context

Dynamic Color Coding

Cyan gradient: Price below ALMA (bullish zone)

Magenta gradient: Price above ALMA (bearish zone)

The ALMA line itself changes color based on price position

Trend Regime Detection

The indicator automatically identifies market regimes:

Strong Uptrend: Trend strength > 0.5% with price above ALMA

Strong Downtrend: Trend strength < -0.5% with price below ALMA

Weak trends and ranging conditions

📈 Trading Strategies

Mean Reversion Strategy

Look for price entering the extreme Gaussian zones (beyond 95% of envelope width) when trend strength is moderate. These represent statistical extremes where mean reversion is probable.

Signals:

Long: Price in lower Gaussian zone with trend strength > -0.5%

Short: Price in upper Gaussian zone with trend strength < 0.5%

Trend Continuation Strategy

Enter when price crosses the ALMA during confirmed strong trend conditions, riding momentum while using the envelope as a trailing stop reference.

Signals:

Long: Price crosses above ALMA during strong uptrend

Short: Price crosses below ALMA during strong downtrend

🎨 Visualization Guide

The gradient layers create a "probability cloud" around the ALMA:

Darker shades (near ALMA): High probability zone - price tends to stay here

Lighter shades (near envelope edges): Lower probability - potential reversal zones

Price at envelope extremes: Statistical outliers - strongest mean reversion setups

⚙️ Customization Options

ALMA Parameters

Adjust period for different timeframes (lower for day trading, higher for swing trading)

Modify offset to tune responsiveness vs. smoothness

Change sigma to control distribution width

Envelope Configuration

Choose envelope mode based on market characteristics

Adjust multiplier to match instrument volatility

Modify gradient depth for visual preference (5-15 layers)

Signal Enhancement

Momentum Length: Lookback for trend strength calculation

Signal Smoothing: Additional EMA smoothing to reduce noise

🔔 Built-in Alerts

The indicator includes six pre-configured alert conditions:

ALMA Trend Long - Price crosses above ALMA in strong uptrend

ALMA Trend Short - Price crosses below ALMA in strong downtrend

Mean Reversion Long - Price enters lower Gaussian zone

Mean Reversion Short - Price enters upper Gaussian zone

Strong Uptrend Detected - Momentum confirms strong bullish regime

Strong Downtrend Detected - Momentum confirms strong bearish regime

💡 Best Practices

Use on clean, liquid markets with consistent volatility

Combine with volume analysis for confirmation

Adjust envelope multiplier based on backtesting for your specific instrument

Higher timeframes (4H+) generally provide more reliable signals

Use adaptive mode for trending markets, hybrid for mixed conditions

⚠️ Important Notes

This indicator works best in markets with normal price distribution

Extreme news events can invalidate Gaussian assumptions temporarily

Always use proper risk management - no indicator is perfect

Backtest parameters on your specific instrument and timeframe

🔬 Technical Background

The Arnaud Legoux Moving Average was developed to solve the classic dilemma of moving averages: the trade-off between lag and noise. By applying Gaussian distribution weighting, ALMA achieves superior smoothing while maintaining responsiveness to price changes.

The envelope system extends this concept by creating probability zones based on volatility and momentum, effectively mapping where price is "likely" vs "unlikely" to be found based on statistical principles.

Created by AlphaNatt - For educational purposes. Always practice proper risk management. Not financial advice. Always DYOR.

Cari dalam skrip untuk "backtesting"

Scalp BTC/ETH — Reversal & Continuation (v1, Pine v6)Scalp BTC/ETH — Reversal & Continuation (1m à 10m)

Cet indicateur détecte des opportunités de micro-scalping sur futures (BTC/ETH) basées sur deux mécaniques courtes validées par structure de prix :

A) Reversal de pression (contre-mouvement contrôlé)

Détection d’une sur-extension brutale suivie d’une absorption sur la bougie suivante.

Objectif : capturer la première respiration après un excès de prix (rejet court).

B) Continuation courte (momentum + reprise)

Détection de 3 bougies directionnelles consécutives suivies d’un pullback léger, puis signal sur la reprise du mouvement initial.

Gestion intégrée (scénario standard TP dynamique)

TP1 → 50% de la position à un gain fixe (% adaptable au timeframe)

Stop déplacé au Break-Even sur le restant

Sortie finale sur bougie inverse significative

(correction ≥ X% du corps précédent) ou timeout (max bars en trade)

Scalp BTC/ETH — Reversal & Continuation (1m to 10m)

This indicator detects short-term futures scalping setups on BTC & ETH using two mechanical price-action models designed for fast execution:

A) Reversal Compression (counter-move entry)

Identifies a sharp impulse (overextension) followed by absorption / failure to extend on the next candle.

Objective: capture the first corrective pullback after exhaustion.

B) Controlled Continuation (momentum follow-through)

Identifies 3 consecutive trend candles, then a shallow pullback, and triggers an entry on the resumption of the main leg.

Built-in trade logic (dynamic TP structure)

TP1 → scale out 50% of the position at a fixed percentage (auto-scaled per timeframe)

Stop moved to Break-Even after TP1

Final exit on either:

• a meaningful opposite candle (≥ X% correction of prior body), or

• a timeout (max bars in trade)

Technical characteristics

Designed for 1m / 3m / 5m / 7m / 10m

No repainting (bar-close confirmed logic)

Works for both LONG & SHORT

Built-in alert events:

ENTRY_LONG / ENTRY_SHORT / TP1 / EXIT_STOP / EXIT_INVERSE / EXIT_TIMEOUT

Suitable for manual execution, semi-automation (alerts) or full bot integration (webhook JSON)

Purpose

Provide a repeatable, rule-based, non-subjective framework to harvest micro-moves with controlled risk, without relying on lagging indicators or long-term prediction.

(A Strategy / backtesting version is planned as a next iteration.)

ICT Liquidity Sweep Asia/London 1 Trade per High & Low🧠 ICT Liquidity Sweep Asia/London — 1 Trade per High & Low

This strategy is inspired by the ICT (Inner Circle Trader) concepts of liquidity sweeps and market structure, focusing on the Asia and London sessions.

It automatically identifies liquidity grabs (sweeps) above or below key session highs/lows and enters trades with a fixed risk/reward ratio (RR).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚙️ Core Logic

-Asia Session: 8:00 PM – 11:59 PM (New York time)

-London Session: 2:00 AM – 5:00 AM (New York time)

-The script marks the Asia High/Low and London High/Low ranges for each day.

-When the market sweeps above a session high → potential Short setup

-When the market sweeps below a session low → potential Long setup

-A trade is triggered when the confirmation candle closes in the opposite direction of the sweep (bearish after a high sweep, bullish after a low sweep).

-Only one trade per sweep type (1 per High, 1 per Low) is allowed per session.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

📈 Risk Management

-Configurable Risk/Reward Target (default = 2:1)

-Configurable Position Size (number of contracts)

-Each trade uses a fixed Stop Loss (beyond the wick of the sweep) and a Take Profit calculated from the RR setting.

-All trades are automatically logged in the Strategy Tester with performance metrics.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

💡 Features

✅ Visual session highlighting (Asia = Aqua, London = Orange)

✅ Automatic liquidity line plotting (session highs/lows)

✅ Entry & exit labels (optional visual display)

✅ Customizable RR and contract size

✅ Works on any instrument (ideal for indices, futures, or forex)

✅ Compatible with all timeframes (optimized for 1M–15M)

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚠️ Notes

-Best used on New York time-based charts.

-Designed for educational and backtesting purposes — not financial advice.

-Use as a foundation for further optimization (e.g., SMT confirmation, FVG filter, or time-based restrictions).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

🧩 Recommended Use

Pair this with:

-ICT’s concepts like CISD (Change in State of Delivery) and FVGs (Fair Value Gaps)

-Higher timeframe liquidity maps

-Session bias or daily narrative filters

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

Author: jygirouard

Strategy Version: 1.3

Type: ICT Liquidity Sweep Automation

Timezone: America/New_York

Pivot Regime Anchored VWAP [CHE] Pivot Regime Anchored VWAP — Detects body-based pivot regimes to classify swing highs and lows, anchoring volume-weighted average price lines directly at higher highs and lower lows for adaptive reference levels.

Summary

This indicator identifies shifts between top and bottom regimes through breakouts in candle body highs and lows, labeling swing points as higher highs, lower highs, lower lows, or higher lows. It then draws anchored volume-weighted average price lines starting from the most recent higher high and lower low, providing dynamic support and resistance that evolve with volume flow. These anchored lines differ from standard volume-weighted averages by resetting only at confirmed swing extremes, reducing noise in ranging markets while highlighting momentum shifts in trends.

Motivation: Why this design?

Traders often struggle with static reference lines that fail to adapt to changing market structures, leading to false breaks in volatile conditions or missed continuations in trends. By anchoring volume-weighted average price calculations to body pivot regimes—specifically at higher highs for resistance and lower lows for support—this design creates reference levels tied directly to price structure extremes. This approach addresses the problem of generic moving averages lagging behind swing confirmations, offering a more context-aware tool for intraday or swing trading.

What’s different vs. standard approaches?

- Baseline reference: Traditional volume-weighted average price indicators compute a running total from session start or fixed periods, often ignoring price structure.

- Architecture differences:

- Regime detection via body breakout logic switches between high and low focus dynamically.

- Anchoring limited to confirmed higher highs and lower lows, with historical recalculation for accurate line drawing.

- Polyline rendering rebuilds only on the last bar to manage performance.

- Practical effect: Charts show fewer, more meaningful lines that start at swing points, making it easier to spot confluences with structure breaks rather than cluttered overlays from continuous calculations.

How it works (technical)

The indicator first calculates the maximum and minimum of each candle's open and close to define body highs and lows. It then scans a lookback window for the highest body high and lowest body low. A top regime triggers when the body high from the lookback period exceeds the window's highest, and a bottom regime when the body low falls below the window's lowest. These regime shifts confirm pivots only when crossing from one state to the other.

For top pivots, it compares the new body high against the previous swing high: if greater, it marks a higher high and anchors a new line; otherwise, a lower high. The same logic applies inversely for bottom pivots. Anchored lines use cumulative price-volume products and volumes from the anchor bar onward, subtracting prior cumulatives to isolate the segment. On pivot confirmation, it loops backward from the current bar to the anchor, computing and storing points for the line. New points append as bars advance, ensuring the line reflects ongoing volume weighting.

Initialization uses persistent variables to track the last swing values and anchor bars, starting with neutral states. Data flows from regime detection to pivot classification, then to anchoring and point accumulation, with lines rendered globally on the final bar.

Parameter Guide

Pivot Length — Controls the lookback window for detecting body breakouts, influencing pivot frequency and sensitivity to recent action. Shorter values catch more pivots in choppy conditions; longer smooths for major swings. Default: 30 (bars). Trade-offs/Tips: Min 1; for intraday, try 10–20 to reduce lag but watch for noise; on daily, 50+ for stability.

Show Pivot Labels — Toggles display of text markers at swing points, aiding quick identification of higher highs, lower highs, lower lows, or higher lows. Default: true. Trade-offs/Tips: Disable in multi-indicator setups to declutter; useful for backtesting structure.

HH Color — Sets the line and label color for higher high anchored lines, distinguishing resistance levels. Default: Red (solid). Trade-offs/Tips: Choose contrasting hues for dark/light themes; pair with opacity for fills if added later.

LL Color — Sets the line and label color for lower low anchored lines, distinguishing support levels. Default: Lime (solid). Trade-offs/Tips: As above; green shades work well for bullish contexts without overpowering candles.

Reading & Interpretation

Higher high labels and red lines indicate potential resistance zones where volume weighting begins at a new swing top, suggesting sellers may defend prior highs. Lower low labels and lime lines mark support from a fresh swing bottom, with the line's slope reflecting buyer commitment via volume. Lower highs or higher lows appear as labels without new anchors, signaling possible range-bound action. Line proximity to price shows overextension; crosses may hint at regime shifts, but confirm with volume spikes.

Practical Workflows & Combinations

- Trend following: Enter longs above a rising lower low anchored line after higher low confirmation; filter with rising higher highs for uptrends. Use line breaks as trailing stops.

- Exits/Stops: In downtrends, exit shorts below a higher high line; set aggressive stops above it for scalps, conservative below for swings. Pair with momentum oscillators for divergence.

- Multi-asset/Multi-TF: Defaults suit forex/stocks on 1H–4H; on crypto 15M, shorten length to 15. Scale colors for dark themes; combine with higher timeframe anchors for confluence.

Behavior, Constraints & Performance

Closed-bar logic ensures pivots confirm after the lookback period, with no repainting on historical bars—live bars may adjust until regime shift. No higher timeframe calls, so minimal repaint risk beyond standard delays. Resources include a 2000-bar history limit, label/polyline caps at 200/50, and loops for historical point filling (up to current bar count from anchor, typically under 500 iterations). Known limits: In extreme gaps or low-volume periods, anchors may skew; lines absent until first pivots.

Sensible Defaults & Quick Tuning

Start with the 30-bar length for balanced pivot detection across most assets. For too-frequent pivots in ranges, increase to 50 for fewer signals. If lines lag in trends, reduce to 20 and enable labels for visual cues. In low-volatility assets, widen color contrasts; test on 100-bar history to verify stability.

What this indicator is—and isn’t

This is a structure-aware visualization layer for anchoring volume-weighted references at swing extremes, enhancing manual analysis of regimes and levels. It is not a standalone signal generator or predictive model—always integrate with broader context like order flow or news. Use alongside risk management and position sizing, not as isolated buy/sell triggers.

Many thanks to LuxAlgo for the original script "McDonald's Pattern ". The implementation for body pivots instead of wicks uses a = max(open, close), b = min(open, close) and then highest(a, length) / lowest(b, length). This filters noise from the wicks and detects breakouts over/under bodies. Unusual and targeted, super innovative.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Historical Matrix Analyzer [PhenLabs]📊Historical Matrix Analyzer

Version: PineScriptv6

📌Description

The Historical Matrix Analyzer is an advanced probabilistic trading tool that transforms technical analysis into a data-driven decision support system. By creating a comprehensive 56-cell matrix that tracks every combination of RSI states and multi-indicator conditions, this indicator reveals which market patterns have historically led to profitable outcomes and which have not.

At its core, the indicator continuously monitors seven distinct RSI states (ranging from Extreme Oversold to Extreme Overbought) and eight unique indicator combinations (MACD direction, volume levels, and price momentum). For each of these 56 possible market states, the system calculates average forward returns, win rates, and occurrence counts based on your configurable lookback period. The result is a color-coded probability matrix that shows you exactly where you stand in the historical performance landscape.

The standout feature is the Current State Panel, which provides instant clarity on your active market conditions. This panel displays signal strength classifications (from Strong Bullish to Strong Bearish), the average return percentage for similar past occurrences, an estimated win rate using Bayesian smoothing to prevent small-sample distortions, and a confidence level indicator that warns you when insufficient data exists for reliable conclusions.

🚀Points of Innovation

Multi-dimensional state classification combining 7 RSI levels with 8 indicator combinations for 56 unique trackable market conditions

Bayesian win rate estimation with adjustable smoothing strength to provide stable probability estimates even with limited historical samples

Real-time active cell highlighting with “NOW” marker that visually connects current market conditions to their historical performance data

Configurable color intensity sensitivity allowing traders to adjust heat-map responsiveness from conservative to aggressive visual feedback

Dual-panel display system separating the comprehensive statistics matrix from an easy-to-read current state summary panel

Intelligent confidence scoring that automatically warns traders when occurrence counts fall below reliable thresholds

🔧Core Components

RSI State Classification: Segments RSI readings into 7 distinct zones (Extreme Oversold <20, Oversold 20-30, Weak 30-40, Neutral 40-60, Strong 60-70, Overbought 70-80, Extreme Overbought >80) to capture momentum extremes and transitions

Multi-Indicator Condition Tracking: Simultaneously monitors MACD crossover status (bullish/bearish), volume relative to moving average (high/low), and price direction (rising/falling) creating 8 binary-encoded combinations

Historical Data Storage Arrays: Maintains rolling lookback windows storing RSI states, indicator states, prices, and bar indices for precise forward-return calculations

Forward Performance Calculator: Measures price changes over configurable forward bar periods (1-20 bars) from each historical state, accumulating total returns and win counts per matrix cell

Bayesian Smoothing Engine: Applies statistical prior assumptions (default 50% win rate) weighted by user-defined strength parameter to stabilize estimated win rates when sample sizes are small

Dynamic Color Mapping System: Converts average returns into color-coded heat map with intensity adjusted by sensitivity parameter and transparency modified by confidence levels

🔥Key Features

56-Cell Probability Matrix: Comprehensive grid displaying every possible combination of RSI state and indicator condition, with each cell showing average return percentage, estimated win rate, and occurrence count for complete statistical visibility

Current State Info Panel: Dedicated display showing your exact position in the matrix with signal strength emoji indicators, numerical statistics, and color-coded confidence warnings for immediate situational awareness

Customizable Lookback Period: Adjustable historical window from 50 to 500 bars allowing traders to focus on recent market behavior or capture longer-term pattern stability across different market cycles

Configurable Forward Performance Window: Select target holding periods from 1 to 20 bars ahead to align probability calculations with your trading timeframe, whether day trading or swing trading

Visual Heat Mapping: Color-coded cells transition from red (bearish historical performance) through gray (neutral) to green (bullish performance) with intensity reflecting statistical significance and occurrence frequency

Intelligent Data Filtering: Minimum occurrence threshold (1-10) removes unreliable patterns with insufficient historical samples, displaying gray warning colors for low-confidence cells

Flexible Layout Options: Independent positioning of statistics matrix and info panel to any screen corner, accommodating different chart layouts and personal preferences

Tooltip Details: Hover over any matrix cell to see full RSI label, complete indicator status description, precise average return, estimated win rate, and total occurrence count

🎨Visualization

Statistics Matrix Table: A 9-column by 8-row grid with RSI states labeling vertical axis and indicator combinations on horizontal axis, using compact abbreviations (XOverS, OverB, MACD↑, Vol↓, P↑) for space efficiency

Active Cell Indicator: The current market state cell displays “⦿ NOW ⦿” in yellow text with enhanced color saturation to immediately draw attention to relevant historical performance

Signal Strength Visualization: Info panel uses emoji indicators (🔥 Strong Bullish, ✅ Bullish, ↗️ Weak Bullish, ➖ Neutral, ↘️ Weak Bearish, ⛔ Bearish, ❄️ Strong Bearish, ⚠️ Insufficient Data) for rapid interpretation

Histogram Plot: Below the price chart, a green/red histogram displays the current cell’s average return percentage, providing a time-series view of how historical performance changes as market conditions evolve

Color Intensity Scaling: Cell background transparency and saturation dynamically adjust based on both the magnitude of average returns and the occurrence count, ensuring visual emphasis on reliable patterns

Confidence Level Display: Info panel bottom row shows “High Confidence” (green), “Medium Confidence” (orange), or “Low Confidence” (red) based on occurrence counts relative to minimum threshold multipliers

📖Usage Guidelines

RSI Period

Default: 14

Range: 1 to unlimited

Description: Controls the lookback period for RSI momentum calculation. Standard 14-period provides widely-recognized overbought/oversold levels. Decrease for faster, more sensitive RSI reactions suitable for scalping. Increase (21, 28) for smoother, longer-term momentum assessment in swing trading. Changes affect how quickly the indicator moves between the 7 RSI state classifications.

MACD Fast Length

Default: 12

Range: 1 to unlimited

Description: Sets the faster exponential moving average for MACD calculation. Standard 12-period setting works well for daily charts and captures short-term momentum shifts. Decreasing creates more responsive MACD crossovers but increases false signals. Increasing smooths out noise but delays signal generation, affecting the bullish/bearish indicator state classification.

MACD Slow Length

Default: 26

Range: 1 to unlimited

Description: Defines the slower exponential moving average for MACD calculation. Traditional 26-period setting balances trend identification with responsiveness. Must be greater than Fast Length. Wider spread between fast and slow increases MACD sensitivity to trend changes, impacting the frequency of indicator state transitions in the matrix.

MACD Signal Length

Default: 9

Range: 1 to unlimited

Description: Smoothing period for the MACD signal line that triggers bullish/bearish state changes. Standard 9-period provides reliable crossover signals. Shorter values create more frequent state changes and earlier signals but with more whipsaws. Longer values produce more confirmed, stable signals but with increased lag in detecting momentum shifts.

Volume MA Period

Default: 20

Range: 1 to unlimited

Description: Lookback period for volume moving average used to classify volume as “high” or “low” in indicator state combinations. 20-period default captures typical monthly trading patterns. Shorter periods (10-15) make volume classification more reactive to recent spikes. Longer periods (30-50) require more sustained volume changes to trigger state classification shifts.

Statistics Lookback Period

Default: 200

Range: 50 to 500

Description: Number of historical bars used to calculate matrix statistics. 200 bars provides substantial data for reliable patterns while remaining responsive to regime changes. Lower values (50-100) emphasize recent market behavior and adapt quickly but may produce volatile statistics. Higher values (300-500) capture long-term patterns with stable statistics but slower adaptation to changing market dynamics.

Forward Performance Bars

Default: 5

Range: 1 to 20

Description: Number of bars ahead used to calculate forward returns from each historical state occurrence. 5-bar default suits intraday to short-term swing trading (5 hours on hourly charts, 1 week on daily charts). Lower values (1-3) target short-term momentum trades. Higher values (10-20) align with position trading and longer-term pattern exploitation.

Color Intensity Sensitivity

Default: 2.0

Range: 0.5 to 5.0, step 0.5

Description: Amplifies or dampens the color intensity response to average return magnitudes in the matrix heat map. 2.0 default provides balanced visual emphasis. Lower values (0.5-1.0) create subtle coloring requiring larger returns for full saturation, useful for volatile instruments. Higher values (3.0-5.0) produce vivid colors from smaller returns, highlighting subtle edges in range-bound markets.

Minimum Occurrences for Coloring

Default: 3

Range: 1 to 10

Description: Required minimum sample size before applying color-coded performance to matrix cells. Cells with fewer occurrences display gray “insufficient data” warning. 3-occurrence default filters out rare patterns. Lower threshold (1-2) shows more data but includes unreliable single-event statistics. Higher thresholds (5-10) ensure only well-established patterns receive visual emphasis.

Table Position

Default: top_right

Options: top_left, top_right, bottom_left, bottom_right

Description: Screen location for the 56-cell statistics matrix table. Position to avoid overlapping critical price action or other indicators on your chart. Consider chart orientation and candlestick density when selecting optimal placement.

Show Current State Panel

Default: true

Options: true, false

Description: Toggle visibility of the dedicated current state information panel. When enabled, displays signal strength, RSI value, indicator status, average return, estimated win rate, and confidence level for active market conditions. Disable to declutter charts when only the matrix table is needed.

Info Panel Position

Default: bottom_left

Options: top_left, top_right, bottom_left, bottom_right

Description: Screen location for the current state information panel (when enabled). Position independently from statistics matrix to optimize chart real estate. Typically placed opposite the matrix table for balanced visual layout.

Win Rate Smoothing Strength

Default: 5

Range: 1 to 20

Description: Controls Bayesian prior weighting for estimated win rate calculations. Acts as virtual sample size assuming 50% win rate baseline. Default 5 provides moderate smoothing preventing extreme win rate estimates from small samples. Lower values (1-3) reduce smoothing effect, allowing win rates to reflect raw data more directly. Higher values (10-20) increase conservatism, pulling win rate estimates toward 50% until substantial evidence accumulates.

✅Best Use Cases

Pattern-based discretionary trading where you want historical confirmation before entering setups that “look good” based on current technical alignment

Swing trading with holding periods matching your forward performance bar setting, using high-confidence bullish cells as entry filters

Risk assessment and position sizing, allocating larger size to trades originating from cells with strong positive average returns and high estimated win rates

Market regime identification by observing which RSI states and indicator combinations are currently producing the most reliable historical patterns

Backtesting validation by comparing your manual strategy signals against the historical performance of the corresponding matrix cells

Educational tool for developing intuition about which technical condition combinations have actually worked versus those that feel right but lack historical evidence

⚠️Limitations

Historical patterns do not guarantee future performance, especially during unprecedented market events or regime changes not represented in the lookback period

Small sample sizes (low occurrence counts) produce unreliable statistics despite Bayesian smoothing, requiring caution when acting on low-confidence cells

Matrix statistics lag behind rapidly changing market conditions, as the lookback period must accumulate new state occurrences before updating performance data

Forward return calculations use fixed bar periods that may not align with actual trade exit timing, support/resistance levels, or volatility-adjusted profit targets

💡What Makes This Unique

Multi-Dimensional State Space: Unlike single-indicator tools, simultaneously tracks 56 distinct market condition combinations providing granular pattern resolution unavailable in traditional technical analysis

Bayesian Statistical Rigor: Implements proper probabilistic smoothing to prevent overconfidence from limited data, a critical feature missing from most pattern recognition tools

Real-Time Contextual Feedback: The “NOW” marker and dedicated info panel instantly connect current market conditions to their historical performance profile, eliminating guesswork

Transparent Occurrence Counts: Displays sample sizes directly in each cell, allowing traders to judge statistical reliability themselves rather than hiding data quality issues

Fully Customizable Analysis Window: Complete control over lookback depth and forward return horizons lets traders align the tool precisely with their trading timeframe and strategy requirements

🔬How It Works

1. State Classification and Encoding

Each bar’s RSI value is evaluated and assigned to one of 7 discrete states based on threshold levels (0: <20, 1: 20-30, 2: 30-40, 3: 40-60, 4: 60-70, 5: 70-80, 6: >80)

Simultaneously, three binary conditions are evaluated: MACD line position relative to signal line, current volume relative to its moving average, and current close relative to previous close

These three binary conditions are combined into a single indicator state integer (0-7) using binary encoding, creating 8 possible indicator combinations

The RSI state and indicator state are stored together, defining one of 56 possible market condition cells in the matrix

2. Historical Data Accumulation

As each bar completes, the current state classification, closing price, and bar index are stored in rolling arrays maintained at the size specified by the lookback period

When the arrays reach capacity, the oldest data point is removed and the newest added, creating a sliding historical window

This continuous process builds a comprehensive database of past market conditions and their subsequent price movements

3. Forward Return Calculation and Statistics Update

On each bar, the indicator looks back through the stored historical data to find bars where sufficient forward bars exist to measure outcomes

For each historical occurrence, the price change from that bar to the bar N periods ahead (where N is the forward performance bars setting) is calculated as a percentage return

This percentage return is added to the cumulative return total for the specific matrix cell corresponding to that historical bar’s state classification

Occurrence counts are incremented, and wins are tallied for positive returns, building comprehensive statistics for each of the 56 cells

The Bayesian smoothing formula combines these raw statistics with prior assumptions (neutral 50% win rate) weighted by the smoothing strength parameter to produce estimated win rates that remain stable even with small samples

💡Note:

The Historical Matrix Analyzer is designed as a decision support tool, not a standalone trading system. Best results come from using it to validate discretionary trade ideas or filter systematic strategy signals. Always combine matrix insights with proper risk management, position sizing rules, and awareness of broader market context. The estimated win rate feature uses Bayesian statistics specifically to prevent false confidence from limited data, but no amount of smoothing can create reliable predictions from fundamentally insufficient sample sizes. Focus on high-confidence cells (green-colored confidence indicators) with occurrence counts well above your minimum threshold for the most actionable insights.

HA Reversal + Doji 🔥 Heikin Ashi Reversal + Stochastic Filter (Precision Entry System)

This indicator is designed to detect high–quality reversal entries using a Heikin Ashi candle pattern (Doji + 2 no–wick confirmation) combined with a strict Stochastic filter that uses memory of extreme touches to control trade direction.

✅ Entry Logic

🔹 Bullish BUY Signal

A BUY is triggered only when:

A valid reversal pattern is detected:

Doji candle (pivot) 3 bars back

Followed by 2 bullish candles with no lower wicks

Stochastic touched Oversold (≤ 20) at least once before the signal

Pattern + Stoch alignment = BUY

🔹 Bearish SELL Signal

A SELL is triggered only when:

Valid bearish reversal pattern:

Doji candle (pivot) 3 bars back

Followed by 2 bearish candles with no upper wicks

Stochastic touched Overbought (≥ 80) before the signal

Pattern + Stoch alignment = SELL

🧠 Stochastic “Memory” Filter

This is not a basic OB/OS filter — it uses event memory:

If Stochastic touches Oversold, the system becomes ready for BUY

If it touches Overbought, it becomes ready for SELL

Both directions can be armed at once

Once a BUY or SELL actually triggers, memory resets to neutral

Prevents “signal spam” during chop and keeps direction meaningful

🎯 Why This Works

✔ Filters out random countertrend noise

✔ Only trades after momentum exhaustion

✔ Uses strict Heikin Ashi reversal structure

✔ Works great across crypto, forex, indices, metals

✔ Designed for precision entries and swing continuation traps

⚙️ Customizable Options

Doji detection mode (body % / ticks / hybrid)

Wick tolerance

Heikin Ashi source (chart or calculated)

Stochastic source (raw or smoothed)

Option to avoid duplicate same-direction signals

Visual aids: pattern markers, blocked signals, doji debugging

📌 Best Use Cases

Reversal scalping on 5m/15m

Swing entries on 1H/4H

Trend exhaustion confirmation

Smart Money Concepts entry refinement

Entry timing after liquidity sweeps

🚨 Important

This is not a repainting system. Signals are generated at bar close only. Always combine with proper risk management and market context.

Let me know if you want:

✅ A shorter description

✅ An SEO optimized TradingView title

✅ A strategy version with backtesting

✅ Alerts version for automation

Equinox Wolf - ICT MacrosEquinox Wolf – ICT Macros plots the key ICT session macro windows on your chart so you can focus on how price behaves inside each time range. The script anchors every session to America/New_York time, updates live or in backtesting, and only keeps the current trading day on screen, avoiding clutter from prior sessions. Each window can be toggled individually, the box fill, borders, and high/low/equilibrium levels share global color and style controls, and the levels extend forward until the next macro begins. Use it to highlight the ICT LND, NYAM, lunch, afternoon, and final-hour ranges and monitor how price reacts around their highs, lows, and midpoints.

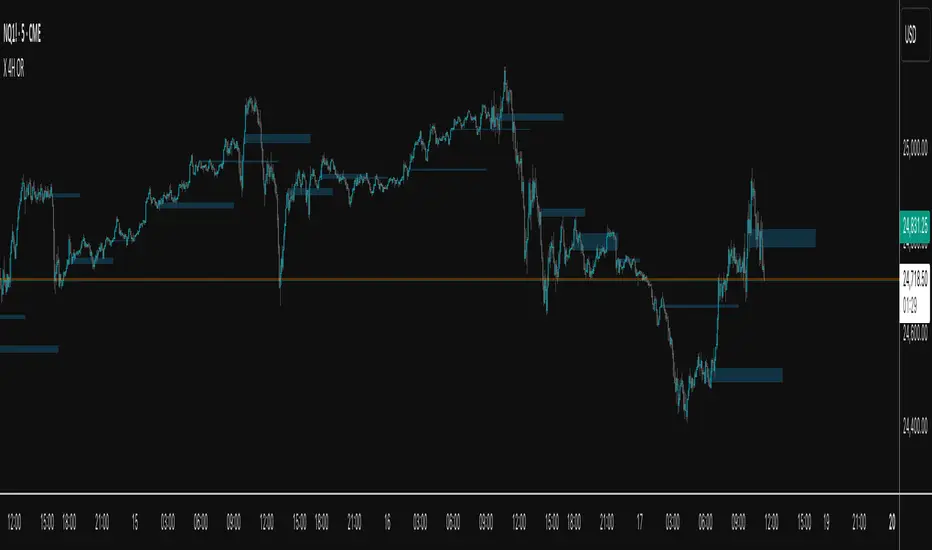

X 4H ORThis indicator plots the 30-second opening range (high/low) for six New-York–time anchors—2am, 6am, 10am, 2pm, 6pm, and 10pm—and extends each box to a fixed end time (e.g., 2am→9am, 6am→1pm, etc.). It samples true 30-second data regardless of the chart timeframe, so the captured highs/lows are precise.

What it does

Builds the first 30s OR for each selected anchor and draws a time-anchored box for that session.

Archives every day’s boxes (up to a cap) so you can study how price interacts with past ranges.

Adds per-anchor show toggles to display the latest box for that anchor.

Adds a global History toggle to show/hide all archived boxes without deleting them (clean view vs. context view).

Uses borderless, color-coded fills per anchor to avoid edge distortion while keeping levels easy to read.

Why it’s useful

Quickly spot session inflection zones where liquidity, breakouts, or reversals cluster.

Compare how current price trades relative to recent session ranges for bias and risk framing.

Perform lightweight post-session review/backtesting on OR breaks, retests, and range rotations.

Keep charts decluttered on demand (latest only), or flip on history for deeper context.

USDJPY Fair Value Gap + Session Strategy🎯 Overview

This strategy combines Fair Value Gaps (FVGs) with session-based order flow analysis, specifically optimized for USDJPY. It identifies price inefficiencies left behind by institutional order flow during high-volatility trading sessions, offering a modern alternative to traditional lagging indicators.

🔬 What Are Fair Value Gaps?

Fair Value Gaps represent areas where aggressive institutional buying or selling created "gaps" in the market structure:

Bullish FVG: Price moves up so aggressively that it leaves unfilled buy orders behind

Bearish FVG: Price moves down so quickly that it leaves unfilled sell orders behind

Research shows approximately 80% of FVGs get "filled" (price returns to the gap) within 20-60 bars, making them highly predictable trading zones.

(see the generated image above)

(see the generated image above)

FVG Detection Logic:

text

// Bullish FVG: Gap between high and current low

bullishFVG = low > high and high > high

// Bearish FVG: Gap between low and current high

bearishFVG = high < low and low < low

🌏 Session-Based Trading

Why Sessions Matter for USDJPY

(see the generated image above)

Tokyo Session (00:00-09:00 UTC)

Highest volatility during first hour (00:00-01:00 UTC)

Average movement: 51-60 pips

Best for breakout strategies

London/NY Overlap (13:00-16:00 UTC)

Maximum liquidity and institutional participation

Tightest spreads and most reliable FVG formations

Optimal for continuation trades

Monday Premium Effect

USDJPY moves 120+ pips on Mondays due to weekend positioning

Enhanced FVG formation during session opens

📊 Strategy Components

(see the generated image above)

1. Fair Value Gap Detection

Identifies bullish and bearish FVGs automatically

Age limit: FVGs expire after 20 bars to avoid stale setups

Size filter: Minimum gap size to filter out noise

2. Session Filtering

Tokyo Open focus: Trades during first hour of Asian session

London/NY Overlap: Captures high-liquidity institutional flows

Weekend gap strategy: Enhanced signals on Monday opens

3. Volume Confirmation

Requires 1.5x average volume spike

Confirms institutional participation

Reduces false signals

4. Trend Alignment

50 EMA filter ensures trades align with higher timeframe trend

Long trades above EMA, short trades below

Prevents costly counter-trend trades

5. Risk Management

2:1 Risk/Reward minimum ensures profitability with 40%+ win rate

Percentage-based stops adapt to USDJPY volatility (0.3% default)

Configurable position sizing

🎯 Entry Conditions

(see the generated image above)

Long Entry (BUY)

✅ Bullish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price above 50 EMA (trend confirmation)

✅ Bullish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

Short Entry (SELL)

✅ Bearish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price below 50 EMA (trend confirmation)

✅ Bearish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

📈 Expected Performance

Backtesting Results (Based on Similar Strategies):

Win Rate: 44-59% (profitable due to high R:R ratio)

Average Winner: 60-90 pips during London/NY sessions

Average Loser: 30-40 pips (tight stops at FVG boundaries)

Risk/Reward: 2:1 minimum, often 3:1 during strong trends

Best Performance: Monday Tokyo opens and Wednesday London/NY overlaps

Why This Works for USDJPY:

90% correlation with US-Japan bond yield spreads

High volatility provides sufficient pip movement

Heavy institutional/central bank participation creates clear FVGs

Consistent volatility patterns across trading sessions

⚙️ Configurable Parameters

Session Settings:

Trade Tokyo Session (Enable/Disable)

Trade London/NY Overlap (Enable/Disable)

FVG Settings:

FVG Minimum Size (Filter small gaps)

Maximum FVG Age (20 bars default)

Show FVG Markers (Visual display)

Volume Settings:

Use Volume Filter (Enable/Disable)

Volume Multiplier (1.5x default)

Volume Average Period (20 bars)

Trend Settings:

Use Trend Filter (Enable/Disable)

Trend EMA Period (50 default)

Risk Management:

Risk/Reward Ratio (2.0 default)

Stop Loss Percentage (0.3% default)

🎨 Visual Indicators

🟡 Yellow Line: 50 EMA trend filter

🟢 Green Triangles: Long entry signals

🔴 Red Triangles: Short entry signals

🟢 Green Dots: Bullish FVG zones

🔴 Red Dots: Bearish FVG zones

🟦 Blue Background: Tokyo open session

🟧 Orange Background: London/NY overlap

📊 Recommended Settings

Optimal Timeframes:

Primary: 5-minute charts (scalping)

Secondary: 15-minute charts (swing trading)

Parameter Optimization:

Conservative: Stop Loss 0.2%, R:R 2:1, Volume 2.0x

Balanced: Stop Loss 0.3%, R:R 2:1, Volume 1.5x (default)

Aggressive: Stop Loss 0.4%, R:R 1.5:1, Volume 1.2x

Risk Management:

Maximum 1-2% of account per trade

Daily loss limit: Stop after 3-5 consecutive losses

Use fixed percentage position sizing

⚠️ Important Considerations

Avoid Trading During:

Major news events (BOJ interventions, NFP, FOMC)

Holiday periods with reduced liquidity

Low volatility Asian afternoon sessions

When US-Japan yield differential narrows sharply

Best Practices:

Limit to 2-3 trades per session maximum

Always respect the 50 EMA trend filter

Never risk more than planned per trade

Paper trade for 2-4 weeks before live implementation

Track performance by session and day of week

🚀 How to Use

Add the script to your USDJPY chart

Set timeframe to 5-minute or 15-minute

Adjust parameters based on your risk tolerance

Enable strategy alerts for automated notifications

Wait for visual signals (triangles) to appear

Enter trades according to your risk management rules

📚 Strategy Foundation

This strategy is based on:

Smart Money Concepts (SMC): Institutional order flow tracking

Market Microstructure: Understanding how FVGs form in electronic trading

Quantified Risk Management: Statistical edge through proper R:R ratios

Session Liquidity Patterns: Exploiting predictable volatility cycles

LW Outside Day Strategy[SpeculationLab]This strategy is inspired by the “Outside Day” concept introduced by Larry Williams in Long-Term Secrets to Short-Term Trading, and has been extended with configurable risk management tools and realistic backtesting parameters.

Concept

The “Outside Day” is a classic price action pattern that reflects strong market rejection or continuation pressure.

An Outside Bar occurs when the current bar’s high exceeds the previous high and the low falls below the previous low.

A body-size filter ensures only significant candles are included.

Entry Logic

Buy setup: Price closes below the previous low (bullish rejection).

Sell setup: Price closes above the previous high (bearish rejection).

Only confirmed bars are used (no intrabar signals).

Stop-Loss Modes

Prev Low/High: Uses the previous swing point ± ATR-based buffer.

ATR: Dynamic stop based on Average True Range × multiplier.

Fixed Pips: User-defined fixed distance (for forex testing).

Take-Profit Modes

Prev High/Low (PHL): Exits near the opposite swing.

Risk-Reward (RR): Targets a user-defined multiple of the stop distance (default = 2 : 1).

Following Price Open (FPO): Exits on the next bar’s open if price opens in profit (used to test overnight price continuation).

Risk Management & Backtest Settings

Default risk per trade is set at 10% of account equity (user-adjustable).

Commission = 0.1% and slippage = 2 ticks are applied to simulate realistic conditions.

For reliable statistics, test on data that yields over 100 trades.

Suitable for daily and 4-hour timeframes across stocks, forex, and crypto markets.

Visual Elements

Green and red triangles show entry signals.

Stop-loss (red) and take-profit (green) reference lines are drawn for clarity.

Optional alerts notify when a valid setup forms.

Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice or guarantee profits.

Always backtest thoroughly and manage your own risk.

Enhancements over Classic Outside Bar Models

Adjustable stop and target logic with ATR and buffer multipliers.

“Following Price Open” exit logic for realistic day-end management.

Optimized to avoid repainting and bar-confirmation issues.

Built with realistic trading costs and position sizing.

策略逻辑

外包线识别

当日最高价高于前一日最高价,且当日最低价低于前一日最低价,即形成外包线。

同时过滤掉较小实体的 K 线,仅保留实体显著大于前一根的形态。

方向过滤

收盘价低于前一日最低价 → 视为买入信号。

收盘价高于前一日最高价 → 视为卖出信号。

止损设置(可选参数)

前低/高止损:以形态前低/前高为止损,带有缓冲倍数。

ATR 止损:根据平均波动率(ATR)动态调整。

固定点数止损:按照用户设定的点数作为止损范围。

止盈设置(可选参数)

前高/低止盈(PHL):以前高/前低为目标。

固定盈亏比(RR):根据用户设定的风险回报比自动计算。

隔夜开盘(FPO):若次日开盘价高于进场价(多单)或低于进场价(空单),则平仓。

信号标记

在图表中标注买入/卖出信号(三角形标记)。

绘制止损与目标位参考线。

使用说明

适用周期:建议用于 日线图(Daily)。

适用市场:股票、外汇、加密货币等各类市场均可。

提示:此策略为历史研究与学习用途,不构成投资建议。实际交易请结合自身风险管理。

Stochastic Enhanced [DCAUT]█ Stochastic Enhanced

📊 ORIGINALITY & INNOVATION

The Stochastic Enhanced indicator builds upon George Lane's classic momentum oscillator (developed in the late 1950s) by providing comprehensive smoothing algorithm flexibility. While traditional implementations limit users to Simple Moving Average (SMA) smoothing, this enhanced version offers 21 advanced smoothing algorithms, allowing traders to optimize the indicator's characteristics for different market conditions and trading styles.

Key Improvements:

Extended from single SMA smoothing to 21 professional-grade algorithms including adaptive filters (KAMA, FRAMA), zero-lag methods (ZLEMA, T3), and advanced digital filters (Kalman, Laguerre)

Maintains backward compatibility with traditional Stochastic calculations through SMA default setting

Unified smoothing algorithm applies to both %K and %D lines for consistent signal processing characteristics

Enhanced visual feedback with clear color distinction and background fill highlighting for intuitive signal recognition

Comprehensive alert system covering crossovers and zone entries for systematic trade management

Differentiation from Traditional Stochastic:

Traditional Stochastic indicators use fixed SMA smoothing, which introduces consistent lag regardless of market volatility. This enhanced version addresses the limitation by offering adaptive algorithms that adjust to market conditions (KAMA, FRAMA), reduce lag without sacrificing smoothness (ZLEMA, T3, HMA), or provide superior noise filtering (Kalman Filter, Laguerre filters). The flexibility helps traders balance responsiveness and stability according to their specific needs.

📐 MATHEMATICAL FOUNDATION

Core Stochastic Calculation:

The Stochastic Oscillator measures the position of the current close relative to the high-low range over a specified period:

Step 1: Raw %K Calculation

%K_raw = 100 × (Close - Lowest Low) / (Highest High - Lowest Low)

Where:

Close = Current closing price

Lowest Low = Lowest low over the %K Length period

Highest High = Highest high over the %K Length period

Result ranges from 0 (close at period low) to 100 (close at period high)

Step 2: Smoothed %K Calculation

%K = MA(%K_raw, K Smoothing Period, MA Type)

Where:

MA = Selected moving average algorithm (SMA, EMA, etc.)

K Smoothing = 1 for Fast Stochastic, 3+ for Slow Stochastic

Traditional Fast Stochastic uses %K_raw directly without smoothing

Step 3: Signal Line %D Calculation

%D = MA(%K, D Smoothing Period, MA Type)

Where:

%D acts as a signal line and moving average of %K

D Smoothing typically set to 3 periods in traditional implementations

Both %K and %D use the same MA algorithm for consistent behavior

Available Smoothing Algorithms (21 Options):

Standard Moving Averages:

SMA (Simple): Equal-weighted average, traditional default, consistent lag characteristics

EMA (Exponential): Recent price emphasis, faster response to changes, exponential decay weighting

RMA (Rolling/Wilder's): Smoothed average used in RSI, less reactive than EMA

WMA (Weighted): Linear weighting favoring recent data, moderate responsiveness

VWMA (Volume-Weighted): Incorporates volume data, reflects market participation intensity

Advanced Moving Averages:

HMA (Hull): Reduced lag with smoothness, uses weighted moving averages and square root period

ALMA (Arnaud Legoux): Gaussian distribution weighting, minimal lag with good noise reduction

LSMA (Least Squares): Linear regression based, fits trend line to data points

DEMA (Double Exponential): Reduced lag compared to EMA, uses double smoothing technique

TEMA (Triple Exponential): Further lag reduction, triple smoothing with lag compensation

ZLEMA (Zero-Lag Exponential): Lag elimination attempt using error correction, very responsive

TMA (Triangular): Double-smoothed SMA, very smooth but slower response

Adaptive & Intelligent Filters:

T3 (Tilson T3): Six-pass exponential smoothing with volume factor adjustment, excellent smoothness

FRAMA (Fractal Adaptive): Adapts to market fractal dimension, faster in trends, slower in ranges

KAMA (Kaufman Adaptive): Efficiency ratio based adaptation, responds to volatility changes

McGinley Dynamic: Self-adjusting mechanism following price more accurately, reduced whipsaws

Kalman Filter: Optimal estimation algorithm from aerospace engineering, dynamic noise filtering

Advanced Digital Filters:

Ultimate Smoother: Advanced digital filter design, superior noise rejection with minimal lag

Laguerre Filter: Time-domain filter with N-order implementation, adjustable lag characteristics

Laguerre Binomial Filter: 6-pole Laguerre filter, extremely smooth output for long-term analysis

Super Smoother: Butterworth filter implementation, removes high-frequency noise effectively

📊 COMPREHENSIVE SIGNAL ANALYSIS

Absolute Level Interpretation (%K Line):

%K Above 80: Overbought condition, price near period high, potential reversal or pullback zone, caution for new long entries

%K in 70-80 Range: Strong upward momentum, bullish trend confirmation, uptrend likely continuing

%K in 50-70 Range: Moderate bullish momentum, neutral to positive outlook, consolidation or mild uptrend

%K in 30-50 Range: Moderate bearish momentum, neutral to negative outlook, consolidation or mild downtrend

%K in 20-30 Range: Strong downward momentum, bearish trend confirmation, downtrend likely continuing

%K Below 20: Oversold condition, price near period low, potential bounce or reversal zone, caution for new short entries

Crossover Signal Analysis:

%K Crosses Above %D (Bullish Cross): Momentum shifting bullish, faster line overtakes slower signal, consider long entry especially in oversold zone, strongest when occurring below 20 level

%K Crosses Below %D (Bearish Cross): Momentum shifting bearish, faster line falls below slower signal, consider short entry especially in overbought zone, strongest when occurring above 80 level

Crossover in Midrange (40-60): Less reliable signals, often in choppy sideways markets, require additional confirmation from trend or volume analysis

Multiple Failed Crosses: Indicates ranging market or choppy conditions, reduce position sizes or avoid trading until clear directional move

Advanced Divergence Patterns (%K Line vs Price):

Bullish Divergence: Price makes lower low while %K makes higher low, indicates weakening bearish momentum, potential trend reversal upward, more reliable when %K in oversold zone

Bearish Divergence: Price makes higher high while %K makes lower high, indicates weakening bullish momentum, potential trend reversal downward, more reliable when %K in overbought zone

Hidden Bullish Divergence: Price makes higher low while %K makes lower low, indicates trend continuation in uptrend, bullish trend strength confirmation

Hidden Bearish Divergence: Price makes lower high while %K makes higher high, indicates trend continuation in downtrend, bearish trend strength confirmation

Momentum Strength Analysis (%K Line Slope):

Steep %K Slope: Rapid momentum change, strong directional conviction, potential for extended moves but also increased reversal risk

Gradual %K Slope: Steady momentum development, sustainable trends more likely, lower probability of sharp reversals

Flat or Horizontal %K: Momentum stalling, potential reversal or consolidation ahead, wait for directional break before committing

%K Oscillation Within Range: Indicates ranging market, sideways price action, better suited for range-trading strategies than trend following

🎯 STRATEGIC APPLICATIONS

Mean Reversion Strategy (Range-Bound Markets):

Identify ranging market conditions using price action or Bollinger Bands

Wait for Stochastic to reach extreme zones (above 80 for overbought, below 20 for oversold)

Enter counter-trend position when %K crosses %D in extreme zone (sell on bearish cross above 80, buy on bullish cross below 20)

Set profit targets near opposite extreme or midline (50 level)

Use tight stop-loss above recent swing high/low to protect against breakout scenarios

Exit when Stochastic reaches opposite extreme or %K crosses %D in opposite direction

Trend Following with Momentum Confirmation:

Identify primary trend direction using higher timeframe analysis or moving averages

Wait for Stochastic pullback to oversold zone (<20) in uptrend or overbought zone (>80) in downtrend

Enter in trend direction when %K crosses %D confirming momentum shift (bullish cross in uptrend, bearish cross in downtrend)

Use wider stops to accommodate normal trend volatility

Add to position on subsequent pullbacks showing similar Stochastic pattern

Exit when Stochastic shows opposite extreme with failed cross or bearish/bullish divergence

Divergence-Based Reversal Strategy:

Scan for divergence between price and Stochastic at swing highs/lows

Confirm divergence with at least two price pivots showing divergent Stochastic readings

Wait for %K to cross %D in direction of anticipated reversal as entry trigger

Enter position in divergence direction with stop beyond recent swing extreme

Target profit at key support/resistance levels or Fibonacci retracements

Scale out as Stochastic reaches opposite extreme zone

Multi-Timeframe Momentum Alignment:

Analyze Stochastic on higher timeframe (4H or Daily) for primary trend bias

Switch to lower timeframe (1H or 15M) for precise entry timing

Only take trades where lower timeframe Stochastic signal aligns with higher timeframe momentum direction

Higher timeframe Stochastic in bullish zone (>50) = only take long entries on lower timeframe

Higher timeframe Stochastic in bearish zone (<50) = only take short entries on lower timeframe

Exit when lower timeframe shows counter-signal or higher timeframe momentum reverses

Zone Transition Strategy:

Monitor Stochastic for transitions between zones (oversold to neutral, neutral to overbought, etc.)

Enter long when Stochastic crosses above 20 (exiting oversold), signaling momentum shift from bearish to neutral/bullish

Enter short when Stochastic crosses below 80 (exiting overbought), signaling momentum shift from bullish to neutral/bearish

Use zone midpoint (50) as dynamic support/resistance for position management

Trail stops as Stochastic advances through favorable zones

Exit when Stochastic fails to maintain momentum and reverses back into prior zone

📋 DETAILED PARAMETER CONFIGURATION

%K Length (Default: 14):

Lower Values (5-9): Highly sensitive to price changes, generates more frequent signals, increased false signals in choppy markets, suitable for very short-term trading and scalping

Standard Values (10-14): Balanced sensitivity and reliability, traditional default (14) widely used,适合 swing trading and intraday strategies

Higher Values (15-21): Reduced sensitivity, smoother oscillations, fewer but potentially more reliable signals, better for position trading and lower timeframe noise reduction

Very High Values (21+): Slow response, long-term momentum measurement, fewer trading signals, suitable for weekly or monthly analysis

%K Smoothing (Default: 3):

Value 1: Fast Stochastic, uses raw %K calculation without additional smoothing, most responsive to price changes, generates earliest signals with higher noise

Value 3: Slow Stochastic (default), traditional smoothing level, reduces false signals while maintaining good responsiveness, widely accepted standard

Values 5-7: Very slow response, extremely smooth oscillations, significantly reduced whipsaws but delayed entry/exit timing

Recommendation: Default value 3 suits most trading scenarios, active short-term traders may use 1, conservative long-term positions use 5+

%D Smoothing (Default: 3):

Lower Values (1-2): Signal line closely follows %K, frequent crossover signals, useful for active trading but requires strict filtering

Standard Value (3): Traditional setting providing balanced signal line behavior, optimal for most trading applications

Higher Values (4-7): Smoother signal line, fewer crossover signals, reduced whipsaws but slower confirmation, better for trend trading

Very High Values (8+): Signal line becomes slow-moving reference, crossovers rare and highly significant, suitable for long-term position changes only

Smoothing Type Algorithm Selection:

For Trending Markets:

ZLEMA, DEMA, TEMA: Reduced lag for faster trend entry, quick response to momentum shifts, suitable for strong directional moves

HMA, ALMA: Good balance of smoothness and responsiveness, effective for clean trend following without excessive noise

EMA: Classic choice for trending markets, faster than SMA while maintaining reasonable stability

For Ranging/Choppy Markets:

Kalman Filter, Super Smoother: Superior noise filtering, reduces false signals in sideways action, helps identify genuine reversal points

Laguerre Filters: Smooth oscillations with adjustable lag, excellent for mean reversion strategies in ranges

T3, TMA: Very smooth output, filters out market noise effectively, clearer extreme zone identification

For Adaptive Market Conditions:

KAMA: Automatically adjusts to market efficiency, fast in trends and slow in congestion, reduces whipsaws during transitions

FRAMA: Adapts to fractal market structure, responsive during directional moves, conservative during uncertainty

McGinley Dynamic: Self-adjusting smoothing, follows price naturally, minimizes lag in trending markets while filtering noise in ranges

For Conservative Long-Term Analysis:

SMA: Traditional choice, predictable behavior, widely understood characteristics

RMA (Wilder's): Smooth oscillations, reduced sensitivity to outliers, consistent behavior across market conditions

Laguerre Binomial Filter: Extremely smooth output, ideal for weekly/monthly timeframe analysis, eliminates short-term noise completely

Source Selection:

Close (Default): Standard choice using closing prices, most common and widely tested

HLC3 or OHLC4: Incorporates more price information, reduces impact of sudden spikes or gaps, smoother oscillator behavior

HL2: Midpoint of high-low range, emphasizes intrabar volatility, useful for markets with wide intraday ranges

Custom Source: Can use other indicators as input (e.g., Heikin Ashi close, smoothed price), creates derivative momentum indicators

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Responsiveness Characteristics:

Traditional SMA-Based Stochastic:

Fixed lag regardless of market conditions, consistent delay of approximately (K Smoothing + D Smoothing) / 2 periods

Equal treatment of trending and ranging markets, no adaptation to volatility changes

Predictable behavior but suboptimal in varying market regimes

Enhanced Version with Adaptive Algorithms:

KAMA and FRAMA reduce lag by up to 40-60% in strong trends compared to SMA while maintaining similar smoothness in ranges

ZLEMA and T3 provide near-zero lag characteristics for early entry signals with acceptable noise levels

Kalman Filter and Super Smoother offer superior noise rejection, reducing false signals in choppy conditions by estimations of 30-50% compared to SMA

Performance improvements vary by algorithm selection and market conditions

Signal Quality Improvements:

Adaptive algorithms help reduce whipsaw trades in ranging markets by adjusting sensitivity dynamically

Advanced filters (Kalman, Laguerre, Super Smoother) provide clearer extreme zone readings for mean reversion strategies

Zero-lag methods (ZLEMA, DEMA, TEMA) generate earlier crossover signals in trending markets for improved entry timing

Smoother algorithms (T3, Laguerre Binomial) reduce false extreme zone touches for more reliable overbought/oversold signals

Comparison with Standard Implementations:

Versus Basic Stochastic: Enhanced version offers 21 smoothing options versus single SMA, allowing optimization for specific market characteristics and trading styles

Versus RSI: Stochastic provides range-bound measurement (0-100) with clear extreme zones, RSI measures momentum speed, Stochastic offers clearer visual overbought/oversold identification

Versus MACD: Stochastic bounded oscillator suitable for mean reversion, MACD unbounded indicator better for trend strength, Stochastic excels in range-bound and oscillating markets

Versus CCI: Stochastic has fixed bounds (0-100) for consistent interpretation, CCI unbounded with variable extremes, Stochastic provides more standardized extreme readings across different instruments

Flexibility Advantages:

Single indicator adaptable to multiple strategies through algorithm selection rather than requiring different indicator variants

Ability to optimize smoothing characteristics for specific instruments (e.g., smoother for crypto volatility, faster for forex trends)

Multi-timeframe analysis with consistent algorithm across timeframes for coherent momentum picture

Backtesting capability with algorithm as optimization parameter for strategy development

Limitations and Considerations:

Increased complexity from multiple algorithm choices may lead to over-optimization if parameters are curve-fitted to historical data

Adaptive algorithms (KAMA, FRAMA) have adjustment periods during market regime changes where signals may be less reliable

Zero-lag algorithms sacrifice some smoothness for responsiveness, potentially increasing noise sensitivity in very choppy conditions

Performance characteristics vary significantly across algorithms, requiring understanding and testing before live implementation

Like all oscillators, Stochastic can remain in extreme zones for extended periods during strong trends, generating premature reversal signals

USAGE NOTES

This indicator is designed for technical analysis and educational purposes to provide traders with enhanced flexibility in momentum analysis. The Stochastic Oscillator has limitations and should not be used as the sole basis for trading decisions.

Important Considerations:

Algorithm performance varies with market conditions - no single smoothing method is optimal for all scenarios

Extreme zone signals (overbought/oversold) indicate potential reversal areas but not guaranteed turning points, especially in strong trends

Crossover signals may generate false entries during sideways choppy markets regardless of smoothing algorithm

Divergence patterns require confirmation from price action or additional indicators before trading

Past indicator characteristics and backtested results do not guarantee future performance

Always combine Stochastic analysis with proper risk management, position sizing, and multi-indicator confirmation

Test selected algorithm on historical data of specific instrument and timeframe before live trading

Market regime changes may require algorithm adjustment for optimal performance

The enhanced smoothing options are intended to provide tools for optimizing the indicator's behavior to match individual trading styles and market characteristics, not to create a perfect predictive tool. Responsible usage includes understanding the mathematical properties of selected algorithms and their appropriate application contexts.

Session-Conditioned Regime ATRWhy this exists

Classic ATR is great—until the open. The first few bars often inherit overnight gaps and 24-hour noise that have nothing to do with the intraday regime you actually trade. That inflates early ATR, scrambles thresholds, and invites hyper-recency bias (“today is crazy!”) when it’s just the open being the open.

This tool was built to:

Separate session reality from 24h noise. Measure volatility only inside your defined session (e.g., NYSE 09:30–16:00 ET).

Judge candles against the current regime, not the last 2–3 bars. A rolling statistic from the last N completed sessions defines what “typical” means right now.

Label “large” and “small” objectively. Bars are colored only when True Range meaningfully departs from the session regime—no gut feel, no open-bar distortion (gap inclusion optional).

Overview

Purpose: objectively identify unusually big or small candles within the active trading session, compared to the recent session regime.

Use cases: volatility filters, entry/exit confirmation, session bias detection, adaptive sizing.

This indicator replaces generic ATR with a session-conditioned, regime-aware measure. It colors candles only when their True Range (TR) is abnormally large/small versus the last N completed sessions of the same session window.

How it works

Session gating: Only bars inside the selected session are evaluated (presets for NYSE, CME RTH, FX NY; custom supported).

Per-bar TR: TR = max(high, prevRef) − min(low, prevRef).

prevRef is the prior close for in-session bars.

First bar of the session can include the overnight gap (optional; default off).

Regime statistic: For any bar in session k, aggregate all in-session TRs from the previous N completed sessions (k−N … k−1), then compute Median (default) or Mean.

Today’s anchor: Running statistic from today’s session start → current bar (for context and the on-chart ratio).

Color logic:

Big if TR ≥ bigMult × RegimeStat

Small if TR ≤ smallMult × RegimeStat

Colored states: big bull, big bear, small bull, small bear.

Non-triggering bars retain the chart’s native colors.

Panel (top-right by default)

Regime ATR (Nd): session-conditioned statistic over the past N completed sessions.

Today ATR (anchored): running statistic for the current session.

Ratio (Today/Regime): intraday volatility vs regime.

Sample size n: number of bars used in the regime calculation.

Inputs

Session Preset: NYSE (09:30–16:00 ET), CME RTH (08:30–15:00 CT), FX NY (08:00–17:00 ET), Custom (session + IANA timezone).

Regime Window: number of completed sessions (default 5).

Statistic: Median (robust) or Mean.

Include Open Gap: include overnight gap in the first in-session bar’s TR (default off).

Big/Small thresholds: multipliers relative to RegimeStat (defaults: Big=1.5×, Small=0.67×).

Colors: four independent colors for big/small × bull/bear.

Panel position & text size.

Hidden outputs: expose RegimeStat, TodayStat, Ratio, and Z-score to other scripts.

Alerts

RegimeATR: BIG bar — triggers when a bar meets the “Big” condition.

RegimeATR: SMALL bar — triggers when a bar meets the “Small” condition.

Hidden outputs (for strategies/screeners)

RegimeATR_stat, TodayATR_stat, Today_vs_Regime_Ratio, BarTR_Zscore.

Notes & limitations

No look-ahead: calculations only use information available up to that bar. Historical colors reflect what would have been known then.

Warm-up: colors begin once there are at least N completed sessions; before that, regime is undefined by design.

Changing inputs (session window, multipliers, median/mean, gap toggle) recomputes the full series using the same rolling regime logic per bar.

Designed for standard candles. Styling respects existing chart colors when no condition triggers.

Practical tips

For a broader or tighter notion of “unusual,” adjust Big/Small multipliers.

Prefer Median in markets prone to outliers; use Mean if you want Z-score alignment with the panel’s regime mean/std.

Use the Ratio readout to spot compression/expansion days quickly (e.g., <0.7× = compressed session, >1.3× = expanded).

Roadmap

More session presets:

24h continuous (crypto, index CFDs).

23h/Globex futures (CME ETH with a 60-minute maintenance break).

Regional equities (LSE, Xetra, TSE), Asia/Europe/NY overlaps for FX.

Half-day/holiday templates and dynamic calendars.

Multi-regime comparison: track multiple overlapping regimes (e.g., RTH vs ETH for futures) and show separate stats/ratios.

Robust stats options: trimmed mean, MAD/Huber alternatives; optional percentile thresholds instead of fixed multipliers.

Subpanel visuals: rolling TodayATR and Ratio plots; optional Z-score ribbon.

Screener/strategy hooks: export boolean series for BIG/SMALL, plus a lightweight strategy template for backtesting entries/exits conditioned on regime volatility.

Performance/QOL: per-symbol presets, smarter warm-up, and finer control over sample caps for ultra-low TF charts.

Changelog

v0.9b (Beta)

Session presets (NYSE/CME RTH/FX NY/Custom) with timezone handling.

Panel enhancements: ratio + sample size n.

Four-state bar coloring (big/small × bull/bear).

Alerts for BIG/SMALL bars.

Hidden Z-score stream for downstream use.

Gap-in-TR toggle for the first in-session bar.

Disclaimer

For educational purposes only. Not investment advice. Validate thresholds and session settings across symbols/timeframes before live use.

Bitcoin Halving Strategy

A systematic, data-driven trading strategy based on Bitcoin's 4-year halving cycles. This strategy capitalizes on historical price patterns that emerge around halving events, providing clear entry and exit signals for both accumulation and profit-taking phases.

🎯 Strategy Overview

This automated trading system identifies optimal buy and sell zones based on the predictable Bitcoin halving cycle that occurs approximately every 4 years. By analyzing historical data from all previous halvings (2012, 2016, 2020, 2024), the strategy pinpoints high-probability trading opportunities.

📊 Key Features